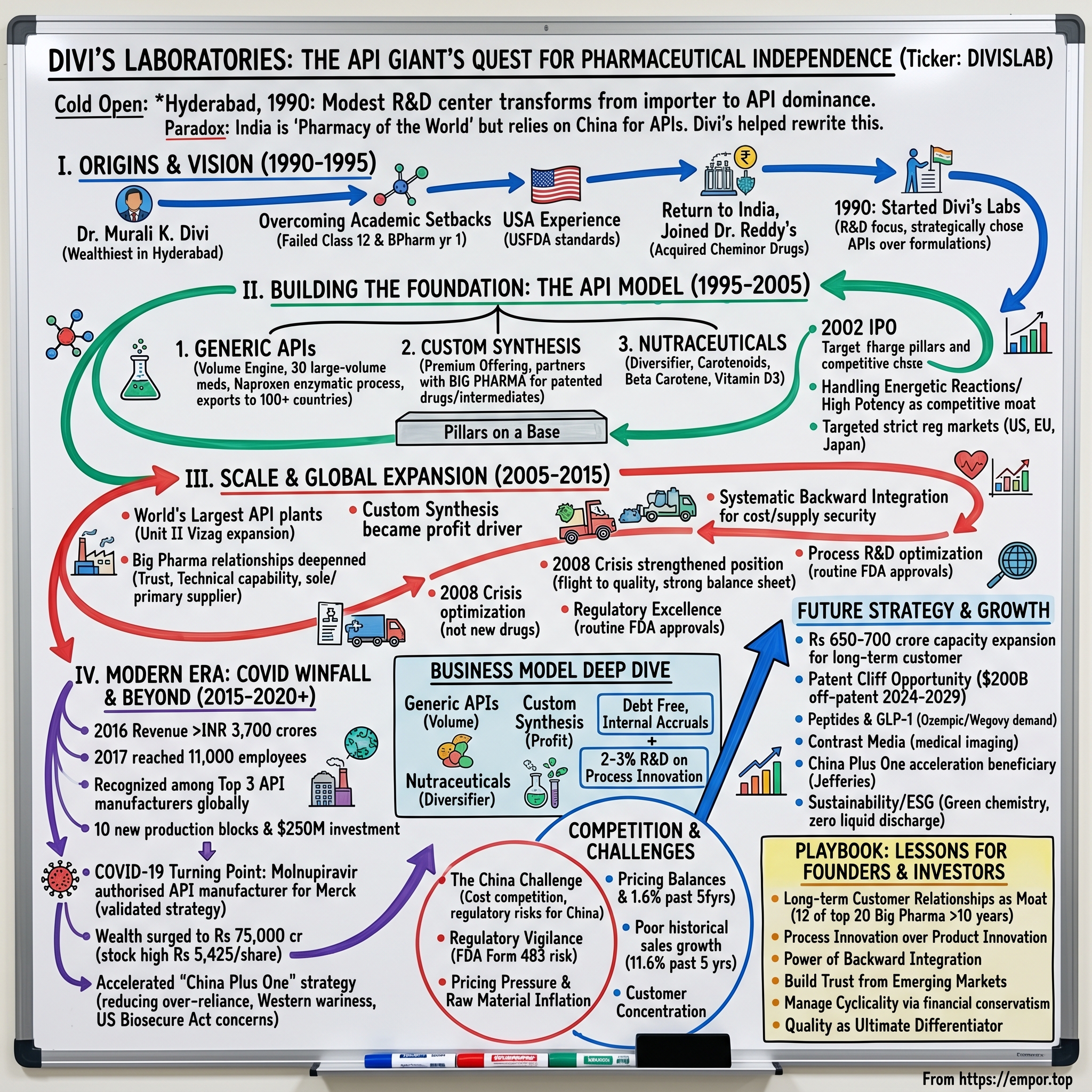

Divi's Laboratories: The API Giant's Quest for Pharmaceutical Independence

I. Introduction & Cold Open

The rain-soaked streets of Hyderabad in 1990 could not have seemed less promising for launching a global pharmaceutical empire. Yet from a modest research center with borrowed capital, one scientist-entrepreneur would build what would become one of the top three API manufacturers in the world. This is the story of Divi's Laboratories—a company that transformed India's role in the global pharmaceutical supply chain, from dependence to dominance, from importer to innovator.

The paradox at the heart of India's pharmaceutical industry has always been striking: while the nation earned the moniker "pharmacy of the world" for its generic drug manufacturing prowess, it remained heavily dependent on China for the critical raw materials—the Active Pharmaceutical Ingredients (APIs) that form the backbone of every medicine. Divi's Laboratories would help rewrite this narrative, building an empire on the foundation of chemistry excellence, relentless backward integration, and relationships with the world's biggest pharmaceutical companies that would span decades.

What makes Divi's story particularly compelling is how it navigated the hidden infrastructure of global pharma—the unglamorous but essential business of making the molecules that save lives. While other Indian pharmaceutical companies chased the spotlight of branded generics and formulations, Divi's founder Dr. Murali K. Divi chose a different path: becoming indispensable to Big Pharma by mastering the art and science of complex chemistry. 12 out of top 20 Big Pharma Companies across US, EU and Japan have been associated with Divi's for 10+ years, a testament to the trust and technical excellence the company has built over three decades.

This episode traces Divi's journey from a small spark in Hyderabad to a $20 billion pharmaceutical powerhouse, exploring how the company built competitive advantages in an industry where margins are thin, competition is fierce, and regulatory scrutiny is unrelenting. We'll examine how Divi's positioned itself to benefit from massive tailwinds—from COVID-19's disruption of global supply chains to the upcoming patent cliff that could unlock $200 billion in generic opportunities over the next five years. And we'll grapple with the fundamental question: in a world increasingly concerned about supply chain resilience and pharmaceutical sovereignty, has Divi's built a model that's not just profitable, but essential?

II. Origins & Dr. Divi's Vision (1990–1995)

The company was founded in 1990 by Dr. Murali K Divi with research and development as its core area. But the story of Divi's Laboratories truly begins with the unlikely journey of its founder—a man who would transform repeated academic failures into pharmaceutical fortune.

Murali Divi was born into a large family in Machilipatnam, Andhra Pradesh, as the youngest of nine sons and four daughters of Divi Satyanarayana, who served as the secretary of a zilla parishad in the Krishna district. Growing up in a modest household, Divi was instilled with values of hard work and perseverance from an early age. His father managed the family on a meager pension, which taught Divi the importance of diligence and resourcefulness.

The path to pharmaceutical prominence was anything but smooth. A young boy who once failed in class 12 and the first year of his BPharm degree went on to become the wealthiest man in Hyderabad. Dr Murali Divi, the founder of Divi's Laboratories, not only failed his class 12 examination but also struggled to pass his first year BPharm exam. Despite experiencing setbacks, he persevered and excelled in his BPharm studies, graduating with distinction. This pattern of overcoming failure would become a defining characteristic of both the man and the company he would build.

After completing his pharmacy education at Manipal, Divi's career took an international turn. After completing his education, Murali Divi embarked on a journey to the United States in 1976. His career began as a pharmacist, and he worked with multiple companies, earning an annual salary of around $65,000. His first job was at Warners Hindustan Company, where he received a salary of Rs 250, a humble start to what would become a remarkable career. Dreaming big, Dr Divi took a risk and decided to move to the US with just USD 7 in his pocket. In those days, that was the maximum amount of foreign exchange permitted for travel abroad.

The American experience proved transformative, not just financially but intellectually. Divi absorbed the rigorous quality standards, regulatory frameworks, and manufacturing excellence that characterized the U.S. pharmaceutical industry. Yet despite his success—or perhaps because of it—the call of home grew stronger. Despite a successful career in the United States, Murali Divi decided to return to India, motivated by a desire to make a difference in the pharmaceutical industry. In 1984, he joined an emerging pharmaceutical company, Dr. Reddy's Laboratories, where he would spend six years honing his skills and gaining invaluable experience.

The collaboration with Dr. Kallam Anji Reddy proved crucial to Divi's entrepreneurial education. Dr Divi established a collaborative venture with him. In the year 1984, the two acquired Cheminor Drugs, an API manufacturer which was struggling at the time. Dr Divi served as the co-promoter and Managing Director and played a pivotal role in steering Cheminor to success. Under his leadership, Cheminor became the first API unit in India to receive USFDA approval for the pain drug Ibuprofen and antacid Ranitidine.

But by 1990, Divi was ready to chart his own course. In 1990, Murali Divi took a bold step and decided to start his own venture, which would later become Divi's Laboratories. The company initially focused on developing commercial processes for the manufacturing of APIs and intermediates, a path that would lead to groundbreaking success. Started initially as a Research and Development Center, it expanded and focused on developing new processes for the production of Active Pharma Ingredients (APIs) & Intermediates, providing complete turnkey solutions and consulting to the domestic pharmaceutical industry.

The strategic decision to focus on APIs rather than finished formulations was both contrarian and brilliant. India's pharmaceutical landscape in the early 1990s was undergoing dramatic transformation. The country had just begun liberalizing its economy in 1991, dismantling the License Raj that had stifled entrepreneurship for decades. Most Indian pharmaceutical companies were rushing into the branded generics space, attracted by higher margins and brand recognition. Divi saw opportunity elsewhere.

Divi's Research Centre changed its name to Divi's Laboratories Limited in 1994 to signal its intent to enter the API and intermediates manufacturing industry. Following this, the company established its first Manufacturing facility in 1995 at Choutuppal, Telangana. The location choice was strategic—close enough to Hyderabad for talent access, but in a less developed area where land was affordable and environmental clearances easier to obtain.

The early consulting model proved crucial for establishing credibility and generating cash flow. Rather than immediately competing with established manufacturers, Divi's initially positioned itself as a knowledge company, developing and licensing improved processes for API production. This approach allowed the company to build relationships with domestic pharmaceutical companies while accumulating capital for its manufacturing ambitions.

In 1994, he made a significant investment to establish a greenfield API plant in Nalgonda. This plant was later renamed Divi's Laboratories. He borrowed Rs 35 crore from IDBI in 1995 and paid it back in nearly five years. The company stopped working capital borrowings in 2010. This financial discipline—borrowing strategically but repaying aggressively—would become a hallmark of Divi's approach to capital management.

The API opportunity that Divi identified was multifaceted. First, APIs represented the highest value-add in the pharmaceutical value chain after drug discovery. Second, the technical barriers to entry were significant, requiring deep chemistry expertise and substantial capital investment. Third, and perhaps most importantly, by focusing on APIs rather than competing in formulations, Divi's could serve the very companies that might otherwise be competitors. It was a strategy of becoming indispensable rather than combative.

III. Building the Foundation: The API Business Model (1995–2005)

The decade from 1995 to 2005 would prove transformative for Divi's Laboratories, as the company evolved from a fledgling manufacturer into a serious player in the global API market. During this period, the three-pillar strategy that would define Divi's business model for decades emerged with remarkable clarity.

The first pillar, Generic APIs, became the company's volume engine. Company manufactures 30 Large Volume Generic APIs in 10's to 100's/1000's of Tons each year and exports them to 100+ countries. The focus on large-volume molecules was deliberate—these were drugs with massive global demand where manufacturing excellence and cost efficiency mattered more than innovation. Products like Naproxen, Gabapentin, and Dextromethorphan became Divi's bread and butter, generating steady cash flows that could fund more ambitious ventures.

What set Divi's apart in the generic API space wasn't just scale but process innovation. Dr. Divi understood that in commoditized markets, the winner isn't necessarily who makes the most, but who makes it most efficiently. The company invested heavily in developing proprietary processes that reduced the number of synthesis steps, improved yields, and minimized waste. For Naproxen, for instance, Divi's developed an enzymatic process that was both more environmentally friendly and cost-effective than traditional chemical synthesis—a breakthrough that made them one of the world's largest producers of this common pain reliever.

The second pillar, Custom Synthesis, represented the company's premium offering. This business involved partnering with Big Pharma companies to manufacture APIs for their patented drugs or to develop complex intermediates for their R&D pipelines. Company under Custom Synthesis of APIs and Intermediates for global companies with a portfolio of products across diverse therapeutic areas. The relationships built through custom synthesis would prove invaluable—not just financially, but strategically. Working with innovator companies gave Divi's early visibility into emerging drug trends, exposed them to cutting-edge chemistry challenges, and most importantly, built trust with the world's most demanding pharmaceutical customers.

The third pillar, Nutraceuticals, emerged somewhat unexpectedly but proved remarkably synergistic. Company's Vishakhapatnam unit produces active ingredient and finished forms of Carotenoids. Products like Beta Carotene, Lutein, and Vitamin D3 leveraged similar manufacturing capabilities but served different markets—food, dietary supplements, and animal feed. This diversification provided a hedge against pharmaceutical market volatility while utilizing excess capacity.

The year 2002 marked a crucial inflection point when Divi's went public on the Indian stock exchanges. The Initial Public Offering, though modest by today's standards, provided crucial growth capital and brought governance discipline that would serve the company well. The public listing also enhanced Divi's credibility with international customers who could now scrutinize the company's financials and governance practices.

By 2005, Divi's Laboratories owner and founder has indeed done a remarkable job in establishing the company as a serious global player, with the company exporting products to over 50 countries by this time. But perhaps more importantly, the foundation was being laid for something bigger—a fully integrated pharmaceutical manufacturing operation that could compete with anyone in the world.

The chemistry advantage that Divi's built during this period cannot be overstated. While competitors often relied on published literature or licensed processes, Divi's invested in fundamental research. The company's scientists didn't just follow recipes; they understood the underlying chemistry well enough to optimize, innovate, and troubleshoot. This deep technical capability became evident in their ability to handle complex chemistries that others avoided—reactions involving cyanides, azides, and other hazardous materials that required specialized expertise and infrastructure.

Quality emerged as another key differentiator during this foundational decade. While many Indian API manufacturers initially focused on less-regulated markets, Divi's from the beginning targeted the most demanding regulatory environments—the United States, Europe, and Japan. This meant investing in quality systems, documentation, and infrastructure that far exceeded Indian regulatory requirements. The first FDA inspection of their facilities wasn't seen as a hurdle but as validation of their approach.

The company's approach to customer relationships during this period also set them apart. Rather than treating API supply as a transactional business, Divi's positioned itself as a partner. They invested in understanding their customers' long-term needs, often developing multiple synthetic routes for the same molecule to provide supply security. They were willing to hold inventory, invest in dedicated capacity, and even co-develop processes with customers—building switching costs that would make these relationships sticky for decades.

Competent in handling high energetic reactions with high potency became more than just a technical capability—it became a competitive moat. Many reactions in pharmaceutical synthesis involve explosive or highly toxic intermediates. Most manufacturers avoid these chemistries due to safety concerns and capital requirements. Divi's made them a specialty, investing in specialized bunkers, safety systems, and training that allowed them to handle reactions others wouldn't touch. This capability opened doors to high-value projects and built a reputation for technical fearlessness.

By 2005, the foundation was complete. Divi's had established itself as a reliable, technically capable, and quality-focused API manufacturer. Revenue had grown from virtually nothing to hundreds of crores. More importantly, the company had proven its model: excellence in chemistry, backward integration for cost advantage, and deep customer relationships could create sustainable competitive advantages even in commoditized markets. The stage was set for explosive growth.

IV. Scale & Global Expansion (2005–2015)

The decade from 2005 to 2015 would see Divi's Laboratories transform from a promising Indian API manufacturer into a global pharmaceutical force. This period of dramatic scaling coincided with significant shifts in the global pharmaceutical landscape—the patent cliff that saw blockbuster drugs worth billions going generic, the financial crisis that forced Big Pharma to restructure supply chains, and growing concerns about API supply concentration in China.

The numbers tell a story of remarkable growth. By 2010, the company was exporting to 100+ countries, doubling its geographic reach in just five years. But geographic expansion was just one dimension of Divi's scaling strategy. The real transformation was happening in Hyderabad and Visakhapatnam, where the company was building what would become the world's largest API manufacturing facilities.

The crown jewel of this expansion was Unit II in Visakhapatnam, which commenced operations in 2002 but saw massive expansion during this period. The Vizag facility wasn't just big—it was sophisticated. With multiple production blocks, each designed for different chemistry types, the facility could handle everything from simple high-volume generics to complex, hazardous custom synthesis projects. The site's proximity to the port also provided logistics advantages for a company that exported the vast majority of its production.

The Big Pharma relationships that would become Divi's most valuable asset deepened significantly during this period. Established relationships with 12 of the top 20 Big Pharma across US, Europe and Japan. These weren't just customer relationships—they were partnerships. Divi's became embedded in their clients' supply chains, often serving as the sole or primary supplier for critical APIs and intermediates.

What made these relationships so durable? First, Divi's reliability. In an industry where a single contamination event or production delay can cost millions, Divi's track record of on-time, in-specification delivery became legendary. Second, technical capability. When Big Pharma companies came with complex chemistry challenges—molecules that required 15 steps of synthesis, or reactions that needed to be run at -70°C—Divi's engineers found solutions. Third, and perhaps most importantly, trust. Divi's had proven they could keep secrets, protect intellectual property, and put customer interests first.

The custom synthesis business, which had been promising in the early 2000s, became a significant profit driver during this period. Unlike generic APIs where margins were constantly under pressure, custom synthesis commanded premium pricing. Divi's wasn't just manufacturing to specifications; they were solving problems, developing new routes, and often improving on the processes their customers had developed. This technical value-add justified margins that were multiples of what generic APIs commanded.

Backward integration, a strategy that would become synonymous with Divi's operational excellence, accelerated during this period. Rather than purchasing key starting materials and intermediates from suppliers, Divi's systematically brought their production in-house. This wasn't just about cost savings, though those were significant. Backward integration provided supply security, quality control, and the ability to optimize the entire production chain. When you control every step from basic chemicals to finished API, you can optimize in ways that non-integrated competitors simply cannot.

The 2008 financial crisis, devastating for many businesses, actually strengthened Divi's position. As Big Pharma companies faced pressure to cut costs, they looked to outsource more API production. But they couldn't afford supply disruptions, so they concentrated orders with the most reliable suppliers. Divi's benefited disproportionately from this flight to quality. Additionally, as credit markets froze, Divi's strong balance sheet and minimal debt became major advantages, allowing them to continue investing while competitors retrenched.

By 2013, Divi's Laboratories was advancing research and development, investing in innovative solutions. The company's R&D wasn't focused on discovering new drugs—that was their customers' domain. Instead, Divi's R&D focused on process innovation: finding better, cheaper, safer ways to make existing molecules. This might seem less glamorous than drug discovery, but it was incredibly valuable. A process improvement that reduces the cost of making a blockbuster drug by 20% can be worth hundreds of millions of dollars.

The regulatory excellence that Divi's demonstrated during this period deserves special mention. By 2015, Manufacturing facilities were inspected and approved by various international health authorities. FDA inspections, which were the nightmare of many Indian pharmaceutical companies, became routine for Divi's. The company didn't just pass inspections; they often received commendations for their quality systems. This regulatory track record became a powerful differentiator, especially as regulators began scrutinizing pharmaceutical supply chains more closely.

The nutraceutical business, which had started as an opportunistic diversification, evolved into a strategic asset during this period. The same carotenoids that went into dietary supplements could also be used in pharmaceutical formulations. The technical capabilities developed for nutraceutical production—particularly in handling light-sensitive, oxygen-sensitive compounds—proved valuable for pharmaceutical projects. Moreover, the nutraceutical business provided a natural hedge, with demand patterns often counter-cyclical to pharmaceuticals.

V. The Modern Era: COVID Windfall & Beyond (2015–2020)

The period from 2015 to 2020 would prove to be transformative for Divi's Laboratories, culminating in the extraordinary circumstances of the COVID-19 pandemic that would validate the company's strategic positioning in ways no one could have anticipated. This era began with steady growth and operational excellence but ended with Divi's at the center of the global pharmaceutical response to the worst pandemic in a century.

In 2016, Divi's Pharma's revenue exceeded sales revenue of INR 3,700 crores with a 22% growth rate. This robust growth wasn't just about volume—it reflected the company's successful mix shift toward higher-margin custom synthesis products and complex generic APIs. The company was no longer competing purely on cost; it was winning on capability.

The human capital story during this period is remarkable. In 2017, Divi's Labs reached a milestone of 11,000 employees. It became one of the largest employers in Telangana and Andhra Pradesh. But these weren't just numbers—Divi's had built one of the most skilled pharmaceutical workforces in India. The company's training programs, often conducted in collaboration with local universities, created a pipeline of chemists and chemical engineers specifically skilled in the complex chemistries Divi's specialized in.

A pivotal moment in Divi's evolution came with their achievement of global recognition. They also joined the elite ranks of the top 3 API manufacturers globally. This wasn't just a vanity metric—it represented real market power. Being in the top three meant Divi's had the scale to influence pricing, the resources to invest in new technologies, and the credibility to win the largest contracts.

The infrastructure investments during this period were staggering. By 2018, Divi had commissioned 10 new production blocks. In 2019, the company made an additional investment of $250 million to expand production blocks in Unit I and Unit II. These weren't just capacity additions—each production block was designed for specific chemistry types, with specialized equipment for handling everything from cryogenic reactions to high-pressure hydrogenations.

Then came COVID-19, and with it, an opportunity that would propel Divi's into the global spotlight. The development of Molnupiravir, Merck's oral antiviral for COVID-19, became a defining moment for the company. On 26 May 2021, Divi's Laboratories had informed that it has been selected by Merck as an authorized manufacturer for the active pharmaceutical ingredient. Divi's Laboratories announced in May that it had been authorised to manufacture the Covid-19 drug's API and supply it to Merck's partners in India.

The Molnupiravir opportunity wasn't just about one contract—it validated Divi's entire strategy. Here was one of the world's largest pharmaceutical companies, facing the most important drug launch in decades, choosing Divi's as a critical supplier. The trust implicit in that decision—given the stakes involved—spoke volumes about Divi's capabilities and reputation.

The financial impact was immediate and dramatic. During the COVID-19 pandemic, his wealth surged to approximately Rs 75,000 crore in October 2021. During this time, the company's stocks reached an all-time high of Rs 5,425 per share. This surge was driven by the rising demand for the antiviral drug Molnupiravir. The stock price appreciation reflected investor recognition that Divi's wasn't just benefiting from a one-time windfall—the pandemic had accelerated trends that would benefit the company for years.

The pandemic also accelerated the "China Plus One" strategy that global pharmaceutical companies had been contemplating for years. COVID-19 exposed the risks of supply chain concentration, with drug shortages making headlines as Chinese factories shut down. Governments worldwide began discussing pharmaceutical supply chain resilience as a national security issue. Divi's, with its proven track record, massive capacity, and location in democratic India, was perfectly positioned to benefit from this shift.

Merck announced supply agreement with US government for experimental Covid-19 drug, molnupiravir. US government has committed to purchase approximately 1.7 million courses of molnupiravir upon issuance of emergency use authorization or approval by the U.S. Food and Drug Administration. The scale of these contracts—worth hundreds of millions of dollars—demonstrated the critical role Divi's played in the global pharmaceutical supply chain.

But COVID-19 also brought challenges. The company had to maintain operations while protecting employee health, manage supply chains disrupted by lockdowns, and meet surging demand for certain products while others saw demand collapse. Divi's response—maintaining near-normal operations throughout the pandemic while keeping employees safe—became a case study in operational excellence.

The regulatory scrutiny that came with COVID-19 prominence was intense. With the world watching, any quality issue could have been catastrophic. Divi's passed this test with flying colors, maintaining their spotless regulatory record even while rapidly scaling production of COVID-related APIs. This performance under pressure further cemented their reputation with both regulators and customers.

VI. Business Model Deep Dive

Understanding Divi's Laboratories requires diving deep into the three revenue streams that form the backbone of their business model. Each stream has distinct economics, competitive dynamics, and strategic importance—together, they create a remarkably resilient business that can weather industry cycles while capturing upside from multiple growth drivers.

Generic APIs: The Volume Foundation

Company manufactures 30 Large Volume Generic APIs in 10's to 100's/1000's of Tons each year. The generic API business is Divi's volume engine, but calling it commoditized would be oversimplifying. World's largest manufacturer in more than 10 Generic APIs, Top 2 in 18 out of 30 molecules. This dominant market position didn't happen by accident—it's the result of three decades of process optimization, backward integration, and relentless focus on cost efficiency.

Take Naproxen, one of Divi's flagship products. While the molecule itself is decades old and manufactured by dozens of companies worldwide, Divi's has achieved a cost position that few can match. Through backward integration to basic chemicals, process innovations that reduce solvent usage, and massive scale that spreads fixed costs, Divi's can profitably sell Naproxen at prices that would bankrupt smaller competitors. This isn't a race to the bottom—it's strategic cost leadership.

The generic API portfolio is carefully curated. Divi's doesn't chase every generic opportunity; they focus on molecules where they can achieve top-three global market share. This concentration strategy creates a virtuous cycle: scale leads to lower costs, which leads to market share gains, which leads to more scale. In molecules like Gabapentin, Dextromethorphan, and Diltiazem, Divi's has become so dominant that many customers have stopped looking for alternative suppliers—the switching costs and risks simply aren't worth the minimal potential savings.

Custom Synthesis: The Profit Engine

Company under Custom Synthesis of APIs and Intermediates for global companies with a portfolio of products across diverse therapeutic areas. 12 out of top 20 Big Pharma Companies across US, EU and Japan have been associated with Divi's for 10+ years. If generic APIs are about volume, custom synthesis is about value. This business involves partnering with innovator pharmaceutical companies to manufacture APIs for their patented drugs or complex intermediates for their development pipelines.

The economics of custom synthesis are fundamentally different from generic APIs. Contracts are typically long-term (5-10 years), with prices that reflect the technical complexity and customer-specific investments required. Margins can be 2-3 times higher than generic APIs, and customer relationships are incredibly sticky. When you're the only qualified supplier for a patented drug generating billions in revenue, your customer cannot easily switch suppliers even if they wanted to.

Competent in handling high energetic reactions with high potency. This technical capability is crucial for custom synthesis success. Many innovative drugs require complex chemistries—reactions that must be run at extreme temperatures, with hazardous reagents, or under precisely controlled conditions. Divi's has invested hundreds of millions in specialized equipment and training to handle these challenges. Cryogenic reactors that can maintain -80°C, high-pressure autoclaves for hydrogenation reactions, and contained facilities for handling compounds active at microgram levels—these aren't just equipment, they're competitive moats.

The custom synthesis business also provides strategic benefits beyond financial returns. Working with innovator companies gives Divi's early visibility into drug development trends. They see which therapeutic areas are attracting investment, which chemistry platforms are emerging, and what manufacturing challenges the industry is grappling with. This intelligence informs everything from capacity planning to R&D investments.

Nutraceuticals: The Diversifier

Beta Carotene, Lutein, Astaxanthin, Lycopene, Vitamin D3 and Vitamin A. The nutraceutical business might seem like an odd fit for a company focused on pharmaceutical APIs, but it's actually highly synergistic. Many nutraceutical ingredients require similar manufacturing capabilities to pharmaceutical APIs—complex organic synthesis, purification technologies, and strict quality control.

The nutraceutical business serves multiple strategic purposes. First, it provides diversification—nutraceutical demand is driven by consumer wellness trends rather than pharmaceutical development cycles. Second, it utilizes capacity that might otherwise be idle, improving asset utilization. Third, and perhaps most importantly, capabilities developed for nutraceuticals often prove valuable for pharmaceutical projects. The expertise in handling light-sensitive carotenoids, for instance, is directly applicable to certain pharmaceutical compounds.

Working Capital and Cash Conversion

One of the most impressive aspects of Divi's business model is its working capital management. Despite being in a business that requires holding significant inventory (raw materials, work-in-process, and finished goods), Divi's has consistently maintained industry-leading cash conversion cycles. This is achieved through a combination of operational excellence (reducing production cycle times), strategic inventory management (holding the right products in the right quantities), and favorable payment terms with customers (many Big Pharma customers pay promptly given their dependence on Divi's supply).

Company is almost debt free. This isn't just conservative financial management—it's a strategic advantage. In an industry where capacity additions require hundreds of millions in capital investment, being able to fund growth from internal accruals means Divi's can move faster than leveraged competitors. It also means they can weather downturns without the pressure of debt service, allowing them to maintain R&D spending and even make countercyclical investments when competitors are retrenching.

R&D Philosophy

Divi's R&D investment philosophy deserves special attention. Unlike innovator pharmaceutical companies that spend 15-20% of revenue on R&D trying to discover new drugs, Divi's spends approximately 2-3% of revenue on R&D focused entirely on process innovation. This might seem modest, but it's incredibly efficient. Every rupee spent on process R&D can generate returns across multiple products and customers. A new synthetic route that reduces costs by 10% for a high-volume generic API can generate millions in additional profit. A process innovation that enables manufacture of a complex custom synthesis project can lock in a customer relationship worth hundreds of millions over a decade.

VII. Competition, Challenges & Market Dynamics

Divi's Laboratories is India's fourth largest publicly listed pharmaceutical company by market capitalization. Yet despite this prominent position, the company faces intense competition from multiple angles—Chinese manufacturers on cost, Western CDMOs on capability, and emerging Indian players on ambition. Understanding these competitive dynamics is crucial to evaluating Divi's future prospects.

The China Challenge

Chinese API manufacturers remain formidable competitors, particularly in generic APIs. Companies like Zhejiang Huahai, Hebei Jiheng, and Shandong Xinhua have advantages in raw material access, energy costs, and government support that allow them to offer aggressive pricing. For many simple, high-volume APIs, Chinese manufacturers can undercut Indian producers by 20-30%.

Divi's response to Chinese competition has been strategic rather than reactive. Instead of trying to match Chinese prices, they've focused on reliability, quality, and regulatory compliance. The series of FDA warning letters and import bans that hit Chinese manufacturers between 2018-2020 validated this approach. When customers factor in the total cost of ownership—including supply risk, regulatory risk, and quality issues—Divi's premium pricing becomes justifiable.

The geopolitical tensions between China and the West, accelerated by COVID-19, have created a structural shift that benefits Divi's. The proposed U.S. Biosecure Act, which would restrict federal funding for companies working with certain Chinese biotechnology companies, exemplifies growing Western wariness about pharmaceutical supply chain dependence on China. As international drugmakers increasingly seek to diversify away from China, Indian firms report a surge in interest, investment, and strategic partnerships. The "China plus one" strategy, a move by companies to reduce over-reliance on Chinese manufacturing, isn't new, but recent events have injected a palpable "sense of urgency". Concerns around the proposed US Biosecure Act, lingering trade tensions, and the spectre of potential US tariffs are compelling global pharma executives to actively court alternatives.

Regulatory Challenges

The pharmaceutical industry is one of the most heavily regulated in the world, and regulatory compliance remains a constant challenge. A single FDA Form 483 (inspection observation) can damage customer confidence, while a Warning Letter can shut down exports to the U.S. market entirely. Indian pharmaceutical companies have learned this lesson painfully, with several major players facing import bans that destroyed billions in market value.

Divi's has maintained an exceptional regulatory track record, but this requires constant vigilance and investment. The company employs hundreds of quality assurance professionals, conducts regular mock audits, and invests continuously in upgrading facilities to meet evolving regulatory standards. The cost of this compliance infrastructure is substantial—but the cost of a regulatory failure would be catastrophic.

Pricing Pressure and Margin Compression

Higher raw material costs, regulatory challenges constraining margins. The generic API business faces structural pricing pressure as more manufacturers enter the market and customers become increasingly sophisticated in their procurement. Even in custom synthesis, where Divi's has stronger pricing power, Big Pharma customers are using competitive bidding and dual sourcing strategies to negotiate better terms.

Raw material cost inflation has been a particular challenge. Many of the basic chemicals and solvents used in API manufacturing are petroleum derivatives, making Divi's exposed to oil price volatility. The company's backward integration strategy provides some insulation, but they still face pressure when input costs rise faster than they can pass through price increases.

Growth Challenges

The company has delivered a poor sales growth of 11.6% over past five years. This relatively modest growth rate, especially compared to Divi's historical performance, reflects several challenges. The generic API market has become increasingly competitive, with new entrants from China and India driving price erosion. The custom synthesis business, while higher margin, is lumpy—dependent on winning large contracts and customer product lifecycle dynamics.

The patent cliff opportunity ahead could reignite growth, but capitalizing on it won't be automatic. As drugs worth billions go off patent in the coming years, generic manufacturers worldwide will rush to capture share. Divi's will need to execute flawlessly—selecting the right molecules, scaling production efficiently, and managing the inevitable pricing pressure as competition intensifies.

Customer Concentration Risk

While Divi's relationships with Big Pharma are a strategic asset, they also create concentration risk. If a major customer decides to insource production, switch to a competitor, or if their drug fails in the market, Divi's could see significant revenue impact. The Molnupiravir experience, while positive, also illustrates this risk—the surge in COVID-related revenue in 2021 created a difficult comparison base for subsequent years.

VIII. Financial Performance & Valuation

The financial story of Divi's Laboratories is one of consistent execution punctuated by periods of exceptional performance. The current market capitalization of Divi's Laboratories is $20.5B. The trailing twelve month revenue for Divi's Laboratories is $1.1B. These headline numbers reflect a company that has created enormous value, but the details reveal both strengths and areas of concern.

Recent Financial Performance

The third quarter of fiscal year 2025 showcased Divi's at its operational best. Active pharmaceutical ingredients manufacturer Divi's Laboratories posted a 64.52% increase in its consolidated profit after tax (PAT) to ₹589 crore in the quarter ended December 2024. In the year ago period, the net profit was ₹358 crore. Revenue from operations surged 25% to ₹2,319 crore in the third quarter of the financial year 2024-25, compared to ₹1,855 crore a year back.

EBITDA (Earnings before interest, taxes, depreciation and amortisation) rose 52% to ₹743 crore in the latest October-December quarter as compared to ₹489 crore in Q3 FY24. The EBITDA margin was at 32% vs 26.4% in the same period the previous year. This margin expansion is particularly impressive given the industry-wide pressure from raw material inflation and competitive intensity.

Looking at the nine-month performance provides additional context. In 9M FY25, "The company earned a consolidated total income of ₹7,041 crore as against a consolidated total income of ₹5,804 crore during the corresponding nine months period of the previous year. PBT for the current nine months period accounted to ₹2,052 crore as against ₹1,450 crore for the corresponding nine months period of the previous year," Divi's Lab said.

Margin Evolution

The evolution of Divi's margins tells a story of operational improvement and mix shift. EBITDA margins have expanded from the mid-20s five years ago to over 30% in recent quarters. This improvement reflects several factors: increasing contribution from higher-margin custom synthesis, benefits from backward integration, and operational leverage from capacity utilization improvements.

However, margin expansion hasn't been linear. The company faced margin pressure in 2022-2023 as raw material costs spiked and competition in certain generic APIs intensified. The recent margin recovery demonstrates both the resilience of the business model and management's ability to navigate challenges.

Capital Allocation and Investment

Divi's capital allocation strategy balances growth investment with shareholder returns. Company has been maintaining a healthy dividend payout of 43.2%. This consistent dividend policy reflects confidence in cash generation while retaining sufficient capital for growth investments.

The Kakinada facility represents the largest capital commitment in the company's history. Divis Laboratories has commenced commercial operations from a part of the Phase I of Unit III greenfield project at Ontimamidi Village (Kona), Thondangi Mandal, Kakinada, Andhra Pradesh from 01 January 2025. The phase I of the Unit III greenfield project of the Company at Kakinada, Andhra Pradesh is being implemented on 200 acres of 500 acres Unit III site, with an estimated investment between Rs 1,200 crore to Rs 1,500 crore.

The company's Kakinada Project (Unit-III) also commenced commercial operations from January 1, 2025. "We have capitalised assets of ₹433 crore for the quarter and of ₹557 crore for the 9-month period of the current year. Of this, capitalisation for Kakinada Project is ₹418 crore during the 9-month period," the firm said. This massive investment, funded entirely from internal accruals, demonstrates both financial strength and confidence in future demand.

Return Metrics

Return on Equity (ROE) and Return on Capital Employed (ROCE) are critical metrics for evaluating Divi's capital efficiency. The company has consistently generated ROE in the 20-25% range and ROCE above 25%, placing it among the best performers in the global pharmaceutical industry. These returns are particularly impressive given the capital-intensive nature of API manufacturing and the company's conservative balance sheet.

The debt-free status deserves emphasis. Company is almost debt free. In an industry where many competitors carry debt equal to 2-3x EBITDA, Divi's zero-debt position provides strategic flexibility. They can make countercyclical investments during downturns, pursue acquisitions if attractive opportunities arise, and weather industry cycles without financial distress.

Valuation Considerations

At current levels, Divi's trades at a significant premium to both Indian and global pharmaceutical peers. The P/E multiple of approximately 70x and EV/EBITDA of around 35x reflect high market expectations. Bulls argue this premium is justified by the company's superior returns, growth prospects from the patent cliff, and strategic positioning as a China+1 beneficiary. Bears point to slowing historical growth and increasing competition as reasons for caution.

IX. Future Strategy & Growth Vectors

The next five years represent a period of unprecedented opportunity for Divi's Laboratories, with multiple growth vectors converging to create potential for substantial value creation. The company's strategic positioning at the intersection of several powerful trends—patent expiries, supply chain diversification, and emerging therapeutic areas—could drive a new phase of growth.

Capacity Expansion and Customer Agreements

Divi's Laboratories revealed plans to invest between Rs.650 crore and Rs.700 crore to expand its manufacturing capacity. This investment will be used to meet the increasing demand from a long-term customer agreement, with the expansion expected to be operational by January 2027. This targeted expansion, tied to specific customer commitments, exemplifies Divi's disciplined approach to capital allocation. Rather than building capacity speculatively, they're expanding in response to contracted demand.

Divi's Laboratories recently signed a long-term manufacturing and supply agreement with an unnamed global pharma major for advanced intermediates. Supporting this, Divi's announced plans to invest Rs 650-700 crore ($78-84 million) in capacity expansion, funded internally, aiming to secure supply for its customers and expand its own custom synthesis footprint. The identity of this customer, while undisclosed, is likely one of the major pharmaceutical companies preparing for significant patent expiries or launching new products requiring complex intermediates.

The Patent Cliff Opportunity

The pharmaceutical industry is approaching one of the largest patent cliffs in history, with drugs worth over $200 billion in annual sales expected to lose patent protection between 2024 and 2029. This includes blockbusters in therapeutic areas where Divi's has strong capabilities—cardiovascular, central nervous system, and diabetes medications. Each patent expiry represents an opportunity for generic API manufacturers, but success requires preparation years in advance.

Divi's is well-positioned to capitalize on this opportunity. Their process development capabilities allow them to develop cost-effective manufacturing routes for complex molecules. Their regulatory track record ensures quick approval times. Their manufacturing scale enables them to meet the massive demand that emerges when a blockbuster goes generic. And their financial strength allows them to invest in inventory and capacity ahead of generic launch.

Peptides and GLP-1 Opportunity

The explosive growth of GLP-1 agonists for diabetes and weight loss represents one of the most significant opportunities in pharmaceutical history. Drugs like Ozempic and Wegovy are already generating tens of billions in revenue, with demand far exceeding supply. As these markets mature and new entrants emerge, the need for high-quality peptide manufacturing capacity will be enormous.

Co working on glucose stabilising hormone GLP-1 manufacturing process to diversify. While peptide synthesis is different from small molecule API manufacturing, requiring specialized equipment and expertise, Divi's has the technical capabilities and financial resources to enter this space successfully. The company's track record of mastering complex chemistries suggests they can develop the necessary capabilities for peptide manufacturing.

Contrast Media Expansion

Contrast media, used in medical imaging procedures, represents another strategic growth area. These products require specialized manufacturing capabilities, particularly in iodination chemistry, which Divi's has developed over years of making other iodinated compounds. The global contrast media market is growing steadily, driven by aging populations and increasing diagnostic imaging usage. Moreover, supply has been constrained by quality issues at some manufacturers, creating opportunities for reliable suppliers like Divi's.

China Plus One Acceleration

Jefferies ("hold") says Divi's will be a key beneficiary of diversification out of China. The structural shift away from Chinese pharmaceutical supply chains is accelerating, driven by geopolitical tensions, quality concerns, and supply chain resilience considerations. This isn't just about moving existing business from China to India—it's about Western pharmaceutical companies fundamentally restructuring their supply chains to reduce concentration risk.

Divi's is ideally positioned to benefit from this trend. They have the scale to absorb large contracts, the quality systems to meet Western regulatory standards, and the track record to give customers confidence. Moreover, their location in democratic India, with its strong intellectual property protection and stable regulatory environment, provides comfort to Western pharmaceutical companies concerned about geopolitical risk.

Sustainability and ESG Initiatives

Environmental, Social, and Governance (ESG) considerations are becoming increasingly important in pharmaceutical supply chain decisions. Divi's has invested heavily in green chemistry processes, waste reduction, and renewable energy. Their enzymatic processes for certain APIs reduce environmental impact while lowering costs. Their zero liquid discharge facilities minimize water pollution. These investments position Divi's well as customers increasingly factor sustainability into supplier selection.

X. Playbook: Lessons for Founders & Investors

The Divi's Laboratories story offers powerful lessons for entrepreneurs and investors navigating complex, regulated industries. These insights, distilled from three decades of building a global pharmaceutical powerhouse, provide a playbook for creating sustainable competitive advantages in seemingly commoditized markets.

Long-term Customer Relationships as Moat

12 out of top 20 Big Pharma Companies across US, EU and Japan have been associated with Divi's for 10+ years. This isn't just a statistic—it's the foundation of Divi's business model. In an industry where switching suppliers can require regulatory requalification, technology transfer, and supply chain risk, customer relationships become incredibly sticky. Divi's didn't just win these customers; they invested in understanding their needs, solving their problems, and becoming indispensable to their operations.

The lesson for founders: In B2B businesses, especially those with high switching costs, customer retention is more valuable than customer acquisition. Invest disproportionately in serving existing customers excellently rather than constantly chasing new ones. The lifetime value of a Big Pharma customer relationship can be measured in billions of dollars.

Process Innovation vs. Product Innovation

While the pharmaceutical industry obsesses over drug discovery and product innovation, Divi's built a $20 billion company through process innovation. They don't discover new drugs; they find better ways to make existing ones. This focus on process has several advantages: lower risk (the molecule is already proven), faster returns (no lengthy clinical trials), and cumulative learning (each process improvement builds on previous knowledge).

The insight for entrepreneurs: Not every successful company needs to be on the bleeding edge of product innovation. Sometimes, doing known things better—more efficiently, more reliably, more sustainably—can be just as valuable. Process innovation is often less glamorous but can create more sustainable competitive advantages.

The Power of Backward Integration

Divi's systematic backward integration—manufacturing their own raw materials and intermediates—created multiple competitive advantages. Cost reduction is obvious, but the strategic benefits are more important: supply security, quality control, and the ability to optimize the entire value chain. When you control every step from basic chemicals to finished API, you can make trade-offs and optimizations that non-integrated competitors cannot.

For founders building in complex supply chains: Consider vertical integration not just as a cost play but as a strategic moat. Controlling critical inputs or processes can create competitive advantages that are difficult for others to replicate.

Building Trust from Emerging Markets

As an Indian company selling to Western pharmaceutical giants, Divi's faced inherent skepticism. They overcame this through relentless focus on quality, regulatory compliance, and reliability. They didn't try to be the cheapest; they aimed to be the most trustworthy. This strategy required patience—building credibility takes years—but created a sustainable competitive position.

The lesson for emerging market entrepreneurs: When selling to developed market customers, trust is your most valuable currency. Invest in quality systems, regulatory compliance, and track record building even if it means slower initial growth. Once established, trust becomes a powerful competitive moat.

Managing Cyclicality

The pharmaceutical industry is cyclical, with patent expiries, regulatory changes, and demand shifts creating volatility. Divi's managed this through diversification (three business segments with different cycle dynamics), financial conservatism (no debt provides flexibility during downturns), and countercyclical investment (expanding capacity when competitors retreat).

For investors and founders in cyclical industries: Build your business model to survive the troughs and capitalize on the peaks. This means conservative financial management, diversified revenue streams, and the patience to make long-term investments when others are focused on short-term survival.

Quality as Ultimate Differentiator

In an industry where a single contamination event can cause patient deaths and destroy company value, quality isn't just important—it's existential. Divi's investment in quality systems, training, and culture created a track record that became their calling card. When FDA inspections that terrified competitors became routine for Divi's, they had achieved true differentiation.

The broader lesson: In industries where failure has catastrophic consequences, excellence in execution becomes the ultimate competitive advantage. Customers will pay premium prices for the confidence that comes from a spotless track record.

XI. Bear vs. Bull Case

As we evaluate Divi's Laboratories' future prospects, the investment community remains divided between those who see continued dominance and those who worry about mounting challenges. Both perspectives deserve careful consideration.

Bull Case: The Optimistic View

The patent cliff opportunity alone could transform Divi's growth trajectory. With over $200 billion worth of drugs losing patent protection over the next five years, the generic API opportunity is massive. Divi's is one of the few companies with the scale, regulatory track record, and technical capabilities to capture a meaningful share of this opportunity. Even capturing 1-2% of this market would double their current revenue.

The China Plus One theme is not a temporary phenomenon but a structural shift. A mix of geopolitical friction, supply chain vulnerabilities, and the threat of new trade tariffs is accelerating the shift, presenting a golden opportunity for India's Contract Development and Manufacturing Organisations (CDMOs). As international drugmakers increasingly seek to diversify away from China, Indian firms report a surge in interest, investment, and strategic partnerships. Divi's, as one of the largest and most capable Indian CDMOs, is a natural beneficiary.

The custom synthesis business appears poised for revival. After several years of relatively slow growth, the pipeline of new projects looks promising. Big Pharma companies are increasingly outsourcing not just manufacturing but also process development for complex molecules. Divi's technical capabilities in handling hazardous chemistries and complex syntheses position them well for these high-value projects.

The regulatory track record remains spotless. In an industry where competitors regularly face FDA warning letters and import bans, Divi's consistent compliance is a powerful differentiator. This track record becomes even more valuable as regulators increase scrutiny of pharmaceutical supply chains.

The debt-free balance sheet provides enormous strategic flexibility. Company is almost debt free. In an environment of rising interest rates and economic uncertainty, having no financial leverage is a significant advantage. Divi's can invest countercyclically, pursue acquisitions if attractive opportunities arise, and weather any downturn without financial distress.

Bear Case: The Skeptical View

Margin pressure from competition is real and intensifying. Chinese competitors are becoming more sophisticated, Indian peers are expanding capacity, and Western CDMOs are moving into generic APIs. The golden age of 30%+ EBITDA margins may be behind us. Jefferies sees some near-term earnings pain due to competition as drugmakers' patents expire.

Customer concentration risk remains concerning. While relationships with Big Pharma are sticky, they also create vulnerability. If a major customer decides to insource production or if their key drug fails, Divi's could see significant revenue impact. The pharmaceutical industry's consolidation trend could also affect customer relationships.

The company has delivered a poor sales growth of 11.6% over past five years. This historical growth rate, while respectable, is far below what investors expect from a company trading at premium valuations. If Divi's cannot accelerate growth, multiple compression seems inevitable.

Capital intensity of expansion is increasing. The Kakinada facility requires over Rs 1,500 crore investment. As environmental and safety regulations become stricter, the cost of new capacity continues to rise. This could pressure returns on invested capital even if revenue growth accelerates.

Regulatory risk, while well-managed historically, remains ever-present. A single FDA warning letter could damage customer confidence and shut down U.S. exports. As Divi's becomes larger and more visible, regulatory scrutiny will only intensify. The company's spotless record makes them a target for competitors and regulators looking to make examples.

The valuation leaves little room for error. At current multiples, Divi's is priced for perfection. Any disappointment in growth, margins, or execution could lead to significant multiple compression. The stock's volatility during earnings seasons demonstrates how sensitive the market is to any deviation from expectations.

XII. Epilogue & Reflection

As we conclude this deep dive into Divi's Laboratories, it's worth stepping back to appreciate the broader significance of this remarkable company. In an era of software unicorns and digital disruption, Divi's represents something different—a testament to the enduring value of manufacturing excellence, technical expertise, and patient capital allocation.

Divi's Place in India's Pharmaceutical Story

Divi's Laboratories embodies the evolution of India's pharmaceutical industry from a copycat generic manufacturer to a global innovation partner. When Dr. Murali Divi started the company in 1990, India was known for reverse-engineering patented drugs and selling cheap copies in unregulated markets. Today, companies like Divi's are trusted partners to the world's most sophisticated pharmaceutical companies, handling their most complex chemistry challenges and ensuring supply of life-saving medications to billions of people.

The company's success challenges simplistic narratives about emerging market companies. Divi's didn't succeed by being cheap; they succeeded by being excellent. They didn't copy Western business models; they created their own, suited to their capabilities and market position. They didn't seek quick exits or financial engineering; they built for the long term with patient capital and operational excellence.

The Hidden Infrastructure of Global Healthcare

One of the most striking aspects of researching Divi's is realizing how invisible yet essential companies like this are to global healthcare. When patients take medications for blood pressure, depression, or pain, they don't think about where the active ingredients come from. Yet without companies like Divi's, operating massive chemical plants with precision and reliability, modern medicine would be impossible.

This hidden infrastructure is becoming increasingly visible and strategic. COVID-19 exposed the fragility of pharmaceutical supply chains. Geopolitical tensions are making countries reconsider their dependence on single sources. Climate change is forcing reconsideration of where and how we manufacture essential goods. In this context, Divi's isn't just a successful company—it's a critical node in global health security.

What the API Business Tells Us About Globalization

The Divi's story is also a globalization story, but not the simple narrative of offshore manufacturing for cost reduction. It's about the emergence of specialized capabilities in unexpected places, the importance of trust in global supply chains, and the complex interplay between competition and cooperation in interconnected industries.

As of 31-Mar-2025, Divi's Laboratories has a trailing 12-month revenue of $1.1B. That a company founded in Hyderabad, with manufacturing in Andhra Pradesh and Telangana, generates over a billion dollars serving customers in America, Europe, and Japan, tells us something profound about how global commerce has evolved. Excellence can emerge anywhere; trust can be built across vast cultural and geographic distances; and competitive advantage can be sustained even in seemingly commoditized industries.

Biggest Surprises from the Research

Several aspects of Divi's story surprised us during this research. First, the founder's journey from academic failure to pharmaceutical fortune—A young boy who once failed in class 12 and the first year of his BPharm degree went on to become the wealthiest man in Hyderabad—reminds us that early setbacks don't determine ultimate outcomes.

Second, the power of process innovation in creating value. While the world celebrates product innovation and breakthrough discoveries, Divi's built enormous value by finding better ways to make existing molecules. This suggests that there's still tremendous opportunity in optimizing and improving established products and processes.

Third, the importance of trust and relationships in B2B businesses. 12 out of top 20 Big Pharma Companies across US, EU and Japan have been associated with Divi's for 10+ years. In an era of disruption and rapid change, these decade-long relationships seem anachronistic. Yet they're the foundation of Divi's business model, suggesting that in certain industries, stability and reliability create more value than disruption.

Why This Matters for the Future of Pharma

Looking forward, the Divi's model—technical excellence, manufacturing sophistication, and long-term relationships—seems increasingly relevant rather than outdated. As pharmaceutical innovation becomes more complex, with biologics, cell therapies, and personalized medicine, the need for sophisticated manufacturing partners will only grow. As supply chain resilience becomes a strategic imperative, companies with proven track records and diversified capabilities become more valuable. As sustainability concerns mount, manufacturers who can produce efficiently with minimal environmental impact will have advantages.

The challenges facing Divi's are real—competition is intensifying, growth is slowing, and valuations are stretched. But the fundamental drivers of their business—patent expiries creating generic opportunities, Western companies diversifying from China, and increasing outsourcing of complex manufacturing—remain intact. Whether Divi's can navigate these challenges while capitalizing on opportunities will determine whether the next chapter of their story is as remarkable as the first three decades.

In the end, Divi's Laboratories represents something important beyond financial returns or business strategy. It's a reminder that value creation doesn't always come from disruption or innovation in the traditional sense. Sometimes, it comes from doing essential things extraordinarily well, from building trust over decades, and from the patient accumulation of capabilities that become increasingly valuable over time. In a world obsessed with the new and disruptive, there's something profound about a company that creates enormous value by mastering the established and essential.

The story of Divi's Laboratories is far from over. With the Kakinada facility coming online, patent expiries accelerating, and global supply chains restructuring, the next chapter could be even more dramatic than the journey so far. Whether Divi's can maintain its culture of excellence while scaling to meet these opportunities, whether it can navigate increasing competition while maintaining margins, and whether it can continue innovating in process while others innovate in products—these questions will determine whether Divi's Laboratories remains a hidden champion or emerges as a true global pharmaceutical leader.

For founders, investors, and students of business, Divi's offers lessons that transcend industry boundaries: the power of focus, the value of operational excellence, the importance of patient capital, and the potential to build world-class companies from unexpected places. As we face a future where supply chain resilience, manufacturing capability, and technical excellence become increasingly strategic, the Divi's model doesn't look outdated—it looks prescient.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube