Howmet Aerospace: From Dental Castings to Aerospace Dominance

I. Introduction & Episode Roadmap

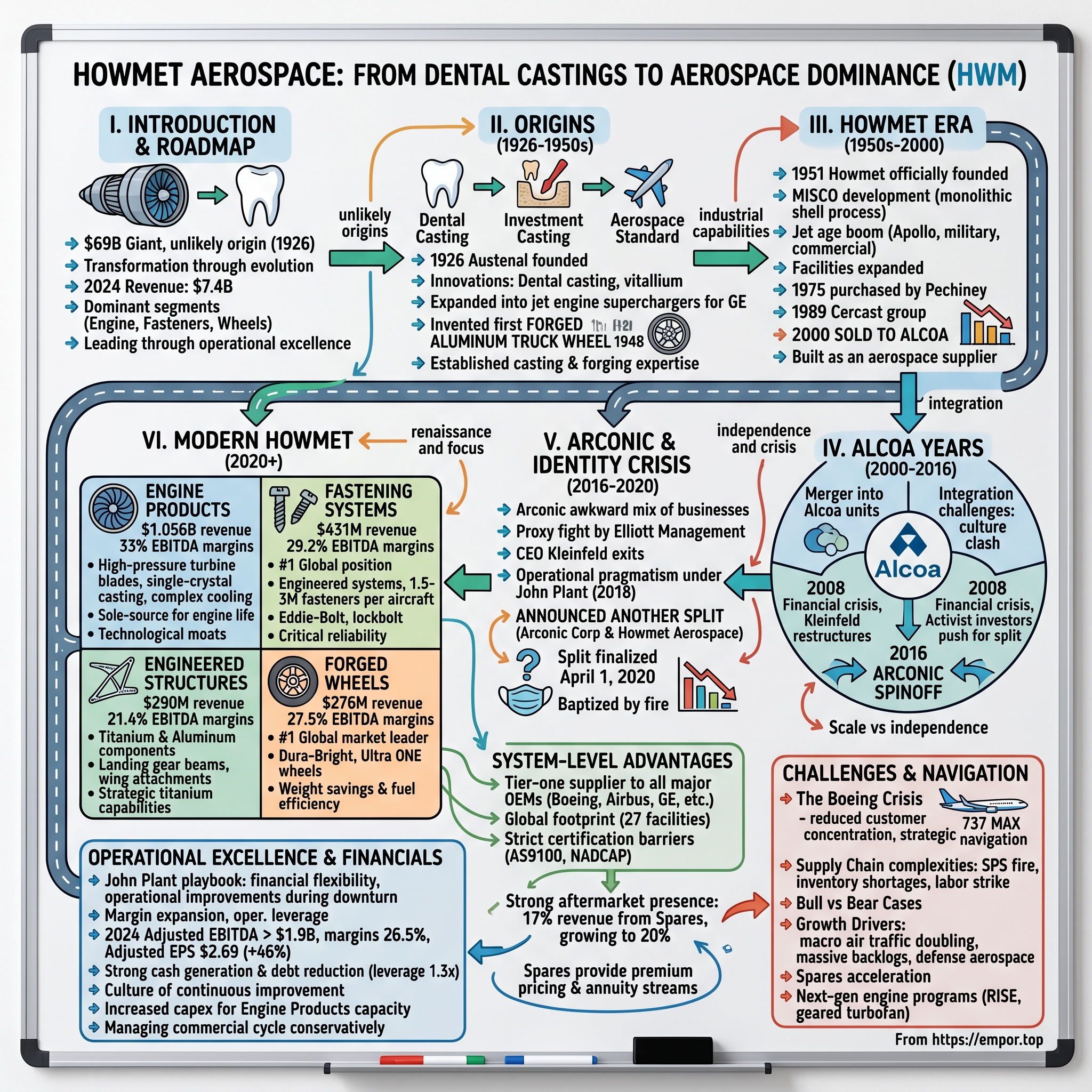

Picture this: a $69 billion aerospace giant whose components are inside virtually every commercial jet engine flying today, whose fasteners hold together the world's most advanced aircraft, and whose forged wheels support millions of miles of highway transportation. Now imagine that this industrial powerhouse traces its origins not to an aircraft hangar or defense contractor, but to a dental laboratory in 1926. This is the unlikely story of Howmet Aerospace.

The company's roots go back to 1926, when Austenal, a company that manufactured materials for dental appliances, was founded. What began as an innovation in dental casting technology would evolve through nearly a century of transformation, acquisition, and reinvention to become one of the most critical suppliers in modern aerospace.

Today, Howmet Aerospace stands as a testament to industrial evolution done right. Revenue for the full year of 2024 was approximately $7.4 billion, up 12 percent from 2023, with the company commanding leading positions across four distinct business segments. The Engine Products division, its crown jewel, generates over $1 billion annually with industry-leading 33% EBITDA margins. The company holds the number one global position in aerospace fastening systems, while also maintaining leadership in forged aluminum wheels—a market it literally created.

But this isn't just a story about industrial might. It's about timing, transformation, and the power of operational excellence. It's about how a company navigated from dental appliances to aircraft superchargers during the Great Depression, survived multiple ownership changes, emerged from the shadow of aluminum giant Alcoa, and ultimately positioned itself at the center of the aerospace super-cycle we're witnessing today.

The narrative arc we'll explore spans four major eras: the unlikely origins in dental casting that provided the technological foundation; the Howmet years where aerospace capabilities were built brick by brick; the Alcoa integration that provided scale but ultimately constrained potential; and finally, the modern renaissance under John Plant's leadership that has unlocked extraordinary value through focus and operational discipline.

We'll examine how seemingly unrelated innovations—like precision dental castings—can become the foundation for mission-critical aerospace components. We'll dissect the economics of aerospace suppliers, where 90% learning curves and decades-long customer relationships create nearly impenetrable moats. And we'll analyze how the current aerospace recovery, combined with structural shifts in the spares market, positions Howmet for potentially its greatest chapter yet.

II. Origins: The Unlikely Beginning (1926–1950s)

The year was 1926. Charles Lindbergh was still a year away from his transatlantic flight. Commercial aviation existed only in the dreams of visionaries. In this pre-jet age world, two men named Reiner Erdle and Charles Prange were focused on an entirely different challenge: improving the quality of dental appliances through better casting techniques.

Their founders worked to improve investment chrome base castings using two separate investments: The first coating, named "protective coat", gives a smooth finish. This might seem like mundane dental technology, but it represented a breakthrough in precision casting that would have implications far beyond dentistry. This technology replaced gold alloy with vitallium and was popular during the Great Depression.

The timing was fortuitous. As the Great Depression gripped America, Austenal's cost-effective casting solutions found eager customers among dentists whose patients could no longer afford gold dental work. But the real transformation came from an unexpected source: General Electric.

During the 1930s, Austenal expanded into aircraft engine superchargers with superior castings when General Electric asked for help. Think about the audacity of this moment—a dental appliance company being asked to solve aerospace engineering challenges. GE's engineers had recognized something that would define Howmet's trajectory for the next century: the precision required for dental castings translated directly to the exacting standards needed for aircraft components.

The technical leap from teeth to turbines wasn't as far-fetched as it might seem. Both required the ability to cast complex shapes with extreme precision, minimal porosity, and consistent material properties. The investment casting process Austenal had perfected for dental applications—creating a ceramic mold around a wax pattern, then melting out the wax and pouring in molten metal—was exactly what the nascent aerospace industry needed for components that traditional forging or machining couldn't produce economically.

But the company's most audacious move came in 1948, in the aftermath of World War II. As America's highways began their great expansion and the trucking industry started its rise, Austenal made a bet that would create an entirely new market. The company invented the first forged aluminum truck wheel in 1948—and by doing so, created an entire industry.

Consider the context: steel wheels had been the standard since the invention of the automobile. They were heavy, prone to rust, and required constant maintenance. Austenal's engineers saw aluminum—lightweight, corrosion-resistant, but notoriously difficult to forge into load-bearing structures—as the solution. Alcoa had been the industry leader since inventing the forged aluminum wheel in 1948 using an alloy it had developed for the aerospace industry.

The innovation wasn't just about material substitution. It required developing entirely new forging techniques, creating alloys that could withstand millions of miles of highway punishment, and convincing a skeptical trucking industry that these lightweight wheels could be trusted with precious cargo. The weight savings were compelling—switching from steel to aluminum wheels could save over 1,400 pounds on a typical truck, translating directly to increased payload capacity and fuel efficiency.

This period established three critical capabilities that would define Howmet's future: precision casting expertise inherited from dental applications, the ability to serve the demanding aerospace market, and the innovative spirit to create entirely new product categories. By 1950, what had started as a dental appliance company had planted seeds in aerospace and transportation that would grow into billion-dollar businesses.

The transformation from dental castings to aerospace components might seem like an historical curiosity, but it established a pattern that would repeat throughout Howmet's history: taking specialized manufacturing expertise and applying it to progressively more demanding, higher-value applications. This DNA of continuous technological advancement, combined with the willingness to make bold bets on new markets, would carry forward through every subsequent era of the company's evolution.

III. The Howmet Era: Building an Industrial Powerhouse (1950s–2000)

The year 1951 marked a critical inflection point. The Korean War had begun, the jet age was dawning with the first commercial jet flights just years away, and American manufacturing was entering its golden age. It was in this environment that Howmet Corporation was officially founded, no longer as a subsidiary operation but as a focused casting company with aerospace ambitions.

The timing couldn't have been better. The transition from propeller-driven aircraft to jets created unprecedented demand for components that could withstand extreme temperatures and stresses. Traditional manufacturing methods simply couldn't produce the complex cooling channels needed in turbine blades or the precise tolerances required for jet engine components. Howmet's investment casting expertise, refined through decades of dental and early aerospace work, positioned it perfectly for this revolution.

The real breakthrough came in 1952 with the MISCO development. Howe acquired Michigan Steel Casting Co. (MISCO), which provided the monolithic shell process. This process uses a ceramic shell with thin, strong walls to increase control of the solidification process and produce a sounder casting. This wasn't just an incremental improvement—it was a fundamental leap in casting technology that would become the backbone of modern aerospace manufacturing.

The monolithic shell process solved a problem that had plagued investment casting since its inception: how to create molds strong enough to contain molten superalloys yet thin enough to allow precise control of cooling rates. By using multiple layers of ceramic slurry and stucco, MISCO's process created shells that were both stronger and more dimensionally stable than anything previously available. This meant Howmet could now cast turbine blades with internal cooling passages so complex they looked more like circulatory systems than metal parts.

In 1958, Howe Sound Company, a metals and mining business, acquired Austenal. This acquisition brought critical capital and resources just as the aerospace industry was about to explode. The Boeing 707 entered service in 1958, ushering in the jet age for commercial aviation. Every one of these new jets needed hundreds of precision-cast components, from turbine blades to structural fittings.

Howe became Howmet in 1965, marking a transition from a mining company to a manufacturer of precision metal products. The name change was more than cosmetic—it signaled a fundamental strategic shift. The company was no longer a mining concern with a manufacturing subsidiary; it was now a technology-driven manufacturer serving the most demanding customers in the world.

The 1960s and early 1970s saw Howmet riding the aerospace boom. The Apollo program, the Vietnam War's military aircraft demand, and the continued growth of commercial aviation drove unprecedented growth. The company expanded its facilities across the United States, each one specialized for specific types of components or alloys. A plant in Michigan might focus on large structural castings, while a facility in Connecticut specialized in single-crystal turbine blades—a technology so advanced that each blade was essentially one continuous metal crystal, eliminating grain boundaries that could become failure points under stress.

Then came a pivotal moment in 1975. Howmet, in turn, was purchased in 1975 by Pechiney, a multinational aluminum company. For the French industrial giant Pechiney, Howmet represented a downstream integration opportunity—a way to add value to their aluminum production through advanced manufacturing. For Howmet, it meant access to global markets, advanced metallurgy research, and the deep pockets needed to invest in next-generation technologies.

Under Pechiney's ownership, Howmet underwent its most significant technological transformation yet. In 1989, Pechiney purchased the Cercast group of companies, bringing Howmet into the aluminum casting industry. This wasn't just about adding capacity—Cercast brought proprietary directional solidification technology that allowed for even more precise control of grain structure in cast components.

The 1990s brought new challenges and opportunities. The end of the Cold War initially dampened defense spending, but the commercial aerospace market was entering an unprecedented boom. Airlines were retiring older, less efficient aircraft and replacing them with new models from Boeing and Airbus. Each new aircraft generation required more sophisticated components—turbine blades that could run hotter, structural parts that were lighter yet stronger, and fastening systems that could handle greater stresses.

In 1995, Pechiney sold Howmet to a joint venture between Thiokol and The Carlyle Group. By late 1997, the ownership structure of Howmet had become Thiokol, with 62% ownership, Carlyle 23%, and the public 15%. In 1998, Thiokol changed its name to Cordant Technologies Inc.; by February 1999, Cordant owned 84.7% of Howmet.

This period of financial engineering might seem like a distraction, but it actually catalyzed important operational improvements. The Carlyle Group, with its operational expertise and portfolio company best practices, helped modernize Howmet's manufacturing processes. Lean manufacturing principles were introduced, statistical process control became standard, and investments in automation began to pay dividends in both quality and cost.

By the late 1990s, Howmet had evolved from a simple casting company into a sophisticated aerospace supplier with capabilities spanning the entire value chain. The company could take raw materials and transform them into finished components ready for installation in jet engines or aircraft structures. It had developed proprietary alloys, patented manufacturing processes, and relationships with every major aerospace OEM.

The culmination of this era came in 2000 with a decision that would define the next two decades: In 2000, Cordant sold its stake in Howmet to Alcoa, which placed Howmet into its Alcoa Industrial Components unit. For Howmet, joining Alcoa meant becoming part of one of the world's largest aluminum companies, with resources and reach that dwarfed anything in its previous history. But it also meant losing its independence and becoming one division among many in a massive conglomerate.

The Howmet era had transformed a dental casting company into a world-class aerospace supplier. The company had survived multiple ownership changes, adapted to shifting market demands, and continuously pushed the boundaries of materials science and manufacturing technology. But as it entered the Alcoa fold, the question became: could this culture of innovation and technical excellence survive within a massive corporate structure focused primarily on commodity aluminum production?

IV. The Alcoa Years: Integration & Transformation (2000–2016)

The morning of Howmet's integration into Alcoa in 2000 must have felt like entering a different universe. Alcoa was a $23 billion behemoth, one of the 30 companies in the Dow Jones Industrial Average, with operations spanning from bauxite mines in Australia to aluminum smelters in Iceland. Howmet, with its specialized aerospace focus, was now a small fish in an enormous aluminum ocean.

Initially, the acquisition seemed to make strategic sense. Alcoa CEO Alain Belda was pushing to move the company downstream, away from the commodity aluminum business's brutal cyclicality toward higher-margin, value-added products. Howmet was the crown jewel of this strategy—a business that took Alcoa's aluminum and transformed it into components selling for hundreds of times the value of the raw metal.

In 2004, Howmet was part of a merger that created Alcoa Investment Casting and Forged Products unit. This reorganization brought together various acquired aerospace businesses under one umbrella, creating synergies in procurement, technology sharing, and customer relationships. The combined entity could now offer aerospace customers a one-stop shop for everything from raw forgings to finished assemblies.

But integration wasn't without its challenges. Howmet's entrepreneurial, technology-driven culture clashed with Alcoa's more bureaucratic, commodity-focused mindset. Where Howmet engineers were accustomed to making quick decisions to solve customer problems, they now faced layers of corporate approval. Where the company had once invested aggressively in new technologies, capital allocation now competed with aluminum smelter upgrades and other corporate priorities.

In 2007, Howmet was renamed Alcoa Howmet as a newly formed Alcoa Power and Propulsion unit division. This represented another reorganization, another attempt to find the right structure to maximize value. But these constant reshufflings took their toll, creating uncertainty among employees and customers about the company's direction and commitment.

Despite these organizational challenges, the business continued to grow, driven by powerful secular trends in aerospace. The period from 2000 to 2008 saw unprecedented growth in air travel, particularly in emerging markets. Boeing and Airbus were locked in a fierce competition, driving innovation and production volumes to new heights. Every new aircraft needed Howmet's components, from the fasteners holding the fuselage together to the turbine blades at the heart of the engines.

The 2008 financial crisis brought this growth to a screeching halt. Airlines canceled or deferred aircraft orders, aerospace OEMs cut production rates, and Howmet faced its most severe downturn since the post-9/11 aviation crisis. But this crisis also catalyzed important changes. Klaus Kleinfeld, who became Alcoa's CEO in 2008, recognized that the company's diverse portfolio was becoming a liability rather than an asset.

Kleinfeld was a different breed of CEO—a German-born former Siemens executive who brought a European sensibility to American industrial management. He immediately set about restructuring Alcoa, closing high-cost smelters, divesting non-core assets, and investing in the downstream businesses like Howmet that offered better growth and margins. Under his leadership, Alcoa began to transform from an aluminum company that happened to make aerospace parts into an industrial company with significant aerospace exposure.

The recovery from 2010 to 2015 was remarkable. As airlines returned to profitability and began refreshing their fleets, demand for Howmet's products soared. The company invested heavily in new technologies, including additive manufacturing capabilities that could produce components impossible to make with traditional casting. It expanded its footprint in emerging markets, opening facilities in China and Eastern Europe to serve growing aerospace markets.

But by 2015, it was becoming clear that Alcoa's structure was holding back both its upstream and downstream businesses. The commodity aluminum business needed different strategies, different capital allocation priorities, and different investor bases than the engineered products businesses. Activist investors began circling, arguing that the company would be worth more split apart than together.

The Alcoa years had brought Howmet scale, resources, and global reach. The company had weathered the financial crisis, invested in new technologies, and built relationships with every major aerospace customer globally. The firm operates 27 facilities in the United States, Canada, Mexico, France, the United Kingdom, China, Brazil, Hungary and Japan. But it had also suffered from being part of a conglomerate with competing priorities, inconsistent strategies, and a stock price that reflected the worst of both commodity and specialty businesses.

As 2016 dawned, the pressure for change became irresistible. What happened next would be one of the most complex corporate separations in American industrial history, setting the stage for Howmet's emergence as an independent aerospace champion.

V. Arconic Spinoff & Identity Crisis (2016–2020)

The announcement came on November 1, 2016, ending months of speculation and years of activist pressure. Alcoa Inc. spun off its bauxite, alumina, and aluminum operations to a new company called Alcoa Corp. Alcoa Inc. was renamed Arconic Inc., and retained the operations in aluminum rolling, aluminum plate, precision castings, and aerospace and industrial fasteners. After decades as part of the aluminum giant, Howmet was finally free—or so it seemed.

But freedom came with its own complications. The new Arconic wasn't quite the focused aerospace play investors had hoped for. It was an awkward amalgamation of businesses—some focused on aerospace, others on automotive, building and construction, and industrial markets. The company had inherited $2.9 billion in debt from the separation and faced the challenge of creating a new identity while managing disparate operations.

Klaus Kleinfeld, who had orchestrated the split, stayed on as Arconic's CEO with a vision of creating a "precision engineering company." His pitch to investors was compelling: take advantage of megatrends like the aerospace super-cycle, automotive lightweighting, and urbanization. Arconic would be the picks-and-shovels play on all of these themes, providing the advanced materials and components that made modern transportation and construction possible.

But Elliott Management, the feared activist hedge fund led by Paul Singer, saw things differently. On January 31, 2017, barely three months after the separation, Elliott launched a blistering proxy fight. Elliott Management's push to replace Arconic's leadership was based on "unfair" evidence that paints the newly created company as worse than it is, Chairman and CEO Klaus Kleinfeld told CNBC. In November, Alcoa Inc. split into two companies, Arconic, a metal parts maker for airplanes and cars, and Alcoa Corp., which retained its slower-growing aluminum refining business.

Elliott's critique was devastating. They argued that Kleinfeld had botched the separation, leaving Arconic with an unwieldy portfolio, excessive costs, and a muddled strategy. They pointed to missed earnings targets, poor execution, and a stock price that had dramatically underperformed peers. The company should consider replacing Kleinfeld with Larry Lawson, former CEO of Spirit AeroSystems Holdings Inc., whom Elliott has hired as a consultant.

What followed was one of the most bizarre episodes in corporate governance history. As the proxy fight intensified, Kleinfeld made a fatal error. The CEO exited the aluminum-parts maker after the board said he showed "poor judgment" in sending a letter to Elliott amid a proxy fight. The letter, which mentioned Singer's family trip to Germany and included a soccer ball as a "souvenir," was interpreted by Elliott as a veiled threat.

Arconic on Monday cited this letter as the reason for Kleinfeld stepping down from its board. The board, which had initially supported Kleinfeld, concluded he had crossed a line. On April 17, 2017, Kleinfeld resigned, bringing an abrupt end to his tenure and leaving Arconic rudderless at a critical moment.

David Hess, a board member and former operations executive, stepped in as interim CEO. The next eighteen months were a period of soul-searching and strategic review. Should Arconic double down on aerospace? Divest the building and construction business? Pursue acquisitions to build scale? The lack of clear direction frustrated investors and employees alike.

In October 2018, the board made a decisive choice, appointing John Plant as CEO. Plant was an inspired selection—a veteran automotive executive who had led TRW Automotive before its sale to ZF Friedrichshafen for $13.5 billion. Mr. Plant is the former Chairman of the Board, president and Chief Executive Officer of TRW Automotive, which was acquired by ZF Friedrichshafen AG in May 2015. Under his leadership, TRW employed more than 65,000 people in approximately 190 major facilities around the world and was ranked among the top 10 automotive suppliers globally.

Plant brought a different philosophy to Arconic. Where Kleinfeld had been a visionary strategist, Plant was an operational pragmatist. He immediately set about simplifying the business, improving execution, and most importantly, preparing for another separation. On February 8, 2019, just four months into Plant's tenure, Arconic announced what investors had been hoping for: Arconic announced that it would split into two separate businesses. Arconic Inc. would be renamed Howmet Aerospace Inc. and a new company, Arconic Corporation, would be set up and spun out. Arconic Corporation will be focused on rolled aluminum products, and Howmet Aerospace will focus on engineered products.

The separation process was complex, requiring the untangling of shared services, IT systems, and supply chains that had been integrated over decades. But Plant and his team executed with precision. They negotiated the allocation of debt, divided the assets, and prepared both companies to stand on their own.

The separation was scheduled to become effective on April 1, 2020. The timing seemed perfect—aerospace markets were strong, the 737 MAX was returning to service after its grounding, and investors were hungry for pure-play aerospace exposure.

Then COVID-19 hit.

As the separation date approached, the world was shutting down. Air travel had virtually ceased, Boeing and Airbus were slashing production rates, and aerospace suppliers were facing an existential crisis. Some board members and advisors suggested delaying the separation, waiting for markets to stabilize.

But Plant made a crucial decision: proceed as planned. On April 1, 2020, as the world grappled with a pandemic, Howmet Aerospace began trading as an independent company for the first time in two decades. The company faced the worst aerospace downturn in history on its first day of independence.

What seemed like terrible timing would prove to be a blessing in disguise. The crisis gave Plant and his team the burning platform needed to make dramatic changes quickly. They cut costs aggressively, restructured operations, and positioned the company to emerge stronger when markets recovered. The very fact that Howmet survived and thrived through such a baptism by fire would become a testament to its resilience and Plant's operational excellence.

The Arconic years had been turbulent—marked by proxy fights, leadership changes, and strategic confusion. But they had also been necessary, providing the crucible in which Howmet's independent identity was forged. The company that emerged in 2020 was leaner, more focused, and ready to capitalize on the aerospace recovery that lay ahead.

VI. Modern Howmet: Products, Markets & Competitive Position

Walking through a Howmet facility today is like entering the hidden backbone of modern aviation. In one corner, a five-axis CNC machine mills turbine blades from single crystal superalloys, each blade worth more than a luxury car. Across the floor, workers inspect aerospace fasteners so precisely manufactured that tolerances are measured in ten-thousandths of an inch. This is high-stakes manufacturing where a single defect could ground an aircraft or worse.

Howmet's modern structure revolves around four distinct but synergistic segments, each addressing critical needs in aerospace and transportation markets.

Engine Products, the largest segment generating approximately $1.056 billion in revenue, is where Howmet's technological superiority shines brightest. The division manufactures airfoils, rings, disks, and forgings that operate in the hottest, most stressed sections of jet engines. Consider the high-pressure turbine blade: operating at temperatures exceeding 2,000 degrees Fahrenheit, spinning at 10,000 RPM, each blade endures centrifugal forces equivalent to hanging a double-decker bus from its tip. Howmet's single-crystal casting technology eliminates grain boundaries that could become failure points, while internal cooling channels—some no wider than a human hair—keep the metal from melting.

The segment's 33% EBITDA margins tell a story of technological moats and customer captivity. Once Howmet's components are designed into an engine program, they typically remain sole-sourced for the engine's entire production life—often 30-40 years. The qualification process alone can take 3-5 years and cost millions of dollars, creating switching costs that border on prohibitive.

Fastening Systems, with $431 million in revenue and 29.2% EBITDA margins, might seem pedestrian compared to exotic turbine blades, but represents an equally critical technology. Howmet holds the number one global position in aerospace fastening systems, and its high-tech, multi-material fastening systems are found nose to tail on aircraft and aerospace engines. A modern commercial aircraft contains approximately 1.5 to 3 million fasteners. Each must maintain precise torque specifications despite repeated stress cycles, temperature extremes from -65°F to 120°F, and exposure to hydraulic fluids, de-icing chemicals, and salt spray.

Howmet's fasteners aren't simple bolts—they're engineered systems. The company's Eddie-Bolt, for instance, features a pin within a sleeve that expands to fill the hole precisely, eliminating the play that causes fatigue failure. Their lockbolt technology provides vibration resistance superior to conventional nut-and-bolt combinations while reducing installation time by up to 75%.

Engineered Structures, generating $290 million in revenue with 21.4% EBITDA margins, produces titanium and aluminum structural components for aircraft. These aren't just metal shapes—they're complex geometries that must bear tremendous loads while minimizing weight. Howmet's expertise in hot forming, chemical milling, and precision machining allows it to create parts that would be impossible or prohibitively expensive for others to manufacture.

The division's titanium capabilities are particularly strategic. Titanium is notoriously difficult to machine—it work-hardens readily, generates tremendous heat, and eats through cutting tools. Howmet's proprietary processes and decades of experience allow it to shape this challenging material into components like landing gear beams and wing attachment fittings that must never fail.

Forged Wheels, the smallest segment at $276 million revenue but carrying important strategic value, maintains 27.5% EBITDA margins despite current market weakness. Howmet invented the first forged aluminum truck wheel in 1948—and by doing so, created an entire industry. Seven decades later, the company is proud to be the number one global market leader in the forged, aluminum heavy-duty truck wheel market.

The wheels business showcases Howmet's ability to create and dominate niches. Their Dura-Bright wheels eliminate the need for polishing through a surface treatment that penetrates the aluminum, maintaining mirror finish even after 100,000 miles. The Ultra ONE wheels with MagnaForce alloy are the lightest on the market, saving up to 1,400 pounds per truck—weight savings that translate directly to increased payload capacity and lifetime fuel savings exceeding $20,000 per vehicle.

Howmet's competitive position extends beyond individual product superiority to system-level advantages. The company operates as a tier-one supplier to every major aerospace OEM—Boeing, Airbus, GE, Pratt & Whitney, Rolls-Royce, Safran. These aren't vendor relationships; they're decades-long partnerships involving joint development, shared intellectual property, and integrated supply chains.

The firm operates 27 facilities in the United States, Canada, Mexico, France, the United Kingdom, China, Brazil, Hungary and Japan. This global footprint isn't just about market access—it's about being within the OEMs' supply chain ecosystems, participating in their development programs, and maintaining the certifications required to serve different markets.

The certification barriers alone are staggering. AS9100 for aerospace quality, NADCAP for special processes, individual OEM approvals for specific parts and processes—each requiring extensive documentation, regular audits, and continuous improvement. A new entrant would need to invest hundreds of millions of dollars and spend years just to achieve the certifications Howmet already holds.

But perhaps Howmet's greatest competitive advantage is its position in the aerospace aftermarket. Total spares revenue represented approximately 17% of total Howmet Aerospace revenue in 2024, significantly higher than the 11% of total revenue that spares represented in 2019. We envision spares to continue to be healthy again in 2025 and grow towards 20 percent of total Howmet Aerospace revenue in the coming years.

The spares business is the gift that keeps giving. An engine produced today will need replacement parts for 30+ years. As engines age, parts wear out more frequently. As flight hours increase—which they are post-COVID—spares demand accelerates. And unlike new production, where OEMs squeeze suppliers on price, spares carry premium pricing that can be 2-3x the original part cost.

This is the modern Howmet: a collection of businesses that seem disparate but share common threads of materials expertise, precision manufacturing, and positions in markets with extraordinary barriers to entry. It's a company that makes products most people will never see but absolutely depend upon every time they board an aircraft or share the road with a commercial truck.

VII. Financial Performance & The Plant Playbook

John Plant's first earnings call as CEO of the newly independent Howmet Aerospace on April 1, 2020, was surreal. As he spoke from Pittsburgh, commercial aviation was essentially grounded worldwide. Boeing had shut down production. Airbus was furloughing workers. Industry forecasts suggested air travel might not recover to 2019 levels until 2024 or beyond.

Yet Plant's tone was remarkably confident: "We've been through downturns before. We know what to do. And when this market recovers—and it will recover—we'll be ready."

What followed was a masterclass in operational excellence and financial discipline that transformed Howmet from a COVID casualty-in-waiting to one of the best-performing industrial stocks of the recovery.

Plant's playbook was deceptively simple but ruthlessly executed. First, protect the balance sheet. Within weeks of independence, Howmet had drawn down its revolver, suspended the dividend, and implemented emergency cost reductions. But unlike peers who slashed indiscriminately, Plant's cuts were surgical—protecting critical capabilities and customer relationships while eliminating redundancies exposed by the crisis.

The second move was counterintuitive: accelerate operational improvements while demand was weak. Plant knew that when aerospace production ramped back up, Howmet couldn't afford production bottlenecks or quality issues. Teams used the downturn to implement lean manufacturing initiatives, automate processes, and cross-train workers. Statistical process control was enhanced. Predictive maintenance was deployed. Digital twins were created for critical production assets.

By late 2020, green shoots were appearing. Domestic air travel in China had recovered. Cargo demand was booming. Airlines were retiring older aircraft faster than expected, driving spares demand. Plant's preparations paid off—Howmet could immediately capture this demand while competitors scrambled to restart operations.

The financial results have been extraordinary. Revenue for the full year of 2024 was approximately $7.4 billion, up 12 percent from 2023. Adjusted EBITDA of over $1.9 billion was up 27 percent year-over-year and was an all-time high. Adjusted Earnings per Share was $2.69 per share, up 46 percent year-over-year.

But the real story is in the margins. Operating income margin was 22.9%, up approximately 440 basis points year over year. In an industry where 15% operating margins are considered excellent, Howmet is approaching software-like profitability. This isn't financial engineering—it's operational excellence converting to bottom-line results.

The margin expansion has multiple drivers. Mix shift toward higher-margin engine products and spares. Pricing discipline as capacity constraints give suppliers leverage. Operational improvements reducing scrap, rework, and cycle times. But the biggest driver is simply operating leverage—as volumes recover, the fixed cost base Plant protected during COVID is being spread across more revenue.

Cash generation has been equally impressive. Free cash flow for the year was $977 million, with a healthy free cash flow conversion of net income excluding special items at 88 percent, which is in-line with our long-term target of 90 percent. This isn't the typical aerospace supplier pattern of consuming cash as production ramps. Howmet is generating cash while investing for growth—a rare combination.

Plant's capital allocation framework prioritizes financial flexibility and shareholder returns in equal measure. The company has systematically paid down debt, with net leverage now at just 1.3x EBITDA—remarkable for a capital-intensive manufacturer. In full year 2024, the Company generated $977 million of Free Cash Flow for an 88% conversion of Net Income, and deployed approximately $975 million of cash in the form of common stock repurchases, debt reduction, and dividends.

The debt reduction wasn't just about deleveraging—it was strategic. On July 1, 2024, Howmet Aerospace completed the early redemption of all the remaining outstanding aggregate principal amount of $205 million of its 5.125% Notes due October 2024 with cash on hand at par value plus accrued interest. By refinancing high-cost debt and terming out maturities, Plant has reduced interest expense by over $50 million annually while securing investment-grade ratings from all three agencies.

The operational improvements extend beyond financial metrics. Plant has instituted a culture of continuous improvement that permeates the organization. Every facility has daily huddles tracking safety, quality, delivery, and cost metrics. Problems are solved at the lowest possible level. Best practices are shared across facilities through a formal knowledge management system.

Quality, in particular, has seen dramatic improvement. In an industry where parts-per-million defect rates are standard, Howmet is pushing toward parts-per-billion in critical applications. This isn't just about avoiding recalls or customer complaints—it's about becoming the supplier aerospace OEMs turn to for their most critical, can't-fail components.

The investment in technology and capacity is equally strategic. Engines spares volumes increased again in the quarter and are expected to be approximately $1.25 billion for the full year. Recognizing this trend, Howmet has increased capital expenditure to $390 million, focused primarily on Engine Products capacity expansion. But this isn't just adding machines—it's investing in advanced manufacturing cells that can produce multiple part numbers with minimal changeover, providing flexibility as mix shifts.

Plant's most underappreciated innovation might be his approach to the commercial cycle. Unlike previous management teams who chased volume at any cost, Plant has been deliberately conservative in his planning assumptions. CEO John Plant has tempered expectations, assuming a 737 Max production rate of 25 units per month in 2025—lower than Boeing's internal targets—due to uncertainties around inventory drawdowns and supply chain fragility.

This conservatism isn't bearish—it's strategic. By planning for lower volumes, Howmet ensures it has the flexibility to capture upside without the fixed cost burden that crushes margins in downturns. It's a lesson learned from decades in automotive: plan for the trough, profit from the peak.

The Plant playbook has delivered spectacular results, but it's not finished. With the aerospace recovery still in early innings and operational improvements continuing, the financial trajectory remains compelling. The question isn't whether Howmet can maintain these margins—it's how much higher they can go as volumes recover and mix continues to shift toward higher-value products.

VIII. The Boeing Crisis & Supply Chain Navigation

The Alaska Airlines Flight 1282 incident on January 5, 2024, was every aerospace supplier's nightmare. At 16,000 feet, a door plug blew out of a nearly new Boeing 737 MAX 9, leaving a gaping hole in the fuselage. Passengers' phones were ripped from their hands. A teenager's shirt was torn from his body. Miraculously, no one died, but the images of that hole—and what it represented about Boeing's quality control—sent shockwaves through the industry.

For Howmet, which supplies critical fastening systems and engine components for the 737 MAX program, this presented an existential challenge. Boeing was not just a customer but the customer, representing nearly 30% of commercial aerospace revenue. The immediate question wasn't about fault—Howmet's parts weren't implicated in the door plug failure—but about what would happen to MAX production rates and, by extension, Howmet's order book.

The FAA temporarily grounded affected MAX 9 aircraft, and investigations raised further concerns about production quality and safety practices at Boeing. The regulatory response was swift and severe. The FAA capped Boeing's 737 production at 38 aircraft per month until quality improvements could be demonstrated—a cap that remains in place as of early 2025.

Plant's response revealed the strategic thinking that separates great industrial executives from merely good ones. Rather than publicly lamenting the situation or desperately seeking alternative volume, Howmet made a calculated decision: Revenue growth of 11% year over year took account of actions which restricted volumes shipped to the Boeing Company and notably weaker Europe market conditions impacting Forged Wheels.

Think about the audacity of this move. In the middle of an aerospace recovery, with competitors scrambling for every dollar of revenue, Howmet deliberately restricted shipments to its largest customer. The logic was compelling: Boeing's inventory management was chaotic, with parts piling up at Renton while production sputtered. By controlling shipments, Howmet avoided building excess inventory, maintained pricing discipline, and preserved cash flow.

But the Boeing crisis went deeper than production rates. It exposed fundamental weaknesses in aerospace supply chain management that had been building for decades. The relentless pursuit of cost reduction had created a system optimized for efficiency but lacking resilience. Single-source suppliers, just-in-time inventory, and globally distributed production created multiple points of failure.

Then came the strike. On September 13, 2024, 33,000 Boeing machinists walked off the job, bringing 737 production to a complete halt. For 53 days, the Renton and Everett factories stood silent. The strike's resolution on November 4 came with a 38% wage increase over four years—a victory for workers but another cost pressure for Boeing to potentially pass on to suppliers.

We are pleased that the Boeing strike was settled on November 4th, and we look forward to Boeing's gradual production recovery. But Plant's optimism was tempered with realism. He understood that Boeing's problems weren't just about labor relations or even quality control—they were about a production system that had been pushed beyond its limits.

The supply chain challenges extended beyond Boeing. A fire at an SPS Technologies fastener plant and global inventory shortages have highlighted vulnerabilities in the aerospace supply chain. Every disruption rippled through the entire ecosystem, affecting production schedules, delivery commitments, and financial planning across hundreds of suppliers.

Howmet's response to these challenges revealed the strength of its competitive position. Unlike smaller suppliers who lived hand-to-mouth on Boeing's payment terms, Howmet had the balance sheet strength to weather production volatility. Unlike single-program suppliers, Howmet's diversification across Boeing, Airbus, engine OEMs, and defense programs provided cushion. And unlike commodity suppliers, Howmet's specialized components couldn't simply be sourced elsewhere if relationships soured.

The company also benefited from an unexpected dynamic: the very chaos in Boeing's production system increased demand for Howmet's expertise. As Boeing struggled with traveled work (assembly tasks performed out of sequence), quality escapes, and supplier management, they leaned more heavily on trusted partners like Howmet. The crisis actually strengthened Howmet's position as a critical supplier whose reliability was worth premium pricing.

Plant's strategic navigation extended to managing investor expectations. We continue to employ a cautious view on underlying build rates in our guidance, assuming The Boeing Company produces approximately 25 737-MAX aircraft per month and 6 787 aircraft per month on average across 2025. By under-promising on Boeing's recovery, Howmet positioned itself to exceed expectations as production gradually improved.

The Boeing crisis also accelerated a strategic shift that had been underway since Plant's arrival: reducing customer concentration. While Boeing remains critical, Howmet has aggressively pursued Airbus content, won new engine programs with next-generation platforms, and expanded its defense aerospace exposure. The goal isn't to abandon Boeing but to ensure no single customer—or single program—can dictate Howmet's destiny.

Looking forward, the Boeing situation remains fluid. Since the January 2024 accident, Boeing must receive approval from the FAA to increase output of the 737 Max to above 38 jets a month. Boeing said once it has stabilized its production rate at 38 per month, it will move up to 42, if it receives approval, and then increase it in five-per-month increments. Each increment represents substantial revenue opportunity for Howmet, but Plant continues to plan conservatively.

The Boeing crisis has been painful for the entire aerospace supply chain, but for Howmet, it's also been clarifying. It's validated Plant's operational excellence focus—when production is chaotic, quality and reliability command premiums. It's proven the value of financial strength—when customers struggle, suppliers with strong balance sheets gain share. And it's demonstrated that in aerospace, as in any industry with extreme barriers to entry, the strongest players emerge from crises even stronger.

IX. Growth Drivers & Future Strategy

Standing in Howmet's Engine Products facility in Hampton, Virginia, you can literally hear the future of aerospace being forged. The rhythmic pounding of massive hydraulic presses shapes superalloy disks that will spin at the heart of next-generation engines. Each strike represents not just metal being formed, but a bet on where aviation is heading: hotter, faster, more efficient, and paradoxically, much more complicated.

The numbers tell a compelling story of an industry in the early stages of a multi-decade super-cycle. The Company reported third quarter 2024 revenue of $1.84 billion, up 11% year over year, primarily driven by growth in the commercial aerospace market of 17%. But focusing on quarterly growth rates misses the structural forces that will drive Howmet's business for the next decade.

Start with the macro picture: global air traffic is projected to double by 2040. This isn't speculative—it's driven by demographics and economics. Three billion people in Asia are entering the middle class, and their first major purchase after housing isn't a car—it's an airline ticket. Meanwhile, in developed markets, the hub-and-spoke model is giving way to point-to-point travel, requiring more aircraft to serve the same number of passengers.

The aircraft order books reflect this reality. Boeing and Airbus have combined backlogs exceeding 15,000 aircraft—nearly eight years of production at current rates. But these aren't just replacement orders. Airlines are expanding fleets, upgauging from regional jets to narrow-bodies, and narrow-bodies to wide-bodies. Each step up means more content per aircraft for Howmet.

The defense aerospace market, for which our revenue increased 15 percent in 2024 compared to 2023, was also a source of strength, and we expect this continuing into 2025 for both the F-35 aircraft and legacy fighter programs. Defense aerospace spares revenue growth was healthy in 2024, and we expect this trend to continue in 2025 as the fleet of F-35 aircraft continues to expand worldwide.

The defense opportunity is particularly intriguing. The F-35 program, despite its troubled history, is ramping toward full-rate production with planned deliveries of 150+ aircraft annually. Each F-35 contains approximately $500,000 of Howmet content—fasteners, engine components, structural elements. With over 3,000 F-35s planned globally and a service life extending beyond 2070, this single program represents billions in future revenue.

But the real growth driver—the one that transforms Howmet's economics—is the aftermarket. Spares growth was significant in 2024, and we expect robust growth again in 2025, driven by significant needs from both legacy and current engine programs. The math here is compelling. An engine that generates $1 million in original equipment revenue will generate $3-5 million in spares over its 30-year life. And unlike new equipment, where Howmet faces pricing pressure from OEMs, spares are typically sole-sourced with escalation clauses.

The spares acceleration isn't just about fleet growth—it's about utilization and demographics. Airlines are flying aircraft harder than ever, with utilization rates approaching 12-14 hours per day for narrow-bodies. Higher utilization means more cycles, more wear, more parts replacement. Meanwhile, the global fleet is aging. The average age of the commercial fleet has increased from 10.5 years in 2010 to nearly 12 years today. Older aircraft require more maintenance, driving spares demand.

Howmet's investment strategy reflects these opportunities. The company has increased capital expenditure to $390 million, with the majority directed toward Engine Products capacity. But this isn't just about adding furnaces and forging presses. Howmet is investing in flexible manufacturing systems that can handle multiple part numbers, automated inspection systems that reduce quality escapes, and digital systems that provide real-time visibility into production status.

The technology investments are particularly strategic. Howmet is deploying artificial intelligence for demand forecasting, using machine learning to optimize casting parameters, and implementing blockchain for supply chain traceability. These aren't buzzword initiatives—they're practical applications that reduce cost, improve quality, and strengthen customer relationships.

The next-generation engine programs represent another growth vector. CFM's RISE program, targeting 20% fuel efficiency improvement, will require materials and manufacturing techniques that don't exist today. Pratt & Whitney's geared turbofan evolution, Rolls-Royce's UltraFan—each program represents years of development work, followed by decades of production and aftermarket revenue.

Howmet's role in these programs extends beyond simple supply. The company is co-developing materials, sharing intellectual property, and investing alongside engine OEMs. This deep partnership model creates switching costs that approach infinity—no OEM will change suppliers for critical rotating parts mid-program when hundreds of millions in certification costs are at stake.

The sustainability angle adds another dimension. This optimism is further fueled by the growing demand for spares, as airlines extend the lifespan of older aircraft due to lingering supply chain bottlenecks. As airlines face pressure to reduce emissions, they're caught between ordering new, more efficient aircraft (good for Howmet's OE business) or upgrading existing aircraft with new engines and components (good for spares). Either path drives demand.

Even the commercial transportation segment, currently facing cyclical headwinds, has strategic value. The commercial truck market entered a cyclical downturn in 2024, as expected. For 2025, we do not expect the market to recover before mid-year 2025. A potential increase in commercial truck builds is less certain in the second half of the year, given tariff-related and economic uncertainty in North America.

But Howmet isn't just waiting for the cycle to turn. The company is developing aluminum wheels for electric trucks, where weight savings are even more critical given battery weight penalties. They're expanding in Europe, where stricter emissions regulations drive aluminum adoption. And they're pushing into adjacent markets like buses and specialty vehicles.

The international expansion opportunity remains underexploited. While Howmet has facilities globally, international sales are still primarily to multinational OEMs. As Chinese, Indian, and Brazilian aerospace companies mature, they'll need the same sophisticated components Howmet supplies to Western OEMs. The company's strategy here is careful—protecting intellectual property while capturing growth in emerging markets.

Plant's vision for Howmet extends beyond riding industry tailwinds. He's positioning the company to shape those winds. By investing ahead of demand, developing next-generation capabilities, and maintaining financial flexibility, Howmet isn't just participating in the aerospace super-cycle—it's helping to enable it.

The growth trajectory seems almost too good to be true: secular growth in air travel, aging fleet dynamics driving spares, new engine programs requiring advanced materials, defense spending increasing globally. But that's the nature of aerospace cycles—the downs are brutal, but the ups can last for decades. And Howmet, after surviving the worst downturn in aviation history, is positioned to capture more than its fair share of the upturn.

X. Competitive Analysis & Market Position

In the rarefied air of aerospace suppliers, Howmet occupies a unique position—not the largest, not the most diversified, but arguably the most strategically positioned. Understanding this requires examining the competitive landscape through multiple lenses: capability, customer relationships, and capital allocation.

Start with Precision Castparts (PCC), the $40 billion Berkshire Hathaway-owned giant that's Howmet's most direct competitor. PCC is roughly twice Howmet's size with broader capabilities spanning fasteners, forgings, and castings. When Warren Buffett bought PCC for $37 billion in 2015, he called it "the deal of a lifetime," attracted by its wide moat and predictable cash flows.

But PCC's size has become a liability in some ways. The company's bureaucratic culture—a common affliction of Berkshire industrial subsidiaries—has slowed decision-making. Customer complaints about delivery delays and quality issues have mounted. And critically, PCC's investment in next-generation manufacturing has lagged, with the company still relying on processes developed decades ago for many products.

Howmet's advantage over PCC isn't in scale but in focus and agility. Where PCC spreads investment across dozens of businesses, Howmet concentrates on four core segments. Where PCC relies on Berkshire's patience with long-term returns, Howmet must deliver quarterly results to public markets—a pressure that drives operational excellence.

TransDigm represents a different competitive model entirely. With its acquire-and-optimize strategy, TransDigm has rolled up dozens of aerospace suppliers, typically those with proprietary products and aftermarket exposure. The company's playbook is consistent: buy businesses, dramatically raise prices, cut costs, and generate extraordinary margins—often exceeding 40% EBITDA.

TransDigm's model works because of the certification barriers and switching costs in aerospace. Once a TransDigm part is designed into an aircraft, it's essentially a monopoly for that component's life. The company has faced Congressional scrutiny for "price gouging," but continues to generate exceptional returns for shareholders.

Howmet can't—and shouldn't—replicate TransDigm's model entirely. The company's critical position in engine programs and structural components requires maintaining trust with OEMs. But Howmet has adopted some TransDigm principles: focus on proprietary products, maximize aftermarket exposure, and use pricing power judiciously but consistently.

Hexcel, the advanced composites manufacturer, represents another competitive dynamic. As aircraft shift from aluminum to carbon fiber composites, companies like Hexcel have captured substantial value. The Boeing 787 is 50% composites by weight; the Airbus A350, 53%. This secular shift theoretically threatens aluminum-focused suppliers like Howmet.

But the composite threat has proven overblown for several reasons. First, engines remain predominantly metal—the temperatures and stresses are simply too extreme for composites. Second, many structural joints and attachment points still require metal for strength and fatigue resistance. Third, the repairability and recyclability challenges of composites have slowed adoption in some applications. Howmet's response has been strategic: develop expertise in titanium and other advanced metals that complement composites rather than compete with them.

The competitive dynamics in fasteners deserve special attention. Howmet competes with specialists like Lisi Aerospace and smaller players like TriMas. The fastener market might seem commoditized—after all, how differentiated can a bolt be? But aerospace fasteners are anything but commodities. Each is designed for specific loads, materials, and environmental conditions. The installation process, not just the fastener itself, is often proprietary.

Howmet's fastener advantage comes from integration. While competitors supply fasteners, Howmet supplies fastening systems—the fastener, the installation tooling, the training, the engineering support. This systems approach creates switching costs that transcend the component itself.

The engine components market presents the highest barriers to entry. Here, Howmet competes with captive suppliers (GE's own casting operations), Japanese specialists (IHI, MHIAEL), and European players (Safran's various subsidiaries). The competition isn't just about capability—it's about relationships built over decades and shared investment in development programs.

Howmet's position in engines is nearly unassailable for rotating parts. The combination of single-crystal casting capability, capacity to handle large parts, and track record of zero-defect quality makes the company irreplaceable for certain applications. When Pratt & Whitney needs high-pressure turbine blades for the geared turbofan, or when GE needs shrouds for the GE9X, Howmet is often the only viable supplier.

The moats protecting Howmet's market position are multifaceted:

Certification Barriers: A new entrant would need 5-7 years and hundreds of millions of dollars just to achieve the certifications Howmet already holds. Each customer, each facility, each process requires separate certification. The documentation alone—literally millions of pages—represents decades of accumulated knowledge.

Metallurgical Expertise: Howmet's knowledge of superalloys, built over 70 years, can't be replicated by hiring a few engineers. The company holds composition secrets, process parameters, and failure analysis data that represent thousands of person-years of experience.

Customer Relationships: Aerospace isn't transactional. Engineers from Howmet sit in Boeing's facilities, participate in design reviews, and have security clearances for classified programs. These relationships, built over decades, create switching costs that transcend economics.

Capital Requirements: A single vacuum induction melting furnace for superalloys costs $20-30 million. A modern forging press, $50 million. The capital required to replicate Howmet's capabilities would exceed $5 billion—and that's before considering the learning curve losses during ramp-up.

Network Effects: Howmet's position across multiple programs creates virtuous cycles. Lessons learned on one engine program improve performance on another. Materials developed for defense applications migrate to commercial. Scale in one area funds R&D in another.

The competitive landscape is evolving with new challenges. Chinese companies, backed by state investment, are developing aerospace capabilities. Additive manufacturing threatens some traditional casting applications. Electric aircraft could disrupt engine component demand.

But Howmet's competitive position has actually strengthened through recent crises. COVID eliminated marginal competitors. Boeing's troubles favored established suppliers over newcomers. Supply chain chaos rewarded companies with strong balance sheets and operational excellence. As Plant noted in a recent earnings call, "The weak players have been washed out. What remains are the strong, and we intend to be the strongest."

XI. Bull vs. Bear Case

The investment case for Howmet Aerospace crystallizes around a fundamental question: Is this a cyclical industrial riding a temporary aerospace recovery, or a transformed company with secular growth drivers that transcend the cycle? The answer determines whether the stock's 100%+ gain in 2024 represents the end of a recovery trade or the beginning of a multi-year compounding story.

The Bull Case: Aerospace Super-Cycle Beneficiary

The bulls start with industry structure. The commercial aerospace duopoly of Boeing and Airbus has backlogs stretching nearly a decade. According to the International Air Transport Association (IATA), a record-breaking 1,802 new planes are expected to be delivered in 2025, following 1,254 deliveries in 2024. This isn't speculative demand—these are firm orders with deposits, from airlines with financing, for routes with demonstrated passenger demand.

The production ramp ahead is unprecedented. Boeing, despite its troubles, is targeting 52 737 MAX per month by 2025-26. Airbus aims for 75 A320neo family aircraft monthly by 2026. Every aircraft needs Howmet's components—not as options but as certified, sole-sourced parts with no alternatives. The revenue visibility extends not quarters but years into the future.

The spares story is even more compelling. Total spares revenue represented approximately 17% of total Howmet Aerospace revenue in 2024, significantly higher than the 11% of total revenue that spares represented in 2019. We envision spares to continue to be healthy again in 2025 and grow towards 20 percent of total Howmet Aerospace revenue in the coming years. This isn't just mix shift—it's margin expansion. Spares typically carry 40-50% gross margins versus 30-35% for original equipment.

The math on spares is inexorable. The global commercial fleet of 28,000 aircraft will grow to 45,000 by 2040. Each aircraft requires more maintenance as it ages. Flight hours are recovering to exceed pre-COVID levels. The installed base of engines with Howmet components grows every day, creating an annuity stream that compounds annually.

Operational leverage amplifies the recovery. Howmet's cost structure was right-sized for survival during COVID. As volumes recover, incremental margins approach 35-40%. Adjusted EBITDA grew faster than revenue, up 27% year over year, resulting in margins up approximately 350 basis points to 26.5%. The company is already approaching software-like margins in a heavy manufacturing business.

The balance sheet provides both safety and optionality. Net debt of just 1.3x EBITDA gives Howmet capacity for acquisitions, aggressive buybacks, or simply weathering any unexpected turbulence. The investment-grade rating achieved in 2024 reduces financing costs and expands strategic flexibility.

Management quality under Plant represents a step-change improvement. He brings a track record of successfully leading businesses through periods of downturns and challenges and periods of growth and market development. His expertise in the aerospace and defense and automotive industries and his deep familiarity with all aspects of the Company's businesses enable him to develop and lead the execution of the Company's strategic vision. Plant's operational focus, conservative planning, and capital allocation discipline address the execution risks that plagued previous management teams.

The valuation remains reasonable despite the stock's appreciation. At roughly 18x forward earnings, Howmet trades at a discount to aerospace peers like TransDigm (24x) and HEICO (35x), despite superior organic growth prospects and cleaner accounting. On an EV/EBITDA basis, Howmet at 14x compares favorably to precedent transactions in the sector typically done at 15-20x.

The Bear Case: Multiple Risks Converging

The bears start with Boeing's intractable problems. Despite optimistic projections, Boeing managed to deliver just 348 commercial aircraft in 2024, far below targets. The 737 MAX production rate remains capped by regulators. Quality problems persist. As of February 2024, the MAX 7 and MAX 10 have not been certified, with the FAA declining to put any timetable on approval. Each Boeing disappointment directly impacts Howmet's volumes.

Customer concentration remains uncomfortable. Despite diversification efforts, Boeing and its supply chain represent nearly 30% of revenue. A prolonged Boeing crisis—whether from production problems, certification delays, or competitive losses to Airbus—would materially impact Howmet's growth trajectory.

The commercial transportation segment faces structural headwinds. For 2025, we do not expect the market to recover before mid-year 2025. A potential increase in commercial truck builds is less certain in the second half of the year, given tariff-related and economic uncertainty in North America. Electric vehicle adoption could disrupt demand for traditional diesel truck wheels. Autonomous vehicles might reduce the total number of commercial vehicles needed.

Supply chain constraints could limit growth regardless of demand. The aerospace supply chain remains fragile, with single points of failure throughout. Skilled labor shortages persist. Raw material availability, particularly for exotic superalloys, remains tight. Any significant disruption could prevent Howmet from capitalizing on demand recovery.

Geopolitical risks are multiplying. US-China tensions could impact Howmet's Asian operations and customers. European defense spending, while increasing, faces budget constraints. Trade wars and tariffs could disrupt carefully optimized global supply chains. The company's international footprint, while providing diversification, also increases exposure to geopolitical volatility.

Technological disruption lurks on the horizon. Additive manufacturing continues to improve, potentially eliminating the need for some cast or forged components. Electric aircraft, while still experimental, could reduce demand for traditional engine components. New materials like ceramic matrix composites could substitute for metal in some applications.

The valuation embeds aggressive assumptions. Current multiples assume aerospace production rates that have never been achieved. Margin expansion expectations may prove optimistic if mix shifts unfavorably or competition intensifies. Any disappointment in execution could trigger multiple compression given high investor expectations.

Cyclical risks haven't disappeared. Aerospace remains a cyclical industry despite current secular growth drivers. A global recession, another pandemic, or a major aviation accident could quickly reverse demand trends. Howmet's operational leverage works both ways—just as margins expanded rapidly during recovery, they could compress quickly in a downturn.

The Verdict: Asymmetric Risk-Reward

The bull case ultimately appears stronger, but not without caveats. The secular growth drivers in aerospace are real and sustainable. Howmet's competitive position has strengthened through the crisis. Management execution has been exceptional. The spares growth story provides cushion against OE volatility.

But the risks are equally real. Boeing's problems aren't quickly solvable. Supply chains remain fragile. Valuations reflect significant future growth. Investors must weigh whether the potential for continued outperformance justifies these risks.

The key insight may be timeframe. Short-term traders face significant volatility risk from Boeing production updates, quarterly earnings variations, and macro concerns. Long-term investors can look through this volatility to the structural growth opportunity in aerospace over the next decade.

For those with conviction in the aerospace super-cycle and confidence in Plant's execution, Howmet represents a compelling opportunity to own a high-quality industrial at the beginning of a multi-year growth phase. For those concerned about near-term risks and valuation, waiting for a better entry point may prove prudent. The beauty—or curse—of public markets is that both views will eventually be proven right or wrong, just on different timelines.

XII. Playbook: Business & Investing Lessons

Every great business story contains lessons that transcend the specific company or industry. Howmet's journey from dental castings to aerospace dominance offers a masterclass in industrial transformation, operational excellence, and the power of patient capital allocation. These lessons apply whether you're running a manufacturing company, analyzing industrial stocks, or simply trying to understand what separates exceptional businesses from mediocre ones.

Lesson 1: Operational Excellence Beats Financial Engineering

The contrast between Howmet under Arconic's financial engineering and under Plant's operational leadership is stark. Arconic's management focused on complex corporate structures, ambitious margin targets without clear paths to achievement, and promises of synergies that never materialized. The stock languished despite favorable industry conditions.

Plant's approach was radically different. No grand visions, no transformational acquisitions, just relentless focus on the basics: improve quality, reduce costs, deliver on time, generate cash. Adjusted Earnings per Share was $2.69 per share, up 46 percent year-over-year. This wasn't financial engineering—it was blocking and tackling executed at an elite level.

The lesson extends beyond Howmet. In industrial businesses, sustainable value creation comes from operational improvements that compound over time, not from financial gymnastics that look clever on PowerPoint slides. When evaluating management teams, look for leaders who talk about process improvements, cycle time reduction, and customer satisfaction—not just margin targets and EPS guidance.

Lesson 2: The Power of Focused Separation

Howmet's history is littered with conglomerate structures that destroyed value: Howe Sound, Cordant, Alcoa, Arconic. Each combination promised synergies that never materialized while creating complexity that hindered execution. Only when Howmet achieved focused independence did its true potential emerge.

Arconic announced that it would split into two separate businesses. Arconic Inc. would be renamed Howmet Aerospace Inc. and a new company, Arconic Corporation, would be set up and spun out. Arconic Corporation will be focused on rolled aluminum products, and Howmet Aerospace will focus on engineered products.

The separation wasn't just about corporate structure—it was about strategic clarity. Rolled aluminum products and aerospace components require different capabilities, different investment priorities, and different management skills. Combining them created a muddle that served no one well.

For investors, the lesson is clear: beware of conglomerates claiming synergies between unrelated businesses. The market consistently awards higher multiples to focused companies than to diversified ones, and for good reason. Complexity destroys value more often than it creates it.

Lesson 3: Aftermarket Economics Transform Business Models

The shift in Howmet's revenue mix toward spares represents more than just a product mix change—it's a fundamental business model transformation. Original equipment is essentially a customer acquisition cost. The real value creation happens in the aftermarket, where margins are higher, competition is limited, and relationships deepen over decades.

Total spares revenue represented approximately 17% of total Howmet Aerospace revenue in 2024, significantly higher than the 11% of total revenue that spares represented in 2019. We envision spares to continue to be healthy again in 2025 and grow towards 20 percent of total Howmet Aerospace revenue in the coming years.

This mirrors successful models across industries. Elevators companies lose money installing elevators but generate enormous profits from maintenance contracts. Printer manufacturers sell printers at a loss but make fortunes on ink. The lesson: look for businesses where the initial sale creates an installed base that generates recurring, high-margin revenue streams.

Lesson 4: Managing Through Cycles Requires Balance Sheet Strength

Howmet survived COVID, the Boeing crisis, and multiple downturns because it maintained financial flexibility when times were good. The temptation in aerospace upturns is to leverage up, acquire aggressively, and maximize current returns. Howmet chose a different path: steady debt reduction, conservative capital allocation, and maintaining dry powder for opportunities or challenges.

The company's net debt-to-EBITDA ratio of 1.3x might seem overly conservative in an era of cheap capital and aggressive financial engineering. But this conservatism provided the flexibility to restrict Boeing shipments, invest through the downturn, and emerge stronger when competitors struggled.

For investors, the lesson is about risk management. In cyclical industries, balance sheet strength isn't just about surviving downturns—it's about having the capability to play offense when competitors are playing defense. The best returns often come from investing through cycles, not timing them.

Lesson 5: Customer Captivity Requires Continuous Investment

Howmet's moats might seem impregnable—certifications, switching costs, decades-long relationships. But maintaining these advantages requires continuous investment in technology, quality, and customer relationships. The moment a supplier becomes complacent, assuming switching costs will protect them, is when disruption begins.

The company's increased capital expenditure despite already strong market positions reflects this understanding. Investing in next-generation manufacturing, developing new alloys, and co-investing with customers in development programs—these aren't just growth investments but moat maintenance.

The broader lesson: competitive advantages in industrial businesses are never permanent. They must be continuously renewed through investment, innovation, and customer focus. When analyzing companies with apparent moats, look for evidence of reinvestment to maintain those advantages.

Lesson 6: Crisis Creates Opportunity for Prepared Operators

COVID and the Boeing crisis were catastrophes for aerospace. But for Howmet under Plant's leadership, they became catalysts for transformation. The company used the downturn to restructure operations, implement new systems, and prepare for recovery. When demand returned, Howmet could capture more than its fair share.

This pattern repeats across industries. The 2008 financial crisis enabled the strongest banks to acquire weaker competitors at attractive prices. The dot-com bust allowed Amazon to build infrastructure while competitors retreated. Crisis creates opportunity, but only for those with the preparation and resources to capitalize.

Lesson 7: Pricing Power Comes from Being Mission-Critical

Howmet's ability to maintain and even expand margins during industry turbulence reflects a fundamental truth: customers will pay premium prices for products they absolutely cannot do without. A fastener might cost $50, but if its failure grounds a $100 million aircraft, the airline will happily pay $55 for better quality.

This extends beyond aerospace. Find businesses that solve mission-critical problems where the cost of failure far exceeds the cost of the solution. These businesses have pricing power that transcends normal competitive dynamics.

The Meta-Lesson: Compound Learning

Perhaps the most important lesson from Howmet's century-long journey is the power of compound learning. Each era built on previous capabilities: dental casting expertise enabled aerospace entry, aerospace expertise enabled engine component leadership, engine component leadership enabled aftermarket dominance.

This isn't just corporate history—it's a model for building enduring competitive advantages. In a world obsessed with disruption and transformation, Howmet shows the power of patient capability building. The company's success didn't come from pivoting to the latest trend but from steadily accumulating expertise that compounds over decades.

For investors, this suggests looking for companies with similar learning curves—businesses where each year's experience makes next year's execution better. For operators, it argues for patience in capability building rather than constantly chasing new opportunities. And for anyone studying business, it demonstrates that sustainable success comes not from revolutionary breakthroughs but from evolutionary improvements that compound over time.

The Howmet playbook isn't about grand strategies or brilliant insights. It's about doing ordinary things extraordinarily well, consistently, over long periods. In a business world obsessed with disruption, there's something profoundly powerful about simply being excellent at what you do.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube