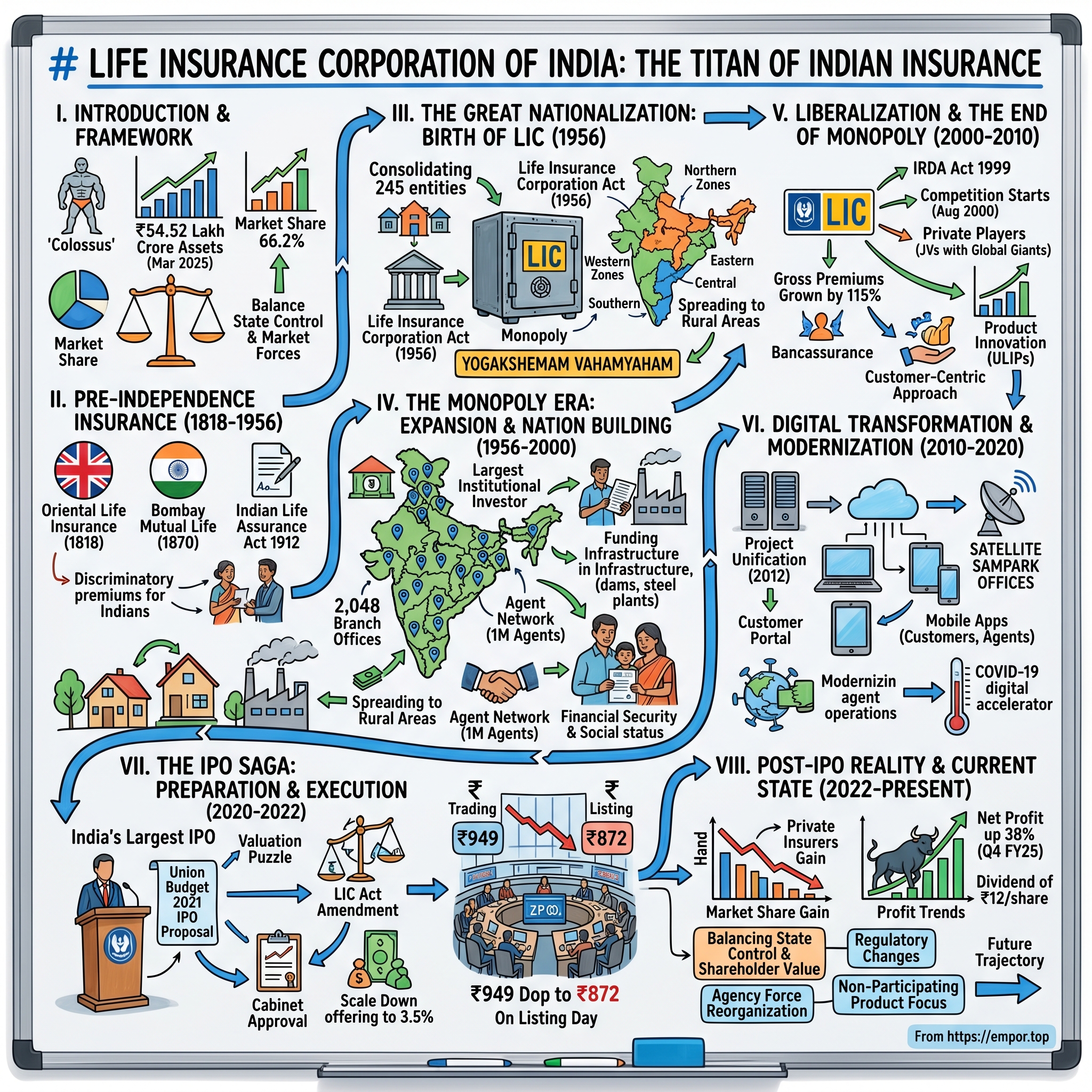

Life Insurance Corporation of India: The Titan of Indian Insurance

I. Introduction & Episode Framework

Life Insurance Corporation of India stands as a colossus in the global insurance landscape, managing assets worth ₹54.52 lakh crore (US$640 billion) as of March 2025—a figure that surpasses the GDP of many nations. With a commanding 66.2% market share in new business premium, LIC isn't just India's largest insurance company; it's a financial institution so deeply woven into the fabric of Indian society that for millions of citizens, the words "life insurance" and "LIC" are synonymous.

The story of how a government-created monopoly rose to become the 98th company on the 2022 Fortune Global 500 list is a tale of nation-building, market dominance, and adaptation. It's a narrative that spans from the socialist ideals of post-independence India to the cutthroat competition of modern capital markets. This is the story of an institution that has insured the dreams of three generations of Indians, survived the end of its monopoly, and emerged as a publicly traded company in one of the most watched IPOs in Indian market history.

To understand LIC is to understand modern India itself—its economic evolution, its middle-class aspirations, and the delicate balance between state control and market forces. This institution has been the government's Swiss Army knife: a tool for rural development, a stabilizer of markets, a funder of infrastructure, and above all, the primary savings vehicle for hundreds of millions of Indians. From the chai-wallah in Mumbai to the software engineer in Bangalore, from the farmer in Punjab to the teacher in Kerala, LIC policies have been passed down through families like heirlooms, each policy number a testament to dreams deferred and futures secured.

The central question that drives this analysis is deceptively simple yet profoundly complex: How did an organization born from the nationalization of 245 private insurers in 1956 not only survive but thrive through India's economic liberalization, the entry of aggressive private competitors, and the digital revolution? The answer lies in understanding LIC not just as an insurance company, but as a social institution that has masterfully balanced its commercial objectives with its nation-building mandate.

Our journey begins in colonial India, where the seeds of the insurance industry were first planted, travels through the heady days of nationalization when Prime Minister Nehru's government consolidated the fragmented insurance market, explores the monopoly era when LIC became synonymous with financial security for middle-class India, examines the challenges of liberalization when private players entered the market, and culminates in the dramatic IPO of 2022 that transformed this government behemoth into a publicly traded entity accountable to millions of shareholders.

This is more than a business story—it's a chronicle of how a single institution shaped and was shaped by the economic destiny of the world's most populous nation. It's about the delicate dance between socialist ideals and capitalist realities, between serving the masses and generating returns, between preserving legacy and embracing innovation. As we unpack the LIC story, we'll discover not just how insurance works in India, but how India itself works.

The roadmap ahead takes us from the early insurance pioneers of the 1800s to the digital battlegrounds of today, from the villages where LIC agents became trusted advisors to the glass towers where investment decisions worth billions are made. We'll examine how LIC built an army of 1.3 million agents, why its policies became the preferred dowry in Indian marriages, how it survived the onslaught of nimble private competitors, and what its future holds in an increasingly digital and competitive landscape.

II. Pre-Independence Insurance & The Roots (1818-1956)

The story of life insurance in India begins not with Indians insuring Indian lives, but with the British insuring British lives on Indian soil. The Oriental Life Insurance Company, established in Kolkata in 1818, marked the genesis of the life insurance industry in India. This Calcutta-based company, however, was designed exclusively for the European community—a financial apartheid that would characterize the early decades of Indian insurance. The company's founding in the then-capital of British India was no coincidence; it served the growing community of British administrators, merchants, and military officers who needed financial protection in what they considered a hostile and disease-prone environment.

The discriminatory practices of early insurance companies weren't merely social prejudices; they were built into the actuarial models themselves. Indian lives were either refused coverage entirely or charged premiums that were 15-20% higher than their European counterparts, based on the spurious logic of higher mortality risk. This systematic exclusion would plant the seeds of resentment that would later fuel the nationalist movement's demand for indigenous insurance companies.

The year 1870 marked a watershed moment with the establishment of the Bombay Mutual Life Assurance Society, the first life insurance company founded by Indians, for Indians. Started by a group of Parsi and Hindu merchants in Bombay, this company represented more than just a business venture—it was an act of economic nationalism. The founders, led by pioneering businessmen like Nowrojee Furdoonjee and others, explicitly positioned the company as a response to the discriminatory practices of British insurers. Their prospectus boldly declared that the company would offer "life assurance to Indian lives at the same rates as European lives," a revolutionary concept for its time.

The success of Bombay Mutual Life Assurance Society triggered a wave of indigenous insurance companies. By the turn of the century, companies like the Oriental Government Security Life Assurance Company (1874), Bharat Insurance Company (1896), and Empire of India Life Assurance Company (1897) had emerged. Each new company represented not just entrepreneurial ambition but a growing assertion of Indian economic capability. These companies became symbols of swadeshi (self-reliance), with their agents often doubling as nationalist sympathizers who sold insurance policies alongside ideas of economic independence.

The Indian Life Assurance Companies Act of 1912 marked the colonial government's first serious attempt to regulate the burgeoning insurance industry. This legislation, while ostensibly aimed at protecting policyholders, also served to formalize the industry and bring it under government scrutiny. The Act mandated that companies maintain reserves, submit returns, and undergo periodic valuations—requirements that would inadvertently prepare the ground for the sector's eventual nationalization. Interestingly, the Act also legally ended the practice of charging differential premiums based on race, though informal discrimination continued through other means.

By the 1920s and 1930s, the insurance industry had become a battleground for economic nationalism. The Swadeshi movement actively promoted Indian insurance companies, with leaders like Lala Lajpat Rai establishing companies like the National Insurance Company. Gandhi himself, while personally skeptical of insurance as a concept (believing it showed lack of faith in God), recognized its importance for the Indian middle class and endorsed Indian companies over foreign ones. The period saw intense competition, with Indian companies using nationalist rhetoric in their marketing—"Insure with us and serve the motherland" was a common refrain.

The proliferation of insurance companies, however, came with its own challenges. By the 1940s, the Indian insurance landscape had become a chaotic marketplace of about 154 Indian insurers, 16 non-Indian companies, and 75 provident societies. Many of these companies were undercapitalized, poorly managed, and engaged in speculative investments. The failure rate was alarming—between 1935 and 1945, over 25 insurance companies collapsed, wiping out the savings of thousands of policyholders. These failures weren't just business casualties; they represented broken promises to families who had entrusted their future security to these institutions.

The Insurance Act of 1938 attempted to address these systemic issues by introducing stricter capital requirements, investment regulations, and government oversight. The Act created the position of Controller of Insurance and mandated that companies invest a certain percentage of their funds in government securities. While these measures brought some stability, they couldn't address the fundamental problem: the industry was too fragmented, with too many weak players competing for too small a market. The average Indian still viewed insurance with suspicion, seeing it either as gambling or as a luxury only the wealthy could afford.

World War II paradoxically boosted the insurance industry. The uncertainties of war, combined with inflation and the growth of the salaried middle class in government and military service, created new demand for life insurance. Companies reported record growth during the war years, with premium collections increasing by over 300% between 1939 and 1945. This growth, however, was unevenly distributed, concentrated mainly in urban areas and among the educated elite. Rural India, representing 85% of the population, remained largely uninsured.

The post-independence period brought a fundamental shift in how insurance was viewed. No longer was it merely a financial product; it became a tool for nation-building. The new government, led by Prime Minister Jawaharlal Nehru, saw insurance as a means to mobilize savings for planned economic development. The First Five Year Plan (1951-1956) explicitly identified insurance as a priority sector that could channel household savings into productive investments. This philosophical shift from insurance as private protection to insurance as public resource would set the stage for nationalization.

The demand for nationalizing the life insurance industry had been percolating since 1944, when the issue was first seriously raised in political circles. The arguments were compelling: private insurers were failing to expand coverage to rural areas, many companies were financially unstable, there were widespread allegations of malpractice including misuse of funds and excessive commission payments, and the fragmented industry couldn't mobilize resources for national development. The failure of major insurers like the Hindustan Co-operative Insurance Company in 1950 and the Indian Mercantile Insurance Company in 1952 added urgency to these demands.

By 1955, the die was cast. Finance Minister C.D. Deshmukh announced in Parliament that the government was considering nationalization, triggering fierce debate. Private insurers argued that nationalization would stifle innovation and efficiency, while proponents countered that only a state-backed institution could provide the trust and reach needed to make insurance truly universal. The debate wasn't just economic but ideological, representing the larger question of the state's role in independent India's economy.

The fragmented market on the eve of nationalization presented a complex picture. The 245 entities operating in the life insurance space ranged from well-established companies with decades of history to fly-by-night operators with dubious credentials. Combined, they had about 55 lakh policies in force, covering less than 1% of India's population. Premium income totaled about ₹150 crores annually, with assets of approximately ₹400 crores. These numbers, while respectable, fell far short of what planners believed was needed to support India's ambitious development goals.

The stage was thus set for one of the most dramatic consolidations in business history. The chaos of the fragmented market, the failures that had eroded public trust, the nationalist imperative for self-reliance, and the socialist vision of insurance as a tool for development all converged to make nationalization not just possible but seemingly inevitable. On January 19, 1956, the government made the momentous announcement that would transform Indian insurance forever.

The decision to nationalize wasn't taken lightly. Behind closed doors, fierce debates raged about implementation, compensation, and structure. Some argued for gradual nationalization, others for immediate takeover. Some wanted regional corporations, others a single national entity. The blueprint that emerged—a single corporation with zonal structures—represented a compromise between centralized control and regional flexibility. This structure would prove remarkably durable, surviving essentially unchanged for decades.

The human dimension of this transition often gets lost in the macro narrative. For the thousands of employees of private insurance companies, nationalization brought both uncertainty and opportunity. Many senior executives of private companies found themselves suddenly reporting to government appointees. Agents wondered if their relationships with clients would survive the transition. Policyholders worried about the safety of their investments. The government's challenge wasn't just operational but emotional—converting skepticism into trust, resistance into acceptance.

The months between the announcement and the actual formation of LIC were frenzied. Teams of government officials worked round the clock to value assets, verify liabilities, and create the administrative structure for the new corporation. The complexity was staggering—each of the 245 entities had different accounting systems, investment portfolios, and operational procedures. Standardizing these into a single system while ensuring no policyholder lost coverage required meticulous planning and execution.

III. The Great Nationalization: Birth of LIC (1956)

The political theater surrounding the nationalization of life insurance in India was as dramatic as any in the young nation's history. Prime Minister Jawaharlal Nehru, the architect of India's socialist-leaning mixed economy, viewed the consolidation of the insurance sector through an ideological lens that transcended mere economics. For Nehru, insurance nationalization represented a crucial step in wresting control of the "commanding heights" of the economy from private—and often foreign—hands. In his speeches to Parliament, he articulated a vision where insurance premiums collected from millions of Indians would fund the great dams, steel plants, and infrastructure projects that would transform India from a colonial backwater into a modern industrial power.

The political momentum for nationalization had been building since 1944, but it was the spectacular failures of several insurance companies in the early 1950s that provided the immediate catalyst. When the Hindustan Co-operative Insurance Company collapsed in 1950, wiping out the life savings of thousands of middle-class families, public outrage reached a crescendo. The failure wasn't just financial; it was a betrayal of trust that struck at the heart of the emerging Indian middle class's aspirations. Opposition politicians seized on these failures, with socialist leaders like Ram Manohar Lohia arguing that only state ownership could protect ordinary Indians from the "rapacious greed" of private insurers.

The announcement on January 19, 1956, that life insurance would be nationalized sent shockwaves through India's business community. Finance Minister C.D. Deshmukh, presenting the decision to Parliament, framed it not as an attack on private enterprise but as a necessary step for national development. His speech, lasting over two hours, meticulously laid out the government's case: private insurers had failed to extend coverage beyond urban elites, many companies were financially unsound, excessive commissions and management expenses were eating into policyholders' returns, and the fragmented industry couldn't mobilize savings for planned development. The opposition, led by leaders from the Swatantra Party, warned of inefficiency and bureaucratization, but their voices were drowned in the socialist fervor of the times.

The Life Insurance Corporation of India officially came into existence on September 1, 1956, through an Act of Parliament that remains one of the most sweeping pieces of economic legislation in Indian history. The Act didn't just create a new company; it fundamentally redefined the relationship between the state and financial services. The legislation granted LIC monopoly status, making it illegal for any other entity to conduct life insurance business in India. This wasn't merely market dominance—it was complete market control backed by the full force of law.

The merger of 245 insurance companies and provident societies into a single entity was an operational challenge of unprecedented scale. Each company brought its own legacy systems, corporate cultures, and client relationships. The Oriental Life Insurance Company, nearly 140 years old, had to be integrated with companies that were barely a few years old. The Bombay Mutual Life Assurance Society, with its proud history of indigenous enterprise, had to merge with companies that had been British-owned until independence. The government appointed teams of administrators, accountants, and actuaries who worked eighteen-hour days to complete the amalgamation. Files had to be physically transported from hundreds of offices across the country to newly established zonal headquarters. In an era before computers, policy records were maintained in massive ledgers that had to be manually reconciled.

J.L. Bansal, appointed as LIC's first Chairman, was a career civil servant who brought to the role a combination of administrative acumen and nationalist fervor. Bansal, who had previously served in the Finance Ministry, understood that LIC's success would be measured not just in financial terms but in its ability to fulfill its social mandate. In his first address to LIC employees, he declared, "We are not just insurance administrators; we are nation builders. Every policy we sell, every claim we settle, contributes to India's march toward prosperity." This rhetoric wasn't empty; it reflected a genuine belief that LIC would be instrumental in India's economic transformation.

The corporation's initial capital structure was modest by today's standards but ambitious for its time. With an authorized capital of ₹5 crores (₹50 million), LIC began operations with assets of approximately ₹400 crores inherited from the amalgamated companies. By the end of its first year, the corporation had collected total premiums of approximately ₹200 crores, exceeding even the most optimistic projections. This early success validated the government's belief that a unified, state-backed insurer could mobilize savings more effectively than the fragmented private market ever could.

The mission and mandate given to LIC went far beyond conventional insurance operations. The corporation was explicitly charged with spreading life insurance to rural areas, where private insurers had feared to tread. This wasn't just about market expansion; it was about social transformation. The government believed that bringing insurance to villages would not only provide financial security to rural families but also integrate them into the formal financial system, teaching them about savings, investment, and long-term planning. LIC was to be a vehicle for financial inclusion decades before the term became fashionable.

The monopoly structure granted to LIC was both its greatest strength and its defining characteristic. Unlike monopolies that emerge through market competition, LIC's monopoly was created by legislative fiat and maintained by legal prohibition of competition. This guaranteed market position came with implicit and explicit obligations. The corporation was expected to serve segments that private insurers would consider unprofitable, invest in government securities and infrastructure projects regardless of returns, and maintain offices in remote areas where business volumes couldn't justify the costs. The monopoly wasn't a privilege—it was a social contract.

Building trust through government guarantee became LIC's most powerful competitive advantage, even in the absence of competition. The corporation's policies came with the explicit backing of the Government of India, a guarantee that transformed life insurance from a risky financial product into something as safe as a government bond. For a population that had witnessed numerous insurance company failures, this guarantee was invaluable. Marketing materials from the early years repeatedly emphasized this point: "LIC—backed by the Government of India" appeared on every advertisement, every policy document, every agent's visiting card.

The organizational structure that emerged reflected both the scale of LIC's ambitions and the realities of governing a vast, diverse nation. The corporation was organized into five zones—Northern, Eastern, Western, Southern, and Central—each headed by a Zonal Manager who reported directly to the Chairman. This structure balanced centralized policy-making with regional autonomy, allowing LIC to adapt its products and marketing to local conditions while maintaining uniform standards. Each zone was further divided into divisions and branches, creating a hierarchical structure that could effectively manage operations across India's vast geography.

The early operational challenges were formidable. Integrating 245 different policy formats into standardized products required extensive actuarial work. The corporation had to honor policies written by defunct companies, some with terms and conditions that were poorly documented or financially unviable. Claims settlement procedures had to be standardized across thousands of cases with varying documentation standards. The corporation also inherited approximately 50,000 employees from the amalgamated companies, each with different salary structures, benefits, and expectations. Creating a unified corporate culture from this diverse workforce would take years of careful management.

The investment philosophy adopted by LIC from its inception reflected its dual mandate as a commercial institution and a tool for national development. Unlike private insurers who had often invested in speculative ventures or maintained large cash reserves, LIC was directed to invest primarily in government securities and approved infrastructure projects. This wasn't just prudent investment policy; it was economic nationalism in action. LIC's investments funded the Bhakra Nangal Dam, the steel plants at Bhilai and Rourkela, and countless other projects that formed the backbone of India's industrial infrastructure.

The role of agents in LIC's early years deserves special attention. The corporation inherited approximately 30,000 agents from the amalgamated companies, but this number would grow exponentially in the following years. These agents weren't just salespeople; they became LIC's ambassadors in communities across India. In villages where bank branches didn't exist and formal financial services were unknown, the LIC agent often became the first and only connection to the financial system. The corporation invested heavily in agent training, creating elaborate instruction manuals in multiple languages and establishing training centers across the country.

The cultural significance of LIC's formation extended beyond economics into the realm of national identity. The corporation's motto, "Yogakshemam Vahamyaham"—a Sanskrit phrase from the Bhagavad Gita meaning "Your welfare is our responsibility"—wasn't chosen randomly. It represented a deliberate attempt to root this modern financial institution in ancient Indian wisdom, making it appear less foreign and more familiar to a population still skeptical of Western-style financial products. This cultural positioning would prove masterful, helping LIC penetrate segments of society that had never before considered insurance.

The first year's operations exceeded all expectations. Not only did LIC collect ₹200 crores in premiums, but it also settled over 100,000 claims, demonstrating efficiency that skeptics had claimed would be impossible for a government organization. The corporation opened 150 new branch offices, extending its reach into districts that had never before had insurance services. More importantly, it began the slow process of changing Indian attitudes toward insurance, transforming it from an elite financial product into a middle-class necessity.

IV. The Monopoly Era: Expansion & Nation Building (1956-2000)

The forty-four years of LIC's monopoly represent one of the most successful episodes of state-directed capitalism in the developing world. During this period, LIC transformed from an experimental consolidation of a fragmented industry into an institution so deeply embedded in Indian society that it became impossible to imagine middle-class life without an LIC policy. The corporation's geographic expansion during these decades was nothing short of revolutionary. From 33 divisional offices at its inception, LIC grew to over 2,048 branch offices by 2000, with at least one office in every district of India. This wasn't organic growth—it was planned penetration, with the corporation often opening offices in areas where the business case was marginal at best, fulfilling its mandate to serve every Indian regardless of profitability.

The rural penetration strategy adopted by LIC was particularly innovative for its time. Recognizing that traditional insurance products designed for urban salary earners wouldn't work in villages, the corporation developed specialized rural products with lower premiums, simplified documentation, and benefits tailored to agricultural cycles. The Gram Suraksha scheme, launched in 1971, allowed entire villages to be covered under group insurance, with premiums as low as ₹2 per year. By 1980, LIC had covered over 10 million rural lives, a feat that no private insurer had even attempted. The corporation's rural agents, often local teachers or postmasters who worked part-time, became trusted advisors in their communities, helping families plan for education, marriages, and retirement.

The evolution of LIC's product portfolio during the monopoly era reflected the changing needs and aspirations of Indian society. The early years focused on basic whole life and endowment policies, simple products that combined insurance with savings. As the Indian middle class grew and became more sophisticated, LIC introduced money-back policies, pension plans, and unit-linked products. The Jeevan Akshay immediate annuity plan became popular among retirees, while the Jeevan Kishore policy targeted parents saving for their children's education. Each product launch was accompanied by extensive market research and careful actuarial modeling, ensuring that LIC maintained its financial stability while expanding coverage.

The Sanskrit motto "Yogakshemam Vahamyaham" became more than just a corporate slogan—it evolved into a cultural promise that resonated across India's diverse linguistic and religious communities. The phrase, drawn from the 22nd verse of the Bhagavad Gita's 9th chapter, where Lord Krishna promises to preserve what devotees have and bring what they lack, positioned LIC as a quasi-religious institution providing divine protection through financial planning. This brilliant positioning helped overcome religious objections to insurance (some conservative Muslims and Hindus viewed insurance as showing lack of faith in divine providence) by framing it as a form of devotional responsibility toward one's family.

LIC's role in India's capital markets during the monopoly era cannot be overstated. By 1990, the corporation had become the largest institutional investor in India, holding substantial stakes in virtually every major Indian company. LIC's investment decisions could make or break IPOs, and its annual investment policy was awaited with the same anticipation as the government budget. The corporation's investment philosophy, while conservative, provided crucial patient capital to Indian industry during its formative years. When private investors shied away from long-gestation infrastructure projects, LIC stepped in, funding power plants, ports, and highways that would generate returns only after decades.

The agency model perfected by LIC during these years created what would become one of the world's largest sales forces. From 30,000 agents inherited at formation, the number grew to over 600,000 by 1990 and exceeded 1 million by 2000. This army of agents represented every segment of Indian society—retired government servants, housewives supplementing family income, young graduates waiting for permanent employment, and career insurance professionals. The corporation's agency development programs were sophisticated, including regular training workshops, recognition ceremonies for top performers, and a complex commission structure that rewarded both new business and policy persistence.

The cultural impact of LIC policies on middle-class India during this period was profound and multifaceted. An LIC policy became a marker of financial responsibility and social status. Parents would proudly mention their LIC policies when arranging marriages for their children, demonstrating their prudent planning. The physical policy document, often kept in the family's steel almirah alongside property papers and gold jewelry, became a tangible symbol of security. The annual premium payment was a family ritual, with agents often invited for tea and treated as extended family members. Stories abound of agents who attended family weddings, advised on financial matters beyond insurance, and even helped arrange marriages within their client networks.

LIC's transformation into the government's "go-to" institution for economic intervention became particularly pronounced during financial crises. When banks faced runs, LIC provided liquidity. When the stock market crashed, LIC increased its purchases to provide stability. During the balance of payments crisis of 1991, LIC's foreign currency reserves were pledged to international lenders. The corporation's role in bailing out troubled public sector units became so routine that it was factored into government planning. While these interventions often came at the cost of optimal returns for policyholders, they cemented LIC's position as a pillar of India's economic stability.

The corporation's investment in technology during the monopoly era, while often overlooked, laid the foundation for its later digital transformation. In 1964, LIC became one of the first Indian organizations to use computers, installing an IBM 1401 system for policy administration. By the 1980s, the corporation had developed sophisticated actuarial models and investment analysis systems. The LIC of India Management Development Centre, established in 1970, became a premier training institution not just for insurance but for financial services broadly, with its alumni going on to lead major financial institutions across India.

The social schemes implemented by LIC during this period went beyond traditional insurance. The corporation pioneered micro-insurance before the term existed, with schemes targeting specific vulnerable groups. The Social Security Group Insurance Scheme covered landless laborers, the Integrated Rural Development Programme provided coverage to families below the poverty line, and the Janashree Bima Yojana offered insurance to families living in urban slums. These schemes, while often loss-making, demonstrated LIC's commitment to its social mandate and helped millions of Indians experience the security of insurance coverage for the first time.

The monopoly years also saw LIC become one of India's largest real estate owners, with prime properties in every major city. The iconic LIC buildings—art deco structures in Mumbai, modernist towers in Delhi, classical edifices in Chennai—became landmarks in their own right. These buildings served not just as offices but as symbols of LIC's permanence and stability. The corporation's policy of constructing its own buildings rather than renting space reflected both its long-term thinking and its role in urban development. Many LIC buildings included public spaces, auditoriums, and cultural centers, furthering the corporation's integration into community life.

The relationship between LIC and India's five-year plans during this period was symbiotic. The Planning Commission counted on LIC's investments to fund planned expenditure, while LIC used the plans to guide its expansion strategy. During the Fourth Plan (1969-74), LIC was tasked with doubling life insurance coverage; it exceeded the target by 150%. The Sixth Plan (1980-85) emphasized rural coverage; LIC responded by opening 500 new rural branches. This alignment between corporate strategy and national planning was unique in the non-socialist world and demonstrated how effectively a monopoly could be harnessed for development goals.

The challenges faced during the monopoly era weren't insignificant. Bureaucratic inefficiencies crept in, with claim settlement times stretching to months in some cases. The absence of competition led to complacency in customer service, with policyholders having no alternative but to accept whatever service standards LIC provided. Product innovation slowed, with new launches taking years from conception to market. The corporation's investment returns, while stable, often lagged inflation, eroding the real value of policyholder savings. Critics argued that the monopoly had become a tax on the middle class, forcing them to accept suboptimal returns in exchange for security.

Yet, the achievements of the monopoly era remain remarkable. By 2000, LIC had 180 million policies in force, covering approximately 75 million lives—roughly 7.5% of India's population. The corporation's assets had grown from ₹400 crores at inception to over ₹2 lakh crores. More importantly, LIC had fundamentally changed Indian attitudes toward insurance. What had been viewed with suspicion in 1956 had become, by 2000, an essential component of financial planning. The corporation had created a culture of insurance that would survive even after its monopoly ended.

The human stories from this era illuminate LIC's impact beyond statistics. There's the account of Kamala Devi, a widow in rural Karnataka, who received her husband's death claim in 1975—₹10,000 that seemed impossible wealth to a family that had never seen more than ₹100 at once. She used the money to educate her three children, all of whom became successful professionals. There's the story of Mohammed Yusuf, an LIC agent in Lucknow, who over his 30-year career sold policies to three generations of the same families, becoming their trusted advisor on everything from education planning to property purchases. These millions of individual stories aggregate into a narrative of social transformation that transcends corporate history.

The monopoly era also established LIC's unique corporate culture, blending government service ethos with insurance professionalism. Employees took pride in working for "Mother LIC," as the corporation was affectionately known. The job security, comprehensive benefits, and social prestige associated with LIC employment made it one of India's most coveted employers. The corporation's promotion policies, while slow, were transparent and merit-based, creating a stable, motivated workforce. The LIC Officers' Federation and LIC Employees' Union became powerful voices in India's labor movement, negotiating not just for better wages but for maintaining LIC's social mission.

As the 1990s drew to a close, however, the winds of change were unmistakable. Economic liberalization, initiated in 1991, had transformed every other sector of the Indian economy. The insurance sector remained the last bastion of state monopoly, increasingly anachronistic in a liberalizing economy. International pressure, particularly from the World Trade Organization, mounted for India to open its insurance sector to foreign competition. Domestic private players, having tasted success in banking and financial services, lobbied intensively for entry into insurance. The Malhotra Committee, constituted in 1993 to examine the insurance sector, had recommended ending LIC's monopoly, though its recommendations were initially shelved due to political opposition.

By 1999, the decision to liberalize insurance had become inevitable. The Insurance Regulatory and Development Authority (IRDA) Act was passed, setting the stage for private players to enter the market. For LIC, the monopoly era was ending, but the challenges and opportunities of competition were just beginning. The corporation that had grown comfortable in its protected space would now have to prove itself in the marketplace. The question on everyone's mind was whether this gentle giant, accustomed to operating without competition for 44 years, could survive and thrive in the brutal world of competitive insurance.

V. Liberalization & The End of Monopoly (2000-2010)

August 2000 marked the end of an era and the beginning of a revolution in Indian insurance. When the Indian government embarked on its program to liberalize the insurance sector, opening doors that had been firmly shut for 44 years, the comfortable monopoly that LIC had enjoyed came to an abrupt end. LIC and private insurers respectively held a market share of 87.44 and 12.56 per cent during 2003-04, demonstrating how quickly private players had captured market share in just three years of operation. The liberalization wasn't just about allowing competition; it represented a fundamental shift in how insurance would be sold, marketed, and consumed in India.

The entry of private players was orchestrated with careful regulatory oversight. The IRDA Bill was passed in December 1999 and became an Act in April 2000. In July 2000, immediately after the first meeting of the Insurance Advisory committee, 11 essential regulations relevant for players entering the Indian market were notified. In October 2000, six licenses to new players in the life and non-life sectors were issued. The smooth transition from monopoly to competition was remarkable—once the legislation was put through, the actual process of inducting private players into the market had gone off smoothly. I do not think there is any other sector in this country where the transition from state monopoly to free market has been as hassle free as the insurance sector.

The new entrants weren't just any companies—they were joint ventures between Indian financial powerhouses and global insurance giants. HDFC partnered with Standard Life, ICICI with Prudential, Birla with Sun Life, and Tata with AIG. These partnerships brought together local market knowledge with international insurance expertise, creating formidable competitors to LIC's dominance. Each partnership represented billions of dollars in capital commitment and decades of global insurance experience. The foreign partners brought sophisticated actuarial models, innovative product designs, and modern distribution strategies that had been tested in developed markets.

LIC, however, maintained its dominance, reporting a compound annual growth rate (CAGR) of 24.53% in first-year premiums and 19.28% in total life premiums between 2000 and 2013. This resilience can be attributed to its strong brand, extensive network, and customer trust. The corporation's response to competition was measured but effective. Rather than panic at the entry of private players, LIC leveraged its massive advantages—brand recognition that was universal, an agent network that reached every corner of India, and most importantly, the trust of millions of policyholders who had grown up seeing LIC as synonymous with life insurance.

The competitive dynamics that emerged were fascinating. Private insurers targeted urban, educated, high-income segments with sophisticated products like Unit-Linked Insurance Plans (ULIPs) that combined insurance with market-linked returns. They emphasized need-based selling, conducting detailed financial planning sessions with potential customers rather than the traditional approach of selling insurance primarily as a tax-saving instrument. Their sales forces were younger, better trained, and more aggressive. They used technology extensively, with online policy issuance and premium payment becoming standard features from day one.

By 2006, there were 14 private insurers in India whose market share was increasing every year. Innovative products, smart marketing and aggressive distribution helped the private sector grow within a very short period. The private players brought a customer-centric approach that was revolutionary for Indian insurance. They introduced concepts like free-look periods, where customers could return policies within 15 days if unsatisfied. They offered flexible premium payment options, partial withdrawals, and transparent fund performance reporting for ULIPs. Customer service, long a weakness in the monopoly era, became a key differentiator.

The distribution revolution initiated by private insurers was particularly significant. While LIC relied primarily on its agency force, private insurers pioneered bancassurance in India, leveraging their parent banks' branch networks to sell insurance. ICICI Prudential could tap into ICICI Bank's thousands of branches, instantly gaining distribution reach that would have taken decades to build organically. They also experimented with alternative channels—online sales, telemarketing, and mall kiosks—that LIC had never seriously explored.

LIC sold its policies as tax instruments and not as products giving protection against risk. Most of the customers were under-insured with no flexibility or transparency in the services provided. This criticism, while somewhat harsh, captured a fundamental truth about how insurance had been sold during the monopoly era. Private insurers changed this narrative, emphasizing protection first and tax benefits second. They educated customers about the importance of adequate life cover, introducing term insurance products that offered high coverage at low premiums—a concept that was virtually unknown in India before liberalization.

The impact on LIC's market share was immediate and sustained. From virtually 100% market share in 2000, LIC's share in new business premiums declined steadily. In the case of life insurance the private sector accounts for 9% of the gross premium with the remaining 91% accounted for by Life Insurance Corporation (LIC). The issue for consideration is whether the acquisition of the market share by the private companies is at the expense of the LIC. The answer to this question was nuanced. While LIC was losing market share percentage, its absolute premium collections continued to grow robustly.

The LIC's gross premium has grown by 115% in 2004-05 over the premium collected in 2000-01. If we compare this post liberalization growth with the growth for the corresponding number of years prior to 2000, we find that between 1996-97 and 2000-2001 the LIC registered a growth in gross premium of 114.36% (Rs.16277 crs in 96-97 to Rs.34898 crs in 2000-01). The LIC has obviously not lost its growth momentum and the market share of the private players has come out of an enlarged market.

This phenomenon—declining market share but growing absolute business—reflected the dramatic expansion of the insurance market post-liberalization. Competition wasn't just dividing an existing pie; it was dramatically expanding the pie itself. Private insurers were creating new markets, reaching customer segments that LIC had never effectively served. Young professionals, entrepreneurs, and the emerging affluent class found private insurers' products and service more aligned with their needs and expectations.

LIC's strategic response evolved through the decade. Initially defensive, the corporation gradually became more proactive. It launched new products to compete with private players' ULIPs, though its product development cycle remained slower due to bureaucratic processes. The corporation invested in technology, computerizing its vast network of branches and introducing online services, though the pace of digitalization lagged behind nimbler private competitors. LIC also revamped its agency training programs, introducing professional development courses and modern sales techniques.

The regulatory environment during this period sought to balance competition with stability. IRDA introduced regulations on ULIP charges, minimum sum assured requirements, and commission structures that affected both LIC and private insurers. The regulator's approach was generally even-handed, neither favoring the incumbent nor the new entrants. This regulatory neutrality was crucial in establishing the credibility of the liberalized market.

LIC registered a growth of 0.6 per cent while private insurers registered a growth rate of 92.4 percent in terms of new offices opened during the 2000-2007 period. This stark difference in expansion rates highlighted the aggressive growth strategies of private insurers versus LIC's more measured approach. Private insurers were in a land-grab mode, rapidly establishing presence in urban and semi-urban markets. They targeted cities where disposable incomes were rising fastest, where banking penetration was highest, and where customers were most receptive to new financial products.

The talent war that erupted during this period reshaped India's insurance industry. Private insurers poached aggressively from LIC, offering salaries that were multiples of government pay scales. LIC's best and brightest—actuaries, investment managers, senior sales leaders—were lured away with compensation packages that the corporation couldn't match. This brain drain forced LIC to confront uncomfortable questions about its ability to compete in a market economy while constrained by government pay structures.

The product innovation introduced by private insurers during this decade transformed Indian insurance. ULIPs became the fastest-growing product category, offering market-linked returns that appealed to India's increasingly equity-savvy middle class. Riders—additional benefits that could be attached to base policies—proliferated, allowing customers to customize coverage. Critical illness riders, accident benefit riders, and waiver of premium riders became standard offerings. Private insurers also introduced innovative premium payment options, including single premium and limited payment policies that appealed to different customer segments.

Customer service standards underwent a revolutionary transformation. Private insurers introduced service level agreements (SLAs) for claim settlement, policy issuance, and customer queries. They invested heavily in call centers, providing 24/7 customer support in multiple languages. Claim settlement ratios became a key marketing metric, with insurers competing to demonstrate faster and higher claim settlement rates. This focus on service forced LIC to improve its own standards, though the corporation's massive scale and legacy systems made rapid improvement challenging.

The impact of liberalization extended beyond business metrics to fundamental changes in insurance consciousness. Insurance penetration, which had stagnated around 2% during the monopoly era, began rising steadily. Insurance density—premium per capita—showed even more dramatic improvement. The concept of financial planning gained currency, with insurance becoming one component of a comprehensive approach to personal finance rather than a standalone tax-saving instrument.

The bancassurance model pioneered during this period deserves special attention. Banks discovered that insurance distribution could be highly profitable, generating fee income without capital requirements. Bank customers, already trusting their banks with their savings, were receptive to insurance products sold through the same channel. The integration of banking and insurance created powerful synergies—banks could offer comprehensive financial solutions, while insurers gained access to pre-qualified customer bases.

By 2010, the competitive landscape had stabilized into a clear hierarchy. LIC remained the dominant player but with a much-reduced market share. Among private players, ICICI Prudential, HDFC Life, and SBI Life had emerged as clear leaders, each with distinct strategies and target segments. The remaining private insurers were struggling to achieve scale and profitability, with some beginning to question the sustainability of their India ventures.

VI. Digital Transformation & Modernization (2010-2020)

The decade from 2010 to 2020 would test LIC's adaptability like never before as the insurance industry underwent a digital revolution that threatened to make traditional distribution models obsolete. The corporation, with its massive legacy infrastructure and deeply entrenched processes, faced the herculean task of transforming itself while continuing to serve its existing base of hundreds of millions of policyholders. This period would reveal both the constraints of being a government-owned behemoth and the surprising agility that crisis can inspire even in the most bureaucratic organizations.

The technology adoption challenges LIC faced were emblematic of large-scale digital transformation complexities. The corporation's IT infrastructure, built over decades, consisted of multiple legacy systems that barely communicated with each other. Policy data for products launched in the 1970s resided on mainframe systems, while newer products ran on different platforms. Customer data was fragmented across branches, with no unified view of a policyholder who might have multiple policies. The corporation's 2,048 branches operated on varying levels of computerization, with some still maintaining physical ledgers for certain transactions. Integrating these disparate systems while ensuring zero disruption to daily operations—processing thousands of claims, issuing new policies, and managing investments worth trillions—was akin to rebuilding a plane while flying it.

The digital transformation journey began in earnest with Project Unification, an ambitious initiative to create a centralized, integrated IT platform. The project, launched in 2012, aimed to consolidate all policyholder data into a single system, enable real-time transaction processing across all branches, and provide customers with unified access to all their policies through digital channels. The scale was staggering—migrating data for over 300 million policies, training over 100,000 employees, and ensuring compatibility with thousands of different product variations launched over six decades. The project faced numerous setbacks, including vendor disputes, cost overruns, and resistance from employees fearful of job losses. Yet, by 2017, the core infrastructure was operational, marking a crucial milestone in LIC's modernization journey.

The competitive pressure from private insurers' digital-first approaches was relentless and multifaceted. Companies like ICICI Prudential and HDFC Life had built their operations on modern technology stacks from inception, giving them inherent advantages in digital innovation. They launched mobile apps that allowed customers to buy policies, pay premiums, and file claims entirely online. Their turnaround times for policy issuance dropped to hours, compared to LIC's weeks. They used data analytics to personalize product recommendations and optimize pricing. They leveraged social media for customer service and marketing, building communities of engaged customers. For LIC, matching these capabilities required not just technology investment but fundamental changes in organizational culture and processes.

The corporation's digital initiatives, while slow to start, gradually gained momentum. The launch of LIC's customer portal in 2011 was a watershed moment, allowing policyholders to view policy details, pay premiums, and download statements online. Though initially plagued by technical glitches and limited functionality, the portal evolved into a comprehensive digital service platform. By 2015, over 50 million customers had registered, though this represented less than 20% of LIC's policyholder base. The challenge wasn't just building digital platforms but convincing customers, many of whom were older and less tech-savvy, to adopt them.

Mobile technology became a crucial battleground in the digital transformation war. LIC's first mobile app, launched in 2013, was basic compared to private competitors' offerings, providing mainly information services rather than transactional capabilities. The corporation's approach to mobile evolved slowly, constrained by security concerns, regulatory requirements, and the need to support multiple languages and device types. By 2018, however, LIC had launched a suite of mobile apps catering to different stakeholders—customers, agents, and development officers—each providing role-specific functionality. The customer app alone recorded over 10 million downloads by 2020, though active usage remained lower than private insurers' apps.

The digitization of agent operations represented one of LIC's most successful transformation initiatives. The corporation equipped its 1.3 million agents with tablets and mobile apps, enabling them to generate quotes, submit applications, and track commissions digitally. The Smart Agent platform, launched in 2016, transformed the agent from a mere salesperson into a financial advisor equipped with sophisticated tools for need analysis, financial planning, and product recommendation. This digital empowerment of agents was crucial, as they remained LIC's primary distribution channel, generating over 90% of new business even as digital direct sales grew. Info Centres have been commissioned at Mumbai, Ahmedabad, Bangalore, Chennai, Hyderabad, Kolkata, New Delhi, Pune and many other cities. These Info Centres represented LIC's attempt to create modern, technology-enabled customer service hubs that could compete with private insurers' sleek branch offices. With a vision of providing easy access to its policyholders, Life Insurance Corporation has launched its SATELLITE SAMPARK offices. The satellite offices are smaller, leaner and closer to the customer, representing a significant shift from LIC's traditional large branch model to a more distributed, accessible presence.

The satellite offices concept was particularly innovative for LIC. These smaller offices, staffed with just 2-3 employees, could handle basic services like premium collection, new business acceptance, and customer queries without the overhead of full branches. By 2020, LIC had opened over 1,559 satellite offices, dramatically improving its accessibility in semi-urban and rural areas where full branches weren't economically viable. This network expansion was crucial in maintaining LIC's competitive edge in markets where private insurers had limited presence.

The challenge of maintaining relevance with millennials while serving traditional customers created a strategic dilemma that defined much of LIC's digital transformation efforts. The corporation's customer base was bipolar—millions of older, rural customers who preferred face-to-face interactions and physical documentation, and a growing segment of young, urban customers who expected seamless digital experiences. Creating systems and processes that could serve both segments effectively required careful balancing. LIC's solution was a hybrid model—maintaining traditional channels while building parallel digital capabilities, allowing customers to choose their preferred interaction mode.

Data analytics and artificial intelligence adoption at LIC progressed slowly but steadily through the decade. The corporation established a dedicated analytics center in 2015, tasked with leveraging its vast data repository for business insights. With data on over 300 million policies spanning six decades, LIC possessed one of the richest insurance datasets globally. However, extracting actionable insights from this data proved challenging due to data quality issues, lack of standardization, and regulatory constraints on data usage. By 2018, LIC had implemented predictive models for fraud detection, customer churn prediction, and risk assessment, though the sophistication lagged behind private competitors who had built analytics into their DNA from inception.

The corporation's approach to insurtech partnerships evolved from skepticism to cautious embrace. Initially viewing technology startups as threats or irrelevant to its traditional business model, LIC gradually recognized the potential of collaboration. In 2017, the corporation launched an innovation lab to explore partnerships with insurtech companies, focusing on areas like automated underwriting, claims processing, and customer engagement. While these initiatives were modest compared to private insurers' aggressive insurtech investments, they marked an important shift in LIC's innovation mindset.

Customer experience transformation became a key focus area, driven by increasing customer expectations and competitive pressure. LIC introduced several initiatives to improve service delivery—automated claim settlement for straightforward cases, reducing processing time from weeks to days; SMS and email alerts for premium due dates and policy updates; simplified forms and documentation requirements; and dedicated customer service teams for high-value policies. While these improvements were significant, customer satisfaction surveys consistently showed LIC trailing private insurers in service quality perceptions, highlighting the challenge of changing entrenched perceptions.

The regulatory environment during this period pushed digitalization through various mandates and incentives. IRDAI's regulations on electronic policy issuance, digital KYC, and online claim settlement created a level playing field that forced all insurers, including LIC, to upgrade their digital capabilities. The regulator's push for insurance repository systems, where all policies would be held in dematerialized form, particularly benefited LIC given its massive policy base. By 2020, over 70 million LIC policies had been dematerialized, simplifying policy servicing and reducing fraud.

The COVID-19 pandemic that struck in early 2020 became an unexpected accelerator of LIC's digital transformation. With physical branches closed during lockdowns, digital channels became the only means of customer interaction. LIC rapidly scaled up its digital infrastructure, enabling completely digital policy purchases for select products, video-based medical examinations for underwriting, and digital claim submission and processing. The corporation reported that digital premium collections increased by over 300% during the lockdown months, demonstrating both the latent demand for digital services and LIC's ability to respond quickly when necessary.

During the year 2015-16 the Corporation has adopted Government of India's RTI online portal, developed by DOPT, across the country, connecting all Offices of the Corporation under a single system. This adoption of the Right to Information (RTI) online portal exemplified LIC's broader approach to digital transformation—leveraging government initiatives and platforms where possible rather than building everything from scratch. This pragmatic approach allowed LIC to modernize more quickly and cost-effectively than pure custom development would have permitted.

The investment in employee digital literacy proved crucial to the transformation's success. LIC launched massive training programs to upskill its workforce, covering everything from basic computer skills to advanced data analytics. The corporation established e-learning platforms where employees could access training modules at their own pace. Special focus was given to training older employees who formed a significant portion of LIC's workforce and were often resistant to technological change. By 2020, over 90% of LIC employees had undergone some form of digital skills training, though the depth and effectiveness varied significantly.

The decade also saw LIC experimenting with emerging technologies like blockchain and Internet of Things (IoT). The corporation participated in industry consortiums exploring blockchain for policy administration and claims processing, though practical implementation remained limited. IoT experiments focused on usage-based insurance products and health monitoring for life insurance underwriting, areas where private insurers were already making significant strides. While these initiatives demonstrated LIC's willingness to explore cutting-edge technologies, they also highlighted the challenges of innovation within a large, risk-averse organization.

Social media engagement became another frontier in LIC's modernization journey. The corporation launched official accounts on major platforms, using them for customer service, marketing, and brand building. However, LIC's social media strategy remained conservative compared to private insurers who leveraged these platforms for viral marketing campaigns and influencer partnerships. The corporation's cautious approach reflected both its government ownership—requiring careful communication—and its traditional customer base's limited social media usage.

By the end of 2020, LIC's digital transformation had achieved mixed results. On one hand, the corporation had successfully modernized its core infrastructure, digitized millions of policies, and created functional digital channels for customers and agents. Digital adoption metrics showed steady improvement, with over 60% of premium collections happening through digital channels by year-end. On the other hand, LIC still lagged private insurers in digital innovation, customer experience, and operational efficiency. The corporation's digital transformation was more evolutionary than revolutionary, reflecting the constraints and complexities of modernizing a massive, legacy-laden organization while maintaining its social obligations and serving diverse customer segments.

VII. The IPO Saga: Preparation & Execution (2020-2022)

Finance Minister Nirmala Sitharaman announced a proposal for an initial public offering (IPO) for the Life Insurance Corporation of India (LIC) in the 2021 Union budget of India. The announcement, made in February 2021, sent shockwaves through India's financial markets and triggered one of the most complex financial engineering exercises in the country's history. The decision to list LIC wasn't just about raising capital; it represented a fundamental shift in the government's approach to its crown jewels—strategic disinvestment of an institution that had been synonymous with government-backed financial security for 65 years.

The valuation puzzle that confronted the government and its advisors was unprecedented in complexity. If investors agree with the $203 billion valuation sought by the government, LIC would compete against India's biggest companies—Reliance Industries Ltd. and Tata Consultancy Services Ltd. The IPO would account for the bulk of a $23.5 billion asset-sale target. The challenge wasn't just arriving at a number but justifying it to skeptical investors who questioned whether a government-controlled insurer could generate market-competitive returns while maintaining its social obligations.

The embedded value calculation became the cornerstone of LIC's valuation exercise. The government's IPO document filed on February 13 put LIC's embedded value at Rs 5.4 trillion ($71.7 billion), a figure that represented the present value of future profits from existing policies plus adjusted net worth. This embedded value was calculated using methodologies common in global insurance markets but required significant adjustments for Indian conditions—mortality rates, persistency ratios, and investment return assumptions all had to be carefully calibrated. The valuation exercise involved teams of actuaries, investment bankers, and consultants working round the clock to build models that could withstand scrutiny from global investors.

The preparation for the IPO involved a massive organizational transformation within LIC. The corporation, which had operated with government accounting standards for decades, had to transition to Indian Accounting Standards (Ind AS) compliant with international norms. This wasn't just a technical exercise—it required restating years of financial data, creating new reporting systems, and training thousands of employees in new accounting principles. The corporation had to establish investor relations functions, create detailed management discussion and analysis documents, and prepare for the scrutiny that comes with being a public company.

The regulatory amendments required for the IPO were substantial and politically sensitive. The government had to amend the LIC Act of 1956, which had created the corporation as a government monopoly. The amendment, passed in March 2021, allowed for divestment while ensuring the government retained majority control. The cabinet approved a policy amendment allowing foreign direct investment of up to 20 per cent in LIC, a change aimed at facilitating the listing of the state-run insurer. These legislative changes triggered heated debates in Parliament, with opposition parties questioning the wisdom of privatizing what they called the "family silver."

The IPO, initially planned for February, was postponed because of the Ukraine war and the outflow of institutional funds from the stock market. Since January, about $16 billion of foreign capital has left Indian markets. The Russia-Ukraine crisis escalated dramatically in late February 2022, with Russia declaring war on Ukraine, followed by multiple sanctions imposed on the country by Western nations, leading to a surge in oil prices to over 7-year highs. Indian markets became volatile, and government officials grew concerned that international and domestic investors would shy away from buying shares in the insurance firm.

"It's a full blown war now so we will have to assess the situation for going ahead with the LIC IPO," a government source said. Finance Minister Sitharaman's public statements reflected the government's dilemma: "Ideally, I'd like to go ahead with it because we had planned it for some time based purely on Indian considerations. If global considerations warrant that I need to look at it, I wouldn't mind looking at it again." She further added, "When a private sector promoter takes this call, he has to only explain this to the company's board but I would have to explain it to the whole world."

In February, overseas investors pulled out 38,068 crore rupees ($5.03 billion) from Indian equities and debt, which was the highest monthly outflow of foreign funds since March 2020. This massive capital flight created a challenging environment for what was supposed to be India's largest IPO. The government faced a difficult choice—proceed with the IPO in adverse market conditions and risk a failed or poorly subscribed offering, or postpone and miss crucial disinvestment targets.

The decision to scale down the offering size reflected pragmatic acceptance of market realities. The size of LIC's offering, which was initially pegged at 5%, was scaled down to 3.5%. The Government of India aimed to raise ₹21,000 crore through the IPO, which was significantly lower than the initially expected ₹65,000 to ₹70,000 crore by diluting a 5% equity stake. Instead, the IPO offered a 3.5% stake, valuing the company at approximately ₹6 lakh crore. This scaling down was a strategic compromise—maintaining the IPO's viability while accepting lower proceeds.

The company's current implied valuation of $80 billion is roughly half of what it was in February, falling at least in part due to market conditions. It had previously planned to offer a 5% stake for about $8 billion. This dramatic valuation compression reflected both deteriorating market conditions and growing investor skepticism about LIC's growth prospects in an increasingly competitive market. The valuation multiple applied to LIC's embedded value dropped from the initially hoped-for 3x to barely 1.1x, a sobering reflection of market sentiment.

The mechanics of the IPO were carefully designed to ensure broad participation while protecting retail investors. The offering structure included specific reservations: 10% for existing policyholders, 35% for retail investors, and 55% for institutional investors. Policyholders were offered a discount of ₹60 per share, while retail investors received a ₹45 discount from the issue price of ₹949. These discounts were designed to ensure full subscription and create a positive listing experience, though they also reduced the government's proceeds.

The policyholder reservation was particularly innovative and complex. LIC had to identify and verify millions of eligible policyholders, create systems for them to apply for shares, and educate them about equity investment—many had never invested in stocks before. The corporation launched massive awareness campaigns, conducting workshops, creating educational materials in multiple languages, and training agents to guide policyholders through the application process. This effort to convert policyholders into shareholders was unprecedented in scale and complexity.

The anchor investor book building process revealed global investors' cautious stance toward LIC. While domestic institutions showed strong interest, foreign institutional investors remained selective, concerned about government control, regulatory constraints on LIC's operations, and the corporation's declining market share. The anchor book was eventually subscribed with participation from sovereign wealth funds, domestic mutual funds, and select foreign investors, but the enthusiasm was notably muted compared to other large Indian IPOs.

The LIC IPO opened to the public on 4 May 2022, and concluded on 9 May 2022. The five-day subscription window saw intense marketing efforts, with LIC employees, agents, and even government officials mobilized to ensure success. The corporation's agent force of 1.3 million became an army of IPO evangelists, reaching out to their clients to encourage participation. Banks extended loans for IPO applications, brokers offered special services for LIC applications, and the media coverage was unprecedented.

The subscription data revealed interesting patterns. The policyholder portion was subscribed 6.12 times, indicating strong support from LIC's traditional base. The retail portion received 1.99 times subscription, showing decent but not overwhelming interest from individual investors. The employee portion was subscribed 4.40 times, demonstrating internal confidence. However, the Qualified Institutional Buyer (QIB) portion was subscribed only 2.83 times, the lowest among major categories, reflecting institutional investors' lukewarm response.

The road shows conducted for the IPO were extensive and exhausting. LIC's senior management, led by Chairman M.R. Kumar, traveled globally to meet investors, presenting the corporation's equity story to skeptical fund managers. The pitch emphasized LIC's dominant market position, massive customer base, potential for margin improvement, and role in India's under-penetrated insurance market. However, investors consistently raised concerns about government interference, competition from private players, and the corporation's ability to innovate.

The pricing discovery process was particularly contentious. Investment bankers initially proposed a price band that would value LIC at over ₹8 lakh crore, but market feedback forced a significant reduction. The final price of ₹949 per share represented a conservative valuation, prioritizing successful listing over maximizing proceeds. This pricing decision reflected the government's fear of a failed IPO, which would have been politically embarrassing and damaged market sentiment.

The technology infrastructure required for the IPO was massive. LIC had to upgrade its systems to handle real-time reporting requirements, create investor portals, and establish connections with stock exchanges and depositories. The corporation also had to ensure its registrar could handle millions of applications, particularly from policyholders who were first-time equity investors. The technical preparation took months and required significant investment, adding to the IPO's overall cost.

The regulatory scrutiny during the IPO process was intense. SEBI, IRDAI, and other regulators examined every aspect of LIC's operations, governance, and disclosures. The Draft Red Herring Prospectus (DRHP) ran to over 500 pages, providing unprecedented detail about LIC's operations, risks, and financials. The disclosure requirements forced LIC to reveal information that had never been public before, including detailed product profitability, agent compensation structures, and investment strategies.

The employee stock option component added another layer of complexity. LIC's employee unions negotiated hard for favorable terms, eventually securing options at a discount to the IPO price. The challenge was balancing employee expectations with market considerations, ensuring employees felt rewarded while not diluting shareholder value excessively. The ESOP structure had to account for different employee categories, from senior management to clerical staff, each with different vesting schedules and exercise prices.

Marketing the IPO required careful messaging to different stakeholder groups. To policyholders, the message emphasized continuity—becoming a shareholder wouldn't affect policy benefits or service. To retail investors, the pitch focused on LIC's stability and dividend potential. To institutions, the emphasis was on growth potential and operational improvements. To employees and agents, the communication stressed that public listing would strengthen LIC, not weaken it. This multi-pronged communication strategy required careful coordination to avoid mixed messages.

The legal preparations for the IPO were extensive. LIC had to resolve numerous legacy legal issues, clarify property titles for its vast real estate portfolio, and ensure compliance with hundreds of regulations. The corporation's legal team, supplemented by external law firms, worked to create a corporate structure suitable for a listed entity while maintaining special provisions required by the LIC Act. The legal documentation for the IPO reportedly exceeded 10,000 pages, covering every conceivable contingency.

VIII. Post-IPO Reality & Current State (2022-Present)

The public issue of LIC IPO (LICI,543526) was offered at ₹949 per share and was listed at ₹872.00, resulting in a listing loss of -8.11%. With a minimum lot size of 15 shares, the IPO incurred a loss of ₹-1155 per lot on listing. The disappointing debut on May 17, 2022, sent shockwaves through the market and marked the beginning of a challenging journey for LIC as a publicly listed entity. The grey market premium, which had been positive before the listing, evaporated as global markets remained volatile and investor sentiment soured.

LIC is under extreme pressure, with its valuation plummeting by a staggering ₹2 trillion since its highly anticipated IPO (initial public offering) in May 2022. With an issue price of ₹949, LIC's market capitalization skyrocketed to an astounding ₹6,00,242 crore (₹6 trillion) on May 17, 2022, but has since experienced significant erosion. This dramatic destruction of value has raised fundamental questions about the corporation's ability to compete in a market that increasingly values growth and innovation over size and stability.

The post-IPO performance has been a sobering reality check for all stakeholders. Retail investors who had invested their savings based on trust in the LIC brand found themselves nursing losses. Policyholders who had become shareholders questioned whether the listing had been beneficial. The government, which had hoped to showcase LIC as a successful disinvestment story, faced criticism for the timing and execution of the IPO. The corporation's management found themselves under unprecedented scrutiny, with every business decision now subject to market judgment.

LIC market share declined from nearly 68% in September 2022 to 64% in February 2023. In contrast, the share of private insurers increased from nearly 32% to 36% during the same period. This accelerating market share loss post-IPO reflected multiple challenges. Private insurers, sensing opportunity in LIC's transition period, intensified their competitive efforts. They launched aggressive marketing campaigns, introduced innovative products, and leveraged LIC's distraction during the IPO process to win customers. The market share erosion was particularly pronounced in the high-margin segments that LIC had traditionally dominated.

The quarterly results announcements became moments of high drama, with the stock price showing extreme volatility around earnings releases. The market's reaction often seemed disconnected from fundamental performance, reflecting the challenge of educating investors about insurance company valuation. Metrics like Value of New Business (VNB), embedded value growth, and persistency ratios—standard in global insurance markets—were new to many Indian investors accustomed to simpler metrics like revenue and profit growth.

The regulatory changes implemented post-IPO added another layer of complexity to LIC's challenges. Effective 1 April 2023, the government eliminated the tax exemption on life insurance policies (other than ULIP) with an aggregate premium exceeding ₹500,000 (₹5 lakhs) per year. This change directly impacted LIC's high-value traditional policies, which had been sold primarily for tax benefits. The corporation had to quickly reorient its product mix and sales strategy, moving toward protection-oriented products that were less dependent on tax incentives.

The balancing act between government ownership and market expectations has proven to be LIC's most fundamental challenge. As a listed company, LIC is expected to maximize shareholder value, improve returns on equity, and maintain competitive growth rates. As a government-controlled institution, it's expected to fulfill social obligations, support government programs, and maintain services in unprofitable areas. These dual mandates often conflict, creating strategic dilemmas that private competitors don't face.