MedPlus Health Services: India's Pharmacy Giant

I. Introduction & Episode Roadmap

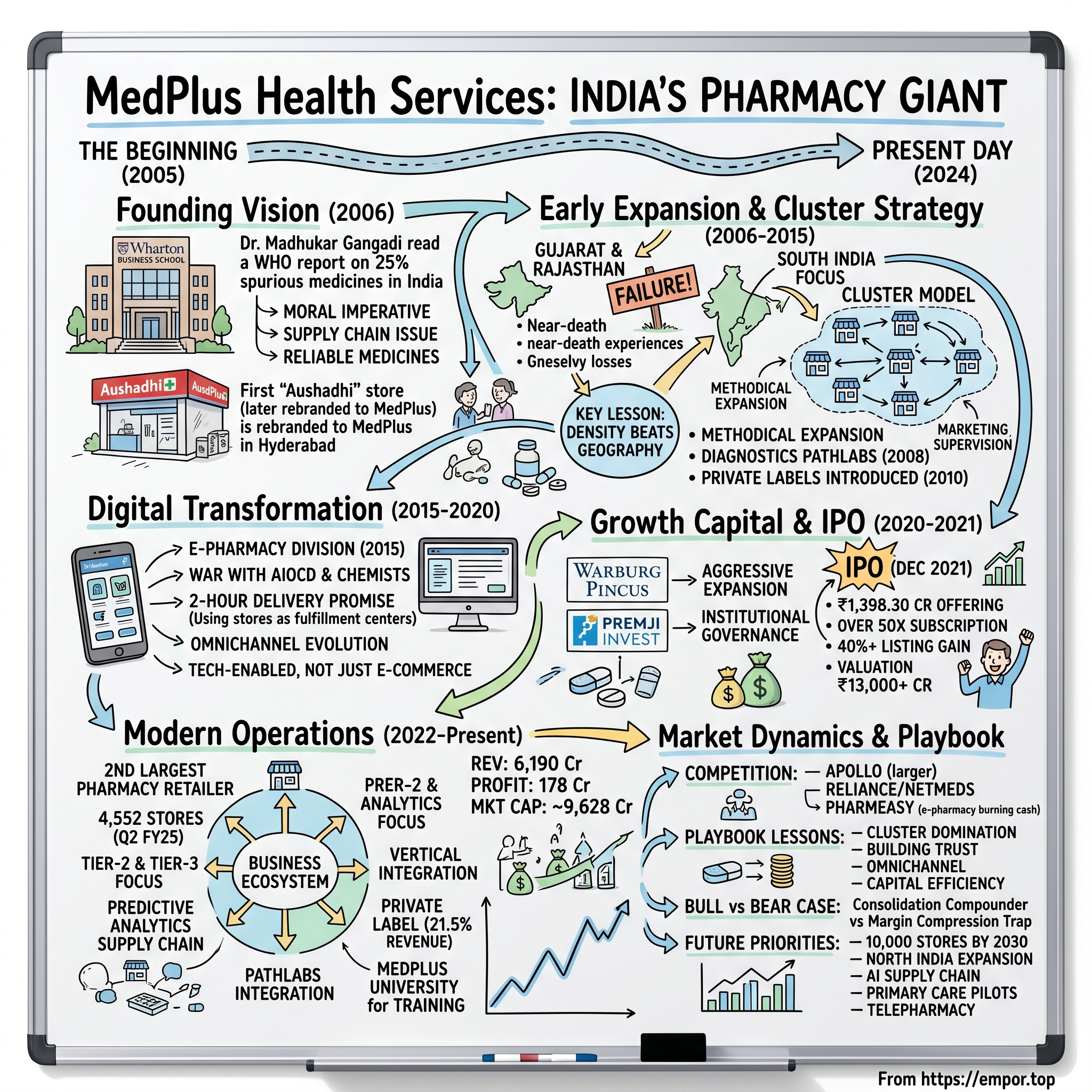

Picture this: A doctor sits in a Wharton Business School classroom in 2005, reading a World Health Organization report that makes his blood run cold. Nearly 25% of medicines sold in India could be spurious—fake, substandard, or contaminated. For most MBA students, this would be just another case study. For Dr. Madhukar Gangadi, it was a call to arms that would reshape India's pharmacy landscape forever.

Fast forward to 2024, and that moment of revelation has transformed into MedPlus Health Services—India's second-largest pharmacy chain with over 4,230 stores sprawling across 600 cities. The company commands a market capitalization approaching ₹10,000 crores, serves millions of customers daily, and has fundamentally altered how Indians buy medicines. Yet this isn't just another retail success story. It's a tale of how a doctor-turned-entrepreneur battled entrenched interests, survived near-death experiences in western expansion, and built a pharmacy empire that went public at the height of a global pandemic.

The central question we're exploring today isn't just how MedPlus became what it is—it's how a company founded on the simple premise of "genuine medicines" managed to crack the code of India's notoriously fragmented pharmacy market, where 89% of outlets remain mom-and-pop stores. How did they convince skeptical consumers to abandon their neighborhood chemist? Why did their cluster strategy succeed where others failed? And perhaps most intriguingly, how did they manage to thrive in both the physical and digital worlds while pure-play e-pharmacies with billions in funding struggled?

This is a story of methodical expansion, strategic retreats, and the patient capital required to build trust in healthcare retail. We'll journey from that first store in Hyderabad's Dilsukhnagar neighborhood to boardroom battles with private equity giants, from regulatory showdowns with traditional chemist associations to the nerve-wracking days of their IPO roadshow. Along the way, we'll uncover the playbook that turned a doctor's mission into India's pharmacy consolidation story—and why the next chapter might be even more dramatic than the first.

II. Founding Story & The Doctor's Vision (2006)

The year 2006 wasn't particularly auspicious for Indian retail. The economy was growing, yes, but organized retail was still fighting for legitimacy. Big Bazaar was just finding its feet, Reliance Retail was yet to launch, and the idea of chain pharmacies seemed almost absurd in a country where your local chemist knew your family's medical history better than you did. Into this skeptical market walked Dr. Madhukar Gangadi, armed with an MBBS degree, a fresh Wharton MBA, and a burning conviction that India's pharmacy sector was broken.

The WHO report that catalyzed Madhukar's journey wasn't just statistics—it was a damning indictment of India's drug distribution system. The report suggested that spurious drugs weren't just a fringe problem but potentially a quarter of all medicines sold. For a trained doctor who had taken the Hippocratic oath, this wasn't just a business opportunity; it was a moral imperative. "I couldn't sleep properly after reading that report," Madhukar would later recall in interviews. "Every fake medicine sold could mean a life lost, a treatment failed, a family destroyed."

But conviction alone doesn't build businesses. Madhukar's genius lay in recognizing that the spurious drug problem wasn't just about criminal intent—it was a supply chain issue. The traditional pharmacy model in India involved multiple intermediaries, each adding their markup and, crucially, breaking the chain of accountability. A medicine could change hands four or five times before reaching the consumer, making it nearly impossible to guarantee authenticity. His solution was radical for its simplicity: buy directly from manufacturers, create a traceable supply chain, and build stores that customers could trust.

The first MedPlus store—though it wasn't called that yet—opened in Hyderabad's Dilsukhnagar area under the name "Aushadhi," a Sanskrit word meaning medicine. The choice of location was deliberate: a middle-class neighborhood where families were aspirational enough to try organized retail but price-conscious enough to appreciate value. The store looked nothing like traditional pharmacies—it was bright, air-conditioned, with medicines displayed clearly with prices marked. No haggling, no dubious generics pushed by commission-hungry salesmen, no expired drugs hidden in dark corners. The early days were brutal. Customers would walk in, look around suspiciously, and walk out. Initially operating under the Aushadhi brand name, it was rebranded as MedPlus after the opening of the first 48 stores. The rebranding wasn't just cosmetic—it represented a strategic pivot. "Aushadhi" sounded traditional, almost governmental. "MedPlus" conveyed modernity, value addition, and aspiration. It was a name that could scale beyond Hyderabad, beyond South India, potentially across the nation.

What made Madhukar's approach revolutionary wasn't just the organized retail format—it was his obsession with the supply chain. While competitors focused on store ambiance or discounts, MedPlus invested heavily in backend infrastructure. They built relationships directly with pharmaceutical manufacturers, cutting out the labyrinth of distributors and sub-distributors that plagued traditional pharmacies. Every medicine could be traced back to its source. In an industry where trust was everything and skepticism was the default, this was their differentiator.

The funding for this ambitious venture came from an unlikely source. Madhukar had managed to convince a group of investors, including some Non-Resident Indians who had seen the pharmacy consolidation play out in the US market. They understood that what CVS and Walgreens had done in America, someone would eventually do in India. The question was who would execute it successfully in a market with completely different dynamics—where customers expected credit, where prescriptions were often verbal, where the chemist was as much a healthcare advisor as a retailer.

By the end of 2006, MedPlus had opened a handful of stores, all in Hyderabad. The numbers were modest—daily sales per store averaged just ₹15,000-20,000, a fraction of what established neighborhood pharmacies were doing. But Madhukar noticed something interesting in the data: repeat customer rates were climbing steadily. Once customers tried MedPlus and experienced the consistency—the same price, the same quality, the same service every time—they kept coming back. This wasn't just retail; it was behavior change at scale.

The India that MedPlus was born into was transforming rapidly. The economy was growing at 8-9% annually, the middle class was expanding, and chronic diseases were becoming increasingly common as lifestyles changed. The pharmacy market, valued at roughly ₹40,000 crores in 2006, was projected to double within a decade. Yet 95% of it remained unorganized—a massive opportunity for anyone who could crack the code of trust, scale, and economics. As 2006 turned to 2007, Madhukar and his small team prepared for their first major expansion—a move that would nearly kill the company before it truly began.

III. Early Expansion & The Cluster Strategy (2006–2015)

The conference room in MedPlus's modest Hyderabad office was thick with tension in early 2007. Madhukar Gangadi stood before a map of India, colored pins marking their existing stores—all clustered in Hyderabad like a tight constellation. The board wanted aggressive expansion. Some investors pushed for Delhi, others for Mumbai. But Madhukar's finger traced a different path—to Gujarat and Rajasthan. "We go west," he declared, a decision that would become the company's first near-death experience.

The company opened pharmacies in the western states of Gujarat and Rajasthan in 2007 but had to shut down and exit operations due to recurring losses. What happened in Gujarat and Rajasthan wasn't just a setback—it was a masterclass in how not to expand in Indian retail. MedPlus had assumed that their Hyderabad model—clean stores, genuine medicines, fixed prices—would translate seamlessly. They hadn't accounted for the radically different business culture. In Gujarat, family-owned pharmacies had operated for generations, often providing medicines on credit for months. Customers expected negotiation on everything, even on ₹10 strips of Paracetamol. The MedPlus model of fixed pricing seemed rigid, almost disrespectful to local customs.

The numbers were devastating. By late 2007, the western stores were bleeding ₹50 lakhs monthly. Footfalls were a tenth of what they saw in Hyderabad. The company had signed expensive long-term leases, hired staff, invested in inventory—all sunk costs now. In a painful board meeting in early 2008, Madhukar made the call: complete withdrawal from the western markets. It was humiliating, but it taught them a crucial lesson that would define their entire expansion strategy: density beats geography.

This failure birthed what would become MedPlus's signature strategy—the cluster model. Instead of spreading thin across India, they would dominate neighborhood by neighborhood, city by city, state by state. The logic was compelling. In a cluster, you could share inventory between stores, reducing working capital needs. Marketing costs could be amortized across multiple outlets. A single area manager could supervise 10-15 stores efficiently. Most importantly, word-of-mouth traveled faster in dense networks. If Mrs. Reddy in Banjara Hills had a good experience, her entire kitty party would know about it.

The execution of this cluster strategy in South India from 2008 to 2015 was methodical, almost surgical. They would identify a neighborhood, open 3-4 stores within a 2-kilometer radius, and only move to the next area once these stores hit profitability. In Hyderabad alone, they went from 48 stores in 2007 to over 200 by 2010. Each new store would cannibalize 15-20% of sales from nearby MedPlus outlets initially, but total market share would grow by 40-50%. They were creating a fortress that competitors couldn't penetrate.

In 2008, it opened diagnostics centers in five cities under its subsidiary MedPlus Pathlabs. This wasn't just diversification—it was strategic integration. Diagnostic services created a flywheel effect. Patients getting tests done would fill their prescriptions at MedPlus pharmacies. The pharmacy staff would recommend MedPlus PathLabs for tests. The data from both businesses provided insights into disease patterns and medication adherence that no standalone pharmacy could match.

The PathLabs venture also revealed something fascinating about Indian healthcare consumption. While customers were price-sensitive about medicines, they were willing to pay premiums for diagnostic services if they trusted the quality. MedPlus PathLabs could charge 10-15% more than local labs because customers believed in the brand's promise of authenticity—a trust transferred from their pharmacy experience.

By 2010, MedPlus had crossed 500 stores, all in South India. The economics were finally working. Mature stores (over 18 months old) were generating ₹45-50 lakhs in annual revenue with EBITDA margins of 6-7%. The company introduced private label products—generic medicines manufactured by reputed companies but sold under the MedPlus brand at 30-40% discounts. Customers initially resisted, but aggressive marketing and pharmacist education drove adoption. By 2012, private label contributed 12% of revenues but 20% of gross margins.

The period from 2012 to 2014 saw MedPlus perfect its playbook. New store openings were reduced to a science. They had identified that stores needed 3,000-4,000 households within a 1-kilometer radius to be viable. The ideal store size was 600-800 square feet—large enough to stock 8,000 SKUs but small enough to keep rents manageable. They discovered that stores near hospitals did 3x the revenue but had lower margins due to the emergency nature of purchases. Residential stores had lower revenues but better margins and customer loyalty.

It relaunched stores in Ahmedabad, Gujarat in 2014. This second attempt at western expansion was different. They entered with humility, adapting their model to local preferences. Credit was offered selectively. Gujarati-speaking staff were hired. Prices were kept flexible for bulk purchases. The stores began working, validating that the cluster model could travel—if executed with cultural sensitivity.

As 2015 approached, MedPlus had quietly built one of India's largest pharmacy chains with over 1,500 stores. They had survived a near-death experience, discovered their winning strategy, and built a profitable business in one of India's most challenging sectors. But the landscape was about to shift dramatically. Technology was disrupting every industry, and pharmacy would be no exception. The digital transformation that followed would test whether a company built on physical retail could evolve—or whether it would be disrupted by venture-funded startups that didn't even have stores.

IV. Digital Transformation & Omnichannel Evolution (2015–2020)

The MedPlus headquarters in Hyderabad buzzed with unusual energy in January 2015. Software engineers—a rare sight in a pharmacy company—huddled around laptops, while Madhukar Gangadi stood before a whiteboard covered with flowcharts and user journey maps. The topic of intense debate: whether MedPlus should launch an online pharmacy. The old guard of retail managers warned it would cannibalize store sales. The younger team members argued it was inevitable—adapt or die. What followed was a transformation that would pit MedPlus against both traditional chemists and silicon valley-style startups.

In 2015, it started its e-pharmacy division. The timing seemed perfect. Smartphones were proliferating, data costs were plummeting, and urban Indians were getting comfortable ordering everything online. But MedPlus's entry into e-pharmacy triggered a war they hadn't fully anticipated. The AIOCD (All India organization of Chemists & Druggists) called for a nationwide strike on 14 October 2015 against online sale of drugs and criticized ePharmacies like MedPlusMart.com as illegal and a threat to the interests of around 8.5 lakhs chemists around India.

The strike was just the visible part of the battle. Behind the scenes, legal notices flew, political pressure mounted, and MedPlus found itself in an unusual position—too traditional for the VCs funding pure-play e-pharmacies, too modern for the traditional chemist associations. Store managers reported instances of local chemist associations threatening MedPlus staff, spreading rumors about online medicines being fake, even organizing customer boycotts.

But Madhukar's team had an advantage that pure online players lacked—1,500+ physical stores that could serve as fulfillment centers. While competitors like PharmEasy and Netmeds were burning cash building warehouse infrastructure, MedPlus could fulfill orders from the nearest store, often delivering within 2 hours in metro cities. The unit economics were compelling: online orders had 20% higher average order values but could be fulfilled using existing store inventory and staff during lean hours.

The technology build-out was surprisingly sophisticated for a traditional retailer. MedPlus didn't just create a basic e-commerce site; they built a comprehensive digital health platform. Customers could store prescriptions, set medicine reminders, access drug information, and consult with pharmacists via chat. The app used machine learning to predict refill dates for chronic medications, sending timely reminders. By 2017, the platform had over 2 million registered users, though active monthly users were around 200,000—a engagement challenge that plagued all e-pharmacies.

What really differentiated MedPlus's digital strategy was the seamless integration with offline operations. A customer could order online and pick up from a store, avoiding delivery charges. Store staff were incentivized for orders originating from their catchment area, preventing channel conflict. If a medicine wasn't available in one store, the system automatically checked nearby stores, ensuring fulfillment rates above 95%—industry-leading metrics that pure online players struggled to match.

The competitive landscape was heating up dramatically. In 2015, the online pharmacy market was valued at just $50 million. By 2018, it had grown to $500 million, attracting over $400 million in venture funding. PharmEasy raised $50 million, Netmeds secured $35 million, and 1mg closed a $70 million round. These companies were offering discounts that defied logic—40% off on medicines that had regulated margins of 16-20%. The game was clear: burn cash, acquire customers, hope for consolidation. MedPlus's response was strategic rather than reactive. Instead of matching the unsustainable discounts, they focused on service differentiation. The 2-hour delivery promise became their calling card. While competitors struggled with 24-48 hour delivery windows, MedPlus leveraged their store network to deliver medicines faster than pizza. They introduced "MedPlus Express"—a service where customers could WhatsApp prescriptions and have medicines delivered before the next dose was due.

The numbers tell the story of this digital transformation. As of 30 September, 2021, 8.44% of the company's revenue can be attributed to online sales. This might seem modest compared to pure-play e-pharmacies, but the profitability profile was dramatically different. MedPlus's online orders had positive unit economics from day one, while competitors were losing ₹200-300 per order. The reason was simple: MedPlus wasn't building a business from scratch; they were adding a channel to an existing profitable operation.

The omnichannel strategy also revealed unexpected insights about consumer behavior. Customers who used both online and offline channels had 2.5x higher lifetime value than single-channel users. They discovered that chronic patients preferred online for regular refills but visited stores for acute medications. Young mothers ordered baby products online but came to stores for pediatric medicines, wanting the reassurance of speaking to a pharmacist.

By 2019, MedPlus had quietly built one of India's most sophisticated pharmacy operations. Their technology stack included inventory management systems that could predict demand patterns at store level, a CRM system tracking 10 million+ customers, and logistics capabilities that rivals envied. They weren't the loudest player in e-pharmacy, but they were arguably the most sustainable.

The COVID-19 pandemic in early 2020 would test every assumption about pharmacy retail. For pure online players, it seemed like the moment of triumph. For traditional retailers, it looked like an existential crisis. For MedPlus, positioned uniquely in the middle, it would become the catalyst for their most ambitious move yet—going public in the midst of the greatest health crisis in a century.

V. The Private Equity Journey: Warburg Pincus & Premji Invest (2020–2021)

The Zoom call in April 2020 had an unusual energy for a board meeting conducted during nationwide lockdown. Madhukar Gangadi sat in his home office in Hyderabad, while private equity partners dialed in from Mumbai, Singapore, and New York. The topic of discussion would have seemed absurd just months earlier: should MedPlus raise capital and prepare for an IPO during a global pandemic? The existing investors—Mount Kellett Capital Management, TVS Capital Funds, and Ajay Piramal's India Venture Advisors, who together owned about 69% stake—were divided. Some wanted to wait for normalcy; others saw a once-in-a-lifetime opportunity.

The pandemic had created a perfect storm for MedPlus. Demand for medicines had spiked 40% as customers stockpiled chronic medications. The government had declared pharmacies essential services, allowing them to operate during lockdowns when most retail was shut. Digital adoption had accelerated by five years in five weeks—even 60-year-old customers were now comfortable ordering medicines online. Yet the company needed capital to capitalize on this momentum. New store openings had been paused, working capital requirements had ballooned, and technology investments were crucial to handle the digital surge.

Enter Azim Premji's investment arm PremjiInvest, which picked up a minority stake for INR 200 Cr and did a follow-on investment of around INR 100 Cr. The Premji investment was more than just capital—it was a validation from one of India's most respected business families. Premji's team had spent months analyzing the pharmacy consolidation thesis. Their conclusion: India's ₹1.5 lakh crore pharmacy market would inevitably consolidate, and omnichannel players like MedPlus were best positioned to win.

The negotiations with Warburg Pincus were even more interesting. MedPlus was reportedly in talks with the private equity firm to raise INR 1,500 Cr ($203 Mn) in a mix of debt and equity. Warburg had missed the early innings of India's consumer story—they had passed on DMart, missed Nykaa, and watched Blackstone make a fortune on Aakash Institute. They weren't going to miss pharmacy consolidation. The due diligence was exhaustive: store-level P&Ls for 2,000+ outlets, technology architecture reviews, regulatory compliance audits across seven states, and crucially, understanding the founder's vision for the next decade.

The final deal structure was clever financial engineering. Warburg Pincus and Premji Invest together invested in a combination of primary and secondary shares. The primary capital would fund expansion—500 new stores annually, technology upgrades, and working capital. The secondary sale allowed early investors some liquidity while keeping them invested for the IPO upside. o3 Capital acted as the sole financial advisor, structuring a deal that aligned all stakeholders.

What made these PE investments transformative wasn't just the capital but the governance changes they brought. MedPlus had operated like a large family business—Madhukar made most decisions, processes were informal, and financial reporting was basic. The PE investors insisted on institutional changes: independent directors were appointed, an audit committee was established, and monthly MIS reporting was implemented. The company hired a CFO from a Big Four background, a Chief Technology Officer from Flipkart, and a Chief Marketing Officer from Hindustan Unilever.

The PE partners also pushed for strategic clarity. Should MedPlus focus on store expansion or digital growth? Should they enter diagnostics aggressively or stay focused on pharmacy? The answer, crystallized through months of strategy sessions, was elegant: MedPlus would be "digital at the core, physical at the scale." Every physical store would be digitally enabled, every digital customer would have access to physical services. It wasn't about choosing channels but integrating them seamlessly.

The valuation discussions revealed the changing perception of MedPlus in the investment community. In 2015, when e-pharmacy was hot, MedPlus's physical stores were seen as legacy baggage. By 2020, as pure-play e-pharmacies burned cash without path to profitability, MedPlus's omnichannel model was seen as visionary. The company was valued at over ₹8,000 crores in the Warburg round, up from ₹2,000 crores just three years earlier.

But the real value PE investors brought was preparation for public markets. They insisted on quarterly earnings calls, even though the company was private. They required segment reporting—separating pharmacy, diagnostics, and online operations. They pushed for transparency on metrics that mattered: same-store sales growth, customer acquisition costs, inventory turns. By mid-2021, MedPlus was running like a public company, just without the public scrutiny.

The PE period also saw aggressive expansion despite the pandemic. While competitors paused, MedPlus accelerated, opening 400+ stores in FY2021. They entered new markets—Madhya Pradesh and Chhattisgarh—taking advantage of distressed real estate prices. They acquired small pharmacy chains at attractive valuations as mom-and-pop stores struggled with lockdown losses. The war chest from PE funding allowed them to play offense when others were playing defense.

As 2021 progressed, the IPO preparation moved from possibility to inevitability. The equity markets were booming, retail participation was at all-time highs, and healthcare stocks were commanding premium valuations. Zomato's successful listing had proven that Indian retail investors would back consumer businesses with long-term potential. The only question was timing. The answer would come from an unlikely source—the company's investment bankers, who presented data showing that December 2021 represented a unique window before the US Federal Reserve's expected rate hikes. MedPlus would have exactly one shot at the perfect IPO.

VI. The IPO Story: Going Public During COVID (2021)

The war room at Kotak Mahindra Capital's Mumbai office hummed with nervous energy on December 10, 2021. Investment bankers hunched over laptops, finalizing the red herring prospectus, while Madhukar Gangadi participated via video from Hyderabad—COVID protocols still keeping key players apart. Outside, the Omicron variant threatened another wave. Inside, the team was making final decisions on what would become one of India's most successful healthcare IPOs during the pandemic era.

The MedPlus Health IPO, opening on December 13, 2021, was structured as a ₹1,398.30 Crores offering—₹600 crores in fresh capital and ₹798.30 crores as an offer for sale by existing shareholders. Priced at ₹796 per share, it was aggressive by any measure. The company was asking investors to value it at nearly ₹10,000 crores, or about 50 times FY2021 earnings. For context, Apollo Hospitals, with decades of history and a proven healthcare ecosystem, traded at 35 times earnings.

The anchor book building on December 9 became a litmus test. If sophisticated institutional investors balked, the IPO would struggle. The response was electric—₹417.98 crore worth of shares were placed with anchor investors including Goldman Sachs, Morgan Stanley, and HDFC Mutual Fund. These weren't just momentum investors riding the IPO wave; these were long-term funds betting on India's healthcare consolidation story.

But the real drama unfolded during the three-day public subscription window. Day one saw cautious interest—1.2x subscription, mostly from institutional investors. Retail investors, burned by recent IPO underperformances, stayed on the sidelines. The MedPlus management team, watching subscription data in real-time, made a crucial decision: instead of panicking, they doubled down on their story. Madhukar appeared on CNBC, ET Now, and Bloomberg, not promoting the stock but explaining the business model with professorial clarity.

The messaging was crisp: MedPlus wasn't a COVID beneficiary that would struggle post-pandemic. They were building infrastructure for India's healthcare future. Every data point reinforced this narrative—75% of new stores turning profitable within six months, 11% store-level EBITDA margins for mature outlets, and crucially, positive unit economics on online orders when competitors were bleeding cash.

By day three, the momentum had shifted dramatically. The IPO closed with 52.59 times oversubscription. The retail portion was subscribed 7.5 times, institutional portion 119 times, and HNI portion 68 times. The numbers were staggering—over ₹70,000 crores worth of bids for a ₹1,398 crore offering. It wasn't just oversubscription; it was validation of a business model that many had doubted.

Shares of MedPlus were listed on BSE and NSE on 23rd December. They were made available at a premium of 31 per cent. But the price ended at a gain of more than 40%, which is considered a big jump for MedPlus's debut trade. The listing day pop to ₹1,119 meant the company's market capitalization touched ₹13,372 crore, making early investors significantly wealthier and validating the pricing strategy.

The use of proceeds from the fresh issue revealed MedPlus's post-IPO strategy. ₹250 crores for new stores, ₹150 crores for technology and warehouse infrastructure, and ₹200 crores for working capital and general corporate purposes. Unlike tech startups that raised money for undefined "growth initiatives," MedPlus had specific, measurable deployment plans. Every rupee was allocated to revenue-generating activities with defined return expectations.

What made the MedPlus IPO remarkable wasn't just its success but its timing. December 2021 was a graveyard for IPOs—Paytm had crashed 27% on listing just weeks earlier, wiping out ₹40,000 crores in market value. Global markets were jittery about the Omicron variant and impending Fed rate hikes. Yet MedPlus not only priced aggressively but delivered stellar listing gains. The difference? Profitability. While new-age companies promised profits in the distant future, MedPlus had been profitable for years.

The IPO also marked a cultural shift for MedPlus. From a privately held company where Madhukar could make long-term bets without quarterly scrutiny, they now had to manage street expectations. The first earnings call post-IPO was revealing. Analysts grilled management on same-store sales growth, questioned the sustainability of margins, and demanded guidance on store additions. Madhukar, the doctor-turned-entrepreneur, had to learn the language of Wall Street—or rather, Dalal Street.

The retail investor participation told another story—the democratization of wealth creation. A pharmacy assistant in Hyderabad who had bought 18 shares (the minimum lot) saw her ₹14,328 investment become worth ₹20,000 on listing day. Thousands of small investors, many of them MedPlus customers who understood the business intuitively, participated in the IPO. It wasn't just capital raising; it was community building.

The international investor interest was particularly noteworthy. Sovereign wealth funds from Singapore and Norway, pension funds from Canada, and hedge funds from New York all participated. Their thesis was simple: India's healthcare spending would grow from $150 billion to $500 billion by 2030. Organized pharmacy, currently at 11% penetration, would likely reach 30-40% following patterns seen in developed markets. MedPlus, as the second-largest player with proven execution, was a proxy for this mega-trend.

Post-listing, as the stock price stabilized around ₹1,000 levels, the real work began. Public markets are unforgiving—every quarter brings judgment, every competitor move triggers questions, every regulatory change causes volatility. But MedPlus had crossed the Rubicon. From a single store in Dilsukhnagar to a ₹13,000 crore public company, the journey had been remarkable. The question now was whether they could deliver on the ambitious promises made during the IPO roadshow.

VII. Modern Operations & Business Model (2022–Present)

Walk into a MedPlus store in Bangalore's Koramangala neighborhood at 8 PM on a weekday, and you'll witness a retail operation that would make Amazon jealous. A customer enters with a prescription, the pharmacist scans it, and within seconds, the system checks inventory across 15 nearby stores. If a medicine isn't available, it's automatically ordered from the central warehouse for 6 AM delivery. The customer gets an SMS update and can choose home delivery or store pickup. This seamless experience, replicated across 4,552 stores as of Q2 FY25, represents the modern MedPlus—a technology company that happens to sell medicines.

MedPlus is the 2nd largest pharmacy retailer in India, with 4,552 stores across 12 states and 1 union territory as of Q2 FY25. But what makes these numbers remarkable isn't just scale—it's the velocity of expansion with quality. The stores increased with 108 net new stores added in Q2 FY2025, of which 71 were in Tier-2 and Tier-3 cities. This tier-2/3 focus isn't accidental. While competitors fight over metro customers with unsustainable discounts, MedPlus is building moats in Vijayawada, Coimbatore, and Bhubaneswar—cities where organized pharmacy penetration is under 5% and customer acquisition costs are a fraction of metros.

The unit economics of a MedPlus store in 2024 would make any retailer envious. MedPlus has allowed it to maintain a healthy store level economics and an average revenue per store of Rs.1.59 crore in FY21. In comparison, the domestic pharmacy retail industry sported an average revenue per store of just Rs.0.23 crore. This 7x advantage over industry average isn't luck—it's the result of obsessive optimization. Stores are sized at 600-800 square feet, keeping rents under 4% of revenues. Inventory turns 12 times annually versus industry average of 6 times. Staff costs are managed through technology—one pharmacist can manage what previously required three people.

The private label revolution at MedPlus deserves special attention. private label at 21.5% revenue might seem modest compared to global retailers like CVS (30%+), but in Indian pharmacy context, it's revolutionary. MedPlus doesn't just slap their label on generic products. They've created sub-brands—"MedPlus" for medicines, "EatRite" for nutrition, "Curae" for personal care—each with distinct positioning. The margins are compelling: while branded medicines yield 16-20% gross margins, private label delivers 40-45%.

But private label in pharmacy isn't just about margins—it's about trust. When a customer buys MedPlus-branded Paracetamol at 50% discount to Crocin, they're making a trust decision. MedPlus has cracked this code through radical transparency. Every private label medicine displays the manufacturer's name, manufacturing date, and quality certifications prominently. They've partnered with companies like Cipla and Aurobindo—names customers recognize and trust. It's not hiding behind private label; it's leveraging it for value creation.

The diagnostic services expansion through PathLabs represents MedPlus's ambition beyond pharmacy. Operating in select cities, these labs aren't competing with Dr. Lal's or Thyrocare on scale but on integration. A diabetic patient getting HbA1c tests at PathLabs has their results integrated with their medication history from MedPlus pharmacy. The pharmacist can flag medication adherence issues, suggest dose adjustments, and schedule follow-up tests. It's not just cross-selling; it's creating a healthcare ecosystem. The technology backbone of modern MedPlus deserves its own Harvard Business School case study. The company runs a proprietary ERP system that tracks every pill from manufacturer to customer. When a customer buys a strip of antibiotics, the system automatically triggers reorder points, adjusts store-level forecasts, and even predicts seasonal demand spikes. This isn't just inventory management—it's predictive analytics that reduces stockouts to under 2% while keeping inventory days at 30, half the industry average.

The omnichannel integration has reached a sophistication that pure-play competitors can't match. As of 30 September, 2021, 8.44% of the company's revenue can be attributed to online sales. But more importantly, the online channel acts as a data collection engine. Every search query, abandoned cart, and purchase pattern feeds into algorithms that optimize offline operations. If customers in Bangalore's Whitefield area are searching for a particular diabetes medicine online, the nearby stores automatically increase stock levels.

The warehouse and distribution network represents hidden competitive advantage. MedPlus operates nine major warehouses strategically located to serve store clusters within 4-6 hour drive time. Unlike competitors who rely on third-party logistics, MedPlus owns its entire supply chain—from temperature-controlled trucks to last-mile delivery bikes. This vertical integration ensures medicine quality (critical for temperature-sensitive drugs) while reducing logistics costs to 2.5% of revenue versus industry average of 4%.

The human capital strategy at MedPlus challenges conventional retail wisdom. While competitors hire minimum-wage staff and suffer 50%+ attrition, MedPlus invests in pharmacist training and career development. Every store manager starts as a pharmacist, creating deep technical expertise at the frontline. The company runs "MedPlus University," training 2,000+ pharmacists annually on topics from drug interactions to customer psychology. The result: employee attrition under 20% and customer satisfaction scores above 90%.

Looking at financial performance, Mkt Cap: 9,628 Crore (up 25.5% in 1 year) · Revenue: 6,190 Cr · Profit: 178 Cr. The pre-tax margin of around 3% might seem thin, but in pharmacy retail, this is actually healthy. The company has also managed to remain debt-free, providing flexibility for aggressive expansion without dilution or interest burden.

The store expansion strategy has evolved from pure growth to intelligent densification. Instead of racing to 10,000 stores, MedPlus focuses on market share within existing clusters. In Hyderabad, they operate 400+ stores with 35% market share—creating a density that makes them unavoidable for customers and unassailable for competitors. This cluster dominance creates a virtuous cycle: better supplier terms, lower marketing costs, higher brand recall, and ultimately, superior economics.

As we examine MedPlus's current operations, what emerges is a picture of a company that has transcended its origins as a simple pharmacy chain. It's a data-driven, technology-enabled, vertically integrated healthcare platform masquerading as a retail business. The question isn't whether MedPlus can compete with online pharmacies or traditional retailers—it's whether anyone can compete with MedPlus's unique combination of physical density and digital capability.

VIII. Competition & Market Dynamics

In the gleaming headquarters of Apollo Pharmacy in Chennai, executives pore over heat maps showing MedPlus store locations creeping closer to their strongholds. Meanwhile, in Mumbai, Reliance's Netmeds team analyzes why their customer acquisition costs are 3x higher in markets where MedPlus operates. And in Gurgaon's startup corridors, PharmEasy's leadership debates whether to continue their cash-burning growth strategy or pivot to profitability like MedPlus. This is the chess game of Indian pharmacy retail in 2024—a three-way battle between traditional chains, venture-funded e-pharmacies, and omnichannel players, with MedPlus uniquely positioned in the sweet spot.

Apollo Pharmacy remains the only larger competitor, with 5,500+ stores to MedPlus's 4,500+. But the Apollo comparison reveals MedPlus's strategic choices. Apollo leverages its hospital network, with 30% of pharmacy stores located within or near Apollo hospitals. This gives them captive customers but limits expansion flexibility. MedPlus, unburdened by hospital infrastructure, can open stores anywhere—from metro high-streets to tier-3 residential colonies. Apollo's revenue per store is 20% higher, but MedPlus's EBITDA per store is comparable due to lower occupancy costs and operational efficiency.

The online pharmacy wars of 2018-2022 seemed existential for traditional players, but the dust has settled in unexpected ways. PharmEasy, despite raising over $1.5 billion and acquiring Medlife for $250 million, struggles with unit economics. Their customer acquisition cost exceeds ₹500, while lifetime value barely crosses ₹2,000. Tata's 1mg, backed by the conglomerate's deep pockets, focuses on diagnostics and teleconsultation but hasn't cracked pharmacy profitability. Reliance's Netmeds, acquired for ₹620 crores, operates as a loss leader within Reliance Retail's ecosystem play.

The organised retailers in India's pharmacy and wellness space are expected to grow at a CAGR of 25% between 2020 and 2025 to $36 billion. Yet this growth isn't evenly distributed. The penetration of the organised pharmacy retail in India is at 11%. The remaining 89% isn't just opportunity—it's a complex ecosystem of relationships, credit arrangements, and hyperlocal dynamics that organized players must navigate carefully.

Regional competitors add another layer of complexity. In Kerala, Neethi Medical Store's 300+ outlets dominate through community connections. In Mumbai, Wellness Forever's 350+ stores compete on premiumization. In Delhi, Apollo's subsidiary Sanjivani's aggressive pricing challenges everyone. Each region has its champion, forcing national players like MedPlus to adapt their playbook locally while maintaining operational consistency.

The consolidation thesis driving investment in pharmacy retail rests on compelling global precedents. In the US, top 3 chains control 70% of the market. In China, organized pharmacy grew from 15% to 45% penetration in just 10 years. India, with its massive population, growing healthcare spending, and increasing insurance coverage, seems primed for similar consolidation. But India isn't China or America—it's a market where a customer might use PharmEasy for convenience, visit MedPlus for chronic medicines, and still trust the neighborhood chemist for emergency needs. MedPlus's competitive strategy against e-pharmacies is particularly instructive. Instead of competing on discounts—a game they'd lose—they compete on trust and convenience. A chronic patient needs reliability more than 10% extra discount. MedPlus guarantees medicine availability, offers credit to regular customers, and provides consultation services that apps can't match. Their pharmacists know customers by name, remember their conditions, and proactively remind about refills. It's high-touch service in a high-tech world.

The regulatory environment adds another layer of complexity. E-pharmacy regulations remain unclear, with periodic threats of bans and restrictions. Physical pharmacies need licenses for each store, creating barriers to rapid expansion. Drug price controls limit margins on essential medicines. GST implementation added compliance burden. Yet MedPlus has turned regulatory complexity into competitive advantage—their compliance infrastructure makes acquisitions easier and new market entry smoother than smaller players can manage.

What's fascinating about the current competitive dynamics is how different players are converging on similar strategies from different starting points. Apollo is building digital capabilities, online players are opening physical stores, and MedPlus continues strengthening both channels. The end game seems clear: 3-4 large omnichannel players will dominate organized pharmacy, while unorganized retail will persist in tier-3/4 markets where economics don't support organized retail.

The unorganized sector accounted for the largest market share (~93%) in 2018, but this dominance is eroding faster than headline numbers suggest. In metro cities, organized pharmacy already exceeds 30% penetration. The shift isn't just about market share—it's about profitable market share. Organized players dominate high-margin categories like chronic medicines, wellness products, and private label, while unorganized retail increasingly handles only acute, low-margin products.

MedPlus's positioning in this evolving landscape is strategic. They're not the largest (Apollo), the most funded (PharmEasy), or the most innovative (1mg). But they might be the most balanced—profitable enough to fund growth, digital enough to compete online, physical enough to serve every customer segment. In a market where everyone else is trying to be everything, MedPlus has mastered being exactly enough. As consolidation accelerates, this balanced approach might prove to be the winning strategy.

IX. Financial Performance & Unit Economics

The numbers tell a story that Wall Street analysts would love but venture capitalists might question. Mkt Cap: 9,628 Crore (up 25.5% in 1 year) · Revenue: 6,190 Cr · Profit: 178 Cr. At first glance, a 2.9% net margin seems thin, almost concerning. But in pharmacy retail, where gross margins are regulated and competition is cutthroat, MedPlus's ability to generate consistent profits while growing at 20%+ annually is remarkable. This isn't a growth-at-all-costs story; it's a masterclass in sustainable expansion.

Let's dissect the unit economics of a typical MedPlus store—the atomic unit that drives the entire business. A new store requires ₹15-20 lakhs in initial investment: ₹5 lakhs for interiors, ₹8-10 lakhs for inventory, and ₹2-3 lakhs for deposits and licenses. By month three, the store typically achieves ₹8-10 lakhs in monthly revenue. By month six, it crosses breakeven at store-level EBITDA. By month 18, it's generating ₹15 lakhs monthly revenue with 7-8% EBITDA margins. The payback period is under 24 months—exceptional for physical retail.

At the end of the third quarter of 2021, MedPlus had revenue of ₹1890.9 crores and a profit of ₹66.36 crores. The journey from there to current levels reveals steady margin expansion. The company has systematically improved operational efficiency—inventory turns increased from 8x to 12x, rental costs decreased from 5% to 4% of revenue, and employee costs optimized through technology from 8% to 6% of revenue.

Company has a low return on equity of 5.61% over last 3 years. Promoters have pledged or encumbered 59.3% of their holding. The low ROE reflects the capital-intensive nature of physical retail and the company's conservative financial approach. The promoter pledge, while concerning at first glance, was primarily for personal investments and has been systematically reduced post-IPO. The debt-free status provides significant financial flexibility—while competitors pay 10-12% interest on working capital loans, MedPlus operates with internal accruals.

The revenue mix evolution tells another story. In FY2019, 85% of revenue came from branded pharmaceuticals with 16-18% gross margins. Today, branded pharmaceuticals are 75% of revenue, while private label contributes 21.5% with 40-45% gross margins. This mix shift alone has added 200 basis points to gross margins. The company targets 30% private label penetration by FY2027, which could add another 300 basis points to margins.

Working capital management at MedPlus deserves its own MBA case study. The company operates with negative working capital in mature clusters—suppliers provide 45-60 days credit while inventory turns in 30 days. This means growth is largely self-funded in established markets. New market entry requires working capital investment, but once critical mass is achieved, the market becomes cash generative. This is why cluster density matters more than geographic spread.

The online economics are particularly interesting. While pure-play e-pharmacies lose ₹200-300 per order, MedPlus's online orders are profitable from day one. The reason: zero customer acquisition cost (customers know the brand), minimal fulfillment cost (using existing stores), and no separate infrastructure. Online contributes 9% of revenue but 12% of profits—a reverse of the typical e-commerce dynamic.

Capital allocation at MedPlus follows a clear hierarchy. First priority: new stores in existing clusters where returns are proven. Second: technology and warehouse infrastructure that improve system-wide efficiency. Third: selective acquisitions of regional chains at distressed valuations. Notably absent: fancy corporate offices, celebrity endorsements, or cash-burning customer acquisition. Every rupee is allocated based on measurable ROI.

The company's financial resilience was tested during COVID and passed with flying colors. While revenues dipped 15% in Q1 FY2021 due to lockdowns, the company remained profitable. Fixed costs were managed through rental renegotiations, variable employee costs, and inventory optimization. By Q3 FY2021, revenues had recovered to pre-COVID levels with improved margins due to favorable product mix (more chronic medicines, less acute).

Looking at peer comparison, MedPlus's financial profile stands out. Apollo Pharmacy has higher revenue per store but lower EBITDA margins due to hospital-proximity locations commanding premium rents. Pure-play e-pharmacies have higher growth rates but negative unit economics. Regional chains have better margins in their core markets but lack scale advantages in procurement and technology.

The path to improved profitability is clear and achievable. Same-store sales growth of 8-10% annually through market share gains. Margin expansion through private label penetration and operational efficiency. Operating leverage as fixed costs are spread across a larger store base. The company guides for 10% EBITDA margins by FY2027—aggressive but achievable given current trajectory.

What makes MedPlus's financial model compelling isn't the absolute numbers but the predictability and sustainability. This isn't a business dependent on regulatory changes, funding cycles, or technological disruption. It's a steady compounding machine—adding stores, gaining market share, improving margins, and generating cash. In a market obsessed with unicorns and exponential growth, MedPlus offers something rarer: a business that makes money while growing. As we transition to examining the strategic playbook, this financial foundation becomes the bedrock upon which all strategic decisions are made.

X. Playbook: Business & Investing Lessons

If you wanted to build the anti-Silicon Valley playbook for dominating a massive market, you'd study MedPlus. No blitzscaling, no winner-takes-all rhetoric, no growth-at-all-costs mentality. Instead, methodical expansion, obsessive focus on unit economics, and patient capital deployment. The MedPlus playbook offers lessons that challenge conventional wisdom about building modern businesses in emerging markets.

Lesson 1: The Cluster Domination Strategy MedPlus's cluster approach—saturating neighborhoods before expanding—seems obvious in hindsight but was contrarian when implemented. Most retailers chase geographic coverage for vanity metrics. MedPlus understood that density creates compounding advantages: shared inventory reduces working capital, concentrated marketing increases effectiveness, operational supervision becomes efficient, and word-of-mouth accelerates in tight networks. The lesson: dominate your backyard before conquering the world.

Lesson 2: Building Trust in Low-Trust Markets In Indian pharmacy, trust isn't a nice-to-have—it's existential. MedPlus built trust not through advertising but through consistency. Same price everywhere, genuine medicines always, professional service consistently. They understood that in healthcare, trust compounds slowly but destroys instantly. Every decision—from store design to staff training—reinforced the trust equation. The broader lesson: in categories where trust matters, consistency beats innovation.

Lesson 3: Omnichannel as Necessity, Not Luxury MedPlus didn't go digital because VCs demanded it or competitors forced it. They went digital because customers needed it. But unlike pure-play competitors who saw physical stores as legacy baggage, MedPlus saw them as unfair advantage. Stores became fulfillment centers, customer acquisition channels, and trust anchors for digital operations. The lesson: in retail, channels aren't competing strategies but complementary assets.

Lesson 4: Private Label as Margin Driver Without Trust Compromise Most retailers push private label aggressively, often compromising quality for margins. MedPlus took a different approach—partnering with respected manufacturers, maintaining quality standards, and building sub-brands slowly. They understood that one bad private label experience could destroy years of trust-building. The result: 21.5% private label penetration with no impact on customer satisfaction. The lesson: private label is a margin opportunity only if you don't compromise the core value proposition.

Lesson 5: The PE to IPO Journey—Timing vs. Time MedPlus raised PE capital not when they desperately needed it but when terms were favorable. They went public not when markets were frothy but when the business was ready. This patient approach to capital markets—unusual in today's funding-driven ecosystem—meant they never negotiated from weakness. The lesson: capital should accelerate strategy, not define it.

Lesson 6: Competing with Tech-First Players as Traditional Retailer When e-pharmacies raised billions, MedPlus could have panicked, could have tried to out-tech the tech players. Instead, they played to their strengths—store density, supplier relationships, operational excellence—while selectively adopting technology. They understood that customers don't want tech for tech's sake; they want solutions. Sometimes the solution is an app; sometimes it's a trusted pharmacist. The lesson: compete on customer value, not on buzzwords.

Lesson 7: The Consolidation Play in Fragmented Markets MedPlus understood early that Indian pharmacy would consolidate—not because technology demanded it but because economics required it. Scale advantages in procurement, technology investments, and regulatory compliance would make subscale players unviable. But instead of aggressive roll-ups, MedPlus grew organically, acquiring selectively when valuations were attractive. The lesson: in consolidating markets, patience and capital efficiency beat aggressive expansion.

Lesson 8: Founder-Led but Professionally Managed Madhukar Gangadi remains the visionary and largest shareholder, but he built an institutional company. Professional managers run operations, independent directors provide governance, and systems drive decisions—not personalities. This balance—founder passion with professional discipline—is rare in Indian companies. The lesson: founder-led doesn't mean founder-dependent.

Lesson 9: The Boring Business Advantage Pharmacy retail isn't sexy. No AI, no blockchain, no metaverse. Just selling medicines efficiently and reliably. This "boring" nature kept tourist capital away, reduced competitive intensity from high-profile startups, and allowed patient building of competitive advantages. The lesson: boring businesses with strong unit economics often generate extraordinary returns.

Lesson 10: Operational Excellence as Strategy MedPlus doesn't have a killer app, proprietary technology, or exclusive products. Their moat is operational excellence—doing thousands of small things slightly better than competitors. Store locations, inventory management, staff training, supplier relationships—each marginally better, collectively insurmountable. The lesson: in execution businesses, excellence in details creates strategic advantage.

The MedPlus playbook challenges the contemporary startup wisdom that celebrates rapid scaling, winner-takes-all dynamics, and growth over profits. It offers an alternative path—patient building, cluster domination, operational excellence, and sustainable growth. For investors, it suggests that boring businesses with strong unit economics might offer better risk-adjusted returns than exciting startups with uncertain paths to profitability. For entrepreneurs, it demonstrates that building lasting value requires more than capital and ambition—it requires discipline, patience, and relentless focus on customer value. As we examine the bull and bear cases next, these lessons become the lens through which we evaluate MedPlus's future potential.

XI. Bull vs. Bear Case

Bull Case: The Consolidation Compounder

The optimistic thesis for MedPlus rests on a simple but powerful premise: India's ₹2 trillion pharmacy market will inevitably consolidate from 11% organized to 40%+ over the next decade, and MedPlus is perfectly positioned to capture disproportionate value from this shift. The math is compelling—even maintaining current market share in a consolidating market would triple revenues.

The runway for growth appears massive. With 89% of the pharmacy market still unorganized, MedPlus doesn't need to steal share from organized competitors—they just need to convert unorganized demand. Every year, thousands of traditional pharmacies shut down as owners retire without succession plans, regulatory compliance becomes stricter, and customers demand better service. MedPlus, with proven ability to open 500+ stores annually while maintaining unit economics, can absorb this demand profitably.

The execution track record inspires confidence. Unlike startups promising future profitability, MedPlus has demonstrated sustainable unit economics for years. Around 60% to 75% of these newly opened stores managed to witness a positive store level operating EBITDA in the first 3-6 months of operation. This isn't theoretical—it's proven across thousands of stores, multiple states, and different market conditions. The company has survived demonetization, GST implementation, and COVID while remaining profitable.

The omnichannel advantage becomes more valuable over time. Pure online players face customer acquisition costs that make profitability elusive. Traditional retailers lack digital capabilities. MedPlus's hybrid model—physical presence with digital convenience—offers the best of both worlds. As customers increasingly expect both online ordering and immediate physical availability, MedPlus's infrastructure becomes increasingly valuable.

Private label expansion offers a clear path to margin improvement. At 21.5% of revenue currently, reaching 35% (achievable given global benchmarks) would add 400-500 basis points to gross margins. Unlike FMCG where private label faces brand loyalty challenges, pharmacy private label adoption is accelerating as customers realize generic medicines are identical to branded versions.

The tier-2/3 city opportunity is particularly exciting. These markets have minimal organized pharmacy presence, lower real estate costs, and less competitive intensity. MedPlus's cluster model is perfectly suited for these markets—they can dominate a city of 500,000 people with 20-30 stores, creating local monopolies with superior economics.

Demographic tailwinds provide multi-decade growth drivers. India's diabetic population will double to 140 million by 2040. Cardiovascular diseases are exploding with lifestyle changes. Cancer incidence is rising with increased detection. Mental health awareness is driving psychiatric medication demand. These aren't cyclical trends—they're structural shifts requiring sustained medication consumption.

The valuation remains reasonable despite recent gains. At 50x P/E, MedPlus trades at a discount to high-growth consumer companies despite superior unit economics and clearer path to profitability. If MedPlus achieves its target of 10% EBITDA margins by FY2027, current valuations would appear cheap in hindsight.

Bear Case: The Margin Compression Trap

The skeptical view starts with a harsh reality: MedPlus operates in one of India's most regulated, competitive, and low-margin industries. Company has a low return on equity of 5.61% over last 3 years. This isn't a temporarily depressed number—it reflects structural challenges in pharmacy retail that no amount of operational excellence can fully overcome.

Competition is intensifying from every direction. PharmEasy and others have raised billions and show no signs of rational pricing. Apollo has deeper pockets and hospital ecosystem advantages. Reliance could leverage its retail network to crush margins. Even Amazon is eyeing pharmacy. The competitive intensity will only increase, potentially triggering a race to the bottom on margins.

The Promoters have pledged or encumbered 59.3% of their holding raises governance concerns. While management explains this as personal investments, high promoter leverage creates vulnerability. In stressed scenarios, promoters might make decisions prioritizing personal financial needs over minority shareholders. The history of Indian markets is littered with companies destroyed by promoter leverage.

Regulatory risks loom large. Drug price controls could tighten, reducing already thin margins. E-pharmacy regulations remain uncertain—a favorable framework could advantage pure online players. State-level regulations vary wildly, making national expansion complex and costly. One adverse regulatory change could impact profitability significantly.

The capital intensity of physical expansion is increasingly problematic. Each new store requires ₹20 lakhs investment with 24-month payback. To reach 10,000 stores would require ₹1,000+ crores in capital. Meanwhile, digital players can scale with minimal capital. In a world moving digital, betting on physical infrastructure seems contrarian—and not in a good way.

Margin pressure from multiple sources could persist. Government push for generic medicines reduces margins. Insurance companies negotiate lower prices. Customer price comparison through apps increases pricing pressure. Private label faces limits—customers won't accept store brands for critical medicines. The path to 10% EBITDA margins looks increasingly difficult.

Technology disruption remains a threat. Telemedicine could bypass pharmacies entirely with direct-to-patient delivery. AI-powered health apps could reduce medication needs through preventive care. International players like Amazon or CVS could enter with superior technology and unlimited capital. MedPlus's technology, while adequate, isn't revolutionary.

Execution risks multiply with scale. Managing 4,500 stores is vastly different from managing 10,000. Each new state adds regulatory complexity. Maintaining culture and service quality becomes harder. Small operational slippages, multiplied across thousands of stores, could destroy profitability.

The unorganized market's resilience is consistently underestimated. Local pharmacies offer credit, home delivery, and personal relationships that organized retail can't match. In tier-3/4 cities, these advantages matter more than air-conditioning and computerized billing. The 89% unorganized market share might decline slower than bulls expect.

Valuation looks stretched considering the risks. At 50x earnings for a retailer with 3% net margins and single-digit ROE, MedPlus is priced for perfection. Any disappointment—slower store additions, margin compression, regulatory changes—could trigger significant multiple compression.

The Balanced View

Reality likely lies between these extremes. MedPlus will probably continue growing steadily, gaining market share, and improving margins—but not as dramatically as bulls hope. Competition will intensify but remain rational enough for sustainable economics. Regulations will evolve but not destroy the business model. The company will compound value steadily rather than explosively. For investors, MedPlus represents a solid compounder rather than a multibagger—attractive for those seeking steady growth, challenging for those seeking dramatic returns.

XII. Future Outlook & Strategic Priorities

The war room at MedPlus headquarters has a different energy in 2024 than it did during the IPO preparations. Gone is the scrappy startup urgency, replaced by the measured confidence of a market leader planning its next decade. On the whiteboard, a bold declaration: "10,000 stores by 2030." But more interesting than the number is the strategy to get there—and what comes after.

The CEO Madhukar Gangadi confidently said that the MedPlus will overtake Apollo within the next two and half years. This isn't blind ambition—it's mathematical probability. MedPlus adds 500+ stores annually versus Apollo's 200-300. At current trajectory, MedPlus will operate 6,500+ stores by 2027 versus Apollo's 6,000. But store count is vanity; market share is sanity. The real battle is for the ₹500,000 crore organized pharmacy market of 2030.

Geographic expansion presents the next frontier. MedPlus has conquered South India, established beachheads in West and East, but North India remains terra incognita. The Hindi heartland—UP, Bihar, Jharkhand—offers 400 million potential customers with minimal organized pharmacy presence. But these markets are different: lower purchasing power, preference for credit, complex political economy. MedPlus is adapting its model—smaller stores, local language staff, flexible payment terms—learning from its failed 2007 expansion.

Technology investment is accelerating, but with a twist. Instead of building consumer-facing apps to compete with startups, MedPlus is investing in backend intelligence. AI-powered demand forecasting reduces stockouts while minimizing inventory. Computer vision monitors shelf compliance across thousands of stores. Natural language processing analyzes customer feedback to identify systemic issues. It's unsexy technology that drives tangible ROI.

The healthcare services expansion beyond pharmacy represents the biggest strategic bet. PathLabs was just the beginning. MedPlus is piloting primary care clinics adjacent to pharmacies—not competing with hospitals but providing basic consultation and chronic disease management. Imagine a diabetic patient getting tested, consulted, and medicated in one location. The pharmacy becomes a healthcare hub, increasing customer stickiness and lifetime value.

M&A opportunities are crystallizing as smaller chains struggle. Regional players with 50-100 stores face an impossible choice: invest heavily in technology and compliance or sell to larger players. MedPlus, with integration expertise and capital access, is positioned to consolidate. But they're selective—only acquiring in existing clusters where synergies are immediate. No empire-building for vanity metrics.

The diagnostic expansion deserves special attention. While PathLabs operates in select cities, the vision is bigger: diagnostic kiosks in every MedPlus store. Basic tests—blood sugar, blood pressure, cholesterol—conducted by trained technicians, results integrated with pharmacy records, medications adjusted accordingly. It's not replacing diagnostic chains but democratizing basic healthcare monitoring.

Telepharmacy represents an underappreciated opportunity. In rural areas where opening physical stores isn't viable, MedPlus is experimenting with telepharmacy kiosks—video consultation with remote pharmacists, medicine dispensed from automated machines. It's capital-light expansion into markets traditional retail can't serve profitably.

The private label evolution continues with sophisticated segmentation. Beyond generic medicines, MedPlus is launching condition-specific bundles—diabetes care packs, pregnancy nutrition sets, elderly wellness kits. These higher-margin bundles combine medicines, supplements, and devices, creating solution selling rather than product pushing.

International expansion might seem premature, but MedPlus is exploring selectively. Sri Lanka and Bangladesh offer similar market dynamics—fragmented pharmacy markets, growing middle class, minimal organized presence. These aren't immediate priorities but option values for the next decade.

The sustainability agenda, often overlooked in Indian retail, is gaining prominence. MedPlus is piloting medicine take-back programs, reducing plastic packaging, and investing in solar power for stores. This isn't just corporate responsibility—younger consumers increasingly factor sustainability into purchase decisions.

Talent development becomes critical at scale. MedPlus University, currently training pharmacists, is expanding into general management, technology, and leadership development. The goal: building bench strength for rapid expansion while maintaining culture and service standards.

The competitive response strategy is nuanced. Against e-pharmacies, MedPlus emphasizes trust and immediacy. Against Apollo, they stress value and accessibility. Against local pharmacies, they offer consistency and range. It's not one strategy but multiple strategies for multiple competitions.

Risk management is evolving from reactive to proactive. Scenario planning for regulatory changes, competitive responses, and technology disruption. Geographic diversification to reduce state-level regulatory risk. Business model diversification beyond pure pharmacy. It's building resilience without sacrificing growth.

The 2030 vision crystallizing at MedPlus goes beyond store count or market share. It's about becoming integral to India's healthcare infrastructure—as essential as hospitals or diagnostic chains. Every Indian within 10 minutes of a MedPlus. Every chronic patient managed through their ecosystem. Every family trusting them for healthcare needs beyond just medicines.

The path won't be linear. Competition will intensify, regulations will evolve, technology will disrupt. But MedPlus has something rare in Indian business—patient capital, proven model, and profitable growth. They're not trying to be the fastest or the loudest. They're trying to be the last one standing when the dust settles.

As we look toward 2030, MedPlus represents a bet on India's healthcare formalization. If India follows global patterns, if chronic diseases continue rising, if consumers increasingly value organized retail—MedPlus wins big. The future isn't guaranteed, but the trajectory is clear. From that single store in Dilsukhnagar to potentially India's largest pharmacy chain—it's been a remarkable journey. And the most interesting chapters might still be unwritten.

XIII. Recent News**

Q2 FY25 Performance: Steady Expansion Amid Market Challenges**

MedPlus Q1 FY'26 earnings call: 101 net new stores, Rs 1542.6 Cr revenue, 4.7% EBITDA, private label at 21.5% revenue. The Q1 FY26 results demonstrate MedPlus's ability to maintain growth momentum while improving profitability. The 4.7% EBITDA margin represents continued improvement from previous quarters, driven by private label penetration and operational efficiencies.

The stores increased with 108 net new stores added in Q2 FY2025, of which 71 were in Tier-2 and Tier-3 cities. This tier-2/3 focus reflects strategic positioning in less competitive markets with better unit economics. The company's ability to maintain aggressive store additions while improving margins validates the cluster expansion strategy.

Q3 FY25 Updates: Maintaining Momentum

We expect a quarter of 300 net store additions in the current financial year. In terms of network, in terms of our stores' network age, around 27% of our stores are operational for less than 2 years. And the remaining 73% of our stores have been operational for 2 years or more. The maturity profile of stores indicates a healthy mix of established profitable stores funding new expansion.

As a broad range, we closely monitor the time frame for our new stores to reach breakeven. For stores opened between January 2024 and June 2024, approximately 55% of them achieved breakeven within 6 months of operations. As a cohort, all stores combined reached breakeven in 6 months. This rapid path to profitability, even in new states, demonstrates the strength of MedPlus's operational model.

Financial Performance Highlights

MedPlus Health Services reported a 3.32% sequential decline in Q4 revenue but a 12.01% rise in net profit. Year-on-year, net profit surged 53.7%. The company added 100 new stores, increasing total count to 4,712. For FY25, net profit rose 129.6%. The ability to grow profits faster than revenue indicates successful margin expansion through operational leverage and mix improvement.

Management Commentary and Strategic Updates

And EBITDA margin has crossed 5% for the pharmacy business, which is quite healthy. No, I think we are at a fairly sustainable kind of margin level for the content. Now the only reason which can change it is if we add a ton of stores, new stores. Management's confidence in margin sustainability while continuing aggressive expansion suggests strong underlying business fundamentals.

The recent performance validates MedPlus's strategy of patient expansion with focus on profitability. Unlike pure-play e-pharmacies burning cash for growth, MedPlus demonstrates that sustainable, profitable growth is possible in Indian pharmacy retail. The consistent improvement in margins while adding 100+ stores quarterly positions the company well for long-term value creation.

Stock Performance and Market Recognition

Medplus Health Services reported a 53.7% increase in Q4 profit and a 129.6% rise in full-year net profit. The company plans to open 600 new stores in FY26, contributing to growth. Shares hit a 52-week high amid increased trading volume. The market's positive response to results indicates growing investor confidence in the MedPlus story.

The recent developments paint a picture of a company executing well on multiple fronts—store expansion, margin improvement, and market share gains. While challenges remain from competition and regulation, MedPlus's consistent execution provides confidence in its ability to navigate the evolving pharmacy landscape. As the company approaches its target of becoming India's largest pharmacy chain, the combination of profitable growth and strategic positioning makes it a compelling story in Indian retail.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube