Jaiprakash Power Ventures: The Infrastructure Empire's Power Play

I. Introduction & Episode Roadmap

Picture this: It's 2024, and in a sprawling courtroom in New Delhi, creditors are circling around the carcass of what was once India's infrastructure crown jewel. Jaiprakash Associates Limited—builder of dams, highways, and cities—lies prostrate under a crushing ₹57,000 crore debt burden. Yet curiously, one of its offspring still breathes. Jaiprakash Power Ventures, the power generation arm that should have been dragged down with the parent, trades on the National Stock Exchange with a market cap north of ₹12,000 crore.

This is a story about survival against impossible odds. About how a company can watch its parent empire crumble while somehow keeping its own lights on—literally, in this case, as JPPOWER continues operating 2,220 MW of power generation capacity across India. It's a tale that spans three decades, from the heady days of India's infrastructure boom to the sobering reality of overleveraged balance sheets, from the vision of nation-building to the harsh mathematics of insolvency courts. Today, JPPOWER reports revenues of ₹5,291 crore and profits of ₹743 crore, yet despite repeated profits, it pays no dividends. The stock that once touched ₹84 in 2010 and crashed to a devastating ₹0.35 in 2020 now trades around ₹20, having rallied on whispers of a potential savior. Because here's the twist: Adani Group, India's infrastructure behemoth, is reportedly circling with a ₹12,500 crore bid for the parent company's assets.

The central question isn't just how JPPOWER survived—it's whether this survival story is about to transform into a resurrection tale. Can a company born from the ambitions of India's infrastructure dreams, nearly killed by debt, find new life under new ownership? Or is this merely the final chapter of a cautionary tale about leverage, ambition, and the perils of building a nation's infrastructure on borrowed money?

What follows is the complete saga: from Jaiprakash Gaur's vision of nation-building through concrete and turbines, through the intoxicating boom years when every infrastructure company believed India's growth story would never end, to the sobering collapse and the unexpected survival of this particular piece of the empire. It's a story that teaches us about capital allocation, the dangers of conglomerate structures, and perhaps most importantly, how sometimes the children can outlive their parents—even in corporate India.

II. The Jaypee Empire Origins & Vision

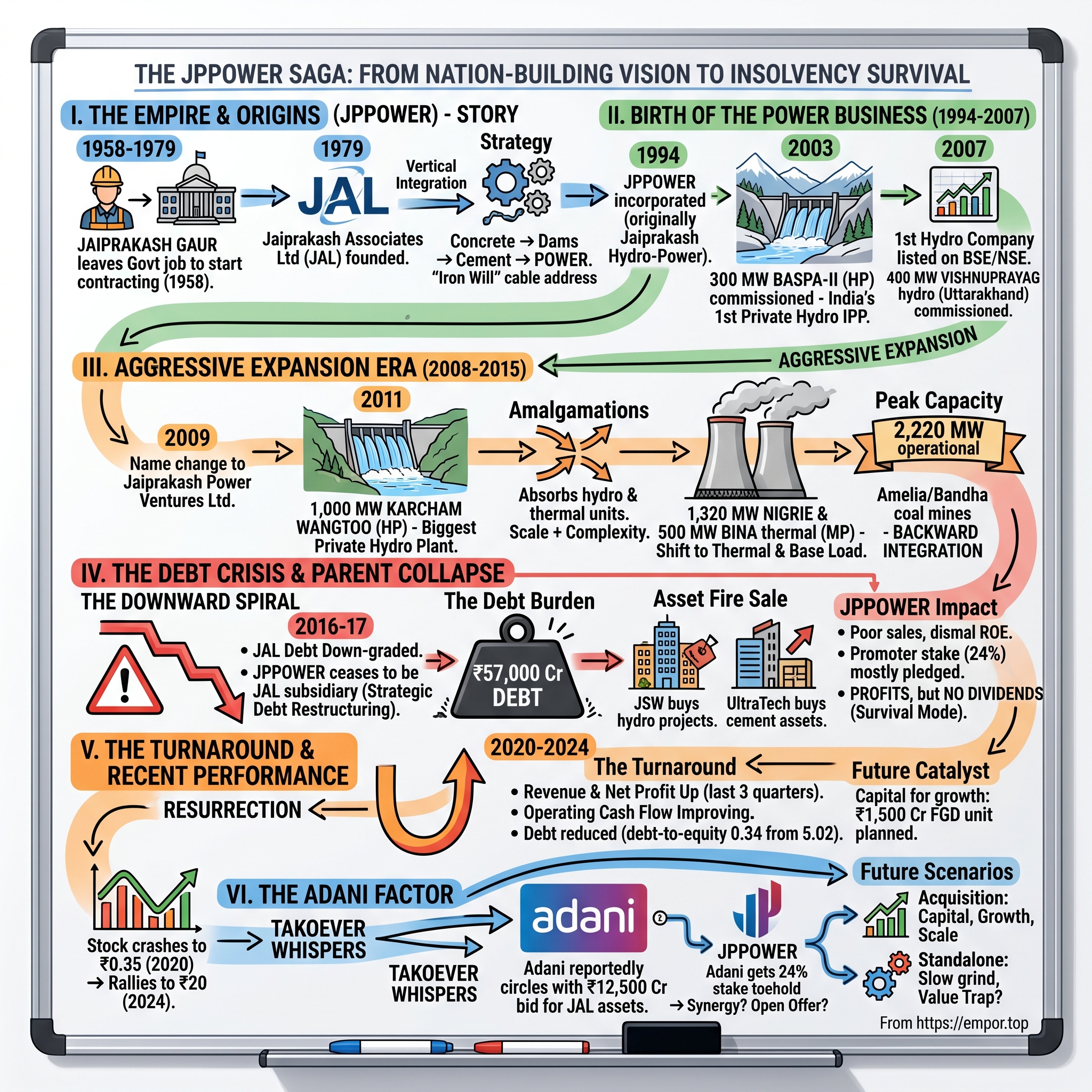

In 1950, a young man named Jaiprakash Gaur walked out of India's premier engineering institution—IIT Roorkee (then known as Thomason College of Civil Engineering)—with a degree and dreams larger than the newly independent nation's infrastructure deficit. Fresh out of college, he did what most bright engineers did in those days: joined the government. But by 1958, something had shifted. Perhaps it was watching India struggle to build its basic infrastructure, or perhaps it was simply the entrepreneurial itch that afflicts certain individuals. Whatever the catalyst, Gaur left his government post to start what would become one of India's most ambitious infrastructure stories. The twenty-one years between Gaur's first entrepreneurial steps in 1958 and the formal founding of Jaiprakash Associates Limited in 1979 were spent building credibility, relationships, and most importantly, execution capability. Jaiprakash Gaur founded the conglomerate in 1979, but the real foundation was laid through two decades of grinding it out as a civil contractor, learning the intricacies of India's infrastructure development from the ground up.

What made Gaur different wasn't just his engineering credentials or his government experience—it was his philosophy of nation-building through infrastructure. "To leave a secure government job and pursue contractorship in 1958, when it was considered to be most prestigious, required courage", as company documents would later note. But Gaur saw what others didn't: India needed builders, not bureaucrats.

The transformation from contractor to conglomerate chairman was methodical. In 1967, he led and transformed a motley group of persons into a company which took pride in its cable address "Iron Will". That cable address tells you everything about the man's approach to business. By the time he formally established Jaiprakash Associates, Gaur had already proven his mettle on some of India's most challenging infrastructure projects.

The crown jewel of these early achievements was the Sardar Sarovar Dam – India's largest dam with 7.2 million cu.m. of chilled concrete; larger by 75% in terms of volume than Bhakra Nangal Dam. Think about that for a moment: a private contractor taking on a project that dwarfed what the government had achieved with Bhakra Nangal, the engineering marvel that had defined India's post-independence ambitions.

But dams were just the beginning. Gaur understood something fundamental about infrastructure businesses: they're all interconnected. Build a dam, you need cement. Have cement capacity, you need power. Have power, you can expand into more infrastructure. This wasn't diversification for the sake of empire-building—it was strategic backward and forward integration at its finest.

In the early 80's in order to achieve backward integration, a cement plant was established in District Rewa, Madhya Pradesh. This wasn't random expansion; it was calculated strategy. Every major infrastructure project consumed massive amounts of cement. Why pay margins to someone else when you could capture that value yourself? Since then a series of cement plants, all over India, have been commissioned with a capacity of 35.40 MT making the Jaypee Group the third largest cement producer in the country.

The power business followed similar logic. Infrastructure projects needed reliable power supply. Cement plants consumed enormous amounts of energy. Why not control that critical input? By the time JPPOWER was incorporated in 1994, the Jaypee Group had already established itself as a formidable force across the infrastructure value chain.

What's remarkable about Gaur's journey is how he maintained the entrepreneur's hunger even as the empire grew. In 2012 he was ranked by Forbes magazine as the 70th-richest person in India, with an estimated net worth of US$855 million. Yet wealth was never the point—it was always about building, about leaving a mark on India's landscape.

The group's reach became staggering: engineering, construction, power, real estate, hospitality, IT, sports and education. They built the Yamuna Expressway, which opened 9 August 2012, India's first Formula One track at Buddh International Circuit, universities, hospitals, and townships. This wasn't just a business conglomerate—it was an attempt to build the infrastructure of modern India through private enterprise.

But here's where the story takes its crucial turn: ambition without discipline in capital allocation is a recipe for disaster. The same interconnected strategy that drove growth would eventually become the web that nearly strangled the empire. Because when you're leveraged across multiple capital-intensive businesses, all feeding into each other, a problem in one area can cascade through the entire structure.

III. Birth of the Power Business (1994-2007)

The boardroom at Jaypee headquarters in 1994 must have been electric with possibility. India's power deficit was chronic—rolling blackouts were the norm, not the exception. Industrial growth was being throttled by inadequate electricity supply. And here was Jaiprakash Gaur, fresh off decades of dam-building success, ready to solve yet another piece of India's infrastructure puzzle.JPPOWER was incorporated in 1994 as Jaiprakash Hydro-Power Limited, receiving its Certificate of Commencement in January 1995. But the real genesis of the power business had begun three years earlier, in the remote Kinnaur district of Himachal Pradesh, where the Baspa river cuts through the Himalayas with a force that engineers dream of harnessing.

The MOU was signed with Government of Himachal Pradesh in November, 1991 and was granted approval to develop 300 MW Baspa Stage-II Hydroelectric project in private sector on "Build, Own and Operate" basis by the Government of Himachal Pradesh in October 1992. This wasn't just another infrastructure project—it was India testing whether private capital could solve its power crisis. The government had just liberalized the power policy, inviting private sector participation for the first time. And Jaypee, with its dam-building expertise, was perfectly positioned to be the pioneer.

The Baspa-II project represented everything ambitious and risky about India's infrastructure privatization experiment. 300 MW Baspa Stage II Project is the first Independent Power Producer (IPP) project after the Government of India liberalized the power policy by inviting private sector participation for setting up hydropower project on "BOO" basis. Baspa Hydro-electric project stage II (300 MW) is the first plant of this size in the private sector.

Building in the Himalayas is not for the faint-hearted. The diversion barrage at village Kuppa near Sangla, the 7.95km tunnel boring through mountain rock, the underground surge shaft and powerhouse near Karcham—every component was an engineering challenge multiplied by altitude, weather, and logistics. This was infrastructure development at its most capital-intensive and technically demanding.

The project was fully commissioned on 8th June, 2003 and has since been generating power. Ten years from MOU to commissioning—a decade of capital locked up, of engineering challenges overcome, of regulatory hurdles navigated. But when those three 100 MW Pelton turbines finally spun to life, Jaypee had achieved something historic: India's first major private hydropower success story.

The market responded enthusiastically. When shares of JHPL listed on BSE/NSE, it became the first hydropower company to be listed in the country. Investors saw what Gaur saw: India's chronic power deficit wasn't going away anytime soon, and whoever could generate reliable electricity would have pricing power for decades.

Success at Baspa emboldened the company to think bigger. By 2007, they had commissioned the 400 MW Vishnuprayag Hydro-Electric Plant in Uttarakhand, operational since October of that year. This project, built on the Alaknanda River, doubled down on the high-altitude hydropower expertise Jaypee had developed.

But hydropower in India came with inherent challenges that would eventually haunt the sector. The capital costs were staggering—building in remote mountain locations meant every bag of cement, every piece of equipment had to be transported through treacherous terrain. Environmental clearances were becoming increasingly complex as awareness of ecological impacts grew. Local communities, initially welcoming of development, began questioning whether they were getting a fair share of the benefits.

The execution complexities were mind-boggling. Tunnel boring through unpredictable geology, managing water flows that could vary dramatically with monsoons and glacier melt, dealing with the constant threat of landslides and earthquakes—every project was a masterclass in risk management. Or at least, that's what it needed to be.

Then there was the regulatory maze. Power purchase agreements with state electricity boards, environmental clearances from multiple agencies, land acquisition in sensitive border areas, rehabilitation and resettlement issues even when projects claimed to be "environment friendly devoid of any rehabilitation or resettlement issue"—each project required navigating a bureaucratic labyrinth that could delay commissioning by years and inflate costs exponentially.

Yet despite these challenges, or perhaps because of them, Jaypee's power business was seen as strategic. The high barriers to entry meant limited competition. The BOO (Build, Own, Operate) model meant long-term revenue visibility through power purchase agreements. And most importantly, it fit perfectly into the Jaypee ecosystem—the cement plants needed power, the construction arm built the projects, and the power generation provided steady cash flows to fund further expansion.

By 2007, as India's economy was heating up and power demand was soaring, JPPOWER looked perfectly positioned. They had proven execution capability in both hydro projects, a pipeline of opportunities, and access to capital through both internal accruals and their listed status. The stage was set for aggressive expansion.

What nobody fully appreciated at the time was how the very interconnectedness that made the strategy elegant would become its Achilles heel. When you're building capital-intensive projects with borrowed money, betting on continued economic growth and stable power prices, you're essentially making a leveraged bet on India's development story. And leverage, as we would all learn in the years to come, cuts both ways.

IV. Aggressive Expansion Era (2008-2015)

The year 2008 should have been a warning. Lehman Brothers collapsed, global credit markets froze, and infrastructure companies worldwide discovered that cheap money could disappear overnight. But in the boardrooms of Indian infrastructure giants, including Jaypee, the financial crisis seemed like a distant American problem. India's growth story, they believed, was decoupled from Western woes. Power demand was still growing at 8-10% annually. The government was talking about adding 100,000 MW of generation capacity. This was the time to be aggressive, not cautious. In 2009, the company underwent a significant restructuring, renaming itself from Jaiprakash Hydro-Power Limited to Jaiprakash Power Ventures Limited. The name change signaled intent—this was no longer just a hydropower company. They were ready to venture into whatever forms of power generation the market demanded.

The crown jewel of this expansion phase was the 1,000 MW Karcham Wangtoo project. In 1993, and after years of delays, the Jaypee Karcham Hydro Corporation Limited of Jaypee Group signed a memorandum of understanding to develop the dam. On 18 November 2005, the construction on the power station began. In May 2011, the first generator was commissioned, the second in June and the final two in September.

Karcham Wangtoo was hydropower on steroids—four units of 250 MW each, making it the biggest hydel project in the private sector at the time. The engineering statistics were staggering: a 98-meter tall dam, a 17.2 km long headrace tunnel with a 10.48-meter diameter boring through the Himalayas, and 44.60 km of total tunneling in challenging Himalayan geology. This wasn't just scaling up; it was pushing the boundaries of what private companies could execute in India.

The 2011 amalgamations marked a pivotal moment in JPPOWER's trajectory. The company absorbed both Jaypee Karcham Hydro Corporation Limited (JKHCL) and Bina Power Supply Company Limited (BPSCL) with effect from April 1, 2010. Through these amalgamations, JPPOWER didn't just acquire assets—it acquired complexity. The 1,000 MW Karcham Wangtoo added scale in hydro, while the 1,250 MW Bina Thermal project marked the company's serious entry into thermal power generation.

But why thermal? The logic seemed impeccable at the time. Hydro was seasonal, dependent on water flows and monsoons. Thermal provided base load power, the steady generation that utilities desperately needed. Moreover, thermal plants could be built closer to demand centers, avoiding the transmission losses that plagued remote hydro projects. And crucially, India had abundant coal reserves—or so everyone believed.

The Bina Thermal Power Plant, with its initial 500 MW capacity commissioned between 2012-2013, represented JPPOWER's first major thermal bet. Located in Madhya Pradesh, it was strategically positioned to serve the power-hungry states of central India. The plant was designed to be expanded, and expand it did.

Then came the Nigrie Super Thermal Power Plant—the company's magnum opus in thermal generation. With 1,320 MW capacity (2x660 MW units) commissioned between 2014-2015, Nigrie was a statement of intent. Jaypee has two thermal power plants (Bina Thermal Power plant – 500 MW and Nigrie Thermal Power Plant – 2X660 MW). This wasn't just adding capacity; it was betting the company's future on India's continued economic expansion and power demand growth.

The thermal expansion came with another strategic element: backward integration into coal mining. The company secured coal mining operations in Amelia and Bandha, Madhya Pradesh. The logic was similar to the cement-power integration—control your key input costs, ensure supply security, capture more of the value chain. In a country where Coal India's monopoly often meant uncertain supplies and quality issues, having captive coal blocks seemed like a masterstroke.

The infrastructure boom context of this period cannot be overstated. India's GDP was growing at 8-9% annually. The government was promising "Power for All" by 2012. Industrial corridors were being planned. New cities were being built. Every projection showed massive power deficits for the next decade. In this environment, adding generation capacity seemed less like speculation and more like nation-building.

By 2015, JPPOWER had achieved peak capacity—2,220 MW operational across hydro and thermal. The company had successfully transformed from a pure hydro player to a diversified power generator. They had a 2 MTPA cement grinding unit at Nigrie, creating additional synergies. The portfolio looked balanced: hydro for peak power and environmental credentials, thermal for base load and steady revenues, coal mines for input security, cement for additional cash flows.

The market positioning seemed strong. JPPOWER was among the largest private power generators in India. They had long-term power purchase agreements (PPAs) with state utilities. The assets were operational, not under development—a crucial distinction in an industry littered with stalled projects. Management spoke confidently about further expansion, about India's growth story, about being perfectly positioned for the infrastructure super-cycle.

But beneath the surface, cracks were forming. The thermal plants had been built assuming certain coal costs, certain power tariffs, certain capacity utilization rates. The hydro projects had been financed assuming certain water flows and seasonal patterns. The entire expansion had been funded primarily through debt, with the assumption that operational cash flows would service the borrowings.

What nobody wanted to acknowledge was that India's power sector was heading for a crisis. State electricity boards were bankrupt. Power demand growth was slowing as the economy cooled. Coal supplies were becoming erratic. Environmental regulations were tightening. And most critically, the cost of capital was rising while power tariffs were being kept artificially low for political reasons.

By the end of 2015, JPPOWER's installed capacity had grown from 300 MW to 2,220 MW in just over a decade. The debt had grown even faster. The parent company, Jaiprakash Associates, was already showing signs of stress, with rating agencies beginning to downgrade its debt. The aggressive expansion that had seemed so logical, so inevitable, was about to meet the harsh reality of over-leveraged balance sheets and a power sector in crisis.

V. The Debt Crisis & Parent Company Collapse

The unraveling began not with a bang but with a rating downgrade. In 2016, credit rating agencies started marking down Jaiprakash Associates' debt, citing "stretched liquidity position" and "high leverage." These sterile financial terms masked a more dramatic reality: the empire that Jaiprakash Gaur had built over six decades was drowning in debt, and the lifeboats were few and far between. The year 2017 marked a watershed moment. JAL ceases to be holding company under Strategic Debt Restructuring, retains 29.74% stake in JPPOWER. This wasn't a voluntary reorganization—it was forced deleveraging, creditors seizing control and forcing asset sales to recover their loans. The parent that had nurtured JPPOWER since 1994 was no longer in control of its destiny.

The numbers tell the story of a spectacular collapse. As of February 20, 2025, Jaiprakash Associates Ltd (JAL) carried a total outstanding debt of ₹55,493.43 crore, including both principal and accumulated interest. The scale of the financial distress is underscored by the involvement of 22 different lenders, reflecting the systemic impact of JAL's liabilities across the banking sector. To put this in perspective, JAL's debt burden was larger than the GDP of several Indian states.

The asset fire sale began in earnest. UltraTech Cement completed the Rs 16,189 crore acquisition of Jaiprakash Associates' six integrated cement plants and five grinding units, having a capacity of 21.2 million tonnes. In September 2015, JSW Energy acquired two hydropower Projects of Jaiprakash Associates in a deal worth ₹ 9,700 crore. These weren't strategic divestments—they were desperate attempts to raise cash and appease creditors.

For JPPOWER, watching its parent's collapse was like watching a slow-motion train wreck. The company's own challenges were mounting. The company has delivered a poor sales growth of 10.7% over past five years. The three-year ROE stood at a dismal 6.86%. But perhaps most tellingly, Though the company is reporting repeated profits, it is not paying out dividend—every rupee of profit was being used to service debt or maintain operations.

The promoter holding situation became increasingly precarious. 79.2% of the promoter's 24% stake was pledged or encumbered—essentially, the founding family had mortgaged their ownership to keep the lights on. This created a bizarre situation where the promoters technically owned the company but had no real control, with lenders holding the economic interest through pledged shares.

On June 03, 2024, in a setback for Jaiprakash Associates, the Allahabad bench of the National Company Law Tribunal (NCLT) admitted ICICI Bank and SBI's insolvency plea against the company. This wasn't unexpected—The first insolvency plea against Jaiprakash Associates Ltd (JAL), a diversified infrastructure company operating across cement, power, hospitality, and construction, dates back to 2018, when ICICI Bank first approached the tribunal for debt recovery.

The insolvency admission triggered a feeding frenzy among potential buyers. A total of 25 companies have shown interest in taking over Jaiprakash Associates. Big names like Gautam Adani's Adani Enterprises, Anil Agarwal's Vedanta, and Baba Ramdev's Patanjali Ayurveda are among the top bidders aiming to acquire the company.

So why did JPPOWER survive while its parent collapsed? The answer lies in the structure of Indian corporate law and the peculiarities of listed subsidiaries. JPPOWER, as a separate listed entity, had its own balance sheet, its own creditors, and critically, its own operational cash flows. While the parent was a holding company dependent on dividends and asset sales, JPPOWER had actual power plants generating actual electricity sold under long-term PPAs.

The debt metrics tell the story. While JAL was drowning in ₹57,000 crore of debt with no clear path to service it, JPPOWER had managed to bring its debt-to-equity ratio down to 0.34 from a peak of 5.02. This wasn't accidental—it was survival mode, every decision focused on deleveraging rather than growth.

The operational performance, while not stellar, was at least stable. The 400 MW Vishnuprayag hydro project continued generating power. The 500 MW Bina thermal plant kept running. The 1,320 MW Nigrie thermal plant, despite challenges, maintained operations. These weren't just assets on a balance sheet—they were critical infrastructure serving millions of consumers in Madhya Pradesh and Uttar Pradesh.

But survival isn't the same as thriving. The company was essentially in a holding pattern—generating enough cash to service debt and maintain operations, but not enough to invest in growth or reward shareholders. The no-dividend policy despite profits was a clear signal: this was a company in preservation mode, not expansion mode.

The parent's collapse also created unique challenges. Potential partners and lenders viewed JPPOWER with suspicion—if the parent could collapse so spectacularly, what did that say about the subsidiary's governance and risk management? The tainted legacy made raising capital more expensive and finding strategic partners more difficult.

Yet paradoxically, the parent's insolvency might have been JPPOWER's salvation. With JAL in NCLT and creditors taking control, the pressure to upstream cash from JPPOWER disappeared. The subsidiary could focus on its own survival rather than being milked to service the parent's obligations.

VI. Operations & Asset Portfolio Deep Dive

Inside the control room of the Nigrie Super Thermal Power Plant, the hum of turbines provides a constant soundtrack to JPPOWER's operational reality. This isn't the glamorous world of deal-making and financial engineering—this is the unglamorous business of keeping the lights on, literally. Every day, coal trains arrive, furnaces burn, turbines spin, and electricity flows into the grid. It's this operational bedrock that has kept JPPOWER alive while its parent crumbled.

The current portfolio reads like a textbook case in Indian power generation diversity. The 400 MW Vishnuprayag hydro project in Uttarakhand harnesses the Alaknanda River's force through a 10-meter diameter tunnel boring through the Himalayas. During the monsoon months, when water flows are abundant, this plant operates at peak capacity, generating premium-priced peak power for the northern grid.

The Bina Thermal Power Plant's 500 MW capacity serves as the reliable workhorse. Located strategically in Madhya Pradesh, it benefits from relatively better coal linkages and proximity to demand centers. The plant's load factor—a measure of actual generation versus capacity—has been consistently higher than the national average for thermal plants, a testament to operational efficiency amid sectoral challenges.

But it's the 1,320 MW Nigrie Super Thermal Power Plant that represents JPPOWER's biggest operational bet. Two units of 660 MW each make this a significant player in the central Indian power market. The plant's location in Singrauli district places it in India's energy capital, surrounded by coal mines and other thermal plants. This clustering provides operational synergies—shared transmission infrastructure, established coal transportation routes, and a deep pool of technical expertise.

The 2 MTPA cement grinding unit at Nigrie adds an interesting dimension to the portfolio. This isn't core to power generation, but it provides diversification and utilizes fly ash from the thermal plant—a classic example of industrial symbiosis. In an industry where environmental compliance is increasingly stringent, turning waste into product is both good business and good PR.

The market focus on Madhya Pradesh and Uttar Pradesh isn't accidental—it's strategic. These states have massive power deficits, growing industrial demand, and relatively stable regulatory regimes. The power purchase agreements with state utilities, while not always promptly honored, provide long-term revenue visibility that pure merchant power plants lack.

JPPOWER's subsidiary structure reveals the complexity beneath the surface. Jaypee Powergrid Limited handles transmission assets—the crucial link between generation and consumption. Jaypee Arunachal Power Limited represents future potential, with hydro projects in India's northeastern frontier. Sangam Power Generation Company Limited adds additional thermal capacity to the portfolio.

Each subsidiary is a bet on a different aspect of India's power sector evolution. Transmission assets benefit from regulated returns and lower risk. Northeastern hydro projects offer massive potential but face execution challenges. Additional thermal capacity provides scale but requires careful management of fuel costs and environmental compliance.

The operational performance metrics paint a picture of competent, if not exceptional, execution. Plant availability factors—the percentage of time plants are available to generate—hover around industry averages. Heat rates, measuring efficiency in converting coal to electricity, show gradual improvement but remain constrained by the age and design of certain units.

The revenue model, anchored in long-term PPAs, provides stability but limits upside. Unlike merchant power plants that can capitalize on spot market price spikes, JPPOWER's contracted capacity means predictable but capped revenues. In a volatile power market, this is both a blessing and a curse—protection from price crashes but inability to capture windfalls.

Coal sourcing remains the critical operational challenge for thermal plants. Despite having mining operations in Amelia and Bandha, Madhya Pradesh, the company still depends partially on Coal India supplies and imported coal. Coal quality variations, supply disruptions, and price volatility directly impact operational margins. Every percentage point change in coal costs can swing profitability significantly.

The hydro operations face different challenges. Water flow variability due to changing monsoon patterns and glacier melt affects generation predictability. Silt management in Himalayan rivers requires constant dredging and maintenance. Environmental regulations around minimum flow requirements reduce effective capacity. And increasingly, local communities demand a larger share of benefits from projects in their backyards.

Yet despite these challenges, the plants keep running. This operational resilience—the ability to generate power day after day despite financial stress, regulatory changes, and market volatility—is what separates JPPOWER from paper companies with undeveloped projects. These are real assets generating real electricity for real consumers.

The technical teams deserve credit here. Managing a diverse portfolio of hydro and thermal assets across multiple states requires deep expertise. Keeping aging thermal units running efficiently while meeting tightening emission norms demands constant innovation. Operating hydro plants in challenging Himalayan terrain needs both engineering excellence and relationship management with local communities.

The cement grinding unit, while small in the overall scheme, demonstrates operational opportunism. Utilizing fly ash from thermal plants, located at the same site to minimize transportation costs, selling into local markets with established distribution—it's a model of operational efficiency even if financial returns remain modest.

What emerges from this operational deep dive is a company that knows how to run power plants. This isn't cutting-edge technology or revolutionary business models—it's blocking and tackling, the daily grind of operational excellence. In an industry littered with stalled projects and non-performing assets, simply keeping the lights on is an achievement worth noting.

VII. The Turnaround & Recent Performance

The numbers tell a story of resurrection that seemed impossible just five years ago. ₹5,291 Cr revenue, ₹743 Cr profit, ₹12,939 Cr market cap—these aren't the metrics of a company on life support. They're the vital signs of an organization that has somehow navigated through the valley of death and emerged, scarred but breathing, on the other side.

The debt reduction success is perhaps the most remarkable achievement. The debt-to-equity ratio has plummeted from a catastrophic peak of 5.02 to a manageable 0.34. Think about that transformation—from being leveraged five times over to having debt at just one-third of equity. This wasn't financial engineering or accounting jugglery—this was grinding, painful deleveraging through asset sales, operational cash flows, and sheer survival instinct.

The stock price journey reads like a cardiac monitor during a heart attack. From an all-time high of ₹84 in 2010, when India's infrastructure boom was at its peak and every power company was valued like a tech startup, to an all-time low of ₹0.35 in 2020, when COVID-19 and the parent's collapse made survival seem impossible. At ₹0.35, the market was essentially valuing JPPOWER as an option on survival—probably worthless, but maybe, just maybe, worth something if miracles happened. The recent rally tells a different story. The stock has fallen by −3.20% compared to the previous week, the month change is a −16.37% fall, yet Over the past six months, its share price has outperformed the S&P BSE 100 Index by +14.99%. This volatility isn't random noise—it's the market trying to price in competing narratives: the turnaround story versus the parent's insolvency, the operational improvements versus the sector headwinds, the Adani acquisition speculation versus standalone survival.

The improving fundamentals deserve attention. The debt reduction from that peak of 5.02 times equity wasn't achieved through financial engineering—it was brutal deleveraging. Asset sales, yes, but also operational cash flow generation, working capital management, and most painfully, the complete cessation of growth investments. Every rupee that could be used to pay down debt was used for exactly that purpose.

Operating cash flow improvements tell the real story of the turnaround. When you strip away the financial noise, what you see is a company that has learned to generate cash from operations. The thermal plants are running more efficiently. The hydro projects are benefiting from better water management. Coal procurement has been optimized. These aren't headline-grabbing improvements, but they're the difference between survival and bankruptcy.

The lack of dividends despite repeated profits sends a clear message about capital allocation priorities. Though the company is reporting repeated profits, it is not paying out dividend. In normal times, this would anger shareholders. But these aren't normal times—this is survival mode, where every rupee of retained earnings improves the balance sheet and reduces bankruptcy risk.

The company faced a 19% revenue decline in FY25 due to thermal plant maintenance, yet profitability was maintained. This operational resilience—the ability to manage through planned outages without destroying the bottom line—demonstrates improved cost management and operational efficiency.

The AGM and takeover speculation have added fuel to the stock's volatility. Jaiprakash Power Ventures shares saw significant fluctuations, with a sharp decline after a rally fueled by acquisition speculation from Adani Group. The market is essentially trading on binary outcomes: either JPPOWER gets acquired at a premium by a strategic buyer, or it continues its slow, grinding turnaround as a standalone entity.

Looking at analyst perspectives, The analyst consensus target price for shares in Jaiprakash Power Ventures is IN₹3.00. That is 85.09% below the last closing price of IN₹20.12. This massive disconnect between analyst targets and market prices reflects the uncertainty around the parent's resolution and potential change in control.

The transformation metrics are worth emphasizing. Revenue is up for the last 3 quarters, 1.25K Cr → 1.63K Cr (in ₹), with an average increase of 12.1% per quarter. Netprofit is up for the last 3 quarters, 126.68 Cr → 278.13 Cr (in ₹), with an average increase of 31.3% per quarter. These aren't the numbers of a dying company—they're the metrics of a business finding its operational footing.

In the last 3 years, JP Power's share price has increased around 165% as of 16th May, 2025. For context, this performance has come despite the parent's insolvency, a challenging power sector environment, and no dividend payments. The market is clearly pricing in either operational improvements or M&A optionality, or both.

The capital expenditure plans signal confidence in the future. Plans to invest ₹1,500 crore in an FGD unit aim to enhance efficiency and generate byproducts. Flue Gas Desulfurization isn't sexy, but it's necessary for environmental compliance and operational continuity. The fact that JPPOWER can contemplate a ₹1,500 crore investment after years of capital starvation shows how far the balance sheet has recovered.

But challenges remain substantial. The company has delivered a poor sales growth of 10.7% over past five years. This isn't just about market conditions—it's about the inability to invest in growth while firefighting balance sheet issues. The three-year ROE of 6.86% is below the cost of capital, meaning the company is technically destroying value even while reporting profits.

What we're witnessing is a turnaround in progress, not a turnaround completed. The debt has been reduced to manageable levels, but growth remains elusive. Operations have stabilized, but excellence remains distant. The company has survived the worst, but thriving seems years away without a catalyst.

The stock price volatility reflects this uncertainty. From ₹0.35 to ₹20+ is a 57x return for those brave enough to buy at the bottom. But from ₹84 to ₹20 is still a 76% destruction of value for those who bought at the peak. Where you stand on JPPOWER depends entirely on where you sit in this journey.

VIII. The Adani Factor & Future Scenarios

The conference rooms at Adani Enterprises' headquarters in Ahmedabad have seen many ambitious plans, but the potential acquisition of Jaiprakash Associates' assets, including the crown jewel 24% stake in JPPOWER, represents something different. This isn't about building new capacity or entering new markets—it's about acquiring distressed assets at liquidation prices and plugging them into one of India's most efficient infrastructure machines. The headlines scream the numbers: The Adani group has emerged the frontrunner to acquire Jaiprakash Associates Ltd (JAL), which is currently undergoing insolvency proceedings, with a bid of up to ₹12,500 crore. The conglomerate has proposed more than ₹8,000 crore as an upfront payment without any preconditions. For context, this values the entire JAL empire—once worth ₹65,000 crore at its peak—at less than 20% of its former glory.

But the competition is fierce. Rival bidder Dalmia group is also in the fray and is willing to top Adani's offer — provided a key legal hurdle related to JAL's Sports City project is resolved. The case is currently pending before the Supreme Court. Other serious bidders include Vedanta at ₹12,500 crore, Jindal Steel & Power at ₹10,300 crore, and PNC Infratech at ₹9,500 crore.

For JPPOWER, the Adani acquisition scenario represents both opportunity and uncertainty. Jaiprakash Associates currently holds a 24% stake in JP Power, and the acquisition is expected to unlock value for the power firm. Under Adani's ownership, JPPOWER would gain access to the conglomerate's deep pockets, operational expertise, and crucially, synergies with Adani Power's existing portfolio.

The strategic fit is compelling. Four cement plants in UP and MP, with 5.6 MTPA (metric tonne per annum) capacity and 12 leased limestone mines, could fold neatly into Adani's Ambuja-ACC cement empire. Its 279 MW captive thermal plant adds power capacity. And JP Associates' 24% stake in JP Power Ventures also gives Adani a toehold in thermal, hydro and mining operations.

For Adani Group, this isn't a rescue or even a turnaround bet, but something far more calculated. It's kind of an arbitrage about not buying value, but buying disorder. Adani specializes in acquiring distressed assets and plugging them into its industrial machine—the 2022 acquisition of Holcim's cement assets for $6.5 billion being the template.

The market's reaction has been volatile but telling. With a market capitalization of Rs 15,208 Crores, the share price of Jaiprakash Power Venture Limited was trading over 18% up to hit an intraday high of Rs 22.25 per share. Investors expect the deal to benefit the company, as the parent holds a big stake and the businesses fit well with Adani's plans.

But there are significant complications. The bids are subject to the outcome of a crucial case relating to Jaiprakash's 1,000-hectare Sports City project in Greater Noida. Earlier in March 2025, the Allahabad High Court upheld the YEIDA decision to cancel the land allotment. The case is currently under review by the Supreme Court. This legal overhang could derail the entire process.

The NCLT and creditor approval process adds another layer of complexity. The Committee of Creditors (CoC) of Jaiprakash Associates is in its final phase of evaluating the resolution plans of five shortlisted bidders. Even if Adani's bid is selected, it needs 66% creditor approval and NCLT sanction—neither guaranteed in India's evolving bankruptcy jurisprudence.

For minority shareholders in JPPOWER, the Adani scenario presents a classic good news/bad news situation. The good news: new ownership could mean capital for growth, operational improvements, and removal of the parent overhang. The bad news: Equity sits at the bottom of the IBC waterfall (and in most cases, it doesn't even make the queue). Minority shareholders might see their stakes diluted or restructured.

The benefits of new ownership under Adani are tangible. Funding access would transform JPPOWER from a capital-starved survivor to a growth-oriented power company. Operational scale through integration with Adani Power could improve plant efficiency and reduce costs. Group synergies in coal procurement, logistics, and even renewable energy transition could accelerate.

But risks from past Jaypee insolvencies loom large. The Jaypee Infratech insolvency, where thousands of homebuyers juggle EMIs and rent while their buildings stall, has created regulatory scrutiny and reputational damage that could spill over. The complex web of inter-company transactions and guarantees might create unexpected liabilities.

The independent survival scenario—where no acquisition happens and JPPOWER continues as a standalone entity—isn't necessarily dire. The company has proven it can survive without parent support. Debt has been reduced to manageable levels. Operations continue to generate cash. But growth would remain constrained, and the company would likely remain a value trap—cheap for good reasons.

India's power sector dynamics add another dimension. The country still faces massive power deficits, especially during peak summer demand. The transition to renewable energy creates both opportunities and threats for thermal operators. Environmental regulations are tightening but thermal capacity remains essential for grid stability. In this context, JPPOWER's 2,220 MW of operational capacity has strategic value regardless of ownership.

The most likely scenario? Adani or another bidder acquires JAL, gains control of the 24% JPPOWER stake, and eventually makes an open offer for the remaining shares. This would provide an exit opportunity for minority shareholders while transforming JPPOWER into a subsidiary of a larger power conglomerate. The company would lose independence but gain resources—a Faustian bargain that might be the best available outcome.

IX. Playbook: Infrastructure & Turnaround Lessons

Every infrastructure boom ends the same way: a graveyard of overleveraged balance sheets and half-completed projects, picked over by vulture funds and strategic buyers who understand that one company's distress is another's opportunity. The JPPOWER story isn't unique in its broad strokes—it's the execution details that provide the masterclass in survival.

Lesson One: Capital intensity and leverage management in infrastructure are not just important—they're existential. When Jaypee was building the Karcham Wangtoo project, the capital cost was approximately ₹7 crore per MW. Today, solar projects cost ₹4-5 crore per MW and can be built in months, not years. The infrastructure company that loads up on debt to build long-gestation projects is making a bet that the economics won't change during construction. History suggests this is a bad bet.

The leverage mathematics are brutal and unforgiving. At 5x debt-to-equity, a 20% drop in revenues or a 200 basis point rise in interest rates can trigger a death spiral. JPPOWER's journey from 5.02x leverage to 0.34x wasn't strategy—it was chemotherapy, killing growth to save the patient. Every infrastructure investor needs to understand this: leverage amplifies returns in good times but destroys companies in bad times with mathematical certainty.

Lesson Two: Surviving parent company bankruptcy as a subsidiary requires legal firewalls and operational independence. JPPOWER survived because it was a separate legal entity with its own cash flows, its own creditors, and crucially, its own public shareholders who could cry foul if value was inappropriately transferred to the parent. The ring-fencing wasn't perfect—the 79.2% pledged promoter stake shows the pressure—but it was enough.

The key insight: operational assets with contracted revenues (like power plants with PPAs) can survive parent distress if they're legally separated and operationally independent. Development projects and land banks cannot—they're the first to be sacrificed. This is why JPPOWER's operational plants survived while JAL's real estate projects became litigation nightmares.

Lesson Three: Valuation perspectives in distressed infrastructure require a different lens. JPPOWER trades at a 31% premium to intrinsic value according to some metrics, yet the stock has been a multi-bagger from its lows. The lesson: in distressed situations, survival probability matters more than traditional valuation metrics. A company trading at 2x book value that has a 50% chance of bankruptcy is more expensive than one trading at 5x book that will definitely survive.

The importance of operational assets versus developmental projects cannot be overstated. Markets value bird-in-hand operational infrastructure at reasonable multiples. They value development projects at massive discounts, especially from distressed sellers. JPPOWER's operational 2,220 MW saved it; JAL's pipeline of projects condemned it.

Lesson Four: Regulatory relationships and PPA sanctity in Indian power sector are everything. Despite JAL's distress, state utilities continued to honor PPAs with JPPOWER. This wasn't charity—it was self-interest. States need power, and abrogating PPAs would destroy their ability to attract future investment. The sanctity of these contracts, tested through parent bankruptcy, proved robust.

But regulatory relationships go beyond contracts. Environmental clearances, coal linkages, water rights—these are valuable assets that can't be easily replicated. A distressed company that maintains regulatory compliance and relationships preserves option value even if financial metrics look terrible. JPPOWER's continued operations despite parent distress preserved these intangible but crucial assets.

Lesson Five: Infrastructure boom-bust cycles are predictable in pattern if not in timing. The cycle always follows the same pattern: economic growth drives infrastructure demand, cheap capital floods in, projects proliferate, capacity exceeds demand, prices crash, leverage kills the weak, consolidation begins, and the cycle resets. We've seen it in telecom, airlines, steel, and power. The winners are those who survive the down cycle with capacity intact.

JPPOWER is now in the consolidation phase, where stronger players acquire distressed assets at attractive valuations. This is exactly where you want to be as an acquirer, and exactly where you don't want to be as a distressed seller. The lesson: in infrastructure, timing the cycle matters more than picking the right projects.

Lesson Six: The human element in turnarounds is underappreciated. JPPOWER retained operational staff and technical expertise even during its darkest hours. Plants kept running, maintenance schedules were met, regulatory compliance continued. This operational continuity preserved value that financial restructuring alone couldn't have saved.

Contrast this with other distressed infrastructure companies where key personnel fled, maintenance was deferred, and assets deteriorated. A power plant that hasn't run for two years isn't worth its book value—it's worth scrap value minus rehabilitation costs. JPPOWER's operational continuity preserved option value that enabled the turnaround.

Lesson Seven: The importance of diversification within focus. JPPOWER's mix of hydro and thermal, while adding complexity, provided resilience. When coal prices spiked, hydro provided relief. When water flows disappointed, thermal provided backup. This isn't the conglomerate diversification that killed JAL—it's thoughtful portfolio construction within a focused sector.

The infrastructure financing lessons are sobering. The assumption that India's growth would continue uninterrupted, that power demand would always exceed supply, that regulated returns meant guaranteed returns—all proved false. Infrastructure investment requires not just patient capital but humble capital that acknowledges uncertainty.

For turnaround investors, JPPOWER offers a template: identify operational assets with contracted revenues, ensure legal separation from distressed parents, wait for leverage to become manageable, and bet on survival rather than growth. It's not exciting, but it works.

The broader lesson for emerging market infrastructure: the gap between ambition and execution is filled with debt, and debt kills more companies than competition ever will. The survivors aren't necessarily the best operators or the most innovative—they're the ones who managed leverage conservatively enough to survive the inevitable downturn.

X. Analysis & Investment Case

Strip away the noise—the parent's insolvency, the Adani speculation, the sector challenges—and what remains? A power generation company with 2,220 MW of operational capacity, generating real electricity for real customers, with debt at manageable levels and improving operational metrics. That's the bull case in its simplest form. The bear case is equally simple: a company in a structurally challenged sector with limited growth prospects and governance questions.

Let's start with competitive positioning in the Indian power sector. JPPOWER is a minnow in an ocean of whales. NTPC has 76,000 MW of capacity. Adani Power has 17,000 MW. Tata Power has 14,000 MW. At 2,220 MW, JPPOWER isn't setting industry direction—it's along for the ride. This scale disadvantage manifests in higher costs (no bulk procurement benefits), limited negotiating power (can't push back on regulatory changes), and constrained growth options (can't bid for mega projects).

Yet being small has advantages in distressed situations. JPPOWER is easier to fix than a 20,000 MW portfolio. Its problems are contained, its assets manageable. For a strategic acquirer, 2,220 MW is a bite-sized acquisition that doesn't require betting the company. This "goldilocks" size—big enough to matter, small enough to manage—might be its salvation.

The solvency score of 50/100 indicates moderate financial health—not great, not terrible, but surviving. This middling score reflects the improved but still-stressed balance sheet, the operational stability but limited growth, the reduced but not eliminated parent overhang. It's the financial equivalent of a patient out of ICU but still in recovery.

The low promoter holding at 24% raises governance implications that cut both ways. Negative: founders with minimal skin in the game might not fight for minority shareholders. Positive: professional management might emerge without promoter interference. The reality is more nuanced—the promoters can't extract value because they don't control the company, but they also can't be easily removed because of India's takeover regulations.

Growth prospects in India's energy transition present both opportunity and threat. India needs to add 500 GW of renewable capacity by 2030 to meet climate commitments. But it also needs thermal capacity for grid stability when the sun doesn't shine and wind doesn't blow. JPPOWER's thermal plants could become more valuable as backup capacity, earning capacity charges even if generation decreases. Or they could become stranded assets if renewable plus storage becomes cheaper than thermal generation.

The hydro assets are better positioned for the energy transition. Hydro provides the flexibility that grids need to integrate intermittent renewables. The 400 MW Vishnuprayag project could see improved economics as grid flexibility becomes more valuable. But climate change affecting water flows adds uncertainty to long-term hydro economics.

Key risks read like a infrastructure investor's nightmare checklist. Parent resolution uncertainty: will the acquirer be friendly to minorities? Sector headwinds: state utility finances remain stressed, renewable competition intensifying. Leverage: while reduced, debt could spike if growth investments resume. Regulatory: environmental norms tightening, coal availability uncertain. Execution: can the company maintain operations while navigating ownership transition?

The bull case rests on three pillars. First, the turnaround story is real—debt has been cut, operations have stabilized, and the company has proven it can survive independently. Second, the strategic assets have value—operational plants in power-deficit states with long-term PPAs. Third, the new ownership catalyst could unlock value through better capital allocation, operational improvements, and growth investments.

But every bull has its bear. The bear case argues that survival isn't success. Yes, JPPOWER survived, but at what cost? No dividends despite profits. Minimal growth investment. ROE below cost of capital. The stock might be a "value trap"—optically cheap but structurally impaired. The parent overhang might resolve badly for minorities. The sector's structural challenges—state utility bankruptcies, renewable disruption, environmental regulations—might overwhelm any operational improvements.

The investment case ultimately depends on your view of three variables: India's power demand growth, the value of operational infrastructure in a consolidating sector, and the probability of favorable resolution of parent insolvency. Bulls believe power demand will surprise to the upside, operational assets will command premiums, and Adani or another strategic buyer will treat minorities fairly. Bears believe the opposite on all counts.

What's indisputable is that JPPOWER is no longer a bankruptcy candidate. The company has proven it can survive the worst—parent collapse, sector crisis, pandemic disruption. The question now is whether survival is enough for investment success, or whether investors need to see a path to growth and value creation.

The current valuation reflects this uncertainty. At ₹20, the stock has recovered dramatically from the ₹0.35 lows but remains 76% below the ₹84 peaks. The market is essentially saying: we believe the company will survive, we're not sure it will thrive, and we're waiting for clarity on ownership and strategy before committing further capital.

For fundamental investors, JPPOWER presents a classic special situation. It's not a quality compounder—the ROE is too low, the growth too constrained. It's not a deep value play—the balance sheet isn't fortress-like, the assets aren't hidden. It's a turnaround story in the middle innings, where the patient has stabilized but full recovery remains uncertain.

The decision to invest or avoid depends on your assessment of asymmetry. Bulls see 50-100% upside if the Adani deal happens and operations improve, with limited downside given the current valuation and operational stability. Bears see dead money at best, with potential for significant downside if the parent resolution goes badly or sector challenges intensify.

XI. Epilogue & Final Thoughts

As the sun sets over the Nigrie Super Thermal Power Plant, its twin cooling towers releasing steam into the Madhya Pradesh sky, we're reminded that infrastructure is ultimately about physical assets serving human needs. Behind the financial engineering, the debt restructuring, the insolvency proceedings, there are turbines spinning, electrons flowing, and homes being lit. JPPOWER's survival, against considerable odds, means these essential services continued even as the corporate superstructure collapsed around them.

The broader Jaypee Group saga offers a cautionary tale about infrastructure ambition in emerging markets. Jaiprakash Gaur's vision of building India's infrastructure through private enterprise wasn't wrong—it was essential. India needed someone to build dams, highways, power plants, and townships. The government couldn't do it alone. But the execution—leveraging every asset to build the next project, assuming growth would never stop, believing that infrastructure assets would always find buyers—proved fatal.

India's infrastructure financing challenges run deeper than one company's mistakes. The fundamental mismatch between long-gestation infrastructure projects and short-term debt financing creates systemic fragility. Add in regulated returns that don't adjust for market realities, state utilities that don't pay on time, and environmental regulations that change mid-project, and you have a recipe for sector-wide distress.

Yet infrastructure must be built. India's per capita power consumption is still one-third of the global average. Hundreds of millions still face regular power cuts. Industrial growth depends on reliable electricity. The transition to electric vehicles and renewable energy will require massive grid investments. Someone has to build this infrastructure, and someone has to finance it.

What JPPOWER's journey tells us about emerging market investing is both sobering and inspiring. Sobering because it shows how quickly leverage can destroy value, how corporate governance can fail minority shareholders, how sector dynamics can overwhelm company-specific excellence. A stock that falls 99.6% (from ₹84 to ₹0.35) destroys generational wealth and shatters investor confidence.

But it's also inspiring because it demonstrates that operational excellence and financial discipline can overcome even parent bankruptcy. The employees who kept plants running, the managers who cut costs and reduced debt, the board members who protected minority interests—these unsung heroes preserved value when destruction seemed inevitable.

The infrastructure boom-bust cycle will repeat, as it always does. The next generation of entrepreneurs will see India's infrastructure gaps and mobilize capital to fill them. They'll leverage up, believing this time is different. Most will fail when the cycle turns. But some will survive, scarred but wiser, to participate in the next upturn.

For JPPOWER specifically, the next chapter is being written now. Whether under Adani's ownership or as an independent entity, the company faces critical decisions. Should it double down on thermal despite environmental pressures? Should it pivot to renewables despite lacking expertise? Should it return cash to shareholders or invest for growth? These decisions will determine whether JPPOWER becomes a turnaround success story or merely a survivor.

The lessons for investors are clear but uncomfortable. In infrastructure investing, avoiding the losers matters more than picking the winners. The company with the best projects but worst balance sheet will underperform the company with mediocre projects but manageable debt. Boring survival beats exciting growth when leverage is involved.

India's infrastructure development story is far from over. The country needs $1.4 trillion of infrastructure investment by 2025 to sustain growth. Power generation capacity must double by 2030. The transition to renewable energy requires massive grid investments. These needs create opportunities, but also risks for investors who forget the lessons of the past cycle.

What makes JPPOWER's story relevant isn't its uniqueness but its universality. Around the world, from Chinese real estate developers to European utilities to American shale producers, the same drama plays out: ambition fueled by debt, growth that seems unstoppable until it stops, and the painful deleveraging that follows. The survivors aren't heroes—they're the ones who managed risk when others chased returns.

As we close this analysis, JPPOWER trades at ₹20, having traveled from ₹0.35 to ₹84 and back to ₹20 over fifteen years. For early investors, it's been value destruction. For bottom-fishers who bought at ₹0.35, it's been a 57-bagger. For those buying today, it's a bet on India's power future and corporate India's capacity for resurrection.

The final lesson might be the most important: in infrastructure investing, there are no final lessons. Each cycle brings new challenges, new opportunities, and new ways to lose money. The only constant is that essential infrastructure must be built, operated, and financed. Companies like JPPOWER—flawed, stressed, but operational—will continue to play their part in this eternal drama of development.

Whether JPPOWER represents a cautionary tale or an investment opportunity depends entirely on where you stand in the cycle and what lessons you choose to learn. The infrastructure will keep running regardless, its turbines spinning through bankruptcy and boom, generating the power that keeps the lights on in a billion Indian homes.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube