The Wire That Connected India's Electrical Revolution

I. Cold Open & Episode Thesis

The monsoon of 2023 had just broken over Mumbai when Inder Jaisinghani stood atop the gleaming headquarters of Polycab India, surveying a city that his father once entered as a refugee with nothing but hope. Below him sprawled the financial nerve center of a nation whose GDP had grown 65-fold since that desperate flight from Sindh in 1947. The company he built from his father's modest electrical shop now commanded revenues of ₹14,206 crores, controlled over a quarter of India's organized wires and cables market, and had quietly become the invisible backbone powering the world's fifth-largest economy.

Yet few outside India's business circles know this story—how a partition survivor's son built an empire by literally wiring a nation, how a commodity business became a consumer brand, or how a family operation professionalized into a public company worth over ₹100,000 crores while still maintaining the paranoid discipline of its refugee origins.

This is more than a business success story. It's a chronicle of how infrastructure gets built in emerging markets, how trust networks form among displaced communities, and how patient capital can outlast flashier competitors. It's about timing waves of deregulation, surviving commodity cycles, and the audacious bet that India's electrical consumption would explode from 30 units per capita in 1970 to over 1,200 units today.

The Polycab saga matters now more than ever. As India races toward a $10 trillion economy by 2035, as giants like UltraTech and Adani circle the industry with their war chests, and as the nation prepares to add 500 gigawatts of renewable energy capacity by 2030, the question isn't whether India needs more electrical infrastructure—it's who will build it, and whether the scrappy upstarts can survive the coming consolidation.

What follows is the definitive account of how refugees became industrialists, how traders became manufacturers, how a B2B supplier became a consumer brand, and how a family business navigated the treacherous passage to public markets while new threats emerge from unexpected quarters. It's a playbook for building in chaos, scaling through trust, and creating value in the most competitive of commodity markets.

The story begins not in a boardroom or factory, but in the smoke and ash of Partition, where the seeds of an empire were planted in loss.

II. The Partition Origins: From Sindh to Mumbai (1947-1983)

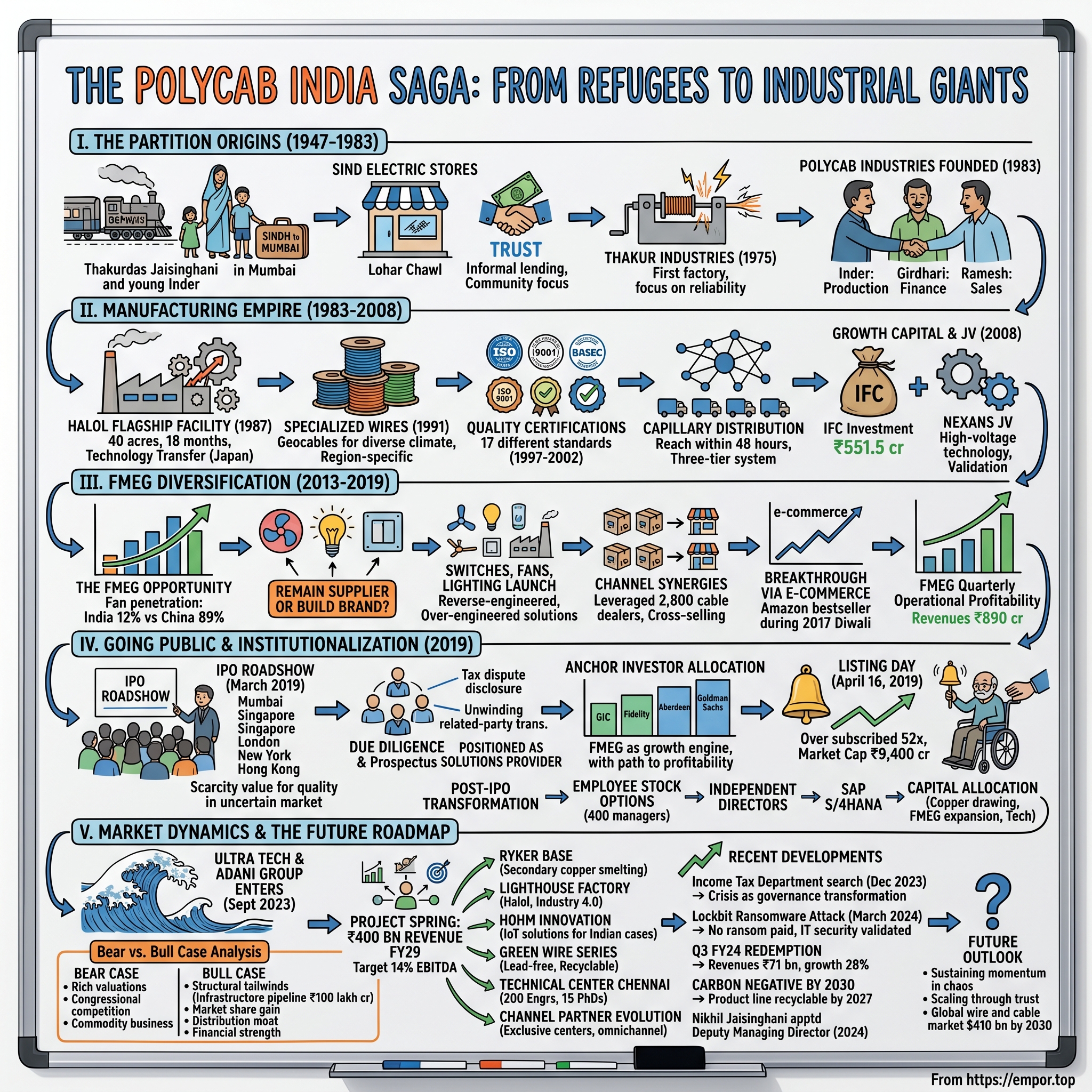

The train from Karachi to Bombay in 1964 carried more than passengers—it carried the dreams of those who had lost everything but refused to lose hope. Among them was Thakurdas Jaisinghani, clutching his family's meager possessions and the address of a cousin in Lohar Chawl, the narrow lanes of South Bombay that had become a haven for Sindhi refugees. He had waited seventeen years after Partition to make this journey, watching as his textile trading business in Pakistan slowly strangled under policies that favored Muslim merchants. When he finally arrived at Victoria Terminus with his young family, including his son Inder, the only capital he possessed was the unshakeable belief that in business, trust was the only currency that mattered.

Lohar Chawl in the 1960s was not just a neighborhood—it was an ecosystem. The metal traders and small manufacturers who populated its cramped shops had created an informal economy worth crores, operating on handshake deals and community guarantees. Thakurdas understood this world intimately. Within months of arrival, he had established Sind Electric Stores, a ten-by-twelve-foot shop that sold electrical components to the small factories sprouting across Bombay's periphery.

The genius of Thakurdas wasn't in what he sold but how he sold it. While established dealers demanded cash upfront or letters of credit, he offered thirty-day terms to fellow Sindhis, knowing that community shame was better collateral than any bank guarantee. His ledger, written in Sindhi script that few tax inspectors could read, tracked not just transactions but relationships—who was related to whom, whose son was getting married, which factory owner was expanding. This social capital would prove more valuable than any working capital.

Young Inder absorbed these lessons while manning the shop after school. At fifteen, he could identify the quality of copper wire by its bend, negotiate in four languages, and calculate compound interest in his head. But he saw something his father didn't: India was changing. The socialist rhetoric of the 1960s was giving way to pragmatic industrialization. The Bombay Plan's vision of a mixed economy meant government contracts for infrastructure, and infrastructure meant electrical equipment.

The transformation came in 1975, a year when Indira Gandhi's Emergency froze political life but paradoxically unleashed entrepreneurial energy in unexpected ways. While established businesses cowered under arbitrary raids and arrests, smaller players who knew how to navigate the byzantine permit system thrived. Inder convinced his father to mortgage their shop and two small flats to raise ₹3 lakhs—enough to rent a shed in Andheri and buy second-hand wire-drawing equipment from a failed factory in Pune.

Thakur Industries was born not with a business plan but with a problem to solve. The state electricity boards were desperate for low-voltage cables but couldn't afford imports and didn't trust the quality of local suppliers. Inder's insight was devastatingly simple: rather than compete on price with fly-by-night operators who adulterated copper with cheaper metals, he would compete on reliability. Every spool of wire would be slightly over-spec, every delivery would arrive two days early, and every complaint would be addressed within hours.

The strategy worked because it exploited a market failure. In an economy where getting an industrial license could take two years and a phone connection five, reliability was revolutionary. By 1980, Thakur Industries had grown from one shed to three, from five workers to fifty, and from serving local contractors to supplying Maharashtra State Electricity Board directly.

But Inder saw the real opportunity wasn't in serving the government—it was in serving the economy the government was inadvertently creating. The Sixth Five-Year Plan had allocated ₹97,500 crores for development, with power generation as a priority. Every megawatt of capacity added meant kilometers of transmission lines, and every transmission line meant cables, connectors, and components. The infrastructure boom was coming, and Inder was determined to supply it.

The formal founding of Polycab Industries in 1983 marked not just a corporate restructuring but a generational transition. Thakurdas, now in his sixties, handed operational control to Inder and his brothers Girdhari and Ramesh. The name itself was carefully chosen—"Poly" suggesting modern polymer technology, "cab" abbreviating cables, together conveying technical sophistication while remaining easy to pronounce in any Indian language.

The brothers divided responsibilities with the precision of a Marwari family firm: Inder handled production and technology, Girdhari managed finances with legendary tightfistedness, and Ramesh built relationships with dealers and contractors. They instituted a peculiar but effective policy: every family member, regardless of position, had to spend one month annually working on the factory floor and another month traveling with salesmen. This wasn't mere symbolism—it was intelligence gathering, ensuring that no quality issue or market trend escaped leadership attention.

The License Raj, much maligned by economists, actually provided Polycab with unexpected advantages. The Small Scale Industries reservation policy meant that certain products could only be manufactured by companies below specific investment thresholds. By carefully structuring multiple legal entities, each technically within SSI limits but operationally integrated, Polycab could access subsidized credit, tax breaks, and protection from large industrial houses while building scale through the back door.

This regulatory arbitrage was coupled with technological pragmatism. While competitors imported expensive European machinery, Polycab bought reliable Japanese equipment from the 1970s, retrofitted with local innovations. A visiting German consultant once remarked that their extrusion line was "either genius or insanity"—copper wire was being drawn using modified textile machinery, cooled with a system adapted from ice factories, and wound on spools designed for the film industry. But it worked, producing cable at 60% of the cost of conventional setups.

As 1983 drew to a close, Polycab Industries employed 127 people, operated from 20,000 square feet of factory space, and had annual revenues approaching ₹1 crore. In the photograph from their first Diwali celebration as an incorporated company, the entire workforce fits in a single frame, Inder at the center, his father beside him, both wearing the same expression—not of satisfaction with what they'd built, but anticipation of what was to come.

The real test wasn't whether they could manufacture quality products or navigate regulations—it was whether a family of refugees could transform themselves into industrialists capable of seizing the opportunity that India's economic opening would soon present.

III. The Manufacturing Journey: Wires to Empire (1983-2008)

The letter arrived on a humid Tuesday in August 1987, bearing the seal of Gujarat Industrial Development Corporation. Inder Jaisinghani read it three times before allowing himself to believe: Polycab had been allocated forty acres in Halol, a dusty town 45 kilometers from Vadodara, to establish what would become their flagship manufacturing facility. The land came at a subsidized rate—₹50,000 per acre—but with conditions that would have frightened most entrepreneurs: production had to commence within eighteen months, 70% of workers had to be local, and the facility had to meet export quality standards from day one.

Inder saw opportunity where others saw obstacles. Halol's isolation meant land was cheap and labor disputes rare. Its position on the Delhi-Mumbai railway corridor provided logistics advantages. Most critically, Gujarat's newly elected Chief Minister Chimanbhai Patel was offering ten-year tax holidays to industries that could demonstrate technology transfer. Polycab's partnership with a retiring Japanese engineer named Yamamoto-san, who had spent three decades perfecting PVC insulation techniques at Furukawa Electric, qualified them perfectly.

The Halol facility's construction became Polycab lore. Inder lived on-site in a modified shipping container for fourteen months, personally supervising everything from foundation depth to cafeteria menu planning. He instituted a practice that would become company tradition: every concrete pour included a copper wire blessed at the local temple, literally building trust into the infrastructure. Workers were recruited not just for skills but for family reputation—the sons of farmers known for honor, the brothers of local teachers, creating a workforce bound by community ties stronger than any employment contract.

Production began in March 1989 with a single extrusion line producing 1.5mm household wire. The first spool was ceremonially delivered to the village panchayat to electrify the primary school—a gesture that earned more goodwill than any advertising campaign could have achieved. Within six months, the facility was producing eighteen different specifications, from delicate telephone cables to heavy-duty industrial feeders.

The 1991 liberalization should have been Polycab's moment of triumph, but it nearly destroyed them. Suddenly, imported cables from Korea and Taiwan flooded Indian markets, offering seemingly comparable quality at 20% lower prices. Established players like Finolex and Havells had the brand recognition to maintain premium pricing. Polycab, caught in the middle, saw orders evaporate overnight.

The company's response revealed the strategic thinking that would define its rise. Rather than compete on price or brand, they chose to compete on specificity. India's diverse climate—from Rajasthan's 50°C summers to Kashmir's -40°C winters, from Mumbai's salt-laden air to Jharia's coal dust—destroyed generic cables designed for temperate conditions. Polycab developed what they called "geocables": region-specific formulations that could survive local extremes. The Rajasthan variant included UV stabilizers and heat-resistant compounds. The coastal version featured enhanced salt corrosion resistance. The mining specification incorporated abrasion-resistant sheaths.

This hyperlocalization strategy required reimagining manufacturing. Instead of long production runs of standard items, Halol operated on a job-shop model with rapid changeovers. Yamamoto-san's contribution was crucial here—he introduced single-minute exchange of die (SMED) techniques that reduced changeover time from four hours to forty minutes, making small-batch customization economically viable.

The 1996 incorporation as Polycab Wires Private Limited wasn't merely legal housekeeping—it marked the professionalization phase. External directors were inducted, including R.K. Sharma, former chief of Rural Electrification Corporation, who brought government contacts and credibility. Management consultants from Arthur Andersen were hired to implement SAP, making Polycab one of the first mid-sized Indian manufacturers with enterprise resource planning. The shop-floor resistance to computerization was overcome through a clever gambit: workers who learned to use terminals received a 10% "technology bonus," turning potential saboteurs into evangelists.

Quality certifications became an obsession. Between 1997 and 2002, Polycab acquired seventeen different standards: ISO 9001 for quality management, ISO 14001 for environmental systems, OHSAS 18001 for occupational health, BASEC certification for fire-resistant cables, UL listing for exports, and dozen others. Each certification was treated not as paperwork but as organizational transformation. The BASEC process alone required rebuilding the entire testing laboratory, training forty engineers in British standards, and implementing batch-level traceability that could track any meter of cable back to its raw material source.

The infrastructure boom of the early 2000s validated every strategic choice. The Golden Quadrilateral highway project, the Accelerated Power Development Programme, and the telecom revolution created unprecedented demand. But Polycab's masterstroke was recognizing that the real opportunity lay not in the megaprojects themselves but in the secondary development they triggered. Every kilometer of highway meant service stations, hotels, and townships. Every power plant meant transmission infrastructure and distribution networks. Every cell tower meant backhaul connectivity and power supply systems.

To capture this distributed demand, Polycab built what they called the "capillary network"—a three-tier distribution system that could reach any construction site within 48 hours. Primary distributors in state capitals held bulk inventory. Secondary dealers in district headquarters provided local availability. Tertiary retailers, often electrical contractors themselves, offered last-mile connectivity. The entire network operated on a sophisticated credit system where payment terms shortened with each tier, ensuring cash generation even while scaling rapidly.

The 2008 joint venture with Nexans, the French cable giant, represented both culmination and new beginning. Nexans brought technology for high-voltage cables—the massive transmission lines that carry power from generation stations to cities. But more importantly, they brought validation. When a 110-year-old European company with €7 billion in revenues chose Polycab as their Indian partner over established players like Havells and Finolex, it sent a powerful signal to the market.

The IFC investment that September was equally strategic. The World Bank's private sector arm didn't just provide ₹551.5 crores in growth capital—they provided governance frameworks, environmental standards, and international credibility. The valuation of ₹4,600 crores made Inder and his brothers paper billionaires, but more importantly, it established Polycab as an institutional-grade investment, attracting talent and partners who would have previously looked only at listed companies.

The 2008 financial crisis struck just weeks after the IFC investment closed. Orders collapsed, working capital dried up, and several competitors declared bankruptcy. Polycab not only survived but used the crisis to consolidate. They acquired distressed assets at fraction of replacement cost, hired talented engineers laid off by competitors, and locked in long-term copper contracts at decade-low prices. When recovery came in 2010, Polycab had emerged with 40% more capacity, 30% lower costs, and relationships with customers who remembered who had maintained supply when others defaulted.

By the end of 2008, Polycab operated six manufacturing facilities, employed 3,400 people, and generated revenues exceeding ₹2,000 crores. The refugee's son who had started with a single wire-drawing machine now controlled an industrial empire. But Inder understood that manufacturing excellence alone wouldn't secure Polycab's future—the company needed to own the customer relationship, not just supply components.

IV. The FMEG Diversification Play (2013-2019)

The PowerPoint slide that changed Polycab's destiny contained just one graph: household penetration of electrical appliances in India versus China. In 2013, as Inder Jaisinghani presented to his board, the data was stark—only 12% of Indian homes had ceiling fans in every room, compared to 89% in China. For switches and sockets, the gap was even wider. The electrical accessories market that Polycab had supplied for three decades was about to explode, and the company faced a choice: remain a component supplier watching others capture value, or forward-integrate into consumer products themselves.

The board meeting erupted. Girdhari, ever the financial conservative, calculated that entering FMEG would require ₹500 crores in brand building alone. Technical directors argued that consumer products required completely different capabilities—design aesthetics, retail management, advertising expertise—none of which existed in Polycab's engineering-heavy culture. The independent directors worried about losing focus, pointing to diversification disasters like Videocon's airline adventure or BPL's mobile phone misadventure.

But Inder had done his homework with characteristic thoroughness. For six months, he had personally visited 200 electrical retailers across tier-2 and tier-3 cities, posing as a contractor to understand purchase behavior. His findings were revelatory: consumers didn't buy fans or switches—they bought "electrical solutions." The same contractor who installed wiring also recommended switches. The electrician who fixed fans also influenced cable purchases. The dealer who stocked wires inevitably got asked about lighting. Polycab already owned these relationships; they just weren't monetizing them fully.

The switches launch in late 2013 was deliberately modest—just forty SKUs targeting the mid-market segment. Rather than competing with Havells' premium Roma series or Anchor's budget offerings, Polycab positioned itself in the vacant middle: reliable but not luxurious, affordable but not cheap. The product development was quintessentially Polycab—they reverse-engineered seventeen competitor products, identified twelve common failure points, and over-engineered solutions for each. Their switches were 20% heavier due to thicker copper contacts, rated for 20% more cycles, and tested at 20% higher loads than standards required.

The real innovation wasn't in the product but the go-to-market strategy. Instead of building separate distribution, Polycab leveraged its existing network of 2,800 cable dealers, offering them exclusive territory rights for FMEG products. Dealers who achieved sales targets received retroactive discounts on cable purchases, creating powerful cross-selling incentives. Training programs taught cable salesmen to position switches as natural add-ons: "You're already buying Polycab quality in cables, why compromise on switches?"

The 2014 expansion into fans and LED lighting followed similar logic but required deeper capability building. Polycab acquired Sigma Electricals, a struggling Kolkata-based fan manufacturer with good designs but poor execution. Rather than integrate Sigma's culture, Polycab kept it as a semi-autonomous design studio while rebuilding manufacturing from scratch. The Halol facility added a 100,000-square-foot fan assembly unit that applied automotive-style quality control to ceiling fans—each motor underwent computerized balancing, every blade was wind-tunnel tested, and final products faced 500-hour continuous operation trials.

The LED lighting entry proved more challenging. The technology was evolving rapidly, Chinese imports were dumping products below cost, and established players like Philips and Syska had massive head starts. Polycab's response was counterintuitive: instead of competing in consumer bulbs where margins were negligible, they focused on commercial and industrial lighting where their B2B relationships provided advantage. Stadium floodlights, warehouse high-bays, and street lighting became entry points, with consumer products following once brand credibility was established.

Marketing required cultural transformation. Polycab hired Sameer Tobaccowala, former JWT executive who had built Havells' consumer brand, as marketing advisor. He introduced concepts alien to Polycab's engineering culture: brand archetypes, emotional positioning, lifestyle imagery. The first television commercial—featuring a young couple choosing Polycab fans for their new home—was reshot seven times before Inder approved it. He kept rejecting versions that didn't show product features prominently enough, unable to initially grasp that consumers bought feelings, not specifications.

The distribution battles were brutal. Established FMEG players used every tactic to block Polycab's entry. Dealers were threatened with supply cuts if they stocked Polycab fans. Retailers received under-the-table payments to hide Polycab products. Competitor sales forces spread rumors about quality issues. Polycab responded with overwhelming force: dealer margins 3% higher than competition, retailer incentive programs that included foreign trips, and a rapid-response team that addressed any quality complaint within 24 hours, even if it meant flying engineers to remote locations.

The financial hemorrhaging was severe. FMEG losses touched ₹112 crores in FY2016, dragging overall margins down by 200 basis points. Analysts questioned the strategy, especially as the cable business was generating record profits that diversification was destroying. But Inder had studied Havells' journey—how Qimat Rai Gupta had lost money for seven years building consumer products before the business became a cash machine. Patience and persistence were prerequisites for consumer brand building.

The breakthrough came through an unexpected channel: e-commerce. While established players treated online sales as experimental, Polycab went all-in, becoming the first major electrical company to establish dedicated Amazon and Flipkart teams. They created online-exclusive SKUs with subtle differences—different colors, minor feature additions—that prevented price comparison with offline products. During the 2017 Diwali sale, Polycab fans became Amazon's bestseller in the category, generating ₹18 crores in just three days and proving that brand preference was building.

Product innovation accelerated as confidence grew. The 2018 launch of HOHM home automation solutions represented ambitious technological leap—IoT-enabled switches, app-controlled fans, and voice-activated lighting. While sales remained modest, the products established Polycab as innovative rather than imitative. The "Shakti" series of energy-efficient fans, consuming 35% less power than conventional models, won the National Energy Conservation Award and provided differentiation beyond price.

Channel synergies finally materialized by 2019. Dealers reported that contractors who came for cables increasingly bought complete electrical packages. The average transaction value increased 40% when customers bought across categories. More importantly, Polycab products were specified together in architectural plans, creating pull-through demand that competitors couldn't disrupt through dealer incentives alone.

The social media strategy evolved from non-existent to sophisticated. Rather than celebrity endorsements that competitors favored, Polycab focused on influencer electricians and contractors—the actual decision-makers in electrical purchases. YouTube channels featuring installation tutorials, WhatsApp groups for technical support, and Instagram pages showcasing project completions created community-driven marketing that resonated with trade audiences while building consumer awareness.

By March 2019, as Polycab prepared for its IPO, FMEG had achieved what seemed impossible five years earlier: quarterly operational profitability. Revenues touched ₹890 crores, losses had transformed into modest profits, and distribution reached 125,000 retail outlets. The segment still contributed just 8% of overall revenues versus 92% from cables, but trajectory mattered more than current contribution. Polycab had proven it could build consumer brands, compete with established players, and leverage its B2B heritage into B2C success.

The diversification debate that had raged in that 2013 board meeting was settled. Polycab wasn't abandoning its cable heritage—it was extending it. Every fan that spun, every switch that clicked, every light that illuminated carried copper from Polycab cables, creating an ecosystem play that competitors had missed. The company that had powered India's infrastructure was now powering its homes, and the IPO would provide capital to accelerate both journeys.

V. Going Public: The ₹1,346 Crore IPO (2019)

The conference room at Trident Hotel, Nariman Point, fell silent as Inder Jaisinghani walked to the podium on March 15, 2019. The roadshow for Polycab's initial public offering had reached Mumbai, the final stop after presentations in Singapore, London, New York, and Hong Kong. The audience—fund managers controlling over ₹2 lakh crores—had heard hundreds of IPO pitches. Most were forgettable. Inder intended to ensure Polycab's wasn't.

He began not with financial projections or market opportunities, but with a photograph: his father's original electrical shop in Lohar Chawl, barely visible through monsoon flooding, the inventory floating in muddy water. "Forty-three years ago, we lost everything in one night. The next morning, we started again. That resilience—not our factories or products—is what you're investing in." The room's energy shifted. This wasn't another PowerPoint recitation; it was a founder's manifesto.

The IPO timing seemed questionable to many observers. Election uncertainty loomed with polls just weeks away. The IL&FS crisis had frozen credit markets. Jet Airways had just collapsed, spooking investors about corporate governance. Yet Kotak Mahindra Capital, Axis Capital, and Citigroup—the investment banks managing the offering—saw opportunity in adversity. The very factors deterring others created scarcity value for quality companies willing to brave uncertain markets.

The pricing negotiations revealed fascinating dynamics. Polycab sought valuations comparable to Havells, which traded at 45 times earnings. Investors countered that Havells had stronger brands and higher FMEG mix. The middle ground emerged through creative structuring: a price band of ₹533-538 per share, valuing Polycab at ₹8,000 crores—premium to pure cable players like KEI Industries but discount to diversified competitors. The offer included ₹400 crores of fresh capital for expansion and ₹946 crores of offer-for-sale by existing investors, primarily IFC's partial exit.

Due diligence uncovered skeletons that required delicate handling. Tax disputes totaling ₹287 crores needed disclosure. Related-party transactions with family-owned trading entities required unwinding. The discovery that certain dealers were actually controlled by extended family members necessitated restructuring distribution agreements. Each issue was methodically addressed—disputes provisioned, transactions ceased, agreements formalized—transforming potential deal-breakers into proof of governance commitment.

The prospectus itself became a strategic document. Rather than standard boilerplate, Polycab crafted a narrative arguing that India's electrical consumption would triple by 2030, driving ₹5 lakh crores of infrastructure investment. They positioned themselves not as cable manufacturers but as "electrical solutions providers," highlighting that 65% of costs in electrical projects involved products Polycab manufactured. The FMEG losses, rather than being hidden in footnotes, were presented as investment in future growth engines, with detailed path-to-profitability metrics.

Anchor investor allocation proved surprisingly competitive. Government of Singapore Investment Corporation bid for the entire anchor portion. Fidelity, Aberdeen, and Goldman Sachs fought for allocations. The final anchor book of ₹404 crores was covered four times, with marquee investors like Nomura, HDFC Mutual Fund, and SBI Mutual Fund receiving allocations. This institutional validation proved crucial for retail confidence.

The subscription period from April 5-9, 2019, witnessed drama worthy of a thriller. Day one saw modest 3.2 times subscription, primarily from retail investors attracted by the brand recognition. Day two exploded to 18 times as high-net-worth individuals piled in, sensing momentum. The final day reached crescendo with 52 times oversubscription—institutional investors bid for ₹31,000 crores against ₹600 crores available, while retail portion was covered 10 times despite the ₹2 lakh individual limit.

Listing day, April 16, 2019, began before dawn. Inder arrived at NSE at 6 AM, performing puja at the building's temple—a ritual he had observed at every milestone since Halol's inauguration. The opening bell ceremony, typically formulaic, turned emotional when Thakurdas, now 89 and wheelchair-bound, was wheeled onto the stage. His hand, guided by Inder's, rang the bell that marked the transformation of a refugee's dream into public corporation.

The stock opened at ₹633, an 18% premium to issue price, and touched ₹668 within minutes. Volume exceeded 5 crore shares in the first hour alone. By day's end, Polycab's market capitalization had reached ₹9,400 crores, creating wealth of ₹2,800 crores for the Jaisinghani family while still leaving them with 68% control. Inder's personal stake was worth ₹4,200 crores, officially entering him into India's billionaire ranks, though he learned this from newspapers rather than checking himself.

The post-IPO transformation was immediate and profound. Quarterly earnings calls replaced annual vendor meetings as primary communication channels. Independent directors, including former SEBI chairman M. Damodaran and ex-Hindustan Unilever CFO Tara Murali, brought institutional discipline. Employee stock options worth ₹140 crores were distributed to 400 managers, aligning interests and preventing talent poaching. The legal structure simplified from seventeen entities to four, improving transparency and reducing complexity.

Capital allocation became more sophisticated. The ₹400 crores raised was deployed with surgical precision: ₹180 crores for backward integration into copper drawing, ₹120 crores for FMEG capacity expansion, ₹60 crores for working capital optimization, and ₹40 crores for technology upgradation. Each investment included specific return hurdles and milestone tracking, a departure from the intuitive decision-making of private years.

The institutionalization extended beyond finances. Hiring practices transformed—campus recruitment from IITs and IIMs replaced referral-based selection. McKinsey was engaged to redesign organizational structure, creating strategic business units with P&L responsibility. Salesforce CRM replaced Excel-based dealer tracking. SAP S/4HANA unified operations across locations. The family business was becoming a professionally managed corporation while retaining entrepreneurial agility.

Investor relations became a strategic function. Quarterly presentations evolved into comprehensive documents analyzing industry trends, competitive dynamics, and strategic initiatives. Management started hosting annual investor days, plant visits for analysts, and regular conference calls with international investors. The transparency was radical by Indian mid-cap standards—even disappointing news was communicated proactively rather than buried in footnotes.

The wealth creation extended beyond promoters. Dealers who had partnered during difficult years were allocated shares in the IPO's reserved category. Long-serving employees received bonuses linked to stock performance. Even the security guard at Halol, who had served since 1989, received shares worth ₹5 lakhs—life-changing wealth for someone earning ₹15,000 monthly. This inclusive approach built loyalty that money alone couldn't buy.

Market reaction validated the IPO's success. Within six months, the stock had doubled to ₹1,100, outperforming the Sensex by 40%. Research coverage expanded from two domestic brokerages to twelve global firms. Inclusion in MSCI indices brought automatic buying from passive funds. The liquidity improved dramatically—daily trading value increased from ₹10 crores pre-IPO to ₹200 crores post-listing, ensuring that large investors could build or exit positions without impacting price.

By December 2019, as the first fiscal year as a public company concluded, the transformation was complete. Revenues had grown 17% to ₹8,800 crores. Profits increased 23% to ₹690 crores. Market capitalization touched ₹15,000 crores. The Forbes India Rich List ranked the Jaisinghani family at 62nd position with collective wealth of $2.3 billion. But for Inder, the most meaningful metric was different: Polycab had become the first Indian electrical company to successfully transition from family enterprise to institutional ownership while maintaining entrepreneurial culture.

The IPO proceeds had funded expansion, the public scrutiny had improved governance, and the currency of listed shares had enabled acquisitions. But most importantly, it had forced Polycab to articulate its vision beyond family ambitions—to become India's electrical infrastructure champion, a goal that would soon be tested by competition from unexpected quarters.

VI. Market Dynamics & Competitive Landscape

The press conference on September 12, 2023, lasted exactly seven minutes. Kumar Mangalam Birla, chairman of the Aditya Birla Group, announced that UltraTech Cement would invest ₹18,000 crores to enter the wires and cables business. The stock market's reaction was immediate and brutal—Polycab crashed 8%, KEI Industries fell 11%, and Havells dropped 6%. In those seven minutes, ₹12,000 crores of market value evaporated from established players. The comfortable oligopoly that had controlled India's electrical industry for two decades was under assault from an unexpected direction.

Understanding why cement companies and infrastructure giants suddenly coveted the cable business requires examining the industry's hidden economics. While outsiders see commodity products with thin margins, insiders understand a different reality. The organized cable market generates 15-18% EBITDA margins, requires minimal technology investment once established, and enjoys negative working capital as customers pay upfront while suppliers accept credit. Most critically, it provides steady cash flows relatively immune to economic cycles—people might defer buying cars during recessions, but electrical maintenance continues regardless.

The market structure itself invited disruption. Despite India's ₹75,000 crore cable market being the world's third-largest after China and the United States, the organized sector controlled just 40%. The remaining 60% consisted of 2,000-plus small manufacturers, often operating from single sheds, selling unbranded products through local contractors. This fragmentation created opportunity for consolidation, especially as GST implementation and quality regulations progressively disadvantaged informal players.

Polycab's 26% market share in the organized segment meant it sold just ₹11,000 crores in a ₹75,000 crore market—dominant yet paradoxically subscale. This mathematical reality explained why new entrants saw opportunity. If they could accelerate the shift from unorganized to organized—through brand building, distribution reach, or regulatory enforcement—the addressable market would double even without overall growth. Add India's 9% annual electrical consumption growth, and the opportunity became irresistible.

The competitive landscape resembled a medieval battlefield with multiple armies converging. KEI Industries, the second-largest player, had pursued aggressive capacity expansion, adding three plants in two years. RR Kabel, backed by private equity firm Chrys Capital, was rolling up regional players to build national scale. Havells leveraged its consumer brand strength to premium-price commodity cables. Finolex exploited backward integration into PVC manufacturing for cost advantage. Each had distinct strategies, but all faced the same new threat.

Adani Group's entry through a joint venture with Mundra Copper added another dimension. They controlled copper smelting—the primary raw material constituting 70% of cable costs. This vertical integration theoretically provided 5-7% cost advantage, enough to destroy industry pricing while remaining profitable. The threat wasn't immediate—building distribution would take years—but the direction was clear. Industries previously considered too fragmented for conglomerates were now consolidation targets.

The distribution moat that established players considered impregnable proved more fragile than expected. Polycab's 3,200 dealers and 165,000 retailers had been cultivated over decades through relationship building, credit support, and exclusive territories. But new entrants brought different weapons. UltraTech could leverage its cement dealer network—many sold building materials including electrical products. Adani could bundle cables with solar panels and transmission equipment. Digital platforms like Moglix and Zetwerk were bypassing traditional distribution entirely, connecting manufacturers directly with contractors.

Technology disruption compounded competitive pressure. Smart cables with embedded sensors for preventive maintenance were emerging. Aluminum cables were substituting copper in certain applications. Optical fiber was replacing copper in communication infrastructure. Superconducting materials promised to revolutionize power transmission. While these remained niche, they signaled that competitive advantage would increasingly depend on innovation rather than just manufacturing scale.

Polycab's response revealed strategic sophistication. Rather than engaging in price wars that would destroy industry profitability, they accelerated premiumization. The "Etira" brand for super-premium houses wires commanded 25% price premiums through superior fire resistance and lifetime warranties. The "Green Wire" series targeted environmentally conscious consumers with lead-free, recyclable products. Commercial products emphasized total cost of ownership rather than purchase price, highlighting energy savings and longevity that justified premium positioning.

The international expansion strategy provided another differentiation vector. While domestic competition intensified, Polycab quietly built presence in 50 countries, generating ₹1,200 crores in exports. Middle Eastern construction booms, African infrastructure development, and Southeast Asian industrialization offered growth without domestic competition. The acquisition of a distribution company in Dubai and a manufacturing joint venture in Ethiopia demonstrated commitment beyond opportunistic exports.

Channel partner loyalty programs intensified to combat poaching. "Project Bandhan" created family-like bonds through initiatives beyond business—educating dealers' children, providing health insurance, organizing pilgrimages to religious sites. The "Privileged Partner" program offered working capital support at below-market rates, effectively sharing financial strength with channel partners. These soft benefits proved harder for new entrants to replicate than price discounts.

The brand building acceleration was visible everywhere. Television commercials during Indian Premier League matches, billboard campaigns in tier-2 cities, and digital marketing targeting young homeowners. The ₹200 crore annual marketing spend seemed excessive for a B2B company until you realized the game had changed—cables were becoming consumer products where brand preference mattered as much as technical specifications.

Competitive intelligence became military-grade. Polycab's strategy team tracked competitor capacity additions, monitored import data for equipment purchases, analyzed job postings to understand capability building, and maintained databases of dealer defections. Weekly war room meetings assessed threats and coordinated responses. The paranoia that Inder inherited from his refugee father—assuming someone was always trying to take what you'd built—proved valuable in this environment.

The financial market's initial panic about new competition gradually moderated as reality emerged. Building cable manufacturing wasn't technically complex, but building profitable cable businesses required capabilities that took years to develop. Product portfolios with thousands of SKUs, quality consistency across batches, rapid customer response, dealer relationship management—these organizational muscles couldn't be bought, only built through experience.

By early 2024, the competitive landscape had stabilized into uneasy equilibrium. UltraTech's cable factory remained under construction with commercial production eighteen months away. Adani was focusing on industrial cables, avoiding direct competition in building wires. Regional players were consolidating through mergers rather than competing independently. The feared price war hadn't materialized as rational players recognized mutual destruction served nobody's interests.

The unorganized sector's decline accelerated, shrinking from 60% to 55% market share in just eighteen months. This 5% shift represented ₹3,750 crores of addressable market moving to organized players—enough growth for everyone without fratricide. Quality regulations, GST compliance, and customer preference for branded products drove this transition, validating Polycab's long-term thesis that formalization would create more opportunity than competition.

Market share data by late 2024 showed Polycab had actually strengthened its position, reaching 27.5% of the organized market. The threat of new entrants had paradoxically helped by accelerating industry consolidation, improving pricing discipline, and forcing capability building that improved competitiveness. The company that had survived Partition, License Raj, liberalization, and demonetization was proving equally resilient to competition.

The real insight wasn't that Polycab was invulnerable—no company is. Rather, it was that in industries with deep technical knowledge, extensive distribution, and relationship-based selling, insurgents faced higher barriers than financial capital alone could overcome. The refugees who had built from nothing understood something the conglomerates were learning: in India, trust travels through handshakes, not spreadsheets.

VII. Financial Performance & Unit Economics

The Excel spreadsheet on CFO Gandharv Tongia's screen told a story of transformation that few outside Polycab's finance team fully grasped. As he prepared for the Q2 FY25 earnings call in October 2024, the numbers revealed not just growth but a fundamental reimagining of what a cable company could achieve financially. Revenue for the quarter had touched ₹59.06 billion, up 25.71% year-over-year, but that headline number obscured the intricate machinery generating these results.

The unit economics of cable manufacturing appear deceptively simple: buy copper at ₹750 per kilogram, add ₹50 of PVC insulation and labor, sell for ₹900, earn ₹100 gross profit. This kindergarten math dissolves upon closer examination. Copper prices fluctuate 2-3% daily, meaning inventory bought Monday might be uncompetitive by Friday. Customer payment terms average 60 days while copper suppliers demand cash within 15 days, creating working capital chasms. Product mix complexity—Polycab manufactures 10,600 different SKUs—means that overall margins obscure massive variation between products, with some generating 40% gross margins while others lose money but maintain customer relationships.

The working capital optimization that Polycab achieved between 2019 and 2024 represented financial engineering at its finest. The cash conversion cycle—days inventory plus days receivables minus days payables—compressed from 67 days to 41 days. This 26-day improvement released ₹1,800 crores of cash from operations without selling additional products. The secret lay in seemingly mundane process improvements: RFID tracking that reduced inventory counting from weekly to real-time, dynamic credit scoring that adjusted customer terms based on payment history, and vendor financing programs that extended payables without damaging supplier relationships.

Segment analysis revealed the strategic chess game being played. Wires and cables generated ₹188 billion of FY25's ₹224 billion revenues—84% of total sales but 91% of EBITDA. The much-celebrated FMEG business contributed ₹35 billion in revenues but just ₹1.8 billion in EBITDA, a 5.1% margin that would horrify consumer goods companies. Yet this portfolio construction was deliberate. Cables provided cash generation and customer relationships. FMEG built brand value and consumer touchpoints. Together, they created competitive advantages that neither alone could achieve.

The copper hedging strategy deserved its own business school case study. Polycab maintained three-layer protection against commodity volatility. Physical inventory was hedged through forward contracts covering 60-70% of three-month requirements. Customer contracts included price variation clauses that passed through material cost changes beyond 3%. Strategic reserves were maintained in duty-free warehouses at ports, allowing arbitrage between domestic and international prices. This sophisticated approach meant that while competitors suffered margin compression during copper price spikes, Polycab's EBITDA remained remarkably stable at 11-12% regardless of commodity cycles.

Return on capital employed (ROCE) told the story of operational excellence. From 18% in FY19, ROCE had climbed to 29% by FY24, placing Polycab among the most efficient capital allocators in Indian manufacturing. This improvement came through asset sweating rather than financial leverage—capacity utilization increased from 65% to 82%, machine productivity improved through IoT-based monitoring, and outsourcing of non-critical processes reduced capital intensity. Every percentage point of ROCE improvement translated to ₹200 crores of additional value creation.

The geographic revenue distribution highlighted risk diversification. While 65% of revenues came from five states—Maharashtra, Gujarat, Rajasthan, Uttar Pradesh, and Tamil Nadu—no single state exceeded 18%. This prevented dependence on regional economic cycles. International revenues of ₹12 billion, though just 5% of total, carried 18% EBITDA margins due to premium positioning and dollar denomination that provided natural hedge against rupee depreciation.

Project business economics differed radically from retail sales. Large infrastructure projects—metros, airports, smart cities—generated 35% of revenues but required different financial management. These contracts involved performance guarantees, retention deposits, and milestone-based payments that could stretch across years. Polycab's project finance team had developed sophisticated models that evaluated not just stated returns but risk-adjusted returns incorporating execution delays, cost escalations, and collection uncertainties. The discipline to walk away from prestigious but unprofitable projects had prevented the margin dilution that plagued competitors chasing topline growth.

The dividend policy balanced growth investment with shareholder returns. The 25% payout ratio seemed conservative compared to FMCG companies distributing 60-70% of profits, but it reflected capital intensity of manufacturing and long-term expansion plans. The ₹50 per share annual dividend provided 3.2% yield at current prices—attractive for income investors while retaining sufficient capital for organic growth. Special dividends during exceptional years rewarded shareholders without creating unsustainable expectations.

Tax optimization, while never advertised, contributed meaningfully to bottom-line performance. Manufacturing facilities in backward areas enjoyed ten-year tax holidays. Export revenues qualified for reduced rates. R&D investments earned weighted deductions. Transfer pricing between units was structured to maximize benefits while remaining compliant. The effective tax rate of 22% versus statutory 30% meant an additional ₹180 crores annually flowing to shareholders rather than government coffers.

The financial technology infrastructure supporting these operations was world-class. Real-time dashboards tracked sales, collections, and inventory across locations. Predictive analytics forecasted demand by SKU and geography. Robotic process automation handled routine transactions. Artificial intelligence algorithms optimized pricing based on competitive dynamics, inventory levels, and customer lifetime value. This digital backbone enabled financial performance that manual processes could never achieve.

Quarterly earnings volatility had reduced remarkably. The coefficient of variation in quarterly EBITDA—a measure of earnings stability—had declined from 0.31 in 2019 to 0.18 in 2024. This predictability, rare in commodity-linked businesses, came through portfolio diversification, hedging strategies, and operational excellence that cushioned external shocks. Institutional investors valued this stability, accepting lower returns for reduced volatility.

The cash generation narrative was compelling. Operating cash flow had grown from ₹800 crores in FY19 to ₹2,200 crores in FY24, a 22% CAGR that exceeded profit growth due to working capital efficiency. This cash funded capacity expansion without debt, enabled strategic acquisitions, and provided buffer against economic downturns. The net cash position of ₹1,400 crores meant Polycab could survive extended disruptions or seize opportunities that leveraged competitors couldn't afford.

Comparative analysis with global peers revealed Polycab's unique position. While European cable manufacturers like Nexans and Prysmian had higher absolute margins, they operated in mature markets with 2-3% growth. Chinese competitors like Hengtong had larger scale but lower profitability due to intense domestic competition. Polycab occupied the sweet spot—emerging market growth rates with developed market margins, a combination that explained premium valuations despite commodity exposure.

The forward-looking guidance suggested confidence without complacency. Management projected FY26 revenues of ₹280 billion, implying 25% growth, with EBITDA margins expanding to 12.5% through operating leverage and premiumization. The capital expenditure plan of ₹5 billion over two years would add 30% capacity while improving efficiency through automation. These projections, historically conservative, suggested that the financial performance trajectory would continue despite competitive pressures.

As Gandharv concluded his earnings presentation, he emphasized what numbers couldn't capture: the financial discipline embedded in Polycab's DNA. Every manager understood their unit's ROCE. Every salesperson knew customer profitability. Every factory worker recognized the connection between quality and margins. This financial literacy, rare in traditional manufacturing, created alignment that no incentive system alone could achieve.

The transformation from ₹1 crore revenue in 1983 to ₹224 billion in 2024 represented a 26% compound annual growth rate sustained over four decades—a feat that fewer than dozen Indian companies had achieved. But for Polycab, this was prologue rather than climax. The financial foundation was built; now came the challenge of maintaining momentum while navigating new threats and opportunities.

VIII. Strategic Initiatives & Future Roadmap

The war room on the seventh floor of Polycab House hummed with controlled urgency on a humid August morning in 2024. Project Spring, the company's five-year strategic transformation initiative, was entering its most critical phase. Inder Jaisinghani, now 71 but still arriving at office by 7 AM daily, studied the giant digital dashboard displaying real-time metrics from 28 manufacturing facilities, 4,000 distributors, and 165,000 retailers. The numbers told a story of success—Project Leap's FY26 targets had been achieved two years early—but Inder's expression suggested satisfaction with the past was dangerous when the future arrived at digital speed.

Project Spring represented audacious ambition: reaching ₹400 billion revenue by FY29 while improving EBITDA margins to 14%. The arithmetic was simple—12% annual growth for five years. The execution would require reimagining every aspect of operations. Unlike Project Leap, which focused on capacity and distribution expansion, Spring emphasized capability building in areas where Polycab had limited expertise: digital commerce, sustainable manufacturing, and solution selling rather than product pushing.

The backward integration strategy had evolved beyond simple copper sourcing. The Ryker Base joint venture, established with Digvijay Finlease in 2021, was constructing India's largest secondary copper smelting facility in Gujarat. This ₹2,000 crore investment would process 200,000 tons of copper scrap annually, converting electronic waste and industrial recycling into high-grade copper rods. The economics were compelling—secondary copper cost 15% less than primary copper while reducing carbon footprint by 60%. More strategically, it provided supply security as global copper demand exceeded mine production capacity.

But Ryker Base represented just one node in an ambitious vertical integration plan. Polycab was establishing a PVC compounding unit to produce specialized insulation materials in-house. A aluminum rolling mill would enable entry into aerial cables where aluminum was replacing copper. A fiber optic drawing tower was under construction to serve the telecom infrastructure boom. Each investment followed the same logic: control critical inputs, capture value addition, and build technical capabilities that competitors couldn't easily replicate.

The international expansion strategy had shifted from opportunistic exports to systematic market building. Dubai had become the Middle Eastern hub, with a 50,000-square-foot warehouse serving six Gulf countries. The Ethiopian manufacturing joint venture, 51% owned by Polycab, had commenced production of building wires for East African markets. Negotiations were advanced for acquiring a struggling cable manufacturer in Indonesia, providing entry to Southeast Asia's fastest-growing economy. The target was 15% of revenues from international markets by FY29, up from current 5%.

Digital transformation went beyond ERP systems and e-commerce platforms. Polycab was building what they called the "Connected Electrical Ecosystem"—an IoT platform where every product would communicate status and performance. Smart cables would predict failures before they occurred. Intelligent panels would optimize power distribution. Connected fans would adjust speed based on room occupancy. This wasn't science fiction—pilot installations in Pune's Tech Mahindra campus and Mumbai's Oberoi Mall were already operational, generating data that would define next-generation products.

The HOHM brand, launched quietly in 2020, was being positioned as Polycab's innovation spearhead. Rather than competing with established home automation players like Schneider or Legrand on their terms, HOHM targeted uniquely Indian use cases. The "PowerSaver" module identified and eliminated phantom power consumption from devices in standby mode—a ₹2,000 device that saved ₹500 monthly in typical homes. The "SafetyNet" system sent alerts if electrical parameters indicated fire risk. The "LoadOptimizer" prevented tripping by intelligently managing power distribution. These solutions addressed real problems rather than offering technology for its own sake.

Manufacturing excellence initiatives bordered on obsessive. The Halol facility was being transformed into a "lighthouse factory"—Industry 4.0 showcase with full automation, artificial intelligence-driven quality control, and zero-waste operations. Collaborative robots worked alongside humans, handling repetitive tasks while workers focused on problem-solving. Computer vision systems detected defects invisible to human eyes. Digital twins simulated production scenarios to optimize scheduling. The productivity improvements were staggering—output per worker had increased 40% while quality defects decreased 60%.

The sustainability agenda went beyond regulatory compliance to competitive advantage. Polycab had committed to carbon neutrality by 2030, requiring 50% reduction in emissions and offsetting remainder through renewable energy investments. Solar panels would cover 60% of factory rooftops. Wind power purchase agreements would provide another 30% of electricity needs. Energy-efficient equipment would reduce consumption by 25%. These investments, totaling ₹800 crores, would generate 18% IRR through energy cost savings while positioning Polycab as the sustainable choice for environmentally conscious customers.

Human capital development received unprecedented investment. Polycab University, established in partnership with IIT Bombay, provided technical education to employees and channel partners. The curriculum ranged from basic electrical theory for shop-floor workers to advanced material science for engineers. Leadership development programs, designed by Harvard Business School executive education, prepared next-generation managers for complexity beyond traditional manufacturing. The ₹100 crore annual investment in training seemed excessive until you realized that competence gaps, not capital constraints, limited growth.

The R&D transformation was remarkable for a company that had historically been fast followers rather than innovators. The new Technical Center in Chennai employed 200 engineers and scientists, including 15 PhDs recruited from premier institutions. Research focused on next-generation materials—graphene-enhanced conductors, bio-based insulations, self-healing cables that automatically repaired minor damage. While commercial applications remained years away, the patent filings—47 in FY24 alone—signaled serious innovation intent.

Channel partner evolution was equally dramatic. The traditional dealer model was supplemented with new formats addressing changing customer behavior. Polycab Galleries—exclusive brand stores in high-street locations—provided immersive experience centers where architects and homeowners could visualize electrical solutions. Mobile vans equipped with AR/VR demonstrations reached tier-3 towns where permanent stores weren't viable. Digital catalogues with 3D product models enabled virtual selection. The omnichannel approach ensured that customers could engage however they preferred.

The acquisition strategy had matured from opportunistic purchases to systematic capability building. Polycab was evaluating three targets: a German specialty cable manufacturer with advanced fire-resistant technology, an Indian IoT startup developing energy management solutions, and a Vietnamese trading company providing Southeast Asian distribution. Each would bring capabilities that organic development would take years to build. The ₹2,000 crore war chest for acquisitions suggested serious intent beyond evaluation.

Strategic partnerships multiplied as Polycab recognized that controlling everything internally limited growth. Collaboration with Siemens brought industrial automation expertise. Partnership with Amazon Web Services enabled cloud-based IoT platforms. Alliance with Indian Institute of Science fostered advanced materials research. Joint development with Larsen & Toubro created specialized cables for metro rail projects. These partnerships provided capabilities without capital, expertise without employment, and speed without sacrifice.

The competitive response strategy had evolved from reactive defense to proactive offense. Rather than waiting for UltraTech and Adani to build positions, Polycab was creating barriers through customer lock-in. Long-term contracts with major real estate developers guaranteed five-year supply agreements. Exclusive partnerships with electrical contractors included training, financing, and technology support. Original equipment manufacturer (OEM) relationships with fan and appliance manufacturers embedded Polycab components in finished products. These structural advantages would persist regardless of competitive intensity.

Risk management had become sophisticated as complexity increased. Enterprise risk management systems identified and quantified 127 distinct risks—from copper price volatility to cyber attacks, from regulatory changes to climate disruptions. Each risk had mitigation plans, early warning indicators, and crisis response protocols. The business continuity planning that seemed excessive proved prescient when ransomware attacks and tax raids tested organizational resilience.

The governance evolution continued as professional management gradually assumed operational control from the founding family. Inder remained Executive Chairman, providing vision and values. His son Nikhil, with an MBA from Wharton, led strategy and innovation. Professional CEOs managed day-to-day operations. Independent directors, now forming majority of the board, brought global perspectives and governance discipline. This transition, managed gradually to preserve culture while improving capability, positioned Polycab for institutional longevity beyond founder dependence.

As 2024 drew to a close, Project Spring was ahead of schedule. Q3 revenues would exceed ₹70 billion for the first time. FMEG had achieved 8% EBITDA margins, approaching profitability targets. International revenues were growing 40% annually. Digital sales had reached ₹500 crores monthly. The strategic initiatives were delivering results that validated ambitious planning.

Yet Inder remained restless. During the monthly strategy review, he reminded his team of his father's words: "Success makes you comfortable, comfort makes you vulnerable, vulnerability makes you a victim." The strategic roadmap wasn't about reaching destinations but maintaining momentum. In an industry where Chinese competitors had 10x scale and American giants had 10x margins, Polycab's advantage lay in agility, ambition, and the immigrant's instinct that nothing was permanent except change itself.

IX. Playbook: Lessons from the Polycab Story

The Harvard Business School case study on Polycab, published in September 2024, opened with a provocative question: "How does a commodity manufacturer in a capital-intensive industry with powerful competitors achieve 26% CAGR over four decades while maintaining family control?" The 37-page analysis that followed dissected strategic decisions, operational choices, and cultural factors that enabled this performance. But the real insights—the tacit knowledge that couldn't be captured in frameworks and matrices—emerged from pattern recognition across Polycab's journey.

Building trust in a low-trust market represented Polycab's foundational insight. In India, where contract enforcement remains weak and payment delays endemic, trust becomes competitive advantage. Polycab's approach wasn't sophisticated—it was consistent. Every commitment, however small, was treated as sacred. When the 1992 Babri Masjid riots disrupted supply chains, Polycab chartered planes to maintain deliveries. During the 2016 demonetization crisis, they extended unlimited credit to dealers facing cash crunches. This reliability, accumulated over decades, created switching costs that no discount could overcome.

The trust architecture extended beyond commercial relationships. Factory workers received salaries on the 1st of every month, even when customers delayed payments. Suppliers were paid within agreed terms, even during working capital crunches that required promoters to inject personal funds. Quality complaints were addressed without questioning validity, with replacement products shipped before investigations concluded. This systematic over-delivery on promises created network effects—dealers recommended Polycab to peers, workers referred relatives for employment, suppliers prioritized Polycab orders during shortages.

Patient family capital provided strategic flexibility that public companies couldn't match. The FMEG business lost money for five years before turning profitable—losses that would have triggered activist investor revolts in listed companies. The Halol facility expansion proceeded despite 18-month delays and 40% cost overruns because the family viewed it as generational investment rather than quarterly earnings impact. The decision to maintain full employment during COVID-19 lockdowns, costing ₹200 crores, reflected values rather than valuations.

But patient capital didn't mean sleepy capital. The Jaisinghani family's involvement was intense and intimate. Inder personally interviewed every manager hire until the company had 500 employees. Family members rotated through different functions, understanding operations from ground up. Board meetings lasted entire days, with detailed operational reviews rather than high-level presentations. This depth of engagement enabled quick decisions during crises and long-term thinking during stability.

Channel partner management transcended traditional distribution relationships. Polycab's 4,000 dealers weren't just customers—they were extended family. The company maintained detailed databases on dealers' children's education, family health issues, and business challenges beyond Polycab products. Dealer meets weren't sales conferences but community gatherings, with religious ceremonies, cultural programs, and family participation. When dealers faced financial difficulties—from medical emergencies to business losses—Polycab provided interest-free loans, sometimes written off quietly.

The channel loyalty this created proved invaluable during competitive attacks. When Havells offered 5% extra margins to poach dealers in 2018, less than 3% switched. When Amazon approached dealers for direct supply relationships bypassing Polycab, most declined despite attractive terms. This wasn't sentiment but rational calculation—dealers understood that Polycab's support during difficulties outweighed marginal economic gains from switching.

Timing market transitions required patience and preparation that looked like inaction to outside observers. Polycab entered organized retail five years after competitors, but when they did, they had products, processes, and people ready. They launched e-commerce operations three years after category creation, but with dedicated fulfillment centers and digital-specific SKUs. This deliberate delay wasn't indecision but discipline—waiting until business models clarified, learning from others' mistakes, then executing with precision.

The unorganized-to-organized transition that Polycab rode wasn't accident but anticipation. They invested in quality certifications when customers didn't value them, built brands when B2B purchases seemed purely functional, and created documentation systems when handshake deals sufficed. These investments, which seemed premature, positioned Polycab perfectly when GST implementation and quality regulations suddenly advantaged organized players.

Managing commodity cycles required contrarian thinking that challenged conventional wisdom. When copper prices spiked, competitors raised prices immediately to protect margins. Polycab absorbed increases temporarily, gaining share from customers grateful for stability. When copper crashed, they reduced prices slowly, using windfall margins to invest in capability building. This counter-cyclical approach smoothed earnings while building competitive advantages during volatility.

The intellectual property approach was uniquely Indian. Rather than pursuing patents that were difficult to enforce, Polycab focused on trade secrets embedded in processes. The specific temperature profiles for PVC extrusion, the mixing sequences for fire-resistant compounds, the annealing procedures for copper drawing—these were protected through employee contracts, compartmentalized knowledge, and cultural conditioning rather than legal frameworks. Competitors could copy products but not processes, resulting in quality differences that customers recognized.

The diversification versus focus debate that paralyzed many Indian companies was resolved through pragmatic experimentation. Rather than strategic planning exercises, Polycab tested ideas through small bets. The FMEG entry began with one product in one city. The backward integration started with trading before manufacturing. International expansion commenced with exports before local operations. This experimental approach limited downside while providing real-world learning that informed larger commitments.

Corporate governance evolution demonstrated that professionalization needn't mean de-familialization. The family retained majority control while ceding operational management to professionals. Independent directors brought expertise while respecting entrepreneurial culture. Transparency increased through voluntary disclosures beyond regulatory requirements. This hybrid model—family values with professional processes—attracted institutional investors while maintaining strategic flexibility.

The talent management philosophy reflected refugee pragmatism. Polycab hired attitude and trained aptitude, recruiting from tier-2 engineering colleges and community colleges rather than competing for IIT graduates. The ten-year average tenure, exceptional in Indian manufacturing, came through cultural integration rather than golden handcuffs. Employees became stakeholders through stock options, dealers through preferred allotments, and communities through CSR investments that created shared prosperity.

The technology adoption strategy was refreshingly practical. Rather than digital transformation for its own sake, Polycab digitized where it created value. IoT sensors were installed on critical equipment but not everything. AI was applied to quality control but not forecasting. Blockchain was explored for supply chain but not implemented prematurely. This selective adoption avoided the technology tourist trap that distracted many manufacturers.

The competitive response framework was sophisticated in its simplicity. Polycab categorized competitors into three buckets: those to fight (direct competitors in core markets), those to avoid (deep-pocketed conglomerates in adjacent spaces), and those to embrace (technology startups with complementary capabilities). Resources were allocated accordingly—aggressive defense in cables, cautious expansion in FMEG, and collaborative exploration in digital solutions.

The internationalization approach reflected lessons from Indian companies' global misadventures. Rather than marquee acquisitions in developed markets, Polycab focused on similar markets at different development stages. Ethiopia resembled India of the 1990s. Vietnam looked like India of the 2000s. These markets were comprehensible, allowing replication of proven strategies rather than requiring new capabilities.

The financial discipline wasn't about sophistication but simplicity. Every employee understood three metrics: ROCE for capital efficiency, inventory turns for working capital, and customer complaints for quality. These simple measures, tracked obsessively and rewarded consistently, aligned thousands of employees without complex balanced scorecards or key performance indicators that nobody understood.

The cultural elements were hardest to replicate. The morning prayer at every facility, mixing Hindu, Sikh, Muslim, and Christian traditions, created inclusive identity. The open-door policy, where workers could approach Inder directly, prevented bureaucratic ossification. The promotion-from-within philosophy, with 80% of senior managers rising through ranks, ensured cultural continuity. These soft factors created hard advantages that financial engineering couldn't replicate.

As business schools worldwide studied Polycab's playbook, they discovered something profound: success in emerging markets required different models than developed economy frameworks suggested. Patient capital trumped quarterly earnings. Relationships preceded transactions. Trust substituted for contracts. Evolution beat revolution. These weren't compromises but conscious choices, creating competitive advantages that global giants couldn't match despite superior resources.

The playbook's final lesson was perhaps most important: there was no playbook, only principles. Every decision reflected context rather than convention. Every strategy evolved through experimentation rather than planning. Every success prepared for the next challenge rather than providing permanent advantage. In this sense, Polycab's story wasn't about answers but about questions—how to build trust, create value, and sustain success in environments where the only constant was change itself.

X. Bear vs. Bull Case Analysis

The investment committee at Singapore's GIC faced a dilemma as they evaluated their Polycab position in November 2024. The stock had delivered 300% returns since their anchor investment in the 2019 IPO, but new threats and opportunities made the forward outlook unusually uncertain. The debate that unfolded over three hours captured the tensions inherent in Polycab's position—dominant yet vulnerable, growing yet cyclical, transforming yet traditional.

The bear case began with mathematical inevitability. At 52 times trailing earnings, Polycab traded at valuations that implied perfection. The PEG ratio of 2.1 suggested the market was pricing in growth rates that history suggested were unsustainable. Every manufacturing company that had sustained 25% growth eventually hit physical constraints—supplier capacity, skilled labor availability, or market saturation. The law of large numbers meant that growing ₹20,000 crores by 25% required adding ₹5,000 crores annually—equivalent to creating a mid-sized company every year.

The new competition wasn't ordinary—it was existential. UltraTech brought ₹18,000 crores of committed capital, a distribution network reaching every Indian pin code, and the Aditya Birla Group's century-old reputation. Their cement dealers already sold construction materials; adding cables was natural extension. More concerning, they could afford to lose money for a decade while building position—a luxury Polycab's public market obligations prevented. The stock market's initial 8% decline on UltraTech's announcement suggested investors understood this threat's magnitude.

Adani's entry through copper smelting was even more insidious. Controlling raw material that constituted 70% of cable costs provided structural advantage no operational excellence could overcome. They could squeeze independent manufacturers through supply restrictions or price discrimination while maintaining profitability through vertical integration. Historical precedents were sobering—when Reliance entered polyester, independent textile manufacturers were decimated. When Birla entered aluminum, downstream processors struggled. Vertical integration by giants usually ended badly for specialists.

The commodity nature of the core business created permanent vulnerability. Despite brand building efforts, purchasing decisions for cables remained primarily price-driven. Electrical contractors, who influenced 60% of purchases, showed minimal brand loyalty. Switching costs were negligible—a different brand of cable required no equipment changes or retraining. Product differentiation was limited—copper was copper, PVC was PVC, and claims of superior quality were difficult to verify. This commoditization meant that competitive advantage was temporary, eroded by imitation or substitution.

The FMEG business, despite recent profitability, remained subscale against specialists. Havells generated ₹8,000 crores from fans and lighting with 15% EBITDA margins. Crompton achieved similar metrics. Polycab's ₹3,500 crores FMEG revenue with 5% margins looked inadequate by comparison. Building consumer brands required decades, not years. The marketing investments needed to achieve relevance—₹500-1,000 crores annually—would destroy near-term profitability. The celebration of quarterly FMEG profitability obscured the reality that return on invested capital remained below cost of capital.

Technological disruption posed underappreciated risks. Wireless power transmission, though nascent, could eliminate vast categories of cables. Aluminum substitution for copper in multiple applications was accelerating. Smart grids reduced transmission losses, requiring fewer cables for equivalent power delivery. LED lighting's efficiency meant lower amperage requirements, enabling smaller cable sizes. Solar panels with integrated storage bypassed grid connections entirely. While none of these were immediate threats, their collective impact could shrink addressable markets significantly.