KPIT Technologies: From IT Services to Automotive Software Powerhouse

I. Introduction & Episode Roadmap

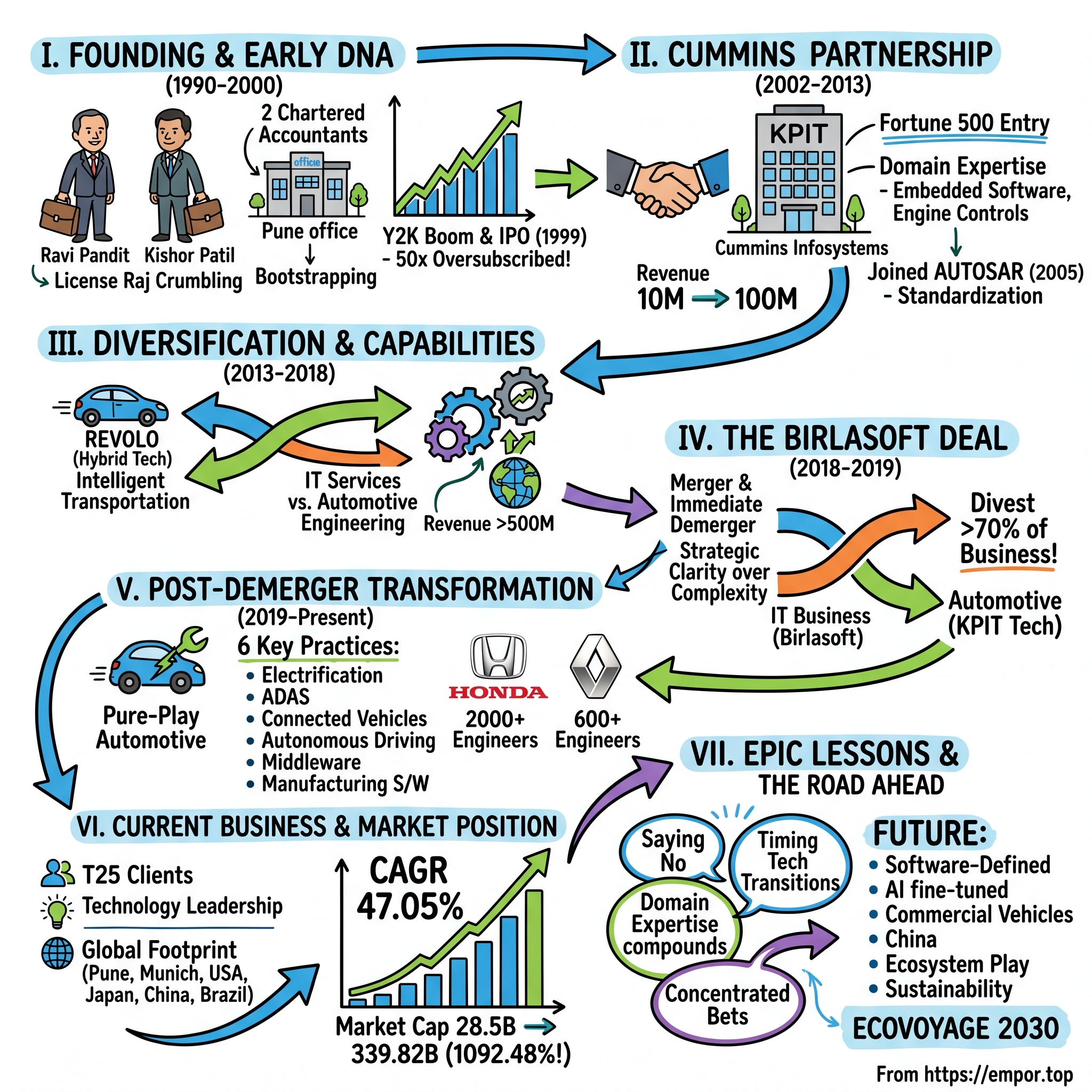

Picture this: Two chartered accountants in post-liberalization India decide to abandon the predictable comfort of their accounting practice to build a technology company. It's 1990, and while the world is talking about personal computers and the internet revolution, Ravi Pandit and Kishor Patil are sketching out dreams in a modest Pune office. Fast forward three decades—their company, KPIT Technologies, now powers the software brains of over 10 million vehicles globally, partnering with 25 of the world's top automotive companies.

But here's the twist that makes this story extraordinary: In 2018, at the peak of their success, these founders made a decision that seemed almost irrational—they chose to divest over 70% of their business to focus solely on automotive software. The IT Business of KPIT was more than double in revenue than Birlasoft at the time of the transaction. Why would anyone walk away from 70% of their revenue? Why bet everything on one vertical when diversification was the mantra of Indian IT?

The answer lies in a vision that saw what others couldn't—that software would become the defining force in automobiles, that cars would transform from mechanical marvels to computers on wheels, and that being mediocre at many things was far less valuable than being exceptional at one.

This is the story of how KPIT evolved from a small IT services firm to become one of the world's leading automotive software companies—a journey marked by bold pivots, strategic partnerships, and the courage to sacrifice size for focus. It's about recognizing that in the race to build tomorrow's vehicles, the real winner wouldn't be the biggest player, but the most specialized one.

Today, we'll explore how two accountants built a company that helps Honda, Renault, BMW, and other automotive giants navigate the most significant transformation in their century-old history: the shift to software-defined vehicles. We'll examine the Cummins partnership that provided the first major inflection point, the complex Birlasoft merger-demerger that shocked the market, and the remarkable post-2019 transformation that has seen KPIT's market cap increase from 28.50B to 339.82B, an increase of 1,092.48% since April 22, 2019.

What can investors and entrepreneurs learn from a company that chose depth over breadth, expertise over expansion, and focus over fortune? Let's dive into one of Indian technology's most fascinating transformation stories.

II. Founding Story & Early DNA (1990–2000)

The monsoon of 1990 brought more than just rain to Pune—it brought the birth of an idea that would reshape India's technology landscape. Ravi Pandit and Kishor Patil co-founded KPIT in 1990 as KPIT Infosystems. Both of them are chartered accountants by profession, and they were partners in an accountancy firm, Kirtane & Pandit Chartered Accountants (KPCA).

Picture the scene: India had just begun its economic liberalization journey. The License Raj was crumbling, foreign investment was trickling in, and a new generation of entrepreneurs sensed opportunity in the air. But while others rushed toward manufacturing or trading, two chartered accountants saw something different—the transformative power of information technology.

Between the late 1980s and early 1990s, Pune emerged as a hotbed for early startups and technology companies. During this period, the idea of KPIT was born out of deep passion and ambition to create a firm of global repute by 2 chartered accountants Mr. Ravi Pandit and Mr. Kishor Patil.

The early days weren't glamorous. Operating from modest offices in Pune, KPIT Infosystems started with basic IT services—the unglamorous work of helping local businesses computerize their operations. The company's early focus was on ERP solutions and IT consulting, with initial funding coming from bootstrapping and support from friends and family. But even then, there was something different about their approach. Where other IT startups chased quick government contracts or body-shopping opportunities, Pandit and Patil insisted on building genuine technical capabilities.

The founding DNA was unique—a blend of financial discipline from their CA background and technological ambition. This wasn't just about writing code; it was about understanding business processes deeply and then applying technology to transform them. Starting in Pune, they aimed to combine financial discipline with engineering innovation to address challenges in emerging industries.

By the mid-1990s, KPIT had begun to find its rhythm. The company expanded from basic IT services to more sophisticated offerings, including Oracle implementations and enterprise software solutions. The domestic market was growing, but Pandit and Patil had their eyes on a bigger prize—the global IT services opportunity that companies like TCS and Infosys were beginning to tap.

Then came 1999—a watershed year not just for KPIT but for Indian technology. The Y2K boom was at its peak, Indian IT companies were the darlings of global corporations, and investor appetite for technology stocks was insatiable. KPIT decided to go public.

The big milestone for KPIT came in 1999 with its IPO announcement. It received overwhelming response getting oversubscribed 50 times. Think about that for a moment—fifty times oversubscribed. In an era before online trading, when investors had to physically submit application forms, the demand was so intense that the issue was oversubscribed fifty-fold. This wasn't just an IPO; it was a vote of confidence in the company's vision and execution capabilities.

The IPO success provided more than just capital—it provided validation and visibility. Suddenly, KPIT wasn't just another Pune IT company; it was a listed entity with the credibility to pursue larger clients and bigger dreams.

But success brought its own challenges. The dot-com bubble was inflating rapidly, and every IT company was promising revolutionary growth. The question for KPIT was simple yet profound: Would they follow the herd into generic IT services, or would they find their own path?

As the millennium approached, with Y2K projects winding down and the dot-com crash looming, KPIT's founders faced a critical decision. They had built a successful IT services company, but they sensed that sustainable differentiation would require something more—domain expertise, deep partnerships, and the courage to specialize when everyone else was generalizing.

The company closed the decade with revenues approaching the $10 million mark—respectable but not remarkable. What happened next, however, would transform KPIT from a competent IT services provider into something far more significant. The stage was set for the Cummins partnership, a deal that would catapult the company into an entirely new orbit.

III. The Cummins Partnership: First Major Inflection (2002–2013)

The year 2002 opened with global IT services in turmoil. The dot-com bubble had burst, 9/11 had shaken corporate confidence, and Indian IT companies were scrambling to reinvent themselves beyond Y2K remediation. It was precisely in this moment of industry-wide crisis that KPIT made the move that would define its next decade.

In 2002, Cummins Infotech, the IT department of Cummins merged with KPIT, and the name of the company became KPIT Cummins Infosystems Ltd. But this wasn't just any merger—it was a masterclass in strategic transformation. This decision paved the way for a game-changing partnership with Cummins around 2002 to establish KPIT Cummins Infosystems, catapulting the JV's revenues from $10 million to $100 million.

Consider the audacity of this move. Here was KPIT, a relatively small IT services company, absorbing the entire IT division of a Fortune 500 company. Cummins wasn't just bringing contracts and revenues; it was bringing something far more valuable—deep domain expertise in engineering, particularly in the automotive and manufacturing sectors.

The transformation was immediate and dramatic. Overnight, KPIT went from being a vendor to being a strategic partner. Cummins engineers didn't see KPIT as just another IT supplier; they saw them as colleagues, as part of the extended Cummins family. This insider status opened doors that would have taken decades to unlock through traditional business development.

But the real genius of the partnership lay deeper. While other Indian IT companies were fighting for generic application development projects, KPIT was learning the intricacies of embedded software, engine control systems, and automotive electronics. They weren't just writing code; they were understanding how modern vehicles functioned at the most fundamental level.

KPIT, a premium member of AUTOSAR consortium since 2005 has actively contributed to drive the consortium efforts in software standardization. This wasn't a casual membership—AUTOSAR (Automotive Open System Architecture) was reshaping how automotive software would be developed globally. By joining as a premium member, KPIT signaled its serious intent to be not just a service provider but a technology leader in automotive software.

The period from 2002 to 2010 saw explosive growth. Revenues grew from $10 million to over $100 million—a ten-fold increase. But more importantly, KPIT's capabilities evolved dramatically. The company made strategic acquisitions that would prove prescient:

The company acquired companies like CG Smith, TVS Harita Mechanical Engineering Team and Germany's in2Soft Diagnostics, integrating them into the KPIT network. Each acquisition wasn't about size; it was about capability. CG Smith brought expertise in automotive electronics, particularly in safety systems and clusters. TVS Harita added mechanical engineering depth. In2Soft, a German company, provided a European foothold and deep vehicle diagnostics expertise.

The CG Smith acquisition in 2006 deserves special attention. KPIT Cummins acquired 100% equity of Bangalore based CG Smith Software Private Limited, an SEI CMM Level 5 company, focused in the realm of embedded and real-time systems for automotive electronics. The all-cash acquisition is for a consideration of Rs 38 crores (Rs 35 crores upfront and balance upon fulfillment of certain performance conditions). KPIT Cummins will leverage the in-depth automotive expertise of all the 200+ members of Team CG Smith to create a truly dominant force in automotive electronics.

By 2010, KPIT Cummins wasn't just another IT services company with automotive clients. It had become a genuine automotive technology company that happened to also offer IT services. The company was working on everything from engine control software to telematics systems, from safety electronics to hybrid vehicle technologies.

But success brought complexity. The Cummins name opened doors, but it also created dependencies. As KPIT grew, questions emerged: Was this Cummins' captive unit, or was it an independent technology company? Could KPIT work with Cummins' competitors? How much of the revenue was too dependent on a single relationship?

In September 2013, KPIT Cummins Infosystems changed its name to "KPIT Technologies Limited". This was in line with Cummins' decision to reduce its shareholding in KPIT, to focus on its core business of engine and generator manufacturing.

The 2013 rebranding to KPIT Technologies was more than a name change—it was a declaration of independence. After eleven years of partnership, KPIT had absorbed what it needed from Cummins: domain expertise, global credibility, and most importantly, a deep understanding of how automotive companies think and operate.

The company that emerged from this period was fundamentally different from the one that entered it. In 2002, KPIT was an IT services company with aspirations. By 2013, it was an automotive technology specialist with IT services capabilities. The foundation was set, but the biggest transformation was yet to come. The company would soon face a choice that would test everything it had learned: continue growing as a diversified technology company, or make a bold bet on the future of mobility.

IV. Diversification & Building Capabilities (2013–2018)

The conference room at KPIT's Pune headquarters buzzed with an energy that mixed ambition with anxiety. It was 2013, and the newly independent KPIT Technologies faced a classic innovator's dilemma: Should they leverage their automotive expertise to dominate one vertical, or should they hedge their bets across multiple industries?

They chose both—a decision that would lead to spectacular growth, increasing complexity, and ultimately, the most dramatic restructuring in the company's history.

The period from 2013 to 2018 saw KPIT unleash its entrepreneurial spirit in multiple directions. After the split, the automotive software company, KPIT Technologies, forayed into the mobility software products such as REVOLO (hybrid electric vehicle tech), Intelligent Transportation Systems and Maximum Pro. These weren't just service offerings; they were bold product plays.

REVOLO, in particular, represented KPIT's ambition to move beyond services. This hybrid electric vehicle technology could retrofit existing vehicles to improve fuel efficiency by 30-40%. Imagine the audacity—a services company from Pune developing technology that could compete with solutions from global automotive giants. The technology found its way into buses in major Indian cities, proving that KPIT could innovate, not just integrate.

Meanwhile, the company's geographic expansion accelerated dramatically. It expanded globally and inaugurated a new software engineering centre in various places such as the USA and Europe. But this wasn't the typical Indian IT company's expansion of setting up offshore development centers. KPIT was establishing innovation hubs, close to their automotive clients, staffed with engineers who understood local market needs.

The company essentially operated as two distinct businesses under one roof. On one side was the traditional IT services business—steady, profitable, serving BFSI, manufacturing, and energy clients with ERP implementations, application development, and maintenance services. This business generated predictable revenues and cash flows, keeping investors happy and funding growth investments.

On the other side was the engineering services business—dynamic, specialized, focused entirely on automotive and mobility. This was where KPIT's heart lay, but it required constant investment in new capabilities, from ADAS (Advanced Driver Assistance Systems) to electric powertrain software.

The numbers told a story of success. By 2017, KPIT had grown to over $500 million in revenue, with more than 15,000 employees across the globe. The company was winning large deals, expanding its client base, and consistently delivering strong financial performance. From the outside, everything looked perfect.

But inside KPIT, a different conversation was happening. The automotive industry was undergoing its most significant transformation in a century. Electric vehicles were moving from concept to reality. Autonomous driving was transitioning from science fiction to engineering challenge. Software was becoming the differentiator in vehicles, not hardware.

"Focus is a powerful concept, and it has given us a tremendous edge," Patil asserts. This wasn't just a retrospective observation—it was a growing realization during this period that trying to be everything to everyone was preventing KPIT from being exceptional at anything.

The tension was palpable. The IT services business was larger, generating about 70% of revenues. It was stable, profitable, and had excellent growth prospects. The engineering business was smaller but growing faster, more exciting, and aligned with where the founders believed the future lay. But resources were getting stretched. Top talent was being pulled in different directions. Investment decisions were becoming increasingly complex.

Moreover, the market was penalizing this complexity. Despite strong performance, KPIT's valuation multiples lagged behind both pure-play IT services companies and specialized engineering services firms. Investors couldn't figure out how to value a company that was part Infosys, part automotive specialist.

By late 2017, the leadership team had reached a conclusion that would have seemed unthinkable just a few years earlier: The two businesses needed different strategies, different investment levels, and potentially, different owners. But how do you split a company that has grown organically over 27 years? How do you divide teams, technologies, and client relationships that are deeply intertwined?

The answer would come in the form of one of the most complex corporate restructurings ever attempted by an Indian technology company. In January 2018, KPIT announced a deal that left the market stunned: a merger with Birlasoft followed by an immediate demerger. It was financial engineering at its most sophisticated, driven by strategic clarity at its most bold.

The diversification years had been successful by any conventional measure. But KPIT's leadership understood that in the rapidly evolving automotive landscape, being good wasn't good enough. You had to be exceptional. And exceptional required focus—laser-sharp, unwavering focus on one thing: becoming the world's best automotive software company.

V. The Birlasoft Deal: The Boldest Move (2018–2019)

January 29, 2018. The press release that hit the wires that morning read like a corporate puzzle. KPIT and Birlasoft announced the coming together to create a USD 700+ million combined entity that will later demerge into two separate companies, focused on 'Automotive Engineering and Mobility Solutions' (the new KPIT Technologies) and 'Digital Business IT Services' (Birlasoft) respectively.

The financial press scrambled to understand: Why merge only to immediately demerge? Why go through this elaborate corporate dance when a simple sale of the IT business would have been cleaner?

The answer lay in the intricate architecture of value creation that Ravi Pandit and Kishor Patil had designed. This wasn't just a transaction; it was a masterpiece of financial engineering aimed at solving multiple problems simultaneously.

First, consider the challenge: The IT Business of KPIT was more than double in revenue than Birlasoft at the time of the transaction. KPIT's IT business alone was generating over $350 million in revenue, while Birlasoft was roughly $160 million. A straight sale would have been difficult—few buyers could afford it, and those who could might not value it appropriately.

The merger-demerger structure was genius in its simplicity once you understood the logic. By first merging with Birlasoft, KPIT created a combined entity worth over $700 million. This larger entity had better scale, more comprehensive capabilities, and stronger market positioning. Then, by immediately demerging, they created two focused companies, each with clear strategies and appropriate investor bases.

"Segregating business IT and automotive tech businesses will provide sharper focus on each business." Ravi Pandit's words captured the essence of the strategy, but the execution was anything but simple.

The deal structure was meticulously crafted. The transaction included a joint open offer before the merger in Birlasoft Limited from KPIT promoter group & Birlasoft promoter group and post demerger, by KPIT promoter group in KPIT Technologies Limited. Shareholders of the original KPIT would end up owning shares in both companies—the automotive-focused KPIT Technologies and the IT services-focused Birlasoft.

The complexity was staggering. Legal teams worked around the clock to navigate Indian corporate law. The National Company Law Tribunal (NCLT) had to approve a scheme that had few precedents. Investment bankers structured swap ratios that had to be fair to multiple stakeholder groups. The exchange ratio was 2.44 (Rs 492/Rs 202) i.e 22 Equity shares of Rs 2 of KPIT for every 9 Equity shares of Rs 10 held in BIL.

But perhaps the boldest aspect was what KPIT was giving up. This saw KPIT divest over 70% of its business to zero in on automotive software solutions. Imagine the board meetings where this was discussed. Imagine explaining to shareholders that you're voluntarily shrinking from a $500+ million company to a $200 million company. In a corporate world obsessed with scale, KPIT was choosing to become smaller.

The months between announcement and execution tested everyone involved. Employees were uncertain about their futures. Clients worried about service continuity. Investors questioned the rationale. The stock price reflected this uncertainty, swinging wildly as the market tried to price in the implications.

KPIT Technologies Limited's name changed to Birlasoft Limited & KPIT Engineering Limited's name changed to KPIT Technologies Limited. Even the name changes added to the complexity, requiring careful communication to avoid confusion.

Then came the technical execution. IT systems had to be separated. Contracts had to be assigned to the appropriate entity. Intellectual property had to be divided. Employee transfers had to be managed sensitively. Each decision had tax implications, legal ramifications, and operational consequences.

On April 22, 2019, KPIT Technologies (NSE:KPITTECH | BSE:542651) announced listing of its new stock on NSE and BSE. This follows KPIT's merger and demerger transaction with Birlasoft, announced in January 2018 and effective from Jan 2019. The transaction resulted in two publicly-traded specialized technology companies – KPIT Technologies – focused on automotive engineering and mobility solutions; and Birlasoft – focused on IT services.

The market's initial reaction was skeptical. Here was a company that had voluntarily made itself smaller, operating in a single vertical, competing against global giants. The new KPIT Technologies was just 30-40% the size of the pre-merger entity in terms of revenue.

But Pandit and Patil saw what others didn't. They understood that in the age of software-defined vehicles, being the best automotive software company was far more valuable than being a mediocre conglomerate. They bet that focus would trump scale, that depth would beat breadth, and that specialization would outperform diversification.

As KPIT's new stock began trading on April 22, 2019, few could have predicted what would happen next. The company that had just divested 70% of its business was about to embark on one of the most spectacular growth stories in Indian corporate history. The bold bet on focus was about to pay off in ways that even its architects might not have fully anticipated.

VI. Post-Demerger Transformation: Pure-Play Automotive (2019–Present)

The morning of April 23, 2019, brought a new reality for KPIT. The company that once boasted 15,000 employees now had fewer than 6,000. Revenues had shrunk from over $500 million to around $200 million. By conventional metrics, KPIT had become smaller, weaker, more vulnerable. Yet Kishor Patil stood before his team with unmistakable confidence: "We are not smaller; we are sharper."

What followed would vindicate this confidence in spectacular fashion. Since April 22, 2019, KPIT Technologies's market cap has increased from 28.50B to 339.82B, an increase of 1,092.48%. That is a compound annual growth rate of 47.05%.

But the transformation went far deeper than financial metrics. The new KPIT wasn't just a smaller version of the old one—it was a fundamentally different company with a radically different approach to the automotive industry.

"Focus is a powerful concept, and it has given us a tremendous edge," Patil asserts. This focus manifested in multiple ways. First, KPIT doubled down on the megatrends reshaping mobility: electrification, autonomous driving, connected vehicles, and software-defined architectures. These weren't just buzzwords; they became the organizing principles for everything KPIT did.

The company restructured itself around six key practices: Architecture & Networking, ADAS & Autonomous Driving, Connected Vehicle Solutions, Electrification, Manufacturing Software, and Middleware & AUTOSAR. Each practice wasn't just a service line; it was a center of excellence with deep domain expertise, proprietary tools, and accelerators.

The investment in R&D intensified dramatically. While the old KPIT spread its innovation budget across multiple industries, the new KPIT concentrated everything on automotive. The company began filing patents at an unprecedented pace, developing intellectual property that would differentiate it from both IT services companies and traditional engineering firms.

Strategic acquisitions accelerated the capability building. Each acquisition was surgical, targeted at specific capability gaps:

- PathPartner Technologies (2022) brought expertise in intelligent edge solutions critical for ADAS and autonomous driving

- Technica Engineering (2023) added specialized automotive ethernet and connectivity capabilities

- Microfuzzy deepened electric powertrain expertise

- Somit Solutions enhanced software testing and validation capabilities

But the real breakthrough came in client relationships. Free from the constraints of being a diversified company, KPIT could now position itself as a pure-play automotive specialist. The pitch was simple but powerful: "We do one thing, and we do it better than anyone else."

Major automotive OEMs took notice. KPIT Technologies announced their partnership with Honda to realize the journey of Honda's Software-Defined Mobility (SDM). With Honda's next-generation software architecture and control-safety technology and KPIT's deep domain & software expertise, Honda will continue to provide various services and enhanced value to customers around the world. The partnership in mid to long term will expand to over 2,000 Software and Vehicle System Professionals from KPIT across the globe to power Honda's SDM roadmap until year 2030 and beyond.

The Renault partnership followed a similar pattern. KPIT, a global leader in automotive and mobility software, will bring its expertise to Renault Group in creating a world-class technology solution for the next decade. KPIT software scope in the SDV programs will encompass contributions for ADAS, Chassis, Body Electronics, Platforms, Systems Engineering, and Vehicle validation. KPIT will globally deploy 600+ engineers, multiple software IPs, and platforms to bring scale and success to this partnership.

These weren't typical vendor relationships. KPIT was becoming embedded in its clients' product development cycles, participating in strategic decisions about vehicle architectures, and co-creating the software platforms that would power the next generation of vehicles.

The financial performance reflected this strategic clarity. Revenue growth accelerated, margins expanded, and cash generation improved. But more importantly, the quality of revenue changed. Instead of commodity IT services work, KPIT was now engaged in strategic, long-term programs with multi-year visibility.

There are more than 10 million vehicles on the road globally equipped with software solutions developed by KPIT technologies. Every vehicle running KPIT software became a testament to the company's capabilities, a rolling advertisement for its expertise.

The employee value proposition transformed as well. The old KPIT competed with every IT services company for talent. The new KPIT attracted engineers who specifically wanted to work on automotive technology. It is one of the largest independent software and system integration partner to the mobility ecosystem with 13,000 employees.

By 2024, the transformation was complete. KPIT had evolved from a company that happened to have automotive clients to a company that lived and breathed automotive technology. The focus that seemed like a risky bet in 2019 had become its greatest competitive advantage. In a world where cars were becoming computers on wheels, KPIT had positioned itself as the company that understood both worlds better than anyone else.

VII. Current Business & Market Position

The Numbers Tell a Story of Exceptional Execution

Standing at the close of fiscal year 2024, KPIT's transformation from a diversified IT services company to a focused automotive software powerhouse has delivered results that vindicate every difficult decision made along the way.

KPIT clocks FY24 $ revenue growth of 40.4% and PAT growth of 56%, beating increased guidance for the year. These aren't just good numbers; they're exceptional by any standard. Consider that this growth came during a period when global automotive production faced headwinds from chip shortages, inflation, and economic uncertainty.

The company's financial trajectory tells a compelling story of accelerating momentum:

KPIT Technologies announced financial results for Q2FY25 with CC revenue growth of 20.1% Y-o-Y and $ revenue growth. Quarter after quarter, KPIT has delivered consistent growth, with marked 15th consecutive quarter of steady revenue and EBITDA growth. This consistency in a cyclical industry like automotive speaks to the structural nature of KPIT's growth—this isn't about catching a temporary wave but riding a fundamental transformation of the industry.

The Strategic Client Model

KPIT's go-to-market strategy represents a deliberate choice of depth over breadth. The company focuses on what it calls its "T25 clients"—the top 25 automotive OEMs and Tier-1 suppliers globally. The partnership with Honda will expand to over 2,000 Software and Vehicle System Professionals from KPIT across the globe to power Honda's SDM roadmap until year 2030 and beyond.

This isn't about having Honda as a client; it's about having 2,000 engineers embedded in Honda's transformation journey. Similarly, with Renault, KPIT's software scope encompasses contributions for ADAS, Chassis, Body Electronics, Platforms, Systems Engineering, and Vehicle validation, with KPIT globally deploying 600+ engineers.

These relationships go beyond traditional vendor-client dynamics. KPIT engineers sit in client design centers, participate in architecture decisions, and often know the client's product roadmap better than many of the client's own employees. This deep integration creates switching costs that go beyond commercial considerations—KPIT becomes part of the client's intellectual DNA.

Technology Leadership and Innovation

KPIT has been a premium member of AUTOSAR consortium since 2005 and has actively contributed to drive the consortium efforts in software standardization. This early bet on industry standards has paid off handsomely. Today, as every automotive company grapples with software standardization, KPIT's two-decade expertise in AUTOSAR has become invaluable.

The company's patent portfolio continues to expand, with 58 patents filed and 51 patented rights granted. These aren't defensive patents but offensive weapons—technologies that clients specifically seek out KPIT to access.

Global Footprint, Local Presence

The company is headquartered in Pune and has development centers in Europe, USA, Brazil, Japan and China, apart from India. But this global presence isn't about labor arbitrage—it's about being where automotive innovation happens. The Munich center works closely with German OEMs on next-generation architectures. The Japan center understands the unique requirements of Japanese automotive philosophy. The Detroit presence ensures deep integration with American automotive giants.

Financial Strength and Market Recognition

The market has recognized KPIT's transformation with remarkable revaluation. The market capitalisation of KPIT Technologies stood at over ₹41,500 crore as of December 16, 2023. In the past three years, KPIT share price has appreciated over 1,279% return to investors.

But beyond the stock price appreciation, the quality of earnings has improved dramatically. EBITDA margins have expanded from the mid-teens to over 20%, reflecting the value clients place on KPIT's specialized expertise. Cash generation has strengthened, giving the company firepower for strategic investments without diluting shareholders.

The Competitive Moat Deepens

What makes KPIT's position particularly defensible is the convergence of multiple competitive advantages:

- Domain Expertise: Two decades of exclusive focus on automotive software

- Scale in Specialization: 13,000 engineers focused solely on automotive

- Client Relationships: Multi-decade partnerships with strategic clients

- Technology Assets: Proprietary tools, accelerators, and platforms

- Ecosystem Position: Premium memberships in key industry consortiums

The company's recent performance demonstrates that the automotive software opportunity is not just large but accelerating. Basis committed investments by Strategic Clients, a strong pipeline and solid wins of $261 million in Q4, we continue to witness robust demand. We start FY25 on a strong footing and expect to deliver CC revenue growth of 18%-22% with EBITDA margins of 20.5%+.

As vehicles transform from mechanical products to software platforms, KPIT has positioned itself at the center of this transformation. The company that chose to become smaller to become better has proven that in technology, focus and expertise trump size and diversification every time.

VIII. Playbook: Business & Investing Lessons

Lesson 1: The Power of Saying No

The most profound lesson from KPIT's journey isn't about what they chose to do—it's about what they chose not to do. KPIT divested over 70% of its business to zero in on automotive software solutions. In a business culture that celebrates growth at any cost, KPIT demonstrated that strategic subtraction can be more valuable than addition.

Consider the opportunity cost: The IT services business they divested was growing, profitable, and had excellent prospects. But keeping it would have meant diluted focus, divided resources, and confused positioning. By saying no to 70% of their revenue, they said yes to becoming exceptional at one thing.

For investors, this teaches a crucial lesson: Companies that have the courage to narrow their focus often create more value than those that try to be everything to everyone. Look for management teams willing to make hard choices, even when those choices temporarily reduce size or revenue.

Lesson 2: Timing Technology Transitions

KPIT's journey offers a masterclass in timing technology transitions. They didn't jump into automotive software when it was hot; they built capabilities when it was still emerging. Joining AUTOSAR as a premium member in 2005 seemed premature then—AUTOSAR was just a consortium with ambitious ideas. Today, it's the foundation of automotive software architecture.

The lesson: The best time to enter a transformative technology market is before it's obvious, but after the direction is clear. KPIT entered automotive software when cars were still primarily mechanical, but the digitalization trend was unmistakable. They built capabilities when competition was limited and client relationships were available.

Lesson 3: The Compound Effect of Domain Expertise

The Cummins partnership catapulted revenues from $10 million to $100 million. But the real value wasn't the revenue multiplication—it was the domain expertise accumulated. Every project, every challenge, every client interaction added to KPIT's understanding of automotive systems.

This expertise compounds over time. The engineer who worked on engine control systems in 2005 understands vehicle architectures in ways that can't be learned from textbooks. The team that struggled with early AUTOSAR implementations now guides global OEMs through software transformation.

For investors: Companies with deep domain expertise have moats that are nearly impossible to replicate quickly. Money can buy talent and technology, but it can't buy two decades of accumulated knowledge.

Lesson 4: Strategic Corporate Restructuring as Value Creation

The Birlasoft merger-demerger wasn't financial engineering for its own sake—it was value creation through strategic clarity. By creating two focused companies from one diversified entity, KPIT unlocked value that the market couldn't see in the combined entity.

The lesson extends beyond KPIT: When businesses have fundamentally different economics, growth trajectories, and investment needs, keeping them together destroys value even if it provides diversification. The market values strategic clarity over diversified complexity.

Lesson 5: Client Concentration as Strength, Not Weakness

Conventional wisdom warns against client concentration. KPIT turned this on its head by deliberately concentrating on 25 strategic clients. The Honda partnership alone will expand to over 2,000 Software and Vehicle System Professionals from KPIT.

This concentration isn't weakness—it's strength. By putting 2,000 engineers on a single client, KPIT becomes irreplaceable. The switching costs aren't just financial; they're operational, intellectual, and strategic. Honda would need years to replace the institutional knowledge KPIT has built.

Lesson 6: The Venture Capital Approach to Corporate Strategy

KPIT's transformation mirrors venture capital thinking: make concentrated bets on massive opportunities rather than diversified bets on moderate opportunities. They bet everything on one thesis: software would transform automobiles. When that thesis proved correct, the returns were exponential.

KPIT share price has appreciated over 1,279% return to investors in the past three years. These aren't equity market returns; these are venture-scale returns from a public company.

Lesson 7: Building for the Customer's Future, Not Their Present

When KPIT began investing in autonomous driving and electrification capabilities, most of their clients weren't asking for these services. But KPIT understood that by the time clients asked, it would be too late to build capabilities.

"For years, banking was the biggest spender on technology. Now, it's automotive." KPIT positioned itself for this shift before it happened, not after.

The Meta-Lesson: Courage in Capital Allocation

Perhaps the overarching lesson is about courage in capital allocation. Every decision—from the Cummins partnership to the Birlasoft demerger—required betting the company on a vision of the future. These weren't incremental decisions; they were transformational ones.

For investors, KPIT's journey illustrates that the biggest returns often come from companies willing to make bold, concentrated bets on structural transformations. The key is distinguishing between reckless gambling and calculated courage. KPIT's bets were always grounded in deep domain understanding and clear strategic logic.

The playbook KPIT has written isn't just about building an automotive software company. It's about having the courage to become smaller to become better, the wisdom to build capabilities before they're needed, and the discipline to say no to good opportunities in pursuit of great ones.

IX. Analysis & Bear vs. Bull Case

Bull Case: Riding the Software-Defined Vehicle Revolution

The bull case for KPIT rests on a fundamental premise: we are witnessing the most significant transformation in automotive history since Henry Ford's assembly line, and KPIT sits at the epicenter of this change.

1. Structural Growth in Automotive Software The automotive software market is expected to grow from $20 billion to over $80 billion by 2030. But this isn't just market growth—it's a fundamental reallocation of value. Where mechanical components once differentiated vehicles, software now determines competitiveness. More than 10 million vehicles on the road globally are equipped with software solutions developed by KPIT. Each of these vehicles is a proof point, a reference client, a competitive moat.

2. Irreplaceable Partner Status The Honda partnership will expand to over 2,000 KPIT professionals globally, while Renault will deploy 600+ engineers. These aren't vendor relationships; they're symbiotic partnerships. Replacing KPIT wouldn't just mean finding another supplier—it would mean recreating years of institutional knowledge, established working relationships, and deep system understanding. The switching costs are prohibitive.

3. Margin Expansion Trajectory KPIT increased its FY25 EBITDA outlook to 21%+ from earlier 20.5%+. This margin expansion isn't coming from cost-cutting but from value creation. As KPIT moves up the value chain from services to platforms to intellectual property, margins should continue expanding. The company is transitioning from selling time to selling expertise to selling products.

4. Technology Disruption as Opportunity Every disruption in automotive—electrification, autonomous driving, connected vehicles—creates opportunity for KPIT. Legacy OEMs need partners who understand both traditional automotive systems and new technologies. New entrants need partners who can help them navigate automotive complexity. KPIT serves both.

5. Financial Strength Enabling Strategic Flexibility Strong cash generation and a debt-free balance sheet give KPIT the flexibility to invest in capabilities, acquire strategic assets, and weather industry downturns. The company can play offense while others play defense.

Bear Case: Concentrated Risks in a Cyclical Industry

1. Single Vertical Concentration Risk KPIT has bet everything on automotive. Unlike diversified IT services companies that can offset weakness in one vertical with strength in another, KPIT is entirely exposed to automotive cycles. A prolonged automotive downturn—whether from recession, technology disappointment, or changing consumer preferences—would directly impact KPIT.

2. Customer Concentration Vulnerability While deep client relationships are a strength, they're also a vulnerability. The Honda partnership expanding to 2,000 professionals means massive exposure to Honda's success or failure. If Honda's EV strategy fails or its market share declines, KPIT suffers proportionally.

3. Technology Disruption Risk KPIT is betting on certain technology trajectories—AUTOSAR standards, traditional OEM transformation, evolutionary rather than revolutionary change. If the industry shifts to radically different architectures, if new entrants like Tesla or Chinese EV makers create entirely different software paradigms, KPIT's expertise could become obsolete.

4. Talent War Intensification As every technology company recognizes the automotive opportunity, competition for specialized talent intensifies. Google, Apple, Amazon, and Microsoft are all building automotive teams. They can offer compensation packages and career opportunities that KPIT might struggle to match.

5. Margin Pressure from Commoditization As automotive software matures, what's specialized today becomes standardized tomorrow. KPIT must continuously move up the value chain to maintain margins. If they fail to innovate faster than commoditization, margins will compress.

6. Geographic and Geopolitical Risks Rising protectionism, data localization requirements, and geopolitical tensions could fragment the global automotive market. KPIT's model assumes relatively free movement of talent and technology across borders. Trade wars or technology restrictions could disrupt this model.

The Balanced View: Execution Will Determine Outcome

The truth likely lies between the extremes. KPIT has positioned itself brilliantly for the software-defined vehicle era, but execution will determine whether it captures the opportunity.

Key Monitorables for Investors:

- Client Diversification Progress: Are they reducing dependence on top clients while maintaining depth?

- Technology Leadership Indicators: Patent filings, consortium participation, client wins in emerging technologies

- Margin Trajectory: Sustained expansion would validate the value-addition thesis

- Talent Metrics: Attrition rates, hiring quality, capability building investments

- Competitive Win Rates: Are they winning against global giants in strategic deals?

The bull case seems stronger given current momentum—market cap has increased from 28.50B to 339.82B since April 2019, a compound annual growth rate of 47.05%. But the bear risks are real and require constant monitoring.

For long-term investors, KPIT represents a clear bet: if software truly becomes the defining element of vehicles, and if traditional OEMs successfully navigate the transformation, KPIT will be a massive winner. If either assumption proves wrong, the concentration that enabled exceptional returns could lead to exceptional losses.

The investment decision ultimately comes down to one's conviction about the automotive industry's transformation trajectory and KPIT's ability to maintain its competitive position through that transformation.

X. Epilogue & "What's Next"

As Kishor Patil looks out from KPIT's Pune headquarters, the view has changed dramatically from that day in 1990 when two chartered accountants decided to build a technology company. The parking lot below is filled with test vehicles—some electric, some autonomous, all running KPIT software. The irony isn't lost on him: they started by helping businesses with accounting software; now they're helping vehicles think.

"Focus is a powerful concept, and it has given us a tremendous edge." These words, spoken after the dramatic restructuring, have proven prophetic. But focus is not a destination; it's a continuous journey. The question now is: what's next for a company that has already achieved what seemed impossible?

The Software-Defined Future is Just Beginning

While KPIT has established itself in the current paradigm of automotive software, the real transformation is just starting. Vehicles are evolving from products to platforms, from purchases to services. The car you buy tomorrow might have the same hardware for a decade, but its capabilities will continuously evolve through software updates.

This shift fundamentally changes the automotive business model. OEMs won't just sell cars; they'll sell experiences, features, and capabilities delivered through software. KPIT's role evolves from helping build cars to helping operate automotive platforms that generate recurring revenue streams for decades.

We are investing in AI technologies fine-tuned with automotive-specific data. Our AI philosophy is rooted in developing human-centric, innovative, safe, and responsible AI solutions that drive value creation for our clients.

The China Question

One of KPIT's most intriguing strategic moves is its increased focus on China. While geopolitical tensions make this complicated, the reality is undeniable: China is becoming the epicenter of automotive innovation, particularly in electric vehicles. Chinese automakers are moving faster, taking more risks, and reimagining what vehicles can be.

There are new relationships being explored and built with the Passenger Car and Truck makers in China and Rest of Europe outside Germany. This isn't just geographic expansion; it's about being where innovation happens, regardless of political complexity.

The Truck and Commercial Vehicle Opportunity

We have been developing new sub-verticals viz Trucks and Off-highway. There are sizable opportunities through these investments, and they are now contributing to building our pipeline across the geographies. These will contribute to our growth from the second half of the next financial year.

Commercial vehicles represent a massive, underappreciated opportunity. While passenger vehicles get attention, commercial vehicles are where autonomous driving might first become reality. A truck that drives itself on highways is easier to achieve than a car navigating city streets. The economics are more compelling—a self-driving truck can operate 24/7, transforming logistics economics.

The Ecosystem Play

KPIT's future isn't just about bilateral relationships with OEMs. It's about orchestrating ecosystems. As vehicles become platforms, they need to integrate with smart cities, energy grids, insurance systems, and service networks. KPIT's role evolves from software provider to ecosystem orchestrator.

The recent acquisitions hint at this direction. Each acquisition adds a piece to a larger puzzle—not just capabilities but connections, relationships, and ecosystem positions.

The Sustainability Imperative

Launch of ECOVOYAGE 2030, KPIT's journey towards Sustainability. Goals anchored on Science-based Targets towards carbon-neutral footprint.

This isn't corporate greenwashing. In automotive, sustainability is becoming a core differentiator. KPIT's software directly impacts vehicle efficiency, emissions, and environmental impact. Every optimization in their code translates to real-world environmental benefits multiplied across millions of vehicles.

The Talent Transformation

The company that started with two chartered accountants now employs 13,000 automotive software specialists. But the next phase requires different capabilities—AI experts, data scientists, cybersecurity specialists, user experience designers. KPIT must transform its workforce while maintaining its engineering culture.

We have launched a new ESOP scheme to strengthen the long term incentivization for our people. This isn't just about retention; it's about alignment. When engineers own stakes in the company, they think like owners, not employees.

The Ultimate Question: What Defines KPIT?

Is KPIT an Indian company that happens to be global, or a global company that happens to be headquartered in India? The answer matters less than the reality: KPIT represents a new model for technology companies from emerging markets. Instead of competing on cost, they compete on expertise. Instead of being back-office providers, they're innovation partners.

As the automotive industry undergoes its greatest transformation, KPIT has positioned itself not as a spectator but as an architect of change. The company that chose to become smaller to become better now faces its next choice: having achieved focus, how does it achieve scale without losing what makes it special?

The answer will unfold over the coming decade. But if the past is prologue, expect KPIT to make choices that seem counterintuitive at first but brilliant in hindsight. In a world where everyone is trying to be everything, KPIT has proven that being one thing exceptionally well is the ultimate competitive advantage.

For investors, entrepreneurs, and industry observers, KPIT's journey offers a masterclass in strategic transformation. It demonstrates that in technology, courage matters more than capital, focus matters more than size, and expertise matters more than everything else.

The road ahead for KPIT is as exciting as the road traveled. As vehicles evolve from mechanical marvels to digital platforms, KPIT stands ready to power that transformation. The two chartered accountants who started with a dream of building a technology company have built something far more valuable: a company that's helping reimagine how the world moves.

The story is far from over. In many ways, it's just beginning.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube