Innodisk: From SATADOM to Edge AI Dominance

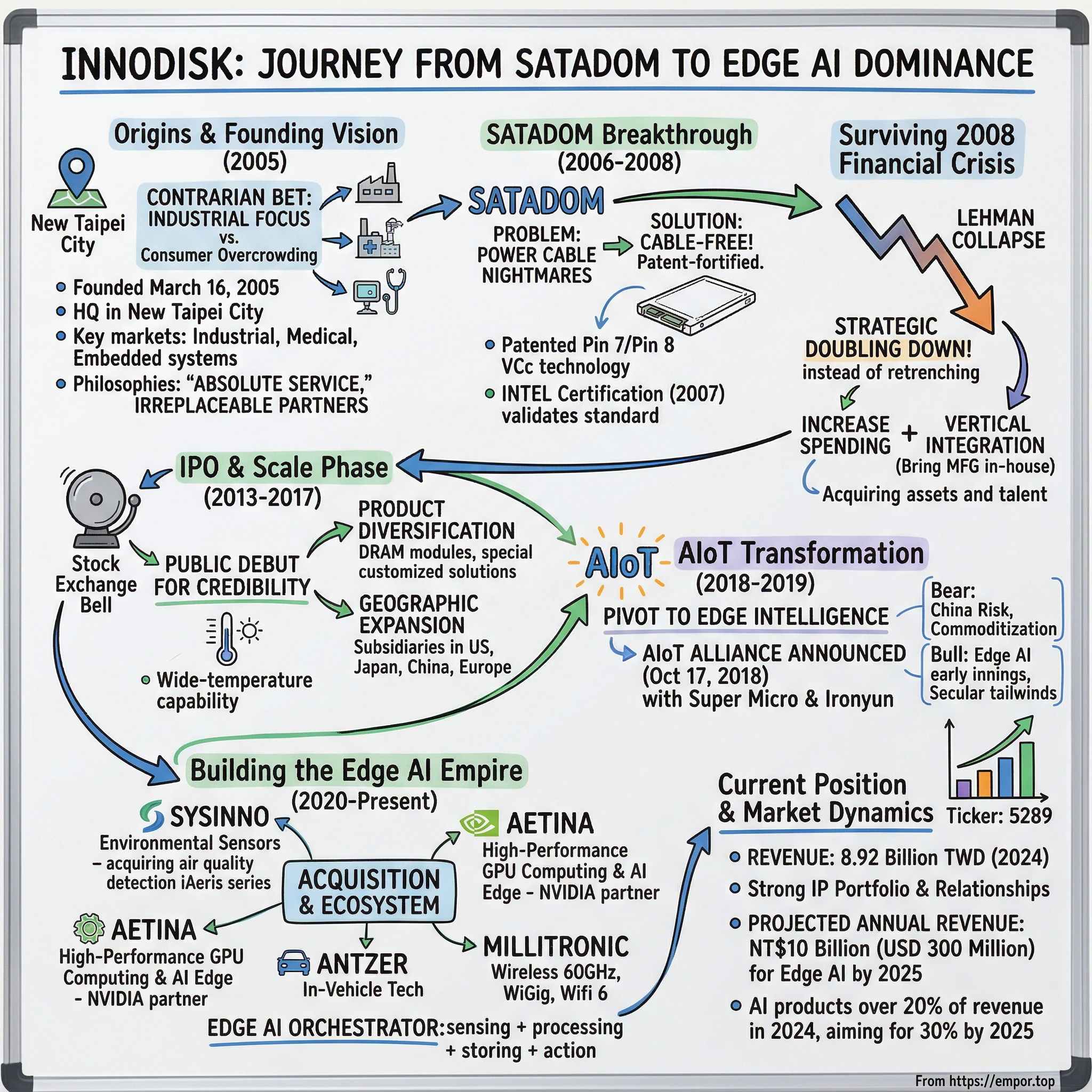

Picture a small office in New Taipei City, Taiwan, March 2005. The aftermath of the dot-com crash still lingers, consumer electronics manufacturers are locked in a brutal race to the bottom, and a group of engineers is huddled around a whiteboard sketching out what seems like a contrarian bet: forget consumers, focus on industrial. The company was founded on March 16, 2005 and is headquartered in New Taipei City, Taiwan. While giants like SanDisk and Kingston chase retail shelves and razor-thin margins, these founders see opportunity where others see obsolescence—in factory floors, medical devices, and embedded systems that demand something consumer products could never deliver: absolute reliability.

This was the birth of Innodisk Corporation, a company that would transform from an unknown Taiwanese startup into a multi-billion TWD powerhouse by mastering the art of saying "no" to 99% of the storage market to own the 1% that actually mattered.

Introduction & Episode Roadmap

The storage industry in 2005 was experiencing a gold rush. Flash memory prices were plummeting, digital cameras were everywhere, and USB drives were the hot consumer gadget. Yet here was Innodisk, deliberately turning away from this massive consumer opportunity to chase industrial customers with their peculiar demands: storage that could survive -40°C in Siberian oil rigs, operate flawlessly in casino gaming machines running 24/7, and withstand the vibrations of mining equipment.

The company offers flash storage products, such as solid state drives (SSDs); SATA Slim, nano SSD, compact flash memory card, SATADOM horizontal and vertical, embedded disk card; SD and MicroSD cards; USB and EDC; and CFexpress. But this wasn't just about rugged hardware. The real genius lay in what would become their breakthrough innovation: eliminating the very cables that everyone else took for granted.

How do you build a storage empire by focusing on the most demanding, lowest-volume customers? How do you survive a global financial meltdown when your competitors are slashing R&D? And how do you pivot from being a component supplier to an AI platform company without losing your industrial DNA? This is the story of Innodisk's remarkable journey from SATADOM pioneer to edge AI orchestrator, a transformation that saw them grow revenue to 8.92 billion TWD in 2024 while maintaining the discipline to stay focused on the unsexy markets that built their moat.

Origins & Founding Vision (2005)

Taiwan's technology ecosystem in 2005 was at an inflection point. The island had successfully transitioned from assembly to design, TSMC was establishing semiconductor dominance, and ODMs like Quanta were manufacturing the world's laptops. But in storage, Taiwan was still playing catch-up to American and Japanese giants. The consumer market seemed like the obvious entry point—except everyone else thought the same thing.

The founding team at Innodisk saw the chaos differently. Richard Lee founded Innodisk in 2005, and expected to bring momentum to the advancement of the industry. They noticed something peculiar: while consumer storage vendors fought over pennies, industrial customers were desperately underserved. A casino operator in Las Vegas couldn't use consumer SSDs that might fail after a million write cycles. A medical imaging company in Germany needed storage that wouldn't corrupt during an MRI scan. Defense contractors required solutions that could operate in extreme temperatures without any performance degradation.

The founding philosophy wasn't just about making reliable products—it was about becoming irreplaceable partners. They called it "Absolute Service," a commitment that went beyond selling hardware to understanding each customer's specific nightmare scenario and engineering around it. Products are used in the aerospace, embedded systems, server applications, casino gaming, in-vehicles, ICAP Air, and AIoT, as well as surveillance, automation, networking, healthcare, and retail markets.

While competitors automated customer service and pushed customers toward standard products, Innodisk engineers would spend weeks at customer sites, observing how products actually failed in the field. When a client needed storage for a railway monitoring system that would experience constant vibrations, they didn't just offer a "rugged" option—they built custom dampening solutions and tested them on actual trains. This wasn't scalable, but it was defensible. Each solution created knowledge that couldn't be easily copied, relationships that couldn't be poached, and specifications so precise that switching costs became prohibitive.

The initial focus deliberately spread across geographies to reduce concentration risk. Rather than dominating one market, they established beachheads in Taiwan, Asia, Japan, Germany, China, Europe, the United States, and internationally. Each market taught them different failure modes: Japanese customers obsessed over consistency, Germans wanted extensive documentation, Americans prioritized speed-to-market. This geographic diversity would prove crucial when the 2008 crisis hit, as no single market collapse could sink the company.

The SATADOM Breakthrough & Patent Innovation (2006-2008)

The conference room at Innodisk's headquarters in 2006 witnessed a debate that would define the company's future. Engineers had been wrestling with a persistent customer complaint: power cables in embedded systems were a nightmare. They got tangled, came loose during shipping, and in cramped server chassis, there simply wasn't room for traditional cable management. The conventional solution was to make cables more reliable. Innodisk's solution was to eliminate them entirely.

With our patented Pin 7 / Pin 8 Vcc technology, these drives enable plug-and-play functionality, eliminating the need for additional power cables and ensuring a streamlined, cable-free setup. The innovation seemed almost too simple: why not power the drive directly through the SATA interface itself? But simplicity in concept masked complexity in execution. The SATA specification wasn't designed for this. Pin 7 and Pin 8 were sitting there, technically available but never utilized for power delivery. Making this work required not just electrical engineering but deep understanding of the SATA protocol, thermal management to handle power delivery through the same interface, and most importantly, ensuring zero compatibility issues with the thousands of motherboards already in the field.

The SATADOM—SATA Disk On Module—was born from months of iterations. Early prototypes literally melted. Power delivery was unstable. Some motherboards wouldn't recognize the devices. But each failure taught them something crucial about the edge cases that mattered in industrial applications. Unlike consumer products where you could ship updates later, industrial storage had to work perfectly from day one—lives and millions of dollars could depend on it.

The real masterstroke wasn't just the technology but the patent strategy around it. Rather than filing one broad patent that competitors could design around, Innodisk filed multiple interlocking patents covering every aspect of the implementation. They patented the specific pin configurations, the power management circuitry, the thermal solutions, even the mechanical design that ensured proper seating without cables. By the time competitors realized the value of cable-free storage, Innodisk had built a patent fortress that would take years to navigate around.

Intel's certification of the technology in 2007 changed everything. When the world's largest chip maker validates your non-standard implementation, it becomes the standard. The innovative Pin 8 uses the SATA connector itself as a power supply to drive the device without external cables. It could be connected directly to the SATA on-board socket on a customer's system without an additional power cable. Suddenly, server manufacturers who had been skeptical were placing orders. The cable-free design meant assembly time dropped by minutes per unit—at scale, this translated to millions in savings.

But the true validation came from an unexpected source: counterfeiters. By late 2008, fake SATADOMs were appearing in Shenzhen markets. While the knockoffs violated their patents, Innodisk saw this as proof they'd created something valuable enough to copy. They responded not with lawsuits but with innovation—adding authentication chips, unique serial numbers, and firmware signatures that made genuine Innodisk products verifiable. Customers learned that saving 20% on a counterfeit wasn't worth the risk when a storage failure could shut down a production line costing thousands per minute.

Surviving the 2008 Financial Crisis

September 15, 2008: Lehman Brothers collapses. Within weeks, the global financial system is in freefall. Technology spending freezes overnight. Consumer electronics demand craters. Storage competitors begin mass layoffs, slash R&D budgets, and cancel product roadmaps. At Innodisk's headquarters, the leadership team faces a defining choice: retrench or double down.

The conventional playbook demanded cuts. Reduce headcount, minimize inventory, preserve cash. But CEO Randy Chien saw opportunity in crisis. While competitors retreated, Innodisk did something that seemed insane: they increased R&D spending. Experiences from past downturns suggest that companies having the farsightedness and the courage to invest more in R&D and innovation activities while others are cutting back have a significant advantage in the inevitable upswing that will come.

The logic was counterintuitive but sound. Their industrial customers—factories, medical equipment manufacturers, defense contractors—couldn't simply stop operating. While consumer spending collapsed, industrial systems still needed maintenance, upgrades, and replacements. Moreover, with consumer storage prices in freefall, component costs plummeted. Innodisk could now afford to use higher-grade components while maintaining margins, further differentiating their reliability.

They also made a crucial strategic decision: vertical integration. While competitors outsourced more production to cut costs, Innodisk brought manufacturing in-house. They acquired testing equipment at fire-sale prices from failing competitors. They hired the best engineers being laid off elsewhere, particularly those with deep expertise in firmware and failure analysis. This wasn't about cost-cutting—it was about control. When you promise industrial-grade reliability, you can't blame a supplier when something fails.

The crisis also accelerated a shift in customer relationships. As weaker storage vendors failed or withdrew from industrial markets, their customers needed new suppliers urgently. Innodisk's reputation for reliability became even more valuable when switching suppliers carried existential risk. They gained customers that, in normal times, would have taken years to win. A European railway system that had used the same storage vendor for a decade switched to Innodisk after their supplier couldn't guarantee delivery. That customer remains with Innodisk today.

The 2008 crisis taught Innodisk a crucial lesson: in industrial markets, antifragility beats efficiency. While competitors optimized for margins, Innodisk optimized for survival—their customers' and their own. This philosophy would guide them through the next phase of growth and position them perfectly for the AIoT revolution that nobody saw coming.

IPO and Scale Phase (2013-2017)

The bell ringing ceremony at the Taiwan Stock Exchange in 2013 marked more than just Innodisk's public debut—it signaled the transformation of a scrappy startup into an industrial storage institution. Innodisk Corporation was founded in 2005 and is headquartered in New Taipei City, Taiwan, and after eight years of patient building, they were ready to scale.

Going public wasn't about the money—Innodisk was already profitable and cash-flow positive. It was about credibility. Industrial customers making 10-year infrastructure decisions needed assurance their storage vendor would outlive their equipment. Public company governance, audited financials, and stock market validation provided that confidence. The IPO proceeds weren't spent on marketing or acquisitions but poured into the unglamorous work of expanding product reliability: more testing equipment, longer validation cycles, and redundant supply chains.

The product portfolio expansion from 2013 to 2017 revealed Innodisk's systematic approach to market domination. Rather than revolutionary breakthroughs, they executed thousands of incremental innovations. DRAM modules comprising industrial embedded DRAM memory modules, server workstation memory, wide temperature/ultra-temperature, and special customized solutions became a significant revenue driver. But the real innovation was in customization at scale—creating a platform that could efficiently deliver semi-custom solutions without the cost penalty of full customization.

Wide-temperature DRAM that operated from -40°C to +85°C opened up entirely new markets: outdoor surveillance systems in Siberia, automotive applications in the Sahara, mining equipment in the Australian outback. Each extreme environment taught them something new about failure modes. They discovered that it wasn't just temperature that mattered but thermal cycling—a device that could survive sustained heat might fail when rapidly alternating between hot and cold. This knowledge, accumulated through thousands of field failures and successes, became an irreplaceable competitive moat.

Geographic expansion during this period followed industrial logic, not conventional market sizing. Subsidiaries were established in the following years, with the U.S. subsidiary in October 2008, the subsidiary in Japan in February 2010 and a subsidiary in China in January 2011. They didn't chase the largest markets but the most demanding ones. The Japanese subsidiary wasn't created because Japan was a huge market but because Japanese quality requirements would push Innodisk to improve. German customers' obsession with documentation forced them to systematize their technical knowledge. American customers' rapid prototyping demands improved their response times.

By 2017, Innodisk had achieved something remarkable: they'd become the default choice for applications where failure wasn't an option. The company's revenue trajectory was steady rather than explosive, growing from hundreds of millions to billions of TWD through compound improvements rather than hockey-stick moments. This wasn't the path to becoming a unicorn, but it was the path to becoming indispensable.

The AIoT Transformation (2018-2019)

October 17, 2018, The Westin Taipei. Randy Chien steps onto the stage not to announce a product but to declare a transformation. The AIoT Alliance was announced at a conference held on Wednesday, October 17 that also showcased comprehensive solutions on smart city data storage, edge computing, software, analytics, cloud-management and more. The industrial storage company was positioning itself at the center of the AIoT (Artificial Intelligence of Things) revolution.

The pivot wasn't reactive—Innodisk had been preparing for years. They recognized that industrial IoT would generate massive amounts of data, but the real value would come from processing that data at the edge. Their storage expertise gave them a unique vantage point: they already sat at the edge, in the devices generating the data. Why not expand from storing data to making it intelligent?

Innodisk president Randy Chien has strongly encouraged this partnership and states: "As the leading industrial-grade storage provider our next step is the AIoT market which will be major business focus for the next few years. However, realizing AI in the industrial field requires not only expertise and technology, but also a deep understanding of different vertical markets". The formation of the AIoT Alliance alongside partners like Super Micro and Ironyun wasn't just marketing—it was architectural. Innodisk understood they couldn't build everything themselves. Instead, they would become the orchestration layer, the trusted integrator that could combine AI capabilities with industrial reliability.

The strategic masterstroke came in December 2019 with the Sysinno acquisition. With the acquisition of Sysinno, Innodisk Group doubles down on its vision of a smart future where innovative connected products improve business and life in any environment. Innodisk combined with Sysinno's advanced sensor technologies, bring considerable synergies that will create long-term value for customers and shareholders. Sysinno's state-of-the-art products include the iAeris series of air quality detection units, as well as cloud-connected, IoT-enabled controllers that help provide a 360-degree solution to air quality concerns. iAeris's cutting-edge technology enables it to track up to nine environmental factors critical to both operational safety and quality of life, including temperature, humidity, CO, CO2, PM10 and PM2.5, TVOC, and formaldehyde—delivered with industrial-grade accuracy in real time.

Randy Chien said: "Innodisk and Sysinno share the same vision of a connected future powered by AIoT". This wasn't Innodisk buying AI capability—it was about understanding that edge intelligence requires sensing, storage, processing, and action. Sysinno's environmental sensors weren't just collecting data; in semiconductor fabs, pharmaceutical clean rooms, and food processing facilities, air quality directly impacts yield and safety. A few parts per million of contamination could destroy millions in product. Sysinno's sensors, combined with Innodisk's storage and edge processing, could predict and prevent these disasters.

The integration revealed Innodisk's evolved M&A philosophy. Rather than strip-mining acquisitions for technology, they preserved Sysinno's identity and expertise while providing industrial channels and reliability engineering. Sysinno President Linch Lin said: "Joining Innodisk Group means that Sysinno is better positioned than ever to deliver exceptional products to our customers". The message to the market was clear: Innodisk wasn't just pivoting to AIoT—they were building an empire of specialized subsidiaries, each a leader in their niche, unified by industrial-grade reliability.

Adding the IPA (Intelligent Peripheral Appliance) division formalized this transformation. No longer were they just responding to storage RFPs; they were designing complete edge AI solutions. A smart factory didn't just need SSDs—it needed cameras for quality inspection, sensors for predictive maintenance, edge servers for real-time processing, and software to orchestrate it all. Innodisk could now deliver the entire stack, tested and integrated.

Building the Edge AI Empire (2020-Present)

The COVID-19 pandemic should have been a disaster for a company dependent on industrial customers. Factories shut down. Supply chains shattered. Yet 2020 became an inflection point for Innodisk's edge AI strategy. The pandemic didn't reduce the need for industrial automation—it accelerated it. Factories needed to operate with minimal human presence. Quality inspection couldn't depend on engineers traveling to sites. Remote monitoring went from nice-to-have to mission-critical overnight.

Innodisk's subsidiary ecosystem revealed its strategic value during this period. Aetina high-performance AI edge computing and GPU-accelerated computing; Antzer in-vehicle technologies, with fleet management and data collection capabilities; Millitronic wireless networking, providing the wireless 60GHz, WiGig and Wifi 6 know-how for the backbone of IoT infrastructure; Sysinno air quality monitoring sensors to round out the measuring package. Each subsidiary addressed a critical piece of the edge AI puzzle. The genius wasn't in any individual acquisition but in how they reinforced each other.

Randy Chien, Chairman of Aetina and Innodisk, remarked, "Aetina stands at the forefront of Innodisk Group's AI initiatives. With the backing of Innodisk's extensive resources and collective experiences from thousands of global clients, Aetina is committed to implementing intelligence at the edge for real-world scenarios". Aetina's GPU expertise, particularly their partnership with NVIDIA, transformed Innodisk from a storage company to an AI compute provider. In 2013, Aetina joined the Innodisk Group, strengthening its corporate foundation with the group's resources.

The transformation from component supplier to solution architect manifested in unexpected ways. When a European manufacturer needed to retrofit legacy equipment with AI-powered predictive maintenance, Innodisk didn't just provide edge servers. They delivered a complete solution: vibration sensors from their sensor division, edge AI processing from Aetina, wireless connectivity from Millitronic, and industrial storage for data logging. More importantly, they provided integration expertise—understanding which AI models worked in resource-constrained environments, how to handle intermittent connectivity, and how to ensure failover without data loss.

Fire Shield SSD, unveiled in 2019, epitomized Innodisk's approach to innovation. The Fire Shield SSD™ consists of a triple layer of protection between the environment and the core components. The layers include flame-resistant copper alloy, drive-protecting connector design, and heat-isolating lining material. After having been bathed in direct flames at 800 degrees Celsius for more than 30 minutes, comparisons show 100% data accuracy before and after tests. While competitors chased consumer markets with faster speeds and higher capacities, Innodisk created storage that could survive literal hellfire. This wasn't a mass-market product—but for applications like aircraft black boxes, industrial accident investigation, and critical infrastructure monitoring, it was irreplaceable.

The financial performance validated the strategy. Despite global semiconductor shortages and supply chain chaos, Innodisk maintained growth. More tellingly, their product mix shifted dramatically. By 2024, AI-related products had grown from negligible to over 20% of revenue, with projections to reach 30% by 2025. Innodisk's consolidated revenue for the first half of 2024 achieved NT$4.366 billion (US$137 million), a slight 4.2% growth from its 2023 performance. Overall, revenue appears to be growing each quarter with a stable gross margin. With the IPC market hitting rock bottom, demands will soon gradually return, making its growth in revenue and profit greater in the second half of 2024 than in the first half.

Current Position & Market Dynamics

Standing at the end of 2025, Innodisk occupies a unique position in the technology landscape. They're not the largest storage company, nor the most visible AI player, yet they've become irreplaceable infrastructure for edge intelligence. In 2024, Innodisk's revenue was 8.92 billion, an increase of 7.24% compared to the previous year's 8.31 billion.

The financial metrics tell only part of the story. The last dividend per share was 10.20 TWD. As of today, Dividend Yield (TTM)% is 4.07%. This isn't a hypergrowth story that venture capitalists love—it's a compound growth story that Warren Buffett would appreciate. Steady margins, consistent dividends, and a business model that becomes stronger with each customer deployment.

The competitive landscape has evolved dramatically from Innodisk's early days. Pure Storage and Western Digital dominate enterprise storage, while specialized industrial players compete in niches. But Innodisk's edge AI transformation has moved them into a different competitive arena. They're not competing with storage companies anymore—they're competing with edge AI platforms, and their industrial heritage gives them unique advantages.

Randy Chien, forecasts that while cloud AI dominated in 2024, attention will turn to edge AI in 2025. He anticipates significant growth in edge AI, fueled by the rise of generative AI and the potential for Artificial General Intelligence, with projected annual revenues reaching NT$10 billion (US$300 million). This projection isn't just optimistic thinking—it's based on concrete pipeline visibility. Innodisk's May and June 2025 revenues each exceeded NT$1 billion (US$34.1 million). May revenue grew 51.10% year-over-year; June grew 37.52% year-over-year, marking the third-highest single-month revenue ever. Total consolidated revenue for January to June 2025 reached NT$5.65 billion, reflecting near-30% annual growth.

The geographic revenue mix reflects both opportunity and risk. China exposure remains significant, creating geopolitical vulnerability. But Innodisk has systematically diversified, with growth in Japan, Europe, and the Americas offsetting China concentration. More importantly, their industrial customers tend to be sticky—when your storage is embedded in critical infrastructure with 10-year lifecycles, switching vendors is nearly impossible.

The shift from selling components to selling intelligence has transformed Innodisk's customer relationships. They're no longer vendors responding to RFPs—they're partners involved from system architecture through deployment. The Pro-AI service has helped Aetina double its business performance and accumulated over 600 AI application cases in recent years. When a smart factory needs to implement visual inspection, Innodisk doesn't just provide the hardware—they help select AI models, optimize for edge deployment, and ensure integration with existing systems.

Playbook: Strategic Lessons

Lesson 1: Find the unsexy niche. Innodisk's founding insight—that industrial storage mattered more than consumer volumes—seems obvious in hindsight. But in 2005, choosing factories over consumers required contrarian courage. The lesson isn't just about avoiding competition but understanding that the most demanding customers often create the most defensible businesses. Every specification that made industrial storage harder to build became a moat against competitors.

Lesson 2: Own the innovation. The SATADOM patent portfolio demonstrates how intellectual property can define markets. But the real lesson goes deeper: Innodisk didn't just patent a technology, they patented a solution to a specific customer pain point. The innovation wasn't removing cables for the sake of elegance—it was understanding that in cramped server chassis, every cable was a potential point of failure and assembly complexity.

Lesson 3: Vertical integration in crisis. While competitors outsourced during the 2008 crisis, Innodisk integrated. This wasn't about cost savings—vertical integration often costs more. It was about control and learning. Every manufacturing step brought in-house meant another variable they could optimize, another failure mode they could understand, another differentiation point competitors couldn't match.

Lesson 4: Platform transformation. The evolution from component supplier to edge AI platform wasn't planned—it emerged from customer needs. But once the pattern became clear, Innodisk systematically built toward it. The lesson: platforms aren't built through grand strategy but through solving adjacent problems for existing customers until the solutions connect into something larger.

Lesson 5: Strategic M&A. The Sysinno acquisition worked because Innodisk understood what they were really buying: not technology but capability. They preserved Sysinno's culture and expertise while providing industrial channels and reliability engineering. Too many acquisitions fail because acquirers try to digest their purchases. Innodisk's federation model—independent subsidiaries united by common standards—preserved entrepreneurial energy while achieving scale benefits.

Lesson 6: Ecosystem orchestration. The AIoT Alliance revealed sophisticated ecosystem thinking. Rather than trying to own every layer of the stack, Innodisk became the trusted integrator. In complex industrial deployments, the integrator captures enormous value—they own the customer relationship, understand the system architecture, and become indispensable for future expansions.

Bear vs. Bull Case

Bear Case:

The China risk looms largest. Not just revenue exposure but supply chain dependency. If geopolitical tensions escalate to technology embargoes, Innodisk could face component shortages and customer losses simultaneously. The company has diversified geographically, but unwinding decades of China integration would be painful and expensive.

Commoditization threatens from below. As industrial storage becomes standardized, margins could compress. Chinese competitors are already offering "good enough" industrial storage at significant discounts. While Innodisk's reliability reputation provides some protection, price pressure in commodity components is relentless. The edge AI pivot helps, but storage remains the revenue foundation.

Big tech companies are bringing AI compute to the edge. Google's Coral, Amazon's Panorama, Microsoft's Azure Stack Edge—all represent potential competitive threats. These giants have unlimited resources, established customer relationships, and ecosystem lock-in. While they focus on different market segments today, expansion into industrial edge AI seems inevitable.

Supply chain vulnerabilities persist. Innodisk depends on leading-edge components from concentrated suppliers. The 2020-2022 semiconductor shortage demonstrated how quickly component availability can constrain growth. As edge AI drives demand for advanced processors and memory, competition for supply could intensify. Unlike consumer electronics makers who can delay launches, Innodisk's industrial customers expect multi-year supply commitments.

Bull Case:

Edge AI adoption remains in early innings. The global edge AI market size was estimated at USD 20.78 billion in 2024 and is projected to reach USD 66.47 billion by 2030, growing at a CAGR of 21.7% from 2025 to 2030. The market is experiencing significant growth, driven by the increasing demand for real-time data processing and analysis at the network's edge. Innodisk's industrial heritage positions them perfectly for this transition. While competitors must learn industrial reliability, Innodisk must only add AI capabilities—an easier path.

Industrial IoT TAM expansion creates secular tailwinds. Every factory becoming "smart" needs edge infrastructure. Unlike consumer markets where a few platforms dominate, industrial edge remains fragmented—perfect for Innodisk's customization capabilities. The group has completed over 1,000 edge AI projects in recent years and expects exponential growth in edge AI adoption, aiming to increase related AI revenue share from just over 20% in 2025 to 30% by 2026.

Strong IP portfolio and customer relationships create competitive moats. Industrial customers don't switch storage vendors lightly—the validation costs and risks are too high. Combined with patents, customization, and system-level integration, Innodisk's position becomes nearly unassailable in their niches. Customer lifetime values measured in decades justify higher acquisition costs and sustained R&D investment.

Platform network effects are strengthening. Each edge AI deployment teaches Innodisk something new. Each subsidiary acquisition adds capabilities that benefit all customers. Each partnership expands the addressable market. Unlike linear businesses where growth requires proportional investment, Innodisk's platform model exhibits increasing returns to scale. The company that started with storage now offers complete edge AI solutions—and the ecosystem continues expanding.

Epilogue: What's Next?

The next decade will test whether Innodisk can complete its transformation from component supplier to intelligence infrastructure provider. Generative AI at the edge represents both opportunity and challenge. While cloud-based models grab headlines, practical deployment requires edge processing for latency, privacy, and cost reasons. Innodisk's challenge: becoming the trusted platform for deploying these models in industrial settings where failure has real-world consequences.

Automotive and autonomous systems expansion seems inevitable. Modern vehicles are becoming data centers on wheels, generating terabytes daily from sensors, cameras, and control systems. Innodisk's combination of automotive-grade storage, edge AI processing, and sensor integration positions them well. But automotive customers demand different validation cycles, supply commitments, and price points than traditional industrial markets.

Data sovereignty is driving edge compute demand. Regulations increasingly require data processing within national borders. Industrial facilities can't send sensitive operational data to foreign clouds. This regulatory fragmentation favors edge solutions and companies like Innodisk that can deliver complete on-premise stacks. The challenge: maintaining profitability while customizing for regional requirements.

The path from storage to intelligence infrastructure isn't complete. Today, Innodisk sells products and solutions. Tomorrow, they might sell intelligence as a service—monitoring, predicting, and optimizing industrial operations. This would transform the business model from one-time sales to recurring revenue, from hardware margins to software multiples.

Key metrics to watch: Edge AI revenue mix climbing toward 30%, gross margins holding despite mix shift, and geographic diversification reducing China concentration. But the most important metric might be the least visible: the number of industrial processes that become dependent on Innodisk's intelligence infrastructure.

Twenty years ago, a group of engineers in Taiwan bet that industrial storage mattered more than consumer volumes. They were right. Today, they're betting that edge intelligence matters more than cloud scale. The early returns suggest they might be right again. The company that mastered the art of making storage boring and reliable is now making edge AI practical and dependable. In the end, that might be the most valuable transformation of all—not from components to platforms, but from invisible infrastructure to indispensable intelligence.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube