Gland Pharma: The Injectable Empire from Hyderabad

I. Introduction & Episode Roadmap

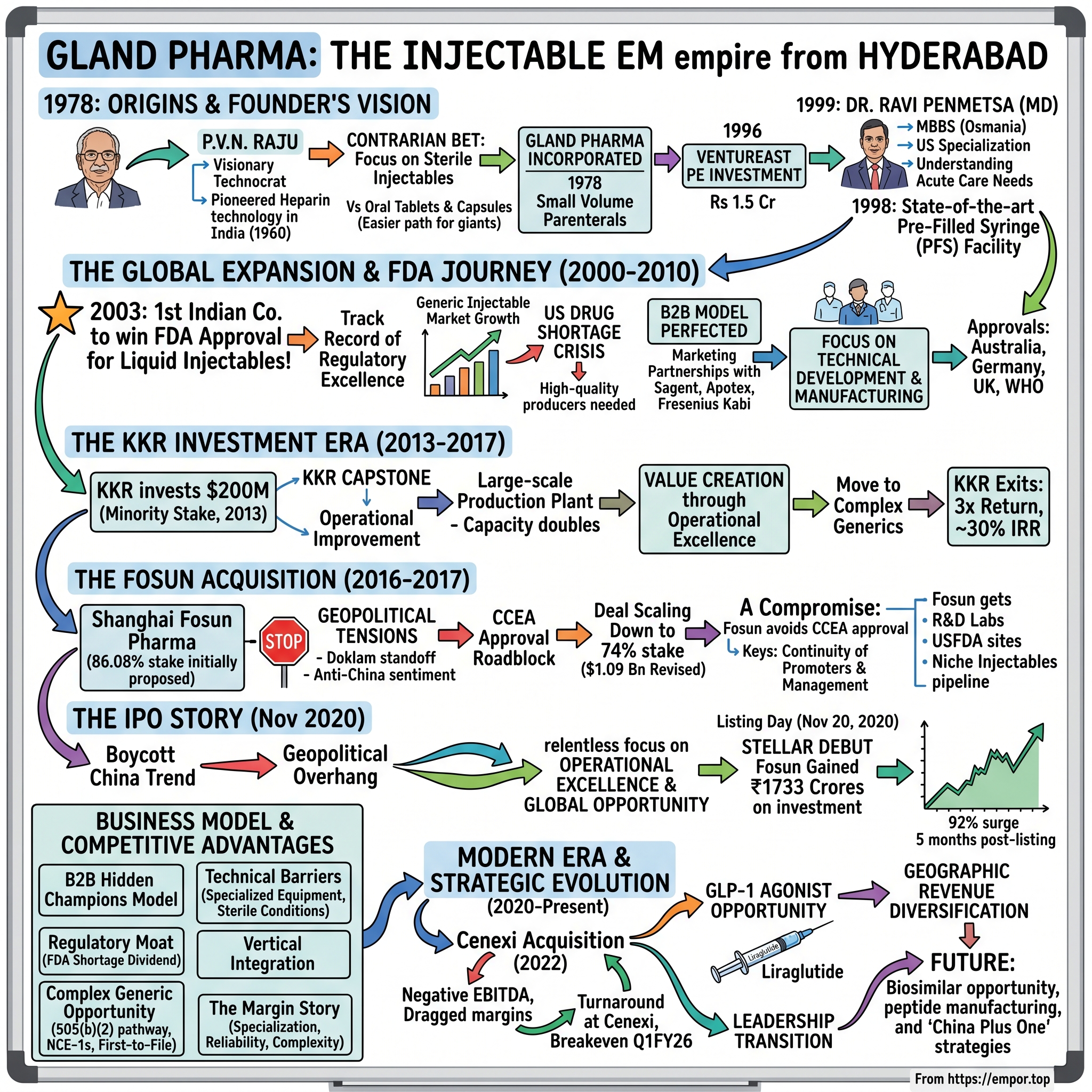

Picture the outskirts of Hyderabad in 1978. The air is thick with the promise of a new India—a nation just beginning to shake off decades of socialist stagnation. In a modest facility, a chemist named P.V.N. Raju is mixing compounds, not in pursuit of blockbuster drugs that would capture headlines, but something far more technical: sterile liquid injectables. While pharmaceutical giants chased the easier path of oral tablets and capsules, Raju saw opportunity in complexity itself—in the vials, ampoules, and syringes that most Indian companies wouldn't touch.

Forty-six years later, this contrarian bet has transformed into one of the most remarkable pharmaceutical stories you've likely never heard of: Gland Pharma, established in 1978 by PVN Raju, has evolved from a contract manufacturer of small volume liquid parenteral products to become one of the largest and fastest-growing generic injectable-focused companies with a global footprint across 60 countries.

Here's the question that should grab any investor's attention: How did a family-run injectable maker from Hyderabad become the vehicle for the largest takeover of an Indian pharma giant by a Chinese company? And perhaps more intriguingly, why would a company list on the NSE and BSE on November 20, 2020—right in the middle of anti-China sentiment sweeping across India—and still manage to deliver a stellar listing performance?

This is not your typical pharmaceutical success story. It's a tale of technical mastery over marketing muscle, of choosing the hardest path when everyone else was taking shortcuts, of a father-son duo who built a business so specialized that when private equity came knocking, they brought not just capital but genuine operational expertise. It's about becoming the first Indian company to win FDA approval for a liquid injectable in 2003—a credential that would prove to be worth its weight in gold.

What unfolds over the next several hours is a masterclass in focus. While Indian pharma was busy becoming the "pharmacy of the world" through generic oral solids, Gland was quietly mastering the art of sterile manufacturing. While others expanded horizontally into every therapeutic area imaginable, Gland went deep into injectables. And while most Indian companies struggled with FDA inspections, Gland's facility received USFDA acceptance in 2003, another first in India, establishing a track record of regulatory excellence that continues to this day.

But this isn't just a story of operational excellence. It's a financial engineering saga that would make any PE investor salivate: KKR, which invested $200 million in Gland Pharma in 2013, made a return of more than three times and an internal rate of return (IRR) of nearly 30%. It's a geopolitical thriller where the Chinese firm had to scale down its proposed acquisition in Gland Pharma to 74 per cent stake at a valuation of not more than $1.09 billion after regulatory pushback. And it's a public markets phenomenon where Fosun gained ₹1733 Crores on their investment through the IPO alone.

What you're about to discover is how a company built on the unglamorous foundation of contract manufacturing transformed itself into a strategic asset so valuable that it commanded premium valuations even when Chinese ownership was a liability. You'll understand why in the US alone, over 20 billion injectable drugs are expected to expire in next 5-6 years, creating an opportunity that Gland is uniquely positioned to capture. And you'll see how the company's Q1 FY26 revenue stood at ₹1,505.6 crore, up 7% from ₹1,401.7 crore in Q1 FY25, with Cenexi achieving breakeven with €0.9 million (₹86 million) in Q1FY26, signaling that even their troubled European acquisition is turning around.

II. Origins & The Founder's Vision (1978-2000)

The story begins not with Gland Pharma itself, but with a man whose understanding of complex molecules would reshape India's pharmaceutical landscape. P.V.N. Raju, a Graduate in Chemistry from the Presidency College of Madras and a Post Graduate from the Indian Institute of Chemists, received training at Evans Medical in the UK and Pharmacia in Sweden, before starting Gland Chemicals in 1974 and Gland Pharma in 1978. The visionary technocrat pioneered Heparin technology in India in 1960.

Think about that timeline for a moment. While India was still finding its feet post-independence, Raju was already mastering one of the most complex pharmaceutical molecules—Heparin, an anticoagulant derived from biological sources that requires extraordinary precision to manufacture. This wasn't a man chasing quick profits in simple generics; this was someone who understood that complexity creates moats.

The decision to focus on injectables in 1978 was either brilliantly prescient or foolishly ambitious. India's pharmaceutical industry was still in its infancy, protected by process patents that allowed reverse engineering but struggling with quality standards that would satisfy global regulators. Most companies were content making tablets and capsules—solid oral dosage forms that were simpler to manufacture, easier to transport, and faced less stringent regulatory scrutiny.

But Raju saw what others missed. Injectable drugs bypass the digestive system, delivering medication directly into the bloodstream. They're essential in hospitals, critical in emergencies, and irreplaceable in many therapeutic protocols. The catch? Manufacturing them requires sterile conditions that make a semiconductor clean room look casual by comparison. One contamination incident could kill patients and destroy a company overnight.

Gland Pharma was incorporated in 1978, but took off in 1996 following an investment of Rs 1.5 crore by private equity investor Ventureast. The company had just touched sales of Rs 2.5 crore when Sarath Naru, the Managing Partner of Ventureast, was impressed by the approach of its founders. "One, Gland's manufacturing capability in small volume parenterals was impressive. Two, the founders were extremely hung up on quality and execution. It was the first company to get an SPV facility approved by the US FDA in India."

This early PE investment is crucial to understanding Gland's DNA. Unlike many family businesses that viewed external capital with suspicion, Raju embraced sophisticated investors who could provide not just money but credibility. Ventureast wasn't just writing checks; they were validating a vision.

The 1990s marked a critical inflection point. As Managing Director, the younger generation brought a unique blend of medical training and business acumen to the company. After obtaining his MBBS degree from Osmania University (India), Dr Ravi specialized in Science of Medicine from East Carolina University School of Medicine (USA). After seven years' hospital-based practice there, he joined Gland Pharma as its Executive Director in 1992. Assuming the mantle of the company's Managing Director in 1999, Dr Ravi spearheaded its rapid, multi-dimensional growth over the next two decades.

This wasn't your typical second-generation story of an heir reluctantly joining the family business. Dr. Ravi Penmetsa had spent seven years practicing medicine in the United States, understanding firsthand how critical injectable medicines were in acute care settings. He'd seen the quality standards that American hospitals demanded and knew that if Gland could meet those standards, the opportunity was massive.

The late 1990s saw two strategic moves that would define Gland's future. First, the company set up the country's first state-of-the-art Pre-Filled Syringe (PFS) facility for LMWHs in 1998. Pre-filled syringes were a game-changer—they reduced dosing errors, minimized contamination risk, and improved patient convenience. But they required sophisticated technology and significant capital investment. Most Indian companies wouldn't attempt this for another decade.

Second, and more importantly, Gland began preparing for what would become its defining achievement: US FDA approval. The company understood that regulatory excellence wasn't just about compliance—it was about building systems and cultures that made quality inevitable rather than aspirational. Every standard operating procedure, every quality control checkpoint, every training program was designed with one goal: to meet the standards of the world's toughest regulator.

By 2000, Gland had built something unique in Indian pharma: a specialized capability in complex injectables backed by world-class manufacturing infrastructure. Revenue was still modest, the company was still largely unknown outside industry circles, but the foundation was set. The next phase would test whether this foundation could support global ambitions.

III. The Global Expansion & FDA Journey (2000-2010)

The morning of 2003 changed everything. When Gland Pharma became the first Indian company to win FDA approval for a liquid injectable in 2003, the drug shortage problem was in its infancy. Over the past decade, a FDA crackdown on sterile injectables has escalated the issue, creating opportunities for high-quality producers of these complex products. In 2003, Gland Pharma was the first company in India to get US Food and Drug Administration (FDA) approval for pharmaceutical liquid injectable products.

This wasn't just another regulatory approval—it was a paradigm shift. To understand its significance, consider the context: Indian pharmaceutical companies had been getting FDA approvals for oral solid dosage forms since the 1980s, but injectables were a different beast entirely. The sterility requirements, the particulate matter controls, the endotoxin testing—every aspect was exponentially more complex.

Dr. Ravi Penmetsa, now firmly at the helm as Managing Director, understood that this FDA approval was not a destination but a launching pad. The US generic injectables market was dominated by a handful of players, and quality issues were beginning to surface at established suppliers. The U.S. has struggled with shortages of products in these classes in recent years, in part because the FDA has found fault with quality standards at leading suppliers such as Hospira. When the number of new shortages of medically necessary drugs peaked in 2011, the FDA calculated 73% of affected products were sterile injectables.

The company's approach to the US market was methodical rather than aggressive. Instead of trying to compete across the entire spectrum of injectable products, Gland focused on specific molecules where it could leverage its technical expertise. Heparin, which P.V.N. Raju had pioneered in India decades earlier, became the spearhead product. Having pioneered Heparin technology in India, Gland Pharma has a strong position in the US market for that product through its marketing partnerships.

But here's where Gland's strategy diverged from typical Indian pharma playbooks. Rather than building its own sales force in the US—an expensive and risky proposition—the company perfected the B2B model. We operate primarily under a business to business (B2B) model and have an excellent track record in the pharmaceutical research and development, manufacturing and marketing of complex injectables. They would develop products, file applications, manufacture to the highest standards, but let established players handle the last-mile distribution.

This B2B approach had multiple advantages. First, it required significantly less capital than building a consumer-facing brand. Second, it allowed Gland to focus on what it did best—technical development and manufacturing excellence. Third, it de-risked the business by spreading sales across multiple partners rather than depending on direct market success.

The numbers tell the story of rapid scaling. While we don't have precise revenue figures for this period, we know that according to Fosun's filing, Gland revenues in the fiscal year ending in March were Rs 1,490 crore ($232 million), with 3.14 million rupees in profits—this was by 2016, but the growth trajectory had been established much earlier.

The European expansion followed a similar pattern but with an important twist. Gland's world-class manufacturing facilities have also received approvals from a number of key medical regulatory agencies around the globe including those in Australia, Germany and the UK, in addition to the World Health Organization ("WHO"). Each approval opened new markets, but more importantly, each approval validated Gland's quality systems. When you can satisfy German regulators—notorious for their stringency—you can satisfy anyone.

What's fascinating about this period is what Gland didn't do. They didn't diversify into oral solids. They didn't launch a branded generics division. They didn't acquire struggling companies for their marketing authorizations. Every decision reinforced the core focus on injectable manufacturing excellence.

The R&D strategy during this period deserves special attention. While most Indian companies were content with simple generic copies, Gland was building capabilities in complex generics—products that required specialized manufacturing processes or novel drug delivery systems. These products had less competition and better margins, but they required significant upfront investment in development.

By 2010, Gland had achieved something remarkable: a reputation for quality that transcended its size. Global pharmaceutical companies—including some of the biggest names in the industry—were comfortable sourcing critical injectable products from a company most consumers had never heard of. The foundation was now strong enough to attract a different kind of capital—the kind that could transform a successful family business into a global pharmaceutical platform.

IV. The KKR Investment Era (2013-2017)

In November 2013, Gland Pharma Limited announced an agreement under which KKR, a leading global investment firm, would acquire a minority stake in the Company for approximately US$200 million, including KKR's acquisition of the entire stake held by Evolvence India Life Sciences Fund, an existing private equity investor in Gland Pharma.

This wasn't just another private equity deal in Indian pharma—it was the largest at the time and marked a fundamental shift in how global investors viewed specialized Indian manufacturers. To understand why KKR—a firm that could invest anywhere in the world—chose to bet $200 million on an injectable manufacturer in Hyderabad, you need to understand the perfect storm that was brewing in global pharmaceutical markets.

When Gland Pharma became the first Indian company to win FDA approval for a liquid injectable in 2003, the drug shortage problem was in its infancy. Over the past decade, a FDA crackdown on sterile injectables has escalated the issue, creating opportunities for high-quality producers of these complex products. By 2013, this shortage had become a crisis. Hospitals in the United States were struggling to source basic injectable medicines—saline solutions, anesthetics, antibiotics. The FDA's quality crackdown had shut down production lines at major suppliers, creating massive supply gaps.

KKR saw what many missed: this wasn't a temporary disruption but a structural shift in the industry. The days of cutting corners in sterile manufacturing were over. Companies with proven quality track records would command premium valuations and capture disproportionate market share. Gland, with its decade-long history of FDA compliance, was perfectly positioned.

Gland Pharma Founder-Chairman P V N Raju said, "Gland Pharma is at an important juncture in its evolution where we have proven our sterile manufacturing capabilities, established ourselves as a high-quality manufacturer of complicated injectables products and achieved a track-record of strong financial performance. Our partnership with KKR will help us in our next phase of growth as we look to materially expand our manufacturing capacities and invest more in our development work with the goal of expanding our product registrations."

The KKR investment thesis was elegant in its simplicity: take a company with world-class manufacturing capabilities but capital constraints, inject growth capital, and help it scale to meet exploding global demand. But KKR brought more than just money. After our investment was announced in 2013, and subsequently closed in 2014, members of the KKR team worked alongside Gland's founder and management team to help grow the company's capacity and profits. Through our collective efforts — and those of the KKR Capstone team — Gland established itself as a multinational leader in health care, and today remains the first Indian pre–filled injectables producer to have received FDA approval for product distribution in the U.S.

The KKR Capstone team—the operational improvement arm of the private equity giant—worked closely with Gland's management on several fronts. They helped optimize manufacturing processes, reducing cycle times and improving yields. They brought in expertise on automation and digitalization, helping Gland modernize its operations without compromising its quality standards. They also provided strategic guidance on product selection, helping Gland focus on high-value, complex generics rather than commoditized products.

Work on a large-scale production plant--which the Financial Times reports will double Gland Pharma's capacity--is now underway. The KKR investment, which reportedly gives it a 35% stake, will help advance the project. This capacity expansion was critical. The injectable market was growing rapidly, but more importantly, the complexity of products was increasing. Oncology injectables, peptide drugs, long-acting formulations—these required specialized facilities that took years to build and validate.

The financial transformation under KKR was remarkable. While exact numbers for the period aren't all available, we know the outcome: KKR had acquired nearly 36% in the company in 2013 for $200 million, which is now valued at $540 million by the time of the Fosun acquisition in 2016-17. This wasn't financial engineering—this was value creation through operational excellence.

But perhaps the most important contribution of the KKR era was professionalization. Family businesses, even successful ones, often struggle with governance and succession planning. KKR helped Gland implement world-class governance structures, brought in independent directors with global pharmaceutical experience, and created systems that would allow the company to operate at scale.

The product portfolio evolution during this period tells its own story. Gland moved from simple generic injectables to complex products like enoxaparin (a low molecular weight heparin), daptomycin (a complex antibiotic), and various oncology drugs. Each of these products required significant technical expertise and regulatory know-how, creating barriers to entry that protected margins.

Since then, the company has seen its capacity and profit grow significantly. This was achieved, in part, by Gland's investment into a new manufacturing plant, significant optimization of existing facilities, enhanced R&D spend and focus, and Gland's ability to file for and own further intellectual property.

By 2016, Gland had transformed from a successful family business into an institutional-grade pharmaceutical platform. Revenue had scaled significantly, margins had expanded despite pricing pressure in generic markets, and the company had built a pipeline of complex products that would drive growth for years to come. The stage was set for the next chapter—one that would test the company's resilience in ways no one could have predicted.

V. The Fosun Acquisition: China Meets India (2016-2017)

The boardroom in Mumbai must have been electric on that July day in 2016. Shanghai Fosun Pharmaceutical (Group) Co. Ltd. announced the signing of a definitive agreement under which Fosun Pharma will acquire an approximate 86.08% stake in Gland Pharma for no more than US$ 1261.37 million, including paying no more than US$ 50 million contingent consideration for Gland Pharma's Enoxaparin sales in the U.S. market. This is, so far, the largest overseas acquisition of a Chinese pharmaceutical company.

Stop and consider the audacity of this deal. A Chinese pharmaceutical company—from a country still building its quality credentials—was acquiring one of India's most respected injectable manufacturers for over a billion dollars. This wasn't just a financial transaction; it was a geopolitical statement.

The timing seemed perfect. China was flush with capital and hungry for global pharmaceutical assets. India was opening up to foreign investment. And Gland, having proven its model under KKR's ownership, was ready for the next level of scale. But between the announcement and closing, the world shifted.

Border tensions between India and China escalated. The Doklam standoff brought the two nuclear powers to the brink of conflict. Anti-China sentiment in India reached fever pitch. And suddenly, a straightforward acquisition became a test case for India's foreign investment regime.

The Cabinet Committee on Economic Affairs (CCEA) had raised objections to the proposal earlier this year, a development that came amid heightened tensions between India and China over border dispute. The Indian government faced a dilemma. On one hand, blocking the deal would send a negative signal to foreign investors. On the other, allowing a Chinese company to control a strategic pharmaceutical asset during heightened tensions was politically untenable.

The solution was classically Indian—a compromise that satisfied no one fully but allowed everyone to save face. Shanghai Fosun Pharmaceutical Group has agreed to cut the size of the stake it would buy in Hyderabad-based injectable maker Gland Pharma to 74 per cent in a revised $1.09-billion deal after its earlier proposal to acquire 86 per cent met approval roadblock. In a statement to Hong Kong stock exchange on Sunday, Fosun said its board had approved the new plan, which would involve an investment of no more than $1.09 billion.

The 74% threshold was crucial. Under Indian foreign investment rules, acquisitions up to 74% in pharmaceuticals were considered under the automatic route, while anything higher required government approval. By scaling back from 86% to 74%, Fosun avoided the need for CCEA approval while still gaining control.

The Indian company's promoters Ravi Penmetsa and his father P V N Raju will continue on the board of the company, Gland Pharma said in a statement. Besides, the present management team will be in-charge of the day to day running of the company, it added. Mr Penmetsa would remain managing director.

This continuity was critical for multiple stakeholders. For Fosun, it ensured that the technical expertise and regulatory relationships that made Gland valuable would remain intact. For the founding family, it provided a graceful transition that preserved their legacy. For employees and customers, it signaled stability despite the ownership change.

But why was Fosun so determined to acquire Gland, even at a premium valuation and despite political headwinds? The answer lies in understanding Fosun's global ambitions and China's pharmaceutical challenges.

With this deal, Fosun gets access to two state-of-the art R&D laboratories, four USFDA, MHRA approved manufacturing sites, 60+ niche injectables and a growing oncology pipeline. The deal will thus help the Chinese drug maker to leverage capabilities and expand its product offerings. More importantly, this acquisition will give Fosun easy access to the US and Europe markets as well as increase its presence in Asia and India.

For context, Chinese pharmaceutical companies in 2016 were facing their own FDA crisis. Between 2010 and 2015, FDA inspections in China had nearly tripled, and failure rates were alarming. Chinese companies desperately needed FDA-compliant manufacturing capabilities and regulatory expertise. Gland offered both in abundance.

The valuation—roughly 8 times sales based on available figures—raised eyebrows. Piramal's formulations business was acquired by Abbott for nine times its sales, while Ranbaxy was acquired at five times its sales. Gland, going by the March 2015 sales figures of Rs 1,000 crore, roughly translate into eight times sales - something that the Indian pharma companies, including Dr Reddy's, Torrent and Baxter, were not willing to pay.

Why didn't Indian companies bid more aggressively? The answer reveals much about the Indian pharmaceutical industry's mindset at the time. Most Indian companies were focused on forward integration—building front-end marketing capabilities in developed markets. The idea of paying a premium for manufacturing excellence seemed antiquated. They would soon learn otherwise.

In October 2017, the acquisition of 74% stake of Gland Pharma was completed. When the dust settled, Fosun had paid approximately $1.09 billion for 74% of Gland—still making it the largest Indian corporate takeover by a Chinese company.

For KKR, the exit was spectacular. KKR, which invested $200 million in Gland Pharma in 2013, made a return of more than three times and an internal rate of return (IRR) of nearly 30%. This wasn't just a financial win; it validated the thesis that specialized pharmaceutical manufacturers could generate private equity-style returns.

The market's reaction was mixed. Some saw it as a validation of Gland's quality and potential. Others worried about Chinese control of an Indian pharmaceutical asset. But everyone agreed on one thing: the injectable space would never be the same again.

VI. The IPO Story: Public Markets Debut (2020)

Gland Pharma IPO bidding started from November 9, 2020 and ended on November 11, 2020. The shares got listed on BSE, NSE on November 20, 2020.

The timing couldn't have been more challenging—or more ironic. In 2020, as India reeled from border clashes with China in Galwan Valley and "Boycott China" trended across social media, a Chinese-controlled pharmaceutical company was attempting India's largest pharma IPO in years.

Gland Pharma IPO is a main-board IPO of 4,31,96,968 equity shares of the face value of ₹1 aggregating up to ₹6,479.55 Crores. The issue is priced at ₹1500 per share. This wasn't just any IPO—it was a statement of confidence in Indian capital markets by a Chinese parent company at the worst possible time for India-China relations.

The structure of the IPO was telling. The offer comprised a fresh issue of 8,333,333 equity shares aggregating up to Rs. 1250 crores and an offer for sale of 34,863,635 equity shares, including 19,368,686 equity shares by Fosun Pharma Industrial Pte. Fosun was selling approximately 17% of its stake, but retaining clear control. This was about partial monetization and providing liquidity, not exit.

The investment bankers had their work cut out for them. How do you sell a Chinese-controlled company to Indian investors when anti-China sentiment is at its peak? The answer: focus relentlessly on operational excellence and global opportunity.

The pitchbook told a compelling story. Revenues rose 29% to Rs 2633.24 crore and net profit rose 71% to Rs 772.86 crore in year ended March 2020. Revenues rose 31% to Rs 884.21 crore in Q1FY21. Operating margins jumped 770 bps to 46.7% resulting into 57% increase in operating profits to Rs 412.62 crore. Net profit was up 71% to Rs 313.59 crore. At the higher price band of Rs 1500, the offer is made at around 31.7 times its FY 2020 EPS of Rs 47.4.

These weren't just good numbers—they were exceptional. In a year when COVID-19 had disrupted global supply chains, Gland had delivered explosive growth. The pandemic had actually validated Gland's business model: hospitals needed reliable supplies of critical injectable medicines, and Gland could deliver.

But the China overhang was real. While, it is not unusual for a growing pharma company to command such valuations, the Chinese ownership may not be received well by the market, given the strong anti-China sentiments within India. The gray market premium—the unofficial premium at which IPO shares trade before listing—told the story of investor nervousness. The GMP has fallen sharply from 170 to 60 in Gland Pharma.

The roadshows were exercises in diplomatic messaging. Management emphasized that Gland remained an Indian company—incorporated in India, manufacturing in India, employing Indians. The Chinese parentage was acknowledged but downplayed. The focus was on the US market opportunity, where Gland generated the majority of its revenues.

Then came listing day, November 20, 2020. The market's verdict was decisive and surprising. Despite all the concerns, despite the geopolitical tensions, despite being the first Chinese-controlled company to list in India, Gland delivered a stellar debut. The stock opened at a premium and closed the first day up over 21%, validating both the business model and investor appetite for quality pharmaceutical assets.

Total Gain on Investment = (1500-605) * 1,93,68,686 = 1733 Crores. For Fosun, this was vindication. They had recovered a significant portion of their investment while retaining control. The paper gains on their remaining stake were enormous.

The IPO's success had broader implications. It showed that Indian investors could separate business quality from geopolitical concerns. It validated the premium valuations for specialized pharmaceutical manufacturers. And it opened the door for more complex cross-border transactions, even in sensitive sectors.

But perhaps most importantly, it gave Gland a new currency—publicly traded stock—that it could use for acquisitions and employee incentives. It also brought new scrutiny. As a listed company, Gland would now face quarterly earnings pressure, analyst questions, and the relentless demands of public markets.

With the past four days' surge, Gland Pharma is now trading 92 per cent higher over its initial public offer (IPO) issue price of Rs 1,500 per share. By April 2021, just five months after listing, the stock had nearly doubled, reaching new highs above ₹2,800. The market was voting with its feet: Gland's specialization in complex injectables was worth the premium.

VII. Business Model & Competitive Advantages

To truly understand Gland Pharma, you need to grasp why manufacturing sterile injectables is fundamentally different from making pills. Imagine trying to manufacture a product where a single particle of dust, invisible to the naked eye, could kill a patient. Where the water you use must be purer than what NASA sends to space. Where your employees must dress like they're entering a biosafety level-4 laboratory just to walk onto the production floor.

We operate primarily under a business to business (B2B) model and have an excellent track record in the pharmaceutical research and development, manufacturing and marketing of complex injectables. This presence across the value chain has helped us witness exponential growth.

The B2B model is Gland's strategic masterstroke. While companies like Sun Pharma and Dr. Reddy's spent billions building consumer-facing brands and sales forces, Gland remained invisible to end consumers but indispensable to the companies that served them. Think of it as being the Intel Inside of injectable medicines—critical to the final product but never seeking the spotlight.

Let's break down why this model is so powerful:

Technical Barriers: Manufacturing sterile injectables requires specialized equipment that can cost tens of millions of dollars per production line. A single lyophilization unit (freeze-drying equipment for injectable drugs) can cost more than an entire oral solid dosage facility. Gland Pharma has seven manufacturing facilities in India, comprising four finished formulations facilities with a total of 22 production lines and three API facilities. This represents hundreds of millions of dollars in specialized infrastructure that would take competitors years to replicate.

Regulatory Moat: In 2003, Gland Pharma was the first company in India to get US Food and Drug Administration (FDA) approval for pharmaceutical liquid injectable products. This first-mover advantage has compounded over two decades. Each successful FDA inspection builds credibility. Each approved product becomes a reference for the next application. Today, one ANDA was filed and nine were approved in Q1 FY26, contributing to a cumulative total of 372 ANDA filings in the U.S. (325 approved, 47 pending).

The Complex Generic Opportunity: Here's where Gland's strategy gets really interesting. While everyone else was racing to the bottom in simple generics, Gland focused on complex products. We are present in sterile injectables, oncology and ophthalmic segments, and focus on complex injectables including NCE-1s, First-to-File products and 505(b)(2) filings.

What makes a generic "complex"? It could be the molecule itself (like enoxaparin, which is derived from biological sources), the delivery mechanism (like long-acting suspensions that release drug over weeks), or the manufacturing process (like liposomal formulations that encapsulate drugs in fat particles). These products have fewer competitors and better margins because most generic companies lack the technical capabilities to make them.

The Capacity Edge: Recently, the firm increased its manufacturing capacity from 670 million units in 2018 to 755 million units in 2020. But raw capacity tells only part of the story. Gland's facilities can handle multiple product types—vials, pre-filled syringes, ampoules, lyophilized products, and bags. This flexibility allows them to optimize production based on market demand and margin opportunities.

Partner Relationships: It has a track record of operating a B2B model with some leading pharmaceutical companies like Sagent Pharmaceuticals Inc., Apotex Inc., Fresenius Kabi USA LLC, Athenex Pharmaceutical Division LLC (US), etc. These aren't just customers; they're strategic partners who depend on Gland for critical products. Switching suppliers for injectable products is complex and risky, creating significant customer stickiness.

The FDA Shortage Dividend: This is perhaps Gland's most underappreciated advantage. The U.S. has struggled with shortages of products in these classes in recent years, in part because the FDA has found fault with quality standards at leading suppliers such as Hospira. When the number of new shortages of medically necessary drugs peaked in 2011, the FDA calculated 73% of affected products were sterile injectables.

When competitors stumble with FDA compliance, Gland gains. When production lines shut down elsewhere, hospitals turn to reliable suppliers. Gland's pristine compliance record becomes more valuable with each competitor's failure.

Vertical Integration: Unlike pure-play contract manufacturers, Gland develops its own products, files its own regulatory applications, and owns its intellectual property. Fifteen products are in co-development (seven under the 505(b)(2) pathway and eight ANDAs), with commercialisation expected to begin in FY28. One ready-to-use (RTU) infusion bag was filed this quarter, bringing the total RTU product filings in the US to 20 (14 approved).

The 505(b)(2) pathway is particularly interesting. It allows companies to file applications for drugs that aren't entirely new but have some modification—maybe a new formulation, dosage, or delivery method. These products can get three to seven years of market exclusivity, providing monopoly-like margins in a generic industry.

The Margin Story: The gross margin improved to 65%, up from 60% a year ago. EBITDA jumped 39% YoY to ₹367.8 crore, from ₹265.4 crore in Q1 FY25. The EBITDA margin expanded to 24%, gaining 549 basis points (bps) YoY. These aren't typical generic drug margins. They reflect the value of specialization, the premium for reliability, and the rewards of technical complexity.

VIII. Modern Era & Strategic Evolution (2020-Present)

The post-IPO era has tested Gland in ways that private ownership never could. Public markets are unforgiving—they demand growth every quarter, punish misses severely, and constantly question strategic decisions. For a company that built its reputation on patient, long-term thinking, this adjustment hasn't been entirely smooth.

The Cenexi acquisition in 2022 exemplifies both the ambition and challenges of Gland's modern era. On November 29, 2022, the Hyderabad-based drug contract development and manufacturing company (CDMO) had entered into a put option agreement to acquire Cenexi Group for up to EUR 120 million (around Rs 1,015 crore), marking its foray into the international markets.

On paper, Cenexi looked perfect. Founded in 2004, Cenexi, along with its subsidiaries, is engaged primarily in the business of contract development and manufacturing organisation (CDMO) of pharmaceutical products with expertise in sterile liquid and lyophilized fill-finished drugs, including capabilities on oncology and complex products. It has a presence across four manufacturing sites in Europe which include three sites in France and one site in Belgium.

The strategic rationale was compelling. Cenexi would give Gland a European manufacturing footprint, access to new technologies, and relationships with European pharmaceutical companies. It would transform Gland from an Indian exporter to a global manufacturer. But integration proved harder than expected.

The decrease in the group's consolidated Ebitda margin is being attributed to the negative Ebitda reported by Cenexi, its recent acquisition. Cenexi reported an Ebitda of Rs -28.6 crore in the June quarter, according to the company's investor presentation. For several quarters, Cenexi dragged down Gland's consolidated margins, testing investor patience.

But by Q1 FY26, the turnaround began showing results. Reported a turnaround at the EBITDA level, achieving breakeven with €0.9 million (₹86 million) in Q1FY26, versus a loss of €3 million (₹286 million) last year. EBITDA margin turned positive at 2%, compared to -7% in Q1FY25.

This turnaround story illustrates a crucial aspect of Gland's evolution: the company is no longer just a manufacturer but an operator of pharmaceutical assets. The ability to acquire underperforming assets and improve them through operational excellence adds a new growth vector beyond organic expansion.

The geographic revenue mix tells another story of evolution. On the geographical revenue front, Revenue from the US market stood at Rs 744.3 crore (down 2.42% YoY), revenue from Europe was at Rs 330.2 crore (up 28.68% YoY), Canada, Australia, and New Zealand stood at Rs 73.9 crore (up 65.32% YoY). While the US remains dominant, Gland is successfully diversifying its geographic exposure, reducing dependence on any single market.

The product pipeline evolution is equally impressive. The company is moving beyond traditional generics into more sophisticated territories. The focus on GLP-1 agonists—the diabetes and weight-loss drugs that have become pharmaceutical blockbusters—shows Gland's ability to identify and capitalize on emerging opportunities.

The company launched 12 new molecules in regulated markets, including Colistimethate, Epinephrine, Vancomycin (three new strengths), Liraglutide and Acetaminophen bags. Its in-house complex pipeline saw six product launches, with three more awaiting approval. Complex injectables remain a key driver of long-term growth, with more products being added to the pipeline.

Liraglutide is particularly significant—it's a GLP-1 agonist, part of the same class as Ozempic and Wegovy. These are complex peptide drugs that require sophisticated manufacturing capabilities. The fact that Gland can manufacture these products positions it well for the next wave of generic opportunities as patents expire.

The R&D strategy has also evolved. During the quarter, research and development (R&D) expenses stood at ₹46 crore, accounting for 4.4 per cent of revenue. This might seem low compared to innovator companies, but for a generic manufacturer, it represents a significant commitment to development capabilities.

Leadership transition marks another evolution. Srinivas Sadu, Executive Chairman of Gland Pharma, said, We're off to a positive start this year with a growth in revenue and a significant jump in profitability, which was driven by a strong performance in our base business and a turnaround at Cenexi. The transition from founder family leadership to professional management, while maintaining continuity, shows institutional maturity.

The market dynamics have also shifted. The era of easy generic approvals and quick profits is over. Gland Pharma has been facing challenges over the past three years due to increased competition and operational losses at Cenexi. However, the company is reinforcing its position in the complex injectable space through in-house product development and partnerships.

But challenges create opportunities for companies with staying power. As smaller players exit or struggle with compliance, Gland can capture market share. As products become more complex, Gland's technical capabilities become more valuable. As supply chain resilience becomes critical, Gland's multiple facilities and proven track record command premiums.

IX. Playbook: Business & Investing Lessons

After spending hours dissecting Gland Pharma's journey, several powerful lessons emerge—lessons that challenge conventional wisdom about building businesses in emerging markets.

Lesson 1: Complexity as Competitive Advantage

Most business strategists preach simplification. Gland did the opposite. By choosing the most complex pharmaceutical manufacturing—sterile injectables—they built moats that even well-funded competitors struggle to cross. Estimates show that if EBITDA margins were 20-25 per cent for generics tablets and capsules, for injectables it is 50-60 per cent EBIDTA in the US market.

The lesson for investors: Look for companies that embrace technical complexity rather than avoid it. The harder something is to do, the fewer competitors will attempt it, and the better the economics for those who succeed.

Lesson 2: The Power of Saying No

Throughout its history, Gland resisted obvious temptations. They didn't diversify into oral solids when everyone said they should. They didn't build a front-end sales force when that was the fashion. They didn't acquire weak companies for their marketing authorizations when roll-ups were popular.

As per offer documents, GPL has no listed peers to compare with. This uniqueness isn't accidental—it's the result of decades of disciplined focus. Every strategic decision reinforced the core thesis: be the best at sterile injectable manufacturing.

Lesson 3: Regulatory Excellence as Strategy

Most companies view regulatory compliance as a cost center. Gland turned it into a competitive weapon. By achieving FDA approval before any other Indian injectable manufacturer, by maintaining a spotless compliance record, by investing in quality systems that exceeded requirements, they turned regulation into a barrier that protected their business.

The numbers validate this strategy. While competitors faced FDA warning letters and import alerts, Gland captured their market share. While others struggled with regulatory submissions, Gland's applications sailed through. Compliance became a revenue generator, not a cost.

Lesson 4: The B2B Hidden Champions Model

Gland proves you don't need consumer recognition to build a valuable business. By focusing on B2B relationships, they avoided the massive marketing costs that consumer-facing pharmaceutical companies bear. They let their customers—global pharmaceutical giants—handle the expensive last mile while Gland focused on what it did best.

Gland Pharma is typically a B2B company. This isn't a limitation—it's a strategic choice that allows for better capital allocation, higher returns on investment, and more predictable cash flows.

Lesson 5: Patient Capital and Staged Evolution

Look at Gland's capital evolution: Family → Domestic PE (Ventureast) → Global PE (KKR) → Strategic (Fosun) → Public Markets. Each stage brought not just capital but capabilities. Ventureast brought credibility. KKR brought operational excellence. Fosun brought global market access. Public markets brought permanent capital and acquisition currency.

This staged approach allowed the founding family to retain influence while accessing increasingly sophisticated capital. P.V.N. Raju, Founder of Gland, and his son, Dr. Ravi Penmetsa, will continue to be on the Board, and Dr. Penmetsa will continue as Managing Director and CEO. The family will retain a stake in Gland.

Lesson 6: Market Timing and Structural Shifts

Gland's major inflection points coincided with structural industry shifts. FDA approval came just as injectable shortages began. KKR invested as the shortage became acute. Fosun acquired as Chinese companies needed FDA-compliant assets. The IPO happened as COVID validated the importance of injectable medicines.

This wasn't luck—it was positioning. By building capabilities ahead of demand, Gland could capitalize when market dynamics shifted in their favor.

Lesson 7: The China Paradox

Gland's experience with Chinese ownership offers nuanced lessons. Despite massive geopolitical headwinds, despite anti-China sentiment, the business fundamentals prevailed. Negative sentiment for China connection globally raises major concern. Yet the stock performed well post-listing.

The lesson: In the long run, business quality trumps narrative. But narrative matters in the short run, and companies must actively manage stakeholder perceptions during sensitive transitions.

Lesson 8: Operational Leverage in Specialized Manufacturing

EBITDA for the quarter came in at Rs 367.8 crore, marking a 38.58% growth YoY. The EBITDA margin improved to 24%, compared to 19% in the same period last year. These improving margins despite pricing pressure demonstrate the operational leverage in specialized manufacturing. Once you've built the infrastructure, trained the people, and validated the systems, incremental volume drops largely to the bottom line.

Lesson 9: The Platform Value of Regulatory Assets

Each FDA approval, each successful inspection, each validated process becomes an asset that can be leveraged for future products. Gland's 372 ANDA filings represent not just current products but a platform for launching future products faster and cheaper than competitors starting from scratch.

Lesson 10: Strategic Patience in Acquisitions

The Cenexi acquisition initially looked like a mistake. Integration was difficult, margins suffered, investors questioned the strategy. But Gland stayed the course, and by Q1 FY26, Cenexi achieved EBITDA breakeven. The lesson: Strategic acquisitions often take longer to pay off than financial models suggest, but patient operators can create substantial value.

X. Analysis & Investment Case

Gland Pharma · Mkt Cap: 31,874 Crore (down -4.53% in 1 year) · Revenue: 5,720 Cr · Profit: 770 Cr · Stock is trading at 3.48 times its book value · Company has a low return on equity of 9.22% over last 3 years.

Let's address the elephant in the room: Why has a company with such strong fundamentals delivered mediocre returns for shareholders recently? The answer reveals both the challenges and opportunities in Gland's investment case.

The Valuation Conundrum

At current levels, Gland trades at approximately 41x trailing earnings—not cheap by any measure. The market is clearly pricing in significant future growth. But is this justified?

The bull case rests on several pillars. First, the injectable market opportunity remains massive. The global injectable drug market is on an impressive growth trajectory. It was valued at $569.9 billion in 2024, and is expected to reach $820 billion by 2029, growing at 7.5% compounded annually. Gland's current revenues represent a tiny fraction of this market.

Second, the complexity shift in generics favors Gland. As simple generics become commoditized, complex injectables offer better economics. Gland's technical capabilities position it well for this shift.

Third, the Cenexi turnaround suggests management can execute on inorganic growth. If they can replicate this with other acquisitions, it opens a new growth vector beyond organic expansion.

The ROE Challenge

Company has a low return on equity of 9.22% over last 3 years. This is concerning for a specialized manufacturer with supposed competitive advantages. The explanation is partly mathematical—the large equity base from the IPO diluted returns. But it also reflects integration challenges and investment in future capacity.

The counter-argument: ROE should improve as: (1) Cenexi returns to profitability, (2) New capacity gets utilized, (3) Complex products with better margins launch, (4) Operating leverage kicks in with scale.

The China Overhang

Despite successful listing, Chinese ownership remains a valuation headwind. Fosun acquired Gland Pharma in 2017 for $1.1 billion. It was listed in 2020 in a Rs 6,480 crore IPO. Fosun still controls the company, and in the current geopolitical environment, this creates uncertainty.

Three scenarios could play out: 1. Fosun exits completely, removing the overhang 2. Fosun remains but geopolitics normalize 3. Status quo continues with persistent discount

Reports suggest the first scenario might be in play. Bloomberg News broke the story that Chinese conglomerate Fosun was working with an adviser to weigh buyer interest in its controlling stake in Gland Pharma. Fosun Pharma picked up a 74% stake in Gland for about $1.1 billion back in 2017.

Competitive Dynamics

The injectable space is getting crowded. Indian players like Aurobindo and Lupin are building injectable capabilities. Global players are investing in supply chain resilience post-COVID. The easy wins from FDA compliance failures at competitors are behind us.

But Gland's head start matters. Their 20-year track record with FDA, relationships with global pharmaceutical companies, and technical expertise in complex formulations create barriers that money alone can't quickly overcome.

Capital Allocation Questions

With nearly ₹2,000 crores in cash and minimal debt, Gland has significant financial flexibility. But how they deploy this capital will determine future returns. More acquisitions like Cenexi? Organic capacity expansion? Dividends? The track record here is mixed.

The company has not paid any dividend in the last three fiscals. For the last three fiscals, GPL has not declared any dividend payouts. This might change as the company matures, but for now, shareholders aren't seeing cash returns.

The ESG Angle

Increasingly important for institutional investors, Gland's ESG profile is mixed. Environmental compliance in pharmaceutical manufacturing is strong—it has to be for FDA approval. Social factors are positive with significant employment in India. But governance concerns around Chinese control and related party transactions need monitoring.

Margin Trajectory

Strategic initiatives, coupled with steady price erosion in the base portfolio and new product introductions across major markets, are expected to drive a 20% earnings CAGR over FY25-27. If achieved, this would justify current valuations. But execution risk is real.

The key variables to watch: - Gross margins (currently 65%, up from 60%) - R&D productivity (new product approvals per dollar spent) - Cenexi contribution (breakeven achieved, but can it become meaningfully profitable?) - Market share in complex generics

Investment Conclusion

Gland Pharma represents a classic growth-at-a-reasonable-price (GARP) opportunity—if you believe the growth will materialize. The company has unique assets (FDA track record, injectable expertise, global relationships) that should command premium valuations. But execution challenges, Chinese ownership, and high starting valuations create risks.

For long-term investors, the key question isn't whether Gland is a good company—it clearly is. The question is whether it's a good investment at current prices. The answer depends on your view of: 1. The sustainability of injectable market growth 2. Management's ability to execute on complex products 3. The resolution of the China overhang 4. The company's capital allocation decisions

XI. Epilogue & Future Outlook

As we conclude this deep dive into Gland Pharma, it's worth stepping back to appreciate the remarkable journey from a small Hyderabad facility to a global pharmaceutical platform. But more importantly, what does the future hold?

The Fosun Exit Question

Reports say various global funds are in discussion to buy a majority stake in Gland Pharma, at a potential valuation of $3 billion. If true, this would be transformative. A new owner—particularly a Western pharmaceutical company or PE fund—could remove the China discount entirely. The stock could re-rate significantly on announcement alone.

But exits are complex. Fosun needs to balance price maximization with finding a buyer acceptable to Indian regulators. The new owner would need to maintain management continuity and operational excellence. And the timing—amid global recession fears—isn't ideal.

The Biosimilar Opportunity

Gland has been notably quiet about biosimilars—the generic versions of complex biological drugs. This is a massive opportunity, with the biosimilar market expected to reach $100 billion by 2030. Gland's expertise in sterile manufacturing and complex molecules positions it well for biosimilars, but significant investment would be required.

The strategic question: Should Gland enter biosimilars organically, through acquisition, or via partnership? Each path has trade-offs, but standing still might mean missing the next wave of pharmaceutical innovation.

The GLP-1 Gold Rush

The success of GLP-1 drugs like Ozempic has created a gold rush in peptide manufacturing. The company launched 12 new molecules in regulated markets, including...Liraglutide. Liraglutide is a GLP-1 agonist, positioning Gland at the forefront of this opportunity.

As patents expire on blockbuster GLP-1 drugs, the generic opportunity will be massive. But manufacturing these complex peptides requires exactly the kind of expertise Gland has built over decades. This could be the next major growth driver.

The India Opportunity Paradox

Ironically, Gland has limited presence in India—Revenue from India was at Rs 59.4 crore (up 12.71% YoY), a tiny fraction of total revenue. As India's healthcare spending grows, as insurance coverage expands, as hospital infrastructure improves, the domestic opportunity could become significant.

But capturing this opportunity would require a different model—possibly B2C, definitely requiring marketing investments. Does Gland have the appetite to build these capabilities, or will they stick to their B2B focus?

The Manufacturing Renaissance

Post-COVID, there's a global push for supply chain resilience in critical medicines. Governments are offering incentives for domestic manufacturing. Companies are diversifying supplier bases. This environment favors established manufacturers with proven track records.

Gland could benefit from both sides of this trend—as an Indian company benefiting from "China Plus One" strategies, and as a reliable supplier to companies diversifying their supply chains.

The Consolidation Catalyst

The injectable space might be ready for consolidation. Smaller players struggle with regulatory compliance and scale requirements. Larger players seek specialized capabilities. Gland, with its strong balance sheet and operational expertise, could be a consolidator.

Imagine Gland acquiring struggling injectable facilities in the US or Europe, upgrading them to its standards, and leveraging its regulatory expertise. This could create significant value, similar to what private equity does in other industries.

Leadership Evolution

The transition from founder family to professional management is ongoing. Shyamakant Giri, Chief Executive Officer, Gland Pharma, said: "I am honoured and excited to lead Gland Pharma as its new CEO. Building on the company's strong foundation, my focus will be on enhancing operational excellence in our base business, ensuring Cenexi's successful turnaround, identifying and pursuing new growth opportunities, and further solidifying our position as a leader in the CDMO space, particularly in biologics and complex injectables. I believe that by fostering a culture of innovation, collaboration, and customercentricity, we can achieve sustainable growth and create long-term value for all our stakeholders."

New leadership brings fresh perspectives but also execution risk. The key will be maintaining Gland's technical excellence while adapting to changing market dynamics.

The Ultimate Question

Will Gland Pharma become India's injectable champion globally? The pieces are in place—technical expertise, regulatory track record, global relationships, financial strength. But execution in an increasingly competitive environment will determine success.

The company that started with a chemist's vision of mastering complex molecules has evolved into a platform capable of serving global pharmaceutical needs. Whether it fulfills this potential depends on strategic choices made in the next few years—about ownership, about markets, about products, about capital allocation.

For investors, employees, and stakeholders, the Gland Pharma story is far from over. In many ways, it's just beginning. The foundation built over 46 years can support a much larger edifice. Whether that edifice gets built—and who builds it—remains to be seen.

What's certain is that in a world increasingly dependent on injectable medicines, companies with Gland's capabilities will be essential. The question isn't whether Gland will remain relevant, but whether it will capture the full value of its relevance.

As P.V.N. Raju might say, looking at what his small facility has become: the complexity was worth it. The focus was justified. The patience paid off. Now it's up to the next generation to write the next chapter of the injectable empire from Hyderabad.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube