DocuSign: How a Document Signing Company Built (and Nearly Lost) a $13 Billion Empire

I. Introduction: The Signature That Changed Everything

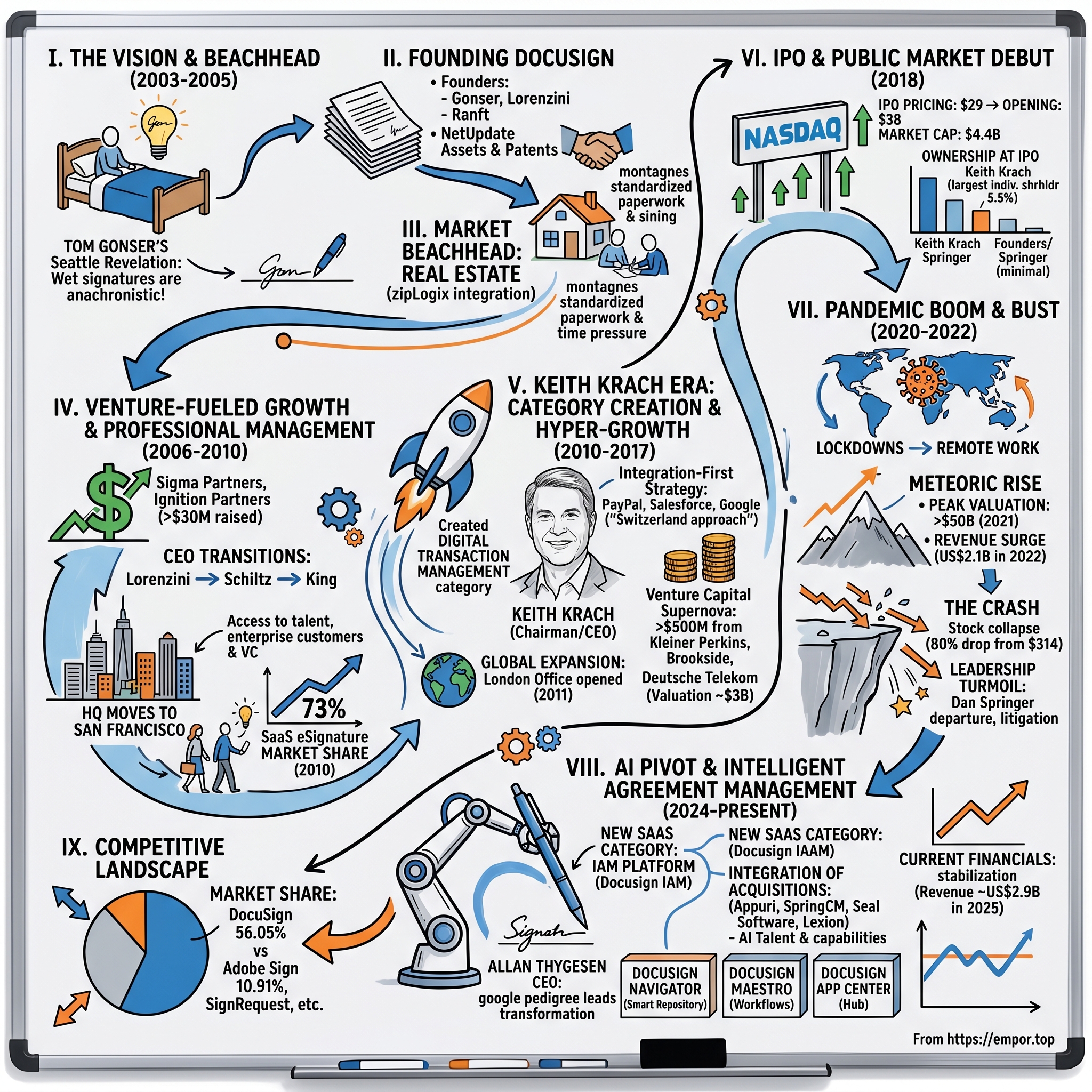

Picture a sweltering Seattle afternoon in 2003. Tom Gonser, a seasoned technology executive who had cut his teeth at Apple and McCaw Cellular, sat bolt upright in bed with a revelation that would reshape how the world does business. The mortgage industry, where he'd been working, still required wet signatures on stacks of paper documents—a maddening anachronism in an increasingly digital world. What if, Gonser wondered, signatures could live entirely in the cloud?

Fast forward two decades, and DocuSign has become more than a company—it's a verb. With nearly 1.7 million customers and 6,838 employees as of January 31, 2025, DocuSign operates across more than 180 countries. In the Digital Signatures market, DocuSign commands a 53.51% market share—over five times larger than its nearest competitor, Adobe Sign, at 9.79%.

But this dominance came at a cost few anticipated. The company that rode the pandemic wave to a staggering $50+ billion market capitalization watched helplessly as that valuation collapsed by 80% when the world returned to normal. CEO Dan Springer's departure came less than two weeks after DocuSign posted fiscal first-quarter earnings that fell short of analyst expectations, accelerating the company's stock plunge even further.

The central question animating this deep dive: How did a seemingly simple signature tool become a pandemic darling worth over ten times its IPO valuation, crash spectacularly, and now attempt a reinvention through artificial intelligence? The answer lies in a masterclass of venture-backed growth, visionary leadership, and the brutal reality that even the most essential software companies can overshoot their sustainable trajectory.

This story unfolds across three acts: the scrappy Seattle startup that found product-market fit in real estate, the Keith Krach transformation that professionalized the company for IPO, and the pandemic boom-bust that taught Wall Street the difference between temporary acceleration and permanent shifts in demand. Along the way, we'll examine the strategic acquisitions that built DocuSign's "Agreement Cloud," the leadership turmoil that followed the crash, and the ambitious AI pivot that represents the company's best hope for its next act.

II. The Origin Story: From DocuTouch to DocuSign (1998-2005)

The Founder's Journey Through the Dot-Com Wreckage

Tom Gonser came up with the idea when he was CEO of NetUpdate, a company he founded in 1998. Before founding DocuSign in 2003, Gonser had a rich background in technology and business development, including roles at Apple, McCaw Cellular Communications (which became AT&T Wireless), and NetUpdate.

The late 1990s mortgage industry presented a peculiar paradox. Technology could process loan applications, run credit checks, and manage billions in capital flows—but at the critical moment of commitment, everything ground to a halt. Borrowers had to physically appear to sign documents. Couriers shuttled paper across cities. Deals died because someone couldn't get to a notary public before a rate lock expired.

When the market collapsed in 2000, NetUpdate had to make a tough choice. "Like, 'we need to shrink. We need to refocus.' The company effectively became an online mortgage origination platform, which wasn't that interesting to me given I was trying to build something much bigger. That was a perfect time for me to exit that business and start focusing on making the electronic signature process actually work online."

What made Gonser's vision different from the failed attempts that preceded it? "There were a bunch of companies that were trying to do that at the time, but they were all doing it wrong. I literally sat up in bed one morning and I had an idea that turned the existing processes that people were pushing inside out."

The DocuTouch Connection: How Patents Became a Company

The origin of DocuSign involved more than pure inspiration—it required strategic asset acquisition during the dot-com bust. Throughout its history, NetUpdate had acquired several companies, including an e-signature start-up in Seattle called DocuTouch, funded by Timberline Venture Partners, Bill Kallman, and Jeff Tung with $4M.

DocuTouch held something invaluable: patents on web-based digital signatures and collaboration technology. In the aftermath of the dot-com crash, these patents became available at fire-sale prices. With internal support from Gonser, Lorenzini negotiated the purchase of certain DocuTouch assets from NetUpdate and started DocuSign. Gonser then left the NetUpdate Board to focus on DocuSign full-time.

The Founding Team and Early Capital

DocuSign was founded in 2003 by Court Lorenzini, Tom Gonser, and Eric Ranft. DocuSign was incorporated in April 2003 in Washington state by founders Tom Gonser, Court Lorenzini, and Eric Ranft, with an initial focus on automating the cumbersome manual processes involved in obtaining physical signatures on documents.

The initial funding came from founders and angel investors, with a seed round of approximately $2.6 million. In 2004, DocuSign raised $4.6 million from Ignition Partners and Frazier Technology Ventures.

These were modest sums even by 2004 standards, but they proved sufficient for what Gonser understood to be the company's primary challenge: proving legal validity. E-signatures weren't just a technology problem—they were a legal and trust problem. According to DocuSign, mock trials featuring licensed attorneys and judges highlighted the admissibility of DocuSign contracts in court based on encrypted audit logs of signature events, and the impossibility of changing contracts.

Real Estate as the Beachhead Market

The choice of real estate as DocuSign's entry point was strategic genius. The firm began sales in 2005 when zipForm, now zipLogix, integrated DocuSign into its virtual real estate forms.

Why real estate? The industry combined several characteristics that made it ideal for e-signature adoption. First, real estate transactions involve mountains of standardized paperwork—disclosure forms, purchase agreements, inspection addendums, and closing documents. Second, time pressure is intense: mortgage rate locks expire, buyers compete for properties, and deals die when signatures aren't obtained quickly. Third, real estate agents are independent contractors accustomed to adopting tools that help them close deals faster.

The top three industries that use DocuSign for digital signatures are Real Estate (395), Property Management (347), and Wealth Management (314). This legacy of the beachhead strategy persists today—real estate remains DocuSign's strongest vertical even as the company has expanded far beyond it.

III. The Venture-Fueled Growth Era (2006-2010)

Building the War Chest

The years between 2006 and 2009 transformed DocuSign from a promising startup into a venture-backed growth company with serious ambitions. In 2006, Sigma Partners became the largest shareholder, a position it held at the time of the IPO, with returns over $700 million. Between 2006 and 2009 DocuSign raised $30 million that allowed the firm to add corporate clients and process 48 million signatures.

Sigma Partners' entry represented more than capital—it represented conviction from serious institutional investors that e-signatures were a category capable of producing venture-scale returns. The $700 million return Sigma would eventually realize ranks among the most successful venture investments of its vintage.

Leadership Transitions: The Professional Management Era Begins

The transition from founder-led to professionally managed marked a critical inflection point. In January 2007, Court Lorenzini stepped down as CEO and board chairman and was replaced as CEO by Matthew Schiltz, who served in that role until January 2010. Steven King replaced Schiltz as CEO and moved the corporate headquarters from Seattle to San Francisco.

The move to San Francisco was more than geographic. Seattle in 2010 was not yet the technology hub it would become—Amazon was still primarily an e-commerce company, and Microsoft dominated the region's tech identity. San Francisco offered proximity to enterprise software customers, venture capital partners, and a deep talent pool of SaaS-experienced executives.

Market Dominance Emerges

By the end of 2010, DocuSign had established a commanding lead that competitors would struggle to challenge. DocuSign also began referring to its service as "eSignature Transaction Management." By the end of 2010, the company handled 73 percent of the SaaS-based electronic signature market with 80 million signatures processed.

Seventy-three percent market share in a category you're simultaneously defining and dominating—this was the beginning of DocuSign's network effects moat. Every signature sent through DocuSign introduced new potential users to the platform. Every integration with a third-party system (CRM, ERP, document management) increased switching costs for existing customers.

Scale Venture Partners led an investment round of $27 million in December 2010. This capital would fund the next phase of expansion under leadership that would take the company from startup to IPO-ready.

IV. The Keith Krach Era: Professional Management & Hyper-Growth (2010-2017)

The Transformative CEO Arrives

Krach joined DocuSign as Chairman of the Board in 2010 and took on the role of CEO in 2011. Keith Krach became DocuSign's board chairman in January 2010 and its CEO in August 2011.

Who was Keith Krach, and why did DocuSign need him? Keith J. Krach (born April 1, 1957) is an American businessman and former diplomat. He is the former chairman and CEO of DocuSign. Krach co-founded Ariba, and was chairman and CEO, and is recognized for his work in B2B Commerce and Digital Transaction Management. Krach was chairman of the board of Angie's List. Krach was the youngest-ever Vice President of General Motors.

The Ariba pedigree mattered enormously. Krach co-founded Ariba and served as Chairman and CEO (1996–2003), creating the world's largest business-to-business e-commerce network. After taking it public, Ariba achieved a market capitalization of $40 billion, and today, more than $1.7 trillion of commerce is transacted annually through the Ariba network.

Krach understood something that would prove essential for DocuSign's trajectory: how to create and dominate a category. Remarkable innovation followed: Launched the DTM (Digital Transaction Management) category, going beyond eSignature to integration, payment, workflow, administration and scalability—paving the way toward the System of Agreement Platform.

Strategic Expansion Goes Global

DocuSign opened an office in London, England, in September 2011. In the same year, DocuSign opened an office in San Francisco that now functions as its global headquarters.

The London office represented DocuSign's first major international push. European markets presented both opportunity (large enterprises, regulated industries requiring audit trails) and challenge (varying e-signature legal frameworks across jurisdictions). Krach's approach was to establish presence and adapt products to local requirements rather than impose a one-size-fits-all American model.

The Partnership Strategy: Switzerland of Software

DocuSign signed an agreement with PayPal in April 2012 that allowed users to capture signatures and payments in a single transaction. Similar partnerships with Salesforce and Google Drive preceded the PayPal agreement.

This integration-first strategy—what some industry observers called the "Switzerland approach"—proved crucial. DocuSign embedded itself so deeply into enterprise workflows that extracting it became prohibitively disruptive. In July 2012, Business Insider reported that about 90% of Fortune 500 companies had signed up to use DocuSign.

The Salesforce partnership deserves particular attention. Salesforce represented the epicenter of enterprise SaaS adoption, and DocuSign's integration meant that every Salesforce customer was a DocuSign prospect. The relationship would prove durable through multiple leadership changes at both companies.

The Venture Capital Supernova

In July 2012, DocuSign raised $47.5 million in venture funding from investors including Kleiner Perkins Caufield & Byers; the round later grew closer to $56 million. In March 2014, the company announced it had raised $85 million in a new funding round. Though unconfirmed, The Wall Street Journal reported the round was based on a company valuation of $1.6 billion. In May 2015, the company announced it had raised $233 million in a new funding round, with some estimating a $3 billion company valuation.

The news comes a day after DocuSign announced that Deutsche Telekom had joined the company's broad investor base, bringing total capital raised in the company to $525 million. The company—founded in Seattle in 2003 by Tom Gonser—is reportedly valued at more than $3 billion.

The investor syndicate tells its own story of credibility accumulation: Kleiner Perkins, one of Silicon Valley's most prestigious venture firms; Brookside Capital and Bain Capital Ventures providing growth equity; Deutsche Telekom signaling international enterprise endorsement. By 2015, DocuSign had raised over half a billion dollars from blue-chip investors who saw the company as a category leader with significant room to expand.

Setting Up the Succession

Keith Krach, who was named CEO of DocuSign in 2011, plans to step down from the electronic signature powerhouse. The company plans to begin a search for a new CEO, and Krach will remain as executive chairman for three years after the new CEO is named.

Krach's announced departure in 2015 reflected his intentional approach to leadership transitions. He had built DocuSign from a 50-person startup to a $3 billion valuation company—and recognized that the next phase required different skills. Prior to government service, Krach served as CEO and Chairman of DocuSign (2009–2019), leading its transformation from a 50-person startup to a public company and global standard it is today.

V. The IPO & Public Market Journey (2018)

Going Public in Style

DocuSign began trading on the Nasdaq at $38 per share on April 27, 2018 after being priced at $29 per share the evening before its public debut. By the end of the trading day, DocuSign shares had hit an intraday high of $40.69 and secured a market cap of $4.4 billion.

In 2018, the company announced plans for an initial public offering on the Nasdaq. The IPO was completed on April 27, in which the company raised $543 million.

The IPO pop—from $29 pricing to $38+ opening—reflected pent-up demand for a company that had remained private longer than typical. In April 2018, Krach led DocuSign through a successful IPO which raised $629 million, increasing company valuation to $4.41 billion.

The $4.4 billion market cap represented over one-third higher than the $3 billion valuation from the 2015 private round—a healthy appreciation that rewarded patient investors while leaving significant upside for public market participants.

Ownership Structure at IPO: The Founder Dilution Story

Neither the original founders nor CEO Daniel Springer were major shareholders at that time. Former CEO Keith Krach was the largest individual shareholder at 5.5%, about 8.5 million shares at the time of the IPO.

This ownership pattern tells a story common to venture-backed companies that raise substantial capital over many years. Tom Gonser, Court Lorenzini, and Eric Ranft had founded the company but no longer held major stakes. The trajectory from founding in 2003 to IPO in 2018—fifteen years and over $1.3 billion in funding—meant significant dilution at each round.

Springer took on the role of chief executive in 2017 and took the company public in 2018. Dan Springer, a professional CEO brought in to navigate the public markets, would lead the company through its most volatile period.

For investors, the takeaway is nuanced. Heavy venture funding enabled DocuSign to establish market dominance before competitors could catch up. But that same funding structure meant founders retained relatively small ownership—a trade-off that shaped incentives throughout the company's lifecycle.

VI. Building the Agreement Cloud: Strategic Acquisitions (2017-2024)

The Platform Expansion Vision

DocuSign's strategic vision evolved from "e-signature tool" to "Agreement Cloud platform" to, most recently, "Intelligent Agreement Management." Each transition required acquisitions that extended capabilities beyond the original product.

The acquisition strategy followed a clear logic: if DocuSign owned only the signature moment, it captured value at a single point in the contract lifecycle. But agreements involve creation, negotiation, execution, storage, analysis, and management. Each phase represented an opportunity to deepen customer relationships and expand wallet share.

Appuri Acquisition (2017): The AI Seeds

The acquisition of machine learning startup Appuri's IP rights in December 2017 represented DocuSign's first significant move toward AI capabilities. While the Appuri acquisition was relatively modest, it signaled awareness that the future of agreement management would involve intelligent automation rather than simple digital capture.

SpringCM Acquisition (2018): Contract Lifecycle Management

On July 31, 2018, DocuSign announced plans to acquire SpringCM for $220 million. On September 4, 2018, DocuSign acquired SpringCM Solution.

DocuSign today announced that it has signed a definitive agreement to acquire SpringCM, a leading cloud-based document generation and contract lifecycle management software company based in Chicago. With the addition of SpringCM's capabilities in document generation, redlining, advanced document management, and end-to-end agreement workflow, the deal further accelerates DocuSign's broadening of its solution beyond e-signature to the rest of the agreement process.

SpringCM brought capabilities that DocuSign lacked: document generation, collaborative editing (redlining), and sophisticated workflow automation. SpringCM empowers companies to become more productive by reducing the time spent managing critical business documents. Intelligent, automated workflows enable document collaboration across an organization from any desktop or mobile device. Delivered through a secure, scalable cloud platform, SpringCM document and contract management solutions seamlessly integrate with Salesforce, or work as a standalone solution.

Seal Software Acquisition (2020): AI-Powered Contract Analytics

DocuSign announced today it would acquire Seal Software, which develops AI-powered contract discovery and contract management software solutions, for $188 million.

Aragon estimates that Seal had revenues of just under $20 million. At $180 Million, DocuSign again paid a large multiple—9x revenues for Seal. This is eerily similar to the large price it paid for SpringCM two years ago.

The Seal acquisition brought AI capabilities for automated contract analysis—extracting key terms, identifying risk factors, and categorizing clauses without human review. Seal will also augment DocuSign CLM, its contract lifecycle management solution. DocuSign says that this will help it to automatically categorize clauses, extract their key terms, and then use that information to drive workflows—for example, automatically routing content to specific reviewers based on risk analysis and corporate policies.

Clause Acquisition (2021): Smart Legal Contracts

On June 1, 2021, DocuSign acquired Clause, a smart legal contract technology startup. The Clause acquisition brought capabilities for creating contracts that could execute automatically based on data inputs—a step toward the vision of contracts as active business systems rather than static documents.

Lexion Acquisition (2024): Completing the AI Arsenal

DocuSign today announced its agreement to acquire Lexion, a leading provider of AI-powered agreement management software, for $165 million in cash, subject to customary adjustments.

The deal looks to be a successful exit for Lexion, which got its start in 2018 after co-founders Gaurav Oberoi (CEO), Emad Elwany (CTO), and James Baird (principal architect) met at the Allen Institute for AI in Seattle. Lexion raised about $36 million since its founding, including a $20 million round in April 2023, after tripling its revenue in 2022.

Lexion was founded by CEO Gaurav Oberoi, CTO Emad Elwany, and Principal Architect James Baird, who met at the Allen Institute for AI, a leading research lab created by late Microsoft co-founder Paul Allen.

The Lexion acquisition brought world-class AI talent to DocuSign at a critical moment. The co-founders, who met at the Allen Institute for AI, have extensive expertise in AI and contract management. Lexion also brings to DocuSign a team of world-class AI engineers with backgrounds at Amazon, Google, Meta, and Microsoft.

VII. The Pandemic Boom & Bust: A Cautionary Tale (2020-2022)

COVID-19: The Perfect Storm Creates a Pandemic Darling

The year 2020 was big for emerging technologies, in some cases accelerating their growth trajectory as the pandemic pushed people into remote work. Most companies that delivered useful platform technologies garnered favor with investors, growing to dizzying market valuations as demand for their services exploded. E-signature software company DocuSign is an example of this phenomenon.

The COVID-19 pandemic created ideal conditions for DocuSign's explosion. With offices shuttered globally, every business transaction that once required physical presence became a digital imperative. DocuSign has emerged as a go-to resource during the pandemic. With offices closed around the world, its eSignature tool is enabling its half a million paying customers and hundreds of millions of individual users to continue to complete contracts, close real estate transactions, onboard new employees, and engage in a host of other agreements over the Internet.

The Meteoric Rise: Revenue and Valuation Surge

Net sales continued to steadily increase at DocuSign. In 2020, net sales were US$974 million, which increased by 49.19% in 2021 to US$1.45 billion. Sales continued to rise in 2022, with an increase of 45.02% to US$2.1 billion.

DocuSign's highest market cap was recorded in 2020, at $41.47 billion. Fun fact: DocuSign's market cap in 2020 saw a 212.04% increase compared to the market cap from 2019.

With just days remaining until 2021, shares of DocuSign are up over 200% on the year, boosting the stock's total return to 480% since its early 2018 IPO.

The stock peaked around $310 in 2021—a tenfold gain from its IPO price. At its peak valuation above $50 billion, DocuSign traded at a price-to-sales ratio above 40x, a level historically sustainable only by companies with decades of high growth ahead.

The Crash: When Reality Reasserted Itself

"Third quarter revenue growth of 42% year-over-year and operating margin of 22% exceeded our expectations. After six quarters of accelerated growth, we saw customers return to more normalized buying patterns, resulting in 28% year-over-year billings growth," said Dan Springer, CEO of DocuSign.

Discussing this slowdown, DocuSign's CEO, defendant Daniel D. Springer, stated that the growth boost from the Covid-19 pandemic had deteriorated earlier than expected—a growth boost that DocuSign did not acknowledge until this point. That same day, DocuSign also announced guidance for the fourth quarter fiscal year 2022, providing midpoint revenue guidance of $560 million, missing analysts' consensus estimates of $573.8 million. DocuSign's guidance also provided a midpoint billing guidance of $653 million, missing consensus estimates of $705.4 million. On this news, DocuSign's stock price fell by more than 42%, damaging investors.

The stock decline proved relentless. The stock is back where it was pre-pandemic, around $60/share, but during the pandemic it was as high as $314. So technically shareholders have lost nothing compared to the original investment, but that's not how shareholders or Board members think. They think it dropped from $314 to $60 because that was the high.

Leadership Turmoil and Legal Battles

DocuSign CEO Dan Springer is stepping down in his role after the e-signature software maker lost more than 60% of its value year to date. Chairman of the Board Maggie Wilderotter will serve as interim CEO as the company begins its search for the next executive.

The company didn't provide a reason for his departure but said Springer "has agreed to step aside," effective immediately. Chairman of the Board Maggie Wilderotter will serve as interim CEO as the company begins its search for the next executive.

The departure was acrimonious. CEO Daniel Springer sued the company and its chairwoman in Delaware, claiming they issued a securities filing in early October falsely stating that he had stepped down from the board after realizing they lacked the authority to oust him.

In the demand, Mr. Springer alleges that he was wrongfully terminated as Chief Executive Officer; asserts related claims against DocuSign and Ms. Wilderotter, including defamation, withholding promised compensation and breach of contract; and seeks unspecified damages and other relief. DocuSign has engaged legal counsel to defend the matter.

The legal disputes added uncertainty at a moment when the company needed clarity. All persons and entities who or which, during the period from June 4, 2020 through June 9, 2022, inclusive, purchased the publicly traded common stock of DocuSign and were damaged thereby. A trial date in the Action has been scheduled for July 13, 2026.

Lessons from the Pandemic Boom

The DocuSign crash offers a template for understanding pandemic-era technology investments. The company wasn't broken—revenue continued to grow, and the core product remained essential to modern business operations. But the valuation had priced in a permanent acceleration of demand that proved temporary.

DocuSign was able to capitalize on the Covid-19 pandemic as more consumers shifted to online transactions and deals, but it has been tough to keep up with comparisons while also struggling with macroeconomic trends.

VIII. The AI Pivot & Intelligent Agreement Management (2024-Present)

The IAM Platform Launch: DocuSign's Second Act

SAN FRANCISCO, April 11, 2024—Docusign (NASDAQ: DOCU) today announced a significant expansion of its company strategy, opening up a new SaaS category—Intelligent Agreement Management—and unveiling Docusign IAM, an Intelligent Agreement Management platform and suite of applications to lead that category.

"Agreements are the foundation of every business, but the way people manage them is stuck in the past," said Allan Thygesen, Chief Executive Officer at Docusign. "Poor agreement management and outdated systems cost businesses time, opportunity, and nearly $2 trillion in global economic value every year. Intelligent Agreement Management will help change that; businesses all around the world will be able to operate more efficiently and grow revenue more quickly."

The Intelligent Agreement Management announcement represented DocuSign's most ambitious strategy shift since Keith Krach's "Digital Transaction Management" category creation. Just as Customer Relationship Management (CRM), Human Capital Management (HCM), and Enterprise Resource Planning (ERP) leveraged the internet to modernize sales, HR, and resource management, we believe Intelligent Agreement Management will transform the agreement management process and how agreement data informs every part of your business.

Key New Products: Navigator, Maestro, and the App Center

Docusign Navigator: A central repository that automatically and intelligently captures, stores, organises all your agreements—unlocking the data trapped in your agreements and allowing you to capture more value. Docusign Maestro: An easy-to-use platform to build and deploy customised workflows that automate and accelerate agreement processes without writing any code. Docusign App Center: A hub that provides critical integrations to third-party business systems and thus eliminates the problems around disconnected tools, inaccurate information and a slower pace of business.

DocuSign Navigator: Lexion's AI capabilities were released to the IAM platform, including the ability to surface insights from a more extensive array of agreement types. Additionally, Navigator now includes the ability to import documents from third-party partners including Box, Dropbox, Google Drive, and Microsoft OneDrive. Also, Navigator now has an upgraded search experience that includes predictive type-ahead functionality, more filters, and the ability to export results.

Docusign announced the global release of IAM for Sales and IAM Core in December 2024, excluding Japan. As part of the global expansion, Navigator became available to customers in every country where Docusign products are available for sale. Navigator has been localized in all 14 Docusign-supported languages.

Allan Thygesen: The CEO Leading the Transformation

Allan Thygesen is the CEO of Docusign, the company that brings agreements to life. Since joining the company in 2022, Allan has led Docusign to expand on its market leadership positions in e-signature and contract lifecycle management, and launched the SaaS category of Intelligent Agreement Management. Today, more than 1.6 million customers and more than a billion users in over 180 countries use Docusign products and solutions. Before he joined Docusign, Allan served as President, Americas & Global Partners at Google, leading the company's $100 billion+ advertising business across North and South America.

Chief Executive Officer and Board Director, Docusign (NASDAQ:DOCU). Board member, A P Moller Maersk (NASDAQ CPH: MAERSK). Led Google's $100B+ advertising business in North and South America, previously led Google's global mid-market and SMB advertising business. Lecturer, Stanford Business School for 7 years.

Thygesen brings a different skillset than his predecessors. "I was very keen to, instead of having this super large violin section, to have the whole orchestra, and that wasn't really going to be possible at Google. And the reality is, Google is a very functionally organized company. What I mean by that is, with the exception of Google Cloud, which is sort of an operating division within the company that's somewhat autonomous, everything else is functionally organized."

Current Financial Performance: Stabilization After the Storm

DocuSign annual revenue for 2025 was $2.977B, a 7.78% increase from 2024.

Second Quarter Financial Highlights: Revenue was $800.6 million, a 9% year-over-year increase with no material impact from foreign exchange rates. Subscription revenue was $784.4 million, a 9% year-over-year increase.

Docusign's board of directors has authorized an increase to its existing stock repurchase program of an additional amount of up to $1.0 billion of Docusign's outstanding common stock. The program has no minimum purchase commitment and no mandated end date. As of June 5, 2025, our total remaining authorization under our stock repurchase plan is up to $1.4 billion.

The company's transformation from growth-at-all-costs to profitable operations is evident in these metrics. Revenue growth has moderated to high-single digits, but profitability has improved dramatically. The $1.4 billion share repurchase authorization signals confidence in the company's cash-generating capability.

IX. Competitive Landscape Analysis

The Major Competitors: A Fragmented Field

DocuSign has market share of 56.05% in digital-signatures market. DocuSign competes with 33 competitor tools in digital-signatures category. The top alternatives for DocuSign digital-signatures tool are Adobe Sign with 10.91%, SignRequest with 10.71%, Smartwaiver with 9.69% market share.

The digital signature market is led by some of the globally established players, such as Adobe (US), DocuSign (US), Thales (France), Zoho (India), Entrust (US), DigiCert (US), OneSpan (US), Ascertia (UK), GlobalSign (Belgium), eSign (China) and IdenTrust (US).

Adobe Acrobat Sign represents DocuSign's most formidable competitor. Adobe leverages its Adobe Acrobat suite to integrate digital signatures seamlessly with document creation, editing, and collaboration tools. The company drives adoption through Adobe Sign, focusing on enterprise-level customers and integrating its solutions with popular software applications like Microsoft Office 365.

Adobe's advantage lies in its existing enterprise relationships and integrated document workflow. The disadvantage: e-signature is a small piece of Adobe's massive business, which may limit investment and attention.

HelloSign (Dropbox) targets the simplicity-focused segment of the market. Acquired by Dropbox in 2019, HelloSign emphasizes clean user experience and seamless integration with Dropbox's storage platform. The competitive threat is primarily at the lower end of the market, where simplicity matters more than enterprise features.

PandaDoc goes beyond signatures to encompass the entire document workflow—proposal creation, approval workflows, and document analytics. PandaDoc's approach overlaps significantly with DocuSign's Agreement Cloud vision, making it a more direct strategic competitor than pure e-signature tools.

Porter's Five Forces Analysis

Threat of New Entrants: MODERATE While the e-signature market has relatively low barriers to entry for basic functionality, enterprise adoption requires regulatory compliance, security certifications, integration ecosystems, and brand trust. DocuSign's established position, with over a billion users and 1.7 million customers, creates significant network effects that new entrants struggle to replicate.

Bargaining Power of Suppliers: LOW DocuSign's primary inputs are cloud infrastructure (AWS, Azure, Google Cloud), engineering talent, and computing resources. All are available from multiple suppliers at competitive prices. The company faces no significant supplier concentration risks.

Bargaining Power of Buyers: MODERATE Large enterprise customers can negotiate favorable terms, and switching costs—while present—are not prohibitive. The abundance of competitors gives buyers options, though the integration complexity of enterprise deployments provides some protection.

Threat of Substitutes: MODERATE TO HIGH For basic e-signature, numerous alternatives exist (including free options and built-in features from Microsoft, Google, and others). The substitution threat is lower for complex agreement management workflows where DocuSign has built integrated solutions.

Competitive Rivalry: HIGH The digital signature market size is projected to grow from USD 13.4 Billion in 2025 to USD 70.2 Billion by 2030 at a compound annual growth rate (CAGR) of 39.2%. This attractive growth rate invites competitive intensity from both established players and new entrants.

Hamilton Helmer's 7 Powers Framework

Scale Economies: MODERATE DocuSign benefits from scale in infrastructure costs (more signatures processed on the same platform architecture) and brand investment (marketing costs spread across larger customer base). However, software economics mean competitors can achieve viable scale at smaller sizes than traditional industrial businesses.

Network Effects: STRONG Every document sent through DocuSign invites new users to the platform. Recipients become familiar with the interface and may adopt it for their own organizations. This creates a virtuous cycle of adoption that reinforces market leadership.

Counter-Positioning: WEAK (NOW) DocuSign's original counter-position—cloud-native e-signature versus legacy paper processes—has eroded as competitors adopted similar models. The company's current effort to establish "Intelligent Agreement Management" as a new category represents an attempt to recreate counter-positioning through AI.

Switching Costs: MODERATE Enterprise customers with deep DocuSign integrations face significant switching costs in terms of workflow disruption, retraining, and integration rework. SMB customers face lower switching costs due to simpler implementations.

Branding: STRONG "During his tenure, DocuSign became a verb and the benchmark for trust in digital transactions." The company's brand recognition as the default choice for e-signature represents a durable competitive advantage.

Cornered Resource: WEAK DocuSign does not possess unique resources (patents, regulatory licenses, exclusive partnerships) that competitors cannot replicate over time.

Process Power: MODERATE Years of optimization have made DocuSign's operations highly efficient, with strong gross margins and proven go-to-market motions. However, these processes are not fundamentally unreplicable by well-resourced competitors.

X. Investment Considerations: Bulls, Bears, and Key Metrics

The Bull Case

Market Position Durability: DocuSign's strategy emphasizes ease of use and integration with popular business software like Salesforce and Microsoft. DocuSign aims to expand its capabilities in contract lifecycle management (CLM) and enterprise automation while scaling globally with a cloud-first approach. It builds partnerships with regulatory authorities to ensure compliance across various regions. The company's market leadership is reinforced through its extensive ecosystem integrations and strong product reliability, making it the preferred choice for enterprises seeking streamlined signing processes.

IAM Platform Expansion: The Intelligent Agreement Management strategy represents a significant opportunity to expand average revenue per customer by selling additional capabilities beyond e-signature. The broader DTM market, valued at $14 billion in 2024, is projected to grow at a 23.9% CAGR, reaching $39.83 billion by 2029. DocuSign's focus on AI-driven innovation—such as integrating Lexion's AI for contract analysis—positions it to capitalize on this growth.

Profitability Improvement: The company has successfully transitioned from growth-at-all-costs to profitable operations. EBITDA also keeps going up and up. In 2020, EBITDA was at US$97.51 million. Then, in 2021, it grew a whopping 131.88% to US$226.1 million. The good times kept rolling with EBITDA in 2022 shooting up by 110.62% to US$476.2 million.

Capital Return: The $1.4 billion share repurchase authorization demonstrates both cash-generating ability and commitment to returning value to shareholders.

The Bear Case

Growth Deceleration: Revenue growth has moderated from 45%+ during the pandemic to high-single digits. By then, the growth rate had slowed in 2023, albeit at a positive 19.4% increase, leading to net sales of US$2.52 billion. In 2024, net sales reached US$2.76 billion, reflecting an increase of 9.78% compared to the previous year.

Competitive Intensity: Adobe, Microsoft, Google, and numerous startups continue to invest in the agreement management space. The e-signature core product faces commoditization risk.

Legal Overhang: The ongoing securities class action and related litigation create uncertainty. A trial date in the Action has been scheduled for July 13, 2026.

AI Execution Risk: The Intelligent Agreement Management strategy requires successful integration of multiple acquisitions (Seal, Clause, Lexion) and development of AI capabilities that customers will pay for. Success is not guaranteed.

Key Performance Indicators to Watch

For investors tracking DocuSign's ongoing performance, three KPIs merit particular attention:

-

Dollar-Based Net Retention Rate (DBNR): This metric measures revenue growth from existing customers, capturing both expansion and churn. A DBNR above 100% indicates that existing customers are spending more over time—essential for a SaaS business model. The company's historical DBNR has ranged from 113% to over 120% during peak periods.

-

Billings Growth: We believe billings can be used to measure our periodic performance, when taking into consideration the timing aspects of customer renewals, which represents a large component of our business. Since DocuSign recognizes revenue ratably over subscription periods, billings provide a leading indicator of future revenue trends.

-

IAM Attach Rate: As the company expands from e-signature to Intelligent Agreement Management, the percentage of customers adopting IAM products (Navigator, Maestro) will indicate whether the platform strategy is gaining traction.

MYTH VS. REALITY: DocuSign's Competitive Position

MYTH: DocuSign faces existential threat from Adobe, Microsoft, and free alternatives.

REALITY: While competitive intensity is real, DocuSign's >50% market share has proven durable through multiple competitive cycles. The company's challenge is less about defending the core e-signature business and more about expanding into adjacent markets where competition is less established. Adobe Sign has existed for years without significantly eroding DocuSign's position. The greater risk may be slowing growth rather than market share loss.

XI. Conclusion: The Path Forward

DocuSign's journey from a Seattle startup with a simple idea to a $13 billion enterprise software company encompasses many of the themes that define modern technology business building: vision-driven founders who recognized an underserved need, professional managers who scaled the company for public markets, pandemic-era euphoria that inflated valuations beyond sustainable levels, and the painful recalibration that followed.

The company saw exponential growth during the pandemic—booming by 60% when the corporate world went remote, and contracts had to be signed virtually. But when the globe returned to "normal," Thygesen, a father of four born and raised in Denmark, wanted to retain some of the pandemic's benefits, namely, a more flexible work model.

The company today faces a fundamentally different challenge than at any point in its history. The pandemic-driven pull-forward in adoption means the easy growth is behind them. The competitive landscape has matured. The AI revolution creates both opportunity (new capabilities to offer customers) and threat (potential disruption to existing workflows).

Under Thygesen's guidance, DocuSign is well-positioned to tap into a largely untapped $50 billion market opportunity and transform the way businesses manage agreements through intelligent agreement management.

Whether this vision materializes depends on execution—integrating acquisitions, developing AI capabilities that customers value, and successfully selling expanded solutions to an installed base accustomed to simple e-signature functionality.

For long-term investors, DocuSign represents a fascinating case study in category creation, growth management, and reinvention. The company pioneered a market that barely existed before its founding, achieved dominant market share, weathered a dramatic boom-bust cycle, and now attempts to expand its relevance through artificial intelligence.

The core e-signature business remains essential to modern commerce. The question is whether DocuSign can translate that foundational position into a broader platform company—or whether it will remain a very good, but growth-constrained, single-product leader in a commodity market.

The next chapters of this story will be written by Allan Thygesen's ability to execute the IAM vision, by competitive responses from Adobe and Microsoft, and by the broader adoption of AI in enterprise workflows. As with all such transitions, the outcome remains uncertain—but the company's dominant market position, strong cash generation, and substantial investment in AI capabilities provide a foundation for the attempt.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube