Jubilant Ingrevia: The Demerger That Built a Chemical Champion

I. Introduction & Episode Teaser

Picture this: February 1, 2021. As India emerges from pandemic lockdowns, a corporate event unfolds that most investors overlook. A 43-year-old conglomerate called Jubilant Life Sciences splits itself in two. The pharmaceutical assets go one way. The specialty chemicals business—making everything from vitamin B3 to pyridine derivatives—goes another. This new entity, christened Jubilant Ingrevia, debuts on the stock exchange six weeks later with a peculiar name (a portmanteau of "ingredients" and the French word for life, "vie") and an ambitious promise: to become India's specialty chemicals champion.

Today, Jubilant Ingrevia commands a market capitalization of ₹11,096 crore, generating ₹4,191 crore in annual revenue. It's the world's lowest-cost producer of pyridine-based derivatives, one of only two global manufacturers of vitamin B3, and serves 15 of the top 20 pharmaceutical giants plus 7 of the top 10 agrochemical companies worldwide. But here's the hook that makes this story fascinating: How did a demerger—typically a sign of corporate distress or strategic confusion—actually unlock value and create a focused chemical powerhouse?

The answer lies in understanding a fundamental shift in global supply chains, the unique economics of specialty chemicals, and why sometimes the best corporate strategy is knowing when to let go. This is the story of how two brothers from Kolkata built a chemical empire over four decades, why they chose to split it at its peak, and what this means for the future of India's chemical industry.

We'll explore three core themes: First, how backward integration from trading to manufacturing created sustainable competitive advantages. Second, why the specialty chemicals business model—with its blend of commodity inputs and value-added outputs—creates unique moats when executed correctly. And third, how the China+1 strategy and global supply chain realignment are creating once-in-a-generation opportunities for Indian chemical companies.

II. The Jubilant Empire: Origins & Foundation

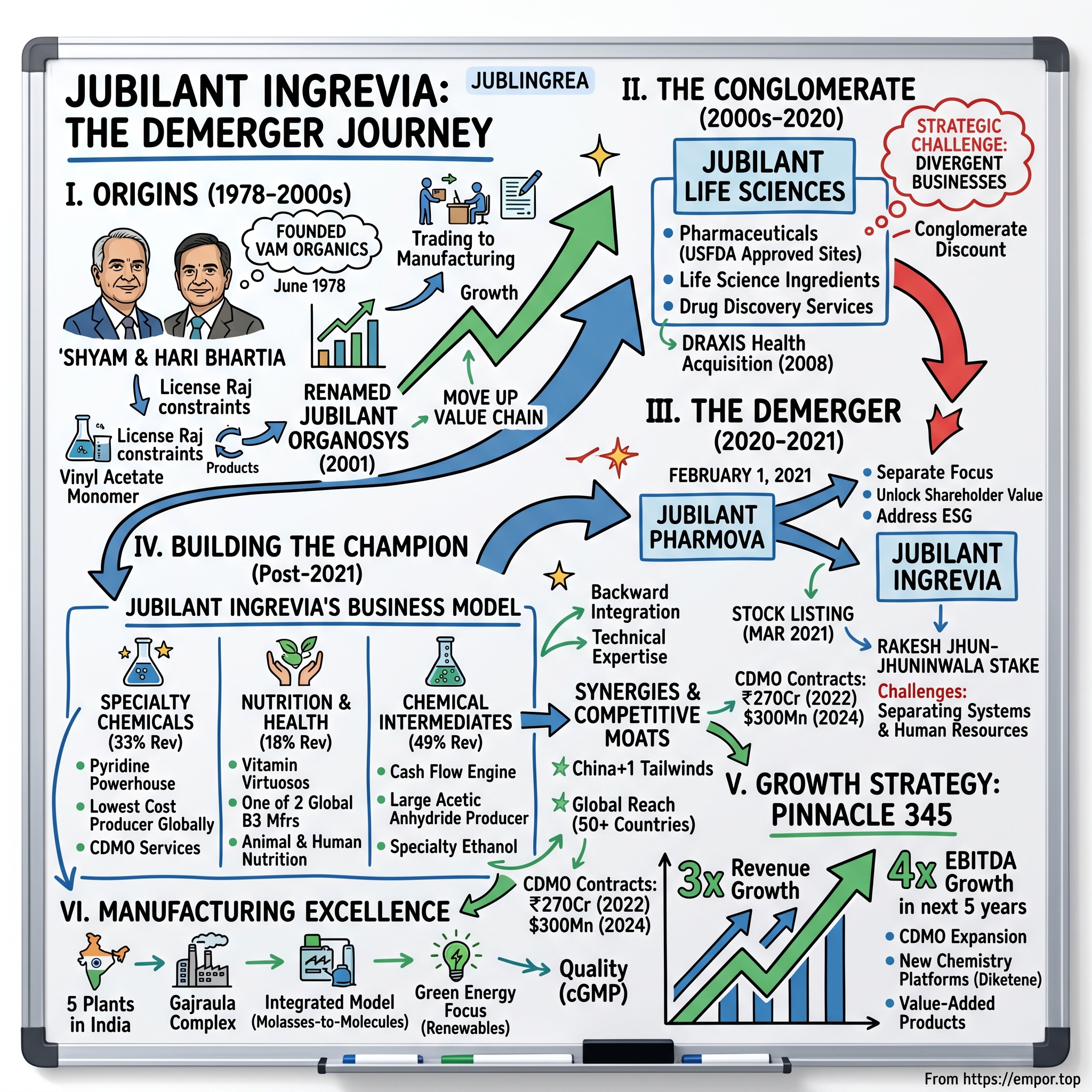

The year is 1978. Jimmy Carter occupies the White House, China is just beginning to open up under Deng Xiaoping, and in India, the Emergency has just ended but the economy remains shackled by the License Raj. In this environment of economic constraints and limited opportunities, two brothers in Kolkata—Shyam Sundar Bhartia and Hari Bhartia—make a decision that would define the next four decades of their lives.

Their father, Mohan Lal Bhartia, ran a modest but profitable business trading steel wire and, curiously, Rolex watches in Kolkata's bustling markets. The brothers could have continued in trading—a safe, established path. Instead, on June 21, 1978, they founded Vam Organics Limited with seed capital from their father. The name VAM wasn't chosen for aesthetic reasons; it was simply the abbreviation of vinyl acetate monomer, the chemical compound they planned to manufacture.

This was audacious for its time. Manufacturing chemicals in 1978 India meant navigating a maze of licenses, dealing with unreliable power supply, and competing against established players with decades of experience. The Bhartia brothers had none of these advantages. What they did have was timing—they entered just as India's pharmaceutical industry was beginning its remarkable journey from reverse-engineering to innovation.

The brothers' strategy was deceptively simple: start with basic chemicals that everyone needed but few wanted to make. Vinyl acetate monomer wasn't glamorous—it went into adhesives, paints, and textiles. But it was essential, import-dependent, and offered steady demand. More importantly, mastering its production taught them the fundamentals of chemical engineering, plant operations, and global sourcing that would prove invaluable later.

By the late 1980s, Vam Organics had established itself as a reliable domestic supplier. But the real transformation came with India's economic liberalization in 1991. Suddenly, the protective walls that had sheltered inefficient domestic producers came down. Foreign companies could enter India. Indian companies could access global markets. For many manufacturers, this was terrifying. For the Bhartia brothers, it was the opportunity they'd been preparing for.

They recognized that liberalization would create demand for higher-value chemicals—intermediates for pharmaceuticals, specialty ingredients for agrochemicals, fine chemicals for various industries. In 2001, marking this strategic shift, they renamed the company Jubilant Organosys. The word "Jubilant" captured their optimism about India's economic future; "Organosys" signaled their evolution from basic chemicals to sophisticated organic synthesis.

The renamed company didn't just change its identity—it transformed its entire approach. Instead of competing on price in commoditized products, Jubilant began moving up the value chain. They acquired technologies for producing pyridine and its derivatives, chemicals crucial for pharmaceutical synthesis. They invested in research facilities, hired PhD chemists, and began filing patents. By 2010, when the company renamed itself again to Jubilant Life Sciences Limited, it had evolved from a single-product manufacturer to a diversified life sciences conglomerate.

This 40-year journey from a vinyl acetate monomer producer to a global specialty chemicals player offers crucial lessons. First, in chemicals, patient capital wins—the brothers reinvested profits for decades before taking significant dividends. Second, backward integration creates resilience—by controlling their raw material sources, they insulated themselves from supply shocks. Third, technical expertise compounds—each new chemical process they mastered made the next one easier to learn.

But perhaps the most important lesson from this foundation period was about focus. As Jubilant grew, it accumulated businesses across the chemical value chain—from basic intermediates to finished pharmaceuticals. This diversification provided stability but also created complexity. By 2020, the conglomerate structure that had enabled growth was becoming a constraint. Different businesses required different strategies, different capital allocation, different management focus. The stage was set for the great unbundling.

III. Life Within Jubilant Life Sciences (1978–2020)

Inside the sprawling Jubilant Life Sciences conglomerate of the 2000s and 2010s, a fascinating tension emerged. The company had evolved from a single-product manufacturer into a sprawling empire spanning pharmaceuticals, life science ingredients, and drug discovery services. By 2000, it had penetrated the bio/chemo informatics arena through Jubilant Biosys Ltd, and by 2006 had inaugurated India's largest Drug Discovery facility in Bangalore for integrated Drug Discovery solutions. But this diversity, initially a strength, was becoming a strategic liability.

The numbers tell a story of impressive scale but increasing complexity. By the late 2010s, Jubilant operated 6 USFDA approved manufacturing facilities across the US, Canada and India, employed around 7,700 multicultural people globally, and served customers across over 100 countries. The pharmaceutical segment alone operated through a network of over 50 radio-pharmacies in the US, making it the second-largest commercial radio pharmacy network in America.

Yet beneath this success lay a fundamental challenge: the specialty chemicals business—particularly the pyridine and acetyls operations that formed the company's historical core—operated on entirely different dynamics than the pharmaceutical business. Chemical manufacturing required massive capital investments in production capacity, operated on thinner margins, and faced commodity price volatility. Pharmaceuticals, by contrast, offered higher margins, required different regulatory expertise, and demanded distinct go-to-market strategies.

The pyridine business exemplified this dichotomy. Jubilant had become one of the global leaders in pyridine and its derivatives, competing with giants like Vertellus Holdings LLC (US), Lonza Group AG (Switzerland), and Nanjing Redsun Co. Ltd. (China). The company wasn't just participating in this market—it was dominating specific niches. Its pyridine derivatives served as critical building blocks for vitamin B3 (niacin), pharmaceutical intermediates, and agrochemicals. Yet this business required constant reinvestment to maintain cost leadership and faced pressure from Chinese competitors who could leverage lower input costs.

The vitamin B3 story illustrates both the promise and peril of the specialty chemicals business. Jubilant had backward-integrated from basic pyridine production into downstream derivatives, becoming one of only two global manufacturers of vitamin B3. This gave them pricing power and customer stickiness—once a pharmaceutical or nutrition company qualified Jubilant's vitamin B3 for their formulations, switching suppliers became costly and risky. But producing vitamin B3 also meant exposure to agricultural commodity prices (for molasses), energy costs, and environmental regulations that had little relevance to the company's pharmaceutical operations.

Meanwhile, the pharmaceutical business was evolving rapidly. In April 2008, Jubilant acquired DRAXIS Health for $255 million, gaining a 100% stake in the Canadian pharmaceutical company. This acquisition, along with others in the radiopharmaceutical and allergy therapy spaces, transformed Jubilant from primarily a supplier of pharmaceutical ingredients into an integrated player offering finished dosage forms, contract manufacturing, and specialized therapeutic products.

The contract manufacturing opportunity was particularly compelling. Global pharmaceutical companies were increasingly outsourcing production to reduce costs and focus on drug discovery and marketing. India, with its established pharmaceutical manufacturing base, skilled workforce, and improving regulatory compliance, was perfectly positioned to capture this trend. But serving as a contract manufacturer for Big Pharma required different capabilities than producing commodity chemicals—stringent quality systems, regulatory expertise across multiple jurisdictions, and the ability to handle complex, often proprietary processes.

By 2019, the strain of managing these divergent businesses under one roof was becoming apparent to both management and investors. The market was valuing Jubilant Life Sciences as a conglomerate—applying a discount to its sum-of-parts value. Analysts struggled to model the company, unsure whether to treat it as a pharmaceutical play, a specialty chemicals company, or something in between. The different businesses competed for management attention and capital allocation, with neither achieving its full potential.

During 2013-14, the company had already shown willingness to prune non-core assets, selling its Hospital business to Narayana Health. This divestiture signaled management's recognition that not all diversification created value. But the bigger question remained: should the core life sciences and pharmaceutical businesses themselves be separated?

The board and management team, led by the Bhartia brothers, spent months analyzing options. They studied successful demergers like Abbott's split into Abbott and AbbVie, and failures where separated entities struggled to find their footing. They engaged investment bankers to model various scenarios, consulted with major shareholders, and carefully evaluated the operational complexities of separation.

What tipped the scales toward demerger was a confluence of factors. First, the specialty chemicals industry was entering a golden period, driven by supply chain shifts away from China. Second, the pharmaceutical business needed significant capital investment to compete in biologics and complex generics. Third, ESG considerations were becoming crucial, and chemical manufacturing faced different sustainability challenges than pharmaceuticals. Finally, the COVID-19 pandemic had highlighted the strategic importance of both pharmaceutical and chemical supply chains, potentially unlocking higher valuations for focused pure-play companies.

The strategic logic was compelling: create two focused entities, each with clear investment theses, distinct management teams, and the flexibility to pursue their optimal strategies. The specialty chemicals business could double down on cost leadership, capacity expansion, and backward integration. The pharmaceutical business could accelerate its shift toward complex generics, biologics, and contract manufacturing for innovator companies. Investors could choose their exposure rather than being forced to accept a conglomerate structure.

Thus, as 2020 drew to a close, Jubilant Life Sciences announced one of the most significant corporate actions in Indian chemical industry history—a demerger that would create Jubilant Ingrevia and Jubilant Pharmova, setting the stage for the next chapter in this remarkable corporate saga.

IV. The Great Demerger: Creating Focused Champions (2020–2021)

The boardroom at Jubilant's Noida headquarters buzzed with nervous energy on a humid September morning in 2020. As India grappled with COVID-19 lockdowns, the Bhartia brothers were orchestrating one of the most complex corporate restructurings in Indian chemical industry history. The decision had been made: Jubilant Life Sciences would split into two. But between decision and execution lay a minefield of regulatory approvals, stakeholder management, and operational challenges that would test the organization's resilience.

On February 1, 2021, Jubilant Life Sciences was officially demerged to create Jubilant Ingrevia, with the original entity being renamed Jubilant Pharmova Limited. The demerger wasn't just a financial engineering exercise—it represented a fundamental reimagining of how these businesses would compete in their respective markets.

The rationale was elegant in its simplicity yet complex in its implications. The Bhartia brothers articulated three core objectives: create separate and focused entities for pharmaceuticals and life science ingredients businesses, unlock value for shareholders by eliminating the conglomerate discount, and position each entity to capture attractive growth opportunities in their respective domains. But beneath these corporate objectives lay a more nuanced story about industrial evolution, market timing, and strategic foresight.

The name "Ingrevia" itself told a story—a portmanteau of "ingredients" and "vie" (French for life). This wasn't just clever wordplay; it signaled the company's positioning as a life science ingredients specialist, distinct from commodity chemical producers. The name suggested sophistication, global ambition, and a focus on value-added products rather than basic chemicals.

The demerger structure was carefully crafted to ensure fairness to existing shareholders. For every share of Jubilant Life Sciences held, shareholders received one share of Jubilant Ingrevia. This 1:1 ratio meant that investors who believed in the original Jubilant story could maintain exposure to both businesses, while those preferring focused bets could adjust their portfolios post-listing.

When Jubilant Ingrevia listed on the Bombay Stock Exchange on March 19, 2021, the market response was closely watched. The listing came at a peculiar moment—Indian equity markets were in a bull run, specialty chemical stocks were trading at premium valuations due to China+1 tailwinds, and retail investor participation had surged during the pandemic. The stock opened at ₹340, a modest premium to its discovery price, but what happened next surprised even the optimists.

Within weeks of listing, a dramatic development captured headlines: Ace investor Rakesh Jhunjhunwala, often called India's Warren Buffett, along with persons acting in concert, had accumulated a significant stake in Jubilant Ingrevia. Jhunjhunwala's investment philosophy—betting on India's growth story through companies with strong fundamentals and sectoral tailwinds—aligned perfectly with Ingrevia's positioning. His entry validated the demerger thesis and attracted attention from institutional investors who closely tracked his moves.

But the demerger wasn't without challenges. Separating a 43-year-old conglomerate required untangling shared services, dividing assets, and most critically, splitting human resources. Employees who had built careers spanning both businesses suddenly had to choose sides. The specialty chemicals business retained most of the manufacturing expertise and plant operations teams, while pharmaceutical regulatory experts and formulation scientists went to Pharmova.

Information technology systems posed another hurdle. The companies had operated on integrated ERP systems, shared data centers, and common digital infrastructure. Creating two independent IT architectures while ensuring business continuity required months of planning and execution. Vendor contracts had to be renegotiated, customer agreements reassigned, and banking relationships restructured.

The operational separation was equally complex. Some manufacturing sites housed both pharmaceutical and chemical operations. The Gajraula plant in Uttar Pradesh, for instance, produced both pyridine derivatives and pharmaceutical intermediates. Deciding which assets went where, how to handle shared utilities, and managing the logistics of physical separation required surgical precision.

Regulatory approvals added another layer of complexity. The National Company Law Tribunal (NCLT) had to approve the scheme of arrangement. Environmental clearances had to be transferred. Drug manufacturing licenses needed to be reissued. Each regulatory step required detailed documentation, stakeholder consultations, and careful navigation of bureaucratic processes.

The financial structuring of the demerger revealed interesting strategic choices. As of 2022, specialty chemicals contributed 33% of Jubilant Ingrevia's revenue, nutrition and health solutions contributed 18%, and life science chemicals contributed 49%. This revenue mix showed that Ingrevia wasn't just the "chemical" part of the old Jubilant—it was a carefully curated portfolio of businesses with strong synergies and growth potential.

Market reaction in the months following the demerger validated the strategy. Both entities saw their valuations expand as investors could now value each business on its own merits. Specialty chemical investors, riding high on the China+1 theme and supply chain diversification trends, bid up Ingrevia's valuation. Pharmaceutical investors, excited about Pharmova's radiopharmacy network and complex generics pipeline, assigned premium multiples to that business.

The demerger also unlocked strategic flexibility. Ingrevia could now pursue acquisitions in specialty chemicals without worrying about pharmaceutical investors' reactions. It could optimize its capital structure for a chemical business—higher debt tolerance given stable cash flows from long-term contracts. Environmental, social, and governance (ESG) initiatives could be tailored to chemical industry standards rather than trying to satisfy divergent stakeholder expectations.

For employees, the demerger created new opportunities. In the combined entity, a talented chemical engineer might have seen limited career progression into senior management dominated by pharmaceutical executives. Now, Ingrevia offered clear pathways for chemical industry professionals to reach the C-suite. This clarity attracted talent from competitors and motivated existing employees who saw expanded opportunities.

The timing of the demerger, in retrospect, was masterful. It came just as global supply chains were being reconfigured post-COVID, as ESG considerations were becoming central to chemical industry valuations, and as India was emerging as a credible alternative to China in specialty chemicals. Had the demerger happened even two years earlier, it might not have captured these tailwinds. Two years later, and the opportunity might have been partially lost to competitors.

As 2021 progressed, both companies began executing their independent strategies with newfound focus and vigor. The great unbundling of Jubilant Life Sciences wasn't just a corporate event—it was a statement about the evolution of Indian industry from conglomerates to focused champions, from domestic players to global competitors, from value chain participants to value chain leaders.

V. The Three-Pillar Business Model

Walk through Jubilant Ingrevia's Gajraula manufacturing complex in Uttar Pradesh, and you'll encounter a fascinating industrial symphony. In one section, massive reactors convert molasses—a humble sugarcane byproduct—into specialty-grade ethanol. A few hundred meters away, sophisticated distillation columns purify pyridine to pharmaceutical-grade specifications. Further still, fermentation tanks produce vitamin B3 through carefully controlled biological processes. This isn't just chemical manufacturing; it's an orchestrated transformation of basic materials into high-value ingredients that touch billions of lives daily.

Specialty Chemicals (33% of revenue): The Pyridine Powerhouse

Jubilant Ingrevia stands as the world's lowest-cost producer of pyridine-based derivative products and one of only two global producers of pyridine, maintaining leadership in 14 pyridine derivatives. This dominance didn't happen overnight—it's the result of four decades of process optimization, backward integration, and relentless focus on cost leadership.

The pyridine story begins with a simple molecule—C₅H₅N—that forms the backbone of countless pharmaceutical and agrochemical products. What makes Jubilant's approach unique is their mastery of the entire value chain. While competitors typically purchase pyridine and convert it to derivatives, Jubilant produces pyridine from basic raw materials, giving them a 20-30% cost advantage that compounds through the value chain.

Consider the production of 2-methylpyridine (α-picoline), a crucial intermediate for vitamin B3 synthesis. Most producers rely on petroleum-based feedstocks, making them vulnerable to oil price volatility. Jubilant's process, refined over decades, uses a proprietary catalyst system that enables production from alternative feedstocks, providing both cost advantages and supply security. This technical edge translates directly to market dominance—the company supplies α-picoline to 15 of the top 20 global pharmaceutical companies.

The CDMO (Contract Development and Manufacturing Organization) services within specialty chemicals represent the business's future growth engine. In 2022, Jubilant signed a ₹270 crore specialty chemicals CDMO contract with a top-10 globally leading innovator pharmaceutical company—a validation of their technical capabilities and regulatory compliance. These aren't commodity transactions; they're multi-year partnerships where Jubilant becomes integrated into their customers' supply chains, creating switching costs that ensure customer retention.

The fine chemicals portfolio extends beyond pyridine into specialized molecules for crop protection. When a global agrochemical major needed a complex intermediate for their next-generation herbicide, Jubilant's team developed a novel synthetic route that reduced production steps from seven to four, cutting costs by 35% while improving yield. This innovation didn't just win a contract; it established Jubilant as a strategic partner in the customer's innovation pipeline.

Nutrition & Health Solutions (18% of revenue): The Vitamin Virtuosos

As one of the two largest manufacturers of vitamin B3 globally and one of India's largest manufacturers of vitamin B4, Jubilant Ingrevia has carved out a defensible position in the nutrition market. But calling this simply "vitamin manufacturing" understates the sophistication involved.

Vitamin B3 (niacin/niacinamide) production at Jubilant follows a vertically integrated model that starts with pyridine and ends with pharmaceutical-grade vitamins meeting the specifications of every major pharmacopeia—USP, EP, JP, and IP. The company produces multiple grades: standard niacinamide for nutritional supplements, ultra-pure grades for pharmaceutical formulations, and specialized forms for cosmetic applications. Each grade requires different purification processes, quality controls, and regulatory compliance.

The animal nutrition segment reveals another dimension of this business. As global meat consumption rises and consumers demand antibiotic-free protein, animal nutrition becomes critical. Jubilant's vitamin B portfolio helps poultry and livestock producers improve feed conversion ratios—a metric that directly impacts profitability in tight-margin animal agriculture. A 2% improvement in feed conversion, enabled by optimal vitamin supplementation, can mean the difference between profit and loss for a poultry farm.

Human nutrition applications extend beyond basic supplementation. Jubilant's niacinamide serves the booming skincare industry, where it's valued for anti-aging and skin-brightening properties. The company developed a specialized grade with controlled particle size distribution and enhanced stability, commanding premium prices in the cosmetic market. This product differentiation strategy—creating multiple grades for distinct applications—maximizes value extraction from core manufacturing capabilities.

Chemical Intermediates (49% of revenue): The Cash Flow Engine

Jubilant Ingrevia ranks as one of the two largest producers of acetic anhydride and a major producer of ethyl acetate. These might sound like commodity chemicals, but Jubilant's approach transforms them into a strategic business generating consistent cash flows that fund growth investments.

The acetyls business—encompassing acetic anhydride, ethyl acetate, and other acetate derivatives—exemplifies operational excellence. Acetic anhydride, primarily used in manufacturing cellulose acetate for cigarette filters and pharmaceutical intermediates, requires precise process control and quality consistency. Jubilant's plants achieve 99.9% purity levels with less than 10 ppm of critical impurities—specifications that qualify their products for the most demanding pharmaceutical applications.

The specialty ethanol business showcases clever positioning within apparent commoditization. While fuel ethanol trades as a commodity, Jubilant focuses on specialty grades for pharmaceuticals, cosmetics, and agrochemicals. Their Extra Neutral Alcohol (ENA) meets stringent requirements for aldehydes, esters, and higher alcohols—impurities measured in parts per billion. This quality differentiation allows them to command prices 30-40% above commodity ethanol.

The strategic brilliance lies in the interconnections between these businesses. Ethanol production from molasses generates CO₂ as a byproduct, which is captured and sold to beverage companies. The fermentation process yields potash-rich spent wash, processed into fertilizer for sugarcane farmers who supply the molasses—creating a circular economy that reduces waste and enhances sustainability credentials.

Geographic diversity adds resilience. While 65% of chemical intermediate sales occur domestically, leveraging India's growing pharmaceutical and agrochemical industries, exports to Southeast Asia, Middle East, and Latin America provide natural hedging against regional demand fluctuations. Long-term contracts with anchor customers—some extending five years—provide revenue visibility that's unusual in chemical markets.

The integrated business model creates competitive moats beyond individual product leadership. When a customer buys pyridine derivatives from Jubilant, they often source vitamin B3 and specialty solvents too. This multi-product relationship increases switching costs, provides cross-selling opportunities, and strengthens negotiating power. It's not just about making chemicals; it's about becoming indispensable to customers' operations.

VI. Manufacturing Excellence & Global Footprint

Dawn breaks at 5:30 AM at Jubilant Ingrevia's Gajraula manufacturing complex, and already the facility pulses with activity. Trucks loaded with molasses queue at the gates, steam billows from cooling towers, and the sharp tang of chemicals mingles with the sweet smell of fermentation. This 250-acre site, one of five state-of-the-art manufacturing facilities in India, embodies the company's manufacturing philosophy: scale, integration, and relentless cost optimization.

The geographic distribution of Jubilant's manufacturing footprint reveals strategic thinking. Manufacturing facilities span Gajraula (Uttar Pradesh), Bharuch and Savli (Gujarat), Nira (Maharashtra), and Ambernath (Maharashtra). This isn't random distribution—each location offers specific advantages. Gajraula, close to India's sugarcane belt, provides access to molasses for ethanol production. Gujarat's chemical corridor offers proximity to ports for exports and a skilled workforce familiar with chemical operations. Maharashtra facilities tap into the state's strong pharmaceutical ecosystem.

The Gajraula facility stands as the crown jewel of this manufacturing network. The site includes its own captive power plant, a critical advantage in India where power reliability remains challenging. This 40-megawatt cogeneration plant doesn't just ensure uninterrupted production—it transforms waste heat from chemical processes into electricity, reducing energy costs by 25% compared to grid power. During the 2012 North India blackout that crippled industries across states, Jubilant's Gajraula operations continued uninterrupted, fulfilling critical orders while competitors scrambled.

Current capacity utilization stands at around 80-85%, a sweet spot that balances efficiency with flexibility. Running plants at 100% capacity might maximize asset utilization but leaves no room for maintenance, product mix optimization, or surge demand. The 15-20% headroom allows Jubilant to accept rush orders, conduct preventive maintenance without disrupting supply, and optimize product mix based on margin dynamics.

The company's cost leadership strategy—positioning as a "Leading Low-Cost provider"—permeates every aspect of manufacturing operations. Consider the pyridine production process. While competitors rely on imported petroleum-based feedstocks, Jubilant's backward integration into molasses-based ethanol provides a 30% cost advantage. But cost leadership isn't just about cheap inputs—it's about process excellence. The company's pyridine distillation columns achieve 99.9% recovery rates, meaning virtually no product is lost to waste streams. Continuous process improvements have reduced steam consumption per ton of product by 40% over the past decade.

Quality standards represent another dimension of manufacturing excellence. Most of the plants are cGMP certified, meeting current Good Manufacturing Practice standards required for pharmaceutical ingredients. This certification isn't merely a regulatory checkbox—it's a competitive differentiator that allows Jubilant to serve the world's most demanding pharmaceutical customers. When a European pharmaceutical major audited Jubilant's facilities, they found defect rates of less than 10 parts per million—exceeding their own internal manufacturing standards.

The global footprint extends beyond physical manufacturing to market reach. Sales reaching more than 50 countries create natural hedging against regional economic cycles. When European demand softened during the 2011 debt crisis, growing Asian markets compensated. When COVID-19 disrupted Indian operations, inventory strategically positioned in overseas warehouses ensured supply continuity.

The recent expansion into diketene derivatives illustrates how manufacturing excellence enables strategic growth. In 2022, Jubilant commissioned a new Diketene derivatives facility at Gajraula with about 7,000 TPA capacity to produce various esters. This wasn't just capacity addition—it represented entry into a new chemistry platform. The company leveraged its niche expertise in Ketene chemistry technology to develop a range of Diketene derivatives, demonstrating how core manufacturing competencies can be extended into adjacent markets.

The integrated business model amplifies manufacturing advantages. When producing vitamin B3, Jubilant doesn't just manufacture the final product—they produce the pyridine precursor, the intermediate compounds, and even recover and purify byproducts for sale. This integration provides cost advantages, supply security, and quality control that competitors buying intermediates from third parties cannot match.

Environmental compliance and sustainability have evolved from regulatory requirements to competitive advantages. Jubilant's zero liquid discharge systems, mandated by increasingly stringent environmental regulations, initially seemed like cost burdens. But the company turned compliance into opportunity—wastewater treatment systems recover valuable chemicals, reducing raw material costs. Solid waste is converted to fuel for cement kilns, generating revenue from what competitors treat as disposal costs.

The manufacturing organization's human dimension often goes unnoticed but proves crucial. The Gajraula facility employs over 2,000 people, from PhD chemical engineers to skilled operators who've spent decades perfecting their craft. The company's training programs don't just teach process operations—they instill a culture of continuous improvement. Operators are empowered to suggest process modifications, with successful ideas rewarded and scaled across facilities.

Safety performance provides another lens into manufacturing excellence. Jubilant's facilities have achieved over 10 million man-hours without lost-time injuries—remarkable for chemical manufacturing where handling hazardous materials is routine. This safety record isn't luck—it results from systematic hazard analysis, rigorous training, and a culture where anyone can stop operations if they observe unsafe conditions.

The capital allocation strategy for manufacturing reveals disciplined thinking. In FY22, the company planned ₹360 crore in capex for a CDMO facility at Bharuch, two multi-purpose plants for specialty chemicals, food-grade acetic acid capacity, an acetic anhydride plant, and Agro Actives Phase-1. Each investment targets either margin expansion through value-added products or capacity addition in sold-out product lines—no speculative capacity additions hoping demand will materialize.

Technology adoption enhances traditional manufacturing strengths. Advanced process control systems optimize reaction conditions in real-time, improving yields by 2-3 percentage points—seemingly small gains that translate to millions in additional profit given the scale of operations. Predictive maintenance algorithms analyze equipment vibration patterns, temperature trends, and other parameters to schedule maintenance before failures occur, reducing unplanned downtime by 60%.

The manufacturing excellence story culminates in competitive moats that become increasingly difficult for competitors to replicate. It's not just about having factories—it's about four decades of accumulated knowledge, optimized processes, trained workforces, and cultures of continuous improvement. When customers choose Jubilant, they're not just buying chemicals—they're buying reliability, quality, and the assurance that comes from partnering with a manufacturer that has mastered its craft.

VII. The CDMO Play & Growth Strategy

The conference room at Jubilant Ingrevia's Noida headquarters hummed with anticipation in April 2022. CEO Rajesh Srivastava had just signed what would become a defining moment for the company—a ₹270 crore CDMO contract with a top-10 global pharmaceutical innovator. This wasn't just another supply agreement; it represented validation of a strategic pivot years in the making, transforming Jubilant from a commodity chemical supplier into a strategic partner for the world's most sophisticated pharmaceutical and agrochemical companies.

The CDMO (Contract Development and Manufacturing Organization) model represents the apex of chemical manufacturing sophistication. Unlike traditional toll manufacturing, where customers provide specifications and manufacturers simply execute, CDMO partnerships involve collaborative development from molecule design through commercial production. The company was awarded these CDMO projects a few years ago and with extensive work in R&D and scale-up, it has successfully demonstrated its capability in process development, optimisation and scaling-up of complex chemistries.

The April 2022 pharmaceutical contract exemplified this sophistication. Through the contract, the company will supply two key GMP intermediates for one of the 'patented drugs' of the innovator pharmaceutical customer. Both these products involve 7 steps of specialised chemistry. Seven-step synthesis isn't just complex—it requires mastering multiple chemical transformations, each with its own yield optimization, purification challenges, and quality control requirements. The fact that a global pharmaceutical giant entrusted this to Jubilant speaks volumes about their technical capabilities.

But the CDMO story accelerated dramatically in 2024. The company signed a significant five-year contract with a multinational agro-innovator, expected to boost revenue share from its agrichemical CDMO business. This wasn't just another contract—it was a $300 million commitment that would fundamentally reshape Jubilant's business mix. The company is now transitioning to become a CDMO player and has already signed 2 contracts for agro CDMO, one of which is worth USD300mn and will start contributing to revenue from Q4FY26.

The strategic brilliance of the CDMO pivot becomes clear when examining the economics. Traditional chemical manufacturing operates on razor-thin margins—5-10% EBITDA margins are common for commodity chemicals. CDMO contracts, by contrast, can generate 20-30% margins. The ₹270 crore pharmaceutical contract, spread over three years, generates approximately ₹90 crore annually—but with margins potentially double that of commodity sales, the profit contribution is disproportionately higher.

Jubilant's approach to CDMO differs from competitors chasing every opportunity. They focus on chemistries where they possess deep expertise—pyridine derivatives, acetyls, and increasingly, diketene chemistry. When a customer approaches with a molecule requiring pyridine chemistry, Jubilant doesn't just offer manufacturing capacity; they bring four decades of experience optimizing pyridine reactions, understanding side-product formation, and managing the unique safety challenges of heterocyclic chemistry.

The growth strategy, branded "Pinnacle 345," reveals ambitious targets: Jubilant Ingrevia's growth strategy, known as Pinnacle 345, is a bold and ambitious strategy that is focused on delivering 3x revenue growth and 4x EBITDA growth in the next five years. The 4x EBITDA growth target exceeding 3x revenue growth explicitly acknowledges that CDMO and specialty chemicals will drive margin expansion, not just top-line growth.

The firm is stepping up its R&D activities, with a target to double its R&D expenditure over the next few years. This R&D investment isn't academic curiosity—it's directed toward solving customer problems. When an agrochemical innovator struggled with a synthetic route requiring expensive platinum catalysts, Jubilant's R&D team developed an alternative using base metal catalysis, reducing production costs by 40% while improving environmental sustainability.

The David versus Goliath narrative plays out daily in global markets. Jubilant competes against European giants like Lonza and BASF with centuries of chemical heritage and R&D budgets exceeding Jubilant's entire revenue. Yet Jubilant wins contracts through a combination of cost competitiveness, agility, and increasingly, technical excellence. While a European competitor might quote 18 months for process development and scale-up, Jubilant commits to 12 months and often delivers in 10.

The China+1 strategy provides powerful tailwinds. The China plus one strategy is gaining momentum, with many global clients seeking reliable suppliers outside China. This trend is reflected in our new CDMO contracts and increased customer engagement. When supply chains broke during COVID-19 and geopolitical tensions escalated, global companies realized the risks of single-source dependence on China. Jubilant, with its established manufacturing base, regulatory compliance, and track record, emerged as an obvious alternative.

But executing the CDMO strategy requires more than just winning contracts—it demands operational excellence at every level. GMP (Good Manufacturing Practice) compliance for pharmaceutical intermediates means documenting every gram of material, every minute of reaction time, every degree of temperature variation. A single deviation can trigger regulatory scrutiny and jeopardize multi-million dollar contracts.

Our CDMO project pipeline for our pharmaceuticals & agrochemical continues to be strong and we stay committed to further strengthening our presence in the CDMO business, through a comprehensive and planned capex. The capital allocation strategy reflects this commitment. Unlike capacity additions for commodity chemicals that might generate 15% returns, CDMO investments target 25%+ returns on capital employed.

The competitive landscape in CDMO is evolving rapidly. Indian players like Syngene, Divi's Laboratories, and Laurus Labs have demonstrated that Indian companies can compete globally in sophisticated chemistry. But Jubilant's unique position—straddling specialty chemicals and CDMO—provides advantages. When developing a new agrochemical active ingredient, customers can source the key intermediate, obtain analytical standards, and access formulation expertise all from Jubilant.

Customer concentration metrics reveal the success of the diversification strategy. Serves 15 of the top 20 Global Pharma & 7 of the top 10 Global Agrochemical companies. This isn't just about customer count—it's about embedding Jubilant into the innovation pipelines of the world's leading life science companies. Once Jubilant develops a process for a patented molecule, switching to another supplier requires re-validation, regulatory filings, and supply chain reconfiguration—creating substantial switching costs.

Looking ahead, the CDMO opportunity appears vast. As highlighted in our previous report, 7 more molecules with pyridine chemistry are expected to go off-patent by 2028, thus making Jubilant a good fit to manufacture them. Patent cliffs create opportunities for generic manufacturers, but they also create opportunities for companies like Jubilant that can provide the complex intermediates these generic manufacturers need.

The strategic evolution from commodity chemical manufacturer to CDMO partner represents more than business model transformation—it's about moving from selling products to selling solutions, from competing on price to competing on capability, from being a vendor to becoming a partner. This journey, still in its early stages, positions Jubilant to capture value that extends far beyond what traditional chemical manufacturing could ever offer.

VIII. Financial Performance & Market Position

The numbers tell a story of transformation. Jubilant Ingrevia's market capitalization stands at ₹11,096 crore with revenue of ₹4,191 crore and profit of ₹278 crore, but these headline figures mask a more nuanced financial evolution playing out quarter by quarter since the 2021 demerger.

The post-demerger journey began with volatility. In Q2 FY22, the first full quarter as an independent entity, the company reported 43% growth in net profit to ₹111 crore for the quarter ending September 2021 vs ₹77 crore during the same period last year, with revenue jumping 56% to ₹1,223 crore compared to ₹406 crore in Q2FY21, and EBITDA growing 44% to ₹202 crore. But EBITDA margins fell to 16.5% vs 17.9% during the same period last year, signaling the challenges of operating independently.

Fast forward to the most recent quarters, and a different picture emerges. In Q1 FY26, revenue from operations reached ₹1,037.95 crore with net profit of ₹75.1 crore vs ₹48.74 crore YoY—a 54% year-on-year jump. The improved profitability despite flattish revenue growth reveals the strategic shift toward higher-margin products taking hold.

The Q3 FY25 results provide even more compelling evidence of transformation. Revenue reached INR1,057 crores, up from INR966 crores in Q3 FY24, with EBITDA of INR148 crores, a 9% sequential increase and 42% year-on-year rise. More importantly, the specialty chemicals segment achieved its highest ever EBITDA of INR121 crores in a quarter, with a 26% EBITDA margin, the highest in the last 14 quarters.

This margin expansion story becomes clearer when examining segment performance. Specialty Chemicals Revenue grew 28% year-on-year and 8% quarter-on-quarter, while the Nutrition Business Revenue grew 25% year-on-year. These high-margin businesses are gradually offsetting the commodity-like acetyls business, which faced challenges due to low demand in the paracetamol segment, impacting acetic anhydride volumes and margins.

The balance sheet tells its own story of disciplined capital allocation. Net debt stands at INR684 crores with a net debt-to-EBITDA ratio of 1.36 times—conservative for a chemical manufacturing business. This leverage provides flexibility for growth investments while maintaining financial stability. Net working capital at 18.4% of turnover, reduced from 22% in the previous year, demonstrates improving operational efficiency.

Capital allocation priorities reveal strategic intent. Capital expenditure of INR92 crores for the quarter and INR299 crores year-to-date targets high-return projects—CDMO facilities, specialty chemical capacity, and value-added nutrition products. The company isn't chasing growth for growth's sake; each rupee of capex targets margin-accretive opportunities.

The dividend policy reflects confidence in cash generation. The company announced an interim dividend of 250%, equating to INR2.5 per equity share, resulting in a cash outflow of INR39.8 crores. This generous payout, while maintaining growth investments, signals management's confidence in sustainable cash flows.

Export dynamics add another dimension to the financial story. Export share increased to 48% in Q2 FY25 from 38% in Q2 FY24, demonstrating growing global competitiveness. Exports grew by 30% year-over-year, with increased interest from global clients due to the China plus one strategy. This geographic diversification provides natural currency hedging and reduces dependence on Indian market cycles.

Return metrics, however, present a mixed picture. The company has a low return on equity of 9.24% over last 3 years. This seemingly modest ROE requires context—it includes the transition period of the demerger, COVID disruptions, and significant growth investments yet to reach full utilization. As new capacity comes online and CDMO contracts mature, ROE should improve substantially.

The market's assessment reflects both promise and concern. The stock is trading at 3.79 times its book value, suggesting investors see value beyond current book assets—likely the intangible value of customer relationships, technical expertise, and growth optionality. Yet promoter holding has decreased over last quarter by 6.26% to 45.2%, raising questions about insider confidence or potentially creating overhang concerns.

Margin dynamics reveal the ongoing transformation. EBITDA reached ₹135 crores in Q2 FY25, a 13% sequential increase QoQ and 7% YoY increase, but the real story lies in margin mix. High-margin specialty chemicals and CDMO business are gradually increasing their revenue contribution, while lower-margin acetyls face headwinds. Jubilant Ingrevia Q1 FY26 showed 29% EBITDA growth, acceleration that suggests the strategy is gaining momentum.

The cyclicality challenge remains real. Chemical markets swing between shortage and surplus, impacting both volumes and margins. The acetyls business exemplifies this—when paracetamol demand drops, acetic anhydride prices collapse. But the company's response—diversifying into specialty grades, expanding the customer base, and focusing on value-added products—demonstrates adaptive capability.

Operational efficiency improvements contribute to financial performance. EBITDA gains were supported by lower raw material costs and relatively stable power and fuel expenses. This isn't just fortunate timing—it reflects backward integration advantages, long-term raw material contracts, and energy efficiency investments paying dividends.

The financial trajectory suggests Jubilant Ingrevia is successfully navigating the transition from commodity chemical producer to specialty player. Revenue growth may appear modest, but margin expansion, working capital efficiency, and strategic capital allocation create value beyond top-line expansion. The next phase—as CDMO contracts mature and specialty chemical capacity expands—should see acceleration in both growth and profitability.

Looking at peers in the specialty chemical space trading at 20-25x earnings, Jubilant appears reasonably valued given its transformation potential. But execution remains key—delivering on CDMO contracts, managing commodity cycles, and continuing operational improvements will determine whether current valuations prove prescient or optimistic.

IX. Playbook: Lessons in Specialty Chemicals

The conference room falls silent as the management team reviews the quarterly results. Someone asks the question that's been hanging in the air: "What would we do differently if we were starting over today?" The answer to that question reveals the hard-won lessons that constitute Jubilant Ingrevia's playbook—a guide not just for running a specialty chemicals business, but for industrial transformation in emerging markets.

The Demerger Playbook: When and How to Split

The decision to demerge wasn't made in a boardroom vacuum—it emerged from recognizing fundamental incompatibilities. Pharmaceutical businesses require FDA compliance, clinical trial expertise, and regulatory navigation across multiple jurisdictions. Chemical businesses need process engineering excellence, commodity risk management, and environmental compliance expertise. When management attention gets split between such divergent requirements, neither business reaches its potential.

The timing lesson proves crucial: demerge from a position of strength, not distress. Jubilant split when both businesses were profitable, growing, and had clear strategic paths. This allowed negotiation from strength—with bankers, with regulators, with employees. Distressed demergers often destroy value; strategic demergers can unlock it.

The execution blueprint matters as much as the decision. Start with systems separation two years before the legal split. Create shadow P&Ls for each division. Separate bonus pools and performance metrics. By the time the legal demerger occurs, the businesses should already be operating independently. Jubilant's relatively smooth transition reflected years of preparation, not months.

Building Moats Through Cost Leadership and Technical Expertise

Cost leadership in chemicals isn't about cutting corners—it's about fundamental advantages that compound over time. Jubilant's position as the world's lowest-cost pyridine producer didn't result from cheaper labor or lax environmental standards. It came from backward integration into molasses-based feedstocks, providing a 30% raw material cost advantage that competitors using petroleum feedstocks cannot match.

But cost leadership alone creates a race to the bottom. The real moat comes from combining cost leadership with technical expertise that customers value. When Jubilant develops a new synthesis route that reduces steps from seven to four, they don't just cut costs—they reduce impurities, improve yields, and accelerate time-to-market for their customers. This technical value-add allows premium pricing even from a cost leadership position.

The expertise moat deepens through specialization. By focusing on pyridine chemistry for four decades, Jubilant accumulated knowledge that would take competitors decades to replicate. They understand not just the primary reactions but the side reactions, the impurity profiles, the stability issues, the safety hazards. This deep expertise becomes invaluable when customers need to solve complex problems quickly.

Customer Diversification as Risk Management

The top 10 customers accounting for only 20% of sales might seem like weak customer relationships, but it's actually sophisticated risk management. In specialty chemicals, customer concentration creates vulnerability—a single customer loss can devastate profitability. Jubilant's broad customer base provides resilience against individual customer issues, industry downturns, or geographic disruptions.

But diversification without focus leads to complexity without benefit. Jubilant's approach—serving 15 of the top 20 pharmaceutical companies and 7 of the top 10 agrochemical companies—provides diversification within focused end markets. They're not trying to serve everyone; they're serving many customers within their target segments.

The customer diversification strategy extends to contract structures. Mix long-term contracts providing volume certainty with spot sales capturing price upside. Balance cost-plus contracts that ensure margin stability with fixed-price contracts that reward efficiency improvements. This portfolio approach to customer contracts provides both stability and upside opportunity.

Backward Integration and the Molasses-to-Molecules Journey

The journey from molasses to specialty chemicals exemplifies value creation through backward integration. Start with a waste product from sugar manufacturing selling for ₹3-4 per kilogram. Ferment it to specialty-grade ethanol worth ₹40-50 per kilogram. Convert that to acetic anhydride worth ₹80-100 per kilogram. Use that to produce pharmaceutical intermediates worth ₹500-1000 per kilogram. Each step up the value chain multiplies value while providing supply security.

But backward integration requires discipline. Not every upstream opportunity makes sense. Jubilant doesn't grow sugarcane or operate sugar mills—that's a different business with different economics. They integrate where they add value through chemical transformation, not where they'd simply be competing in commodity agriculture.

The integration strategy must be flexible. When molasses prices spike, the ability to switch to grain-based alcohol provides options. When acetic anhydride demand drops, the ability to sell ethanol to other markets provides outlets. Integration provides security, but flexibility prevents integration from becoming a straitjacket.

Managing Commodity Cycles in Specialty Chemicals

Specialty chemicals aren't immune to commodity cycles—they're just different cycles with different drivers. Pyridine prices might be stable while acetic anhydride crashes. Vitamin B3 might boom while fine chemicals struggle. Managing these multiple, often uncorrelated cycles requires sophisticated thinking.

The first lesson: maintain financial flexibility to survive downturns. Conservative leverage, strong cash generation, and diversified revenue streams provide staying power when specific products face headwinds. Companies that leverage up during booms often don't survive the inevitable busts.

The second lesson: use downturns to gain share. When competitors struggle with cash flow during downturns, Jubilant can maintain customer supply, invest in new capacity, and acquire distressed assets. The best chemical companies are built during downturns, not booms.

The third lesson: create counter-cyclical hedges. When pharmaceutical intermediates struggle, agrochemicals might thrive. When domestic markets weaken, exports might strengthen. Building a portfolio of imperfectly correlated businesses provides natural hedging against cycles.

The India Advantage in Global Chemicals

India's advantages in specialty chemicals extend beyond labor cost—that gap is narrowing anyway. The real advantages are more sustainable: a large pool of chemical engineers and PhD chemists, English language capability facilitating global business, a developing but functional regulatory regime, and proximity to both Middle Eastern feedstocks and Asian growth markets.

The talent advantage proves particularly crucial. India produces more chemistry graduates than any country except China. These aren't just operators—they're innovators who can develop new processes, optimize existing ones, and solve complex technical problems. This talent density creates clusters of expertise that become self-reinforcing.

The regulatory evolution, while sometimes frustrating, actually creates competitive advantage for companies that master it. As India's environmental and quality regulations tighten, companies like Jubilant that have already invested in compliance gain advantage over smaller competitors who cannot afford the investment. Regulatory complexity becomes a barrier to entry.

The playbook's final lesson might be the most important: patience. Chemical businesses aren't built in quarters or even years—they're built over decades. Customer relationships take years to establish and decades to mature into strategic partnerships. Technical expertise accumulates slowly through thousands of experiments and optimizations. Manufacturing excellence emerges from millions of operating hours and continuous improvements.

This patience requirement explains why financial investors often struggle in chemicals while strategic operators succeed. It's not an industry for quick flips or financial engineering. It's an industry for builders who understand that sustainable competitive advantage comes from doing difficult things consistently over long periods. Jubilant's 40-year journey from a single-product manufacturer to a global specialty chemical leader exemplifies this patient building.

X. Analysis & Investment Case

Standing at the crossroads of India's chemical industry transformation, Jubilant Ingrevia presents a fascinating study in contrasts. Bulls see a specialty chemical champion riding massive tailwinds; bears see commodity exposure and execution risks. The truth, as often happens, lies in the nuanced middle—but understanding where requires examining both cases with clear eyes.

Bull Case: The Convergence of Favorable Forces

The bull thesis starts with global leadership positions that are difficult to displace. As of 2022, Jubilant Ingrevia is the world's lowest cost producer of pyridine-based derivative products, one of the two producers of pyridine and a leader in 14 pyridine derivatives. The company is one of the two largest manufactures of vitamin B3 globally, one of India's largest manufactures of vitamin B4, one of the two largest producers of acetic anhydride, and a large producer of ethyl acetate. These aren't participation trophies—they're dominant positions in essential chemicals that would take competitors decades and billions to replicate.

The CDMO growth potential adds rocket fuel to this base. With $300 million in agrochemical CDMO contracts already signed and more in the pipeline, Jubilant is transitioning from selling commodities to selling solutions. CDMO relationships are sticky—once a customer integrates Jubilant into their supply chain for a patented molecule, switching costs become prohibitive. These multi-year contracts provide revenue visibility and margin expansion that commodity chemicals never could.

The China+1 strategy beneficiary status cannot be overstated. When global companies seek to diversify from China, they don't just need capacity—they need proven operators with regulatory compliance, technical capability, and track records. Jubilant checks every box. The company already serves 15 of the top 20 global pharma and 7 of the top 10 global agrochemical companies. These aren't customers experimenting with India; they're strategic partners expanding existing relationships.

Sustainability and green chemistry focus position Jubilant for the future, not the past. The firm has a 95% waste recycling rate and is striving to raise its renewable energy consumption to 35%. The company commissioned a new cGMP-compliant vitamin B3 facility in Bharuch, Gujarat, enhancing its presence in the value-added products market. Using molasses—a renewable feedstock—for chemical production provides both cost and sustainability advantages as carbon taxes and environmental regulations tighten globally.

Jubilant Ingrevia Ltd received the prestigious Global Lighthouse Network Award from the World Economic Forum for its Bharuch manufacturing facility's integration of Fourth Industrial Revolution technologies. This isn't just recognition—it validates that an Indian chemical company can match global best practices in digitalization and automation, critical for competing against developed market peers.

The financial flexibility to pursue growth while returning capital to shareholders demonstrates strength. The company maintains conservative leverage while investing aggressively in high-return projects. The generous dividend policy signals management confidence in cash generation sustainability.

Bear Case: The Shadows Behind the Sunshine

The bear case begins with commodity price volatility that hasn't disappeared despite strategic initiatives. The Acetyl business faced pressure due to low demand in the Paracetamol segment, impacting overall performance. When your largest revenue contributor faces structural headwinds, no amount of specialty chemical growth can immediately compensate.

Environmental regulations and compliance costs continue escalating. While Jubilant has invested heavily in compliance, the goalposts keep moving. Zero liquid discharge requirements, air emission standards, and hazardous waste management regulations require continuous capital investment that doesn't directly generate returns. Smaller competitors might struggle more, but Jubilant still bears the burden.

Competition from Chinese manufacturers remains fierce despite China+1 narratives. Chinese chemical companies aren't standing still—they're improving quality, meeting international standards, and maintaining cost advantages through scale and government support. When geopolitical tensions ease, Chinese competition could intensify again.

Promoter holding has decreased over last quarter: -6.26%, raising questions about insider confidence. While this could reflect portfolio rebalancing or personal financial needs, consistent promoter selling would signal concerns about future prospects that outside investors cannot see.

The CDMO execution risk looms large. Winning contracts is one thing; executing them profitably is another. Seven-step synthesis for pharmaceutical intermediates leaves little room for error. Quality failures, delays, or cost overruns could damage carefully cultivated customer relationships and future business prospects.

Valuation at 3.79 times book value prices in significant growth and margin expansion. If CDMO contracts disappoint, if specialty chemical markets soften, or if execution stumbles, multiple compression could drive significant stock price declines even if the business remains fundamentally sound.

The Synthesis: Probability-Weighted Outcomes

The investment case ultimately depends on probability-weighted scenarios rather than binary outcomes. The base case (60% probability) sees steady execution of the current strategy—CDMO contracts deliver expected returns, specialty chemicals grow steadily, and acetyls remain challenged but manageable. This scenario supports current valuations with modest upside.

The bull case (25% probability) sees accelerated CDMO wins, successful new product launches, and margin expansion exceeding expectations. Multiple global innovators choose Jubilant as their primary Indian partner. Specialty chemicals margins expand to 30%+. The stock re-rates to 25-30x earnings, delivering 50-70% upside.

The bear case (15% probability) sees execution challenges, customer losses, or regulatory issues. CDMO contracts face delays or cancellations. Environmental compliance costs escalate beyond expectations. The stock de-rates to 10-12x earnings, implying 30-40% downside.

The Verdict: Attractive but Not Without Risk

Jubilant Ingrevia represents a compelling opportunity for investors who understand chemical industry dynamics and can tolerate cyclicality. The company possesses genuine competitive advantages—global leadership positions, deep technical expertise, and customer relationships that would take decades to replicate. The strategic transformation from commodity to specialty chemicals, while incomplete, shows clear progress.

The risks are real but manageable. Commodity exposure will pressure margins during downturns, but diversification and financial conservatism provide staying power. Execution challenges might delay the growth trajectory but seem unlikely to derail it given management's track record.

For long-term investors seeking exposure to India's chemical industry transformation, Jubilant Ingrevia offers an attractive entry point. The company trades at reasonable valuations relative to peers while offering superior growth prospects through CDMO expansion. Patient investors who can look through quarterly volatility toward the five-year transformation story should find rewards commensurate with risks.

For traders or momentum investors, Jubilant presents challenges. Quarterly results will remain volatile as different businesses face different cycles. The stock might underperform during risk-off periods when investors flee cyclical sectors. The transformation story requires patience that short-term investors might lack.

The investment decision ultimately comes down to time horizon and risk tolerance. For those who believe in India's emergence as a global chemical manufacturing hub, who see sustainability and supply chain diversification as secular trends, and who possess patience to allow strategic transformations to unfold, Jubilant Ingrevia offers compelling opportunity. For those seeking quick returns or smooth earnings trajectories, better opportunities likely exist elsewhere.

XI. Epilogue & Future Outlook

The sun sets over Jubilant Ingrevia's Bharuch facility, painting the distillation columns in shades of gold and amber. Inside the control room, operators monitor screens displaying real-time data from hundreds of sensors—temperature, pressure, flow rates, quality parameters. This marriage of decades-old chemical engineering with cutting-edge digitalization embodies Jubilant's future: respecting the fundamentals while embracing transformation.

The Next Phase: EVs, Bio-based Chemicals, and Sustainability

The electric vehicle revolution presents both threat and opportunity. Traditional acetyl demand from automotive applications might decline as internal combustion engines fade. But EV batteries require specialized chemicals for electrolytes, separators, and thermal management—markets where Jubilant's expertise in high-purity chemicals and customer relationships with global manufacturers position them well.

Bio-based chemicals represent the next frontier. Jubilant Ingrevia also offers speciality grades of ethanol, for uses in the pharmaceuticals, agrochemicals, personal care, and fuel blending sectors. The company produces the ethanol from sugarcane molasses. This existing bio-based production capability could extend into bio-plastics, bio-solvents, and other sustainable alternatives to petroleum-based chemicals. As carbon taxes and environmental regulations tighten, bio-based routes might shift from premium-priced alternatives to cost-competitive necessities.

The sustainability transformation goes beyond products to processes. The company's 95% waste recycling rate and renewable energy initiatives position it for a world where ESG metrics determine access to capital, customer relationships, and regulatory licenses to operate. The Global Lighthouse recognition validates that Jubilant can lead, not just follow, in sustainable manufacturing.

Can Jubilant Ingrevia Become India's BASF?

The comparison to BASF might seem audacious—the German giant generates €70 billion in revenue against Jubilant's ₹4,191 crore. But BASF started as a dye manufacturer in 1865 and built its empire through patient expansion into adjacent chemistries. Jubilant's journey from vinyl acetate monomer to global specialty chemical player over 40 years suggests similar DNA.

The path to becoming India's BASF doesn't require matching BASF's scale—it requires matching BASF's approach: technical excellence, customer focus, strategic patience, and willingness to invest through cycles. Jubilant demonstrates these characteristics. The question isn't capability but ambition and execution.

The building blocks are in place. Dominant positions in key chemistries provide the foundation. CDMO relationships create customer intimacy and innovation opportunities. The Global Lighthouse recognition demonstrates operational excellence. Financial strength enables strategic investments. What's needed is continued execution, strategic acquisitions to fill capability gaps, and perhaps most importantly, developing next-generation leadership to carry the vision forward.

Key Metrics to Watch and Inflection Points Ahead

Investors should monitor several key metrics to gauge transformation progress. CDMO revenue as a percentage of total sales indicates strategic shift success—reaching 30-40% would validate the transformation thesis. Specialty chemicals EBITDA margins sustained above 25% would confirm value-addition success. Export percentage exceeding 60% would demonstrate global competitiveness.

Working capital days below 60 would indicate operational excellence. R&D spending reaching 3-4% of sales would signal innovation commitment. Most critically, return on capital employed exceeding 20% would confirm that growth investments generate attractive returns.

Several inflection points loom ahead. The $300 million agrochemical CDMO contract commencing commercial production in Q4 FY26 will test execution capabilities. The next major CDMO win—particularly if in a new chemistry area—would validate platform extensibility. Environmental regulations tightening further could advantage compliant players like Jubilant or burden them with additional costs.

Potential acquisitions could accelerate capability building or prove distracting. Entry into new chemistry platforms beyond current expertise would demonstrate innovation capability but carries execution risk. Most importantly, the next economic downturn will test the resilience of the transformed business model.

Final Reflections on the Demerger Strategy

Three years after the demerger, the strategic logic appears validated. The 2021 spun-off company has set its goals high to emerge as a global champion in its core chemistries. Both Jubilant Ingrevia and Jubilant Pharmova trade at higher combined valuations than the pre-demerger entity. Each business has attracted investors aligned with their specific strategies and risk profiles.

But the demerger's true success won't be measured in stock prices alone. It will be measured in whether each entity achieves its full potential—something the combined structure might have prevented. Early evidence suggests they're on the right path, but the journey remains long.

The demerger also offers lessons for Indian industry broadly. As Indian companies mature from domestic champions to global competitors, conglomerate structures that served well during protected markets might constrain global ambitions. The courage to split successful businesses to unlock greater success requires vision that extends beyond quarterly earnings.

The Road Ahead: Challenges and Opportunities

The next five years will determine whether Jubilant Ingrevia becomes a case study in successful transformation or another example of unfulfilled potential. The opportunities are massive—the global specialty chemicals market exceeds $800 billion and grows faster than GDP. India's share remains under 5%, suggesting enormous headroom for competitive players.

But challenges abound. Chinese competition won't disappear. Developed market peers won't cede ground easily. Technology disruption—from artificial intelligence in drug discovery to synthetic biology in chemical production—could reshape competitive dynamics. Environmental regulations will continue tightening. Customer expectations for sustainability, reliability, and innovation will only increase.

Success requires maintaining strategic focus while remaining adaptable. The core business of pyridines, acetyls, and nutrition ingredients must be protected and strengthened—they generate the cash that funds transformation. But new opportunities in CDMO, specialty chemicals, and sustainable solutions must be pursued aggressively.

Most critically, Jubilant must continue evolving its organizational capabilities. Technical expertise must deepen through R&D investment and talent development. Digital capabilities must expand beyond manufacturing into customer engagement and innovation. Leadership development must ensure the next generation can carry forward the entrepreneurial spirit that built the company.

A Story Still Being Written

Jubilant Ingrevia's story remains unfinished. The transformation from commodity chemical producer to specialty chemical champion continues. The evolution from domestic player to global competitor proceeds. The journey from family-controlled enterprise to professionally-managed corporation advances.

What makes this story compelling isn't just financial metrics or strategic positioning—it's what it represents for Indian industry. If Jubilant Ingrevia can successfully transform into a global specialty chemical leader, it validates India's potential to compete in sophisticated, technology-intensive industries. It demonstrates that emerging market companies can create genuine competitive advantages, not just labor cost arbitrage.

The next chapters will be written by how well Jubilant executes its strategy, how effectively it navigates challenges, and how successfully it captures opportunities. But regardless of outcome, the attempt itself—the ambition to transform a commodity chemical producer into a global specialty chemical champion—deserves recognition.

For investors, customers, employees, and competitors watching this transformation, Jubilant Ingrevia represents more than a company—it represents possibility. The possibility that patient building creates lasting value. The possibility that technical excellence transcends geographic boundaries. The possibility that emerging market companies can define industries, not just participate in them.

The story continues, the transformation proceeds, and the future remains unwritten. But if the past four decades provide any indication, Jubilant Ingrevia's next chapter promises to be as interesting as those that came before.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube