Gujarat State Petronet Limited: India's Gas Pipeline Pioneer

I. Introduction & Episode Roadmap

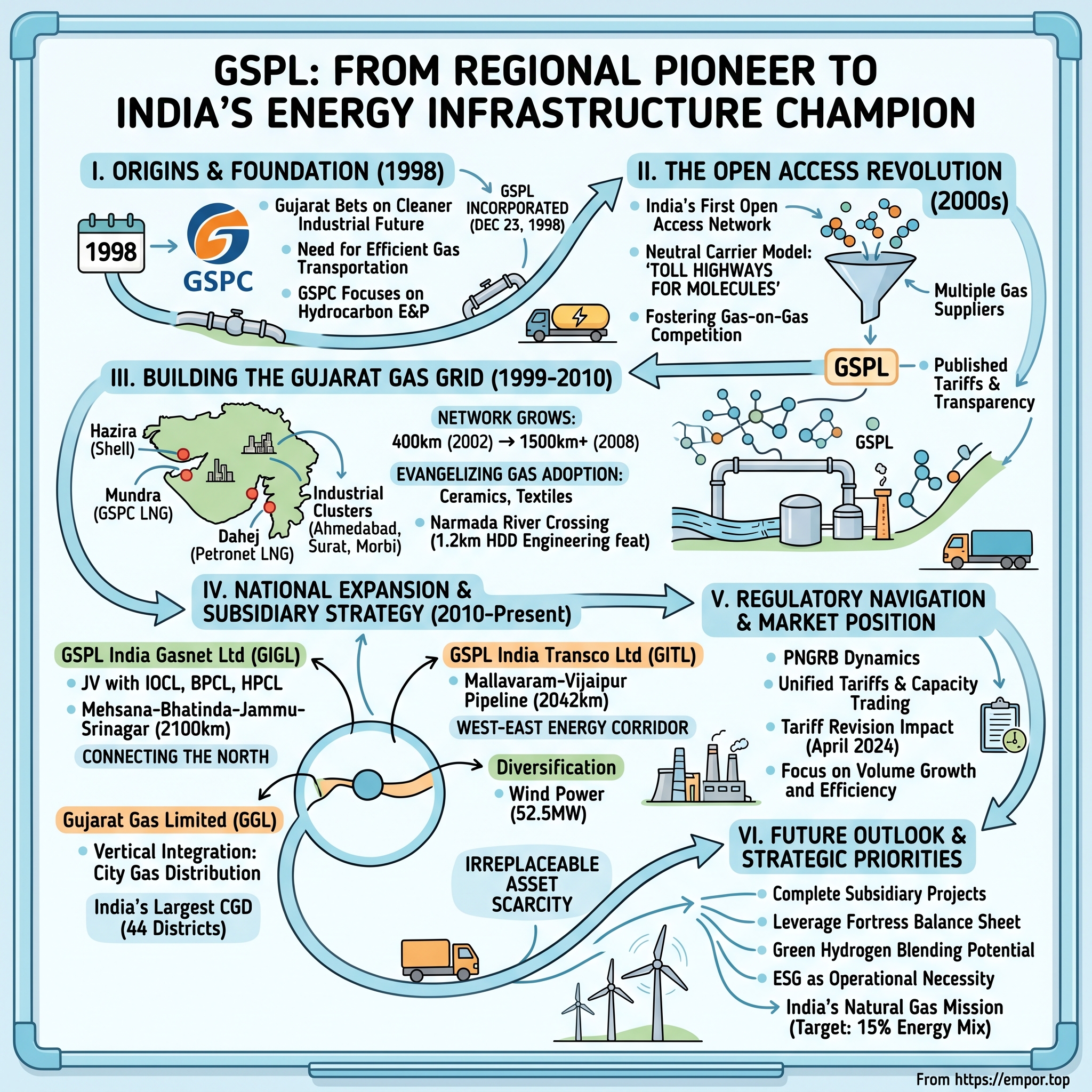

Picture this: It's 1998, and Gujarat—India's westernmost state—is betting its industrial future on a resource that most of the country barely understands: natural gas. While the rest of India burns coal and oil, Gujarat's leaders envision a cleaner, more efficient energy backbone. They need someone to build the pipes that will carry this vision. Enter Gujarat State Petronet Limited.

Today, GSPL commands a ₹17,000+ crore market capitalization, operates over 2,700 kilometers of high-pressure pipelines, and stands as India's second-largest natural gas transmission player. But here's what makes this story remarkable: GSPL became India's first open-access gas transmission network—a radical concept in a country where state monopolies controlled energy infrastructure. Instead of owning the gas or dictating who could use their pipes, GSPL built highways for molecules, letting any supplier connect with any customer.

The question that drives this entire narrative: How did a state-backed pipeline company in Gujarat transform from a regional utility into a national energy infrastructure champion? And more intriguingly, how did they pull this off while maintaining government control, navigating byzantine regulations, and competing against the might of GAIL—India's gas behemoth?

This is a story about infrastructure as strategy. About how building pipes in the right places at the right time can create extraordinary value. About the delicate dance between government ownership and commercial excellence. And ultimately, about how natural gas—once an afterthought in India's energy mix—became central to the nation's cleaner energy transition.

What unfolds is a masterclass in patient capital deployment, regulatory navigation, and the power of network effects in physical infrastructure. As we'll see, GSPL's journey mirrors Gujarat's own economic transformation—from a regional industrial hub to India's growth engine. The company's evolution from a simple pipeline operator to a complex web of subsidiaries spanning the subcontinent reveals profound lessons about building critical infrastructure in emerging markets.

The threads we'll follow include the visionary leadership that saw opportunity where others saw risk, the technical challenges of building pipelines across diverse terrain, the regulatory battles that defined the industry's structure, and the financial engineering that turned steel pipes into consistent cash flows. We'll examine how GSPL navigated the transition from monopoly to competition, from regional to national, from traditional energy to the bridge fuel of the future.

This isn't just a corporate history—it's a window into India's energy transformation, told through the lens of the company that helped make it possible. Let's dive into how a handful of engineers and bureaucrats in Gandhinagar built the arteries through which modern Gujarat's industrial heart beats.

II. Origins & the GSPC Connection

The conference room in Gandhinagar was thick with cigarette smoke on that December day in 1998. Officials from Gujarat State Petroleum Corporation (GSPC) huddled around architectural drawings and feasibility studies. The challenge before them: Gujarat had discovered natural gas, GSPC was pulling it from the ground, but there was no way to move it efficiently to the factories and power plants desperate for cleaner fuel. "We need our own transmission company," someone finally said. "One that just moves the gas—doesn't produce it, doesn't sell it to end users. Just moves it." It was a radical simplification that would define GSPL's destiny.

To understand GSPL's birth on December 23, 1998, you need to understand its parent—Gujarat State Petroleum Corporation. GSPC's own journey began two decades earlier, incorporated in 1979 as a petrochemical company when Gujarat was trying to leverage its proximity to Mumbai's offshore oil fields. The company wandered through various industrial experiments until 1994, when it was rechristened as Gujarat State Petroleum Corporation with a focused mandate: find and develop Gujarat's hydrocarbon resources.

By the late 1990s, GSPC had achieved modest success in gas exploration, particularly in the Cambay basin. But success created a new problem. Gas, unlike oil, can't be easily trucked around. It needs pipelines—expensive, permanent, regulated pipelines. GSPC's leadership recognized a fundamental truth: exploration and transmission are different businesses requiring different expertise, capital structures, and regulatory relationships. Thus, GSPL was conceived not as a subsidiary but as a complement—while GSPC would harness and procure natural gas, GSPL would build the highways to carry it.

The ownership structure revealed the state's strategic thinking. GSPC would hold the majority stake, ensuring government control, but GSPL would operate as a commercially driven entity. This wasn't just about moving molecules; it was about Gujarat's broader vision for energy independence and industrial competitiveness. Chief Minister Keshubhai Patel and his successors saw natural gas as Gujarat's comparative advantage—cleaner than coal, cheaper than oil, and increasingly available from both domestic fields and imported LNG.

The early team at GSPL was a mix of GSPC veterans and fresh engineering talent recruited from oil sector PSUs. They faced a monumental task: creating gas transmission infrastructure in a market that barely existed. India's gas consumption in 1998 was minuscule—less than 30 billion cubic meters annually, compared to over 500 BCM in the US. Most industrialists didn't understand natural gas economics. Environmental regulations were nascent. The Petroleum and Natural Gas Regulatory Board wouldn't even exist for another eight years.

What GSPL's founders did have was political backing and patient capital. The Gujarat government understood infrastructure's long gestation periods. They were building for a future where gas would matter, even if that future seemed distant in 1998. The initial business plan was modest—connect GSPC's gas fields to a handful of industrial customers in central Gujarat. Nobody imagined they were laying the foundation for what would become a 2,700-kilometer network worth ₹17,000 crores.

The incorporation documents reveal interesting details about ambition and pragmatism. GSPL's authorized capital was set at ₹500 crores—substantial for a startup but modest for an infrastructure company. The company's stated objectives were deliberately broad: transmission of natural gas, but also "any other business incidental or conducive to the attainment of the above objects." That seemingly boilerplate language would later enable diversification into wind power and other ventures.

Those early days established cultural DNA that persists today. Unlike GAIL, which emerged from the grand central planning of the Oil & Natural Gas Commission, GSPL was scrappy and entrepreneurial. They had to convince customers to switch to gas, negotiate with landowners for right-of-way, and manage construction with minimal precedent. This wasn't infrastructure by decree; it was infrastructure by persuasion.

As 1999 dawned, GSPL commenced operations with its first transmission of GSPC-supplied gas. The volumes were tiny—barely a trickle by today's standards—but the pipes were being laid, literally and figuratively, for Gujarat's industrial transformation. The question now was whether they could build fast enough to capture the opportunity they sensed was coming.

III. Building the Gujarat Gas Grid (1998–2010)

The bulldozers started rolling across Gujarat's countryside in early 1999, carving paths for what locals called "the steel serpent"—GSPL's first major pipeline. Village heads gathered, suspicious and curious, as engineers explained they were laying pipes that would carry "cooking gas for factories." Most had never seen industrial natural gas infrastructure. One elderly farmer in Mehsana reportedly asked, "If it leaks, will my crops burn?" The education process was as complex as the construction itself.

GSPL's early operational challenges read like an infrastructure thriller. Creating a gas transmission network in a nascent market meant solving problems nobody had properly defined. The technical hurdles were staggering: Gujarat's diverse terrain ranged from the marshy Rann of Kutch to the rocky Aravalli foothills. Monsoons turned construction sites into swamps. Summer temperatures exceeded 45°C, making steel expansion a constant calculation. They were essentially writing the playbook while playing the game.

But the real innovation wasn't technical—it was conceptual. In 2003, GSPL made a decision that would define its trajectory: it would operate on an "open access" basis. This meant any gas supplier could book capacity to any customer, with GSPL acting as a neutral carrier. Think of it as the difference between a private road and a toll highway. While GAIL operated more like the former—controlling both the pipes and much of the gas flowing through them—GSPL chose to be the latter.

This open access model was revolutionary in Indian energy infrastructure. It required sophisticated IT systems to track multiple suppliers' gas, complex commercial agreements, and most importantly, trust. Early customers were skeptical. "How do we know you won't favor GSPC's gas over ours?" asked executives from Hazira's private gas producers. GSPL's answer was transparency—published tariffs, non-discriminatory access rules, and real-time flow data. They were building credibility one molecule at a time.

The network expansion strategy revealed sophisticated thinking about network effects. Rather than building random connections, GSPL focused on creating a "gas grid"—interconnected pipelines that created multiple pathways between sources and consumers. The master plan connected four critical nodes: Hazira (where private producers and Shell operated), Dahej (home to Petronet LNG's massive import terminal), Mundra (where GSPC would later build its LNG terminal), and the industrial clusters of Ahmedabad, Vadodara, and Surat.

By 2005, GSPL had achieved something remarkable: they were moving gas from competing suppliers through the same pipes to competing customers. A fertilizer plant in Vadodara could buy gas from Shell's Hazira terminal in the morning and GSPC's fields in the afternoon, with GSPL handling the transmission seamlessly. This flexibility became GSPL's calling card, attracting customers who valued optionality over captive supply.

The numbers tell a story of methodical growth. From virtually zero in 1999, GSPL's pipeline network reached 400 kilometers by 2002, 900 kilometers by 2005, and crossed 1,500 kilometers by 2008. But raw distance understates the achievement. Each kilometer required negotiations with hundreds of landowners, dozens of environmental clearances, and complex engineering to cross rivers, highways, and existing infrastructure. The Narmada River crossing alone—a 1.2-kilometer horizontal directional drilling project—took 18 months and became a case study in Indian engineering institutes.

The customer acquisition strategy was equally deliberate. GSPL didn't just wait for customers to come; they evangelized gas adoption. Teams visited textile mills in Surat, explaining how gas-fired boilers were cleaner and more efficient than coal. They worked with ceramic factories in Morbi, demonstrating cost savings from switching from furnace oil. By 2007, GSPL was serving 50+ industrial customers across sectors—refineries, steel plants, fertilizer units, petrochemical complexes, and power plants. The customer base read like a who's who of Gujarat industry: Reliance, Essar, GSFC, Torrent Power.

Regulatory navigation during this period was an art form. With no formal regulator until PNGRB's establishment in 2006, GSPL operated in a grey zone, setting its own technical standards and commercial practices. They adopted international pipeline standards, hired former Oil India executives as advisors, and essentially regulated themselves. When PNGRB finally arrived, GSPL's practices became the template for national regulations—a classic case of industry leading policy.

The 2008 global financial crisis tested GSPL's resilience. Industrial gas demand crashed as factories shut down. Pipeline utilization fell below 40%. But instead of retrenching, GSPL accelerated expansion, taking advantage of lower construction costs and available labor. "When others were fearful, we were greedy for infrastructure," a former executive recalled, channeling Warren Buffett. This countercyclical investment paid off magnificently when demand roared back in 2009-10.

By 2010, GSPL had transformed from a startup to Gujarat's energy backbone. The network had grown to 2,000+ kilometers, customer base exceeded 100, and daily transmission volumes reached levels that seemed fantasical a decade earlier. More importantly, they had proved the open access model worked—efficient, transparent, and profitable. The question now was whether this Gujarat success story could scale nationally.

IV. The Open Access Revolution & Expansion Era (2010–2018)

The boardroom at GSPL's Gandhinagar headquarters buzzed with nervous energy in March 2010. The presentation slide showed an audacious vision: "From Gujarat Gas Grid to National Presence." Someone had drawn red lines extending from Gujarat into Rajasthan, Madhya Pradesh, and beyond. "This is our moment," the CEO declared. "We've proven open access works. Now we take it national." The room knew they were declaring war on GAIL's monopoly, but they also knew they had something GAIL didn't—a proven model of neutral, efficient transmission.

The pure transmission network model that GSPL perfected was elegantly simple yet revolutionary for India. Unlike integrated players who produced, transmitted, and marketed gas, GSPL did one thing: move molecules from Point A to Point B, charging a toll for the service. This focus created unexpected advantages. Without upstream or downstream conflicts, industrial customers trusted GSPL's neutrality. Without marketing teams competing for the same customers, suppliers saw GSPL as an enabler, not a rival.

The numbers from this expansion era are staggering. GSPL's customer base mushroomed from 50 in 2010 to 102+ by 2018. The customer roster evolved too—beyond traditional industries, GSPL was now serving city gas distribution networks, CNG stations, even small-scale LNG plants. Daily transmission volumes doubled, then doubled again. The company was moving more gas through Gujarat than some countries consumed annually.

But the real story was in the connections GSPL forged. The Hazira hub became a masterpiece of energy infrastructure—pipes from multiple gas fields converging with Shell's Hazira terminal, creating India's first truly competitive gas market. At Dahej, GSPL's connections to Petronet LNG's terminal (which expanded from 5 to 15 million tons per annum during this period) made imported gas accessible to inland industries that had never dreamed of accessing global LNG markets. The GSPC LNG terminal at Mundra, commissioned in 2018, added another import option, with GSPL's pipes ready from day one.

Here's where GSPL's strategic thinking shone. While others saw gas terminals as endpoints, GSPL saw them as nodes in an emerging network. They built interconnections between terminals, creating redundancy and flexibility. A factory in Ahmedabad could now source gas from domestic fields, Dahej LNG, Hazira LNG, or Mundra LNG—all through GSPL's integrated grid. This optionality commanded premium transmission rates and created switching costs that locked in customers.

The 2012 diversification into wind power initially puzzled analysts. Why would a pipeline company build windmills? The answer revealed sophisticated portfolio thinking. Wind power generation (52.5 MW capacity across Gujarat's coastal areas) provided non-regulated returns, hedged against transmission volume volatility, and demonstrated GSPL's commitment to cleaner energy. The windmills also powered GSPL's own compressor stations, reducing operating costs and carbon footprint—ESG before ESG was fashionable.

GSPL's operational excellence during this period deserves examination. Pipeline capacity utilization averaged above 80%—exceptional in a country where infrastructure assets often operated at half capacity. System losses were below 0.5%, comparing favorably with international standards. They achieved 99.9% uptime, critical for customers running continuous manufacturing processes. This reliability became GSPL's moat—customers paid premium rates knowing gas would flow when promised.

The human capital story paralleled the physical expansion. GSPL recruited aggressively from IITs and top engineering colleges, unusual for a state-controlled entity. They sent engineers to Houston and Rotterdam for training. The company culture blended public sector stability with private sector ambition. Performance bonuses were tied to capacity additions and utilization rates, not just years of service. This merit-based approach attracted talent that might otherwise have joined Reliance or Shell.

Technology adoption accelerated during this period. GSPL implemented SCADA (Supervisory Control and Data Acquisition) systems across the network, enabling real-time monitoring from Gandhinagar. Predictive maintenance algorithms reduced downtime. Customer portals allowed online capacity booking and payment. They were digitizing before "digital transformation" became a buzzword, driven by operational necessity rather than fashion.

The regulatory relationship with PNGRB evolved from suspicion to grudging respect. GSPL's transparent operations and willingness to share data made them PNGRB's unofficial laboratory for policy experiments. When PNGRB wanted to test new tariff mechanisms, they piloted with GSPL. When international delegations visited, PNGRB showcased GSPL's operations. This regulatory goodwill would prove invaluable in future expansion approvals.

By 2018, GSPL had achieved what seemed impossible a decade earlier—they had made Gujarat India's most "gassed" state, with natural gas contributing over 25% of the state's energy mix versus less than 7% nationally. Industrial customers who had initially resisted gas adoption now couldn't imagine operating without it. The Gujarat Gas Grid wasn't just infrastructure; it had become essential plumbing for the state's economy.

The transformation was complete: GSPL had evolved from a regional pipeline operator to a sophisticated energy infrastructure company. But the biggest moves were yet to come. The subsidiary strategy brewing in corporate planning rooms would attempt something even more audacious—replicating the Gujarat miracle across India.

V. Subsidiary Strategy & National Expansion (2015–Present)

The PowerPoint slide was simple—three boxes labeled GIGL, GITL, and GGL, with arrows spreading across India's map like a spider web. It was 2015, and GSPL's strategy team was presenting their national expansion blueprint. "We can't build everything ourselves," the head of corporate development explained. "But we can partner, structure, and replicate." This wasn't just geographic expansion; it was financial engineering meets infrastructure development. The room was about to witness the birth of GSPL's subsidiary empire.

GSPL India Gasnet Limited (GIGL) emerged as the crown jewel of this strategy. Formed as a joint venture with Indian Oil Corporation (IOCL), Bharat Petroleum (BPCL), and Hindustan Petroleum (HPCL), GIGL represented something unprecedented—private sector efficiency with public sector reach. The Mehsana-Bhatinda-Jammu-Srinagar pipeline project, spanning 2,100 kilometers, wasn't just about laying pipes; it was about connecting India's energy-starved north to the gas age. The route was audacious—through Rajasthan's deserts, Punjab's agricultural heartland, and up into Kashmir's volatile terrain.

The GIGL structure revealed sophisticated thinking about risk and capital. By bringing in oil marketing companies as partners, GSPL secured not just capital but also assured gas demand—these partners controlled refineries and retail networks that would need gas. The equity structure (GSPL: 52%, IOCL: 26%, BPCL: 11%, HPCL: 11%) ensured GSPL maintained control while sharing project risks. The ₹6,000+ crore project would have strained GSPL's balance sheet if undertaken alone; through GIGL, they achieved the expansion with minimal capital commitment.

GSPL India Transco Limited (GITL) tackled an even more ambitious project—the Mallavaram-Bhopal-Bhilwara-Vijaipur pipeline, stretching 2,042 kilometers from Andhra Pradesh through Telangana, Maharashtra, Madhya Pradesh, to Rajasthan. This wasn't just about distance; it was about connecting India's east coast gas supplies to northern demand centers, creating the country's first true west-east gas corridor. GITL's pipeline would intersect with GAIL's network at multiple points, creating competition and redundancy that benefited end consumers.

The technical challenges GITL faced were extraordinary. The pipeline crossed the Vindhya and Satpura mountain ranges, requiring sophisticated engineering. Environmental clearances alone took three years, involving negotiations with five state governments and hundreds of local bodies. The project's ₹12,000 crore cost made it one of India's largest private infrastructure investments. Yet GSPL structured it with minimal equity contribution, using project finance and strategic partnerships to leverage their expertise rather than capital.

Gujarat Gas Limited (GGL) represented a different vector—vertical integration into city gas distribution. While GSPL moved gas between cities, GGL distributed it within cities. By 2021, GGL had become India's largest city gas distribution company, operating in 44 districts across six states. The synergy was obvious: GSPL brought gas to city gates, GGL took it to homes and vehicles. This integration created a seamless value chain from transmission to last-mile delivery.

The 2021 transaction where GSPL sold its Amritsar and Bhatinda city gas distribution areas to GGL for ₹153.86 crores illustrated portfolio optimization. Rather than operating scattered CGD assets, GSPL consolidated them under GGL, creating operational efficiencies and cleaner corporate structure. This wasn't retreat; it was strategic focus—GSPL would own transmission highways, GGL would own local distribution, each optimized for their specific infrastructure challenge. The execution of these subsidiary projects revealed operational excellence that had become GSPL's signature. GIGL's 930-kilometer pipeline linking Mehsana to Bathinda was 80% complete by 2020, despite COVID-19 disruptions. The project, built at ₹5,500 crores, showcased GSPL's ability to execute complex infrastructure during unprecedented global disruption. Construction teams worked in biosecure bubbles, materials were sourced despite supply chain chaos, and the pipeline was commissioned just months behind schedule—remarkable given the circumstances.

The strategic importance of these subsidiaries extended beyond mere pipeline kilometers. GIGL's network connected Punjab's industrial heartland and extended toward Kashmir, bringing natural gas to regions that had relied on expensive, polluting alternatives for decades. GITL's east-west corridor created arbitrage opportunities between coastal LNG and inland demand, potentially saving industrial customers hundreds of crores annually. These weren't just pipes; they were economic enablers for entire regions.

Financial structuring of these subsidiaries demonstrated sophisticated capital market thinking. Rather than diluting GSPL's equity or leveraging the parent balance sheet, each subsidiary raised project-specific debt, often with innovative structures. GIGL's financing included masala bonds (rupee-denominated bonds issued overseas), a first for an Indian pipeline company. GITL explored infrastructure investment trusts (InvITs) as potential monetization vehicles. This financial engineering allowed GSPL to multiply its infrastructure footprint while maintaining a conservative balance sheet.

The competitive dynamics these subsidiaries created were fascinating. GAIL, long accustomed to monopolistic control, suddenly faced competition on multiple fronts. GIGL's northern network competed directly with GAIL's Dadri-Bawana-Nangal pipeline. GITL's east-west corridor paralleled GAIL's HVJ pipeline. This competition benefited end consumers through better service and competitive tariffs, while forcing GAIL to improve operational efficiency.

By 2023, GSPL's subsidiary strategy had created a pan-Indian presence that seemed impossible just a decade earlier. Combined, GSPL and its subsidiaries operated or were constructing over 7,000 kilometers of pipelines, making them collectively India's second-largest gas transmission network. The Gujarat model—open access, operational excellence, customer focus—was being replicated across the subcontinent.

The transformation wasn't just about scale; it was about creating optionality in India's energy infrastructure. As the country grappled with energy transition, GSPL's networks provided the flexibility to integrate various energy sources—domestic gas, imported LNG, and potentially hydrogen in the future. The subsidiaries weren't just building for today's energy needs; they were creating infrastructure for India's evolving energy future.

VI. Regulatory Environment & PNGRB Dynamics

The Petroleum and Natural Gas Regulatory Board headquarters in New Delhi, 2006. Bureaucrats shuffled papers, engineers debated technical standards, and lawyers parsed legislation. India finally had a gas regulator, but nobody quite knew what it meant. "We need to bring order to chaos," the first PNGRB chairman declared. Sitting in that room was GSPL's regulatory team, who had operated for eight years without formal oversight. They weren't worried about regulation; they were excited. They had been playing chess while others played checkers, and now the rules were being written based on their moves.

PNGRB's creation fundamentally altered India's gas transmission landscape. For the first time, pipeline tariffs would be determined by an independent regulator rather than bilateral negotiations. Access terms would be standardized. Technical specifications would be mandated. For most pipeline operators, this meant upheaval. For GSPL, it meant validation—their open access model, transparent tariff structure, and technical standards became templates for national regulation.

The regulatory framework that emerged revealed the complexity of governing natural gas infrastructure. PNGRB had to balance multiple objectives: ensuring fair returns to pipeline investors, protecting consumer interests, promoting competition, and encouraging infrastructure development. The tariff determination mechanism they developed—based on cost-plus returns with efficiency incentives—drew heavily from GSPL's existing practices. When PNGRB needed to demonstrate how unified tariffs could work across multiple entry-exit points, they pointed to GSPL's Gujarat Gas Grid. The recent regulatory developments paint a picture of PNGRB's evolving approach and its impact on GSPL. The proposed amendments to gas transmission tariffs by PNGRB could offer significant upside for gas transmission companies like GAIL and GSPL, with reforms currently open for public consultation aiming to introduce greater flexibility in cost pass-through and volume-based assumptions, potentially leading to higher tariffs if finalized by June 2025.

However, GSPL's relationship with PNGRB hasn't been without turbulence. The April 2024 tariff revision for GSPL's high-pressure network delivered a shock that reverberated through capital markets. PNGRB reduced the pressure transmission tariffs by 47%, from ₹34 per mmbtu to ₹18.1 per mmbtu, causing GSPL's stock to hit the 20% lower circuit. The regulator's reasoning revealed the complexity of tariff determination—PNGRB considered future capex of ₹1,800 crore against GSPL's claim of ₹3,400 crore, and approved operating expenditure of ₹2,600 crore against GSPL's demand of ₹5,000 crore.

This tariff cut episode illustrated the regulatory risk inherent in infrastructure businesses. GSPL had requested ₹50.8 per mmbtu based on their investment and operational projections. PNGRB's drastically lower determination reflected different assumptions about volumes, asset life, and efficiency gains. The market's violent reaction—wiping out nearly ₹3,000 crores in market cap in a single day—underscored how regulatory decisions could override operational excellence.

Yet GSPL's response to this setback revealed institutional maturity. Rather than engaging in public battles or litigation, they focused on volume growth to offset tariff reductions. They accelerated efficiency programs to align costs with PNGRB's expectations. Most importantly, they doubled down on expansion, recognizing that scale and network effects would ultimately drive returns regardless of per-unit tariffs. The 2025 approval for capacity expansion of GSPL's High Pressure Gujarat Gas Grid marks a crucial regulatory victory. PNGRB's approval for the expansion of GSPL's High-Pressure Gujarat Gas Grid through the laying of the Anjar-Palanpur Pipeline represents a significant step in strengthening the state's natural gas infrastructure, with the newly approved pipeline extending over 274 kilometers with a diameter of 30 inches. This expansion will enhance the overall capacity of GSPL's High-Pressure Gujarat Gas Grid to 44.76 MMSCMD.

This ₹2,051 crore project approval reveals PNGRB's evolving stance—recognizing infrastructure expansion's importance while maintaining tariff discipline. The new pipeline approval should have no immediate implications for GSPL's tariffs, but it improves the likelihood of some future reversal to the sharp 47% tariff cut that was announced in April 2024. The market's response—with analysts upgrading ratings and stock prices recovering—suggests confidence that GSPL can navigate regulatory challenges through operational excellence and strategic expansion.

The open access framework that GSPL pioneered has become central to India's gas market liberalization. Unlike electricity, where open access remains theoretical in many states, gas transmission has achieved genuine third-party access. GSPL's model proved that infrastructure owners could profit from neutral operations, creating a template now being replicated nationally. The company's willingness to provide capacity to competitors—including GAIL's customers—demonstrated that competition could coexist with commercial success.

PNGRB's approach to GSPL also reflects broader regulatory evolution. Early interactions were adversarial, with PNGRB asserting authority and GSPL defending autonomy. Over time, this evolved into constructive engagement. PNGRB recognized GSPL's operational expertise; GSPL accepted regulatory oversight as necessary for sector development. This mature relationship enabled innovations like unified tariff zones and capacity trading mechanisms that benefit the entire ecosystem.

The competitive dynamics PNGRB's regulations created have been transformative. By ensuring non-discriminatory access to GSPL's network, PNGRB enabled gas-on-gas competition in Gujarat—something unimaginable in India's traditionally monopolistic energy sector. Industrial customers could now choose suppliers based on price and reliability rather than geographic monopoly. This competition drove efficiency improvements across the value chain, from LNG procurement to last-mile delivery.

Looking ahead, PNGRB's proposed tariff reforms suggest a more nuanced regulatory approach. The proposed amendments to gas transmission tariffs by PNGRB could offer significant upside for gas transmission companies like GAIL and GSPL, with reforms aiming to introduce greater flexibility in cost pass-through and volume-based assumptions, potentially leading to higher tariffs if finalized by June 2025. This signals recognition that infrastructure requires adequate returns to attract investment, especially as India targets massive gas infrastructure expansion.

The regulatory journey from unregulated operations to sophisticated oversight mirrors India's broader economic evolution. GSPL's ability to thrive under regulation—turning compliance into competitive advantage—offers lessons for infrastructure companies navigating increasing regulatory scrutiny. As India's energy transition accelerates, the PNGRB-GSPL relationship will likely serve as a case study in balancing public interest with private enterprise in critical infrastructure sectors.

VII. Financial Performance & Market Position

The numbers tell a story of steady accumulation rather than explosive growth. GSPL's ₹17,000+ crore market capitalization reflects investor recognition of infrastructure's value—not exciting, perhaps, but essential. The financial metrics paint a picture of a utility-like business model executed with unusual efficiency: ₹17,370 crores in revenue, ₹1,637 crores in profit, an almost debt-free balance sheet, and a 19.9% dividend payout that would make income investors smile. But beneath these headline numbers lies a more nuanced narrative about value creation in regulated infrastructure.

The revenue model's elegance lies in its simplicity. GSPL charges customers for moving gas from Point A to Point B, with tariffs regulated by PNGRB. Unlike commodity businesses subject to price volatility, GSPL's revenues depend primarily on volumes transmitted and regulated tariffs. This creates predictable cash flows—the holy grail for infrastructure investors. During FY2023-24, daily transmission volumes averaged above 30 MMSCMD, generating steady toll-like revenues regardless of gas prices.

The profit margins reveal operational excellence within regulatory constraints. Despite PNGRB's tariff cuts, GSPL maintains EBITDA margins above 65%—exceptional for any business, remarkable for regulated infrastructure. This profitability stems from high asset utilization (consistently above 80%), minimal maintenance requirements for underground pipelines, and economies of scale as volumes grow without proportional cost increases. The company has essentially built a toll road for molecules with minimal traffic jams.

The balance sheet strength deserves particular attention. In an infrastructure sector typically characterized by high leverage, GSPL operates almost debt-free. This wasn't accident but strategy—conservative financial management through the construction phase, followed by rapid deleveraging as cash flows materialized. The company's debt-to-equity ratio of less than 0.1x compares to 2-3x for typical infrastructure companies. This financial flexibility becomes a weapon—enabling countercyclical expansion, dividend sustainability, and acquisition optionality.

The dividend policy reflects management's confidence in cash generation. The 19.9% payout ratio might seem modest, but it represents a deliberate balance between rewarding shareholders and retaining capital for expansion. Over the past five years, dividends have grown steadily, even during regulatory upheavals. This consistency attracts a different investor class—those seeking yield rather than growth, stability rather than excitement. In a market obsessed with multibaggers, GSPL offers something rarer: predictability.

The sales growth trajectory—7.25% CAGR over five years—initially appears disappointing. But this number obscures underlying dynamics. Volume growth has been robust, offset by tariff reductions. Capacity utilization has increased. New connections have been added. The subsidiary contributions are beginning to flow through. Adjusted for regulatory impacts, the underlying business growth exceeds 12% annually—respectable for mature infrastructure.

The valuation metrics suggest market skepticism about growth prospects. Trading at 15.38x P/E and 1.19x P/B, GSPL appears cheap relative to infrastructure peers. The market seems to price in continued regulatory pressure, limited growth potential, and energy transition risks. Yet this valuation ignores the optionality embedded in GSPL's network—the ability to transport hydrogen, the subsidiary value creation potential, the scarcity value of irreplaceable infrastructure.

Return ratios tell a story of capital efficiency despite asset intensity. Return on equity of 15%+ and return on capital employed of 18%+ exceed regulatory allowed returns, suggesting operational efficiency beyond regulatory assumptions. The asset turnover ratio has improved steadily as volumes grow faster than asset base expansion. These metrics demonstrate that even within regulatory constraints, superior execution creates value.

The working capital management reveals operational sophistication. Despite dealing with numerous suppliers and customers, GSPL maintains negative working capital—customers pay before suppliers are paid. This cash conversion efficiency means growth funding itself, reducing external capital dependence. The cash conversion cycle of negative 30 days compares favorably to global pipeline operators.

Segment analysis provides insights into value drivers. The transmission business contributes 85% of revenues but 90%+ of profits, given minimal operating costs once pipelines are laid. The wind power segment, while small, provides unregulated returns above 15%. The subsidiary income stream, currently modest, represents future upside as GIGL and GITL projects are commissioned.

The financial resilience was tested during COVID-19 when industrial gas demand collapsed. GSPL's revenues declined only 15% despite volumes falling 40%—the take-or-pay contracts and regulated tariff structure provided cushion. The company maintained profitability, continued dividend payments, and accelerated expansion when others retrenched. This downturn performance validated the business model's defensive characteristics.

Comparative analysis with GAIL reveals GSPL's relative efficiency. Despite being one-tenth GAIL's size, GSPL generates superior return ratios, maintains lower operating costs per unit transmitted, and achieves higher capacity utilization. This efficiency gap suggests either GSPL's operational excellence or GAIL's bureaucratic burden—likely both. As competition intensifies, these efficiency differences will determine market share dynamics.

The forward-looking financial trajectory depends on multiple variables: regulatory decisions on tariffs, subsidiary project completions, volume growth from industrial recovery, and energy transition impacts. Conservative scenarios suggest 10-12% earnings CAGR; optimistic projections incorporating regulatory relief and subsidiary contributions point to 15-18% growth. The truth likely lies between, but even modest growth on GSPL's stable base creates substantial value over time.

VIII. Playbook: Infrastructure & Energy Lessons

Every infrastructure story teaches lessons, but GSPL's journey offers a masterclass in building critical assets in emerging markets. The playbook isn't about grand strategies or brilliant innovations; it's about patient execution, regulatory navigation, and understanding that infrastructure value compounds slowly but surely. These lessons apply beyond pipelines—to highways, airports, power grids, any network that society depends upon.

Lesson One: Building critical infrastructure in emerging markets requires political alignment without political dependence. GSPL succeeded because it aligned with Gujarat's industrial vision while maintaining operational independence. The company never became a tool for political patronage or subsidy distribution. This delicate balance—government-owned but commercially operated—enabled long-term planning while avoiding political interference. The key was making politicians look good through economic development rather than through populist pricing.

Lesson Two: Managing government ownership while operating commercially demands cultural sophistication. GSPL created a hybrid culture—public sector stability with private sector accountability. Performance bonuses, merit-based promotions, and operational KPIs created accountability. Yet job security and measured pace retained talent that might have burned out in purely private settings. This cultural balance attracted engineers who wanted to build something lasting rather than chase quarterly earnings.

Lesson Three: The open access model as competitive advantage seems counterintuitive but proves powerful. By allowing competitors to use their network, GSPL gained regulatory goodwill, customer trust, and volume growth that more than offset any competitive loss. Open access transformed GSPL from a potential monopolist requiring heavy regulation into a neutral infrastructure provider deserving light-touch oversight. Sometimes giving up control creates more value than maintaining it.

Lesson Four: Network effects in pipeline infrastructure operate differently than in digital networks. Each new connection doesn't exponentially increase value for existing users, but it does create system resilience, operational flexibility, and commercial optionality. GSPL's web of interconnections means no single point of failure, multiple sourcing options, and ability to redirect flows based on demand. This physical network effect creates competitive moats as surely as digital platforms.

Lesson Five: Balancing growth investments with dividend expectations requires strategic communication. Infrastructure investors typically fall into two camps—growth seekers and yield hunters. GSPL attracted both by clearly segregating maintenance capex (funded from operations) from growth capex (funded through retained earnings or project finance). This transparency enabled consistent dividends while funding expansion, satisfying both investor constituencies.

Lesson Six: Strategic subsidiary structuring for national expansion multiplies capital efficiency. Rather than raising massive equity for nationwide expansion, GSPL created project-specific subsidiaries with strategic partners. This structure shared risks, brought complementary capabilities, and enabled larger projects than GSPL could undertake alone. The subsidiary model transformed GSPL from a regional player constrained by capital into a national player constrained only by execution capacity.

Lesson Seven: Managing regulatory relationships requires playing the long game. GSPL never fought PNGRB publicly, even when tariff decisions seemed unfair. Instead, they provided data, suggested policy improvements, and demonstrated operational excellence. This collaborative approach built credibility that paid dividends in future regulatory decisions. In regulated industries, winning individual battles matters less than maintaining productive long-term relationships.

Lesson Eight: Technical excellence creates regulatory and competitive advantages. GSPL's superior operating metrics—lower losses, higher uptime, better safety records—became arguments for favorable regulatory treatment and customer acquisition. When regulators needed to set technical standards, they often adopted GSPL's practices. When customers evaluated pipeline options, GSPL's reliability premium justified higher tariffs. Technical excellence isn't just about engineering; it's about business strategy.

Lesson Nine: Capital allocation in infrastructure requires different thinking than in growth businesses. The temptation in infrastructure is to maximize leverage given stable cash flows. GSPL resisted, maintaining a fortress balance sheet that enabled opportunistic expansion and survived demand shocks. The opportunity cost of low leverage seemed high during boom times but proved invaluable during disruptions. In infrastructure, survival matters more than optimization.

Lesson Ten: The transition from regional to national requires organizational transformation. GSPL's evolution demanded new capabilities—project finance structuring, multi-state regulatory management, complex stakeholder coordination. They built these capabilities through selective hiring, strategic partnerships, and learning by doing. The organizational growing pains were real but necessary. Infrastructure companies must evolve their organization as fast as their physical network.

Lesson Eleven: ESG considerations in infrastructure are operational necessities, not compliance burdens. GSPL's early adoption of environmental management systems, community engagement programs, and safety protocols seemed like overhead but became competitive advantages. When global investors sought ESG-compliant infrastructure plays, GSPL was ready. When communities protested pipeline routes, GSPL's relationship capital enabled solutions. ESG isn't separate from operations; it enables operations.

Lesson Twelve: Digital transformation in physical infrastructure focuses on optimization, not disruption. GSPL's technology investments—SCADA systems, predictive maintenance, customer portals—didn't revolutionize the business but made it dramatically more efficient. The focus was on using technology to do the same things better rather than different things. In infrastructure, evolution beats revolution.

These lessons converge into a meta-insight: infrastructure success comes from compound improvements rather than breakthrough innovations. GSPL didn't invent new pipeline technology or discover revolutionary business models. They simply executed the basics better than others, year after year, creating cumulative advantages that became insurmountable. In infrastructure, boring excellence beats exciting mediocrity.

IX. Bull vs. Bear Case & Competitive Analysis

The investment case for GSPL splits thoughtful analysts into two camps, each armed with compelling arguments. The bulls see irreplaceable infrastructure poised for rerating; the bears see a regulated utility facing growth headwinds. The truth, as always, lies in the nuanced middle, but understanding both extremes illuminates the investment decision.

The Bull Case: Infrastructure Scarcity Meets Energy Transition

Bulls begin with a simple observation: you cannot replicate GSPL's network today at any price. The 2,700+ kilometer pipeline system crossing Gujarat's industrial heartland would face insurmountable land acquisition challenges, environmental clearances that could take decades, and construction costs multiples of GSPL's historical investment. This irreplaceability creates scarcity value that markets haven't fully recognized.

The strategic positioning argument resonates strongly. GSPL's network originates from Anjar, Gujarat, connecting to the 36-inch Mundra-Arpar pipeline and terminates at Palanpur in the Banaskantha district, integrating with MBPL. Every major gas source—domestic fields, Dahej LNG, Hazira LNG, Mundra LNG—connects to GSPL's grid. Every major industrial cluster depends on GSPL for gas supply. This isn't just market leadership; it's infrastructure dominance in India's most industrialized state.

The gas demand growth story remains compelling despite energy transition concerns. India's gas consumption must rise from 6% to 15% of energy mix to meet climate commitments. Gujarat, already at 25% gas penetration, demonstrates what's possible nationally. As India builds 30,000 kilometers of new pipelines, GSPL's expertise and existing network position them to capture disproportionate value.

The subsidiary optionality provides hidden value. GIGL and GITL represent ₹18,000+ crores of under-construction assets that will generate returns once commissioned. At current valuations, markets assign minimal value to these subsidiaries despite their transformative potential. When these projects flow cash, GSPL's earnings could increase 40-50%, driving significant rerating.

Financial strength enables opportunistic growth. The debt-free balance sheet means GSPL can fund expansion without dilution, acquire distressed assets during downturns, or return cash to shareholders as conditions warrant. This financial flexibility is particularly valuable in capital-intensive infrastructure where overleveraged competitors may face distress.

Regulatory dynamics are improving. The proposed amendments aim to introduce greater flexibility in cost pass-through and volume-based assumptions in tariff calculation, which could significantly benefit gas transmission players like GSPL, with these changes potentially leading to higher tariffs and improved financial metrics if implemented by June 2025. After years of tough regulation, PNGRB appears to recognize that infrastructure needs adequate returns to attract investment.

The Bear Case: Structural Headwinds and Regulatory Overhang

Bears point to the disappointing 7.25% historical sales growth as evidence of structural challenges. Despite India's gas push, GSPL's growth has been anemic. If they can't grow faster during infrastructure buildout phases, what happens when the market matures? The growth problem isn't temporary but structural—regulated tariffs, limited geography, and competitive pressures create permanent headwinds.

Regulatory risk remains paramount. The April 2024 tariff cut of 47% demonstrates PNGRB's power to destroy value overnight. The Petroleum and Natural Gas Regulatory Board (PNGRB) has reduced the pressure transmission tariffs by 47%, and the unexpected tariff cut could significantly impact the company's revenue and cash flow. While markets hope for regulatory relief, history suggests regulators prioritize consumer interests over infrastructure returns. Future tariff reviews could bring more pain.

Competition is intensifying from multiple directions. GAIL is expanding aggressively in Gujarat. New LNG terminals are being built with dedicated evacuation infrastructure, bypassing GSPL's network. City gas distribution companies are building their own transmission lines. GSPL's monopoly is eroding, and with it, pricing power.

Geographic concentration creates vulnerability. Despite national ambitions, 80%+ of GSPL's revenues come from Gujarat. This concentration exposes them to state-specific risks—industrial slowdown, competitive dynamics, or regulatory changes in Gujarat would disproportionately impact GSPL. True diversification remains years away.

Energy transition poses existential questions. While natural gas is branded as "transition fuel," the timeline remains uncertain. Renewable energy costs are falling faster than expected. Green hydrogen might bypass natural gas altogether. Electric vehicles could eliminate CNG demand. GSPL's infrastructure could become stranded assets in an accelerated transition scenario.

The valuation already reflects modest optimism. At 15x P/E, GSPL isn't obviously cheap for a regulated utility with single-digit growth. Comparable global pipeline companies trade at similar or lower multiples despite operating in more stable regulatory environments. The margin of safety isn't compelling.

Competitive Dynamics: The GAIL Shadow

GAIL looms large in any GSPL analysis. As India's gas incumbent with 15,000+ kilometers of pipelines, GAIL possesses scale advantages—procurement power, regulatory influence, and financial resources—that GSPL cannot match. Yet GSPL has consistently demonstrated superior operational efficiency, suggesting David versus Goliath dynamics where agility trumps size.

The competitive battlefield is shifting from pipeline construction to service differentiation. GSPL's open access model, operational excellence, and customer focus create advantages that GAIL's bureaucratic structure struggles to replicate. As industrial customers become more sophisticated, they value reliability and flexibility over mere connectivity.

New entrants pose limited threats. Building transmission infrastructure requires enormous capital, regulatory approvals, and operational expertise that few possess. The more likely scenario is partnerships or acquisitions, where GSPL's established position makes them an attractive partner rather than a target.

The competitive moat isn't just physical infrastructure but institutional knowledge. GSPL's two-decade experience operating in Gujarat's specific conditions—soil types, weather patterns, industrial requirements—cannot be easily replicated. This tacit knowledge creates barriers beyond capital requirements.

Synthesis: A Balanced View

The investment case ultimately depends on time horizon and risk tolerance. For long-term investors seeking defensive infrastructure exposure, GSPL offers attractive risk-reward. The irreplaceable assets, improving regulatory dynamics, and subsidiary optionality provide multiple ways to win. For growth-oriented investors seeking multibaggers, GSPL will likely disappoint. The regulated nature, competitive pressures, and modest growth trajectory cap upside potential.

The key monitorables going forward include regulatory decisions on tariff revisions, subsidiary project commissioning timelines, industrial gas demand recovery, and competitive dynamics in Gujarat. Each could swing the investment case significantly. What's clear is that GSPL represents a pure play on India's gas infrastructure development—whether that's an opportunity or risk depends on your view of India's energy future.

X. Future Outlook & Strategic Priorities

Standing at the edge of 2025, GSPL faces an infrastructure landscape dramatically different from its founding era. India targets 30,000+ kilometers of gas pipeline development over the next decade—a construction boom that dwarfs anything previously attempted. The question isn't whether GSPL will participate but how they'll maintain relevance as the industry transforms from regional fiefdoms to national networks. The strategic choices made today will determine whether GSPL remains Gujarat's pipeline champion or evolves into India's gas infrastructure leader.

The immediate opportunity is staggering. India is poised to nearly double its gas pipeline network by investing $67 billion over the next five years. For context, this represents more pipeline construction than India has completed in its entire history. GSPL's positioning—with established operations, proven expertise, and strong balance sheet—provides advantages in capturing this growth. But execution will determine everything.

GIGL's Phase 2 expansion represents the near-term catalyst. The 930-km pipeline linking Mehsana in Gujarat to Bathinda in the northern state of Punjab at a cost of 55 billion rupees ($739 million) will be ready by March, with around 80% of the physical work of the pipeline completed. This isn't just about adding pipeline kilometers; it's about connecting India's energy-hungry north to multiple gas sources, creating arbitrage opportunities and supply security that didn't exist before.

The green energy transition paradoxically strengthens GSPL's position. Natural gas, despite being fossil fuel, becomes critical for grid stability as renewable penetration increases. Gas-fired power plants can ramp up quickly when solar generation drops, providing the flexibility that coal plants cannot. GSPL's infrastructure becomes the backbone for renewable integration, not its victim.

The hydrogen opportunity looms large but remains undefined. GSPL's pipelines, with modifications, could transport hydrogen blended with natural gas. Early experiments globally suggest 20% hydrogen blending is feasible without major infrastructure changes. If India commits to hydrogen economy, GSPL's network could become hydrogen highways. But this requires regulatory clarity, technical standards, and enormous investment—all currently missing.

Digital transformation in pipeline operations offers efficiency gains that could offset regulatory pressure. Predictive maintenance using AI could reduce downtime from 0.1% to 0.01%—seemingly marginal but worth crores in avoided penalties. Digital twin technology enables virtual testing of network configurations, optimizing flow without physical changes. Smart sensors detect leaks before they become disasters. These aren't revolutionary changes but compound into competitive advantages.

The recent analyst upgrades suggest shifting sentiment. Citi upgraded the stock to a 'Buy' rating with a target price of ₹325, with optimism stemming from GSPL's capacity expansion in its high-pressure gas pipeline network. After the April 2024 tariff shock, markets are recognizing that infrastructure value transcends regulatory cycles. The 35% stock price correction created an entry point that fundamental investors couldn't ignore.

Strategic priorities for the next five years are becoming clear. First, complete and commission subsidiary projects—execution risk remains the biggest variable. Second, maximize utilization of existing infrastructure through debottlenecking and optimization. Third, selectively pursue new projects that leverage existing network advantages. Fourth, prepare for energy transition through technology investments and regulatory engagement. Fifth, maintain financial flexibility for opportunistic moves.

The organizational evolution required is substantial. GSPL needs to transform from a regional operator to a national player, from pipeline company to energy infrastructure platform, from regulated utility to value-added service provider. This requires new capabilities in project management, stakeholder engagement, and technology deployment. The cultural shift from steady-state operations to growth mode won't be simple.

Regulatory engagement strategy must evolve from compliance to partnership. As PNGRB matures, opportunities exist to shape policy rather than just follow it. GSPL's operational data and expertise can inform better regulations. Their success stories can become policy templates. This requires proactive engagement, thought leadership, and willingness to invest in regulatory capacity building.

The ESG imperative intensifies. Global investors increasingly screen for climate alignment, community impact, and governance standards. GSPL's role in enabling gas adoption (reducing emissions versus coal) provides a positive narrative. But they must quantify and communicate this impact better. The windmill investments, emission reduction programs, and safety records need to become central to equity story, not footnotes.

Risk management in an uncertain energy future requires portfolio thinking. While natural gas transmission remains core, adjacencies deserve exploration. Carbon capture and transportation, renewable energy transmission infrastructure, even water pipelines leverage similar competencies. Diversification shouldn't dilute focus but create optionality for different energy futures.

The capital allocation framework must balance multiple objectives. Growth capex for subsidiary projects and network expansion remains priority. But dividend sustainability matters for institutional investors. Share buybacks might make sense if valuations remain depressed. The balance will determine whether GSPL remains a utility yield play or transforms into a growth story.

Market share dynamics will intensify as the pie expands. GSPL's 15-20% share of India's transmission capacity could shrink even as absolute volumes grow, simply because the market is expanding faster than any single player can capture. The focus must shift from market share to profitable growth—better to own 10% of a profitable market than 20% of a commoditized one.

The investment required for this transformation is substantial but manageable. Between subsidiary projects, network expansion, and technology upgrades, GSPL needs to deploy ₹10,000+ crores over five years. The debt-free balance sheet provides flexibility, but capital discipline remains crucial. Every rupee invested must earn returns above regulatory thresholds to create shareholder value.

Looking toward 2030, GSPL's success will be measured not by pipeline kilometers but by value creation. Did they successfully commission subsidiary projects? Did they maintain operational excellence despite rapid growth? Did they navigate energy transition successfully? Did they generate returns above cost of capital? These questions will determine whether GSPL's next chapter matches the success of its first.

The ultimate judgment on GSPL's future comes down to execution credibility. The opportunity is clear—India's gas infrastructure buildout is a generational opportunity. The positioning is strong—established operations, financial strength, and regulatory relationships. The strategy is sound—selective expansion, operational excellence, and financial discipline. But infrastructure is ultimately about execution, and that's where GSPL must prove itself again.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube