Energy Transfer Partners: Building America's Pipeline Empire

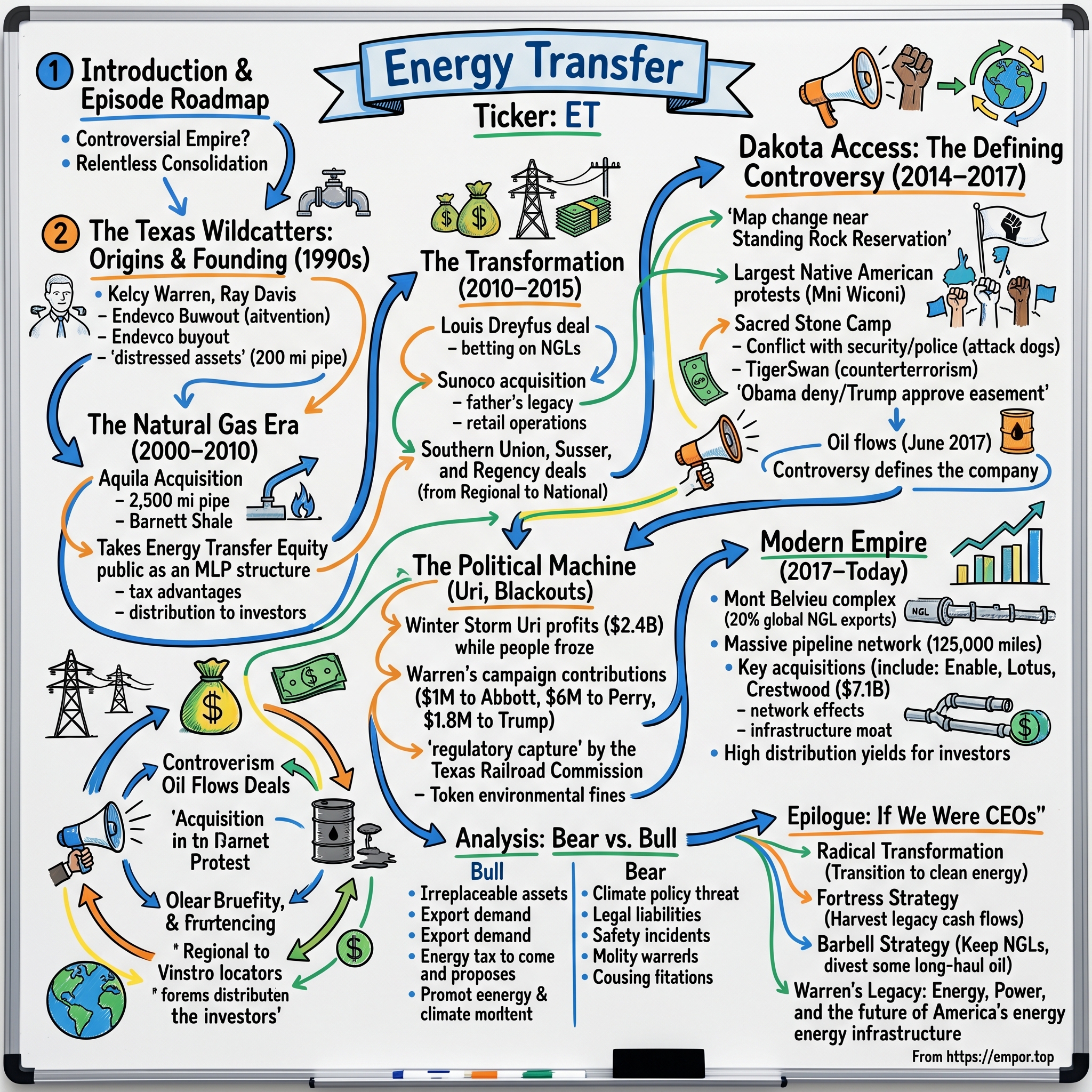

I. Introduction & Episode Roadmap

Picture this: A network of steel arteries stretching 125,000 miles across America, pumping the lifeblood of modern civilization—natural gas, crude oil, refined products—through mountains, under rivers, across prairies. This isn't some futuristic vision; it's Energy Transfer Partners today, moving 30% of America's natural gas and petroleum. The company exports more natural gas liquids than almost anyone on Earth, operating from both Gulf and East Coast terminals. Yet most Americans have never heard of ET, the ticker symbol that represents one of the most essential—and controversial—energy empires ever built.

How did two Texas entrepreneurs transform 200 miles of rusty East Texas pipe into a $50 billion infrastructure colossus? How did a civil engineer whose father worked as a field hand end up owning the very pipeline company that once employed him? And how did a business built on moving molecules become the lightning rod for America's most explosive environmental battles?

This is the story of Energy Transfer Partners—a tale of audacious dealmaking, political power plays, and the brutal realities of building critical infrastructure in modern America. It's about Kelcy Warren and Ray Davis, two wildcatters who saw opportunity where others saw obsolescence, who built an empire on the simple insight that America would always need to move energy from where it's produced to where it's consumed.

We'll trace their journey from those humble 200 miles of pipeline through the shale revolution, the Dakota Access protests that brought militarized security to North Dakota prairies, and the Texas blackouts that netted them $2.4 billion while millions froze. We'll examine how infrastructure becomes power—both electrical and political—and why owning the pipes matters more than owning what flows through them.

Major themes emerge: the relentless consolidation of America's midstream sector, the intertwining of energy infrastructure with political influence, and the collision between fossil fuel realities and environmental imperatives. This isn't just a business story—it's about the invisible architecture of American energy, the people who control it, and what that means for the future.

II. The Texas Wildcatters: Origins & Founding (1990s)

The conference room at Endevco was tense that day in 1992. The natural gas marketing company was hemorrhaging cash, creditors circling like vultures. Among the executives trying to salvage the wreckage sat Kelcy Warren, a 36-year-old civil engineer with an unusual background and an even more unusual ability to see opportunity in chaos. Across from him: Ray Davis, a seasoned dealmaker with deep pockets and deeper connections in Texas energy circles.

Warren's path to that room was anything but typical. The youngest of four sons born to a Sun Pipeline field hand in East Texas, he'd grown up literally in the shadow of the infrastructure he'd one day own. His father spent decades maintaining the very pipelines that would eventually become part of Warren's empire—a Shakespearean twist that Warren himself would later acknowledge with emotion. "My dad worked his whole life for a company I ended up buying," he'd tell reporters, his voice catching slightly.

After earning his civil engineering degree from UT Arlington, Warren joined Lone Star Gas in 1978, learning the nuts and bolts of pipeline operations. But he was restless, ambitious. By 1981, he'd jumped to Endevco, where he spent eleven years climbing the ranks, studying not just how to move gas but how to make money moving it. The company taught him about basis differentials, transport arbitrage, the financial engineering that turns commodity flows into cash flows.

When Endevco hit the rocks in 1992, Warren saw what others missed. The company had good assets, solid contracts, just terrible timing and worse management. He pitched Ray Davis and their colleague Ben Cook on a radical idea: buy the company, fix it, flip it. Davis, who'd made his fortune in real estate and oil & gas, liked Warren's confidence. Cook brought operational expertise. Together they acquired Endevco, restructured its debt, optimized its contracts, and sold it for a tidy profit by 1996.

That deal forged a partnership that would reshape American energy infrastructure. Warren was the visionary—he could look at a map and see not just pipelines but possibilities, interconnections, arbitrage opportunities. Davis was the operator, the steady hand who could execute on Warren's grand plans. "Ray runs the business," Warren would later say. "I see possibilities where others don't."

In 1996, flush with Endevco profits, Warren and Davis founded Energy Transfer Company. Their initial stake: approximately 200 miles of natural gas pipelines scattered across East Texas, acquired from a distressed seller for a few million dollars. The pipes were old, some dating to the 1940s, running through piney woods and cotton fields, connecting small producers to local distribution companies. It wasn't glamorous. It wasn't even particularly profitable.

For the first few years, Energy Transfer barely survived. "We floundered around, just paying salaries," Warren later admitted. They'd make maybe $50,000 one month, lose $30,000 the next. The late 1990s were brutal for natural gas—prices were low, producers were struggling, and the big players like Enron seemed to have locked up all the profitable trades. Warren and Davis would drive around East Texas in Warren's pickup, inspecting pipelines, meeting with small producers, trying to scrape together enough throughput to cover their bank loans.

The Texas regulatory environment offered both opportunity and frustration. The Railroad Commission of Texas, despite its name, regulated oil and gas pipelines with a light touch that favored established players. But it also meant that if you could acquire assets and prove yourself reliable, regulators wouldn't stand in your way. Warren studied the commission's rules obsessively, learning how to structure deals, how to get permits expedited, which commissioners to cultivate.

Everything changed in 2001. Enron, the 800-pound gorilla of energy trading, began to wobble. By early 2002, it had collapsed entirely, taking with it not just billions in shareholder value but also the complex web of contracts and relationships that had governed natural gas markets. Suddenly, producers needed new outlets, utilities needed new suppliers, and everybody needed reliable pipeline operators who wouldn't disappear overnight.

Warren and Davis pounced. They acquired distressed assets from Enron's bankruptcy, picked up contracts from shell-shocked counterparties, positioned themselves as the stable alternative in a chaotic market. By late 2002, Energy Transfer had grown from 200 to nearly 1,000 miles of pipeline. Revenue jumped from barely break-even to $10 million annually. They'd found their opening—now they needed to exploit it before the window closed.

III. The Natural Gas Era: Growth Through Acquisition (2000–2010)

The call came on a Sunday afternoon in 2004. Aquila, a Kansas City utility giant, was imploding—Enron-style accounting issues, massive debt, desperate for cash. They needed to unload their Texas pipeline assets fast. The asking price: $495 million. Warren hung up the phone and immediately called Davis. "This is it," he said. "This is the deal that changes everything."

But Energy Transfer didn't have $495 million. They barely had $50 million in annual revenue. What they did have was Warren's ability to see value where others saw problems and Davis's talent for structuring complex financings. Within 72 hours, they'd assembled a consortium of banks, negotiated the price down to $265 million, and signed the deal that would catapult Energy Transfer into the big leagues.

The Aquila acquisition brought 2,500 miles of pipeline, including critical infrastructure in North Texas's booming Barnett Shale. Overnight, Energy Transfer's footprint quintupled. More importantly, it gave them scale—the kind of scale that attracts serious investors, enables larger financings, and creates operational leverage. Warren later called it "the deal that positioned us to become who we are today."

The Barnett Shale was exploding. George Mitchell's hydraulic fracturing breakthrough had unlocked massive gas reserves right in Energy Transfer's backyard. Producers were drilling thousands of wells, each needing pipeline connections. Warren and Davis moved aggressively, acquiring TXU Fuel Company's pipeline assets to deepen their Barnett position, then pushing south to buy Houston Pipeline System, which connected them to the Gulf Coast's massive petrochemical complex.

In 2005, they made a crucial structural decision: taking Energy Transfer Equity public on the NYSE. The IPO raised $350 million, giving them currency for acquisitions and access to public markets. But more importantly, they'd discovered the magic of the Master Limited Partnership structure—a tax-advantaged vehicle that could distribute cash to investors while avoiding corporate taxes. MLPs were like REITs for pipelines, and Warren understood their power immediately.

"A pipeliner makes money two ways," Warren would explain to investors. "On volume or on spreads." Volume was straightforward—more gas through the pipes meant more fees. But spreads were where the real money lived. Buy gas cheap in West Texas, transport it to Houston where it's worth more, pocket the difference. The MLP structure meant they could pass most of these profits directly to unitholders, attracting yield-hungry investors while building an acquisition war chest.

By 2007, Energy Transfer was swinging for the fences. They built Texas Independence, the first large-diameter (42-inch) natural gas pipeline constructed in Texas in years, connecting Barnett production to markets across the state. The $1.4 billion project was audacious—Warren personally guaranteed portions of the financing—but it established Energy Transfer as a serious infrastructure player, not just an acquirer of distressed assets.

The business model was evolving rapidly. No longer just moving gas for fees, Energy Transfer was becoming an integrated midstream company—gathering gas from wellheads, processing it to remove valuable liquids, transporting it to markets, even storing it in underground caverns for seasonal arbitrage. Each acquisition added another piece to the puzzle, another way to extract value from hydrocarbon flows.

Davis focused relentlessly on operations while Warren played dealmaker and visionary. "Ray would make sure the pipes didn't blow up and the gas kept flowing," one former executive recalled. "Kelcy would be out there charming bankers, wooing sellers, seeing three moves ahead on the chess board." The partnership worked because each trusted the other completely—Warren to dream big, Davis to execute flawlessly.

The 2008 financial crisis should have destroyed them. Natural gas prices crashed from $13 to $3 per thousand cubic feet. Producers shut in wells, industrial demand evaporated, credit markets froze. But Energy Transfer had locked in long-term contracts with minimum volume commitments. While trading companies collapsed and leveraged producers went bankrupt, Energy Transfer's pipes kept flowing and their cash kept coming. They even managed to steal some distressed assets from desperate sellers.

By 2010, Energy Transfer controlled over 17,000 miles of pipeline, moved 7 billion cubic feet of gas daily, and generated over $1 billion in annual revenue. They'd gone from two guys with 200 miles of rusty pipe to one of America's largest midstream companies in just 14 years. But Warren wasn't satisfied. Natural gas prices remained depressed, and he could see the next transformation coming. The shale revolution wasn't just about gas—it was about liquids, and liquids were where the money was heading.

IV. The Transformation: From Gas to Everything (2010–2015)

The boardroom at Energy Transfer's Dallas headquarters was silent. It was 11 PM on a Friday in 2011, and Kelcy Warren had just proposed the unthinkable: spend $2 billion they didn't have to buy assets in a business they didn't understand from a French company most board members couldn't pronounce. Natural gas prices had cratered to $2 per million cubic feet, Energy Transfer's stock was getting hammered, and Warren wanted to bet the company on natural gas liquids.

"Gentlemen," Warren said, his Texas drawl more pronounced when he was excited, "Louis Dreyfus is desperate. They need out of these NGL assets tonight—I mean tonight. If we don't move now, Enterprise or Kinder Morgan will grab them by Monday. This is our chance to transform from a gas company to an everything company."

The Louis Dreyfus deal was classic Warren—audacious, perfectly timed, slightly insane. The French commodity giant had ventured into U.S. midstream during the boom, built world-class NGL infrastructure, then got cold feet when prices collapsed. Their Mont Belvieu fractionation facilities and pipeline network were hemorrhaging cash. Warren saw what others missed: shale wells produced not just methane but ethane, propane, butane—natural gas liquids worth far more than regular gas. As drilling shifted from dry gas to liquids-rich plays, whoever controlled NGL infrastructure would print money.

The board approved the deal at 2 AM. By Monday morning, Energy Transfer owned critical NGL assets that would generate $500 million in annual EBITDA within two years. Warren's instincts had been perfect—NGL demand exploded as petrochemical companies built massive ethane crackers along the Gulf Coast, feeding plastic production for global markets.

But the deal that truly transformed Energy Transfer—and revealed Warren's emotional side—came in 2012. Sunoco, the 125-year-old Philadelphia refining giant, was exiting the refining business and selling its logistics assets. For most buyers, this was just another distressed energy deal. For Warren, it was deeply personal.

"My father worked his entire career for Sun Pipeline," Warren told the board, his voice thick with emotion. "He maintained those lines, knew every valve, every compression station. Buying Sunoco isn't just business—it's bringing things full circle." The $5.3 billion acquisition added 7,900 miles of refined products pipelines, letting Energy Transfer move gasoline and diesel alongside natural gas and NGLs. More importantly, it gave Warren ownership of the very infrastructure where his father had labored for decades.

The Sunoco deal also brought something unexpected: retail operations. Suddenly Energy Transfer owned gas stations, convenience stores, the consumer-facing side of energy. Warren initially planned to sell these assets but realized they provided stable cash flow and a natural hedge against commodity volatility. When oil prices crashed, retail margins often expanded. It was another form of the spread arbitrage Warren loved.

The consolidation accelerated at a dizzying pace. Southern Union Company fell next—$9.4 billion including debt for 20,000 miles of pipeline connecting the Permian Basin to Florida. Warren was building a transcontinental network, each acquisition strategically chosen to fill gaps, create connections, enable new arbitrage opportunities. PennTex brought Terryville processing capacity. Susser Holdings added more retail. Regency Energy Partners, run by Warren's old colleague Mike Bradley, merged in, bringing gathering and processing assets across Texas and the mid-continent.

"We're not just buying pipelines," Warren explained to investors. "We're buying optionality. Every connection point, every storage cavern, every processing plant gives us another way to capture value as molecules move from wellhead to end user." The strategy was working—Energy Transfer's enterprise value ballooned from $10 billion to over $90 billion between 2010 and 2015.

The dual revenue strategy Warren had preached—volume and spreads—was firing on all cylinders. When gas prices were low, they made money on volume as producers pumped more to maintain cash flow. When prices spiked, they captured massive spreads between regions. The integrated network meant they could optimize across the entire hydrocarbon value chain—gathering, processing, fractionation, transportation, storage, even retail distribution.

But the rapid growth came with challenges. Integration was messy—different systems, cultures, contracts. Environmental violations piled up as Energy Transfer struggled to maintain assets acquired from distressed sellers. The company paid millions in fines for pipeline leaks, air quality violations, and safety incidents. Warren's response was typically blunt: "We're not perfect, but we're essential. You want heat in winter and gas in your car? Someone has to build and run these pipes."

By 2015, Energy Transfer had become exactly what Warren envisioned: not just a gas company but an everything company. They moved every hydrocarbon molecule America produced—natural gas, NGLs, crude oil, refined products. They operated in 38 states plus Canada. They'd gone from regional player to national champion in five years of relentless acquisition. But Warren's biggest, most controversial deal was just beginning to take shape in the Bakken shale of North Dakota.

V. Dakota Access: The Defining Controversy (2014–2017)

The meeting at the Bismarck Civic Center in December 2014 was supposed to be routine. Energy Transfer's engineers presented their planned route for the Dakota Access Pipeline—1,172 miles of 30-inch steel from North Dakota's Bakken shale to Illinois, where it would connect to Energy Transfer's existing network and flow to Gulf Coast refineries. The original route crossed the Missouri River just north of Bismarck. But when white residents raised concerns about their drinking water, the Army Corps of Engineers asked for alternatives. The engineers pulled up an alternate map—crossing instead near Standing Rock Sioux Reservation.

That map change would transform Energy Transfer from an obscure pipeline company into a household name, trigger the largest Native American protests in decades, and create a defining flashpoint in America's climate battles. It would also reveal exactly how far Warren was willing to go to complete a project.

By April 2016, a small camp had formed near Cannon Ball, North Dakota. LaDonna Brave Bull Allard, a Standing Rock historian, established Sacred Stone Camp on her property, inviting people to peacefully resist the pipeline. "Mni wiconi," became the rallying cry—Lakota for "water is life." The camps grew slowly at first—dozens, then hundreds, as summer temperatures rose and social media spread the word.

Warren initially dismissed the protests as "a small group of agitators." Energy Transfer had all its permits, had conducted archaeological surveys, had followed the legal process. But he fundamentally misread the moment. This wasn't just about one pipeline—it had become a symbol of indigenous rights, environmental justice, and resistance to fossil fuel infrastructure.

September 3, 2016, changed everything. On the Saturday of Labor Day weekend, Energy Transfer's construction crews showed up at a section of land where tribal archaeologists had just identified sacred sites and burial grounds. As bulldozers carved through the earth, protesters broke through the fence. Private security contractors from Frost Kennels released attack dogs. Video of blood-streaked protesters, snarling dogs, and sacred sites being destroyed went viral. Six protesters were treated for dog bites. The world was watching.

Warren's response was to double down. Energy Transfer hired TigerSwan, a military contractor founded by retired Army Colonel James Reese, who had run special operations in Iraq and Afghanistan. Internal documents later revealed TigerSwan described the protests as an "ideologically driven insurgency" and implemented "military-style counterterrorism measures." They flew drones over camps, infiltrated protest groups, and compiled detailed intelligence reports referring to water protectors as "jihadist fighters."

The camps swelled to thousands as autumn arrived. Military veterans joined in solidarity. Celebrities like Mark Ruffalo and Shailene Woodley showed up. The hashtag #NoDAPL trended globally. When police used water cannons in sub-freezing temperatures on November 20, injuring hundreds and nearly causing one woman to lose her arm, international condemnation poured in. UN human rights experts called for construction to halt.

Inside Energy Transfer, the pressure was immense. The company was burning $10 million weekly on security and delays. Banks financing the project faced protests and boycott threats. Warren remained defiant: "This pipeline is going to get built," he told investors. "We have the legal right, the economic need, and the political will." That political will was about to shift dramatically.

On December 4, 2016, President Obama's Army Corps of Engineers denied the crucial easement to cross under Lake Oahe, ordering a full environmental impact statement that could delay the project by years. Energy Transfer's stock plummeted. Warren was reportedly apoplectic, calling the decision "purely political." But he had an ace up his sleeve—he'd contributed $103,000 to Donald Trump's campaign, and Trump had invested between $500,000 and $1 million in Energy Transfer.

Four days after taking office, President Trump signed an executive memorandum directing the Army Corps to expedite approval. By February 7, 2017, the easement was granted. Within weeks, the camps were forcibly cleared by militarized police, and oil began flowing through Dakota Access by June 1. Warren had won, but at extraordinary cost—not just the $3.8 billion construction price but immeasurable reputational damage.

The aftermath continues reverberating. Multiple lawsuits challenged the permits. In 2020, a federal judge ordered the pipeline shut down pending environmental review, though appeals courts let it continue operating. In 2025, a remarkable verdict: a New York jury ordered Greenpeace to pay Energy Transfer approximately $660 million in damages for their role in the protests, finding the environmental group had conspired to delay construction through illegal means.

Warren remained unrepentant about Dakota Access, calling it "the most unfairly maligned infrastructure project in American history." The pipeline now moves 750,000 barrels daily, generating hundreds of millions in annual revenue. But the controversy fundamentally changed Energy Transfer's relationship with the public, transforming it from an unknown midstream company into a symbol of everything wrong—or right, depending on your perspective—with American energy infrastructure.

VI. The Political Machine: Power, Influence & Texas Politics

The lights went out across Texas at 1:47 AM on February 15, 2021. As an unprecedented arctic blast sent temperatures plummeting to single digits, the state's power grid collapsed. Millions of Texans huddled in freezing homes, burst pipes flooding their houses, desperately burning furniture for warmth. At least 246 people died. Meanwhile, in Energy Transfer's trading operations, dealers were having the most profitable week in company history.

As Texans froze and power prices spiked to the $9,000 per megawatt-hour regulatory cap—275 times normal—Energy Transfer's gas trading desk was printing money. The company would ultimately report $2.4 billion in gains from Winter Storm Uri, part of an estimated $11 billion in profits that natural gas companies extracted from the catastrophe. Warren called it "the market working as designed." Critics called it disaster profiteering.

Three months later, Warren cut a $1 million check to Governor Greg Abbott's campaign—four times his usual $250,000 contribution. The timing was purely coincidental, Energy Transfer insisted. But the donation fit a pattern of political investments that had paid dividends for decades. Since 2000, Warren personally and through Energy Transfer had contributed over $10 million to Texas politicians, with particularly generous support for those overseeing energy regulation.

Warren's political philosophy was straightforward: "I support politicians who support American energy." That translated to $6 million for Rick Perry's failed 2016 presidential campaign, where Warren served as finance chairman. When Perry flamed out, Warren quickly pivoted to Trump, contributing $103,000 and hosting fundraisers at his 8,000-square-foot Dallas mansion. After Trump's victory, Perry became Energy Secretary—a remarkable coincidence that benefited Energy Transfer's federal permitting efforts.

The 2020 election saw Warren go all-in, contributing $1.8 million to Trump's reelection effort and Republican causes. He hosted multiple fundraisers, including one where Trump reportedly promised to continue supporting pipeline construction. Warren's political generosity extended beyond federal races—he maxed out contributions to every member of the Texas Railroad Commission, the oddly named agency that regulated his pipelines.

In 2015, Governor Abbott appointed Warren to the Texas Parks and Wildlife Commission, a coveted position that seemed odd for a pipeline magnate until you realized it gave him influence over land use and conservation easements that could affect pipeline routes. Warren used the position to push for more "business-friendly" park management while also, to his credit, donating millions for conservation efforts including his spectacular 33,000-acre ranch transformation into wildlife habitat.

The regulatory capture was barely disguised. Railroad Commission members regularly attended Energy Transfer events, praised the company in public statements, and fast-tracked permits. When environmental groups challenged pipeline approvals, the commission reliably sided with Energy Transfer. One commissioner even admitted to reporters: "These are the companies that keep Texas running. We need to support them."

Environmental violations piled up, but penalties remained token. Energy Transfer accumulated hundreds of violations between 2015 and 2020—pipeline leaks, methane releases, contaminated water discharges. Total fines: less than $5 million against billions in annual profit. The EPA and state regulators seemed more interested in negotiating settlements than enforcing regulations. Warren's response to criticism was predictably combative: "We operate 125,000 miles of pipe. Things happen. But we're safer than trucks, trains, or any other way of moving energy."

The political protection proved invaluable during controversies. When Dakota Access faced federal scrutiny, Texas politicians rallied to Energy Transfer's defense. When environmentalists sued to block pipeline expansions, state attorneys general intervened on the company's behalf. When local communities tried to restrict pipeline construction, state legislators passed laws stripping them of that authority.

Warren understood that in Texas, energy and politics were inseparable. The state's economy depended on oil and gas, which provided hundreds of thousands of jobs and billions in tax revenue. Politicians who challenged the industry didn't last long. Those who supported it could count on generous campaign contributions and positive media coverage from industry-friendly outlets.

But the relationship went deeper than just transactional politics. Warren cultivated personal relationships with power brokers, hosting them at his ranch, attending their family events, becoming part of Texas's informal oligarchy. He served on civic boards with their spouses, donated to their favorite charities, hired their former staffers. It was a web of influence that made Energy Transfer essentially untouchable in Texas.

The February 2021 disaster and Energy Transfer's windfall profits did trigger some backlash. Congressional Democrats demanded investigations. But in Texas, the political machine Warren had helped build and fund ensured nothing changed. No windfall profit taxes, no increased regulations, no meaningful penalties. The legislature even passed laws making it easier to build gas infrastructure and harder to develop renewables—protecting Energy Transfer's market position for decades to come.

VII. Modern Empire: Scale, Scope & Strategy (2017–Today)

Stand at the Mont Belvieu complex on a humid Gulf Coast morning and you witness the hidden heart of American energy. Massive fractionation towers rise like steel cathedrals, processing 950,000 barrels of natural gas liquids daily. Underground, 120 million barrels of storage capacity sits carved into ancient salt domes. Rail cars and trucks queue endlessly while ships load at Energy Transfer's Nederland terminal, bound for plastics plants in China and power plants in India. This single complex—just one node in Energy Transfer's vast network—handles 20% of global NGL exports.

The numbers are staggering: 125,000 miles of pipeline, equivalent to circling Earth five times. Daily throughput of 30% of America's natural gas and petroleum. Export capacity from both Gulf and East Coast terminals—a capability only Energy Transfer possesses. The company moves 7.5 million barrels of crude oil, 15 billion cubic feet of natural gas, and 1.3 million barrels of NGLs every single day. It's an energy circulation system so vast and complex that even Warren sometimes seems amazed by what they've built.

The modern Energy Transfer emerged from relentless consolidation. The 2018 acquisition of Enable Midstream for $7.2 billion added another 14,000 miles of pipeline and crucial Anadarko Basin assets. Lotus Midstream brought Permian crude oil gathering. The $7.1 billion Crestwood Equity Partners deal in 2023—Warren's latest mega-acquisition—added premier positions in the Bakken, Powder River, and DJ basins. Each deal wasn't just about adding miles of pipe but creating network effects, connecting previously isolated systems into an integrated continental energy highway.

Warren stepped down as CEO in 2020, handing day-to-day operations to Mackie McCrea and Tom Long while remaining Executive Chairman and the company's largest investor with a 13% stake worth over $6 billion. "I'm 68 years old," Warren explained. "Time to let younger folks handle the daily blocking and tackling while I focus on strategy and capital allocation." But nobody doubted who really controlled Energy Transfer—Warren remained the visionary force, the dealmaker, the face of the empire.

The infrastructure moat Energy Transfer has built appears almost impregnable. Try to replicate their network today and you'd face decades of permitting battles, tens of billions in construction costs, and endless environmental lawsuits. The Dakota Access controversy ironically made their existing assets more valuable—new long-haul pipelines have become nearly impossible to build. Energy Transfer's pipes are like toll roads with no alternative routes, extracting fees from every molecule that needs to move from America's shale fields to global markets.

Financial performance reflects this dominance. Energy Transfer generated $89 billion in revenue and $5.3 billion in EBITDA for 2023. The MLP structure means most of this cash flows directly to unitholders—the distribution yield often exceeds 8%, attracting income-focused investors despite the environmental controversies. The units have returned over 400% since the 2020 pandemic lows, dramatically outperforming broader energy indices.

But challenges mount from every direction. Environmental lawsuits proliferate—indigenous groups, landowners, and environmental organizations have filed dozens of cases challenging everything from eminent domain takings to Clean Water Act violations. A federal judge's 2020 order to shut down Dakota Access, though ultimately reversed, showed how vulnerable even operating pipelines remain to legal challenges. Climate activists have made Energy Transfer a primary target, with protests at banks financing their operations and shareholder resolutions demanding emissions reductions.

Safety incidents continue plaguing operations. The Revolution Pipeline explosion in Pennsylvania destroyed homes and triggered evacuations. The Mariner East pipelines have leaked repeatedly, leading to criminal charges and hundreds of millions in fines. Energy Transfer's safety record—over 500 incidents since 2010—ranks among the worst in the industry. Warren's response remains consistent: "We move dangerous products safely 99.9% of the time. The media only covers the 0.1%."

The energy transition poses existential questions Warren seems unwilling to fully confront. Electric vehicles, renewable power, and hydrogen could eventually strand Energy Transfer's fossil fuel infrastructure. Warren's public position remains defiantly skeptical: "Wind and solar are intermittent toys. The world runs on hydrocarbons and will for decades." But privately, Energy Transfer has begun hedging—investing in renewable diesel infrastructure, exploring carbon capture projects, and discussing hydrogen transport capabilities.

Recent acquisitions suggest a strategy of doubling down on hydrocarbons while they remain essential. The Crestwood deal deepened Energy Transfer's position in premium basins where production economics remain favorable even at lower prices. Expansion projects focus on export capacity—the Lake Charles LNG terminal, Nederland terminal expansions—betting that global demand for American energy will grow even as domestic consumption potentially peaks.

The modern Energy Transfer is thus a paradox: an essential company operating irreplaceable infrastructure that society increasingly views as incompatible with climate goals. Warren has built an empire that generates enormous cash flows, wields significant political influence, and controls critical energy arteries. But it's an empire facing questions about its long-term viability that no amount of political contributions or pipeline acquisitions can fully answer.

VIII. Playbook: Business & Investing Lessons

Study Energy Transfer's ascent and a clear playbook emerges—one that transformed two wildcatters with 200 miles of pipe into masters of a continental energy empire. The strategies aren't subtle, but their execution has been devastatingly effective.

The Consolidation Playbook stands as Warren's signature achievement. The formula: identify distressed sellers facing bankruptcy or strategic exits, move with lightning speed when others hesitate, pay prices that seem cheap in hindsight but risky at signing. The Louis Dreyfus deal exemplified this—a Friday night emergency board meeting to grab $2 billion in NGL assets that would generate $500 million in annual EBITDA within two years. Warren understood that in distressed situations, speed beats perfection. "You can always fix integration problems," he'd say. "You can't fix missing the deal."

But consolidation without integration is just empire building. Energy Transfer's secret sauce was operational optimization post-acquisition. They'd buy underutilized assets, then immediately connect them to their existing network, creating new flow patterns and arbitrage opportunities. Southern Union's pipelines became more valuable connected to Energy Transfer's system than they ever were standalone. Each acquisition multiplied the value of previous acquisitions—network effects in steel and valves.

The MLP Advantage provided the financial engineering that made everything possible. Master Limited Partnerships avoid corporate taxes while providing tax-advantaged distributions to investors. This structure gave Energy Transfer a lower cost of capital than traditional corporations, letting them outbid competitors for assets. The complexity that scared away some investors—K-1 tax forms, incentive distribution rights, general partner economics—became a moat protecting Energy Transfer from activists and hostile takeovers.

Warren also mastered the art of dropdown transactions—selling assets from the parent company to affiliated MLPs at attractive valuations, creating multiple bites at the apple. He'd buy assets at distressed prices, improve operations, then drop them into publicly traded MLPs at higher multiples. Financial engineering at its finest, though critics called it self-dealing.

Warren's Leadership Style—"bold, agile, and inventive" as colleagues described it—shaped the company's DNA. He combined an engineer's attention to detail with a riverboat gambler's risk appetite. Warren would personally review pipeline routes, study basis differentials between markets, and understand the technical minutiae. But he'd also bet billions on weekend handshake deals, trusting his instincts over investment banking analysis.

His approach to controversy was equally distinctive: never apologize, always attack. When environmentalists protested, Warren sued them. When regulators pushed back, he hired their former colleagues. When communities resisted pipelines, he lobbied for state laws overriding local authority. This combativeness created enemies but also sent a message: fighting Energy Transfer would be long, expensive, and probably futile.

Infrastructure as Irreplaceable Assets became Warren's core insight. In technology, competitive advantages erode quickly. In energy infrastructure, they compound over decades. Every year that passes without new pipeline construction makes existing pipes more valuable. Environmental opposition that Warren fought actually strengthened his moat—protesters made new pipelines nearly impossible, granting monopoly power to existing operators.

The company treated pipelines like toll roads, storage caverns like parking garages, processing plants like mandatory inspection stations. Once hydrocarbons entered Energy Transfer's system, the company found multiple ways to extract fees—gathering, treating, processing, fractionating, storing, transporting. They called it the "value chain strategy," but it was really about creating unavoidable tollbooths.

Political Capital as Business Strategy distinguished Energy Transfer from peers who viewed lobbying as a necessary evil. Warren saw political relationships as assets to be invested in and cultivated. The $10 million in political contributions over two decades bought more than access—it bought protection, favorable regulations, and swift permit approvals. When Warren needed something from government, he didn't send lobbyists; he called personal cell phones.

This extended beyond simple contributions. Warren understood that in Texas, business and politics formed an ecosystem. He joined the right boards, attended the right galas, hired the right former officials. Energy Transfer became woven into the state's power structure so thoroughly that attacking the company meant attacking Texas itself.

Managing Through Commodity Cycles revealed Warren's deepest wisdom. Energy markets are viciously cyclical—boom to bust in months. Warren positioned Energy Transfer to profit regardless of commodity prices. Low prices? Producers pump more volume to maintain cash flow, filling Energy Transfer's pipes. High prices? Energy Transfer captures massive basis differentials between regions. Price volatility? Energy Transfer's storage assets become ATMs as traders pay premiums for optionality.

The fee-based model—where shippers pay for capacity regardless of usage—provided stability through downturns. Take-or-pay contracts meant revenue kept flowing even when drilling stopped. This contrasted sharply with upstream producers who lived and died by commodity prices. Energy Transfer surfed above the chaos, collecting tolls regardless of market turmoil.

Capital Allocation Discipline—or occasional lack thereof—marked Warren's evolution as a CEO. Early acquisitions were surgically precise, each filling specific gaps. Later deals sometimes seemed driven by empire-building impulses. The $37 billion attempt to merge with Williams Companies in 2016, which Warren ultimately sabotaged through bizarre legal maneuvers, suggested he'd begun believing his own invincibility.

But Warren generally maintained discipline where it mattered: leverage ratios, distribution coverage, and maintaining investment-grade ratings at key subsidiaries. He understood that in capital-intensive industries, access to cheap debt determines winners and losers. Energy Transfer's ability to raise billions at attractive rates, even during controversies, reflected bankers' confidence in the irreplaceable nature of their assets.

IX. Analysis & Bear vs. Bull Case

The investment case for Energy Transfer splits minds like few companies can. Bulls see irreplaceable infrastructure generating growing cash flows for decades. Bears see stranded assets facing existential climate risks. Both are right—and that's what makes Energy Transfer fascinating.

The Bull Case starts with physical reality: America produces 13 million barrels of oil and 100 billion cubic feet of natural gas daily, and virtually all of it must flow through pipelines to reach markets. Energy Transfer controls the critical arteries—not just random pipelines but strategic chokepoints connecting major basins to demand centers. Try building competing infrastructure today and you'd face 10-15 years of permitting battles and tens of billions in costs. The moat isn't just wide; it's essentially uncrossable.

The export story becomes increasingly compelling. Global LNG demand is projected to double by 2040 as Asia shifts from coal to gas. Energy Transfer's Gulf Coast position—with Nederland's export capacity and the planned Lake Charles LNG terminal—positions them to capture enormous value from American energy feeding global growth. Their unique ability to export from both Gulf and East Coast terminals provides unmatched optionality as global trade patterns shift.

Network effects compound value daily. Every new connection point, every acquisition, makes the existing network more valuable. The Crestwood acquisition didn't just add Bakken gathering—it created new pathways from Bakken crude to Gulf Coast refiners, from Powder River gas to Midwest markets. These aren't just pipelines; they're an integrated continental energy system that becomes more essential as complexity increases.

The energy transition, paradoxically, might strengthen Energy Transfer's position medium-term. Renewable electricity requires natural gas backup for intermittency. Plastics and petrochemicals—fed by Energy Transfer's NGL systems—face growing demand from developing nations. Even in net-zero scenarios, the International Energy Agency projects substantial hydrocarbon usage through 2050. Energy Transfer's infrastructure could be repurposed for hydrogen or carbon capture, extending asset life beyond fossil fuels.

Financially, the numbers are compelling. Trading at 7-8x EBITDA versus historical averages of 10-12x, the units appear cheap. The distribution yield exceeding 8% attracts income investors in a low-yield world. Free cash flow after distributions is growing, enabling debt reduction and opportunistic buybacks. If Energy Transfer simply maintains current operations without growth, investors could see 15%+ annual returns from distributions and modest multiple expansion.

The Bear Case sees the same facts through a darker lens. Climate policy represents an existential threat that markets haven't fully priced. The Inflation Reduction Act's massive renewable subsidies, state clean energy mandates, and potential federal carbon pricing could crater hydrocarbon demand faster than expected. Europe's rapid pivot from Russian gas showed how quickly energy systems can transform under pressure.

Legal liabilities proliferate beyond manageable levels. Indigenous groups have valid treaty claims that courts increasingly recognize. Environmental lawsuits multiply with each spill and explosion. The $660 million Greenpeace verdict, while a victory, demonstrates how Dakota Access created permanent opposition. Future projects face insurmountable resistance—witness the decades-long failure to build Keystone XL.

Stranded asset risk looms larger than management admits. Electric vehicle adoption could eliminate 30% of oil demand by 2040. Renewable electricity plus batteries increasingly outcompete gas plants. Green hydrogen could replace natural gas in industrial processes. Energy Transfer's 125,000 miles of pipeline could become 125,000 miles of stranded steel, generating massive decommissioning liabilities instead of cash flows.

ESG exclusions increasingly constrain capital access. Major banks have stopped financing Energy Transfer projects. Institutional investors face pressure to divest. Insurance companies refuse coverage for certain operations. As capital becomes scarcer and more expensive, Energy Transfer's cost advantage evaporates. The MLP structure, once an advantage, now signals "uninvestable" to ESG-focused allocators.

Safety and operational issues suggest deeper problems. Five hundred incidents since 2010 isn't just bad luck—it suggests systematic underinvestment in maintenance as Energy Transfer prioritized growth over safety. Aging infrastructure requires massive capital just to maintain, let alone improve. The Revolution Pipeline explosion and Mariner East leaks demonstrate how one catastrophic incident could trigger billions in liabilities and permanent shutdowns.

Management's combative approach creates unnecessary risks. Warren's scorched-earth tactics—suing Greenpeace, fighting regulators, dismissing environmental concerns—might have worked in 2010s Texas but seem dangerously outdated for the 2020s. The next Democratic administration could make Energy Transfer a poster child for climate action, using executive orders to halt operations that courts previously approved.

The Texas concentration poses underappreciated risks. Energy Transfer depends on Texas's political protection and regulatory favoritism. But Texas itself faces climate vulnerabilities—drought threatening water-intensive fracking, hurricanes disrupting Gulf Coast infrastructure, grid failures revealing systemic fragility. Demographics and politics are shifting even in Texas. Energy Transfer's political moat could evaporate faster than its physical one.

The Verdict depends entirely on timeline and worldview. For investors believing hydrocarbons remain essential through 2040, Energy Transfer offers remarkable value—irreplaceable assets trading at distressed multiples with growing cash flows. For those seeing rapid energy transition, it's a melting ice cube—superficially cheap but fundamentally impaired. The truth likely lies between extremes: Energy Transfer will generate substantial cash flows for years, perhaps decades, but terminal value assumptions that underpin traditional valuations may prove illusory.

X. Epilogue & "If We Were CEOs"

The conference room at Energy Transfer's Dallas headquarters offers a commanding view of the city Kelcy Warren helped power—gleaming towers built on oil money, highways clogged with gasoline-burning cars, a sprawling metropolis that couldn't exist without the hydrocarbons flowing through Energy Transfer's pipes. Warren, now 69, still occupies the executive chairman's office, his desk cluttered with pipeline maps and acquisition targets. The empire he built seems simultaneously permanent and precarious, essential and endangered.

What would different strategic choices look like if we were running Energy Transfer today? The bold move would be radical transformation: announce a 20-year transition plan to become America's premier energy infrastructure company, not just hydrocarbon infrastructure. Leverage the irreplaceable rights-of-way to lay hydrogen pipelines alongside natural gas. Convert storage caverns for hydrogen and compressed air energy storage. Build the carbon capture and transport infrastructure that heavy industry will desperately need. The pipeline network that moves fossil fuels today could move the clean molecules of tomorrow.

The financial engineering would be complex but achievable. Create a new subsidiary focused on energy transition infrastructure, qualify it for Inflation Reduction Act benefits, attract ESG capital priced out of traditional Energy Transfer. Use cash flows from legacy operations to fund transformation. Partner with renewable developers who need firm transmission for green hydrogen projects. The same political influence that protected fossil infrastructure could accelerate clean infrastructure permitting.

But this transformation requires something Warren seems incapable of: acknowledging that the fossil fuel era, while not ending tomorrow, is beginning its decades-long descent. His pugilistic style—perfect for building an empire in Texas's anything-goes energy market—seems poorly suited for navigating an energy transition requiring collaboration with environmentalists, communities, and clean energy advocates.

A different leader might pursue the "fortress strategy"—accept that Energy Transfer is a declining but highly cash-generative business, maximize distributions to investors while the getting is good, and prepare for elegant retreat rather than ugly stranding. Stop acquiring, start divesting marginal assets, return every penny to unitholders, and give investors clarity that this is a 15-20 year harvesting operation, not a perpetual growth story.

Or perhaps the answer is selective transformation. Keep the Gulf Coast NGL and petrochemical infrastructure that will thrive regardless of energy transition—plastics aren't disappearing anytime soon. Divest the long-haul crude pipelines most vulnerable to stranding. Double down on the last-mile distribution that will handle whatever fuel vehicles ultimately use. This "barbell strategy" maintains upside while reducing downside, though it lacks the bold vision Warren typically embraces.

Warren's legacy defies simple categorization. He built essential infrastructure that powered American prosperity, created thousands of jobs, and generated hundreds of billions in wealth. The shale revolution that restored American energy independence couldn't have happened without pipelines like Energy Transfer's. Every American who heated their home last winter or drove to work this morning benefited from Warren's empire.

Yet that same empire contributed to climate change, trampled indigenous rights, and corrupted political processes. The images from Standing Rock—water protectors facing attack dogs, elders praying before bulldozers, militarized police defending pipeline construction—will forever mark Energy Transfer as a symbol of corporate power crushing community resistance. The $2.4 billion Energy Transfer extracted during Texas's deadly freeze epitomizes disaster capitalism at its worst.

History might remember Warren as the last great fossil fuel empire builder, the Texas wildcatter who consolidated an entire industry just as that industry began its terminal decline. Or perhaps as a visionary who understood that civilization runs on energy, that someone must build and operate the ugly infrastructure that enables modern life, that pragmatism beats idealism when winter arrives and furnaces need fuel.

The future of American energy infrastructure will be written by forces beyond any CEO's control—technological breakthroughs, climate impacts, political upheavals, social movements. But companies like Energy Transfer, and leaders like Warren, will shape how that transition unfolds—whether gracefully or violently, whether capturing value or destroying it, whether accelerating progress or defending the past.

Can Energy Transfer navigate the energy transition? The assets suggest yes—rights-of-way are eternal, steel can be repurposed, and engineering expertise translates across molecules. The culture suggests no—Warren's combative style, the company's fossil fuel identity, and the accumulated enemies seem insurmountable barriers to transformation. Most likely, Energy Transfer muddles through—generating cash for another decade or two, fighting rearguard actions against climate policies, slowly shrinking as the energy system transforms around it.

Warren recently told investors, "I'll be gone before these pipelines stop flowing." He's probably right. But the empire he built—those 125,000 miles of steel veins carrying America's energy lifeblood—will outlive him by decades, either as essential infrastructure adapted for a clean energy future or as rusting monuments to the hydrocarbon age. The choice isn't entirely Warren's anymore, but how Energy Transfer navigates the next decade will determine which fate awaits his pipelines.

The story of Energy Transfer is really the story of American energy—how we power our civilization, who controls that power, and what prices we're willing to pay. It's a story without heroes or villains, just humans building the infrastructure they believe necessary, fighting for the future they think possible, and reckoning with consequences they couldn't fully foresee. Kelcy Warren built an empire moving molecules through pipes. What moves through those pipes next—and whether those pipes move anything at all—will define not just Energy Transfer's future but America's energy future itself.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube