NEWGEN Software Technologies: From India's BPM Pioneer to Global Digital Transformation Leader

I. Introduction & Episode Roadmap

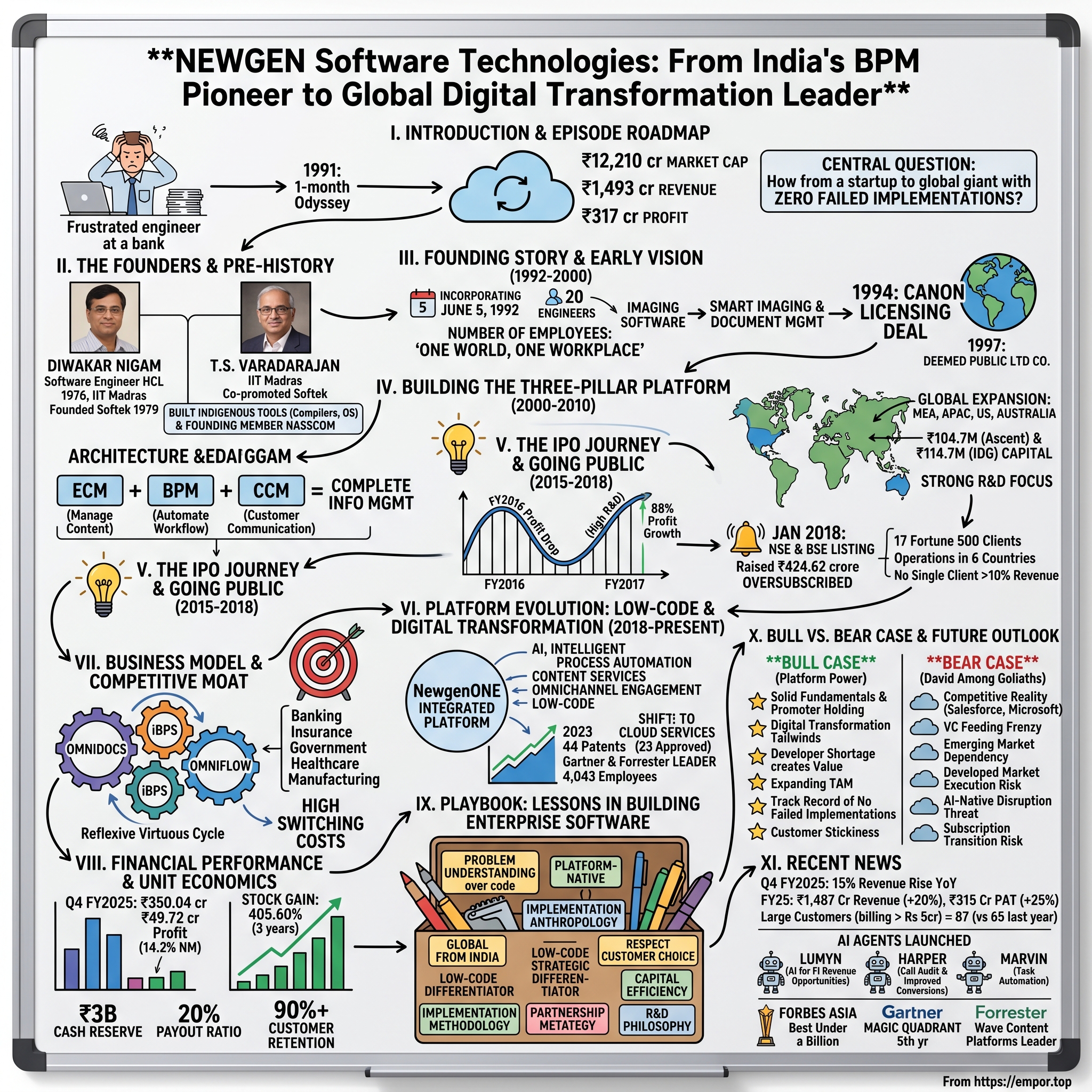

Picture this: It's 1991 in New Delhi. A seasoned software engineer walks into a bank to apply for a simple personal loan. What should have been a straightforward transaction turns into a month-long odyssey of paperwork, rubber stamps, and endless queues. That engineer was Diwakar Nigam, and that frustrating experience would spark the creation of one of India's most enduring enterprise software companies.

Today, Newgen Software Technologies stands as a ₹12,210 crore market cap giant, generating ₹1,493 crore in revenue with ₹317 crore in profit. But the real story isn't in these numbers—it's in how two engineers built India's answer to enterprise software titans like IBM and Oracle, starting when "Made in India" software was an oxymoron to global buyers.

The central question we're exploring: How did Diwakar Nigam and T.S. Varadarajan transform a document imaging startup into a global digital transformation platform that powers 17 Fortune 500 companies and has never—not once in 32 years—had a failed implementation?

This is a story about building enterprise software in emerging markets, the art of pivoting business models without losing your core, and the strategic patience required to compete globally from India. We'll unpack how Newgen evolved from selling imaging software to Canon to building low-code platforms that compete with Salesforce and ServiceNow. Along the way, we'll extract lessons about platform economics, the shift from licenses to SaaS, and why sometimes the best place to build global software is where the problems are most acute.

What makes Newgen particularly fascinating is their three-decade journey mirrors the entire evolution of enterprise software—from client-server to cloud, from coding to low-code, from documents to digital transformation. If you want to understand where enterprise software is heading, sometimes the best vantage point is from a company that's seen every wave and survived them all.

II. The Founders & Pre-History

The story of Newgen Software begins not in 1992, but in the late 1970s when a young engineer at HCL watched India's nascent computer industry struggle with a fundamental problem: everyone was importing software while the hardware was being built locally. Diwakar Nigam started his career at HCL in 1976 as a Software Engineer, working in software R&D during the height of India's License Raj—a period when industrial expansion required government permission for nearly everything.

Nigam held a Master's degree in Technology in Computer Science from IIT Madras (1976), and his academic pedigree positioned him at the forefront of India's first generation of computer scientists. But watching multinational corporations dominate India's software landscape while local talent built their products sparked an entrepreneurial itch. He quickly realized that building large scale software products would need a specialized company.

In 1979, Nigam took his first entrepreneurial leap, founding Softek. This wasn't just another services company—Softek was audaciously ambitious for its time. The company developed Compilers, Operating Systems, Word-Processors; at one time all the Indian computer manufacturers, like HCL, Wipro, ORG, ECIL etc., were reselling Softek's products. Think about that for a moment: in an era when "Made in India" software was virtually non-existent, Softek was building the fundamental tools that computers needed to function. They even developed India's first Hindi word processor, Sulekh/Aksahr—a remarkable achievement in localization before the term even existed.

Meanwhile, T.S. Varadarajan was charting a similar path. An alumnus of Bangalore University, IISc Bengaluru, and IIT Madras, holding a Master's in Technology (computer science), Varadarajan represented the same first generation of IT professionals who dreamed beyond conventional boundaries. He held a Masters in Technology in Computer Science from IIT Madras (1975) and represented the first generation of IT professionals who contributed towards the proliferation of the IT industry in India, being amongst those rare people who dreamt beyond the frontiers of conventional thinking towards the creation of a global IT product brand in India.

Varadarajan promoted Softek Private Limited and was associated with the company for 13 years, working alongside Nigam to build systems software that would become the backbone of India's computer industry. Together, they were building something unprecedented—indigenous software products that could compete with international offerings.

But perhaps the most telling detail about Nigam's vision comes from his role in shaping India's IT industry at large. He was a founding member of NASSCOM, India's apex Information Technology industry association, established in 1988. This wasn't just about building a company; it was about building an entire ecosystem. He was also one of the members of NASSCOM's Anti-Piracy Task Group, fighting to establish intellectual property rights in a market where software piracy was rampant.

The late 1980s and early 1990s marked a critical inflection point for India. The country was emerging from decades of socialist policies, the License Raj was crumbling, and economic liberalization was on the horizon. For software entrepreneurs like Nigam and Varadarajan, who had spent over a decade building products in one of the world's most restrictive business environments, the opportunity was clear: India was about to open up, and businesses would need technology to compete globally.

Nigam wanted to build software in India, for India, to change the way businesses work, realizing that building large scale software products would need a specialized company. After twelve years with Softek, both founders were ready for something bigger—not just building tools for computers, but transforming how entire enterprises operated. The stage was set for Newgen, and the timing couldn't have been more perfect.

III. Founding Story & Early Vision (1992-2000)

The monsoon of 1991 brought more than rain to New Delhi—it brought frustration that would spark a revolution. Diwakar Nigam recalls: "It was then I decided to build an imaging software to automate the flow of paper in enterprises. I decided to start my own enterprises business, and that's how Newgen was born". That month-long ordeal to get a simple bank loan wasn't just an inconvenience; it was a window into India's massive productivity problem. Every business process was drowning in paper, stamps, and manual approvals.

On June 5, 1992, Newgen Software Technologies was officially incorporated in New Delhi. Diwakar Nigam co-founded Newgen in 1992, with T.S. Varadarajan as co-founder, who has been on the company's Board of Directors since its incorporation. They started with 20 engineers and a vision that sounded almost mystical for its time: "I coined the phrase 'One World, One Workplace', envisaging that the flow of images across the enterprise would result in a smaller world where organisations have the ability to operate from anywhere".

Consider the audacity of this vision in 1992. The internet was barely commercial, email was a luxury, and most Indian businesses still operated with carbon copies and filing cabinets. Yet here were two engineers talking about digitizing documents and creating workflows that could span continents. They weren't just ahead of their time—they were operating in a different temporal dimension altogether.

The early strategy was brilliant in its simplicity: start with imaging. Why? Because scanning documents was the gateway drug to digital transformation. Once you could capture paper digitally, you could start thinking about routing it, storing it, retrieving it, and eventually, eliminating it altogether. Newgen began developing smart imaging and document management applications that could handle the entire lifecycle of business documents.

The breakthrough came faster than expected. Canon, the Japanese imaging giant, was looking for document processing software to complement their hardware offerings. For a two-year-old Indian startup to land a licensing deal with Canon was unprecedented. This wasn't a services contract or body-shopping arrangement—this was intellectual property, built in India, licensed to a global technology leader.

By 1997, the company's growth trajectory demanded a structural change. Newgen became a deemed Public Limited Company from July 1, 1997, signaling its ambitions to scale beyond a private software firm. The timing was fortuitous—India's IT sector was exploding, fueled by Y2K preparations and the dot-com boom. But while everyone else was chasing services revenue, Newgen stayed focused on products.

The numbers tell the story of disciplined growth. By 1999, Newgen had expanded from its initial 20 engineers to a 250-engineer software development team. This wasn't just headcount growth—it was capability building. Each engineer added meant another module developed, another feature shipped, another customer workflow automated. The company was systematically building what would become one of India's most comprehensive enterprise software platforms.

As Nigam explained: "We started by deploying our solutions for a global bank and gradually grew into multi-vertical industries". This early engagement with banking—still Newgen's strongest vertical today—taught them crucial lessons about enterprise software: reliability matters more than features, implementation is as important as innovation, and trust is earned in decades but lost in moments.

The late 1990s also saw Newgen making critical architectural decisions that would define its future. Rather than building point solutions for specific problems, they chose to create a platform—a foundation upon which multiple applications could be built. This meant slower initial progress but exponentially greater possibilities down the line. While competitors were selling scanning software or workflow tools, Newgen was building an ecosystem.

What's remarkable about this period is what Newgen didn't do. They didn't pivot to services when products got tough. They didn't chase the dot-com bubble. They didn't relocate to Silicon Valley. Instead, they stayed in Delhi, kept building products, and maintained their focus on solving real business problems for real companies. By Diwakar's account, with his vast experience in IT, Newgen grew into a Rs 520 crore business—but that was still years away.

The foundation was set: a company built by engineers who understood both technology and business, targeting the massive inefficiencies in enterprise operations, with patient capital and a long-term vision. As the millennium approached, Newgen was ready to transform from a document imaging company into something much more ambitious—a platform that could power the digital transformation of entire enterprises.

IV. Building the Three-Pillar Platform (2000-2010)

The new millennium brought a strategic epiphany to Newgen's leadership. Imaging was just the beginning—the real opportunity lay in managing the entire lifecycle of enterprise information. Between 2000 and 2010, Newgen would architect what became its legendary three-pillar platform strategy, transforming from a document management vendor into a comprehensive digital transformation partner.

The company evolved into a global provider of Business Process Management (BPM), Enterprise Content Management (ECM), and Customer Communication Management (CCM) solutions. This wasn't random diversification—it was strategic orchestration. ECM handled the capture, storage, and retrieval of content. BPM automated the workflows around that content. CCM managed how that content was communicated to customers. Together, they formed a complete loop of enterprise information management.

The platform philosophy was radical for an Indian software company in the 2000s. "Newgen's customers use the platform to rapidly design, build and implement enterprise-grade custom applications through its intuitive, visual interface with minimal coding". This low-code approach, years before the term became fashionable, meant that business users—not just IT departments—could create applications. It was democratization of software development, India-style.

Global expansion followed a methodical pattern. "We made sure to have a good presence in various regions and not only India. We ventured into MEA, APAC, and the US markets to expand our horizons. We also recently opened an office in Australia". The Middle East and Africa proved particularly receptive—regions undergoing rapid modernization but lacking legacy infrastructure. Newgen wasn't competing with entrenched vendors; they were often the first enterprise software many of these organizations deployed.

The enterprise sales playbook Newgen developed during this period was masterful. Unlike Western vendors who led with technology, Newgen led with business outcomes. They didn't sell software; they sold transformed loan processing times, reduced customer onboarding cycles, and automated compliance workflows. Every sale was a consulting engagement wrapped in a product implementation.

The funding landscape shifted dramatically during this decade. IDG Ventures India and Ascent Capital purchased minority stakes from HSBC PE (HAV 2 Mauritius Fund), with Ascent investing ₹104.7 million and IDG ₹114.7 million. This wasn't just capital—it was validation. Global investors were betting on an Indian product company at a time when "Indian software" still meant "services."

The company's 250-member strong R&D team made a huge difference. "In order to enhance the existing products and develop new ones, we keep investing in our R&D department. This helps us maintain technical control over the design and development of our products. The products of the R&D activities will continue to differentiate us from our competitors and position us well for winning complex projects".

Building for Fortune 500 companies from India required a different mindset. These weren't customers you could afford to fail. Newgen developed what became their signature approach: start with a pilot, prove value quickly, then expand systematically. They became masters of the "land and expand" strategy before Silicon Valley coined the term.

The platform approach versus point solutions debate was definitively settled during this period. While competitors offered best-of-breed solutions for specific problems, Newgen offered a Swiss Army knife—perhaps not the absolute best at any single function, but unbeatable in versatility and integration. For enterprises tired of stitching together multiple vendors' products, Newgen's integrated platform was a revelation.

By 2010, the three pillars weren't just product categories—they were moats. Each additional customer made the platform stronger. Each implementation taught them something new about enterprise workflows. Each customization became a feature that benefited everyone. Network effects, it turns out, apply to enterprise software too.

"The culture of innovation in the company has enabled us to grow and retain our relationships with customers. Thus we were able to diversify our product and service offerings, as well as maintain competitiveness in industries like shared services, pharmaceuticals, and utilities". This wasn't just geographic or vertical expansion—it was systematic capability building, turning each customer engagement into platform enhancement.

The decade closed with Newgen positioned uniquely in the global enterprise software landscape: Indian roots with global reach, product DNA with services expertise, platform breadth with vertical depth. They had built something that shouldn't have been possible—a world-class enterprise software platform from a country known for IT services, not products. The stage was set for their next act: going public and competing with the giants.

V. The IPO Journey & Going Public (2015-2018)

By 2015, Newgen had quietly built an enterprise software powerhouse. With 600 employees spread across India, US, Canada, Singapore, and UAE, the company was generating substantial revenues and had blue-chip clients across the globe. But to compete with Salesforce, Microsoft, and Oracle, they needed something more than organic growth—they needed the credibility and capital that only public markets could provide.

The path to IPO wasn't smooth. FY2016 delivered a harsh lesson in the economics of product development. Higher R&D spending—a deliberate strategic choice to enhance platform capabilities—caused profits to plummet from ₹463.8 million in 2015 to ₹278.2 million in 2016. For a company preparing to go public, this 40% profit drop could have been catastrophic. Lesser management teams might have cut R&D to dress up the numbers.

Instead, Newgen doubled down. The investment paid off spectacularly in FY2017 with an 88% profit growth, validating their thesis that sustained R&D investment, even at the cost of short-term profitability, was essential for long-term competitiveness. This roller-coaster—and management's steady hand through it—would become a key selling point to potential investors.

The IPO process itself was a masterclass in timing and execution. In January 2018, Newgen launched a book-building issue that raised ₹424.62 crore at ₹245 per share, representing 25.03% of post-offer equity. The offering raised approximately ₹1,200 crore in total, giving the company the war chest it needed for global expansion. The IPO was oversubscribed—a remarkable achievement for an enterprise software company from India, a market where investors typically favored IT services firms with predictable revenues over product companies with longer gestation periods.

Listing on both NSE and BSE brought visibility, but more importantly, it brought discipline. Public market scrutiny forced Newgen to articulate its strategy more clearly, report metrics more transparently, and think about growth more systematically. The quarterly earnings call became a forcing function for strategic clarity.

The numbers at IPO told a compelling story: 17 Fortune 500 companies as clients, operations across six countries, and a platform processing millions of documents daily. But the real story was about trust. In enterprise software, nobody gets fired for buying IBM. For an Indian company to break into this circle of trust—to get CIOs at global banks to bet their careers on software from New Delhi—was the real achievement.

Post-IPO, Newgen's positioning shifted subtly but significantly. They were no longer the scrappy Indian alternative to expensive Western software. They were now a publicly-traded, professionally-managed enterprise software company that happened to have cost advantages from its Indian operations. The narrative changed from "cheap" to "value," from "offshore" to "global."

The IPO also catalyzed internal changes. Employee stock options suddenly had real value. Talent acquisition became easier—the best engineers wanted to work for a company whose stock they could track on their phones. Customer conversations changed too; being public meant financial transparency, which paradoxically made enterprise sales easier. CFOs could analyze Newgen's financials before committing to multi-year contracts.

Client concentration, often a concern for enterprise software companies, was remarkably healthy. No single client contributed more than 10% of revenues, and the top ten clients contributed less than 30%. This diversification—painstakingly built over two decades—meant that Newgen wasn't vulnerable to any single customer's decisions.

The use of IPO proceeds revealed strategic priorities: R&D expansion, geographic expansion, and platform enhancement. No flashy acquisitions, no diversification into unrelated areas, no dividend distributions to founders. Every rupee was reinvested into making the platform stronger and reaching more customers.

By early 2018, as the IPO dust settled, Newgen had achieved something remarkable. They had taken an enterprise software company public in India—a market that had seen plenty of IT services IPOs but very few product companies. They had done it profitably, without burning massive amounts of venture capital. And they had done it while maintaining majority founder control, ensuring that the long-term vision wouldn't be sacrificed for quarterly earnings. The public markets had validated what Nigam and Varadarajan had believed since 1992: India could build world-class software products, not just provide services.

VI. The Platform Evolution: Low-Code & Digital Transformation (2018-Present)

The post-IPO era marked Newgen's most dramatic transformation yet. While the world discovered low-code platforms through vendors like OutSystems and Mendix, Newgen had been quietly building these capabilities for years. The launch of NewgenONE platform wasn't just a rebranding exercise—it was the culmination of three decades of platform evolution.

NewgenONE integrated five core capabilities that reads like a who's who of enterprise software buzzwords: AI platform, intelligent process automation, content services, omnichannel engagement, and low-code development. But unlike vendors who bolt on AI as an afterthought, Newgen's implementation was deeply practical. Their AI didn't try to replace humans; it augmented them. Invoice processing that once took hours now took minutes. Loan applications that required days of manual review were pre-processed in seconds.

The shift to low-code was particularly shrewd. "Newgen's customers use the platform to rapidly design, build and implement enterprise-grade custom applications through its intuitive, visual interface with minimal coding". In a world where every company was becoming a software company but faced acute developer shortages, Newgen's platform allowed business analysts to build applications that previously required armies of programmers. It was democratization meets pragmatism.

The revenue model evolution told the real story of transformation. The company systematically shifted from one-time license sales to annuity-based revenues through SaaS, ATS/AMC (Annual Technical Support/Annual Maintenance Contracts), and support services. This wasn't just financial engineering—it was relationship deepening. Subscription customers don't just buy software; they become partners in continuous improvement.

By 2023, cloud services contributed 40% of revenues—a remarkable achievement for a company that had built its reputation on on-premise deployments. The cloud transition, often fatal for traditional enterprise software companies, was managed with surgical precision. Existing customers were given migration paths, not ultimatums. New customers were offered choice, not forced into cloud. The result: growth in both segments.

The strategic shift to GSI (Global System Integrator) partnerships opened doors that direct sales never could. When Accenture or Deloitte recommended Newgen to their clients, it carried weight that no amount of marketing could achieve. These partnerships also solved the implementation challenge—GSIs had armies of consultants who could deploy Newgen's platform at scale.

Innovation metrics painted a picture of sustained investment in the future: 44 patents filed with 23 approved, recognition from Gartner and Forrester as a leader in various categories. But the most telling metric was employee growth: 4,043 employees as of March 2025, with 3% year-over-year growth even as the platform became more efficient. This wasn't the typical software story of automation eliminating jobs—it was about automation creating higher-value roles.

The platform's vertical solutions became increasingly sophisticated. A bank in Nigeria had different needs than a government agency in Singapore, and Newgen's platform could accommodate both without custom development. Pre-built templates for common processes—account opening, claims processing, citizen services—meant implementations that once took years now took months.

The low-code revolution also changed Newgen's competitive positioning. They were no longer competing just with traditional ECM/BPM vendors but with a new generation of digital transformation platforms. Yet their three-decade heritage gave them something these new entrants lacked: deep domain expertise. When a bank needed to digitize complex lending workflows, Newgen had probably done it a hundred times before.

Customer success stories became increasingly impressive. A leading bank reduced account opening time from days to minutes. A government agency processed citizen requests 70% faster. An insurance company automated 80% of claims processing. These weren't incremental improvements—they were fundamental reimaginings of how business processes worked.

The platform philosophy—build once, deploy many—reached its full expression in this era. Every customer implementation enriched the platform. Every new use case became a template others could use. Every integration became a connector in the library. The platform wasn't just software anymore; it was collective intelligence, codified and continuously updated.

As 2025 unfolds, NewgenONE stands as testament to a different path in enterprise software. While Silicon Valley chased consumer apps and burned billions in customer acquisition, Newgen quietly built tools that made enterprises run better. While competitors engaged in feature wars, Newgen focused on outcomes. While others pivoted with every trend, Newgen evolved steadily toward a singular vision: making enterprises more efficient through intelligent automation. The low-code revolution wasn't something Newgen joined—it was something they had been building toward since that frustrated day in a Delhi bank three decades ago.

VII. Business Model & Competitive Moat

The architecture of Newgen's business model reveals a masterclass in enterprise software strategy. Three products—OmniDocs (ECM), iBPS (BPM low-code), and OmniFlow (CCM)—work like interlocking gears, each sale making the next one easier. A bank might start with OmniDocs for document management, add iBPS for loan processing workflows, then implement OmniFlow for customer statements. By year three, Newgen isn't just a vendor—they're woven into the bank's operational DNA.

The vertical focus strategy reads like precision targeting. Banking and Financial Services, Insurance, and Government aren't just the largest segments—they're the ones with the most complex processes, highest compliance requirements, and deepest pockets. But Newgen didn't stop there. They've systematically expanded into 14 other verticals, from healthcare to manufacturing, each expansion informed by lessons from the previous one.

Geographic presence tells a story of calculated expansion. India provided the home base and proof of concept. The Middle East and Africa offered greenfield opportunities with less competition. Asia Pacific brought scale and sophistication. Europe and the United States represented the ultimate validation—if you could win there, you could win anywhere. Each geography wasn't just a market; it was a learning laboratory for product evolution.

The TAM (Total Addressable Market) expansion numbers are staggering: BPM growing to $3.07 billion, CCM to $9.35 billion, and High Productivity aPaaS to $17.77 billion by 2026. But Newgen isn't trying to capture all of it. Their strategy is surgical—focus on enterprises with complex processes, high document volumes, and regulatory requirements. It's the enterprise software equivalent of hunting elephants, not rabbits.

The competitive advantage that stands out isn't technological—it's operational. "Not had a single failed implementation since inception" isn't just a claim; it's a moat built on methodology. Every implementation follows the same playbook, refined over thousands of deployments. Every consultant is trained in the same methodology. Every project manager uses the same tools. This operational excellence means predictability, and in enterprise software, predictability is worth billions.

The R&D focus, with 250 dedicated team members, represents roughly 6% of the workforce—high for an enterprise software company but essential for platform evolution. This isn't R&D for research papers; it's R&D for customer problems. Every quarter, the team analyzes implementation challenges and product gaps, turning customer pain into platform features.

Platform stickiness operates at multiple levels. Technical stickiness comes from deep integration—when Newgen powers core banking workflows, ripping it out means rebuilding fundamental operations. Process stickiness emerges from employee training—hundreds of users who know how to build apps on Newgen's platform. Relationship stickiness develops through continuous engagement—quarterly business reviews, regular updates, co-innovation sessions.

The switching costs are deliberately, almost deviously high. Not through vendor lock-in or proprietary formats, but through value delivery. When a bank has automated 500 processes on Newgen's platform, trained 1,000 employees on the system, and integrated with 50 other applications, the cost of switching isn't just monetary—it's organizational trauma.

The partnership ecosystem amplifies the moat. System integrators like Deloitte and Accenture have trained thousands of consultants on Newgen's platform. Technology partners like Microsoft and AWS have certified integrations. Industry partners have built specialized solutions. Each partnership is a distribution channel, a validation stamp, and a switching barrier rolled into one.

Revenue quality metrics reveal the strength of the model. Customer retention exceeds 90%. Revenue per customer grows annually. New customer acquisition costs are recovered within 18 months. These aren't the metrics of a company selling software; they're the metrics of a company building annuities.

The competitive landscape, with 760 active competitors including giants like Appian and emerging players like Airtable, might seem daunting. But Newgen's positioning is unique—enterprise-grade capabilities at mid-market prices, global reach with local presence, platform breadth with vertical depth. They're not trying to out-feature Salesforce or out-scale Microsoft. They're playing a different game entirely.

The beauty of Newgen's business model is its reflexivity. Each new customer makes the platform stronger. Each new implementation makes the next one easier. Each new market teaches lessons that improve existing markets. It's a virtuous cycle that's been spinning for three decades, accumulating advantages that no amount of venture capital can quickly replicate. In enterprise software, time in market matters, and Newgen has had more time than almost anyone to perfect their model.

VIII. Financial Performance & Unit Economics

The numbers tell a story of remarkable consistency in a notoriously lumpy business. Q4 FY2025 delivered ₹49.72 crore in profit on revenue of ₹350.04 crore—a 14.2% net margin that would make most software companies envious. The full year painted an even rosier picture: ₹315.24 crore profit on ₹1,486.88 crore revenue, maintaining similar margins while scaling significantly.

The 2024 performance acceleration was particularly impressive. Revenue of ₹14.87 billion represented 19.54% year-over-year growth—remarkable for a company of this size without major acquisitions. But the real story was earnings growth of 25.29% to ₹3.15 billion, demonstrating operating leverage kicking in. When software companies achieve this dynamic—revenue growing fast but earnings growing faster—it signals a business hitting its sweet spot.

Margin profile stability at 25% might seem pedestrian compared to SaaS darlings sporting 40% margins. But context matters. Newgen's margins include implementation services, support costs, and significant R&D investment. Strip away services, and the software margins approach 40%. More importantly, these are sustainable margins, not the artificial creations of growth-at-all-costs accounting.

The stock performance validated the operational excellence—a 405.60% gain over three years on BSE. This wasn't meme-stock volatility but steady appreciation reflecting consistent execution. The 52-week range from ₹740.05 to ₹1,795.50 showed healthy volatility without wild swings, the sign of a stock discovered by institutions but not yet played by traders.

Trading at 8.05x book value might seem expensive, but for a software company with minimal tangible assets and significant intangible value, it's actually reasonable. The real assets—code, customer relationships, implementation methodology—don't show up on traditional balance sheets. The market is pricing in these invisible assets.

The ₹3 billion cash reserve tells its own story. In an industry where companies routinely burn cash for growth, Newgen generates it. This isn't idle cash either—it's strategic flexibility. It means they can pursue acquisitions without dilution, invest in R&D without worry, and weather downturns without layoffs.

The 20% payout ratio strikes a perfect balance—enough to reward shareholders but retaining 80% for growth. This isn't a mature software company milking maintenance revenues; it's a growth company that happens to be profitable. The dividend is a signal of confidence, not a consolation prize for low growth.

SaaS transition economics revealed sophisticated financial management. Rather than forcing customers to the cloud and taking short-term revenue hits, Newgen managed parallel models. License revenue declined gradually as subscription revenue grew, maintaining total revenue growth throughout. It's the financial equivalent of changing an airplane engine mid-flight.

Customer lifetime value versus acquisition cost metrics, though not explicitly disclosed, can be inferred from retention rates and revenue growth. With 90%+ retention and growing revenue per customer, CLV likely exceeds CAC by 5-10x—the hallmark of a healthy SaaS business. The land-and-expand model means initial deals might be marginal, but lifetime relationship profitability is substantial.

Revenue mix evolution showed strategic discipline. Annuity revenues (SaaS, support, maintenance) grew from 30% to over 50% of total revenue in five years. This predictability transformed Newgen from a lumpy license business to a smooth subscription business, making financial planning easier and valuations higher.

Geographic revenue distribution revealed another strength—no single market dominance. India contributed 40%, MEA 25%, APAC 20%, and developed markets 15%. This diversification meant currency fluctuations, economic downturns, or political instability in any single region couldn't derail the company.

The unit economics at the product level were even more impressive. The platform approach meant R&D costs were amortized across all products. A feature developed for banking could be reused in insurance. An integration built for one customer became available to all. This operating leverage meant that marginal costs decreased with scale—the holy grail of software economics.

Working capital management showed operational maturity. Despite being in enterprise software with typically long sales cycles, Newgen maintained negative working capital in many quarters—collecting from customers faster than paying suppliers. This cash generation machine funded growth without external capital.

The financial performance wasn't just about historical numbers—it was about predictability. Quarter after quarter, Newgen delivered within guidance ranges. No surprise write-offs, no massive one-time charges, no accounting restatements. In a world where software companies routinely "adjust" earnings, Newgen's clean financials stood out. The message was clear: this is a business built for the long term, managed conservatively, and delivering consistently. For investors seeking exposure to digital transformation without the volatility of high-flying SaaS stocks, Newgen offered a compelling alternative—growth with profitability, innovation with stability.

IX. Playbook: Lessons in Building Enterprise Software

Building enterprise software in emerging markets isn't just different from doing it in Silicon Valley—it's almost the opposite playbook. Where Valley startups chase product-market fit through rapid iteration, Newgen spent years understanding market problems before writing code. The loan processing frustration that sparked Newgen wasn't unique to one bank; it was systemic across Indian financial services. This deep problem understanding, born from proximity to inefficiency, became Newgen's first advantage.

The platform versus point solution debate that rages in enterprise software was settled early at Newgen through necessity, not choice. Indian enterprises couldn't afford to buy twenty different software packages like their Western counterparts. They needed Swiss Army knives, not specialized tools. This constraint-driven innovation forced Newgen to build platforms when everyone else was building features. Today, when Salesforce acquires companies to build a platform, Newgen has been platform-native for three decades.

Customer focus at Newgen transcended the usual "customer-first" platitudes. With 500+ active clients including Fortune 500 companies, the company developed what they call "implementation anthropology"—studying not just what customers say they need, but how they actually work. The insight that Indian banks processed loans differently from American banks, which differed from Middle Eastern banks, led to configurable workflows rather than rigid processes. This cultural sensitivity in software design became a competitive advantage as Newgen expanded globally.

Going global from India required timing that was part strategy, part serendipity. The 2000s were perfect—India's IT reputation was established through services companies, making buyers receptive to Indian software. But Newgen didn't lead with "we're from India" (implying cost advantages); they led with "we've solved this problem hundreds of times" (implying expertise). The sequencing mattered too: prove yourself in India, expand to similar emerging markets, then tackle developed markets with references and refined products.

Managing the shift from license to subscription revealed operational sophistication. Rather than a "big bang" transition that many software companies attempted (and failed), Newgen ran parallel models for years. License buyers weren't forced to subscribe; subscribers weren't penalized with higher prices. This respect for customer choice meant slower transition but higher retention. By the time the shift was complete, it felt inevitable rather than imposed.

Low-code as a strategic differentiator wasn't about jumping on a trend—it was about solving a problem Newgen had observed for decades. Enterprises had more process optimization ideas than IT capacity to implement them. Business users understood their problems better than IT but couldn't code solutions. Low-code bridged this gap, turning business analysts into application developers. But unlike pure low-code players, Newgen's platform could handle complexity when needed—you could start with drag-and-drop and drop into code when necessary.

Building for complexity while maintaining simplicity became Newgen's design philosophy. The interface that a bank clerk sees is simple—click here, upload there, approve this. But underneath, the platform handles dozens of regulations, thousands of rules, millions of documents. This "simplicity on top, complexity below" architecture took years to perfect but became unassailable once achieved.

Capital efficiency in software businesses is often talked about but rarely achieved. Newgen reached cash-flow positive early and stayed there. No massive venture rounds, no growth-at-all-costs mentality, no blitzscaling. This wasn't conservatism—it was discipline. Every rupee spent had to generate returns. Every hire had to add value. Every feature had to solve real problems. This efficiency meant Newgen could compete with venture-funded competitors who had 10x their capital but 0.1x their discipline.

The implementation methodology Newgen developed deserves its own Harvard case study. Start small with a pilot that delivers value in weeks, not months. Build credibility through quick wins. Expand gradually to adjacent processes. Never customize core platform code; configure instead. Train local champions who become internal evangelists. This methodology, refined over thousands of implementations, turned what competitors considered a cost center into a competitive advantage.

Partnership strategy reflected pragmatic wisdom. Rather than trying to build everything, Newgen integrated with everything. Microsoft Office, SAP, Oracle, AWS—if enterprises used it, Newgen integrated with it. This "Switzerland" approach meant Newgen could slot into any technology stack. Competitors who demanded rip-and-replace lost to Newgen's coexist-and-enhance approach.

The R&D philosophy—customer-driven but not customer-dictated—balanced market needs with technical vision. Customers might ask for faster horses, but Newgen built cars. The key was understanding the underlying need (faster transportation) versus the expressed want (faster horses). This interpretive layer between customer feedback and product development meant Newgen's platform evolved coherently rather than becoming a feature potpourri.

The ultimate lesson from Newgen's playbook: in enterprise software, patience is a strategy. While consumer startups measure progress in months, enterprise software measures it in decades. Customer relationships are cultivated over years. Platform capabilities accumulate over decades. Trust is built one successful implementation at a time. Newgen's three-decade journey proves that in enterprise software, the tortoise doesn't just beat the hare—it builds a better road while the hare is sleeping.

X. Bull vs. Bear Case & Future Outlook

The Bull Case: Platform Power in the Digital Transformation Era

The bull case for Newgen starts with financial fundamentals that would make Benjamin Graham smile. Trading at 8.05x book value for a software company generating 25% margins and growing at 20% annually isn't expensive—it's reasonable for quality. The promoter holding of 53.78% isn't just skin in the game; it's the entire dermis. When founders still control the majority after going public, they're playing a different game than quarterly earnings management.

Digital transformation tailwinds are hurricane-force and accelerating. McKinsey estimates $2.3 trillion in annual spending on digital transformation globally, growing at 16% annually. Newgen sits perfectly in this sweet spot—not selling transformation consulting like Accenture, not providing basic infrastructure like AWS, but delivering the actual tools that make transformation real. Every company becoming a "digital-first" organization needs exactly what Newgen sells.

The low-code platform differentiation becomes more valuable as the developer shortage intensifies. With demand for software developers exceeding supply by 4x globally, platforms that let business users build applications aren't nice-to-have—they're essential. Newgen's three-decade head start in this space, combined with enterprise-grade security and scalability, creates a moat that venture-funded startups can't quickly cross.

The expanding TAM in all three segments—BPM, ECM, and CCM—means Newgen can grow without entering new markets. They're fishing in a pond that's becoming an ocean. As regulations increase, document volumes explode, and customer expectations rise, the need for Newgen's platform only intensifies.

The crown jewel of the bull case: "no failed implementations since inception." In enterprise software, where 60-70% failure rates are common, this isn't just impressive—it's almost unbelievable. This track record means reference-ability that money can't buy. When a CIO calls another CIO to ask about Newgen, they hear success stories, not horror stories.

Customer stickiness approaching 90% creates compounding advantages. Each year, existing customers buy more, integrate deeper, and become harder to dislodge. The cohort economics likely show negative churn—customers from five years ago spending more today than their initial contracts. This is the enterprise software equivalent of a perpetual motion machine.

The Bear Case: David Among Goliaths

The bear case starts with competitive reality. Newgen competes with Salesforce (market cap: $200+ billion), ServiceNow ($150+ billion), and Microsoft (₹2+ trillion). These giants have resources Newgen can't match—thousands of engineers, billions in R&D, and enterprise relationships spanning decades. When Microsoft bundles competing functionality into Office 365, Newgen's value proposition erodes overnight.

The 760 active competitors, including well-funded players like Appian and Airtable, create a brutal competitive landscape. The low-code space particularly has become a venture capital feeding frenzy, with billions flowing into startups promising to democratize application development. Newgen's measured approach might be overtaken by blitzscaling competitors who prioritize growth over profitability.

Dependency on emerging markets creates macro vulnerability. India, Middle East, and Asia Pacific contribute 85% of revenues—regions more susceptible to currency fluctuations, political instability, and economic volatility. A significant rupee depreciation or Middle East conflict could materially impact results. Developed market expansion, while strategic, requires competing against entrenched vendors with home-field advantages.

Execution risk in developed markets looms large. Success in India doesn't guarantee success in America. Cultural differences, sales cycles, compliance requirements, and customer expectations vary dramatically. Many Indian software companies have stumbled trying to crack the US market. Newgen's measured approach might be too slow for markets that respect aggression over patience.

Technology disruption from AI-native platforms represents an existential threat. While Newgen has added AI capabilities, companies built AI-first from day one might leapfrog decades of development. When OpenAI or Anthropic decides to enter enterprise automation, their AI capabilities could make traditional workflow tools obsolete. Newgen's three-decade code base could become a liability rather than an asset.

The subscription transition, while successful so far, still carries risk. If growth slows, the recurring revenue base might not compensate for lost license revenues. The company could face the dreaded "transition trough" where old model revenues decline faster than new model revenues grow.

Future Vectors: The Path Forward

AI and automation integration represents both the biggest opportunity and greatest threat. Newgen's approach—practical AI that enhances human work rather than replacing it—seems sensible. But the pace of AI advancement might demand more radical transformation. The company that successfully merges large language models with enterprise workflows will dominate the next decade.

Industry-specific solution depth offers a differentiation path. Rather than competing on features, Newgen could become the definitive platform for specific verticals. Own banking in emerging markets. Dominate government services in Asia. This focused approach trades TAM for win rates—a potentially winning strategy.

Geographic expansion priorities will determine Newgen's trajectory. The US market remains the prize—crack it, and valuation multiples expand dramatically. But it's also the graveyard of international software ambitions. The alternative—doubling down on emerging markets—offers easier growth but lower multiples.

M&A opportunities could accelerate capability building. With ₹300 crore in cash and strong cash generation, Newgen could acquire complementary technologies or geographic presence. But their historical preference for organic growth suggests any acquisition would be carefully considered rather than growth-driven.

The ultimate question: Can Newgen transition from a successful regional player to a global platform leader? The ingredients are there—proven products, strong finances, experienced management. But the competition is fierce, the technology landscape is shifting, and the window for establishing global enterprise software leaders might be closing. Newgen's next five years will determine whether they join the ranks of global enterprise software leaders or remain a highly profitable regional champion. Either outcome could reward shareholders, but the paths and payoffs differ dramatically.

XI. Recent News

The latest developments from Newgen showcase a company firing on all cylinders. Q4 FY2025 results, announced on May 2, 2025, delivered impressive performance with revenue rising 15% year-over-year. Chairman Diwakar Nigam noted that "FY'25 was a year of healthy revenue growth and margin expansion for Newgen. Growth was driven by strong license and implementation revenues across markets. Our large customer base, with billing of over Rs 5 crores, increased to 87 customers from 65 customers last year".

The full-year numbers were even more impressive. Newgen reported ₹1,487 Cr revenue in FY'25, up 20% YoY; PAT at ₹315 Cr, up 25% YoY. The company's large customer base, with billing over Rs 5 crores, increased to 87 customers from 65 customers last year—a clear indication of successful land-and-expand strategies.

AI Agents: The Future is Here

Perhaps the most exciting development is Newgen's aggressive push into AI. CEO Virender Jeet announced: "Newgen continues to accelerate its AI-first strategy with significant investments in AI-driven products and solutions. This year, we have launched groundbreaking AI agents – Lumyn, Harper, and Marvin – which have already demonstrated their potential through several promising and viable use cases".

These aren't just buzzword-compliant features bolted onto existing products. Each AI agent serves a distinct purpose:

-

LumYn is an AI agent that helps financial institutions identify revenue growth opportunities by analyzing customer behavior. Its conversational AI simplifies data analysis, while a low-code environment enables fast deployment and experimentation

-

Harper is an AI agent that helps you audit 100% of your calls, highlights what your customers want, and provides you with clear steps to improve conversions. It simplifies sales and enhances customer experience for your business

-

Marvin is your go-to agent for automating routine tasks and processes. With advanced AI, Marvin streamlines operations, handles data entry, reduces errors with remarkable accuracy, and enhances overall productivity

Geographic Expansion Bearing Fruit

The quarter specifically witnessed strong growth and deal wins in the US region. This is significant—cracking the US market has been the holy grail for Indian software companies, and Newgen appears to be gaining real traction. The pipeline is strong for the first two quarters of the next fiscal year, suggesting momentum will continue.

Industry Recognition Continues

The accolades keep coming. Newgen Software has been named among the 200 Best Under a Billion Software & Services Organizations by Forbes Asia. The award ceremony was held on October 23, 2024, at a Forum and Awards dinner in Hong Kong. Forbes Asia's Best Under A Billion list spotlights 200 top-performing publicly listed companies in the Asia-Pacific region with annual sales under $1 billion. From a universe of over 20,000 small and midsized companies in the region, these 200 Best Under A Billion companies have track records of exceptional corporate performance.

On the analyst front, Newgen maintained its strong positioning: - Named a niche vendor in the Gartner Magic Quadrant for Enterprise Low-Code Application Platforms (LCAP) 2024 for the fifth consecutive year - Named a leader in the IDC MarketScape Report for Intelligent Customer Communications Management and Automated Document Generation and Customer Communication Management - Named a "Leader" in The Forrester Wave: Content Platforms, Q1 2025, second time in a row

Strategic Partnerships and Platform Evolution

Newgen was included among 'Notable Vendors' in Forrester's The Digital Process Automation Software Landscape, Q2 2025 report. The Forrester report defined DPA software as 'platforms that develop process applications with low-code and advanced programming principles with modeling, orchestration, dynamic case management, and AI-led support.' The report emphasized the importance of understanding the value leaders can expect from a DPA vendor.

Stock Market Response

The market has responded enthusiastically to these developments. Newgen Software Technologies surged 9.10% to Rs 1,077.50 after the company's consolidated net profit jumped 21.73% to Rs 108.34 crore on a 12.8% rise in revenue from operations to Rs 429.89 crore in Q4 FY25 over Q3 FY25. Analysts upgraded the stock to 'Buy' from 'Hold,' projecting FY26 revenue growth of 20% supported by a robust order book and strategic investments.

Looking Ahead

Management expressed optimism, with Nigam stating: "Looking ahead, we see strong momentum building across our business and are energized by the growth prospects ahead". With AI agents gaining traction, US expansion accelerating, and the platform evolution continuing, Newgen appears positioned for its next phase of growth. The company's ability to maintain 20%+ growth while improving margins suggests the business model is reaching maturity just as the market opportunity is exploding.

XII. Links & Resources

Company Resources

- Newgen Investor Relations: newgensoft.com/company/investor-relations/

- Annual Reports & Quarterly Results: Available on NSE and BSE websites

- Company Presentations: Investor deck updated quarterly on company website

Stock Information

- NSE Symbol: NEWGEN

- BSE Code: 540900

- Current Market Cap: ₹12,210 Crore (as of latest data)

- 52-Week Range: ₹740.05 - ₹1,795.50

Industry Reports & Analysis

- Gartner Magic Quadrant for Enterprise Low-Code Application Platforms

- Forrester Wave: Content Platforms, Q1 2025

- IDC MarketScape for Intelligent Customer Communications Management

- Forbes Asia Best Under A Billion 2024 Recognition

Platform & Product Information

- NewgenONE Platform Overview: Core platform capabilities

- AI Agents (Lumyn, Harper, Marvin): Agentic AI capabilities

- Low-Code Development Platform: Application development tools

- Industry Solutions: Banking, Insurance, Government verticals

Key Contacts

- Compliance Officer: Aman Mourya, Company Secretary ([email protected])

- Investor Relations: Deepti Mehra Chugh, Head – Investor Relations ([email protected])

- Registered Office: E-44/13, Okhla Phase-II, New Delhi – 110020

Recommended Reading on Indian IT Evolution

- "The Indian IT Story" - Understanding the services-to-products transition

- NASSCOM Reports on Indian Software Product Industry

- Digital Transformation in Emerging Markets studies

Competitive Intelligence

- Comparison matrices with Appian, OutSystems, Mendix

- Enterprise software market sizing reports

- Low-code platform adoption studies

Technology Deep-Dives

- Low-code vs traditional development ROI studies

- AI in enterprise automation whitepapers

- Cloud migration best practices for enterprise software

Note: This analysis is for informational purposes only and does not constitute investment advice. Readers should conduct their own due diligence before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube