Carlisle Companies: From Pennsylvania Tire Shop to Building Envelope Empire

I. Introduction & The Big Picture

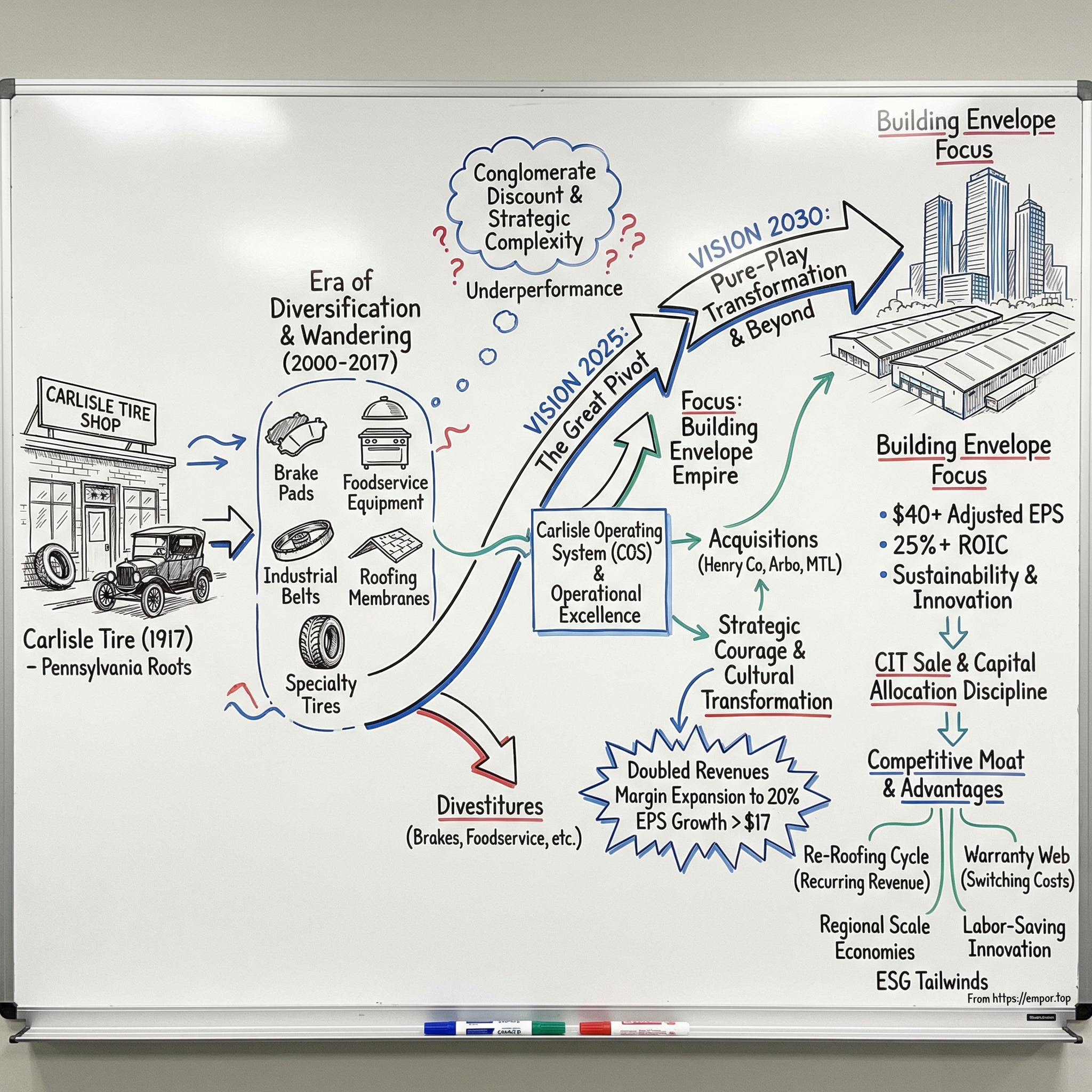

Picture this: A century-old tire repair shop in small-town Pennsylvania, founded when Model T Fords still ruled the roads, somehow transforms itself into a $20 billion market cap powerhouse that waterproofs America's skyscrapers and keeps Amazon warehouses dry. That's the Carlisle Companies story—a transformation so complete that if founder Charles S. Moomy walked into headquarters today, he wouldn't recognize a single product line.

The numbers tell one story: approaching $6.2 billion in revenues for 2024, operating margins pushing toward 20%, and a stock price that's quintupled over the past decade. But the real story is about strategic courage—the willingness to kill your darlings, to walk away from businesses you've run for decades, and to bet everything on a single insight about where American construction was heading.

This is a masterclass in corporate reinvention. While General Electric floundered trying to manage its sprawling empire, while United Technologies spun itself into pieces, Carlisle quietly executed one of the most successful pivots in industrial history. They didn't just trim around the edges; they fundamentally reimagined what business they were in.

The transformation accelerated dramatically with Vision 2025, launched in 2018, which set audacious targets: double revenues from 2019 levels, achieve $15 earnings per share, maintain 20% operating margins. Four years in, they'd already blown past the EPS target with $17.58 in 2022. Now Vision 2030 aims even higher—$40+ adjusted EPS and 25%+ return on invested capital.

Today's Carlisle is laser-focused on the building envelope—the critical systems that keep water out and energy in. It's a massive market opportunity hidden in plain sight: every aging strip mall, every new distribution center, every storm-damaged roof represents potential revenue. The company estimates its total addressable market doubled from $15 billion in 2012 to $30 billion in 2022, and that's before factoring in infrastructure spending and climate resilience mandates.

The beauty of this business model? Once a Carlisle roof system is installed, with its 20-year warranty and integrated components, switching to a competitor becomes prohibitively complex. It's the razor-and-blades model applied to commercial construction—get specified into the building plans, and you've locked in decades of replacement revenue.

What follows is the inside story of how a tire company became a building products empire, why that transformation worked when so many conglomerate restructurings fail, and what it tells us about the future of American manufacturing. It's about recognizing when your century-old business model has run its course—and having the guts to build something entirely new.

II. The Century-Long Foundation (1917-2000)

The year is 1917. America has just entered World War I, the Russian Revolution is underway, and in the small Pennsylvania town that shares its name with the company, Charles S. Moomy is running a tire repair shop. Not manufacturing tires—just fixing them. The roads around Carlisle were rough, mostly unpaved, and pneumatic tires were still newfangled technology that failed constantly. Moomy saw opportunity in all those punctures.

What started as Carlisle Tire wasn't trying to compete with Goodyear or Firestone. Moomy understood something fundamental about business: you don't need to be the biggest to be successful, you just need to find your niche and execute flawlessly. His niche? Specialty tires for agricultural and industrial equipment—the unglamorous workhorses that bigger manufacturers ignored.

The company's early growth came from this contrarian positioning. While the giants fought over passenger car tires, Carlisle quietly dominated obscure but profitable segments: wheelbarrow tires, lawn mower tires, airport ground support equipment. By the 1950s, they'd built a reputation for solving problems others wouldn't touch. Need a tire for a experimental piece of mining equipment? Call Carlisle. Custom rubber compound for extreme temperatures? Carlisle could figure it out.

Post-World War II America transformed Carlisle's trajectory. The suburban building boom created insatiable demand for construction equipment, all needing specialized tires. The interstate highway system meant more truck traffic, more tire wear, more replacement demand. But rather than just ride this wave, Carlisle's leadership made a pivotal decision: become a holding company.

This wasn't the ego-driven conglomerate building that would later destroy companies like ITT or Gulf+Western. Carlisle's diversification followed a logic: acquire businesses that served similar end markets but didn't compete directly. A roofing membrane company made sense—same construction industry customers. Brake and friction materials? Natural extension of rubber expertise. Food service equipment? Well, that one was harder to justify, but the margins were attractive.

By the 1970s, Carlisle had evolved into something unique: a collection of niche industrial businesses, each typically holding the #1 or #2 position in narrow markets most people never thought about. The company culture that emerged reflected this approach—entrepreneurial business units run by operators who knew their industries cold, backed by patient capital from headquarters.

The Pennsylvania roots mattered more than outsiders realized. This wasn't Wall Street financial engineering; it was Rust Belt manufacturing pragmatism. Executives had dirt under their fingernails. They understood production floors, talked to foremen, knew which machines broke down and why. When they acquired a company, the first thing they did was visit the factory floor, not the executive suite.

Geographic expansion followed naturally. A roofing plant in Iowa to serve Midwest markets. A friction materials facility in Japan through joint venture. Each move was calculated, methodical—never betting the company on a single big swing. This conservatism would later prove crucial when the time came for real transformation.

The 1980s and 1990s saw Carlisle perfect its acquisition playbook. Target family-owned businesses in the second or third generation, where founders wanted liquidity but cared about legacy. Pay fair prices, keep existing management, provide capital for growth, share best practices. It wasn't sexy, but it worked. The company's annual reports from this era read like catalogs of obscure industrial products: single-ply roofing membranes, commercial kitchen equipment, specialty tires, wire and cable, brake pads.

Yet beneath this sprawl, a pattern was emerging. The construction materials businesses—particularly roofing—were growing faster and generating higher margins than everything else. Commercial buildings were getting bigger, flat roofs were replacing sloped ones, and energy efficiency was becoming a selling point. Carlisle's EPDM rubber roofing membranes were perfectly positioned for this shift.

By 2000, Carlisle Companies had grown to over $2 billion in revenues across dozens of business units. To outsiders, it looked like another unfocused industrial conglomerate destined for breakup. But inside the company, executives were already asking hard questions: What if we weren't trying to be everything to everyone? What if we picked our best business and went all-in?

The foundation was set, built on 83 years of operational excellence, acquisition expertise, and deep customer relationships. Now came the hard part—deciding what to keep and what to leave behind.

III. The Diversification Years & Strategic Wandering (2000-2017)

The dawn of the new millennium found Carlisle at a crossroads, though few recognized it at the time. The company's stock was trading at a conglomerate discount—that persistent markdown Wall Street applies to companies it can't easily categorize. Analysts would tour Carlisle's facilities and come away confused: "So you make roofing materials... and brake pads... and commercial kitchen equipment?" The story was too complicated, the synergies too abstract.

Inside headquarters, a quiet civil war was brewing. The construction materials division, particularly roofing, was posting 15% EBITDA margins while some industrial segments barely cleared 8%. The roofing team wanted more capital for expansion; the legacy tire business needed investment to stay competitive; the food service equipment division saw opportunity in casino expansion. Everyone had a compelling case, but there wasn't enough capital to fund every dream.

The early 2000s acquisition spree only amplified these tensions. Carlisle bought Dayco Industrial Power Transmission in 2001, adding conveyor belts to the portfolio. They acquired Tensolite in 2002, entering the high-performance cable market. Each deal made sense in isolation—decent businesses, reasonable prices, operational synergies with something in the portfolio. But collectively, they were building a harder-to-manage octopus.

Then came 2008. The financial crisis hit Carlisle's diverse portfolio like a shotgun blast—scattered damage everywhere, but nothing fatal. Construction materials revenues plummeted as commercial projects froze. Industrial segments saw orders evaporate. The food service division, surprisingly, held up best as restaurants kept replacing equipment even in tough times. This divergent performance sparked intense strategic debates: Was diversification protecting them or holding them back?

The recession's aftermath revealed an uncomfortable truth: Carlisle's unfocused structure was preventing it from capitalizing on recovery opportunities. While pure-play roofing competitors could tell a simple story to investors and raise capital cheaply, Carlisle had to explain why a roofing membrane purchase would fund growth better than investing in brake pads or restaurant equipment. The complexity tax was real and growing.

Between 2010 and 2015, management attempted strategic focus through operational excellence rather than portfolio surgery. They implemented lean manufacturing, centralized procurement, shared services—all the standard playbook moves. Margins improved incrementally, but the fundamental challenge remained: running a tire company required different skills than running a construction materials business, which required different skills than running a commercial kitchen equipment operation.

The construction materials division, meanwhile, was quietly becoming a juggernaut. The commercial roofing market was consolidating, sustainability mandates were driving demand for energy-efficient building envelopes, and climate change was making weatherproofing mission-critical. Carlisle's CCM division was capturing market share, innovating with new membrane technologies, and generating returns that made other divisions look pedestrian by comparison.

By 2016, the strategic wandering had produced a peculiar result: Carlisle had become excellent at running mediocre businesses efficiently. Operating margins had improved across the board, but they were optimizing local maxima while missing the global opportunity. The company was like a talented athlete playing three sports pretty well instead of focusing on the one where they could be world-class.

The board meetings from this period, according to those familiar with the discussions, were studies in frustration. Directors would review divisional performance, nod at incremental improvements, then return to the elephant in the room: Why not double down on construction materials? The answer always came back to transition risk, customer relationships, employee impact—all valid concerns that nevertheless perpetuated the status quo.

What finally broke the logjam wasn't internal pressure but external opportunity. Private equity firms had begun circling Carlisle's underperforming divisions, offering prices that made exit attractive. Meanwhile, construction materials acquisition targets were becoming available as founders aged out. The math was becoming undeniable: selling low-margin businesses at reasonable multiples and reinvesting in high-margin construction materials at similar valuations was pure arbitrage.

The transformation that followed would be radical, but it was rooted in these years of strategic wandering. Carlisle had learned what it was truly good at, understood where markets were heading, and built the operational capabilities to execute a massive pivot. Sometimes you need to wander in the wilderness before finding the promised land.

IV. Vision 2025: The Great Pivot (2018-2022)

The boardroom at Carlisle headquarters in early 2018 witnessed something rare in corporate America: leadership admitting the current strategy wasn't working and proposing to blow it up entirely. CEO Chris Koch stood before directors with a presentation that would have been career suicide at most companies: "We're going to sell or shut down businesses we've run for decades, businesses our employees have devoted careers to, businesses that still make money."

Vision 2025 wasn't born from crisis—Carlisle was profitable, growing, debt was manageable. It emerged from ambition and clarity. The target was audacious: reach $8 billion in revenues (nearly double 2019 levels), achieve 20% operating margins, deliver $15 earnings per share, and maintain 15% return on invested capital. But the real revolution was the how: transform from a diversified industrial conglomerate into a focused building products platform.

The Carlisle Operating System (COS) became the engine of transformation. This wasn't just lean manufacturing with a branded name—it was a comprehensive playbook for running industrial businesses at peak efficiency. Every acquisition would be put through the COS wringer: standardize processes, eliminate redundancies, optimize pricing, accelerate innovation cycles. The system could reliably add 300-500 basis points to operating margins within 24 months.

The divestiture drumbeat began immediately. In 2018, Carlisle sold its Thermax and Trimax brake businesses. The foodservice equipment platform went next. Each sale was painful—these were good businesses with loyal employees—but necessary. The capital recycling was ruthless: every dollar from divestitures went straight into construction materials acquisitions or organic growth investments.

The acquisition strategy was equally aggressive but more targeted. Carlisle wasn't just buying revenues; they were assembling a building envelope ecosystem. Arbo Holdings in 2018 brought specialty construction fasteners. Petersen Aluminum in 2019 added metal edging systems. Each deal filled a specific gap in the product portfolio, allowing Carlisle to offer complete building envelope solutions rather than individual components.

Cultural transformation proved harder than financial engineering. Carlisle had thousands of employees in businesses marked for divestiture. The company's approach was unusual: full transparency about strategic direction, generous severance packages, assistance finding buyers who would preserve jobs, and celebration of these businesses' contributions even as they were being sold. It wasn't perfect, but it maintained more goodwill than typical corporate restructurings.

The timing seemed terrible when COVID-19 hit in early 2020. Construction sites shut down, commercial projects were postponed, and Carlisle's newly focused strategy appeared vulnerable to a single industry's volatility. But the pandemic revealed an unexpected truth: buildings still needed roofs, warehouses for e-commerce required weatherproofing, and deferred maintenance created pent-up demand that would surge during recovery.

Management's response to the pandemic crisis showcased the power of focus. Instead of managing dozens of different businesses through distinct crisis responses, they could concentrate resources on construction materials. They maintained supply chains when competitors faltered, gained share from disrupted smaller players, and positioned for the recovery everyone knew was coming.

By 2021, Vision 2025 was ahead of schedule. The company that year acquired Henry Company for $1.575 billion, the largest deal in Carlisle's history. Henry brought building envelope systems for vertical surfaces—walls to complement Carlisle's horizontal roofing expertise. The strategic logic was compelling: contractors who installed Carlisle roofs could now waterproof entire buildings with integrated systems.

The financial results validated the strategy spectacularly. In 2022, just four years into Vision 2025, Carlisle reported $17.58 in earnings per share—already beating the 2025 target of $15. Operating margins in the construction materials segment approached 20%. Return on invested capital exceeded 15%. The stock price responded accordingly, outperforming industrial peers by wide margins.

But the real achievement wasn't hitting arbitrary financial targets—it was completing a cultural transformation. Carlisle had evolved from a holding company that happened to own construction materials businesses into a construction materials company that happened to have a few other operations. The mindset shift was profound: from portfolio management to category domination, from financial engineering to operational excellence, from diversification to focus.

The lesson for other industrial conglomerates was clear but difficult to execute: sometimes the best strategy is admitting your current strategy isn't working. Vision 2025 succeeded because it wasn't incremental optimization but fundamental restructuring. It required leadership to disappoint some stakeholders to delight others, to sacrifice breadth for depth, to choose clarity over optionality.

As 2022 ended with results exceeding every Vision 2025 target three years early, the question became: what next? The answer would be even more ambitious.

V. The Building Envelope Focus & Strategic Acquisitions

The boardroom atmosphere at Carlisle in July 2021 was electric. CEO Chris Koch was proposing the company's largest acquisition ever—$1.575 billion in cash for Henry Company, a building envelope systems provider that had been quietly dominating vertical waterproofing while Carlisle owned the horizontal roofing market. The strategic logic was compelling: contractors installing Carlisle roofs would now have access to integrated wall systems from the same supplier.

Henry generated revenue of $511 million and adjusted EBITDA of $119 million, representing an adjusted EBITDA margin of 23%, for the twelve months ending May 31, 2021. The purchase price represented 10.5x Henry's adjusted EBITDA when including run-rate cost synergies—a full valuation, but justified by the strategic fit. Henry controlled the flow of water, vapor, air and energy in buildings, perfectly complementing Carlisle's roofing expertise.

The Henry acquisition wasn't just about products—it was about market positioning. More than half of Henry's revenue derived from products that improve energy efficiency, elevating Carlisle's sustainability narrative at a time when ESG considerations were becoming central to institutional investment decisions. The company's 80-year heritage and trusted brand relationships couldn't be replicated organically.

But even as Carlisle was doubling down on construction materials, they maintained a hedge through their Interconnect Technologies division. In May 2019, Carlisle Interconnect Technologies acquired MicroConnex Corporation, a manufacturer of highly engineered microminiature flex circuits for medical and test & measurement markets. Later that year, they added Providien LLC, expanding into medical device markets including robotics, drug delivery, oncology, and kyphoplasty.

These medical technology acquisitions seemed incongruous with the building envelope focus, but they reflected a strategic optionality—maintaining exposure to high-growth healthcare markets while the construction materials transformation played out. The medical device components business generated attractive margins and provided diversification against construction cyclicality.

The operational integration of Henry showcased Carlisle's evolved M&A capabilities. Rather than immediately merging sales forces or eliminating redundancies, they maintained Henry's brand identity and customer relationships while selectively applying the Carlisle Operating System to manufacturing processes. The acquisition was expected to generate pre-tax cost synergies of approximately $30 million by 2025, but the real value lay in revenue synergies—cross-selling opportunities that wouldn't show up in spreadsheets for years.

The transformation accelerated with strategic divestitures that funded growth investments. In 2021, Carlisle announced the sale of its Brake and Friction business, a profitable but non-core operation that no longer fit the building products vision. Each divestiture was executed with surgical precision—maximizing value while minimizing disruption to remaining operations.

By 2023, the portfolio surgery was nearly complete. Carlisle had sold CFT (Carlisle Fluid Technologies) and CBF (Carlisle Brake & Friction), exiting businesses that had been part of the company for decades. These weren't distressed sales—they were strategic value maximization plays, selling good businesses to buyers who valued them more highly than the market valued them within Carlisle's conglomerate structure.

The 2024 acquisition of MTL Holdings represented the final piece of the building envelope puzzle. Carlisle purchased MTL from GreyLion Partners for $410 million in cash. MTL generated revenue of $132 million for the twelve months ended February 29, 2024, making it a smaller deal than Henry, but strategically crucial.

MTL's portfolio included pre-fabricated edge metal products under the flagship brands of Metal-Era and Hickman, as well as non-insulated aluminum composite material (ACM) architectural wall panels under the Citadel brand. This acquisition established Carlisle as one of the industry's most comprehensive providers of architectural metal products, including "roof-to-grass" color coordinated metal building envelope solutions.

The MTL deal valuation was more conservative than Henry—8.7x adjusted EBITDA inclusive of run-rate cost synergies and net of the $43 million tax step up benefit—reflecting both market conditions and Carlisle's increased discipline. Cost synergies of approximately $13 million were expected within the first three years, with the transaction expected to be approximately $0.60 accretive to adjusted EPS in the first full fiscal year.

What emerged from this acquisition spree was not just a larger company but a fundamentally different one. Carlisle had assembled a complete building envelope ecosystem: roofing membranes, wall systems, edge metal, fasteners, adhesives, coatings. A contractor could now specify Carlisle products from foundation to roofline, creating switching costs that would lock in customer relationships for decades.

The medical technology business remained an outlier, but even this made strategic sense. It provided exposure to secular growth trends in healthcare, generated cash for building products investments, and could be sold when valuations peaked. It was optionality incarnate—a valuable asset that didn't need to fit the narrative to create shareholder value.

The transformation from conglomerate to focused platform required not just strategic vision but tactical excellence. Each acquisition was integrated using the Carlisle Operating System, each divestiture was timed for maximum value, each synergy was tracked and measured. This wasn't financial engineering—it was operational transformation at scale.

VI. Vision 2030: The Pure-Play Transformation (2023-Present)

The December 2023 investor presentation felt different from typical corporate strategy unveilings. Chris Koch, standing before a room of analysts who'd watched Carlisle's transformation for years, wasn't promising incremental improvements. He was declaring victory on Vision 2025—three years early—and immediately raising the stakes with Vision 2030.

Vision 2030 outlines the next phase of profitable growth and superior returns following the pivot of Carlisle's portfolio of general industrial businesses to a pure play building products company and the successful achievement of its key Vision 2025 objectives three years ahead of plan. The financial targets were audacious: Adjusted EPS of $40+ and ROIC of 25%+, more than doubling earnings from the 2023 baseline while maintaining world-class returns on capital.

But the real story wasn't the numbers—it was the strategic clarity. After a century of meandering through various industrial businesses, Carlisle had found its true calling. The company was no longer trying to be many things to many people; it was committed to being the best at one thing: building envelopes for commercial and industrial structures.

The mega-trends supporting this focus were compelling. America's commercial building stock was aging rapidly, with the average roof now 17 years old and approaching the 20-year replacement cycle. Climate change was driving more severe weather events, accelerating roof damage and replacement needs. Energy efficiency mandates were tightening, making high-performance building envelopes mandatory rather than optional. And perhaps most critically, skilled labor shortages in construction were creating demand for simpler, faster installation systems—exactly what Carlisle specialized in.

Chris Koch commented, "Vision 2030 presents a new chapter in Carlisle's now 106 year journey as a company, focused on unleashing the full potential of our pure play building products portfolio with best-in-class returns." The confidence wasn't misplaced—Carlisle had already demonstrated the power of focus with margins expanding from 15% in 2010 to 27% in 2023.

The transformation wasn't complete without one final, dramatic move. In early 2024, Carlisle announced the sale of Carlisle Interconnect Technologies (CIT) to Amphenol Corporation for $2.025 billion—a stunning valuation that validated management's timing. CIT had been a profitable, growing business serving aerospace and medical markets, but it no longer fit the pure-play building products vision.

The CIT sale crystallized everything Vision 2030 represented. Here was a business generating solid returns, with defensible positions in attractive markets, and Carlisle was walking away from it. Not because it was failing, but because it was a distraction. The proceeds would fund share buybacks, debt reduction, and strategic acquisitions in building products—a textbook example of portfolio optimization.

By the end of 2024, Carlisle had achieved record adjusted EPS of $20.20, a 30% increase over 2023, with full year revenue growth of 9% along with record adjusted EBITDA margin of 26.6% and ROIC of 28.5%. The company was already halfway to its $40 EPS target with six years remaining.

The operational excellence driving these results went beyond financial engineering. Carlisle had fundamentally reimagined how building products were designed, manufactured, sold, and serviced. The Carlisle Experience—their customer value proposition—integrated product innovation, technical support, warranty programs, and training into a comprehensive solution that created switching costs far beyond the products themselves.

Innovation investment accelerated under Vision 2030. R&D spending increased not just in absolute dollars but in focus—every project had to contribute to energy efficiency, labor savings, or system integration. The company developed self-adhering membranes that eliminated the need for adhesives, reducing installation time by 30%. They created integrated edge metal systems that coordinated perfectly with roofing membranes, eliminating compatibility issues that had plagued contractors for decades.

The sustainability narrative became central to the investment thesis. Carlisle leveraged mega trends around energy efficiency, labor savings and the re-roofing cycle that were expanding the company's market opportunity. Green building certifications were transitioning from nice-to-have to mandatory, and Carlisle's products were essential for achieving these standards.

Geographic expansion under Vision 2030 took a different form than historical international forays. Rather than building factories in emerging markets, Carlisle focused on following its multinational customers globally. When Amazon built distribution centers in Europe, Carlisle's roofing systems went with them. When Walmart expanded in Latin America, Carlisle was specified into the plans.

The two-segment structure—Carlisle Construction Materials (CCM) and Carlisle Weatherproofing Technologies (CWT)—provided clarity while maintaining operational flexibility. CCM focused on horizontal applications (roofs), while CWT handled vertical surfaces (walls) and specialty applications. The segments shared technology, customer relationships, and best practices while maintaining distinct go-to-market strategies.

Capital allocation under Vision 2030 reflected newfound discipline. The company committed to maintaining its 43-year streak of dividend increases while opportunistically buying back shares when valuations were attractive. M&A remained important but selective—only deals that strengthened the building envelope ecosystem and met strict return criteria would be considered.

The cultural transformation was perhaps most impressive. A company that had spent a century as a holding company for disparate businesses had evolved into a unified organization with a singular mission. Employees who had worked in tire factories or brake pad plants were either transitioned to new opportunities or had found roles in the building products divisions. The organization that remained was leaner, more focused, and more motivated than ever.

Market reception to Vision 2030 was initially mixed. Some investors questioned whether $40 EPS was achievable without significant multiple expansion or aggressive financial engineering. Others worried about concentration risk—what if commercial construction entered a prolonged downturn? But as quarterly results consistently exceeded expectations, skepticism gave way to enthusiasm.

The lesson from Vision 2030 wasn't just about strategic focus—it was about strategic courage. Carlisle had walked away from businesses generating billions in revenue, businesses they'd run successfully for decades, because they recognized that being good at many things prevented them from being great at one thing. In an era of index funds and diversified portfolios, Carlisle bet that investors would reward focus over diversification, excellence over adequacy, clarity over optionality.

VII. The Business Model & Competitive Advantages

Stand on a commercial rooftop anywhere in America, and you're likely standing on a Carlisle product. The ubiquity isn't accidental—it's the result of a business model so elegantly constructed that competitors struggle to replicate it even when they understand exactly how it works.

Carlisle achieved record adjusted EBITDA margin of 26.6% in 2024, a level that would be impressive for a software company, let alone a manufacturer of what many consider commodity building products. The Construction Materials segment achieved even more remarkable performance, with adjusted EBITDA margin of 32.8% in Q3 2024. These aren't temporary spikes—they represent sustainable competitive advantages built over decades.

The foundation of Carlisle's business model is the re-roofing cycle, a remarkably predictable revenue stream that provides ballast during economic volatility. Commercial roofs typically last 15-20 years, creating a replacement wave that's largely independent of new construction activity. When a roof fails, it gets fixed—recession or not. This isn't discretionary spending; it's emergency maintenance that can't be deferred without risking catastrophic building damage.

But Carlisle's genius lies not in serving this market, but in how they've structured their participation. The company doesn't just sell roofing membranes; they sell complete roofing systems with 20-year warranties. The warranty is the hook—it requires using Carlisle-approved contractors, Carlisle-specified installation methods, and often Carlisle accessories and adhesives. Once a building owner accepts a Carlisle warranty, they're essentially locked into the Carlisle ecosystem for two decades.

The Carlisle Experience, their branded customer value proposition, transforms a product sale into a consultative relationship. Technical representatives work with architects during building design, ensuring Carlisle products are specified into plans. They train contractors on installation techniques, creating a skilled workforce that prefers Carlisle products because they know them best. They provide on-site support during installation, reducing contractor risk and callbacks.

This service layer creates switching costs that transcend price competition. A contractor who's spent years learning Carlisle's installation methods, built relationships with Carlisle's technical team, and staked their reputation on Carlisle warranties won't switch to save 5% on material costs. The risk of installation errors, warranty disputes, and lost productivity far outweighs marginal savings.

The distribution strategy amplifies these advantages. Carlisle sells primarily through specialized roofing distributors who carry inventory, provide credit to contractors, and offer technical support. These distributors have invested millions in Carlisle-specific inventory and training. They're not just customers; they're partners whose success depends on Carlisle's success.

Labor-saving innovation has become increasingly critical as construction faces severe skilled worker shortages. Carlisle's self-adhering membranes eliminate the need for adhesives, reducing installation time by 30% and removing the complexity of adhesive application in various weather conditions. Their prefabricated accessories arrive ready to install, eliminating on-site fabrication. Every innovation that saves labor hours becomes a competitive advantage in a labor-constrained market.

The company estimates it doubled its total addressable market from $15 billion in 2012 to $30 billion in 2022, but this understates the opportunity. Climate change is accelerating roof replacement cycles—severe weather events that might have occurred once per decade now happen every few years. Energy efficiency mandates are forcing building owners to upgrade insulation and membranes even on functioning roofs. The shift to white reflective roofing for urban heat island mitigation creates replacement demand independent of roof condition.

Raw material integration provides another competitive edge. Carlisle produces its own polyiso insulation, EPDM rubber, and thermoplastic polyolefin (TPO) membranes. This vertical integration isn't about cost savings—it's about quality control and supply chain reliability. When raw material shortages hit the industry, Carlisle can prioritize its own production, maintaining customer deliveries while competitors scramble for supply.

The Carlisle Operating System drives continuous improvement across all operations. CCM's impressive 32.8% adjusted EBITDA margin reflected strong volume leverage, a positive raw material environment, and excellent operating execution through the Carlisle Operating System. COS isn't just lean manufacturing with a branded name—it's a comprehensive approach to operational excellence that touches everything from factory layouts to customer service protocols.

Pricing power in this business model comes from value creation rather than market power. Carlisle products command premium prices because they reduce total installed cost. A membrane that costs 10% more but installs 30% faster and lasts 20% longer provides clear economic value. The warranty protection adds insurance value. The technical support reduces contractor risk. Customers pay premiums not because they have to, but because the value proposition is compelling.

The competitive moat deepens with scale. Carlisle can afford more R&D investment, broader geographic coverage, deeper technical support, and more comprehensive training programs than smaller competitors. These investments raise the bar for competition while improving customer outcomes—a virtuous cycle that strengthens over time.

Geographic density matters more than most investors realize. Roofing materials are bulky and expensive to ship, creating natural regional markets. Carlisle's network of manufacturing facilities and distribution partnerships provides local availability and rapid delivery—critical when contractors need materials immediately for emergency repairs. This regional density creates micro-monopolies where Carlisle might have 40-50% market share in specific metropolitan areas.

The acquisition integration playbook amplifies organic advantages. When Carlisle acquires a competitor, they don't just cut costs—they upgrade capabilities. The acquired company's products get the Carlisle warranty backing, their contractors get Carlisle training, their distributors get Carlisle support. The acquired business typically sees margin expansion of 300-500 basis points within 24 months, not from cost cuts but from value creation.

Weather volatility, counterintuitively, benefits Carlisle. Severe storms create immediate replacement demand while also accelerating wear on undamaged roofs. Climate change isn't a risk to this business model—it's an accelerant. Every hurricane, hailstorm, and extreme temperature cycle creates future revenue opportunities.

The sustainability angle provides another competitive dimension. Green building solutions projected to save customers $20 billion demonstrate real economic value beyond environmental benefits. Carlisle's sustainable products now represent 70% of revenue, positioning them perfectly for increasingly strict building codes and ESG mandates. This isn't greenwashing—it's products that measurably reduce building energy consumption and operating costs.

Digital integration, while less visible than physical products, is becoming a differentiator. Carlisle's contractor portal provides project management tools, warranty tracking, technical documentation, and training resources. This digital ecosystem increases switching costs while improving contractor productivity—another win-win value creation.

The business model's resilience was proven during COVID-19. While new construction froze, re-roofing continued because building owners couldn't defer critical repairs. Carlisle maintained operations, supported contractors with safety protocols, and gained share from disrupted competitors. The pandemic wasn't a crisis—it was a market share opportunity.

This isn't a commodity business that happens to have good execution. It's a value creation machine built on deep customer relationships, technical expertise, operational excellence, and continuous innovation. The margins aren't lucky—they're earned through decades of compound improvements that competitors can't quickly replicate.

VIII. Capital Allocation & Financial Engineering

The capital allocation story at Carlisle reads like a masterclass in financial discipline married to strategic ambition. Carlisle Companies Incorporated (CSL) has increased its dividends for 49 consecutive years—a record that places them among an elite group of American companies that have navigated recessions, industry transformations, and global crises while never missing a dividend increase.

But the real story isn't the streak—it's how Carlisle transformed from a company that returned capital because it could to one that returns capital as part of a deliberate value creation strategy. The 2024 numbers tell the tale: $1.6 billion deployed in share repurchases, funded entirely by the CIT divestiture proceeds, while simultaneously investing nearly $700 million in strategic acquisitions.

The dividend philosophy evolved with the business transformation. The company is currently on a 43-year streak of consecutive annual increases to the quarterly rate. The company last hiked the dividend by 25% y/y to $0.50 per share in August of 2019, reflecting confidence in the building products pivot even before Vision 2025 was fully executed. The payout ratio remains conservative—around 14% of earnings—providing ample coverage while retaining capital for growth investments.

What makes Carlisle's capital allocation distinctive is the balance between discipline and opportunism. When the CIT sale closed in 2024 for $2.025 billion, management didn't rush to deploy the proceeds. They methodically executed share repurchases when the stock traded below intrinsic value, accelerating buybacks during market volatility while maintaining dry powder for acquisitions.

The M&A strategy under Vision 2030 represents evolved thinking about value creation. Rather than pursuing transformational deals that would recreate conglomerate complexity, Carlisle targets bolt-on acquisitions in the $100-500 million range that fill specific gaps in the building envelope ecosystem. Each deal must meet strict criteria: strategic fit with existing products, clear path to margin expansion through COS implementation, and returns exceeding the cost of capital within three years.

The integration playbook has become a competitive weapon. When Carlisle acquires a company, they don't just cut costs—they invest to accelerate growth. The Henry acquisition demonstrated this approach perfectly: maintaining brand identity and customer relationships while selectively applying operational improvements that expanded margins without disrupting market position.

Working capital management in a cyclical industry requires particular finesse. Carlisle maintains higher inventory levels than pure efficiency would dictate because product availability during peak construction season drives market share gains. They'd rather carry extra inventory through winter months than lose a customer who can't get materials when needed. This strategic inefficiency creates competitive advantage.

The company's approach to debt reflects operational confidence. Despite generating significant cash flow, Carlisle maintains modest leverage—typically 1.5-2x net debt to EBITDA—providing flexibility for opportunistic acquisitions while maintaining an investment-grade credit rating. They could leverage up for higher returns, but management prioritizes financial flexibility over optimization.

Share repurchase execution shows similar sophistication. Rather than announcing massive buyback programs that signal stock price floors to sellers, Carlisle executes opportunistically through 10b5-1 plans and accelerated share repurchase agreements. During the nine months ended September 30, 2024, we deployed $1.2 billion toward share repurchases, including $466 million in the current quarter, demonstrating consistent execution rather than sporadic activity.

The capital intensity of the business—typically 3-4% of sales—seems modest but represents significant competitive advantage. These aren't maintenance investments; they're capability expansions that increase production flexibility, reduce labor requirements, and improve product quality. A new TPO membrane line might cost $20 million but generate $100 million in high-margin revenue within three years.

Return on invested capital (ROIC) has become the north star metric, with management targeting 25%+ by 2030. This isn't financial engineering—it's operational excellence translating to superior returns. Every capital allocation decision gets evaluated through the ROIC lens: Will this acquisition improve portfolio ROIC? Will this organic investment exceed hurdle rates? Should we return capital rather than invest marginally?

The treatment of acquisition goodwill reveals management's long-term orientation. Rather than taking massive impairment charges that boost future reported returns, Carlisle maintains conservative goodwill valuations and focuses on cash-on-cash returns. They're more interested in actual value creation than accounting optics.

Tax optimization, while never the primary driver, enhances returns meaningfully. The CIT sale structure, the MTL acquisition's tax benefits, and strategic use of accelerated depreciation all contribute to after-tax returns that exceed pre-tax metrics. This isn't aggressive tax avoidance—it's thoughtful structuring that maximizes shareholder value within regulatory frameworks.

The geographic allocation of capital reflects market realities. Rather than pursuing international expansion for growth's sake, Carlisle concentrates investment in North American markets where they have competitive advantages. The few international ventures support global customers rather than pursuing local market share—a focused approach that maximizes returns on invested capital.

Innovation investment has accelerated under Vision 2030, but with clear commercial focus. R&D spending targets specific customer pain points—labor savings, installation speed, energy efficiency—rather than technical advancement for its own sake. Every innovation dollar must have a clear path to revenue generation within 24 months.

The balanced capital deployment philosophy—organic investment, strategic M&A, dividends, and buybacks—provides multiple paths to value creation. When acquisition multiples are high, Carlisle accelerates buybacks. When attractive targets emerge, they have the flexibility to act. When organic returns are compelling, they invest internally. This optionality is itself valuable.

Supplier financing programs represent hidden capital efficiency. By helping smaller suppliers access working capital financing, Carlisle maintains supply chain stability without tying up its own cash. These programs cost virtually nothing but create meaningful competitive advantage during supply chain disruptions.

The pension management strategy deserves mention. While many industrial companies struggle with underfunded pensions, Carlisle's disciplined funding and conservative return assumptions have created a fully funded status that removes a significant risk factor while freeing capital for growth investments.

Perhaps most impressively, Carlisle has achieved this capital allocation excellence while transforming the entire business. They've sold divisions, acquired companies, restructured operations, and refocused strategy—all while maintaining dividend growth, executing buybacks, and generating superior returns. It's not just good capital allocation; it's good capital allocation during fundamental transformation.

The lesson for investors is clear: great capital allocation isn't about following formulas or maximizing any single metric. It's about understanding the business deeply, maintaining discipline while preserving flexibility, and consistently making decisions that compound value over time. Carlisle's 49-year dividend growth streak isn't luck—it's the natural result of decades of thoughtful capital stewardship.

IX. Playbook: Lessons from the Transformation

The conference room at a Fortune 500 industrial conglomerate could be anywhere in America—Cleveland, Milwaukee, Charlotte. The CEO is presenting to the board, pointing to slides showing Carlisle's transformation from $2 billion in diversified industrial revenues to $5 billion in focused building products with margins that doubled along the way. "We should do exactly what Carlisle did," the CEO declares. Eighteen months later, that CEO is gone, the transformation has failed, and the company is trading at multi-year lows.

Why do some portfolio transformations create billions in value while others destroy it? Carlisle's playbook offers lessons, but they're not the ones most executives want to hear.

Lesson One: Portfolio simplification only works when you know what you're simplifying toward. Carlisle didn't just sell random businesses—they identified construction materials as their crown jewel and systematically divested everything that didn't strengthen that core. Too many companies start divesting before deciding what they want to become, creating strategic chaos rather than strategic focus.

The timing of Carlisle's transformation mattered enormously. They began pivoting toward building products just as megatrends—aging infrastructure, climate resilience, energy efficiency mandates—were accelerating. But this wasn't luck; it was pattern recognition. Management saw that their roofing business consistently outperformed other divisions not because of superior execution but because of superior industry structure.

Lesson Two: The conglomerate discount is real, but it's not automatic. Markets don't punish diversification per se—they punish complexity without purpose. Berkshire Hathaway trades at a premium despite ultimate diversification because investors understand the logic. Carlisle traded at a discount because investors couldn't understand why a roofing company also made brake pads and food service equipment.

The psychological challenge of transformation often proves harder than the operational challenge. Executives who built careers running diverse businesses must admit those businesses would be better owned by someone else. Board members who approved acquisitions must support divestitures. Employees must accept that good businesses will be sold not because they're failing but because they don't fit.

Lesson Three: Operational excellence must precede portfolio transformation. The Carlisle Operating System wasn't implemented after the transformation—it enabled it. By having standardized processes for improving any industrial business, Carlisle could maximize value before divestiture and accelerate integration after acquisition. Companies that try to transform through deal-making without operational capabilities usually fail.

The communication strategy during transformation determines success more than most executives realize. Carlisle was transparent about strategic direction years before execution, giving stakeholders time to adjust expectations. They celebrated divested businesses rather than disparaging them, maintaining morale and maximizing sale prices. They explained the why, not just the what.

Lesson Four: Building through the cycle requires conviction and capital. During the 2008 recession and COVID-19 pandemic, Carlisle maintained investment in their core businesses while competitors retrenched. This wasn't recklessness—it was calculated aggression based on understanding that downturns are temporary but market share gains can be permanent.

The acquisition integration philosophy matters more than acquisition strategy. Carlisle doesn't fully integrate acquisitions—they selectively apply best practices while maintaining what made the target successful. They'd rather leave money on the table than destroy value through forced integration. This patience creates better long-term outcomes than aggressive synergy capture.

Lesson Five: Customer switching costs in industrial markets are psychological, not just economic. Carlisle understood that contractors don't switch roofing systems to save 5% on materials—they switch when trust breaks down. By focusing relentlessly on contractor success through training, support, and warranty protection, Carlisle created switching costs that transcended price competition.

The role of middle management in transformation is consistently underestimated. Senior executives set strategy, but plant managers and regional sales directors execute it. Carlisle invested heavily in middle management development, ensuring that the people running factories and managing customer relationships understood and believed in the transformation strategy.

Lesson Six: When to pivot versus persevere isn't a data question—it's a pattern recognition question. Carlisle could have persevered with the conglomerate model indefinitely, generating decent returns for shareholders. But management recognized that "decent" was the enemy of "exceptional." They pivoted not from failure but from mediocrity, which requires more courage than pivoting from crisis.

The importance of financial flexibility during transformation cannot be overstated. Carlisle maintained conservative leverage throughout their pivot, providing capacity for opportunistic acquisitions and protecting against execution mistakes. Companies that leverage up to fund transformations often find themselves forced to abandon strategy when markets turn.

Lesson Seven: Creating switching costs in commodity-like markets requires systems thinking. Carlisle didn't just sell better roofing membranes—they created an ecosystem where every component worked better together. The warranty required system integration. The training reinforced product preferences. The technical support created relationship lock-in. Competitors selling individual products couldn't match this system-level value proposition.

Board composition during transformation matters enormously. Carlisle's board included executives who'd led similar transformations, providing pattern recognition and emotional support during difficult decisions. Boards dominated by status quo thinkers often sabotage transformations through risk aversion disguised as prudence.

Lesson Eight: Operational excellence in industrial businesses isn't about cost cutting—it's about capability building. The Carlisle Operating System improved margins not primarily through cost reduction but through faster innovation cycles, better quality, superior delivery, and enhanced customer support. These capabilities command premium pricing that more than offsets investment costs.

The sequencing of transformation moves can determine success or failure. Carlisle built capabilities before divesting businesses, strengthened the core before major acquisitions, and achieved operational excellence before financial engineering. Companies that reverse this sequence—financial engineering first, operations later—typically fail.

Lesson Nine: The power of focus compounds over time. In year one of transformation, Carlisle wasn't obviously better at roofing than as a conglomerate. By year five, the focused R&D, specialized sales force, dedicated management attention, and targeted capital investment had created capabilities that would have been impossible in a diversified structure.

Culture change follows structure change, not vice versa. Carlisle didn't try to change culture first—they changed the business portfolio, and culture evolved to match. The entrepreneurial, customer-focused culture they wanted emerged naturally from running focused businesses where everyone understood their role in value creation.

Lesson Ten: Knowing when transformation is complete might be the hardest decision. Some companies transform perpetually, never allowing new strategies to fully develop. Others declare victory too early, missing opportunities for further value creation. Carlisle's Vision 2030 suggests they see transformation as a continuous process with discrete phases rather than a one-time event.

The ultimate lesson from Carlisle's transformation isn't about portfolio strategy or operational excellence or capital allocation. It's about leadership courage—the willingness to walk away from businesses you know how to run toward opportunities you believe are better. Most industrial conglomerates won't follow Carlisle's playbook not because they can't, but because they won't. The playbook requires admitting current strategies aren't good enough, and that admission is harder than any operational challenge.

X. Bear vs. Bull Case Analysis

Bull Case: The Roofing Renaissance

Start with the math that matters: 4.5 billion square feet of commercial roofing in the United States, average lifespan of 20 years, replacement cost of $5-10 per square foot. That's $1.5 billion in mandatory replacement demand annually before considering storm damage, energy upgrades, or new construction. This isn't discretionary spending—when a roof fails, it gets fixed.

The energy efficiency megatrend is still in early innings. Only 10% of commercial buildings meet modern energy efficiency standards, and building codes are tightening annually. California's Title 24, requiring cool roofs on virtually all commercial buildings, is being replicated across states. Every code update creates replacement demand independent of roof condition—a building owner with a functioning 10-year-old black roof must install a white reflective system to comply.

Labor scarcity in construction is structural, not cyclical. The median age of roofers is 42 and rising. Vocational training programs have collapsed. Immigration restrictions limit worker supply. Carlisle's labor-saving innovations—self-adhering membranes, prefabricated accessories, simplified installation systems—become more valuable every year. Contractors will pay premium prices for products that solve their primary constraint: skilled labor availability.

The M&A pipeline remains robust with hundreds of regional building products manufacturers that would benefit from Carlisle's scale, operational expertise, and customer relationships. Private equity ownership of many targets creates regular opportunities as funds seek exits. Carlisle can acquire at 8-10x EBITDA and expand margins by 300-500 basis points through COS implementation—a repeatable value creation formula.

Climate change is an accelerant, not a risk. Every hurricane, hailstorm, and extreme weather event creates immediate replacement demand while accelerating wear on undamaged roofs. The increasing frequency and severity of weather events transforms roofing from a 20-year replacement cycle to a 15-year cycle—a 33% increase in annual demand.

Carlisle's margins have expansion runway despite already impressive levels. Private label penetration remains low, pricing discipline continues improving, and operational efficiencies compound annually. Best-in-class chemical companies achieve 30%+ EBITDA margins; there's no structural reason Carlisle can't approach these levels over time.

The balance sheet provides strategic flexibility with modest leverage and strong cash generation. Carlisle could easily support $3-4 billion in additional debt for transformational acquisitions while maintaining investment-grade ratings. This dry powder becomes particularly valuable during economic disruptions when distressed assets become available.

International expansion remains largely untapped. While Carlisle focuses on North American markets, the building envelope challenges are global. European energy efficiency standards exceed U.S. requirements. Asian commercial construction dwarfs American activity. Selective international expansion following multinational customers could double addressable markets.

ESG tailwinds are strengthening as institutional investors increasingly favor companies enabling carbon reduction. Carlisle's products directly reduce building energy consumption—the largest source of carbon emissions globally. As ESG mandates evolve from voluntary to mandatory, Carlisle's products transition from nice-to-have to must-have.

Valuation remains reasonable despite strong performance. At 20x forward earnings, Carlisle trades at a discount to pure-play building products peers and specialty chemical comparables. As the transformation story becomes better understood and results compound, multiple expansion to 25x or higher seems probable.

Bear Case: Storm Clouds Gathering

Commercial construction is notoriously cyclical, and leading indicators are flashing warning signs. Office vacancy rates remain elevated post-COVID. Retail apocalypse continues with store closures accelerating. Rising interest rates make new construction projects uneconomical. When new construction stops, the entire ecosystem suffers—even re-roofing gets deferred when building owners face financial stress.

Competition from larger players intensifies as everyone recognizes attractive building envelope economics. Owens Corning, with its massive fiberglass insulation business, could leverage existing contractor relationships to take roofing share. Standard Industries, having rolled up roofing manufacturers globally, has scale advantages Carlisle can't match. Private equity-backed competitors will accept lower returns to gain market position.

Raw material inflation could squeeze margins faster than price increases can offset. Petroleum-based inputs for membranes, MDI for polyiso insulation, aluminum for metal accessories—all face supply constraints and cost pressures. Carlisle's vertical integration provides some protection but can't fully insulate from input cost spikes that customers won't accept in higher prices.

Interest rate sensitivity is real and painful. Higher rates reduce new construction activity, decrease building values that justify roof replacement, and increase Carlisle's acquisition costs. The Fed's higher-for-longer stance could suppress construction activity for years, not quarters.

Residential exposure through CWT creates vulnerability to housing cycles. Mortgage rates above 7% have frozen housing turnover. New home construction faces affordability crisis. The residential recovery that management expects might be years away, creating a persistent drag on growth and margins.

Customer concentration risk is underappreciated. Large national roofing contractors control increasing market share, giving them negotiating leverage. If the top 10 customers represent 30% of revenues, losing even one relationship would materially impact results. Contractors play suppliers against each other, eroding margins over time.

Technology disruption, while seemingly unlikely in roofing, shouldn't be dismissed. Solar roof integration, drone inspection services, predictive maintenance analytics—all threaten traditional replacement cycles. If building owners can extend roof life through better maintenance, replacement demand could decline significantly.

The transformation story is largely complete, removing a key driver of multiple expansion. Investors who bought for the conglomerate-to-pure-play transformation have likely already won. Future returns must come from operational execution rather than strategic repositioning—a less exciting narrative for growth investors.

Regulatory risks are mounting as governments scrutinize chemical companies more closely. PFAS regulations could impact membrane chemistry. VOC restrictions could limit adhesive formulations. Environmental regulations add compliance costs while restricting product innovation. The regulatory landscape only becomes more challenging over time.

Execution risk in M&A increases as obvious targets get acquired. Carlisle must venture into adjacent markets or accept higher valuations to maintain acquisition-driven growth. Integration challenges multiply as acquisitions become less strategically obvious. The low-hanging fruit has been picked.

Capital allocation flexibility decreases as the dividend commitment constrains options. Carlisle is committed to generating superior shareholder returns and maintaining a balanced capital deployment approach, including investments in our businesses, strategic acquisitions, share repurchases and continued dividend increases. The 49-year dividend growth streak becomes a burden during downturns, forcing shareholder returns when capital preservation might be prudent.

Management succession looms as current leadership approaches retirement. Chris Koch has masterfully executed the transformation, but his successor faces the challenge of maintaining momentum without the burning platform of conglomerate underperformance. Second acts are harder than turnarounds.

Private equity ownership of competitors creates irrational competition. PE-backed companies will accept minimal returns to show growth, undercutting rational pricing. The industry could face years of margin pressure as financial buyers prioritize revenue growth over profitability.

Market saturation in core products limits organic growth potential. Carlisle already commands leading shares in key categories. Growing faster than GDP becomes increasingly difficult without category expansion or geographic diversification—both carrying execution risk.

The Verdict

The bull case rests on structural demand drivers and operational excellence. The bear case emphasizes cyclical risks and competitive threats. The truth, as always, lies somewhere between. Carlisle has transformed into a high-quality business with sustainable competitive advantages, but it operates in cyclical markets with real risks.

For long-term investors, the bull case appears stronger. The structural drivers—aging infrastructure, energy efficiency, labor scarcity—are multi-decade trends that overwhelm cyclical fluctuations. The operational excellence that generates 25%+ ROIC isn't easily replicated. The management team that executed one of the most successful industrial transformations deserves benefit of the doubt.

But the bear case provides useful caution. Paying growth multiples for a cyclical business at peak margins could disappoint. Competition will intensify. Execution won't always be flawless. The easy gains from transformation are captured; future value creation requires grinding operational excellence.

The investment decision ultimately depends on time horizon and risk tolerance. For patient investors who believe in American infrastructure renewal and commercial construction resilience, Carlisle offers compelling value. For those worried about near-term recession or rising rates, better entry points might emerge.

What's clear is that this isn't the sleepy industrial conglomerate of a decade ago. Whether bull or bear, investors must recognize they're analyzing a fundamentally different company—one whose future will be determined by building envelope dynamics rather than diversified industrial trends. That transformation alone is remarkable, regardless of where the stock trades tomorrow.

XI. Power, Counter-Positioning & Final Analysis

Hamilton Helmer's 7 Powers framework provides a lens to understand how Carlisle transformed from a mediocre conglomerate into a building envelope powerhouse generating 25%+ returns on invested capital. The powers they've developed—and those they lack—explain both the transformation's success and its limits.

Scale Economies: The Regional Paradox

Carlisle exhibits scale economies, but not in the traditional sense. This isn't about producing millions of identical units to spread fixed costs. Instead, it's about regional density creating micro-scale advantages. A roofing plant serving a 200-mile radius achieves local scale economies that matter more than national scale. Shipping costs for bulky materials create natural geographic boundaries where the local leader enjoys 20-30% cost advantages over distant competitors.

The scale that truly matters is in R&D and technical support. Carlisle can afford to spend $50 million developing a new membrane technology because they can amortize it across billions in revenue. A regional competitor with $100 million in sales can't match this innovation investment. The scale economies compound—better products command premium prices that fund more R&D that creates better products.

Switching Costs: The Warranty Web

The 20-year warranty system creates switching costs that transcend simple economic calculation. When a building owner accepts a Carlisle warranty, they're not just buying product insurance—they're entering a two-decade relationship that compounds over time. Each repair, each inspection, each technical support interaction deepens the relationship and raises switching barriers.

For contractors, switching costs are even more insidious. Learning installation techniques, building supplier relationships, understanding warranty requirements—these investments in Carlisle-specific knowledge become sunk costs that discourage experimentation with alternatives. A contractor who's installed Carlisle systems for a decade won't risk their reputation trying unfamiliar products to save marginal amounts.

Network Effects: Weak but Present

Traditional network effects—where each additional user makes the product more valuable for all users—don't strongly apply to roofing materials. However, weak network effects exist in the contractor-distributor-manufacturer ecosystem. As more contractors specify Carlisle products, distributors stock deeper inventory. Deeper inventory improves availability, attracting more contractors. It's not Facebook-level network effects, but it creates meaningful competitive advantage.

The technical support network exhibits stronger network properties. As Carlisle's installed base grows, their database of problem-solution pairs expands, making technical support more effective. This knowledge accumulation benefits all customers—a solution developed for a problem in Phoenix helps a contractor in Philadelphia.

Counter-Positioning: The Un-Conglomerate

Carlisle's transformation represents classic counter-positioning against diversified industrials. While competitors maintained portfolio complexity to reduce volatility, Carlisle accepted concentration risk for superior returns. This wasn't just different positioning—it was counter-positioning that existing players couldn't match without destroying their own business models.

The focused pure-play strategy counters traditional industrial thinking about diversification. General Electric, 3M, Honeywell—these conglomerates couldn't follow Carlisle's playbook without acknowledging their fundamental strategy was wrong. Carlisle's success doesn't just create a new model; it invalidates the old one.

Process Power: The Carlisle Operating System

The COS represents genuine process power—embedded capabilities that improve with experience and resist imitation. It's not a manual competitors can copy but a living system refined over decades. The ability to acquire a business and expand margins by 300-500 basis points within 24 months isn't luck—it's process power that compounds with each iteration.

This process power extends beyond operations to M&A integration, customer relationship management, and innovation commercialization. Each acquisition teaches lessons that improve the next integration. Each customer interaction refines the service model. Each product launch accelerates time-to-market for the next innovation.

Branding: Reputation, Not Consumer Brand

Carlisle lacks consumer brand power—building owners don't know or care what membrane sits on their roof. But B2B reputation power is real and valuable. Among contractors, architects, and building owners who care, Carlisle's reputation for quality, reliability, and support commands premium pricing.

This reputation took decades to build and would take decades for competitors to replicate. Every successful warranty claim honored, every technical problem solved, every innovation that actually works—these compound into reputation power that resists erosion even when individual transactions disappoint.

Cornered Resource: Limited but Valuable

Carlisle doesn't control unique resources like pharmaceutical patents or mining rights. However, they've cornered certain resources that matter: the best roofing contractors' mindshare, prime manufacturing locations near major markets, and deep relationships with national accounts. These aren't exclusive, but they're practically difficult to replicate.

The accumulated knowledge from billions of square feet of installed roofing represents a cornered resource. This isn't documented knowledge but embedded expertise—understanding why certain installations fail, which climates challenge which chemistries, how building types affect membrane performance. Competitors can't buy this knowledge; they must earn it over decades.

The Missing Powers

Notably, Carlisle lacks certain powers that protect other industrial leaders. They don't have regulatory capture that protects utilities. They lack patents that protect pharmaceuticals. They don't enjoy winner-take-all dynamics that protect software platforms. This absence of certain powers explains why Carlisle trades at industrial multiples rather than software valuations.

The Aggregation of Advantage

What makes Carlisle powerful isn't any single advantage but the aggregation of multiple reinforcing powers. Scale economies fund innovation that increases switching costs that deepen counter-positioning against subscale competitors. Process power improves acquisition integration that builds scale that enhances process power. The powers compound rather than simply add.

This aggregation creates what Buffett calls a "moat"—sustainable competitive advantage that resists erosion. But unlike a castle's moat that's either crossed or not, Carlisle's moat has variable depth. In core commercial roofing, it's deep and widening. In adjacent markets, it's shallow and uncertain. Understanding this variability is crucial for assessing future returns.

The Counter-Positioning Against ESG

Ironically, Carlisle's greatest counter-positioning might be against ESG-focused competitors who prioritize environmental metrics over business fundamentals. While competitors tout carbon neutrality, Carlisle focuses on products that actually reduce building energy consumption. This practical environmentalism—doing well by doing good—counters both greenwashing and virtue signaling.

Final Analysis: The Transformation Verdict

Carlisle's transformation from diversified conglomerate to focused building products leader represents one of the most successful industrial pivots of the past decade. They didn't just change their portfolio; they fundamentally reimagined what business they're in and how to create value within it.

The strategic clarity is remarkable. In an era of corporate complexity, Carlisle simplified. While competitors pursued digital transformation and services pivots, Carlisle doubled down on manufacturing excellence. As markets rewarded asset-light business models, Carlisle invested in production capacity. This contrarian clarity created value precisely because it ran counter to conventional wisdom.

The execution excellence matches strategic clarity. Vision 2025 wasn't just achieved—it was exceeded three years early. Vision 2030 appears similarly achievable, perhaps conservative. Management under-promised and over-delivered consistently, building credibility that compounds into valuation premium over time.

But the transformation isn't without risks. Concentration in building products exposes Carlisle to construction cyclicality that diversification previously mitigated. The acquisition pipeline won't remain robust forever. Competition from larger players could intensify. The easy gains from transformation are captured; future value creation requires relentless operational execution.

The investment implications depend on perspective. For those seeking a transformation story, it's largely complete—the conglomerate discount has become a pure-play premium. For those seeking a high-quality industrial with sustainable competitive advantages and skilled management, Carlisle offers compelling value. For those worried about recession or rising rates, patience might be prudent.

What's undeniable is that Carlisle has created substantial value through strategic focus and operational excellence. They've proven that industrial companies can successfully transform, that conglomerate discounts can become pure-play premiums, that operational excellence beats financial engineering. These lessons matter beyond Carlisle's stock price.

The ultimate judgment on Carlisle's transformation won't come for years. Will Vision 2030's targets be achieved? Can margins expand further? Will acquisition integration continue succeeding? Does management succession maintain momentum? These questions remain unanswered.

But one thing is certain: Carlisle Companies is no longer a sleepy Pennsylvania tire company or an unfocused industrial conglomerate. It's a focused, ambitious, excellently managed building products leader with genuine competitive advantages and significant growth potential. Whether that makes it a great investment depends on price, timing, and alternatives—decisions each investor must make individually.

The transformation from tire shop to building envelope empire is complete. The question now isn't whether Carlisle transformed successfully—it clearly did. The question is whether the transformed Carlisle can continue compounding value at rates that justify premium valuations. History suggests betting against this management team is unwise, but markets are forward-looking, and past success doesn't guarantee future returns.

For students of business strategy, Carlisle offers rich lessons about portfolio transformation, operational excellence, and value creation. For investors, it offers a high-quality business at a reasonable price with capable management and favorable industry dynamics. Whether that's enough depends on your alternatives, timeline, and tolerance for cyclicality.

The tire shop has become a building envelope empire. The transformation is complete. The future remains unwritten.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube