JK Lakshmi Cement: Building India's Infrastructure Dreams

I. Introduction & Episode Roadmap

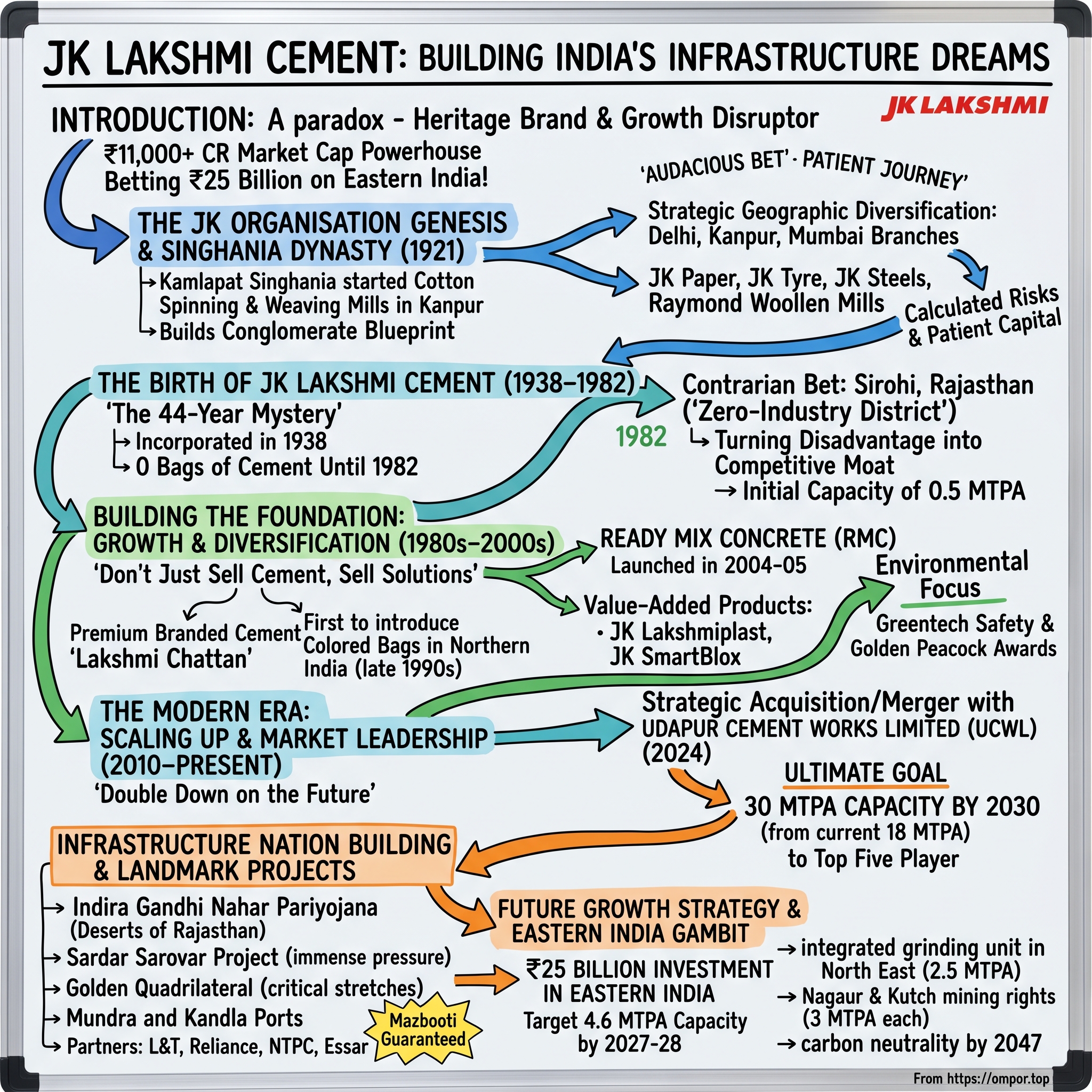

Picture this: The year is 1982. In Sirohi, Rajasthan—a district so remote it's officially classified as "zero-industry"—a grinding mill roars to life for the first time. The locals gather, dust swirling in the desert heat, watching as the first bags of cement roll off the production line. This isn't just another factory opening. This is JK Lakshmi Cement's audacious bet that India's infrastructure revolution would need builders in the most unlikely places.

Fast forward four decades. That remote Rajasthan plant has morphed into a ₹11,000+ crore market cap powerhouse, with tentacles spreading across six states and ambitions to triple capacity by 2030. How did a company that took 44 years from incorporation to production become one of India's most aggressive cement expansionists?

The answer lies in a paradox that defines JK Lakshmi: it's simultaneously a heritage brand carrying the weight of a century-old conglomerate legacy and a growth disruptor making moves that would make venture-backed startups jealous. While peers consolidate and optimize, JK Lakshmi is betting ₹25 billion on Eastern India alone—a region where it barely had presence five years ago.

This is the story of how patience meets ambition, how regional dominance battles national scale, and how a third-generation family business navigates the brutal economics of commoditized infrastructure. We'll journey from the cotton mills of 1920s India through the License Raj maze, into today's infrastructure supercycle where cement isn't just building material—it's nation-building material.

The roadmap ahead takes us through the Singhania dynasty's rise, the peculiar 44-year gestation period, the strategic chess moves of vertical integration, and the high-stakes gambit to become a top-five player by 2030. Along the way, we'll decode what makes this mid-cap David think it can dance with the Goliaths of Indian cement.

II. The JK Organisation Genesis & Singhania Dynasty

The British Raj, 1921. In the bustling markets of Kanpur, a young Marwari businessman named Lala Kamlapat Singhania makes a decision that would echo through a century. Instead of continuing the traditional trading business of his forefathers, he takes every rupee he can muster and pours it into something radical for a Marwari merchant family: manufacturing. The Juggilal Kamlapat Cotton Spinning & Weaving Mills springs to life, named after Kamlapat and his father Seth Juggilal—the "JK" that would become synonymous with Indian industry.

But here's what the official histories don't tell you: Kamlapat wasn't just building a cotton mill. He was architecting a conglomerate blueprint that would outlive empires. While Gandhi was spinning khadi as protest, Kamlapat was spinning cotton as prophecy—betting that independent India would need industrialists, not just traders.

The JK Group's rise from 1950 to 1980 reads like a playbook in diversification done right. By the 1960s, they weren't just making textiles; they were making everything India needed: paper for its bureaucracy, tyres for its vehicles, cement for its buildings. The group became India's third-largest industrial house, trailing only the Tatas and Birlas—a stunning achievement for a family that started with a single cotton mill. The genius wasn't just in diversification—it was in timing. The family expanded into three major branches based out of Kanpur, Mumbai and Delhi, each carving out its own empire. Padampat controlled the Kanpur operations. Kailashpat moved to Mumbai to run Raymond Woollen Mills, acquired from E.D. Sassoon in 1944. Lakshmipat, the youngest, led the acquisition of Aluminium Corporation of India in Asansol in 1942, established JK Steels in West Bengal and a paper mill in Odisha, but labor troubles and nationalization forced the family to move from Kolkata to Delhi in the 1960s.

This three-way split wasn't a breakup—it was strategic geographic diversification before McKinsey consultants had a name for it. Each brother controlled his fiefdom but maintained the JK brand, creating what was essentially India's first multi-city, multi-business conglomerate with unified branding but decentralized operations.

After Lakshmipat, his eldest son Hari Shankar Singhania took over control of the companies, managing the Delhi branch alongside his brothers. The succession planning was meticulous: Hari Shankar helmed JK Paper, JK Tyre, and crucially for our story, JK Lakshmi Cement. His brother Bharat Hari Singhania would later become the current President of JK Organisation and Chairman of JK Lakshmi Cement—a position he holds to this day.

The Singhania story is one of calculated risks and patient capital. While their Marwari peers stuck to trading and money-lending, the Singhanias bet on manufacturing when India barely had factories. They expanded during wars, survived nationalization, navigated the License Raj, and emerged as one of India's most enduring business dynasties. That DNA—part risk-taker, part survivor—would define JK Lakshmi Cement's journey from a file number in 1938 to a cement powerhouse in 2024.

III. The Birth of JK Lakshmi Cement (1938–1982)

Here's a mystery that would baffle any business school case study: How does a company get incorporated in 1938 but not produce a single bag of cement until 1982? The answer reveals everything about doing business in pre-liberalization India and the Singhania family's legendary patience.

JK Lakshmi Cement Limited was incorporated on August 6, 1938, in Rajasthan. But this wasn't a company—it was a placeholder, a corporate shell waiting for its moment. For 44 years, it existed primarily on paper, a testament to the family's belief that someday, somehow, India would need massive amounts of cement. They were playing a game measured not in quarters but in generations.

The real story begins in 1982, in Sirohi—a district so underdeveloped it was officially classified as having zero industries. While competitors rushed to set up plants near major cities, JK Lakshmi made a contrarian bet that would define its strategy for decades: go where others won't, build where others can't, and turn geographic disadvantage into competitive moat.

Why Sirohi? The official narrative talks about limestone deposits and government incentives for backward area development. But dig deeper, and you find strategic brilliance. In a "zero-industry district," you become the largest employer overnight. Local politicians become your champions. Labor issues that plagued urban plants don't exist when you're the only game in town. And those government incentives? They turned marginal economics into profitable ventures. The company began with a modest capacity of 0.5 million tonnes per annum (MTPA)—tiny by today's standards but ambitious for a greenfield project in a backward area during the License Raj. Technology partnerships were crucial: they brought in expertise from Blue Circle Industries (UK) and equipment from Fuller International (USA), ensuring world-class standards from day one.

The early 1980s timing was prescient. India was on the cusp of major infrastructure investments. The Indira Gandhi Nahar Pariyojana was transforming Rajasthan's agricultural landscape. The cement demand was about to explode. And here was JK Lakshmi, perfectly positioned with fresh capacity in a region where competitors had ignored the opportunity.

But the real masterstroke was the company's legal structure evolution. Starting as Straw Products Ltd (the original 1938 entity), it transformed into J.K Corp Limited in February 1995, briefly flirting with multi-product diversification into paper, cement, and even magnetic tape. Finally, on October 6, 2005, it crystallized its identity as JK Lakshmi Cement Limited—a focused cement pure-play ready for the infrastructure boom ahead.

This 44-year journey from incorporation to production wasn't wasted time—it was strategic patience. While waiting, the family learned the cement business through other ventures, built relationships with technology partners, understood market dynamics, and most importantly, waited for the perfect moment when government policies, market demand, and their own capabilities aligned. When they finally struck in 1982, it wasn't a tentative first step but a confident stride into an industry they had studied for decades.

IV. Building the Foundation: Growth & Diversification (1980s–2000s)

The 1990s opened with India liberalizing its economy, and JK Lakshmi was ready with a playbook that would seem obvious in hindsight but was revolutionary at the time: don't just sell cement, sell solutions.

In 1998, while competitors were fighting price wars in the commodity cement market, JK Lakshmi launched something audacious—Lakshmi Chattan, a premium branded cement. This wasn't just new packaging; it was a philosophical shift. In an industry where cement was cement was cement, they dared to ask: what if cement could be aspirational?

The move into colored bags might seem trivial today, but in the late 1990s North Indian cement market, it was revolutionary. JK Lakshmi became the first cement manufacturer in Northern India to introduce colored packaging. Suddenly, construction sites became brand showcases. Contractors started specifying "the cement in the blue bags." Homeowners began asking for cement by brand name, not just grade. The company became the first cement manufacturer in Northern India to introduce colored bags, but the innovation didn't stop at packaging. In 2004-05, they made another contrarian move: launching Ready Mixed Concrete (RMC) from a Gurgaon-based plant under the brand name JK Lakshmi Ready Mix Concrete. While peers saw RMC as a separate business, JK Lakshmi saw it as vertical integration—controlling not just the input (cement) but the final product (concrete) delivered to construction sites.

The company's environmental credentials also emerged during this period. They won the prestigious Greentech Safety Award 2003-04 for Safety and Environment from the Greentech Foundation and the Golden Peacock National Award for Environment Management System from the World Environment Foundation. This wasn't greenwashing—it was strategic positioning for an era where ESG would matter.

By 2005, the transformation was complete. The company shed its multi-product avatar and officially became JK Lakshmi Cement Limited, signaling laser focus on cement and allied products. The timing was perfect—India's infrastructure spending was about to go parabolic, and JK Lakshmi had spent two decades building the capabilities to capture it.

The geographic expansion strategy during this period was textbook market penetration. Instead of competing head-on with giants in saturated markets, they built density in underserved regions. Their network expanded to 70-80 cement dumps and over 2200 dealers spread across Rajasthan, Gujarat, Delhi, Haryana, UP, Punjab, J&K, MP, Mumbai & Pune. Each dealer wasn't just a distribution point but a brand ambassador, trained by JK Lakshmi's technical service cell to provide construction solutions, not just bags of cement.

The introduction of value-added products like JK Lakshmiplast (premium branded Plaster of Paris) and later JK SmartBlox (Autoclaved Aerated Concrete blocks) showed a company thinking beyond commodity cement. Each product launch targeted specific pain points in construction—consistency, quality, ease of use—turning JK Lakshmi from a supplier into a solutions partner.

V. The Modern Era: Scaling Up & Market Leadership (2010–Present)

The drums of war were beating in India's infrastructure sector by 2010. The government was pouring billions into roads, bridges, and urban development. Real estate was booming. And JK Lakshmi, after three decades of patient capacity building, was ready to sprint.

The company had established itself as a prominent player in the Indian cement industry for four decades, boasting an annual turnover exceeding Rs. 6,000 crores. But this wasn't about celebrating past success—it was about doubling down on the future. The most significant strategic move of the modern era was the merger with Udaipur Cement Works Limited (UCWL) and two other subsidiaries approved by the board in 2024. UCWL wasn't just any acquisition—it brought a single integrated plant in Rajasthan with a cement capacity of 4.7 million tonnes and a clinker capacity of 3 million tonnes. This wasn't empire-building for the sake of scale; it was strategic consolidation to create operational synergies and eliminate redundancies.

The merger structure revealed sophisticated financial engineering: shareholders of UCWL received four shares of JK Lakshmi Cement for every 100 shares held in UCWL, while the two other subsidiaries required no new shares as they were already wholly owned. Post-merger, the simplified structure left JK Lakshmi with just two subsidiaries, streamlining governance and operations.

But the real ambition lies ahead. JK Lakshmi Cement has plans to increase its production capacity to 30 million tonnes per annum (MTPA) by 2030, up from the current 18 MTPA. This isn't incremental growth—it's a moonshot to become one of India's top five cement producers.

The value-added products strategy accelerated during this period. Ready Mix Concrete (RMC) operations expanded from a single Gurgaon plant to multiple facilities across North and West India. AAC blocks, wall putty, and other construction solutions transformed JK Lakshmi from a cement supplier to a construction solutions provider. Each product addressed specific pain points: RMC solved quality consistency issues at construction sites, AAC blocks offered lightweight alternatives for modern construction, and wall putty provided finishing solutions.

Digital transformation initiatives, though less visible, were equally important. The company invested in operational excellence programs, supply chain optimization, and customer engagement platforms. The technical service cell evolved from providing basic support to offering comprehensive construction consultancy, helping architects and builders optimize cement usage and improve structure quality.

The leadership transition during this period was seamless yet significant. Bharat Hari Singhania, born 1939 and son of Lakshmipat Singhania, serves as current President of JK Organisation and Chairman & MD of JK Lakshmi Cement, providing continuity while bringing fresh perspectives on growth and expansion.

VI. Infrastructure Nation Building & Landmark Projects

In the annals of Indian infrastructure, certain projects stand as monuments to national ambition. Behind many of these monuments, literally holding them together, is JK Lakshmi Cement. The company's tagline "Mazbooti Guaranteed" (Strength Guaranteed) isn't just marketing—it's a promise validated by some of India's most critical infrastructure projects.

Take the Indira Gandhi Nahar Pariyojana—one of the largest irrigation projects in the world, bringing water to the deserts of Rajasthan. When engineers needed cement that could withstand extreme temperature variations and saline conditions, JK Lakshmi delivered. The Sardar Sarovar Project, controversial yet transformative, required cement that could handle immense water pressure and seismic activity. Again, JK Lakshmi was there.

The Golden Quadrilateral—India's highway modernization marvel connecting Delhi, Mumbai, Chennai, and Kolkata—used JK Lakshmi cement for critical stretches. When you drive on these highways at 100 kmph, you're trusting concrete mixed with JK Lakshmi cement to hold firm under millions of vehicle passes.JK Lakshmi Cement is the strength behind structures that India is proud of—Indra Gandhi Nahar Pariyojana, Sardar Sarovar Project, Golden Quadrilateral, Mundra and Kandla Port stands to name a few. It partners India's leading corporations such as L&T, Reliance, NTPC and Essar to create the new India's success story.

From government organisations like Airport Authority of India to infrastructure and real estate giants like Larsen & Toubro, it is our customer's trust in us that makes a preferred premium cement brand in India.

Mundra and Kandla ports—critical nodes in India's maritime trade—used JK Lakshmi cement for their expansion. These aren't just construction projects; they're nation-building exercises where failure isn't an option and quality isn't negotiable.

The partnerships with infrastructure giants like L&T, Reliance, NTPC, and Essar weren't transactional relationships but strategic alliances. When L&T won mega contracts from NTPC for thermal power plants, JK Lakshmi was often the cement partner of choice. When Reliance built its petrochemical complexes, JK Lakshmi's technical service cell worked alongside their engineers to optimize concrete mixes for chemical resistance.

The technical service cell became JK Lakshmi's secret weapon in winning these marquee projects. Unlike competitors who sold cement and disappeared, JK Lakshmi embedded their engineers at project sites, solving problems in real-time. When a contractor faced challenges with concrete setting in extreme temperatures, JK Lakshmi's team was there with solutions. When architects needed special finishes, the technical team developed custom formulations.

This approach transformed JK Lakshmi from vendor to partner. Project managers began specifying JK Lakshmi not just for quality but for the expertise that came with it. The company's involvement in these landmark projects created a virtuous cycle: prestigious projects enhanced brand credibility, which attracted more prestigious projects.

The customer engagement model extended beyond mega projects to individual house builders (IHBs). Regular training programs for masons, architects' meets, and contractor engagement initiatives created a ecosystem where JK Lakshmi wasn't just selling cement but building capability across the construction value chain. Every mason trained became a brand ambassador; every architect educated became a specifier.

VII. Competitive Dynamics & Market Position

The Indian cement industry is a brutal arena where scale matters, costs kill, and regional dynamics can make or break companies. With a market cap of ₹11,324 crore (up 14.8% in one year), revenue of ₹6,370 crore, and profit of ₹366 crore, JK Lakshmi occupies a unique position—too big to be ignored, too small to dominate nationally, but perfectly sized to be nimble. The Indian cement market is led by UltraTech Cement with a 28% market share and consolidated capacity of 152.7 MTPA. Adani Group's cement entities (Ambuja and ACC) hold the second position with 77.4 MTPA combined capacity. In this landscape of giants, JK Lakshmi's position is fascinating—with 18 MTPA current capacity, it's neither a national champion nor a regional minnow.

The stock is trading at 3.27 times its book value—a premium to book but a discount to peers like UltraTech (trading at 5.12 times). This valuation gap reveals market perception: JK Lakshmi is quality but not quite blue-chip, growth-oriented but not hypergrowth.

The company has delivered a poor sales growth of 7.25% over the past five years and has a return on equity of 12.4% over the last three years—numbers that would concern growth investors but might attract value hunters. The promoter holding of 46.3% signals skin in the game without being so high as to concern minority shareholders about governance.

JK Lakshmi's competitive moats are subtle but real. The JK brand carries eight decades of trust—invaluable in a market where contractors and builders are risk-averse. Their dealer relationships, built over generations, create switching costs that pure economics can't capture. Location advantages in Rajasthan and Gujarat, where they hold mining rights, provide raw material security that new entrants can't replicate.

The mid-cap advantage in a consolidating industry is counterintuitive but real. While UltraTech and Adani duke it out for national dominance, burning capital on mega acquisitions, JK Lakshmi can cherry-pick regional opportunities. They're too big to be acquisition targets (without a massive premium) but small enough to grow without moving markets.

ESG initiatives have become a differentiator. The company's focus on renewable energy, water conservation, and community development isn't just corporate responsibility—it's strategic positioning for an era where environmental compliance will separate winners from losers. Their sustainable mining practices and efforts to reduce carbon emissions position them well for future carbon taxes and environmental regulations.

The regional versus national player debate is central to understanding JK Lakshmi's strategy. Unlike peers chasing pan-India presence, JK Lakshmi has chosen density over spread. In their core markets of North and West India, they often have higher market share than national players. This regional dominance creates pricing power and logistics advantages that offset the lack of national scale.

VIII. Eastern India Gambit & Future Growth Strategy

The year 2024 will be remembered as when JK Lakshmi stopped playing defense and went on offense. The announcement to invest ₹25 billion in Eastern India isn't just capacity expansion—it's a declaration of intent to reshape India's cement geography.

Eastern India has always been cement's final frontier. Rich in limestone but poor in organized players, dominated by small regional manufacturers but underserved by quality brands. JK Lakshmi's eastern gambit involves both brownfield and greenfield projects that will increase the region's capacity to 4.6 MTPA by 2027-28.The company is targeting to become the fifth largest cement maker in the country with an installed capacity of 30 MTPA by FY30. This requires nearly doubling capacity in six years—aggressive by any standard but calculated in execution.

The expansion blueprint is multi-pronged: 4.6 MTPA capacity will be added in the East by FY27-FY28, leveraging both brownfield expansions at existing facilities and greenfield projects in virgin territories. The company has acquired mining lease rights in Nagaur, Rajasthan and Kutch, Gujarat where it plans to add 3 MTPA capacity each. Plans include setting up an integrated grinding unit in the North East with about 2.5 MTPA capacity and adding a third line in the Udaipur Cement Works plant by FY29-FY30.

The recent signing of an MoU with the Government of Assam for a ₹110 billion greenfield cement production project reveals the scale of ambition. This project, to be developed over 7-8 years, isn't just about cement production—it's about positioning JK Lakshmi as a key player in the Northeast's industrialization story.

Adjacent business expansion forms another pillar of the growth strategy. The company is working to increase revenue from concrete solutions and ready-mix business, aiming for 10% contribution from these areas in the next 3-4 years. This isn't diversification for its own sake but vertical integration to capture more value per ton of cement sold.

Renewable energy investments are becoming a competitive necessity. With power costs constituting 25-30% of cement production costs, the push toward renewable energy isn't just about ESG credentials—it's about cost optimization. The company's commitment to carbon neutrality by 2047 might seem distant, but the investments being made today in waste heat recovery, solar power, and alternative fuels will determine competitiveness in the 2030s.

The geographic expansion strategy reveals sophisticated thinking. Instead of competing in oversupplied markets, JK Lakshmi is targeting regions where demand-supply dynamics favor new entrants. Eastern India, with its infrastructure deficit and government focus on development, offers better pricing power than the hyper-competitive western and southern markets.

IX. Playbook: Business & Investing Lessons

JK Lakshmi Cement's journey offers a masterclass in navigating commodity businesses with patient capital and strategic thinking. The lessons extend far beyond cement, offering insights for any business operating in capital-intensive, cyclical industries.

Family Conglomerate Advantages and Challenges: The JK Organisation structure provides JK Lakshmi with advantages rarely discussed in business schools. Access to patient capital means they can wait 44 years from incorporation to production. Cross-holdings and group companies provide financial flexibility during downturns. Shared corporate services reduce overhead costs. But it also brings challenges: succession planning complexities, potential for family disputes, and the constant balancing act between group interests and company interests.

Patient Capital in Commodity Businesses: In industries where others measure success quarterly, JK Lakshmi measures in decades. Their willingness to hold mining leases for years before developing them, to build capacity ahead of demand, and to invest in markets before they mature exemplifies the power of patient capital. This isn't just about having deep pockets—it's about having the conviction to deploy capital when others are retreating.

Regional Dominance vs Pan-India Presence: JK Lakshmi's strategy challenges the conventional wisdom that bigger is always better. By choosing regional density over national spread, they achieve logistics advantages, brand recognition, and market share that national players struggle to match in these regions. The lesson: in commodity businesses, being #1 in five states might be better than being #5 nationally.

Managing Cyclicality: Cement is brutally cyclical—boom periods of capacity shortage followed by bust periods of oversupply. JK Lakshmi's playbook involves counter-cyclical investments (expanding during downturns when costs are low), maintaining a strong balance sheet to survive downturns, and using downturns to gain market share from weaker players. The discipline to not overpay for acquisitions during boom times has preserved capital for organic growth.

Brand Building in B2B2C Markets: Cement is unique—sold to dealers (B2B) but the brand matters to end consumers (B2C). JK Lakshmi's approach of building brand equity through technical service, mason training, and architect engagement creates pull demand that transcends traditional B2B relationships. The colored bags innovation wasn't about aesthetics—it was about making the brand visible at every construction site.

Backward Integration and Mining Rights: In cement, those who control limestone control destiny. JK Lakshmi's focus on securing mining rights, even in areas where they don't have immediate production plans, is strategic optionality. These rights become more valuable over time as environmental regulations make new mining leases nearly impossible to obtain.

X. Bear vs Bull Case & Valuation

The investment case for JK Lakshmi Cement presents a classic mid-cap dilemma: significant upside potential balanced against execution risks and competitive pressures.

Bull Case:

India's infrastructure spending trajectory appears unstoppable. With the government committing unprecedented capital to roads, railways, airports, and urban infrastructure, cement demand could surprise on the upside. JK Lakshmi, with its strategic capacity additions and eastern expansion, is perfectly positioned to capture this growth.

The consolidation thesis is compelling. As the industry consolidates, mid-sized players like JK Lakshmi become increasingly valuable. They're large enough to have economies of scale but small enough to be acquisition targets at significant premiums. Even if they remain independent, industry consolidation improves pricing dynamics for all players.

Eastern expansion opens new growth markets precisely when traditional markets are becoming saturated. Being an early mover in underserved regions provides first-mover advantages that could translate into sustained market share leadership.

The company's strong balance sheet enables opportunistic acquisitions. In an industry where distressed assets regularly come to market, having the financial flexibility to acquire assets at attractive valuations could accelerate growth beyond organic expansion plans.

ESG leadership in the cement sector is becoming a differentiator. As carbon taxes and environmental regulations tighten, companies with better ESG credentials will enjoy cost advantages and preferential access to capital.

Bear Case:

The company has delivered poor sales growth of 7.25% over the past five years and has a return on equity of 12.4% over the last three years—metrics that suggest execution challenges or structural headwinds.

Competition from larger players with deeper pockets intensifies every year. UltraTech and Adani aren't just adding capacity; they're adding multiples of JK Lakshmi's entire capacity every few years. In a commodity business, scale increasingly determines success.

Regional concentration risks remain significant. Despite expansion plans, JK Lakshmi remains heavily dependent on North and West India. Any regional economic slowdown or oversupply situation could disproportionately impact performance.

Input cost pressures and energy transition costs could squeeze margins. The shift to renewable energy, while necessary, requires significant upfront investment that might not yield returns for years.

Execution risks on aggressive expansion plans are real. Doubling capacity requires flawless execution across multiple projects simultaneously. Any delays, cost overruns, or demand disappointments could impact returns significantly.

Valuation Perspective:

Trading at 3.27 times book value, JK Lakshmi appears reasonably valued relative to its own history but at a discount to peers. This valuation gap could represent opportunity or risk, depending on execution of growth plans.

The market seems to be pricing in execution risk and competitive pressures but not giving full credit for the eastern expansion opportunity and consolidation optionality. For patient investors willing to wait for the 2030 vision to materialize, current valuations might represent an entry point. For those concerned about near-term headwinds and execution risks, waiting for proof of execution might be prudent.

XI. Epilogue: "If We Were CEOs"

Standing at the helm of JK Lakshmi Cement in 2024, the strategic choices ahead would define not just the next quarter but the next quarter-century.

National vs Regional Strategy: The temptation to go national would be strong, but the math favors regional dominance. We would double down on becoming the undisputed leader in North, West, and East India before considering southern expansion. Better to be the regional champion than a national also-ran.

M&A Opportunities: In a consolidating market, we would be selective acquirers, not aggressive consolidators. Focus on distressed assets in our core regions that can be acquired at replacement cost or below. Avoid bidding wars for trophy assets that destroy shareholder value.

Technology Investments: The future of cement isn't just about capacity but efficiency. Investing in AI-driven demand forecasting, IoT-enabled plant optimization, and blockchain for supply chain transparency could provide competitive advantages that scale can't match.

Green Cement Initiatives: Carbon-negative cement isn't science fiction—it's the future. We would establish a dedicated R&D division focused on alternative binders, carbon capture technologies, and circular economy initiatives. Being first to market with truly green cement could command premium pricing that transforms economics.

Capital Allocation: The balance between growth and dividends would tilt toward growth until 2030. Once the 30 MTPA target is achieved, shift toward returning capital to shareholders while maintaining flexibility for opportunistic investments.

Next Generation Leadership: The fourth generation of the Singhania family needs to be prepared not just to run a cement company but to lead a construction solutions enterprise. Rotation through operations, technology, and sustainability roles would build well-rounded leaders for an industry in transformation.

The path ahead for JK Lakshmi Cement is neither easy nor certain. But for a company that waited 44 years to produce its first bag of cement and then built a ₹11,000+ crore enterprise, patience and persistence are encoded in its DNA. The next chapter of this story is being written today in the grinding mills of Sirohi, the boardrooms of Delhi, and the construction sites across India where JK Lakshmi cement is literally building the nation's future, one bag at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube