Hindustan Petroleum Corporation Limited: From Colonial Roots to Energy Giant

I. Introduction & Cold Open

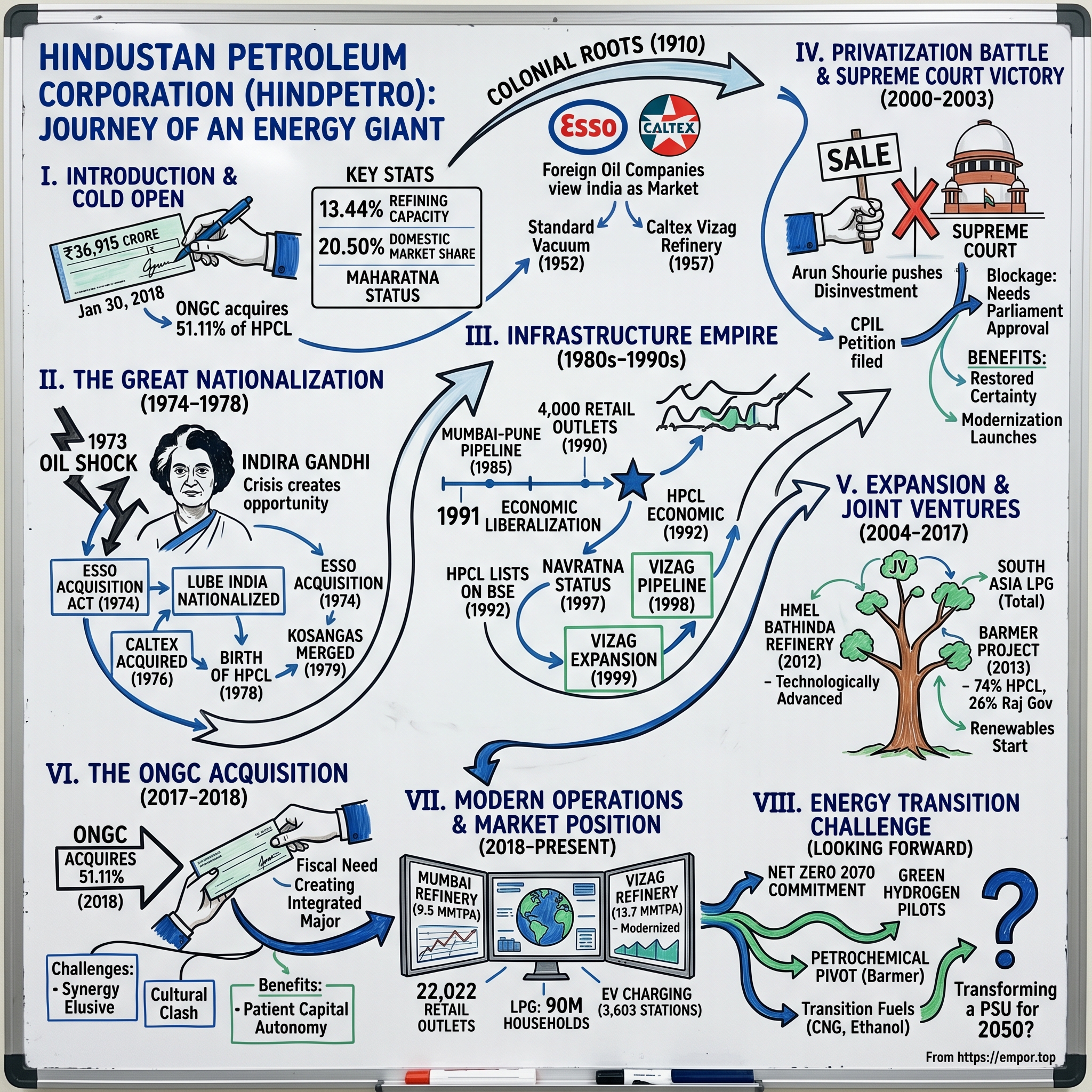

Picture this: It's January 30, 2018. In a nondescript conference room in New Delhi, officials from Oil and Natural Gas Corporation sign papers transferring ₹36,915 crore—one of the largest checks ever written by an Indian PSU. With that signature, ONGC acquires 51.11% of Hindustan Petroleum Corporation Limited, a company that started life as the Indian subsidiaries of American oil giants Esso and Caltex. The irony is delicious: foreign oil assets nationalized in the 1970s to assert India's sovereignty, now being passed between government entities like trading cards. But this isn't just bureaucratic shuffling—it's the culmination of a century-long saga of colonial exploitation, nationalist fervor, and the relentless pursuit of energy security.

Today, HPCL commands 13.44% of India's total refining capacity and holds 20.50% of the domestic petroleum products market. With its Maharatna status—the highest recognition for government enterprises—it operates with remarkable autonomy for a PSU. Yet beneath these impressive statistics lies a more complex story: How did a company assembled from the seized assets of foreign oil majors not just survive but thrive through nationalization, liberalization, and now the energy transition?

The questions multiply: Why did the Supreme Court intervene to block HPCL's privatization in 2003, setting a precedent that reverberates through India's disinvestment debates today? How did a refiner with no upstream assets convince markets it could compete with integrated giants like Reliance? And perhaps most intriguingly—in an era where every oil company claims to be pivoting to clean energy, can a 1970s-era PSU truly transform itself for India's net-zero future?

This is not just the story of pipelines and refineries. It's a tale of how India wrestled control of its energy destiny from colonial powers, built industrial champions through state capitalism, and now faces the ultimate test: navigating the twilight of the oil age. Along the way, we'll encounter midnight nationalizations, Supreme Court showdowns, and billion-dollar acquisitions that reshape India's energy landscape.

What you're about to read isn't just corporate history—it's the story of how a nation's anxieties about energy independence shaped one of its most important companies. And as global oil markets gyrate and electric vehicles proliferate, HPCL's next chapter may be its most challenging yet.

II. Colonial Origins & The Foreign Oil Era (1910-1974)

The year is 1910. British India's first automobiles are puttering through the streets of Bombay and Calcutta, and kerosene lamps light the homes of the emerging middle class. Into this nascent market steps what would eventually become part of HPCL—though nobody could have imagined the circuitous path ahead. The company's deepest roots trace back to this pre-independence era, when foreign oil companies saw India not as a nation but as a market to be exploited.

Fast forward to July 5, 1952—five years after independence, but the economic architecture of colonialism remains largely intact. Standard Vacuum Refining Company of India Limited is incorporated, a subsidiary of the American oil giant that would later become ExxonMobil. The timing is no accident: India's first Five Year Plan has just launched, industrialization is accelerating, and demand for petroleum products is set to explode. Standard Vacuum's executives in New York see opportunity in this newly independent nation still finding its economic feet.

By 1957, another American giant makes its move. Caltex—the joint venture between Chevron and Texaco—commissions a 0.65 million metric tons per annum fuel refinery in Visakhapatnam. The location is strategic: Vizag, as locals call it, offers a deep natural harbor on India's east coast, perfect for receiving crude tankers from the Middle East. The refinery rises from the coastal plains like an industrial cathedral, its distillation columns and catalytic crackers representing the cutting edge of 1950s petroleum technology.

The Americans aren't just building refineries; they're creating an entire ecosystem of dependence. In 1962, Standard Vacuum restructures, and its Indian operations become ESSO Standard Refining Company of India Limited—a name that would soon grace petrol pumps across the subcontinent. ESSO's red oval logo becomes as familiar to Indian motorists as the Ambassador car itself. Meanwhile, in 1969, Lube India Limited—another foreign-controlled entity—commissions a 165,000 tons per annum lubricants refinery in Mumbai. This isn't just about motor oil; industrial lubricants are the lifeblood of India's growing manufacturing sector.

But beneath this industrial expansion, tensions simmer. Indian politicians and bureaucrats watch with growing unease as foreign companies control the commanding heights of the energy sector—the very fuel that powers industrialization. Every barrel refined, every liter sold at the pump, generates profits that flow back to Houston and New York. The foreign oil companies operate with a colonial mindset: India is a market, not a partner. Technology transfer is minimal, senior management remains expatriate-dominated, and strategic decisions are made in boardrooms thousands of miles away.

By the early 1970s, these foreign oil companies control nearly 85% of India's refining capacity and petroleum product marketing. They operate as a oligopoly, coordinating prices and dividing territories with the efficiency of a cartel. Indian consumers have no choice but to buy from ESSO, Caltex, or Burmah Shell. The irony is bitter: a nation that fought for political independence remains economically shackled to foreign oil.

The stage is set for confrontation. India's political climate is shifting leftward, economic nationalism is rising, and a certain Prime Minister named Indira Gandhi is about to make a move that will transform these foreign oil assets into national champions. The companies that entered India to exploit a colonial market are about to discover that the rules of the game have fundamentally changed.

So what for investors: The foreign oil era established critical infrastructure and technical capabilities that would become HPCL's foundation. Understanding this colonial legacy helps explain both the company's inherent strengths (prime refinery locations, established distribution networks) and its historical weaknesses (technology dependence, bureaucratic culture).

III. The Great Nationalization: Birth of HPCL (1974-1978)

October 1973. Tel Aviv. Egyptian and Syrian forces launch a surprise attack on Israel during Yom Kippur. Within days, a regional conflict transforms into a global economic crisis. Arab oil producers embargo nations supporting Israel, and crude prices quadruple from $3 to $12 per barrel. In New Delhi, the impact is immediate and devastating. India imports 70% of its oil, and the foreign exchange reserves can't handle the shock. Inflation soars to 20%. The government implements drastic measures: Sunday driving bans, early shop closures to save electricity, even a brief experiment with daylight saving time.

But for Indira Gandhi, crisis presents opportunity. Her advisors at the Planning Commission have long advocated for nationalizing the oil sector. The oil shock provides perfect political cover. "Why should foreign companies profit from India's misery?" becomes the rallying cry. The business press speculates, opposition parties debate, but Gandhi's inner circle maintains strategic silence. They're planning something bigger than anyone imagines.

January 24, 1974. Parliament is in session when the announcement comes: the government will acquire ESSO's Indian operations through the ESSO (Acquisition of Undertakings in India) Act. The legislation is already drafted, the votes secured. ESSO's American executives in Mumbai wake up to discover they no longer own their refineries. There's no negotiation, no gradual transition—just swift, decisive action. The compensation formula is set by the government: book value of assets, nothing more. ESSO's lawyers scramble, but the writing is on the wall. This is sovereignty in action.

The same act simultaneously nationalizes Lube India Limited. Overnight, India gains control of the country's primary lubricants manufacturing capacity. The strategic logic is impeccable: control the lubricants, control the machinery of industrialization. Every factory, every truck, every piece of heavy equipment depends on these products.

But acquiring assets is easier than running them. The newly nationalized entities need leadership, and Gandhi turns to an unlikely source: the Indian Administrative Service. IAS officers—trained as generalist administrators, not oil industry experts—suddenly find themselves managing refineries. The early days are chaotic. American technicians depart with little handover. Operating manuals are in English, but the critical tribal knowledge—which valve to turn when pressures spike, how to detect problems before they cascade—walks out the door.

At the Mumbai refinery, Indian engineers work 18-hour shifts to keep operations running. They reverse-engineer processes, decode computer systems (still mainframes in those days), and slowly master the complex alchemy of turning crude into products. It's industrial archaeology in real-time, uncovering the secrets the foreigners never meant to share.

1976 brings the second wave. The government acquires Caltex Oil Refining (India) Limited. This time, they're better prepared. Teams of Indian engineers have spent months shadowing operations, documenting processes, preparing for the transition. When the hammer falls, the handover is smoother, though Caltex's American management still protests futilely to the State Department.

The masterpiece of organizational architecture comes in 1978 when these disparate entities merge into Hindustan Petroleum Corporation Limited. The name itself is a statement: "Hindustan"—the ancient name for India, asserting cultural ownership over industrial assets. The merger isn't just administrative; it's about creating a unified corporate culture from fragments of foreign companies. ESSO's Mumbai refinery, Caltex's Vizag operations, and Lube India's facilities must now function as one entity.

1979 adds a final piece: Kosangas Company, a small but strategic LPG player, is acquired through the Kosangas Company Acquisition Act and merged with HPCL. This gives the new entity a foothold in the rapidly growing cooking gas market—crucial for a government promoting LPG as a cleaner alternative to wood and kerosene.

The transformation is remarkable. In less than five years, foreign oil assets representing billions in investment have been welded into a national champion. But challenges mount immediately. The company inherits aging equipment—some dating to the 1950s—that needs urgent modernization. The workforce, while technically competent, lacks exposure to global best practices. Most critically, HPCL must now serve two masters: operating as a commercial entity while fulfilling the government's social objectives of ensuring energy access to all Indians.

By 1980, HPCL has expanded Mumbai refinery capacity to 5.5 million metric tons per annum and Vizag refinery to 4.5 MMTPA. These aren't just numbers—they represent India's newfound ability to process crude oil on its own terms, setting its own prices, serving its own priorities. The foreign oil era is definitively over.

So what for investors: Nationalization created HPCL's unique competitive position—strategic assets acquired at book value, not market prices. But it also embedded cultural DNA that persists today: a public service mentality that can conflict with profit maximization, and a complex relationship with government that provides both protection and constraints.

IV. Building the Infrastructure Empire (1980s-1990s)

August 15, 1985. Independence Day. As India celebrates 38 years of freedom, HPCL quietly commissions what will become one of its most strategic assets: the Mumbai-Pune pipeline. This 168-kilometer artery doesn't just connect two cities; it links India's commercial capital with its emerging IT and manufacturing hub. The pipeline can move products at 20% the cost of road transport, transforming the economics of fuel distribution across Maharashtra. For the first time, an Indian company—not a foreign corporation—controls this critical infrastructure.

The pipeline's construction tells a larger story about HPCL's evolution. The company must navigate land acquisition across two states, negotiate with hundreds of farmers, manage environmental clearances, and master technologies previously monopolized by foreign engineering firms. Indian engineers, many trained at IITs but with no pipeline experience, learn by doing. They make mistakes—a section near Khandala has to be re-laid after monsoon damage—but each error builds institutional knowledge that can't be bought or imported.

The retail network expansion during this period resembles a military campaign. HPCL identifies strategic locations along the Golden Quadrilateral highway project, anticipating where India's economic growth will concentrate. By 1990, the company operates 4,000 retail outlets—each one a small fortress in the war for market share. But these aren't just fuel stations; they're becoming convenience stores, truck stops, and community centers. In rural Karnataka, an HPCL outlet might be the only place for miles with clean restrooms and safe drinking water.

Then comes 1991. India's foreign exchange reserves drop to barely three weeks of imports. The government airlifts gold to London as collateral for emergency loans. Prime Minister Narasimha Rao and Finance Minister Manmohan Singh unleash reforms that will transform India's economy—and HPCL must transform with it. The License Raj crumbles, foreign investment floods in, and suddenly HPCL faces a terrifying prospect: competition.

The company's response is counterintuitive but brilliant. On January 19, 1992, HPCL becomes the first public sector enterprise to list on the Bombay Stock Exchange. The initial public offering is modest—only 49% of equity—but the signal is revolutionary. A government company submitting to market discipline, publishing quarterly results, answering to shareholders beyond just the petroleum ministry. The IPO is oversubscribed 3.8 times, validating HPCL's strategy.

Listing brings unexpected benefits. Suddenly, HPCL can access capital markets for expansion without begging the finance ministry. Stock options can attract talent that might otherwise join Reliance or the emerging IT sector. Most importantly, market pressure forces operational improvements that decades of government oversight never achieved. Inventory turns accelerate, working capital management tightens, and return on capital employed becomes a boardroom obsession.

1996 sees another milestone: listing on the National Stock Exchange. HPCL is no longer just a PSU; it's becoming a blue-chip stock that mutual funds and foreign institutional investors can own. The company's ADRs trade in London and New York, putting it on the radar of global energy investors.

The Navratna status conferred in 1997 is more than ceremonial. It grants HPCL's board unprecedented autonomy: the ability to make capital investments up to ₹1,000 crore without government approval, enter joint ventures, raise debt independently. For a company that once needed ministry permission to buy typewriters, this is revolutionary freedom.

The Visakhapatnam-Vijayawada pipeline, commissioned in 1998, showcases this new operational freedom. The 198-kilometer pipeline opens up Andhra Pradesh's interior, but more importantly, it's financed through internal accruals and market borrowings—no government budgetary support needed. HPCL is becoming financially self-sufficient, a remarkable transformation for an entity born from nationalization.

By 1999, the Vizag refinery expands to 7.5 million metric tons per annum capacity. This isn't just about processing more crude; it's about processing more complex, cheaper grades. The refinery adds a catalytic cracker, allowing it to convert heavy fuel oil into high-value gasoline and diesel. The economics are compelling: every percentage point improvement in light product yield adds ₹100 crore to annual profits.

But the real achievement of this era isn't visible in pipelines or refineries—it's in corporate culture. HPCL develops a unique identity: more entrepreneurial than typical PSUs, more socially conscious than private competitors. Engineers take pride in keeping remote hill stations supplied during monsoons. Marketing managers innovate with rural distribution models that multinational consultants later study as case studies. The company develops an esprit de corps: "HPCLites," as employees call themselves, see themselves as nation-builders, not just oil workers.

The 1990s close with HPCL positioned remarkably: extensive infrastructure built with patient capital, a retail network rivaling any competitor, and financial independence from government budgets. But storm clouds gather. The Vajpayee government talks of privatization, Reliance is building the world's largest refinery complex at Jamnagar, and global oil majors eye India's deregulated market hungrily. The infrastructure empire is built, but can it survive the coming onslaught?

So what for investors: The 1980s-1990s established HPCL's competitive moats: pipeline networks and retail locations that would cost tens of billions to replicate today. Early capital market access created financial discipline unusual for PSUs. However, this period also locked in capital allocation patterns—prioritizing network expansion over refinery complexity—that would later limit margins versus more sophisticated competitors.

V. The Privatization Battle & Supreme Court Victory (2000-2003)

March 2002. Arun Shourie, the journalist-turned-disinvestment minister, strides into a press conference with characteristic confidence. "The government will divest its stake in HPCL and BPCL," he announces. "These companies need private sector efficiency to compete globally." The business press erupts. Foreign oil majors—Shell, BP, Total—immediately begin assembling bid teams. Investment bankers smell the deal of the decade: two Navratna oil companies, thousands of petrol pumps, strategic refineries—all potentially up for sale.

But Shourie underestimates the opposition. Within days, the Centre for Public Interest Litigation files a petition in the Delhi High Court. The petitioners make a fascinating argument: HPCL and BPCL weren't created through executive action but through acts of Parliament—the ESSO Acquisition Act and Burmah Shell Acquisition Act. To undo what Parliament created, you need Parliament's explicit approval. It's a constitutional chess move that catches the government off-guard.

The legal team is formidable: Rajinder Sachar, former Chief Justice of Delhi High Court, and a young firebrand lawyer named Prashant Bhushan. They argue this isn't just about two oil companies—it's about whether the executive can bypass Parliament to reverse decisions of national importance. The petroleum ministry, caught between political masters pushing privatization and bureaucrats defending their turf, maintains studied neutrality.

Inside HPCL, the mood is surreal. Senior executives continue expansion plans while knowing they might soon report to Shell or BP. The stock price gyrates wildly on every rumor. Employees unions mobilize—15,000 workers threaten indefinite strikes. But the most interesting resistance comes from an unexpected quarter: HPCL's retail dealers. These aren't employees but small businessmen who've invested crores in outlets. They fear foreign owners will squeeze margins or worse, terminate dealerships to create company-owned stations.

September 2003. The Supreme Court hearing begins. The government's attorney general argues that economic reform requires flexibility, that Parliament's approval for every disinvestment would paralyze the process. But the petitioners counter brilliantly: if the government can privatize HPCL without Parliament, what stops it from privatizing Railways, Defense establishments, or any public asset? It's not about economics but constitutional process.

The Court's questions reveal their thinking. "If Parliament specifically legislated to acquire these companies in national interest, shouldn't Parliament decide if that national interest has changed?" asks one judge. Another observes: "The government argues efficiency, but HPCL is profitable, pays dividends, and serves remote areas private companies might abandon. Where is the urgent need that justifies bypassing Parliament?"

The verdict, when it comes, is devastating for the government's privatization agenda. The Supreme Court rules that HPCL and BPCL cannot be privatized without Parliament's explicit approval through legislative amendment. The judgment notes that these companies were acquired through specific legislation reflecting Parliament's will, and executive action cannot override legislative intent.

The implications ripple far beyond HPCL. The ruling essentially requires the government to command majorities in both Lok Sabha and Rajya Sabha to privatize any entity created through legislation. In India's coalition politics, where the ruling party rarely controls the Rajya Sabha, this is an almost insurmountable barrier. The judgment becomes a shield for public sector enterprises across India.

For HPCL, the victory brings unexpected benefits. The privatization threat had frozen major decisions for two years—why invest in upgrades if new owners might have different plans? Now, with ownership certainty restored, the company unleashes pent-up initiatives. A ₹5,000 crore refinery modernization program launches immediately. Plans for new pipelines, dormant during the uncertainty, receive board approval.

The stock market's reaction is intriguing. Conventional wisdom suggested private ownership would unlock value, but HPCL shares actually rise 15% in the month after the verdict. Analysts realize that HPCL keeping its PSU status means continued access to government support, regulatory forbearance, and a protected market position—valuable in India's political economy.

But the most profound impact is psychological. HPCL employees and management, who spent three years in existential uncertainty, emerge with renewed purpose. The company wasn't saved by government decree but by constitutional process and public interest litigation. This creates a unique sense of legitimacy and responsibility. Internal surveys show employee engagement scores jumping 30% post-verdict.

The failed privatization also triggers introspection. If HPCL remains in public hands, how can it compete with private rivals? The answer comes through selective partnerships—joint ventures that bring technology and capital without surrendering control. The company begins exploring collaborations with Mittal Energy for a new refinery, with Total for lubricants, with multiple players for city gas distribution. It's privatization by stealth: accessing private sector capabilities while maintaining public sector control.

So what for investors: The 2003 Supreme Court verdict created a permanent floor under HPCL's valuation—the company cannot be privatized without extraordinary political consensus. This provides stability but also removes the takeover premium that often drives PSU valuations. The verdict also explains HPCL's joint venture strategy: unable to be acquired, it must partner to access capabilities.

VI. Expansion & Joint Ventures Era (2004-2017)

December 2007. Visakhapatnam. Two hundred feet below ground, engineers complete India's first commercial LPG cavern—a 60,000 metric ton underground storage facility carved from solid rock. The technology, borrowed from South Korea but adapted for Indian conditions, solves a critical problem: how to store volatile LPG safely in a cyclone-prone coastal area. The cavern, built through South Asia LPG Company (a joint venture between HPCL and Total), represents a new model—accessing foreign technology through partnerships rather than dependence.

But the real jewel in HPCL's joint venture crown is taking shape 2,000 kilometers away in Punjab's Bathinda district. The story begins in 2005 when Lakshmi Mittal, the steel magnate, approaches the Indian government with an audacious proposal: build a grassroots refinery to process heavy crude from Latin America. Mittal needs a local partner with refining expertise and distribution networks. HPCL, fresh from its privatization victory and hungry for growth, sees opportunity.

The Guru Gobind Singh Refinery—operated by HPCL-Mittal Energy Limited (HMEL)—commissioned in 2012, is a technological marvel. At 9 million metric tons per annum capacity, it's India's first refinery designed from scratch to process ultra-heavy crude. The economics are compelling: heavy crude trades at a $15-20 per barrel discount to light sweet crude, but with sophisticated processing, yields similar products. Every dollar of discount translates to ₹450 crore in annual margin.

The refinery's configuration reads like an engineer's dream: delayed coker unit, hydrocracker, diesel hydrotreater, continuous catalytic reformer. This isn't just oil refining; it's molecular transformation, breaking heavy hydrocarbons into high-value products. The plant achieves 88% distillate yield—meaning almost 9 of every 10 liters of crude becomes gasoline, diesel, or aviation fuel rather than low-value fuel oil.

HMEL also pioneers environmental standards. It's India's first refinery to produce only BS-VI (equivalent to Euro-VI) fuels from day one, anticipating emission norms by years. The sulfur content in its diesel is below 10 parts per million—cleaner than what most European refineries produced then. This forward-thinking approach positions HPCL advantageously when India leapfrogs from BS-IV to BS-VI standards in 2020.

The joint venture's success triggers a strategic shift at HPCL. Rather than going alone on mega-projects, the company systematically identifies partners bringing specific capabilities. In city gas distribution—a sector requiring massive capital and local expertise—HPCL forms region-specific joint ventures. In Bengaluru with GAIL, in Mumbai with Mahanagar Gas, in other cities with local players who understand municipal politics and consumer behavior.

The renewable energy push begins modestly but strategically. In 2014, HPCL installs a 5 MW wind farm in Rajasthan—tiny by global standards but significant symbolically. The company isn't abandoning oil; it's hedging its bets. Solar panels appear on retail outlet roofs, initially to reduce electricity costs but later as a customer amenity—charging stations for phones and laptops while vehicles refuel.

But the most ambitious project is brewing in Rajasthan's Barmer district. In 2013, HPCL announces a ₹43,129 crore refinery project with an unusual structure: 74% HPCL stake, 26% Rajasthan government. This isn't charity—Barmer sits atop India's largest onshore oil discovery, and a local refinery can process this waxy, acidic crude that coastal refineries can't handle economically. The configuration includes a petrochemical complex, recognizing that the real money in oil refining increasingly comes from chemicals, not transport fuels.

The Barmer project showcases HPCL's evolved capabilities. The company manages everything: land acquisition (4,700 acres in water-scarce desert), technology selection (licensing from global leaders like UOP and Axens), financing (a complex mix of internal accruals, debt, and government support), and critically, stakeholder management in a politically sensitive border state.

By 2015, HPCL's joint venture portfolio reads like a who's who of global energy: Total for lubricants, Mittal for refining, multiple partners for gas distribution, technology licenses from everyone from Shell to Chevron. The company has quietly assembled capabilities that would have taken decades to develop independently.

The retail network continues expanding but with a twist. New outlets aren't just fuel stations but "energy stations"—offering CNG, eventually electric charging, and even battery swapping for two-wheelers. The company experiments with non-fuel retail, turning highway outlets into food courts and convenience stores. Some locations generate more profit from selling coffee than diesel—a shocking transformation for an oil company.

This era also sees HPCL's digital transformation. The company launches a mobile app for LPG booking—mundane perhaps, but revolutionary for millions of households previously dependent on phone bookings or dealer visits. Digital payment systems eliminate cash handling at retail outlets, reducing pilferage and improving working capital. The company even experiments with drone delivery of LPG cylinders in remote Himalayan villages—more publicity stunt than commercial success, but signaling technological ambition.

By 2017, HPCL has transformed from a simple refiner-marketer into an energy conglomerate. The joint venture strategy has added 9 million tons of refining capacity without full capital burden, entered new sectors like gas and petrochemicals, and most critically, created options for an uncertain energy future. The company that couldn't be privatized has effectively privatized parts of itself through partnerships.

So what for investors: The JV strategy leveraged HPCL's distribution strength while accessing technology and capital. HMEL particularly showcases value creation—HPCL's share of profits often exceeds ₹1,000 crore annually on a ₹3,000 crore investment. However, complex JV structures also create governance challenges and limit management control over key assets.

VII. The ONGC Acquisition: Creating an Oil Major (2017-2018)

July 19, 2017. The Cabinet Committee on Economic Affairs meets in a special session. The agenda item seems routine—"Strategic Restructuring of Oil PSUs"—but the decision will reshape India's energy landscape. Finance Minister Arun Jaitley presents the proposal: ONGC will acquire the government's 51.11% stake in HPCL for approximately ₹37,000 crore. The room falls silent. This isn't privatization—it's PSU-to-PSU transfer, a uniquely Indian solution to creating an integrated oil major.

The logic appears compelling on paper. ONGC produces 35 million tons of crude annually but lacks refining capacity. HPCL refines 23 million tons but has no upstream assets. Merge them, and you create India's first truly integrated oil company—exploration to retail—with $100 billion in revenue. Officials invoke international comparisons: ExxonMobil, Shell, BP all combine upstream and downstream. Why shouldn't India have its own oil major?

But beneath the strategic rhetoric lies fiscal desperation. The government needs money—lots of it. GST implementation has disrupted revenues, bank recapitalization demands resources, and fiscal deficit targets loom. Selling HPCL to ONGC brings immediate cash without the political cost of privatization. It's financial engineering disguised as strategic restructuring.

ONGC's board meeting on January 19, 2018, is tense. Independent directors question the price—₹473.97 per share, a 14% premium to market price. Is HPCL worth it? The government nominees argue yes: HPCL's refineries, 25,000 retail outlets, and pipeline network would cost twice as much to build. Critics counter that ONGC is a deep-water drilling specialist—what does it know about retail marketing?

The funding structure reveals the deal's complexity. ONGC borrows ₹24,000 crore from banks, deploys ₹13,000 crore from cash reserves. The debt burden immediately impacts ONGC's balance sheet—debt-to-equity ratio jumps from 0.2 to 0.35. Rating agencies place ONGC on watch. The market's verdict is swift: ONGC shares fall 15% in six months while HPCL rises 20%. Investors see HPCL getting a rich parent while ONGC suffers indigestion from an expensive acquisition.

Inside HPCL, reactions are mixed. Senior management sees opportunity—access to ONGC's crude could improve refining margins, upstream cash flows could fund downstream expansion. But middle management worries about cultural clash. ONGC is an explorer's company—geologists and drilling engineers dominate. HPCL is a marketer's company—focused on consumers and competition. These cultures don't naturally mesh.

The integration challenges emerge immediately. ONGC wants HPCL to process its crude, but HPCL's refineries are configured for Middle Eastern grades, not ONGC's waxy Bombay High crude. Modification would cost billions and take years. ONGC expects immediate synergies—shared services, combined procurement, integrated planning. But HPCL operates under its own board, maintains separate listed status, and resists being treated as a subsidiary.

The promised synergies prove elusive. A joint committee identifies ₹4,700 crore in annual benefits—crude sourcing optimization, logistics sharing, combined technology development. But execution stalls on everything from IT system integration to organizational structure. Two years post-acquisition, realized synergies are below ₹500 crore annually—a 10% achievement rate.

January 30, 2018—the day ONGC formally acquires HPCL—marks a curious milestone. It's India's largest acquisition, but there's no celebration, no grand integration plan unveiled. Both companies continue operating independently, connected more by ownership documents than operational integration. The stock market notices: the anticipated "oil major premium" never materializes.

But something unexpected happens. HPCL's operational performance actually improves post-acquisition. Freed from constant government interference—ONGC acts as a buffer—management focuses on operations. Refinery utilization rates hit 106%, marketing margins expand, and return on capital employed reaches 15%. The acquisition paradoxically gives HPCL more autonomy than it had as a direct government entity.

October 24, 2019, brings validation of sorts: HPCL achieves Maharatna status, joining India's most elite PSUs. This grants unprecedented operational freedom—₹5,000 crore investment authority, ability to float subsidiaries, strategic alliance flexibility. The company that was almost privatized, then acquired by another PSU, now operates with more independence than ever.

The ONGC-HPCL combination also creates strategic options previously impossible. When global crude prices crash in 2020, ONGC's upstream losses are partially offset by HPCL's downstream gains—the natural hedge that integrated oil companies enjoy. During refining margin squeezes, ONGC's cash supports HPCL's working capital needs. It's not the tight integration originally envisioned, but it provides stability in volatile markets.

By 2023, ONGC has increased its stake to 54.90%, cementing control. The relationship has evolved into something uniquely Indian: not quite a merger, more than just shareholding, a confederation of energy assets that compete and collaborate simultaneously. HPCL maintains its brand, culture, and operational independence while benefiting from ONGC's balance sheet and political clout.

So what for investors: The ONGC acquisition provides HPCL with patient capital and political protection but hasn't delivered promised operational synergies. The 14% acquisition premium set a valuation floor, while Maharatna status ensures operational autonomy. The structure—listed subsidiary of a listed parent—creates unique governance dynamics that can both protect and constrain minority shareholders.

VIII. Modern Operations & Market Position (2018-Present)

March 2023. At HPCL's integrated command center in Mumbai, screens display real-time data from across India: refinery run rates, pipeline pressures, retail outlet sales, even traffic patterns near key highways. An AI algorithm suddenly flags an anomaly—diesel sales spiking 40% along the Delhi-Jaipur highway. Within minutes, analysts trace it to a major infrastructure project requiring additional tanker deliveries. Supply chain managers reroute products from the Mathura depot. What once took days of phone calls now happens in minutes through digital orchestration.

This command center symbolizes HPCL's transformation. The Mumbai refinery, expanded to 9.5 million tons annually, doesn't just process crude—it optimizes molecular transformation in real-time. Advanced process control systems adjust parameters every few seconds, squeezing extra margins from every barrel. The refinery achieves 99.7% operational availability—world-class by any standard—while processing increasingly complex crude slates.

The Visakhapatnam refinery tells an even more impressive story. At 13.7 million tons capacity, it's become HPCL's crown jewel. The recent ₹21,000 crore modernization hasn't just expanded capacity but transformed configuration. A new hydrocracker produces ultra-low sulfur diesel, a continuous catalytic reformer maximizes gasoline octane, and a propylene recovery unit feeds the emerging petrochemical business. The refinery's Nelson Complexity Index—a measure of sophistication—has jumped from 6.8 to 8.7, approaching global best-in-class levels.

But physical assets tell only part of the story. HPCL's retail network—22,022 outlets as of March 2024—has become a digital ecosystem. The company's mobile app serves 80 million customers, processing everything from fuel payments to LPG bookings. At premium outlets, customers pre-order fuel while driving, arriving to find attendants ready with exact quantities. It's convenience retail disguised as oil marketing.

The LPG business showcases similar evolution. HPCL's 6,349 distributors and 56 bottling plants serve 90 million households—nearly every third Indian family cooks with HPCL gas. But the real innovation happens in last-mile delivery. In urban areas, customers track cylinder delivery like pizza orders. In remote regions, the company experiments with composite cylinders—lighter, safer, easier to transport to mountain villages or island communities.

Aviation fuel presents different challenges and opportunities. HPCL operates at 55 airports, competing fiercely with Indian Oil and Bharat Petroleum for airline contracts. The business runs on razor-thin margins but massive volumes—every international flight might consume 100,000 liters. HPCL wins contracts through operational excellence: faster refueling turnarounds, fewer quality complaints, innovative credit terms that help cash-strapped airlines.

The electric vehicle revolution, rather than threatening HPCL, has become an opportunity. The company operates 3,603 EV charging stations—India's second-largest network. But HPCL isn't just installing chargers; it's reimagining the energy station. New outlets combine petrol pumps, CNG dispensers, EV chargers, battery swapping stations, and even hydrogen fuel cells (in pilot projects). It's betting that the future isn't electric versus fossil but multiple energy sources coexisting.

The renewable energy pivot accelerates. HPCL commits to 5,000 MW of renewable capacity by 2040—ambitious for an oil company. Solar panels cover refineries, wind farms power pipelines, and the company explores green hydrogen production. At the Visakhapatnam refinery, a pilot project produces hydrogen through electrolysis powered by solar energy. It's expensive today but could become competitive as carbon pricing evolves.

Lubricants remain a hidden gem. HPCL operates India's largest lube refinery, producing 428,000 tons annually of products ranging from motorcycle oil to industrial greases. The business generates 15% EBITDA margins—double that of fuel marketing. HPCL's "HP Racer" brand dominates motorcycle racing circuits, creating brand pull among young consumers. Industrial lubricants serve everything from steel plants to wind turbines, providing steady, high-margin revenues.

The cross-country pipeline network—India's second-largest—has become a competitive advantage. HPCL operates 5,100 kilometers of pipelines, moving products at one-fifth the cost of road transport. The newest addition, the 443-kilometer Vijayawada-Dharmapuri pipeline, opens up South India's interior markets. Smart sensors detect leaks within minutes, automated valves prevent disasters, and optimization algorithms minimize pumping costs.

Financial performance reflects operational excellence. Revenue reaches ₹4.5 lakh crore in FY2023, though this inflates with oil prices. More importantly, EBITDA margins stabilize around 3-4%—respectable for a predominantly marketing company. Return on capital employed consistently exceeds 15%, beating most PSU peers. The company generates ₹5,000-7,000 crore in annual free cash flow, funding both growth investments and generous dividends.

But challenges persist. Private sector competition intensifies—Reliance and Nayara (formerly Essar) operate with fewer constraints. Global oil majors eye India's growing market. The energy transition threatens long-term demand. Margin volatility remains severe—a $1 change in crack spreads impacts annual profits by ₹500 crore. Government interference, while reduced, hasn't disappeared—fuel prices remain politically sensitive.

Yet HPCL in 2024 stands remarkably transformed from its nationalization origins. It's simultaneously an oil refiner, fuel marketer, digital platform, renewable energy developer, and logistics company. The company processes 40,000 barrels of crude daily, serves 10 million customers, and employs 10,000 people directly while supporting 100,000 jobs across its ecosystem. It's not just surviving the energy transition—it's attempting to lead it.

So what for investors: Modern HPCL offers exposure to India's energy consumption growth with improving operational metrics. The company's infrastructure—impossible to replicate—provides a competitive moat. Digital initiatives improve margins while renewable investments hedge transition risks. However, significant capital allocation toward energy transition projects carries execution risk and uncertain returns.

IX. Playbook: Strategic Lessons

Surviving Nationalization and Thriving Under Government Ownership

The conventional wisdom says government ownership breeds inefficiency, but HPCL's story suggests nuance. The key was maintaining operational autonomy within political ownership. When petroleum secretaries resisted micromanaging daily operations, when boards included industry experts not just bureaucrats, when performance metrics focused on commercial returns not just social objectives—the company thrived. The lesson: ownership structure matters less than governance quality.

Consider HPCL's response to the 2008 fuel subsidy crisis. The government mandated selling diesel below cost, creating massive under-recoveries. Rather than simply demanding compensation, HPCL's management innovated—hedging crude purchases, optimizing product mix toward unregulated products, expanding non-fuel revenues. They turned political constraints into operational discipline. When subsidies finally ended, HPCL emerged leaner than competitors who'd grown complacent on government support.

The Art of Political Navigation in a PSU

Every HPCL CEO masters a delicate dance: serving political masters while protecting commercial interests. The successful ones understand that ministers want visible achievements—new refineries in their states, retail outlets in their constituencies, CSR projects that generate positive headlines. Smart CEOs bundle these political necessities with commercial projects. That refinery in a minister's home state? It happens to sit near newly discovered oil fields. Those rural retail outlets? They're testing ground for innovation before urban rollout.

The company also learned to use its PSU status strategically. When competing for aviation fuel contracts, HPCL emphasizes reliability—"We're government-backed, we won't default." When negotiating with state governments for land, they invoke national interest. When facing environmental activists, they highlight renewable investments. It's shape-shifting corporate identity, adapted to each stakeholder's concerns.

Building Scale Through Patient Capital Allocation

Private companies operate on quarterly earnings cycles; HPCL thinks in decades. The Mumbai-Pune pipeline took five years to build and seven more to reach full capacity—no private player would have waited. The Barmer refinery will take eight years from conception to commissioning—impossible for companies facing activist investors. This patient capital creates competitive advantages: infrastructure that generates returns for generations, market positions that competitors can't quickly erode.

But patience doesn't mean passivity. HPCL learned to sequence investments strategically. First, build refining capacity to ensure supply. Second, create distribution infrastructure to reach markets. Third, establish retail presence to capture margins. Finally, integrate backwards into petrochemicals and forwards into renewable energy. Each stage funds the next, creating self-reinforcing growth.

Managing Upstream-Downstream Integration Post-ONGC

The ONGC acquisition could have been a disaster—forced marriage between incompatible cultures. Instead, HPCL turned it into selective collaboration. Where integration makes sense—crude sourcing, technology sharing, financial support—the companies cooperate. Where it doesn't—retail operations, refinery configuration, organizational structure—they maintain independence.

The key insight: integration value comes from optionality, not uniformity. When crude prices spike, HPCL can access ONGC's production at cost. When refining margins compress, ONGC's cash cushions the blow. During stable periods, both companies optimize independently. It's portfolio theory applied to corporate structure—diversification benefits without operational complexity.

Competing with Private Players While Being Government-Owned

Reliance operates with entrepreneurial aggression, making bold bets on massive refineries and retail disruption. HPCL can't match that—government ownership brings scrutiny, procedures, and political considerations. Instead, HPCL competes through resilience and reach. When Reliance focuses on urban markets, HPCL dominates rural distribution. When private players chase premium customers, HPCL serves everyone.

The company also leverages its PSU status for competitive advantage. Government contracts default to PSUs. Defense establishments buy from HPCL. Public sector banks provide cheaper financing. State governments facilitate land acquisition. These aren't unfair advantages—they're compensation for serving non-commercial objectives like maintaining supplies to remote areas that private players abandon.

The Renewable Energy Pivot: Too Late or Just in Time?

Critics argue HPCL is late to renewables—global oil majors started pivoting a decade ago. But India's energy transition will differ from Europe's. Fossil fuel demand will grow until at least 2040. Electric vehicles will penetrate slowly given infrastructure constraints. Industrial processes will need oil products for decades. HPCL's measured approach—maintaining oil cash flows while building renewable options—might prove optimal for India's context.

The company's renewable strategy also leverages existing assets creatively. Refineries become sites for green hydrogen production. Retail outlets host EV chargers. Pipeline corridors accommodate solar panels. LPG distribution networks could eventually handle bio-gas. It's transformation through adaptation, not abandonment of legacy assets.

Capital Allocation in a Cyclical Commodity Business

Oil refining is viciously cyclical—margins can swing from $15 to $2 per barrel within months. HPCL learned to separate operational cash flow from investment planning. During margin booms, the company doesn't rush expansion—it builds reserves. During downturns, it doesn't slash investment—it deploys accumulated cash. This counter-cyclical approach creates value: building assets when construction costs are low, avoiding overcapacity when everyone else expands.

The company also diversifies margin exposure. Refining provides commodity leverage. Marketing generates stable volumes. Lubricants deliver premium margins. Pipelines offer utility-like returns. Renewable energy promises growth. This portfolio approach smooths earnings volatility that destroys value in pure-play refiners.

So what for investors: HPCL's playbook reveals how PSUs can create value despite ownership constraints. Patient capital, political navigation, and strategic flexibility compensate for lack of entrepreneurial freedom. The ONGC integration and renewable pivot show adaptation capabilities. However, these strategies require long investment horizons and tolerance for political interference—not suitable for all investors.

X. Bear vs. Bull Case Analysis

Bull Case: The Emerging Energy Champion

ONGC's Strengthening Grip: From Burden to Blessing

ONGC's stake increase to 54.90% by March 2023 isn't just about control—it's about commitment. ONGC sits on ₹50,000 crore in cash reserves and generates ₹40,000 crore in annual operating cash flow. This war chest backs HPCL's ambitious expansion plans. When banks hesitate to fund the Barmer refinery, ONGC can provide bridge financing. When working capital spikes during crude price volatility, ONGC ensures liquidity. It's like having a sovereign wealth fund as your majority shareholder.

The relationship is evolving strategically. ONGC's latest discoveries in the Krishna-Godavari basin could feed directly into HPCL's Visakhapatnam refinery. ONGC's gas production supplies HPCL's city gas ventures. The companies jointly explore green hydrogen production, combining ONGC's offshore wind potential with HPCL's refinery demand. What started as financial engineering is becoming industrial logic.

Maharatna Autonomy: The Best of Both Worlds

Maharatna status transforms HPCL's decision-making. The board can approve ₹5,000 crore investments without government clearance—enough to build a new refinery unit or acquire a competitor. International joint ventures need no political approval. The company can raise $2 billion in international markets independently. This autonomy, combined with government backing, creates unique competitive positioning: entrepreneurial freedom with sovereign support.

Consider how this plays out practically. When a European technology company offers partnership for sustainable aviation fuel, HPCL can negotiate and sign within months—private sector speed with public sector credibility. When state governments auction retail outlet locations, HPCL gets preferential treatment as a Maharatna PSU. It's systematic advantage accumulation.

Strategic Infrastructure: The Unreplicable Moat

Try building HPCL's infrastructure today. The Mumbai refinery sits on 450 acres of land now worth ₹20,000 crore—more than HPCL's entire market capitalization in 2010. The 5,100-kilometer pipeline network would require ₹50,000 crore to replicate, assuming you could even get right-of-way permissions across seven states. The 22,000 retail outlets occupy prime real estate that money alone can't buy—corner locations in Delhi, highway frontage in Tamil Nadu, city centers in Gujarat.

But physical assets are just the beginning. HPCL's operating knowledge—how to run refineries at 106% capacity, how to manage 90 million LPG customers, how to coordinate fuel supplies across a subcontinent—took 50 years to accumulate. New entrants can't Google this expertise or hire it from consultants. It's embedded in standard operating procedures, supplier relationships, and institutional memory.

India's Insatiable Energy Appetite

India's per capita energy consumption is one-third the global average. As 400 million Indians enter the middle class by 2030, energy demand will explode. Every percentage point of GDP growth drives 1.2% energy consumption increase. Even assuming aggressive electric vehicle adoption, oil demand will grow 3-4% annually through 2035. HPCL, controlling 20% of domestic distribution, captures this growth automatically.

The consumption patterns favor HPCL's positioning. Rural India, where HPCL dominates, drives incremental petroleum demand—new motorcycle owners, first-time car buyers, households switching from wood to LPG. Urban India might go electric, but rural India will burn oil for decades. HPCL's 8,000 rural outlets become more valuable as this consumption shifts.

The Renewable Option Value

HPCL's renewable investments might seem subscale—5 GW by 2040 is modest compared to dedicated renewable players. But that misses the strategic logic. HPCL isn't trying to become a renewable utility; it's creating options for multiple energy futures. If hydrogen becomes viable, HPCL's refineries are ready. If biofuels scale, HPCL's distribution network can handle them. If carbon capture works, HPCL's industrial sites can host it.

The company's approach—renewable energy integrated with existing operations—might prove superior to pure-play strategies. Green hydrogen produced at refineries has immediate industrial use. Solar power at retail outlets reduces operating costs. Bio-refineries can process agricultural waste from areas HPCL already serves. It's energy transition through evolution, not revolution.

Bear Case: The Structural Decline

Government Control: The Invisible Tax

Every fuel price decision involves the petroleum ministry. Every major appointment requires bureaucratic approval. Every CSR project faces political pressure. This isn't just red tape—it's value destruction. When global crude crashes but retail prices don't adjust because elections approach, HPCL absorbs the margin hit. When a minister wants a refinery in an economically unviable location, HPCL complies. The government ownership that provides stability also imposes an invisible tax on returns.

The numbers reveal the burden. HPCL's return on equity averages 12-15%—respectable until you compare with Reliance Industries' refining business at 20-25%. The gap isn't operational efficiency; it's capital allocation freedom. Reliance invests only in high-return projects. HPCL invests where politics demands. Over time, this ROE gap compounds into massive value destruction.

Refining Margin Volatility: The Commodity Curse

Singapore complex refining margins—HPCL's benchmark—swung from $15 per barrel in 2022 to $3 in 2024. Each dollar change impacts HPCL's annual profits by ₹500 crore. This isn't manageable volatility; it's existential uncertainty. In bad years, HPCL barely covers capital costs. In good years, windfall profits attract political interference. The company never truly wins.

Worse, refining margins face structural pressure. Global refining capacity exceeds demand by 3 million barrels per day. China adds massive export-oriented refineries. Middle Eastern national oil companies integrate downstream. Electric vehicles reduce transport fuel demand in developed markets. HPCL's core business faces overcapacity, competition, and disruption simultaneously.

The Reliance Problem: David vs. Goliath

Reliance's Jamnagar complex processes 68 million tons annually—triple HPCL's total capacity. But scale is just the beginning. Jamnagar's Nelson Complexity exceeds 12—it can process any crude into any product. Reliance exports half its production, accessing global markets HPCL can't reach. When domestic margins compress, Reliance pivots to exports. HPCL remains trapped in India.

The competition intensifies in marketing. Reliance's Jio-BP venture plans 5,500 retail outlets in premium locations with superior technology and customer experience. They're cherry-picking HPCL's most profitable markets. Meanwhile, HPCL must maintain rural outlets that lose money but serve social objectives. It's asymmetric warfare where HPCL fights with one hand tied.

Electric Vehicle Disruption: The Slow-Motion Train Wreck

Bulls argue India's EV adoption will be slow, but the direction is unmistakable. Two-wheelers—30% of petroleum demand—are going electric rapidly. Urban commercial vehicles follow. By 2030, 30% of new vehicle sales could be electric. By 2040, the majority. HPCL's retail network, built for fossil fuels, becomes stranded assets.

The company's EV charging network seems impressive—3,603 stations—until you realize the economics. EV charging generates one-tenth the margin of fuel sales. Utilization rates remain below 20%. The payback period exceeds 15 years. HPCL invests in EV infrastructure not for returns but for survival. It's value-destructive adaptation to existential threat.

Subsidy and Policy Risk: The Sword of Damocles

The government hasn't mandated fuel subsidies since 2014, but the power remains. When global crude spiked in 2022, political pressure for price controls intensified. HPCL's stock fell 20% on subsidy fears alone. Even without actual subsidies, the possibility creates permanent valuation discount. Markets price HPCL not on earnings but on political risk.

Environmental regulations pose different but equally serious threats. India's net-zero commitment by 2070 means petroleum demand must eventually decline. Carbon taxes could destroy refining economics. Fuel efficiency standards reduce consumption. Pollution controls require massive capital investment with no return. HPCL faces regulatory obsolescence even if technology doesn't disrupt.

ROE Reality: The Mediocrity Trap

HPCL's 12-15% ROE seems acceptable until you adjust for risk. Commodity price volatility, regulatory uncertainty, and technology disruption warrant 20%+ returns. HPCL delivers utility-like returns with technology stock risks. This risk-return mismatch explains why HPCL trades at book value while software companies trade at 10x.

The ROE problem compounds. Low returns mean less retained earnings for growth. Dependence on debt or government support increases. Credit ratings suffer, raising capital costs. It's a vicious cycle where inadequate returns create constraints that further depress returns. Without dramatic margin expansion or capital efficiency improvement, HPCL remains permanently subscale in value creation.

So what for investors: The bull case rests on India's structural energy demand growth and HPCL's irreplaceable infrastructure. The bear case highlights government interference, margin pressure, and disruption risks. Reality likely lies between: a steady but unspectacular business generating utility-like returns with commodity volatility. Suitable for dividend-focused investors, challenging for growth seekers.

XI. Looking Forward: The Energy Transition Challenge

India's Net-Zero Tightrope: 2070 and the Path Between

In Glasgow, November 2021, Prime Minister Modi stunned climate observers by committing India to net-zero emissions by 2070. For HPCL, this wasn't just another government announcement—it was an existential deadline. The company has 46 years to transform from fossil fuel refiner to... what exactly? The answer isn't clear, but the implications are profound.

India's energy transition differs fundamentally from developed nations'. The country must simultaneously lift 300 million people from poverty, industrialize its economy, and decarbonize—an unprecedented trinity of challenges. Energy demand will double by 2040 even with efficiency improvements. This creates a paradox for HPCL: grow fossil fuel business to generate cash for transition, but transition fast enough to remain relevant post-2070.

The company's response reveals strategic pragmatism. Unlike European oil majors making dramatic renewable pivots, HPCL pursues "transition fuels"—products that bridge fossil and clean energy. Compressed natural gas for vehicles—50% cleaner than petrol. Ethanol blending in gasoline—targeting 20% by 2025. These aren't zero-carbon solutions, but they're implementable today with existing infrastructure.

Green Hydrogen: The Refinery Revolution

HPCL's Visakhapatnam refinery consumes 100,000 tons of hydrogen annually for desulfurization—currently produced from natural gas, generating massive CO2 emissions. The company's pilot project aims to produce this hydrogen through electrolysis powered by renewable energy. If successful, it transforms refineries from carbon emitters to clean fuel producers.

The economics remain challenging. Green hydrogen costs $6 per kilogram versus $2 for grey hydrogen from natural gas. But HPCL sees convergence by 2030 driven by carbon taxes, renewable energy cost declines, and electrolyzer efficiency improvements. The company partners with Greenstat Norway for technology, with L&T for engineering, with NTPC for renewable power. It's ecosystem building for an uncertain but essential future.

The real opportunity lies beyond refinery consumption. HPCL's infrastructure—pipelines, storage tanks, distribution networks—could handle hydrogen with modifications. Imagine the Mumbai-Pune pipeline carrying hydrogen to fuel cell vehicles, the retail network dispensing hydrogen alongside petrol. It's a $100 billion opportunity if hydrogen becomes transport fuel. HPCL wouldn't need to abandon its assets, just repurpose them.

Petrochemical Pivot: From Fuel to Materials

Even in a net-zero world, humanity needs plastics, chemicals, and materials currently derived from petroleum. HPCL's Barmer refinery includes a petrochemical complex producing polypropylene and polyethylene—materials for everything from medical devices to wind turbine blades. As transport fuel demand declines, petrochemicals could become the primary refinery output.

The strategic shift is already visible. HPCL targets 10% of refinery output for petrochemicals by 2030, up from 2% today. New units maximize propylene and aromatics production. Research focuses on bio-based chemicals from agricultural waste. The company essentially prepares for a world where refineries become chemical plants that happen to produce some fuel.

But competition intensifies. Reliance already derives 30% of refining value from petrochemicals. Saudi Aramco builds massive integrated complexes. Chinese companies flood markets with cheap products. HPCL enters this battle late, subscale, and capital-constrained. Success requires technological leapfrogging or niche specialization—neither guaranteed.

Competition from New Energy Companies

The threat isn't just from traditional competitors going green—it's from entirely new players. Adani Green Energy, with 30 GW renewable capacity, generates more clean electricity than HPCL's entire energy throughput. Ola Electric manufactures 10 million electric scooters annually, directly displacing petroleum demand. These companies aren't constrained by legacy assets or fossil fuel mindsets.

More concerning are global tech giants entering energy. Shell partners with Google for AI-driven energy optimization. BP works with Microsoft on digital energy platforms. These collaborations combine energy assets with digital capabilities HPCL lacks. The company responds by partnering with Indian startups, but the technology gap widens.

The financing landscape also shifts against traditional energy. ESG-focused investors divest from oil companies. Banks restrict fossil fuel lending. Insurance companies won't cover new petroleum projects. HPCL's cost of capital rises precisely when it needs massive investment for transition. It's a Catch-22: need money to transform, can't get money without transforming.

Can a 1970s PSU Transform for 2050?

The question isn't whether HPCL can install solar panels or build EV chargers—it's whether a company with 50-year-old organizational DNA can fundamentally reinvent itself. The challenges are cultural as much as technical. Engineers trained in refinery operations must learn battery chemistry. Managers focused on volume growth must optimize for carbon efficiency. A workforce expecting lifetime employment must accept startup-style disruption.

Some signs encourage. HPCL's digital transformation shows adaptation capability. The company's joint venture strategy demonstrates partnership openness. Younger employees push sustainability initiatives internally. But institutional inertia remains powerful. Decision-making is still hierarchical. Risk-taking is limited. Innovation happens at the margins, not the core.

The government ownership adds complexity. Political leaders want energy transition but also employment stability, energy security, and tax revenues. HPCL must balance these competing demands while competing with private players focused solely on commercial returns. It's like playing chess while solving a Rubik's cube.

Final Thoughts: HPCL's Energy Future

HPCL in 2070 won't resemble today's company—that much is certain. The optimistic scenario sees a diversified energy company: still refining petroleum for chemicals and specialty products, but also producing green hydrogen, distributing biofuels, operating renewable power plants, and providing integrated energy solutions. The pessimistic scenario sees a stranded asset, its refineries obsolete, its retail network abandoned, its workforce redundant.

Reality will likely fall between extremes. HPCL will probably survive—government support and India's gradual energy transition ensure that. But thriving requires transformation more radical than anything in its 50-year history. The company must simultaneously milk declining fossil fuel cash flows while building new energy capabilities—a strategic balance that defeats many companies.

The path forward demands not just capital and technology but imagination. Can HPCL reimagine refineries as carbon recycling centers? Can it transform retail outlets into mobility hubs? Can it evolve from selling products to providing energy services? These aren't just business model questions—they're existential choices that determine whether HPCL leads India's energy transition or becomes its casualty.

For investors, HPCL represents a complex bet on India's energy future. It's simultaneously a play on continued fossil fuel demand (bull case) and successful energy transition (survival case). The company offers defensive qualities—government backing, essential infrastructure, dividend yield—but also transformation optionality. It's not a growth story or a value play but something more nuanced: a transition story where success means becoming something fundamentally different from what you are today.

So what for investors: HPCL's energy transition creates unprecedented uncertainty but also optionality. The company's infrastructure and market position provide time to adapt, but success isn't guaranteed. Investors must weigh stable near-term cash flows against long-term transformation risks. This isn't a buy-and-hold forever stock—it requires active monitoring of transition progress versus market expectations.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube