Indraprastha Gas Limited: How a Supreme Court Verdict Built India's CNG Empire

I. Introduction & Opening Hook

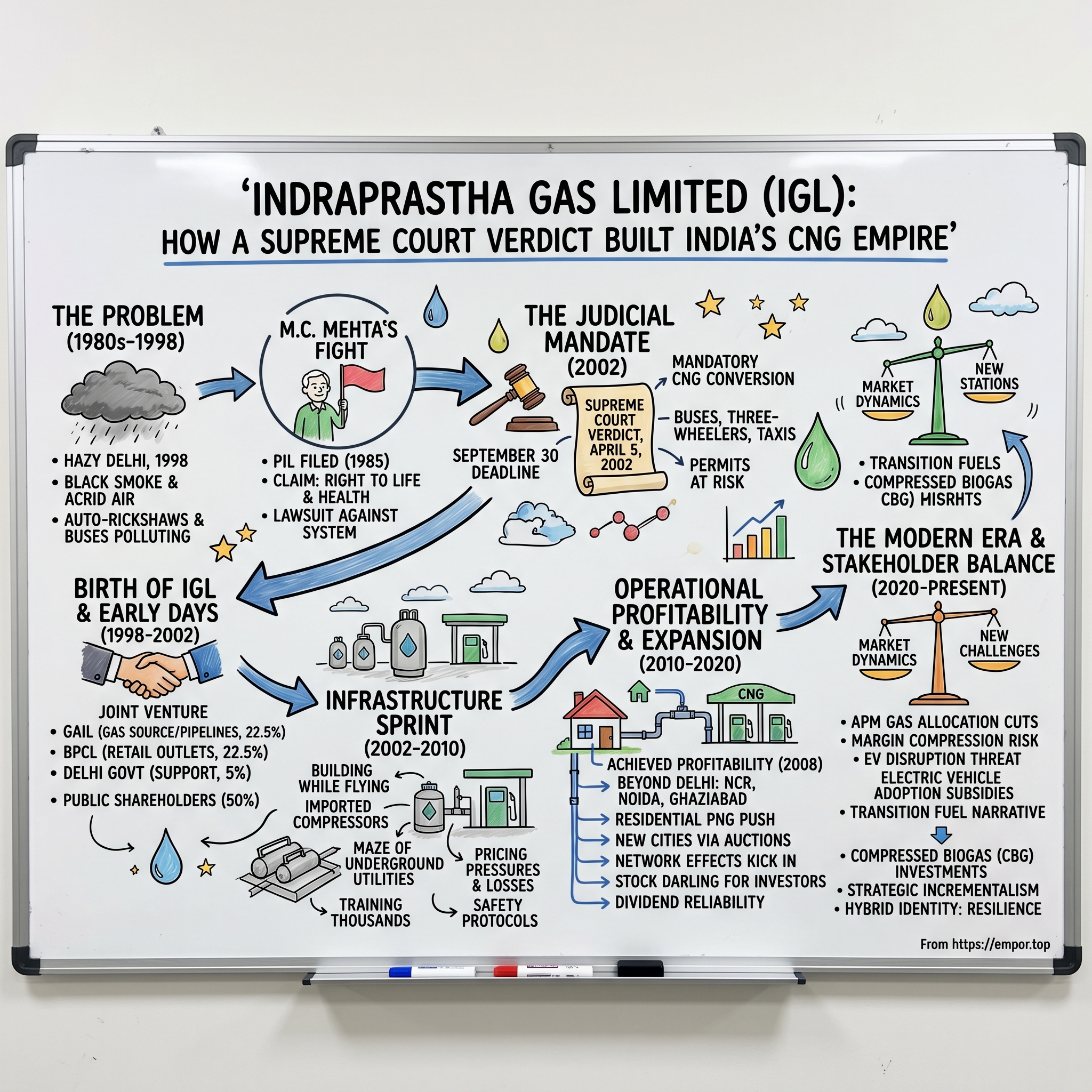

Picture this: It's a hazy morning in Delhi, circa 1998. The air is thick enough to taste—metallic, acrid, the kind that makes your eyes water before you've even stepped outside. In the streets below, auto-rickshaws belch black smoke while buses lumber through intersections, each one a mobile chimney adding to the grey shroud that has become Delhi's signature. The city's air quality index regularly hits "hazardous," though most residents don't need a number to tell them what their burning lungs already know.

Now fast-forward to today. Those same streets hum with the distinctive whir of CNG-powered vehicles—cleaner, quieter, their exhaust barely visible. Behind this transformation sits a company that shouldn't exist, at least not according to free-market orthodoxy. Indraprastha Gas Limited, or IGL, is a ₹28,763 crore behemoth that dominates Delhi's gas distribution landscape with 819 CNG stations and 25.60 lakh residential connections. It's a profit machine that generated ₹15,318 crore in revenue last year, boasts near-zero debt, and pays dividends like clockwork.

But here's the twist that would make any business school professor squirm: IGL exists because nine judges in black robes decided it should. Not venture capitalists, not market demand, not entrepreneurial vision—but the Supreme Court of India, wielding its gavel like a magic wand to conjure an entire industry out of thin air.

This is the paradox at the heart of our story today. How does a government-created monopoly, born from judicial activism rather than market forces, become one of India's most reliable dividend aristocrats? How does a company with captive demand—literally mandated by law—navigate the delicate balance between public service and profit maximization? And perhaps most intriguingly, what happens when the very foundation of your business model is a court order that could, theoretically, be reversed?

The IGL story reads like a business school case study written by Kafka. It's a tale where environmental lawyers become inadvertent venture capitalists, where Supreme Court justices act as product managers, and where a pollution crisis becomes the foundation for a four-billion-dollar enterprise. It challenges everything we think we know about how successful businesses are built—no founder's garage, no Silicon Valley pitch decks, no disruption narrative. Just black-robed justices, choking citizens, and a bet that you could build a profitable business by government decree.

Over the next several hours, we're going to unpack this unlikely empire. We'll trace IGL's journey from a desperate response to an environmental catastrophe to its current status as a quasi-monopolistic cash cow. We'll explore how it built infrastructure for a fuel nobody wanted, created demand through legal mandate, and then somehow transformed that forced adoption into genuine market acceptance. We'll examine the delicate dance between being a public utility and a publicly-traded company, between serving citizens and serving shareholders.

This isn't just a story about natural gas or clean air or even Indian bureaucracy. It's about what happens when traditional market mechanisms fail so spectacularly that the judiciary steps in to play entrepreneur. It's about building a business not on product-market fit but on court-market fit. And it's about the unexpected ways that environmental mandates can create durable competitive moats.

So buckle up. We're about to dive into one of the most unusual business origin stories you'll ever hear—where the founding document wasn't a business plan but a Supreme Court verdict, where the initial customers weren't early adopters but legally compelled users, and where the path to profitability ran straight through the halls of justice.

II. The Pre-History: Delhi's Pollution Apocalypse (1980s-1998)

The year is 1985, and M.C. Mehta is standing at a traffic intersection in Connaught Place, Delhi's commercial heart. A successful environmental lawyer, Mehta watches as a Delhi Transport Corporation bus rumbles past, leaving behind a cloud of black smoke so thick it momentarily obscures the colonial-era buildings across the street. He covers his nose with his handkerchief—a futile gesture that has become as routine as checking his watch. But today, something snaps. This isn't just an inconvenience anymore; it's an assault on human dignity, a slow-motion catastrophe unfolding in plain sight.

Mehta heads straight to his office and begins drafting what will become one of India's most consequential Public Interest Litigations. His target isn't a company or even a government department—it's an entire system that has allowed Delhi to transform from the garden city envisioned by Edwin Lutyens into what environmental scientists are calling a "gas chamber."

The numbers tell a story of breathtaking negligence. At independence in 1947, Delhi's population stood at roughly 5 lakh. By the 1990s, it had exploded to 96 lakh—a nineteen-fold increase that no amount of urban planning could have anticipated. But it wasn't just the human population that was exploding. The vehicular population had hit 13.5 lakh by 1990, with each vehicle a tiny factory producing its own toxic cocktail of pollutants. By the mid-1990s, an estimated 1,385 excess deaths and 51,400 life years were being lost annually for every 100 μg/m³ increase in total suspended particulate matter concentrations. The human cost was staggering, yet it remained largely invisible—dispersed across hospitals, hidden in statistics, buried under the din of economic growth.

But Mehta's PIL wasn't just another lawsuit. It was a declaration of war against the status quo, filed under Article 32 of the Constitution, which guarantees the right to life. His argument was elegantly simple: if the Constitution promises life, and pollution kills, then the state has a constitutional obligation to act. The case, officially titled M.C. Mehta vs. Union of India, would drag on for over a decade, spawning multiple orders, creating committees, and ultimately birthing an entire industry.

The regulatory landscape—or rather, the absence of one—was the perfect breeding ground for this crisis. India's environmental laws were a patchwork of good intentions and weak enforcement. The Central Pollution Control Board existed, yes, but it was like a traffic cop without a whistle in a city without traffic lights. Industries self-reported their emissions (when they bothered to report at all), vehicle emission standards were suggestions rather than requirements, and the penalty for violations was often cheaper than compliance.

Market forces, that great invisible hand that economists love to invoke, were utterly impotent here. The tragedy of the commons was playing out in real-time: each individual actor—whether a bus operator, factory owner, or auto-rickshaw driver—had every incentive to pollute and no incentive to stop. Clean technology cost money; black smoke cost nothing. The social cost of pollution was enormous but completely externalized. No market mechanism existed to price in the health costs, the lost productivity, the shortened lives.

Consider the economics of a typical Delhi bus operator in 1995. A diesel bus cost roughly ₹8 lakh. Running it on the cheapest, dirtiest diesel available saved maybe ₹20,000 per year in fuel costs. Installing pollution control equipment? That would cost ₹50,000 upfront with ongoing maintenance expenses. The math was simple: pollute and profit, or go clean and go broke. Multiply this calculation by thousands of vehicles, add in industries with similar incentives, and you had a formula for atmospheric apocalypse.

The government's response through the early 1990s was a masterclass in bureaucratic hand-wringing. Committees were formed, reports were written, targets were set and missed. The Delhi Administration would announce odd-even schemes that never materialized, promise to phase out old vehicles without providing alternatives, and issue stern warnings that nobody took seriously. It was governance by press release—all talk, no action.

Meanwhile, the city's growth continued its inexorable march. Every day, roughly 500 new vehicles hit Delhi's roads. The ring of unauthorized colonies around the city expanded, each one adding its share of construction dust, garbage burning, and vehicular emissions to the toxic mix. The Yamuna River, once Delhi's lifeline, had become a sewage canal, its methane emissions adding another layer to the city's pollution burden.

International comparisons were damning. While Los Angeles had cleaned up its infamous smog through stringent regulations and London had long since banished its "pea soupers," Delhi seemed to be racing backward, recreating the worst of 19th-century industrial pollution with 20th-century intensity. The city that was supposed to showcase India's emergence as a modern nation was instead becoming a cautionary tale about development without planning.

By 1997, the situation had reached a breaking point. Winter inversions trapped pollutants like a lid on a pot, creating conditions where visibility dropped to mere meters. Hospitals reported a 40% increase in respiratory admissions during winter months. Children were developing asthma at rates that would have been unthinkable a generation earlier. The city's birds were disappearing—the house sparrow, once ubiquitous, was becoming rare, a canary in this urban coal mine.

It was into this chaos that a new player would emerge—not a company or entrepreneur, but an idea backed by judicial force. The stage was set for one of the most unusual corporate origin stories in business history: a company created not to meet market demand but to create it, not to serve customers but to serve a court order, not to maximize profits but to minimize pollution. The answer to Delhi's pollution crisis wouldn't come from the market or even from the government's executive branch. It would come from nine judges in black robes who decided that if nobody else would act, they would.

III. Birth of IGL: The Joint Venture Genesis (1998-2002)

The boardroom at GAIL Bhawan in New Delhi had seen many negotiations, but nothing quite like the meeting on December 23, 1998. Around the polished teakwood table sat an unlikely collection of executives: bureaucrats from the Delhi government, petroleum engineers from Bharat Petroleum Corporation Limited (BPCL), and gas pipeline specialists from Gas Authority of India Limited (GAIL). They weren't there to discuss profits or market share. They were there to create a company for a market that didn't exist, to serve customers who didn't want their product, using infrastructure that hadn't been built.

The formation of Indraprastha Gas Limited was less a business decision and more an act of institutional desperation. GAIL had been struggling with the Delhi City Gas Distribution Project since 1992—a well-intentioned but poorly executed attempt to bring piped natural gas to India's capital. Six years and countless crores later, they had little to show for it: a handful of industrial connections, some incomplete pipelines, and mounting losses that were becoming difficult to justify to their board.

"We need fresh blood," GAIL's chairman had reportedly said in an internal meeting. "And more importantly, we need partners who can share the risk." The solution was elegant in its simplicity: create a joint venture that would pool resources, spread risk, and bring together complementary capabilities. GAIL would contribute its gas sourcing and pipeline expertise (and transfer its struggling Delhi project), BPCL would provide retail outlets that could be converted to CNG stations, and the Delhi government would offer political cover and regulatory support.

The equity structure revealed the delicate balance of power: GAIL and BPCL each took 22.5%, making them equal partners without giving either outright control. The Government of NCT Delhi took 5%—enough to have a seat at the table but not enough to dominate decisions. The remaining 50% was left for public shareholders, though at the time, finding investors for a company with no clear business model was about as easy as finding clean air in Chandni Chowk.

The initial mandate was breathtakingly vague: "To supply compressed natural gas to the transport sector and piped natural gas to domestic, commercial, and industrial sectors in the National Capital Territory of Delhi." In any business school case study, this would be flagged immediately as a recipe for disaster. No market research showing demand. No clear revenue model. No competitive advantage. Just a belief—or hope—that if you built it, they would come.

Except they wouldn't come. Not voluntarily, anyway.

The early challenges read like a startup nightmare. First, there was the infrastructure problem. Delhi's underground was a maze of water pipes, electrical cables, telephone lines, and sewage systems—most of them unmapped, many of them unauthorized. Laying gas pipelines meant navigating this subterranean chaos while trying not to disrupt the city above. Every kilometer of pipeline required permissions from multiple agencies, each with its own bureaucratic process, its own timeline, its own palm to grease.

Then there was the customer problem. CNG as a vehicular fuel was virtually unknown in India. Bus operators looked at IGL executives like they were selling snake oil. "Why should we spend lakhs converting our fleet for a fuel that costs almost the same as diesel?" they would ask. The answer—"because it's cleaner"—was met with skeptical laughter. Clean air didn't pay for new engines.

The economics were brutal. Setting up a single CNG station cost approximately ₹1.5 crore. IGL needed hundreds of them. Each station needed compressors (imported from Italy or America at substantial cost), dispensers, safety equipment, and trained staff. The company was burning through cash to build infrastructure for a product nobody wanted to buy.

The synergy between parent companies, touted in press releases, proved more complex in practice. GAIL was a monopoly accustomed to dealing with large industrial customers who had no choice but to buy their gas. BPCL was used to the retail petroleum business where customers came to you. Neither had experience with the hybrid challenge IGL faced: building infrastructure like a utility while trying to acquire customers like a retail business.

Internal tensions emerged quickly. GAIL representatives pushed for focusing on industrial customers—safer, more predictable, better margins. BPCL wanted to leverage their retail network but was wary of cannibalizing their petroleum business. The Delhi government representatives, meanwhile, kept reminding everyone about air pollution and public health, concerns that seemed quaint in business discussions about ROI and payback periods.

By mid-2000, IGL had spent over ₹100 crore and had little to show for it. They had 9 CNG stations (in a city with over 13 lakh vehicles), a few dozen converted vehicles (mostly government fleet vehicles converted for demonstration purposes), and a growing sense that perhaps this whole enterprise was doomed.

Board meetings became exercises in managed pessimism. The 2001 annual report, written in the bureaucratic prose that tries to make disaster sound like opportunity, noted "challenges in market development" and "infrastructure creation proceeding as per revised timelines." Translation: nobody was buying what they were selling, and everything was behind schedule.

The company's first CEO, a GAIL veteran named S.K. Gupta, tried to maintain morale with town halls that emphasized the "long-term vision" and "first-mover advantage." But privately, executives were updating their resumes. Who wanted to be associated with what looked increasingly like a very expensive, very public failure?

Yet something was stirring in the background. The Supreme Court, which had been hearing M.C. Mehta's PIL for years, was losing patience with the government's half-measures. Committees had been formed—the Bhure Lal Committee, the Environment Pollution (Prevention & Control) Authority—and their recommendations were gathering dust. The court was moving toward something unprecedented: not just ordering the government to act, but specifying exactly what that action should be.

IGL's executives didn't know it yet, but they were about to win the lottery—not through luck or skill, but through judicial decree. The company built for a market that didn't exist was about to have that market handed to them on a silver platter. Or rather, a Supreme Court order.

IV. The Supreme Court Bombshell: Creating a Market by Decree (2002)

April 5, 2002. The Supreme Court of India, Court Room No. 2. As Chief Justice B.N. Kirpal read out the verdict, lawyers packed into the courtroom exchanged glances of disbelief. The court wasn't just interpreting law; it was rewriting the rules of an entire industry.

"All public transport vehicles plying in Delhi, including buses, three-wheelers, and taxis, shall convert to CNG by September 30, 2002," the Chief Justice intoned. "Failure to comply will result in cancellation of permits."

The silence that followed was deafening. Then the courtroom erupted. Transport union lawyers jumped to their feet, shouting about impossibility and economic ruin. Government counsels looked stunned—they had expected guidelines, perhaps targets, not this sledgehammer of a mandate. In the corner, IGL's legal observer was frantically texting his CEO: "You need to see this. Everything has changed."

The verdict was the culmination of a four-year battle that had seen the Supreme Court transform from adjudicator to administrator. The Bhure Lal Committee, headed by the former Central Vigilance Commissioner, had submitted report after report documenting Delhi's air quality crisis. The committee didn't mince words: Delhi was dying, and diesel vehicles were the primary killers.

What made the court's intervention remarkable wasn't just its specificity but its scope. The judges had essentially decided that when the executive fails to execute and the legislature fails to legislate, the judiciary must step in. They weren't just interpreting Article 21 (Right to Life); they were operationalizing it, turning constitutional principle into street-level policy.

The July 1998 order had actually laid the groundwork, though few recognized it at the time. In that order, the court had directed that 16.1 lakh kg per day (2 mmscmd) of CNG supply be ensured by June 2002. This wasn't a random number—it was based on calculations of what would be needed if Delhi's entire public transport fleet converted to CNG. The court had been playing chess while everyone else was playing checkers.

The resistance from transport operators was immediate and fierce. The Delhi Transport Corporation (DTC) claimed it would need ₹800 crore for fleet conversion. Private bus operators, operating on thin margins, said the conversion cost of ₹2-3 lakh per bus would bankrupt them. Auto-rickshaw unions announced indefinite strikes. Taxi associations filed review petitions. The international context was damning. South Korea had actively pursued CNG bus policies from 2000 to improve air quality, converting their fleet ahead of the 2002 World Cup with substantial government support. Meanwhile, Delhi was choking on its own exhaust. The Supreme Court took note of these global precedents, particularly how other nations had successfully implemented alternative fuel programs for major international events.

But the transport operators' most potent argument was timing. Converting thousands of vehicles in mere months? Impossible, they said. The infrastructure didn't exist. The technology wasn't proven in Indian conditions. The supply chain couldn't handle it.

Yet IGL's executives, watching from the sidelines, knew this was their moment. The company had been bleeding money, building infrastructure for a non-existent market. Now, suddenly, the highest court in the land was about to create that market by judicial fiat. It was unprecedented—a business model built not on innovation or consumer demand but on legal compulsion.

The verdict's language was uncompromising. It wasn't a suggestion or a guideline. It was an order, enforceable by contempt of court. Any vehicle that didn't comply would lose its permit. In a city where commercial vehicles were the lifeblood of millions of livelihoods, this was the nuclear option.

For IGL, the Supreme Court had just turned their white elephant into a golden goose. The company that had been preparing for a market that might never come was suddenly the only game in town. Every bus, every auto-rickshaw, every taxi would need their product. It wasn't product-market fit in any traditional sense—it was court-mandated market fit, and IGL held all the cards.

V. The Infrastructure Sprint: Building While Flying (2002-2010)

The scene at IGL's headquarters on the morning of April 6, 2002, was controlled chaos. Engineers huddled over city maps, marking potential CNG station locations with colored pins. Finance teams frantically recalculated cash flow projections. Operations managers fielded calls from panicked transport operators. The Supreme Court had given them less than six months to transform Delhi's entire public transport fuel infrastructure. It was like being asked to change the engines on a plane while it was still flying.

"We need 200 stations operational by September," the operations head announced in an emergency meeting. "We currently have 9."

The math was staggering. They needed to build roughly one new CNG station every day for the next six months. Each station required land acquisition, safety clearances, equipment installation, and staff training. In a city where getting a simple building permit could take months, IGL had to navigate the bureaucratic maze at warp speed.

The first challenge was physics. Natural gas, unlike liquid petroleum, needs to be compressed to 200 times atmospheric pressure to be viable as a vehicle fuel. This requires sophisticated compression equipment, mostly imported from Italy and the United States. The global supply chain wasn't prepared for Delhi's sudden demand. IGL executives found themselves on red-eye flights to Rome and Houston, negotiating with equipment manufacturers who couldn't believe their order volumes.

Then there was the pipeline problem. CNG stations need to be connected to gas pipelines, but Delhi's underground was already a chaotic tangle of utilities. Every excavation risked hitting a water main, electrical cable, or sewage line. The company developed a new protocol: "probe, pray, and proceed." Teams would carefully excavate test pits every few meters, mapping the underground maze inch by inch.

The human dimension was equally complex. IGL needed to train thousands of people—station operators, safety inspectors, maintenance crews—in a technology that was virtually unknown in India. They flew in experts from Argentina and Brazil, countries that had pioneered CNG adoption, to conduct crash courses. These experts were bemused by the scale of Delhi's ambition. "In Buenos Aires, we took ten years to do what you're trying to do in six months," one Argentine engineer remarked.

The economics revealed the paradox at the heart of IGL's business model. Industries were paying just ₹3.55 per kg for CNG, while commercial vehicles were charged ₹13.11 per kg—a pricing structure that reflected political realities more than market dynamics. Industrial users had lobbying power; auto-rickshaw drivers didn't. This cross-subsidization would become a defining feature of IGL's financial architecture.

Meanwhile, the conversion of vehicles was its own odyssey. A typical diesel bus engine couldn't simply be modified for CNG—it needed complete replacement. Each conversion cost between ₹2-3 lakh, a fortune for operators already running on thin margins. The government announced subsidies, but the paperwork was Byzantine. Bus operators would queue for hours at government offices, only to be told they were missing some obscure form.

The auto-rickshaw segment presented unique challenges. These three-wheelers, the workhorses of Delhi's last-mile connectivity, were often decades old, held together by wire and prayer. Converting them to CNG was like performing heart surgery on a patient who was already on life support. Many simply couldn't survive the procedure. IGL found itself not just as a fuel supplier but as an inadvertent catalyst for fleet modernization.

International comparisons provided both inspiration and sobering reality checks. Beijing had deployed 800 hydrogen fuel cell buses for the 2022 Winter Olympics, but that was with years of planning and unlimited government resources. Delhi was attempting something similar with a fraction of the time and budget, driven not by Olympic glory but by judicial decree.

The early months were marked by spectacular failures. Newly opened stations would run out of gas during peak hours, leaving hundreds of vehicles stranded. Compression equipment, not designed for Delhi's dust and heat, would break down regularly. One station in Dwarka suffered three compressor failures in its first month of operation. The Italian manufacturer sent increasingly exasperated engineers who couldn't understand why their equipment, which worked perfectly in Milan, was failing in Delhi.

Safety concerns added another layer of complexity. CNG, being lighter than air, dissipates quickly if leaked, making it safer than LPG in some ways. But the high pressure required for compression created its own risks. IGL instituted what they called "paranoid safety protocols"—multiple redundant safety systems, daily inspections, and emergency response drills that seemed excessive until they weren't. When a minor leak at a station in Rohini was detected and contained without incident, the over-engineering suddenly seemed justified.

The financial hemorrhaging continued through 2003 and 2004. IGL was spending crores on infrastructure while revenue trickled in slowly. Banks were nervous, asking pointed questions about loan servicing. The company's CFO later recalled presenting to a room full of skeptical bankers: "I couldn't show them profit projections because we didn't have any. All I could show them was the Supreme Court order. That document was our business plan."

By 2005, a transformation was becoming visible. The black smoke that had been Delhi's signature was noticeably reduced. Air quality indices, while still poor, showed improvement. The health data was even more compelling—hospital admissions for respiratory ailments during winter months dropped by 15%. It wasn't solving Delhi's pollution crisis, but it was making a dent.

The network effects began to kick in by 2006. As more CNG stations opened, more vehicle owners felt confident about conversion. As more vehicles converted, the utilization rates at CNG stations improved, making them profitable. It was a virtuous cycle, but one that had been initiated by judicial force rather than market dynamics.

IGL's management, sensing the momentum shift, made a crucial strategic decision: expand beyond transport into residential piped natural gas (PNG). The same pipeline infrastructure that fed CNG stations could also supply homes. It was a classic adjacency move, leveraging existing assets for new revenue streams. The pitch to households was simple: safer than LPG cylinders, cheaper in the long run, and no more booking and waiting for cylinder deliveries.

By 2008, IGL had achieved something remarkable: operational profitability. The company that had been born from a court order, that had spent years building infrastructure for unwilling customers, was actually making money. The transformation was complete. Or so it seemed. The global financial crisis was about to test whether IGL's court-mandated business model could survive real-world economic shocks.

VI. The Expansion Playbook: Beyond Delhi (2010-2020)

The boardroom at IGL's Scope Complex office had witnessed many pivotal moments, but the meeting in March 2010 felt different. The presentation on the screen showed a map of North India with Delhi at its center, surrounded by rapidly growing satellite cities. "Delhi is just the beginning," the strategy head declared. "The real opportunity lies in the entire National Capital Region and beyond."

IGL had spent the previous decade proving that a court-mandated business model could work. Now came the real test: could they replicate that success in markets where the Supreme Court's writ didn't run? Could they compete without the protective moat of judicial compulsion?

The expansion into Noida and Greater Noida seemed like a natural first step. These satellite cities, with their planned infrastructure and growing population, were perfect testing grounds. But IGL quickly discovered that each city had its own political economy, its own bureaucratic maze, its own set of vested interests. What worked in Delhi didn't necessarily translate across the Yamuna.

In Ghaziabad, they encountered a different challenge altogether. The city's transport union was powerful and skeptical. Without a Supreme Court order forcing conversion, IGL had to actually sell the benefits of CNG. Their sales teams, accustomed to dealing with captive customers in Delhi, had to learn the art of persuasion. They organized "CNG melas" (fairs) where bus operators could test-drive converted vehicles, see the cost calculations, and meet others who had made the switch.

The residential PNG push revealed the genius of IGL's vertical integration. Every household that connected to PNG became a stable, predictable revenue stream. Unlike CNG for vehicles, which fluctuated with traffic patterns and economic cycles, cooking gas demand was remarkably consistent. A family might skip a trip, but they wouldn't skip a meal. By 2012, IGL was adding 1,000 new PNG connections daily, each one a small but steady contribution to the bottom line.

The competitive landscape was evolving too. IGL's promoters, GAIL and BPCL, were both potential competitors. It was an awkward dance—your largest shareholders were also your biggest threats. GAIL, which supplied IGL's gas, was also bidding for city gas distribution licenses in other cities. BPCL, which had provided land for CNG stations, was exploring its own gas distribution ambitions. Board meetings became exercises in careful navigation, with independent directors playing referee between conflicting interests.

By 2013, a new player had entered the scene: Mahanagar Gas Limited (MGL) in Mumbai. MGL's success story was remarkably similar to IGL's—court mandates, forced adoption, eventual profitability. The two companies became unlikely allies, sharing best practices while carefully avoiding each other's territories. When executives from both companies met at industry conferences, they would exchange knowing smiles. They were members of an exclusive club: companies that owed their existence to judicial intervention.

The government's push for city gas distribution (CGD) networks across India created new opportunities and threats. The Petroleum and Natural Gas Regulatory Board (PNGRB) was auctioning CGD licenses for cities across India. IGL bid aggressively, winning rights to cities like Rewari, Karnal, and Kaithal in Haryana, Kanpur and Muzaffarnagar in Uttar Pradesh, and even Ajmer in Rajasthan. Each new city was a bet that the IGL playbook—build infrastructure, create network effects, achieve profitability through scale—could work without judicial compulsion.

Kanpur proved to be a particularly interesting case study. One of India's most polluted cities, it seemed ripe for CNG adoption. But Kanpur's transport sector was fragmented, informal, and deeply resistant to change. IGL had to innovate. They partnered with local banks to provide conversion loans, set up mobile CNG stations for areas where permanent stations weren't viable, and even created a "CNG ambassador" program where early adopters were incentivized to bring in others.

The technology was evolving too. By 2015, IGL was experimenting with mother-daughter station concepts—large "mother" stations would compress gas and transport it in cascades to smaller "daughter" stations in areas without pipeline connectivity. It was a way to expand the network without the massive capital expenditure of laying pipelines. The model worked, but margins were thinner. Every innovation came with trade-offs.

Financial markets had taken notice. IGL's stock, listed since 2003, had become a darling of institutional investors. The company's dividend payout ratio of 59% made it attractive to income-focused funds. Foreign institutional investors, initially skeptical of a government-controlled utility, were won over by the consistent cash flows and growth trajectory. By 2016, FIIs owned 18% of the company, a remarkable vote of confidence in what had once been a court-ordered experiment.

The network effects were now undeniable. Each new PNG connection made the network more valuable. Each new CNG station increased the convenience for vehicle owners. Each converted vehicle increased utilization rates at stations. It was a self-reinforcing cycle that MBA students would later study as a textbook example of network economics—if they could get past the unusual origin story.

But success brought scrutiny. The Comptroller and Auditor General (CAG) raised questions about IGL's pricing, noting the significant gap between industrial and transport CNG prices. Environmental activists argued that while CNG was cleaner than diesel, it was still a fossil fuel. The transition to electric vehicles, still nascent but gathering momentum, posed existential questions. Was IGL building tomorrow's stranded assets?

Management's response was pragmatic. They couldn't control technology disruption, but they could control their balance sheet. The company maintained minimal debt, ensuring they had flexibility to adapt. They invested in compressed biogas (CBG) projects, hedging against the fossil fuel critique. They even explored electric vehicle charging infrastructure, though half-heartedly—it felt like a betrayal of their core business.

By 2018, IGL had transformed from a Delhi-centric utility to a regional energy distribution powerhouse. They were present in 11 cities, operated over 500 CNG stations, and had crossed 10 lakh PNG connections. The company that had been forced into existence by the Supreme Court was now expanding by choice, competing on merit, winning on economics.

The irony wasn't lost on long-time employees. They had started as reluctant servants of a judicial order and evolved into aggressive capitalists seeking new markets. The transformation was complete, yet the DNA remained unchanged. IGL was still, at its core, a company that existed because a judge decided Delhi's air was too dirty to breathe.

As the decade drew to a close, IGL faced a new challenge: success had made them conservative. The scrappy startup mentality that had built infrastructure at breakneck speed had given way to bureaucratic processes and committee decisions. Innovation slowed. Young engineers complained about hierarchical approvals for simple decisions. The company that had been born from disruption was becoming the establishment.

VII. The Modern Era: Market Dynamics & New Challenges (2020-Present)

The WhatsApp forward arrived on every IGL employee's phone almost simultaneously on a humid August morning in 2024: "Government slashes APM gas allocation by 20%. Stock down 8% in pre-market." The message was followed by a flurry of anxious emojis. For a company that had weathered Supreme Court mandates, infrastructure sprints, and market expansion, this felt different. This was an attack on the fundamental economics of their business model.

APM (Administered Pricing Mechanism) gas had been IGL's secret sauce—domestic natural gas allocated at government-controlled prices, significantly cheaper than market rates. It was the subsidy that made CNG affordable compared to petrol and diesel. Now, with a 20% cut in APM allocation, IGL would need to source replacement gas at market prices. The new well gas, priced at 12% of the Indian crude basket, would cost almost double.

The management's response was swift but concerning. They announced that the shortfall would be met through a combination of new well gas and imported LNG, but everyone knew what this meant: either margins would compress or prices would rise. Neither option was palatable for a company that had built its moat on being the cheaper, cleaner alternative.

The timing couldn't have been worse. Electric vehicles, once a distant threat, were now a clear and present danger. Two-wheelers were going electric at an alarming rate. Ola and Uber were piloting electric cab fleets. Even the Delhi government, IGL's original patron, was offering massive subsidies for electric vehicle adoption. The same environmental arguments that had created IGL's market were now being used against them.

But the company that had survived judicial diktat wasn't going down without a fight. In December 2024, IGL announced a 1:1 bonus share issue—a signal to markets that management remained confident about future cash flows. The move was classic IGL: conservative yet optimistic, rewarding patient shareholders while maintaining balance sheet strength.

The competitive landscape had evolved dramatically. Adani Total Gas, backed by the infrastructure giant's execution capabilities and Total's technical expertise, was aggressively bidding for new city gas licenses. They were offering better terms to industrial customers, faster connection times to residential users, and were unencumbered by the bureaucratic processes that had calcified within IGL. The new entrants were hungrier, more agile, and better capitalized.

Yet IGL's moat remained formidable. With 819 CNG stations and 25.60 lakh residential connections serving the NCR Delhi region, the network effects were deeply entrenched. Switching costs for consumers were high. The infrastructure was already amortized. The company was generating cash like a machine—almost debt-free with consistent dividends.

The retail investor revolution added another dimension. By 2024, retail investors owned 51% of IGL, up from less than 20% a decade ago. These weren't sophisticated institutional investors running discounted cash flow models. These were middle-class Indians who filled their cars at IGL stations, cooked with IGL gas, and saw the company as a stable dividend-paying utility. They created a floor under the stock price through sheer conviction.

Management's strategy evolved to embrace the "transition fuel" narrative. Yes, the future might be electric, but the transition would take decades. In the meantime, CNG was the cleanest viable option for commercial vehicles. Heavy-duty trucks and buses couldn't go electric yet—battery technology wasn't there. IGL positioned itself as the bridge between diesel's dirty past and electricity's clean future.

The company also doubled down on compressed biogas (CBG). Agricultural waste could be converted to biogas, which could then be compressed and distributed through existing CNG infrastructure. It was a circular economy play that addressed both the fossil fuel critique and the stubble burning crisis that plagued North India every winter. The economics were still questionable, but the optics were excellent.

The international context remained relevant. Cities worldwide were implementing low emission zones and congestion charging. Delhi, with its recurring winter pollution crises, seemed perpetually on the verge of similar measures. Each time air quality plummeted and public health emergencies were declared, IGL's stock would paradoxically rise. Investors were betting that crisis would drive policy, and policy would protect IGL's market.

But internal challenges were mounting. The company's cost structure had bloated over the years. Employee costs had risen faster than revenue. The procurement processes, designed for a government-controlled utility, were too slow for a competitive market. Young talent was leaving for startups and new-age energy companies. IGL was becoming what every successful disruptor fears: a slow-moving incumbent.

The board composition reflected these tensions. Independent directors pushed for aggressive expansion and digital transformation. Nominee directors from GAIL and BPCL advocated for conservative growth and dividend distribution. Government nominees wanted social objectives prioritized. The result was strategic paralysis masquerading as consensus.

Climate change added another layer of complexity. Natural gas, while cleaner than coal or oil, was still a fossil fuel. Methane leakage from distribution networks was a growing concern. International ESG investors were asking harder questions. IGL's pitch as an environmental solution was becoming harder to sustain as the world's climate ambitions expanded.

The Russia-Ukraine conflict in 2022 had already demonstrated the volatility of global gas markets. LNG prices had spiked, spreading fear through IGL's treasury department. While domestic gas allocation provided some insulation, the company was increasingly exposed to international price swings. The comfortable predictability of a regulated utility was giving way to the harsh realities of commodity markets.

Yet the fundamental paradox remained: IGL was a climate solution that relied on fossil fuels, a free-market success built on government mandate, a growth story constrained by its own success. Every strength contained the seed of weakness. Every moat could become a trap.

As 2025 dawned, IGL stood at an inflection point. The company that had been created by judicial intervention to solve an environmental crisis now faced an existential question: What happens when the solution becomes the problem? When the bridge fuel is no longer needed? When the transition it enabled makes it obsolete?

The answer would determine whether IGL's next chapter would be one of reinvention or decline. But one thing was certain: the company that had emerged from the chaos of Delhi's pollution crisis had proven remarkably adaptable. Whether that adaptability would be enough for the challenges ahead remained an open question.

VIII. Power Dynamics & Stakeholder Analysis

The annual general meeting at Delhi's Siri Fort Auditorium in September 2024 was a masterclass in stakeholder management. On stage sat IGL's board—a carefully orchestrated ensemble representing the company's three-way power structure. The GAIL nominee directors sat to the left, BPCL representatives to the right, and independent directors in the center, a physical manifestation of the delicate balance that governed India's most unusual utility company.

In the audience, the composition told its own story. The first few rows were occupied by institutional investors in dark suits, armed with detailed questions about gas sourcing agreements and margin compression. Behind them sat retail shareholders, many of them senior citizens who had bought IGL shares at listing and never sold, content with steady dividends. At the back, a handful of environmental activists waited their turn at the microphone, ready to challenge the company's green credentials.

"Who really controls IGL?" was a question that had no simple answer. On paper, GAIL owned 26%, making it the largest shareholder. But GAIL was also IGL's primary gas supplier, creating an inherent conflict. Could GAIL negotiate hard on gas prices when it would hurt a company it partially owned? The arrangement was either brilliantly synergistic or deeply problematic, depending on whom you asked.

BPCL's position was equally complex. As a petroleum refiner watching the world slowly transition away from oil, BPCL saw IGL as both a hedge and a threat. Every CNG vehicle was one less petrol customer. Yet BPCL's retail outlets hosting CNG stations created a powerful distribution advantage. It was cooperation and competition rolled into one.

The Delhi government's 5% stake was small but symbolically powerful. It represented the public interest, the original mandate to clean Delhi's air. When pricing decisions came up, the government nominee would invariably invoke the common citizen, the auto-rickshaw driver struggling with fuel costs, the middle-class family managing household expenses. It was a moral voice in a room full of financial calculations.

But the real power shift had been toward institutional investors, particularly foreign funds. With FIIs owning 18% and domestic institutions another 15%, they had become the swing vote on major decisions. These investors cared little for the origin story or social mandate. They wanted returns, growth, and capital efficiency. Their analysts would grill management on ROCE improvements and competitive positioning, not air quality indices.

The retail investor revolution added another dimension to this power dynamic. With 51% ownership dispersed among hundreds of thousands of small shareholders, IGL had become truly public in a way few Indian companies were. These shareholders showed up at AGMs, asked questions in Hindi, and shared WhatsApp forwards about company news. They were emotionally invested, seeing IGL as both a financial asset and a civic institution.

This diverse ownership created what management privately called "the paralysis problem." Every decision had to be evaluated through multiple lenses. Would it satisfy GAIL's strategic objectives? Would BPCL see it as encroachment? Would the government find it politically acceptable? Would institutional investors reward it? Would retail shareholders understand it?

Take the electric vehicle charging infrastructure debate. Institutional investors wanted IGL to aggressively enter this space, seeing it as a natural adjacency. GAIL and BPCL were lukewarm—it wasn't their core competency. The government was enthusiastic—it aligned with environmental objectives. Retail shareholders were confused—why would a gas company sell electricity? The result: a pilot project so small it satisfied no one.

The regulatory overlay added another layer of complexity. The Petroleum and Natural Gas Regulatory Board (PNGRB) set network tariffs and monitored service quality. The Delhi Pollution Control Committee could mandate environmental compliance. The Ministry of Petroleum and Natural Gas influenced gas allocation. Each regulator had its own agenda, its own metrics, its own interpretation of public interest.

This multi-stakeholder complexity manifested most clearly in pricing decisions. IGL's pricing wasn't just about supply and demand—it was political theater. Every price increase triggered protests from transport unions, questions in the Delhi Assembly, and editorial outrage. The company had to navigate between commercial viability and political acceptability, often choosing suboptimal pricing to avoid controversy.

The board meetings, according to sources who requested anonymity, were fascinating studies in corporate diplomacy. Nominee directors would arrive with positions pre-determined by their parent companies. Independent directors would try to forge consensus while protecting minority shareholders. Government nominees would invoke public interest at crucial moments. Decisions that should take minutes would stretch to hours.

Yet somehow, this unwieldy structure worked. Perhaps because everyone had too much to lose from conflict. GAIL needed IGL as a steady customer for its gas. BPCL needed the CNG stations to remain relevant in a transitioning energy landscape. The government needed IGL to keep Delhi's air breathable. Investors needed the dividends to keep flowing.

The Supreme Court, the invisible stakeholder that had created this entire ecosystem, remained a looming presence. Though the original PIL had been disposed of, the precedent remained. Any significant deterioration in Delhi's air quality could trigger new judicial intervention. IGL's existence was predicated on a legal mandate that could theoretically be modified or revoked.

This created what economists would call a "political economy equilibrium"—a stable but not necessarily efficient arrangement where all parties were sufficiently satisfied to not rock the boat. IGL was profitable enough to keep investors happy, clean enough to satisfy environmental mandates, affordable enough to avoid political backlash, and strategic enough to serve its promoters' interests.

The company's management, caught in the middle of these competing forces, had developed a unique operating philosophy: "strategic incrementalism." Never make bold moves that could upset the equilibrium. Grow steadily but not disruptively. Innovate cautiously but not radically. It was a strategy born of constraint, but it had delivered remarkable consistency.

This stakeholder complexity also created an unexpected strength: resilience. Because IGL served so many masters, it had developed multiple capabilities. It could navigate bureaucracy like a government company, execute projects like a private corporation, manage networks like a utility, and generate returns like a growth stock. This hybrid identity, born of necessity, had become a competitive advantage.

The question for the future was whether this delicate balance could survive disruption. As electric vehicles gained ground, as new competitors emerged, as gas markets volatilized, would the stakeholder coalition hold? Or would competing interests finally tear apart the careful consensus that had sustained IGL for over two decades?

IX. Playbook: Business & Investment Lessons

If you had to teach a business school class on how to build a successful company in the most unlikely circumstances, IGL would be your case study. But it would come with a warning label: "Results not replicable in normal market conditions."

The first lesson is perhaps the most counterintuitive: sometimes the best business models are created by constraint, not choice. IGL didn't choose its market, its customers, or even its product. The Supreme Court chose for them. This forced focus eliminated the paralysis of optionality that kills many startups. When you can only do one thing, you tend to do it exceptionally well.

Consider the traditional startup wisdom about finding product-market fit. IGL inverted this entirely. They had market-product fit—a market was legally mandated, and IGL had to create a product to serve it. This guaranteed demand but came with its own challenges. How do you price a product that customers are forced to buy? How do you ensure quality when switching isn't an option? IGL's answer was to act as if competition existed even when it didn't, maintaining service standards that would survive the eventual arrival of rivals.

The infrastructure-first strategy that seemed like cash incineration in the early years turned out to be genius in retrospect. By the time competitors arrived, IGL had already depreciated much of its capital expenditure. New entrants had to invest billions to build networks while competing against IGL's marginal cost pricing. It's the equivalent of showing up to a gold rush after someone else has already built all the mines.

The network effects in regulated utilities present a fascinating paradox. Traditional network effects rely on user choice—more users make the network more valuable, attracting even more users. IGL's network effects were different. More CNG stations made conversion more attractive even for those not legally mandated. More PNG connections justified pipeline extensions that made further connections economical. The compulsion created the initial network, but voluntary adoption sustained its growth.

Capital allocation in monopolistic markets requires unusual discipline. When you have a captive market and pricing power, the temptation is to maximize extraction. IGL did the opposite, maintaining reasonable margins that wouldn't invite regulatory backlash or competitive entry. They understood that in a politically sensitive business, the cost of capital wasn't just financial—it was social and political too.

The regulatory arbitrage opportunity was subtle but powerful. IGL operated in the gap between environmental regulation (which favored them), energy regulation (which protected them), and competition law (which hadn't caught up to their unique situation). They navigated this three-dimensional regulatory space like a chess grandmaster, using each framework to defend against threats from the others.

ESG before ESG was cool turns out to be valuable. IGL was solving environmental problems before sustainability became a boardroom priority. When ESG investing took off, IGL was already positioned as an environmental play, attracting capital that wouldn't touch pure fossil fuel companies. They had accidentally built a green moat.

The dividend policy as a strategic weapon deserves attention. IGL's consistent high dividend payout (59% ratio) created a powerful shareholder base of income-seeking investors. These investors—particularly retail—became a political constituency that made adverse government action costly. Every dividend cut would anger voters. It was financial engineering as political insurance.

The power of boring businesses is understated. IGL isn't disrupting anything. They're not reimagining the gas distribution experience. They're just reliably delivering a commodity through pipes and pumps. But boring businesses with predictable cash flows and high barriers to entry can be extraordinary investments. The lack of excitement keeps valuations reasonable and competition manageable.

Vertical integration in utilities creates resilience. IGL's expansion from CNG to PNG wasn't just about growth—it was about risk distribution. When oil prices spike, transport fuel demand might drop, but cooking gas demand remains stable. When electric vehicles threaten CNG, residential gas connections provide ballast. Multiple revenue streams from the same infrastructure create operational leverage and risk mitigation.

The India-specific lesson about PIL as a business catalyst is particularly fascinating. Public Interest Litigations have reshaped entire industries in India—from pollution control to prohibition. Understanding the judicial system as a potential market creator or destroyer is crucial for Indian businesses. IGL benefited from this, but others have been decimated. The Supreme Court giveth, and the Supreme Court taketh away.

Managing conflicted shareholders is an art IGL has mastered. When your largest shareholders are also your suppliers (GAIL) and potential competitors (BPCL), every board meeting is a delicate dance. IGL's solution was radical transparency and strategic ambiguity—share enough information to maintain trust but not enough to enable competition.

The talent paradox in regulated industries is real. How do you attract top talent to a company with limited upside, bureaucratic processes, and regulatory constraints? IGL's answer was to offer stability, purpose, and the opportunity to build critical infrastructure. They attracted a different kind of talent—engineers who wanted to build things, not flip them.

The optionality of infrastructure is often undervalued. IGL's pipeline network, built for natural gas, could theoretically carry hydrogen or biogas in the future. The CNG stations could become EV charging hubs. Physical infrastructure, unlike software, can be repurposed. This optionality has value even if never exercised.

For investors, IGL teaches that moats can come from unexpected sources. Not technology, brand, or scale, but judicial mandate. Not innovation, but regulation. Not disruption, but stability. The deepest moats are often the most boring ones.

The ultimate lesson might be about adaptability within constraints. IGL couldn't pivot like a startup, couldn't innovate like a tech company, couldn't expand like a conglomerate. But within their narrow mandate, they displayed remarkable creativity. They turned a judicial order into a business model, a pollution crisis into a profit center, and a government mandate into a market opportunity.

These lessons come with caveats. IGL's playbook isn't universally applicable. You can't replicate judicial intervention. You can't manufacture environmental crises. You can't guarantee regulatory protection. But you can learn from how IGL navigated these unique circumstances to build a sustainable, profitable business.

X. Bull vs. Bear Case

The Bull Case: Why IGL Could Be the Ultimate Defensive Play

The bull thesis for IGL starts with a simple observation: Delhi isn't getting less polluted anytime soon, and the government isn't getting less interventionist. As long as these two facts remain true, IGL's moat remains intact.

Start with the monopolistic position in India's capital region. Delhi NCR isn't just any market—it's India's power center, home to policy makers, influencers, and the wealthy. When Delhi chokes on pollution every winter, it makes international headlines. This visibility creates political pressure for action, and IGL remains the most viable immediate solution. You can't electrify the entire transport fleet overnight, but you can mandate CNG adoption with a bureaucratic order.

The growing urbanization and PNG penetration story has decades of runway. India's urbanization rate is still only 35%, compared to 80%+ in developed countries. As cities grow and densify, piped gas becomes more economical than LPG cylinders. IGL is capturing this secular trend, adding thousands of connections monthly. Each connection is a 30-year annuity stream.

ESG tailwinds and pollution concerns are only intensifying. Every climate conference, every air quality study, every respiratory disease statistic strengthens IGL's position. They're not perfect—natural gas is still a fossil fuel—but they're demonstrably better than the alternatives available at scale. In a world of imperfect choices, being the least bad option is a winning position.

The cash generation and dividend reliability makes IGL a bond proxy in equity form. In a world of negative real interest rates, a company yielding 3-4% with growing dividends is attractive. The 51% retail ownership creates a floor under the stock—these investors measure returns in dividends received, not stock price appreciation.

The transition fuel argument has more longevity than bears assume. Heavy commercial vehicles—trucks, buses, construction equipment—can't go electric with current battery technology. The weight and range requirements don't work. Hydrogen is decades away from commercial viability. CNG remains the only viable clean alternative for heavy-duty applications.

Geographic expansion opportunities remain substantial. IGL has licenses for multiple cities beyond Delhi. Each new city is a 10-year infrastructure build and 30-year harvest opportunity. The playbook is proven—they just need to execute it repeatedly.

The regulatory framework remains protective. City gas distribution is a licensed business with infrastructure requirements that create natural monopolies. Once IGL builds a network, competing overbuilds are economically irrational. Regulators understand this and protect incumbents while ensuring reasonable returns.

The Bear Case: Why IGL Might Be Tomorrow's Stranded Asset

The bear thesis begins with an uncomfortable truth: IGL is a climate solution that relies on fossil fuels, and the world is moving faster than expected toward net-zero commitments.

EV disruption to CNG vehicles is the existential threat. Two-wheelers are already going electric at an accelerating pace. Cars are following. Even buses are starting to electrify. IGL's transport fuel business—historically its most profitable segment—could evaporate faster than anyone expects. When technology transitions happen, they happen suddenly, then all at once.

Regulatory risk and price controls are ever-present. IGL exists at the government's pleasure. A single policy change—removing gas allocation, mandating price cuts, opening sectors to competition—could destroy the business model overnight. The company that was created by regulation could just as easily be destroyed by it.

Gas allocation uncertainties are mounting. The 20% cut in APM gas allocation is just the beginning. As domestic gas production stagnates and demand grows, IGL will increasingly depend on expensive imported LNG. The input cost advantage that made CNG economical could disappear, making the entire business model unviable.

Competition in new geographic areas is intensifying. Adani Total Gas, Torrent Gas, and others are bidding aggressively for new licenses. They're offering better terms, faster execution, and modern technology. IGL's bureaucratic processes and legacy systems make them vulnerable in competitive bidding.

The stranded asset risk is real. IGL has thousands of crores invested in pipeline infrastructure predicated on decades of natural gas demand. If that demand disappears faster than expected, these assets become worthless. The depreciation might be accounting fiction, but the cash invested was real.

Technology disruption beyond EVs could blindside the company. Green hydrogen, though currently uneconomical, could become viable. Biogas might scale differently than expected. Synthetic fuels could emerge. IGL's narrow focus on natural gas makes them vulnerable to any alternative energy breakthrough.

The talent and innovation deficit is widening. IGL struggles to attract top engineering talent who prefer startups and tech companies. The company's innovation pipeline is thin. They're not leading in any technology area. In a rapidly evolving energy landscape, standing still is moving backward.

Political risk from populism could escalate. As inflation bites and elections loom, populist politicians could demand price cuts that destroy margins. Transport unions remain powerful vote banks. The temptation to squeeze IGL for political gain is ever-present.

The Verdict: A Battle Between Inertia and Innovation

The bull-bear debate ultimately comes down to timeframes and beliefs about change velocity. Bulls are betting on inertia—that infrastructure transitions take decades, that regulatory capture persists, that cash flows continue. Bears are betting on acceleration—that technology shifts happen suddenly, that policies can reverse overnight, that disruption is always faster than expected.

What makes IGL particularly interesting is that both cases could be right sequentially. The bull case could dominate for the next five years—steady growth, reliable dividends, expanding networks. Then the bear case could materialize suddenly—EV adoption hits a tipping point, government policy shifts, stranded assets multiply.

For investors, this creates a fascinating game theory problem. Do you ride the cash flows while they last, trusting you can exit before disruption? Or do you avoid the risk entirely, potentially missing years of returns? The answer depends on your time horizon, risk tolerance, and belief about the pace of energy transition.

The market's current pricing suggests a middle ground—IGL trades at reasonable multiples, not the premium of a growth stock nor the discount of a dying business. The market is essentially saying: "This company will be around for a while, generating decent returns, but don't expect miracles."

Perhaps that's the right framework. IGL isn't a bet on transformation or disruption. It's a bet on transition—that the path from dirty to clean energy will be long, winding, and profitable for those who build the bridges. Whether those bridges become monuments or ruins depends on how fast the world decides to cross them.

XI. Final Analysis & Reflections

Standing at the IGL CNG station in Connaught Place today, watching auto-rickshaws queue for fuel, it's hard to imagine that this entire ecosystem exists because of a Public Interest Litigation filed by one determined lawyer nearly four decades ago. The infrastructure we now take for granted—the thousands of kilometers of pipeline, hundreds of stations, millions of connections—all trace back to that moment when M.C. Mehta decided enough was enough.

The unintended consequences of judicial activism have been profound. The Supreme Court never intended to create a four-billion-dollar company. The judges weren't thinking about network effects, dividend yields, or competitive moats. They just wanted Delhiites to breathe easier. Yet their intervention created one of India's most unusual corporate success stories, a company that proves markets can be created by mandate, not just discovered through competition.

This tells us something important about India's unique path to development. Unlike the West, where industrialization preceded environmental consciousness by centuries, India is attempting both simultaneously. This creates contradictions—promoting coal power while pushing solar, subsidizing petroleum while mandating CNG, celebrating GDP growth while lamenting pollution. IGL embodies these contradictions, being simultaneously a fossil fuel company and an environmental solution.

The parallels to other government-created markets are instructive. India's Aadhaar system created a digital identity market that spawned entire industries. The Unified Payments Interface (UPI) was a regulatory intervention that revolutionized digital payments. GST created a tax compliance industry worth billions. In each case, government mandate created markets that private enterprise then optimized. IGL fits this pattern—judicial mandate created the market, private enterprise made it efficient.

But the sustainability question looms large: Can mandated markets survive without mandates? IGL's evolution suggests yes, but with caveats. The company has successfully expanded beyond Delhi, competing without court orders. PNG connections grow organically, driven by convenience rather than compulsion. But the core CNG business still depends heavily on regulatory support. Remove the economic advantages—tax benefits, preferential allocation, regulatory protection—and the business model wobbles.

What makes IGL fascinating as a business case is how it challenges conventional wisdom. Business schools teach that sustainable competitive advantages come from innovation, brand building, or operational excellence. IGL's advantage came from none of these. It came from being the first to build infrastructure in response to a court order. It's a reminder that in emerging markets, the ability to navigate institutional voids—gaps in markets, regulations, or governance—can be more valuable than traditional business capabilities.

The company also illustrates the power of path dependence. Once IGL built Delhi's gas distribution infrastructure, every subsequent decision by regulators, competitors, and customers was constrained by that existing network. It became easier to work with IGL than around them. This first-mover advantage in infrastructure is nearly impossible to replicate, creating a moat that deepens with time rather than erodes.

The environmental impact, while significant, remains complex. IGL has undoubtedly improved Delhi's air quality. The reduction in particulate matter, the decrease in respiratory ailments, the clear winter skies—these are real achievements. But natural gas is still a fossil fuel, contributing to greenhouse gas emissions. IGL improved local air quality at the cost of global climate impact. It's a trade-off that made sense in 1998 but looks increasingly problematic in 2025.

For policymakers, IGL offers lessons about market creation through regulation. When markets fail to deliver public goods—like clean air—government intervention can create new market structures. But these interventions must be carefully designed. Too heavy-handed, and you stifle innovation. Too light, and you achieve nothing. IGL succeeded because the Supreme Court's intervention was specific (convert to CNG), time-bound (deadlines for compliance), and enforceable (permit cancellation for non-compliance).

The corporate governance implications are equally interesting. IGL demonstrates that complex stakeholder structures can work if properly balanced. Despite having government ownership, competitor-shareholders, and regulatory oversight, the company has delivered consistent returns to minority shareholders. This suggests that the traditional dichotomy between state-owned enterprises and private companies is false. Hybrid models can capture the benefits of both.

Looking forward, IGL faces an existential question about purpose. If the company was created to solve Delhi's pollution crisis, what happens when that crisis evolves? As electric vehicles proliferate and renewable energy scales, does IGL pivot to remain relevant or accept obsolescence gracefully? The answer will determine whether IGL's next chapter is about transformation or terminal decline.

The broader implications for energy transition are sobering. If a company created specifically to enable clean fuel adoption struggles to adapt to the next wave of clean technology, what hope do traditional fossil fuel companies have? IGL's challenges preview the disruption coming for the entire energy sector. The transition from dirty to clean was easier than the transition from cleaner to cleanest will be.

Perhaps the most profound lesson is about institutional entrepreneurship. IGL's story shows that businesses can emerge from the most unlikely places—not just garages and dorm rooms, but also courtrooms and government offices. Sometimes the best opportunities lie not in creating new markets but in organizing existing ones that have been mandated into existence.

As we reflect on IGL's journey from judicial mandate to market leader, several truths emerge. First, necessity is indeed the mother of invention—or in this case, the mother of infrastructure. Second, monopolies created for public good can evolve into profitable enterprises if properly managed. Third, the intersection of regulation, environment, and business creates unique opportunities for those able to navigate the complexity.

The ultimate question is whether IGL represents a model to be replicated or an anomaly to be studied. Can judicial activism create other sustainable businesses? Should courts intervene in market failures? Is forced adoption a legitimate path to infrastructure development? The answers matter because India faces numerous challenges—water scarcity, waste management, healthcare access—that markets alone seem unable to solve.

IGL's story is far from over. The company stands at an inflection point, facing technological disruption, regulatory uncertainty, and existential questions about purpose. How it navigates these challenges will determine whether it remains a case study in successful judicial intervention or becomes a cautionary tale about the limits of mandated markets.

But regardless of what the future holds, IGL has already secured its place in Indian corporate history. It proved that a company born from a court order could become a profitable enterprise. It demonstrated that environmental mandates could create economic value. It showed that in a country like India, sometimes the most unusual business models are the most successful ones.

The lesson for investors, entrepreneurs, and policymakers is clear: in emerging markets, the most valuable opportunities often lie at the intersection of market failure and government intervention. The skill lies not in avoiding these intersections but in navigating them successfully. IGL did just that, turning a pollution crisis into a profit center, a judicial mandate into a market opportunity, and a government directive into a growth story.

As Delhi's winter air clears and citizens breathe a little easier, they might not think about the complex corporate structure, the regulatory framework, or the business model that made it possible. But for those who study business and markets, IGL remains a fascinating example of how capitalism adapts to constraints, how markets emerge from mandates, and how sometimes, the best businesses are built not in spite of government intervention, but because of it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube