MapMyIndia: Building India's Digital Atlas

I. Introduction & Hook

Picture this: It's 1995 in New Delhi. The internet won't become publicly available in India for another few months. Google doesn't exist. GPS devices are military-grade equipment costing thousands of dollars. And two engineers—a husband-wife duo who'd given up comfortable careers in America—are walking the chaotic streets of Indian cities with handheld GPS units, manually plotting every turn, every landmark, every nameless alley.

This is the origin story of MapMyIndia, the company that built India's digital mapping infrastructure before anyone believed it was possible—or even necessary.

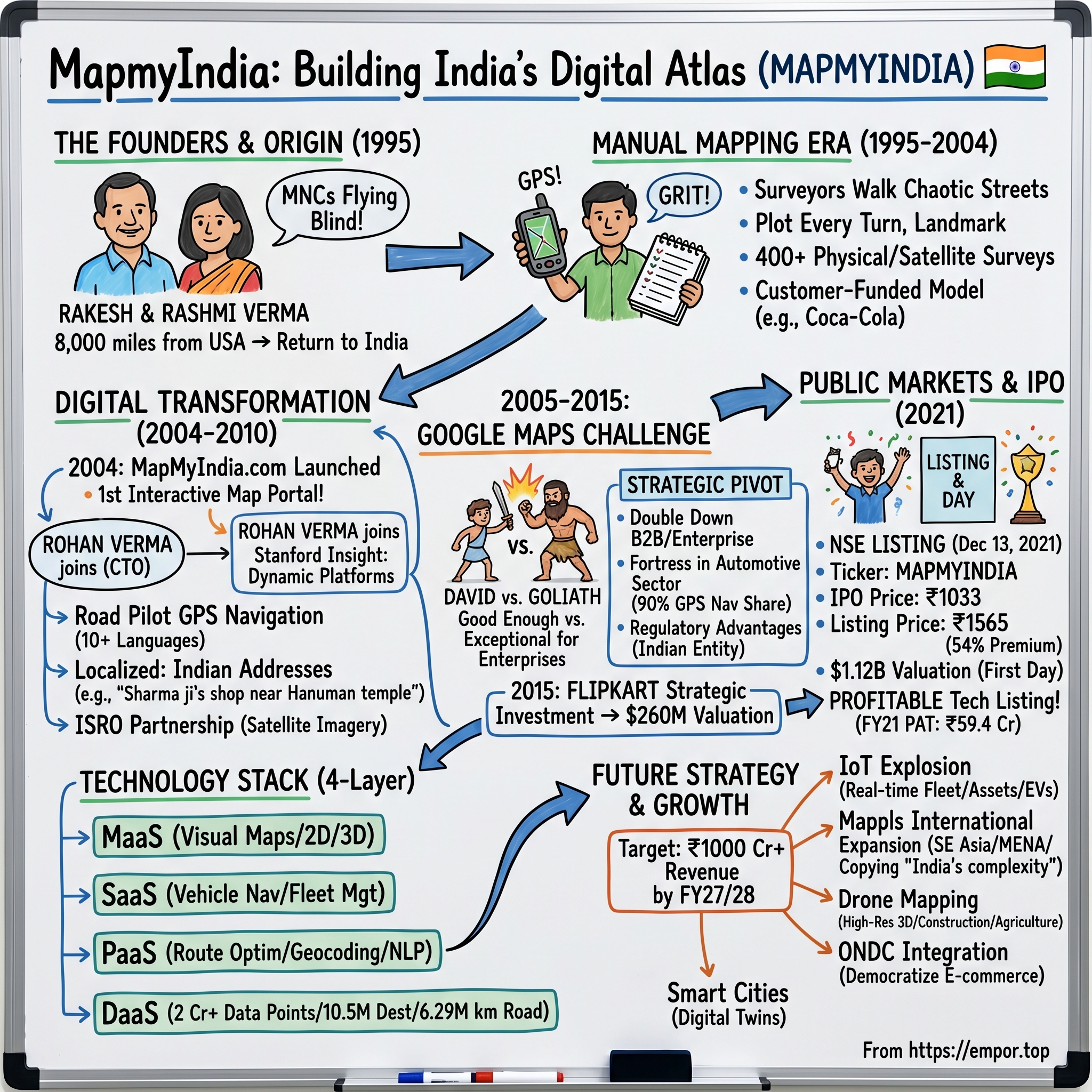

When Rakesh and Rashmi Verma founded CE Info Systems in 1995, the conventional wisdom was clear: mapping India digitally was impossible. The country sprawled across 3.2 million square kilometers, contained over 600,000 villages, and lacked any existing digital infrastructure. Roads changed daily. Addresses were suggestions at best. Even the Indian government's Survey of India maps were decades old, classified as sensitive, and legally restricted.

Yet on December 13, 2021, their company hit the public markets with a bang—listing at a 54% premium and achieving a $1.12 billion valuation on its first day of trading. The stock soared from its IPO price of ₹1,033 to ₹1,565, as investors scrambled to own a piece of India's answer to Google Maps.

But this isn't just another IPO success story. It's a three-decade saga of building when no one was watching, competing when everyone said you'd lose, and creating a moat so deep that even Google—with its infinite resources and billion-plus users—hasn't been able to cross it in certain segments of the Indian market.

MapMyIndia today powers the navigation systems in 90% of cars sold in India with built-in GPS. Its maps guide deliveries for Amazon, enable transactions for PhonePe and Paytm, and yes—even provide the India mapping data for Apple Maps. The company claims over 5,000 enterprise customers and has mapped 10.54 million unique destinations across the subcontinent.

How did two engineers build what venture capitalists wouldn't fund, create what Silicon Valley said was impossible, and defend what Big Tech couldn't commoditize? The answer lies in understanding not just technology or business models, but the peculiar dynamics of building digital infrastructure in an analog nation—and the power of being irrationally committed to a market everyone else ignores until it's too late.

II. The Founders & Origin Story

The MapMyIndia story begins not in India, but 8,000 miles away in the Pacific Northwest of the United States, where two Indian engineers were living the American dream—and preparing to abandon it.

Rakesh Verma had followed the classic IIT-to-America pipeline, though with a twist. After graduating from BITS Pilani with a mechanical engineering degree in 1972, he'd pursued an MBA at Eastern Washington University, completing it in 1979. For the next decade, he worked in corporate America, including a significant stint at EDS, the technology services giant that Ross Perot had built and sold to General Motors. At EDS, Rakesh witnessed firsthand how technology could transform traditional industries—lessons that would prove invaluable decades later.

His wife Rashmi had an even more impressive pedigree. An IIT Roorkee chemical engineering graduate with distinction from the class of 1977, she'd also earned her Master's from Eastern Washington University in 1979. By 1989, she was deep into a successful career at IBM Corporation, working on enterprise systems at a time when Big Blue still dominated global technology.

The couple had everything immigrant engineers dream of: stable careers, good salaries, green cards, a house in the suburbs. Their children could grow up American. Yet in 1989, at the peak of their careers, they made a decision that baffled their peers: they would return to India.

"Everyone thought we were crazy," Rashmi would later recall. India in 1989 was pre-liberalization, pre-internet, pre-everything. The economy was still closed. Getting a phone line took years. Starting a business meant navigating Byzantine regulations. Why leave Silicon Valley for this?

The answer lay in what they saw that others didn't. Rakesh had noticed something during his trips back to India: multinational corporations trying to enter the Indian market were flying blind. They had no maps, no data, no way to understand the geography of their own operations. Coca-Cola executives couldn't figure out optimal distribution routes. Cellular companies couldn't plan tower locations. Real estate developers couldn't assess catchment areas. The breakthrough came with their first major client. In 1993, after being un-banned in India, Coca-Cola acquired the Indian cola company Thumbs Up and found itself with a problem unfamiliar to companies accustomed to developed markets: very few accurate maps existed at that point. Thumbs Up had a vast network of bottlers, each with an assigned distribution territory, but nothing depicted the overlapping of boundaries of the territories (descriptions such as "along the river" substituted for maps).

This was exactly the opportunity the Vermas had been waiting for. They approached Coca-Cola, Cellular One, and other companies and obtained contracts to create digital maps that contained information that could aid these respective companies with business (bottlers' territories) or topographic features (high ground suitable for cell towers).

The genius of their business model emerged early. They received advance payments from the companies, which enabled them to make high-quality maps that they could later modify and sell to other clients, including the Indian Defense Department. Build once, sell many times—but with a twist. Each client's needs would enhance the master database, creating a virtuous cycle of data enrichment.

By 1995, when they formally incorporated CE Info Systems, the Vermas had cracked the code: India didn't need consumer mapping services (yet). It needed enterprise-grade geographical intelligence. And they would be the ones to build it, one GPS coordinate at a time.

Their son Rohan, then studying engineering at Stanford, would occasionally hear about his parents' venture during phone calls home. "My parents were literally walking the streets of Delhi with GPS devices," he'd later recall. "Most of my Stanford classmates were building dot-coms. My parents were building atoms—real, physical data about India that no one else had."

The stage was set for one of the most audacious infrastructure plays in Indian tech history. But first, they'd have to survive the manual mapping era—a period that would test not just their technology, but their sheer physical endurance.

III. The Manual Mapping Era (1995–2004)

If you wanted to understand true entrepreneurial grit, you'd need to shadow a MapMyIndia surveyor in 1997. Picture this: It's 42 degrees Celsius in Delhi's Karol Bagh market. The surveyor carries a Trimble GPS unit—a brick-sized device that cost more than most Indians' annual salary. He's been walking for six hours, meticulously recording every shop, every turn, every landmark. His notebook is filled with hand-drawn sketches annotating what the GPS can't capture: "Sharma Sweets next to blue gate," "Turn left after large peepal tree," "Road narrows near temple."

This was MapMyIndia's reality for nearly a decade. No Google Street View cars. No satellite imagery detailed enough to distinguish buildings. No crowdsourced data from millions of smartphones. Just humans with GPS devices, notebooks, and an almost irrational commitment to documenting every corner of India.

The company built a team of more than 400 surveyors for physical and satellite surveys, creating what was essentially a human neural network spread across the country. Each surveyor was trained not just in GPS technology but in the art of Indian geography—understanding that addresses like "opposite Gandhi statue, near old bus stand" were more reliable than official street numbers that often didn't exist or weren't used.

The economics of this operation were brutal. A single city like Bangalore took months to map comprehensively. The cost of surveying ran into lakhs of rupees per square kilometer when factoring in equipment, salaries, and verification. Traditional venture capital math would have killed this business model instantly. But the Vermas weren't playing by Silicon Valley rules.

All this via a customer-funded business model. Instead of raising venture capital and burning cash to build maps on speculation, they used advance payments from enterprise clients to fund their expansion. Each new client—whether Coca-Cola needing distribution mapping or a telecom company planning tower locations—would essentially finance the mapping of new territories.

The technical challenges were equally daunting. GPS accuracy in the late 1990s was nowhere near today's standards. The US military's Selective Availability program intentionally degraded civilian GPS signals until 2000, meaning position errors could be 100 meters or more. MapMyIndia's surveyors had to use differential GPS techniques and multiple readings to achieve acceptable accuracy—a time-consuming process that made each day's progress painfully slow.

But perhaps the biggest challenge was credibility. In boardrooms across India, executives would ask: "Why do we need digital maps? We've operated for decades with paper maps and local knowledge." The Vermas had to evangelize not just their product but the entire concept of location intelligence.

Their journey began with Coca Cola coming onboard as an enterprise customer. Later on, they counted players like Marico, Hindustan Unilever, and the Indian Defence services as their enterprise customers. The number of enterprise customers for MapmyIndia grew to 500 by the early 2000s.

Each client brought unique challenges that expanded MapMyIndia's capabilities. Hindustan Unilever needed to understand rural distribution networks where roads appeared and disappeared with monsoons. The Indian Defence services required topographical precision that consumer applications would never need. Marico wanted to optimize their supply chain in markets where street vendors outnumbered formal retail outlets.

1998 saw satellite imagery becoming available in the country. This led to a lot of productivity enhancement for the company. Collecting data became way easier and the entire process was accelerated heaps. But even with satellite imagery, human verification remained essential. India's cities grew so rapidly that satellite images were often outdated by the time they were processed. New flyovers, relocated markets, renamed streets—only ground-truth surveying could capture this dynamism.

The company developed a sophisticated data architecture during this period. Every point of interest was tagged with multiple attributes: GPS coordinates, address descriptions, landmark relationships, business categories, operating hours, and even informal local names. This rich metadata would prove invaluable when they eventually built their digital platform.

By 2004, MapMyIndia had achieved something remarkable: they'd built the most comprehensive geographic database of India without raising institutional capital, without government support, and without the technology tools that would later make such efforts trivial. The company now had a repository of more than 2 Cr data points, including 3D data visualisations, telematics, and navigation systems under its belt.

But the manual era was ending. The internet was finally gaining critical mass in India. GPS devices were becoming affordable. And a small search engine company called Google was beginning to eye the mapping space. MapMyIndia would need to transform from a data collection company to a technology platform—and fast.

IV. The Digital Transformation (2004–2010)

The company launched MapMyIndia's website in 2004 – claimed to be the first interactive mapping portal of India. Within months, as reported by the company, it was getting 5,000-6,000 unique visitors a day. The year also marked the entry of the prodigal son, Rohan Verma, a Stanford engineering graduate and presently the CTO of MapMyIndia. He built the portal where anybody could access these maps for free.

The timing of Rohan's return was no accident. The Stanford-trained engineer had been watching the emergence of MapQuest and early Google Maps in the US. He understood that the future of mapping wasn't in selling static data but in building dynamic, interactive platforms. "I did my preliminary research, and found that India had nothing like this," Rohan begins candidly in later interviews.

The technological leap from physical surveying to digital platform was staggering. MapMyIndia had to build everything from scratch: the server infrastructure to handle geographic queries, the algorithms to calculate routes through India's chaotic traffic patterns, the rendering engine to display maps at different zoom levels, and the search functionality to parse Indian addresses that followed no standard format.

Consider the complexity of Indian address search alone. A user might search for "Sharma ji's shop near Hanuman temple, opposite SBI bank, Lajpat Nagar." MapMyIndia's system had to understand that this wasn't a formal address but a series of landmark relationships—and still return accurate results. This required natural language processing capabilities that Google, with all its resources, would struggle to replicate for Indian conditions years later.

The launch of www.mapmyindia.com in 2004 marked a pivotal strategic moment. For the first time, the company was offering something for free—a radical departure from their enterprise-focused model. But this wasn't charity. It was a calculated move to build brand awareness and create a consumer feedback loop that would improve their data quality.

Every search, every route query, every user correction fed back into their master database. If multiple users searched for a location that didn't exist in their database, it flagged it for surveyor verification. If users consistently chose alternative routes, it suggested real-world traffic patterns their algorithms hadn't captured. The free consumer portal became, in essence, a massive quality assurance system.

By 2010, MapMyIndia made another leap with the launch of "Road Pilot," their GPS navigation service. This wasn't just another navigation device—it was navigation built specifically for Indian conditions. The system came preloaded with detailed maps of Indian cities and villages, offered voice guidance in 10+ Indian languages, and understood the peculiarities of Indian driving.

The localization went deep. Road Pilot could navigate through areas where roads had no names, where U-turns were prohibited but commonly taken, where landmarks mattered more than street numbers. It could distinguish between the "new bypass" and the "old bypass" that locals referred to, even when officially both had different names. The integration with ISRO's satellite imagery marked another technological leap. The services combined the power of MapMyIndia's digital maps and technologies with ISRO's catalogue of satellite imagery and earth observation data. This partnership gave MapMyIndia access to detailed satellite and hybrid maps that dramatically enhanced their offering. They could now offer aerial views, terrain data, and change detection capabilities that were previously available only to government agencies.

The company's four-layer service architecture began taking shape during this period: Maps as a Service (MaaS), Software as a Service (SaaS), Platform as a Service (PaaS), and Data as a Service (DaaS). Each layer served different customer needs while feeding off the same core geographic database. An automotive manufacturer might use their SaaS layer for in-dash navigation, while a logistics company might tap into their DaaS layer for route optimization.

By the end of this transformation period, MapMyIndia had evolved from a data collection company to a full-stack mapping platform. They weren't just digitizing India anymore—they were making it navigable, searchable, and analyzable. The foundation was set for the next phase of their journey, where they would face their greatest challenge yet: the arrival of Google Maps in India.

V. The Google Maps Challenge & Strategic Pivot (2005–2015)

2006: Google becomes popular in India; Rohan: "Most of my adult life has been spent seeing Google Maps do things after we have done and gain more visibility"—this candid admission from MapMyIndia's CTO captures the David versus Goliath dynamic that would define the company's next decade.

When Google Maps launched globally in 2005 and began gaining traction in India by 2006, the conventional wisdom was clear: MapMyIndia was finished. Google had infinite capital, the world's best engineers, and a brand that was becoming synonymous with the internet itself. Industry observers predicted MapMyIndia would be crushed within years, if not months.

But the Vermas saw something others missed. Google's strategy was to build a good-enough product for the masses—free, fast, and functional. MapMyIndia's opportunity lay in being exceptional for those who needed more than good enough. "They focused on being good enough so that you use them, we focused on being better, so that you pay us," became their internal mantra.

This strategic pivot wasn't just about positioning—it required fundamental changes to their business model. While Google chased consumer eyeballs to sell advertising, MapMyIndia doubled down on enterprise depth. They built features Google wouldn't: indoor mapping of corporate campuses, truck-specific routing that accounted for low bridges and weight restrictions, APIs that could handle millions of delivery optimization queries, and white-label solutions that let enterprises brand the maps as their own.

The automotive sector became their fortress. By 2015, MapMyIndia claimed to power navigation in 14 car manufacturers with 40 car models using built-in MapMyIndia navigation, claiming 90% market share in GPS navigation by car deals. This wasn't luck—it was the result of understanding that automotive OEMs had requirements Google couldn't or wouldn't meet.

Car manufacturers needed maps that worked offline (Indian highways had patchy data coverage), updated through proprietary channels (OEMs wanted control over the user experience), and integrated deeply with vehicle systems (turn-by-turn directions on the instrument cluster, speed limit warnings tied to cruise control). Google's one-size-fits-all approach couldn't accommodate these needs. MapMyIndia built custom solutions for each manufacturer.

The company also leveraged India's unique regulatory environment. The Survey of India's regulations around map data were complex and restrictive. Foreign companies faced limitations on the resolution of imagery they could use, the accuracy of border depictions, and access to certain sensitive locations. MapMyIndia, as an Indian company with relationships dating back to their Defense Department contracts, could navigate these restrictions more easily.A pivotal moment came in 2015 when Flipkart acquired a strategic minority stake in MapMyIndia. With Flipkart's investment, MapMyIndia's early financial investors, Nexus Venture Partners and Lightbox Ventures, would exit the company. Though the exact transaction value wasn't disclosed publicly, the deal valued MapMyIndia at about $260m, providing crucial validation and liquidity for early investors who had backed the company when digital mapping seemed like a quixotic pursuit.

The Flipkart partnership wasn't just about capital—it was strategic validation. India's largest e-commerce company choosing MapMyIndia over Google Maps for its logistics operations sent a powerful signal to the market. The deal would help Flipkart strengthen supply chain through technology as it would license map data and location technologies from MapMyIndia.

This period also saw MapMyIndia refine its narrative around competition with Google. Rather than positioning themselves as "India's Google Maps"—a comparison that invited unfavorable contrasts—they began emphasizing their role as India's geospatial data infrastructure. They weren't competing with Google; they were doing something Google couldn't or wouldn't do: building deep, India-specific location intelligence that went far beyond consumer navigation.

The company's resilience during this period offers crucial lessons about competing with platform giants. First, depth beats breadth in enterprise markets. Second, regulatory advantages matter more than most founders realize. Third, patient capital and a long-term view can outlast even the most aggressive competitors. And finally, sometimes the best response to disruption is to refuse to be disrupted—to stay focused on what you do best while others chase the next shiny object.

VI. Building the Technology Stack

By 2015, MapMyIndia had evolved far beyond its origins as a mapping company. The technology stack they'd built represented one of India's most sophisticated geospatial platforms—a four-layer architecture that would become the backbone of location services for thousands of enterprises.

At the foundation lay Data as a Service (DaaS)—the raw geographic intelligence that made everything else possible. 25 years of research, a team of more than 400 surveyors, post-physical and satellite surveys and the company now had a repository of more than 2 Cr data points, including 3D data visualisations, telematics, and navigation systems under its belt. This wasn't just points on a map; it was a living, breathing database that captured the constant evolution of Indian geography.

The numbers were staggering: 10.54 million unique destinations mapped, 6.29 million kilometers of road network documented, 7,068+ cities covered at street level, over 600,000 villages included, and 18+ million places catalogued. Each data point contained multiple layers of information—not just location, but context, relationships, and temporal patterns.

Above the data layer sat Platform as a Service (PaaS), where MapMyIndia's algorithms transformed raw geographic data into actionable intelligence. Route optimization engines that understood Indian traffic patterns. Geocoding services that could parse addresses written in Hindi, English, or Hinglish. Polygon mapping tools that let enterprises define custom service areas. The platform processed millions of queries daily, each one making the system smarter.

The Software as a Service (SaaS) layer packaged these capabilities into industry-specific solutions. For automotive manufacturers, it meant navigation systems that could be embedded directly into vehicle infotainment systems. For logistics companies, it meant fleet management dashboards that tracked thousands of vehicles in real-time. For government agencies, it meant urban planning tools that could model infrastructure changes before implementation.

At the top sat Maps as a Service (MaaS)—the visual layer that most users interacted with. But this wasn't just about pretty pictures. MapMyIndia's maps could render in 2D or 3D, show real-time traffic, display indoor layouts of malls and airports, and seamlessly switch between satellite and street views. Each rendering was optimized for Indian bandwidth constraints and device capabilities.

The API economy became MapMyIndia's secret weapon. MapmyIndia's cloud mapping services are used by many developers and tech companies in India such as PhonePe, Paytm, Amazon, Alexa voice, Flipkart, Uber, Apple, etc. Every API call generated revenue, created stickiness, and improved data quality through usage patterns. The company built over 200 different APIs, each solving specific use cases—from store locator widgets to complex multi-modal route planning.

The automotive sector emerged as MapMyIndia's fortress within this technology stack. The company's navigation and location services are primarily used by vehicle manufacturers (cars, bikes, commercial vehicles, electric vehicles) and it claims to have 90% market share on GPS navigation in India. This wasn't accidental. Automotive integration required capabilities that consumer apps couldn't provide: offline functionality, real-time traffic via RDS-TMC, integration with vehicle sensors, and update mechanisms that didn't rely on app stores.

It also claims to have 5,000 enterprise customers with 80% market share in the location intelligence space. Each enterprise brought unique requirements that pushed MapMyIndia's technology forward. Banks needed ATM locators that worked across rural India. Insurance companies needed risk assessment based on location. Retailers needed catchment analysis for new store locations.

The IoT and telematics expansion represented the next evolution. MapMyIndia wasn't just providing maps anymore—they were providing real-time location intelligence. Fleet owners could see not just where their vehicles were, but how efficiently they were being driven, whether they were deviating from planned routes, and when they needed maintenance based on usage patterns.

The company also made a strategic push into international markets under the "Mappls" brand—a subtle but important shift that signaled ambitions beyond India. The technology stack they'd built for India's complexity could handle any market. If you could map India's chaos, mapping Dubai's organized grid or Bangkok's structured sprawl was trivial by comparison.

But perhaps the most important aspect of MapMyIndia's technology stack was what it didn't do. Unlike Google, they didn't chase every possible use case. Unlike Chinese mapping companies, they didn't try to become super apps. They remained focused on being the best at one thing: providing location intelligence for enterprises that needed more than consumer-grade mapping.

This focus would prove crucial as the company prepared for its next major milestone—going public in one of the most volatile market environments in recent history.

VII. The IPO & Public Markets Journey (2021)

August 2021. India's stock markets were in the midst of a tech IPO frenzy. Zomato had just gone public at a $9 billion valuation despite mounting losses. Paytm was preparing what would become one of India's most disastrous listings. Against this backdrop, a 26-year-old profitable mapping company filed its draft prospectus with an ambitious target: raising Rs 1,200 crore at a Rs 6,000 crore valuation.

The IPO was structured unusually—it was entirely an Offer for Sale (OFS) of Rs 1,039.61 crore, meaning no fresh capital would come to the company. Instead, existing shareholders would cash out. Rakesh and Rashmi Verma would sell shares worth Rs 354.99 crore. Qualcomm would exit with Rs 424.97 crore. PhonePe (which had inherited Flipkart's stake) would realize Rs 54.51 crore. After 26 years of building, the founders and early investors would finally see liquidity.

The financials told a story that stood in stark contrast to other tech IPOs of that era. In FY2021, MapMyIndia reported revenues of Rs 190 crore (up 17% YoY) and profits of Rs 59.4 crore (up 150% YoY). The company boasted 83% contribution margins and 35% EBITDA margins. In a market flooded with loss-making tech companies promising profitability "someday," MapMyIndia was already there.

The roadshow revealed interesting dynamics. Institutional investors initially balked at the valuation—the company was asking for 60+ times trailing earnings. The bull case centered on growth potential: digital transformation accelerating, connected cars exploding, location-based services becoming essential. The bear case worried about customer concentration (top 25 customers represented 80% of revenue) and Google's looming presence.

But when the IPO opened for subscription in December 2021, something remarkable happened. The issue was subscribed 154.71 times overall—one of the highest subscription rates for any tech IPO that year. Qualified Institutional Buyers bid for 196.56 times their allocation. High net worth individuals bid for 424.69 times. Even retail investors, typically wary of expensive tech stocks, bid for 15.20 times their reserved portion.

December 13, 2021—listing day. MapMyIndia's shares opened at Rs 1,565 on the NSE, a 54% premium to the issue price of Rs 1,033. The market capitalization touched Rs 8,500 crore ($1.12 billion), officially making it a unicorn in public markets. Rakesh and Rashmi Verma, who had started with personal savings and customer advances, were now worth over Rs 2,000 crore on paper.

The listing day performance surprised even optimists. In a market that had begun souring on tech IPOs (Paytm had crashed 27% on debut just weeks earlier), MapMyIndia's surge suggested investors saw something different here. This wasn't a cash-burning startup with a promise—it was a profitable business with a moat.

The reasons for going public extended beyond just providing exits for early investors. The public listing gave MapMyIndia currency for acquisitions, credibility with enterprise customers who preferred dealing with listed entities, and a platform to tell their story to a wider audience. It also forced financial discipline—quarterly earnings calls meant they couldn't hide behind the "we're investing for growth" excuse that private companies often used. Post-IPO performance would validate the market's confidence. The company showed a 35% YoY growth in revenue from operations, from 281.5 crore rupees to 379 crore in FY2024. The Profit After Tax (PAT) stood at 134.4 crore, with a 32% margin, after growing 25% from the previous year. The company maintained its focus on profitability even while investing in growth, a rare balance in the tech sector.

The IPO marked not an end but a transformation. MapMyIndia was no longer just a mapping company built by two engineers—it was now a public technology infrastructure company with responsibilities to thousands of shareholders. The question was: could they maintain their entrepreneurial edge while navigating the scrutiny of public markets?

VIII. Business Model & Unit Economics

Understanding MapMyIndia's business model requires peeling back layers of complexity that most investors miss. On the surface, it's a mapping company. Dig deeper, and it's a subscription software business with infrastructure-like characteristics and venture-style growth potential.

The revenue mix tells the strategic story: Automotive (40%), Enterprises/Government (40%), and Mobile Internet (20%). This isn't accidental diversification—it's a carefully orchestrated balance that provides stability (automotive contracts), growth (enterprise digital transformation), and optionality (mobile/consumer).

The automotive segment represents MapMyIndia's castle—defensible, profitable, and expanding. 2.5+ million new vehicles (4-wheelers, 2-wheelers and CVs, across ICE and EV segments), went built-in with MapmyIndia Mappls, up from 1.9 million during FY23. Each vehicle with embedded MapMyIndia navigation generates revenue through multiple streams: upfront licensing fees to the OEM, annual map update subscriptions, and increasingly, usage-based fees for connected car services.

The enterprise and government segment operates on a different model—high-touch, high-value, highly sticky. A typical enterprise customer might start with basic mapping APIs, expand to fleet tracking, add analytics, and eventually become dependent on MapMyIndia for mission-critical operations. The switching costs aren't just technical—they're operational. Retraining thousands of delivery drivers, reconfiguring logistics systems, rebuilding analytical models—the friction is enormous.

Revenue streams reflect this stickiness: royalties, subscriptions, and annuities from licensing digital maps, platforms, APIs and software. The company has masterfully shifted from one-time license sales to recurring revenue models. A customer that might have paid Rs 10 lakh once for perpetual map access now pays Rs 3 lakh annually for constantly updated maps, navigation, and analytics—a far better lifetime value equation.

The unit economics are where MapMyIndia truly shines. 83% contribution margins and 35% EBITDA margins in 2021 tell a story of a business with massive operating leverage. Once the base map data exists, the marginal cost of serving additional customers approaches zero. Every new API call, every additional vehicle navigation system, every extra enterprise customer drops almost entirely to the bottom line.

But there's a catch hidden in these attractive economics: customer concentration risk. Top 25 customers represent 80% of revenue—a dependency that would terrify most investors. Yet this concentration is somewhat misleading. Many of these "customers" are automotive OEMs representing millions of end users, or platform companies like PhonePe and Paytm serving hundreds of millions of consumers. The real customer base is far more diversified than the billing data suggests.

The SaaS transformation has been gradual but profound. MapMyIndia no longer sells maps—they sell outcomes. For an e-commerce company, it's faster deliveries. For an insurance company, it's better risk assessment. For a car manufacturer, it's enhanced user experience. The maps are just the enabler; the value creation happens in the application layer.

Revenue from the IoT-led business grew 91% YoY to cross an important revenue milestone of Rs 112 crore, with EBITDA growing 13x from Rs 1 crore in FY23 to Rs 13 crore in FY24. This IoT expansion represents the next evolution of the business model. Instead of just providing maps, MapMyIndia now monitors, tracks, and analyzes movement in real-time. Every tracked vehicle, every monitored asset becomes a recurring revenue stream with minimal marginal cost.

The platform economics create powerful network effects. More customers mean more data, which improves map quality, which attracts more customers. More enterprise integrations mean more developers familiar with MapMyIndia APIs, which reduces adoption friction for new enterprises. More vehicles with embedded navigation mean more real-time traffic data, which improves routing for all users.

"If you look at our 3-year track record, revenue has grown at a 38% CAGR and EBITDA margins and PAT margins have been consistently above 40% and 30% respectively. Our Order Book achievements give us further confidence that we are on track to our stated milestone of crossing Rs 1000 Cr revenue by FY27/FY28", says Rakesh Verma, revealing both the company's impressive track record and ambitious targets.

The beauty of MapMyIndia's model lies in its capital efficiency. Unlike consumer tech companies that burn cash acquiring users hoping to monetize later, or infrastructure companies that require massive upfront investment, MapMyIndia generates cash while growing. They've built a rare combination: the defensibility of infrastructure, the margins of software, and the growth potential of a platform.

Yet challenges remain. The enterprise sales cycle is long—often 12-18 months from initial contact to revenue. The automotive industry's cyclicality affects quarterly results. And the constant need to invest in data updates and technology means capital requirements never truly disappear. But for a company that started by walking streets with GPS devices, these are luxurious problems to have.

IX. Competition & Market Position

In the mapping wars of India, MapMyIndia occupies a peculiar position—dominant in niches Google doesn't care about, invisible where Google dominates, and increasingly valuable as regulations tilt the playing field. Understanding this dynamic requires moving beyond simple market share statistics to examine the intricate layers of competitive advantage and vulnerability.

Google Maps is the 800-pound gorilla no one can ignore. With over 1 billion users globally and dominant consumer mindshare in India, Google's free, fast, and familiar mapping service seems unassailable. Yet MapMyIndia hasn't just survived—it has thrived. The answer lies in classic disruption theory turned upside down: instead of starting with the low end and moving up, MapMyIndia started with the complex, high-value segments Google wouldn't touch.

The regulatory moat has become MapMyIndia's secret weapon. India's new geospatial regulations require foreign players like Google, TomTom, and HERE to partner with local players for certain types of restricted data. Detailed mapping of defense installations, critical infrastructure, and border areas remains the exclusive domain of Indian companies. While Google can show you the way to a restaurant, they can't provide the detailed schematics an enterprise needs for infrastructure planning. The 2021 geospatial guidelines crystallized this advantage. Maps/Geospatial Data of spatial accuracy/value finer than the threshold value can only be created and/or owned by Indian Entities and must be stored and processed in India. Foreign companies and foreign owned or controlled Indian companies can license from Indian Entities digital Maps/Geospatial Data of spatial accuracy/value finer than the threshold value only for the purpose of serving their customers in India. Access to such Maps/Geospatial Data shall only be made available through APIs that do not allow Maps/Geospatial Data to pass through Licensee Company or its servers. Re-use or resale of such map data by licensees shall be prohibited.

This regulatory framework essentially made MapMyIndia a toll gate for high-precision mapping in India. Google can still operate, but for anything requiring accuracy better than one meter—critical for autonomous driving, precision agriculture, or infrastructure planning—they need to work with Indian companies like MapMyIndia.

But MapMyIndia's differentiation goes beyond regulatory protection. They've built depth where Google has breadth. 3D mapping of building interiors, hyperlocal points of interest updated daily, truck-specific routing that knows which bridges have height restrictions, APIs optimized for Indian address formats—these aren't features Google prioritizes globally but are essential for Indian enterprises.

The enterprise stickiness becomes MapMyIndia's true moat. When a bank integrates MapMyIndia's APIs to verify addresses for loan applications, when an insurance company uses their data for risk assessment, when a logistics company builds their entire routing algorithm on MapMyIndia's platform—switching becomes operationally impossible. The technical integration is just the beginning; the business processes, employee training, and accumulated optimizations create switching costs that dwarf any potential savings from using free alternatives.

Other competitors exist but struggle to gain traction. TomTom and HERE, the European mapping giants, face the same regulatory restrictions as Google. Indian startups like Genesys International provide competition in specific niches but lack MapMyIndia's comprehensive coverage. Government initiatives to build public mapping infrastructure remain perpetually delayed and underfunded.

The consumer challenge remains MapMyIndia's Achilles heel. Despite launching the Mappls app with fanfare, consumer adoption remains minimal compared to Google Maps. The network effects are brutal—users go where other users are, where reviews exist, where real-time data is richest. MapMyIndia's attempts to build consumer traction through features like COVID dashboards or hyperlocal discovery have yielded limited results.

Yet this consumer weakness might be strategic strength. By not competing head-on with Google in the consumer space, MapMyIndia avoids triggering an all-out war. Google tolerates MapMyIndia's enterprise dominance because it doesn't threaten their advertising model. MapMyIndia gets to build their B2B empire while Google focuses on consumers—an uneasy but stable equilibrium.

Emerging threats loom on the horizon. The Indian government's periodic announcements about building national mapping infrastructure could eventually materialize. New-age startups using crowdsourcing and AI could leapfrog traditional mapping methods. Autonomous vehicle companies might build their own mapping capabilities. But for now, MapMyIndia's combination of data depth, regulatory protection, and enterprise relationships creates a moat that even Google hasn't been able to cross.

X. Future Strategy & Growth Vectors

"Our Order Book achievements give us further confidence that we are on track to our stated milestone of crossing Rs 1000 Cr revenue by FY27/FY28," Rakesh Verma declared, setting an ambitious target that would represent a 3x growth from current levels. The path to this trillion-rupee milestone runs through multiple growth vectors, each representing both massive opportunity and significant execution risk.

The IoT explosion represents MapMyIndia's most immediate growth driver. The company achieved 52% growth in the number of IoT devices installed during the year to 2.9+ Lakhs, which led to significant growth in our IoT-led business. The vision is audacious: growing the IoT business 10x by FY28. Every commercial vehicle getting mandated GPS tracking, every corporate fleet adopting telematics, every high-value shipment being monitored—each becomes a recurring revenue stream for MapMyIndia.

International expansion under the Mappls brand opens entirely new markets. Southeast Asia and MENA regions share India's infrastructure challenges: rapidly growing cities, informal addressing systems, limited existing digital infrastructure. MapMyIndia's hard-won expertise in mapping chaos becomes their competitive advantage. If you can map Mumbai's slums or Delhi's unauthorized colonies, mapping Bangkok or Cairo seems almost straightforward by comparison. The drone mapping acquisition through Indrones represents a technological leap. MapmyIndia acquired a 20 percent stake in Indrones Solutions Private Limited worth Rs 7 crore in 2023, gaining capabilities in high-resolution 3D mapping and real-time monitoring. "Drones are a sunrise industry, with incredible potential and market opportunity. Our strategic investment in Indrones is in-line with the vision of our Prime Minister's vision of Aatmanirbhar Bharat and making India a drone hub by 2030," Rakesh Verma explained.

This isn't just about better maps—it's about creating entirely new business models. Construction companies using drone monitoring for progress tracking. Mining companies conducting volumetric analysis. Insurance companies assessing disaster damage. Agriculture companies monitoring crop health. Each use case opens a new revenue stream, often with recurring monitoring requirements that create subscription-like economics.

The ONDC (Open Network for Digital Commerce) integration positions MapMyIndia at the center of India's e-commerce revolution. As the government-backed platform aims to democratize digital commerce, location services become critical infrastructure. Every seller needs to be mapped, every delivery needs routing, every service area needs defining. MapMyIndia's comprehensive coverage of even tier-3 and tier-4 cities makes them indispensable to ONDC's vision.

Smart cities represent another massive opportunity. India plans to develop 100 smart cities, each requiring comprehensive digital twins—3D models that integrate real-time IoT data with geographic visualization. MapMyIndia's ability to combine their mapping data with IoT sensors, drone imagery, and analytics platforms positions them as the natural infrastructure provider for these initiatives.

The EV revolution creates unique opportunities. Electric vehicles need different routing algorithms that account for charging station locations, battery range, and regenerative braking on downhill routes. MapMyIndia is building the charging station database, partnering with charge point operators, and developing EV-specific navigation that could become standard in India's electric mobility push.

AI and computer vision applications multiply the value of existing data. "We are seeing MapmyIndia's own ability to generate business through drones in the last 1, 1.5 years, standalone supplying drones to the client, doing drone as a service solutions or incorporating drones into our overall smart city GIS or 3D digital twin solution," CEO Rohan Verma noted. The company is moving from just providing maps to providing intelligence—predicting traffic patterns, identifying infrastructure issues, optimizing city planning.

The consumer app, while still nascent with 20 million downloads, represents optionality rather than core strategy. It's a hedge against platform shifts, a data collection tool, and a brand builder. Success here would be transformative, but isn't necessary for the Rs 1,000 crore target.

International expansion offers perhaps the greatest long-term potential. India's complexity makes other markets seem simple by comparison. The same capabilities that map Mumbai's slums can map Jakarta's kampungs or Cairo's informal settlements. The company is already establishing presence in Southeast Asia and MENA regions, targeting markets with similar infrastructure challenges and regulatory environments favorable to local players.

But execution risks abound. International expansion requires local partnerships and cultural understanding. Drone regulations remain fluid and could become restrictive. Government smart city initiatives often face delays and budget cuts. The EV revolution might take longer than expected. And the constant need for technology investment means capital requirements will remain substantial.

Yet the convergence of trends—digital transformation, IoT proliferation, drone adoption, EV transition, smart city development—creates a generational opportunity. MapMyIndia sits at the intersection of all these trends, with the data, technology, and relationships to capitalize. The Rs 1,000 crore target might prove conservative if even half these growth vectors materialize as expected.

XI. Investment Lessons & Playbook

The MapMyIndia story offers a masterclass in contrarian thinking and patient capital that challenges every assumption about building technology companies in emerging markets. When Rakesh and Rashmi Verma started walking Delhi's streets with GPS devices in 1995, venture capitalists would have laughed them out of the room. No scalable business model. Massive capital requirements. Glacial growth. Competition from global giants inevitable. Every rational analysis said this was a terrible idea.

Yet here we are, nearly three decades later, with a profitable company worth over Rs 9,000 crores that dominates critical segments of India's mapping infrastructure. The lessons from this journey read like a playbook for building in "impossible" markets.

Lesson 1: When conventional wisdom says a market is impossible, that's precisely when to enter. The impossibility of mapping India—its size, complexity, constant change, lack of infrastructure—became MapMyIndia's moat. Google, with all its resources, couldn't replicate 26 years of ground-truth data collection. The very factors that made India "unmappable" made MapMyIndia irreplaceable once they'd done it.

Lesson 2: Choose depth over breadth when competing with platforms. When Google Maps arrived, MapMyIndia didn't try to out-Google Google. They went deeper into enterprise needs, building features Google wouldn't: offline functionality for automotive systems, truck-specific routing, hyperlocal address parsing. They became exceptional for the few rather than adequate for the many. This focus on depth created switching costs that free alternatives couldn't overcome.

Lesson 3: Patient capital beats venture capital in infrastructure plays. MapMyIndia bootstrapped for 12 years before raising institutional capital. This forced discipline, customer focus, and sustainable unit economics from day one. While competitors burned cash acquiring users, MapMyIndia used customer advances to fund expansion. The result: profitability during scaling, not after.

Lesson 4: Local expertise compounds in non-obvious ways. Understanding that "opposite Sharma ji's shop" is a more reliable address than "House #45, Block C" seems trivial. But multiply this by millions of data points, and you have irreplaceable local knowledge. This expertise extends beyond data to relationships (government contracts), regulations (geospatial restrictions), and business practices (enterprise sales cycles). Time in market creates advantages that money can't buy.

Lesson 5: Platform transitions create opportunities for focused players. The shift from paper maps to digital, from desktop to mobile, from offline to connected, from human-driven to autonomous—each transition created opportunities for MapMyIndia to capture value. They didn't need to win every transition, just the ones that mattered to their core customers. While Google focused on consumer mobile, MapMyIndia owned automotive embedded systems.

Lesson 6: Regulatory complexity can be a competitive advantage. India's byzantine mapping regulations, inherited from colonial-era survey restrictions and amplified by security concerns, seemed like a burden. MapMyIndia turned them into a moat. Foreign players faced restrictions they couldn't navigate. Domestic competitors lacked the relationships and compliance infrastructure MapMyIndia had built over decades.

Lesson 7: The power of being boringly profitable. In an era of growth-at-all-costs startups, MapMyIndia's focus on profitability seemed quaint. But this discipline meant they controlled their destiny. No desperate fundraising rounds. No forced pivots to chase growth. No fire sales when capital dried up. Profitability provided the ultimate optionality.

Lesson 8: Timing markets matters more than entering first. MapMyIndia didn't invent digital mapping. They didn't launch the first navigation device. They didn't create the first mapping API. But they timed each market transition perfectly: building data when it was hard, platformizing when enterprises digitized, going public when markets rewarded profitability. Being early is the same as being wrong if the market isn't ready.

Lesson 9: Building for enterprises creates stickier value than consumer plays. Every consumer app fears the next platform shift. But enterprise infrastructure, once embedded, becomes nearly impossible to displace. MapMyIndia's APIs running mission-critical logistics operations, their navigation systems embedded in millions of vehicles, their data powering loan underwriting—these integrations create decade-long relationships, not monthly subscriptions.

Lesson 10: The best moats are built before anyone realizes they're valuable. When MapMyIndia started mapping India, digital maps seemed like a nice-to-have feature. By the time they became mission-critical infrastructure, MapMyIndia had already mapped everything. The moat was built before competitors realized there was a castle worth attacking.

The metalesson transcends mapping or India: in an age of blitzscaling and unicorn hunting, there's still room for patient, focused, profitable building. MapMyIndia proves that you can compete with Big Tech without becoming Big Tech. You can build valuable companies without venture capital steroids. You can create lasting value by solving hard, boring, essential problems that others ignore.

For founders, the playbook is clear: find markets others consider impossible, build depth over breadth, bootstrap until you can't, turn regulatory complexity into competitive advantage, and focus relentlessly on profitability. For investors, the lesson is equally clear: the best investments often look like the worst ideas, patient capital beats fast money in infrastructure plays, and boring B2B businesses can generate spectacular returns.

XII. Bear vs Bull Case

Bear Case: The Structural Challenges

The bear case for MapMyIndia starts with an uncomfortable truth: Google's dominance in consumer mapping is insurmountable. With over 1 billion users globally and overwhelming mindshare in India, Google Maps has become the default verb for navigation. "Google it" has a parallel in "Google Maps pe dekh lo." This consumer dominance matters because it drives data network effects—every search, every navigation session, every user correction makes Google's maps better. MapMyIndia's 20 million app downloads pale in comparison, and without consumer scale, they miss the most valuable real-time data.

Customer concentration presents another red flag. Top 25 customers represent 80% of revenue—a dependency that would terrify any risk-conscious investor. Lose a major automotive OEM to in-house mapping or a competing solution, and quarterly results crater. This concentration also gives large customers enormous pricing power during contract renewals. When your biggest customer knows they represent 15% of your revenue, negotiations become one-sided.

The slowing automotive sector clouds the growth outlook. MapMyIndia claims 90% market share in automotive GPS navigation, but what happens when the market itself shrinks? Indian automotive sales have been cyclical, and any prolonged slowdown directly impacts MapMyIndia's largest revenue segment. Moreover, the shift to electric vehicles might reset competitive dynamics—new EV manufacturers might choose different mapping partners or build their own solutions.

Government infrastructure ambitions pose an existential threat. India's Survey of India has announced plans to modernize and digitize mapping infrastructure. The government's Svamitva scheme aims to map all rural properties. ISRO is launching more sophisticated satellites. If the government decides to provide high-quality mapping data as public infrastructure—like GPS itself—MapMyIndia's entire business model evaporates.

Valuations remain stretched even after recent corrections. Trading at 60+ times trailing earnings, MapMyIndia is priced for perfection. Any disappointment in growth rates, customer losses, or margin compression could trigger significant multiple contraction. For comparison, established global mapping companies trade at 20-30x earnings. The premium assumes flawless execution that rarely materializes.

Technology disruption looms large. What if crowdsourced mapping becomes accurate enough for enterprise use? What if satellite imagery advances make ground surveying obsolete? What if autonomous vehicles develop their own mapping systems that don't need traditional navigation? What if augmented reality changes navigation paradigms entirely? MapMyIndia must defend against multiple technological attack vectors simultaneously.

The international expansion story remains unproven. Success in India doesn't guarantee success in Indonesia or Egypt. Each market has unique characteristics, entrenched competitors, and local regulations. Google and regional players won't cede ground easily. International expansion often becomes a capital sink that distracts from core operations.

Bull Case: The Structural Advantages

The bull case begins with regulatory moats that are strengthening, not weakening. India's 2021 geospatial guidelines didn't just protect MapMyIndia—they enshrined their advantage into law. Foreign companies cannot own high-precision mapping data. They must partner with Indian entities. They can only access data through APIs. As India becomes more concerned about data sovereignty and national security, these restrictions will likely tighten, not loosen.

Digital India tailwinds are accelerating across every metric. E-commerce penetration growing at 25% annually. Digital payments exploding. Logistics and delivery becoming ubiquitous even in tier-3 cities. Each of these trends increases demand for location intelligence. MapMyIndia sits at the infrastructure layer of this digital transformation, collecting tolls on every transaction that requires mapping.

The IoT and telematics explosion is just beginning. India mandated vehicle tracking for commercial vehicles. Insurance companies are pushing usage-based insurance. Supply chains need end-to-end visibility. Smart cities need real-time monitoring. MapMyIndia's 52% growth in IoT devices installed is just the start. With IoT devices projected to reach 5 billion in India by 2025, the addressable market is massive.

Local data advantage proves irreplaceable despite technological advances. India's addresses aren't getting more structured—if anything, rapid urbanization makes them more chaotic. Local language variations, informal settlements, constantly changing infrastructure—these complexities require human understanding that pure technology can't replicate. MapMyIndia's 26-year head start in understanding these nuances creates a moat that deepens with time.

Multiple growth vectors provide optionality. Even if automotive slows, IoT can compensate. If government mapping improves, drone services expand. If Google dominates consumer, enterprise deepening accelerates. The company isn't dependent on any single growth driver. This diversification, unusual for a focused technology company, provides resilience.

The management team's track record inspires confidence. The same founders who navigated from paper maps to digital, from GPS devices to cloud APIs, from bootstrapping to IPO, remain at the helm. They've consistently adapted to technological and market shifts. Their conservative approach—profitable growth, customer funding, gradual expansion—might seem slow but has proven sustainable.

Acquisition potential adds asymmetric upside. MapMyIndia could be extremely valuable to multiple acquirers: global automotive OEMs wanting to control their mapping stack, Indian conglomerates building digital ecosystems, or even government entities recognizing mapping as critical infrastructure. At current valuations, a strategic acquirer could pay a significant premium and still find it economical versus building from scratch.

The Verdict: Asymmetric Risk-Reward

The bear and bull cases reveal a fundamental tension: MapMyIndia is either a niche player in a commodity market or critical infrastructure for India's digital economy. The answer likely depends on time horizon and India's broader trajectory.

Short-term risks are real—customer concentration, valuation multiples, and competitive threats could cause significant volatility. But long-term structural advantages—regulatory moats, local expertise, infrastructure positioning—suggest durability that markets might be undervaluing.

The key insight: MapMyIndia doesn't need to win everything to succeed. They don't need to beat Google in consumer. They don't need international expansion to work perfectly. They don't need every growth vector to materialize. They just need to remain the irreplaceable mapping infrastructure for enough critical use cases in India.

For investors, this creates an interesting setup. The downside might be 30-40% if growth disappoints or multiples compress. But the upside could be 3-5x if they achieve their Rs 1,000 crore revenue target, successfully expand internationally, or become acquisition targets. It's asymmetric risk-reward for those who believe in India's digital transformation and MapMyIndia's role in enabling it.

XIII. Epilogue & Reflections

As we conclude this deep dive into MapMyIndia's three-decade journey, it's worth stepping back to appreciate what Rakesh and Rashmi Verma have actually built. This isn't just a company that makes digital maps. It's a testament to the power of compound effort, the value of solving hard problems, and the possibility of building world-class technology companies from India.

From manual surveying to powering Apple Maps: The 30-year journey captures something profound about technological progress. When the Vermas started, they were literally walking streets with notebooks and GPS devices. Today, when someone in California asks Siri for directions in Delhi, MapMyIndia's data provides the answer. This transformation—from manual to digital, from local to global, from data to intelligence—mirrors India's own technological evolution.

The story teaches essential lessons about building in emerging markets. First, infrastructure gaps that seem like obstacles are actually opportunities. The absence of existing digital maps wasn't a barrier—it was MapMyIndia's opening. Second, developed market solutions don't always translate. Google Maps works brilliantly in Manhattan but struggles with Mumbai's complexity. Local problems require local solutions. Third, patience pays. Building fundamental infrastructure takes time. The companies that survive long enough to see markets mature capture disproportionate value.

The importance of founder persistence cannot be overstated. Rakesh and Rashmi's three-decade commitment is remarkable in an era of quick flips and early exits. They weathered the dot-com bust, survived the 2008 financial crisis, competed against Google's arrival, navigated COVID disruptions, and took the company public—all while maintaining control and vision. This isn't just longevity; it's evolution. The same founders who sold paper maps to Coca-Cola in 1995 are now building drone-based 3D mapping platforms.

MapMyIndia's story is also India's digital infrastructure story told through one company's lens. When they started, India had no internet, no smartphones, no digital payments, no e-commerce. Today, India has the world's largest digital identity system (Aadhaar), unified payments interface (UPI), and one of the fastest-growing digital economies. MapMyIndia both benefited from and contributed to this transformation. They're not just documenting India's geography—they're enabling its digital economy.

Looking forward, MapMyIndia stands at an inflection point. The next five years will determine whether they remain a successful niche player or become fundamental infrastructure for the world's most populous nation. The pieces are in place: regulatory protection, technological capabilities, customer relationships, and growth vectors. Execution will determine outcomes.

For founders, MapMyIndia offers a different template for success. You don't need to blitzscale. You don't need venture capital on day one. You don't need to be a consumer brand. You can build valuable, durable companies by solving unglamorous problems with patience and persistence. The highest returns often come from the least obvious opportunities.

For investors, the lesson is about recognizing value in unfashionable places. While everyone chases the next consumer app unicorn, companies like MapMyIndia quietly build irreplaceable infrastructure. The best investments often look boring, take forever to mature, and operate in markets others ignore. But when they work, the moats are permanent and the returns are spectacular.

The broader implications extend beyond business. In an increasingly digital world, mapping isn't just about navigation—it's about representation, access, and opportunity. When MapMyIndia maps a rural village, they're not just creating data points. They're making that village visible to government services, accessible to e-commerce, and connected to the digital economy. This is infrastructure as empowerment.

As India accelerates its digital transformation, the question isn't whether mapping will be valuable—it's who will capture that value. Google offers breadth and convenience. Government provides authority and scale. But MapMyIndia offers something unique: deep local expertise, proven execution, and alignment with India's strategic interests.

The ultimate judgment of MapMyIndia's success won't be its stock price or revenue growth. It will be whether they achieved their fundamental mission: making India mappable, navigable, and connected. By that measure, they've already succeeded. Everything else—the IPO, the billion-dollar valuation, the international expansion—is just validation of what Rakesh and Rashmi Verma knew three decades ago: India needed its own maps, and someone had to build them.

The story continues. New chapters on autonomous vehicles, drone delivery, smart cities, and technologies we can't yet imagine await. But the foundation—painstakingly built over 30 years of walking streets, writing code, and serving customers—remains solid. In a world of overnight unicorns and instant obsolescence, MapMyIndia proves that some things still take time, and some moats still last forever.

For those betting on India's digital future, MapMyIndia represents a rare combination: a picks-and-shovels play on digital transformation, a regulatory moat in a strategic sector, and a profitable business with multiple growth vectors. Whether that makes it a good investment depends on your timeline, risk tolerance, and belief in India's trajectory. But one thing is certain: as long as India keeps growing, changing, and digitizing, someone needs to keep mapping it. And for now, that someone is MapMyIndia.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube