CBRE Group: Building the World's Largest Commercial Real Estate Empire

I. Introduction & Episode Roadmap

Picture this: It's April 18, 1906, 5:12 AM. The earth beneath San Francisco ruptures with devastating force—a 7.9 magnitude earthquake that would kill over 3,000 people and destroy 80% of the city. As the dust settles and fires rage for three days, consuming 500 city blocks, something remarkable happens. Amid the rubble and ruin, opportunity emerges. Real estate brokers begin sketching plans on makeshift desks, helping displaced families find temporary shelter, connecting landowners with builders, orchestrating one of history's greatest urban reconstructions.

Four months later, on August 27, 1906, Colbert Coldwell opens a small real estate office in the heart of this devastation. He couldn't have imagined that this modest brokerage, born from catastrophe, would evolve into CBRE Group—today's $30 billion revenue colossus that orchestrates real estate transactions from Manhattan penthouses to Singapore warehouses, from London office towers to Dallas data centers.

How exactly does a post-earthquake San Francisco brokerage transform into the world's largest commercial real estate services and investment firm? How does a company that started by helping rebuild one city end up managing 7 billion square feet of property across the globe—roughly equivalent to managing all the real estate in New York City, London, and Tokyo combined?

This is a story of relentless acquisition, strategic pivots, and an uncanny ability to surf economic cycles that destroy lesser firms. It's about building recurring revenue streams in a notoriously cyclical industry, creating technology moats in a relationship business, and assembling a platform so comprehensive that Fortune 500 CEOs have one number to call for everything from finding new headquarters to managing their global facilities to developing their next distribution center.

CBRE today stands as number 135 on the Fortune 500, having maintained that prestigious ranking every year since 2008—through the financial crisis, the pandemic, and countless real estate cycles. With 130,000 employees across more than 100 countries, it's the undisputed heavyweight champion of commercial real estate. But the path here wasn't obvious or inevitable.

We'll explore how a regional brokerage became a national player, survived absorption by Sears, executed a management buyout, merged with a 200-year-old British firm, went public twice, assembled the industry's most aggressive M&A playbook, and built four distinct business segments that feed each other in a virtuous cycle. We'll examine the financial engineering, the integration expertise, and the strategic vision that created today's empire.

This isn't just a real estate story—it's a masterclass in platform building, a case study in converting transactional revenue to recurring fees, and a blueprint for dominating a fragmented global industry through disciplined consolidation. Along the way, we'll uncover the pivotal decisions, near-death experiences, and bold bets that shaped this century-spanning journey.

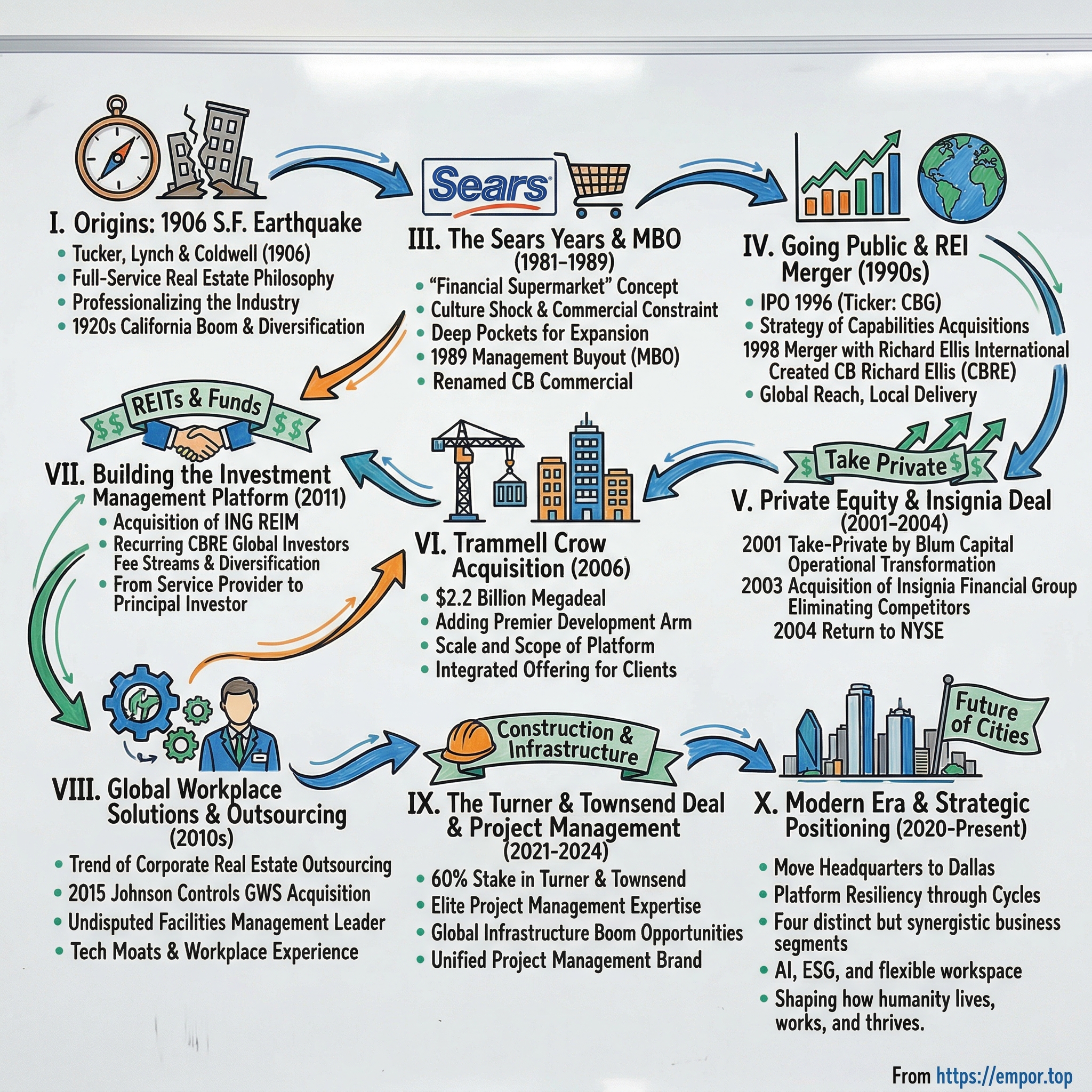

II. Origins: From the 1906 San Francisco Earthquake

The morning after the Great San Francisco Earthquake, Colbert Coldwell stood at the corner of Montgomery and California Streets, surveying the devastation. The 32-year-old had been working in real estate for several years, but nothing had prepared him for this moment. Where the city's financial district once stood, twisted metal and broken stone stretched to the horizon. The smell of smoke lingered from fires that had consumed everything the earthquake hadn't destroyed.

But Coldwell saw something others missed. As he later recalled to colleagues, "When everything is destroyed, everything must be rebuilt." The earthquake hadn't just leveled buildings—it had reset the entire real estate market. Property lines were disputed, insurance claims needed settling, reconstruction required financing, and thousands of businesses needed new locations immediately.

On August 27, 1906, just four months after the disaster, Coldwell established Tucker, Lynch & Coldwell with two partners. They set up shop in a hastily constructed wooden building on Montgomery Street, joining dozens of other businesses operating from temporary structures while the city rebuilt around them. Their timing was impeccable—San Francisco's reconstruction would become one of history's greatest building booms, with over $235 million (roughly $7 billion in today's dollars) invested in new construction over the next three years.

The firm's early innovation was recognizing that post-disaster real estate required different skills than traditional brokerage. They didn't just match buyers and sellers; they became urban planning consultants, insurance claim advisors, and reconstruction coordinators. Coldwell pioneered what he called "full-service real estate"—a philosophy that would echo through the company's DNA for the next century.

In 1913, Benjamin Arthur Banker joined as a partner. Banker brought East Coast connections and a more systematic approach to operations. Where Coldwell was the visionary and relationship builder, Banker was the operator who standardized processes and built scalable systems. Together, they created the West Coast's first truly professional real estate organization, moving beyond the informal, handshake-based culture that dominated the industry.

The partnership evolution tells its own story of growth: Tucker, Lynch & Coldwell became Coldwell, Kern & Banker in 1918 after restructuring, then Coldwell, Cornwall & Banker in 1920 following another partner change. Each iteration brought new capabilities—Kern added industrial expertise, Cornwall brought retail knowledge. By 1922, they were handling over $50 million in annual transactions, making them California's largest real estate firm.

The 1920s California boom transformed the company from regional player to West Coast powerhouse. As Hollywood emerged, oil discoveries drove growth, and agricultural exports exploded, Coldwell Banker (as locals already called it) was there facilitating the deals. They handled Douglas Aircraft's first factory purchase, brokered land for several major movie studios, and assembled parcels for what would become UCLA's Westwood campus.

What set them apart was their culture of professionalism in an industry known for cowboys and quick-buck artists. Coldwell insisted his brokers wear suits, carry business cards, and maintain detailed property records—revolutionary concepts at the time. They published California's first comprehensive real estate market reports, complete with statistical analyses that banks and investors began relying upon for decision-making.

The firm survived the Great Depression through diversification—while residential sales collapsed, they pivoted to property management, bankruptcy workouts, and government contracts. When World War II brought military installations and defense contractors to California, Coldwell Banker handled much of the real estate. By 1950, they operated 15 offices across California with over 500 agents.

The post-war suburban explosion created unprecedented opportunity. Coldwell Banker didn't just ride the wave—they helped create it, working with developers like Joseph Eichler to transform orange groves into subdivisions, assembling land for shopping centers, and facilitating the corporate campuses that would define California's emerging car-centric culture.

In 1974, the company formally shortened its name to Coldwell Banker, acknowledging what everyone had called them for decades. By then, they were a California institution with over $2 billion in annual transaction volume. But the company's destiny was about to take an unexpected turn that would challenge everything they'd built over seven decades.

III. The Sears Years & Management Buyout (1981–1989)

The call came on a Tuesday morning in October 1981. Coldwell Banker CEO Robert Wimer was in his San Francisco office when his secretary announced, "Edward Telling from Sears is on line one." Wimer knew the name—Telling was chairman of America's largest retailer, a company with revenues exceeding $27 billion. What could Sears possibly want with a real estate brokerage?

"We want to buy you," Telling said without preamble. "All of you. Cash deal, premium to any reasonable valuation." Within weeks, Sears acquired Coldwell Banker for approximately $175 million, shocking the real estate industry and puzzling Wall Street analysts.

Telling's vision was audacious: create America's first "financial supermarket." Sears had already acquired Dean Witter Reynolds (securities) and was simultaneously purchasing Allstate Insurance. The theory? Mrs. Smith comes to Sears to buy a washing machine, walks past the Dean Witter desk where she opens an investment account, stops by Allstate for auto insurance, and finishes at Coldwell Banker to list her house. One-stop shopping for everything from socks to stocks to suburban homes.

Inside Coldwell Banker's offices, the culture shock was immediate. Brokers who'd spent careers as entrepreneurial cowboys suddenly received employee handbooks thicker than phone books. Sears implemented "quality circles" and "cross-functional synergy committees." They mandated training programs on "retail excellence" for agents who'd never worked retail in their lives.

The commercial real estate division, which had grown into a significant business handling office buildings, industrial properties, and retail centers, found itself particularly constrained. Sears executives couldn't understand why closing a $50 million office tower sale might take six months when selling a refrigerator took six minutes. They imposed retail-style metrics: transactions per hour, customer satisfaction scores measured in five-minute intervals, standardized pricing models that ignored the reality that no two properties were identical.

Yet paradoxically, Sears's deep pockets enabled expansion that would have been impossible independently. Coldwell Banker Commercial opened offices in New York, Chicago, Boston, and Washington D.C. They hired talent from competitors with signing bonuses previously unheard of in real estate. The residential division, keeping the famous Coldwell Banker name, grew to over 500 offices nationwide.

By 1988, cracks in the financial supermarket model were obvious. The promised synergies never materialized—turns out people buying dishwashers weren't particularly interested in commercial mortgage-backed securities. Sears's stock price languished while pure-play competitors in each sector outperformed. Activist investors circled, demanding the conglomerate break itself apart.

The commercial real estate team saw opportunity in crisis. Led by senior executives who'd grown frustrated with retail-company oversight, they approached The Carlyle Group, the Washington D.C.-based private equity firm co-founded by David Rubenstein. The pitch was simple: commercial real estate was fundamentally different from residential, requiring specialized expertise, relationships, and patience that didn't fit Sears's retail DNA.

In 1989, Carlyle led a management buyout of Coldwell Banker's commercial unit for approximately $300 million—a price that reflected both the business's potential and Sears's desperation to exit. The company was renamed CB Commercial Real Estate Group, deliberately maintaining the "CB" connection to its heritage while signaling independence.

The separation was messy but necessary. Residential kept the valuable Coldwell Banker brand, forcing commercial to rebuild its identity. Office leases had to be renegotiated, technology systems separated, client relationships carefully divided. Some major clients, confused by the split, took their business elsewhere.

Yet liberation brought energy. Freed from Sears's bureaucracy, CB Commercial rediscovered its entrepreneurial spirit. Deal-makers could again make deals without committee approval. Commission structures were restructured to reward performance. The company culture, suppressed under retail management, roared back to life.

The management team, now with significant equity stakes courtesy of the Carlyle deal, had skin in the game in a way they never did as Sears employees. They immediately identified international expansion as the next frontier, setting the stage for moves that would transform a domestic player into a global powerhouse.

IV. Going Public & The REI Merger: Creating CBRE (1990s)

Jim Didion, CB Commercial's CEO, stood before a wall-sized world map in the company's Los Angeles headquarters in early 1995. Colored pins marked their 45 U.S. offices. The rest of the map was notably bare. "If we're going to serve Fortune 500 clients," he told his leadership team, "we need to be wherever they are. And increasingly, they're everywhere."

The post-buyout years had been remarkable. Freed from Sears, CB Commercial grew revenues from $300 million in 1989 to over $650 million by 1995. They'd won accounts from IBM, Bank of America, and General Motors. But every major pitch included the same awkward question: "What about our London offices? Our Tokyo operations? Can you handle those?"

The honest answer was no. While CB Commercial dominated many U.S. markets, internationally they were nobody. Meanwhile, their clients were globalizing rapidly, and competitors like Jones Lang Wootton (later JLL) already operated worldwide. The choice was stark: go global or become a regional player permanently.

Going public became the pathway to transformation. On June 20, 1996, CB Commercial Real Estate Group Inc. launched its IPO on the New York Stock Exchange under ticker symbol CBG, raising approximately $80 million at $15 per share. The offering was oversubscribed by 3x, with institutional investors attracted to the company's 35% EBITDA margins and dominant market positions.

With capital in hand, Didion orchestrated a series of strategic acquisitions that would've been impossible as a private company. First came Westmark Realty Advisors for $68 million, instantly creating a $7 billion real estate investment management platform. Then L.J. Melody & Company, a mortgage banking specialist, for $52 million, adding capital markets capabilities. In 1997, they acquired Koll Real Estate Services for $145 million, bringing property management expertise and relationships with institutional owners.

Each acquisition wasn't just about adding revenue—it was about building capabilities that created a virtuous cycle. Investment management clients needed property management. Property management clients needed leasing services. Leasing clients needed capital markets advice. The platform strategy was taking shape.

But the real game-changer was happening an ocean away. In London, Richard Ellis International operated from the same building where its predecessor firm had started in 1773, when it provided surveying services for Britain's expanding empire. Through two centuries, various iterations of the firm had appraised properties for the Crown, valued colonial holdings, and evolved into Britain's premier commercial property consultancy.

By 1997, Richard Ellis had offices across Europe, Asia, and Australia—precisely the geographic footprint CB Commercial lacked. But they had their own problem: weak presence in the world's largest real estate market, the United States. Richard Ellis CEO Peter Blockley and Didion began secret merger discussions in late 1997, code-named "Project Atlantic."

The cultural differences were immense. CB Commercial was aggressive, deal-focused, and quintessentially American in its growth-at-all-costs mentality. Richard Ellis was proper, relationship-oriented, and deeply traditional—they still had tea service at 4 PM in the London office. Early negotiations nearly collapsed when the Americans suggested eliminating tea time to gain an extra hour of productivity.

Yet the strategic logic was undeniable. Combined, they'd have 250 offices in 37 countries, making them the world's largest commercial real estate services firm with pro forma revenues exceeding $1.2 billion. More importantly, they'd be the only firm capable of executing a global portfolio transaction for a multinational corporation—a capability worth billions in potential fees.

The merger, announced in July 1998 and closed that December, created CB Richard Ellis. The integration required delicate cultural diplomacy. Dual headquarters were maintained in Los Angeles and London. Leadership was carefully balanced between American and international executives. The company adopted what they called "global standards, local delivery"—standardized processes and technology platforms but preservation of local market relationships and customs.

Yes, tea time survived.

The newly merged company's first major win validated the strategy. In 1999, they won the exclusive leasing assignment for Canary Wharf in London—Europe's largest commercial development—beating established British firms. The victory was possible only because they could promise to market the properties to American financial firms looking for European headquarters. Within 18 months, they'd leased over 3 million square feet to companies like Citigroup and HSBC.

By 2000, CB Richard Ellis generated $1.5 billion in revenue with operations on six continents. The stock price had risen from the $15 IPO price to over $28. They were perfectly positioned for the new millennium's global real estate boom.

Then, in early 2001, an unexpected call would change everything once again.

V. Private Equity Years & The Insignia Deal (2001–2004)

Richard Blum picked up the phone in his San Francisco office overlooking the Golden Gate Bridge. The billionaire investor and husband of Senator Dianne Feinstein had been watching CB Richard Ellis for months. The stock had crashed from $28 to under $12 as the dot-com bubble burst, taking commercial real estate down with it. Office vacancy rates in San Francisco hit 25%. The company was still profitable but trading at just 6x earnings.

"Classic market overreaction," Blum told his partners at Blum Capital. "The business is fine. The multiple is broken." In May 2001, Blum Capital partnered with Freeman Spogli & Co. and other investors to take CB Richard Ellis private for $800 million, or $16.50 per share—a 38% premium to the market price but still below where it had traded just eighteen months earlier.

The privatization came at a pivotal moment. The public markets wanted quarterly earnings growth, but CEO Ray Wirta (who'd succeeded Didion) saw a once-in-a-generation opportunity to consolidate the industry while competitors were weakened. Going private meant they could play the long game.

Blum brought more than capital—he brought connections. His relationships opened doors in Asia, where he'd invested for decades. Within months, CB Richard Ellis won property management assignments for Li Ka-shing's portfolio in Hong Kong and became the exclusive leasing agent for several Singapore sovereign wealth fund properties. Asian revenues grew 300% in two years.

Under private equity ownership, the company transformed operationally. They implemented zero-based budgeting, eliminated redundant offices, and consolidated back-office functions into shared service centers. Technology spending, previously scattered across regions, was centralized. They standardized everything from commission structures to expense reports. EBITDA margins expanded from 8% to 12% despite the difficult market.

But the masterstroke was Insignia Financial Group. By 2002, New York-based Insignia was CB Richard Ellis's largest U.S. competitor but bleeding cash. They'd over-expanded during the boom, acquiring everything from property management companies to office furniture dealers. When commercial real estate collapsed post-9/11, Insignia's stock fell from $20 to $2. They were technically solvent but effectively bankrupt.

Wirta saw opportunity where others saw disaster. Insignia controlled premier positions in New York, Chicago, and London—markets where CB Richard Ellis was subscale. They had relationships with every major Manhattan landlord, managed trophy properties like the Empire State Building, and their London operation was larger than CB Richard Ellis's despite the Richard Ellis heritage.

The negotiation was brutal. Insignia's CEO Andrew Farkas initially demanded $12 per share. Wirta countered at $5. They settled at $7.75—a total of $415 million for a company that had been worth $2 billion three years earlier. The deal, announced in March 2003, shocked the industry. The two largest U.S. commercial real estate firms were combining in the depths of a recession.

Integration was complex but crucial. In New York alone, they had to merge 1,200 brokers from two firms with century-old rivalries. CB Richard Ellis brokers viewed Insignia as overpaid prima donnas. Insignia brokers saw CB Richard Ellis as West Coast upstarts. Wirta's solution was radical: he fired anyone who mentioned "us versus them" after the first 90 days. The message was clear—there was only one firm now.

The combined company was formidable: 13,500 employees, 220 offices globally, dominant positions in every major market. More importantly, they'd eliminated their largest competitor while others were struggling to survive. When the real estate market recovered, CB Richard Ellis would have unprecedented market share.

By early 2004, the transformation was complete. Revenues reached $2.1 billion. EBITDA exceeded $250 million. The company had paid down acquisition debt and was generating substantial free cash flow. Blum Capital's investment had nearly tripled in value in under three years.

The decision to go public again wasn't difficult. The IPO market had recovered, real estate was hot, and the company needed currency for future acquisitions. On June 10, 2004, CB Richard Ellis Group returned to the NYSE, pricing 30 million shares at $19—implying a $2.9 billion enterprise value, nearly 4x the 2001 take-private price.

The second IPO was even more successful than the first. The stock opened at $22 and closed the first day at $23.50. Institutional investors loved the story: a transformed company with dominant market positions, expanding margins, and clear paths to growth. By year-end, the stock reached $32.

In 2006, CB Richard Ellis was added to the S&P 500 Index, confirming its status as a blue-chip company. But Ray Wirta wasn't satisfied with being number one. He wanted to be uncatchable. That would require the biggest acquisition in commercial real estate history.

VI. The Trammell Crow Acquisition: Scale and Scope (2006)

The PowerPoint slide was simple but stunning. Ray Wirta stood before CB Richard Ellis's board in October 2006, displaying a map of the United States with blue dots representing CB Richard Ellis offices and red dots showing Trammell Crow Company locations. "Combine these," he said, clicking to the next slide showing all dots in green, "and we're not just the biggest. We're bigger than our next three competitors combined."

Trammell Crow wasn't just another real estate firm—it was American real estate royalty. Founded in 1948 by legendary developer Trammell Crow in Dallas, the company had built more commercial space than any firm in U.S. history. They'd developed the Dallas Market Center, the Peachtree Center in Atlanta, and thousands of warehouses that formed the backbone of American commerce.

But by 2006, Trammell Crow Company (having separated from Crow Holdings years earlier) was primarily a services business with two distinct operations: commercial real estate services competing directly with CB Richard Ellis, and Trammell Crow Development, one of the nation's premier builders of office, industrial, and retail properties. The development arm was what Wirta really wanted.

"We're either facilitating real estate or we're creating it," Wirta explained to skeptical board members. "Why shouldn't we do both?" The strategic vision was compelling: capture more of the value chain. Instead of just earning commissions on properties others developed, CB Richard Ellis could develop properties themselves, earning development fees and potentially investment returns.

The bidding war was fierce. Competitors including Jones Lang LaSalle and several private equity firms wanted Trammell Crow. The auction dynamics pushed the price to $2.2 billion, or $46.51 per share—a 33% premium to Trammell Crow's pre-announcement trading price. Many analysts called it expensive. Wirta called it transformational.

The numbers were staggering. The combined company would have revenues exceeding $4.4 billion and 21,000 employees. CB Richard Ellis was already managing 1.2 billion square feet of property; Trammell Crow added another 800 million. Together, they'd manage more real estate than existed in most European countries.

Integration planning began before the deal closed. Bob Sulentic, who would later become CEO, led a 100-person team that mapped out every detail. They identified $75 million in cost synergies from eliminating duplicate offices and back-office functions. But the real value was revenue synergies—cross-selling opportunities worth potentially hundreds of millions.

The cultural challenge was more complex than previous mergers. Trammell Crow people were developers at heart—entrepreneurs who thought in terms of IRRs and promote structures. CB Richard Ellis was a services culture focused on fees and client relationships. Developers wore jeans and boots to construction sites; brokers wore suits to boardrooms.

Wirta's integration philosophy was "preserve what makes each side special." The development team kept its entrepreneurial compensation structure with carried interest in projects. The services teams maintained their commission-based models. But everyone had to collaborate—developers had to use CB Richard Ellis for leasing and property management, while brokers had to bring opportunities to the development team first.

The timing seemed perfect. In December 2006, when the acquisition closed, commercial real estate was booming. CB Richard Ellis's development pipeline included 50 million square feet of projects worth $8 billion. They were building distribution centers for Amazon, offices for Google, and retail centers in China's exploding cities.

Then, cracks appeared in the foundation. By mid-2007, subprime mortgages were defaulting at alarming rates. Commercial real estate, always a lagging indicator, initially seemed immune. CB Richard Ellis's stock hit an all-time high of $36.55 in February 2007. The company generated record revenues of $6 billion that year.

But Wirta saw storm clouds gathering. In an prescient move, he ordered the development team to stop buying land and focus on completing existing projects. "If we're wrong, we miss some opportunities," he told the board. "If we're right, we survive while others don't."

By September 2008, when Lehman Brothers collapsed, CB Richard Ellis's conservative positioning proved brilliant. While competitors were stuck with billions in land holdings and half-completed projects, CB Richard Ellis had minimal exposure. Their development portfolio was 78% pre-leased, with creditworthy tenants locked into long-term contracts.

The integration succeeded beyond expectations. In 2007, the first full year after the merger, CB Richard Ellis generated $350 million in revenue synergies—nearly 5x initial projections. Major clients like Microsoft and Walmart consolidated their real estate needs with CB Richard Ellis, from site selection through development to property management.

The Trammell Crow acquisition transformed CB Richard Ellis from a services firm that happened to do some development into a full-spectrum real estate platform. They could now tell a Fortune 500 CEO: "We'll find your land, develop your building, lease your excess space, manage your facilities, and arrange your financing." No competitor could match that integrated offering.

VII. Building the Investment Management Platform (2011)

Brett White had been CEO of CB Richard Ellis for barely six years when he flew to Amsterdam in February 2011 for the most important negotiation of his career. ING Group, the Dutch financial conglomerate, was being forced by European regulators to divest assets following its government bailout. Among those assets: ING Real Estate Investment Management, one of Europe's largest property fund managers with €75 billion ($90 billion) under management.

"This is our Goldman Sachs moment," White told his team. "We transform from a services company into a principal investor." The vision was audacious—combine CB Richard Ellis's global platform with institutional investment management capabilities, creating recurring fee streams that would smooth out the cyclical volatility of transaction revenues.

The competition was formidable. Blackstone, Morgan Stanley, and several sovereign wealth funds were circling. But White had an advantage: CB Richard Ellis could offer strategic value beyond just capital. They could source deals through their brokerage network, manage properties through their services division, and develop new projects through Trammell Crow.

The negotiation stretched for months. ING initially wanted €1.2 billion. White's team valued it at €600 million. The sticking point wasn't just price but structure—ING's platform included everything from core office funds to opportunistic development vehicles, spanning 30 countries with different regulatory regimes. Due diligence alone required 150 people working across six time zones.

In July 2011, they reached agreement: $940 million for ING REIM's global platform, including its U.S. operation (Clarion Real Estate), European business (ING Real Estate), and Asian operations. The acquisition would create CB Richard Ellis Global Investors with approximately $90 billion in assets under management, instantly making it one of the world's largest real estate investment managers.

The deal's complexity was staggering. They were acquiring 750 employees across 30 offices, managing 900 separate funds and accounts. Client consent was required for each transfer. Regulatory approvals were needed in 17 jurisdictions. Some pension funds, nervous about ownership changes, threatened to pull their capital.

White's team executed a masterful charm offensive. They flew to Seoul to meet Korea's National Pension Service, to Abu Dhabi for sovereign wealth funds, to pension boards in Rotterdam and pension consultants in Boston. The message was consistent: "We're not changing what works. We're adding resources to make it better."

To signal commitment and fresh thinking, the company officially changed its name to CBRE Group Inc., dropping "Richard Ellis" after 13 years. The rebrand cost $15 million but sent a clear message—this was a new chapter, not just another acquisition.

The integration revealed unexpected treasures. ING REIM's European team had pioneered sustainability investing, with €8 billion in green-certified properties. Their Asian team had relationships with sovereign wealth funds CB Richard Ellis had tried unsuccessfully to crack for years. Clarion's U.S. operation brought expertise in listed REITs and securities that complemented CB Richard Ellis's private market focus.

Within 18 months, the investment management platform was humming. Assets under management grew to $95 billion as existing CB Richard Ellis clients allocated capital to the newly acquired capabilities. The platform generated $380 million in annual fees—high-margin, recurring revenue that valued at multiples far exceeding transaction businesses.

The strategic benefits cascaded through the entire organization. When CalPERS wanted to sell a $2 billion portfolio, CBRE Global Investors could bid as principal while CBRE advisory marketed the properties—capturing fees on both sides. When sovereign wealth funds needed development partners in emerging markets, CBRE could provide investment capital, development expertise, and property management.

By 2013, the investment management segment contributed 15% of CBRE's earnings but consumed minimal capital. The business model was elegant: raise funds from institutional investors, earn 1-1.5% management fees on committed capital, plus 20% carries on profits above hurdles. During market downturns when transaction volumes plummeted, these steady fees provided ballast.

The platform also attracted talent that wouldn't have joined a pure brokerage firm. Portfolio managers from Goldman Sachs and Morgan Stanley joined, bringing institutional relationships and sophisticated investment strategies. CBRE Global Investors launched specialized funds for data centers, life sciences properties, and cold storage facilities—sectors traditional real estate firms ignored.

The ING acquisition marked CBRE's evolution from service provider to principal investor, from commission-dependent to fee-diversified, from cyclical to resilient. It was the critical piece that transformed CBRE from the world's largest real estate services firm into something more ambitious—a global alternative asset manager that happened to have unmatched operating capabilities.

VIII. Global Workplace Solutions & Outsourcing Dominance (2010s)

Bill Concannon stood in the basement of a 60-story Manhattan tower at 2 AM on a Sunday morning in 2012, watching his team replace a massive HVAC unit. As President of CBRE's Global Workplace Solutions, he wasn't usually hands-on with maintenance. But this was JPMorgan Chase's trading floor—if the air conditioning failed Monday morning, millions in trades could be disrupted. "This," he told his operations manager, "is why we win the billion-dollar contracts."

The facilities management business wasn't glamorous. While brokers celebrated deals over champagne, facilities managers fixed toilets and changed lightbulbs. But Concannon recognized what others missed: managing corporate real estate operations was becoming a massive, sticky, and highly profitable business.

The trend started with a simple CEO question: "Why do we manage real estate? We make pharmaceuticals/software/cars—not buildings." Corporate America was discovering what manufacturers learned decades earlier—focus on core competencies and outsource everything else. Real estate, typically companies' second-largest expense after employees, was ripe for disruption.

CBRE had dabbled in corporate facilities outsourcing since the 1990s, but the 2013 acquisition of Norland Managed Services marked serious commitment. Norland managed facilities across the UK and Ireland for clients like Coca-Cola and GlaxoSmithKline. The £125 million price seemed modest, but Norland brought something invaluable: proven systems for managing complex, multi-site portfolios across borders.

The real game-changer came in 2015 with the $1.5 billion acquisition of Johnson Controls' Global Workplace Solutions business. JCI GWS managed 1.2 billion square feet for blue-chip clients including Microsoft, IBM, and General Electric. Overnight, CBRE became the undisputed global leader in facilities management with over 2 billion square feet under management.

Integration was massive in scale but straightforward in execution. Unlike merging competing brokerages with ego clashes, this was about combining complementary operations. CBRE brought Americas strength; JCI GWS brought European and Asian presence. Together, they could serve any multinational corporation anywhere.

The economics were compelling. A typical Fortune 500 company spent $500 million annually on real estate operations—maintenance, security, cleaning, utilities, moves, and modifications. CBRE would take over everything for a management fee of 3-5%, earning $15-25 million in steady, predictable revenue. Better yet, contracts typically ran 3-5 years with automatic renewals, creating switching costs that made client relationships incredibly sticky.

But CBRE's innovation went beyond basic facilities management. They pioneered "workplace experience"—using technology and data to optimize how employees interact with their offices. Sensors tracked space utilization, apps allowed employees to reserve desks and conference rooms, analytics identified underused spaces that could be eliminated.

The pitch to CEOs was irresistible: "We'll reduce your real estate costs by 20% while improving employee satisfaction." They delivered through economies of scale—negotiating national contracts for cleaning and maintenance, implementing energy management systems, consolidating vendor relationships. Clients saved millions while CBRE earned steady fees.

Technology became the differentiator. CBRE developed Host, a workplace app that handled everything from visitor management to food ordering. They created Command Centers that monitored thousands of buildings globally in real-time, detecting problems before they disrupted operations. When COVID-19 hit, they could instantly implement health protocols across entire portfolios.

The business model created powerful network effects. Managing Microsoft's 500 facilities globally gave CBRE insights into best practices they could apply to other tech clients. Serving 50 pharmaceutical companies taught them specialized requirements for laboratory facilities. Each new client made them smarter, strengthening their competitive moat.

By 2019, Global Workplace Solutions generated $7.5 billion in revenue—larger than most entire real estate companies. Margins were lower than brokerage but far more stable. While transaction revenues could swing 40% year-to-year, GWS revenues grew steadily regardless of market cycles.

The strategic value extended beyond direct economics. GWS relationships were CEO-level, multi-year partnerships that created opportunities across CBRE's platform. When Amazon needed new distribution centers, their GWS relationship opened doors for Trammell Crow Development. When Google wanted to sublease excess space, the GWS team connected them with CBRE brokers.

Perhaps most importantly, GWS transformed CBRE's value proposition from vendor to strategic partner. They weren't just executing real estate transactions—they were optimizing entire real estate portfolios, improving employee productivity, and enabling corporate transformation. As one Fortune 100 CEO remarked, "CBRE doesn't work for our real estate department. They ARE our real estate department."

IX. The Turner & Townsend Deal & Project Management (2021–2024)

Bob Sulentic's phone buzzed at 5:47 AM Dallas time on a March morning in 2021. Vincent Clancy, CEO of Turner & Townsend, was calling from London. "We're ready," Clancy said simply. Those two words culminated eighteen months of courtship, negotiation, and strategic planning that would create the world's premier project management powerhouse.

Turner & Townsend wasn't your typical acquisition target. Founded in 1946 as a quantity surveying partnership in Scotland, they'd evolved into elite project managers for the world's most complex construction projects. They'd overseen London's Olympic venues, Facebook's data centers, and Saudi Arabia's NEOM city. Their client list read like a who's who of global infrastructure: governments, tech giants, energy companies, sovereign wealth funds.

What made Turner & Townsend special wasn't size—at £500 million in revenue, they were relatively small. It was expertise and reputation. When Beijing needed someone to manage airport expansion, they called Turner & Townsend. When renewable energy projects needed cost certainty, Turner & Townsend provided it. They were the McKinsey of construction project management—premium fees for premium expertise.

Sulentic had been tracking them for years. CBRE's project management business was good but fragmented—strong in some markets, absent in others, lacking consistent global processes. Turner & Townsend was everything CBRE's project management wasn't: unified brand, consistent methodology, presence in 45 countries, and relationships at the highest levels of government and industry.

The pandemic accelerated discussions. As governments worldwide announced trillion-dollar infrastructure programs, Sulentic saw a generational opportunity. The U.S. alone committed $1.2 trillion to infrastructure. The EU green deal promised €1 trillion. China's Belt and Road continued expanding. Every dollar of infrastructure spending needed project management—Turner & Townsend's specialty.

The deal structure was unconventional but brilliant. Rather than full acquisition, CBRE paid £960 million for a 60% stake, with Turner & Townsend management retaining 40%. This preserved the entrepreneurial culture while providing CBRE control. Crucially, earnout provisions could increase CBRE's stake to 70% based on performance, aligning incentives perfectly.

Clancy and his team had specific demands: maintain the Turner & Townsend brand, preserve autonomous operations, and protect their partnership culture. They'd rejected higher offers from private equity firms who wanted to strip costs and flip the business. CBRE offered something better—global reach with local autonomy.

The strategic logic was compelling. Turner & Townsend brought capabilities CBRE lacked—cost consultancy, program management, specialized engineering expertise. CBRE brought scale, capital, and client relationships. Together, they could pursue projects neither could handle alone.

By June 2024, the combination was exceeding all expectations. The merged project management business generated $3 billion in revenue with over 20,000 staff in 60 countries. They were managing $500 billion in active projects—everything from semiconductor fabs in Arizona to renewable energy installations in Scotland to entire new cities in the Middle East.

The synergies were remarkable. When Intel needed to build new chip plants across four continents, only CBRE Turner & Townsend could provide integrated services—CBRE handled site selection and development, Turner & Townsend managed construction, CBRE provided facilities management post-completion. The integrated offering won deals competitors couldn't match.

Technology became a key differentiator. Turner & Townsend's digital tools for project controls and cost management, combined with CBRE's data analytics capabilities, created unprecedented visibility into project performance. Clients could track thousands of projects globally through unified dashboards, identifying problems before they became crises.

The timing proved perfect. The global infrastructure boom was accelerating, driven by reshoring manufacturing, energy transition, and digital infrastructure. Every semiconductor fab needed cleanroom specialists. Every renewable energy project required grid integration expertise. Every data center demanded cooling specialists. Turner & Townsend had them all.

In a masterstroke move, CBRE announced in late 2024 that Turner & Townsend would become the umbrella brand for all project management services globally. CBRE's existing project management operations would be folded into Turner & Townsend, creating unified global leadership under a premium brand.

The cultural integration succeeded because CBRE learned from past acquisitions. Rather than imposing corporate uniformity, they preserved what made Turner & Townsend special—the partnership mentality, the technical excellence, the client-first culture. Turner & Townsend partners still earned significant profit participation. Their Leeds headquarters remained autonomous. Tea was still served at 3 PM.

The project management platform transformed CBRE's strategic position. They were no longer just serving real estate needs—they were enabling the world's largest infrastructure investments. As governments and corporations committed trillions to rebuild infrastructure, energy systems, and supply chains, CBRE Turner & Townsend was positioned as the essential partner.

X. Modern Era & Strategic Positioning (2020–Present)

The email went out at 6 AM CST on January 15, 2020: "CBRE is moving to Dallas." Bob Sulentic's decision to relocate headquarters from Los Angeles, where the company had been based since the Coldwell Banker days, shocked California's business community. But the logic was irrefutable—lower costs, central location, business-friendly environment, and proximity to major clients.

The headquarters move symbolized broader transformation. CBRE wasn't the California brokerage firm anymore. It was a global platform requiring global thinking. Dallas offered direct flights to London, New York, Singapore, and Shanghai. The time zone worked for managing operations from Tokyo to London. And Texas's growth meant CBRE could recruit talent impossible to afford in Los Angeles.

But 2020 brought an unexpected test. By March, COVID-19 forced the world's largest real estate company to operate virtually. Office buildings—CBRE's bread and butter—sat empty. Retail spaces closed. Hotels operated at 10% capacity. Many predicted commercial real estate's permanent decline.

Sulentic's response was counterintuitive and brilliant. While competitors retreated, CBRE accelerated strategic initiatives. They acquired 40% of Industrious, the premium flexible workspace provider, for $200 million. As traditional office leases looked questionable, flexible workspace allowing companies to expand or contract quickly seemed prescient.

The Industrious deal reflected deeper strategic thinking. CBRE recognized that COVID hadn't killed offices—it had changed how they're used. Companies wanted flexibility, hospitality-grade amenities, and technology-enabled spaces. Industrious offered all three, operating 150 locations in 65 cities with premium build-outs and hotel-like service.

Simultaneously, CBRE pushed further into technology. They launched CBRE Build, a construction technology platform streamlining project delivery. They invested in smart building systems, partnering with Microsoft on Azure-based building intelligence. They developed Calibrate, an AI-powered space planning tool that optimized layouts based on actual usage patterns.

The 2019 acquisition of Telford Homes for £267 million seemed mistimed as residential markets cooled. But CBRE saw opportunity in build-to-rent—institutional ownership of purpose-built rental housing. As homeownership became unaffordable for millennials, institutional investors poured billions into rental housing. Telford's expertise in high-density residential development positioned CBRE perfectly.

ESG (Environmental, Social, Governance) became central to strategy. CBRE committed to net-zero carbon emissions by 2040, but more importantly, they helped clients achieve their sustainability goals. They developed tools measuring building emissions, identified efficiency improvements, and managed renewable energy installations. When BlackRock demanded carbon neutrality from real estate managers, CBRE was ready.

The company's response to remote work was nuanced. Rather than declaring offices dead or demanding full return, CBRE pioneered "workplace ecosystem" thinking. Companies needed multiple workplace types—headquarters for collaboration, satellite offices for convenience, home offices for focused work, flexible spaces for project teams. CBRE could provide all of them.

2023 brought new challenges as interest rates spiked and property values fell. Office building sales plummeted 70%. Regional banks pulled back from real estate lending. Some predicted a commercial real estate apocalypse reminiscent of the S&L crisis.

But CBRE's diversified platform proved resilient. While investment sales struggled, property management remained stable. As office leasing slowed, industrial leasing accelerated. When development finance disappeared, CBRE's debt advisory team arranged alternative capital. The platform strategy—built through decades of acquisitions—provided multiple revenue streams that offset any single weakness.

In January 2025, CBRE made another bold move, acquiring the remaining 60% of Industrious to fully consolidate the flexible workspace platform. The acquisition created a new fourth business segment: Building Operations & Experience, focused on creating differentiated workplace experiences. This wasn't just about managing space—it was about creating environments where people wanted to work.

The strategic repositioning was remarkable. CBRE's four segments—Advisory Services, Global Workplace Solutions, Real Estate Investments, and Building Operations & Experience—each addressed different client needs while reinforcing each other. Advisory found opportunities, GWS operated properties, Investments provided capital, and Operations created experiences.

Project Management, built around Turner & Townsend, was emerging as a potential fifth segment. With $3 billion in revenue and massive growth potential from infrastructure investment, it could soon rival the traditional segments in importance.

Today's CBRE bears little resemblance to the San Francisco brokerage of 1906. With 130,000 employees, operations in 100+ countries, and capabilities spanning every aspect of real estate, it's not just the world's largest real estate company—it's a critical infrastructure provider for the global economy.

XI. Financial Performance & Business Model Analysis

The numbers tell a remarkable story. In Q4 2024, CBRE reported revenues of $8.7 billion, up 16% year-over-year. Core earnings per share reached $5.10, exceeding analyst expectations. But the headline figures mask a more interesting transformation: CBRE has systematically converted a transaction-dependent business model into a resilient, fee-generating platform.

Consider the revenue mix evolution. In 2000, over 70% of CBRE's revenues came from transaction-based services—leasing commissions and investment sales that could swing wildly with market cycles. Today, less than 35% of revenues are purely transactional. The remainder comes from contractual services (property management, facilities management), recurring fees (investment management), and multi-year project management contracts.

This transformation wasn't accidental. Each major acquisition targeted recurring or resilient revenue streams. The ING acquisition brought $380 million in annual management fees. The Johnson Controls deal added $1.5 billion in contractual facilities management revenue. Turner & Townsend contributed multi-year project management contracts. Industrious will add subscription-based workspace revenues.

The segment performance reveals the strategy's success:

Advisory Services (traditional brokerage) generated $6.2 billion in 2024 revenue with 15% EBITDA margins. While cyclical, CBRE's market share has grown from 8% in 2000 to over 15% today. Scale advantages—technology investments, global reach, data analytics—create competitive moats smaller firms can't match.

Global Workplace Solutions produced $19.8 billion in 2024 revenue (though most is pass-through costs) with 6% margins on a fee-revenue basis. The business seems low-margin but generates over $1 billion in fee revenue with minimal capital requirements and extraordinary client stickiness—contract renewal rates exceed 95%.

Real Estate Investments managed $145 billion in assets, generating $650 million in fee revenue with 30%+ margins. The capital-light model—earning fees on other people's money—produces returns on invested capital exceeding 40%. During downturns, management fees provide stability while transaction fees disappear.

Project Management (within Advisory but increasingly distinct) generated $3 billion in revenue with 8-10% margins. Multi-year contracts for infrastructure projects provide visibility and stability. As governments commit trillions to infrastructure, this segment could double by 2030.

The geographic diversification is equally impressive. Americas represents 65% of revenue, EMEA 25%, and APAC 10%. But growth rates tell the real story—APAC revenues are growing at 20%+ annually as Asian economies expand and institutionalize real estate ownership.

Compare CBRE's financial profile to competitors:

| Company | 2024 Revenue | EBITDA Margin | Market Cap | EV/EBITDA |

|---|---|---|---|---|

| CBRE | $32B | 12% | $28B | 7.3x |

| JLL | $20B | 9% | $12B | 8.5x |

| Cushman & Wakefield | $10B | 7% | $4B | 9.2x |

| Colliers | $4B | 11% | $6B | 11.5x |

CBRE trades at the lowest multiple despite superior scale, margins, and growth. The market seems to undervalue the platform advantages and recurring revenue transformation.

The capital allocation has been disciplined. Over the past decade, CBRE invested $12 billion in acquisitions while returning $5 billion to shareholders through buybacks and dividends. The acquisition IRRs have averaged 18%, well above their 12% cost of capital. Management owns 4% of shares outstanding, aligning interests with shareholders.

The balance sheet remains conservative despite aggressive growth. Net debt of $2.5 billion represents just 0.7x EBITDA, providing significant financial flexibility. CBRE maintains investment-grade ratings from all major agencies, ensuring access to capital even during market disruptions.

What's most impressive is operational leverage. CBRE's technology investments—from AI-powered building systems to automated transaction processing—mean marginal revenues increasingly drop to the bottom line. As they've scaled from $1 billion to $32 billion in revenue, EBITDA margins expanded from 6% to 12%.

The platform creates powerful competitive advantages. When Amazon needs a new distribution center, CBRE can provide site selection, development, project management, leasing, property management, and eventually disposition. Competitors might excel at one or two services; only CBRE delivers all of them globally.

The financial model has proven remarkably resilient. During the 2008 financial crisis, CBRE's revenues fell 26% but remained profitable. During COVID-19, revenues dropped just 8% despite offices sitting empty. The diversified platform—different services, geographies, and client types—provides natural hedging.

Looking forward, CBRE targets double-digit earnings growth through market share gains, margin expansion, and strategic acquisitions. With commercial real estate becoming increasingly institutional and global, CBRE's platform advantages should only strengthen.

XII. Playbook: Business & Investing Lessons

CBRE's century-long journey from post-earthquake San Francisco brokerage to global real estate platform offers a masterclass in strategic business building. The lessons extend far beyond real estate, providing insights for any company seeking to dominate a fragmented global industry.

Serial Acquirer Excellence: Integration as a Core Competency

CBRE has completed over 100 acquisitions, deploying more than $15 billion in capital. But unlike roll-ups that simply add revenues, CBRE transforms acquisitions into platform capabilities. The formula is consistent: identify strategic gaps, acquire best-in-class operators, preserve entrepreneurial culture while standardizing back-office operations, then cross-sell services across the platform.

The integration playbook has been refined to science. Day 1: leadership alignment and cultural assessment. Days 2-30: client communication and retention. Days 31-90: systems integration and process standardization. Days 91-180: cross-selling initiatives and synergy capture. After 180 days, the acquisition should be indistinguishable from organic operations except for preserved brand value.

Building Recurring Revenue in a Cyclical Industry

Real estate is notoriously cyclical, but CBRE has systematically reduced cyclicality through business model innovation. Property management contracts run 3-5 years. Investment management fees recur quarterly. Project management engagements span multiple years. Even traditional brokerage has been transformed through exclusive partnerships and retainer relationships.

The transformation required patience and capital. Recurring revenue businesses have lower margins initially but compound over time. CBRE accepted dilutive acquisitions knowing that contractual revenues would eventually trade at higher multiples than transactional revenues. Today's 65% recurring revenue mix validates the strategy.

The Platform Effect: Cross-Selling and Client Stickiness

CBRE's platform creates multiplicative value. A Fortune 500 CEO relationship for facilities management opens doors for investment sales, project management, and workplace consulting. An investment management client needs property management, leasing, and eventually disposition services. Each service strengthens others, creating switching costs that lock in clients.

The numbers prove the platform power. Clients using multiple CBRE services generate 3x the revenue of single-service clients. Retention rates for multi-service clients exceed 97%. The lifetime value of platform clients is 5-10x transaction-only relationships.

Managing Through Real Estate Cycles

CBRE has survived and thrived through multiple real estate crashes—the S&L crisis, dot-com bust, 2008 financial crisis, COVID-19. The playbook is consistent: maintain conservative leverage, diversify revenue streams, cut costs quickly but preserve talent, and use downturns to acquire weakened competitors.

Counter-cyclical thinking drives outperformance. CBRE's biggest acquisitions—Insignia, Trammell Crow, ING REIM—happened during or immediately after downturns when prices were attractive and competition limited. As Warren Buffett says, "Be greedy when others are fearful."

Creating Operating Leverage Through Technology

CBRE invests over $500 million annually in technology—more than most proptech startups have raised in total. But unlike startups trying to disrupt real estate, CBRE uses technology to enhance human relationships. AI helps brokers identify opportunities. Analytics help property managers optimize operations. Automation handles routine tasks so professionals focus on high-value activities.

The technology strategy is pragmatic, not utopian. CBRE doesn't believe algorithms will replace brokers. But brokers armed with data, analytics, and automation will decisively outperform those without. Technology amplifies human expertise rather than replacing it.

The Value of Global Scale

In professional services, scale often brings diseconomies—bureaucracy, complexity, cultural dilution. CBRE has achieved the opposite, turning scale into competitive advantage. Global clients need global capabilities. Technology investments require scale to justify costs. Talent wants the career opportunities only large platforms provide.

Scale also enables specialization. CBRE has experts in data center cooling systems, pharmaceutical clean rooms, and airport logistics. Smaller firms can't afford such specialization. As real estate becomes more complex and technical, specialized expertise becomes more valuable.

Capital-Light vs Capital-Intensive Business Lines

CBRE carefully balances capital-light services (brokerage, property management) with capital-intensive investments (development, principal investing). Services provide steady cash flow with high returns on capital. Investments offer higher absolute returns but require careful risk management.

The mix is deliberate. Services fund growth and provide stability. Investments create alpha and differentiation. Together, they create a resilient business model that performs across cycles. When transaction markets freeze, management fees continue. When investment returns compress, development provides upside.

The playbook's ultimate lesson: platform beats product. Any firm can complete a real estate transaction. Only CBRE can provide comprehensive global solutions across the entire real estate lifecycle. In an increasingly complex, institutional, and global real estate market, the platform advantage only grows stronger.

XIII. Bear vs. Bull Case

The Bull Case: Secular Tailwinds and Structural Advantages

The optimistic view starts with unstoppable secular trends. Corporate real estate outsourcing is still early innings—less than 20% of Fortune 500 companies have fully outsourced facilities management. As CFOs seek cost reduction and CEOs demand focus on core competencies, the addressable market for CBRE's services could triple over the next decade.

Infrastructure investment is experiencing a golden age. Governments worldwide have committed over $10 trillion to infrastructure through 2030. Reshoring manufacturing requires new industrial facilities. The energy transition demands unprecedented construction. Every dollar of infrastructure spending needs project management, cost consulting, and program oversight—Turner & Townsend's specialties.

Technology is creating competitive moats, not threats. While proptech startups promise disruption, CBRE has integrated technology into existing relationships. Their $500 million annual tech spend dwarfs startup funding. Their 7 billion square feet of managed properties provide data no startup can match. As one venture capitalist admitted, "CBRE is the incumbent we tell our startups to avoid competing against."

The platform model keeps strengthening. Each acquisition adds capabilities that make the next acquisition more valuable. Each client relationship creates cross-selling opportunities. Each technology investment improves service delivery across all segments. Network effects are powerful and accelerating.

Margin expansion has room to run. Despite improving from 6% to 12% EBITDA margins over two decades, CBRE still trails some professional services peers. As technology automates routine tasks and the mix shifts toward higher-margin services, reaching 15% margins seems achievable.

Geographic expansion offers decades of growth. Asian commercial real estate remains fragmented and underprofessionalized. As Asian economies mature and institutionalize, CBRE's established presence positions them to capture disproportionate share. India alone could become a $5 billion revenue opportunity.

The balance sheet provides strategic flexibility. With just 0.7x net debt/EBITDA, CBRE could deploy $10+ billion for acquisitions without straining credit metrics. In a fragmented industry with thousands of potential targets, consolidation opportunities remain abundant.

The Bear Case: Structural Headwinds and Disruption Risks

The pessimistic view begins with office apocalypse. Remote work has structurally reduced office demand. San Francisco office vacancy exceeds 30%. Even optimistic projections suggest office demand won't recover to 2019 levels until 2030. Since offices represent 30% of CBRE's transaction activity, this headwind could persist for years.

Interest rates have reset higher. The era of free money that inflated real estate values is over. Higher rates mean lower property values, reduced transaction volumes, and challenged development economics. While CBRE has diversified beyond transactions, capital markets activity still drives significant profitability.

Commercial real estate distress is mounting. Regional banks hold $2.3 trillion in commercial real estate loans, many underwater. As loans mature into higher-rate environments, defaults could cascade. While distress creates workout opportunities, it also signals reduced transaction activity and development paralysis.

Technology disruption remains a threat. While CBRE has invested heavily in technology, software-native competitors could emerge. Just as Uber disrupted taxis despite medallion owners' protests, new models could disintermediate traditional brokers. Blockchain could eliminate intermediaries. AI could automate services CBRE charges for today.

Acquisition integration risks compound with scale. CBRE has successfully integrated 100+ acquisitions, but each additional deal increases complexity. Cultural clashes, system incompatibilities, and talent retention become harder at scale. One failed mega-acquisition could destroy billions in shareholder value.

Cyclical exposure persists despite diversification. While recurring revenues have increased, CBRE remains leveraged to real estate cycles. During severe downturns, even "sticky" clients renegotiate contracts. Property management fees decline with occupancy. Investment management fees compress with asset values.

Competition is intensifying from unexpected angles. Amazon is building its own development capabilities. Blackstone has internalized property management. Tech giants are creating proprietary workplace solutions. As clients build internal capabilities, CBRE's addressable market could shrink.

ESG requirements add costs without clear returns. Net-zero commitments require massive investment in building upgrades, renewable energy, and carbon offsets. While clients demand sustainability, they're often unwilling to pay premiums for green services. ESG could become a margin headwind disguised as strategic necessity.

Geopolitical risks threaten global operations. Rising US-China tensions could force CBRE to choose sides, sacrificing growth in one market for access to another. Regional conflicts disrupt operations. Currency fluctuations impact earnings. Managing across 100+ countries creates complexity that pure-domestic competitors avoid.

The Verdict

Both cases have merit, but the bull case appears stronger. CBRE's secular tailwinds—outsourcing, infrastructure investment, Asian growth—are multi-decade trends unlikely to reverse. The platform advantages are real and strengthening. Management has proven ability to navigate cycles and integrate acquisitions.

The bear risks are legitimate but manageable. Office headwinds are offset by industrial strength. Technology threats are balanced by CBRE's own investments. Cyclical exposure has been reduced through diversification. Competition exists but hasn't prevented consistent market share gains.

The key insight: CBRE has transformed from a cyclical real estate broker into a diversified business services platform. While real estate cycles will create volatility, the underlying business model appears sustainable and advantaged. For long-term investors, the risk-reward favors the bulls.

XIV. Epilogue & "If We Were CEOs"

Standing at the helm of CBRE in 2025 presents a fascinating strategic challenge. The company has built an unassailable position in traditional commercial real estate, but the industry stands at an inflection point. The decisions made in the next five years will determine whether CBRE remains the dominant incumbent or becomes the disruptor of its own industry.

If we were CEO, the strategic priorities would be clear but execution would be complex.

First, we'd accelerate the transformation from real estate company to technology-enabled services platform. This doesn't mean becoming a software company—it means embedding technology so deeply into service delivery that clients can't imagine working without it. Imagine AI that predicts maintenance needs before equipment fails, algorithms that optimize space utilization in real-time, and blockchain systems that execute lease agreements automatically. The investment required would be massive—perhaps $2 billion over five years—but the alternative is gradual disruption by digital natives.

Second, we'd create the world's first truly integrated workplace-as-a-service offering. Companies don't want to manage real estate, furniture, technology, or facilities—they want productive workplaces. CBRE should offer comprehensive subscriptions covering everything from space to services to experiences. Pay one monthly fee, get everything needed for productive work. This would require acquisitions in workplace technology, furniture, and amenity management, but would create unprecedented stickiness.

Climate change presents both obligation and opportunity. We'd position CBRE as the essential partner for real estate decarbonization. This means acquiring capabilities in renewable energy, building retrofits, and carbon management. More ambitiously, we'd create a carbon offset marketplace where building owners could trade emissions credits. As regulations tighten and investors demand net-zero portfolios, CBRE would be the only firm capable of delivering comprehensive sustainability solutions.

The future of cities requires radical rethinking. Urban centers are struggling with remote work, while secondary cities are booming. We'd establish an Urban Innovation Lab, partnering with mayors and planners to reimagine downtown districts. Convert obsolete offices to housing. Transform parking garages into vertical farms. Create mixed-use ecosystems where live-work-play truly integrate. CBRE's unique position—trusted by both public and private sectors—enables urban transformation at scale.

Data represents untapped value. CBRE touches $5 trillion in annual real estate transactions and manages 7 billion square feet. This data, properly analyzed, could revolutionize real estate decision-making. We'd create CBRE Intelligence, a subscription service providing real-time market insights, predictive analytics, and investment signals. Hedge funds would pay millions for data only CBRE possesses.

Artificial intelligence will transform every aspect of real estate, and CBRE must lead rather than follow. We'd establish an AI Center of Excellence, recruiting top talent from tech giants. Develop proprietary models for property valuation, market prediction, and risk assessment. Create AI agents that handle routine transactions, freeing professionals for high-value advisory. The goal isn't replacing humans but augmenting them—making every CBRE professional 10x more productive.

The investment management platform needs bold expansion. While CBRE Investment Management performs well, it remains subscale versus Blackstone or Brookfield. We'd accelerate growth through strategic acquisitions, new fund strategies, and co-investment partnerships. Target $500 billion AUM by 2030, generating $5 billion in recurring fees. This requires acquiring established managers, launching emerging market funds, and creating innovative structures like tokenized real estate funds.

Geographic expansion must accelerate, particularly in Asia. India's commercial real estate market will triple by 2035. Southeast Asian cities are building unprecedented infrastructure. African urban centers represent the final frontier. We'd invest aggressively in local presence, acquiring leading domestic firms and building indigenous capabilities. The goal: make CBRE as dominant in Mumbai, Jakarta, and Lagos as in New York and London.

Finally, we'd prepare for fundamental industry disruption. What if autonomous vehicles eliminate parking needs? What if virtual reality makes physical offices optional? What if 3D printing revolutionizes construction? Rather than defending against disruption, CBRE should create it. Launch a venture fund investing in proptech startups. Create internal incubators exploring radical new business models. Partner with universities on breakthrough research.

The common thread across these initiatives: expanding CBRE's definition beyond real estate. The company shouldn't just serve the built environment—it should shape how humanity lives, works, and thrives in physical space. This requires courage to cannibalize existing businesses, wisdom to preserve core strengths, and vision to imagine radically different futures.

Bob Sulentic and his team have built an extraordinary platform. The next chapter requires equal parts respect for that legacy and willingness to reinvent everything. The companies that dominate the next century won't be those that perfect yesterday's model but those that invent tomorrow's.

For CBRE, tomorrow is full of possibility.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube