MOIL: India's Manganese Monopoly Story

I. Cold Open & Episode Thesis

Picture this: Deep beneath the earth in Balaghat, Madhya Pradesh, miners descend 360 meters into darkness—deeper than the Eiffel Tower is tall—to extract a silvery-gray metal that most people have never heard of. Yet without this metal, the modern world would grind to a halt. No skyscrapers, no railways, no automobiles. This is manganese, and the company that controls half of India's supply has roots stretching back to the British Raj.

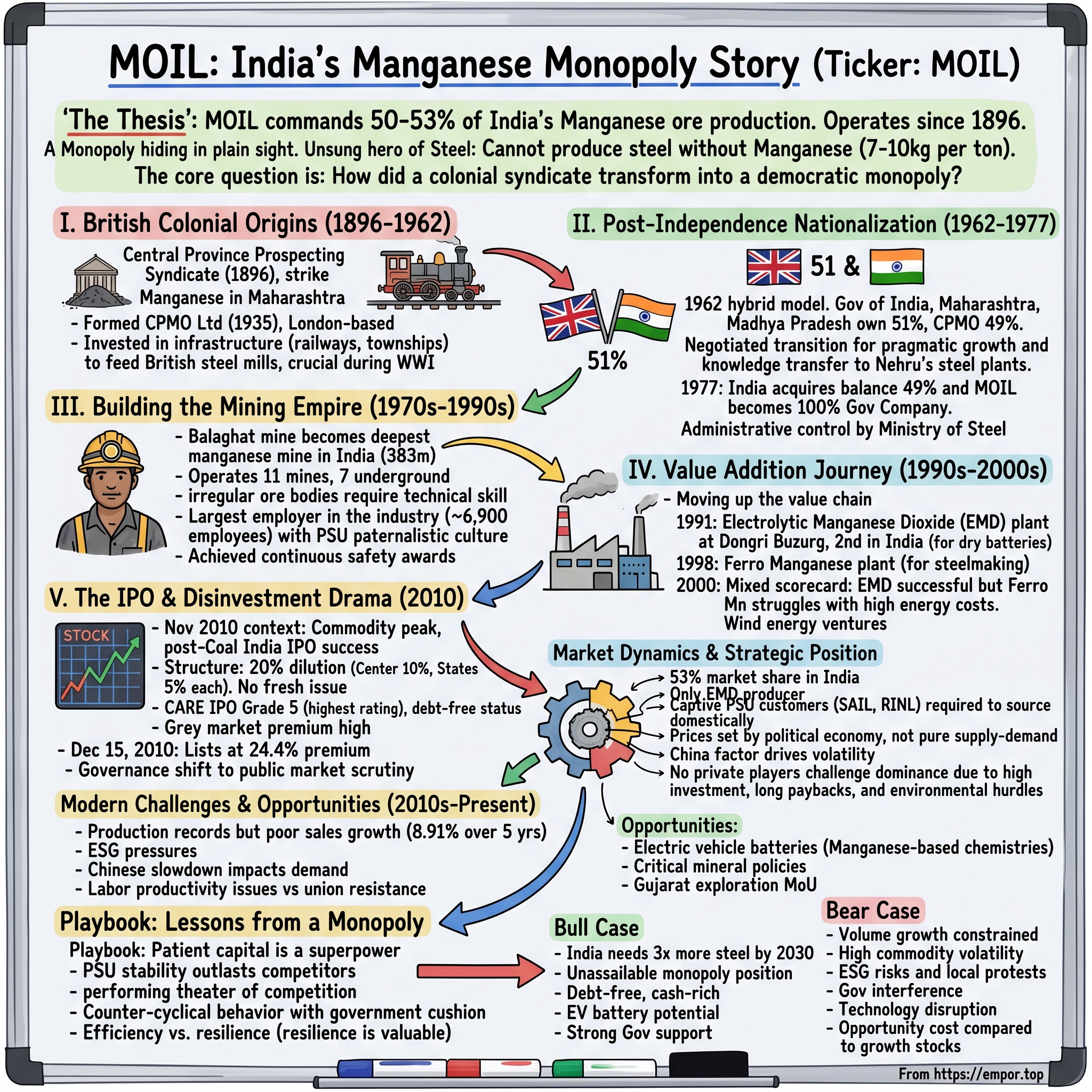

MOIL Limited commands 50-53% of India's manganese ore production, operating from the same mines that British colonizers first exploited in 1896. It's a monopoly hiding in plain sight—a ₹6,600 crore company that most investors overlook, yet one that holds strategic importance for India's entire steel industry. Here's the extraordinary fact: you cannot produce a single ton of steel without manganese. It's the unsung hero that removes impurities and adds strength, consuming about 7-10 kg for every ton of steel produced.

The central question we're exploring today is fascinating: How did a Victorian-era British mining syndicate, formed to extract colonial wealth, transform into India's strategic manganese monopoly? And more intriguingly, why has this government-controlled entity maintained its dominance for over six decades in democratic, liberalized India?

This is a story of geological accidents, colonial exploitation, socialist nationalism, and the peculiar economics of mining. It's about how certain businesses—unglamorous, capital-intensive, politically sensitive—become natural monopolies that private capital won't touch. We'll journey from the prospecting tents of 1896 Maharashtra to the trading screens of the NSE, uncovering how MOIL became the unlikely kingmaker of Indian steel.

What you'll discover is that MOIL isn't just a mining company—it's a lens through which to understand India's industrial strategy, the complexities of resource nationalism, and why some monopolies persist not despite government ownership, but because of it.

II. The British Colonial Origins (1896-1962)

The year was 1896. While Marconi was sending his first wireless signals and Henry Ford was tinkering with his Quadricycle, a group of British prospectors trudged through the dense forests of Central India's Nagpur region. They weren't searching for gold or diamonds—they were after manganese, the industrial age's secret weapon. What they found would become one of India's most enduring mining operations.

The Central Province Prospecting Syndicate, as they called themselves, struck manganese in the hills of what is now Maharashtra. The timing was perfect. The British Empire's steel mills were hungry for manganese, and here was a virgin deposit in the heart of their crown colony. By 1908, they had formalized operations, and by 1935, renamed themselves the Central Provinces Manganese Ore Company Limited (CPMO)—a London-registered entity with its soul firmly planted in Indian soil.CPMO wasn't your typical colonial extraction operation. While other British companies strip-mined India's resources for quick profits, CPMO invested in infrastructure that would last centuries. The syndicate commenced work on the previously known Mansar deposit in 1899, expanding through Balaghat, Chikhla, and Bhandara districts. They built narrow-gauge railways to connect mines to mainline tracks, established worker colonies, and developed extraction techniques suited to India's unique geology.

The colonial resource extraction model was brutally efficient. Indian labor, British capital, global markets. Manganese ore would travel from the depths of Maharashtra to the furnaces of Birmingham and Sheffield, transforming into the steel that built the Empire's railways, ships, and weapons. During World War I, CPMO's manganese became strategic—essential for armor plating and munitions. The company's profits soared while Indian miners worked in conditions that would horrify modern safety inspectors.

What made manganese so valuable to the British? Unlike iron ore, which India had in abundance, manganese deposits were geologically scarce and concentrated. The British recognized that controlling manganese meant controlling steel quality. Every blast furnace needed it to produce strong, workable steel. It was the difference between brittle iron that shattered under stress and steel that could support bridges and battleships.

MOIL operates 11 mines in Nagpur and Bhandara districts of Maharashtra and Balaghat district of Madhya Pradesh, all of which are about a century old. These aren't just holes in the ground—they're engineering marvels from the Edwardian era, still productive after 125 years. The Balaghat mine, in particular, would become CPMO's crown jewel, though its full potential wouldn't be realized until decades later.

The geopolitics were fascinating. Manganese was one of the few strategic minerals where India had a global advantage. While the British controlled the mines, they couldn't simply relocate them to England. This created an unusual dynamic—the colonizers needed to maintain and develop Indian operations rather than just extract and abandon. CPMO became deeply embedded in local economies, employing thousands and creating entire townships around their mines.

By the 1940s, as independence movements gained momentum, CPMO faced an existential question: What happens to a British mining company when the British leave? The answer would surprise everyone. Rather than flee or fight, CPMO would negotiate one of the most unusual corporate transitions in post-colonial history—setting the stage for MOIL's birth.

III. Post-Independence Nationalization (1962-1977)

The Ashoka Chakra had barely stopped spinning on India's new flag when Jawaharlal Nehru faced a dilemma that would define the nation's industrial future. It was 1962, fifteen years after independence, and a British company still controlled India's manganese—the very mineral essential for building the steel plants at the heart of Nehru's industrial vision. The solution would be neither purely capitalist nor completely socialist, but something uniquely Indian.

In 1962, the Government of India reached an agreement with CPMO where the assets were taken over and MOIL was formed with 51% capital held between the Government of India and the State Governments of Maharashtra and Madhya Pradesh, while CPMO retained 49%. This wasn't a hostile takeover or revolutionary seizure—it was a negotiated transition that reflected the pragmatism of early post-independence India.

Think about the elegance of this structure. The government gained control without full payment, CPMO retained significant value without operational burden, and both parties avoided the messy litigation that plagued other nationalizations. Nehru's advisors had learned from the chaos of sudden nationalizations elsewhere. This hybrid model—majority government, minority foreign—was revolutionary for its time.

Why was manganese considered strategic enough to nationalize? The answer lay in Nehru's temples of modern India—the steel plants. Bhilai, Rourkela, Durgapur, Bokaro—each of these massive public sector steel plants needed manganese. Without it, India's industrial revolution would stall. The mathematics were simple: every ton of steel needed 7-10 kg of manganese, and India planned to produce millions of tons. Importing manganese meant spending precious foreign exchange and depending on potentially hostile nations. The hybrid ownership structure from 1962 to 1977 created fascinating dynamics. CPMO executives still sat on boards, British engineers continued advising operations, but Indian bureaucrats controlled strategic decisions. It was corporate schizophrenia—quarterly earnings calls in London, five-year plans in New Delhi. Yet somehow, it worked. Production increased, new shafts were sunk, and technology transfer accelerated.

The fifteen-year transition period wasn't just about changing ownership—it was about knowledge transfer. Indian engineers learned from their British counterparts, absorbing decades of mining expertise. The government wisely retained experienced managers regardless of nationality, prioritizing operational continuity over political optics. This pragmatism would pay dividends when full nationalization finally came.

In 1977, the balance 49% shareholding was acquired from CPMO and MOIL became a 100% Government Company under the administrative control of the Ministry of Steel. The timing wasn't coincidental. Indira Gandhi's Emergency had just ended, and the new Janata government wanted to demonstrate economic sovereignty. Acquiring CPMO's remaining stake sent a message: India's strategic resources would be fully Indian-controlled.

The price paid for the remaining 49% remains shrouded in bureaucratic archives, but industry veterans suggest it was a bargain. CPMO, facing political headwinds in post-colonial India and limited growth prospects, was ready to exit. The Indian government, flush with confidence from successful public sector expansions, was eager to consolidate control. Both sides got what they wanted.

Under the Ministry of Steel's administrative control, MOIL's mandate expanded beyond mere mining. It became an instrument of industrial policy, tasked with ensuring domestic steel plants never lacked manganese. Pricing decisions balanced multiple objectives: covering costs, generating surpluses for expansion, yet keeping steel production competitive. This wasn't capitalism or socialism—it was the mixed economy at its most complex.

The complete nationalization marked MOIL's transformation from a colonial vestige to a pillar of India's industrial infrastructure. But with government ownership came government culture—the next chapter would test whether a public sector undertaking could maintain mining efficiency while navigating political pressures and bureaucratic procedures.

IV. Building the Mining Empire (1970s-1990s)

Dawn breaks over Balaghat, and the morning shift descends into India's deepest manganese mine. They're going down 383 meters—deeper than most Mumbai skyscrapers are tall—into a labyrinth of tunnels that stretches for kilometers underground. The cage drops through geological time, past rock formations that predate the dinosaurs, toward ore deposits that formed when the Earth was young. This is MOIL's crown jewel, and by the 1980s, it had become one of Asia's most sophisticated underground mining operations.

MOIL operates 11 mines, seven located in the Nagpur and Bhandara districts of Maharashtra and four in the Balaghat district of Madhya Pradesh. All these mines are about a century old. Except 4, rest of the mines are worked through underground method. Each mine had its personality, its challenges, its legends. Balaghat was the deep giant, pushing the limits of underground mining technology. Dongri Buzurg was the open-cast maverick, producing specialized manganese dioxide for batteries. Kandri, Munsar, Beldongri—each name represented a community, an ecosystem of miners, engineers, and families who had worked these deposits for generations.

The technical challenges of deep mining in India were immense. Unlike coal, which often lies in predictable seams, manganese ore bodies are irregular, following ancient geological faults and folds. Miners couldn't just blast and haul; they needed to follow the ore wherever it led, sometimes leaving pillars of rock to support the earth above, sometimes chasing veins that suddenly disappeared into barren rock. The in-situ reserves of manganese ore in MOIL's leasehold areas stand at around 62.69 million tonnes. To put this in perspective, at current production rates, MOIL has enough reserves to mine for another 35-40 years. But reserves aren't just about quantity—they're about accessibility, grade, and economics. Some ore bodies sit beneath villages, others under water tables, many interlaced with barren rock that makes extraction costly.

Labor relations in the PSU culture created a unique dynamic. MOIL is the largest employer in the manganese mining industry with about 6,900 employees—a workforce that included everyone from mining engineers with IIT degrees to third-generation miners who knew the underground tunnels better than their own homes. The PSU model meant lifetime employment, company housing, schools for miners' children, hospitals at every mine site. It was paternalistic capitalism, Indian-style.

The 1980s brought mechanization challenges. While Western mines deployed massive machines, MOIL's narrow ore bodies and century-old infrastructure limited options. Engineers had to innovate—developing smaller equipment that could navigate tight spaces, reinforcing old shafts to handle modern loads, balancing productivity improvements with employment guarantees. It was engineering jugaad at industrial scale.

Safety became an obsession, especially after several accidents in the 1970s. MOIL started winning National Safety Awards continuously from 1982, transforming from colonial-era practices to modern standards. Miners were trained in rescue operations, ventilation systems were upgraded, and underground communication networks installed. The company that once sent men down with candles now operated with international safety protocols.

By the 1990s, MOIL had mastered the art of underground manganese mining. The Balaghat mine alone was producing more manganese than entire countries. But success brought complacency. While MOIL perfected traditional mining, the world was changing. Steel production was shifting to electric arc furnaces, battery technology was evolving, and global commodity markets were integrating. The comfortable monopoly was about to face uncomfortable questions about its future.

V. The Value Addition Journey (1990s-2000s)

The problem with selling rocks is that everyone else is also selling rocks. This fundamental truth hit MOIL's boardroom in the early 1990s as liberalization opened India's doors to global competition. The company that had enjoyed decades of captive customers suddenly faced a stark reality: commodity producers who don't move up the value chain eventually become price-takers in someone else's game. What followed was MOIL's ambitious, sometimes quixotic, attempt to transform from a mining company into an integrated materials producer.

The first step was bold: an Electrolytic Manganese Dioxide (EMD) plant installed at Dongri Buzurg mine with an initial capacity of 800 tonnes per year. EMD is used in the manufacture of dry batteries, and MOIL's plant was only the second of its kind in India, based solely on indigenous technology. After overcoming initial hurdles, the plant made a turnaround in 1995-96, with capacity expanded to 1,000 TPY. Think about the audacity—a government mining company deciding to compete in specialty chemicals. It was like a coal miner deciding to manufacture diamonds.

The EMD plant represented more than diversification; it was a bet on India's consumer electronics boom. Every transistor radio, every flashlight, every remote control needed batteries, and batteries needed EMD. MOIL wasn't just mining manganese anymore—it was powering India's electronic revolution. The technology was indigenous, developed through collaboration with Indian research institutes, proving that PSUs could innovate when pushed.

In 1998, MOIL commissioned a ferro manganese plant with 10,000 MT capacity (later expanded to 12,000 MT), entering the ferroalloy business that private players had dominated. Ferro manganese is manganese's most valuable form for steelmaking—concentrated, refined, ready to add directly to furnaces. The economics seemed compelling: instead of selling ore at ₹5,000 per ton, sell ferro manganese at ₹50,000. Simple multiplication suggested ten-fold value addition.

But reality proved messier. Ferro manganese production is energy-intensive, requiring massive amounts of electricity to run furnaces at 1,500°C. MOIL's plants, located in Maharashtra and Madhya Pradesh, faced chronic power shortages and high electricity costs. Private competitors in mineral-rich Odisha and Jharkhand, with captive power plants and better logistics, could produce cheaper despite buying MOIL's ore. The value addition that looked profitable on paper struggled against operational realities.

The wind energy ventures—4.8 MW at Nagda Hills and 15.2 MW at Ratedi Hills—seemed incongruous for a mining company. But they made strategic sense. Mining operations need reliable power, the government offered incentives for renewable energy, and MOIL had vast land holdings perfect for wind farms. It was diversification through the back door, using mining infrastructure for energy generation.

Yet the wind farms also revealed MOIL's limitations. While private companies were building 100 MW wind installations, MOIL's 20 MW total capacity felt token. The company had the land, the capital, even the government backing, but lacked the entrepreneurial urgency to scale. It was innovation by committee, bold enough to start but too cautious to dominate.

The mixed results of diversification taught hard lessons. EMD succeeded because MOIL controlled the raw material and faced limited competition. Ferro manganese struggled because energy costs and logistics mattered more than ore access. Wind energy remained subscale because it wasn't core to the mining mindset. The pattern was clear: MOIL could innovate within its ecosystem but struggled to compete in open markets. By 2000, the diversification scorecard was mixed. The Ferro Manganese Plant commissioned in 1998 with 10,000 TPA capacity (later expanded to 12,000 TPA) produced high-quality product—78% Mn, 0.35% Phosphorus, 6-8% Carbon—earning ISO 9001-2000 certification. But profitability remained elusive due to power costs. The EMD plant had stabilized at 1,500 MT annual capacity, becoming India's only producer and fulfilling 50% of domestic dioxide ore requirements.

The challenge wasn't technical competence—MOIL could build and operate complex plants. The challenge was competitive dynamics in markets where being a PSU was a disadvantage, not an advantage. Private competitors could make faster decisions, take bigger risks, and optimize ruthlessly for profits. MOIL had to balance multiple stakeholders, follow tender procedures for every purchase, and couldn't easily shed excess workers.

Looking back, the value addition journey revealed a fundamental truth about industrial strategy: moving up the value chain requires more than technical capability and capital. It requires market timing, operational excellence, and sometimes, a willingness to fail fast and pivot—qualities that PSUs, by their nature, struggle to cultivate. MOIL's diversification wasn't a failure, but it wasn't the transformation the company had hoped for either. The next decade would bring a different kind of transformation—from a government department to a listed company facing public market scrutiny.

VI. The IPO and Disinvestment Drama (2010)

The year 2010 marked a watershed in India's disinvestment history. Coal India's blockbuster IPO had just raised ₹15,200 crores, proving that retail investors would queue up for PSU offerings. In the corridors of North Block, bureaucrats were drawing up lists of the next candidates. MOIL's name was circled in red—profitable, debt-free, strategic yet sellable. What followed was a masterclass in financial engineering and political theater that would transform a sleepy mining PSU into a stock market darling.

The context was electric. The UPA government, facing fiscal pressure and ideological shifts, had embraced disinvestment as policy virtue rather than necessary evil. Finance Minister Pranab Mukherjee needed resources for ambitious social programs. The global commodity supercycle was peaking—iron ore prices had tripled, steel demand was soaring, and anything mining-related attracted investor frenzy. MOIL, with its monopoly position and hundred-year operating history, seemed like the perfect candidate. The IPO details were meticulously crafted. Price band: ₹340-375 per share. Timing: November 26 to December 1, 2010. Size: 3.36 crore shares, raising ₹1,237.51 crores. The structure was elegant—20% dilution with the central government selling 10%, Maharashtra and Madhya Pradesh each selling 5%. No fresh issue, pure offer for sale. The government would cash out while retaining control.

CARE assigned an IPO Grade 5 to MOIL—the highest rating, indicating "strong fundamentals." Only Coal India had received similar grading that year. This wasn't just certification; it was validation that a PSU could match private sector quality. The grading report highlighted MOIL's debt-free status, consistent profitability, strategic market position, and substantial reserves.

The pricing strategy was brilliant. At ₹375 upper band, MOIL traded at just 9.5 times earnings—a fraction of Coal India's 24 times or NMDC's 17 times. The government had learned from previous IPO failures. Price it cheap, create a frenzy, ensure listing gains, and build long-term retail loyalty. Retail investors got a 5% discount, making the effective price ₹356.25. It was designed to be irresistible.

The grey market told the real story. Premium soared to ₹225-250 per share even before the IPO opened. Applications worth ₹2 lakh were trading at ₹5,500-6,000—investors were paying premiums just for the right to apply. Brokers reported unprecedented demand. HNIs borrowed at 15% monthly interest to maximize applications. The commodity supercycle narrative had captured imaginations.

On December 15, 2010, MOIL listed at ₹466.50—a 24.4% premium to the issue price. Within minutes, it touched ₹530, giving retail investors who got allotment returns of over 40%. The financial media celebrated another PSU IPO success. The government had raised over ₹1,200 crores without losing control. Retail investors made quick profits. Investment bankers earned hefty fees. Everyone won—or so it seemed.

But listing day euphoria masked deeper questions. MOIL was now a listed company with quarterly earnings pressure, analyst scrutiny, and shareholder activism. Could a PSU culture adapt to market capitalism? The government retained 53.35% directly, with Maharashtra and Madhya Pradesh holding another 11.34%—enough for control but not enough to ignore minority shareholders. After the listing, the shareholding in the company stood at Government of India (71.57%), Government of Maharashtra (4.62%), Government of Madhya Pradesh (3.81%), and Public (20%). The governments retained absolute control with 80% combined stake, but now had 35,000 new shareholders watching every move. Quarterly earnings calls replaced annual parliamentary questions. Stock price movements mattered more than ministerial memos.

The IPO's success had unintended consequences. MOIL's stock price became a barometer of PSU health, its dividend policy a political flashpoint, its capital allocation decisions scrutinized by fund managers who'd never seen a manganese mine. The company that had operated in comfortable obscurity for decades was suddenly in the spotlight, expected to balance public service with shareholder returns.

In retrospect, the 2010 IPO marked MOIL's transition from a government department to a quasi-corporate entity. It retained the benefits of state backing—assured customers, political support, regulatory favor—while gaining access to capital markets and the discipline they impose. Whether this hybrid model would create long-term value remained an open question, one that the next decade would begin to answer.

VII. Market Dynamics & Strategic Position

In the corporate headquarters of every Indian steel company, there's a number that procurement chiefs track obsessively: MOIL's monthly price circular. With 53% market share in India and position as the only producer of Electrolytic Manganese Dioxide, MOIL doesn't just participate in the manganese market—it is the market. This pricing power, combined with India's structural manganese deficit, creates a moat that Warren Buffett would admire, if only he understood commodity markets in emerging economies.

MOIL fulfills about 48% of India's total dioxide ore requirement, a seemingly modest number until you realize the remaining 52% comes from imports at volatile international prices. When global manganese prices spike, as they did during the 2021-2022 commodity boom, Indian steel producers have two choices: pay MOIL's prices or pay even higher prices to Australian and South African miners, plus shipping costs, plus import duties. It's a beautiful position for a monopolist.

The steel industry connection runs deeper than simple supplier relationships. Steel Authority of India (SAIL), Rashtriya Ispat Nigam Limited (RINL), and other PSU steel plants are essentially captive customers. They're required by informal government directive to source domestically when possible—a "Make in India" policy before Make in India became fashionable. Private steel producers like JSW and Tata Steel also buy from MOIL, not from loyalty but from logistics. Transporting manganese from Nagpur to Jamshedpur is simpler than shipping from Port Elizabeth.

Yet the import substitution story reveals MOIL's constraints. Despite monopoly position, the company can't fully exploit pricing power. Raise prices too high, and the Steel Ministry receives angry calls from steel producers. The government, wearing two hats as MOIL's majority owner and steel industry promoter, inevitably sides with the larger economic interest. MOIL's pricing isn't set by supply-demand but by political economy—high enough to ensure profitability, low enough to keep steel competitive.

The competition landscape is peculiar. No private player has seriously challenged MOIL's dominance despite liberalized mining policies. The reasons are instructive. First, manganese mining requires massive upfront investment with 10-15 year payback periods—too long for private capital seeking quick returns. Second, ore bodies are geologically concentrated in areas where MOIL already holds leases. Third, environmental clearances for new mines take years, sometimes decades. Fourth, and most importantly, competing against a government-backed incumbent in a strategic sector is a fool's errand in India. The China factor looms large in global manganese markets. China consumes over 60% of global manganese production for its massive steel industry, creating price volatility that ripples through to India. When China sneezes, MOIL catches a cold. Yet paradoxically, this volatility strengthens MOIL's domestic position. Indian steel producers prefer paying stable prices to MOIL rather than facing international market swings.

Customer concentration tells an interesting story. While MOIL supplies dozens of customers, the top five account for over 60% of sales—mostly PSU steel plants. This concentration seems risky until you realize these customers have nowhere else to go. They can't import easily due to logistics, can't develop new mines due to regulations, and can't pressure MOIL too hard due to government relationships. It's mutual dependence disguised as customer concentration.

The pricing power equation is fascinating: MOIL can raise prices when global prices rise (passing through increases) but faces pressure to maintain prices when global prices fall (social obligation). This asymmetric pricing creates a ratchet effect—margins expand during booms but don't fully contract during busts. Over cycles, this leads to margin expansion, explaining why MOIL's EBITDA margins have crept up from 30% to 40% over the decades.

Technology disruption seems distant but bears watching. Direct reduced iron (DRI) processes use less manganese than blast furnaces. Electric arc furnaces, increasingly popular globally, have different manganese requirements. Battery chemistry evolution could increase manganese demand (lithium-manganese batteries) or decrease it (solid-state batteries). MOIL's monopoly is secure for now, but technological shifts could erode its strategic importance over decades.

The real competitive threat isn't from new miners but from changing steel economics. If Indian steel becomes globally uncompetitive, manganese demand drops regardless of MOIL's market share. The company's fate is tied to Indian steel's fate, which is tied to infrastructure spending, which is tied to economic growth. It's a derivative play on India's development story, with monopoly characteristics providing downside protection but not immunity.

VIII. Modern Challenges & Opportunities (2010s-Present)

The conference room at MOIL's Nagpur headquarters has witnessed a decade of soul-searching since the IPO. Quarterly earnings calls replaced annual plan meetings, analyst questions supplanted parliamentary queries, and market expectations collided with mining realities. The company that once measured success in tonnes now tracks stock price movements by the minute. This cultural whiplash—from socialist enterprise to market-facing corporation—defines MOIL's modern era. Current production stands at approximately 1.8 million tonnes annually, with market cap of ₹6,617 crores, revenue of ₹1,440 crores, and profit of ₹281 crores. The company has delivered poor sales growth of 8.91% over five years, with ROE of 12.8%—numbers that would doom a private company but are acceptable for a strategic PSU. It's almost debt-free with healthy dividend payout of 34%, reflecting the classic PSU model: steady operations, conservative growth, regular dividends.

The challenges read like a mining company's nightmare checklist. Environmental clearances take years for new exploration. The Ministry of Environment treats mining like nuclear warfare, demanding impact assessments that cost crores and deliver little. Labor productivity remains stuck in the 1990s—MOIL employs 6,900 people to produce what Australian mines achieve with 500. Mechanization attempts face union resistance, with every efficiency improvement negotiated like international treaties.

ESG pressures are intensifying. International steel buyers increasingly demand supply chain transparency, carbon footprint disclosure, and sustainable mining practices. MOIL has planted 12 lakh trees (survival rate: 80%), implemented zero-discharge water systems, and won environmental awards. But these feel like checkbox exercises rather than fundamental transformation. The company that strips mountains for metal struggles to convince stakeholders it's environmentally conscious.

The China factor looms larger than ever. Chinese steel production drives global manganese demand, and any slowdown immediately impacts prices. The 2021-2022 commodity supercycle pushed manganese prices to record highs, but the subsequent correction reminded everyone that commodity booms don't last forever. MOIL's earnings volatility—profit swinging from ₹200 crores to ₹400 crores based on global prices—makes long-term planning nearly impossible.

Technology upgrades offer both promise and peril. MOIL has introduced side discharge loaders, load-haul-dump machines, and electro-hydrostatic drill jumbos. The Balaghat mine now reaches 435 meters depth, pushing engineering limits. But each modernization reduces employment needs, creating political pressure in regions where MOIL is often the largest employer. The company must balance operational efficiency with social responsibility—a tightrope walk that private miners don't face. Exploration activities offer both hope and frustration. MOIL has recorded its second-highest production since inception, with 13.02 lakh tonnes in FY 2022-23 and an all-time high of 17.56 lakh tonnes in 2023-24, showing 35% growth. The company continues exploratory drilling, reaching 13,352 meters, reflecting strategic push in expanding resource potential. In 2022, MOIL signed an MoU with Gujarat Mineral Development Corporation to explore manganese ore in Gujarat—the first significant expansion beyond traditional territories in decades.

But exploration in India is a Kafkaesque nightmare. Environmental clearances require impact assessments that take years and cost crores. Local communities protest any new mining activity, regardless of economic benefits. State governments demand revenue shares before exploration begins. The result: MOIL's reserves haven't materially increased despite decades of exploration spending. The ore bodies discovered in the British era remain the primary source of production.

The opportunity landscape is evolving rapidly. Electric vehicle batteries increasingly use manganese-based chemistries. Lithium-manganese oxide and nickel-manganese-cobalt batteries could dramatically increase manganese demand. Steel production methods are evolving, with hydrogen-based direct reduction potentially changing manganese requirements. MOIL has positioned itself to benefit, but execution remains the challenge.

Recent performance shows improvement. Production records are being broken regularly—highest-ever May production of 1.71 lakh tonnes (18% YoY growth), record April production of 1.62 lakh tonnes. Sales of ferro manganese hit record 12,942 MT (54% YoY growth). These operational improvements suggest MOIL is finally modernizing effectively, though whether this translates to sustainable competitive advantage remains uncertain.

The government's strategic minerals push offers tailwinds. India's vulnerability to Chinese control of critical minerals has sparked policy action. MOIL, as the domestic manganese champion, benefits from import substitution drives, production-linked incentives, and preferential procurement policies. The company that seemed like a relic of socialist planning suddenly looks prescient in an era of resource nationalism.

Yet fundamental questions persist. Can a PSU culture truly embrace the entrepreneurial risk-taking needed for growth? Will political pressures always trump commercial considerations? Can MOIL expand beyond its traditional territories given India's federal complexities? The next decade will determine whether MOIL transforms from a colonial-era mining company into a modern materials champion, or remains a steady but sleepy custodian of India's manganese reserves.

IX. Playbook: Lessons from a Government Monopoly

If you wanted to design a business school case study on how to operate a strategic resource monopoly, MOIL would be your template. Not because it's perfect—far from it—but because it demonstrates the unique dynamics of running a government-controlled monopoly in a democracy. The playbook that emerges isn't about maximizing profits or crushing competitors; it's about balancing contradictory objectives while maintaining operational continuity across political cycles.

Lesson 1: Patient Capital is a Superpower (When Used Wisely) MOIL can think in decades while private miners think in quarters. The Balaghat mine took 30 years to reach current depths—no private company would have that patience. The EMD plant lost money for years before turning profitable. Wind farms were built not for ROI but for energy security. This patient capital allows counter-cyclical investing: expanding when commodity prices crash and others retreat. But patience can become complacency. MOIL's growth has been glacial compared to global mining giants. The company mistakes stability for strategy.

Lesson 2: The PSU Disadvantage is Also an Advantage Every government tender must follow elaborate procedures. Every hire requires committee approval. Every capital allocation faces political scrutiny. This seems like a competitive disadvantage until you realize it creates predictability. Suppliers know MOIL will pay (eventually). Workers know jobs are secure. Customers know supplies won't suddenly stop. In commodity markets where boom-bust cycles destroy companies, MOIL's bureaucratic stability becomes a strength. Private competitors can move faster, but MOIL outlasts them all.

Lesson 3: Monopolies Must Perform Theater MOIL carefully orchestrates the appearance of competition while maintaining dominance. It allows imports to continue (showing openness) while ensuring domestic preference policies favor local procurement. It keeps prices just high enough to earn profits but low enough to avoid attracting competitors or regulatory scrutiny. It invests in CSR and environmental projects not from conviction but as political insurance. This theatrical performance—monopolist playing the role of market participant—is essential for legitimacy.

Lesson 4: Capital Allocation in a Goldfish Bowl Every dividend becomes political. Pay too much, and you're accused of starving growth. Pay too little, and the government (as majority owner) demands cash for fiscal needs. MOIL has mastered the art of goldfish bowl capital allocation: maintaining 30-40% dividend payout (enough to satisfy but not excite), keeping debt near zero (avoiding interest burden debates), and investing just enough in growth projects to show ambition without risking failure. It's financial engineering as political art.

Lesson 5: Managing Cyclicality with a Government Cushion When manganese prices crash, private miners cut production, fire workers, and sometimes go bankrupt. MOIL continues operating, absorbing losses as "social responsibility." When prices boom, MOIL doesn't maximize profits but "stabilizes markets." This counter-cyclical behavior, impossible for private companies answering to shareholders, actually creates value over full cycles. The government cushion isn't just protection—it's a strategic tool for capturing market share during downturns.

Lesson 6: The Disinvestment Tightrope The 2010 IPO created a perpetual tension: minority shareholders want profit maximization while the government wants multiple objectives. MOIL walks this tightrope by segmenting stakeholders. Retail investors get steady dividends and occasional bonuses. Institutional investors get a defensive commodity play. The government gets a cash cow that also serves strategic purposes. Nobody is thrilled, but everyone is satisfied enough to maintain the status quo.

Lesson 7: Why This Model is Hard to Replicate You need several ingredients: a strategic resource with limited deposits, historical operations creating entry barriers, government willingness to accept below-market returns for strategic control, and a federal structure where multiple governments have stakes (preventing any single actor from disrupting the system). Remove any ingredient, and the model collapses. This is why India has only a handful of successful PSU monopolies despite hundreds of attempts.

The Meta-Lesson: Efficiency vs. Resilience Private markets optimize for efficiency: maximum output for minimum input. MOIL optimizes for resilience: consistent output regardless of external shocks. In normal times, efficiency wins. But in a world of supply chain disruptions, geopolitical tensions, and resource nationalism, resilience becomes valuable. MOIL's inefficiencies—excess workers, conservative growth, bureaucratic processes—are also its shock absorbers.

The playbook ultimately reveals a paradox: MOIL succeeds not by competing in the market but by operating outside normal market logic. It's a 19th-century solution to a 21st-century problem—using government ownership to ensure strategic resource security. For investors, the lesson is clear: don't evaluate MOIL like a mining company. Evaluate it like a utility—steady, boring, essential, and ultimately, irreplaceable.

X. Bull vs. Bear Case

Bull Case: The Inevitability Thesis

Start with the macro picture: India needs to produce 300 million tonnes of steel annually by 2030 to support its infrastructure ambitions. Every tonne requires manganese. Do the math—that's 3 million tonnes of manganese demand annually, double current consumption. MOIL controls the only meaningful domestic supply. It's not about whether demand will grow; it's about how much MOIL can capture.

The monopoly position is unassailable. After 75 years of independence and 30 years of liberalization, no private player has successfully challenged MOIL. Why? Because manganese mining in India is a terrible business for private capital—massive upfront investment, 15-year paybacks, environmental nightmares, political complications. Only a government-backed entity can navigate these challenges. MOIL's moat isn't just wide; it's radioactive.

The balance sheet is a thing of beauty for value investors. Zero debt in a capital-intensive industry. ₹1,700+ crores in cash and investments. Consistent free cash flow generation even during commodity downturns. Trading at single-digit P/E multiples when global miners trade at 15-20x. The dividend yield of 3-4% provides income while you wait for rerating. It's Graham and Dodd's dream stock—asset-heavy, cash-rich, and ignored by growth investors.

The electric vehicle revolution could be manganese's iPhone moment. Next-generation batteries increasingly use manganese-rich cathodes. Tesla's considering lithium-manganese batteries for mass-market vehicles. If even 10% of global EV batteries shift to high-manganese chemistries, demand could increase 50%. MOIL is the only Indian company positioned to benefit, with both raw ore and value-added EMD production capabilities.

Government support isn't weakening; it's strengthening. The Production Linked Incentive schemes favor domestic sourcing. The China +1 strategy requires secure supply chains. Critical mineral policies explicitly protect domestic producers. Environmental regulations make new mining nearly impossible, protecting MOIL's existing operations. It's regulatory capture, but legal and strategic.

The hidden optionality is enormous. Those 62.69 million tonnes of reserves, valued at historical costs on the balance sheet, are worth multiples at current prices. The Gujarat exploration MoU could open entirely new territories. The company's land bank in prime Maharashtra and MP locations has real estate value exceeding market cap. It's like buying dollar bills for fifty cents, except the dollar bills are buried underground and require government permission to extract.

Bear Case: The Slow Decline Thesis

The growth mirage is obvious to anyone reading beyond headlines. Yes, production hit records, but from a low base after years of stagnation. Revenue growth of 8.91% over five years barely beats inflation. Volume growth is constrained by century-old mines reaching geological limits. The Balaghat mine at 435 meters depth faces exponentially rising extraction costs. MOIL is running harder to stay in the same place.

Commodity price volatility makes this uninvestable for serious money. Manganese prices can swing 50% in months based on Chinese steel production, Brazilian weather, or South African politics. MOIL has zero pricing power internationally and limited pricing power domestically. When global prices crash, MOIL's profits evaporate regardless of volumes. It's a price-taker in a volatile market—the worst position in commodities.

The ESG sword of Damocles hangs over every mining company, but especially over government-owned ones. International customers increasingly demand carbon-neutral supply chains. Mining is inherently destructive—no amount of tree-planting changes that. Young Indians oppose mining in principle. Every expansion faces protests, litigation, and delays. MOIL might have monopoly over existing mines, but it may never open new ones.

Government interference is a feature, not a bug. Every pricing decision gets politicized. Steel producers lobby for lower prices. Workers unions demand higher wages regardless of productivity. State governments extract royalties and taxes. Environmental ministries impose arbitrary restrictions. The company serves too many masters to serve shareholders well. You're not buying a business; you're buying a government department with a stock ticker.

The technology disruption risk is real and accelerating. Direct reduced iron uses less manganese. Aluminum alloys substitute for steel in many applications. Battery chemistry evolution is unpredictable—solid-state batteries might not need manganese at all. Carbon fiber and composites reduce metal usage in vehicles. 3D printing changes material requirements. MOIL is perfectly positioned for yesterday's technology.

The opportunity cost is crushing. While MOIL plods along with single-digit growth, Indian markets offer dozens of compounders growing at 20-30% annually. Why tie up capital in a commodity producer with government baggage when you could own technology, financial, or consumer companies with secular tailwinds? The stock has underperformed Nifty for years and will likely continue. It's not that MOIL will collapse; it's that everything else will do better.

The Verdict

Both cases are simultaneously true. MOIL is indeed an irreplaceable strategic asset with monopoly characteristics and hidden value. It's also a slow-growth, government-controlled commodity producer in a structurally challenged industry. The bull case works for deep value investors with five-year horizons who view it as a inflation hedge with optionality. The bear case works for growth investors who see opportunity costs and structural headwinds.

The real question isn't whether MOIL is good or bad, but whether it fits your investment philosophy. If you believe in mean reversion, asset values, and strategic positioning, MOIL offers asymmetric upside. If you believe in growth, efficiency, and market dynamics, MOIL offers symmetric disappointment. Like manganese itself—essential but unglamorous—MOIL will never be a market darling, but it might be a portfolio stabilizer.

XI. Epilogue: The Future of Strategic Resources

As we close this deep dive into MOIL's century-long journey, we're left contemplating bigger questions about resources, sovereignty, and the changing nature of strategic advantage. MOIL isn't just a mining company or a stock ticker—it's a window into how nations think about critical resources in an increasingly fragmented world.

The new geopolitics of resource nationalism is reshaping global trade. What started as Trump's trade war and accelerated during COVID has become the new normal: countries hoarding critical minerals like medieval kingdoms hoarding gold. China restricts rare earth exports. Indonesia bans nickel ore shipments. Chile nationalizes lithium. In this environment, MOIL's boring monopoly suddenly looks prescient. India secured its manganese supply chain decades before supply chain security became fashionable.

The lesson extends beyond manganese. Every country is now mapping its critical mineral dependencies and finding uncomfortable truths. The green transition requires massive amounts of copper, lithium, cobalt, and yes, manganese. The same countries preaching environmental sustainability are realizing they need to dig huge holes in the ground. The cognitive dissonance is spectacular, and MOIL has been living this contradiction for decades.

What MOIL tells us about India's industrial strategy is both reassuring and concerning. Reassuring because it shows long-term thinking about strategic resources. Concerning because it reveals the limitations of state-led development. MOIL succeeded in securing manganese supply but failed to create a globally competitive mining industry. It's the classic Indian compromise: good enough to function, not good enough to excel.

For investors, MOIL offers a masterclass in analyzing government-controlled resources. Don't focus on quarterly earnings or management guidance. Focus on replacement cost, strategic value, and political economy. The stock price might stagnate for years, then double overnight on a government policy change. It's not investing; it's applied political science with a financial wrapper.

The deeper lesson is about monopolies in democratic societies. Unlike private monopolies that extract maximum value, or state monopolies in autocracies that serve political ends, MOIL represents a third way: a democratic monopoly that balances multiple stakeholders while maintaining operational continuity. It's inefficient by design, profitable by accident, and sustainable by necessity.

Looking ahead, MOIL faces an existential question: Can a 20th-century institution adapt to 21st-century realities? The company born in the British Raj, nationalized under Nehruvian socialism, and listed during India's liberalization must now navigate digital disruption, climate change, and geopolitical realignment. The answer will determine not just MOIL's future but offer lessons for resource security globally.

The final irony is perfect: In an age of artificial intelligence, quantum computing, and space exploration, economic power still depends on who controls holes in the ground. MOIL's manganese mines, dug by British colonizers and worked by generations of Indian miners, remain as strategic today as they were a century ago. Technology changes everything except geology.

For the patient investor, MOIL offers a bet on permanence in an impermanent world. Wars will be fought, governments will fall, technologies will disrupt, but steel will still need manganese, and India will still need steel. It's not a growth story or a value play—it's a survival story. And in a world where most companies won't exist in 50 years, betting on survival might be the smartest investment of all.

The story of MOIL is ultimately the story of modern India—colonial exploitation transformed into national asset, socialist experiment evolved into market participant, strategic resource balanced against commercial pressures. It's messy, complicated, and occasionally brilliant. Just like India itself.

As Ben and David would say at the end of an Acquired episode: MOIL isn't trying to be the best mining company in the world. It's trying to be the only manganese company India needs. And for 128 years and counting, it's succeeded in that modest but essential mission. In the grand casino of capitalism, sometimes the house doesn't win by having the best odds—it wins by being the only game in town.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube