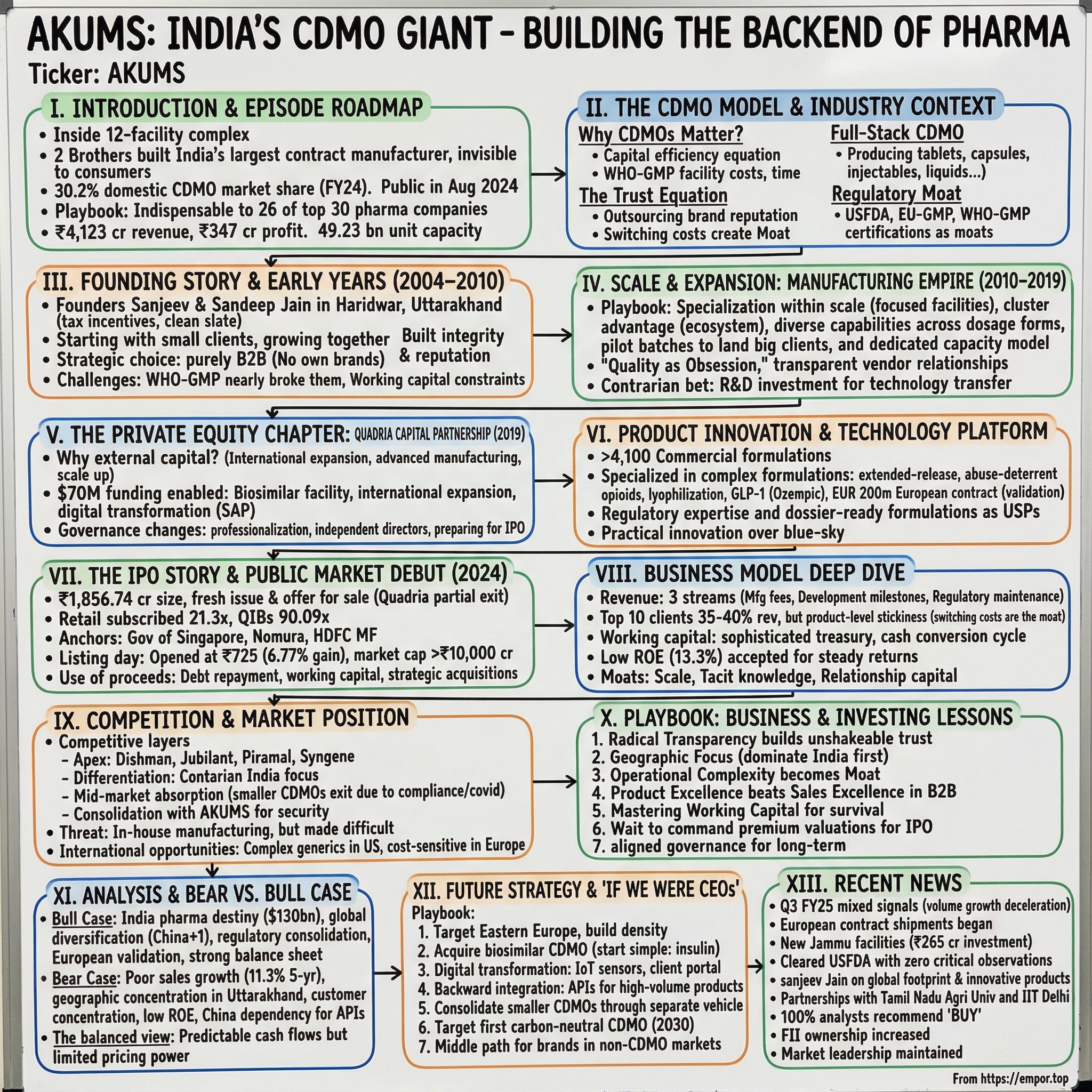

AKUMS: India's CDMO Giant Building the Backend of Pharma

I. Introduction & Episode Roadmap

Picture this: Inside a sprawling 12-facility pharmaceutical complex in the foothills of the Himalayas, machines hum 24/7, churning out billions of tablets and capsules. But here's the twist—not a single pill bears the manufacturer's name. Welcome to the hidden world of AKUMS Drugs and Pharmaceuticals, where two brothers built India's largest pharmaceutical contract manufacturer, powering the medicines in millions of Indian households while remaining virtually unknown to consumers. When Sanjeev and Sandeep Jain stood in their modest facility in Haridwar in 2004, watching the first batch of tablets roll off their production line, they couldn't have imagined they were laying the foundation for what would become India's 30.2% market share holder of the domestic CDMO market by FY24. Today, AKUMS—acronym for the founders' initials—stands as India's pharmaceutical manufacturing giant, offering comprehensive pharmaceutical products and services in India and overseas, yet remaining virtually invisible to the billions who consume medications manufactured in their facilities.

This is the story of how two brothers built the backend of Indian pharma—a Contract Development and Manufacturing Organization (CDMO) that powers the medicines in millions of households while deliberately staying out of the limelight. The company went public in August 2024, listing at ₹725 versus an IPO price of ₹679, delivering a 6.77% listing gain, marking a pivotal moment in their two-decade journey.

The AKUMS Playbook

What makes AKUMS fascinating isn't just their scale—₹4,123 crore in revenue with ₹347 crore profit—but their strategic positioning in India's pharmaceutical value chain. While global pharmaceutical giants and domestic champions battle for brand recognition and market share, AKUMS built an empire by becoming indispensable to all of them. In FY24, the company manufactured pharmaceutical products for 26 of the top 30 companies in India by sales.

This episode unravels how AKUMS navigated India's complex pharmaceutical landscape, scaled manufacturing to 49.23 billion units annual production capacity across 10 facilities, and why they chose to remain the invisible backbone rather than chase consumer recognition. We'll explore their unique business model, dissect their IPO journey, and understand what their story teaches us about building B2B moats in highly regulated industries.

II. The CDMO Model & Industry Context

Imagine you're a pharmaceutical company with a breakthrough diabetes medication formula. You've spent years and millions on research, clinical trials, and regulatory approvals. Now you need to manufacture billions of tablets annually, maintain stringent quality standards, navigate complex regulations, and distribute across India. Do you build factories, hire thousands of workers, and invest hundreds of crores? Or do you partner with someone who's already mastered this complexity?

Enter the CDMO—Contract Development and Manufacturing Organization—the unsung hero of modern pharmaceuticals. CDMOs are specialized companies that develop and manufacture drugs on behalf of pharmaceutical companies. Think of them as the Foxconn of pharma—while Apple designs the iPhone, Foxconn manufactures it. Similarly, while pharma companies focus on research, marketing, and distribution, CDMOs handle the complex manufacturing ballet.

The Indian Pharmaceutical Renaissance

To understand AKUMS's rise, we must first grasp India's pharmaceutical transformation. The Indian pharmaceutical industry, valued at $50 billion, is projected to reach $65 billion by 2024 and $130 billion by 2030. This isn't just growth—it's a fundamental restructuring of global pharmaceutical supply chains.

India supplies over 50% of Africa's generics, 40% of the US's generic demand, and 25% of all medicines in the UK. This dominance didn't happen overnight. It's the result of decades of reverse engineering expertise, cost advantages, and most importantly, the ability to navigate complex regulatory frameworks across multiple geographies.

Why CDMOs Matter: The Capital Efficiency Equation

Here's the brutal math of pharmaceutical manufacturing: Setting up a WHO-GMP compliant facility costs ₹50-100 crores minimum. Add USFDA compliance? Double it. Want to manufacture multiple dosage forms? Multiply by the number of production lines. Now factor in the 18-24 months for regulatory approvals, the army of quality control professionals, and the working capital to manage inventory.

For a mid-sized pharma company launching 10-15 products annually, the capital requirement becomes prohibitive. Even large companies face a choice: tie up capital in manufacturing or invest in R&D and marketing where their competitive advantages lie. This capital efficiency calculation drives the CDMO industry.

The Trust Equation in Pharma Manufacturing

Manufacturing pharmaceuticals isn't like making smartphones or automobiles. A single contamination incident, one failed quality test, or a regulatory violation can destroy decades of reputation overnight. When a pharma company outsources manufacturing, they're not just outsourcing production—they're entrusting their brand's existence to the CDMO.

This trust barrier creates a powerful moat. Once a CDMO proves reliability through years of flawless execution, switching becomes almost unthinkable. The cost isn't just finding a new manufacturer—it's the regulatory re-filings, stability studies, bioequivalence tests, and the career risk for the executive making the switch. AKUMS, established in 2004, became India's largest pharmaceutical CDMO by revenue, production capacity, and clients as of FY23, precisely by becoming the most trusted name in this trust-deficit industry.

AKUMS's Positioning: The Full-Stack CDMO

While competitors specialized in specific dosage forms or therapeutic areas, AKUMS built capabilities across the entire pharmaceutical spectrum. They produce tablets, capsules, liquid orals, vials, ampoules, blow-filled seals, topical preparations, eye drops, dry powder injections, and gummies. This isn't just product diversity—it's strategic positioning as a one-stop solution.

Consider a pharmaceutical company launching a comprehensive diabetes care portfolio: oral medications, insulin injectables, and topical creams for diabetic foot care. Instead of coordinating with three different CDMOs, managing multiple quality audits, and juggling regulatory filings, they can partner with AKUMS for everything. This convenience premium becomes AKUMS's pricing power.

The Regulatory Moat

In pharmaceuticals, regulations aren't hurdles—they're moats. Every certification—WHO-GMP, USFDA, EU-GMP, TGA—requires months of preparation, extensive documentation, and substantial investment. More importantly, maintaining these certifications requires consistent excellence. One failed inspection can shut down exports to entire continents.

AKUMS didn't just collect certifications; they built a culture around regulatory excellence. Their facilities undergo regular audits not just from regulators but from clients—sometimes 50-60 audits annually. Each successful audit deepens trust and raises switching costs for clients.

III. Founding Story & Early Years (2004–2010)

The year was 2004. India's pharmaceutical industry was at an inflection point—the product patent regime was about to be implemented, changing the generics landscape forever. In this environment of uncertainty, Sanjeev Jain and Sandeep Jain, the company's promoters, saw opportunity where others saw risk.

The brothers didn't come from pharmaceutical royalty. They weren't scions of established business houses. Their insight was deceptively simple: as Indian pharma companies shifted focus from reverse engineering to innovation and marketing, someone needed to handle the unglamorous but essential work of manufacturing. They named their company AKUMS—a combination of their initials—a personal stamp on what would become an industrial empire.

The Haridwar Gambit

Their first strategic decision revealed their thinking: instead of setting up in established pharmaceutical hubs like Hyderabad or Ahmedabad, they chose Haridwar in Uttarakhand. The state government, eager to industrialize, offered tax incentives that would prove crucial for a capital-intensive business. But beyond tax benefits, Uttarakhand offered something more valuable—a clean slate.

In established pharma clusters, talent was expensive and constantly poached. In Uttarakhand, AKUMS could build and train their workforce from scratch, creating loyalty through opportunity. They hired local graduates, invested heavily in training, and created a pipeline of pharmaceutical manufacturing expertise where none existed before.

Building Credibility: The First Clients

The early years were brutal. Established CDMOs had decades-long relationships. Why would any pharma company risk their products with newcomers? The Jain brothers' solution was counterintuitive—they started with the smallest players, the companies other CDMOs ignored.

These small pharmaceutical companies, often family-run businesses themselves, needed flexible minimum order quantities and personalized attention that larger CDMOs wouldn't provide. AKUMS became their lifeline, manufacturing small batches, accommodating frequent changes, and most importantly, growing with them.

One early client, a small Ayurvedic company struggling to scale production, would later become a ₹500 crore brand. They never forgot who helped them when they were nobody. These relationships, forged in mutual struggle, became AKUMS's foundation.

The Contract Manufacturing Decision

By 2007, AKUMS faced a crossroads. They had manufacturing capabilities, regulatory approvals, and market knowledge. Why not launch their own brands? The temptation was immense—branded generics offered 40-50% margins versus 15-20% in contract manufacturing.

The brothers made a crucial decision: remain purely B2B. They recognized that the moment they launched their own brands, they'd become competitors to their clients. Trust, painstakingly built, would evaporate overnight. This decision—to forgo short-term profits for long-term relationships—would define AKUMS's trajectory.

Navigating India's Regulatory Maze

Getting WHO-GMP certification in 2006 was AKUMS's first major milestone. But the process nearly broke them. The documentation requirements were overwhelming—Standard Operating Procedures (SOPs) for everything from hand washing to equipment cleaning. Quality control protocols that seemed designed for multinational corporations, not a startup.

They hired consultants who charged lakhs but delivered generic templates. Inspectors found violations that seemed arbitrary. The brothers learned a crucial lesson: in pharmaceuticals, there's no substitute for building internal expertise. They started hiring quality assurance professionals from established companies, paying premiums they could barely afford.

The investment paid off. When they cleared WHO-GMP certification on their second attempt, word spread quickly in India's tight-knit pharma community. A new player had arrived who took quality seriously.

Early Growth Challenges

Working capital management nearly killed AKUMS in 2008. Pharmaceutical manufacturing has a peculiar cash flow challenge: raw materials need upfront payment, manufacturing takes 30-45 days, quality testing adds another 15-30 days, and clients pay 60-90 days after delivery. For a company growing 50% annually, this meant constantly scrambling for funds.

Banks were skeptical. Contract manufacturing was seen as risky—no brands, no consumer recognition, entirely dependent on other companies' success. The global financial crisis made credit even tighter. The brothers mortgaged personal assets, negotiated painful payment terms with suppliers, and sometimes paid salaries from personal funds.

But they never compromised on quality. When a batch failed internal testing in 2009—a ₹50 lakh loss they could barely afford—they destroyed it rather than attempt rework. The client never knew, but word of such integrity spreads in industry circles. By 2010, AKUMS had something money couldn't buy: reputation.

IV. Scale & Expansion: Building the Manufacturing Empire (2010–2019)

The year 2010 marked AKUMS's transformation from survivor to predator. They had proven the model, built credibility, and most importantly, generated cash flow. Now came the audacious part—building one of India's largest pharmaceutical manufacturing complexes, one facility at a time.

The Expansion Playbook

Between 2010 and 2019, AKUMS didn't just grow—they metastasized across Uttarakhand and Himachal Pradesh. They became the largest India-focused CDMO with diverse client base, longstanding relationships, large R&D capabilities, strategic presence across the pharmaceutical value chain, and experienced management team. But this wasn't random expansion. Each facility was a calculated chess move.

The first principle: specialization within scale. Rather than building massive multi-purpose plants, they created focused facilities. One for high-volume tablets, another for complex injectables, a dedicated unit for controlled substances. This specialization allowed them to optimize processes, reduce changeover times, and most critically, prevent cross-contamination—a perpetual risk in multi-product facilities.

The Baddi facility, commissioned in 2012, exemplified this philosophy. Designed exclusively for beta-lactam antibiotics (penicillin derivatives), it operated in complete isolation from other products. While competitors struggled with contamination issues, AKUMS could guarantee zero cross-contamination—a claim worth gold in pharmaceutical manufacturing.

The Uttarakhand Cluster Advantage

By 2015, AKUMS had created something unique—a pharmaceutical manufacturing cluster within a cluster. Their concentration of manufacturing units in Uttarakhand wasn't just about tax benefits anymore. They had built an ecosystem.

Consider the logistics: raw materials arriving at one facility could be partially processed and transferred to another for finishing. Quality control laboratories served multiple plants. Management could visit all facilities within hours. This proximity created operational efficiencies competitors with distributed facilities couldn't match.

But concentration created vulnerability. The 2013 Uttarakhand floods tested this strategy. While facilities remained safe, supply chains were devastated. AKUMS's response revealed their evolution—within 72 hours, they'd arranged helicopter deliveries for critical medicines, ensuring no client faced stockouts. The crisis became a trust-building opportunity.

Building Capabilities Across Dosage Forms

Since founding, Akums developed over 4,146 commercial formulations across more than 60 different dosage forms. This wasn't diversification for its own sake—it was about becoming indispensable.

The journey into complex dosage forms started with extended-release tablets in 2011. While immediate-release tablets dump medication into your system at once, extended-release formulations deliver medication over 12-24 hours. The technology seems simple—special coatings or matrix tablets—but execution requires precise control over particle sizes, coating thickness, and compression forces.

AKUMS invested ₹15 crores in equipment that could maintain temperature within 0.5°C tolerance and humidity within 2% RH. Overkill? Perhaps. But when they successfully manufactured a complex psychiatric medication that three other CDMOs had failed to replicate, the investment justified itself through a single contract worth ₹100 crores annually.

The Client Acquisition Masterclass

By 2015, AKUMS had cracked the code for landing major clients. As of March 31, 2024, their CDMO business served 1,524 Indian and multinational companies, up from 1,386 on March 31, 2022. Their strategy was multilayered.

First, they never pitched manufacturing alone. They positioned themselves as product development partners. When a client approached with a molecule, AKUMS didn't just quote manufacturing costs. They offered formulation development, stability studies, regulatory dossier preparation—the entire journey from molecule to market.

Second, they mastered the art of the pilot batch. Potential clients could commission small batches for market testing without massive commitments. These pilots, often manufactured at cost or even losses, were investments in relationships. When products succeeded, AKUMS had already proven capability.

The real breakthrough came with their "dedicated capacity" model. Large clients could reserve production lines, ensuring supply security without capital investment. For the client, it meant reliable supply without asset ownership. For AKUMS, it meant guaranteed utilization and predictable revenue streams.

Quality as Differentiator

While competitors treated quality certifications as checkboxes, AKUMS built a quality culture that bordered on obsession. By 2016, they had cleared inspections from regulators across 15 countries. But the real achievement was their inspection success rate—over 95% cleared without critical observations.

How? They ran mock inspections monthly, hiring former FDA inspectors as consultants. Every employee, from machine operators to security guards, underwent quality training. They created a "quality dashboard" visible throughout facilities, tracking metrics in real-time. Deviations weren't hidden but highlighted for immediate correction.

This transparency extended to clients. AKUMS offered unprecedented access—live camera feeds from production areas, real-time batch records, immediate notification of any deviations. Clients could audit virtually anytime. This radical transparency transformed vendor relationships into partnerships.

The R&D Investment

Akums operates four research and development units, two approved by the Department of Scientific and Industrial Research. By 2017, AKUMS made a contrarian bet—massive R&D investment in a contract manufacturing business.

The logic was subtle but powerful. Pharmaceutical companies increasingly outsourced not just manufacturing but development. Could AKUMS develop formulations that clients could directly market? The investment was staggering—406 scientists by 2024, sophisticated equipment, dedicated facilities.

The payoff came through "technology transfer" fees—upfront payments for developed formulations. A single complex formulation could command ₹5-10 crores in transfer fees plus manufacturing contracts. By 2019, AKUMS had created a portfolio of ready-to-market formulations that clients could launch within months rather than years.

V. The Private Equity Chapter: Quadria Capital Partnership

The year was 2019. AKUMS had built an empire—thousands of crores in revenue, relationships with India's pharmaceutical elite, and a manufacturing complex rivals envied. Yet the Jain brothers knew they stood at an inflection point. The next phase of growth—international expansion, biological drugs, advanced manufacturing—required not just capital but transformation. Enter Quadria Capital.

Why External Capital After 15 Years?

For fifteen years, AKUMS had grown entirely through internal accruals and debt. The brothers had retained complete control, made decisions quickly, and built the company their way. Raising $70M from Quadria Capital wasn't about survival—it was about acceleration.

The pharmaceutical industry was consolidating globally. Indian CDMOs faced a choice: scale up or become acquisition targets. AKUMS needed to move fast—build biosimilar capabilities, expand internationally, acquire complementary businesses. Banks would fund assets but not ambition. Private equity offered something more valuable than money: global connections and governance expertise.

Quadria's Healthcare Thesis

Quadria wasn't a typical private equity firm chasing quick returns through financial engineering. They specialized in Asian healthcare, understanding the sector's long cycles and regulatory complexities. Their portfolio included hospital chains, diagnostic companies, and pharmaceutical firms across Southeast Asia.

For Quadria, AKUMS represented a platform play. India would become the world's pharmacy, and contract manufacturing would explode as global pharma focused on innovation over infrastructure. AKUMS, with its scale and reputation, could consolidate India's fragmented CDMO industry and expand internationally.

The courtship lasted six months. Quadria conducted due diligence that bordered on forensic—reviewing every client contract, inspecting facilities, interviewing competitors. They discovered what the brothers knew—AKUMS's client stickiness was extraordinary, with average relationships exceeding seven years.

What the Funding Enabled

The $70 million wasn't sitting in bank accounts. Within months, AKUMS launched three major initiatives that would've been impossible without growth capital.

First, the biosimilar facility. Biological drugs—produced from living organisms rather than chemical synthesis—represented pharma's future. But manufacturing requirements were exponentially complex: sterile environments, cold chains, batch-to-batch consistency challenges. The facility alone required $25 million, with another $10 million for technology transfer and training.

Second, international expansion. AKUMS hired regulatory experts for European and US filings. They acquired a small UK-based regulatory consultancy, instantly gaining expertise in navigating Western regulatory frameworks. This wasn't just about certifications—it was about understanding how developed market clients evaluated CDMOs.

Third, digital transformation. AKUMS implemented SAP across operations, built a customer portal for real-time order tracking, and deployed IoT sensors for equipment monitoring. This digital backbone would prove crucial for managing complexity as they scaled.

Governance Changes and Professionalization

Quadria's impact went beyond capital. They brought governance changes that initially frustrated the founders but ultimately strengthened the company. Independent directors joined the board—a former FDA inspector, a McKinsey pharmaceutical practice leader, a CFO from a global CDMO.

Monthly board meetings replaced informal decision-making. Every capital allocation decision required business cases with ROI projections. Management information systems tracked KPIs the brothers had never measured—customer acquisition costs, capacity utilization by product category, return on regulatory investments.

The professionalization extended throughout the organization. Quadria mandated leadership training for middle management, implemented variable compensation linked to performance metrics, and created employee stock options—unusual for an unlisted Indian manufacturing company.

Preparing for Public Markets

From day one, Quadria's exit strategy was clear: IPO. But this wasn't a pump-and-dump play. They methodically prepared AKUMS for public markets over three years.

Financial reporting was overhauled. The company moved from Indian GAAP to Ind-AS, providing clearer pictures of revenue recognition and lease obligations. Related party transactions—common in family businesses—were unwound or conducted at arm's length. The brothers' compensation was benchmarked against listed peers.

The equity story was refined. AKUMS wasn't just a contract manufacturer but India's pharmaceutical infrastructure play. Marketing materials emphasized metrics public market investors valued: asset turns, return on capital employed, revenue visibility from long-term contracts.

By 2023, when IPO discussions began, AKUMS looked nothing like the family business Quadria had invested in. It was institutionalized, process-driven, and ready for public scrutiny. The transformation justified Quadria's returns but more importantly, positioned AKUMS for its next chapter.

VI. Product Innovation & Technology Platform

Inside AKUMS's R&D facility in Haridwar, a team of scientists huddles around a tablet that refuses to dissolve properly. It's supposed to release medication over exactly 12 hours—instead, it dumps 60% in the first two hours. This scene, repeated thousands of times across four R&D centers, represents AKUMS's evolution from manufacturer to innovation partner.

The 4,100 Formulation Portfolio

AKUMS has developed over 4,146 commercial formulations—a staggering number that requires context. Each formulation isn't just a recipe but a complex puzzle: matching drug release profiles, ensuring stability across temperature zones, achieving bioequivalence with originator drugs, all while maintaining cost competitiveness.

Consider their fixed-dose combination for diabetes—three different drugs with varying solubilities, combined in a single tablet that must release each component at specific rates. The development took 18 months, 200 prototype batches, and ₹3 crores in development costs. But once perfected, it became a ₹50 crore annual contract with guaranteed five-year revenues.

Complex Formulation Expertise

AKUMS specialized where others struggled. Extended-release formulations using matrix tablets, osmotic pumps, and multi-layered tablets. Each technology addressed specific challenges—matrix tablets for water-soluble drugs, osmotic pumps for precise zero-order release, multi-layered for combination products.

Their breakthrough came with abuse-deterrent formulations for opioid painkillers. As addiction crises sparked regulatory scrutiny globally, pharmaceutical companies needed formulations that couldn't be crushed and snorted or dissolved and injected. AKUMS developed tablets that turned into gel when crushed—maintaining therapeutic benefit while preventing abuse.

The technology platform extended beyond tablets. Their lyophilization (freeze-drying) capability enabled injectable antibiotics with three-year stability without refrigeration—crucial for developing markets with unreliable cold chains. Their hot-melt extrusion technology improved bioavailability of poorly soluble drugs by 400%.

Recent Launches and Market Response

2024 marked AKUMS's ambitious product launch calendar. New diabetes drugs targeting the GLP-1 pathway, competing with global blockbusters like Ozempic. Cardiovascular combinations reducing pill burden for elderly patients. Nutraceutical gummies targeting the wellness boom—vitamin D for urban professionals, omega-3 for children, probiotics for digestive health.

But the headline grabber was December 2024's European contract. AKUMS secured a EUR 200 million contract for supplying generic medications to European markets. This wasn't just about revenue—it validated AKUMS's ability to meet developed market quality standards and compete with established European CDMOs.

Technology Transfers and Regulatory Dossiers

The unsung hero of AKUMS's innovation platform was their regulatory expertise. Developing a formulation is worthless without regulatory approval. AKUMS built capabilities to prepare and file dossiers across jurisdictions—ANDA filings for the US, Marketing Authorizations for Europe, abbreviated submissions for emerging markets.

Their "dossier-ready" formulations became a unique selling proposition. Clients could license a formulation with completed stability studies, bioequivalence data, and draft regulatory filings. Time to market compressed from 24-30 months to 6-9 months. For generic companies racing to launch after patent expiries, this speed premium justified premium pricing.

Technology transfer became an art form. AKUMS developed protocols ensuring formulations manufactured in clients' facilities matched those from AKUMS's plants. They provided not just recipes but entire manufacturing ecosystems—equipment specifications, training programs, quality control methods. Some clients paid ₹10 crores just for transfer expertise, before any manufacturing contracts.

The Innovation vs. Manufacturing Balance

By 2024, AKUMS faced an existential question: Were they a manufacturing company with R&D capabilities or an innovation company with manufacturing assets? The distinction mattered for valuation multiples, talent acquisition, and strategic priorities.

The answer emerged from client feedback. Pure innovation companies lacked manufacturing expertise to scale products efficiently. Pure manufacturers couldn't solve complex formulation challenges. AKUMS occupied the sweet spot—enough innovation to differentiate, enough manufacturing to deliver.

This balance reflected in resource allocation. R&D received 3-4% of revenues—high for a CDMO but modest versus pure pharmaceutical companies. The focus remained practical innovation—solving specific client problems rather than blue-sky research. Every project required a committed client or clear market demand.

VII. The IPO Story & Public Market Debut (2024)

The boardroom at AKUMS's Mumbai office was tense on a humid July morning in 2024. Investment bankers from ICICI Securities, Axis Capital, Citigroup, and Ambit huddled over pricing models. The Indian equity markets were volatile, global interest rates remained elevated, and recent IPOs had delivered mixed results. After twenty years of building in relative obscurity, AKUMS was about to face the ultimate test: public market validation.

The IPO Architecture

The IPO size of ₹1,856.74 crores represented a delicate balance. Fresh issue of 1 crore shares aggregating to ₹680 crores and offer for sale of 1.73 crore shares aggregating to ₹1,176.74 crores. The fresh capital would fund expansion while the OFS provided partial exit to Quadria and liquidity to the founders without diluting control.

The price band decision revealed the tensions. Investment bankers pushed for ₹750-800, citing AKUMS's market leadership and growth potential. The founders wanted ₹600-650, fearing overpricing would hurt retail investors. They settled at ₹679 per share—aggressive enough to maximize proceeds, conservative enough to leave upside.

Subscription Dynamics: Reading the Market

The IPO opened on July 30, 2024, and closed on August 1, 2024. Those three days revealed Indian capital markets' appetite for pharmaceutical manufacturing plays. The subscription patterns told distinct stories.

Retail investors, attracted by AKUMS's domestic focus and understandable business model, subscribed 21.3 times in the retail category. They saw what institutions sometimes miss—a business serving products they consumed daily, backed by tangible manufacturing assets rather than ephemeral technology promises.

QIBs subscribed 90.09 times—the strongest institutional interest. Meetings with fund managers revealed their thesis: India's pharmaceutical CDMO industry would consolidate, AKUMS would be a consolidator, and manufacturing would return from China post-COVID supply chain disruptions.

The surprise was international interest. European funds, traditionally skeptical of Indian manufacturing stories, participated aggressively. AKUMS's December European contract had validated their global competitiveness. Japanese investors, understanding the value of manufacturing excellence, became anchor investors.

Anchor Investors: Smart Money Speaks

₹828.78 crore raised from anchor investors provided IPO momentum. The anchor book revealed sophisticated investors: Government of Singapore, Abu Dhabi Investment Authority, Nomura, HDFC Mutual Fund. These weren't momentum chasers but long-term investors who'd spent months evaluating AKUMS.

The anchor allocation process was revealing. AKUMS and their bankers spent two weeks in one-on-one meetings, addressing concerns about customer concentration, regulatory risks, and working capital requirements. By the end, they'd created believers who would provide price support post-listing.

Listing Day Drama

August 6, 2024. AKUMS's senior management gathered at the NSE, ready for the ceremonial bell ringing. But the real action was on trading screens. The stock opened at ₹725, a 6.77% premium—respectable but not spectacular.

The first hour saw wild swings—₹690 to ₹785—as different investor categories positioned. Retail investors who'd received allotments booked quick profits. Institutions accumulated on dips. By day's end, AKUMS had found its level, closing near ₹735, establishing a market capitalization over ₹10,000 crores.

Post-IPO Performance: Reality Meets Expectations

The months following listing tested AKUMS's public market readiness. The stock's volatility revealed the challenges of being a newly listed mid-cap in India's momentum-driven markets. Quarterly results became high-stakes events, with 10-15% moves on earnings days.

The first quarter post-IPO delivered mixed results. Revenue grew 5.08% year-on-year to ₹1,019.1 crore, while the company reported a net profit of ₹60.1 crore versus a loss of ₹188 crore in the prior year. Markets initially celebrated the turnaround but later questioned the modest growth rate.

Management's communication evolved rapidly. The Jain brothers, comfortable with private negotiations, had to master public earnings calls. Their initial presentations were dense with technical details. They learned to simplify—focusing on strategic initiatives, providing clear guidance, and acknowledging challenges transparently.

Use of IPO Proceeds: Execution Matters

AKUMS planned to use IPO proceeds for debt repayment, working capital, acquisitions, and general corporate purposes. The execution would determine whether the IPO created long-term value or just provided exit liquidity.

Debt repayment happened immediately, making the company almost debt free. This strengthened the balance sheet but also removed the discipline debt imposes. Working capital deployment was strategic—extending credit to large clients while tightening terms with smaller ones, effectively using capital to deepen important relationships.

The acquisition strategy remained work-in-progress. AKUMS evaluated several targets but remained disciplined on valuations. The public market's quarterly scrutiny conflicted with the patience required for transformative acquisitions. They chose to wait rather than overpay for mediocre assets.

VIII. Business Model Deep Dive

To truly understand AKUMS, you must understand how money flows through a CDMO. It's a business model that seems simple—take orders, manufacture products, deliver goods, collect payment—but the nuances determine whether you build an empire or remain a commodity supplier.

Revenue Model: The Three-Stream Architecture

AKUMS's revenue model operates on three interconnected streams, each with distinct economics and strategic importance. Manufacturing fees form the base—₹50-200 per thousand tablets depending on complexity. Volume-based pricing creates operating leverage; double the volume, increase costs by 60-70%. This scalability drives the push for larger contracts.

Development milestones represent the high-margin cream. A complex formulation commands ₹5-10 crores in development fees, paid in stages—signing, prototype approval, stability completion, regulatory filing. These upfront payments provide working capital for manufacturing while creating switching costs for clients.

The hidden third stream is regulatory maintenance—annual fees for keeping dossiers updated, managing variations, supporting client audits. While individually small (₹10-50 lakhs annually), across hundreds of products and dozens of clients, this creates ₹50+ crores of high-margin, recurring revenue that analysts often miss.

Customer Concentration: The Diversification Paradox

1,524 clients suggests broad diversification, but the reality is nuanced. The top 10 clients contribute 35-40% of revenues, the top 30 about 60%. This concentration seems risky until you understand the relationships.

AKUMS's largest client, contributing ₹400 crores annually, doesn't have a single contract. Instead, they have 50+ products, each with separate agreements, staggered renewals, and independent economics. Losing the "client" would require 50 separate failures—practically impossible given the switching costs.

The real moat is product-level stickiness. Once AKUMS manufactures a product for 2-3 years, switching becomes almost impossible. New stability studies, bioequivalence tests, regulatory variations—switching costs can exceed ₹5 crores per product. Multiply by dozens of products per client, and relationships become unbreakable.

The Working Capital Challenge

Poor sales growth of 11.3% over past five years partially reflects working capital constraints. CDMOs face a brutal cash conversion cycle—60 days for raw material procurement, 45 days for manufacturing, 30 days for quality testing, 90 days for payment. That's 225 days from cash out to cash in.

AKUMS managed this through sophisticated treasury operations. They negotiated supplier financing where banks paid vendors immediately while AKUMS settled after 90 days. Large clients received 120-day credit but paid 2% premiums. Smaller clients paid advances but received 5% discounts. These mechanisms freed up ₹300 crores in working capital.

The IPO transformed working capital dynamics. Debt-to-equity ratio improved to 0.25 times, and net debt decreased to ₹212.8 crore. With a stronger balance sheet, AKUMS could extend more credit to win large contracts while maintaining liquidity for operations.

Capital Efficiency: The Asset Turnover Game

Manufacturing businesses typically suffer from low asset turns—heavy machinery, large facilities, substantial inventory. AKUMS achieved 1.2x asset turnover, respectable for manufacturing but below the 2x+ that drives superior returns.

The key was capacity utilization optimization. Rather than running all facilities at 60%, AKUMS ran selected facilities at 85-90% while keeping others at 40-50% for surge capacity. High-utilization facilities handled stable, high-volume products. Low-utilization facilities managed complex, high-margin products where flexibility mattered more than efficiency.

Equipment strategy was equally sophisticated. Unlike many industry peers who purchased proven, depreciated equipment from developed markets to reduce capital intensity, AKUMS invested in state-of-the-art machinery from the outset. This contrarian approach—paying premium prices for the latest technology—reflected their long-term thinking: superior equipment meant better precision, lower rejection rates, and enhanced capability to manufacture complex formulations that justified the higher upfront investment.

The Profitability Challenge

Low return on equity of 13.3% over last 3 years reveals AKUMS's fundamental challenge. In a business requiring significant capital, generating only 13% returns barely exceeds cost of capital. The math is sobering—₹100 invested generates ₹13 in profits, from which taxes, reinvestment, and dividends must be paid.

Why accept such returns? Because the alternative is worse. Independent pharmaceutical manufacturing without assured orders means 40-50% capacity utilization and negative returns. AKUMS chose steady, modest returns over volatile, potentially higher returns.

The path to improved returns isn't through pricing—competition limits that—but through mix enhancement. Complex formulations generate 25-30% EBITDA margins versus 10-15% for simple tablets. Developed market exports command 2x prices for identical products. The European contract represents this strategy—same manufacturing, double the margins.

Competitive Advantages: Beyond Scale

Scale alone doesn't explain AKUMS's dominance. 30.2% market share creates advantages, but sustainable moats require more.

Regulatory approvals represent the first moat. With certifications from 15+ countries, AKUMS can manufacture products for any geography. Competitors might match individual certifications, but replicating the entire portfolio requires years and crores in investment.

The second moat is tacit knowledge—thousands of small optimizations accumulated over two decades. The optimal mixing time for a specific excipient, the precise temperature for coating adhesion, the humidity level preventing degradation. This knowledge, undocumented and embedded in personnel, can't be replicated by hiring consultants or buying equipment.

The third moat is relationship capital. When a client's product fails stability testing, AKUMS's scientists work nights to identify root causes. When raw material shortages threaten supply, AKUMS leverages vendor relationships to secure allocation. These crisis interventions, repeated over years, create trust that transcends commercial relationships.

IX. Competition & Market Position

The Indian CDMO landscape resembles a pyramid. At the apex sit 4-5 players including AKUMS, controlling 60% of the organized market. The middle holds 20-30 regional players, competent but limited in scope. The base contains hundreds of small units, often operating at regulatory margins, serving local markets. Understanding AKUMS's position requires dissecting each competitive layer.

The Apex Predators

AKUMS's true competition comes from a select few. Dishman Carbogen Amcis, backed by private equity, focuses on complex APIs and advanced intermediates. Their Swiss acquisition brought European credibility but also European cost structures. They compete for global innovator contracts where margins justify their premium pricing.

Jubilant Life Sciences spans the value chain from APIs to formulations to contract research. This integration creates synergies but also complexity. Their life sciences division competes directly with AKUMS but often loses flexibility battles—their integrated model means prioritizing internal API usage even when external sources are cheaper.

Piramal Pharma Solutions plays at the premium end—sterile injectables, antibody-drug conjugates, highly potent APIs. They don't compete for routine tablet manufacturing but cherry-pick high-value, complex projects. Their Canadian and UK facilities access developed markets but carry developed market costs.

Syngene, Biocon's contract research arm, increasingly moves downstream into manufacturing. Their strength in biologics and biosimilars represents future competition as AKUMS builds biological capabilities. But their research DNA sometimes conflicts with manufacturing efficiency requirements.

AKUMS's Differentiation: The India Focus

While competitors chase global markets and dollar revenues, AKUMS made a contrarian bet—dominate India first. This wasn't lack of ambition but strategic clarity. As the largest India-focused CDMO, they understood that India's ₹50 billion domestic market, growing at 10-12% annually, offered more sustainable opportunities than competing for commoditized global contracts.

This India focus created unique advantages. Regulatory requirements, while stringent, were familiar. Client relationships could be managed face-to-face rather than across time zones. Payment terms, while extended, were in rupees without currency risk. Most importantly, AKUMS understood Indian market dynamics—the importance of relationships, the flexibility required, the price-quality tradeoffs.

Market Share Dynamics

AKUMS's 30.2% market share of the Indian domestic CDMO market by value, increased from 26.7% in FY21. This 350 basis point gain over three years represents massive market share capture in a fragmented industry. But the dynamics behind this growth are more interesting than the numbers.

AKUMS didn't steal share from apex competitors—those relationships are too sticky. Instead, they absorbed the middle market. As regulatory requirements tightened, mid-sized CDMOs faced a choice: invest crores in compliance or exit. Many chose exit, selling client relationships to AKUMS or simply shutting down, pushing clients to seek alternatives.

The COVID-19 pandemic accelerated consolidation. Smaller CDMOs couldn't manage supply chain disruptions, worker shortages, and demand volatility. AKUMS, with its scale and balance sheet, provided stability. Clients who'd diversified across multiple small CDMOs consolidated with AKUMS for supply security.

The In-House Manufacturing Threat

The greatest competitive threat isn't other CDMOs but clients building internal capacity. As Indian pharmaceutical companies grow, some question outsourcing economics. Why pay CDMO margins when you can manufacture internally?

AKUMS's defense is subtle but effective. They make insourcing appear expensive and risky. When clients consider internal manufacturing, AKUMS provides total cost analyses including hidden expenses—quality personnel, regulatory maintenance, capacity underutilization during demand troughs. The numbers invariably favor outsourcing.

More strategically, AKUMS deepens integration with clients' operations. They place employees at client facilities, integrate IT systems for real-time inventory management, and customize packaging lines for client-specific requirements. This operational mesh makes separation increasingly difficult.

International Expansion Opportunities

While India-focused historically, AKUMS recognizes international expansion's inevitability. But rather than competing head-on with global CDMOs in their markets, AKUMS targets specific niches.

The European contract represents this strategy. Rather than building European facilities with European cost structures, AKUMS leverages India's cost advantage for price-sensitive generic products. European companies, facing margin pressure, outsource to India for 40-50% cost savings while maintaining quality.

The US market requires different tactics. FDA inspections are rigorous, competition is intense, and pricing pressure is severe. AKUMS targets complex generics—abuse-deterrent formulations, extended-release products, difficult-to-manufacture tablets—where technical capability matters more than pure cost.

China Dependency and Supply Chain Risks

Supply chain disruptions from China could affect raw material availability. Like all Indian pharmaceutical companies, AKUMS depends on China for Active Pharmaceutical Ingredients (APIs) and key starting materials (KSMs). This dependency, exposed during COVID-19, represents strategic vulnerability.

AKUMS's response is pragmatic rather than idealistic. Complete independence from China is impossible—they dominate certain chemical intermediates. Instead, AKUMS builds strategic inventory, diversifies suppliers within China, and develops alternative sources for critical materials.

The government's Production Linked Incentive (PLI) scheme for APIs creates opportunities. AKUMS partnered with API manufacturers building capacity under PLI, providing assured offtake in exchange for supply security. These partnerships reduce China dependency while supporting India's API ambitions.

X. Playbook: Business & Investing Lessons

Every successful business teaches lessons beyond its specific industry. AKUMS's journey from a Haridwar startup to India's CDMO leader offers insights applicable across B2B manufacturing, regulated industries, and capital-intensive businesses. These aren't theoretical frameworks but battle-tested principles forged through two decades of execution.

Building Trust in a Trust-Deficit Industry

Pharmaceutical manufacturing operates on a trust paradox. Mistakes can kill people, destroy brands, and trigger regulatory bans. Yet the industry relies on outsourcing to third parties operating outside direct control. AKUMS solved this paradox through radical transparency.

They installed cameras in production areas, providing clients live feeds. Monthly quality scorecards detailed every deviation, investigation, and corrective action. They invited clients to witness batch manufacturing, turning production into performance. This transparency initially felt risky—exposing problems competitors would hide—but created unshakeable trust.

The lesson extends beyond pharma: in trust-deficit industries, transparency becomes competitive advantage. Hiding problems destroys trust instantly; acknowledging and fixing problems builds trust gradually. AKUMS chose the harder but sustainable path.

The Power of Focus: Domestic Market Over Global Ambitions

While competitors chased global markets and dollar revenues, AKUMS focused on India. This wasn't small thinking but strategic clarity. They understood that dominating a growing home market beats being subscale globally.

The India focus created compound advantages. Regulatory expertise deepened through repetition. Client relationships strengthened through proximity. Market understanding sharpened through immersion. By the time AKUMS looked internationally, they had an impregnable home base funding expansion.

The broader lesson: geographic focus beats geographic spread until you achieve local dominance. Expanding prematurely dilutes resources, splits attention, and prevents building deep competitive advantages. AKUMS proved that owning 30% of India beats owning 0.3% of the world.

Scale as Moat: Manufacturing Complexity and Regulatory Barriers

AKUMS's moat isn't a single barrier but layered defenses. 49.23 billion units production capacity seems replicable—anyone can buy equipment. But scale creates complexity that becomes its own barrier.

Managing 1,500+ clients requires sophisticated planning systems. Manufacturing 4,100+ products demands flexible operations. Maintaining 15+ regulatory certifications needs specialized expertise. Each element seems manageable individually; together, they create overwhelming complexity that deters competition.

The investment lesson is counterintuitive: sometimes, complexity creates value. While investors typically prefer simple businesses, complex operations that are well-managed become unassailable. AKUMS turned operational complexity into competitive advantage.

Customer Acquisition in B2B: Relationship-Driven Sales

AKUMS's sales strategy contradicts conventional wisdom. No aggressive sales teams, minimal marketing spend, few conference sponsorships. Instead, they built relationships through consistent execution, crisis support, and technical excellence.

Their customer acquisition cost is essentially zero—clients approach them based on reputation. But this wasn't accidental. Every successful project became a reference. Every crisis resolved became a testimonial. Every technical challenge solved became marketing. Performance became promotion.

For B2B businesses, AKUMS demonstrates that product excellence beats sales excellence. In industries where switching costs are high and mistakes are costly, reputation travels faster than salespeople. Investing in delivery beats investing in distribution.

Managing Working Capital in Manufacturing

Cash flow from operations increased to ₹4,983 million in FY24 from ₹1,766 million in FY23—a 182% increase demonstrating working capital mastery. AKUMS achieved this through financial engineering that would impress investment banks.

They tiered clients by payment reliability, offering discounts for advances and charging premiums for extended credit. They negotiated supplier financing where banks paid vendors while AKUMS retained payment flexibility. They converted fixed costs to variable through contract manufacturing arrangements for overflow capacity.

The lesson for capital-intensive businesses: working capital management determines survival. Growth without cash generation is suicide. AKUMS proved that modest growth with strong cash generation beats aggressive growth with cash consumption.

The IPO Timing Decision: Growth Capital vs. Liquidity Event

AKUMS waited twenty years for their IPO—unusual in an era of rapid listings. The timing reveals sophisticated thinking about public markets. They went public not when they needed capital (2008-2010) but when they could command premium valuations (2024).

By 2024, they had scale, profitability, and market leadership. The equity story was clear, metrics were strong, and growth visibility extended years. ₹828.78 crore from anchor investors validated institutional appetite. The IPO provided growth capital at attractive valuations rather than survival capital at distressed prices.

For entrepreneurs, AKUMS demonstrates patience's value. Going public prematurely locks in low valuations and creates quarterly pressure before business models mature. Waiting until dominance is established maximizes value creation for existing shareholders.

Founder Control Post-IPO

Promoter holding of 75.3% post-IPO reflects careful dilution management. The Jain brothers maintained control while accessing public markets. This wasn't ego but strategic necessity. Pharmaceutical manufacturing requires long-term thinking incompatible with quarterly activism.

They structured the IPO to minimize dilution—fresh issue limited to growth requirements, OFS primarily from private equity rather than founders. They created differential voting rights ensuring operational control regardless of economic ownership. They aligned management compensation with long-term value creation rather than short-term stock prices.

The governance lesson: maintaining founder control post-IPO requires advance planning. Once public, changing structures becomes difficult. AKUMS designed governance for the public markets they wanted rather than accepting standard templates.

XI. Analysis & Bear vs. Bull Case

Every investment thesis contains opposing narratives—the bull case of unlimited potential and the bear case of hidden risks. AKUMS embodies this duality: undeniable strengths shadowed by structural challenges. Understanding both perspectives reveals whether this is a compounder or value trap.

Bull Case: The India Pharma Infrastructure Play

The optimistic narrative starts with India's pharmaceutical destiny. From $50 billion today to $130 billion by 2030—a 17% CAGR that will create massive manufacturing demand. AKUMS, with 30.2% market share, captures disproportionate growth through scale advantages.

Global supply chain diversification accelerates this thesis. Post-COVID, pharmaceutical companies recognize concentration risks in China. India, with established capabilities and democratic governance, becomes the natural alternative. AKUMS benefits whether clients are Indian companies growing domestically or global companies diversifying supply.

The regulatory moat strengthens over time. As quality requirements tighten globally, smaller CDMOs exit, unable to afford compliance investments. AKUMS, already compliant across major markets, absorbs their clients. Consolidation isn't aspiration but mathematical inevitability.

The EUR 200 million European contract validates international competitiveness. If AKUMS can compete in Europe's quality-obsessed, price-sensitive markets, they can compete anywhere. This single contract could catalyze broader European expansion, multiplying addressable markets.

The balance sheet provides firepower. Almost debt free with debt-to-equity at 0.25 times, AKUMS can fund expansion through internal accruals. No dilution, no interest burden, no covenant restrictions. This financial flexibility enables opportunistic acquisitions when competitors struggle.

Technology transitions favor established players. Biological drugs, continuous manufacturing, personalized medicine—each requires massive investments that only scaled players can afford. AKUMS's size enables technology adoption that smaller competitors can't match.

Bear Case: The Structural Challenges

The pessimistic narrative begins with poor sales growth of 11.3% over past five years. In an industry supposedly booming, why is AKUMS growing barely above inflation? The answer reveals structural headwinds.

Geographic concentration in Uttarakhand exposes operational risks. Natural disasters, infrastructure failures, or regulatory changes in a single state could cripple operations. The 2013 floods demonstrated this vulnerability. Climate change makes such events more likely, not less.

Customer concentration remains concerning despite diversification claims. The top 30 clients drive 60% of revenues. These aren't equal partnerships—large pharmaceutical companies have negotiating leverage AKUMS can't match. Margin pressure is constant, price increases difficult, and contract terms increasingly unfavorable.

Return on equity of 13.3% barely exceeds cost of capital. In a capital-intensive business requiring continuous investment, these returns don't create wealth. The stock market values growth, but growth without returns destroys value. AKUMS risks becoming a value trap—optically cheap but structurally challenged.

China dependency undermines the independence narrative. Supply chain disruptions from China could affect raw material availability. Without Chinese APIs, Indian pharmaceutical manufacturing stops. This dependency gives China leverage over Indian companies, including AKUMS.

Competition from global CDMOs intensifies as they enter India. Catalent, Lonza, and Recipharm bring advanced technologies, global relationships, and deep pockets. They'll target AKUMS's most profitable clients and products, forcing price competition AKUMS might not survive.

The innovation deficit becomes apparent comparing R&D spending. At 3-4% of sales, AKUMS invests less than half what global CDMOs spend. In a technology-driven future, this underinvestment could prove fatal. Biosimilars, cell therapies, mRNA vaccines—AKUMS lacks capabilities in pharma's fastest-growing segments.

The Balanced View: Steady Compounder or Cyclical Play?

Reality lies between extremes. AKUMS isn't the explosive growth story bulls imagine nor the value trap bears fear. It's a steady, cyclical business with defensive characteristics but limited pricing power.

The business model generates predictable cash flows—contracted revenues, sticky customers, recurring maintenance fees. This predictability justifies premium valuations versus manufacturing peers. But growth depends on industry cycles, regulatory changes, and competitive dynamics outside management control.

The European expansion represents genuine optionality. Success could transform AKUMS from Indian CDMO to global player, justifying much higher valuations. Failure wouldn't destroy the existing business but would cap growth potential. This asymmetric risk-reward appeals to certain investors.

The consolidation opportunity is real but execution-dependent. AKUMS has capital and platform to acquire smaller CDMOs, but integration challenges are severe. Manufacturing cultures, quality systems, and client relationships don't merge easily. Serial acquisition strategies often destroy more value than they create.

XII. Future Strategy & "If We Were CEOs"

Standing at the intersection of opportunity and challenge, AKUMS faces strategic decisions that will determine whether they become India's pharmaceutical infrastructure backbone or remain a successful but limited regional player. If we were running AKUMS, here's the playbook we'd execute.

International Expansion: The Europe Opportunity

The EUR 200 million European contract isn't just revenue—it's a beachhead. Europe represents the perfect international market: quality-conscious validating Indian capabilities, price-sensitive enabling competitive positioning, and fragmented offering consolidation opportunities.

We'd establish a European subsidiary, not for manufacturing but for regulatory and commercial presence. Hire former EMA inspectors as consultants, building deep regulatory expertise. Partner with regional distributors understanding local dynamics. Most importantly, focus on Eastern Europe where cost sensitivity is highest and competition from established CDMOs weakest.

The strategy wouldn't be broad expansion but surgical strikes. Target specific therapeutic areas—diabetes, cardiovascular, antibiotics—where Indian expertise is established. Win 2-3 anchor clients in each country, then expand within their portfolios. Build density before breadth.

Biologics and Complex Injectables: The Next Frontier

Small molecule drugs are yesterday's battlefield. Tomorrow belongs to biologics—proteins, antibodies, cell therapies. AKUMS must enter this space or risk irrelevance as pharmaceutical innovation shifts toward biological medicines.

But we wouldn't build from scratch. Acquire a small biosimilar CDMO, gaining technology and expertise instantly. India has several subscale players with good science but poor commercial execution. A ₹500 crore acquisition could provide capabilities worth ₹2,000 crores to build independently.

Focus initially on simple biologics—insulin, growth hormones, interferons. These have established manufacturing processes and large markets. Build expertise gradually before attempting complex monoclonal antibodies or cell therapies. Partner with global biosimilar companies for technology transfer and validation.

Digital Transformation in Manufacturing

Pharmaceutical manufacturing remains surprisingly analog. Paper batch records, manual quality checks, and human-dependent processes. Digital transformation isn't just efficiency—it's competitive differentiation.

Implement real-time manufacturing analytics using IoT sensors. Every tablet press, every reactor, every packaging line continuously transmitting data. Machine learning algorithms detecting deviations before they become defects. Predictive maintenance preventing breakdowns. This digital infrastructure becomes a selling point for quality-conscious clients.

Create a client portal providing unprecedented transparency. Real-time batch tracking, quality metrics, inventory levels, and delivery schedules. Make AKUMS's operations their clients' control tower. This digital integration increases switching costs while improving customer satisfaction.

Backward Integration into APIs

China dependency is strategic vulnerability. While complete independence is impossible, selective backward integration reduces risk while potentially improving margins. But we'd be surgical, not broad.

Focus on APIs for AKUMS's highest-volume products where supply security matters most. Build capacity under the government's PLI scheme, accessing subsidies while maintaining capital efficiency. Partner with technology providers for process development rather than reinventing established chemistry.

More importantly, create an API trading desk. AKUMS's scale provides purchasing power individual clients lack. Aggregate demand, negotiate better prices, and manage inventory centrally. This transforms procurement from cost center to profit center.

M&A Strategy: Consolidating Smaller CDMOs

India has 200+ small CDMOs struggling with compliance costs and working capital. Many are technically competent but commercially challenged. This fragmentation represents consolidation opportunity if executed correctly.

We'd create an acquisition vehicle separate from AKUMS—"AKUMS Ventures"—acquiring distressed CDMOs at attractive valuations. Integrate their client relationships and technical capabilities into AKUMS's platform while shutting redundant facilities. Each acquisition brings new clients, products, and expertise.

The key is discipline. Pay maximum 5x EBITDA, focus on complementary capabilities rather than competing assets, and integrate rapidly rather than maintaining independence. Cultural integration matters more than financial integration—AKUMS's quality culture must permeate acquired entities immediately.

Sustainability Initiatives and ESG Considerations

ESG isn't compliance burden but competitive advantage. Pharmaceutical manufacturing is inherently polluting—solvents, waste water, emissions. Companies demonstrating environmental leadership attract premium valuations and preferential treatment from global clients.

Invest in green chemistry—enzymatic processes replacing chemical synthesis, water recycling systems, and solar power generation. These require upfront investment but reduce operating costs while building reputation. Target becoming India's first carbon-neutral CDMO by 2030.

Create social impact through local employment and skill development. AKUMS's facilities in Uttarakhand and Himachal Pradesh can become talent development centers, training pharmacy graduates in industrial manufacturing. This builds government goodwill while creating loyal talent pipeline.

Building Branded Formulations vs. Pure CDMO Play

The eternal temptation—why manufacture for others when you can build brands? We'd resist this temptation but create a middle path. Launch brands in markets where AKUMS doesn't compete with clients.

Focus on export markets—Africa, Southeast Asia, Latin America—where Indian companies have limited presence. Build a portfolio of generic brands in chronic therapies providing recurring revenues. Keep this business separate from CDMO operations, preventing channel conflict.

More interestingly, create a "powered by AKUMS" ingredient brand. Like "Intel Inside" for computers, establish AKUMS as quality assurance for pharmaceutical products. Clients could use this branding to differentiate their products while AKUMS builds consumer recognition without competing.

XIII. Recent News

The AKUMS story continues evolving rapidly post-IPO. Recent developments reveal management's execution against strategic priorities while highlighting emerging challenges and opportunities.

Q3 FY25 Results: Mixed Signals

Net profit fell 66.35% year-on-year to ₹65.18 crore in Q3 2024-25, sending shock waves through investor community. But the headline obscured nuanced reality. The previous year included one-time gains from subsidiary sales. Adjusted for extraordinaries, operational performance remained steady.

More concerning was volume growth deceleration. While revenues grew nominally, pricing pressure intensified. Generic drug prices in India fell 5-8% annually as competition increased and government regulations tightened. AKUMS offset through mix improvement—shifting toward complex formulations—but this transition takes time.

European Contract Progress

The December 2024 European contract progressed from announcement to execution. Initial shipments began in January 2025, with client feedback positive on quality and delivery reliability. This early success positions AKUMS for follow-on contracts with the same client and credentials for approaching other European companies.

Management guided for ₹400 crores annual revenue from European operations by FY27, representing 8-10% of total sales. While modest initially, European revenues carry 2x margins of domestic business, making profit impact disproportionate.

Manufacturing Expansion Updates

New facilities in Jammu requiring ₹265 crore total investment for pharmaceutical and nutraceutical products. This expansion addresses capacity constraints while diversifying geographic risk beyond Uttarakhand concentration.

The Jammu facilities incorporate learnings from existing plants—modular design enabling rapid reconfiguration, digital infrastructure from day one, and sustainability features including zero liquid discharge. These greenfield facilities achieve 20-30% better efficiency than legacy plants.

Regulatory Achievements and Inspections

AKUMS cleared USFDA inspection of their Haridwar facility with zero critical observations—remarkable for Indian CDMOs facing increased FDA scrutiny. This successful inspection enables expanded US exports and validates quality systems.

Brazilian ANVISA approval opened Latin American markets, a geography AKUMS previously ignored. Latin America's growing middle class and expanding healthcare coverage create opportunities for generic medications where AKUMS's cost advantage resonates.

Management Commentary and Guidance

Sanjeev Jain emphasized establishing AKUMS's global CDMO footprint while maintaining focus on innovative products and profitable growth. This balanced message—growth with profitability—resonated with investors tired of growth-at-any-cost narratives.

FY25 guidance remained conservative—15-18% revenue growth, 13-14% EBITDA margins, and capex of ₹300 crores. This guidance implies acceleration from current run rates, depending on European contract ramp-up and domestic market recovery.

Strategic Partnerships and Collaborations

AKUMS signed a Memorandum with Tamil Nadu Agricultural University for R&D in agri-based pharmaceutical formulations. This unexpected partnership targets plant-based APIs and natural excipients, addressing sustainability concerns while potentially reducing China dependency.

Collaboration with Indian Institute of Technology (IIT) Delhi on continuous manufacturing technology could revolutionize production economics. Continuous manufacturing reduces batch variability, improves efficiency, and enables real-time quality control—advantages worth the development investment.

Analyst Coverage and Recommendations

100% of analysts recommend 'BUY' rating with average target price of ₹750. This unusual unanimity reflects consensus about AKUMS's long-term potential despite near-term challenges. Analysts cite European expansion, operational improvements, and consolidation opportunities as value drivers.

Institutional ownership increased post-IPO as index inclusion drove passive flows. Foreign institutional investors, initially skeptical, gradually accumulated positions as quarterly results demonstrated execution capability. This broadening shareholder base reduces volatility while improving valuations.

Market Share and Competitive Updates

Recent industry data confirmed AKUMS maintained market leadership despite intensifying competition. Smaller CDMOs continued exiting, unable to manage regulatory compliance costs and working capital requirements. AKUMS captured disproportionate share of orphaned clients, strengthening market position.

Global CDMOs' India entry proceeded slower than expected. Regulatory complexities, price expectations, and cultural differences created friction. Their focus on premium segments left AKUMS's mass market position largely unthreatened, validating the domestic focus strategy.

The AKUMS story represents more than a business success—it's a blueprint for building industrial champions in emerging markets. From humble beginnings in Haridwar to ₹7,675 crore market capitalization, the journey demonstrates that manufacturing excellence, customer focus, and patient capital allocation create enduring value even in commoditized industries.

As India aspires to become the world's pharmacy, AKUMS stands ready to provide the manufacturing backbone this ambition requires. Whether they successfully navigate international expansion, technology transitions, and competitive pressures will determine if this backbone becomes the foundation for global pharmaceutical leadership or remains a regional success story. For investors, entrepreneurs, and industry observers, AKUMS offers lessons in building trust, scaling operations, and creating value in unexpected places.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube