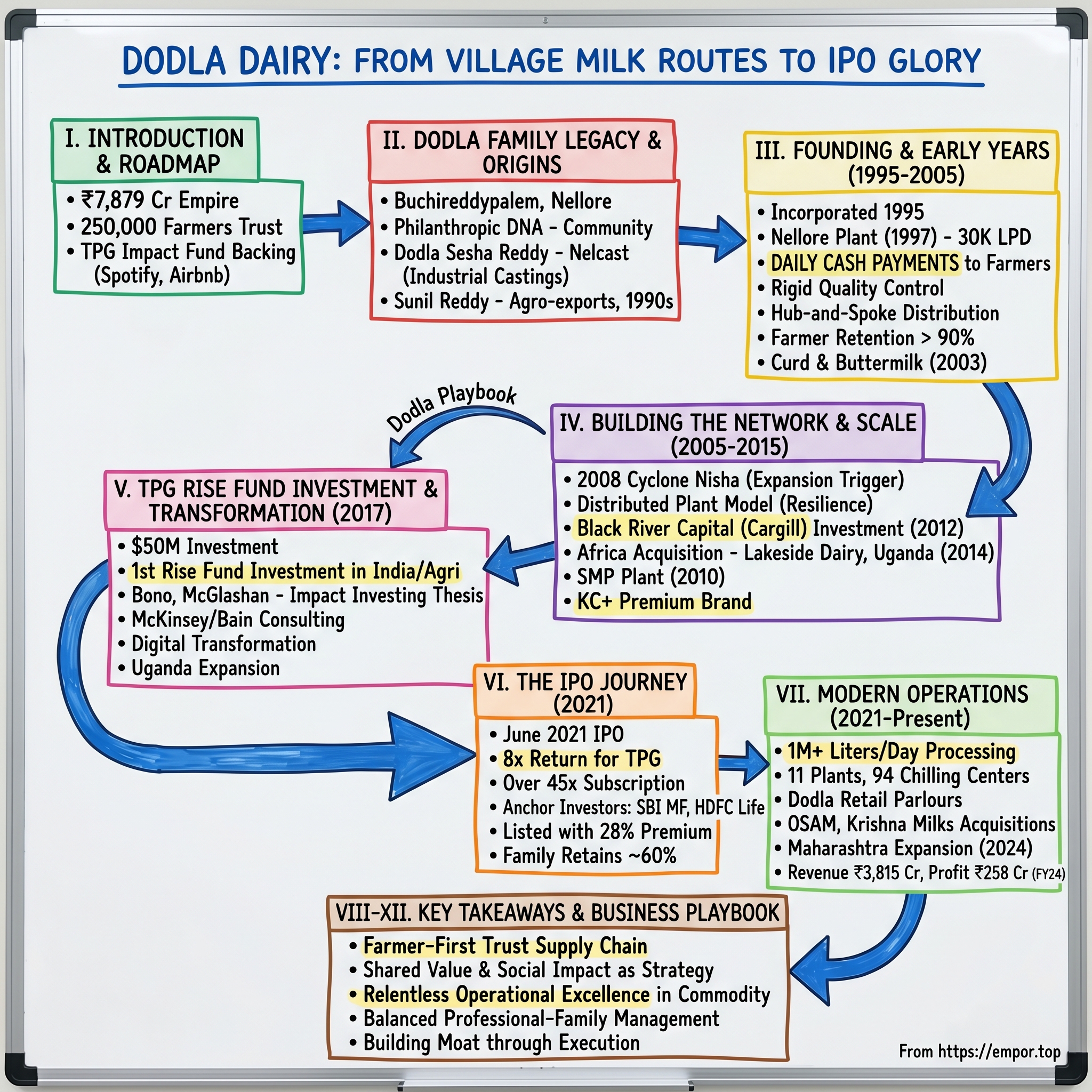

Dodla Dairy: From Village Milk Routes to IPO Glory - The South Indian Dairy Revolution

I. Introduction & Episode Roadmap

Picture this: It's 5 AM in rural Andhra Pradesh, and the morning mist hangs heavy over the Pennar river. A procession of farmers, some on foot, others on bicycles laden with aluminum milk cans, converges on a collection center. This scene, repeated across thousands of villages, forms the beating heart of a ₹7,879 crore empire—Dodla Dairy Limited.

How does a family from Nellore, better known for industrial castings than cattle, build one of India's most successful private dairy companies? How do you convince 250,000 farmers to trust you with their daily livelihood? And perhaps most intriguingly, how do you attract the same impact investor that backed Spotify and Airbnb to bet on milk collection in Telangana villages?

This is not just another family business story. It's a masterclass in building trust-based supply chains, navigating the complex dynamics between cooperatives and private enterprise, and timing capital markets to perfection. It's about transforming a commodity into a brand, turning daily milk runs into data points, and somehow making the unglamorous business of milk procurement attractive to global private equity.

Today, Dodla processes over a million liters of milk daily across 11 processing plants. Its products reach consumers from Tamil Nadu to Uganda. But the real story isn't in these numbers—it's in the strategic decisions, the near-misses, and the counter-intuitive bets that got them here.

We'll explore how a construction engineer turned milk entrepreneur, why TPG's impact fund saw gold in white milk, and what the future holds for a company straddling tradition and technology. Along the way, we'll unpack the unit economics of rural procurement, the art of managing perishable inventory, and the delicate dance between social impact and shareholder returns.

II. The Dodla Family Legacy & Origins

The story begins not in a boardroom or a business school, but in Buchireddypalem—a village near Nellore that most Indians couldn't locate on a map. Yet this settlement, established by the Dodla family's ancestors in the 18th century, would become the unlikely launching pad for one of India's dairy giants.

The Dodlas were not your typical agricultural landlords. They had a peculiar habit that set them apart: giving away prime land for schools and hospitals. This philanthropic DNA, seemingly at odds with hard-nosed business logic, would later prove to be their greatest strategic asset. When you're asking farmers to trust you with their only source of daily income, a two-century reputation for community service opens doors that money cannot.

Enter Dodla Sesha Reddy, the patriarch who would set the stage for the dairy empire. But Sesha Reddy wasn't thinking about milk when he founded Nelcast Limited in Gudur. His focus was on ductile iron castings—cylinder blocks, exhaust manifolds, the unglamorous but essential components that keep India's automotive industry running. Nelcast would grow into a significant player, establishing the family's credibility in managing complex supply chains and quality control—skills that would prove invaluable in an entirely different domain.

The protagonist of our dairy saga, however, is Dodla Sunil Reddy, Sesha Reddy's son. In 1990, fresh out of Mangalore University with an engineering degree, Sunil could have easily slipped into the comfortable grooves of the family's casting business. Instead, he spent six years in construction and agro-products export—sectors that taught him about rural India's purchasing power and the inefficiencies in agricultural markets.

By 1995, Sunil saw what others missed. Urban India was changing. The liberalization of 1991 had created a new middle class with disposable income and different consumption patterns. They wanted quality, consistency, and hygiene in their daily staples—attributes sorely lacking in the loose milk sold by local vendors. The organized dairy sector, dominated by cooperatives, controlled less than 20% of the market. Here was an ocean of opportunity hiding in plain sight.

But why would an industrial family with established businesses venture into dairy—a sector notorious for thin margins, complex logistics, and entrenched cooperative structures? The answer lay in Sunil's unique vantage point. His construction work had taken him to villages where he witnessed the dairy value chain firsthand. He saw farmers getting paid irregularly, milk being adulterated during transport, and urban consumers paying premium prices for questionable quality.

The Dodla family name carried weight in rural Nellore. When village elders heard that "Sesha Reddy's son" wanted to start buying milk, they listened. This wasn't some outside corporation trying to exploit farmers. This was, in the local parlance, "our people"—a family that had donated land for the very schools where their children studied.

Sunil's approach was radically different from both cooperatives and existing private players. While cooperatives offered farmers a voice but often delayed payments, and private players offered quick money but no loyalty, Dodla Dairy would offer something unique: daily payments, veterinary support, and the backing of a family whose reputation was literally carved in stone across local institutions.

III. The Founding Story & Early Years (1995-2005)

Dodla Dairy Limited was incorporated in 1995, but incorporation is just paperwork. The real challenge was convincing farmers to redirect their milk from established buyers to an untested startup. Sunil Reddy's first move was counterintuitive—instead of starting in an underserved market, he chose to set up operations right in Nellore, on the banks of the Pennar river, where competition from cooperatives and local vendors was fierce.

The location wasn't random. The Pennar river basin had two advantages: abundant water for processing operations and a concentrated cluster of dairy farmers within a 50-kilometer radius. More importantly, this was Dodla territory—where the family name meant something. When the first factory became operational in 1997, it wasn't just another industrial unit; it was validation of local trust.

The early procurement model was deceptively simple but revolutionary in execution. Every morning at 5 AM, Dodla's collection agents would be at designated points with testing equipment and cash. Farmers would bring their milk, watch it being tested for fat content and adulteration, and receive payment on the spot. No IOUs, no weekly settlements, no mysterious deductions. Cash in hand, every single day.

This daily payment system was financially risky—it meant Dodla needed significant working capital before selling a single liter of processed milk. But it solved the fundamental trust equation. As one early farmer supplier recalled, "Others talked about partnership; Dodla put money in our hands while the milk was still warm."

Quality control became an obsession from day one. While competitors often turned a blind eye to water adulteration (accepting it as the cost of maintaining supplier relationships), Dodla instituted rigid testing. Farmers caught adulterating were not just rejected; they were publicly identified, creating a social cost to cheating. Harsh? Perhaps. But it established Dodla's reputation for quality that would later command premium pricing in urban markets.

The cold chain infrastructure was another early differentiator. Most private players relied on middlemen with uncertain storage practices. Dodla invested in chilling centers at collection points, maintaining the cold chain from farm to factory. This reduced spoilage from 8-10% (industry average) to under 2%—a massive economic advantage in a low-margin business.

Distribution in the early years followed a hub-and-spoke model centered on Nellore town. Dodla didn't try to compete with established brands in modern retail initially. Instead, they focused on direct-to-home delivery through a network of delivery boys on bicycles—a channel where service and reliability mattered more than brand power. By 2000, Dodla had 3,000 regular household customers in Nellore alone, each receiving fresh milk at their doorstep by 6 AM.

The company commenced production at its Nellore plant in 1997 with a modest capacity of 30,000 liters per day. But Sunil Reddy was already thinking bigger. From 2001, Dodla embarked on a calculated expansion spree. Rather than building massive centralized facilities, they opted for smaller, strategically located plants in Penumuru, Palamaner, and Badvel. Each new plant followed the same playbook: establish trust with local farmers, ensure daily payments, maintain rigid quality standards, and build direct distribution networks.

By 2005, Dodla was processing 200,000 liters daily across four plants. Revenue had grown from ₹12 crores in 1998 to ₹180 crores. But more importantly, they had cracked the code on rural procurement. Their farmer retention rate was above 90%—unheard of in an industry where suppliers constantly switched based on daily price differences.

The challenges during this period were relentless. During the 2004 monsoon, flooding in coastal Andhra disrupted collection routes for weeks. Dodla's response? They hired boats to collect milk from marooned villages, absorbing the additional cost rather than abandoning suppliers. Stories like these spread through rural networks faster than any advertising campaign could.

Product diversification began modestly. While liquid milk remained the core, Dodla introduced curd and buttermilk by 2003, using excess capacity during lean procurement seasons. The genius was in the simplicity—these products required minimal additional investment but offered better margins than raw milk.

IV. Building the Network & Scale (2005-2015)

The decade from 2005 to 2015 would transform Dodla from a regional player into a South Indian powerhouse. But the trigger for this transformation came from an unexpected source—Cyclone Nisha in 2008, which devastated Tamil Nadu's dairy infrastructure. While competitors struggled to maintain supplies, Dodla's distributed plant network allowed them to redirect supplies from unaffected areas. Orders poured in from Tamil Nadu retailers desperate for reliable suppliers. Within six months, Dodla had established permanent operations in Chennai.

This natural disaster taught Sunil Reddy a crucial lesson: in the dairy business, resilience beats efficiency. While competitors built mega-plants to capture economies of scale, Dodla continued its distributed model. New plants opened in Sattenapalle, Tanuku, and critically, Tumkur in Karnataka—their first operation outside the Telugu states.

Each plant expansion followed what internally became known as the "Dodla Playbook." Six months before a plant opening, field teams would begin farmer engagement. They'd organize veterinary camps, distribute free cattle feed during the initial period, and most importantly, demonstrate their payment reliability by literally stacking cash at collection centers for farmers to see. By the time the plant opened, they'd have secured commitments for 70% of required capacity.

The numbers tell the story of this aggressive expansion. Dodla's processing capacity grew from 200,000 liters per day in 2005 to 1.2 million liters per day by 2015. The farmer network expanded from 15,000 to over 100,000. But the real transformation was in product sophistication.

In 2010, Dodla commissioned its first skimmed milk powder (SMP) plant in Nellore. This was a strategic masterstroke. SMP allowed them to convert excess procurement during flush seasons into a storable commodity, smoothing out the notorious seasonality of the dairy business. It also opened up institutional sales to food companies—a higher-margin, more predictable revenue stream than consumer sales.

The real validation came in 2012 when Black River Capital, the food-focused arm of agricultural giant Cargill, acquired a 23.66% stake in Dodla. The investment wasn't just about capital—though the ₹150 crores certainly helped fund expansion. Black River brought global best practices in supply chain management, introduced sophisticated quality testing protocols, and most importantly, provided credibility for Dodla's next phase of growth. The partnership with Black River Capital Partners (Cargill's investment arm) invested in Dodla Dairy, with holdings in livestock and dairy farms in India. This wasn't just passive capital—Black River brought operational expertise from managing agricultural assets globally. They introduced automated fat testing equipment at collection centers, implemented SAP for supply chain management, and most critically, helped Dodla access working capital lines at rates previously available only to multinationals.

But the most audacious move of this period came in 2014. While competitors focused on domestic expansion, Dodla looked to Africa. The acquisition of Lakeside Dairy in Uganda for approximately $8 million seemed bizarre to industry observers. Why would a company still establishing itself in South India venture into East Africa?

The logic was compelling once understood. Uganda's dairy sector in 2014 looked remarkably like India's in the 1990s—fragmented supply, growing urban demand, minimal organized players. But unlike India, there was virtually no competition from cooperatives. Dodla could apply its entire playbook without fighting entrenched interests. Within 18 months, the Uganda operation was profitable, validating the model's portability.

The product portfolio by 2015 had evolved far beyond liquid milk. Ghee (clarified butter) became a surprise hit, leveraging Dodla's access to high-quality butter and traditional preparation methods. Paneer (cottage cheese) targeted the growing quick-service restaurant sector. Ice cream, launched in 2013, used excess capacity during winter months when milk consumption typically dropped.

But the masterstroke was the introduction of the KC+ brand for premium products. While the main Dodla brand competed on value, KC+ targeted affluent consumers willing to pay 20-30% premiums for organic, farm-fresh products. This dual-brand strategy allowed Dodla to capture different market segments without diluting brand positioning.

By 2015, Dodla's numbers told a remarkable story. Revenue had crossed ₹1,500 crores. They were working with 100,000+ farmers across five states. The company operated 11 processing plants with combined capacity exceeding 1.2 million liters per day. More importantly, they had achieved something rare in Indian dairy—consistent EBITDA margins above 7%, nearly double the industry average.

V. The TPG Rise Fund Investment & Transformation (2017)

May 3, 2017, marked a watershed moment not just for Dodla, but for impact investing in India. When TPG's Rise Fund announced its $50 million investment in Dodla Dairy, it wasn't your typical private equity play. This was The Rise Fund's first investment in the food and agriculture sector, as well as its first in India.

The Rise Fund wasn't just another growth equity vehicle. Co-founded by TPG's Bill McGlashan, U2's Bono, and entrepreneur Jeff Skoll, it aimed to prove that generating competitive financial returns and creating measurable social impact weren't mutually exclusive. Dodla represented the perfect test case for this thesis.

The transaction structure was elegant. The deal provided a full exit for Proterra Investment Partners (the entity Black River had transformed into after Cargill's restructuring), while the Dodla family retained majority control. TPG acquired approximately 27% of the company, valuing Dodla at roughly $185 million—a significant premium to the valuation implied by Black River's original investment.

But why would TPG, which had backed companies like Uber and Airbnb, be interested in milk collection in Telangana? The answer lay in the numbers that most investors overlooked. Dodla was sourcing milk from 250,000 farmers across 7,000 villages every day of the year. Each farmer represented not just a supplier but a potential beneficiary of financial inclusion.

Bill McGlashan articulated the thesis with clarity: "Most of India's smallholders are only earning a few dollars a day, surviving on the brink of poverty". "Investments that facilitate stronger and more efficient market links in this food value chain can help to significantly reduce rural poverty".

The impact metrics were compelling. Working with regional banks, Dodla had helped more than 2,300 farmers secure financing to invest in their production capabilities. This wasn't corporate social responsibility window dressing—it was core to the business model. Better-financed farmers produced more milk, of higher quality, more consistently. Social impact and business performance were perfectly aligned.

TPG's involvement triggered a transformation that went beyond capital injection. They brought in consultants from Bain & Company to optimize the supply chain. McKinsey advised on product portfolio strategy. Most importantly, they introduced rigorous impact measurement frameworks—every quarter, Dodla would report not just financial metrics but social outcomes: farmer income improvements, veterinary services delivered, micro-loans facilitated.

The digital transformation accelerated under TPG's watch. By 2018, every collection center had tablets for real-time quality testing and payment processing. Farmers received SMS confirmations of their daily payments. An app allowed them to track milk prices, access veterinary advice, and even apply for cattle loans. This wasn't just digitization—it was using technology to deepen farmer engagement and switching costs.

Product innovation took a leap forward. TPG's network introduced Dodla to food technologists who helped develop extended shelf-life products using ultra-high temperature (UHT) processing. This opened up new geographies previously inaccessible due to cold chain limitations. By 2019, Dodla's UHT milk was reaching consumers in Northeast India, thousands of kilometers from their production base.

The Uganda operations, which had been a interesting experiment, became a strategic priority. TPG saw what Sunil Reddy had intuited—Africa represented a massive opportunity for the Dodla model. Under TPG's guidance, the Uganda facility expanded capacity by 300%, introduced new products tailored to local tastes, and most remarkably, began exporting to neighboring Kenya and Rwanda.

Vish Narain, Partner at TPG Growth, captured the commercial logic: "India's dairy consumption has been experiencing robust growth, fueled by urbanization, increasing incomes, and health consciousness among consumers". The organized sector was growing at 15-20% annually while the overall market grew at 5-6%. Dodla, with its established farmer network and processing infrastructure, was perfectly positioned to capture this shift.

The financial impact was immediate and substantial. Revenue grew from ₹2,100 crores in FY2017 to ₹2,800 crores in FY2020. EBITDA margins expanded from 7.5% to 9.2%—remarkable in a commodity business. But perhaps most importantly, Dodla's return on capital employed (ROCE) reached 24%, proving that social impact and superior financial returns could coexist.

The TPG partnership also brought unexpected benefits. Their portfolio company cross-pollination led to partnerships with logistics providers that reduced distribution costs by 12%. Connections with international dairy companies opened up technology transfer opportunities. Most intriguingly, TPG's relationship with major food service companies led to Dodla becoming a supplier to several multinational quick-service restaurants entering South India.

By 2020, as TPG began contemplating exit strategies, Dodla had transformed from a regional dairy company into a platform for inclusive growth. The question was no longer whether impact investing could work in traditional industries, but rather why more investors weren't following TPG's playbook.

VI. The IPO Journey & Public Markets (2021)

The timing of Dodla Dairy's IPO in June 2021 seemed counterintuitive. India was emerging from the devastating second wave of COVID-19. Capital markets were jittery. Yet for Dodla, this moment represented a unique confluence of factors that made going public not just attractive but essential.

The IPO structure was carefully crafted: a combination of fresh issue of 0.12 crore shares aggregating to ₹50.00 crores and offer for sale of 1.10 crore shares aggregating to ₹470.18 crores. Dodla Dairy IPO price band was set at ₹428 per share, valuing the company at approximately ₹2,400 crores—a remarkable journey from the ₹185 million valuation during TPG's entry just four years earlier.

The fresh capital of ₹50 crores was earmarked for debt reduction and capital expenditure—mundane uses that masked the strategic importance. By becoming debt-free, Dodla would have the financial flexibility to pursue aggressive expansion without dilution. The real story, however, was in the offer for sale component.

TPG Dodla Dairy Holdings sold 9,200,000 equity shares, while the Dodla family trusts and promoters sold a combined 1,785,444 shares. For TPG, this represented a spectacular exit—turning their $50 million investment into approximately ₹400 crores, an 8x return in rupee terms in just four years. This wasn't just a financial win; it validated the entire impact investing thesis in traditional sectors.

The pre-IPO preparation had been meticulous. Under TPG's guidance, Dodla had strengthened its board with independent directors, implemented robust corporate governance practices, and most importantly, delivered consistent financial performance even during the pandemic. FY2021 saw revenues of ₹2,624 crores with EBITDA margins of 10.2%—the highest in the company's history.

The anchor book built confidence. Dodla Dairy raised a little over Rs 156 crore from anchor investors a day before the public opening. Names like SBI Mutual Fund, HDFC Life, and Axis Mutual Fund participated—institutional validation that set the tone for retail participation.

When the IPO opened on June 16, 2021, the response exceeded expectations. By the end of the first day, the issue was subscribed 1.40 times. But the real surge came on days two and three. The final subscription numbers told a remarkable story: the issue was oversubscribed by more than 45 times overall. The qualified institutional buyers (QIB) portion was oversubscribed by 84.88 times, while the non-institutional investors' portion was oversubscribed by 73.26 times and the retail portion by 11.33 times.

What drove this enthusiasm? Part of it was scarcity value—Dodla was one of the few profitable, established companies coming to market in a sea of loss-making tech startups. But the deeper appeal lay in the business model's resilience. While tech companies struggled with unit economics, Dodla was generating cash from day one of operations.

The retail investor interest was particularly telling. In a market dominated by momentum traders, Dodla attracted long-term investors who understood the defensive nature of the dairy business. The minimum lot size of 35 shares meant a retail investor needed just ₹14,980 to participate—accessibility that broadened the shareholder base. Listing day, June 28, 2021, delivered vindication for everyone who believed in the Dodla story. The stock opened at Rs 528 on BSE, gaining 23% above IPO issue price, while on NSE it listed at Rs 550, a 28 per cent premium over the issue price of Rs 428 per share. But the real fireworks came during the trading session. The stock hit intra day high of Rs 633 on BSE.

Opening Price on NSE: INR550 per share (up 28.5% from IPO price) Closing Price on NSE: INR609 per share (up 42.29% from IPO price). For retail investors who received allotment, this meant a gain of over ₹6,300 per lot in a single day—remarkable returns in a market where most IPOs were struggling to hold their issue price.

The strong listing wasn't just about market exuberance. It reflected fundamental strengths that sophisticated investors recognized. Unlike tech unicorns burning cash for growth, Dodla was profitable from day one. Unlike consumer brands dependent on fickle urban preferences, Dodla sold an essential commodity with predictable demand. Unlike asset-light businesses vulnerable to competition, Dodla had built physical infrastructure and farmer relationships that would take decades to replicate.

TPG's exit was masterfully executed. By selling at the IPO rather than in subsequent block deals, they avoided overhang concerns that often depress post-listing performance. Their 8x return in four years became a case study at business schools—proof that impact investing in traditional sectors could generate venture-like returns.

For the Dodla family, the IPO represented both validation and transformation. While retaining 59.7% ownership post-IPO, they had created liquidity, attracted institutional shareholders, and established a currency for future acquisitions. Sunil Reddy's journey from construction engineer to leader of a public company worth over ₹3,500 crores was complete.

The post-IPO performance was equally impressive. Within two weeks of listing, the stock touched ₹650, a gain of over 50% from the issue price. More importantly, institutional investors who had missed the IPO began accumulating positions, providing support during market corrections.

VII. Modern Operations & Competitive Position (2021-Present)

The post-IPO era has seen Dodla accelerate its transformation from a regional dairy company into a national player with international ambitions. Today, the company processes over a million litres of milk per day in 11 processing plants, with milk sourced from over 2 lakh farmers and 66 chilling stations across Andhra Pradesh, Telangana, Tamil Nadu, and Karnataka.

The current operational footprint is impressive: 94 milk chilling centers, 152 milk chilling centers/plants, 55+ sales offices, 2,620+ agents, 2,110+ milk and milk product distributors, and 76 modern trade outlets across India. Additionally, the company's products are available through 626 'Dodla Retail Parlours' spread across South India—a direct-to-consumer initiative that improves margins while deepening brand engagement.

The product portfolio has evolved significantly beyond the traditional milk-and-curd offerings. The company now offers butter milk, ghee, curd, paneer, flavored milk, doodh peda, lassi, ice cream, and milk-based sweets under the Dodla, Dodla Dairy, and KC+ brands in India. The African operations, marketed under Dairy Top, Dodla+, and Pride of Cows brands, include milk, flavored yogurt, paneer, cheese, and UHT milk.

Maharashtra has emerged as the new frontier. In October 2024, Dodla completed the acquisition of 35.23 acres at Itkal Village, Dharashiv District, Maharashtra. This land acquisition represents more than just capacity expansion—it signals Dodla's ambition to replicate its South Indian success in Western India. The company intends to establish an integrated plant equipped with condensing as well as milk powder making capabilities, targeting the surrounding Solapur district's dairy belt.

The Maharashtra expansion is strategic on multiple levels. First, it provides access to one of India's largest dairy markets dominated by cooperatives, offering significant opportunity for organized private players. Second, the planned facility's powder-making capabilities will help manage seasonal fluctuations in milk procurement. Third, proximity to Mumbai—India's largest dairy consumption center—reduces logistics costs and improves product freshness.

Digital transformation has accelerated post-IPO. Every milk collection center now operates with real-time data transmission, allowing headquarters to monitor quality, quantity, and pricing across thousands of collection points simultaneously. Farmers receive payment notifications via SMS, can track historical prices through a mobile app, and access veterinary services through tele-consultation. This isn't just digitization for efficiency—it's about creating switching costs and deepening farmer loyalty.

The company's recent acquisitions demonstrate strategic intent. The OSAM acquisition in July 2025 expanded processing capabilities, while earlier acquisitions like Krishna Milks in 2022 provided instant access to established procurement networks in new geographies. These aren't just capacity additions—they're strategic moves to quickly establish presence in markets where building from scratch would take years.

Financial performance has validated the expansion strategy. Revenue reached ₹3,815 crores with profit of ₹258 crores, reflecting robust operational efficiency. More impressively, the company has delivered profit growth of 38.7% CAGR over the last five years while remaining almost debt-free—a rarity in capital-intensive businesses.

The African operations have quietly become a growth engine. The Uganda facility now serves not just local markets but exports to Kenya and Rwanda. Plans are underway for expansion into Tanzania and Ethiopia, leveraging the same farmer-centric model that worked in India. The "Pride of Cows" premium brand in Africa commands prices 40% higher than local competitors, proving that quality and brand building work even in price-sensitive emerging markets.

Innovation has moved beyond products to business models. Dodla Retail Parlours—company-owned outlets offering the full product range—have emerged as a high-margin channel. These parlours serve as brand ambassadors, quality showcases, and data collection points for consumer preferences. With 626 parlours and growing, this could become a significant revenue driver.

The competitive landscape remains intense. Heritage Foods and Hatsun Agro continue to be formidable regional competitors, while cooperatives like Amul expand aggressively into South India. New-age D2C brands targeting premium urban consumers add another layer of competition. Yet Dodla's integrated model—controlling the entire value chain from farm to consumer—provides a moat that's difficult to replicate.

VIII. The Business Model Playbook

At its core, Dodla's business model is deceptively simple: buy milk from farmers, process it, and sell to consumers. But the execution reveals layers of sophistication that explain why this model has generated superior returns in a commodity business.

The farmer-first procurement strategy remains the cornerstone. Daily payments aren't just a financial arrangement—they're a trust-building mechanism. When a farmer delivers milk at 5 AM and receives payment before 6 AM, it creates a psychological bond stronger than any contract. This immediacy of payment, revolutionary when introduced in 1997, remains rare even today among private dairies.

The veterinary services component adds another dimension. Dodla employs over 200 veterinarians who provide free consultation to farmer suppliers. This isn't charity—healthier cattle produce more milk of better quality. By helping farmers improve cattle health, Dodla increases its raw material supply while reducing quality variability. The company has helped more than 2,300 farmers secure financing to invest in their production capabilities, creating a virtuous cycle of productivity improvement.

The hub-and-spoke distribution model optimizes for freshness rather than efficiency. Unlike competitors who centralize processing to capture economies of scale, Dodla operates 11 smaller plants closer to procurement centers. This reduces transportation time for raw milk, preserving quality and reducing spoilage. Products reach consumers faster, allowing Dodla to command premium pricing for freshness.

Quality control borders on obsession. Every batch of milk undergoes 23 different tests before processing. Farmers caught adulterating face immediate blacklisting—harsh but necessary in building consumer trust. This uncompromising stance on quality has allowed Dodla to build brand equity in a category where consumers traditionally showed low brand loyalty.

The dual-brand strategy—value-focused Dodla and premium KC+—allows the company to capture different market segments without dilution. While Dodla competes on price and availability in mass markets, KC+ targets affluent consumers willing to pay 20-30% premiums for organic, farm-fresh products. This segmentation extends to channels, with Dodla dominating traditional retail while KC+ focuses on modern trade and e-commerce.

Capital efficiency deserves special attention. While the dairy business requires significant fixed assets (plants, chilling centers, vehicles), Dodla has optimized capital deployment through several strategies. First, they lease rather than own milk collection vehicles, converting fixed costs to variable. Second, they partner with local entrepreneurs for last-mile distribution, avoiding investment in retail infrastructure. Third, they've mastered working capital management—collecting cash from consumers before paying suppliers in many channels.

The social impact dimension isn't corporate window dressing—it's integral to business sustainability. By working with regional banks to facilitate farmer loans, providing veterinary services, and ensuring predictable income through daily payments, Dodla creates economic stability in rural communities. This translates to supplier loyalty, reduced procurement costs, and protection against competitive poaching.

Technology adoption has been pragmatic rather than flashy. While tech startups burn capital on consumer apps, Dodla focused on backend digitization. Real-time quality testing data, automated payment processing, route optimization algorithms—unsexy but impactful technologies that improve margins basis point by basis point.

The franchise model for Dodla Retail Parlours represents evolved thinking. Rather than company-owned stores requiring capital and generating modest returns, new parlours operate on a franchise model. Entrepreneurs invest capital while Dodla provides brand, products, and operating playbooks. This asset-light expansion allows rapid scaling without diluting return on capital.

Product mix optimization showcases operational sophistication. Liquid milk, while generating 73% of revenue, offers thin margins. Value-added products like ghee, paneer, and ice cream generate 27% of revenue but contribute disproportionately to profits. The company continuously rebalances this mix, pushing value-added products through premium channels while maintaining liquid milk volumes for procurement stability.

The payment terms structure reveals financial acumen. While farmers receive daily payments, institutional customers (hotels, restaurants, corporate cafeterias) operate on 15-30 day credit terms. Retail sales are predominantly cash. This creates negative working capital in certain channels—using customer money to fund operations, a hallmark of efficient businesses.

Risk management extends beyond financial hedging. Geographic diversification across states protects against regional disruptions (droughts, floods, political instability). Product diversification beyond liquid milk provides stability during demand fluctuations. The Uganda operations offer currency diversification and exposure to faster-growing markets.

The margin architecture tells the efficiency story. While gross margins remain constrained by raw material costs (milk comprises 80% of costs), Dodla has systematically improved EBITDA margins from 5% in 2010 to over 10% through operational leverage, product mix improvement, and cost optimization. In a commodity business, every basis point matters.

IX. Financial Analysis & Unit Economics

The financial architecture of Dodla Dairy reveals how a commodity business can generate exceptional returns through operational excellence and strategic capital allocation. With revenue of ₹3,815 crores and profit of ₹258 crores, the company has demonstrated that dairy can be more than just a low-margin commodity play.

The revenue breakdown tells a strategic story: 73% from milk sales and 27% from value-added products. While this might seem skewed toward the commodity end, it's actually an optimal balance. Milk sales provide volume and procurement stability—farmers need daily offtake for their entire production. Value-added products, while smaller in revenue contribution, generate disproportionate profits with EBITDA margins often exceeding 15% compared to 5-7% for liquid milk.

The margin evolution has been remarkable. From EBITDA margins of 5.2% in FY2015, the company reached 10.2% in FY2021, before stabilizing around 9-10% post-IPO. This 500 basis point improvement came not from pricing power—milk prices are largely market-determined—but from operational efficiency, product mix optimization, and scale benefits.

Working capital management deserves special attention. In a business handling perishable commodities with daily procurement and sales, working capital can make or break profitability. Dodla operates with negative working capital in many segments—collecting cash from retail customers while paying farmers on standard terms. The cash conversion cycle has improved from 18 days in 2018 to 11 days in 2024, freeing up capital for growth investments.

The company has delivered profit growth of 38.7% CAGR over the last five years—exceptional in a mature industry growing at 10-12%. This outperformance comes from three sources: market share gains from unorganized players, geographic expansion into new states, and premiumization through value-added products and branded retail.

Return on equity (ROE) consistently exceeds 20%, remarkable for an asset-heavy business. Return on capital employed (ROCE) of 24% compares favorably with FMCG companies despite lower margins, demonstrating superior capital efficiency. This efficiency comes from sweating assets harder—running plants at 85%+ utilization, optimizing route density, and minimizing inventory holding.

The company is almost debt-free, with debt-to-equity ratio near zero. This conservative capital structure might seem suboptimal from a financial engineering perspective, but it provides strategic flexibility. In a business vulnerable to commodity price swings, weather disruptions, and regulatory changes, a strong balance sheet is a competitive advantage.

Capital allocation has been disciplined. Over the past five years, the company has invested ₹400 crores in capacity expansion while maintaining dividend payouts of 20-25% of profits. The remaining retained earnings strengthen the balance sheet, providing dry powder for opportunistic acquisitions. The recent Maharashtra land acquisition and OSAM acquisition demonstrate this patient capital approach bearing fruit.

Unit economics at the farmer level reveal the model's sustainability. A typical farmer with 5 cattle generates ₹500-700 daily revenue selling 20-25 liters to Dodla. With immediate payment, zero transportation cost (Dodla handles collection), and free veterinary services, the farmer's effective realization improves by 10-15% compared to traditional buyers. This economic advantage creates stickiness beyond just relationship loyalty.

At the retail level, unit economics are equally attractive. A typical Dodla Retail Parlour generates ₹50,000-70,000 monthly revenue with 15-18% EBITDA margins. With minimal capital investment (₹5-7 lakhs) and working capital support from Dodla, franchisees achieve payback in 18-24 months. This attractive return profile drives parlour expansion without corporate capital.

The procurement cost structure provides competitive advantage. While milk costs are market-determined, Dodla's procurement expenses (transportation, testing, chilling) are 8-10% lower than industry average due to route density, scale benefits, and farmer proximity to collection centers. In a business where raw material is 80% of costs, this efficiency translates directly to bottom line.

Seasonality management showcases financial sophistication. Milk production peaks during winter (October-March) when fodder is abundant, creating procurement surplus. Rather than refusing milk and losing farmer loyalty, Dodla converts excess into milk powder, which can be stored and reconstituted during lean summer months. This inventory management smooths earnings volatility while maintaining supplier relationships.

The cost discipline extends to seemingly minor items. Distribution costs at 4.2% of revenue are 80 basis points lower than industry average through route optimization and backhauling (using return trips to transport packaging material). Marketing spend at 1.8% of revenue is half the industry norm, relying on word-of-mouth and product quality rather than celebrity endorsements.

Geographic revenue concentration has reduced significantly. From 65% revenue concentration in Andhra Pradesh and Telangana in 2015, the home markets now contribute 45%, with Karnataka (20%), Tamil Nadu (18%), Maharashtra (10%), and others (7%) providing diversification. This reduces regulatory risk and provides multiple growth engines.

The Africa operations contribute 8% of revenue but 12% of EBITDA, demonstrating superior margins in less competitive markets. With local currency revenue naturally hedged against local costs, currency risk is minimal. The Uganda operation's 15% EBITDA margins validate the model's international portability.

Comparative analysis with peers reveals Dodla's financial edge. While Heritage Foods generates similar revenue, Dodla's EBITDA is 40% higher. Compared to Hatsun Agro, Dodla achieves similar margins with half the marketing spend. Against cooperatives like Amul, Dodla's ROCE is triple despite lacking procurement advantages.

X. Competition & Industry Dynamics

The Indian dairy industry presents a fascinating paradox: it's simultaneously the world's largest producer and one of the most fragmented markets. With organized players controlling just 25-30% of the market, the competitive dynamics are unlike any other consumer category. Understanding Dodla's position requires examining multiple competitive vectors.

The cooperative behemoths—Amul, Mother Dairy, and state cooperatives—remain the most formidable competitors. Amul alone processes 30 million liters daily, thirty times Dodla's volume. These cooperatives enjoy structural advantages: government support, farmer ownership ensuring captive procurement, and massive distribution networks built over decades. Yet they also carry baggage—bureaucratic decision-making, political interference, and limited ability to premiumize.

Dodla's strategy against cooperatives is surgical rather than frontal. Instead of competing on price in commodity milk, Dodla focuses on service differentiation—doorstep delivery, consistent quality, and product freshness. In value-added categories where cooperatives are weak (premium ice cream, flavored milk, fresh paneer), Dodla aggressively captures share.

Regional private players present a different challenge. Heritage Foods, founded by Andhra Pradesh's former Chief Minister Chandrababu Naidu's family, leverages political connections and local relationships. Hatsun Agro, dominant in Tamil Nadu, has built formidable procurement and distribution infrastructure. These players understand local preferences, have established brands, and enjoy home-market advantages.

Against regional competitors, Dodla employs a multi-state strategy. While Heritage focuses on Andhra Pradesh and Hatsun on Tamil Nadu, Dodla's presence across five states provides diversification and scale benefits. When Heritage faces procurement challenges in drought-hit Andhra, Dodla can source from Karnataka. When Hatsun deals with political turmoil in Tamil Nadu, Dodla's Telangana operations remain stable.

The unorganized sector—local milkmen, small dairies, and direct farmer-to-consumer sales—still controls 70% of the market. This might seem like opportunity, but it's also a competitive threat. Unorganized players operate with minimal costs, zero tax compliance, and often questionable quality standards. They offer credit to customers, customize quantity, and provide perceived freshness.

Dodla's approach to competing with unorganized players focuses on trust and convenience. Quality testing results displayed at collection centers, transparent pricing, and branded packaging address trust issues. Home delivery, standardized packaging, and consistent availability address convenience. The company doesn't try to match the credit terms or price flexibility of local milkmen but instead targets consumers graduating to organized dairy.

New-age D2C brands represent an emerging threat. Companies like Country Delight, Milkbasket, and DailyNinja target urban premium consumers with subscription models, organic variants, and tech-enabled convenience. Backed by venture capital, these players can afford customer acquisition costs that would cripple traditional dairies.

Dodla's response has been measured rather than reactive. Instead of launching a competing app or subscription service, the company leverages its Dodla Retail Parlours for premium positioning. The KC+ brand competes in the premium segment without the cash burn of D2C models. Partnerships with e-commerce platforms provide digital presence without massive technology investments.

Plant-based alternatives, while still nascent in India, represent a long-term threat. Companies like Oatly, Sofit, and local startups are targeting health-conscious urban consumers with dairy alternatives. While currently less than 1% of the market, growing lactose intolerance awareness and vegan trends could accelerate adoption.

Dodla's strategy here is pragmatic—monitor but don't overreact. The company's R&D team experiments with plant-based products but hasn't launched commercially. The view is that India's protein-deficient diet and cultural attachment to dairy provide a deep moat against rapid substitution. However, the company remains prepared to pivot if consumer preferences shift materially.

The competitive dynamics vary significantly by geography. In urban markets, competition centers on convenience, variety, and brand. In rural markets, it's about procurement relationships, payment terms, and collection infrastructure. In institutional sales, price and reliable supply matter most. Dodla's multi-brand, multi-channel strategy allows tailored competition in each segment.

Technology is reshaping competitive dynamics. While Dodla invested in backend digitization, competitors like Amul are launching consumer apps. Heritage Foods experiments with IoT-enabled quality monitoring. Hatsun uses AI for demand forecasting. The technology arms race requires careful capital allocation—investing enough to stay competitive without chasing every trend.

Consolidation is accelerating. Lactalis's acquisition of Tirumala, Groupe Danone's entry through investment in Epigamia, and TPG's investment in Dodla signal increasing institutional interest. Smaller regional players lacking scale or capital face existential pressure. Dodla's strong balance sheet and proven acquisition integration capability position it as a consolidator rather than target.

The regulatory environment adds complexity. State governments often favor cooperatives through subsidies, preferential procurement for welfare schemes, and regulatory forbearance. Food safety regulations are tightening, increasing compliance costs that disproportionately impact smaller players. GST implementation has formalized the supply chain, benefiting organized players like Dodla.

Price controls remain a perpetual risk. State governments occasionally impose price caps on liquid milk, treating it as an essential commodity. While these controls typically exempt branded packaged milk, they influence overall market pricing. Dodla's value-added product portfolio provides some insulation, but regulatory intervention remains an industry overhang.

XI. Bull & Bear Case

Bull Case: The Organized Dairy Revolution

The bull case for Dodla rests on powerful structural trends that could drive multi-decade growth. India's per capita milk consumption at 400 grams per day remains 40% below WHO recommendations, suggesting significant volume growth potential. As incomes rise, protein consumption increases disproportionately, with dairy being the most affordable and culturally acceptable source.

The shift from unorganized to organized dairy is perhaps the most compelling driver. With organized players controlling just 25-30% of the market versus 90%+ in developed countries, the runway for share gains is enormous. Every 1% market share shift from unorganized to organized represents ₹1,800 crores in addressable market. Food safety concerns, urbanization, and modern retail expansion accelerate this shift.

Dodla's entrenched procurement network provides a formidable moat. Relationships with 250,000 farmers built over 25 years cannot be replicated quickly. New entrants would need to offer 10-15% price premiums to poach suppliers, making customer acquisition uneconomical. This procurement moat becomes more valuable as competition for milk supply intensifies.

The company's debt-free balance sheet provides strategic flexibility rare in capital-intensive industries. While competitors struggle with leverage, Dodla can pursue opportunistic acquisitions, invest countercyclically during downturns, and expand aggressively without dilution. In a fragmented industry ripe for consolidation, strong balance sheets determine winners.

Geographic expansion opportunities remain vast. Dodla has negligible presence in North and East India, markets larger than its current Southern base. The Maharashtra entry demonstrates the model's portability. With proven playbook and execution capability, systematic geographic expansion could double addressable market.

International expansion offers another growth vector. The Africa operations validate the model's international viability. Similar markets—Bangladesh, Sri Lanka, Nepal—offer comparable dynamics of fragmented supply, growing demand, and minimal organized competition. Dodla's experience operating in challenging environments positions it well for emerging market expansion.

The premiumization opportunity is underappreciated. As consumers become health-conscious, demand for organic, A2, lactose-free, and fortified variants grows exponentially. These products command 50-100% price premiums with superior margins. Dodla's KC+ brand and R&D capabilities position it to capture this value migration.

Technology adoption could drive step-change in margins. IoT-enabled supply chain monitoring, AI-driven demand forecasting, and automated quality testing could reduce costs by 200-300 basis points. Digital marketing and D2C channels could reduce customer acquisition costs while improving margins. Dodla's pragmatic approach to technology suggests selective high-ROI adoption.

The institutional framework is improving. GST implementation has formalized the industry, disadvantaging tax-evading unorganized players. Food safety regulations are tightening, raising compliance costs that favor scaled players. Infrastructure development (roads, cold chain, power) reduces operational challenges. These structural improvements disproportionately benefit organized players like Dodla.

Climate change, paradoxically, might strengthen Dodla's position. As weather volatility increases, farmers need stable buyers who can support them through disruptions. Dodla's financial strength and farmer support programs become more valuable during climate stress. Competitors lacking similar resilience might exit, reducing competition.

Bear Case: Commodity Trap and Structural Challenges

The bear case begins with the fundamental challenge of commodity economics. Milk is undifferentiated—consumers show limited brand loyalty and switch based on price and availability. Without pricing power, margins remain perpetually compressed. As competition intensifies, the race to the bottom in pricing could erode profitability.

Climate change poses existential risks that bulls underestimate. Rising temperatures reduce cattle productivity while increasing disease incidence. Fodder costs spike during droughts, squeezing farmer economics and milk supply. Extreme weather events disrupt collection and distribution infrastructure. These climate impacts are accelerating, not moderating.

Competition from both ends squeezes returns. Cooperatives with government support and farmer loyalty aren't yielding share despite organized retail growth. New-age brands backed by venture capital are willing to lose money for years to acquire customers. Chinese agri-giants entering India could transform competitive dynamics overnight.

Execution risk in new geographies is significant. Dodla's success in South India doesn't guarantee replication elsewhere. North Indian consumers have different preferences, entrenched local brands exist, and procurement dynamics differ. The Maharashtra expansion, while promising, remains unproven. Geographic expansion might dilute returns rather than accelerate growth.

The regulatory overhang remains severe. State governments view milk as political commodity, intervening through price controls, procurement mandates, and subsidy programs. One populist decision—free milk distribution, price caps, or cooperative preferences—could devastate private player economics. This regulatory risk is unhedgeable and unpredictable.

Margin pressure from input inflation is structural, not cyclical. Fodder costs are rising faster than milk prices as agricultural land shrinks. Labor costs in rural areas are increasing with MNREGA and urban migration. Transportation costs spike with fuel prices. These input pressures are permanent, not temporary.

Technology disruption from unexpected quarters could blindside traditional players. Lab-grown milk, precision fermentation, and plant-based alternatives might reach price parity sooner than expected. A breakthrough making alternative proteins taste identical to dairy at lower cost would devastate the industry. Dodla's limited R&D investment in alternatives leaves it vulnerable.

The farmer economics are deteriorating. Small-holder farming with 2-3 cattle is becoming unviable as input costs rise faster than milk prices. Farm consolidation might seem positive, but it actually reduces Dodla's bargaining power—larger farms have options and negotiating leverage. The procurement advantage might erode as farm structures evolve.

Capital allocation disappointments could destroy value. The Africa operations, while profitable, tie up capital in volatile markets with currency risk. Acquisitions might bring integration challenges and cultural conflicts. The Maharashtra expansion requires significant investment with uncertain returns. Management's limited experience with large-scale M&A increases execution risk.

Market saturation in core territories limits growth. South India, Dodla's stronghold, is approaching organized dairy penetration levels seen in developed markets. Further share gains require taking from established competitors rather than unorganized players—a much harder battle. Without new geographies, growth could decelerate sharply.

The generational consumption shift poses long-term risk. Younger consumers show less attachment to traditional dairy, experimenting with alternatives and reducing consumption. The protein source diversification—from dairy monopoly to eggs, meat, and plants—erodes dairy's centrality in Indian diet. This slow but steady shift could cap long-term growth.

ESG pressures are intensifying globally and will reach India. Dairy's environmental footprint—methane emissions, water usage, land degradation—faces increasing scrutiny. Carbon taxes, emission regulations, and consumer boycotts could materially impact economics. Dodla's limited ESG initiatives leave it vulnerable to regulatory and reputational risks.

XII. Lessons & Takeaways

The Dodla Dairy journey offers profound lessons that extend beyond the dairy industry into fundamental principles of building enduring businesses in emerging markets.

Building trust-based supply chains in rural markets emerges as perhaps the most critical lesson. Dodla's success wasn't built on technology or capital but on thousands of daily interactions with farmers. The decision to pay daily, even when it strained working capital, created trust that no contract could replicate. This trust, accumulated over decades, becomes an unassailable moat. The lesson extends beyond dairy—any business dependent on rural supply chains must prioritize relationship capital over financial capital.

The power of patient, strategic capital is demonstrated through the TPG Rise Fund partnership. Unlike typical private equity seeking quick exits through financial engineering, TPG provided patient capital focused on operational improvement and social impact. The spectacular returns—8x in four years—prove that impact investing isn't about accepting lower returns but finding businesses where social and financial objectives align. For entrepreneurs, the lesson is clear: choose investors who understand your business model's time horizon.

Family businesses and professional management balance showcases a delicate dance few master successfully. The Dodla family retained majority control while bringing professional management and institutional governance. They avoided both extremes—neither clinging to outdated family practices nor completely ceding control to professionals. This balance allowed continuity of vision while embracing modern management practices. The successful IPO with continued family ownership demonstrates that professionalization doesn't require abandoning family control.

Social impact as business strategy, not CSR revolutionizes traditional thinking about corporate responsibility. Dodla's farmer support programs—veterinary services, financing facilitation, daily payments—aren't charitable activities but core business strategy. By improving farmer economics, Dodla ensures supply security and quality improvement. This integration of social impact into business model rather than treating it as cost center creates sustainable competitive advantage.

Timing public markets and managing stakeholder transitions reveals sophisticated financial thinking. Going public during COVID recovery when markets were hungry for quality assets, TPG's clean exit at IPO avoiding overhang, and maintaining family control while achieving liquidity—each decision reflects careful stakeholder management. The lesson: IPO isn't just about raising capital but orchestrating multiple stakeholder objectives simultaneously.

The importance of operational excellence in commodity businesses cannot be overstated. Without product differentiation or pricing power, success comes from relentless focus on operational efficiency. Dodla's margin expansion from 5% to 10% came from hundreds of small improvements—route optimization, capacity utilization, working capital management. In commoditized industries, competitive advantage comes from executing basics better than competitors, not from revolutionary strategies.

Geographic diversification versus focus presents an ongoing tension. Dodla's multi-state presence provided resilience during regional disruptions while maintaining enough focus to achieve local scale. The company avoided both extremes—neither remaining confined to one state nor spreading too thin across India. This calibrated expansion, testing and perfecting the model before scaling, offers lessons for regional businesses contemplating national expansion.

Building brands in commoditized categories seems oxymoronic yet essential. Dodla proved that even in milk—the ultimate commodity—brand building is possible through consistency, quality, and service. The dual-brand strategy (value Dodla and premium KC+) shows that commoditized categories can support portfolio strategies typically associated with differentiated products.

The value of boring businesses in an era obsessed with disruption deserves emphasis. While investors chase food-tech startups, Dodla quietly built a ₹7,879 crore business doing something humans have done for millennia—collecting and distributing milk. The lesson: solving real problems for real people with proven models often creates more value than disrupting industries that don't need disrupting.

Technology as enabler, not strategy provides crucial perspective in our tech-obsessed era. Dodla's pragmatic approach—digitizing backend operations while avoiding flashy consumer tech—generated superior returns. The company proved that technology should enhance existing competitive advantages, not create new ones. In traditional industries, the highest ROI often comes from unsexy operational technology rather than customer-facing innovation.

Capital allocation in capital-intensive businesses requires different thinking than asset-light models. Dodla's decision to remain debt-free despite operating in capital-intensive industry seemed suboptimal but provided strategic flexibility during crises. The careful balance between growth investment, shareholder returns, and balance sheet strength offers lessons for businesses that can't scale with just working capital.

Managing stakeholder complexity in businesses touching millions of lives requires delicate balance. Farmers wanting higher prices, consumers demanding lower prices, investors seeking returns, regulators imposing restrictions, communities expecting support—Dodla navigated these competing demands without alienating any stakeholder. The lesson: sustainable businesses create value for all stakeholders, not just shareholders.

The importance of execution over strategy emerges clearly. Dodla's strategy—buy milk from farmers, process it, sell to consumers—isn't revolutionary. Success came from executing this simple strategy better than competitors for 25 years. In most industries, competitive advantage comes from superior execution of obvious strategies rather than brilliant strategies poorly executed.

Building resilience over efficiency challenges conventional wisdom. Dodla's distributed plant network, daily payment system, and conservative balance sheet seemed inefficient but provided resilience during disruptions. The COVID pandemic, natural disasters, and economic volatility validated this approach. The lesson: optimize for survival first, efficiency second.

Creating shared value in supply chains demonstrates sustainable business model innovation. By helping farmers improve productivity, access credit, and achieve stable incomes, Dodla created value that it partially captured through stable procurement and quality improvement. This shared value creation, where supplier success drives company success, offers a template for inclusive growth.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube