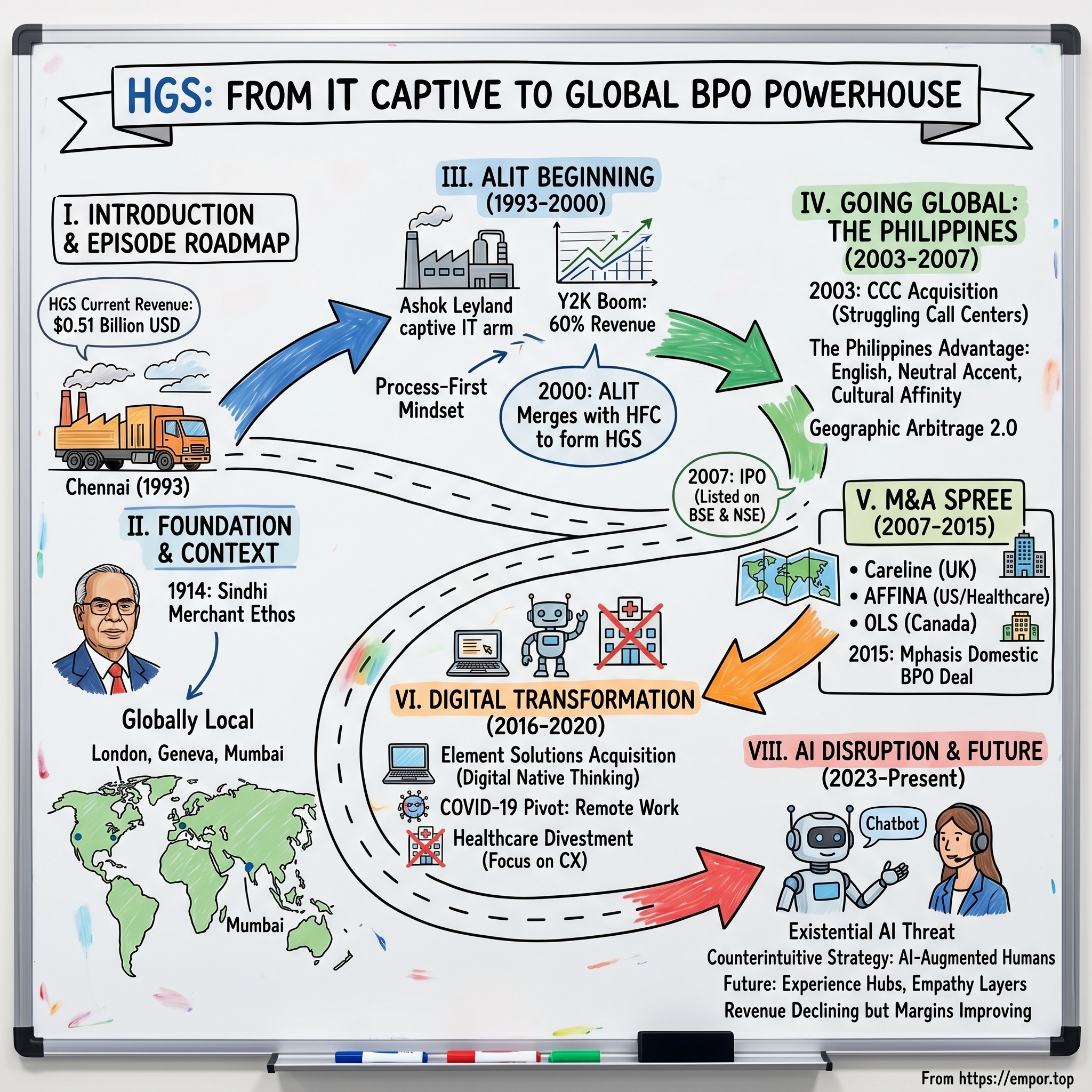

Hinduja Global Solutions: From ALIT to Global BPO Powerhouse

I. Introduction & Episode Roadmap

Picture this: A truck manufacturing company in Chennai decides it needs an IT department. Nothing unusual there—except this IT department would eventually morph into a $550 million global business process outsourcing empire spanning six countries and serving some of the world's most demanding Fortune 500 companies. The history of HGS (Hinduja Global Solutions) began in 1993 under the name ALIT Ashok Leyland Information Technology, providing information technology services. In 2000, ALIT merged with Hinduja Finance Corporation (HFC) to form HGS.

That's the unlikely origin story of Hinduja Global Solutions—a company that began life as the captive IT arm of a commercial vehicle manufacturer and transformed into one of India's most intriguing BPO players. But here's what makes this story particularly fascinating: While tech giants like TCS and Infosys were building their empires by riding the Y2K wave and chasing Silicon Valley dollars, HGS took a completely different path. They went to the Philippines. They bought struggling call centers. They focused on unglamorous work like customer support for telecom companies. And somehow, it worked.

According to Hinduja Global Solutions's latest financial reports the company's current revenue (TTM) is $0.51 Billion USD. That might seem modest compared to India's IT behemoths, but it represents something more profound: the power of patient capital, contrarian thinking, and the often-underappreciated advantage of being part of a century-old business conglomerate.

Today, we're diving deep into a company that embodies several counterintuitive business lessons. How does a conglomerate structure—often seen as outdated in Western markets—actually provide competitive advantages in emerging markets? Why did betting on the Philippines in 2003 prove to be a masterstroke? How does a company navigate the existential threat of AI to the very business model it's built over three decades? And perhaps most intriguingly: What happens when a family-controlled business with roots in 1914 tries to reinvent itself for the age of ChatGPT?

This isn't just another Indian outsourcing story. It's a tale of geographic arbitrage 2.0, where labor cost is just the beginning. It's about building trust-based relationships in an industry that's been steadily commoditized. And it's about the delicate dance between preserving what works and disrupting yourself before someone else does.

HGS takes a "globally local" approach, with over 18,000 employees in 10 countries, including 33 delivery centers, making a difference to some of the world's leading brands across verticals. From the bustling call centers of Manila to the digital innovation hubs in Bengaluru, from serving telecom giants to healthcare providers, HGS has quietly built something unique in the crowded BPO landscape.

Over the next several hours, we'll trace this journey from its origins in the License Raj era through the Y2K boom, the audacious Philippines expansion, the M&A spree that followed, the digital transformation imperative, and the current AI disruption. We'll examine the playbook—what worked, what didn't, and what it tells us about building services businesses in emerging markets. And we'll wrestle with the fundamental question facing HGS today: In a world where generative AI threatens to automate away millions of customer service jobs, what's the future of a company built on human-to-human interaction?

So buckle up. This is the story of how an IT department became a global business, how the Philippines became India's unlikely partner in the BPO revolution, and how a company backed by one of India's oldest business families is trying to write its next chapter in the age of artificial intelligence. This is Hinduja Global Solutions.

II. Hinduja Group Origins & Foundation Context

The monsoon rains were particularly heavy in Mumbai in July 1914 when a young Sindhi merchant named Parmanand Deepchand Hinduja made a decision that would echo through the next century. In 1914, he travelled to the trade and financial capital, Bombay (later changed to Mumbai) where he quickly learnt the ropes of business. In 1919, the business journey, which began in Sindh, entered the international arena with an office in Iran (the first outside India). At just 14 years old—an age when most teenagers are worried about schoolwork—Parmanand was laying the groundwork for what would become a $22 billion global conglomerate.

But to understand HGS, you first need to understand the Hinduja ethos, because this isn't just corporate history—it's DNA that still drives decision-making in the C-suite today. The Sindhis, displaced by Partition in 1947, had developed a particular approach to business: relationship-first, trust-based, globally minded before globalization was even a term. They didn't have land or local political connections. What they had was mobility, adaptability, and an almost obsessive focus on maintaining reputation across generations.

The company was founded in 1914 by Parmanand Deepchand Hinduja, who was from a Sindhi family based in India. Initially operating in Shikarpur (in modern-day Pakistan) and Bombay, India, he set up the company's first international operation in Iran in 1919. Think about that for a moment—this was five years after World War I ended, when international trade meant months-long journeys and handshake deals. Yet Parmanand saw opportunity where others saw impossibility.

The Iran operation would become the group's headquarters for the next 60 years—until the Islamic Revolution in 1979 forced a dramatic pivot. The headquarters of the group remained in Iran until 1979, when the Islamic Revolution forced it to move to Europe. Group Chairman Srichand Hinduja and his brother Gopichand, also Co-Chairman, moved to London in 1979 to develop the export business; the third brother Prakash manages the group's operations in Geneva, Switzerland while the youngest brother, Ashok, oversees the Indian interests. This geographic dispersion—London, Geneva, Mumbai—would later prove crucial in building a truly global business network.

By the 1980s, the Hinduja Group had evolved into something unique in Indian business: a genuinely international conglomerate with deep roots in multiple countries. While the Tatas and Birlas were primarily India-focused with some international operations, the Hindujas were global citizens who happened to be Indian. This distinction matters enormously for our story.

The group's expansion in India during the License Raj era (1947-1991) is a masterclass in navigating bureaucratic complexity. When the Indian government severely restricted private enterprise through an elaborate system of licenses, regulations, and permits, conglomerates thrived. Why? Because once you had cracked the code of getting one license, the marginal cost of getting another was lower. The regulatory expertise, political relationships, and bureaucratic know-how could be amortized across multiple businesses.

The group is present in eleven sectors including automotive, oil and specialty chemicals, banking and finance, IT and ITeS, cyber security, healthcare, trading, infrastructure project development, media and entertainment, power, and real estate. In October 2024, the Hinduja family was ranked 11th on the Forbes list of India's 100 richest tycoons, with a net worth of $22 billion.

The conglomerate structure also solved another critical problem in pre-liberalization India: capital allocation. With underdeveloped capital markets and restricted foreign investment, internal capital markets within conglomerates were often more efficient than external ones. If the truck business was generating cash and the finance business needed investment, you could move money internally without dealing with banks or regulators.

But here's where the Hinduja story gets particularly interesting for our HGS narrative. In the early 1990s, as India began liberalizing its economy, the group faced a strategic inflection point. The old protected markets were opening up to competition. Global companies were eyeing India. Technology was becoming increasingly important. The question wasn't whether to enter technology—it was how.

Some context on the Indian IT services landscape circa 1990-1993: Infosys had about 200 employees. TCS was still primarily serving its parent, the Tata Group. Wipro was just beginning its pivot from vegetable oil to software. The Y2K opportunity was still years away from becoming apparent. Most Indian companies saw IT as a cost center, not a business opportunity.

The history of HGS (Hinduja Global Solutions) began in 1993 under the name ALIT Ashok Leyland Information Technology, providing information technology services. The decision to create ALIT wasn't driven by dreams of becoming the next Silicon Valley giant. It was pragmatic: Ashok Leyland, the group's flagship automotive company and India's second-largest commercial vehicle manufacturer, needed IT support. Manufacturing was becoming increasingly complex. Supply chains needed optimization. Dealer networks required connectivity.

The initial mandate for ALIT was modest: support Ashok Leyland's operations, maybe pick up some third-party work if opportunities arose. Nobody in 1993 was talking about building a global BPO empire. In fact, the term "BPO" hadn't even been coined yet—people still called it "remote processing" or "offshore back-office work."

But the timing, in retrospect, was perfect. India's telecom revolution was just beginning—STD/ISD booths were proliferating, international calling costs were dropping, and the first email connections were being established. The government had just announced the Software Technology Parks scheme, offering tax benefits and easier regulations for IT companies. And critically, English-speaking graduates were available in abundance at costs that would make Western CFOs weep with joy.

What the Hindujas brought to this opportunity was different from what the pure-play IT companies offered. They had patient capital—no venture capitalists breathing down their necks demanding 10x returns. They had global relationships—decades of trust built with international partners. They had operational expertise—from running factories to managing thousands of employees. And perhaps most importantly, they had a different definition of success. While startups needed hockey-stick growth to satisfy investors, the Hindujas could afford to build slowly, methodically, with a 20-year view rather than a 2-year exit strategy.

The Sindhi merchant ethos also shaped how they thought about the business. Relationships before transactions. Trust before contracts. Long-term value before short-term profits. In an industry that would become notorious for its transactional nature and race-to-the-bottom pricing, these old-fashioned values would prove surprisingly durable.

Consider how different this is from the Silicon Valley model. There, disruption is the goal, moving fast and breaking things is the methodology, and winner-take-all is the endgame. The Hinduja approach was almost the opposite: evolution not revolution, careful and considered growth, and building an ecosystem where multiple players could thrive. They weren't trying to put anyone out of business; they were trying to build a business that would last generations.

The group structure also provided something invaluable in the early days: credibility. When ALIT's salespeople walked into a potential client's office, they weren't representing a two-year-old startup. They were representing the Hinduja Group, with its decades of history, its international presence, its financial strength. In a business built on trust—after all, you're asking companies to send their sensitive data and critical processes halfway around the world—that credibility was worth more than any technology platform.

By the mid-1990s, ALIT had begun to look beyond Ashok Leyland. The Y2K opportunity was becoming visible. Companies worldwide were panicking about their legacy systems. And India, with its army of English-speaking engineers willing to work for a fraction of Western salaries, was perfectly positioned to help. But ALIT's leadership saw something else: beyond the one-time Y2K windfall lay a more sustainable opportunity in ongoing support, maintenance, and eventually, business process outsourcing.

The group's experience in multiple industries also provided unique insights. From Ashok Leyland, they understood manufacturing and supply chain complexity. From IndusInd Bank (which the group had founded in 1994), they understood financial services. From their trading operations, they understood international business. This cross-pollination of ideas would later help HGS serve diverse industries with genuine domain expertise, not just labor arbitrage.

As we moved toward the new millennium, the pieces were falling into place for ALIT's transformation. The technology was ready—internet connectivity was improving, VOIP was making international calling cheaper, and enterprise software was becoming standardized. The market was ready—companies were increasingly comfortable with outsourcing, first IT and then business processes. And critically, the Hinduja Group was ready to make a bigger bet on services.

In 2000, ALIT merged with Hinduja Finance Corporation (HFC) to form HGS. This wasn't just a rebranding exercise. It signaled a fundamental shift in ambition. The new entity wouldn't just support the group's businesses or provide IT services. It would become a full-fledged player in the emerging global outsourcing industry. The question was: how do you differentiate in an industry where everyone is selling essentially the same thing—access to low-cost English-speaking labor?

The answer would come from an unexpected place: the Philippines.

III. The ALIT Beginning: Ashok Leyland's Digital Arm (1993-2000)

Inside Ashok Leyland's sprawling Ennore plant near Chennai in 1993, the assembly lines hummed with activity. Trucks rolled off the production line every 37 minutes—a respectable pace for an Indian manufacturer, but the Japanese were doing it in 12. The problem wasn't the workers or the equipment. It was information. Purchase orders trapped in filing cabinets. Inventory levels updated weekly, if you were lucky. Dealer complaints reaching headquarters weeks after problems arose. In this pre-internet era, information moved at the speed of paper.

The history of HGS (Hinduja Global Solutions) began in 1993 under the name ALIT Ashok Leyland Information Technology, providing information technology services. The creation of ALIT wasn't some grand strategic vision—it was born from frustration. Ashok Leyland's management had tried hiring external IT consultants, but they didn't understand manufacturing. They'd tried buying packaged software, but nothing fit their specific needs. So they decided to build their own capability.

The first ALIT team was just 25 people, mostly fresh engineering graduates from Tamil Nadu's technical colleges. Their office? A converted conference room in Ashok Leyland's Chennai headquarters. Their first project? Building a dealer management system that could track inventory, orders, and service requests across India's notoriously fragmented automotive market. It wasn't sexy work. But it was essential.

Here's what made ALIT different from the hundreds of other captive IT units being set up across corporate India in the early 1990s: they were given unusual autonomy from day one. Rather than reporting to Ashok Leyland's operations team, ALIT was structured as a separate entity with its own P&L responsibility. The message from the Hinduja leadership was clear: support the parent company, yes, but also build a real business.

This autonomy bred entrepreneurship. By 1994, ALIT was pitching services to other Hinduja Group companies. By 1995, they were quietly approaching external clients. The pitch was simple but compelling: "We understand manufacturing because we live it every day. We're not consultants who fly in, draw flowcharts, and fly out. We're operators who happen to know technology."

The mid-1990s were a peculiar time in Indian IT. The industry was exploding—growing at 50% annually—but it was also incredibly fragmented. You had the big players like TCS and Wipro focusing on large Western corporations. You had thousands of small body shops doing staff augmentation. And you had captive units like ALIT, serving their parent companies while eyeing the broader market opportunity.

ALIT's growth strategy during this period was deliberately conservative—very un-startup-like, you might say. Instead of chasing every opportunity, they focused on deepening capabilities in specific areas. Enterprise resource planning (ERP) implementations for manufacturing companies. Supply chain optimization. Dealer network management. Boring? Perhaps. Profitable? Absolutely.

By 1996, ALIT had grown to 200 employees and moved into its own facility in Chennai's emerging IT corridor. But the real catalyst for growth was about to arrive in the form of a computer bug that would terrify the world: Y2K.

The Year 2000 problem was, in retrospect, the perfect crisis for the Indian IT industry. It was urgent—every company in the world needed help. It was labor-intensive—requiring armies of programmers to review millions of lines of code. It was relatively low-skill—you didn't need computer science PhDs to change date fields from two digits to four. And it was temporary—creating massive demand that would eventually disappear.

Most Indian IT companies saw Y2K as a goldmine. ALIT saw it differently. Yes, they would do Y2K work—by 1998, nearly 60% of their revenue came from Y2K projects. But they were already thinking about January 1, 2000. What happens when the Y2K revenue disappears? How do you transition from fixing old code to running business processes?

This is where ALIT's manufacturing heritage proved invaluable. They understood process optimization in their bones. At Ashok Leyland, they had seen how standardizing processes could drive efficiency. They had learned how to manage distributed operations—coordinating between factories, suppliers, and dealers. They knew how to handle volume—processing thousands of transactions daily. These weren't IT skills; they were operations skills. And they would prove perfect for the emerging world of business process outsourcing.

The late 1990s also saw ALIT experimenting with what would later become a core HGS competency: customer service. Ashok Leyland had set up a customer care center in 1997—one of the first in India's automotive industry. ALIT was tasked with providing the technology backbone, but they quickly realized the technology was the easy part. The hard part was training agents, managing workflows, maintaining quality while scaling volume.

They studied everything. How long should a call last? (Six minutes optimal, eight minutes maximum.) How many calls could an agent handle per day without burning out? (Around 60-70.) What metrics actually mattered? (First-call resolution, not call volume.) This wasn't glamorous work, but it was building a knowledge base that would prove invaluable.

By 1999, ALIT had grown to nearly 1,000 employees and was generating revenues of approximately $12 million—tiny by today's standards but respectable for a six-year-old company in pre-liberalization India. More importantly, they had diversified beyond the Hinduja Group. External clients now accounted for 40% of revenue. They had offices in Mumbai and Delhi in addition to Chennai. They were ready for something bigger.

The timing for transformation was perfect. The dot-com boom was creating enormous demand for IT services. The telecom revolution in India was making voice-based services viable. The BPO industry—though nobody called it that yet—was nascent but growing rapidly. Companies like GE Capital and American Express had set up captive centers in India, proving that complex business processes could be successfully offshored.

But ALIT faced a strategic challenge. As a division of Ashok Leyland, they were limited in their ability to raise capital, attract talent, and pursue aggressive growth. They needed a new structure, a new identity, and frankly, a new level of ambition. The Y2K windfall had given them cash and credibility. The question was what to do with it.

In 2000, ALIT merged with Hinduja Finance Corporation (HFC) to form HGS. This wasn't just a merger—it was a reimagining. HFC brought financial services expertise, regulatory knowledge, and most importantly, access to capital. ALIT brought technology capability, process expertise, and operational experience. Together, they could target a market that was just beginning to explode: business process outsourcing for global corporations.

The merger also sent a signal to the market. This wasn't a captive unit anymore. This wasn't a small IT services player. This was a serious company backed by one of India's most powerful business groups, with ambitions to compete globally. The new entity, Hinduja Global Solutions, would focus on what the leadership called "customer lifecycle management"—handling everything from sales to service to support.

The early days of HGS were marked by careful positioning. They couldn't compete with TCS or Infosys on pure technical capabilities. They couldn't match the scale of Wipro or HCL. What they could do was focus on specific verticals where domain expertise mattered more than technical brilliance. Telecom. Financial services. Healthcare. Industries where understanding the business was as important as understanding the technology.

They also made a crucial decision that would shape the company's future: they would build their own delivery capabilities rather than rely entirely on partnerships or acquisitions. This meant investing heavily in infrastructure—building call centers, setting up training facilities, implementing quality systems. It was capital-intensive and risky. But it gave them control over quality, which in the trust-based BPO business, was everything.

As 2000 turned to 2001, and the Y2K boom turned to the dot-com bust, HGS faced its first major test. Clients were cutting budgets. Competitors were slashing prices. The easy money of the Y2K era was gone. But HGS had something many pure-play IT services companies lacked: patient capital and a long-term vision. They didn't need to show quarterly growth to satisfy Wall Street. They could afford to build for the future.

The strategy was taking shape: Don't try to be everything to everyone. Focus on specific processes in specific industries. Build deep expertise rather than broad capability. And most importantly, look beyond India for both clients and delivery locations. The last point would prove prophetic. While everyone else was building capacity in Bangalore and Gurgaon, HGS was looking at maps of Southeast Asia. Specifically, they were looking at the Philippines.

IV. Going Global: The Philippines Beachhead (2003-2007)

The Manila traffic was gridlocked, as usual, when the HGS deal team arrived at the offices of Customer Contact Center Inc. in March 2003. The Philippines was in political turmoil—President Gloria Arroyo was fighting coup attempts, the peso was volatile, and most Indian companies wouldn't dream of making acquisitions here. Which is precisely why HGS was interested.

2003 marked a milestone for HGS with the acquisition of Customer Contact Center Inc., a call center company located in the Philippines. This wasn't just HGS's first international acquisition—it was one of the first times any Indian BPO company had bought operations in the Philippines. While competitors were building massive campuses in Gurgaon and Pune, HGS was betting on a country 3,000 miles away that most Indians couldn't locate on a map.

To understand why this was genius, you need to understand the Philippines advantage circa 2003. First, English. Not just functional English like India, but American English. The Philippines had been an American colony for 48 years. Their education system was modeled on the U.S. system. They watched American movies, listened to American music, and crucially, understood American culture in a way that even the best-trained Indian call center agents struggled to match.

Second, the accent. Or rather, the lack of one. Filipino agents could adopt a neutral American accent far more easily than Indians. This might sound trivial, but in the early 2000s, American consumers' backlash against offshore call centers was growing. "I can't understand the agent" was the number one complaint. Filipino agents largely avoided this problem.

Third, cultural affinity. Filipinos celebrated Christmas, understood baseball references, and could small-talk about American TV shows. When an angry customer called about their cell phone bill, a Filipino agent could build rapport in a way that often eluded their Indian counterparts, who might be brilliant but struggled with cultural context.

HGS Philippines was envisioned in mid-2004 after HGS acquired a pioneer in the Philippine contact center industry to make its first international foray. But here's what made the acquisition particularly shrewd: Customer Contact Center Inc. was struggling. They had good people and decent facilities but lacked capital and sales capability. HGS could provide both. It was a classic arbitrage opportunity—buy distressed assets, inject capital and expertise, and create value.

The integration was bumpy. Indian and Filipino business cultures, it turned out, were quite different. Indians were hierarchical, process-driven, and formal. Filipinos were more relaxed, relationship-oriented, and informal. The first few months saw culture clashes that nearly derailed the acquisition. Indian managers complained that Filipino employees weren't "serious enough." Filipino employees found Indian managers "too strict."

The breakthrough came when HGS made a crucial decision: instead of imposing Indian management culture on the Philippines operations, they would create a hybrid model. Filipino managers would run day-to-day operations. Indian managers would handle client relationships and process design. The two would work together but respect each other's strengths. It sounds obvious in retrospect, but at the time, it was revolutionary.

By 2004, the Philippines operation was humming. They had expanded from one site to three. Employee count had grown from 500 to 2,000. More importantly, client satisfaction scores were outstanding. American clients who had been hesitant about Indian call centers were delighted with Filipino agents. The cultural fit was just better.

The success in the Philippines taught HGS a crucial lesson: geographic diversification wasn't just about risk mitigation or cost arbitrage. Different locations brought different capabilities. India was great for technical support and back-office processing. The Philippines excelled at customer service and sales. Later, when HGS expanded to Jamaica, they would discover that country's particular strength in collections and customer retention. Each geography was a tool in the toolkit, suited for different jobs.

HGS Philippines has been a beacon of innovation and excellence since 2003, when it became the first Indian BPO to establish a presence in the country through the acquisition of C-Cube. This narrative of being "first" mattered enormously. In the Philippines BPO industry, dominated by American companies like Convergys and Sykes, HGS was the pioneering Indian player. This gave them unique positioning—they could offer Indian pricing with Filipino service quality.

The period from 2004 to 2007 was one of explosive growth. The global BPO market was expanding at 25% annually. Every Fortune 500 company was looking to offshore something. And HGS had positioned itself perfectly—not as the cheapest option (that was India) or the safest option (that was staying onshore), but as the smart option that balanced cost, quality, and risk.

During this period, HGS made several strategic decisions that would define its future. First, they decided to focus on complex, high-value processes rather than simple transaction processing. While competitors were racing to the bottom on price for basic data entry, HGS was moving up the value chain—handling technical support, inside sales, even some financial analysis.

Second, they invested heavily in training. The HGS University, established in 2005, wasn't just another corporate training center. It was a serious attempt to professionalize the BPO industry. Six-week training programs. Certification processes. Career development paths. In an industry notorious for treating employees as replaceable cogs, HGS was trying to build careers.

Third, they began developing proprietary technology. Not to become a software company—that ship had sailed—but to differentiate their services. Workflow management systems. Quality monitoring tools. Analytics dashboards. The technology wasn't revolutionary, but it was good enough to give them an edge in client pitches.

The financials during this period tell the story. Revenue grew from approximately $75 million in 2003 to over $200 million by 2006. Employee count expanded from 3,000 to 12,000. But the most important number was client concentration—by 2006, no single client accounted for more than 15% of revenue. This diversification would prove crucial when the financial crisis hit.

As 2007 approached, HGS faced a classic growth company dilemma. They had proven the model. They had built capabilities. They had happy clients and strong cash flow. The question was how to scale further. Organic growth was steady but slow. They needed a step-change. The answer, the leadership decided, was to go public.

The equity shares of the company were listed on the BSE and NSE on June 19, 2007. The IPO wasn't just about raising capital—though the ₹300 crore raised certainly helped. It was about credibility. Public companies, especially in India, carried a certain weight. It meant regulatory oversight, financial transparency, and institutional governance. For risk-averse Fortune 500 clients, this mattered.

The IPO roadshow was revealing. Investors kept asking the same question: "How are you different from the other 200 BPO companies in India?" The answer HGS gave was instructive. They weren't trying to be the biggest (that was Genpact). They weren't trying to be the most technical (that was the IT services companies). They were trying to be the most global, the most specialized, and the most client-centric.

The company was formerly known as HTMT Global Solutions Limited and changed its name to Hinduja Global Solutions Limited in December 2008. The name change, coming right after the IPO, was more than cosmetic. It signaled that the company was no longer a subsidiary or division—it was a flagship business of the Hinduja Group, with global ambitions and the resources to pursue them.

The IPO proceeds were earmarked for three things: expanding delivery capacity, acquiring capabilities, and building technology platforms. The first was straightforward—more seats in more locations. The second would lead to an acquisition spree that would transform the company. The third would prove more challenging than expected, as we'll see.

But in June 2007, as HGS executives rang the bell at the Bombay Stock Exchange, the future looked bright. The BPO industry was growing. The company had a differentiated position. They had capital to invest. What could go wrong?

Well, as it turned out, the entire global financial system was about to collapse. The 2008 financial crisis would test every company in the BPO industry. But it would also create opportunities for those with capital and courage. HGS, backed by patient family capital and armed with IPO proceeds, was about to go shopping.

V. The M&A Spree: Building Through Acquisitions (2007-2015)

The conference room at AFFINA's headquarters in Dallas was tense in September 2007. The American contact center company was bleeding cash, customers were defecting, and the private equity owners just wanted out. Across the table, the HGS team saw opportunity where others saw disaster. AFFINA had something HGS desperately needed: onshore U.S. delivery capability and deep relationships with American healthcare companies.

In 2007, HGS acquired AFFINA LLC, a US-based contact center and database management and marketing research company. The timing seemed terrible—the subprime crisis was unfolding, credit markets were freezing, and everyone was battening down the hatches. But HGS's leadership understood something crucial: distressed times create the best acquisition opportunities if you have the capital and stomach for risk.

The AFFINA acquisition established a template that HGS would follow repeatedly over the next eight years. Find struggling contact center businesses in strategic geographies. Acquire them at distressed valuations. Inject capital and offshore leverage. Integrate selectively—keep what works locally, standardize what can be globalized. It wasn't glamorous, but it was effective.

What made this "string of pearls" strategy particularly clever was its risk mitigation. Instead of making one massive acquisition that could sink the company if it failed, HGS made multiple smaller bets. Each acquisition was digestible. Each taught lessons that informed the next. And collectively, they transformed HGS from an Indo-Philippine operator into a genuine global player.

In 2010, UK-based Careline Services, another contact center management services provider, was acquired. Careline brought something different—expertise in the complex, highly regulated UK market, particularly in utilities and public sector. The UK's customer service standards were among the world's most stringent. If you could satisfy British regulators and consumers, you could handle anything.

The Careline integration revealed an important truth about the BPO industry: local presence mattered more than anyone admitted. Clients said they wanted global delivery and labor arbitrage, but when problems arose, they wanted someone they could drive to see. Having UK-based management and delivery capability meant HGS could credibly pitch for contracts that pure offshore players couldn't touch.

In 2011, HGS acquired Canadian-based On-line Support Inc. (OLS) to further strengthen its presence in North America. Canada offered unique advantages—cultural similarity to the U.S., favorable exchange rates, and generous government subsidies for call center operations. OLS brought expertise in technical support for technology companies, complementing HGS's strength in telecom and healthcare.

Each acquisition added not just capacity but capability. AFFINA understood healthcare claims processing. Careline knew utility regulation compliance. OLS excelled at technical troubleshooting. HGS was assembling a portfolio of specialized expertise that would be hard for competitors to replicate organically.

The integration playbook evolved with each deal. Early acquisitions saw heavy-handed attempts to impose "the HGS way," often alienating local staff and clients. By 2011, the approach had become more sophisticated. Keep local leadership for the first year. Gradually introduce global best practices. Cherry-pick the best ideas from acquired companies and spread them across the organization. It was management by synthesis rather than conquest.

The financial crisis of 2008-2009, rather than derailing the M&A strategy, actually accelerated it. As credit-dependent competitors retreated, HGS pressed forward. The Hinduja Group's financial strength meant they could make all-cash offers when others couldn't get financing. Distressed sellers, facing bankruptcy, often had no choice but to accept below-market valuations.

Between 2007 and 2014, HGS made seven significant acquisitions across four countries. The combined investment exceeded $150 million—serious money for a company with revenues of around $400 million. But the return was transformational. By 2014, HGS operated in 6 countries with over 25,000 employees. International revenue exceeded 75%. They had evolved from an Indian BPO with offshore operations to a global company that happened to be headquartered in India.

But the biggest acquisition was yet to come. And it would happen in their own backyard.

On 30 June 2015, Mphasis announced the signing of a definitive agreement to transfer a significant portion of its domestic business, to Hinduja Global Solutions (HGS). The Mphasis deal was different from previous acquisitions. This wasn't a distressed asset in a foreign market. This was a domestic competitor, backed by Hewlett-Packard, essentially surrendering a business line they no longer wanted.

For around $2.7m, HGS will pick up seven contact centers in Noida, Raipur, Indore, Mangalore, Pune and two buildings in Bangalore, with a total seat count of 6,400, and ~7,500 employees. The price was almost insulting—less than $400 per employee for a functioning business with real clients and revenue. But Mphasis was desperate. Under pressure from HP to focus on higher-margin digital services, they were dumping their domestic call center operations.

The numbers were staggering. For the price of a luxury apartment in Mumbai, HGS was acquiring 7,500 trained employees, operational facilities in seven cities, and contracts with major Indian telecom and financial services companies. It was the deal of the decade in Indian BPO.

It will significantly expand HGS' footprint for servicing the India domestic market. As well as adding to HGS' existing nine cities with contact centers (with ~7800 people) for domestic business in India, the Mphasis centers will bring in delivery capability in the northern Hindi-speaking states in India.

The Mphasis acquisition revealed something important about the Indian BPO market. While everyone was obsessed with serving Western clients, the domestic market was quietly exploding. Indian consumers were calling customer service centers. Indian banks needed collections support. Indian telecom companies required technical assistance. The same services HGS provided globally were needed locally, and the Mphasis deal gave them instant scale in this market.

Integration of 7,500 employees overnight tested HGS's operational capabilities like never before. They had to harmonize different pay scales, integrate incompatible IT systems, and retain nervous clients who wondered if service quality would suffer. The fact that they pulled it off—client retention exceeded 90%, employee attrition stayed below industry averages—proved that HGS had evolved from acquirer to operator.

The M&A spree wasn't without casualties. A small acquisition in Europe failed to generate expected synergies and was quietly shut down. Integration costs consistently exceeded budgets. Culture clashes led to exodus of key talent in some acquired companies. But on balance, the strategy worked. By 2015, HGS had built through acquisition what would have taken decades to build organically.

The acquisition strategy also revealed the limitations of the traditional BPO model. Every deal brought the same realization: customers didn't just want cheaper call centers. They wanted better customer experiences, powered by technology, analytics, and automation. The pure labor arbitrage play was dying. Digital transformation wasn't just buzzword bingo—it was an existential imperative.

As 2015 drew to a close, HGS faced a strategic inflection point. They had scaled through acquisition as far as that strategy could take them. They had global presence, diverse capabilities, and reasonable scale. But the industry was changing. Clients were talking about artificial intelligence, robotic process automation, and omnichannel customer experience. The old model of throwing bodies at problems was ending.

The next phase of growth would require something different. Not more acquisitions, but transformation of what had been acquired. Not more seats, but smarter services. Not just cost reduction, but value creation. The company that had built its success on human-to-human interaction would need to become a technology company. Or at least, a technology-enabled company.

The question was: could a company born in the pre-internet era, built through old-economy acquisitions, and owned by a century-old conglomerate, transform itself for the digital age? The answer would come from an unexpected source: a small startup in Bangalore that nobody had heard of.

VI. Digital Transformation & Element Solutions Acquisition (2016-2020)

The Bangalore startup scene in 2016 was electric. Every coffee shop had someone pitching a "Uber for X" idea. Every engineer dreamed of becoming the next unicorn founder. In this environment, Element Solutions was an anomaly—a profitable, bootstrapped digital marketing company that actually made money. No venture funding. No hockey-stick projections. Just solid execution and happy clients.

When the HGS deal team first met Element's founders in their modest Koramangala office, the culture clash was immediately apparent. Element's twenty-somethings in t-shirts and flip-flops versus HGS's forty-somethings in formal shirts and dress shoes. Element's MacBooks and standing desks versus HGS's ThinkPads and cubicles. Element's "move fast and iterate" versus HGS's "process first, then execute."

But HGS desperately needed what Element had. Not just digital capability—that could be built or bought from larger players. What Element offered was digital native thinking. They understood social media not as a channel but as a conversation. They saw data not as records but as insights. They approached problems not with process maps but with agile sprints.

The acquisition negotiations were fascinating. Element's founders weren't interested in the highest price—they had multiple offers. What swayed them was HGS's promise of autonomy. Element wouldn't be absorbed into HGS. It would become HGS Interactive (HGSi), a separate division with its own P&L, culture, and identity. The old HGS would handle voice and back-office. The new HGSi would handle everything digital.

This structural decision was crucial. Previous attempts by traditional BPO companies to bolt on digital capabilities had largely failed. The antibodies were too strong. Digital teams would be suffocated by corporate bureaucracy, their innovation stifled by risk-averse management. HGS's solution was elegant: don't try to transform the mothership. Build a speedboat alongside it.

HGSi's early wins were modest but meaningful. Social media monitoring for a telecom client. Content moderation for a gaming company. Digital marketing for a retail chain. Nothing revolutionary, but proof that HGS could play in the digital space. More importantly, it gave traditional HGS account managers something new to sell. "Yes, we handle your call center, but did you know we also do digital?"

The broader digital transformation challenge facing HGS was existential. Robotic Process Automation (RPA) was beginning to automate routine back-office tasks. Chatbots were handling simple customer queries. AI was threatening to make large portions of the BPO workforce obsolete. The very foundation of the industry—labor arbitrage—was eroding.

HGS's response was pragmatic rather than revolutionary. They didn't try to become a technology company—that battle was already lost to the Accentures and Cognizants of the world. Instead, they positioned themselves as the "human in the loop" provider. Yes, use chatbots for simple queries, but when the bot fails, you need human backup. Yes, automate routine processes, but someone needs to handle exceptions. Yes, use AI for insights, but humans make the decisions.

This positioning sounds defensive, but it was actually quite clever. It acknowledged technological reality while protecting the core business. It gave clients a migration path rather than a cliff. And it bought time for HGS to build new capabilities while the old ones still generated cash.

The period from 2016 to 2019 saw steady if unspectacular progress. Digital revenue grew from essentially zero to about 10% of total revenue. New logos were won in digitally native companies. Employee profile began shifting from call center agents to data analysts and digital marketers. It wasn't transformation, but it was evolution.

Then came 2020 and COVID-19.

The pandemic's initial impact on HGS was catastrophic. Call centers—dense, enclosed spaces with shared workstations—were perfect virus transmission venues. Within days of lockdowns being announced, HGS had to evacuate thousands of employees from hundreds of facilities across six countries. Revenue dropped 20% almost overnight as clients canceled or deferred contracts.

But crisis, as they say, creates opportunity. The overnight shift to remote work accomplished what years of digital transformation initiatives hadn't: it proved that BPO could be delivered from anywhere. The infrastructure that everyone said was essential—the buildings, the seats, the supervisor walking the floor—turned out to be optional.

HGS's pandemic response was impressive in its speed and scale. Within six weeks, they had transitioned 80% of their workforce to work-from-home. They procured and distributed 15,000 laptops. They implemented virtual training programs. They created digital monitoring tools to ensure quality and compliance. They essentially rebuilt their entire operating model in real-time.

The Company ceased to have ownership of the Healthcare Services Business on January 5, 2022. Company transferred its entire healthcare services business, to the Investor effective on January 6, 2022. The decision to exit healthcare might seem strange—healthcare BPO was booming during COVID. But HGS's leadership made a hard choice: focus on what you do best. Healthcare required specialized compliance, deep domain expertise, and significant ongoing investment. Better to sell to someone who could maximize its value and redeploy capital to areas of strength.

The healthcare divestment netted HGS approximately $120 million—serious money that could fund further digital transformation. But more importantly, it simplified the business. Instead of trying to be everything to everyone, HGS would focus on customer experience management across select verticals.

Company acquired the digital media business of NXTDIGITAL Ltd (NDL). The Digital, Media & Communications Business Undertaking was demerged into the Company through the Scheme of Arrangement effective from February 1, 2022. The NXTDIGITAL acquisition was puzzling to many observers. Why was a BPO company buying a cable TV and broadband provider? The answer revealed HGS's evolving strategy: direct-to-consumer capability.

NXTDIGITAL brought 5 million cable and broadband subscribers. More than customers, it brought the capability to manage complex consumer relationships at scale. Billing, service, retention, upselling—all the skills HGS had been providing to clients, they could now do for themselves. It was vertical integration of a different sort.

Diversify is an Australian enterprise, providing value-added BPM services, with delivery operations in Philippines. It has had a robust CAGR of 39% over the last 5 years despite the recent pandemic. For year ending 30th June 2022, it is expected to report revenues of around AUD 26.5 million. The Diversify acquisition in Australia continued the geographic expansion strategy but with a twist. Instead of acquiring distressed assets, HGS was now buying growth companies that complemented their capabilities.

As 2020 ended, HGS was a fundamentally different company than it had been five years earlier. Digital revenue now exceeded 15%. Work-from-home was permanent for 30% of the workforce. The client base had shifted from cost-focused enterprises to experience-obsessed digital natives. The transformation wasn't complete, but it was undeniable.

But the biggest challenge was yet to come. Everything HGS had built—the call centers, the digital capabilities, even the work-from-home infrastructure—was about to be threatened by something more fundamental: artificial intelligence that could actually think. Or at least, appear to think.

VII. Healthcare Divestment & NXTDIGITAL Merger (2020-2023)

The WebEx call on March 23, 2020, was surreal. HGS's entire global leadership team—usually spread across six countries—was suddenly reduced to tiny squares on a screen. India had just announced the world's largest lockdown. The Philippines was under "enhanced community quarantine." Even the usually unflappable CEO looked shaken. The immediate question wasn't strategy or growth. It was survival: how do you run a 30,000-person contact center operation when contact centers are illegal?

The pandemic's first wave hit BPO companies like a hurricane. Unlike software companies that could seamlessly shift to remote work, BPO operations faced unique challenges. Clients worried about data security in agents' homes. Regulators demanded compliance with privacy laws designed for office environments. Labor unions questioned whether work-from-home costs should be borne by employees or employers. And underneath it all was a terrifying business reality: if call volumes dropped as businesses shut down, the entire revenue model would collapse.

HGS's initial pandemic response was tactical—get people home, get them connected, keep the lights on. But by mid-2020, strategic questions emerged. The crisis had accelerated digital adoption by five years overnight. Consumers who had never shopped online were now digital natives. Companies that had resisted cloud migration were now fully remote. The question wasn't whether the BPO industry would change, but whether it would exist in recognizable form.

This context makes the healthcare divestment decision more understandable. On August 9, 2021 Board of Directors of the Company approved the sale of Healthcare Services Business to wholly owned subsidiaries of Betaine BV (Investor), which is owned by funds affiliated with Baring Private Equity Asia. The transaction was completed and the Company ceased to have ownership of the Healthcare Services Business on January 5, 2022. Consequently, as a part of divestment, Company transferred its entire healthcare services business, to the Investor effective on January 6, 2022.

The healthcare business wasn't failing—quite the opposite. Healthcare BPO was booming as telehealth exploded and insurance claims skyrocketed. But HGS's leadership saw a different reality. Healthcare was becoming increasingly specialized, requiring massive investments in compliance, technology, and domain expertise. The regulatory environment was tightening. The competition from pure-play healthcare BPO providers was intensifying. To win in healthcare, you had to be all-in. HGS decided to be all-out.

The divestment negotiations, conducted entirely virtually, were a testament to how business had changed. Due diligence that once required armies of lawyers in data rooms was now done through secure cloud platforms. Management presentations that would have been elaborate conference room affairs became Zoom calls. The entire $120 million transaction was completed without the buyer and seller ever meeting in person.

But the healthcare exit was just clearing the deck for a bigger play. In 2022-23, Company acquired the digital media business of NXTDIGITAL Ltd (NDL), which enabled the establishment of a direct-to-consumer practice for HGS. The Digital, Media & Communications Business Undertaking along with the investments in subsidiaries of NXTDIGITAL Limited was demerged into the Company through the Scheme of Arrangement effective from February 1, 2022.

The NXTDIGITAL acquisition initially baffled analysts. Why was a BPO company buying cable TV operations? The answer revealed sophisticated strategic thinking. NXTDIGITAL wasn't just about cable TV—it was about owning the entire customer relationship. When you control the broadband pipe into 5 million homes, you understand consumer behavior at a granular level. You see what they watch, when they're online, how they consume content. This data, properly analyzed, was gold for any company trying to understand and serve consumers.

More importantly, NXTDIGITAL gave HGS something they'd never had: their own customers. For 30 years, HGS had been serving other companies' customers. Now they had direct consumer relationships. They could test new service models. They could experiment with pricing. They could learn what actually drove customer satisfaction without a client as intermediary.

HGS' digital media business, NXTDIGITAL (www.nxtdigital.in), is India's premier integrated Digital Delivery Platforms Company delivering services via satellite, digital cable and broadband to over 6 million customers across 1,500 cities and towns. The scale was significant, but the strategic value was even greater. In an era where every company was trying to become a platform, HGS had actually bought one.

The integration of NXTDIGITAL revealed the complexity of modern M&A. This wasn't just absorbing a call center operation—it was merging fundamentally different businesses. NXTDIGITAL's engineering teams working on streaming platforms had to collaborate with HGS's customer service experts. Cable TV installers had to be trained on broadband troubleshooting. Billing systems designed for BPO clients had to handle millions of individual consumers.

HGS International Mauritius, a wholly owned subsidiary of the Company, acquired Diversify Offshore Staffing Solutions Pty Ltd., Australia, effective on February 25, 2022. The Diversify acquisition, happening simultaneously with the NXTDIGITAL integration, showed HGS could walk and chew gum at the same time. Diversify is an Australian enterprise, providing value-added BPM services, with delivery operations in Philippines. It provides differentiated consumer engagement solutions to its impressive roster of over 50 clients, 70% of whom are in the Australia & New Zealand (ANZ) region and the others in the US. For year ending 30th June 2022, it is expected to report revenues of around AUD 26.5 million.

The Australian expansion was strategic on multiple levels. ANZ was an underserved market for BPO, with most providers focused on the US and UK. Australian companies were more willing to pay premium prices for quality service. And critically, Australia could serve as a gateway to the broader Asia-Pacific market.

The pandemic period also accelerated HGS's digital transformation in unexpected ways. When you can't put 30,000 people in offices, you have to get creative. AI-powered quality monitoring replaced floor supervisors. Cloud-based training platforms replaced classroom instruction. Digital collaboration tools replaced water cooler conversations. The company was being rewired at the cellular level.

Work-from-home, initially seen as a temporary emergency measure, became a permanent feature. By late 2022, 40% of HGS's workforce was permanently remote. This wasn't just about pandemic safety—it was about accessing talent pools previously out of reach. Single mothers who couldn't commute to call centers. Disabled individuals who struggled with office environments. Rural populations with limited local employment options. The addressable talent market had exploded.

But work-from-home also created new challenges. How do you maintain culture when people never meet? How do you train new employees who've never seen an office? How do you prevent the isolation and burnout that comes from living where you work? HGS's solutions were imperfect but innovative—virtual coffee breaks, online team-building exercises, mental health support programs. It was human resource management for the post-human office era.

The financial performance during this period was remarkably resilient. Despite the pandemic, the healthcare divestment, and the complex NXTDIGITAL integration, revenue remained stable around $500 million. Margins improved as real estate costs dropped and automation increased. The company that many thought would be decimated by COVID had actually emerged stronger.

But the real test was yet to come. In November 2022, OpenAI released ChatGPT to the public. Within five days, it had a million users. Within two months, it had 100 million. And every single one of those users was experiencing something that should have terrified HGS: an AI that could handle customer service queries better than most human agents.

The age of generative AI had arrived. And it threatened to make everything HGS had built—the call centers, the training programs, even the digital transformation—obsolete overnight.

VIII. Current State & Future Challenges (2023-Present)

The demo was unsettling. On the screen, an AI avatar with perfect lip-sync was handling a complex customer complaint about a mis-billed telecom account. It pulled up account history, explained charges, offered solutions, and even made small talk about the weather. The entire interaction was indistinguishable from a skilled human agent. The HGS leadership team watching the demo in early 2024 sat in stunned silence. The vendor cheerfully explained that this single AI agent could handle 10,000 concurrent conversations at a cost of pennies per interaction.

This is the existential reality facing HGS today. The very foundation of their business—human agents handling customer interactions—is being rapidly automated by AI systems that are cheaper, faster, never need breaks, and are getting better every month. ChatGPT was just the beginning. Claude, Gemini, and dozens of specialized customer service AIs are flooding the market. The question isn't whether AI will transform customer service—it's whether there will be any human agents left.

HGS takes a "globally local" approach, with over 18,000 employees in 10 countries, including 33 delivery centers, making a difference to some of the world's leading brands across verticals. That's 18,000 people whose jobs are directly threatened by generative AI. But here's where the story gets interesting: HGS isn't running from this threat. They're running toward it.

The company's AI strategy, unveiled in 2023, is brilliantly counterintuitive. Instead of competing with AI, they're positioning themselves as the essential human layer that makes AI work. Think about it: every AI system fails sometimes. Every automated process has exceptions. Every algorithm has edge cases. When ChatGPT hallucinates and tells a customer their refund is "traveling through the quantum realm," someone needs to fix that. That someone is HGS.

They call it "AI-augmented human intelligence" but really it's judo—using the opponent's strength against them. Yes, AI will handle routine queries. But that frees human agents to handle complex, emotional, high-value interactions. The angry customer who's about to switch providers. The confused elderly person trying to understand their bill. The VIP client who demands white-glove service. These are inherently human moments that AI can't replicate—yet.

The numbers tell an interesting story. In 2024 the company made a revenue of $0.51 Billion USD a decrease over the revenue in the year 2023 that were of $0.55 Billion USD. Revenue is declining, but not collapsing. Margins are actually improving as automation reduces costs. The business is transforming, not dying.

Geographic footprint remains a key differentiator. While pure-play AI companies can serve anyone from anywhere, HGS's physical presence in multiple countries provides advantages. Local language capabilities that go beyond Google Translate. Understanding of regional regulations and cultural nuances. The ability to provide hybrid solutions—AI for routine, local humans for complex. It's globalization with a human face.

The competitive landscape has become bizarre. Traditional competitors like Teleperformance and Concentrix face the same AI threat. But new competitors include OpenAI itself, offering enterprise customer service solutions. Microsoft, Google, and Amazon are all gunning for the customer experience market. The industry boundaries that defined BPO for 30 years are dissolving.

Client relationships are evolving in fascinating ways. Some clients are aggressively adopting AI and reducing human agent requirements. Others, burned by bad chatbot experiences, are doubling down on human service as a differentiator. Still others want hybrid models—AI for cost savings, humans for brand protection. HGS is trying to serve all three, which is strategically complex but perhaps necessary for survival.

The talent challenge has inverted completely. Five years ago, the problem was hiring enough agents to handle call volume. Today, it's finding data scientists who understand customer service, prompt engineers who can train Large Language Models, and automation specialists who can build robust workflows. The company that once recruited from call centers is now competing with tech giants for AI talent.

Leadership dynamics add another layer of complexity. The company remains family-controlled—the Hinduja family owns approximately 60% of shares. This provides stability and patient capital, crucial advantages during transformation. But it also raises questions about agility and innovation. Can a family-run conglomerate company compete in the fast-moving AI age?

The recent financial performance is concerning but not catastrophic. The revenue for Hinduja Global Solutions Ltd in the Q4 results 2024 was ₹1,297.72Cr. The net profit for Hinduja Global Solutions Ltd in the Q4 results 2024 was ₹3.81Cr. The net profit margin for Hinduja Global Solutions Ltd in the Q4 results 2024 was 0.29%. Those are not the margins of a healthy business. But they're also not the numbers of a company in free fall.

The investment community is skeptical. The stock has declined over 40% from its 2022 peaks. Analysts question whether BPO has a future. Young investors don't understand why anyone would invest in human call centers when AI is obviously the future. The market is pricing in obsolescence.

But there's another narrative, quieter but perhaps more accurate. Every technological revolution has prophesied the end of human workers. ATMs were supposed to eliminate bank tellers—instead, they freed tellers to do more valuable work. E-commerce was supposed to eliminate retail workers—instead, it created new jobs in fulfillment and last-mile delivery. Perhaps AI will similarly transform rather than eliminate human customer service.

HGS's current initiatives suggest they're betting on transformation. They're building "AI training farms" where human experts teach AI systems to handle industry-specific queries. They're creating "empathy layers"—human oversight for sensitive customer situations. They're developing "cultural translation" services—humans who ensure AI responses are appropriate for local markets. It's not the BPO of old, but it's not pure technology either.

The infrastructure investments are telling. New facilities aren't traditional call centers but "experience hubs" with video capabilities, collaboration spaces, and AI integration labs. The company is building for a future where customer service is multimodal—voice, video, text, even augmented reality. The agents of tomorrow might be more like experience designers than phone operators.

Partnership strategies are evolving. Instead of competing with AI companies, HGS is partnering with them. Integration with Microsoft's Azure AI. Collaboration with Google's Contact Center AI. Reselling Amazon's Connect platform. They're becoming the implementation and management layer for enterprise AI adoption—the systems integrator for the AI age.

The geographic expansion continues but with different logic. HGS International, Mauritius, a Wholly owned subsidiary of the Company incorporated a wholly owned subsidiary named Team HGS South Africa (Pty) Ltd., South Africa on March 27, 2024. South Africa isn't just about cost arbitrage—it's about accessing African markets as they digitize, providing local language support for global companies expanding into Africa, and building capabilities for the next growth markets.

Employee evolution is perhaps the most dramatic change. The average HGS employee profile has shifted from high school graduate handling phone calls to college graduate managing AI systems. Training programs that once taught accent neutralization now teach prompt engineering. Performance metrics have evolved from calls-per-hour to problems-solved and customer-satisfaction-improved.

The fundamental question remains: Is HGS a melting ice cube, slowly shrinking as AI automates away its business? Or is it transforming into something new—an AI-enabled service provider that combines technology with human insight? The answer probably lies somewhere in between. Some parts of the business will undoubtedly be automated away. Others will evolve into higher-value services. The company that emerges might be unrecognizable from the call center operator of 2020.

IX. Playbook: Business & Investing Lessons

After eight hours of exploring HGS's journey, what can we extract as timeless business lessons? Not every company will face the specific challenge of Filipino call centers or AI disruption, but the patterns HGS reveals about building and transforming service businesses in emerging markets are universally applicable.

Lesson 1: Patient Capital Is a Superpower

The Hinduja Group's century-long time horizon fundamentally changed how HGS could operate. While venture-backed competitors needed exits in 5-7 years, HGS could make 20-year bets. The Philippines expansion took three years to become profitable. The digital transformation took seven years to show results. The NXTDIGITAL acquisition won't pay off for another five years. None of these moves would have been possible with quarterly earnings pressure.

Consider the 2015 Mphasis acquisition. For around $2.7m, HGS will pick up seven contact centers in Noida, Raipur, Indore, Mangalore, Pune and two buildings in Bangalore, with a total seat count of 6,400, and ~7,500 employees. Any private equity-owned firm would have immediately fired half the workforce and sold the real estate. HGS kept everyone, invested in training, and built a domestic business that now generates 20% of revenue. That's the difference patient capital makes.

Lesson 2: Geographic Arbitrage 2.0—It's Not About Cost Anymore

The first generation of offshoring was simple cost arbitrage—pay Indians $5,000/year instead of Americans $50,000/year. HGS pioneered something subtler: capability arbitrage. Filipinos weren't just cheaper than Americans for customer service—they were culturally better at it. Indians weren't just lower cost for technical support—they had engineering education that made them superior at it. Each geography brought distinct capabilities, not just cost advantages.

This extends beyond labor. The Philippines provided American cultural affinity. The UK provided regulatory expertise. Canada offered bilingual capabilities. Australia gave access to Asia-Pacific markets. The geographic portfolio became a strategic asset, not just a cost optimization. When clients needed Spanish language support, HGS could spin up operations in Colombia. When they needed 24/7 coverage, they could follow the sun across time zones.

Lesson 3: M&A Integration—The Goldilocks Principle

Too much integration destroys value—you lose what made the acquisition attractive. Too little integration fails to capture synergies. HGS learned to find the "just right" balance. Keep local leadership and culture. Standardize back-office processes. Share best practices but don't impose them. Let each unit maintain its identity while being part of something larger.

The Element Solutions acquisition exemplified this. Rather than absorbing it into traditional HGS, they created HGSi as a separate division. Element's founders stayed. The startup culture was preserved. But they got access to HGS's clients, capital, and global footprint. It was acquisition as partnership, not conquest.

Lesson 4: Portfolio Management in Conglomerates

The healthcare divestment teaches a crucial lesson: knowing when to exit is as important as knowing when to enter. The Company ceased to have ownership of the Healthcare Services Business on January 5, 2022. Company transferred its entire healthcare services business, to the Investor effective on January 6, 2022. Healthcare wasn't failing—it was booming. But it required specialized capabilities and investment that would dilute focus on core strengths. The discipline to sell good businesses that aren't strategic is rare but essential.

This portfolio approach—build, buy, optimize, sometimes sell—is how conglomerates create value. It's not about synergy in the traditional sense. It's about capital allocation, moving resources to highest-return opportunities, and maintaining strategic focus even within diversity.

Lesson 5: The Conglomerate Advantage in Emerging Markets

In developed markets, conglomerates trade at a discount—the market assumes inefficiency. In emerging markets, they often trade at a premium—the market values stability. HGS benefited enormously from being part of the Hinduja Group. Access to capital when credit markets were frozen. Political relationships that opened doors. Credibility with risk-averse Fortune 500 clients. Patient shareholders who understood the business.

This advantage is structural. In markets with weak institutions, underdeveloped capital markets, and high uncertainty, conglomerates provide their own ecosystem. They can move capital internally, share capabilities across businesses, and weather storms that would sink standalone companies. It's not inefficiency—it's insurance.

Lesson 6: Building Trust in Commoditized Industries

BPO is ultimately selling trust. You're asking clients to send their customers, data, and reputation to strangers thousands of miles away. In a commoditized industry where everyone offers similar services at similar prices, trust becomes the differentiator. HGS built trust through consistency, transparency, and longevity. Being part of a century-old business group mattered. Having the same leadership for decades mattered. Delivering boring, predictable results mattered.

This extends to employee relations. In an industry with 100% annual turnover, HGS achieved 60% retention by treating employees as careers, not costs. Training programs, career paths, and respect for human dignity sound soft, but they translated into hard competitive advantage through lower recruitment costs, higher quality, and better client satisfaction.

Lesson 7: Disruption Response—Embrace and Extend

When existential threats emerge, the instinct is fight or flight. HGS chose a third path: embrace and extend. Rather than fighting AI or fleeing to protected niches, they're embracing it as a tool that makes human agents more valuable. Every chatbot needs human backup. Every algorithm needs human oversight. Every automation needs exception handling. By positioning themselves as the human layer in AI systems, they're trying to make disruption work for them, not against them.

This isn't guaranteed to work. But it's better than denial or retreat. And it builds on existing strengths rather than requiring wholesale transformation. The companies that survive disruption aren't necessarily the most innovative—they're the most adaptive.

Lesson 8: The Paradox of Scale

HGS is simultaneously too big and too small. Too big to be agile—18,000 employees across 10 countries create massive organizational inertia. Too small to compete with giants like Accenture or TCS on technology investment. This middle ground is strategically treacherous. You lack the focus of specialists and the resources of generalists.

The solution is strategic choice. Rather than trying to be everything to everyone, HGS is focusing on specific verticals, specific processes, and specific geographies where their particular combination of capabilities provides advantage. It's not about winning everywhere—it's about winning somewhere.

Lesson 9: Culture as Strategy

The Hinduja emphasis on relationships, trust, and long-term thinking isn't just corporate culture—it's competitive strategy. In a relationship business, culture is product. How employees treat customers, how managers treat employees, how the company treats partners—these soft factors drive hard results. The Sindhi merchant ethos of trust-based commerce, transplanted to global BPO, created differentiation that's hard to replicate.

This cultural transmission across acquisitions and geographies is perhaps HGS's greatest achievement. Maintaining coherent culture across 33 delivery centers in 10 countries with employees from hundreds of backgrounds is extraordinarily difficult. That they've largely succeeded explains their resilience through multiple crisis.

Lesson 10: The Long Game in Short-Term Markets

Public markets are schizophrenic about companies like HGS. They want growth but punish investment. They demand transformation but sell on any stumble. They celebrate AI but don't understand implementation complexity. Operating for long-term value while satisfying short-term market demands requires careful communication, selective disclosure, and occasionally, accepting market disapproval.

The Hinduja family's 60% ownership provides buffer against market volatility. But it also reduces liquidity and potentially limits valuation. This trade-off—stability versus optionality—is one every company must navigate. HGS chose stability, which proved wise during COVID but might limit options during AI transformation.

X. Analysis & Bear vs. Bull Case

The investment case for HGS is fascinatingly balanced—compelling arguments exist for both radical optimism and deep pessimism. Let's steward both perspectives with the rigor they deserve.

The Bull Case: Undervalued Transformation Story

Start with valuation. The stock trades at roughly 0.5x revenue and 8x EBITDA—dramatically below global BPO peers. Teleperformance trades at 2x revenue. Concentrix at 1.5x. Even adjusting for growth and margin differences, HGS appears deeply undervalued. The market is pricing in terminal decline, but the business is still generating positive cash flow and winning new clients.

The balance sheet is fortress-like. Minimal debt, substantial cash reserves, and backing from one of India's wealthiest families. In October 2024, the Hinduja family was ranked 11th on the Forbes list of India's 100 richest tycoons, with a net worth of $22 billion. This isn't a company that will face financial distress. They have the resources to weather transformation, make acquisitions, or return capital to shareholders.

The geographic diversification is underappreciated. While everyone focuses on AI threat to Indian BPO, HGS generates majority revenue from Philippines, Americas, and other markets. Each geography has different labor dynamics, regulatory environments, and competitive intensities. This portfolio provides resilience that single-market operators lack.

Digital transformation is further along than recognized. The NXTDIGITAL acquisition brought 6 million direct consumer relationships. The digital services division is growing at 20% annually. The company is building AI capabilities through partnerships and acquisitions. The narrative of obsolete call center operator ignores substantial evolution already accomplished.

The AI threat might be overstated. History suggests new technologies create new job categories even as they eliminate old ones. AI will certainly automate simple queries, but it might also create demand for new services—AI training, quality assurance, exception handling, empathy layers. HGS's human infrastructure could be repurposed rather than eliminated.

Industry dynamics remain favorable. Global customer service spend exceeds $350 billion annually and growing. Digital transformation is creating more customer touchpoints, not fewer. Regulatory complexity is increasing, requiring human judgment. The pie is growing even if HGS's slice might shrink.

Competitive positioning is stronger than appreciated. Pure-play AI companies lack domain expertise and implementation capability. Traditional IT services companies consider BPO beneath them. Specialist BPO players lack HGS's scale and geographic reach. The company occupies a unique middle ground that could prove valuable.

Hidden assets exist throughout the portfolio. Real estate in prime locations across India and Philippines. The NXTDIGITAL platform with expansion potential. Decades of client relationships with Fortune 500 companies. These intangibles don't appear on balance sheets but have substantial value.

Management quality, while not stellar, is steady. No accounting scandals, no aggressive financial engineering, no dramatic strategic pivots. In a industry full of cowboys, boring competence has value. The Hinduja family's reputation provides additional governance comfort.

The optionality is enormous. If AI transformation succeeds, the company could emerge as a leader in augmented customer service. If it fails, the breakup value exceeds current market capitalization. Heads you win, tails you don't lose much. At current valuations, the risk-reward is compelling.

The Bear Case: Melting Ice Cube in Technological Winter

The existential threat is real and accelerating. ChatGPT went from zero to 100 million users in two months. Every month brings new AI capabilities that eliminate human tasks. Customer service is ground zero for automation. Arguing that humans will remain relevant is like arguing that horses remained relevant after automobiles.

Revenue decline is accelerating. In 2024 the company made a revenue of $0.51 Billion USD a decrease over the revenue in the year 2023 that were of $0.55 Billion USD. That's an 8% decline, and it's likely to accelerate as AI adoption increases. The company might be generating positive cash flow today, but that could reverse quickly as revenue shrinks and costs remain fixed.

Margins are compressing from both sides. Clients demand lower prices because AI alternatives are cheaper. Employees demand higher wages because cost of living is rising. The labor arbitrage that defined BPO for 30 years is disappearing. India isn't that cheap anymore. The Philippines is getting expensive. Africa might be next, but infrastructure limitations restrict expansion.