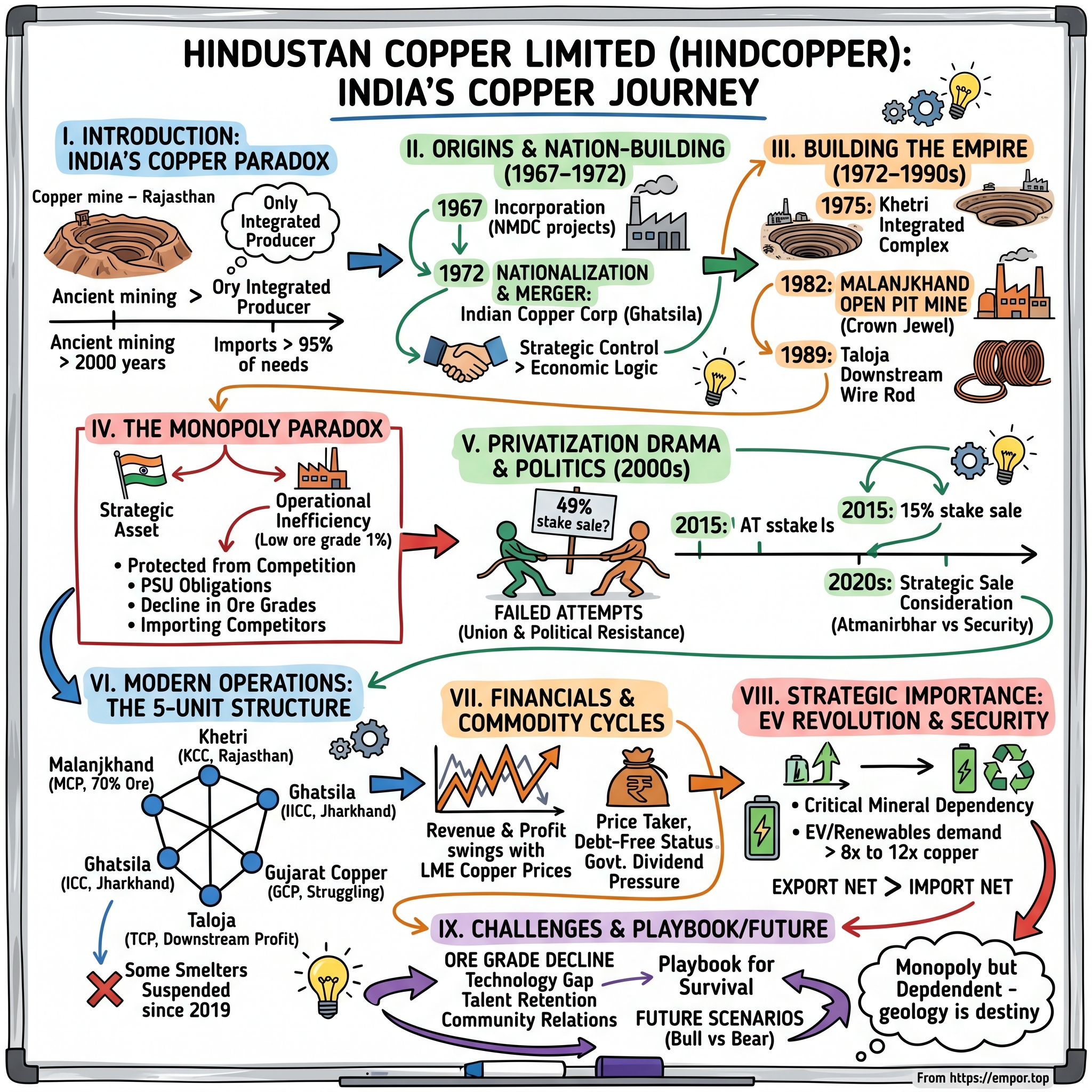

Hindustan Copper Limited: India's Copper Monopoly Story

I. Introduction & Episode Roadmap

Picture this: Deep in the Aravalli hills of Rajasthan, 180 kilometers from Jaipur, lies a mining complex that has been extracting copper for over 2,000 years. The ancient workings at Khetri—some dating back to the Mauryan empire—tell a story of India's long relationship with the red metal. Today, those same mines form the backbone of Hindustan Copper Limited, a company that embodies both the promise and paradox of India's public sector ambitions.

At ₹23,090 crore market cap, Hindustan Copper isn't the largest PSU on Dalal Street. With ₹2,071 crore in revenue and ₹469 crore in profit, it's dwarfed by behemoths like Coal India or ONGC. Yet this company holds a unique distinction: it's India's only integrated copper producer, controlling the entire value chain from ore to finished wire rods. In a nation that imports over 95% of its copper requirements, Hindustan Copper stands as both a strategic asset and an operational enigma.

The fundamental question isn't whether India needs domestic copper production—with the EV revolution and renewable energy buildout accelerating demand, that answer is obvious. The real puzzle is this: How does a company navigate the tension between being a commercial entity expected to deliver returns and a strategic national asset expected to secure mineral independence? Can a PSU monopoly innovate fast enough to matter in a commodity business where Chinese giants process more copper in a month than India does in a year?

This is a story of nation-building mandates colliding with market realities. It's about a company that survived multiple privatization attempts, weathered commodity supercycles, and somehow emerged debt-free while carrying the burden of being India's sole domestic copper miner. Along the way, we'll explore the geology of monopoly, the politics of privatization, and the economics of operating mines in some of India's most remote locations.

What makes this particularly fascinating is timing. As global supply chains fragment and countries scramble to secure critical minerals, Hindustan Copper's strategic importance has never been clearer. Yet its operational challenges—declining ore grades, aging infrastructure, talent retention in remote locations—have never been more acute. The company sits at the intersection of India's industrial past and its electrified future, making it a perfect lens through which to understand the broader tensions in Indian capitalism.

We'll journey from the post-independence mineral security paranoia that birthed the company, through the License Raj protection that shaped its culture, to the liberalization shocks that nearly killed it, and finally to its current position as an unlikely survivor in India's PSU landscape. Along the way, we'll decode why every attempt to privatize it failed, what its near-monopoly really means for India's copper security, and whether the current management's expansion plans are visionary or delusional.

By the end, you'll understand not just Hindustan Copper's business, but the deeper structural forces that shape resource nationalism, the hidden costs of self-reliance, and why sometimes the most important companies aren't the most profitable ones. This is the Hindustan Copper story—a monopoly that India can't afford to lose, yet struggles to make win.

II. Origins & The Nation-Building Mandate (1967–1972)

November 9, 1967. The monsoon had been brutal that year in New Delhi, and the bureaucrats at Shastri Bhavan were still mopping puddles from their offices when the notification came through: Hindustan Copper Limited was officially incorporated, taking over the copper mining operations at Khetri and Kolihan in Rajasthan, along with the Rakha Copper Project in Jharkhand from the National Mineral Development Corporation.

The timing wasn't accidental. India in 1967 was a nation gripped by resource paranoia. Two wars with Pakistan, tensions with China, and the humiliation of depending on American PL-480 wheat shipments had driven home a brutal lesson: India didn't have enough production to meet domestic demand and had to depend on imports, a situation that aggravated in the mid-1960s due to two consecutive drought years, necessitating assistance from the United States. If food dependency was a crisis, what about industrial minerals? What about copper—the metal that would wire the nation's industrial ambitions?

The answer lay in the dusty files of the Geological Survey of India, which had been mapping copper deposits since the 1950s. Mining of copper in India was more than 2000 years old, but production to meet industrial demand only began in the middle of the 1960s. The ancient workings at Khetri—where tribal miners had extracted malachite for centuries—suddenly became strategic assets. The government's solution was characteristically socialist: create a state monopoly that would control every ounce of domestic copper from mine to market.

Development of Khetri Mine had been started by National Mineral Development Corporation (NMDC), and the project was handed over to HCL in 1967 when HCL was formed. But Khetri alone wouldn't suffice. The real prize came five years later, in September 1972, when Prime Minister Indira Gandhi signed the order that would define Hindustan Copper's trajectory for the next half-century.

Indian Copper Corporation Ltd had been established by a British company in 1930 at Ghatsila, consisting of a cluster of underground copper mines, concentrator plants and smelter. On September 25, 1972, the Government of India nationalized the company under provisions of the Indian Copper Corporation (Acquisition of Undertaking Act) and merged it with HCL. The nationalization wasn't just about adding capacity—it was about sending a message. Foreign capital, particularly British legacy assets, would be subordinated to national interest.

The Ghatsila acquisition transformed Hindustan Copper overnight. The private sector company Indian Copper Corporation Limited, located in Ghatsila, Jharkhand, equipped with smelter and refinery facilities, was amalgamated to Hindustan Copper Limited. Suddenly, the company had real production capabilities: underground mines that actually worked, a smelter that could process ore, and most importantly, experienced miners who knew how to extract copper from the challenging geology of the Singhbhum belt.

But this was still Nehruvian India, where every industrial project carried the weight of nation-building mythology. Jawaharlal Nehru, along with statistician Prasanta Chandra Mahalanobis, had formulated economic policy involving rapid development of heavy industry by both public and private sectors, based on direct and indirect state intervention. Copper wasn't just copper—it was the sinew of industrialization, the conductor of modernity.

The irony was palpable. India was building a vertically integrated copper monopoly at precisely the moment when global copper markets were becoming more sophisticated and interconnected. While Chile's nationalization of copper under Allende was making headlines, India's quieter takeover of its tiny copper sector barely registered internationally. India's copper production was only about 2 percent of world copper production, with reserves limited to 60,000 km² (2% of world reserve).

Yet for India's planners, size didn't matter as much as control. The memory of colonial resource extraction—where raw materials flowed out and finished goods flowed in—haunted policy corridors. HCL was established as a Government of India Enterprise to take over all plants, projects, schemes and studies pertaining to the exploration and exploitation of copper deposits from NMDC Ltd. It became the only company in India engaged in mining of copper ore and the only integrated producer of refined copper.

The workforce inherited from these acquisitions tells its own story. At Khetri, you had Rajasthani miners whose families had worked the copper seams for generations, suddenly becoming government employees with guaranteed pensions. At Ghatsila, Anglo-Indian supervisors who'd run the British operations found themselves reporting to IAS officers who'd never been underground. The cultural collision was immediate and lasting.

What's remarkable, looking back, is how little economic logic drove these early decisions. Nobody ran serious feasibility studies on whether India's copper deposits—mostly low-grade, difficult to extract—could compete with the massive porphyry deposits being developed in Chile and Peru. The question wasn't whether it made economic sense; it was whether India could afford not to have domestic copper production.

The administrative structure reflected this strategic imperative over commercial logic. Hindustan Copper Limited, under the administrative control of the Ministry of Mines, had the distinction of being the nation's only vertically integrated copper producing company, manufacturing copper right from mining to beneficiation, smelting, refining and casting into downstream saleable products. Every aspect of the operation—from exploration licenses to pricing decisions—would flow through ministry bureaucracy.

By 1972, as the ink dried on the nationalization papers, Hindustan Copper had assembled the pieces of what would become India's copper monopoly. It controlled ancient mines in Rajasthan, colonial-era operations in Jharkhand, and the promise of new discoveries across the subcontinent. The company's leaders spoke of self-sufficiency by 1980, of India becoming a copper exporter by the century's end.

Those predictions would prove spectacularly wrong. But in that moment, with the nation still celebrating the victory in Bangladesh and Indira Gandhi at the height of her power, anything seemed possible. Hindustan Copper wasn't just mining copper—it was mining sovereignty itself. The real question was whether sovereignty could be smelted into profits, whether nationalism could overcome geology, whether a protected monopoly could ever learn to compete. The next two decades would provide brutal answers.

III. Building the Copper Empire (1972–1990s)

The summer of 1975 was sweltering in Rajasthan. At Khetrinagar, 180 kilometers from Delhi, engineers were running final tests on what would become India's most ambitious copper complex. The $152 million Khetri complex included two mines and was expected to have a capacity of 31,000 metric tons per year of refined copper. For the workers who'd been toiling since 1967 to bring this vision to life, it represented something more than tonnage—it was industrial sovereignty crystallized in copper cathodes.

In 1975, a fully integrated copper complex, spanning from mining to refining, commenced operations at Khetri with a refining capacity of 31,000 tonnes of copper. The complex wasn't just large; it was audaciously comprehensive. Mechanized underground mines at Khetri and Kolihan had a capacity of 1.0 million tonnes of ore per annum, with a beneficiation plant capacity of 1.81 million tonnes per annum. This was India saying: we can do the entire value chain ourselves.

But Khetri was just the opening act. The real drama unfolded on November 12, 1982, when Prime Minister Indira Gandhi arrived at a dusty plateau in Madhya Pradesh to inaugurate what would become Hindustan Copper's crown jewel. Hindustan Copper Limited developed Malanjkhand Copper Project in Madhya Pradesh, the largest hard rock open pit mine in the country which was dedicated to the nation on 12-November-1982.

Malanjkhand Copper Project was established in 1982, after Geological Survey of India took systematic geological exploration at this deposit during 1969 and mining lease was granted to HCL during 1973. The statistics were staggering for India at the time: an open pit mine with a capacity of 2 million TPA of ore with a matching concentrator plant. This wasn't incremental progress—it was a quantum leap.

The Malanjkhand story reveals the contradictions at the heart of Hindustan Copper's expansion. Here was the largest base metal mine in India, yet with ore grades averaging just 1.24% copper—less than half the global average. The engineers knew this meant moving massive amounts of rock for modest amounts of metal. But in the calculus of national self-reliance, efficiency took a backseat to existence.

What made Malanjkhand work wasn't just scale but timing. The early 1980s saw copper prices relatively stable, the Indian economy growing steadily, and most importantly, a political consensus that PSUs should expand aggressively. The complex employed 7,000 people at Khetri alone, creating entire townships in previously barren landscapes. Khetrinagar, maintained by Hindustan Copper Limited, became a model company town—schools, hospitals, recreation clubs, all funded by copper.

Then came 1989, marking Hindustan Copper's boldest downstream move. The Taloja Copper Project was set up in December 1989, based on technology sourced from Southwire, USA. Located just 60 kilometers from Mumbai, the plant produces Continuous Cast Copper Rods (CCR) and has a capacity of producing 60,000 TPA.

This wasn't just another production facility—it was Hindustan Copper's attempt to capture more value downstream. The technology used is the SCR 2000 system of Southwire Co., USA, accepted as the world's leading technology for producing premium quality continuous cast rods. For once, an Indian PSU wasn't settling for second-tier technology.

The Taloja plant represented a philosophical shift. Rather than just mining and refining, Hindustan Copper would now produce the actual products that industries needed—wire rods that would become cables, transformers, motors. The Project has an installed capacity to produce 60,000 MT per year of Continuous Cast Copper Wire Rods of various diameters, offered in coils weighing 3.0 MT, 2.650 MT and 1.00 MT.

By 1990, Hindustan Copper had assembled an impressive empire: underground mines in Rajasthan, an open pit giant in Madhya Pradesh, colonial-era operations in Jharkhand, and a state-of-the-art wire rod plant in Maharashtra. The company produced not just copper but gold, silver, nickel sulphate, selenium, tellurium and fertiliser as by products. On paper, it looked like a vertically integrated success story.

But cracks were already showing. The Khetri smelter, built for 31,000 tonnes annual capacity, struggled with declining ore grades. The underground mines faced increasing depths and costs. Most troublingly, while Hindustan Copper was expanding capacity, private players like Sterlite were building massive smelters using imported concentrate—a model that would prove far more economically viable.

The License Raj protected Hindustan Copper from direct competition, but it couldn't protect it from economic reality. By the late 1980s, India's copper demand was growing at 8-10% annually while Hindustan Copper's production grew at barely 3%. The gap was filled by imports, undermining the very self-reliance logic that justified the company's existence.

Yet within the constraints, there were genuine achievements. The company had created mining expertise where none existed, developed townships in remote areas, and trained thousands of engineers and technicians. The Malanjkhand mine, despite its low grades, was efficiently run by global standards for similar ore bodies. The Taloja plant produced wire rods that competed on quality with international products.

Looking back, the 1972-1990 period was Hindustan Copper's golden age—not because it was profitable (it often wasn't) but because its mission aligned with national priorities. India needed domestic copper production capability, regardless of cost. The company delivered that, creating infrastructure that would survive long after the economic logic shifted.

The irony is palpable: Hindustan Copper built its empire precisely when the economic model supporting it was becoming obsolete. By 1990, as the Taloja plant reached full production, India was months away from economic liberalization that would expose every inefficiency the License Raj had protected. The empire was complete just as the ground beneath it began to shift.

IV. The Monopoly Paradox: Strategic Asset vs. Inefficiency

There's a scene that plays out every morning at commodity trading desks from Mumbai to London: traders check LME copper prices, scan Chilean production reports, and barely glance at Hindustan Copper's output numbers. The company that was supposed to secure India's copper independence has become a rounding error in global markets. Copper production in India is only about 2 percent of world copper production, with mining production just 0.2% of world's production, whereas refined copper production is about 4% of world's production.

This is the central paradox: India built a vertically integrated monopoly to achieve copper self-sufficiency, yet India may need to import between 91%-97% of its copper concentrates by 2047, currently meeting over 90% of its copper concentrate needs through imports. Hindustan Copper controls 100% of domestic mining but satisfies less than 5% of national demand. It's like owning all the wells in a desert—impressive until you realize they're mostly dry.

The monopoly structure itself created perverse incentives. Protected from competition in mining, Hindustan Copper never faced the existential pressure to innovate that drives private miners in Chile or Australia. Why invest in expensive exploration when you're guaranteed to sell every kilogram you produce? Why optimize costs when the government will cover losses in the name of strategic importance?

Consider the labor dynamics. As a PSU, Hindustan Copper inherited not just mines but entire social contracts. Every mine came with townships, schools, hospitals—infrastructure that private companies would outsource or minimize. The company employs thousands not because operations require it, but because retrenchment in a PSU triggers political earthquakes. At Khetri alone, 7,000 people draw salaries, many in roles that automation eliminated elsewhere decades ago.

The government ownership created a schizophrenic identity crisis. Was Hindustan Copper a commercial entity expected to generate returns, or a strategic asset maintaining capability regardless of economics? The answer changed with every budget cycle, every ministerial shuffle, every commodity price swing. This uncertainty paralyzed long-term planning. How do you commit to a 20-year mine development when your political masters change priorities every five?

Union power added another layer of complexity. Unlike private miners who could adjust workforce with demand, Hindustan Copper faced strikes at any hint of restructuring. The unions weren't just protecting jobs—they were defending an entire way of life built around these remote mining townships. Every efficiency improvement was viewed through the lens of potential job losses, creating massive resistance to modernization.

Meanwhile, the competition wasn't standing still. Copper concentrates are imported by the Birla copper of Hindalco Industries Limited and Sterlite Industries Limited to produce copper metal located in the States of Gujarat and Tamil Nadu. These private players built world-scale smelters using imported concentrate—a model that bypassed India's low-grade geology entirely. They could source high-grade ore from Chile at prices that made Hindustan Copper's 1% grade ore look economically absurd.

The burden of being a "nation-builder" PSU manifested in countless non-commercial obligations. Hindustan Copper had to maintain production at uneconomic mines because closure meant devastating remote communities entirely dependent on mining wages. It had to sell at regulated prices during shortage periods, forgoing windfall profits that private players captured. It had to prioritize domestic customers even when exports offered better margins.

India produces about 2% of the world's copper and does not have enough copper ore to meet its needs. The country's demand for copper and its alloys is met through local production, recycling scrap, and imports. This reality renders the monopoly almost meaningless. Hindustan Copper monopolizes a resource India barely has, like being the only company allowed to drill for oil in a country with no petroleum.

The import dependency created a vicious cycle. As domestic production stagnated, downstream industries increasingly relied on imports, building supply chains around international sources. This reduced pressure on government to fix Hindustan Copper's inefficiencies—why fight political battles over PSU reform when Chilean copper was readily available?

The strategic importance argument, once Hindustan Copper's shield, became its cage. Every discussion of privatization or restructuring triggered national security concerns. How could India hand over its only copper mines to private players, possibly foreign ones? Yet this strategic asset was strategically irrelevant—producing too little to matter in war or peace.

Environmental regulations added another constraint. While necessary, they hit Hindustan Copper particularly hard given its old infrastructure and limited capital for upgrades. The Sterlite Copper smelter in Tamil Nadu, operated by Vedanta, was shut down in 2018 due to severe ecological concerns, particularly air and water pollution. This decision significantly impacted India's copper production capacity, as Sterlite was the country's largest copper smelting facility. If Sterlite, with deeper pockets, couldn't navigate environmental challenges, what chance did a cash-strapped PSU have?

The technology gap widened each year. Global miners deployed AI for ore body modeling, autonomous haul trucks, and in-situ leaching. Hindustan Copper struggled to maintain basic equipment, with procurement processes that took years for simple purchases. By the time new technology was approved, budgeted, tendered, and installed, it was already obsolete.

Talent retention became impossible. The best mining engineers, trained at Hindustan Copper's expense, inevitably left for private players offering multiples of PSU salaries. Those who stayed were often those who valued security over ambition—hardly the profile for driving innovation in a challenging industry. The company became a training ground for competitors, subsidizing the private sector's human capital needs.

The financial structure reflected these contradictions. Hindustan Copper needed massive capital for exploration and modernization but faced constant dividend pressure from a cash-strapped government. Every profitable year triggered demands for special dividends, leaving nothing for investment. Every loss year triggered scrutiny about inefficiency, ignoring the structural impossibilities the company faced.

Yet within this dysfunction, pockets of competence survived. The Malanjkhand operation, despite low grades, ran efficiently by global standards for similar ore bodies. The Taloja wire rod plant produced quality matching international standards. Individual engineers and managers fought daily battles against systemic constraints, achieving small victories invisible in aggregate numbers.

The real tragedy isn't that Hindustan Copper failed to achieve copper independence—given India's geology, that was always unlikely. It's that the monopoly structure prevented the emergence of alternatives. A competitive mining sector might have found niche opportunities, developed innovative extraction methods for low-grade ores, or built expertise exportable to other countries. Instead, India got neither efficiency nor security—the worst of both worlds.

The monopoly paradox extends beyond economics to psychology. Hindustan Copper employees know they're protecting a strategic asset, yet daily experience contradicts this narrative. They see imported copper flooding markets, private smelters thriving while their facilities decay, global miners earning billions while they struggle for working capital. This cognitive dissonance breeds a particular form of organizational depression—going through motions without believing in the mission.

Looking at Hindustan Copper's monopoly, you see India's broader PSU challenge in miniature: entities too important to kill, too constrained to thrive, perpetually suspended between commercial reality and political mythology. The company stands as a monument to the gap between intention and outcome, between the copper independence India wanted and the import dependency it got.

V. The Privatization Attempts & Political Drama (2000s)

April 23, 2001. The announcement hit the pink papers like a thunderclap: The Government has decided the following disinvestment strategy for Hindustan Copper Limited. In phase I, the Khetri unit of HCL alongwith Taloja Plant will be formed into a separate company. The assests of these units will be valued and will form 49 per cent contribution from HCL in which 51 per cent equity will be injected by a strategic partner.

This wasn't just another PSU sale. This was India's copper crown jewels being offered to private bidders. The Vajpayee government, riding high on its reformist agenda, had decided that even strategic minerals weren't beyond privatization's reach. Arun Shourie, the disinvestment minister with a reputation for bulldozing through opposition, was determined to prove that no PSU was too sacred to sell.

The plan was surgically precise. Carve out the profitable Khetri operations and the modern Taloja plant, package them attractively for a strategic buyer, then deal with the problematic Malanjkhand and Ghatsila units separately. In phase II the remaining portion of HCL comprising the Indian Copper Complex (ICC) and the Malanjkhand Copper Project (MCP) will be restructured by closure of unviable mines in a phased manner. It was textbook asset stripping, dressed up as strategic restructuring.

But the unions smelled blood. Within hours of the announcement, Khetrinagar erupted. Workers who'd spent decades underground, whose fathers had built these mines, suddenly faced the prospect of new masters—possibly foreign ones. The Communist-affiliated unions called it "economic treason," selling India's mineral security to the highest bidder. The Congress opposition, despite having initiated economic reforms a decade earlier, discovered newfound love for PSU preservation.

The political theatre was extraordinary. Union leaders organized human chains around mine shafts, threatening to seal themselves underground if privatization proceeded. Local MPs from Rajasthan, including some from BJP, quietly expressed "concerns" about job losses in their constituencies. The Rajasthan state government, despite being BJP-controlled, worried about losing influence over a major employer in a politically sensitive region.

What killed the 2001 attempt wasn't just political opposition—it was timing. The global commodity cycle had turned negative, copper prices were depressed, and potential strategic partners weren't enthusiastic about buying aging Indian mines with powerful unions and complex geology. The few expressions of interest came with so many conditions—workforce reduction, environmental liability waivers, guaranteed ore allocations—that even the reform-minded Shourie blanched.

Between 1999 and 2004, BJP privatised central government establishments such as Bharat Aluminium Company (BALCO), Hindustan Zinc (both to Sterlite Industries), Indian Petrochemicals Corporation Limited (to Reliance Industries) and VSNL (to the Tata group). Hindustan Zinc's sale to Sterlite in 2002 became the template—and the cautionary tale. While commercially successful, the political backlash was severe. If zinc privatization caused such uproar, what would happen with copper, explicitly mentioned in ancient texts as a strategic metal?

The 2004 election changed everything. The Congress-led UPA government's National Common Minimum Programme declared: "No profit-making enterprises shall be privatized." Hindustan Copper, despite its marginal profitability, qualified for protection. The privatization file gathered dust in North Block, occasionally retrieved when fiscal deficits spiked, then hastily re-buried when union leaders reminded politicians of electoral arithmetic.

Yet the privatization ghost refused to die. Every budget season, investment bankers would pitch Hindustan Copper sales to the finance ministry. The arguments were compelling: private management could double production, modern technology could make low-grade ores viable, and the government could use sale proceeds for social spending. But political reality always trumped economic logic.

Then came 2015, a different approach from a different government. On 31-July-2015, the Government of India announced a 15% stake sale in Hindustan Copper Limited, reducing its stake from 89.5% to 74.5%. This wasn't privatization—it was "disinvestment," a semantic distinction that made all the difference politically. The government retained control while raising capital and theoretically improving governance through public shareholding.

The 2015 stake sale revealed the market's appetite—or lack thereof—for Hindustan Copper equity. Despite roadshows and aggressive pricing, institutional interest was lukewarm. The company's structural problems were too obvious: declining ore grades, aging equipment, and most critically, competition from private smelters using imported concentrate. The sale succeeded technically but failed strategically—it neither raised significant capital nor improved operational efficiency.

The 2020s brought renewed privatization drama. NITI Aayog Vice-Chairman Rajiv Kumar chaired a meeting on October 27, 2020 to discuss the possibility of strategic disinvestment of Hindustan Copper. The Modi government, facing pandemic-induced fiscal pressure, was reconsidering all PSU assets. The government is all set for series of blockbuster divestments, lining up strategic sales of as many as 11 PSUs, including Hindustan Copper.

But 2020 wasn't 2001. The geopolitical landscape had shifted dramatically. China controlled global copper supply chains, resource nationalism was resurging worldwide, and critical mineral security had become a strategic imperative. Selling India's only copper miner to potentially Chinese-influenced buyers seemed strategically suicidal. Even market fundamentalists paused at the national security implications.

The union resistance had also evolved, becoming more sophisticated. Instead of just street protests, they commissioned studies showing how private copper miners in other countries had abandoned marginal deposits that Hindustan Copper continued operating for social reasons. They highlighted environmental disasters at privately-run mines globally. They even found unexpected allies in strategic affairs experts who argued that maintaining domestic mining capability, however inefficient, was insurance against supply disruptions.

The political economy had also changed. The BJP's 2020s avatar was more economically nationalist than its 2001 version. "Atmanirbhar Bharat" didn't square easily with selling domestic mineral assets. Modi's government wanted PSU revenues without PSU ownership—demanding special dividends that stripped companies of investment capital while keeping them technically public.

Each privatization attempt revealed the same structural dilemma: buyers wanted the assets without the liabilities, particularly the social obligations that made Hindustan Copper what it was. No private player would maintain hospitals in Khetrinagar or schools in Malanjkhand. No strategic partner would keep uneconomic mines running to prevent ghost towns. The very characteristics that made Hindustan Copper inefficient—its social infrastructure, employment guarantees, regional development role—were politically non-negotiable.

The technical challenges of privatization were equally daunting. How do you value ore reserves with declining grades? Who takes environmental liability for decades of mining? What happens to the townships entirely dependent on mining wages? These questions had no easy answers, and attempting to answer them triggered political storms that no government wanted to weather.

The repeated privatization attempts created their own pathology within Hindustan Copper. Management, perpetually uncertain about ownership, avoided long-term planning. Workers, constantly threatened with privatization, resisted any efficiency improvements that might make the company more saleable. The company existed in perpetual limbo—too strategic to sell, too inefficient to thrive.

By 2025, after multiple failed attempts, a consensus had emerged through exhaustion: Hindustan Copper would remain government-owned, not because anyone believed this was optimal, but because alternatives were politically impossible. The privatization attempts had failed, but they'd succeeded in one perverse way—they'd made Hindustan Copper's inefficiencies politically acceptable. Better an inefficient PSU than the political explosion privatization would trigger.

The ultimate irony was that while governments dithered over Hindustan Copper's ownership, private players had built a parallel copper industry using imported concentrate, making the PSU's monopoly over domestic mining increasingly irrelevant. The political drama over privatization had obscured the economic reality: the market had already bypassed Hindustan Copper, making its ownership structure a question of political symbolism rather than economic significance.

VI. Modern Operations & The Five-Unit Structure

The morning shift change at Malanjkhand is a study in contrasts. Modern Komatsu haul trucks rumble past manual laborers still using techniques unchanged since the 1980s. This operational schizophrenia—world-class equipment alongside obsolete practices—defines Hindustan Copper's modern reality across its five integrated units that theoretically form a complete copper value chain.

The crown jewel remains Malanjkhand Copper Project in Madhya Pradesh, contributing nearly 70% of the company's total ore production. The open-pit mine moves 7.5 million tonnes of material annually to extract ore grading just 0.89% copper—a Sisyphean task that would bankrupt most private miners. Yet MCP soldiers on, its massive terraced pit now reaching depths where open-pit economics become questionable. The concentrator plant, with its 2.5 million tonne capacity, runs at barely 80% utilization—not for lack of demand but because ore grades keep declining, requiring more rock to be moved for less metal.

Khetri Copper Complex in Rajasthan operates like a federation of fiefdoms. The underground mines at Khetri and Kolihan plunge more than 650 meters below surface, where temperatures reach 47°C and rock pressures challenge even modern support systems. The 1.91 million tonne concentrator struggles with ore averaging 0.98% copper, while the 31,000 tonne smelter—built for a different era's ore grades—operates at less than half capacity. The complex employs 4,500 people to produce what a modern Chilean mine generates with 500.

Indian Copper Complex at Ghatsila carries the weight of history most heavily. The British-era underground mines at Rakha, Surda, and Kendadih are studies in diminishing returns—deeper shafts, narrower veins, higher costs. The 1.6 million tonne concentrator processes ore that barely justifies the diesel burned to haul it. ICC's real value lies in its institutional memory—generations of mining knowledge that can't be replicated or easily transferred.

Taloja Copper Project near Mumbai represents what Hindustan Copper could have been with different strategic choices. The continuous cast wire rod plant, using Southwire technology, produces 60,000 tonnes annually of world-class copper rods. Fed by cathodes from Hindustan Copper's own refineries and supplemented by market purchases, TCP actually makes money—a rarity in the portfolio. Its proximity to customers, modern technology, and focused product line demonstrate that competence exists within the system when structural constraints are removed.

The newest addition, Gujarat Copper Project acquired in 2015, tells a different story. The 50,000 tonne secondary smelter in Jhagadia was meant to process imported scrap and blister copper, diversifying from mining's geological constraints. But GCP has struggled with raw material procurement, competing against nimbler private recyclers who don't face PSU procurement procedures. The unit operates fitfully, its utilization rates a closely guarded embarrassment. The company's expansion plans reveal desperate optimism masquerading as strategic vision. CMD Ghanshyam Sharma announced at the 57th Annual General Meeting that HCL is implementing expansion projects to increase mine production capacity to 12.2 million tonnes per annum (MTPA). The centerpiece is developing an underground mine below the existing open cast mine at Malanjkhand Copper Project which will augment ore production capacity from 2.5 MTPA to 5 MTPA. But this transition from open-pit to underground mining at Malanjkhand tells its own story—the easy ore is gone, and what remains requires exponentially more effort to extract.

The reality on the ground contradicts official optimism. Operations at the Jhagadia and Ghatsila smelting/refining facilities have been suspended since 2019 due to business considerations. Think about that—two major smelting facilities mothballed because they can't compete even with government backing. The Khetri smelter, once the pride of Indian metallurgy, hasn't operated since 2008, ostensibly due to "old machinery" but really because processing low-grade domestic ore makes no economic sense when high-grade Chilean concentrate is available.

The company achieved ore production of 3.78 million tonnes in FY24 against 3.35 MT in FY23, registering a rise of 13%, with Malanjkhand Underground mine producing 22.48 lakh tonnes, about 60.8% increase from 2022-23. These numbers sound impressive until you realize that ore production doesn't equal copper production—at sub-1% grades, you need to move mountains for molehills of metal.

The workforce distribution across units tells the real story. Khetri employs 4,500 people but its smelter is shut. Malanjkhand moves millions of tonnes with declining grades. Indian Copper Complex maintains British-era shafts that private companies would have abandoned decades ago. Only Taloja, focused purely on downstream processing without mining baggage, consistently generates profits—a damning indictment of the integrated model's economics.

The geographic spread creates its own inefficiencies. Coordinating operations across five states, each with different regulatory regimes, labor cultures, and political pressures, fragments management attention. A crisis at one unit becomes a company-wide distraction. Investment allocation becomes political rather than economic—every state wants its "fair share" regardless of geological or market logic.

VII. Financial Performance & The Commodity Cycle

The numbers tell a story of a company perpetually out of phase with commodity cycles, catching falling knives when it should be selling and missing rallies while navigating bureaucratic approvals. Take the most recent quarter: revenue down 16% year-on-year to ₹343.57 crore, while net profit remained flat at ₹62.87 crore. This divergence—maintaining profits despite falling revenues—seems like operational excellence until you realize it's mostly accounting alchemy and one-time adjustments.

The longer view reveals wild swings that would terrify private investors. H1 FY24-25 saw profit before tax double to ₹289.46 crore, with Q2 PBT up 64% to ₹135.33 crore. Q2 FY24 delivered a 67.5% jump in net profit to ₹101.67 crore on 35.87% higher sales of ₹518.19 crore. These aren't the steady returns of a mature miner—they're the erratic heartbeat of a company whose fortunes swing wildly with global copper prices it can neither predict nor influence.

In FY 2023-24, the company earned a Profit Before Tax of Rs. 410.43 Crore against Net Sales of Rs.1686.51 Crore, while for 9 months ending December 2024, it achieved PBT of Rs.373.92 Crore against Net Sales of Rs.1327.19 Crore. The margin compression is obvious—nine months of FY25 have already delivered 91% of the previous year's PBT on just 79% of sales, suggesting either exceptional current performance or concerning future trends.

What makes Hindustan Copper's financials particularly maddening is their disconnect from operational reality. The company can post stellar quarters not because it mined more efficiently or discovered new deposits, but because LME copper prices spiked or the rupee depreciated. Conversely, operational improvements get swamped by commodity price declines. Management has minimal control over the primary profit driver—a recipe for strategic paralysis.

The near debt-free status, often touted as an achievement, is actually an indictment. In a capital-intensive industry where leverage amplifies returns during upcycles, Hindustan Copper's conservative balance sheet reflects not prudence but inability to deploy capital effectively. Private miners lever up during downturns to acquire assets cheaply; Hindustan Copper sits on its hands, constrained by government approval processes that move at geological timescales.

Government dividend expectations add another layer of perversity. In profitable years, the government demands special dividends to fund fiscal deficits, stripping the company of capital needed for exploration and expansion. In loss years, the same government questions management competence while refusing to inject capital. It's taxation without representation in reverse—representation without investment.

The international copper market dynamics make Hindustan Copper's position even more precarious. When China sneezes, Indian copper prices catch pneumonia. When Chilean miners strike, Hindustan Copper briefly looks profitable. The company is a price taker in the purest sense, with production too small to influence prices but exposure large enough that price swings determine its fate.

Currency fluctuations add another uncontrollable variable. A stronger rupee makes imports cheaper, undermining Hindustan Copper's competitive position. A weaker rupee raises input costs for diesel, equipment, and technology the company must import. There's no natural hedge—unlike exporters who benefit from depreciation, Hindustan Copper gets squeezed from both sides.

The working capital cycle reveals operational stress. Receivables stretch as government customers delay payments, while suppliers demand faster settlement. The company often finances its customers and suppliers simultaneously, acting as an involuntary banker to the ecosystem. Private companies would simply stop supplying deadbeat customers; Hindustan Copper, selling to other PSUs and government departments, lacks this option.

Capital allocation remains politically driven rather than economically rational. Every expansion announcement coincides suspiciously with elections in mining states. Projects get approved based on employment generation potential rather than ore grade economics. The company spreads limited capital across multiple marginal projects instead of concentrating on winners—political equity over economic efficiency.

VIII. The Strategic Importance & National Security Angle

The numbers are stark and damning: India transitioned from being a net exporter in 2017-18 to a net importer in FY19 and has remained on that trajectory since, importing copper ores and concentrates from Indonesia (30%), Chile (20%), Australia (11.4%), and Peru (10%). This isn't gradual decline—it's strategic capitulation. A nation that once exported copper now depends on four countries, two of them Chinese-influenced, for a metal critical to every aspect of modern infrastructure.

The dependency is near-total. Domestic production of 555,000 tonnes annually falls short of consumption exceeding 750,000 tonnes, necessitating imports of 500,000 tonnes. But even these numbers understate the crisis. Production of copper ore fell to 3.78 Mt in FY24 from 4.13 Mt in FY19, and as a result, copper concentrate imports have doubled to Rs 26,000 crore in FY24 from FY19. We're not just import-dependent—we're increasingly import-dependent, with domestic production declining while consumption soars.

The electric vehicle revolution makes this dependency existential. The projected demand for copper due to electric vehicles is expected to increase by 1.7 million tonnes by 2027, as India progresses toward its target of 30% EV market share by 2030. Each EV contains 3-4 times more copper than conventional vehicles. The charging infrastructure needs massive copper investments. Yet we're planning an electric future with no domestic copper security—like launching a space program without rocket fuel.

To meet at least half of energy needs from renewable sources and develop 500 GW non-fossil fuel capacity by 2030, renewable power generators will use 8 to 12 times more copper than traditional generators. Solar panels, wind turbines, transmission lines—all copper-intensive. India's entire green transition depends on a metal it doesn't control. The irony is breathtaking: achieving energy independence requires accepting mineral dependence.

The geopolitical implications are sobering. Copper isn't like software or textiles where supply chains can be quickly reconfigured. Mines take decades to develop. Processing facilities require massive capital investments. If China, controlling much of global copper processing, decided to restrict exports during a border crisis, India's industrial economy would face immediate stress. Hindustan Copper's 5% market share wouldn't even cushion the blow.

The "Make in India" paradox is particularly acute. Government thrust toward "Make in India," Smart Cities, Atmanirbhar Bharat in Defense, renewable energy targets, and PLI schemes for consumer electronics all require copper India doesn't have. We're trying to build self-reliance on a foundation of import dependence. Every smartphone manufactured, every electric motor produced, every kilometer of metro rail laid deepens our copper deficit.

The strategic minerals narrative has evolved globally while India remained stuck in 1960s thinking. Countries are now securing copper assets in Africa, developing recycling capabilities, and investing in substitution technologies. India must strategically engage with copper-rich countries like Zambia, the Democratic Republic of Congo, and Chile where equity in copper assets is available. But while China's belt-and-road tied up African copper, India debated whether to privatize its marginal domestic mines.

The national security establishment finally seems to be awakening to the crisis. Copper appears on every critical minerals list, every strategic assessment. But recognition isn't action. The same reports that flag copper dependency also resist privatization, fearing foreign control. It's strategic schizophrenia—acknowledging the problem while blocking solutions.

India has limited copper ore reserves constituting around 2% of world reserves with mining production just 2% of world production. This geological reality won't change. No amount of exploration will discover Chilean-grade porphyry deposits in the Deccan. The question isn't whether India can achieve copper independence—it can't. The question is whether clinging to Hindustan Copper's marginal production provides any real security or just security theater.

The recycling opportunity remains unexploited. India's growing urban waste stream contains significant copper—old wires, discarded electronics, industrial scrap. A serious recycling industry could provide 20-30% of copper needs. But this requires technology, investment, and regulatory support that PSU-focused policy has ignored. We're mining low-grade ore while high-grade scrap goes to landfills.

The substitution angle offers limited hope. Aluminum can replace copper in some electrical applications but at efficiency costs. Fiber optics reduce copper needs in telecommunications but can't replace power transmission. Every substitution comes with trade-offs, and usually those trade-offs involve using more energy—defeating the purpose in a carbon-constrained world.

IX. Challenges & The Innovation Imperative

The ore grade decline at Hindustan Copper properties reads like a geological death sentence written in percentages. Khetri's ore has declined from 1.5% copper in the 1970s to 0.98% today. Malanjkhand started at 1.4% and now struggles with 0.89%. These aren't just numbers—they represent exponential increases in rock moved, energy consumed, and costs incurred for every kilogram of copper produced. The mathematics are brutal: halving ore grade doesn't double costs; it can triple or quadruple them when considering deeper mining, harder rock, and more complex processing.

The extraction complexity compounds with depth. Kolihan mine now operates at 650 meters below surface where rock temperatures hit 47°C, requiring extensive ventilation and cooling that consume more power than the actual extraction. Rock bursts become frequent, ground support costs skyrocket, and worker productivity plummets in the hellish conditions. Every meter deeper adds not linear but exponential complexity—and Hindustan Copper's shallow deposits are exhausted.

Environmental regulations have evolved from minor irritant to existential threat. The 2018 Sterlite closure in Tamil Nadu sent shockwaves through the industry—if a private giant with deep pockets couldn't navigate environmental clearances, what chance does a cash-strapped PSU have? Every expansion now requires environmental impact assessments that take years, public hearings that become political theater, and compliance costs that can exceed project economics. The regulatory framework designed for coal and iron ore gets blindly applied to copper, ignoring the metal's strategic importance.

Community relations have transformed from corporate social responsibility to operational necessity. The tribals around Malanjkhand, the farmers near Khetri, the villages around Ghatsila—all have learned to leverage their veto power. Mining leases exist on paper, but social license to operate must be negotiated daily. One blocked road, one protest, one PIL can shut operations for weeks. Private miners might negotiate or relocate; PSUs must accommodate, whatever the cost.

The technology gap widens daily. While BHP deploys autonomous haul trucks in Australia and Codelco uses AI for ore body modeling in Chile, Hindustan Copper struggles to maintain basic equipment. The procurement process for new technology is Kafkaesque: technical specifications, tender preparation, bidding, evaluation, appeals, re-tendering—by the time equipment arrives, it's obsolete. The company operates with technology two generations behind global standards, trying to compete in a business where marginal efficiency determines survival.

Talent retention has become impossible. An underground mining engineer at Hindustan Copper earns ₹15 lakhs annually; the same engineer at a private firm commands ₹40 lakhs plus bonuses. The company has become an unofficial training academy for the private sector, investing in fresh graduates who leave the moment they gain experience. Those who stay are often those who value job security over career growth—hardly the profile for driving innovation in a challenging industry.

The PSU procurement processes deserve special mention in this catalogue of constraints. Buying a laptop requires three quotes, committee approval, and financial concurrence—a three-month process for a ₹50,000 purchase. Imagine procuring million-dollar mining equipment or negotiating technology transfers under these constraints. Private competitors make decisions in days that take Hindustan Copper months, and in commodity markets, timing is everything.

Competition from proposed auction of mineral blocks adds a new dimension of threat. The government's plans to auction copper blocks to private players would end Hindustan Copper's monopoly, exposing it to competition from entities unburdened by legacy costs and social obligations. Private miners would cherry-pick the best deposits, leaving Hindustan Copper with marginal resources and massive overheads—a recipe for irrelevance.

The innovation imperative isn't optional—it's existential. Bioleaching could make low-grade ores viable, in-situ recovery could eliminate mining costs, and AI-driven processing could optimize recovery from complex ores. But innovation requires risk-taking, failure tolerance, and rapid iteration—everything PSU culture inhibits. The company needs Silicon Valley urgency with government accountability, an impossible combination.

Remote location challenges multiply every other problem. Attracting talent to Khetrinagar or Malanjkhand means building entire ecosystems—schools, hospitals, entertainment, connectivity. Young engineers accustomed to Bangalore or Mumbai amenities won't spend careers in mining townships, no matter the mission's importance. The isolation that once protected these operations from scrutiny now prevents them from attracting resources needed for modernization.

Climate change adds another layer of complexity. Extreme weather events disrupt operations, water scarcity affects processing, and carbon regulations threaten economics. The global mining industry is investing billions in decarbonization; Hindustan Copper struggles to maintain basic operations. The company might survive geological challenges only to be rendered unviable by climate regulations.

The skills gap extends beyond engineering to modern mining competencies. Data analytics, automation engineering, environmental management, stakeholder engagement—these aren't traditional mining skills but are now essential. Hindustan Copper's training programs, designed for an era of manual mining, produce engineers unprepared for digital mining's demands. Retraining the existing workforce seems impossible; recruiting new talent equally so.

Yet innovation pockets exist, usually despite rather than because of systems. Individual engineers have developed local solutions—improved ventilation designs, modified drilling patterns, adapted processing techniques. But these innovations remain localized, unable to scale across the organization's silos. The company has innovation capability but lacks innovation culture, the difference between potential and performance.

X. Playbook: Lessons from a Monopoly PSU

The Hindustan Copper playbook reads like a masterclass in organizational survival despite operational impossibility. Here's a company that shouldn't exist—mining uneconomic ore, competing against global giants, serving political masters with commercial expectations—yet persists through a peculiar combination of strategic positioning and bureaucratic resilience.

Lesson one: When commercial viability conflicts with strategic mandate, claim strategic importance louder. Every privatization threat triggered national security concerns, every efficiency drive faced social responsibility arguments. The company learned to weaponize its weakness, arguing that its very inefficiencies—maintaining marginal mines, supporting remote communities—made it indispensable. It's jujitsu corporate strategy: using attackers' force against them.

Managing government stakeholder expectations requires Byzantine sophistication. Different ministries want different things: Mines wants production, Finance wants dividends, Labour wants employment, Environment wants compliance. Hindustan Copper learned to give each constituency just enough to avoid crisis while never fully satisfying anyone. It's perpetual sub-optimization, surviving by preventing any stakeholder from reaching breaking point.

The cost of being the "only player" manifests in unexpected ways. Hindustan Copper must maintain capabilities the market wouldn't support—exploration expertise for deposits nobody wants to find, processing knowledge for ores nobody wants to process, mining skills for resources nobody wants to extract. It's like being the only company making typewriters, maintaining the entire supply chain for a product the market has abandoned.

Navigating political cycles requires institutional amnesia combined with perfect memory. Each new government arrives with fresh ideas—privatization, modernization, expansion—that must be entertained enthusiastically while knowing they'll likely reverse when governments change. The company maintains parallel plans for every political scenario, ready to pivot without appearing inconsistent. It's strategic schizophrenia as survival mechanism.

Building capabilities despite bureaucratic constraints requires guerrilla innovation. Official channels may take years, but informal networks can deliver results in weeks. The best managers maintain shadow systems—unofficial supplier relationships, informal technology transfers, personal networks that bypass official processes. It's organizational insurgency, achieving goals despite the organization.

The privatization that never happened offers its own lessons. By constantly being "about to be privatized," Hindustan Copper avoided both the accountability of public ownership and the efficiency demands of private ownership. It existed in perpetual transition, using uncertainty as shield against reform demands. Sometimes the most powerful strategic position is ambiguity.

The PSU paradox extends beyond economics to psychology. Employees simultaneously feel pride in serving national interest and frustration at operational constraints. This cognitive dissonance creates a unique culture—cynical idealists who believe in the mission while knowing it's impossible. Managing this psychological contradiction requires leaders who can inspire despite reality.

Political navigation demands selective deafness combined with perfect pitch. Knowing which ministerial directives to implement immediately and which to slow-walk requires deep institutional knowledge. The company learned that enthusiastic agreement followed by bureaucratic delay often outlasts political attention spans. It's passive resistance elevated to art form.

The labor relations playbook deserves special study. Unions at Hindustan Copper aren't just protecting jobs; they're defending entire communities built around mines. This gives them extraordinary leverage but also makes them stakeholders in survival. The company learned to make unions partners in political battles, deploying worker protests strategically to block unwanted reforms.

The technology adoption strategy—or lack thereof—reveals another paradox. By being perpetually behind, Hindustan Copper avoided the expensive mistakes early adopters make. While private miners wrote off failed automation investments, Hindustan Copper continued with proven, if obsolete, methods. Sometimes being last has advantages, though probably not the ones shareholders want.

Financial engineering in a PSU context requires creativity within constraints. Unable to access capital markets freely or restructure debt aggressively, Hindustan Copper learned to optimize within narrow parameters. It's like playing chess with only pawns—possible but requiring different strategies than those with full pieces.

The social obligation burden, usually seen as constraint, became competitive moat. No private player would assume Hindustan Copper's social infrastructure costs, making privatization economically unattractive. The company learned to make its liabilities so intertwined with assets that separation became impossible. It's corporate hostage-taking, with entire communities as unwitting participants.

XI. Analysis & Future Scenarios

The bull case for Hindustan Copper requires extraordinary faith in geology and government. Start with the EV revolution: Hindustan Copper's ₹2,000 cr expansion will triple capacity to 12.2 MTPA by FY31, theoretically positioning it to capture surging domestic demand. If ore grades stabilize, if new deposits are discovered, if global copper prices remain elevated, if the government provides capital, if environmental regulations ease—if all these align, Hindustan Copper could triple its market cap within five years.

The infrastructure push adds weight to optimism. Every kilometer of metro rail needs 40 tonnes of copper. Every gigawatt of renewable capacity requires 3,000 tonnes. The government's ₹100 trillion infrastructure pipeline translates to massive copper demand that imports might struggle to fulfill during global supply crunches. Hindustan Copper, as the domestic producer, could command premium prices during supply disruptions.

Strategic importance might finally translate to strategic support. As US-China tensions reshape supply chains, countries are reassessing critical mineral dependencies. India might decide that maintaining domestic copper capability, however sub-optimal, is insurance worth paying. This could mean capital injection, technology partnerships, or protective regulations that improve Hindustan Copper's economics.

But the bear case writes itself with geological inevitability. Ore grades will continue declining—physics, not pessimism. Every percentage point drop in grade doubles extraction costs while global competitors access deposits with grades Hindustan Copper can only dream about. It's like competing in Formula One with a handicap that worsens each lap.

Import competition isn't just about price; it's about reliability. Demand potentially doubling to 3.3 million tonnes by 2030 while India maintains over 90% import dependence means the entire downstream industry is structured around imports. Even if Hindustan Copper tripled production, it would remain marginal to India's needs, unable to influence prices or supply security.

The efficiency challenge compounds annually. While Hindustan Copper struggles with 1990s technology, competitors deploy automation that cuts costs by 30-40%. The productivity gap isn't closing; it's widening. Each year of delayed modernization makes catching up harder, like trying to board an accelerating train.

Stock performance tells its own story of cycles and sentiment. The all-time high of ₹658 in 2010 came during the commodity supercycle when investors believed in the China growth story and India's mining potential. The all-time low of ₹18.25 in March 2020 reflected pandemic panic plus fundamental doubts about the company's viability. Current levels around ₹240 suggest market skepticism tempered by option value—the stock as lottery ticket on copper prices or privatization.

The government's 66.14% stake is definitely more burden than blessing. It prevents genuine board independence, delays decision-making, and prioritizes political over commercial considerations. Yet full privatization remains unlikely given strategic concerns and political resistance. The company remains stuck in ownership purgatory—too government-controlled to be efficient, too strategic to be sold.

The discovery of new ore bodies offers tantalizing possibility but geological improbability. HCL has access to about 45% of India's copper ore reserves and resources as of FY25, but these reserves are mostly low-grade and high-cost. Modern exploration might find deposits, but India's geology simply doesn't favor large copper formations. Hope isn't strategy, and geology doesn't care about national aspirations.

Potential scenarios for 2030 range from irrelevance to modest relevance, never true importance. Best case: Hindustan Copper produces 200,000 tonnes annually from expanded operations, employs 15,000 people, and maintains symbolic importance while India imports 95% of needs. Worst case: declining grades make operations unviable, the company becomes purely an employer of last resort, producing token quantities at massive losses.

The strategic sale prospect under new governments remains perpetually possible, never probable. Each election brings privatization promises that die in implementation details. Who buys assets requiring massive investment for marginal returns? How are social obligations handled? What happens to townships dependent on mining? These questions have no politically acceptable answers.

The financial trajectory seems clear: continued mediocrity punctuated by occasional windfall quarters when copper prices spike. The company will survive—political importance ensures that—but won't thrive. It's corporate purgatory, neither dead nor truly alive, sustained by government life support while markets move on.

XII. "If We Were CEOs" & Closing Thoughts

If we were CEO of Hindustan Copper, the first priority wouldn't be mining—it would be brutal honesty about what's possible. The company cannot and will not achieve copper independence for India. Accepting this reality would liberate strategy from impossible mandates, allowing focus on achievable goals: maintaining strategic capability, developing expertise, and capturing value where geology permits.

Modernization and automation would target specific bottlenecks rather than broad transformation. Forget autonomous haul trucks at every mine; focus on automating the single most constraining process at each operation. At Malanjkhand, that might be ore sorting technology to pre-concentrate before processing. At Khetri, perhaps automated development drilling to accelerate underground expansion. Targeted innovation delivering measurable returns, not showcase projects impressing ministers.

Joint ventures for exploration would acknowledge Hindustan Copper's limitations while leveraging its advantages. Partner with global majors who have technology and capital but need local knowledge and licenses. Structure deals where Hindustan Copper provides access and permits while partners bring expertise and investment. It's strategic humility—admitting what you don't know while monetizing what you do.

Downstream value addition deserves aggressive expansion. The Taloja wire rod plant proves Hindustan Copper can compete when freed from mining's geological constraints. Build more downstream facilities near demand centers, processing imported copper into products India needs. Capture value through manufacturing excellence rather than mining marginal ore. It's pivoting from resource extraction to resource transformation.

ESG and community engagement need radical reimagination. Instead of treating communities as stakeholders to manage, make them genuine partners. Share mine revenues directly with local communities, creating aligned incentives. Transform corporate social responsibility from cost center to value creator by building businesses that serve mining operations while creating local employment. It's stakeholder capitalism with Indian characteristics.

The real closing thought isn't about Hindustan Copper but what it represents: India's struggle between aspiration and reality in resource security. The company embodies every contradiction in Indian industrial policy—wanting self-reliance while avoiding hard choices, demanding commercial returns while imposing non-commercial obligations, celebrating indigenous capability while starving it of resources.

The monopoly that must succeed can't succeed, at least not on terms that matter. Hindustan Copper will never make India copper-independent, never compete globally, never generate returns justifying its existence. But it will continue existing, a monument to the gap between intention and outcome, sustained by political necessity rather than economic logic.

Perhaps that's the real lesson. In a perfect market, Hindustan Copper wouldn't exist. But markets aren't perfect, countries need capabilities beyond commercial logic, and sometimes strategic insurance is worth paying even when claims never come. Hindustan Copper is India's copper insurance policy—expensive, inefficient, but possibly essential in ways we won't understand until we need it.

The tragedy isn't that Hindustan Copper fails commercially; it's that India never developed alternatives. While focused on protecting one inefficient producer, the country missed opportunities to build recycling infrastructure, develop substitution technologies, or secure overseas assets. The monopoly didn't just fail to deliver copper independence; it prevented exploration of other paths to copper security.

Looking forward, Hindustan Copper's fate seems sealed: perpetual mediocrity punctuated by political drama. It will announce expansions that underdeliver, attempt modernizations that underwhelm, and continue producing enough copper to matter politically but not economically. It's corporate suspended animation, neither truly living nor allowed to die.

The final irony is that Hindustan Copper's survival might be its greatest failure. By existing, it provides political cover for avoiding harder decisions about resource security. By producing token quantities, it maintains the fiction of domestic capability. By employing thousands, it prevents serious discussion of alternatives. Sometimes the kindest thing for a patient is acknowledging terminal condition; Hindustan Copper's disease is geology, and there's no cure for that.

India needs copper security, but Hindustan Copper can't provide it. India needs mining expertise, but protecting inefficient operations won't develop it. India needs resource strategy, but maintaining monopolies won't create it. The company stands as a warning: good intentions without good economics lead nowhere good. In trying to control copper, India lost the copper game. The monopoly meant to ensure independence instead enshrined dependence, proving that in commodities as in life, geology is destiny, and destiny doesn't care about national plans.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube