Gujarat Gas Limited: India's Natural Gas Distribution Giant

I. Introduction & Episode Overview

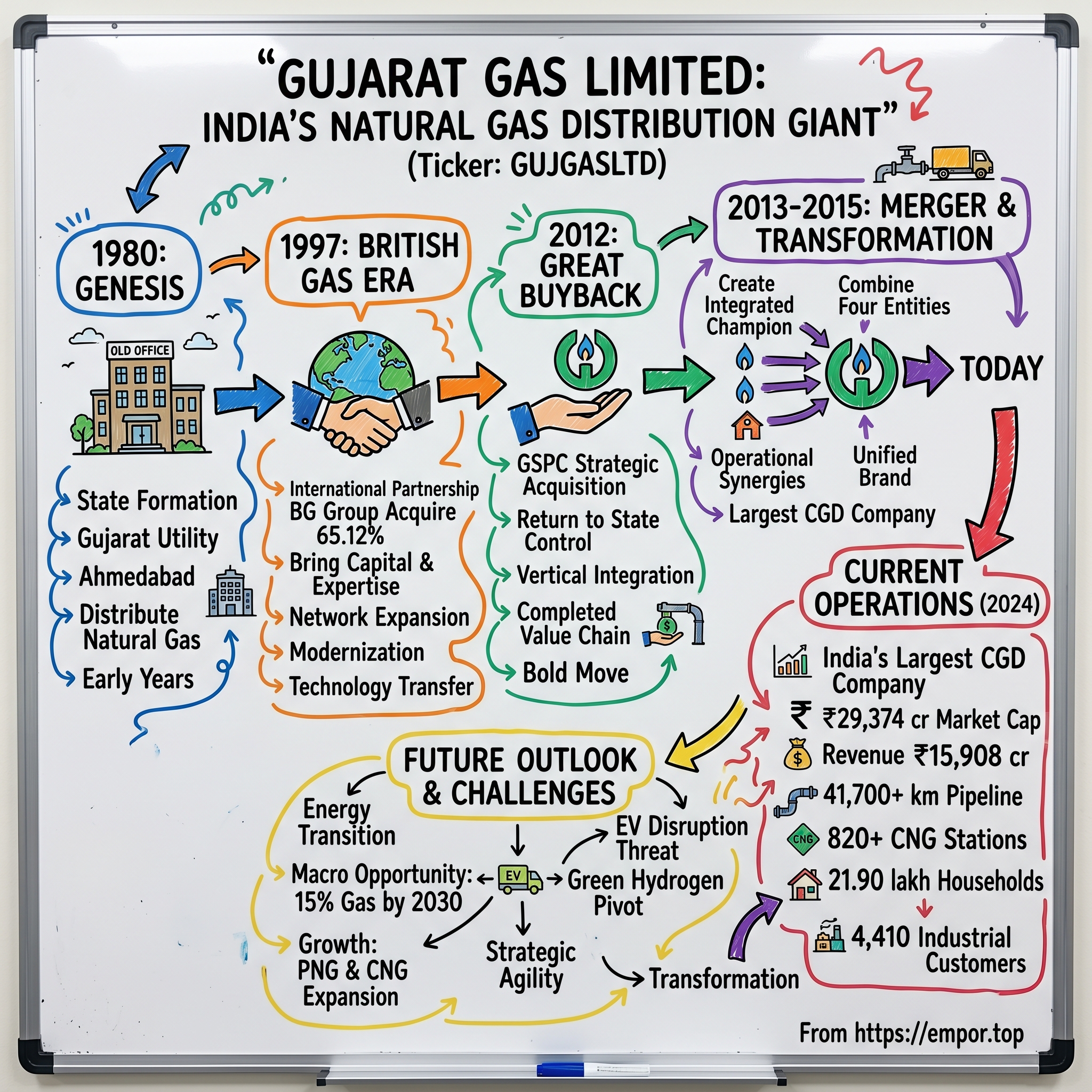

Picture this: It's 1980 in Ahmedabad, and a small team of bureaucrats is setting up what they believe will be a modest state utility company to distribute natural gas in Gujarat. Fast forward four decades, and that same entity—now Gujarat Gas Limited—commands a market capitalization of ₹29,374 crores, operates over 41,700 kilometers of pipeline network, and serves as India's largest city gas distribution company. The journey from that cramped government office to today's natural gas behemoth is a story of patience, timing, and the peculiar dynamics of Indian infrastructure capitalism.

Here's the provocative question that frames our entire analysis: How did a sleepy state-owned gas distributor, born in the socialist era of government control, navigate foreign ownership, return to state hands, and emerge as the dominant force in India's natural gas distribution sector? The answer isn't just about gas pipelines—it's about understanding how infrastructure businesses are built in emerging markets, how foreign capital and expertise can catalyze transformation, and why sometimes the tortoise beats the hare in the race for market dominance.

Gujarat Gas today stands as a colossus in India's energy landscape. With revenue of ₹15,908 crores, the company supplies piped natural gas to approximately 21.90 lakh households, runs 820 compressed natural gas stations, and serves over 15,470 commercial and 4,410 industrial customers across six states and one union territory. But these numbers only tell part of the story. The real narrative is about how a company can transform multiple times—from state entity to foreign-owned subsidiary to state-controlled champion—and emerge stronger each time.

The story we're about to unpack spans multiple eras of Indian economic history. We'll witness the socialist beginnings in 1980, when private enterprise in strategic sectors was viewed with suspicion. We'll explore the dramatic entry of British Gas in 1997, bringing international expertise and capital when India desperately needed both. We'll dive into the fascinating buyback by Gujarat State Petroleum Corporation in 2012—a ₹2,463.8 crore deal that brought the company back under state control. And we'll analyze the subsequent merger and transformation that created today's Gujarat Gas Limited.

What makes this story particularly compelling for investors and business strategists is how Gujarat Gas navigated each transition. Unlike the dramatic boom-and-bust cycles we often see in technology or consumer companies, Gujarat Gas represents a different playbook—one of steady infrastructure building, regulatory navigation, and patient capital deployment. It's a masterclass in how to build and scale a utility-like business in an emerging market, where the rules change, ownership structures shift, and yet the fundamental need for energy infrastructure only grows stronger.

As we journey through this multi-decade saga, we'll uncover several paradoxes. How did foreign ownership actually strengthen the company's eventual return to state control? Why did giving up control to British Gas prove to be the smartest move the Gujarat government made in the 1990s? How has a company dealing in fossil fuels positioned itself for India's green energy transition? And perhaps most intriguingly, how has Gujarat Gas built what might be one of India's most durable competitive moats in a sector that's supposedly commoditized?

The timing of this analysis couldn't be more relevant. As India targets increasing natural gas's share in its energy mix from the current 6-7% to 15% by 2030, and potentially 30% in the longer term, Gujarat Gas sits at the intersection of policy ambition and ground reality. The company isn't just distributing gas—it's building the physical infrastructure that will determine whether India's energy transition succeeds or stumbles.

Our exploration will take us through boardroom negotiations in London, the dusty construction sites of Gujarat's industrial corridors, the complex world of Indian energy regulation, and the high-stakes game of infrastructure financing. We'll meet the key players who shaped the company's destiny, understand the strategic decisions that mattered, and analyze the mistakes that almost derailed the journey.

This isn't just a corporate history—it's a window into how India's economy has evolved, how foreign investment has shaped domestic capabilities, and how patient, strategic thinking can build enduring value in sectors that many investors find too boring or too complex to understand. For those willing to look deeper, Gujarat Gas offers lessons that extend far beyond natural gas distribution.

So buckle up as we embark on this journey from a small state-owned utility to India's natural gas distribution champion. Along the way, we'll discover that sometimes the most powerful business stories aren't about disruption or innovation—they're about execution, timing, and the unglamorous work of building infrastructure that societies depend on. The Gujarat Gas story is ultimately about how a company can reinvent itself multiple times while never losing sight of its core mission: bringing clean, affordable energy to millions of Indians.

II. The Genesis: State Formation & Early Years (1980-1991)

The year was 1980, and India was a very different country. Indira Gandhi had just returned to power after the brief Janata Party interlude. The economy was firmly in the grip of the License Raj—that byzantine system of permits and controls that strangled enterprise. Private sector participation in strategic sectors like energy was not just discouraged; it was practically forbidden. Into this environment, Gujarat Gas Company Limited (GGCL) was born—not with fanfare or vision statements about transforming India's energy landscape, but as a practical response to a unique geological gift.

The story actually begins a few years earlier, in the mid-1970s, when the Oil and Natural Gas Corporation (ONGC) struck gold—or rather, gas—in the Cambay Basin of Gujarat. The discovery of substantial natural gas reserves near Ankleshwar and other fields presented both an opportunity and a challenge. Here was clean, abundant energy literally bubbling up from Gujarat's soil, but how to get it to industries and homes? The existing oil companies were focused on petroleum products. The electricity boards dealt with power generation. Who would build the pipes, compressor stations, and distribution networks needed to harness this resource?

The Gujarat government's answer was characteristically pragmatic: create a state-owned company specifically for this purpose. On a humid August day in 1980, Gujarat Gas Company Limited was incorporated, with a modest authorized capital and a mandate that seemed straightforward—procure natural gas from ONGC and distribute it to industrial and domestic consumers. The founding team, a mix of bureaucrats and engineers borrowed from other state enterprises, set up shop in a nondescript government building in Gandhinagar.

What's fascinating about this period is how different the energy landscape looked. Natural gas was still viewed as a byproduct of oil exploration—useful, but not central to India's energy strategy. Coal was king, petroleum products dominated transportation, and electricity meant either hydro or thermal power. The idea that natural gas could become a mainstream fuel for vehicles, homes, and industries seemed almost fantastical. Yet the Gujarat government, perhaps more by accident than design, was positioning itself at the forefront of what would become a global energy transition.

The early years were about learning by doing. The first challenge was technical: how to build a gas distribution network from scratch? Unlike electricity, which had established engineering practices, or water distribution, which municipalities had managed for decades, city gas distribution was terra incognita in India. The initial team had to figure out everything—from the optimal pipeline pressure for different consumer categories to the safety protocols for household connections. They studied international models, particularly from Europe and Japan, adapting them to Indian conditions where safety standards were lax and consumer awareness about gas handling was virtually non-existent.

The company's first major project was connecting industries in the Ankleshwar-Bharuch belt to the ONGC gas fields. These early industrial customers—textile mills, chemical plants, ceramic factories—were desperate for a cleaner alternative to coal and furnace oil. The economics were compelling: natural gas was not only cleaner but often cheaper than alternatives, especially for processes requiring precise temperature control. By 1985, GGCL had laid its first 100 kilometers of pipeline and connected over 50 industrial units.

But the real ambition lay in city gas distribution—bringing piped natural gas (PNG) to homes and compressed natural gas (CNG) to vehicles. This was where the company faced its steepest learning curve. How do you convince a housewife comfortable with her LPG cylinder to switch to piped gas? How do you ensure safety when running gas lines through densely populated areas where unauthorized construction is rampant? The company's engineers became evangelists, conducting thousands of safety demonstrations, working with local communities, and slowly building trust.

The financial model in these early years was curious. As a state-owned entity, GGCL wasn't primarily driven by profit maximization. The pricing was regulated, with industrial users effectively cross-subsidizing domestic consumers. The company operated more like a public utility than a commercial enterprise, with employment generation and social objectives often taking precedence over efficiency. Yet this approach had an unexpected benefit—it allowed GGCL to take a long-term view, investing in infrastructure that wouldn't pay back for years, even decades.

By the late 1980s, the company had established a solid foundation. The network had expanded to cover major industrial clusters in South Gujarat, and the first residential colonies in Ahmedabad and Surat were receiving piped gas. The technical expertise developed during this period—in pipeline engineering, safety management, and customer service—would prove invaluable in the years ahead. More importantly, GGCL had demonstrated that city gas distribution was viable in India, creating a template that would later be replicated across the country.

Then came 1991—a watershed year for both India and Gujarat Gas. In July, India faced its worst balance of payments crisis, forcing the government to liberalize the economy. The License Raj began its slow dismantling, foreign investment was cautiously welcomed, and state-owned enterprises were pushed to become more commercial. For GGCL, this meant a fundamental shift in approach. The company decided to go public, listing on both the Bombay Stock Exchange and the National Stock Exchange in October 1991.

The timing of this IPO is worth examining. Here was a state-owned company, operating in a strategic sector, going public just months after India's economic liberalization. The offering was modest—raising capital primarily for network expansion—but it signaled something profound. GGCL was acknowledging that the old model of complete state control was ending. To grow and compete in the new India, it would need private capital, market discipline, and eventually, perhaps, a strategic partner who could bring international expertise.

The IPO was reasonably successful, though not spectacular. Institutional investors were intrigued by the infrastructure play and the Gujarat government's continued backing. Retail investors were more skeptical—natural gas was still an unfamiliar commodity, and the company's expansion plans seemed ambitious. The stock traded sideways for several years, reflecting this uncertainty. Little did anyone know that this public listing would set the stage for one of the most interesting foreign investment stories in India's infrastructure sector.

Looking back at this first decade, what strikes you is the patient, almost plodding nature of the company's development. There were no hockey stick growth curves, no dramatic pivots, no charismatic founders making bold proclamations. Just steady, methodical building of pipes, compressor stations, and customer connections. Yet this unglamorous foundation-laying would prove crucial. When British Gas came calling in 1997, they found not a broken state enterprise needing rescue, but a functioning utility with real assets, technical expertise, and market position. The genesis period had created something valuable—it just needed the right catalyst to unlock its potential.

III. The British Gas Era: International Partnership (1997-2012)

The boardroom at British Gas headquarters in London was buzzing with nervous energy in early 1997. Spread across the mahogany table were maps of India, feasibility studies, and financial projections that painted a tantalizing picture. India's economy was opening up, energy demand was soaring, and here was an opportunity to acquire a controlling stake in an established gas distribution company with monopoly-like characteristics in one of India's most industrialized states. For British Gas—soon to become BG Group—this wasn't just another acquisition. It was their big bet on the Asian growth story.

The backstory of how British Gas ended up in Gujarat is quintessentially 1990s. Following Margaret Thatcher's privatization wave, British Gas had transformed from a sleepy state utility into an aggressive international player. By the mid-1990s, CEO David Varney and his team were scouring emerging markets for growth opportunities. They had already made moves in Latin America and Southeast Asia. India, with its billion-plus population and chronic energy deficit, represented the ultimate prize. But entering India's complex market required a local partner, existing infrastructure, and regulatory relationships. GGCL checked all three boxes.

The negotiations were a fascinating dance of cultures and expectations. On one side sat British Gas executives, armed with McKinsey presentations and discounted cash flow models. On the other, Gujarat government officials who viewed GGCL as more than just a commercial asset—it was critical infrastructure, a source of employment, and a symbol of state capability. The discussions went on for months, with multiple rounds in London, Mumbai, and Gandhinagar. The sticking points were predictable yet profound: How much control would British Gas have? What about employment guarantees for existing staff? How would pricing be determined for consumers?

The deal structure that emerged was clever. British Gas would acquire a 65.12% stake, giving them clear control, while the Gujarat government retained a significant minority position. This wasn't a complete exit by the state—it was a partnership where British Gas brought capital and expertise while the government provided regulatory air cover and local credibility. The price tag of approximately $200 million seemed steep for a company with limited profits, but British Gas was betting on the future, not the present.

When the deal closed in late 1997, the transformation began almost immediately. British Gas deployed a team of international experts to Gujarat—engineers who had built gas networks in Argentina, commercial specialists from Southeast Asian operations, and safety experts from the UK. The culture shock was immediate and sometimes comical. British managers accustomed to punctual meetings and written protocols encountered the more fluid Indian business environment where relationships mattered more than PowerPoints and chai breaks could stretch indefinitely.

But beneath these surface frictions, serious capability building was underway. British Gas introduced international safety standards that were revolutionary for India at the time. They implemented SCADA (Supervisory Control and Data Acquisition) systems for remote pipeline monitoring—technology that was cutting-edge globally and unheard of in Indian gas distribution. They brought in modern customer management systems, replacing paper ledgers with computerized billing. Perhaps most importantly, they introduced a commercial mindset that balanced public service with profitability.

The expansion under British Gas was methodical and impressive. The pipeline network, which stood at roughly 1,000 kilometers in 1997, expanded to over 15,000 kilometers by 2010. The number of domestic connections grew from a few thousand to over 300,000. CNG stations, virtually non-existent in 1997, numbered in the hundreds by the end of British Gas's tenure. This wasn't just growth—it was the creation of an entirely new energy ecosystem in Gujarat.

The technology transfer during this period deserves special attention. British Gas didn't just bring equipment; they brought knowledge. They established training centers where Indian engineers learned advanced pipeline welding techniques, gas chromatography, and network optimization. They introduced predictive maintenance protocols that reduced system downtime. They implemented environmental monitoring systems that exceeded Indian regulatory requirements. Many of the Indian engineers trained during this period would later become industry leaders, spreading these practices across India's gas sector.

Yet the British Gas era wasn't without its challenges and contradictions. The foreign ownership created political sensitivities, especially when consumer price increases were proposed. Local competitors and critics questioned why a British company should profit from Indian natural resources. Labor unions worried about job losses from efficiency improvements. The Gujarat government, caught between its roles as regulator and minority shareholder, often found itself in awkward positions.

The regulatory environment during this period was particularly complex. The Petroleum and Natural Gas Regulatory Board (PNGRB) was still being established, creating uncertainty about future rules. Pricing mechanisms were opaque, with different rates for different consumer categories and frequent government interventions. British Gas had to navigate not just commercial challenges but also the delicate politics of energy pricing in a democratic developing country where cooking gas prices could trigger street protests.

One of the most interesting strategic decisions during the British Gas era was the focus on CNG infrastructure. In the early 2000s, the Supreme Court of India mandated CNG conversion for public transport in major cities to combat air pollution. British Gas saw this as an opportunity and aggressively built CNG stations across Gujarat. They worked with automobile manufacturers to develop CNG kits, provided financing for rickshaw drivers to convert their vehicles, and even ran public awareness campaigns about the environmental benefits of natural gas. This early mover advantage in CNG would prove invaluable in later years.

The financial performance under British Gas was solid if not spectacular. Revenues grew steadily, driven by volume expansion and periodic tariff increases. Profitability improved as operational efficiencies kicked in and the customer base expanded. The company started paying regular dividends, something unimaginable in the state-owned era. By 2010, GGCL was generating returns on equity in the mid-teens—respectable for a utility-like business.

But by 2011, the winds were shifting at BG Group's global headquarters. The company was restructuring, focusing on upstream exploration and production rather than downstream distribution. The shale gas revolution in the United States was changing global energy dynamics. BG Group needed capital for massive LNG projects in Australia and Brazil. The Indian distribution business, while profitable, was no longer core to their strategy. The decision to exit was strategic, not a reflection on GGCL's performance.

The announcement in 2012 that BG Group would sell its stake sent ripples through India's business community. Here was a successful foreign investment story potentially ending. Who would buy? Would another international player step in? Chinese companies were rumored to be interested. Indian private sector giants like Reliance and Adani were mentioned. But in a twist that surprised many, it would be the Gujarat government, through GSPC, that would bring the company back home.

Looking back, the British Gas era was transformative in ways that went beyond financial metrics. It demonstrated that foreign investment in Indian infrastructure could work—that international expertise and local knowledge could create value for all stakeholders. It showed that a state-owned enterprise could be modernized without mass layoffs or social disruption. Most importantly, it built capabilities and infrastructure that would position Gujarat Gas for its next phase of growth. The British had come, built, and were now leaving—but their legacy would endure in the pipes, processes, and people they left behind.

IV. The Great Buyback: GSPC's Strategic Acquisition (2012)

The conference room on the 15th floor of GSPC Bhavan in Gandhinagar was thick with tension on that September morning in 2012. D.J. Pandian, the IAS officer heading Gujarat State Petroleum Corporation, sat across from a team of investment bankers, lawyers, and advisors. The numbers on the presentation screen were staggering: ₹2,463.8 crore for a 65.12% stake—₹295 per share. This would be one of the largest acquisitions by an Indian state-owned enterprise, and the stakes couldn't be higher. The question hanging in the air wasn't whether they could afford it, but whether they should. Was bringing Gujarat Gas back under state control a strategic masterstroke or expensive nostalgia?

The backstory of GSPC's interest requires understanding the unique ecosystem that Gujarat had built around natural gas. By 2012, GSPC had evolved from a small state exploration company into a significant player across the gas value chain. They had discovered gas fields (though some would prove disappointing), built the Gujarat State Petronet Limited (GSPL) as a transmission company, and were trading gas through GSPC Gas. What they lacked was the last mile—distribution to end consumers. The opportunity to acquire GGCL wasn't just about buying a company; it was about completing a vertical integration strategy that had been years in the making.

The negotiation with BG Group was a masterclass in cross-border dealmaking. BG Group, under pressure from shareholders to focus on upstream assets, wanted a clean exit at a fair price. They had received expressions of interest from multiple parties—Indian conglomerates, infrastructure funds, even some Chinese companies sniffing around. But GSPC had unique advantages. As a state entity, they could move quickly without lengthy board approvals. They understood the regulatory landscape intimately. Most crucially, they could offer BG Group something others couldn't: a smooth transition without political complications.

The valuation exercise was particularly intricate. How do you value a utility with regulated returns but growing volumes? The bankers built complex models factoring in future gas availability, demographic trends, vehicle conversion rates to CNG, and industrial growth in Gujarat. The ₹295 per share price represented a premium to the market price but a discount to replacement cost—building similar infrastructure from scratch would cost multiples of the acquisition price. For GSPC, this wasn't just a financial investment but strategic infrastructure that would take decades to replicate.

What made this acquisition particularly bold was GSPC's own financial position. The company had made aggressive bets on oil and gas exploration, including the controversial KG Basin blocks that would later prove problematic. Taking on ₹2,463.8 crore in additional commitment required careful financial engineering. They structured a combination of debt and internal accruals, with implicit backing from the Gujarat government. The rating agencies were watching nervously—would this acquisition stretch GSPC too thin?

The regulatory approvals process revealed the complexity of the deal. The Competition Commission of India had to evaluate whether the vertical integration would create unfair advantages. The Ministry of Petroleum and Natural Gas needed to ensure continuity of gas supply. PNGRB wanted assurances about maintaining service quality and expansion commitments. Foreign Investment Promotion Board clearances were needed for BG Group's exit. Each approval came with conditions, undertakings, and timelines that added layers to an already complex transaction.

The October 2012 announcement of the deal created waves in multiple constituencies. The stock market reaction was mixed—GGCL shares jumped on the buyout premium, while questions emerged about minority shareholder treatment. Business newspapers debated whether state ownership would mean a return to inefficiency. Environmental groups worried about commitment to cleaner fuel promotion. Employees wondered about job security and career prospects under new management.

But perhaps the most interesting reactions came from competitors and industry observers. Indraprastha Gas Limited, operating in Delhi, saw this as potential state-backed competition. Private players hoping to enter Gujarat's gas distribution market realized they would now face an integrated incumbent with gas sourcing, transmission, and distribution capabilities. International investors questioned whether this represented a broader trend of resource nationalism in India.

The strategic rationale that GSPC articulated was compelling. By owning the entire value chain from gas trading through transmission to distribution, they could optimize operations, reduce transaction costs, and ensure supply security for Gujarat's consumers. They painted a vision of Gujarat as India's gas hub—leveraging its coastal position for LNG imports, its industrial base for demand, and now its integrated infrastructure for efficient delivery. The acquisition wasn't just about buying assets; it was about creating a energy ecosystem.

The transition planning between signing and closing was meticulous. Teams from GSPC and BG Group worked on knowledge transfer, ensuring that critical expertise wouldn't walk out the door with the British management. Key local managers were retained with enhanced responsibilities. Technology transfer agreements were negotiated to ensure continued access to BG Group's global technical resources during a transition period. Customer service protocols were documented to maintain quality standards.

The financing structure deserves special attention. While the headline number was ₹2,463.8 crore, the actual cash outflow was managed through sophisticated structuring. GSPC used a combination of bridge loans, later replaced by longer-term debt, and dividend flows from GGCL itself to service the acquisition debt. This financial engineering meant that the acquisition was largely self-financing within a few years—a fact that vindicated the premium paid.

The integration challenges were real but manageable. GSPC Gas and GGCL had different corporate cultures—one a trading company with an entrepreneurial spirit, the other a utility with operational excellence. Salary structures needed harmonization. IT systems required integration. Procurement processes had to be aligned. But the shared Gujarat roots and common mission of energy security created enough common ground for successful integration.

An underappreciated aspect of the acquisition was its timing relative to India's energy landscape. In 2012, India was facing severe coal shortages, imported LNG prices were rising, and domestic gas production was disappointing. The government was pushing for increased gas usage to reduce pollution and import dependence. By securing GGCL, GSPC positioned itself at the center of India's energy transition—a prescient move considering the policy support that would follow.

The deal also highlighted the evolving nature of state capitalism in India. This wasn't the heavy-handed nationalization of the 1970s but a sophisticated commercial transaction where a state entity competed with private players and won. GSPC paid market price, respected minority shareholders, and maintained operational continuity. It showed that state ownership could be strategic and efficient—a lesson that would influence similar transactions across India.

By early 2013, as the acquisition completed and integration began, the wisdom of the buyback was becoming apparent. Gas allocation policies favored city gas distribution, giving GGCL preferential access to domestic gas. The vertical integration synergies started materializing through better capacity utilization and reduced transaction costs. Most importantly, Gujarat Gas was now positioned for its next transformation—a merger that would create India's largest city gas distribution company.

The great buyback of 2012 stands as a pivotal moment in Gujarat Gas's history. It brought the company full circle—from state ownership through foreign partnership back to state control, but at each stage adding capabilities and value. The ₹2,463.8 crore price tag that seemed steep in 2012 looks like a bargain in hindsight, considering Gujarat Gas's current market capitalization of ₹29,374 crores. It proved that sometimes, the best acquirer of a strategic asset is the entity that understands its value beyond financial metrics—its role in economic development, energy security, and industrial competitiveness.

V. The Merger & Transformation (2013-2015)

The legal documents stacked on the lawyer's desk in early 2013 were mind-numbingly complex. The Composite Scheme of Amalgamation and Arrangement ran to hundreds of pages, detailing how four different entities—GSPC Gas Company Limited, Gujarat Gas Company Limited, Gujarat Gas Financial Services Limited, and Gujarat Gas Trading Company Limited—would be merged into a single entity. For the legal teams, investment bankers, and accountants, this was a challenging puzzle of share swaps, valuation adjustments, and regulatory approvals. But for D.J. Pandian and his leadership team at GSPC, this was about something much bigger: creating India's first truly integrated city gas distribution champion.

The logic behind the merger was elegant in its simplicity, even if the execution was anything but simple. GSPC Gas brought gas sourcing and trading capabilities. GGCL had the distribution infrastructure and customer base. Gujarat Gas Financial Services offered financial products to customers for vehicle conversion and equipment purchase. Gujarat Gas Trading Company handled spot market transactions. Separately, each was successful but subscale. Together, they could create something formidable—a fully integrated gas company that could source, transport, distribute, and finance natural gas solutions.

The merger process began with a fundamental question: what structure would create maximum value? The advisors presented multiple options—a holding company structure, sequential mergers, or an all-in-one amalgamation. After months of analysis, they chose the boldest path: a simultaneous four-way merger with retrospective effect from April 1, 2013. This would create immediate synergies but required threading the needle through multiple regulatory frameworks, shareholder constituencies, and operational complexities.

The valuation exercise for the share swap ratios was particularly contentious. Each company had different shareholder bases, asset profiles, and growth trajectories. The merchant bankers had to develop a formula that was fair to all stakeholders while creating a coherent capital structure for the merged entity. They used a combination of methodologies—asset values, earnings multiples, discounted cash flows—to arrive at swap ratios. The fact that GSPC controlled all entities helped, but minority shareholders in each company scrutinized every calculation.

The Gujarat High Court proceedings for the merger approval revealed the complexity of the transaction. The court-appointed observer raised pointed questions: Would the merger create anti-competitive effects? Were minority shareholders being treated fairly? How would employee interests be protected? The legal teams presented volumes of evidence, expert testimonies, and fairness opinions. The court hearings stretched over months, with multiple stakeholders—from competitor gas companies to consumer groups—presenting their views.

What made this merger particularly interesting was its operational complexity. Unlike financial mergers where you're mainly combining balance sheets, this involved integrating physical infrastructure, customer databases, billing systems, and operational protocols. The GSPC Gas trading desk had to be merged with GGCL's gas procurement team. The financial services arm's loan portfolio had to be integrated with the main company's books. Different IT systems running on different platforms needed harmonization.

The human dimension of the merger was carefully managed but still challenging. Each company had its own culture and power structures. GSPC Gas traders, used to the fast-paced world of spot markets, had to work with GGCL engineers focused on operational reliability. Salary disparities needed addressing—the trading company paid market rates while the distribution company followed public sector norms. The leadership team conducted town halls, one-on-one meetings, and cultural integration workshops to build a unified identity.

The regulatory approvals came in waves through 2014 and early 2015. PNGRB needed assurance that the merger wouldn't affect service quality or expansion obligations. The Ministry of Corporate Affairs scrutinized the scheme for compliance with the Companies Act. The stock exchanges required detailed disclosures about the impact on listed entities. Each approval came with conditions and timelines that needed careful tracking and compliance.

By May 2015, as the final approvals came through, the company made a symbolic but important decision: to rename itself simply as Gujarat Gas Limited. Dropping the various subsidiary names and creating a unified brand was about more than marketing. It signaled the transformation from a collection of related companies to a single, integrated entity. The new logo, corporate colors, and brand identity were carefully chosen to reflect both heritage and ambition.

The immediate post-merger period was about realizing quick wins to justify the complex restructuring. The integrated gas sourcing capability immediately showed benefits—the company could optimize between long-term contracts, spot purchases, and different gas sources. The combined customer base created economies of scale in operations and maintenance. The unified balance sheet enabled better financing terms for expansion projects. Within months, the synergy benefits were exceeding projections.

The transformation went beyond just operational integration. The merged entity adopted a new strategic vision: to be not just Gujarat's gas company but a national player. With the combined capabilities and balance sheet strength, Gujarat Gas could now bid for city gas distribution licenses outside Gujarat. The company developed a war chest for expansion, identified target geographies, and built teams for multi-state operations.

The technology integration during this period was particularly noteworthy. The company invested heavily in creating a unified ERP system, customer relationship management platform, and geographic information system for network planning. They introduced mobile apps for customer service, automated meter reading systems, and predictive analytics for demand forecasting. This digital backbone would prove crucial for managing the rapid expansion that followed.

The financial engineering of the merger created interesting opportunities. The combined entity's improved credit profile allowed for refinancing existing debt at lower rates. The larger balance sheet enabled access to international markets, with the company exploring dollar bonds and ECB financing. The improved stock liquidity post-merger attracted institutional investors, including foreign portfolio investors who had previously ignored the smaller entities.

An underappreciated aspect of the merger was its impact on talent retention and attraction. The larger, integrated company could offer better career paths, attracting experienced professionals from oil majors and infrastructure companies. The company established a management training program, partnering with international gas companies for expertise exchange. This human capital development would prove crucial for the expansion phase ahead.

The merger also positioned Gujarat Gas advantageously for regulatory changes. The government was moving toward unified licensing for city gas distribution, favoring integrated players over fragmented operators. The company's demonstrated capability to execute complex integration while maintaining service quality became a competitive advantage in bidding for new licenses.

By the end of 2015, the transformation was complete. What had started as four separate entities with combined revenues of around ₹8,000 crores had become a unified company already showing improved margins and accelerated growth. The stock price, which had languished during the uncertainty of the merger process, began its upward trajectory. More importantly, Gujarat Gas had created a template for consolidation in India's fragmented gas distribution sector.

The 2013-2015 merger and transformation period stands as a masterclass in corporate restructuring. It showed that complex, multi-entity mergers could be executed in India's challenging regulatory environment. It demonstrated that state-owned entities could undertake sophisticated financial engineering. Most importantly, it created a platform for the next phase of growth—the massive infrastructure expansion that would establish Gujarat Gas as India's undisputed city gas distribution leader. The legal complexity and operational challenges of the merger would fade from memory, but the integrated powerhouse it created would define India's gas distribution landscape for decades to come.

VI. The Infrastructure Boom: Building India's Gas Grid (2015-2020)

The construction site on the outskirts of Morbi in 2016 was a hive of activity. Giant steel pipes, each weighing several tons, lay stacked like enormous cigarettes. Welding sparks flew as workers joined sections together, while engineers with tablets tracked every weld, every joint, every meter of progress. This wasn't just pipeline construction—it was the physical manifestation of India's energy transition. By 2020, Gujarat Gas would operate approximately 41,700 kilometers of pipeline network, a figure that sounds abstract until you realize it's enough to circle the Earth at the equator. The story of how this infrastructure explosion happened reveals both the ambition and execution capability that set Gujarat Gas apart.

The infrastructure boom didn't happen by accident. Post-merger, the company's leadership made a strategic decision: dominate through network effects. Every kilometer of pipeline laid, every CNG station opened, every household connected made the network more valuable. This wasn't just about first-mover advantage—it was about creating switching costs so high that competition became economically unviable. The board approved capital expenditure plans that seemed audacious: ₹1,000+ crores annually for network expansion. For context, this was more than many Indian infrastructure companies' entire market capitalization.

The expansion strategy revealed sophisticated thinking about infrastructure economics. The company divided territories into three categories: core markets in Gujarat where they had monopoly-like positions, growth markets in adjacent states where they had won licenses, and frontier markets where they were building beachheads. Each required different approaches. In core markets, the focus was on densification—connecting every possible customer to maximize asset utilization. In growth markets, they built backbone infrastructure first, accepting years of losses before customer density made them profitable. In frontier markets, they cherry-picked industrial corridors and CNG opportunities.

The numbers tell only part of the story. By 2020, the company was supplying piped natural gas to approximately 21.90 lakh households—but each connection represented a small drama. Picture the scene in a middle-class apartment complex in Ahmedabad: residents debating in their society meetings whether to allow pipeline installation, concerns about safety, questions about cost savings. Gujarat Gas teams would conduct hundreds of such meetings, addressing fears, demonstrating safety features, sometimes cooking live demonstrations to show the superiority of natural gas over LPG. This grassroots evangelism, repeated thousands of times, built the residential network.

The compressed natural gas infrastructure deserves special attention. By 2020, Gujarat Gas operated 820 CNG stations—more than most countries have in total. But the locations weren't random. The company used sophisticated geographic information systems, traffic pattern analysis, and predictive modeling to identify optimal locations. They pioneered the concept of "mother-daughter" stations—large mother stations on highways feeding smaller daughter stations in city centers through cascades. This innovation reduced land requirements and capital costs while maintaining service coverage.

The industrial and commercial customer acquisition told a different story. Here, the company leveraged Gujarat's manufacturing prowess. With approximately 15,470 commercial and 4,410 industrial customers by 2020, Gujarat Gas became indispensable to the state's economy. Ceramic manufacturers in Morbi, textile mills in Surat, chemical plants in Vapi—each had specific requirements. The company developed expertise in understanding industrial processes, offering customized solutions beyond just gas supply. They would advise on burner optimization, provide energy audits, and even help with environmental compliance.

The geographic expansion beyond Gujarat was perhaps the boldest move. By 2020, Gujarat Gas operated in Maharashtra, Punjab, Madhya Pradesh, Rajasthan, Haryana, and the Union Territory of Dadra and Nagar Haveli and Daman and Diu. Each state presented unique challenges. In Punjab, they had to navigate agricultural politics where farmers received subsidized power. In Maharashtra, they competed with established players like Mahanagar Gas. In Rajasthan, they dealt with vast distances and lower population density. The company developed a playbook: enter through industrial areas, build CNG infrastructure along highways, then gradually expand into city gas distribution.

The technology deployment during this period transformed Gujarat Gas from a utility into a tech-enabled infrastructure company. They implemented SCADA systems across the network, enabling real-time monitoring from centralized control rooms. Imagine operators in Gandhinagar watching pressure levels in pipelines hundreds of kilometers away, detecting leaks before they become problems, optimizing gas flows based on demand patterns. The company also pioneered the use of horizontal directional drilling for laying pipelines without disrupting urban areas—a technique that reduced both costs and public inconvenience.

The financing of this infrastructure boom required creative financial engineering. The company tapped multiple sources: internal accruals from the growing customer base, debt from banks and financial institutions, and strategic use of government subsidies and viability gap funding. They structured special purpose vehicles for specific projects, used infrastructure debt funds, and even explored infrastructure investment trusts. The debt-to-equity ratio was carefully managed, never exceeding levels that would concern rating agencies or investors.

The competitive dynamics during this period were fascinating. The Petroleum and Natural Gas Regulatory Board had opened city gas distribution to competition, conducting regular bidding rounds. Gujarat Gas participated aggressively, leveraging its operational expertise and balance sheet strength. But they also faced new competitors—Adani Gas, Torrent Gas, Indian Oil-Adani Gas joint venture. The bidding became increasingly competitive, with companies offering to connect more customers faster and accepting lower regulated returns. Gujarat Gas's advantage lay in execution capability—they could actually deliver on aggressive bid commitments.

The regulatory environment evolution shaped infrastructure development. PNGRB's regulations on technical standards, safety norms, and third-party access created a level playing field but also raised compliance costs. The company had to maintain detailed documentation for every kilometer of pipeline, every customer connection, every safety inspection. They built specialized teams for regulatory compliance, turning what could have been a burden into a competitive advantage through superior processes and systems.

An overlooked aspect of the infrastructure boom was its employment impact. Gujarat Gas became one of the state's largest employers, with thousands of direct employees and tens of thousands of indirect jobs through contractors, dealers, and service providers. They established training institutes for pipeline welders, gas fitters, and safety inspectors. This created a skilled workforce ecosystem that further reinforced their competitive advantage—competitors couldn't easily replicate this human infrastructure.

The environmental narrative became increasingly important during this period. As India faced severe air pollution challenges, natural gas emerged as a transition fuel. Gujarat Gas positioned itself as an environmental solutions provider, not just a gas distributor. They published sustainability reports, tracked carbon emission reductions, and worked with customers on environmental compliance. The company calculated that their gas supply prevented millions of tons of CO2 emissions compared to alternative fuels—a powerful narrative for ESG-conscious investors.

The market dynamics data revealed the sector's potential. The India City Gas Distribution market was expected to grow from USD 11.33 billion in 2025 at a CAGR of 13.06% to reach USD 20.93 billion by 2030. Within this, CNG emerged as the dominant segment, commanding approximately 55% market share. Gujarat state led with over 19% of India's CNG stations. These weren't just statistics—they represented a fundamental shift in India's energy consumption patterns, with Gujarat Gas at the forefront.

By 2020, as the infrastructure boom phase concluded, Gujarat Gas had transformed from a regional player into a national infrastructure company. The 41,700 kilometers of pipeline network weren't just steel and welds—they were the arteries of a new energy ecosystem. The 820 CNG stations weren't just fuel dispensers—they were nodes in a transportation revolution. The 21.90 lakh household connections weren't just customer numbers—they represented millions of families accessing cleaner, cheaper energy.

The infrastructure boom of 2015-2020 will be remembered as Gujarat Gas's golden period of physical expansion. But more than the impressive statistics, this period demonstrated something profound: that Indian companies could build world-class infrastructure at scale, that patient capital deployed wisely could create lasting value, and that the unglamorous work of laying pipes and connecting homes could be transformational for both company and country. As the company entered the 2020s, the question was no longer whether it could build infrastructure, but how it would leverage this vast network in an energy landscape increasingly shaped by climate concerns and technological disruption.

VII. Market Dynamics & Competition

The war room at Indraprastha Gas Limited's Delhi headquarters in 2019 was tense. On the screens were maps of India showing city gas distribution territories, color-coded by operator. Gujarat Gas's green dominated western India, while IGL's blue controlled the national capital region. But the white spaces—untapped territories up for bidding—were shrinking fast. The CEO turned to his strategy team: "Gujarat Gas just bid aggressively for 11 new geographic areas. How do we respond?" This scene, replicated across boardrooms from Mahanagar Gas in Mumbai to GAIL Gas in Delhi, captured the fierce competition reshaping India's gas distribution landscape.

Understanding the competitive dynamics requires grasping the market structure's evolution. Until 2008, city gas distribution was essentially a series of regional monopolies. Each company operated in its territory without competition. The Petroleum and Natural Gas Regulatory Board's establishment changed everything. PNGRB introduced competitive bidding for new areas and, more controversially, concepts of third-party access to existing infrastructure. Suddenly, what had been comfortable monopolies became contested territories.

The numbers tell a story of explosive growth and intense competition. The India City Gas Distribution market, expected to reach USD 11.33 billion in 2025 and grow at 13.06% CAGR to USD 20.93 billion by 2030, attracted everyone from oil marketing companies to infrastructure funds. The competitive landscape crystallized around five major players: Gujarat Gas, Indraprastha Gas Limited, Mahanagar Gas Ltd, GAIL Gas Limited, and the Indian Oil-Adani Gas joint venture. Each brought different strengths—IGL had first-mover advantage in Delhi, Mahanagar Gas dominated Mumbai, GAIL had gas sourcing advantages, and Indian Oil-Adani combined fuel retailing expertise with infrastructure execution capability.

Gujarat Gas's competitive strategy was built on three pillars: operational excellence, financial strength, and regulatory navigation. On operational excellence, they had the lowest connection costs per customer, fastest rollout times, and highest safety standards. Their financial strength allowed aggressive bidding—they could accept lower returns knowing operational efficiency would eventually deliver profitability. On regulatory navigation, their long history meant deep relationships and understanding of the regulatory mindset.

The bidding rounds conducted by PNGRB became increasingly sophisticated and competitive. Companies had to commit to minimum work programs—number of household connections, CNG stations, pipeline kilometers—within specified timeframes. The winner was selected based on the highest net present value of proposed work program. This created an interesting dynamic: companies bid aggressively to win territories, then had to execute flawlessly to avoid penalties. Gujarat Gas's advantage lay in its proven execution capability—when they committed to connecting 100,000 households in three years, regulators knew they would deliver.

The CNG segment emerged as the primary battlefield. With CNG commanding approximately 55% of the city gas distribution market, control of CNG infrastructure meant market dominance. Gujarat alone had over 19% of India's CNG stations, with Gujarat Gas operating the majority. The economics were compelling: CNG stations generated immediate cash flows, created customer stickiness, and built brand visibility. The competition for prime locations—highway junctions, city centers, transport hubs—was fierce, with companies sometimes bidding multiples of rational valuations for strategic sites.

The pricing dynamics revealed the sector's complexity. While infrastructure was increasingly competitive, gas pricing remained partially regulated. Priority sectors like domestic households and CNG received allocation of cheaper domestic gas, while industrial users paid market prices. This created cross-subsidy mechanisms where industrial margins supported domestic expansion. Companies with better industrial-residential mix, like Gujarat Gas, had advantages. The government's various pricing formulas—APM gas, non-APM gas, imported LNG—created arbitrage opportunities for sophisticated players.

The technology race became a differentiator. Gujarat Gas invested heavily in digital infrastructure—mobile apps for customer service, IoT sensors for pipeline monitoring, AI for demand forecasting. Competitors responded with their own technology initiatives. IGL launched automated CNG stations. Mahanagar Gas introduced prepaid PNG cards. The technology wasn't just about efficiency—it was about customer acquisition and retention in an increasingly competitive market.

The entry of new players added complexity. Torrent Gas, leveraging its power distribution experience, entered city gas distribution. Adani Gas, before merging with Indian Oil, bid aggressively for new territories. Think Gas, backed by private equity, targeted tier-2 cities. Each new entrant brought fresh capital and different approaches, forcing incumbents to innovate. Gujarat Gas responded by accelerating expansion, improving service quality, and exploring adjacent opportunities like electric vehicle charging.

The regulatory evolution continued shaping competition. PNGRB's infrastructure sharing regulations meant incumbents had to provide access to their pipelines for competitors—at regulated tariffs. This created interesting dynamics where Gujarat Gas might carry a competitor's gas through its pipelines. The regulations on marketing exclusivity—protecting new areas from competition for a specified period—became crucial for investment decisions. Companies lobbied intensely for favorable regulatory changes, with industry associations becoming battlegrounds for policy influence.

The state-level political economy added another dimension. Different states had different approaches to city gas distribution. Gujarat's government actively supported Gujarat Gas, seeing it as strategic infrastructure. Maharashtra maintained a more neutral stance between players. Delhi's pollution concerns gave IGL political support. These state-level dynamics influenced everything from land allocation for CNG stations to environmental clearances for pipelines.

The customer acquisition strategies revealed competitive creativity. Gujarat Gas pioneered "community connection drives" where entire housing societies were connected simultaneously, creating peer pressure and economies of scale. IGL leveraged Delhi's public transport system, ensuring every bus and auto-rickshaw became a CNG advertisement. Mahanagar Gas used Mumbai's space constraints to develop compact CNG stations. Each company developed unique approaches suited to their markets.

The financial market's view of competition was nuanced. Despite intense competition, valuations remained robust. Investors recognized that city gas distribution had natural monopoly characteristics—once infrastructure was built, competition was limited. The market valued Gujarat Gas's extensive network and execution capability, IGL's dominance in the national capital, and Mahanagar Gas's Mumbai monopoly. The sector's regulated returns provided downside protection, while volume growth offered upside potential.

The international benchmarking provided perspective. Compared to developed markets where gas penetration exceeded 60%, India's 6-7% offered massive growth potential. The government's target of 15% gas in the energy mix by 2030 meant the pie would grow faster than companies could compete for shares. This "rising tide lifts all boats" dynamic meant competition, while intense, wasn't zero-sum.

Looking at market dynamics through 2020, clear patterns emerged. The sector was consolidating around a few large players with regional strengths. Scale advantages in operations, financing, and regulation were becoming decisive. Technical capabilities and execution excellence separated winners from also-rans. The competition had evolved from grabbing territories to optimizing operations, from winning licenses to executing profitably.

The competitive landscape positioned Gujarat Gas favorably. As India's largest city gas distribution company, it had scale advantages in procurement, operations, and financing. Its vertical integration through GSPC provided gas sourcing security. Its proven execution capability made it attractive for new licenses. Its financial strength allowed patient capital deployment. While competition would intensify, Gujarat Gas had built moats that would be difficult to breach.

The market dynamics and competition analysis reveals a sector in transition. From comfortable monopolies to competitive markets, from regional players to national champions, from infrastructure builders to technology companies—city gas distribution was evolving rapidly. Gujarat Gas's ability to navigate this competition while maintaining market leadership demonstrated not just operational excellence but strategic sophistication. As the sector entered the 2020s, the competition would only intensify, but the foundations laid during this period would determine who would dominate India's gas distribution landscape for decades to come.

VIII. Current Operations & Financial Performance

Walk into Gujarat Gas's network operations center in Gandhinagar on any given day, and you're entering the nerve center of India's largest city gas distribution network. Banks of monitors display real-time data from across 41,700 kilometers of pipelines—pressure readings, flow rates, temperature variations. Controllers track gas molecules from source to burner tip, optimizing routes, managing peak demand, preventing problems before they occur. One controller, a veteran of fifteen years, explains: "We're not just distributing gas; we're orchestrating an energy symphony across six states. Every industrial furnace, every kitchen stove, every CNG vehicle—they're all notes in our composition."

The business model that generates ₹15,908 crores in revenue is deceptively simple yet operationally complex. At its core, Gujarat Gas buys natural gas from various sources—domestic fields, imported LNG, spot markets—and delivers it to three primary customer segments: industrial, commercial and residential (PNG), and transport (CNG). But the elegance lies in the details. The company operates on a cost-plus regulated return model for much of its business, providing stability, while volume growth and operational efficiency drive profitability.

Breaking down the revenue streams reveals strategic positioning. CNG contributes approximately 55% of volumes, benefiting from India's push toward cleaner transport fuels. Industrial and commercial PNG accounts for about 30%, providing stable baseload demand. Domestic PNG, while lower margin, represents 15% of volumes but strategic importance—each household connection is a 30-year annuity. This diversification isn't accidental; it's designed to balance growth, stability, and margins.

The customer segmentation data as of 2024 tells a story of scale and reach: approximately 21.90 lakh domestic households, 15,470 commercial establishments, and 4,410 industrial units depend on Gujarat Gas for their energy needs. Each segment requires different service levels, pricing mechanisms, and infrastructure investments. Industrial customers need reliability above all—a ceramic plant can't afford gas supply interruptions. Domestic customers prioritize safety and convenience. CNG customers demand accessibility and quick refueling times. The company has built specialized teams and processes for each segment.

The operational metrics reveal world-class efficiency. System losses—gas lost through leaks, measurement errors, theft—are below 0.5%, compared to industry averages of 1-2%. Asset utilization, measured as throughput per kilometer of pipeline, has improved 30% over five years through network optimization. Customer acquisition costs have decreased through digital onboarding and community connection drives. The company connects a new domestic customer every 90 seconds, opens a new CNG station every week, and adds industrial customers daily.

The infrastructure utilization strategy deserves attention. With 820 CNG stations and growing, Gujarat Gas has created a network effect where more stations attract more vehicles, which justifies more stations. The average station utilization has increased from 60% to 75% over three years through dynamic pricing, loyalty programs, and strategic locations. The company pioneered 24-hour CNG stations, mobile refueling units for fleet operators, and mother-daughter station configurations that optimize land use.

Financial performance trends reveal consistent growth with improving margins. Revenue has grown at 15% CAGR over the past five years, driven by volume growth and periodic tariff revisions. EBITDA margins have expanded from 12% to 15% through operational efficiencies and favorable gas sourcing. Return on equity consistently exceeds 15%, impressive for a utility-like business. The company maintains a conservative debt-to-equity ratio around 0.5, providing flexibility for growth investments while maintaining financial stability.

The working capital management is particularly sophisticated. The company has negative working capital in many quarters—customers pay weekly or monthly while gas suppliers are paid on longer cycles. This cash flow advantage funds growth without external financing. The company has also optimized inventory management, maintaining just enough line pack (gas in pipelines) for operational needs while minimizing carrying costs.

Capital allocation strategy reflects long-term thinking. Annual capex of ₹1,000-1,500 crores is split between growth projects (new areas, customer connections) and sustenance (replacement, safety upgrades). The company maintains a dividend payout ratio around 30%, balancing shareholder returns with growth capital retention. Strategic investments in technology and digital infrastructure, while not immediately revenue-generating, position the company for future efficiency gains.

The gas sourcing strategy has evolved significantly. Gujarat Gas procures gas through multiple channels: domestic gas allocation from government, long-term LNG contracts, spot market purchases, and gas trading. This diversification reduces supply risk and enables cost optimization. The company has developed sophisticated models for gas portfolio management, balancing cheaper domestic gas allocation with more expensive but flexible imported gas.

The regulatory compliance framework influences operations significantly. The company operates under multiple regulatory jurisdictions—PNGRB for infrastructure, state pollution control boards for environmental compliance, weights and measures for CNG dispensing. Compliance isn't just about avoiding penalties; it's strategic. Gujarat Gas's reputation for exceeding regulatory standards helps in winning new licenses and maintaining social license to operate.

The technology integration in operations has accelerated. The company has implemented SAP for enterprise resource planning, customer relationship management systems for service delivery, and geographic information systems for network planning. Mobile apps allow customers to pay bills, book new connections, and register complaints. IoT sensors monitor pipeline integrity. Artificial intelligence optimizes gas sourcing and demand forecasting. This digital backbone enables managing complexity at scale.

The human capital dimension is crucial for operations. Gujarat Gas employs thousands directly and influences tens of thousands of indirect jobs. The company has established training centers for technical skills, partnerships with engineering colleges for talent pipeline, and leadership development programs for succession planning. The safety culture is particularly strong—millions of man-hours without lost-time injuries isn't luck but systematic safety management.

Risk management has become sophisticated. Operational risks are managed through redundancy, preventive maintenance, and emergency response systems. Financial risks are hedged through currency derivatives and interest rate swaps. Regulatory risks are mitigated through proactive compliance and stakeholder engagement. Cyber risks, increasingly important as operations digitize, are addressed through robust IT security frameworks.

The recent financial results indicate continued momentum. The company's profit after tax has grown consistently, cash flows remain strong, and balance sheet metrics are healthy. More importantly, operational indicators—customer additions, volume growth, network expansion—suggest sustained growth potential. The company has also started reporting ESG metrics, recognizing investor focus on sustainability.

Looking at current operations, Gujarat Gas has evolved from a utility to a sophisticated energy solutions provider. The operational excellence isn't just about efficiency—it's a competitive moat. The financial performance isn't just about current returns—it's about funding future growth. The company has built capabilities that would take competitors years to replicate, creating sustainable advantages in an increasingly competitive market.

The current operations and financial performance analysis reveals a company at the peak of its operational powers. The infrastructure is built, processes are optimized, and financial metrics are strong. But this isn't a mature company resting on laurels. The continued investment in technology, expansion into new territories, and exploration of adjacent opportunities suggest Gujarat Gas sees current success as a platform for future growth. For investors, the question isn't whether Gujarat Gas can operate efficiently—that's proven. The question is how the company will leverage its operational excellence to navigate the energy transition ahead.

IX. Future Outlook & Strategic Challenges

The strategy presentation to Gujarat Gas's board in late 2023 contained a slide that stopped everyone cold. It showed two curves: one depicting India's projected natural gas demand soaring to 30% of the energy mix by 2030, the other showing electric vehicle adoption potentially reaching 30% of new vehicle sales by the same year. The CEO paused before speaking: "Gentlemen, our future depends on navigating between these two realities—massive opportunity in gas demand growth and existential threat to our CNG business from electric vehicles. The decisions we make in the next five years will determine whether Gujarat Gas thrives or merely survives."

The macro opportunity is undeniable. India's current gas consumption at 6-7% of the energy mix is remarkably low compared to the global average of 24%. The government's stated target of increasing this to 15% by 2030 implies a doubling of gas demand. With the India CNG market expected to grow from 7.57 thousand kilotons in 2025 at 18.24% CAGR to 17.5 thousand kilotons by 2030, the growth runway appears massive. But beneath these encouraging headlines lie complex challenges that will test Gujarat Gas's strategic agility.

The electric vehicle disruption threat is real and accelerating. Every major automobile manufacturer has announced EV plans. The government provides substantial subsidies for electric vehicles while gradually reducing support for CNG vehicles. Charging infrastructure is expanding rapidly. For Gujarat Gas, with CNG contributing 55% of volumes, this isn't a distant threat—it's an immediate strategic challenge. The company's response has been measured but decisive: exploring EV charging infrastructure at existing CNG stations, partnering with battery swapping companies, and positioning natural gas as a transition fuel rather than competing directly with electrification.

The infrastructure expansion plans reveal ambitious growth targets. Gujarat Gas has announced intentions to double its pipeline network over the next decade, add 500+ CNG stations, and connect 50 lakh more households. The capital requirements are staggering—potentially ₹15,000-20,000 crores over ten years. This expansion isn't just about growing the existing business; it's about building optionality for future energy systems. Pipelines carrying natural gas today could carry hydrogen tomorrow. CNG stations could become multi-fuel energy hubs.

The regulatory evolution adds complexity. PNGRB is moving toward more market-based mechanisms, potentially reducing regulated returns but increasing operational flexibility. The government's production-linked incentive schemes, carbon markets, and green hydrogen policies create both opportunities and uncertainties. Gujarat Gas must navigate this evolving landscape while maintaining investment momentum—a delicate balance between regulatory compliance and commercial aggression.

The green hydrogen pivot represents both opportunity and challenge. As India develops its hydrogen economy, natural gas infrastructure becomes critical—hydrogen can be blended with natural gas, transported through existing pipelines (with modifications), and distributed through similar networks. Gujarat Gas has started pilot projects for hydrogen blending, studying technical requirements and economic viability. The transition won't be smooth—hydrogen has different properties than methane, requiring infrastructure modifications and new safety protocols—but the company's existing capabilities provide significant advantages.

The competitive landscape is intensifying in unexpected ways. It's not just traditional city gas distribution companies anymore. Reliance's new energy ventures, Adani's green hydrogen ambitions, and international oil companies' net-zero commitments are reshaping the sector. New technologies like renewable natural gas from waste, small-scale LNG for remote areas, and virtual pipelines using trucked CNG are creating new business models. Gujarat Gas must defend its core business while exploring these adjacencies.

The financial implications of the energy transition are profound. The company must maintain current profitability to fund dividends and growth, invest heavily in traditional infrastructure that may have shortened economic life, and simultaneously explore new energy ventures with uncertain returns. This triple challenge requires sophisticated capital allocation, potentially including partnerships, joint ventures, or even restructuring to separate legacy and new energy businesses.

The technology disruption extends beyond electric vehicles. Digital twins for pipeline management, blockchain for gas trading, artificial intelligence for demand prediction, and quantum computing for network optimization are becoming reality. Gujarat Gas must decide where to lead, where to follow, and where to partner. The company has established an innovation lab, partnered with startups, and recruited digital talent—but the pace of change demands even more aggressive technology adoption.

The supply-side dynamics are evolving rapidly. India's domestic gas production has disappointed, import dependence is increasing, and global LNG markets are volatile. The Russia-Ukraine conflict has reshaped global energy flows. The development of the India-Middle East-Europe corridor could position India as an energy transit hub. Gujarat Gas must navigate these geopolitical complexities while ensuring supply security for millions of customers who depend on uninterrupted gas supply.

The customer expectations are shifting. Industrial customers want not just gas supply but complete energy solutions—efficiency audits, carbon accounting, renewable integration. Residential customers expect digital services, flexible pricing, and sustainable options. CNG customers compare refueling experience with EV charging convenience. Meeting these evolving expectations requires Gujarat Gas to transform from an infrastructure company to an energy services provider.

The organizational capabilities needed for the future differ from those that brought past success. The company needs data scientists alongside pipeline engineers, energy traders along with safety inspectors, and sustainability experts along with construction managers. Building these capabilities while maintaining operational excellence in the core business is a human capital challenge that will determine strategic success.

The stakeholder landscape is becoming more complex. Environmental activists scrutinize fossil fuel infrastructure investments. Investors demand ESG compliance and climate risk disclosure. Communities expect local employment and environmental protection. Regulators balance multiple objectives—energy security, environmental protection, consumer affordability. Managing these diverse stakeholder expectations while pursuing growth requires sophisticated engagement strategies.

The strategic options facing Gujarat Gas crystallize around three scenarios. The "steady state" scenario assumes gradual EV adoption, continued gas demand growth, and successful infrastructure expansion—leading to steady but unspectacular returns. The "disruption" scenario sees rapid EV adoption, aggressive renewable energy growth, and stranded gas assets—requiring dramatic business model transformation. The "transformation" scenario envisions Gujarat Gas successfully pivoting to become a multi-energy company, leveraging existing infrastructure for hydrogen, maintaining gas distribution while adding renewable energy services—creating new growth vectors.

The investment requirements for each scenario differ dramatically. The steady-state needs ₹1,500-2,000 crores annual capex. The disruption scenario might require writedowns of existing assets while investing in new capabilities. The transformation scenario demands the highest investment—perhaps ₹3,000+ crores annually—but offers the highest potential returns. The company's strong balance sheet provides flexibility, but choosing the right path is critical.

Risk mitigation strategies are evolving. Traditional risks—pipeline safety, supply disruption, regulatory changes—remain relevant. But new risks—stranded assets from energy transition, technology obsolescence, climate-related physical risks—require different approaches. The company is developing scenario planning capabilities, stress-testing strategies against different futures, and building optionality into investment decisions.

The time horizon for strategic decisions has compressed. Previously, infrastructure investments were evaluated over 30-year periods. Now, with rapid technology change and energy transition, even 10-year forecasts seem uncertain. This requires more flexible investment approaches—modular expansion, reversible decisions, and real options thinking. Gujarat Gas must balance long-term infrastructure development with short-term agility.

Looking ahead, Gujarat Gas faces its most complex strategic challenge since inception. The company must grow traditional business while preparing for its potential obsolescence, invest in proven technologies while exploring uncertain innovations, and serve today's customers while anticipating tomorrow's needs. Success requires not just operational excellence but strategic courage—the willingness to cannibalize existing business to create future value.

The future outlook suggests Gujarat Gas has the capabilities, resources, and positioning to navigate the energy transition successfully. But execution won't be easy. The company must move quickly enough to capture new opportunities but carefully enough to avoid costly mistakes. It must be bold enough to transform but prudent enough to maintain financial stability. The next five years will determine whether Gujarat Gas remains India's leading gas distributor or becomes something more—a multi-energy company powering India's sustainable future.

X. Investment Thesis & Analysis

The investment committee at a major Mumbai mutual fund was in heated debate. The portfolio manager advocating for Gujarat Gas was passionate: "Where else do you find a utility with 15%+ ROE, double-digit volume growth, and government backing?" The skeptic across the table was equally forceful: "You're buying a fossil fuel distributor just as India goes electric. This is like investing in horse carriages after seeing the first automobile." This debate, playing out in investment committees across India, captures the fundamental tension in Gujarat Gas's investment thesis—compelling current fundamentals versus uncertain future trajectory.

The bull case starts with the infrastructure moat. Those 41,700 kilometers of pipeline aren't just steel tubes—they're rights of way secured over decades, customer relationships built over years, and operational expertise that's nearly impossible to replicate. The replacement cost of Gujarat Gas's infrastructure would exceed ₹50,000 crores, far above the current market capitalization. Any competitor would need decades to build similar infrastructure, by which time Gujarat Gas would have expanded further. This isn't a moat that technology can easily disrupt—physical infrastructure in a regulated industry with high safety requirements creates formidable entry barriers.

The demand growth story remains robust despite energy transition concerns. India's per capita gas consumption at 28 standard cubic meters is a fraction of the global average of 367 standard cubic meters. Even reaching China's level of 161 standard cubic meters would require 5x growth. The government's push for gas-based economy isn't just rhetoric—it's backed by policy support, infrastructure investment, and international commitments. With manufacturing shifting to India and urbanization accelerating, industrial and commercial gas demand has structural tailwinds that could persist for decades.

The financial metrics support the bull case. Gujarat Gas consistently generates returns on equity above 15%, remarkable for a utility-like business. Free cash flow generation is strong and growing. The dividend yield around 1.5% might seem modest, but dividend growth has been consistent. The balance sheet is conservative with debt-to-equity around 0.5, providing flexibility for growth investment or returning cash to shareholders. These aren't the metrics of a struggling legacy business but a company generating substantial economic value.