Hexaware Technologies: From Mumbai Startup to PE Unicorn - The Art of Building an IT Services Giant

I. Introduction & Episode Setup

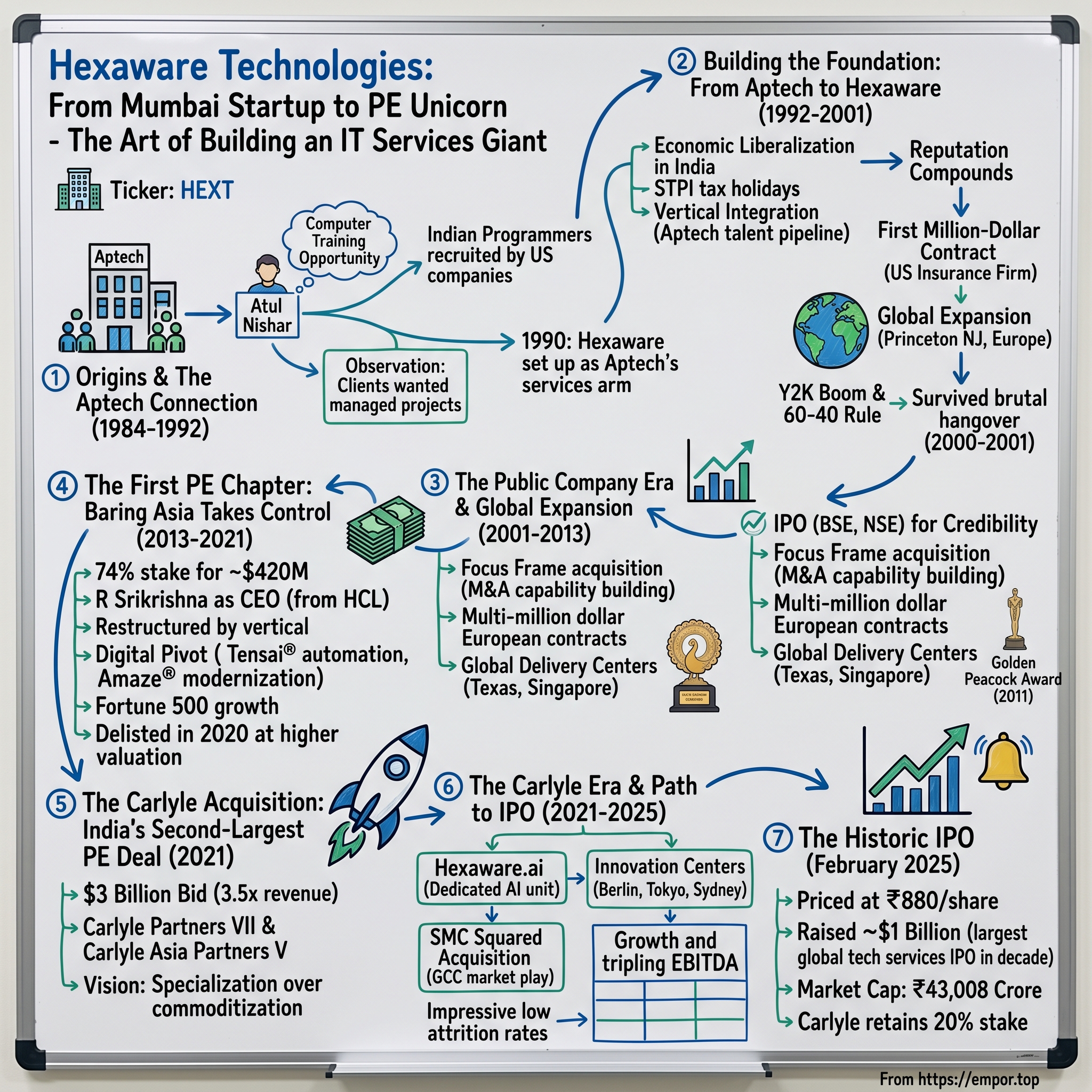

Picture this: It's February 19, 2025, and the trading floor at the National Stock Exchange erupts. Hexaware Technologies has just priced its IPO at ₹880 per share, raising nearly $1 billion in what would become the largest technology services IPO globally in over a decade. The company's market cap soars to ₹43,008 crore on day one. But here's what makes this moment extraordinary—this isn't Hexaware's first time as a public company. This is actually its second act, a resurrection story that traces through three decades of Indian IT evolution, two private equity owners, and a transformation from a computer training spin-off to a digital services powerhouse.

The hook that makes Hexaware's story irresistible isn't just the numbers—though ₹12,759 crore in revenue and 32,310 employees across 30+ countries certainly command attention. It's the audacious playbook: How does a company go public, get taken private for $420 million, change hands for $3 billion, then return to public markets at an even higher valuation? And perhaps more intriguingly—why would some of the world's most sophisticated private equity firms bet billions on what many consider a commoditized IT services business?

This is a story about timing, transformation, and the relentless pursuit of scale in India's technology services industry. It's about how Atul Nishar's side project became Baring Asia's crown jewel, then Carlyle's digital transformation vehicle. Along the way, we'll decode the art of building, selling, and rebuilding an IT services giant—lessons that apply whether you're a founder in Bangalore or a growth investor in Boston.

The roadmap ahead takes us through three distinct eras of ownership, each with its own playbook. We'll see how economic liberalization in 1990s India created the perfect storm for IT services entrepreneurship. We'll witness the Y2K boom that put Indian tech on the global map. We'll decode why private equity firms see gold where others see commoditization. And we'll understand why, in 2025, the public markets are once again ready to embrace what Hexaware has become.

II. Origins & The Aptech Connection (1984-1992)

The Mumbai of 1984 was a city on the cusp of transformation. In the narrow lanes of Fort district, where British colonial architecture meets Indian commercial hustle, Atul Nishar was running a computer training institute called Aptech. Personal computers were exotic machines that most Indians had only read about in magazines. But Nishar saw something others didn't—not just the machines themselves, but the massive human capital opportunity they represented.

Aptech wasn't just teaching BASIC and COBOL to curious engineers. It was creating India's first generation of software professionals at scale. By 1990, with thousands of students passing through Aptech's doors, Nishar noticed a pattern: his best graduates were getting recruited by American companies for software maintenance work. The labor arbitrage was staggering—an Indian programmer cost one-tenth of an American counterpart. But there was a problem: these companies wanted not just individual programmers, but entire teams, managed projects, guaranteed outcomes.

That observation sparked Hexaware's genesis. In 1990, Nishar set up what would become Hexaware as the services arm of Aptech—essentially saying, "Why send our graduates to work for others when we can organize them ourselves?" The initial setup was almost comically modest: a few rooms in Aptech's training center converted into a "development center," with programmers working on overflow projects from US clients who couldn't afford Silicon Valley rates.

The formal incorporation came in 1992 as Aptech Information Systems Limited. The timing was exquisite—India had just launched its economic liberalization under Finance Minister Manmohan Singh. Suddenly, importing computers became easier, satellite links for data transmission were permitted, and foreign companies could actually pay Indian firms in dollars without bureaucratic nightmares. The Software Technology Parks of India (STPI) scheme offered tax holidays. It was as if the government had suddenly discovered that software exports could be India's ticket to the global economy.

But here's what made Nishar's approach different from the hundreds of other IT services startups sprouting across India: vertical integration. While others were pure services plays, Hexaware had Aptech as its talent pipeline. Every year, thousands of trained programmers emerged from Aptech centers, and the best could be channeled directly into Hexaware projects. It was like owning both the university and the consulting firm—a model that would prove invaluable in the talent wars to come.

The early projects were unglamorous—maintenance of legacy COBOL systems, data entry, simple testing work. But Nishar understood something fundamental: in services, reputation compounds. Every successfully delivered project became a reference for the next, slightly larger project. Every satisfied client became an evangelist in their industry. By late 1992, Hexaware had its first million-dollar contract, working with a US insurance firm to modernize their claims processing system.

The philosophy Nishar embedded in those early days would define Hexaware for decades: "Don't just execute projects, build relationships." While competitors chased the latest technical trends, Hexaware focused on becoming indispensable to a core set of clients. This wasn't about being the smartest guys in the room—it was about being the most reliable. As we'll see, this DNA would make Hexaware irresistible to private equity buyers decades later.

III. Building the Foundation: From Aptech to Hexaware (1992-2001)

The year 1995 marked Hexaware's first real test of ambition. The company opened offices in North America and Europe—not just sales outposts, but actual delivery centers. The Princeton, New Jersey facility, established in 1998, was particularly audacious. Here was an Indian company setting up shop in America's backyard, competing for talent with Silicon Valley giants and Wall Street banks. The locals were skeptical: Could a company from Mumbai really deliver enterprise-grade software to Fortune 500 companies?

The answer came through a clever positioning strategy. Instead of competing head-to-head with Accenture or IBM on digital transformation, Hexaware positioned itself as the "night shift" for American IT departments. When New York banks closed at 5 PM, Hexaware's Mumbai team was just starting their day. When those banks opened at 9 AM, tested, debugged code was waiting in their repositories. The company marketed this as "Follow the Sun" development—a 24-hour productivity cycle that was only possible because of the geographic arbitrage.

The name evolution tells its own story of growing confidence. In 1996, the company dropped "Information Systems" to become simply Aptech Ltd. Then in 2001, in a decisive break from its parent company roots, it became Hexaware Technologies Limited. The "Hexa" prefix wasn't random—it represented six core values the company claimed to embody: Human Touch, Excellence, Execution, Accountability, Winning Attitude, and Relationship. Corporate branding aside, the real message was clear: this was no longer just Aptech's side project.

By 1998, development centers in Mumbai and Chennai were humming with over 1,000 engineers. But the real validation came from client wins that seemed impossible just years earlier. General Electric's financial services arm signed a multi-year contract. Deutsche Bank brought them in for derivatives trading systems. British Airways needed help with reservation systems. These weren't just vendors anymore—Hexaware engineers had badges to enter some of the world's most secure corporate facilities.

Then came Y2K—the great paranoia that computer systems would collapse when calendars rolled from 1999 to 2000. For Indian IT services, this was their Marshall Plan moment. Suddenly, every bank, insurance company, and government agency needed armies of programmers to review millions of lines of legacy code. Hexaware's revenue jumped from $12 million in 1997 to $45 million by 1999. The company hired 500 engineers in six months. Aptech training centers ran three shifts to keep up with demand.

But Nishar saw Y2K differently than his competitors. While others were drunk on easy money from mundane code reviews, he knew this windfall would end abruptly on January 1, 2000. So even as Hexaware gorged on Y2K projects, Nishar insisted on maintaining non-Y2K work. "We called it the 60-40 rule," a former executive recalled. "Maximum 60% revenue from Y2K, minimum 40% from real development work. When the music stopped, we wanted to still be dancing."

That discipline paid off spectacularly. When Y2K passed without catastrophe (thanks partly to the very work companies like Hexaware had done), the industry faced a brutal hangover. Hundreds of Indian IT firms shut down in 2000-2001. Day rates collapsed from $150 to $50. But Hexaware, with its diversified base, not only survived but acquired talent and clients from failing competitors. By 2001, as it prepared for its IPO, the company had weathered its first major crisis and emerged stronger—a pattern that would repeat throughout its history.

IV. The Public Company Era & Global Expansion (2001-2013)

The IPO roadshows of 2001 were a masterclass in managing expectations. Indian capital markets were still recovering from the dot-com bust, and technology stocks were toxic. But Hexaware's pitch was different: "We're not a tech company, we're a services company that happens to use technology." The distinction mattered. While investors had been burned by vaporware and phantom revenues, Hexaware could point to real contracts, real clients, and real cash flows.

The listing on the Bombay Stock Exchange and National Stock Exchange gave Hexaware something more valuable than capital—credibility. Fortune 500 procurement departments could now pull up audited financials. European regulators could verify governance standards. The quarterly earnings calls became marketing events where management could showcase client wins to both investors and prospects.

The 2004 expansion into Germany through the European Development Centre was a calculated bet on the enterprise software market. SAP ruled European enterprises, and Hexaware positioned itself as the premier SAP implementation partner for companies wanting offshore advantages without offshore risks. The same year, they launched Caliber Point, a business process outsourcing subsidiary. This wasn't just about following the BPO trend—it was about owning the entire technology stack for clients, from back-office processing to front-end applications.

The $34.3 million acquisition of Focus Frame in 2006 revealed Hexaware's emerging M&A philosophy: buy capabilities, not just revenue. Focus Frame brought sophisticated testing methodologies and automation tools that would normally take years to build organically. More importantly, it brought relationships with Silicon Valley technology companies who needed independent testing for their enterprise products. Within 18 months, Focus Frame's testing frameworks were deployed across all Hexaware projects, improving margins by 300 basis points. The 2007 launch of Risk Technology International Limited as a joint venture where Hexaware owned 85% stake represented their push into specialized financial services. This wasn't just another vertical—it was a bet that risk management would become the next major IT spending category after Y2K and ERP. The timing was prescient: within a year, the 2008 financial crisis would make risk technology mission-critical for every bank on the planet.

The Golden Peacock Award for Corporate Governance in 2011 might seem like corporate back-patting, but it mattered enormously for client acquisition. Post-Enron, post-Satyam scandal, Western corporations were paranoid about vendor governance. This award, along with stringent quarterly reporting, gave procurement departments the cover they needed to sign multi-year contracts with an Indian vendor.

The real momentum came from a string of multi-million dollar European contracts in 2012. One deal alone was worth €20 million over three years—validation that Hexaware could compete with European incumbents on their home turf. In 2012 Hexaware Technologies bagged a multi-million-dollar multi-year contract in the financial sector domain in Europe, proving their strategy of patient relationship building was paying dividends.

In 2013, the company started its Global Delivery Center in Texas, USA and in the same year, a new center was opened in Singapore. These weren't just delivery centers—they were strategic outposts designed to blur the line between offshore and onshore delivery. The Texas center, in particular, was positioned to serve the energy sector, where data residency requirements and real-time processing needs made pure offshore models impossible.

By 2013, Hexaware had evolved into something unique in the Indian IT services landscape: not the biggest, not the flashiest, but arguably the most consistent. Revenue had grown from $45 million in 1999 to over $400 million. The company served 200+ clients across 30 countries. But more importantly, it had survived and thrived through multiple cycles—Y2K boom and bust, dot-com crash, 2008 financial crisis—without ever posting a loss or missing guidance.

This track record made Hexaware irresistible to a particular type of buyer: private equity firms looking for steady, predictable businesses they could optimize and flip. As 2013 drew to a close, founder Atul Nishar, now in his 60s, was ready to cash out. The stage was set for Hexaware's transformation from family-run public company to private equity portfolio asset.

V. The First PE Chapter: Baring Asia Takes Control (2013-2021)

The boardroom at the Trident hotel in Mumbai was tense on that October morning in 2013. Atul Nishar, after building Hexaware for over two decades, was about to sign away control to Baring Private Equity Asia. The price: approximately $420 million (₹1,687 crore) for a 74% stake, valuing the company at around $570 million. General Atlantic, which had invested $67.6 million in 2008, was also exiting with a handsome return. But this wasn't just a financial transaction—it was a bet that private equity could do what public markets couldn't: transform a mid-tier Indian IT services firm into a global digital powerhouse.

Baring Asia wasn't a typical private equity firm. With over $10 billion under management focused exclusively on Asia, they had a playbook specifically designed for Asian services companies: inject capital, professionalize management, accelerate digital capabilities, and prepare for a strategic exit. Their partner leading the deal, Rahul Bhasin, had seen this movie before with investments in healthcare and financial services. "Hexaware has all the ingredients," he told his investment committee, "except the recipe."

The first order of business was leadership. In 2014, Baring brought in R Srikrishna as CEO, poaching him from HCL Technologies where he had built their infrastructure services business from scratch to $2 billion. Srikrishna was known for two things: operational discipline and an ability to sell complex deals to CXOs. His mandate was clear: take Hexaware from being a vendor to becoming a partner.

The transformation under Srikrishna was methodical. First, he restructured the company around industry verticals rather than service lines. Instead of having separate teams for testing, development, and maintenance, Hexaware would have integrated teams focused on banking, insurance, healthcare, and travel. Each vertical head was given P&L responsibility and the authority to make investment decisions. The message was clear: stop thinking like technologists, start thinking like business consultants.

Second came the digital pivot. While public company Hexaware had dabbled in digital services, PE-owned Hexaware went all-in. Between 2014 and 2019, Baring invested over $100 million in building digital capabilities—hiring data scientists, acquiring automation tools, developing proprietary platforms. The crown jewel was Tensai®, an automation platform that could reduce manual testing effort by 40%. Another key innovation was Amaze®, a proprietary tool for application modernization that became a differentiator in winning large transformation deals.

The client portfolio transformation was equally dramatic. When Baring took over, Hexaware's top 10 clients contributed 35% of revenue—a dangerous concentration. By 2019, that figure was down to 22%, even as absolute revenue from these clients grew. The company added 50+ new Fortune 500 logos, including several $100 million+ accounts. The secret? Instead of competing on price, Hexaware competed on business outcomes. "We stopped selling man-hours and started selling business impact," Srikrishna would later explain.

The numbers validated the strategy. Revenue grew from $420 million in 2013 to $845 million in 2020—a CAGR of over 10% during a period when the industry average was 6-7%. More impressively, EBITDA margins expanded from 14% to 18%, despite increasing investment in digital capabilities. Employee count grew from 11,000 to over 20,000, with the mix shifting dramatically toward high-skill roles. By 2020, over 30% of Hexaware's workforce was trained in digital technologies, up from less than 5% in 2013.

But the masterstroke came in November 2020. With public markets frothy and tech valuations soaring, Baring decided to delist Hexaware from the Indian stock exchanges. The delisting offer at ₹475 per share valued the company at approximately $950 million—more than double what Baring had paid seven years earlier. Small shareholders protested, claiming the price was too low, but Baring pressed ahead. They knew something the market didn't: multiple strategic buyers were already circling, and the auction for Hexaware was about to begin.

The timing was exquisite. COVID-19 had accelerated digital transformation by a decade. Every company suddenly needed cloud migration, automation, and digital customer interfaces. IT services firms were seeing unprecedented demand. And Hexaware, with its digital-first positioning and proven execution track record, was perfectly positioned to capitalize. By early 2021, Baring had hired Barclays and JP Morgan to run a sale process. The message to potential buyers was simple: "Hexaware is the last scaled, independent, digital-ready IT services asset available. Who wants it?"

VI. The Carlyle Acquisition: India's Second-Largest PE Deal (2021)

The virtual data room opened in April 2021, and within days, it was clear this would be one of the most competitive auctions in Indian private equity history. The teaser document painted a compelling picture: $845 million in revenue, 18% EBITDA margins, 200+ enterprise clients, and a digital services mix approaching 40%. But what really caught buyers' attention was the growth trajectory—Hexaware was adding $100 million in new revenue annually, with line of sight to becoming a billion-dollar company.

The usual suspects lined up immediately. KKR, fresh off their success with First Data, saw Hexaware as a platform to consolidate mid-tier IT services firms. Bain Capital, which had made a fortune with Genpact, loved the margin expansion opportunity. Teleperformance, the French business services giant, viewed Hexaware as their entry ticket into high-end IT services. Each brought different synergy stories and valuation models to the table.

But it was Carlyle that came with the most compelling vision. The Washington-based firm, managing over $370 billion globally, had been studying the Indian IT services sector for years. Their thesis was contrarian: while everyone else saw commoditization, Carlyle saw specialization. They believed that mid-tier firms like Hexaware could actually gain share from larger players by being more agile and focused. Their operating partner, former Cognizant executive Malcolm Frank, had written the playbook: "In the age of digital, being a $1 billion specialist beats being a $10 billion generalist."

The bidding war was intense. Initial bids in May ranged from $2.5 to $2.8 billion. Baring pushed for a second round, hoping to breach the $3 billion mark—which would make this India's second-largest PE buyout ever, behind only Flipkart. Carlyle's deal team, led by Shankar Narayanan, made a strategic decision: instead of nickel-and-diming, they would make a preemptive offer that would blow others out of the water.

In August 2021, Carlyle emerged victorious with a $3 billion bid—a valuation of roughly 3.5x revenue and 20x EBITDA. The deal structure was notable: it was a cross-platform investment involving both Carlyle Partners VII (their flagship buyout fund) and Carlyle Asia Partners V (their Asia-focused fund). This gave them maximum flexibility for follow-on investments and eventual exit options. The message to the market was clear: Carlyle wasn't just buying Hexaware; they were betting on the future of Indian IT services.

The investment thesis went beyond financial engineering. Carlyle saw three major value creation levers. First, geographic expansion—Hexaware was under-penetrated in Continental Europe and Asia-Pacific, markets growing faster than the traditional US/UK markets. Second, capability building through acquisitions—the mid-tier IT services space was ripe for consolidation, and Hexaware could be the platform. Third, and most ambitiously, positioning for the AI revolution—Carlyle believed that generative AI would create a new S-curve of growth, and nimble players like Hexaware could capture disproportionate value.

Carlyle also brought something Baring couldn't: global connectivity. With portfolio companies across industries and geographies, Carlyle could open doors that would take years for Hexaware to access independently. Within months of closing, Hexaware had signed master service agreements with three other Carlyle portfolio companies, deals worth a combined $50 million annually.

The management team, led by R Srikrishna, was retained with enhanced incentives tied to growth and eventual exit valuations. This continuity was crucial—clients and employees needed reassurance that Hexaware wouldn't be stripped for parts. Carlyle's message was consistent: "We're not here to cut costs; we're here to accelerate growth."

VII. The Carlyle Era & Path to IPO (2021-2025)

Carlyle's ownership began with what they called the "100-day sprint"—a comprehensive review of every aspect of Hexaware's business. The findings were encouraging but highlighted gaps. While Hexaware had strong capabilities in application development and maintenance, it was subscale in cloud services and data analytics—the fastest-growing segments. Customer concentration had improved but was still high, with the top 20 clients contributing over 50% of revenue. And while margins were healthy, there was room for improvement through automation and offshoring of delivery.

The value creation plan that emerged was ambitious yet pragmatic. Revenue would grow from $845 million to $1.5 billion by 2025—implying a 15% CAGR, double the industry average. This would come from three sources: organic growth in existing accounts ($200 million), new logo acquisition ($200 million), and strategic acquisitions ($200 million). Margins would expand by 200 basis points through automation and improved utilization. The combined effect would triple EBITDA from $150 million to $450 million.

Execution began immediately. In 2022, Hexaware launched Hexaware.ai, a dedicated unit focused on artificial intelligence and machine learning solutions. Unlike generic AI offerings, these were industry-specific solutions: fraud detection for banks, claims processing for insurers, predictive maintenance for manufacturers. The unit grew from 0 to $50 million in revenue within 18 months.

The geographic expansion was equally aggressive. Hexaware established innovation centers in Berlin, Tokyo, and Sydney—not just sales offices but actual delivery centers with local talent. The Germany center, in particular, became a hub for serving the DACH region's mid-market companies, a segment traditionally underserved by Indian IT firms. By 2024, Continental Europe contributed 25% of revenue, up from 15% in 2021.The acquisition strategy crystallized in July 2025 with the $120 million acquisition of SMC Squared, involving a $45 million upfront payout, up to $45 million in earnouts, and up to $30 million as an outperformance bonus. This wasn't just another tuck-in acquisition—it was a strategic bet on the Global Capability Center (GCC) market. The number of companies with GCCs in India has more than doubled from approximately 700 in 2010 to over 1,760 in 2024, generating revenue of $65 billion and employing 1.9 million professionals. By FY2030, the GCC landscape is expected to generate $99–105 billion in annual revenue.

SMC Squared brought something unique: 20 years of experience building captive centers, starting with Target, and deep relationships with Fortune 500 companies. As CEO R Srikrishna explained, "improving growth in India and the Middle East is important. And India, for us, really kind of strategy one, two, three is GCCs". The acquisition positioned Hexaware to compete not just as a services vendor but as a partner that could help companies build and operate their own offshore centers—a much stickier, higher-margin business.

Financial performance during the Carlyle era validated the aggressive growth strategy. In the first quarter of 2025, the Mumbai-based company reported revenue of $371.5 million, up 12.4% YoY. Margin expansion of 117 basis points year-over-year demonstrated that growth wasn't coming at the expense of profitability. The company had successfully navigated the post-pandemic normalization, the tech spending slowdown of 2023, and emerged stronger.

But perhaps the most impressive achievement was cultural. Despite changing hands twice in eight years, Hexaware maintained remarkably low attrition rates—15% annually versus the industry average of 20-25%. The secret was Carlyle's hands-off approach to day-to-day operations while being deeply involved in strategic decisions. Town halls were conducted jointly by Carlyle partners and Hexaware management. Investment decisions were made in days, not months. The message to employees was consistent: "You're not working for a PE firm; you're building the next great IT services company."

By late 2024, with revenue approaching $1.5 billion and EBITDA margins touching 20%, Carlyle knew it was time to harvest. The IPO window was open, tech valuations were recovering, and there was genuine scarcity value in independent, scaled IT services firms. The stage was set for Hexaware's return to public markets—not as the company it was when it left, but as something far more valuable.

VIII. The Historic IPO (February 2025)

The morning of February 19, 2025, saw unprecedented scenes at the National Stock Exchange. The Hexaware IPO, priced at ₹880 per share, was oversubscribed 74 times—institutional investors bid for 105 times their allocation, while retail investors clamored for 42 times theirs. By the closing bell, the stock had touched ₹900, giving Hexaware a market capitalization of ₹43,008 crore. This wasn't just an IPO; it was a coronation of Carlyle's value creation playbook and validation of the Indian IT services story in the age of AI.

The IPO raised approximately $1 billion, making it the largest technology services IPO globally in over a decade and the largest sponsor-owned IPO in India's history. The offering was structured as a combination of fresh issue and offer for sale, with Carlyle retaining a 20% stake—signaling continued confidence in the growth story. The fresh capital would fund acquisitions, AI investments, and geographic expansion.

What made this IPO particularly remarkable was the investor base. Unlike typical Indian tech IPOs dominated by domestic mutual funds, Hexaware attracted tier-one global investors: Fidelity, Capital Group, GIC of Singapore, and Norway's sovereign wealth fund all took anchor positions. Their thesis was uniform: in an AI-disrupted world, execution capabilities matter more than ever, and Hexaware had proven it could execute.

The roadshow presentations revealed fascinating insights into Hexaware's transformation. Digital services now comprised 60% of revenue, up from 25% in 2013. The company served 45 of the Fortune 500, with average client relationships spanning 8+ years. Customer concentration had improved dramatically—the top client contributed just 6% of revenue, down from 15% a decade ago. Perhaps most impressively, revenue per employee had grown from $42,000 in 2013 to $58,000 in 2024, even as the employee base nearly tripled.

The valuation metrics sparked debate among analysts. At 33x trailing P/E, Hexaware was trading at a premium to larger peers like Infosys (28x) and Wipro (25x). Bulls argued this was justified given Hexaware's superior growth trajectory and margin profile. Bears worried about macro headwinds and the threat from GCCs. The consensus view: Hexaware deserved a "growth premium" but would need to deliver consistent execution to maintain these multiples.

The IPO's success had broader implications for the Indian IT services sector. It proved that the public markets were willing to pay premium valuations for well-run, focused IT services firms—contradicting the narrative that the sector was permanently impaired by commoditization. It also validated the private equity model in IT services: buy at reasonable valuations, transform operations, and exit at premium multiples. Within weeks of Hexaware's IPO, rumors swirled about other PE-owned IT firms preparing for public offerings.

For Carlyle, the IPO represented a spectacular return. Having invested $3 billion in 2021, their stake was now worth approximately $4.5 billion at IPO pricing—a 50% gain in less than four years, not including dividends received during ownership. More importantly, by retaining a 20% stake, Carlyle positioned itself to benefit from continued upside while gradually reducing exposure over time.

Management's commentary during the IPO was cautiously optimistic. CEO R Srikrishna emphasized three priorities: maintaining growth momentum, expanding margins through automation, and strategic M&A. "Going public again gives us currency for acquisitions and the credibility to win large deals. But it also means delivering quarter after quarter. We're ready for that responsibility."

The first day of trading ended with Hexaware among the top 100 companies by market cap on the NSE. Employees who had received stock options during the private years suddenly found themselves with substantial wealth. The Hexaware story had come full circle—from public to private and back to public—but at a valuation 10x higher than when it first delisted.

IX. Business Model & Competitive Positioning

Understanding Hexaware's business model requires appreciating the delicate balance between scale and specialization that defines successful mid-tier IT services firms. Unlike the giants (TCS, Infosys) that compete on breadth, or the boutiques that compete on depth, Hexaware occupies the sweet spot: large enough to handle enterprise-wide transformations, focused enough to deliver specialized expertise.

The service portfolio is organized around six key segments. Travel & Transportation contributes 18% of revenue, leveraging deep domain expertise in airline reservation systems and logistics platforms. Financial Services (22%) focuses on capital markets and wealth management rather than retail banking where larger players dominate. Banking (15%) specializes in mortgage processing and trade finance—complex, regulation-heavy areas where domain expertise commands premium pricing. Healthcare & Insurance (20%) has built proprietary platforms for claims processing that reduce adjudication time by 40%. Manufacturing (12%) focuses on supply chain digitization and IoT implementations. The remaining 13% comes from emerging verticals like retail and utilities.

What sets Hexaware apart is the platform-led delivery model. Rather than deploying armies of programmers, Hexaware has built proprietary platforms that automate routine work. Tensai®, their automation platform, handles 40% of testing activities that previously required manual intervention. Amaze®, for application modernization, can analyze legacy code and automatically generate cloud-native microservices—reducing modernization time from years to months. These platforms aren't just productivity tools; they're competitive moats that justify premium pricing.

The geographic delivery model has evolved significantly. While 65% of delivery still happens from India (Mumbai, Chennai, Bangalore, Pune), Hexaware has built substantial near-shore capabilities. The Mexico center serves US clients requiring Spanish language support and similar time zones. The Eastern Europe centers serve GDPR-conscious European clients. The Singapore hub acts as the gateway to Asia-Pacific. This distributed model allows Hexaware to offer "right-shore" delivery—optimizing between cost, capability, and client preferences.

Scale metrics tell the story of a company punching above its weight. With 32,310 employees, Hexaware is one-tenth the size of TCS but generates revenue per employee comparable to firms twice its size. The company maintains a 3:1 offshore-to-onshore ratio, optimizing between cost efficiency and client proximity. Utilization rates consistently exceed 80%, well above the industry average of 75%. More importantly, the employee pyramid is inverting—senior consultants and architects now comprise 30% of the workforce, up from 15% a decade ago.

The competitive landscape presents both challenges and opportunities. The Indian IT services sector is brutally competitive, with over 4,000 firms vying for share. At the top, TCS, Infosys, Wipro, and HCL command 40% market share with their scale advantages. At the bottom, thousands of small firms compete on price. In the middle, where Hexaware operates alongside peers like Mindtree, Persistent, and Zensar, differentiation is crucial.

Hexaware's differentiation strategy rests on three pillars. First, vertical depth—knowing more about airline reservation systems or mortgage processing than competitors. Second, automation-led delivery—using platforms to deliver outcomes faster and cheaper. Third, and perhaps most importantly, cultural differentiation—being easier to work with than larger firms, more responsive, more flexible. As one Fortune 500 CIO noted, "With TCS, I'm account number 2,847. With Hexaware, I have the CEO's mobile number."

The threat from GCCs (Global Capability Centers) is real but manageable. Many Western corporations are setting up their own offshore centers, theoretically reducing demand for third-party services. But Hexaware has turned this threat into opportunity through its GCC 2.0 offering—helping companies build and operate their own centers. It's a brilliant judo move: if clients want to in-source, help them do it better.

Pricing power remains a challenge across the industry, but Hexaware has managed better than most. While commodity services like application maintenance see constant price pressure, specialized services command premiums. Hexaware's revenue mix has shifted accordingly—60% now comes from digital services priced at $100+ per hour, versus traditional services at $30-50 per hour. The company has also moved aggressively toward outcome-based pricing, where they're paid for business results rather than time and materials.

X. Playbook: Lessons from Three Ownership Eras

The Hexaware journey offers a masterclass in how ownership structure shapes strategy, culture, and outcomes. Each era—founder-led, Baring-owned, Carlyle-controlled—brought distinct approaches to value creation, and understanding these differences is crucial for investors and operators alike.

The founder era (1990-2013) was about building credibility and scale. Atul Nishar's approach was patient, relationship-driven, and conservative. Debt was avoided, growth was organic, and client relationships were sacred. The motto was simple: "Under-promise, over-deliver." This built a foundation of trust that would prove invaluable through ownership transitions. But it also meant missed opportunities—Hexaware grew steadily but never explosively, content to be profitable rather than dominant.

When Baring took control in 2013, they brought the discipline of professional management. The first insight: Hexaware was under-managed. There were no formal account plans, no systematic approach to cross-selling, no rigorous performance management. Baring installed processes without destroying culture—a delicate balance. They introduced KPIs for everything: deal velocity, margin by project, utilization by skill. But they also preserved what worked: the client-first mentality, the collaborative culture, the focus on execution.

Baring's biggest contribution was the digital pivot. When they bought Hexaware, "digital" meant having a website. By the time they sold, digital services were 40% of revenue. This wasn't luck—it was systematic capability building. Every year, 20% of revenues were reinvested in training, tools, and talent acquisition. Engineers were sent to cloud certification programs. Data scientists were hired from IITs. Partnerships were forged with Microsoft, Amazon, and Google. The transformation was expensive—margins dipped initially—but it positioned Hexaware perfectly for the cloud migration wave.

The Carlyle era brought a different playbook: growth through strategic initiatives. Where Baring focused on operational excellence, Carlyle focused on strategic positioning. The SMC Squared acquisition wasn't just about adding revenue; it was about entering the GCC market before competitors realized its potential. The AI investments weren't just about having cutting-edge capabilities; they were about positioning for the next S-curve of growth.

Carlyle also understood the power of narrative. Under their ownership, Hexaware wasn't just an IT services firm; it was a "digital transformation partner." The company didn't just have employees; it had "digital warriors." This wasn't empty marketing—it reflected a genuine shift in positioning that resonated with clients and investors alike.

The art of timing exits and entries deserves special attention. Nishar sold when founder fatigue set in and professional management could add value. Baring sold when digital transformation was complete and growth acceleration required different skills. Carlyle is partially exiting through the IPO while retaining upside exposure. Each transition was timed to maximize value for sellers while creating opportunity for buyers.

Managing talent through ownership transitions is perhaps the hardest challenge. Employees naturally fear change—new owners might cut costs, change culture, or redirect strategy. Hexaware's approach was transparency and consistency. During each transition, management held town halls explaining the rationale, introduced new owners personally, and guaranteed cultural continuity. Key talent was retained through enhanced stock options tied to new ownership. The message was consistent: ownership might change, but values remain constant.

Capital allocation in a services business presents unique challenges. Unlike product companies that can invest in R&D for future returns, services firms must balance immediate talent needs with long-term capability building. Hexaware's approach evolved with ownership. Under Nishar, capital went primarily to infrastructure—buildings, data centers. Under Baring, it shifted to capability—training, tools, certifications. Under Carlyle, it focused on strategic assets—acquisitions, platforms, IP development.

The role of debt also evolved. The founder era was debt-free, reflecting conservative Indian business culture. Baring introduced modest leverage to fund growth investments. Carlyle used sophisticated capital structures to optimize returns. Each approach was appropriate for its time and circumstance.

What emerges from these three eras is a playbook for services firm transformation: Build trust and scale under founder leadership, professionalize operations under first institutional capital, accelerate growth under growth-oriented capital, and return to public markets when the transformation is complete. It's a template that other Indian IT firms are now following.

XI. Analysis & Investment Thesis

The bull case for Hexaware rests on structural tailwinds that seem almost too good to be true. Global IT services spending is projected to reach $5 trillion by 2030, growing at 8% annually. Within this, digital services—Hexaware's sweet spot—are growing at 15% annually. The rise of generative AI, rather than destroying IT services, is creating new implementation and integration opportunities. Every enterprise needs help navigating the AI transformation, and Hexaware is positioned as the trusted guide.

The company's AI-first positioning is particularly compelling. While larger firms struggle to cannibalize their legacy revenues, Hexaware has embraced automation aggressively. The Tensai® platform doesn't just improve margins; it allows Hexaware to bid for projects competitors can't execute profitably. The company has delivered a 14.0% CAGR during CY20–24, with revenue of $371.5 million in Q1 2025, up 12.4% YoY—growth rates that suggest the strategy is working.

Geographic diversification provides another growth vector. Over 74% of business comes from the Americas followed by 20% from Europe and just 6% from India. The underpenetration in high-growth markets like India and Asia-Pacific represents untapped potential. The GCC 2.0 strategy specifically targets the Indian market, where Western multinationals are rapidly expanding their offshore centers.

The bear case, however, is equally compelling. Macro headwinds are intensifying—enterprise IT budgets are under pressure, interest rates remain elevated, and recession fears persist. Every earnings call features the same question: "When will demand recover?" Management's consistently cautious guidance suggests they don't have clear visibility either.

Client consolidation poses a structural threat. As enterprises rationalize vendor relationships, they're consolidating spend with fewer, larger partners. This theoretically benefits giants like TCS and Accenture at the expense of mid-tier firms. While Hexaware has so far navigated this trend successfully, the pressure is relentless. Losing even one major client could impact revenues by 5-6%.

The GCC threat is evolving from theoretical to actual. Cognizant flagged the potential risks stemming from GCCs operated by its clients, and every major IT firm is scrambling to address this challenge. While Hexaware's GCC 2.0 strategy is clever, it's essentially accepting lower margins to maintain client relationships. The long-term economics of helping clients in-source your own services remain questionable.

Valuation dynamics post-IPO add another layer of complexity. At 33x P/E, Hexaware trades at a premium to peers despite being smaller and potentially more vulnerable. The market is pricing in perfect execution—any earnings miss or guidance cut could trigger a violent re-rating. The presence of Carlyle as a 20% shareholder provides some stability, but also creates overhang risk when they eventually exit.

Management's outlook reflects these crosscurrents. CEO R Srikrishna strikes a cautiously optimistic tone, emphasizing the "quality of growth" over quantity. The focus on financial services—traditionally Hexaware's strongest vertical—suggests a flight to safety rather than aggressive expansion. Guidance for 12-14% revenue growth and stable margins feels achievable but uninspiring.

The investment thesis ultimately depends on time horizon and risk appetite. For short-term traders, Hexaware offers volatility around quarterly earnings and sector rotation. For long-term investors, it's a play on India's continued emergence as the world's technology services hub. The company's proven ability to transform under different ownership structures suggests resilience and adaptability.

What would make Hexaware a compelling buy? A valuation correction to 25x P/E would create attractive entry points. Evidence of AI-led revenue acceleration would validate the transformation story. Strategic acquisitions that meaningfully expand capabilities or market access would justify premium valuations. Conversely, warning signs would include client losses, margin compression from wage inflation, or inability to scale the GCC business profitably.

The broader implications for Indian IT services M&A are significant. Hexaware's successful round-trip from public to private and back demonstrates that financial engineering can create value in supposedly commoditized industries. Expect more PE firms to hunt for under-managed IT services assets. Also expect more strategic consolidation as subscale players struggle to invest in AI and cloud capabilities.

XII. Epilogue & Looking Forward

As Hexaware enters its second incarnation as a public company, the challenges ahead are fundamentally different from those of the past. The company that once fought for credibility now must defend its premium valuation. The firm that built its reputation on reliable execution must now become an innovation leader. The organization that thrived under private ownership must now satisfy quarterly earnings expectations.

The AI revolution presents both the greatest opportunity and existential threat. Generative AI could automate 40% of current IT services work within five years. For companies slow to adapt, this means margin compression and revenue decline. But for those who embrace it, like Hexaware claims to be doing, it means the ability to deliver more value with fewer resources. The company's Tensai® platform is a bet that augmentation beats replacement—that AI-empowered humans deliver better outcomes than AI alone.

The next chapter will likely involve strategic choices about focus versus diversification. Should Hexaware double down on its six core verticals or expand into new industries? Should it remain a pure services player or build product offerings? Should it maintain independence or seek strategic combination with peers? These aren't just strategic questions—they're existential ones that will determine whether Hexaware remains relevant in 2030.

If I were running Hexaware today, three priorities would dominate. First, accelerate the platform strategy—every service should have a platform component that creates switching costs and pricing power. Second, build an AI-native workforce—not just training existing employees but hiring digital natives who think in algorithms and APIs. Third, consider bold M&A—acquiring a product company or SaaS player that transforms Hexaware from services to solutions.

The lessons for founders considering PE partnerships are nuanced. Private equity isn't just capital—it's a transformation catalyst that brings discipline, connections, and credibility. But it also means giving up control, accepting aggressive timelines, and potentially sacrificing long-term vision for medium-term returns. The Hexaware story suggests the trade-offs can be worthwhile if alignment exists on value creation strategy.

For investors, Hexaware represents a fascinating case study in value creation through ownership transitions. The company's enterprise value has grown from ~$570 million in 2013 to over $5 billion today—a 9x increase that outperformed the broader market significantly. This wasn't financial engineering alone—real operational improvements, capability building, and strategic repositioning created genuine value.

Looking ahead, the Indian IT services sector faces an inflection point. The labor arbitrage that drove growth for three decades is diminishing. Automation is eliminating routine work. Clients are getting smarter about vendor management. In this environment, only companies that continuously reinvent themselves will thrive. Hexaware's journey from Mumbai startup to PE unicorn to public market darling suggests it has the DNA for reinvention.

The final lesson might be the most important: in services businesses, culture eats strategy for breakfast. Through three ownership changes, multiple strategic pivots, and countless market cycles, Hexaware maintained its core identity as a client-first, execution-focused, relationship-driven organization. The platforms, processes, and strategies were just enablers. The real asset was always the 32,000+ Hexawarians who wake up every day committed to client success.

As the story continues to unfold, Hexaware stands as testament to Indian entrepreneurship, private equity value creation, and the enduring importance of IT services in our digital age. Whether it becomes a $10 billion giant or gets acquired by a larger player, its journey from Aptech spin-off to global IT services leader has already secured its place in Indian business history.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube