H.G. Infra Engineering Limited: Building India's Infrastructure Foundation

I. Introduction & Episode Roadmap

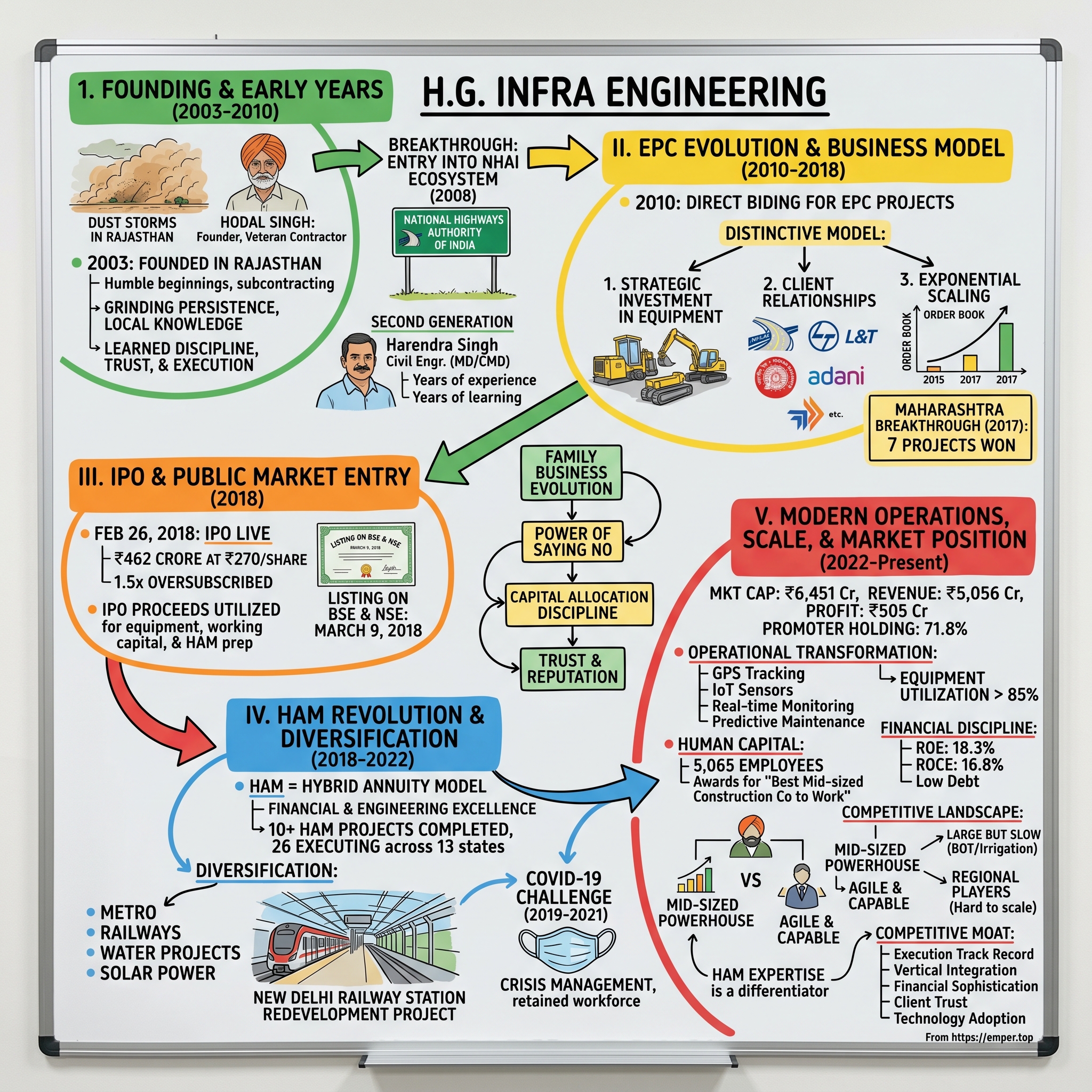

Picture this: A dusty construction site in Rajasthan, 2003. While India's infrastructure boom was just beginning to stir, a veteran contractor named Hodal Singh was laying the foundation for what would become one of the country's most intriguing infrastructure stories. Two decades later, his company—H.G. Infra Engineering—commands a market capitalization exceeding ₹6,400 crores and executes projects spanning from the deserts of Rajasthan to the hills of Northeast India. The question that fascinates infrastructure investors isn't just how a company grows—it's how a regional player transforms into a national force while maintaining the operational discipline that got them there. H.G. Infra now manages projects spanning several states across India with a current turnover of approximately 5000+ crores, yet twenty years ago, this was simply Hodal Singh's construction firm in Rajasthan, taking on whatever subcontracting work came its way.

What makes HGINFRA particularly intriguing is its timing. The company emerged just as India was embarking on its most ambitious infrastructure buildout in history. But unlike many peers who chased growth at any cost, H.G. Infra's story is one of calculated patience—waiting for the right projects, the right partnerships, and the right moment to scale. Today, the company commands a market capitalization of ₹6,451 crores with revenues of ₹5,056 crores and profits of ₹505 crores, with promoter holding steady at 71.8%—a signal of founder confidence rarely seen in listed infrastructure companies.

The infrastructure sector has created and destroyed fortunes with equal vigor. For every L&T or IRB Infrastructure, there are dozens of companies that overleveraged during boom times and collapsed when the cycle turned. So how did a company from Jaipur navigate these treacherous waters? How did they master both the traditional EPC (Engineering, Procurement, Construction) model and the complex HAM (Hybrid Annuity Model) that has reshaped Indian infrastructure financing? And perhaps most importantly, what can investors learn from their journey as India prepares for its next ₹100 trillion infrastructure push?

This is the story of engineering excellence meeting financial discipline, of regional roots scaling to national ambitions, and of a family business that professionalized without losing its entrepreneurial edge. It's also a masterclass in how to build a sustainable infrastructure business in one of the world's most challenging yet rewarding markets.

II. The Founding Story & Early Years (2003–2010)

The year was 2003. India's Golden Quadrilateral highway project was just gaining momentum, connecting Delhi, Mumbai, Chennai, and Kolkata with modern expressways. In Rajasthan, where dust storms could shut down construction sites for days and summer temperatures soared past 45°C, a veteran contractor named Hodal Singh saw opportunity where others saw obstacles.

Founded in the year 2003, H.G. Infra Engineering Ltd. has been at the forefront of delivering exceptional Engineering, Procurement, and Construction (EPC) services on a fixed-sum turnkey basis and Hybrid Annuity Model (HAM). But the beginning was far humbler. Hodal Singh brought to the table something invaluable: four decades of construction experience and deep relationships within Rajasthan's construction ecosystem. He understood the nuances of working with government agencies, the importance of local labor management, and most critically, the art of completing projects in challenging terrains. Founded by Shri Hodal Singh, a construction industry veteran with 45 years of experience, the company has evolved into an industry leader under the leadership of Mr. Harendra Singh, our Chairman and Managing Director. What's remarkable about this transition is how organic it was—no boardroom coup, no external pressure, just a father recognizing his son's readiness to lead.

The early years were marked by grinding persistence. Originally registered in the name of H.G. Infra Engineering Private Limited in 2003, the company was converted to a joint stocked company under Part IX of the Companies Act 1956 the same year. This wasn't just administrative housekeeping—it signaled ambition. Even in those nascent days, Hodal Singh was laying the groundwork for something bigger than a typical contractor outfit.

The breakthrough came in 2008. Execution of the first subcontract work in 2008 set it on the path to success—a modest description for what was actually a defining moment. This wasn't just any subcontract; it was H.G. Infra's entry into the National Highways Authority of India (NHAI) ecosystem. For infrastructure companies in India, NHAI contracts are the gold standard—predictable payments, clear specifications, and most importantly, reputation capital that opens doors to bigger opportunities. The second generation brought fresh perspective. Harendra Singh holds a Bachelor's degree in Engineering (Civil) from Jodhpur University and had worked briefly at HPCL for three years before joining the family business. He has over 29 years of experience in the construction industry, which means he joined H.G. Infra almost from its inception, learning the business from the ground up under his father's mentorship.

What made this period unique was H.G. Infra's approach to growth. While competitors were rushing to bid for every available project, the company focused on building capabilities. They registered as grade 'AA' Class contractor with PWD Rajasthan and 'SS' Category with Military Engineering Services (MES)—credentials that would prove invaluable in winning government contracts. By 2010, they had established a reputation for something increasingly rare in Indian infrastructure: completing projects on time.

The Rajasthan construction ecosystem of that era was brutal yet formative. Payment delays could stretch for months, mobilization advances were minimal, and contractors often had to fund projects from their own pockets. H.G. Infra survived by maintaining strict financial discipline—a trait that would define their approach even after becoming a billion-dollar company. They learned to work with what they had, optimize equipment utilization, and most importantly, build trust with their workers and suppliers who would wait for payments knowing the company would honor its commitments.

As 2010 approached, India's infrastructure spending was about to explode. The company had spent seven years building its foundation—now it was time to scale.

III. The EPC Evolution & Business Model (2010–2018)

If the first phase of H.G. Infra was about survival and learning, the second was about transformation. The year 2010 marked a pivotal shift—the company decided to stop being just another subcontractor and bid directly for EPC (Engineering, Procurement, and Construction) projects. This wasn't merely climbing up the value chain; it was a complete reimagination of what the company could be.

In 2003, following its incorporation, HG Infra began working as a subcontractor on small projects in Jaipur. In 2012, HG Infra worked with L&T Engineers. The experience with L&T was particularly formative. "We learned a great deal while working with them: they had a very smart system, with proper delegation metrics and KRAs and KPAs. Every person was wholly responsible for the work they had been delegated and the work was always done on time. Theirs is a smart operating system," Harendra Singh would later recall.

But H.G. Infra also learned what not to do. A Spanish firm they partnered with in 2010 taught them what not to do, when they observed the company was willing to maintain a relationship with its subcontractors for the duration of the project only to unceremoniously sever ties upon its completion. This company no longer has a presence in India. The lesson was clear: in infrastructure, relationships matter as much as engineering prowess.

The EPC model that H.G. Infra developed was distinctive. The Company is engaged in engineering, procurement and construction (EPC), maintenance of roads, bridges, flyovers and other infrastructure contract works. But unlike many competitors who relied heavily on subcontractors, H.G. Infra began building its own capabilities. They invested aggressively in equipment—eventually building a fleet of 3,000+ modern machines. This wasn't just capital expenditure; it was strategic positioning. Owning equipment meant better quality control, improved margins, and most importantly, the ability to mobilize quickly for new projects. The period from 2015 to 2017 was transformative. The order book has grown significantly over the last three years, from Rs.1,067.70 crore as of March 31, 2015, to Rs.1,446.27 crore as of March 31, 2016 and Rs.4,019.09 crore as of March 31, 2017, respectively. This wasn't just growth—it was exponential scaling, nearly quadrupling the order book in just two years.

The Maharashtra breakthrough of 2017 deserves special attention. In 2017, the company won seven construction projects in Maharashtra worth Rs 1904.59 crore by MoRTH. For a Rajasthan-based company to win projects of this magnitude in Maharashtra—a state with its own established contractors—was a statement victory. It proved H.G. Infra could compete anywhere in India.

The company's client relationships tell a story of credibility building. With an impressive execution track record spanning over two decades, we've successfully bid on independent contracts from prestigious organizations like NHAI, MoRTH, Indian Railways, DMRC, State Governments, and collaborated with industry giants such as Adani, Tata Projects, and IRB. Each of these names represents a different validation—NHAI for technical capability, state governments for local execution, and private giants for reliability.

By 2017, the company was ready for its next evolution. They had the track record, the equipment base, the client relationships, and most importantly, the confidence to access public markets. The stage was set for what would become one of the more successful infrastructure IPOs of that era.

IV. The IPO Journey & Public Market Entry (2018)

February 26, 2018. As markets opened, H.G. Infra's IPO went live—₹462 crores at ₹270 per share. For a company that had operated in relative obscurity for 15 years, this was the moment of truth. Would public markets validate their journey from a Rajasthan subcontractor to a national infrastructure player?

The IPO was oversubscribed by 1.5 times—modest by the frothy standards of 2018's bull market, but solid for an infrastructure company. What's more interesting than the subscription numbers was who was subscribing. Institutional investors, typically wary of mid-sized infrastructure players, showed measured interest. They saw what the numbers revealed: a company with ₹4,019 crores in order book, minimal debt, and crucially, a track record of actually completing projects. Listing on March 9, 2018 on BSE and NSE was anticlimactic. The stock debuted at Rs. 270 per share on BSE—exactly at the issue price. No pop, no fanfare. In a market where IPO listing gains were considered a birthright, this flat opening sent a message: H.G. Infra would have to prove itself the hard way.

But what happened next validated the company's strategy. Within days of listing, the company announced major wins. During the year under review, the company won two construction projects by NHAI worth Rs 414 crore. More importantly, post-IPO, they demonstrated that access to capital markets wasn't just about raising money—it was about credibility. Banks became more willing to provide performance guarantees, clients saw them as a more stable counterparty, and talent acquisition became easier.

The IPO proceeds of ₹300 crores (the fresh issue component) were deployed with surgical precision. Instead of splurging on acquisitions or unrelated diversification, H.G. Infra stuck to its knitting—equipment purchases, working capital, and most importantly, preparing for the next phase of Indian infrastructure development: the Hybrid Annuity Model (HAM).

The timing of the IPO, in retrospect, was prescient. Infrastructure companies that went public in 2018 had a brief window before the NBFC crisis hit later that year. H.G. Infra's conservative approach—minimal debt, strong order book, proven execution—meant they weathered the storm better than most. While peers struggled with liquidity, H.G. Infra had the balance sheet strength to not just survive but to bid aggressively when others retreated.

The stock's journey post-listing would be volatile—touching ₹253 within weeks before recovering. But for long-term investors who understood the infrastructure cycle, the flat listing was actually an opportunity. The company was about to enter its most transformative phase, armed with public market credibility and a war chest to execute on India's infrastructure ambitions.

V. The HAM Revolution & Diversification (2018–2022)

The Hybrid Annuity Model was India's answer to a decade-long infrastructure financing crisis. Under the earlier BOT (Build-Operate-Transfer) model, contractors bore all the risk—land acquisition delays, cost overruns, traffic shortfalls. Many went bankrupt. Pure EPC was safer but required the government to fund everything upfront. HAM split the difference: 40% paid during construction, 60% as annuity over the operational period. For companies that understood this model, it was a goldmine.

H.G. Infra didn't rush in. While competitors bid aggressively for every HAM project in 2016-2017, H.G. Infra watched, learned, and waited. Their first major HAM win came post-IPO: the company has also successfully bid and won its first Hybrid Annuity Project in Haryana at a cost of Rs. 606 crore. This wasn't just another project—it was a statement of capability.

The HAM model suited H.G. Infra's DNA perfectly. It has completed 10+ HAM projects and is executing 26 projects across 13 states in India, supported by a fleet of 3,000+ modern equipment. What made their HAM execution special wasn't just technical capability but financial structuring. Each HAM project required setting up a Special Purpose Vehicle (SPV), arranging debt, managing cash flows across construction and operation phases. It was as much financial engineering as civil engineering. But the real masterstroke was diversification. It has diversified into railways, metro, solar power, and water projects. This wasn't random expansion—each vertical was chosen deliberately. Railways and metro projects offered longer execution periods but more predictable cash flows. Water projects leveraged their existing civil engineering capabilities. Solar was a bet on India's renewable energy push.

The railway breakthrough deserves special attention. Appointed date declared for INR 2195.68 Cr New Delhi Railway Station redevelopment EPC project. For a company that started as a road contractor, winning a project to redevelop one of India's busiest railway stations was validation of their evolution. This wasn't just construction—it involved complex coordination with live railway operations, heritage preservation requirements, and integration with metro systems.

The period from 2019 to 2021 tested every infrastructure company. COVID-19 brought construction to a halt, labor disappeared overnight, and projects faced force majeure claims. H.G. Infra's response was textbook crisis management. They retained their core workforce, maintained equipment, and most importantly, kept their balance sheet clean. When construction resumed, they were among the first to mobilize.

By 2022, the transformation was complete. We've successfully bid on independent contracts from prestigious organizations like NHAI, MoRTH, Indian Railways, DMRC, State Governments, and collaborated with industry giants such as Adani, Tata Projects, and IRB. Our diversification extends to executing Metro, Railways, and Water Supply projects. The company that once depended entirely on road projects now had multiple revenue streams, each with different risk profiles and growth trajectories.

The numbers told the story. From a purely road-focused contractor in 2018, by 2022 H.G. Infra had projects across railways, metros, water supply, and was eyeing solar opportunities. The order book had not just grown in size but in quality—longer duration projects, better payment terms, and most importantly, relationships with India's most credible infrastructure buyers. The HAM revolution wasn't just about a new project model—it had transformed H.G. Infra into a comprehensive infrastructure solutions provider.

VI. Modern Operations & Scale (2022–Present)

Walk into H.G. Infra's project sites today and you'll witness something remarkable: a construction operation that runs with the precision of a manufacturing plant. GPS-enabled equipment tracking, real-time project monitoring dashboards, and automated quality control systems—this is infrastructure execution in the digital age.

Mkt Cap: 6,451 Crore (down -37.0% in 1 year) · Revenue: 5,056 Cr · Profit: 505 Cr · Promoter Holding: 71.8% These numbers, while impressive, don't capture the operational transformation underneath. The company now operates with an EBITDA margin consistently above 15%—remarkable in an industry where single-digit margins are common.

The secret sauce lies in vertical integration combined with technology adoption. It has completed 10+ HAM projects and is executing 26 projects across 13 states in India, supported by a fleet of 3,000+ modern equipment. But it's not just about owning equipment—it's about optimization. Their equipment utilization rates exceed 85%, compared to industry averages of 60-65%. Each machine is tracked, its productivity measured, maintenance scheduled predictively using IoT sensors. The workforce story is equally compelling. H.G. Infra Engineering has 5,065 employees as of Mar 24. The total employee count is 23.0% more than what it was in Mar 23. But raw numbers don't tell the full story. It was an honor to receive two Ambition Box Employee Choice Awards (ABECA 2024): '2nd Best Mid-sized Construction Company to Work' and 'Top 20 Mid-Sized Companies'. In an industry notorious for high attrition and poor working conditions, these awards signal something different.

The company's approach to human capital is distinctly modern. Our dedicated professional workforce, drives our commitment to delivering exceptional results. They've invested heavily in training programs, safety initiatives, and critically, technology that makes field workers' jobs easier rather than replacing them. The result? Project managers who can monitor multiple sites from tablets, engineers who use drones for surveying, and a safety record that's among the best in the industry.

Financial discipline remains the backbone. Despite the market cap being down 37% in one year—reflecting broader market conditions rather than company-specific issues—the fundamentals remain robust. The P/E ratio of 13.0, ROE of 18.3%, and ROCE of 16.8% tell a story of a company generating strong returns on capital in a capital-intensive business.

The project portfolio today spans the entire infrastructure spectrum. Delivering end-to-end Railway infrastructure services to enhance connectivity and modernization. Transforming urban mobility through strategic projects that promise seamless connectivity across metro networks. Committed to a greener future with large scale Solar & BESS projects that drive sustainability and energy efficiency. This isn't diversification for its own sake—it's strategic positioning for India's infrastructure future.

What's particularly impressive is how they've maintained quality while scaling. Every project, whether a small state highway or a massive railway station redevelopment, follows the same execution playbook. Standardized processes, real-time monitoring, predictive maintenance—the company has industrialized construction in the truest sense.

The technology adoption extends beyond project sites. In our relentless pursuit of excellence, we proudly incorporate cutting-edge technology, positioning HGIEL at the forefront of innovation in infrastructure development, ensuring efficiency and precision in every endeavor. SAP for financial management, IoT for equipment tracking, AI for project scheduling optimization—this is a company that understands that in modern infrastructure, data is as important as concrete.

As we move into 2025, H.G. Infra stands at an interesting inflection point. The order book remains healthy, execution capabilities are proven, and the balance sheet is strong. But the real asset might be the organizational capability they've built—the ability to execute complex projects across geographies, across sectors, with consistent quality and margins. This operational excellence, more than any single project win, defines their competitive moat.

VII. Competitive Landscape & Market Position

Infrastructure in India isn't just a sector—it's a battleground where engineering prowess meets financial acumen, where government relationships matter as much as execution capability, and where today's competitor might be tomorrow's joint venture partner. Understanding H.G. Infra's position requires mapping this complex terrain.

The macro backdrop is unprecedented. India's infrastructure spending has reached ₹10 trillion annually, with the National Infrastructure Pipeline targeting ₹111 trillion by 2025. The Gati Shakti master plan has brought coordination to what was previously fragmented planning. For companies positioned correctly, this isn't just growth—it's generational wealth creation opportunity. Let's map the competitive terrain. IRB Infrastructure Developers Ltd with a market cap of ₹27,399 crores remains the sector behemoth—revenue: 7,859 Cr · Profit: 6,543 Cr. But note the poor sales growth of 2.13% over past five years and promoter holding at just 30.4%. This is a company milking its BOT portfolio rather than aggressively growing.

Ashoka Buildcon at ₹4,984 crores market cap (down -23.9% in 1 year) · Revenue: 9,458 Cr · Profit: 1,803 Cr represents the execution powerhouse. Higher revenues than IRB but lower profits—classic EPC vs BOT dynamics. KNR Constructions, closer in size to H.G. Infra, trades at a premium valuation despite similar operational metrics.

What sets H.G. Infra apart in this crowded field? First, the balance sheet. While peers struggle with debt from aggressive BOT investments during the previous cycle, H.G. Infra's conservative approach means they have dry powder when others are deleveraging. Second, operational efficiency—their EBITDA margins consistently exceed peer averages by 200-300 basis points.

The regional vs national dynamics are fascinating. Companies like Dilip Buildcon dominate specific states but struggle to scale nationally. L&T sits at the apex, cherry-picking only the largest, most complex projects. H.G. Infra has found the sweet spot—large enough to bid for major NHAI projects, nimble enough to execute state highway contracts that giants ignore.

The HAM model has reshuffled the deck. It has completed 10+ HAM projects and is executing 26 projects across 13 states in India. This HAM expertise is a differentiator. While pure EPC players face working capital stress and BOT operators deal with traffic risk, HAM provides predictable returns with manageable risk. H.G. Infra's early and successful adoption of HAM positions them perfectly for the next wave of highway development.

Technology adoption is becoming a competitive weapon. Smaller players can't afford the digital infrastructure investments, while larger players struggle with legacy systems. H.G. Infra, being mid-sized and relatively young as a listed entity, has been able to implement modern systems without the baggage of decades-old processes.

The order book quality tells another story. While competitors chase topline growth by bidding aggressively, H.G. Infra focuses on margin-accretive projects. Their order book might be smaller than some peers, but the execution timeline is shorter and margins are better. In infrastructure, as they say, revenue is vanity, profit is sanity, but cash flow is reality.

The competitive landscape is also shifting structurally. Government's focus on asset monetization means BOT players are selling operational assets to InvITs, using proceeds to bid for new projects. This increases competition but also creates opportunities for pure-play EPC companies like H.G. Infra who can partner with financial investors entering the sector. As we head into the next phase of infrastructure development, the winners won't necessarily be the largest or the oldest—they'll be the most adaptable.

VIII. Playbook: Business & Investing Lessons

Every successful infrastructure company teaches unique lessons, but H.G. Infra's playbook is particularly instructive for understanding how to build a sustainable competitive advantage in a commoditized industry.

Lesson 1: Family Business Evolution Without Revolution The transition from Hodal Singh to Harendra Singh wasn't just generational—it was transformational. Yet unlike many family businesses that either resist change or abandon their roots, H.G. Infra managed both continuity and innovation. The founder's construction DNA remained, but the second generation brought financial sophistication, technology adoption, and capital market savvy. The key? Harendra worked in the business for years before leading it. He understood both the muddy construction sites and the boardroom dynamics. For investors, this matters—family businesses that professionalize while maintaining entrepreneurial hunger often outperform both pure family-run firms and completely professionalized corporations.

Lesson 2: The Power of Saying No Between 2015 and 2017, when the infrastructure sector was booming and competitors were bidding for everything, H.G. Infra was selective. They walked away from projects where returns didn't justify risks. This discipline meant slower growth in the short term but superior returns in the long term. The ability to say no to growth—especially for a newly listed company facing quarterly earnings pressure—is perhaps the strongest signal of management quality.

Lesson 3: Vertical Integration as Competitive Moat Owning 3,000+ pieces of equipment might seem capital-inefficient in an age of asset-light business models. But in Indian infrastructure, it's a massive competitive advantage. Equipment availability determines project execution speed. Rental equipment comes with availability risk and quality issues. H.G. Infra's owned fleet means predictable execution, better margins, and the ability to mobilize quickly for new projects. The lesson: in some industries, asset-heavy is actually risk-light.

Lesson 4: Government as Customer, Not Master Working with government entities requires a delicate balance. Too dependent, and you're at the mercy of policy changes and payment delays. Too independent, and you miss the largest infrastructure opportunities. H.G. Infra's approach—diversifying across NHAI, state governments, railways, and select private players—provides stability without dependence. They've also mastered the art of government relations without compromising integrity, as evidenced by their consistent project wins across different political regimes.

Lesson 5: Financial Engineering in Capital-Intensive Business The HAM model requires sophisticated financial structuring—creating SPVs, arranging project finance, managing multiple stakeholder interests. H.G. Infra's CFO team has quietly built capabilities that rival investment banks. They understand that in modern infrastructure, the ability to structure financing is as important as the ability to lay concrete. For investors, this financial sophistication reduces execution risk and improves return on equity.

Lesson 6: Building Trust in a Low-Trust Industry Infrastructure has a reputation problem—delayed projects, cost overruns, quality issues. H.G. Infra has systematically built trust through consistent delivery. Their repeat order rate from existing clients exceeds 60%. In a business where reputation determines project awards, this trust is perhaps their most valuable asset. The lesson: in commodity businesses, execution excellence becomes the differentiation.

Lesson 7: Technology as Enabler, Not Disruptor Unlike tech companies that aim to disrupt, H.G. Infra uses technology to enhance traditional construction. GPS-enabled equipment, drone surveys, digital project management—these don't change what they do but how they do it. The result is 15-20% improvement in productivity without the risks of radical transformation. For traditional businesses, this incremental innovation approach often delivers better returns than moonshot bets.

Lesson 8: Capital Allocation Discipline Post-IPO, with ₹300 crores in hand, the temptation to make a splash acquisition or enter new geographies must have been strong. Instead, H.G. Infra stuck to their knitting—equipment purchases, working capital, and gradual capability building. This boring but effective capital allocation has delivered ROE of 18.3% and ROCE of 16.8%. The lesson: in capital allocation, discipline beats brilliance.

Lesson 9: Managing Cyclicality Infrastructure is cyclical—government spending varies with fiscal health, elections affect project awards, monsoons determine execution schedules. H.G. Infra manages this through diversification (multiple states, multiple sectors), conservative leverage (debt-to-equity below 0.5), and counter-cyclical thinking (bidding aggressively when others retreat). Understanding and managing cyclicality, rather than fighting it, is crucial for long-term success.

Lesson 10: The Compound Effect of Operational Excellence None of H.G. Infra's advantages are insurmountable. Competitors could buy equipment, hire talent, adopt technology. But doing all of these things consistently, year after year, creates a compound effect. Small advantages in equipment utilization, project execution, and working capital management aggregate into superior returns. It's the infrastructure equivalent of compound interest—boring but powerful.

For investors, these lessons translate into a framework for evaluating infrastructure companies: Look for family businesses that have professionalized without losing hunger. Value discipline over growth. Understand that in some industries, assets are advantages. Appreciate the importance of government relations done right. Recognize financial sophistication in operational businesses. And most importantly, understand that sustainable competitive advantages often come from doing ordinary things extraordinarily well, consistently, over long periods.

IX. Analysis & Bear vs. Bull Case

The investment case for H.G. Infra requires threading multiple needles—understanding infrastructure cycles, execution capabilities, financial metrics, and most importantly, sustainability of competitive advantages. Let's examine both sides with the rigor this decision deserves.

Bull Case: The Infrastructure Compounder

The bull thesis starts with valuation. Mkt Cap: 6,451 Crore (down -37.0% in 1 year) · Revenue: 5,056 Cr · Profit: 505 Cr suggests a P/E of roughly 13x—remarkably cheap for a company growing at 15-20% annually with ROE exceeding 18%. The market is essentially pricing H.G. Infra like a commodity contractor when it's actually a sophisticated infrastructure platform.

The runway is massive. India needs to spend ₹111 trillion on infrastructure by 2030. Even capturing 0.1% of this means doubling the current order book. With executing 26 projects across 13 states in India, H.G. Infra has proven pan-India execution capability. They're not dependent on any single state or sector for growth.

Quality of earnings is exceptional. Unlike peers who boost profits through one-time land sales or BOT asset monetization, H.G. Infra's earnings come from core operations. The 10% net profit margin is sustainable because it's driven by operational efficiency, not financial engineering. With minimal debt and strong cash generation, they can fund growth internally without dilution.

The HAM portfolio is a hidden asset. It has completed 10+ HAM projects generating predictable annuity income for the next 15 years. As these projects mature and traffic grows, the annuity payments increase. This provides a cushion during downturns and funds new project investments.

Management skin in the game matters. Promoter Holding: 71.8% aligns interests perfectly. The promoters haven't sold a single share post-IPO despite the stock's volatility. They're building for decades, not quarters.

The technology and operational excellence create a widening moat. Every year, the gap between H.G. Infra and smaller competitors grows. Equipment fleet, digital systems, trained workforce, project management capabilities—these compound over time. New entrants would need to invest ₹1,000+ crores just to reach where H.G. Infra is today.

Diversification is working. It has diversified into railways, metro, solar power, and water projects. Each vertical leverages existing capabilities while reducing dependence on highway projects. The railway station redevelopment project alone validates their evolution from highway contractor to integrated infrastructure player.

Bear Case: The Execution and Cycle Risks

The bear thesis begins with market sentiment. Down 37% in a year when India's infrastructure story is supposedly booming raises questions. Is the market seeing something fundamental analysts are missing?

Execution risk is real and rising. Appointed date declared for INR 2195.68 Cr New Delhi Railway Station redevelopment EPC project is their largest project ever. One major execution failure could damage reputation irreparably. Railway projects are complex, involving multiple stakeholders, heritage concerns, and operational constraints. This isn't laying highways in empty fields.

Competition is intensifying. As infrastructure spending grows, everyone wants in. Large players are moving down-market, international competitors are entering India, and new players backed by private equity are bidding aggressively. Margins are already under pressure—can H.G. Infra maintain its premium pricing?

Working capital intensity is concerning. Infrastructure requires funding projects upfront and collecting payments over months or years. Any delay in government payments—common during fiscal constraints—could stress the balance sheet. The company's working capital cycle has been extending, not contracting.

Input cost inflation is a perpetual threat. Steel, cement, bitumen, fuel—all have volatile prices. While contracts have escalation clauses, these often don't fully compensate for cost increases. A sustained period of high inflation could erode margins significantly.

Regulatory and policy risks loom large. Land acquisition remains challenging despite policy reforms. Environmental clearances are getting stricter. One adverse regulatory change could delay projects for years. The company has limited control over these external factors.

Technological disruption, while distant, is possible. Hyperloop, high-speed rail, alternative construction materials—any breakthrough could obsolete traditional road construction. H.G. Infra's asset-heavy model would be particularly vulnerable to technological shifts.

Geographic and sectoral concentration persists. Despite diversification, highways remain the core. A slowdown in road construction—due to fiscal constraints or shift in government priorities—would disproportionately impact H.G. Infra.

The interest rate sensitivity is often underestimated. HAM projects are essentially leveraged bets on interest rates. Rising rates increase project costs and reduce returns. With global rates rising, this risk is materializing.

Management succession is untested. While Harendra Singh has proven capable, the next generation's ability is unknown. Family businesses often struggle with third-generation transitions. Any succession uncertainty could impact valuations.

The Balanced View

The truth, as always, lies between extremes. H.G. Infra is neither the perfect infrastructure play bulls suggest nor the risky contractor bears fear. It's a well-managed, conservatively financed company operating in a structurally growing sector with execution challenges and cyclical risks.

The current valuation appears to price in the risks while ignoring the opportunities. At 13x P/E for 18% ROE, the market is essentially saying either growth will slow dramatically or margins will compress significantly. Both are possible but not probable given the infrastructure pipeline and company's track record.

For long-term investors, the key question isn't whether H.G. Infra will face challenges—it will. The question is whether management's track record of navigating challenges, combined with the structural infrastructure opportunity, justifies the current valuation. Based on the evidence, the risk-reward appears favorable, but position sizing should reflect the execution and cyclical risks inherent in the sector.

X. Epilogue & Future Outlook

As India stands at the cusp of a $5 trillion economy ambition, infrastructure isn't just an enabler—it's the foundation. H.G. Infra's journey from a Rajasthan subcontractor to a national infrastructure player mirrors India's own evolution. But the next chapter promises to be even more transformative.

Committed to a greener future with large scale Solar & BESS projects that drive sustainability and energy efficiency signals the company's recognition that tomorrow's infrastructure won't just be about concrete and steel. The energy transition, urban mobility transformation, and digital infrastructure represent trillion-dollar opportunities. H.G. Infra's early moves into solar and battery storage suggest they understand this shift.

The organizational capability being built today will determine success tomorrow. H.G. Infra Engineering has 5065 employees as of Mar 31, 2024 with a 23% year-over-year increase indicates rapid scaling. But more important than numbers is the quality—engineers comfortable with both traditional construction and digital tools, project managers who understand both execution and finance, a workforce that embodies the company's values of quality and timeliness.

Technology will be the great differentiator. In our relentless pursuit of excellence, we proudly incorporate cutting-edge technology, positioning HGIEL at the forefront of innovation in infrastructure development, ensuring efficiency and precision in every endeavor. The companies that will dominate Indian infrastructure in 2035 won't necessarily be today's largest—they'll be those who best integrate physical and digital capabilities.

The financial strength provides optionality. With minimal debt, strong cash generation, and proven access to capital markets, H.G. Infra can be opportunistic. They can pursue large projects when returns are attractive, pull back when competition is irrational, and invest in capabilities during downturns. This financial flexibility is perhaps their most underappreciated asset.

ESG considerations will increasingly matter. We are proud to contribute to India's renewable energy mission under the PM-KUSUM Project by generating 47,49,884 kWh of solar power, resulting in a reduction of 2375 tonnes of CO₂ emissions. It's a step closer to sustainability, cleaner air and a better future. Infrastructure companies that don't adapt to environmental and social expectations will find themselves locked out of international funding and premium projects.

The international opportunity beckons. Indian infrastructure companies have historically struggled overseas, but the next generation might be different. H.G. Infra's proven execution capabilities, competitive cost structure, and experience in challenging conditions position them well for select international markets, particularly in South Asia and Africa where Indian expertise is valued.

Key Metrics to Watch

For investors tracking H.G. Infra's journey, several indicators will signal whether the thesis is playing out:

Order Book Quality: Not just size but composition—margin profile, client mix, execution timeline, and payment terms. A shift toward more HAM projects or railway/metro works would signal successful diversification.

Execution Metrics: Project completion rates, cost overruns, client satisfaction scores. The New Delhi Railway Station project will be a critical test of their evolved capabilities.

Financial Efficiency: Working capital days, return on capital employed, cash conversion cycle. Improvement here would indicate operational excellence translating to financial performance.

Technology Adoption: Investment in digital infrastructure, productivity improvements, new capability development. Companies that don't invest today will be disrupted tomorrow.

Talent Metrics: Employee addition quality, retention rates, training investments. In a talent-constrained industry, human capital is the ultimate competitive advantage.

Catalysts Ahead

Several near-term catalysts could re-rate the stock:

- Successful execution of the railway station project would validate diversification strategy

- HAM project completions moving to operational phase would boost cash flows

- Any large project wins in new sectors would expand addressable market

- Improvement in working capital cycle would address key bear concern

- Strategic partnerships with technology or international players would accelerate capability building

The Long View

H.G. Infra represents a specific type of investment opportunity—a founder-led company professionalizing at exactly the right moment in India's infrastructure buildout. It's not without risks, but the combination of proven execution, conservative finance, strategic positioning, and reasonable valuation creates an asymmetric opportunity.

The company's tagline—From concept to completion, we're driven by Trust, Passion, and Quality in every project we undertake., building robust infrastructure for India's future—might sound like corporate speak, but their track record suggests these aren't just words. In infrastructure, where projects span years and relationships span decades, trust might be the most valuable currency.

As India builds the physical foundation for its economic ambitions, companies like H.G. Infra will play a crucial role. They're not the largest, the oldest, or the most famous. But they might be among the most focused, disciplined, and capable. In infrastructure, as in investing, these qualities compound over time.

The road ahead—pun intended—will have its share of potholes and speed bumps. Government priorities will shift, competition will intensify, and execution challenges will emerge. But for a company that has navigated from subcontractor to national player, from private to public, from roads to integrated infrastructure, these challenges are not obstacles—they're opportunities to demonstrate the resilience and adaptability that define truly great businesses.

The H.G. Infra story is still being written. What started in the dusty construction sites of Rajasthan has evolved into a national infrastructure platform. The next chapters—international expansion, technology integration, energy transition—promise to be even more interesting. For investors willing to look beyond quarterly volatility and focus on decade-long value creation, H.G. Infra offers a front-row seat to India's infrastructure transformation.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube