Kirloskar Ferrous Industries: From Iron Ploughs to India's Casting Powerhouse

I. Cold Open & The Puzzle

Picture this: In the heart of Karnataka's Koppal district, massive blast furnaces roar to life every morning, transforming raw iron ore into molten metal that will eventually power India's tractors, trucks, and industrial engines. This isn't some century-old industrial relic—this is Kirloskar Ferrous Industries Limited, a company that, despite being incorporated just in 1991, commands a market capitalization of over ₹9,100 crore and generates annual revenues exceeding ₹6,700 crore.

Here's the puzzle that should intrigue any serious student of Indian business: How does a company barely three decades old become the backbone of India's foundry-grade pig iron industry? How does it convince global automotive giants to trust it with mission-critical engine components? And perhaps most intriguingly, how does it leverage a 130-year engineering legacy while maintaining the agility of a modern manufacturer?

The answer lies not in a single breakthrough moment but in a masterclass of industrial strategy—one that involves calculated spin-offs, strategic acquisitions, backward integration moves that would make Andrew Carnegie nod in approval, and a deep understanding of what it means to build industrial capabilities in modern India.

KFIL isn't just another commodity producer churning out pig iron. It's a vertically integrated powerhouse that has quietly built moats through technical excellence, customer stickiness, and an almost obsessive focus on quality that traces back to a bicycle repair shop in 1888 Belgaum. The company manufactures everything from foundry-grade pig iron to sophisticated grey iron castings weighing up to 1,000 kilograms—components so critical that if they fail, entire engines fail.

What makes this story particularly fascinating is the timing. KFIL was born in 1991, the exact year India embarked on economic liberalization. While software companies grabbed headlines and stock market glory, KFIL was laying foundations—literally pouring concrete for blast furnaces—betting that a liberalizing India would need world-class manufacturing capabilities. Three decades later, with India positioned as the world's fastest-growing major economy and a potential alternative to China in global supply chains, that bet looks prescient.

This is a story about patient capital, engineering excellence passed down through generations, and the unglamorous but essential business of making things that make other things work. It's about a company that generates its own power from waste gases, mines its own iron ore, and has systematically reduced its dependence on external factors in a notoriously cyclical industry. As we'll see, KFIL's journey offers profound lessons about industrial scaling, family business governance, and the art of building competitive advantages in commodity businesses—lessons that resonate far beyond the foundry floor.

II. The Kirloskar Legacy: 130+ Years of Engineering DNA (1888-1991)

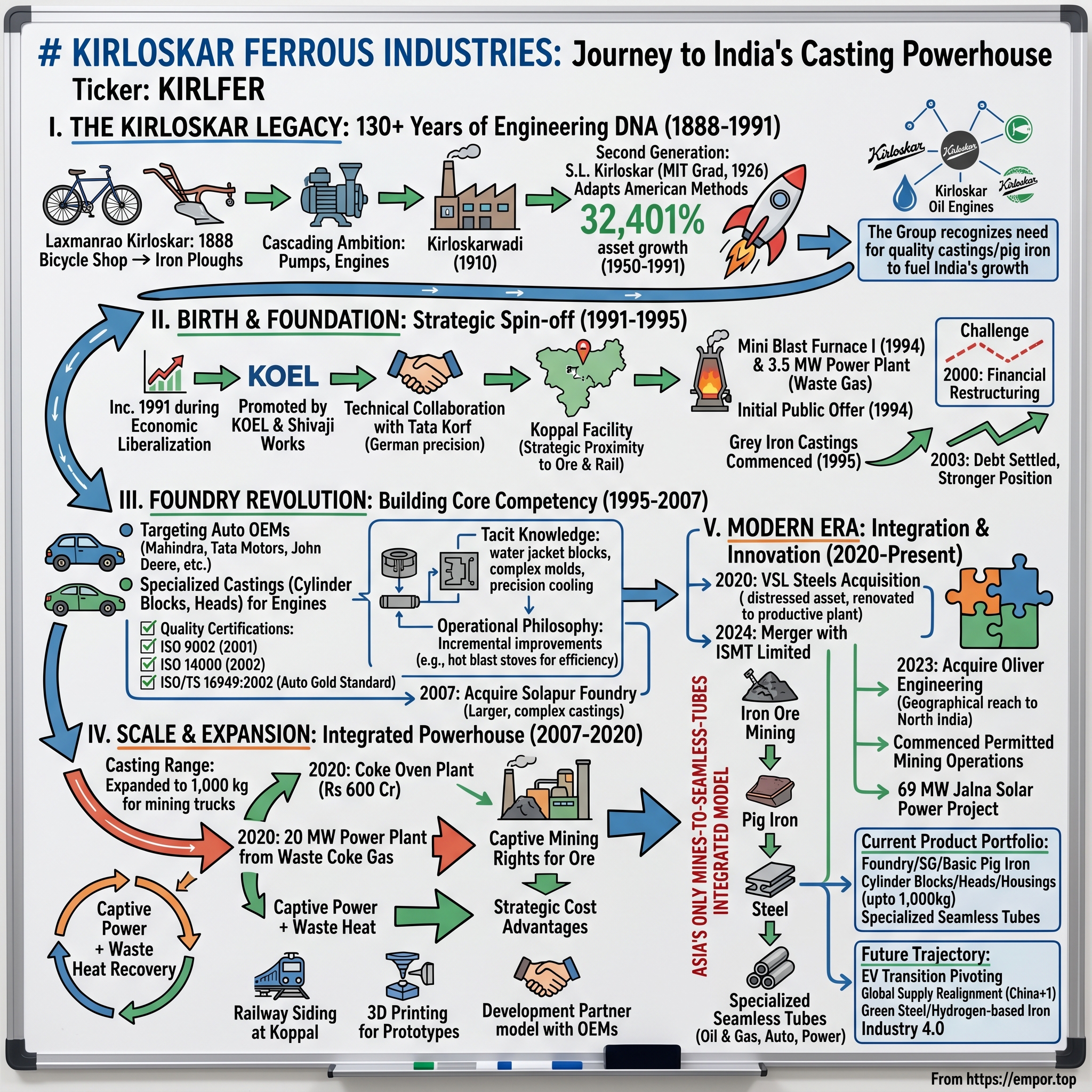

The year was 1888. While the world marveled at the completion of the Washington Monument and Jack the Ripper terrorized London's streets, in the dusty town of Belgaum in British India, a young man named Laxmanrao Kirloskar was tinkering with broken bicycles. He had no formal engineering education, no venture capital, and certainly no five-year business plan. What he had was an obsession with understanding how things worked and an almost irrational confidence that India could make things as well as any British manufacturer.

Laxmanrao's bicycle repair shop was more than a business—it was a statement of defiance against colonial India's role as merely a consumer of British manufactured goods. But bicycles were just the beginning. The real breakthrough came when he observed farmers struggling with wooden ploughs that barely scratched the hard Deccan soil. His response? Design and manufacture iron ploughs specifically engineered for Indian conditions. These weren't imported designs tweaked for local use—they were ground-up innovations that understood the unique challenges of Indian agriculture.

The success of those iron ploughs triggered something profound in Laxmanrao's thinking. If he could make ploughs, why not pumps? If pumps, why not engines? This cascading ambition led to a decision that would have seemed insane to his contemporaries: building an entire industrial township from scratch. Kirloskarwadi, established in 1910, wasn't just a factory with worker quarters. It was Laxmanrao's vision of what industrial India could be—schools, hospitals, training centers, all built around the manufacturing facility. Think of it as India's answer to Bournville or Pullman, but with a distinctly Indian social fabric. Kirloskar Brothers Limited was formally established in 1920, but the real transformation came with the second generation. Enter Shantanurao Laxmanrao Kirloskar—S.L. Kirloskar to those who knew him. Here was a man who bridged two worlds. He earned a Bachelor of Science degree in mechanical engineering from MIT in Cambridge, Massachusetts, becoming among the first Indians to graduate from MIT. But what's fascinating isn't just the MIT degree—it's what he did with it.

When Shantanurao returned to India in 1926, he didn't try to transplant American industrial methods wholesale. Instead, he adapted them to Indian conditions, creating what would become a uniquely Indian model of industrial development. The company under Shantanurao achieved one of the highest growth rates in Indian history, with 32,401% growth of assets from 1950 to 1991. Let that number sink in—a growth rate that would make even the most aggressive Silicon Valley venture capitalist's head spin, achieved not through software or financial engineering, but through making pumps, engines, and industrial equipment.

The Kirloskar approach was methodical, almost Germanic in its precision. First, master one technology. Then, use that mastery to enter adjacent markets. Pumps led to engines. Engines led to machine tools. Each expansion built on the technical capabilities developed in the previous one. By the 1940s, Kirloskar wasn't just one company—it was becoming a constellation of specialized firms, each focused on a particular aspect of engineering.

The group structure that emerged wasn't arbitrary. Kirloskar Electric Company handled electrical equipment. Kirloskar Oil Engines focused on diesel engines. Each entity had its own management, its own capital structure, but all shared the same DNA—that relentless focus on engineering excellence that traced back to Laxmanrao's bicycle shop.

But why did ferrous need its own company? The answer reveals the strategic thinking that would define KFIL's birth. By the late 1980s, the Kirloskar Group recognized that India's industrial growth would create massive demand for high-quality castings and pig iron. These weren't sexy products—no one writes breathless news articles about grey iron castings. But they were essential. Every engine, every pump, every piece of industrial equipment needed them. The group could either remain dependent on external suppliers of varying quality, or it could control this critical input itself.

The decision to create Kirloskar Ferrous Industries Limited wasn't just about vertical integration. It was about recognizing that in industrial businesses, controlling quality at every stage of production isn't just an advantage—it's survival. And it was about timing. Something big was about to happen in India, and the Kirloskars, with their century of industrial experience, could sense it coming.

III. Birth of KFIL: The Strategic Spin-off (1991-1995)

September 10, 1991. While financial newspapers were consumed with India's foreign exchange crisis and the new Finance Minister Manmohan Singh's radical liberalization agenda, a quieter but equally significant event was unfolding in corporate boardrooms in Pune. Kirloskar Ferrous Industries Limited was being incorporated as a flagship company of the Kirloskar Group, promoted by Kirloskar Oil Engines Limited and Shivaji Works Limited.

The timing was no accident. India's economic liberalization wasn't just about removing license raj restrictions—it was about preparing Indian industry for global competition. The Kirloskar leadership understood that the cozy, protected markets of the past four decades were ending. Indian manufacturers would soon compete with international players who had access to better technology, cheaper capital, and decades of experience in competitive markets. The response couldn't be defensive; it had to be aggressive. The technical foundation of KFIL came through a partnership that revealed the group's strategic thinking. In March 1992, KFIL entered into a technical collaboration with Tata Korf Engineering Services Ltd for technical know-how and consultancy services relating to production of hot metal. This wasn't just about importing technology—it was about learning from one of the most advanced metallurgical engineering firms of the time. Tata Korf brought German precision engineering to Indian conditions, a combination that would prove crucial for KFIL's future success.

Building the Koppal facility was an exercise in industrial ambition. In the arid landscape of northern Karnataka, far from major urban centers, KFIL was constructing what would become one of India's most sophisticated pig iron production facilities. The location wasn't chosen for convenience—it was chosen for strategic proximity to iron ore sources and access to railway networks that could move thousands of tons of finished product across India.

Commercial production of pig iron from Mini Blast Furnace I commenced in 1994, along with something that would become a hallmark of KFIL's approach to manufacturing: a 3.5 MW power plant using blast furnace gas. This wasn't just about producing pig iron—it was about creating an integrated system where waste from one process became fuel for another. In an industry where energy costs could make or break profitability, this early focus on energy efficiency would prove prescient.

In the same year, KFIL issued its Initial Public Offer. The timing of the IPO tells us something important about the company's confidence. Just months after commencing commercial production, with no established track record as an independent entity, KFIL was asking public investors to bet on its vision. The fact that they succeeded speaks to both the Kirloskar brand's credibility and the market's hunger for industrial capacity in liberalizing India.

Production of grey iron castings commenced in 1995, marking KFIL's evolution from a pure commodity producer to a value-added manufacturer. This wasn't a small step—it was a fundamental transformation of the business model. Pig iron is essentially a commodity, subject to brutal price competition and cyclical demand. Castings, especially sophisticated ones for automotive applications, are custom-engineered products with higher margins and deeper customer relationships.

The early years weren't without challenges. By 2000, KFIL had to enter into financial restructuring with IDBI and other institutions. This wasn't failure—it was the reality of building capital-intensive businesses in a country where interest rates were high and demand was still developing. The fact that KFIL emerged from this restructuring stronger, completing a one-time settlement with financial institutions by 2003, demonstrated the underlying strength of the business model and the management's ability to navigate financial turbulence.

What's remarkable about this period is how KFIL was simultaneously building three capabilities that would define its future: technical excellence in metallurgy, deep customer relationships with automotive OEMs, and financial discipline that would allow it to fund future expansions. Each of these capabilities reinforced the others, creating a virtuous cycle that would accelerate in the years to come.

IV. The Foundry Revolution: Building Core Competency (1995-2007)

Walking through a foundry is like stepping into Dante's Inferno—molten metal glowing orange-hot, the deafening clang of machinery, workers in heat-resistant suits moving with practiced precision through air thick with metallic dust. It's here, in this harsh environment, that KFIL began transforming itself from a pig iron supplier into something far more sophisticated: a trusted partner to India's automotive giants.

The shift to manufacturing grey iron castings wasn't just about adding a product line—it was about entering an entirely different business. KFIL developed capabilities to produce grey iron castings for applications such as cylinder blocks, cylinder heads, and different types of housings required by automobile, tractor, and diesel engine industries. These aren't simple products. A cylinder block, for instance, must withstand thousands of controlled explosions per minute, maintain precise tolerances measured in microns, and do so reliably for hundreds of thousands of kilometers.

Consider what it takes to win an automotive OEM as a customer. These companies—Mahindra, Tata Motors, John Deere—don't switch suppliers lightly. A failed casting doesn't just mean a warranty claim; it can mean vehicles stranded on highways, brand reputation damaged, lives potentially at risk. Before KFIL could ship its first casting to these customers, it had to prove not just that it could make the product, but that it could make it consistently, at scale, with zero defects, for years.

The quality journey began with certifications, but these were just table stakes. In 2001, KFIL received ISO 9002 certification, followed by ISO 14000 certification in 2002. More importantly, ISO/TS 16949:2002 certification was added to the company's quality list in 2005—this was the automotive industry's gold standard, a signal that KFIL could meet the exacting standards of global automotive supply chains.

But certifications don't make castings—people and processes do. KFIL invested heavily in both. The company developed what it called "matured knowledge on development of water jacketed blocks"—a seemingly simple phrase that represents years of trial and error, countless failed experiments, and gradual mastery of one of the most complex aspects of engine manufacturing. Water jackets—the channels through which coolant flows around an engine—must be precisely positioned, uniformly thick, and completely free of porosity. Get it wrong, and engines overheat.

The technology partnerships during this period were crucial but subtle. Unlike software, where code can be copied and deployed instantly, foundry knowledge is embodied in people, processes, and physical infrastructure. KFIL's engineers had to learn how to read the color of molten metal to judge its temperature, how to design gating systems that would fill complex molds without creating air pockets, how to control cooling rates to prevent stress fractures. This tacit knowledge, accumulated over thousands of production runs, became KFIL's real competitive advantage.

During 2007, the company acquired the Solapur foundry from Kirloskar Oil Engines Ltd. This wasn't just any acquisition—it was bringing a sister company's foundry in-house, along with its customer relationships, technical capabilities, and most importantly, its people who had decades of experience making castings for Kirloskar's own engines. The Solapur facility specialized in larger, more complex castings, expanding KFIL's addressable market.

The integration of Solapur revealed KFIL's operational philosophy. Rather than imposing a top-down integration, the company preserved what worked while upgrading what didn't. The facility's customer relationships were maintained, its specialized knowledge was preserved, but its processes were systematically upgraded with new equipment and quality systems. This respectful integration would become a template for future acquisitions.

By 2007, KFIL had also commissioned hot blast stoves for its mini blast furnace—a technical upgrade that might seem minor but represented a fundamental improvement in efficiency. Hot blast stoves preheat air before it enters the blast furnace, reducing coke consumption and increasing productivity. It's the kind of incremental improvement that doesn't make headlines but drives profitability in commodity businesses.

What emerged from this twelve-year period was a company that had successfully executed one of the hardest transitions in manufacturing: moving from commodity production to engineered products. KFIL was no longer just melting iron—it was solving complex engineering problems for customers who had alternatives. The trust built during these years, casting by casting, delivery by delivery, would prove invaluable when the real growth phase began.

V. Scale & Expansion: The Growth Machine (2007-2020)

The global financial crisis of 2008 should have been a disaster for a company like KFIL. Automotive production collapsed worldwide, industrial activity ground to a halt, and credit markets froze. Yet KFIL emerged from the crisis not weakened but positioned for explosive growth. The secret lay in a contrarian insight: while others were cutting capacity, KFIL recognized that India's infrastructure build-out and automotive growth were secular trends merely interrupted, not reversed, by the crisis.

The Solapur acquisition in 2007 had given KFIL a second manufacturing base, but more importantly, it had proven the company's ability to integrate complex industrial operations. The company now had three manufacturing facilities, situated at Koppal district and Chitradurga district in Karnataka, and at Solapur district in Maharashtra. This geographic diversification wasn't just about risk management—it was about being closer to customers, reducing transportation costs, and having redundancy in production capacity.

The real transformation during this period was in scale and sophistication. KFIL systematically expanded its casting capabilities from 300-kilogram single pieces to a remarkable 1,000-kilogram range. To understand what this means, imagine casting an engine block for a small car versus one for a massive mining truck. The physics changes completely—cooling rates, mold design, handling equipment, everything must be rethought. Yet KFIL made this transition while maintaining quality standards that satisfied the world's most demanding OEMs.The backward integration strategy that truly set KFIL apart came to fruition in 2020 with the commissioning of a ₹600 crore coke oven plant. This wasn't just another capacity expansion—it was a fundamental reimagining of the business model. The company commissioned a 2 lakh Metric Ton Coke Oven project on 31st March, 2020. Coke is essential for blast furnace operations, and by producing it in-house, KFIL could control both quality and costs while reducing dependence on imported metallurgical coke.

But here's where KFIL's engineering DNA really showed: they didn't just build a coke oven plant. A 20MW Power Plant, working on waste gas generated from Coke Oven plant was commissioned in June, 2020. The coke oven produces combustible gases as a byproduct. Most companies would flare these gases or sell them at low prices. KFIL built a power plant to convert them into electricity, creating a circular economy within its own operations. This 20MW of captive power generation meant lower energy costs and greater independence from grid power—crucial advantages in energy-intensive metallurgical operations.

The period also saw KFIL becoming increasingly sophisticated in its approach to customer relationships. The company wasn't just a supplier; it was becoming a development partner. When automotive OEMs needed new engine designs for emission norms or fuel efficiency targets, KFIL's engineers worked alongside them, developing new casting designs, new alloys, new production processes. This co-creation model created switching costs that went beyond commercial contracts—it embedded KFIL into its customers' product development cycles.

Geographic expansion continued strategically. The railway siding project at the Koppal plant, which became operational during this period, might seem like mundane infrastructure, but it represented a significant competitive advantage. Direct rail access meant KFIL could move thousands of tons of pig iron and castings without the trucking costs and logistics complexity that plagued competitors. In a business where transportation can represent 10-15% of delivered costs, this was a meaningful differentiator.

The company also began pushing the boundaries of what was possible in casting technology. The installation of 3D printing facilities at the Koppal plant for rapid prototype castings reduced new product development time from months to weeks. This wasn't about replacing traditional casting—it was about winning new business by being faster and more responsive than competitors. When an OEM needed to test a new engine design, KFIL could produce prototype castings in days, not months.

By 2020, KFIL had transformed from a pig iron producer with some casting capabilities into an integrated metallurgical powerhouse. It could mine ore, produce coke, generate power, manufacture pig iron, create sophisticated castings, and even machine them to final specifications. Each piece of this integration created value, but together they created something more powerful: a business model that was incredibly difficult for competitors to replicate.

VI. The Modern Era: Integration & Innovation (2020-Present)

December 2020 marked a pivotal moment in KFIL's evolution. While the world grappled with pandemic disruptions, the Company acquired movable and immovable assets relating to the pig iron plant of VSL Steels Limited with a capacity of 1,50,000 MT per annum at Paramenahally Village, Chitradurga District, Karnataka. The timing seemed counterintuitive—acquiring distressed assets during a global crisis. But KFIL's management saw opportunity where others saw risk.

The VSL Steels acquisition wasn't just about adding capacity. It was a textbook example of value creation through operational excellence. The plant had been idle, its equipment deteriorating, its workforce dispersed. KFIL's team methodically renovated the plant and machinery, and by February 8, 2021, commenced manufacturing operations. Within months, a dead asset was transformed into a productive facility adding 150,000 MT of annual pig iron capacity. But the real game-changer was the merger with ISMT Limited, creating what brought an opportunity to integrate iron ore to seamless tubes. This wasn't just another acquisition—it was the creation of Asia's only mines-to-seamless-tubes integrated model. For KFIL this was a step towards forward integration and product diversification. On the other hand for ISMT this was a step towards backward integration.

ISMT was the largest integrated specialized seamless tube manufacturer in India, producing tubes ranging from 6 to 273 mm diameter. But it was also financially stressed, burdened with debt, struggling with raw material costs. KFIL saw what others missed: a perfect strategic fit. ISMT needed reliable, cost-effective raw materials; KFIL had them. KFIL wanted to move up the value chain into specialized products; ISMT provided the platform.

The merger, completed in August 2024, wasn't just about combining balance sheets. It was about creating an industrial ecosystem where iron ore mined in Karnataka could be transformed into sophisticated seamless tubes used in critical applications like oil and gas exploration, power generation, and automotive components. The synergies were immediate and substantial—ISMT's raw material costs dropped, KFIL's product portfolio expanded, and customers got a single supplier who could guarantee quality from ore to finished tube.

Simultaneously, KFIL was executing another strategic move. In September 2023, the company completed the acquisition of Oliver Engineering, a specialist in ferrous casting and machining. This acquisition gave KFIL the opportunity to expand geographical reach and cater to the growing needs of customers in Northern India. Oliver Engineering, despite being under financial stress, had valuable assets: established customer relationships in North India, specialized machining capabilities, and a trained workforce.

The mining operations marked another milestone. This quarter marked the commencement of mining operations with an annual permitted capacity of 1.24 lakh MT. For a company that consumes millions of tons of iron ore annually, having captive mining capacity, even if limited, provided a hedge against price volatility and supply disruptions. The sustainability push wasn't just corporate greenwashing. KFIL commissioned Phase II of the Jalna solar power project, bringing total capacity to 69 MW DC at Jalna. In an industry where energy costs can represent 20-30% of total production costs, generating solar power at near-zero marginal cost created a structural advantage. The solar installations, combined with waste heat recovery and coke oven gas power generation, meant KFIL was increasingly insulated from energy price volatility.

What's remarkable about this period is how KFIL managed multiple complex integrations simultaneously while maintaining operational performance. The VSL Steels plant renovation, the ISMT merger, the Oliver Engineering acquisition, the mining operations commencement, the solar project commissioning—any one of these would be a major undertaking for most companies. KFIL executed all of them in parallel, suggesting not just financial strength but deep operational capabilities and management bandwidth.

VII. Product Portfolio & Market Position

Understanding KFIL's product portfolio requires appreciating the technical complexity hidden beneath seemingly simple descriptions. The company's pig iron products include foundry grade pig iron, spherodized graphite (S.G.) grade pig iron and basic grade pig iron. Each grade requires different chemistry, different cooling rates, different handling procedures. Get the silicon content wrong by 0.1%, and foundry-grade pig iron becomes unsuitable for precision castings.

The real technical mastery shows in the casting business. The Company specializes in producing custom grey iron castings for original equipment manufacturers and tier-I suppliers. Its main casting products include cylinder blocks, cylinder heads and housings, which are used in a wide range of engines, across construction machines, farm equipment and utility vehicles. A modern diesel engine cylinder block isn't just a chunk of metal with holes—it's a precisely engineered component with internal cooling channels, oil galleries, bearing surfaces, all cast in a single piece with tolerances measured in hundredths of millimeters.

Consider what it takes to cast a 1,000-kilogram engine block for a mining truck. The mold alone can weigh several tons. The molten iron must flow through intricate channels, filling every cavity without creating air pockets or cold shuts. The cooling must be controlled so precisely that different sections of the casting solidify at different rates, preventing stress concentrations. One mistake, and you have a ton of expensive scrap metal.

KFIL's customer concentration reveals both strength and vulnerability. The company serves virtually every major automotive and industrial OEM in India—Mahindra, Tata Motors, John Deere, Caterpillar, Cummins. This customer list reads like a who's who of global industrial giants. But it also means KFIL's fortunes are tied to the capital expenditure cycles of these industries.

The seamless tubes addition through ISMT created an entirely new dimension to the portfolio. These aren't commodity pipes—they're precision-engineered tubes used in critical applications where failure isn't an option. Oil and gas drilling, power plant boilers, automotive fuel injection systems—all require tubes that can withstand extreme pressures, temperatures, and corrosive environments. ISMT's capability to produce tubes ranging from 6 to 273 mm diameter means KFIL can now serve everything from precision medical equipment to massive industrial heat exchangers.

What creates KFIL's competitive moat isn't any single product but the integrated system. When a customer needs a new engine design, KFIL can provide everything from the initial prototype castings (using 3D printing) to the production castings to the seamless tubes for fuel systems. This one-stop-shop capability creates switching costs that go beyond price—it's about engineering collaboration, supply chain simplicity, and reduced vendor management complexity.

The geographic positioning of manufacturing facilities—Koppal and Chitradurga in Karnataka, Solapur in Maharashtra, and now Oliver Engineering near Chandigarh—isn't random. Each location serves specific customer clusters while maintaining logistics efficiency. Koppal serves the southern automotive belt, Solapur covers western India, Oliver addresses northern markets. This distributed manufacturing also provides risk mitigation—a disruption at one facility doesn't cripple the entire operation.

Market position data reveals KFIL's true standing. The company is among the top three pig iron producers in India, with significant market share in organized sector. In specialized castings for diesel engines above 50 HP, KFIL commands even stronger positions. But perhaps most importantly, in the integrated mines-to-castings and mines-to-tubes space, KFIL stands alone in Asia—a unique position that becomes more valuable as customers increasingly focus on supply chain security and sustainability.

VIII. Financial Architecture & Capital Allocation

The numbers tell a story of both achievement and challenge. For the consolidated Q3 FY25, the company reported a revenue from operations of Rs 1,607.6 crore, reflecting a 4 per cent increase compared to Rs 1,548.2 crore in Q3 FY24. But beneath the modest topline growth lies margin compression that reveals the brutal realities of commodity businesses. The consolidated EBITDA for Q3 FY25 stood at Rs 173.8 crore, showing a significant 25 per cent decrease from Rs 232.1 crore in the same period last year.

PBT also saw a sharp decline of 47 per cent, reaching Rs 78.5 crore in Q3 FY25, down from Rs 147.9 crore in Q3 FY24. These aren't just numbers—they're the financial expression of what happens when pig iron prices collapse, input costs remain elevated, and end-user industries defer capital expenditure. Yet what's remarkable is how KFIL has maintained positive cash flows and continued investing in growth even during this downturn.

The company's return on equity story is more nuanced than headline numbers suggest. Company has a low return on equity of 13.0% over last 3 years. Promoter holding has decreased over last 3 years: -8.05%. The ROE compression reflects both the cyclical downturn and the capital intensity of recent expansions. The promoter holding decrease, while concerning at first glance, actually reflects dilution from the ISMT merger—a strategic move that expanded the business scope dramatically.

Working capital management in KFIL's business is an art form. The company must maintain enormous inventories of raw materials—iron ore, coke, limestone—while managing receivables from automotive OEMs who demand extended payment terms. A single day's production at full capacity consumes raw materials worth crores. Yet KFIL has managed to maintain positive operating cash flows even during downturns, suggesting sophisticated treasury management.

The capital allocation decisions during 2020-2024 reveal strategic clarity. The coke oven plant (₹600 crore), solar installations (estimated ₹300+ crore for 69MW), the ISMT acquisition (₹476 crore for initial stake), mining rights, the VSL Steels assets—total capital deployed exceeds ₹2,000 crore. These weren't random acquisitions; each investment either reduced costs (coke oven, solar), expanded addressable markets (ISMT, Oliver), or secured raw materials (mining, VSL Steels).

Dividend policy has remained conservative but consistent. Despite margin pressures, KFIL has maintained dividend payments, signaling management's confidence in long-term cash generation. The interim dividends announced periodically provide regular income to shareholders while preserving capital for growth investments. This balanced approach—neither starving the business of growth capital nor hoarding cash—suggests mature capital allocation thinking.

The debt position deserves attention. Despite multiple acquisitions and major capex programs, KFIL has maintained manageable leverage ratios. The company's ability to fund the coke oven plant, solar projects, and acquisitions without excessive leverage speaks to both strong internal cash generation and prudent financial management. The ISMT acquisition, which came with its own debt burden, was restructured to ensure the combined entity's balance sheet remained healthy.

What emerges from the financial architecture is a company that understands the cyclical nature of its business and has structured itself accordingly. Variable cost structures where possible, strategic fixed investments where necessary, and always maintaining financial flexibility for opportunistic moves. It's not the financials of a high-growth tech company, but rather those of a disciplined industrial enterprise built for longevity.

IX. Challenges & Headwinds

The elephant in the room is commodity price volatility. Margins remained under pressure due to lower realisations on Pig Iron and Steel. When pig iron prices can swing 30-40% in a single year, and you're producing millions of tons, even the best operational efficiency can't fully offset the impact. KFIL sells into spot markets for pig iron while many input costs are fixed or semi-fixed. This creates an asymmetric risk profile—input costs rise quickly but fall slowly, while selling prices do the opposite.

Competition from imports, particularly from China and other Asian producers, represents a constant threat. Chinese pig iron and castings often arrive in Indian ports at prices below KFIL's production costs. While quality differences and customer relationships provide some protection, the threat of dumping remains real. The government's occasional anti-dumping duties provide temporary relief but aren't a permanent solution.

Environmental regulations are tightening globally and India is no exception. The blast furnace operations, coke ovens, and casting processes all generate emissions that are under increasing scrutiny. While KFIL has invested in pollution control equipment and cleaner technologies, the regulatory goalposts keep moving. Carbon taxes, emission trading schemes, and net-zero commitments from customers all threaten to increase costs or reduce demand for traditional iron and steel products.

The cyclicality of end-user industries creates feast-or-famine dynamics. When tractor sales boom, KFIL's order books overflow. When automotive production slumps, capacity utilization drops. This isn't just about managing working capital—it's about maintaining skilled workforces, keeping complex equipment operational, and satisfying customer needs during both peaks and troughs. The fixed cost base means profitability swings wildly with capacity utilization.

Technology disruption looms larger than many realize. Electric vehicles require different castings than internal combustion engines—sometimes fewer, sometimes none at all. 3D printing threatens to bypass traditional casting for certain applications. While these changes will take years or decades to fully materialize, they require KFIL to constantly evolve its capabilities and product mix.

The human capital challenge is often underappreciated. Operating blast furnaces and foundries requires specialized skills that take years to develop. As India's economy modernizes, fewer young workers want careers in heavy industry. KFIL must compete with IT companies and service sectors for talent, while also managing an aging workforce with irreplaceable technical knowledge. The knowledge transfer from retiring experts to new engineers is a constant challenge.

Customer concentration, while providing stable revenues, creates vulnerability. A single major customer reducing orders can impact utilization rates significantly. The automotive industry's shift toward platform consolidation means fewer engine variants, potentially reducing the variety of castings needed. KFIL must constantly balance the efficiency of serving large customers with the risk mitigation of diversification.

Infrastructure constraints in India add operational complexity. Despite improvements, power availability remains inconsistent, forcing reliance on captive generation. Road and rail networks, while better than a decade ago, still struggle with the volumes KFIL needs to move. Ports face congestion, adding time and cost to export shipments. These aren't company-specific problems, but they affect KFIL's competitiveness versus global peers.

Financial market perceptions pose their own challenges. Industrial companies, particularly those in commodity-exposed sectors, trade at lower multiples than service or technology businesses. This makes raising equity capital expensive and limits financial flexibility. The market's focus on quarterly results conflicts with the long-term nature of industrial investments.

X. The Playbook: Lessons from KFIL

The first lesson from KFIL's journey is the power of patient industrial building on generational foundations. The company didn't emerge from nothing—it built upon 130 years of engineering heritage, customer relationships, and technical knowledge accumulated by the Kirloskar Group. This isn't replicable by financial engineering or private equity rollups. It requires decades of consistent execution, reputation building, and technical capability development.

The art of industrial scaling in India requires understanding that you're not just building factories—you're creating ecosystems. KFIL's success came from recognizing that in India, you often need to build your own infrastructure, train your own workforce, and sometimes even develop your own suppliers. The Koppal facility wasn't just about installing blast furnaces; it was about creating an entire industrial complex in a relatively underdeveloped region.

Backward integration as competitive advantage is perhaps KFIL's most important strategic insight. In developed markets, companies can rely on efficient supplier networks. In India, controlling critical inputs isn't just about cost—it's about ensuring quality, availability, and reliability. The coke oven plant, mining operations, and power generation aren't vanity projects; they're survival mechanisms in a market where supply chains can be unreliable.

Managing commodity businesses with value-added products is a delicate balance. Pure commodity producers are price takers with no differentiation. Pure specialty producers face limited markets and customer concentration. KFIL's approach—maintaining commodity volumes for scale while developing specialized capabilities for margins—provides both stability and growth potential. The pig iron provides cash flow and scale; the sophisticated castings provide margins and customer stickiness.

The sustainability as business strategy approach predates ESG investing trends. KFIL's waste heat recovery, solar installations, and circular economy initiatives weren't driven by investor pressure—they were driven by economic logic. In energy-intensive industries, sustainability and profitability align naturally. Every megawatt generated from waste heat or solar is a megawatt not purchased from the grid. Every ton of slag converted to useful product is revenue that would otherwise be disposal cost.

Family business governance in public markets presents unique challenges and opportunities. The Kirloskar family's continued involvement provides long-term thinking and stakeholder capitalism that pure professional management might lack. But it also requires careful balance—maintaining family control while respecting minority shareholders, ensuring professional management while preserving entrepreneurial culture. KFIL's governance structure, with independent directors and professional managers working alongside family members, offers a template for this balance.

The discipline of core competence focus despite diversification temptations is crucial. KFIL could have ventured into real estate (they own vast land banks), financial services (they have strong cash flows), or unrelated manufacturing. Instead, every expansion—from pig iron to castings to tubes—built on existing metallurgical capabilities. This isn't conservatism; it's recognition that industrial competence is hard-won and easily lost.

The importance of technical depth in leadership cannot be overstated. KFIL's senior management includes engineers who understand the physics of metal solidification, the chemistry of alloy composition, the mechanics of casting design. This isn't just about making better technical decisions—it's about earning respect from customers, suppliers, and shop floor workers who can distinguish real expertise from MBA buzzwords.

Timing market cycles while building through them represents sophisticated strategic thinking. KFIL's major expansions often came during downturns when assets were cheap and competitors were retrenching. But the company also maintained capabilities through cycles, not shutting facilities or firing skilled workers during downturns. This counter-cyclical investment approach requires financial strength and strategic conviction.

The ecosystem orchestration model deserves recognition. KFIL doesn't just manage its own operations—it develops suppliers, supports customer capabilities, and even helps develop local communities around its facilities. This isn't corporate social responsibility—it's recognition that in emerging markets, your success depends on the success of your ecosystem.

XI. Future Trajectory & Strategic Options

The electric vehicle transition presents both existential threat and transformational opportunity. Battery-electric vehicles need fewer castings than internal combustion engines—no engine blocks, no cylinder heads, no exhaust manifolds. But they need other components: motor housings, battery enclosures, structural castings for lightweight construction. KFIL's challenge is pivoting its technical capabilities toward these new requirements while maintaining cash flows from traditional products during the transition.

The global supply chain realignment following COVID-19 and geopolitical tensions creates opportunities. As companies seek to diversify away from China, India emerges as an alternative manufacturing hub. KFIL's established capabilities, quality certifications, and track record position it well to capture this "China plus one" demand. But execution will be crucial—global customers have exacting standards and alternatives.

Export opportunities in specialized castings and seamless tubes could drive the next growth phase. While pig iron exports face commodity pricing pressures, specialized products can command premium prices in global markets. KFIL's technical capabilities already match global standards; the challenge is developing market access, managing currency risks, and meeting diverse regulatory requirements.

Further consolidation in the fragmented Indian foundry industry seems inevitable. Thousands of small foundries operate with outdated technology and marginal economics. Environmental regulations, quality requirements, and customer consolidation will force industry restructuring. KFIL, with its financial strength and operational expertise, could lead this consolidation, acquiring distressed assets and modernizing them—repeating the VSL Steels and Oliver Engineering playbook.

Green steel and hydrogen-based iron production represent long-term technological shifts. While blast furnaces will remain economical for decades, customer pressure for low-carbon products is building. KFIL's solar investments and energy efficiency initiatives position it well for this transition. The company could potentially pilot hydrogen-based direct reduction processes, leveraging India's emerging green hydrogen ecosystem.

We are seeing early signs of recovery in our casting and tube business. The seamless tubes business, particularly through the ISMT integration, opens new growth vectors. Critical sectors like defense, nuclear power, and aerospace require specialized tubes with exacting specifications. These markets offer higher margins and longer-term contracts than traditional industrial applications.

Industry 4.0 and digitalization present efficiency opportunities. Predictive maintenance using IoT sensors could reduce blast furnace downtime. AI-powered quality control could catch defects earlier. Digital twins of casting processes could optimize designs before physical production. While KFIL has begun this journey with 3D printing for prototypes, the full potential remains untapped.

The circular economy focus could differentiate KFIL in commodity markets. Beyond waste heat recovery and slag utilization, opportunities exist in steel scrap processing, industrial symbiosis with other manufacturers, and even carbon capture from blast furnace gases. As carbon pricing mechanisms develop, these initiatives could transform from cost centers to profit centers.

Strategic partnerships with global technology leaders could accelerate capability building. Rather than developing all technologies internally, KFIL could partner with global leaders in green steel, advanced materials, or specialized coatings. The company's strong balance sheet and established operations make it an attractive partner for technology companies seeking Indian market access.

The infrastructure and capital goods cycle in India provides a multi-decade growth runway. India's infrastructure spending, manufacturing ambitions, and urbanization will drive demand for castings and steel products. KFIL's integrated model positions it to capture value across this growth, from supplying pig iron to infrastructure projects to providing specialized components for industrial machinery.

XII. Power & Conclusion

What makes KFIL special in Indian manufacturing isn't any single factor but the combination of several reinforcing advantages. It's a 30-year-old company built on 130-year-old foundations. It operates in commodity markets but with specialized capabilities. It's family-controlled but professionally managed. It's asset-heavy but financially disciplined. These apparent contradictions aren't weaknesses—they're the source of KFIL's resilience and competitive advantage.

The bear case for KFIL is straightforward: it's a commodity business in a mature industry facing technological disruption. Pig iron has been made the same way for centuries. Electric vehicles threaten demand for engine castings. Chinese competition could intensify. Environmental regulations could impose massive costs. Financial markets will never value industrial companies like technology firms. These are all valid concerns that any investor must weigh.

The bull case rests on execution and integration. KFIL isn't just a commodity producer—it's an integrated solutions provider with irreplaceable customer relationships. The mines-to-tubes integration creates cost advantages no standalone player can match. The technical capabilities in sophisticated castings create switching costs that protect against competition. The sustainability initiatives position KFIL for a carbon-constrained future. And India's industrial growth provides a multi-decade tailwind.

Key metrics to watch going forward include capacity utilization rates across facilities (indicating demand recovery), EBITDA per ton (showing pricing power and cost control), successful integration of recent acquisitions (particularly ISMT and Oliver Engineering), progress on sustainability initiatives (especially solar capacity and emission reductions), and customer diversification (reducing concentration risk).

The Kirloskar way—patient capital, technical excellence, stakeholder capitalism, and strategic clarity—offers lessons beyond KFIL itself. In an era of quarterly capitalism and financial engineering, KFIL represents something different: industrial capitalism that creates real value through engineering excellence and operational efficiency. It's not as exciting as software or as glamorous as consumer brands, but it's the foundation upon which modern economies are built.

KFIL's story is ultimately about transformation without abandoning core identity. From iron ploughs to engine blocks to seamless tubes, the products have changed but the engineering excellence remains. From family partnership to public company to integrated conglomerate, the structure has evolved but the values persist. From serving local farmers to supplying global OEMs, the market has expanded but the commitment to quality endures.

The future will bring new challenges—technological disruption, environmental pressures, global competition. But KFIL's history suggests it will adapt as it always has: deliberately, technically, and with an eye on the next generation rather than the next quarter. For investors, customers, and competitors alike, KFIL represents what patient industrial building can achieve in emerging markets—not overnight success, but enduring value creation.

In the grand narrative of Indian industrialization, KFIL occupies a unique position. It's neither a colonial-era giant like Tata Steel nor a liberalization-era startup like newer manufacturing companies. It's something in between and perhaps more interesting: a company that inherited industrial DNA but had to build its own business, that leveraged family legacy but embraced professional management, that started with commodity products but evolved toward specialization.

As India stands at an inflection point—aspiring to become a global manufacturing hub, transitioning toward cleaner energy, building infrastructure for a $10 trillion economy—companies like KFIL will play crucial but often unnoticed roles. Every highway needs steel reinforcement, every factory needs industrial machinery, every vehicle needs precision components. KFIL doesn't make the products consumers see, but it makes the products that make those products possible.

The investment case for KFIL isn't about explosive growth or disruption—it's about steady value creation through cycles, competitive advantages that strengthen over time, and exposure to India's industrial transformation. Whether that appeals to an investor depends on their time horizon, risk tolerance, and belief in India's manufacturing future. What's undeniable is that KFIL has built something substantial and enduring—a modern industrial enterprise rooted in engineering excellence and positioned for whatever future unfolds.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube