Indian Oil Corporation: The Architect of India's Energy Independence

I. Introduction & Episode Setup

The paradox sits at the heart of modern India's energy story: a government-owned oil behemoth, born from socialist ideals and anti-colonial fervor, that today ranks 94th on the Fortune Global 500 list. Indian Oil Corporation Limited (IOCL or IOC), trading as IndianOil, is an Indian multinational oil and gas company under the ownership of the Government of India and administrative control of the Ministry of Petroleum and Natural Gas. It is the largest government-owned oil producer in the country both in terms of capacity and revenue.

This is not merely a corporate success story—it's the chronicle of how a newly independent nation wrested control of its energy destiny from foreign monopolies and built an empire that today commands 42% market share in Petroleum Oil and Lubricants with over 60,900 touch points across the subcontinent. It owns 11 refineries across India with a total capacity of 80.80 MMTPA (including 10.5 MMTPA of subsidiaries), possessing 31% of the total refining capacity of India.

The numbers tell only part of the story. Behind them lies a seven-decade saga of nation-building, geopolitical maneuvering, and the perpetual dance between public service and commercial ambition. How does a state-owned enterprise navigate the treacherous waters of global oil markets while bearing the weight of energy security for 1.4 billion people? How does it compete with nimble private players while shouldering social mandates that would sink any purely commercial entity?

Today's journey takes us from the rain-soaked refineries of post-independence India to the electric vehicle charging stations of tomorrow, from Soviet-era collaborations to modern renewable energy ventures. This is the story of Indian Oil Corporation—architect of India's energy independence, guardian of its fuel security, and now, perhaps its most unlikely champion in the transition to clean energy.

II. The Genesis: Post-Independence Oil Politics

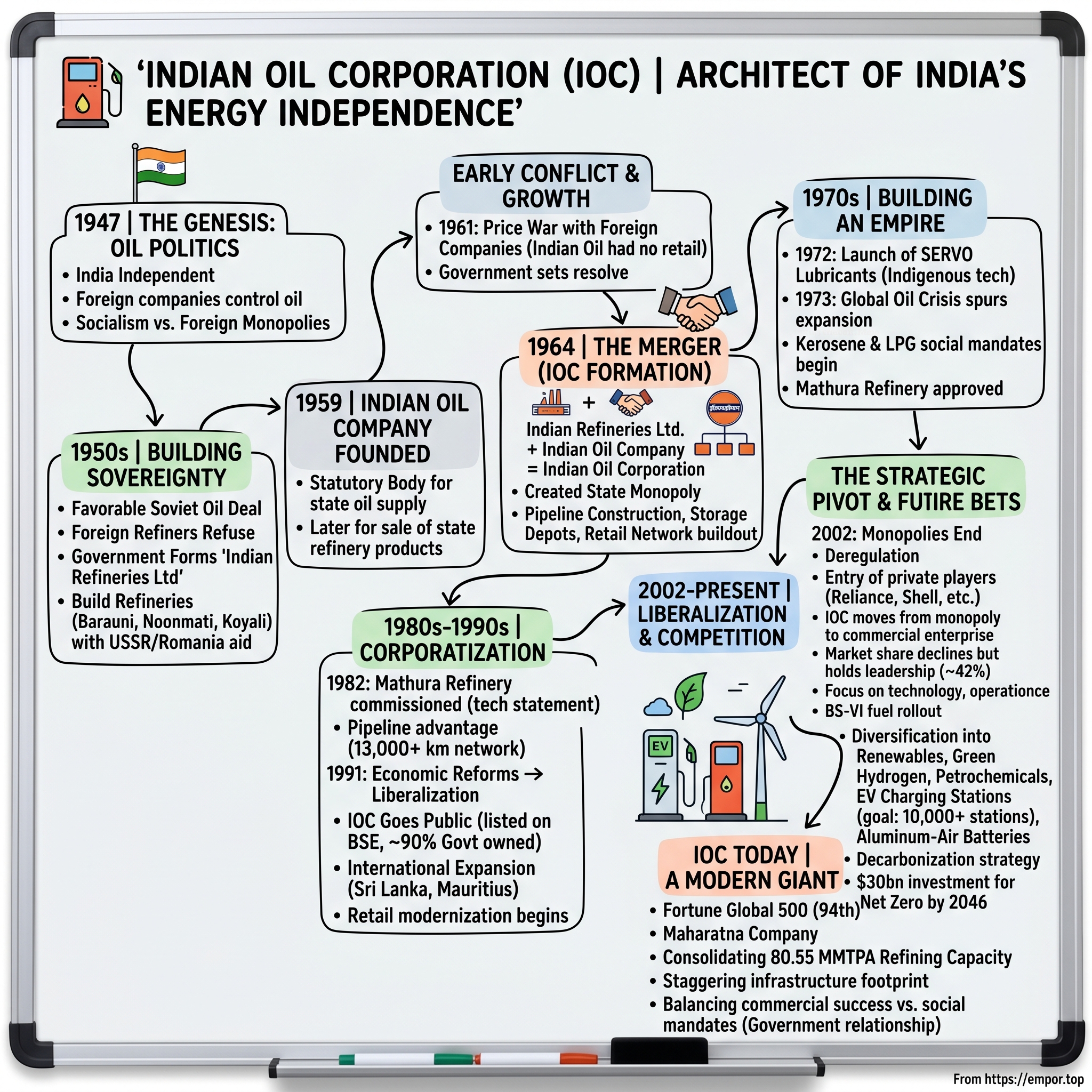

The year was 1947. As the last British administrators packed their bags and the tricolor unfurled over Red Fort, India's new leaders surveyed their inheritance: a nation of 330 million people, widespread poverty, negligible industrial infrastructure, and an oil industry almost entirely controlled by foreign powers. Exploration and production are reserved largely for two other government organizations, the Oil and Natural Gas Commission (ONGC) and Oil India Ltd. Indian Oil owes its origins to the Indian government's conflicts with foreign-owned oil companies in the period immediately following India's independence in 1947. The leaders of the newly independent state found that much of the country's oil industry was effectively in the hands of a private monopoly led by a combination of British-owned oil companies Burmah and Shell and U.S. companies like Caltex and Standard-Vacuum.

The foreign oil monopoly wasn't just an economic problem—it was an existential threat to sovereignty. These companies controlled everything from exploration to retail, setting prices at will, refusing to expand refining capacity, and showing little interest in training Indian personnel. The situation grew increasingly intolerable as India's energy needs exploded with industrialization plans.

Shortly afterward, the government accused the companies of charging excessive prices for importing oil. The companies also refused to refine Soviet oil that the government had secured on very favorable terms. The government was impatient with the companies' reluctance to expand refining capacity or train sufficient Indian personnel.

The breaking point came with India's growing relationship with the Soviet Union. Prime Minister Jawaharlal Nehru, architect of non-alignment but pragmatic about economic necessities, had negotiated favorable oil import deals with the USSR. The terms were revolutionary: oil at below-market prices, payable in Indian rupees rather than precious foreign exchange. But the foreign oil companies refused to refine this Soviet crude, forcing a confrontation that would reshape India's energy landscape.

In 1958, the government formed its own refinery company, Indian Refineries Ltd. With Soviet and Romanian assistance, the company was able to build its own refineries at Noonmati, Barauni, and Koyali. This wasn't just infrastructure development—it was a declaration of energy independence. Soviet and Romanian engineers arrived in India, bringing not just technical expertise but a different model of state-controlled energy development.

The following year marked a pivotal moment. In 1959, the Indian Oil Company was founded as a statutory body. At first, its objective was to supply oil products to Indian state enterprise. Then it was made responsible for the sale of the products of state refineries. What began as a distribution arm for government enterprises would soon become the cornerstone of India's energy architecture.

The foreign companies didn't surrender without a fight. Growing Soviet imports led the foreign companies to respond with a price war in August 1961. At this time, Indian Oil had no retail outlets and could sell only to bulk consumers. The oil companies undercut Indian Oil's prices and left it with storage problems. Picture the scene: a fledgling state enterprise with no retail network, warehouses full of petroleum products, facing price predation from established multinationals with deep pockets and extensive distribution networks.

But the government's resolve only hardened. Foreign companies were told that they would not be allowed to build any new refineries unless they agreed to a majority shareholding by the Indian government. The message was clear: India would control its energy future, with or without foreign cooperation.

This early period established patterns that would define Indian Oil for decades: the delicate balance between socialist ideals and market realities, the strategic use of geopolitical relationships to secure energy supplies, and the unwavering commitment to energy sovereignty even at significant economic cost. The stage was set for what would become one of the most ambitious state-led industrial transformations in post-colonial history.

III. The Merger & Early Years (1964–1970s)

September 1964 marked the birth of a giant. In September 1964, Indian Refineries Ltd. and the Indian Oil Company were merged to form the Indian Oil Corporation. The government announced that all future refinery partnerships would be required to sell their products through Indian Oil. This wasn't merely a corporate restructuring—it was the creation of an energy monopoly designed to break foreign dominance and secure India's industrial future.

The newly formed Indian Oil Corporation inherited a complex mandate: build refineries, lay pipelines, create distribution networks, and do it all while navigating the byzantine world of India's socialist economy. The company's first major achievement had actually preceded the merger—the commissioning of the Guwahati refinery in Assam in 1962, India's first public sector refinery, built with Soviet assistance. This 0.75 million tonne facility, modest by today's standards, represented something far greater: proof that India could build and operate its own refineries.

The monopoly structure granted to Indian Oil was both blessing and curse. On one hand, it guaranteed market share and eliminated domestic competition. Every drop of oil refined in government or joint-venture refineries had to flow through Indian Oil's distribution network. On the other, it placed enormous responsibility on a young organization still finding its feet. The company had to ensure fuel availability across a vast, diverse nation with limited infrastructure, from the Himalayan heights to the coastal plains, from bustling metros to remote villages.

The 1970s brought new challenges and opportunities. The global oil crisis of 1973, triggered by the Arab oil embargo, sent shockwaves through the Indian economy. Overnight, oil prices quadrupled, foreign exchange reserves dwindled, and the vulnerability of import dependence became starkly apparent. For Indian Oil, this crisis became a catalyst for expansion and innovation.

This policy allowed Indian Oil the market share of the output of all refineries that were partly or wholly owned by the government. The company leveraged this monopoly to rapidly expand infrastructure. Pipeline construction accelerated—steel arteries carrying crude and products across thousands of kilometers. Storage depots sprouted in district headquarters. A network of dealers and distributors emerged, creating employment and ensuring last-mile connectivity.

A landmark moment came in 1972 with the launch of SERVO, India's first indigenous lubricant brand. This wasn't just about import substitution—it was about technological capability. Indian Oil's research centers reverse-engineered and improved upon international formulations, creating products suited to Indian conditions: the extreme heat of Rajasthan's deserts, the humidity of Kerala's coasts, the dust and grime of industrial towns.

The company also pioneered what would become a defining characteristic: the integration of social objectives with commercial operations. Kerosene, essential for lighting in rural India, was distributed at subsidized rates through the Public Distribution System. Cooking gas (LPG) connections, then a urban luxury, began their slow march into middle-class homes under the Indane brand. These weren't profitable ventures—they were nation-building exercises, funded through cross-subsidization from other products.

By the mid-1970s, Indian Oil had transformed from a fledgling enterprise into the architect of India's energy security. The company controlled the commanding heights of the oil economy: refining, pipelines, marketing, and increasingly, technology development. The Mathura refinery project, approved in this period though commissioned in 1982, symbolized growing ambitions—an 8 million tonne facility that would become one of Asia's largest.

The socialist-era monopoly dynamics created unique organizational cultures and capabilities. Indian Oil engineers became masters of juggling multiple objectives: maximizing throughput while maintaining strategic reserves, ensuring urban supply while serving rural mandates, generating surpluses while absorbing subsidy burdens. The company developed what observers would later call "frugal engineering"—the ability to build and operate facilities at a fraction of international costs through innovative design and local sourcing.

This period also established Indian Oil's role as more than just an oil company. It became an instrument of state policy, a vehicle for regional development, and a symbol of national capability. Refineries were located not just based on economic logic but also political considerations—bringing development to backward regions, creating employment in restive areas, demonstrating state presence in frontier territories.

The foundation laid in these early years—vertical integration, nationwide presence, technological capability, and deep integration with government policy—would prove both Indian Oil's greatest strength and its most persistent challenge in the decades to come.

IV. Building the Oil Empire (1980s–1990s)

The 1980s dawned with Indian Oil at an inflection point. The company had established dominance in downstream operations, but the real test lay ahead: could it transform from a protected monopoly into a modern, efficient enterprise capable of meeting India's exploding energy demands?

The decade's defining moment came with the commissioning of the Mathura refinery in 1982. This wasn't just another refinery—it was a statement of technological ambition. Located strategically to serve the northern markets, the facility incorporated advanced catalytic cracking and reforming units, producing high-octane gasoline and low-sulfur diesel that met international specifications. The project, executed with French collaboration, demonstrated Indian Oil's growing ability to absorb and adapt global technologies.

Pipeline infrastructure emerged as Indian Oil's hidden competitive advantage. By the late 1980s, the company operated a spider's web of pipelines stretching over 13,000 kilometers—one of the longest networks in Asia. These weren't mere conduits; they were strategic assets that created insurmountable barriers to entry. The Salaya-Mathura pipeline, spanning 1,269 kilometers from Gujarat's coast to the northern heartland, exemplified this infrastructure edge. It could transport 18 million tonnes of crude annually, feeding multiple refineries and eliminating thousands of rail and road movements.

The License Raj, India's notorious system of permits and quotas, paradoxically strengthened Indian Oil's position. While private enterprise suffocated under bureaucratic controls, Indian Oil navigated these waters with ease. Need land for a depot? Government acquisition powers smoothed the way. Environmental clearances? Fast-tracked through inter-ministerial coordination. Labor issues? The prestige of working for a Navratna (nine jewels) company—a status informally accorded to top public sector units—attracted the best talent and ensured industrial peace.

But the 1990s brought seismic shifts. The Soviet Union's collapse in 1991 triggered India's balance of payments crisis, forcing the country to airlift gold reserves to London as collateral for emergency loans. The medicine prescribed by the International Monetary Fund was bitter: liberalize, privatize, globalize. For Indian Oil, comfortable in its monopoly cocoon, the new world order posed existential questions.

The government's response was carefully calibrated. Rather than dismantling Indian Oil, it chose to corporatize it. In 1995, the company went public, listing on the Bombay Stock Exchange. The oil concern is administratively controlled by India's Ministry of Petroleum and Natural Gas, a government entity that owns just over 90 percent of the firm. The IPO was a watershed moment—suddenly, Indian Oil had to answer not just to petroleum ministry bureaucrats but to shareholders, analysts, and market expectations.

The transformation wasn't merely cosmetic. Corporate governance structures were overhauled. Professional managers supplemented bureaucratic appointees. Performance metrics shifted from volume targets to profitability ratios. The company began thinking in terms of return on capital employed, not just barrels refined or tonnage transported.

Yet the tension between public service and commercial objectives intensified. Indian Oil still bore the burden of "universal service obligations"—supplying remote locations where private players wouldn't venture, maintaining strategic reserves for national security, absorbing losses on controlled products like kerosene and LPG. The company developed sophisticated internal accounting to track these social costs, arguing for compensation from the government with mixed success.

International expansion emerged as a strategic priority. In 1995, Indian Oil incorporated subsidiaries in Sri Lanka and Mauritius—modest beginnings of what would become a significant overseas presence. The Lanka IOC venture was particularly significant, marking Indian Oil's first international downstream operation. Despite political tensions and operational challenges, it demonstrated the company's ability to compete outside its protected home market.

Technology advancement accelerated through the 1990s. The Indian Oil Research and Development Centre at Faridabad evolved from a quality control laboratory into a serious research institution. Scientists developed indigenous catalysts for refineries, formulated specialty lubricants for defense applications, and pioneered bio-fuels research. The INDMAX fluid catalytic cracking technology, developed in-house, would later be licensed to refineries globally—a remarkable reversal from the technology-importing days.

The retail network underwent dramatic modernization. The traditional "petrol pump"—often just a couple of dispensers under a tin shed—gave way to modern fuel stations. Indian Oil introduced computerized dispensers, electronic payment systems, and convenience stores. The company's retail outlets, numbering over 20,000 by decade's end, became ubiquitous markers of development—"Where there's a road, there's Indian Oil" became an unofficial motto.

Labor relations, always complex in public sector units, required delicate handling. Indian Oil employed over 30,000 people directly, with hundreds of thousands more dependent on its ecosystem—dealers, distributors, transporters, contractors. The company pioneered progressive HR practices: performance-linked incentives, voluntary retirement schemes, extensive training programs. The Indian Oil Management Academy became a finishing school for petroleum sector executives across Asia.

As the millennium approached, Indian Oil stood transformed yet conflicted. It had successfully evolved from a monopoly to a commercial enterprise, from a domestic player to an international presence, from a volume-driven organization to a value-focused corporation. Yet the fundamental tension remained unresolved: How to balance shareholder returns with social responsibilities? How to compete with nimble private players while carrying legacy burdens? These questions would define Indian Oil's journey into the new century.

V. Liberalization & Competition (1991–2000s)

The economic reforms of 1991 hit Indian Oil like a tsunami. Overnight, the protective walls that had sheltered the company for three decades came crashing down. That changed in April 2002, however, when the Indian government deregulated its petroleum industry and ended Indian Oil's monopoly on crude oil imports. Private players were now free to import, refine, and market petroleum products. The monopoly was dead; competition had arrived.

The new entrants weren't minor players. Reliance Industries, led by the ambitious Dhirubhai Ambani, commissioned the world's largest refinery complex at Jamnagar. Essar Oil built a sophisticated refinery in Gujarat. Shell, BP, and Total returned to India after decades of absence, setting up joint ventures and retail networks. Even state-owned peers like Bharat Petroleum and Hindustan Petroleum, freed from Indian Oil's distribution monopoly, became fierce competitors.

Indian Oil's initial response was defensive—protect market share at all costs. But chairman after chairman realized that the old playbook wouldn't work. The company needed radical transformation, not incremental change. The strategy that emerged was multi-pronged: modernize refineries to compete on efficiency, leverage the distribution network as a competitive moat, and use the brand trust built over decades as a differentiator.

Refinery upgradation became mission critical. Indian Oil invested billions in secondary processing units—hydrocrackers, cokers, catalytic reformers—that could convert low-value fuel oil into high-margin gasoline and diesel. The Panipat refinery expansion, completed in 2006, showcased this approach. Not only did it double capacity to 15 million tonnes, but it also achieved complexity levels matching global benchmarks. The refinery could now process cheaper, heavier crudes while producing cleaner, premium products.

The retail transformation was equally dramatic. Indian Oil realized that location was everything in fuel retail. The company leveraged its first-mover advantage and government relationships to lock up prime sites on highways and city centers. By 2005, Indian Oil operated over 25,000 retail outlets—more than all competitors combined. But quantity wasn't enough; quality mattered too. The company launched the "XtraCare" format—world-class fuel stations with automated systems, convenience stores, ATMs, and food courts. The message was clear: Indian Oil could match any international player in service standards.

Marketing became sophisticated. For decades, Indian Oil had barely advertised—why would a monopoly need to? Now, the company launched creative campaigns targeting different segments. "XtraMile" diesel promised better mileage for truckers. "XtraPower" petrol appealed to performance-conscious urban drivers. The Servo lubricants brand was repositioned from a functional product to an emotional choice—"Inspiring Confidence."

International expansion accelerated as Indian Oil sought growth beyond the increasingly competitive domestic market. Its subsidiaries include Chennai Petroleum Corporation Limited, IndianOil (Mauritius) Limited, Lanka IOC PLC, IOC Middle East FZE, IOC Sweden AB, and others. The company formed joint ventures for overseas exploration, acquired stakes in foreign refineries, and established trading offices in Singapore and Dubai. The Middle East became a particular focus, with Indian Oil securing long-term crude supply agreements with Saudi Aramco, Kuwait Petroleum, and Abu Dhabi National Oil Company.

But competition also exposed Indian Oil's vulnerabilities. Private players cherry-picked profitable segments—aviation fuel at metro airports, bulk diesel to industrial customers, retail outlets in affluent neighborhoods. They avoided loss-making obligations like kerosene distribution or rural fuel stations. Indian Oil, bound by its public sector character, couldn't abandon these responsibilities. The company found itself in an awkward position: competing with one hand tied behind its back.

The subsidy burden became increasingly problematic. While market prices for petrol and diesel rose with global crude, the government kept domestic prices artificially low through a complex subsidy mechanism. Indian Oil, along with other state-owned oil marketing companies, bore the brunt—selling products below cost and awaiting uncertain government compensation. In some years, under-recoveries exceeded the company's entire net worth, creating massive working capital stress.

Technology emerged as a crucial battleground. Reliance's Jamnagar refinery used cutting-edge technology to achieve unprecedented efficiency. Shell brought global R&D capabilities to develop differentiated fuels. Indian Oil responded by ramping up its own innovation efforts. The company's R&D center developed the INDAdeptG technology for producing ultra-low sulfur diesel, meeting Euro-VI standards before they became mandatory. The INDMAX technology for maximizing LPG production from heavy feedstocks found international customers, generating licensing revenues.

Strategic partnerships became essential for capability building. Indian Oil formed joint ventures with global technology leaders: with Oiltanking for terminaling, with Petronas for lubricants, with NTPC for gas-based power plants. Each partnership brought technology, best practices, and market access that would have taken years to develop independently.

The 2008 global financial crisis tested Indian Oil's resilience. Oil prices swung from $147 to $32 per barrel within months, creating inventory losses and demand destruction. The company's size became a liability—high fixed costs and massive working capital requirements amplified the pain. Yet Indian Oil emerged stronger, having learned valuable lessons about risk management, operational flexibility, and the importance of financial discipline.

By the decade's end, Indian Oil had successfully navigated the transition from monopoly to competition. Market share in petroleum products had declined from near-100% to about 42%, but the company remained the undisputed leader. More importantly, it had developed muscles it never needed before: customer focus, operational excellence, innovation capability, and strategic thinking. The question now was whether these new capabilities would be enough for the challenges ahead—the rise of electric vehicles, the global push for renewable energy, and the growing environmental consciousness that threatened the very existence of oil companies.

VI. The Modern Giant (2010–Present)

The year 2010 marked a symbolic milestone in Indian Oil's evolution. Indian Oil Corporation Ltd is a Maharatna Company controlled by GOI that has business interests straddling the entire hydrocarbon value chain - from Refining, Pipeline transportation and marketing of Petroleum products to R&D, Exploration & production, marketing of natural gas and petrochemicals. The Maharatna status wasn't just ceremonial—it granted the company unprecedented autonomy in investment decisions, international ventures, and strategic partnerships. For an organization long accustomed to seeking ministerial approval for major decisions, this freedom was transformative.

The numbers tell a story of sustained dominance despite fierce competition. It has consolidated refining capacity of 80.55MMTPA. The company's infrastructure footprint is staggering: It owns 11 refineries across India with a total capacity of 80.80 MMTPA (including 10.5 MMTPA of subsidiaries), possessing 31% of the total refining capacity of India. This translates to processing capability that can meet nearly half of India's petroleum product demand.

The retail network expansion continued unabated. By 2020, Indian Oil operated approximately 30,000 fuel stations—a number that seems almost incomprehensible until you consider India's geography and population density. Each outlet serves as more than just a fuel stop; they're crucial nodes in India's economic circulation system, enabling the movement of goods and people across vast distances.

The financial performance through this period reflected both strengths and vulnerabilities. The high-water mark came in 2017-18 when Indian Oil recorded a profit of ₹21,346 crores—a testament to operational efficiency and favorable market conditions. However, the volatility inherent in the oil business showed its harsh face too. In 2024, Indian Oil Corporation's revenue was 7.58 trillion, a decrease of -2.35% compared to the previous year's 7.76 trillion. Earnings were 135.98 billion, a decrease of -67.41%.

March 2022 brought a symbolic shift when Indian Oil was replaced by Apollo Hospitals in the Nifty 50 benchmark index. For market watchers, this represented more than just an index rebalancing—it signaled the changing priorities of the Indian economy, from old-economy stalwarts to new-age sectors. Yet the company's response was characteristic: acknowledge the challenge, but stay focused on the long game.

Digital transformation emerged as a critical priority. Indian Oil launched mobile apps for fuel station location, loyalty programs, and LPG booking. The company implemented advanced analytics for demand forecasting, predictive maintenance for refineries, and blockchain for supply chain transparency. These weren't cosmetic changes but fundamental rewiring of operations that had remained largely unchanged for decades.

The international crude sourcing strategy underwent dramatic shifts. Historically dependent on Middle Eastern suppliers, Indian Oil aggressively diversified its procurement. IndianOil has paused term deal talks with Rosneft due to market dynamics, not government pressure, while increasing US energy imports to reduce the trade surplus. In 2017, Indian Oil became the first Indian company to receive U.S. crude oil, marking a geopolitical shift as significant as the economic one. The company now sources crude from over 30 countries, reducing dependency on any single region.

2020: IndianOil launched its first electric vehicle charging station in Nagpur, signaling its foray into the electric mobility sector. This wasn't a token gesture but part of a comprehensive strategy to remain relevant in a decarbonizing world. IOCL envisages to provide 10,000 EV Charging Stations by 2024 transforming retail network to complete energy solutions outlets. With more than 6,000 EV charging stations at present, the company plans to keep expanding its reach.

The renewable energy push gained momentum. State-owned oil and gas company the Indian Oil Corporation has announced an investment of Rs52.15bn ($624.7m) to develop 1GW of renewable energy capacity in India. The initiative, approved by the company's board, will be directed towards establishing standalone ground-mounted solar or onshore wind or wind-solar hybrid projects in a phased approach. The company established solar power plants at its refineries and depots, wind farms in Gujarat and Rajasthan, and began exploring green hydrogen production—a potential game-changer for both refining operations and future energy systems.

Strategic partnerships reflected evolving priorities. The collaboration with Israel's Phinergy for aluminum-air batteries represented a bet on next-generation energy storage. The joint venture with Panasonic for lithium-ion cell manufacturing aimed to capture value in the electric vehicle supply chain. Tata Power announced on Monday that its business, Tata Power EV Charging Solutions Limited, had inked a Memorandum of Understanding (MoU) with Indian Oil Corporation Limited (IOCL). Tata Power announced in a statement that it will deploy EV charging stations at several IOCL retail locations.

The BS-VI fuel rollout in 2020 showcased Indian Oil's technical and operational capabilities. Upgrading refineries to produce ultra-low sulfur fuels required investments exceeding ₹30,000 crores across the industry. Indian Oil led this transition, ensuring seamless supply of cleaner fuels across its network before the deadline—a logistical achievement comparable to India's demonetization or GST rollout.

Petrochemicals emerged as a growth driver. The paradox of oil companies investing in petrochemicals while fuel demand faces long-term decline isn't lost on Indian Oil's strategists. But petrochemicals offer what fuels increasingly don't: demand growth, value addition, and integration with India's manufacturing ambitions. The company's petrochemical complexes at Panipat and Paradip produce polymers and chemicals that feed into everything from packaging to automobiles.

Natural gas became another diversification avenue. Indian Oil entered city gas distribution through joint ventures, laying pipelines for cooking gas and CNG in urban areas. The company's gas trading volumes grew substantially, positioning it as a integrated energy company rather than just an oil refiner and marketer.

Yet challenges mounted. The company has delivered a poor sales growth of 9.40% over past five years. Company has a low return on equity of 13.1% over last 3 years. The stock market's lukewarm response reflected broader concerns: peak oil demand approaching, electric vehicle adoption accelerating, renewable energy costs plummeting, and ESG considerations increasingly driving investment decisions.

The COVID-19 pandemic delivered an unprecedented shock. Demand collapsed as India locked down, refineries operated at historic low utilizations, and thousands of fuel stations saw no customers for weeks. Indian Oil's response demonstrated both vulnerability and resilience—the company maintained fuel supply for essential services, supported employees and dealers through the crisis, and used the downturn to accelerate maintenance and upgrades.

Recent financial performance shows recovery but also persistent challenges. Indian Oil Corporation Ltd's net profit jumped 57.78% since last year same period to ₹8,123.64Cr in the Q4 2024-2025. On a quarterly growth basis, Indian Oil Corporation Ltd has generated 284.04% jump in its net profits since last 3-months. The volatility in earnings—massive quarterly swings based on inventory gains or losses, subsidy burdens, and crude price movements—remains a structural issue.

As Indian Oil navigates its seventh decade, the company stands at perhaps its most crucial crossroads. The core business remains robust but faces existential threats. The new ventures show promise but require capabilities different from traditional strengths. The question isn't whether Indian Oil can survive the energy transition—its size and systemic importance almost guarantee survival. The question is whether it can thrive, transform, and remain relevant in an energy landscape that might look nothing like the one it was created to serve.

VII. Strategic Diversification & Future Bets

The writing on the wall is clear, even if written in multiple languages: peak oil demand for transportation is not a question of if, but when. Indian Oil's leadership knows this, which explains the frenetic pace of diversification initiatives launched in recent years. These aren't desperate throws of dice but calculated bets on where energy markets are heading.

The electric vehicle charging infrastructure buildout represents the most visible pivot. Indian Oil said that the company has already set up 54 battery charging/swapping stations for EVs in partnership with various companies as a part of Indian Oil's foray into alternative energy, adding that to set up an aluminium-air battery manufacturing facility in India, the company has taken a minority stake in Phinergy of Israel for electric vehicles and stationary applications. The partnership with Israel's Phinergy for aluminum-air batteries is particularly intriguing—this technology promises ranges exceeding 1,000 kilometers, potentially solving the range anxiety that haunts EV adoption.

Last year, the union government sanctioned ₹8 billion (~$96 million) under FAME India Program Phase II to the public-sector oil-marketing firms to install 7,432 fast charging stations nationwide. IOCL was responsible for setting up a total of 3,483 fast charging stations, including upstream infrastructure like AC distribution boxes, circuit breakers, protection equipment, mounting structures, and fencing. The company isn't just installing chargers; it's reimagining fuel stations as energy hubs offering multiple fuel options—petrol, diesel, CNG, electric charging, and eventually hydrogen.

The renewable energy thrust goes beyond token installations. IOC said that the company's clean energy agenda includes its renewable energy portfolio of 226 MW (58 MW of solar photovoltaic capacity and 168 MW of wind-power capacity) that generated 393 million units of electricity together during FY20. This is equivalent to emission mitigation of 5% of the company's electricity consumption and 322 TMT of carbon dioxide (TMTCO2e). The target of 1GW renewable capacity by 2025 might seem modest compared to dedicated renewable players, but for an oil company, it represents a fundamental identity shift.

Petrochemicals expansion follows a different logic. As fuel demand plateaus, refineries worldwide are reconfiguring to maximize chemical production. Indian Oil's integrated refinery-petrochemical complexes at Panipat and Paradip can switch between fuel and chemical modes based on market dynamics. The company is betting that even in an electrified future, demand for plastics and chemicals will continue growing—a controversial but probably accurate assessment.

Green hydrogen emerges as perhaps the most strategic bet. Indian Oil Corporation is advancing its green hydrogen initiatives with a major project at Panipat Refinery, while also addressing compliance issues regarding vehicle contracts. The green hydrogen plant aims to significantly reduce carbon emissions and support India's energy transition. Hydrogen serves multiple purposes: it's essential for refining operations (desulfurization), it could power fuel cell vehicles, and it offers a pathway to decarbonize heavy industries. Indian Oil's refineries, with their massive hydrogen production and consumption, provide a ready platform for green hydrogen deployment.

Natural gas infrastructure development reflects another hedged bet. While gas is still a fossil fuel, it's cleaner than oil and coal, making it a transition fuel in India's energy journey. Indian Oil's city gas distribution networks, operated through joint ventures, position the company to benefit from India's goal of increasing gas's share in the energy mix from 6% to 15% by 2030.

Biofuels present both opportunity and challenge. Indian Oil has invested in second-generation ethanol plants that use agricultural waste rather than food crops. The company's compressed biogas (CBG) initiative encourages entrepreneurs to set up plants that convert organic waste to gas, which Indian Oil purchases and markets. These initiatives align with government mandates for ethanol blending and waste management, but scalability remains uncertain.

International exploration and production ventures reflect a desire to move upstream in the value chain. Through overseas acquisitions and joint ventures, Indian Oil has secured equity oil—production that provides supply security and potential windfall profits when prices spike. However, these ventures also expose the company to exploration risk and geopolitical uncertainties.

The venture into battery manufacturing with Panasonic represents a bold step into unfamiliar territory. In March 2024, Indian Oil entered into a preliminary agreement with Japan's Panasonic to explore a joint production of lithium-ion cells for two and three-wheelers. The collaboration with Panasonic is currently undergoing a feasibility study, to leverage battery technology to support India's transition to clean energy. The partners will give the details of their joint venture by summer 2024. Manufacturing batteries requires competencies far removed from refining oil—precision manufacturing, electronics, chemical engineering of a different sort. Success here could position Indian Oil as an integrated energy solutions provider; failure would be an expensive lesson in the limits of diversification.

The challenge with all these initiatives is execution. Indian Oil's core competency lies in large-scale industrial operations—running refineries, managing pipelines, distributing petroleum products. The new ventures require different skills: technology development, customer service, rapid innovation, partnership management. Can an organization built for stability and scale adapt to the agility and innovation these new businesses demand?

Financial allocation presents another dilemma. Every rupee invested in renewable energy or EV infrastructure is a rupee not invested in refinery upgrades or marketing infrastructure. With limited capital and competing priorities, Indian Oil must make Solomon-like choices. The company's solution—creating separate subsidiaries for new ventures—allows focused management but risks creating silos that don't leverage synergies.

The regulatory environment adds complexity. Government policies whipsaw between promoting alternatives (EV subsidies, renewable energy mandates) and protecting traditional industries (fuel tax revenues, refinery employment). Indian Oil must navigate these contradictions, investing in transitions while maintaining current operations.

The ultimate question is whether Indian Oil is transforming fast enough. Global oil majors like Shell and BP have announced net-zero targets and are radically restructuring portfolios. Chinese national oil companies are aggressively investing in batteries and renewable energy. Indian Oil's diversification, while significant by its own standards, might be insufficient given the pace of energy transition. The company's future might depend not on how well it manages gradual change, but on its ability to reimagine itself entirely—from an oil company that dabbles in alternatives to an energy company that happens to refine oil.

VIII. The Government Dance: Politics & Business

The relationship between Indian Oil and the Government of India is perhaps the most complex corporate-sovereign partnership in modern business. Promoter Holding: 51.5% This majority stake ensures government control, but the remaining ownership by public shareholders, institutions, and foreign investors creates competing accountability structures that would challenge any leadership team.

The dance begins with appointment of leadership. The Chairman and Managing Director of Indian Oil is selected not through a corporate board process but through the Public Enterprises Selection Board, a government body. The selected candidate must navigate not just business challenges but political currents, bureaucratic processes, and sometimes, contradictory signals from different ministries. The average tenure of an Indian Oil CMD is just three to four years—barely enough time to implement strategic changes before the next leader arrives with potentially different priorities.

Pricing represents the most visible friction point. While petroleum products are technically deregulated, the government's influence remains pervasive through moral suasion, tax adjustments, and informal pressure. During election seasons, fuel price increases mysteriously pause. When inflation runs high, oil companies are "encouraged" to absorb costs rather than pass them to consumers. Indian Oil's pricing committee must factor not just global crude costs and competitive dynamics but also political sensitivities and social implications.

The subsidy mechanism reveals the complexity of this relationship. For decades, Indian Oil sold kerosene and LPG below cost, with the government promising compensation. But these promises often came with delays, disputes over quantum, and payment through oil bonds rather than cash. At times, Indian Oil's under-recoveries—the euphemistic term for losses on controlled products—exceeded ₹50,000 crores annually, creating massive working capital stress and forcing expensive borrowings.

Social mandates extend beyond pricing. Indian Oil must maintain fuel stations in remote, uneconomical locations—from Ladakh's frozen highlands to Andaman's isolated islands. The company operates mobile fuel dispensers for border areas, supplies subsidized kerosene through the Public Distribution System, and provides free LPG connections under government schemes. These activities serve crucial social purposes but generate minimal returns, creating a permanent drag on profitability.

The employment dimension adds another layer. Indian Oil directly employs over 31,000 people, but political pressure often prevents rightsizing even when technology makes roles redundant. Voluntary retirement schemes require delicate negotiation with powerful unions. Meanwhile, the company must also accommodate "social obligations"—recruiting from disadvantaged communities, providing jobs to project-affected persons, maintaining quotas that sometimes override merit considerations.

International dealings showcase the government's shadow presence. Indian Oil's crude sourcing decisions involve not just commercial considerations but geopolitical calculations. The company increased purchases from Iraq to support reconstruction efforts, bought from Iran despite sanctions pressure, and recently pivoted to U.S. crude to balance trade relationships. Indian Oil Corporation's Chairman indicated a return to pre-Ukraine supply methods if Russian oil is disrupted. JM Financial recommends selling IOC shares due to risk concerns. Each decision reflects government foreign policy as much as commercial logic.

Investment decisions reveal similar dynamics. Major capital expenditures require multiple approvals—from the company board, petroleum ministry, finance ministry, and sometimes the cabinet. A refinery expansion that makes perfect business sense might be delayed for years awaiting clearances. Conversely, projects in politically important regions might receive fast-track approval despite questionable economics.

The dividend policy exemplifies the government's dual role as promoter and revenue collector. Indian Oil consistently pays hefty dividends—often exceeding 50% of profits—because the government needs these flows for budgetary purposes. This limits retained earnings for growth investments, forcing the company to borrow for expansion even when internally generated funds could suffice.

Strategic autonomy, supposedly enhanced by Maharatna status, remains circumscribed. While Indian Oil can now approve investments up to ₹5,000 crores independently, major strategic decisions—mergers, acquisitions, new business ventures—still require government blessing. The proposed merger with other state-owned oil companies, discussed periodically for synergy benefits, remains stuck in political considerations about regional balance and employment implications.

The privatization debate haunts Indian Oil's planning horizon. The Indian Oil Corporation (IOC) is poised to receive significant government support through a compensation package aimed at offsetting losses from subsidized LPG sales. The government is finalizing a ₹32,000–35,000 crore package to alleviate financial pressures on IOC and other oil marketing companies. Every few years, voices emerge advocating privatization to unlock value and improve efficiency. But the government's dependence on Indian Oil—for energy security, revenue generation, and policy implementation—makes privatization politically impossible despite economic arguments.

Yet this relationship isn't entirely constraining. Government ownership provides advantages unavailable to private competitors. Land acquisition for projects becomes easier through government machinery. Diplomatic support opens doors in international markets. Sovereign backing enables favorable financing terms. During crises—whether the 1991 Gulf War or 2020 pandemic—government support ensures survival when private players might fail.

The recent compensation package for LPG under-recoveries illustrates both the burden and benefit of government ownership. While private players enjoy pricing freedom, they also lack the safety net that protects Indian Oil during adverse market conditions. The company operates in a unique space—neither fully commercial nor entirely governmental, bearing responsibilities of both while enjoying complete privileges of neither.

Indian Oil's management has evolved sophisticated strategies to navigate this complex relationship. They maintain strong relationships across political parties, ensuring continuity despite government changes. They document social obligations meticulously, quantifying costs to argue for compensation. They benchmark performance against global peers, demonstrating efficiency despite constraints. Most importantly, they've learned to frame business decisions in language that resonates with political masters—energy security, social justice, national development.

The future of this relationship remains uncertain. As India develops, the rationale for government ownership weakens—energy security seems less precarious, private capital is abundant, market mechanisms work reasonably well. Yet path dependency is powerful. Indian Oil has become so intertwined with government machinery—from subsidy delivery to strategic reserves—that disentanglement seems impossibly complex. The dance continues, sometimes graceful, often awkward, but always fascinating in its complexity.

IX. Playbook: Operating Lessons

Seven decades of operations have given Indian Oil a playbook that reads like a masterclass in managing complexity at scale. These aren't lessons from business school case studies but hard-won insights from running one of the world's most complex energy operations in one of its most challenging markets.

Building and Maintaining Critical Infrastructure at Scale

Indian Oil's pipeline network tells a story of engineering ambition that borders on audacity. Imagine laying 13,000 kilometers of steel pipes across a subcontinent—through deserts where temperatures exceed 50°C, through mountains where winter brings everything to standstill, through densely populated plains where every meter requires negotiation with landowners, and through forests where environmental concerns clash with energy needs.

The execution strategy evolved through painful trial and error. Early pipelines, built with imported technology and expatriate supervision, proved expensive and slow. Indian Oil developed indigenous capabilities, training welders who could work in extreme conditions, engineers who could design around local constraints, and project managers who could navigate India's byzantine approval processes. The company pioneered micro-tunneling techniques to lay pipelines under rivers without disrupting flow, developed hot-tapping technology to connect new segments without shutting down operations, and created mobile quality labs that could test weld integrity in remote locations.

Its business interests span the entire hydrocarbon value-chain, ranging from refining, pipeline transportation and marketing, to exploration and production of crude oil and gas, petrochemicals, gas marketing, alternative energy sources and globalization of downstream operations. It has a network of fuel stations, bulk storage terminals, inland depots, aviation fuel stations, liquefied petroleum gas (LPG) bottling plants and lube blending plants.

Maintenance presents equal challenges. Pipelines carrying millions of tons of petroleum products can't afford failures—environmental disasters, supply disruptions, and economic losses would follow. Indian Oil developed sophisticated integrity management systems, using intelligent pigs (pipeline inspection gauges) that travel through pipelines detecting corrosion, cracks, and deformations. The company maintains emergency response teams stationed strategically along pipeline routes, capable of reaching any point within hours.

Managing Government Ownership While Competing with Private Players

The dual identity—government-owned yet commercially competing—requires constant balancing. Indian Oil developed what insiders call "competitive compartmentalization." Customer-facing operations—retail outlets, industrial sales, aviation fueling—operate with full commercial orientation. Staff are incentivized on market share, customer satisfaction, and profitability. Meanwhile, government-interface functions—subsidy administration, strategic reserves, social schemes—run on different metrics focused on compliance and social impact.

This compartmentalization extends to organizational culture. Retail and marketing teams cultivate entrepreneurial spirit, encouraging innovation and risk-taking. Refinery operations emphasize precision and safety, building a culture of technical excellence. Corporate functions maintain bureaucratic discipline necessary for government reporting and compliance. The challenge lies in preventing these cultures from becoming silos, which Indian Oil addresses through systematic rotation of high-performers across functions.

The Art of Cross-Subsidization and Market Segmentation

Indian Oil has elevated cross-subsidization to an art form. Premium products sold to affluent urban consumers—branded petrol, premium lubricants, specialty chemicals—generate margins that offset losses on kerosene sold to rural poor. Aviation turbine fuel sold to international airlines subsidizes diesel supplied to farmers. Industrial products sold to large corporations support LPG distributed at controlled prices.

This requires sophisticated market segmentation and pricing strategies. Indian Oil maintains detailed customer databases, tracking consumption patterns, payment histories, and price sensitivities. The company uses dynamic pricing for non-controlled products, adjusting margins based on local competition and demand elasticity. Transfer pricing between refineries and marketing divisions is carefully calibrated to ensure fair allocation of profits and losses across the value chain.

Supply Chain Mastery

Operating India's largest petroleum supply chain requires orchestration skills that would challenge any logistics company. Every day, Indian Oil moves roughly 200,000 tonnes of petroleum products—equivalent to filling 8,000 trucks—from refineries to depots to retail outlets. This happens across a country with infrastructure constraints, regulatory bottlenecks, and seasonal disruptions.

The company developed multi-modal transportation strategies, optimizing between pipelines, rail, road, and coastal shipping based on cost, speed, and reliability. Indian Oil operates one of India's largest private rail-wagon fleets, maintains contracts with thousands of truck operators, and charters coastal tankers for peninsular distribution. The logistics team uses advanced analytics to optimize routing, predict demand, and preposition inventory ahead of seasonal spikes.

Brand Building in a Commodity Business

Petroleum products are ultimate commodities—chemically identical regardless of supplier. Yet Indian Oil has built powerful brands that command customer loyalty. Indane cooking gas reaches 130 million households, making it one of India's most recognized brands. SERVO lubricants compete with global brands like Castrol and Shell. XtraMile and XtraPower fuels command premium prices despite chemical similarity to regular products.

The branding strategy focuses on trust and reliability rather than product differentiation. Indian Oil positioned itself as the dependable partner—always available, quality assured, fairly priced. The company invests heavily in preventing adulteration, using molecular markers to track products through the supply chain. Regular quality checks at retail outlets, published in local media, reinforce the trust proposition. During crises—whether natural disasters or supply disruptions—Indian Oil's ability to maintain supplies while competitors fail becomes powerful brand reinforcement.

Navigating Energy Transition While Protecting Core Business

The existential challenge of energy transition requires delicate handling. Indian Oil must invest in alternatives that could eventually cannibalize its core business while ensuring current operations generate cash for transformation. The strategy involves careful sequencing and hedging.

Electric vehicle charging infrastructure is positioned not as replacement but complement to traditional fuels. Fuel stations are reimagined as energy stations offering multiple options. Renewable energy investments focus initially on captive consumption, reducing operational costs before venturing into merchant power. Petrochemical expansion provides hedge against transport fuel decline. Natural gas infrastructure can later carry hydrogen or biogas.

The company maintains strategic ambiguity about transition timing, avoiding commitments that might accelerate demand destruction while signaling enough green intent to maintain social license. This balancing act—appearing progressive without undermining current business—requires sophisticated communication strategies and careful stakeholder management.

Organizational Capabilities

Perhaps Indian Oil's greatest achievement is building organizational capabilities that transcend individual leaders or market conditions. The company created systems and processes robust enough to function despite political interference, market volatility, and technological disruption. Standard operating procedures cover everything from refinery startups to retail outlet audits. Succession planning ensures leadership continuity despite government appointments. Knowledge management systems capture decades of operational experience, accessible to new generations of engineers and managers.

The Indian Oil Management Academy serves as finishing school for petroleum professionals, repository of institutional knowledge, and innovation lab for new ideas. The R&D center bridges the gap between global technology and local application, adapting international best practices to Indian conditions. These institutional capabilities—more than physical assets or market position—represent Indian Oil's true competitive advantage.

X. Bull vs. Bear Analysis

The investment case for Indian Oil presents a fascinating study in contradictions. Bulls and bears can marshal equally compelling arguments, each backed by solid evidence and reasonable projections. The truth, as often happens, likely lies somewhere in between, but the extreme cases illuminate the key variables that will determine Indian Oil's future.

The Bull Case: An Undervalued Energy Infrastructure Giant

Bulls begin with Indian Oil's irreplaceable infrastructure. IOC has a 42% market share in Petroleum Oil and Lubricants with over 60,900 touch points. It owns 11 refineries across India with a total capacity of 80.80 MMTPA (including 10.5 MMTPA of subsidiaries), possessing 31% of the total refining capacity of India. Replacing this infrastructure would cost hundreds of billions of dollars and take decades—time and capital that no competitor possesses. The pipeline network alone, spanning 13,000 kilometers through some of India's most challenging terrain, represents an insurmountable moat.

The scale advantages are undeniable. Indian Oil's refineries, with 80.8 million tonnes annual capacity, benefit from economies that smaller players can't match. Procurement power enables better crude pricing and payment terms. Distribution efficiency improves with density—the cost per liter delivered decreases as volumes increase. Technology investments, whether in refinery automation or digital platforms, can be amortized across massive volumes. These scale benefits create a virtuous cycle: lower costs enable competitive pricing, which drives volume, which further reduces unit costs.

India's energy demand story remains compelling despite energy transition narratives. The country's per capita energy consumption is one-third the global average—massive growth potential remains. Vehicle ownership stands at just 22 per 1,000 people compared to 980 in the United States. Even aggressive EV adoption scenarios show oil demand growing until 2040, driven by aviation, shipping, petrochemicals, and industrial uses. Indian Oil, as the domestic champion, is best positioned to capture this growth.

Government backing provides stability unavailable to private players. The Indian Oil Corporation (IOC) is poised to receive significant government support through a compensation package aimed at offsetting losses from subsidized LPG sales. The government is finalizing a ₹32,000–35,000 crore package to alleviate financial pressures on IOC and other oil marketing companies. Additionally, IOC is upgrading its refinery for sustainable fuel production, enhancing its long-term growth prospects. During crises, whether financial or operational, sovereign support ensures survival. The too-big-to-fail dynamic means creditors lend at favorable rates, suppliers extend generous terms, and customers trust long-term contracts.

Valuation metrics suggest deep undervaluation. The company trades at price-to-book ratios below 1, implying the market values Indian Oil less than its accounting net worth. Dividend yields exceed 10% in many years, providing attractive income even without capital appreciation. Replacement cost of assets far exceeds market capitalization. By almost any traditional metric, Indian Oil appears cheap.

The diversification strategy could unlock hidden value. Success in any new venture—whether EV charging, renewable energy, or petrochemicals—could trigger rerating. The battery manufacturing joint venture with Panasonic, if successful, could be worth billions as a standalone entity. City gas distribution networks, as they mature, generate stable, utility-like returns. These options have substantial value not reflected in current valuations.

The Bear Case: A Melting Ice Cube in a Warming World

Bears see Indian Oil as a melting ice cube—superficially solid but inexorably shrinking. The energy transition isn't a distant threat but a present reality. Electric vehicle sales in India grew 40% in 2024. Solar power costs have fallen below coal, making renewable energy economically superior even without subsidies. Global oil majors are pivoting to renewables, suggesting industry insiders see the writing on the wall.

The financial performance reveals structural weaknesses. The company has delivered a poor sales growth of 9.40% over past five years. Company has a low return on equity of 13.1% over last 3 years. These metrics, during what should be profitable years with stable oil prices and growing demand, suggest fundamental challenges. The earnings volatility—massive swings based on inventory gains/losses and subsidy timing—makes the business uninvestable for many institutional investors.

Competition continues intensifying. Reliance's refinery complex is more efficient, producing higher margins. Private retailers cherry-pick profitable segments. International players bring superior technology and global supply chains. Meanwhile, Indian Oil carries legacy burdens—aging refineries requiring constant upgrades, bloated workforce resistant to change, social obligations that drain resources. Market share erosion, from near-monopoly to 42%, could accelerate as competition intensifies.

Government interference limits upside potential. Even when Indian Oil generates exceptional profits, government extracts value through dividends, leaving insufficient capital for growth. Pricing freedom remains illusory—political pressure prevents margin expansion during favorable conditions. Strategic decisions require bureaucratic approval, slowing response to market changes. The company operates with one hand tied behind its back while competitors enjoy full flexibility.

The stock market's verdict is damning. Removal from the Nifty 50 index signals institutional disinterest. The persistent discount to book value suggests markets doubt asset quality or earning power. Low trading volumes indicate investor apathy. Smart money has moved to new economy stocks, leaving Indian Oil to value investors and index funds obligated to hold public sector units.

Peak oil demand for transport fuels could arrive sooner than expected. Technology adoption often follows S-curves—slow initially, then explosive. India could leapfrog internal combustion engines like it leapfrogged landlines for mobile phones. Urban pollution concerns are driving aggressive EV policies. Global automakers are phasing out ICE development. Once the tipping point arrives, demand destruction could be swift and brutal.

The Verdict: A Complex Reality

The truth likely lies between these extremes. Indian Oil will probably neither collapse nor soar but muddle through—generating decent cash flows, paying attractive dividends, gradually transforming its business mix. The infrastructure moat provides time to adapt. Government support ensures survival if not prosperity. The diversification initiatives might not transform the company but could offset some decline in traditional businesses.

For investors, Indian Oil represents a complex proposition. Value investors might find the discount attractive, especially given dividend yields. Growth investors will likely look elsewhere. ESG-focused funds might avoid oil exposure entirely. Income seekers could appreciate the steady dividends backed by government ownership. Risk-averse investors might worry about technology disruption. The investment case ultimately depends on individual time horizons, risk tolerance, and views on energy transition pace.

The key variables to watch are clear: pace of EV adoption in India, government policy on fuel pricing and subsidies, success of diversification initiatives, global oil price trends, and competitive dynamics in domestic markets. Small changes in these variables could dramatically alter Indian Oil's trajectory. The company's future remains unwritten, making it either an exciting opportunity or a value trap, depending on one's perspective.

XI. Epilogue: India's Energy Future

As dawn breaks over Indian Oil's Mathura refinery, the massive catalytic cracking towers stand silhouetted against the sky—monuments to an industrial age that may be ending. Yet a few kilometers away, at the company's newest fuel station, electric vehicle chargers stand ready beside traditional fuel pumps, solar panels glint on the canopy, and a hydrogen dispensing unit awaits commissioning. This juxtaposition—legacy and future, fossil and renewable, continuity and disruption—captures Indian Oil's existential moment.

The company's role in India's energy security narrative cannot be overstated. For seven decades, Indian Oil has been the reliable backbone of India's energy system. During the 1962 China war, Indian Oil ensured military fuel supplies despite infrastructure constraints. Through the 1991 Gulf War's oil shock, the company maintained domestic supply while prices spiked globally. During the 2020 pandemic lockdown, Indian Oil's workers risked infection to keep essential supplies flowing. This track record of reliability, built over decades, won't be easily replaced.

Yet the question haunting Indian Oil's boardroom is whether past performance predicts future relevance. Can a public sector undertaking, with its inherent constraints and legacy burdens, successfully navigate the clean energy transition? The challenge isn't just technological or financial—it's existential. Indian Oil must essentially disrupt itself, cannibalizing profitable businesses to build uncertain alternatives.

The global context provides mixed signals. International oil majors like Shell and BP proclaim transformation ambitions but continue generating most profits from hydrocarbons. National oil companies from Saudi Aramco to PetroChina double down on oil while making token renewable investments. Tesla's success suggests transportation's electric future, but Toyota's hybrid strategy indicates transition complexity. Indian Oil must chart its course through these contradictory signals.

The lessons for state-owned enterprises globally are profound. Indian Oil demonstrates both the potential and limitations of government ownership in strategic sectors. The company shows that state enterprises can achieve operational excellence, compete with private players, and serve social objectives simultaneously. But it also reveals the constraints: political interference, bureaucratic decision-making, and conflicting objectives that prevent optimization.

The balance between national interest and shareholder value remains Indian Oil's central tension. Promoter Holding: 51.5% means government control continues, but public shareholders demand returns. Energy security requires maintaining unprofitable infrastructure, but commercial viability needs focus on profitable segments. Social mandates necessitate serving all citizens, but competition requires customer selection. These tensions are irreconcilable—they must be managed, not solved.

What would different ownership look like? Full privatization might improve efficiency and profitability but could compromise energy security and social objectives. Foreign ownership might bring technology and capital but raise sovereignty concerns. Fragmentation into smaller companies might increase competition but lose scale advantages. The status quo isn't perfect, but alternatives aren't obviously superior.

Indian Oil's transformation challenge mirrors India's broader energy transition dilemma. The country must balance growth aspirations with climate commitments, energy security with import dependence, affordability with sustainability. Indian Oil, as the largest energy company, becomes the laboratory where these trade-offs play out. Its success or failure in managing transition will influence India's energy future and provide lessons for similar economies globally.

In August 2023, the company disclosed a $30bn investment plan aimed at achieving net zero operational emissions by 2046. This commitment, aligned with India's net-zero target, signals serious intent. But the path from announcement to achievement is treacherous. Technology must mature, economics must align, and politics must support. Indian Oil must maintain current operations generating cash while investing in alternatives that might never generate similar returns.

The human dimension often gets lost in strategic discussions. Indian Oil employs over 31,000 people directly, supports hundreds of thousands indirectly through dealers, distributors, and contractors. These aren't just statistics but families dependent on the company's success. The truck driver delivering diesel to remote villages, the engineer maintaining pipeline integrity, the scientist developing cleaner fuels—their futures intertwine with Indian Oil's transformation journey.

Indian Oil Corporation Ltd. (IOCL) reported a strong sequential improvement in its financial performance for the quarter ended March 31, 2025 (Q4FY25), with net profit rising sharply and operating mar... Recent performance shows resilience, but long-term trends remain concerning. The company generates cash, pays dividends, and maintains operations, but growth remains elusive. The market's skepticism, reflected in valuation discounts, suggests investors doubt transformation promises.

Looking ahead, several scenarios seem plausible. The optimistic case sees Indian Oil successfully transforming into an integrated energy company, leveraging infrastructure advantages to dominate new energy markets while managing traditional business decline. The pessimistic scenario envisions rapid demand destruction, stranded assets, and eventual government bailout or restructuring. The most likely outcome probably lies between—a gradual evolution with periods of crisis and recovery, transformation and retrenchment, progress and setback.

The story of Indian Oil Corporation is far from over. The company that emerged from post-colonial assertion of sovereignty, survived socialist-era constraints, adapted to liberalization's competition, and achieved global scale, now faces its greatest challenge. Whether Indian Oil becomes a case study in successful transformation or institutional inertia remains to be seen. What's certain is that India's energy future—and the welfare of billions—depends partly on how well this giant navigates the turbulent waters ahead.

As the sun sets over those Mathura refinery towers, they cast long shadows—perhaps symbolic of a fading era, or perhaps protective shade for new growth beneath. Indian Oil's next chapter is being written now, in boardrooms and research labs, at fuel stations and construction sites, in policy documents and investment decisions. The outcome matters not just for shareholders and employees but for India's energy security, economic development, and environmental future. The architect of India's energy independence must now redesign itself for an uncertain but inevitably different energy future.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube