Concord Biotech: The Fermentation Empire

I. Introduction & Episode Roadmap

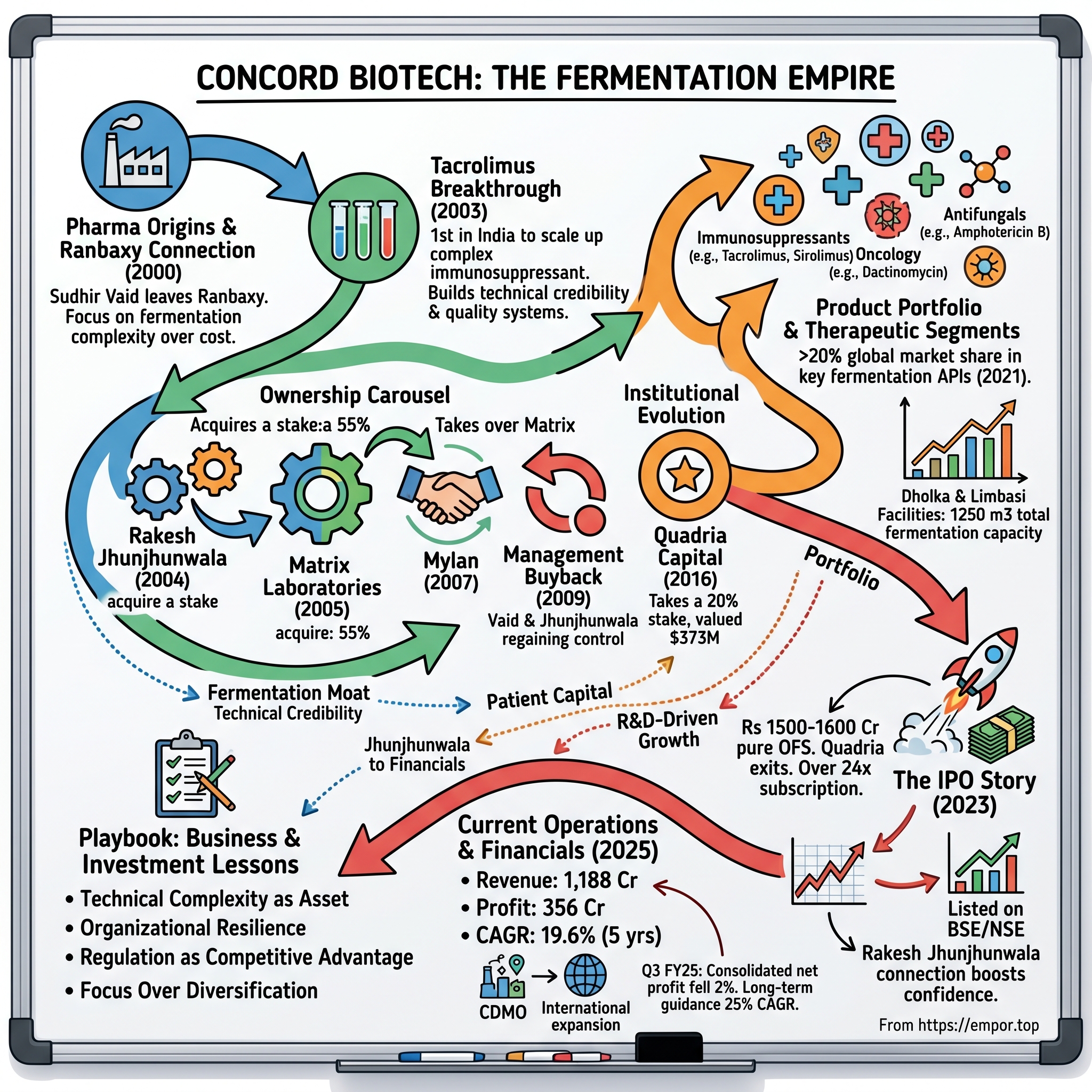

Picture this: In a nondescript industrial area near Ahmedabad, inside temperature-controlled rooms that hum with the steady rhythm of industrial fermenters, microscopic organisms are quietly producing some of the world's most complex pharmaceutical molecules. This isn't Silicon Valley biotech glamour—no gleaming glass towers or venture capital photo ops. This is Concord Biotech's Dholka facility, where industrial fermentation meets pharmaceutical precision, and where a company that started with a single product has built one of the world's most formidable positions in fermentation-based APIs.With a market capitalization of ₹16,968 Crore, Concord Biotech commands a global presence in more than 70 countries worldwide. But here's what makes this story particularly compelling: For identified fermentation-based API products such as dactinomycin, sirolimus, tacrolimus, mycophenolate sodium, and cyclosporine, they held a market share of more than 20% by volume in 2021. In an industry where Chinese manufacturers have historically decimated Indian fermentation players through sheer scale and cost advantages, Concord has not just survived—it has thrived.

The question that frames our exploration today isn't just how a company built a fermentation empire. It's how they built one that could withstand the Chinese tsunami that swept away virtually every other Indian fermentation player, how they navigated multiple ownership changes while maintaining operational excellence, and how they convinced the market to value them at nearly 50 times earnings at IPO—a valuation that would make even software companies blush.

This is a story about technical moats in an era of commoditization, about patient capital in an age of quarterly earnings, and about building complexity as a competitive advantage when everyone else was racing to the bottom on price. It's about understanding that sometimes the best businesses aren't the sexiest ones—they're the ones that solve problems so difficult that most competitors simply give up trying.

Our journey today takes us through multiple acts: from Sudhir Vaid's departure from Ranbaxy to build something of his own, through the strategic chess game of multiple ownership changes, to the eventual IPO that saw unprecedented demand from institutional investors. We'll explore how fermentation—a technology as old as bread and beer—became the foundation for some of modern medicine's most critical drugs. And we'll examine what Concord's trajectory tells us about building enduring value in India's pharmaceutical sector.

II. Pharma Origins & The Ranbaxy Connection

The year 2000 marked a peculiar moment in Indian pharmaceutical history. The industry was riding high on the success of reverse-engineering Western molecules, Y2K had just made Indian IT a global force, and pharmaceutical executives were beginning to dream beyond just copying—they were thinking about creating. Into this milieu stepped Sudhir Vaid, a man who had spent years at Ranbaxy Laboratories watching the company transform from Bhai Mohan Singh's garage startup into India's first truly global pharma company.

Vaid wasn't your typical pharma executive. While his colleagues at Ranbaxy were focused on the lucrative game of generic formulations—taking off-patent molecules and finding cheaper ways to synthesize them—Vaid had become fascinated with fermentation. It was an obsession that seemed almost quaint in an era when chemical synthesis was king. Fermentation was messy, unpredictable, required massive capital investments, and worst of all, the Chinese had already cornered most of the market with their state-subsidized facilities.

But Vaid saw something others missed. The post-liberalization Indian pharma landscape of the late 1990s was creating a unique opportunity. Global pharmaceutical companies were beginning to outsource not just manufacturing but also complex R&D work to India. The patent regime was changing—India would soon have to recognize product patents, not just process patents. And most importantly, the global market for complex, fermentation-derived APIs was growing rapidly, driven by breakthrough drugs in immunosuppression and oncology.

Concord, founded in the year 2000, transformed from a single-product company to a broad-spectrum solution provider, offering products across diversified therapeutic segments. But the story actually begins earlier. The corporate entity that would become Concord Biotech was incorporated in 1984, existing as a shell or dormant company for years before Vaid breathed life into it in 2000. This wasn't uncommon in Indian business—buying an existing corporate structure often simplified regulatory approvals and provided a cleaner capitalization table for future investors.

The decision to focus on fermentation wasn't just contrarian—it was borderline heretical. By 2000, most Indian fermentation units had either shut down or pivoted to other technologies. The economics were brutal: fermentation required enormous upfront capital for bioreactors, extensive utilities for maintaining sterile conditions, and highly skilled microbiologists who were in short supply. A chemical synthesis plant could be set up for a fraction of the cost and operated by chemical engineers that Indian universities were producing by the thousands.

Yet Vaid understood something fundamental about competitive advantage. In Michael Porter's framework, you can compete on cost or differentiation. The entire Indian pharma industry was competing on cost, and they were increasingly losing that battle to China. But fermentation offered a different path—compete on complexity. Working with microbial strains & cultures, managing several process parameters, and carrying out numerous purification processes make fermentation a difficult operation.

The early days were precisely as difficult as one might expect. Vaid started with a small facility, a handful of scientists poached from various research institutes, and a focus on a single product. The choice of that first product would prove crucial—it had to be complex enough to deter easy competition but not so complex that a startup couldn't handle it. It had to have a growing market but not one dominated by entrenched players. And ideally, it would serve as a stepping stone to more valuable molecules.

The financing structure in those early days was modest—Vaid put in his savings from his Ranbaxy years, brought in a few angel investors from the pharma community, and operated on a shoestring budget that would seem laughable by today's standards. But this capital constraint forced discipline. Every fermentation run had to count. Every failed batch was a crisis. Every successful scale-up was a celebration.

What made Vaid's approach unique wasn't just the focus on fermentation, but the systematic way he thought about building capabilities. Rather than trying to compete across the entire fermentation spectrum, he identified specific therapeutic areas where fermentation-based molecules were critical and where the technical barriers were highest. Immunosuppressants emerged as the perfect target—drugs like tacrolimus and sirolimus that were notoriously difficult to produce but absolutely essential for organ transplant patients.

Historically, this business has been a graveyard for Indian companies. 3 decades back, India used to have many companies in the Fermentation API space. These companies eventually died because they could not match the scale and cost economics of Chinese players. Vaid's insight was that the Indian companies that failed had tried to compete with China on China's terms—scale and cost. Instead, Concord would compete on quality, regulatory compliance, and customer service.

The Ranbaxy connection proved invaluable in those early years, though not in the way one might expect. Vaid didn't poach customers or steal trade secrets. Instead, he brought something more valuable—an understanding of how global pharmaceutical companies thought about their supply chains. At Ranbaxy, he had seen firsthand how Western pharma companies evaluated API suppliers: regulatory track record mattered more than price, security of supply trumped lowest cost, and the ability to handle regulatory audits was worth a premium.

This knowledge shaped Concord's early strategy in profound ways. While competitors were building capacity first and worrying about quality later, Vaid insisted on building quality systems from day one. The company invested in documentation, training, and standard operating procedures that seemed excessive for a startup. They hired quality assurance professionals who had experience with FDA audits, even though an FDA inspection was years away.

By 2002, Concord had successfully scaled up its first product and was generating modest revenues. But Vaid knew that being a single-product company was a recipe for disaster in the volatile world of pharma. The company needed to expand its portfolio, but each new fermentation product required significant R&D investment, new production strains, and often entirely different downstream processing equipment.

This is where the strategic vision really came into play. Rather than randomly adding products, Concord focused on building a portfolio of related molecules that could leverage similar fermentation technologies and serve overlapping customer bases. If you were making tacrolimus for immunosuppression, why not also make sirolimus? If you had customers buying immunosuppressants, they probably also needed antifungals for the same immunocompromised patients.

The early 2000s were also a period of significant change in the Indian pharmaceutical landscape. The government was investing heavily in biotechnology, seeing it as the next frontier after IT. Regulatory standards were being upgraded to meet international requirements. And perhaps most importantly, venture capital was beginning to flow into Indian pharma, looking for the next Ranbaxy or Dr. Reddy's.

It was in this context that Concord began to attract attention from investors. The company wasn't the largest or the fastest-growing, but it had something that was increasingly rare in Indian pharma—genuine technical differentiation. While everyone else was racing to file ANDAs for generic drugs in the US market, Concord was quietly building one of India's most sophisticated fermentation capabilities.

The transformation from that single-product startup to a multi-product fermentation specialist didn't happen overnight. It was a gradual process of capability building, customer acquisition, and strategic focus. By 2003, the company had expanded to three products. By 2004, they were working on half a dozen molecules and beginning to attract interest from both customers and investors who saw the potential in their approach.

III. The Tacrolimus Breakthrough & Early Innovation

The moment arrived in 2003, though it had been years in the making. In a modest laboratory in Ahmedabad, a team of microbiologists and fermentation engineers had been working around the clock, monitoring bioreactors, adjusting pH levels, tweaking nutrient feeds, and most importantly, coaxing a temperamental strain of Streptomyces tsukubaensis to produce commercial quantities of tacrolimus. When the HPLC results came back confirming both yield and purity that matched international standards, there was no champagne celebration—just quiet satisfaction and the immediate question: "Can we reproduce this?"

Tacrolimus wasn't just another molecule. Discovered by Fujisawa Pharmaceutical Company in 1984 from a soil sample from Tsukuba, Japan, it had revolutionized organ transplantation by offering superior immunosuppression with fewer side effects than cyclosporine. But producing it was a nightmare. The fermentation process was finicky, yields were low, and the purification process was so complex that only a handful of companies worldwide had mastered it.

Concord's achievement was remarkable: they became the first company in India and reportedly the second in the world to successfully develop and scale up tacrolimus production through fermentation. This wasn't just a technical milestone—it was a statement of intent. If you could make tacrolimus, you could make almost anything in the fermentation space.

The technical challenges were staggering. Tacrolimus is a 23-membered macrolide lactone—a complex molecular structure that the producing organism synthesizes through an intricate biosynthetic pathway involving multiple enzymatic steps. The slightest contamination, temperature fluctuation, or pH deviation could cause the fermentation to fail or produce unwanted analogues. The downstream processing was equally challenging—tacrolimus had to be separated from hundreds of other metabolites, some with very similar chemical properties.

What made Concord's approach unique was their systematic deconstruction of the problem. Rather than trying to simply copy existing processes (which were closely guarded trade secrets anyway), they went back to first principles. They isolated their own production strains, developed their own media formulations, and designed their own purification protocols. This meant the development took longer—almost three years from initiation to commercial production—but it also meant they truly owned the technology.

The R&D team, led by scientists recruited from prestigious institutions like the National Chemical Laboratory and the Institute of Microbial Technology, approached the challenge with academic rigor but commercial urgency. They maintained detailed strain genealogies, documenting every mutation and selection step. They ran hundreds of small-scale fermentation experiments, methodically optimizing each parameter. They developed analytical methods that could detect impurities at parts-per-million levels.

But perhaps the most crucial innovation wasn't in the laboratory—it was in the production philosophy. While most fermentation facilities ran large batches to maximize efficiency, Concord designed their tacrolimus process for flexibility and reliability. They used smaller bioreactors that allowed better process control. They built redundancy into critical steps. They invested in advanced automation and monitoring systems that were unusual for Indian pharma companies at the time.

The early customers were skeptical. Here was an unknown Indian company claiming to produce one of the most complex fermentation products in the pharmaceutical industry. The first samples sent to potential customers in Europe came back with polite rejections—the quality was good, but who was Concord Biotech? Did they have regulatory approvals? Could they ensure consistent supply?

Vaid and his team recognized that technical capability alone wasn't enough. They needed credibility. So they did something unusual for an Indian API company at the time—they invited customers to audit their facilities before making any sales. They opened their books, shared their process validation data, and demonstrated their quality systems. It was a risky strategy—competitors could potentially gather intelligence—but it proved crucial in building trust.

The first commercial order came from a mid-sized European generic company that was struggling with their existing tacrolimus supplier. It was a small order—just a few kilograms—but Concord treated it like it was their only customer. They provided certificates of analysis that exceeded requirements, they shipped ahead of schedule, and when the customer had a technical query, Concord's scientists were on a conference call within hours.

Word spread slowly but surely through the tight-knit community of pharmaceutical procurement professionals. Concord could deliver tacrolimus. Not just once, but consistently. Their prices weren't the lowest—Chinese suppliers could undercut them—but their reliability and quality were exceptional. By 2004, they had three regular customers. By 2005, they were supplying to seven countries.

The tacrolimus success created a virtuous cycle. Revenue from tacrolimus sales funded R&D for other complex fermentation products. The technical capabilities developed for tacrolimus—strain development, fermentation optimization, complex purification—could be applied to other molecules. The regulatory dossiers prepared for tacrolimus provided templates for future submissions. And perhaps most importantly, the credibility gained from tacrolimus opened doors for other products.

The immunosuppressant market was experiencing rapid growth in the early 2000s. Organ transplantation was becoming more common, not just in developed countries but also in emerging markets. The patent on tacrolimus was expiring in various jurisdictions, creating opportunities for generic versions. And new immunosuppressive drugs were being developed that required similar fermentation capabilities.

Concord's timing was impeccable. They had developed their tacrolimus capability just as the market was opening up. But timing alone doesn't explain their success. What set them apart was their deep understanding of the fermentation process. While competitors might buy a strain and follow a recipe, Concord understood the biology. They knew why certain conditions produced better yields. They could troubleshoot problems that would stump others. They could adapt their process for different scales and specifications.

This expertise became evident in their yields and quality. While industry-standard fermentation yields for tacrolimus were closely guarded secrets, industry insiders suggested that Concord's yields were among the highest globally. More importantly, their product purity consistently exceeded pharmacopeial requirements, often reaching levels that surprised even sophisticated customers.

The technical team also made several process innovations that would become hallmarks of Concord's approach. They developed proprietary strain improvement programs that steadily increased yields over time. They created innovative purification techniques that reduced solvent usage and improved recovery. They implemented statistical process control methods that were more common in semiconductor manufacturing than in pharma.

But innovation wasn't limited to the technical sphere. Concord also innovated in how they engaged with customers. Rather than simply being a supplier, they positioned themselves as partners. When a customer needed a specific impurity profile for their formulation, Concord would modify their process. When regulatory requirements changed, Concord would proactively update their documentation. When customers faced regulatory queries about the API, Concord's regulatory team would provide support. The competition with global giants wasn't just about technology—it was about credibility. When Concord sent samples to Novartis or Roche, they weren't just competing with established suppliers; they were fighting centuries of accumulated trust. The fact that an Indian company could produce tacrolimus was impressive; convincing a Swiss pharmaceutical giant to bet patient lives on it was another matter entirely.

By 2005, Concord had established itself as a serious player in the complex fermentation space. They weren't the largest or the most profitable, but they had something invaluable—proven capability in one of pharma's most difficult technologies. This foundation would prove crucial as the company entered its next phase of evolution, one that would see ownership change hands multiple times while the core technology and vision remained intact.

IV. The Ownership Carousel: Matrix, Mylan & Strategic Investors

The Mumbai stock exchange floor in 2004 was still a place where fortunes were made and lost on the trading floor, where brokers shouted orders across the ring, and where one man had become a legend for his ability to spot value where others saw only risk. In 2004, Rakesh Jhunjhunwala acquired around 14% stake in the company. For Jhunjhunwala, known as India's Warren Buffett, Concord represented something different from his usual plays—not a turnaround story or an undervalued giant, but a technology bet in a space most investors didn't understand.

Rakesh Jhunjhunwala and Rekha Jhunjhunwala invested in Concord Biotech in 2004. The investment wasn't headline-grabbing—Concord was still a relatively small company with limited revenues. But Jhunjhunwala saw what others missed: here was a company building genuine technical moats in an industry racing toward commoditization. His investment philosophy had always centered on finding businesses with sustainable competitive advantages, and fermentation complexity was about as sustainable as moats got.

The story took an unexpected turn in 2005. In 2005, Hyderabad-based Matrix Laboratories acquired 55% stake in the company, by buying partial shareholding of Vaid and Jhunjhunwala. Matrix Laboratories was everything Concord wasn't—large, diversified, with established relationships across the global pharmaceutical industry. Led by the ambitious Prasad family, Matrix had built a formidable position in generic APIs and was looking to expand into more complex molecules.

For Sudhir Vaid, the Matrix acquisition presented a dilemma. On one hand, Concord needed capital to expand, and Matrix had deep pockets. On the other, selling majority control meant potentially losing the entrepreneurial culture and technical focus that had defined Concord. The negotiations were intense—Vaid insisted on operational autonomy, Matrix wanted integration synergies. The final deal structure was a compromise: Matrix would provide capital and commercial support, but Concord would maintain its independent R&D and manufacturing operations.

The Matrix era, brief as it would prove to be, was transformative for Concord. Matrix brought professional management systems, international regulatory expertise, and most importantly, customer relationships that would have taken Concord years to build independently. Under Matrix's umbrella, Concord accelerated its facility expansions, upgraded its quality systems to meet US FDA standards, and expanded its product portfolio beyond immunosuppressants into oncology and anti-infectives.

But the pharmaceutical industry in 2006-2007 was experiencing unprecedented consolidation. Global giants were acquiring Indian companies at premium valuations, seeking low-cost manufacturing bases and technical capabilities. Mylan, the American generic giant, had been watching Matrix's growth with interest. Matrix had what Mylan needed—FDA-approved facilities, a broad product portfolio, and established commercial operations.

When Mylan acquired Matrix Laboratories in 2007 for $736 million, Concord found itself as a small subsidiary of a global pharmaceutical giant. For many Indian pharmaceutical entrepreneurs, this would have been the end of the story—absorbed into a multinational, their identity eventually dissolved into the parent company. But Concord's story would take another unexpected turn.

After Matrix Laboratories was acquired by Mylan, the latter sold back its stake in Concord Biotech to Vaid and Jhunjhunwala in 2009. The management buyback was unusual—multinational companies rarely divest profitable subsidiaries back to original founders. But Mylan's strategic priorities lay elsewhere. They were focused on high-volume generics and expanding their formulation capabilities. Concord's complex fermentation business, while profitable, didn't fit neatly into Mylan's operational model.

The buyback negotiations revealed the chess game of pharmaceutical M&A. Mylan wanted to exit cleanly without creating a future competitor. Vaid and Jhunjhunwala wanted to regain control without overpaying for a business they had built. The final terms remain confidential, but industry insiders suggest the valuation was fair—reflecting Concord's profitability but not the strategic value it would later demonstrate.

For Jhunjhunwala, the buyback represented a validation of his original thesis. Rare Enterprises is an asset management firm owned by Rakesh Jhunjhunwala, a high-profile Indian stock market investor, who raised his stake in Concord to 25% when Matrix sold back its stake. He now holds about 30% in Concord. He had maintained his position through the Matrix acquisition and Mylan takeover, believing in the fundamental value of Concord's technology platform. Now, with majority control back with the founders, he doubled down on his investment.

The post-buyback period from 2009 to 2015 was one of steady building. Free from the constraints of corporate bureaucracy, Vaid and his team could move quickly on strategic decisions. They expanded the Dholka facility, adding fermentation capacity and upgrading downstream processing capabilities. They invested heavily in R&D, developing new molecules and improving yields on existing products. Most importantly, they built direct relationships with global customers, no longer relying on a parent company's commercial network.

The financial performance during this period validated the buyback decision. Revenues grew steadily as Concord captured market share in key molecules. Margins expanded as process improvements reduced costs. And the company generated strong cash flows that funded further expansion without requiring external capital. By 2015, Concord had transformed from a subsidiary of a global giant back into an independent Indian success story.

But the capital requirements for the next phase of growth were substantial. Concord needed to build a second manufacturing facility to de-risk operations and add capacity. They needed to invest in an injectable dosage form facility to move up the value chain. And they needed working capital to support growing international sales. The founders and Jhunjhunwala had funded growth through retained earnings, but competing globally required institutional capital.

Ahmedabad-based Concord Biotech has sold a 20% stake in itself to the private equity fund Quadria Capital for about $75 million with the investment valuing the bulk-drug maker at about $373 million. The entry of Quadria Capital in 2016 marked a new chapter. Unlike the Matrix acquisition, this was a minority investment that left founders in control. Unlike typical private equity investors focused on financial engineering, Quadria brought healthcare expertise and Asian market knowledge.

The investment also marked a valuation milestone. Quadria Capital had invested Rs 475.30 crore in 2016 to acquire a 20 per cent stake in the company. The $373 million valuation represented a massive value creation from the management buyback just seven years earlier. It validated the strategy of focusing on complex fermentation products rather than chasing volume in commoditized generics.

The ownership changes—from entrepreneurial startup to Matrix subsidiary to Mylan unit to management buyback to PE-backed growth—might seem like instability. But through each transition, the core of Concord remained intact: the fermentation technology, the scientific team, and the focus on complexity as competitive advantage. Each ownership phase brought something valuable—Jhunjhunwala brought patient capital and credibility, Matrix brought professional systems, Mylan provided a reality check on global competition, and Quadria would bring institutional discipline.

Jhunjhunwala will remain the single largest shareholder after the most recent deal following the Quadria investment. His patience through multiple ownership changes exemplified his investment philosophy—back great entrepreneurs, understand the business deeply, and have the conviction to hold through volatility. For Concord, having such a high-profile investor provided not just capital but credibility in India's close-knit business community.

V. The Quadria Capital Era & Institutional Evolution

The Singapore skyline gleamed in the afternoon sun as the Quadria Capital investment committee gathered in their Marina Bay offices in late 2015. On the table was a thick dossier on an Indian fermentation company most of them had never heard of. The healthcare-focused private equity firm had evaluated dozens of Indian pharmaceutical companies, but Concord Biotech presented a unique proposition—not the typical generic formulation play, but a specialized manufacturer with genuine technical differentiation.

Quadria's due diligence team had spent months in Concord's facilities, poring over quality records, interviewing customers, and understanding the fermentation process. What they discovered impressed them: here was a company that had quietly built one of the world's most sophisticated fermentation platforms while competitors were distracted by the generic gold rush in the US market. The technology moat was real, the regulatory track record was impeccable, and most importantly, the growth potential was substantial.

The 2016 investment of Rs 475.30 crore for a 20% stake valued Concord at approximately $373 million—a valuation that raised eyebrows in Indian pharmaceutical circles. This wasn't a formulation company with hundreds of ANDAs; this was an API manufacturer in a narrow niche. But Quadria saw what others missed: the combination of technical complexity, regulatory excellence, and market position created a business that was very difficult to replicate.

The institutional evolution that followed Quadria's entry was profound but subtle. Unlike the dramatic changes that often follow private equity investments—cost cutting, asset stripping, financial engineering—Quadria's approach was to professionalize and scale what was already working. They brought in consultants not to transform the business but to document and systematize the knowledge that existed in the heads of senior scientists. They invested in enterprise resource planning systems not to cut costs but to provide visibility into operations that had grown too complex for spreadsheets.

The Dholka facility near Ahmedabad became a showcase for this evolution. It has two manufacturing facilities–at Dholka near Ahmedabad, which is approved by USFDA, and at Limbasi in Kheda district. What had started as a modest fermentation unit had grown into a sprawling complex with multiple production blocks, each designed for specific product families. The USFDA approval, achieved through painstaking preparation and multiple mock audits, opened doors to the lucrative US generic market.

But the real transformation was in mindset. Under Quadria's guidance, Concord began thinking beyond individual products to platform capabilities. Instead of just making tacrolimus, they were building a comprehensive immunosuppressant platform. Instead of just fermentation, they were developing integrated capabilities from strain development to finished dosage forms. This platform thinking would prove crucial as the pharmaceutical industry moved toward greater specialization.

The investment in the Limbasi facility exemplified this strategic evolution. In 2021, the Company commissioned another API fermentation manufacturing facility in Limbasi, Gujarat (Unit-3) having 800m3 of fermentation capacity. Rather than simply adding capacity, Limbasi was designed as a next-generation facility incorporating learnings from two decades of fermentation experience. Automated process controls, real-time quality monitoring, and flexible production configurations made it one of India's most advanced fermentation facilities.

International expansion accelerated under Quadria's tenure. While Concord had always exported, their approach had been opportunistic—responding to inquiries, fulfilling orders. Now they built systematic market development capabilities. Regulatory affairs teams prepared comprehensive dossiers for multiple markets simultaneously. Business development executives cultivated relationships with procurement heads at global pharmaceutical companies. Technical service teams provided support that went beyond typical supplier relationships.

The regulatory strategy was particularly sophisticated. Rather than pursuing approvals market by market, Concord developed a chess-like approach to regulatory submissions. As of the date of this Draft Red Herring Prospectus, they had submitted more than 120 Drug Master Files for their APIs across a number of nations, including 20, 63, and four in the US, Europe, and Japan, respectively. Each approval opened not just that market but provided credibility for the next submission. A successful FDA inspection made European approval easier; Japanese certification opened doors across Asia.

The Jhunjhunwala factor during this period cannot be understated. While Quadria brought institutional discipline, Jhunjhunwala provided continuity and credibility. He was the chairman of Hungama Media and Aptech and was on the board of directors of firms such as - Viceroy Hotels, Concord Biotech, Provogue India and Geojit Financial Services. His presence on the board signaled to stakeholders that despite institutional investment, Concord remained rooted in entrepreneurial values. His patient capital philosophy aligned perfectly with the long development cycles of fermentation products.

The financial performance during the Quadria era validated the institutional evolution. Revenues grew from hundreds of crores to approaching the thousand-crore mark. Margins expanded as operational efficiencies kicked in. Return on capital employed reached levels that would make software companies envious. But perhaps most importantly, the company built a sustainable competitive position that went beyond any individual product or customer.

The product portfolio expansion during this period was strategic rather than opportunistic. Each new molecule was chosen not just for its market potential but for how it fit into Concord's capability matrix. Could they leverage existing fermentation expertise? Did it serve their existing customer base? Would it strengthen their position in key therapeutic areas? This disciplined approach meant slower portfolio growth but higher success rates and better margins.

Our total annual installed fermentation capacity for API is 1250 m3. We have a total of 41 manufacturing blocks and 387 reactors in the Dholka and Limbasi facilities, which allows us the flexibility in plant configuration to cater to customer demands. This massive infrastructure, built systematically over the Quadria years, provided the scale and flexibility to compete globally while maintaining the agility to serve niche requirements.

The quality systems evolution was particularly noteworthy. What had started as compliance—meeting minimum regulatory requirements—evolved into excellence. Concord began winning quality awards from customers. Their deviation rates dropped to industry-leading levels. Their batch success rates approached statistical perfection. This wasn't just about avoiding regulatory issues; it was about building a quality culture that permeated every aspect of operations.

The human capital development during this period laid the foundation for future growth. Concord invested heavily in training, sending scientists to international conferences, funding advanced degrees, and creating a culture of continuous learning. They recruited talent from multinational pharmaceutical companies, bringing global best practices to their operations. But crucially, they retained the entrepreneurial spirit and technical focus that had defined the company from the beginning.

Customer relationships evolved from transactional to strategic. Major pharmaceutical companies began viewing Concord not just as a supplier but as a partner in their supply chain strategy. When customers faced regulatory queries about fermentation-derived APIs, Concord's regulatory team would provide support. When customers needed custom specifications for new formulations, Concord's R&D team would develop modified processes. This partnership approach created switching costs that went beyond price.

The CDMO (Contract Development and Manufacturing Organization) opportunity that emerged during this period represented a natural evolution. Global pharmaceutical companies were increasingly outsourcing complex manufacturing to specialized partners. Concord's fermentation expertise, regulatory track record, and manufacturing infrastructure positioned them perfectly for this trend. Rather than just selling APIs, they could partner with innovator companies from development through commercial manufacturing.

By 2022, as Quadria prepared for exit through the IPO route, Concord had transformed from a successful Indian API manufacturer to a global fermentation powerhouse. The institutional evolution hadn't changed the company's DNA—it had amplified it. The technical excellence was now backed by world-class systems. The entrepreneurial agility was now supported by institutional capabilities. The patient capital approach was now validated by sustained financial performance.

VI. Product Portfolio & Therapeutic Segments

Inside Concord's quality control laboratory, a young scientist peers into an HPLC chromatogram showing the purity profile of sirolimus, one of the company's flagship molecules. The peaks are sharp, the baseline clean, the purity exceeding 99.5%—numbers that tell a story of two decades of process refinement. But the real story isn't in this single molecule; it's in how Concord built an entire portfolio around the scientific and commercial logic of fermentation.

It manufactures biopharmaceutical products across therapy segments such as immunosuppressant, oncology, antifungal, antibacterial and anthelmintic. This therapeutic diversification wasn't random—each segment was chosen because fermentation offered unique advantages over chemical synthesis. Immunosuppressants like tacrolimus and sirolimus have molecular structures so complex that chemical synthesis is economically unfeasible. Oncology drugs like dactinomycin are produced by specific bacterial strains that cannot be replicated synthetically. Antifungals like amphotericin B require fermentation's ability to produce large, complex molecular structures.

The market share numbers tell a remarkable story of dominance in narrow niches. For the identified fermentation based API products, such as dactinomycin, sirolimus, tacrolimus, mycophenolate sodium, and cyclosporine, they held a market share of more than 20% by volume in 2021. In some molecules, industry insiders suggest Concord's share is even higher—approaching 30-40% in certain markets. This isn't the distributed market share of a formulation company with hundreds of products; this is concentrated dominance in specific molecules where Concord has become the supplier of choice.

The immunosuppressant portfolio remains the crown jewel. Tacrolimus, the molecule that launched Concord's journey into complex fermentation, continues to be a major revenue driver. But the real sophistication lies in the portfolio approach—tacrolimus for immediate post-transplant immunosuppression, sirolimus for maintenance therapy, mycophenolate for combination regimens, and cyclosporine for specific patient populations. A transplant unit ordering from Concord can source their entire immunosuppressant protocol from a single supplier.

The technical moat in immunosuppressants is formidable. Each molecule requires a specific production strain that has been optimized over years through careful mutation and selection. The fermentation conditions—temperature profiles, pH curves, nutrient feeding strategies—have been refined through thousands of production runs. The purification processes, involving multiple chromatography steps and crystallizations, achieve purity levels that many competitors cannot match. A new entrant would need years just to reach Concord's current yields, by which time Concord would have moved further ahead.

The oncology portfolio represents a different strategic logic. Drugs like dactinomycin are produced in smaller volumes but command premium prices due to their critical nature and limited supplier base. The fermentation process for these molecules is particularly challenging—the producing organisms grow slowly, yields are low, and the products are often cytotoxic, requiring specialized handling. Concord's ability to reliably produce these molecules has made them an essential supplier to oncology drug manufacturers globally.

The antifungal segment showcases Concord's ability to handle diverse fermentation challenges. Amphotericin B, for instance, is produced by Streptomyces nodosus through a complex biosynthetic pathway. The molecule is notorious for its poor solubility and stability issues, requiring sophisticated formulation techniques even at the API stage. Concord's expertise extends beyond just producing the molecule to providing different grades and formulations that meet specific customer requirements.

They had 22 API products as of March 31, 2022. But the number alone doesn't capture the strategic coherence of the portfolio. Each product was selected not just for its individual merit but for how it fit into the overall capability matrix. Could existing fermentation infrastructure be leveraged? Did it serve the same customer base? Would it strengthen Concord's position in key therapeutic areas? This disciplined approach meant that each new product addition enhanced rather than diluted the company's competitive position.

The R&D pipeline reveals the future direction of the portfolio. Concord isn't chasing the latest fads or me-too molecules. Instead, they're systematically identifying fermentation-derived molecules where they can build dominant positions. The criteria are stringent: the molecule must be complex enough to deter easy competition, have a growing market, face supply constraints from existing manufacturers, and fit within Concord's technical capabilities. This filter means few products make it to development, but those that do have high success probability.

The backward integration strategy adds another layer to the moat. Rather than purchasing key starting materials from suppliers, Concord produces many of them in-house. This includes critical fermentation media components, specialized enzymes for biotransformations, and even some of the production strains themselves. This integration provides cost advantages, ensures supply security, and most importantly, prevents competitors from accessing the same input materials.

The API versus formulation debate that consumes many Indian pharmaceutical companies has been resolved decisively at Concord—they do both, but strategically. The formulation business, launched in 2016, isn't an attempt to become a broad-based generic company. Instead, it focuses on complex formulations of their own APIs, particularly in specialized areas like nephrology and critical care. This forward integration captures additional value while maintaining focus on their core fermentation expertise.

As of March 31, 2022, Concord Biotech also had Certification of Suitability to the European Pharmacopoeia Monographs for 13 APIs. These certifications represent more than regulatory compliance—they're competitive weapons. Each certificate requires extensive analytical data, process validation, and impurity profiling that takes years to compile. Once obtained, they create significant barriers for competitors trying to enter the same markets.

The capacity utilization story reveals operational excellence. They had a total installed fermentation capacity of 1,250 m3 as of March31, 2022. But unlike chemical synthesis where capacity utilization can approach 90%, fermentation is inherently batch-based with longer cycle times. Concord's ability to achieve industry-leading utilization rates while maintaining quality and flexibility demonstrates sophisticated production planning and operational excellence.

The customer concentration metrics tell an interesting story. Unlike many API manufacturers dependent on a few large customers, Concord's revenue is distributed across dozens of global pharmaceutical companies. No single customer accounts for more than 15% of revenues. This diversification isn't accidental—it's a deliberate strategy to reduce dependency and maintain pricing power. When you're one of only 2-3 reliable suppliers of a critical API, customers need you as much as you need them.

The pricing power in the portfolio is remarkable. While generic APIs typically face constant price pressure, Concord's specialized molecules command premium pricing. The combination of limited competition, high switching costs, and critical nature of the products means that price increases can be passed through to customers. This pricing power, rare in the commoditized world of pharmaceutical ingredients, drives the superior margins that have attracted investor attention.

The environmental and sustainability angle adds another dimension to the portfolio strategy. Fermentation is inherently more environmentally friendly than chemical synthesis—it uses water-based systems, operates at ambient temperatures, and produces biodegradable waste. As pharmaceutical companies face increasing pressure on ESG metrics, Concord's fermentation-based products become more attractive. This isn't just marketing—it's a genuine competitive advantage as sustainability moves from nice-to-have to must-have in supplier selection.

VII. The IPO Story: Timing, Structure & Market Reception

The Mumbai summer of 2023 was particularly sweltering, but inside the air-conditioned conference rooms of investment banks along Nariman Point, the heat was of a different kind. The IPO pipeline was packed, investor appetite was strong, and everyone was looking for the next big story. Into this frenzy came Concord Biotech—not a digital startup or a consumer brand, but a fermentation company that most retail investors had never heard of.

The size of the IPO is reportedly around Rs 1,500 crore to Rs 1,600 crore, and it will consist entirely of an OFS (offer for sale). The offering will comprise up to 20.93 million shares, representing the entire 20 percent stake held by Helix Investment Holdings Pte Ltd, which is backed by Quadria Capital Fund LP. The pure OFS structure was unusual—no fresh capital raise, no growth story funded by IPO proceeds. This was a clean exit for Quadria Capital, ending their successful seven-year investment journey.

The timing seemed counterintuitive. The global pharmaceutical sector was facing headwinds—pricing pressure in the US generics market, increased FDA scrutiny, and concerns about Chinese competition. Yet here was Concord, seeking a valuation that implied a price-to-earnings multiple typically reserved for technology companies. The bankers had their work cut out for them.

The price band fixation became a crucial strategic decision. Late ace investor Rakesh Jhunjhunwala-backed Concord Biotech Ltd has fixed a price band of Rs 705-741 a share for its initial public offering (IPO). At the upper band, the company was valued at Rs 7,752 crore—a valuation that would have seemed fantastical just a few years earlier for an API manufacturer. The pricing reflected confidence, but also realism about what the market would bear.

The anchor book opening on August 3, 2023, would set the tone for the entire IPO. Anchor investors—the sophisticated institutional players who commit large chunks before the public offering—would signal whether the Concord story resonated with smart money. The response was emphatic. Global funds that typically avoided pharmaceutical IPOs were placing large orders. The anchor book was oversubscribed multiple times within hours.

What attracted these sophisticated investors wasn't immediately obvious from the prospectus. Yes, the financial metrics were strong—debt-free balance sheet, 30%+ EBITDA margins, consistent growth. But dig deeper and the real attraction emerged: here was a company that had solved one of pharma's hardest problems—competing with China in fermentation—and had built a moat that would last decades.

The retail investor roadshow revealed the challenge of explaining complex B2B businesses to a market accustomed to consumer stories. How do you explain fermentation technology to someone who thinks of it only in terms of yogurt and beer? How do you convey the importance of regulatory moats to investors who've never heard of a Drug Master File? The Jhunjhunwala connection proved invaluable—if the Big Bull had backed it for nearly two decades, there must be something special.

Concord Biotech shares were commanding a handsome grey market premium (GMP) of around Rs 325-Rs300 apiece on Monday. The grey market—that unofficial barometer of IPO sentiment—was signaling strong demand. Grey market premiums of 40-45% suggested that institutional and high-net-worth investors were willing to pay substantial premiums to secure allocations. This wasn't just momentum trading; it reflected genuine conviction in the Concord story.

The subscription period from August 4-8, 2023, became a testament to market appetite. Overall subscribed 24.87 times with the QIB portion was booked 67.67 times. The Qualified Institutional Buyers (QIB) subscription number was particularly telling—these weren't retail investors caught up in IPO mania but sophisticated institutions that had done deep due diligence.

The allocation process revealed interesting dynamics. With massive oversubscription, most retail investors received minimal allocations. Institutional investors who had bid aggressively got meaningful chunks. The employee reservation, offered at a Rs 70 discount, was fully subscribed, showing internal confidence. The distribution created a shareholder base of long-term institutional investors rather than short-term traders.

Shares got listed on BSE, NSE on August 18, 2023. Listing day arrived with considerable anticipation. The pre-open session showed strong demand, with indicated prices well above the issue price. When regular trading began, the stock opened at Rs 900, a 21% premium to the issue price of Rs 741. For a pure OFS with no growth capital raising, this was a strong endorsement of the business model.

The listing day performance defied the usual pattern of IPO pops followed by profit booking. The stock held its gains, volume remained robust, and importantly, there was no massive selling from anchor investors looking to book quick profits. This suggested that institutions saw Concord as a long-term holding rather than a trading opportunity.

The post-listing research coverage provided deeper insights into why institutional investors were bullish. Analysts highlighted the oligopolistic market structure in fermentation APIs, where only 3-4 global players competed in each molecule. They emphasized the 10-15 year development cycle for new fermentation products, creating massive barriers to entry. They noted the shift of global supply chains away from China, benefiting established Indian players like Concord.

The valuation debate that followed was instructive. At nearly 50 times trailing earnings, Concord was priced like a technology company, not a pharmaceutical manufacturer. Bears argued this was unsustainable—APIs are commodities, Chinese competition would eventually return, customer concentration was a risk. Bulls countered that the market was pricing in the platform value, not just current earnings. The ability to develop and manufacture complex fermentation products created optionality that justified premium valuations.

The IPO proceeds distribution told its own story. Since it was a pure OFS, Concord received no funds from the issue. Quadria Capital's exit at a substantial profit validated the private equity model in Indian pharma—patient capital, operational improvement, and strategic timing could generate exceptional returns. For Quadria, the roughly 5x return in rupee terms over seven years represented one of their most successful investments.

The shareholding pattern post-IPO created an interesting dynamic. The promoter group, including the Jhunjhunwala family trusts, held about 44% stake. Public shareholding stood at 56%, with institutions holding the majority of the public float. This structure provided stability—enough promoter holding to ensure continuity, enough public float to ensure liquidity, and enough institutional holding to ensure governance.

Market reception in the months following the IPO validated the pricing. The stock continued to trade at premium valuations, research coverage expanded, and importantly, the company's quarterly results met or exceeded expectations. This wasn't a case of IPO hype followed by disappointment—Concord was delivering on the promise that justified its premium valuation.

The signaling effect of the successful IPO was significant for the broader pharmaceutical sector. It showed that markets would pay premium valuations for genuine technical differentiation. It demonstrated that B2B businesses could command consumer-like multiples if they had sustainable moats. And it proved that patient capital, exemplified by Jhunjhunwala's two-decade holding, could generate exceptional returns.

The employee wealth creation from the IPO, while not as dramatic as technology startups, was meaningful. Scientists and managers who had spent decades perfecting fermentation processes saw their employee stock options turn into substantial wealth. This wealth creation, distributed across hundreds of employees, validated the culture of ownership that Concord had cultivated.

VIII. Current Operations & Financial Performance

The quarterly earnings call in early 2025 began with a note of caution that seemed at odds with Concord's historical performance. Q3 FY25: consolidated net profit fell 2% to Rs 75.9 crore, Revenue increased 1% YoY to Rs 244.2 crore, PBT fell 2% YoY. For a company that had delivered consistent double-digit growth, these numbers sparked concern. But CEO Sudhir Vaid's explanation revealed the strategic chess game playing out—temporary weakness in certain molecules was being offset by investments in future growth drivers.

The full-year picture painted a different story. Revenue: 1,188 Cr, Profit: 356 Cr with the Company is almost debt free. These numbers placed Concord among India's most profitable pharmaceutical companies on a margin basis. The debt-free status was particularly remarkable—while competitors leveraged their balance sheets for growth, Concord had funded expansion entirely through internal accruals.

Company has delivered good profit growth of 19.6% CAGR over last 5 years. This consistent growth through multiple industry cycles—COVID disruption, supply chain crises, regulatory tightening—demonstrated the resilience of the business model. When your customers absolutely need your product to keep patients alive, economic cycles become less relevant.

The manufacturing operations in 2025 represent a masterclass in complex process management. The API unit based in Dholka, Ahmedabad (Unit-1), is spread across 112,302 square meters and has 22 manufacturing blocks with total fermentation capacity of 450m3. The fermentation manufacturing blocks are well supported by chemical synthesis downstream recovery blocks and powder processing areas. The manufacturing facility complies with cGMP and has been inspected by global regulatory agencies like U.S. Food & Drug Administration (USFDA), European Union Goods Manufacturing Practice (EUGMP), Japanese Accreditation of Foreign Manufacturers (AFM), Korean Food & Drug Administration & State Goods Manufacturing Practice of India (GMP).

Walking through the Dholka facility today feels like entering a biotechnology cathedral. Massive stainless steel fermenters, some three stories tall, hum with the metabolic activity of billions of microorganisms. Control rooms resembling NASA mission control monitor hundreds of parameters in real-time. Quality control laboratories run 24/7, testing samples at every stage of production. This isn't the scrappy startup that Vaid founded in 2000—it's a world-class biomanufacturing operation.

The Limbasi facility, the newer addition, incorporates lessons learned from two decades of fermentation experience. Automation levels approach those of semiconductor fabs. Single-use technologies reduce contamination risk and changeover times. Modular design allows rapid reconfiguration for different products. The facility was built not for today's products but for molecules that haven't been developed yet—a bet on the continued relevance of fermentation in pharmaceutical manufacturing.

The capacity utilization metrics reveal operational sophistication. With fermentation's inherent batch variability and long cycle times, achieving consistent high utilization requires exceptional planning. Concord manages multiple products across multiple facilities, each with different fermentation times, purification requirements, and customer delivery schedules. The fact that they achieve this while maintaining industry-leading quality metrics demonstrates operational excellence that goes beyond mere technical capability.

The working capital management presents an interesting challenge. Company has high debtors of 159 days. Working capital days have increased from 202 days to 289 days. In the pharmaceutical industry, extended payment terms are common, especially when dealing with large global customers. But the increase in working capital days suggests either changing customer mix toward larger, slower-paying clients or strategic decisions to offer better terms to win business. Given Concord's strong cash generation, this appears to be a conscious choice rather than a weakness.

The customer portfolio in 2025 spans the entire pharmaceutical ecosystem. Big Pharma companies source critical APIs for their branded drugs. Generic giants depend on Concord for complex molecules that differentiate their portfolios. Emerging market pharmaceutical companies rely on Concord for products they cannot manufacture themselves. This diversification across customer types, geographies, and therapeutic areas provides resilience against any single market disruption.

The CDMO business, still in early stages, represents the future growth vector. Global pharmaceutical companies are increasingly outsourcing complex manufacturing to specialized partners. Concord's proposition is compelling—two decades of fermentation expertise, proven regulatory track record, and available capacity. Early CDMO projects have demonstrated Concord's ability to move from lab scale to commercial production faster than competitors, a critical capability in the race to market.

The financial metrics that don't appear in standard reports tell the real story. Customer retention rates exceeding 95% suggest strong relationships and high switching costs. Batch success rates approaching 99% indicate process control that rivals any industry. Employee turnover below 5% in senior scientific positions shows that Concord has created a culture where India's best fermentation scientists want to work.

The capital allocation decisions reveal strategic discipline. Rather than pursuing acquisitions or unrelated diversification, Concord continues to invest in deepening its fermentation capabilities. The recent announcement of an Equity investment of USD 1,500 in Stellon Biotech Inc representing 75% ownership to expand business operations in USA represents a careful step into forward integration rather than a transformative bet.

The R&D spending, while not broken out separately, is embedded throughout the P&L. Scientists working on process improvement are classified as production staff. Analytical method development is part of quality control. This integrated approach means the true R&D investment is higher than apparent, but it also means R&D is directly connected to commercial outcomes rather than isolated in ivory towers.

The margin structure reveals the business model's beauty. Gross margins exceeding 60% reflect the value of complexity—when you're one of three global suppliers of a life-saving drug, pricing reflects value, not cost. EBITDA margins above 30% demonstrate operational efficiency that comes from two decades of process optimization. Net margins approaching 30% in a capital-intensive manufacturing business show the power of the asset-light model—once fermentation capacity is built, incremental revenue requires minimal additional investment.

The regulatory inspection history provides confidence in sustainability. Zero critical observations in recent FDA inspections. EU GMP certification maintained without issues. Japanese regulatory approval, notoriously difficult to obtain, achieved and maintained. This regulatory excellence isn't just about compliance—it's a competitive moat that takes years to build and can be destroyed in a single failed inspection.

IX. Playbook: Business & Investment Lessons

Sitting in his office overlooking the Ahmedabad skyline, Sudhir Vaid occasionally reflects on the journey from that single fermentation tank in 2000 to today's global operation. The lessons learned along the way form a playbook that challenges conventional wisdom about building a pharmaceutical business in India. It's not a story of first-mover advantage or scale economics—it's about choosing complexity when everyone else was choosing simplicity.

The Fermentation Complexity Moat

The first lesson is counterintuitive: in a world racing toward simplification, complexity can be your greatest asset. While the entire Indian pharmaceutical industry was focused on chemical synthesis—faster, cheaper, more predictable—Concord bet on fermentation's inherent complexity. This wasn't contrarianism for its own sake. It was recognition that complexity creates barriers that protect economic returns.

Consider the requirements for fermentation excellence: you need microbiologists who understand strain development, biochemical engineers who can optimize bioprocess parameters, analytical chemists who can separate complex mixtures, and regulatory experts who can explain biological variability to skeptical regulators. This interdisciplinary expertise takes decades to build and cannot be quickly replicated by throwing money at the problem.

The moat compounds over time. Each successful fermentation campaign generates data that improves the next one. Each process optimization makes competition that much harder. Each regulatory approval raises the bar for new entrants. Unlike chemical synthesis where a process can be reverse-engineered, fermentation involves living organisms with genealogies and characteristics that cannot be easily copied.

Navigating Ownership Changes While Maintaining Focus

The second lesson involves organizational resilience. Concord survived multiple ownership changes—from founder-led to Matrix-owned to Mylan subsidiary to management buyback to PE-backed to public—while maintaining operational continuity. How did they manage this?

The key was separating ownership from operations. While shareholders changed, the core technical team remained stable. The fermentation scientists who developed the tacrolimus process in 2003 were still optimizing it in 2023. This technical continuity meant that regardless of who owned the equity, the intellectual capital remained intact.

Each ownership phase brought different benefits that Concord absorbed while maintaining its core identity. Matrix brought professional systems without destroying entrepreneurial culture. Mylan provided global exposure without diluting technical focus. Quadria added institutional capability without sacrificing operational agility. The ability to take the best from each phase while maintaining core values is rare in corporate transitions.

Building in Highly Regulated Markets

The third lesson challenges the notion that regulatory complexity is a burden. For Concord, regulation became a competitive advantage. While competitors saw FDA inspections as hurdles, Concord saw them as moat-builders. Every successful inspection made the next customer conversation easier. Every regulatory approval created switching costs for existing customers.

The approach to regulation was proactive rather than reactive. Instead of meeting minimum standards, Concord aimed for excellence. They invited regulatory scrutiny, opening their facilities to customer audits even before making sales. This transparency built trust and turned regulation from a cost center into a value driver.

The Importance of Patient Capital

The Jhunjhunwala investment exemplifies the fourth lesson: the transformative power of patient capital. Rekha Rakesh Jhunjhunwala, through multiple discretionary trusts, owned 25,199,240 equity shares, or 24.09 per cent stake in Concord Biotech as of September 30, 2024. This two-decade holding period allowed Concord to make long-term decisions without quarterly earnings pressure.

Fermentation products can take 5-10 years from development to meaningful revenue. Traditional investors would demand faster returns. But patient capital understood that the long development cycle was precisely what created the moat. The willingness to wait for returns enabled investments in capability building that wouldn't pay off for years but would eventually create insurmountable advantages.

R&D-Driven Growth in Commoditized Markets

The fifth lesson involves finding differentiation in seemingly commoditized markets. APIs are often viewed as commodities—identical molecules competing on price. But Concord showed that even in commodity markets, R&D can create differentiation. Their R&D didn't focus on discovering new molecules but on making existing molecules better—higher purity, improved stability, consistent quality, better yields.

This incremental innovation might seem mundane compared to drug discovery, but it creates real value. A 5% improvement in fermentation yield might not make headlines, but it dramatically improves economics. A reduction in impurities from 0.5% to 0.1% might seem trivial, but it can open new market opportunities. The accumulation of these small improvements over two decades created a capability gap that competitors cannot easily close.

Managing Cyclicality in Pharma APIs

The sixth lesson addresses the cyclical nature of pharmaceutical ingredients. API markets swing between shortage and oversupply, between pricing power and commoditization. Concord's approach to managing these cycles provides a template for building resilient businesses in volatile markets.

First, focus on products with limited supplier bases where cyclicality is dampened by high entry barriers. Second, maintain a diversified portfolio across therapeutic areas with different demand drivers. Third, build flexible manufacturing assets that can shift between products based on market conditions. Fourth, maintain strong balance sheets to survive downturns and capitalize on competitor distress.

Pure-Play vs Diversification Debate

The final lesson involves strategic focus. Concord faced constant temptation to diversify—into formulations, into chemical synthesis, into biosimilars. The capital was available, the opportunities were obvious. But they remained committed to fermentation-based products, believing that focus creates excellence.

This isn't dogmatic adherence to a narrow strategy. Concord did expand into formulations, but only for their own APIs. They did add chemical synthesis capability, but only for downstream processing of fermentation products. Every expansion enhanced rather than diluted their core fermentation franchise. The discipline to say no to attractive but unrelated opportunities is perhaps the hardest lesson for successful companies to learn.

The playbook that emerges isn't about financial engineering or market timing. It's about building genuine technical capability, maintaining long-term focus, and having the patience to let competitive advantages compound over time. In an era of quarterly capitalism and instant gratification, Concord's two-decade journey to building a fermentation empire offers timeless lessons about building enduring value.

X. Analysis & Future Outlook

The global pharmaceutical industry in 2025 stands at an inflection point. The easy generics opportunity in the US has largely played out. China's API dominance faces geopolitical headwinds. Biological drugs are cannibalizing small molecules. In this evolving landscape, where does a fermentation specialist like Concord fit? The answer reveals both extraordinary opportunity and sobering challenges.

Competitive Positioning vs Global Peers

Concord's global competitive set is surprisingly small. In the fermentation API space, only a handful of companies compete at scale: Biocon and Aurobindo Pharma in India, Antibioticos and Olon in Europe, and several Chinese players like North China Pharmaceutical. Each has different strengths—Biocon's biosimilar integration, Aurobindo's formulation presence, Chinese players' scale advantages. But none matches Concord's focused excellence in complex small-molecule fermentation.

The competitive dynamics are more oligopolistic than competitive. In tacrolimus, perhaps 4-5 companies supply 90% of global demand. In dactinomycin, the supplier base is even more concentrated. This market structure creates pricing discipline—nobody benefits from price wars when switching costs are high and capacity addition takes years. It's a gentleman's game where competition happens through reliability and quality rather than price.

China+1 Strategy Benefits

The geopolitical tensions between China and the West have created an unprecedented opportunity for Indian API manufacturers. Global pharmaceutical companies, burned by supply disruptions during COVID, are actively diversifying away from Chinese suppliers. But this isn't just about moving orders from China to India—it's about building resilient supply chains with multiple qualified suppliers.

Concord is perfectly positioned for this shift. They already have the regulatory approvals, the customer relationships, and most importantly, the track record of reliable supply. When a global pharmaceutical company needs a second source for a critical fermentation API, Concord is often the only viable option. This isn't capturing market share through competition—it's expanding the market through supply chain de-risking.

Biosimilars and Complex Generics Opportunity

The next wave of pharmaceutical innovation involves biological drugs—antibodies, proteins, cell therapies. But fermentation remains crucial even in this biological era. Many biological drugs require complex excipients and auxiliary materials produced through fermentation. The media used to grow cell cultures, the enzymes used in downstream processing, the complex sugars used in formulation—all potential opportunities for fermentation specialists.

Concord's early moves into this space have been cautious but strategic. Rather than competing directly in biosimilars, they're positioning as suppliers of critical materials to biosimilar manufacturers. It's a picks-and-shovels strategy—let others take the regulatory and commercial risk of biosimilars while Concord provides essential inputs with attractive margins and limited risk.

Injectable Facility and New Product Launches

The planned injectable facility represents Concord's most significant strategic evolution. Injectable formulations command premium pricing, face less competition, and create stronger customer relationships than oral formulations. But they also require significant investment in sterile manufacturing, specialized equipment, and enhanced quality systems.

The strategy isn't to become a broad-based injectable manufacturer but to focus on complex injectable formulations of their own APIs. An injectable formulation of tacrolimus for hospital use. Specialized oncology injectables where Concord already supplies the API. Niche products with limited competition but critical medical need. This forward integration captures value while leveraging existing capabilities.

The management remains committed to launching 8-10 new products in 3-4 years in oncology, anti-infectives, and anti-fungal, which are complex in nature and achieve a long-term revenue CAGR guidance of 25 per cent. This guidance seems aggressive given the long development cycles in fermentation, but the pipeline visibility suggests confidence. These aren't me-too generics but complex molecules where Concord's fermentation expertise provides genuine differentiation.

Long-term Growth Guidance and Achievability

The 25% revenue CAGR guidance has raised eyebrows among analysts accustomed to single-digit growth in pharmaceutical manufacturing. But decompose the growth drivers and the target seems achievable: existing products growing at GDP+ rates (7-8%), market share gains in existing molecules (5-7%), new product launches (5-7%), and forward integration into formulations (5-7%). Each component is reasonable; together they compound to aggressive growth.

The margin trajectory is equally important. Unlike typical manufacturing businesses where growth requires proportional capital investment, Concord's model generates operating leverage. Once fermentation capacity is installed, incremental revenue requires minimal additional investment. This means growth translates directly to margin expansion, creating a virtuous cycle of reinvestment and capability building.

Key Risks: Regulatory, Competition, Customer Concentration

The risk factors cannot be ignored. A single failed FDA inspection could shut down US sales overnight. A contamination event could destroy years of reputation building. A major customer deciding to dual-source could impact revenues significantly. These are not theoretical risks—they have destroyed pharmaceutical companies before.

Regulatory risk is particularly acute in fermentation. Biological processes have inherent variability that regulators increasingly scrutinize. The FDA's focus on data integrity means any documentation lapse can trigger warning letters. European regulators' emphasis on nitrosamine impurities has caught many manufacturers off-guard. Japanese regulators' exacting standards mean constant vigilance. One mistake can cascade across multiple markets.

Competition from Chinese manufacturers remains a long-term threat. While geopolitical tensions currently favor Indian suppliers, this could reverse. Chinese companies are moving up the value chain, improving quality, and obtaining international regulatory approvals. Their cost advantages from scale and government support remain formidable. Concord's moat is real but not impregnable.

Customer concentration, while managed, remains a structural issue. Company has high debtors of 159 days. Large pharmaceutical companies have bargaining power that manifests in extended payment terms, pricing pressure, and demanding service requirements. While Concord has diversified its customer base, losing any major customer would impact not just revenues but capacity utilization and operational efficiency.

New technology risks cannot be dismissed. Continuous manufacturing could disrupt batch-based fermentation. Synthetic biology could enable production of complex molecules without traditional fermentation. Cell-free protein synthesis could bypass cellular production entirely. While these technologies remain nascent, they represent long-term threats to traditional fermentation.

The human capital risk is often overlooked. Concord's success depends on specialized expertise that takes years to develop. The loss of key fermentation scientists or process engineers could set back development programs significantly. As the Indian pharmaceutical industry grows, competition for talent intensifies. Retaining and developing technical talent becomes increasingly critical and expensive.

Despite these risks, the fundamental outlook remains positive. The global demand for complex pharmaceutical ingredients continues to grow. The barriers to entering fermentation remain high. The shift toward supply chain resilience favors established players. And Concord's track record of execution provides confidence in their ability to navigate challenges.

XI. Epilogue & Reflections

The August 2022 passing of Rakesh Jhunjhunwala marked the end of an era, not just for Indian capital markets but for Concord Biotech specifically. His final public appearance at Akasa Air's launch, followed by his death just days later, meant he never saw Concord's IPO—the culmination of an investment journey that began in 2004. Yet his legacy in the company extends far beyond financial returns.

Her stake in the company as of November 14, 2024 stood nearly Rs 4,675 crore. The wealth creation for the Jhunjhunwala family from this single investment validates the power of patient capital and conviction investing. But the real legacy isn't in the numbers—it's in demonstrating that Indian companies could build world-class capabilities in complex technologies, that manufacturing excellence could create as much value as software, and that patience and conviction could generate extraordinary returns.

The Jhunjhunwala Legacy and Wealth Creation Story

Jhunjhunwala's investment philosophy—buy quality businesses, back strong managements, and hold for the long term—found perfect expression in Concord. He saw beyond the immediate financials to the strategic value of fermentation capability. His presence provided not just capital but credibility, attracting other investors and customers who trusted his judgment.

The wealth creation extended beyond the Jhunjhunwala family. Early employees who received stock options became millionaires. Scientists who spent decades perfecting fermentation processes saw their patience rewarded. Even vendors and partners who grew with Concord benefited from the ecosystem of value creation. This distributed wealth creation, while modest compared to technology startups, was meaningful in the context of Indian manufacturing.

Lessons for Indian Biotech Entrepreneurs

Concord's journey offers crucial lessons for Indian biotech entrepreneurs. First, technical excellence alone isn't enough—you need commercial acumen to monetize innovation. Second, regulatory compliance isn't a burden but a moat-builder. Third, patient capital aligned with long-term vision is essential for biotech success. Fourth, focus beats diversification in technically complex fields.

The timing lesson is particularly important. Concord didn't try to time the market or chase hot trends. They built capabilities steadily over two decades, positioning themselves for opportunities that eventually emerged. When the world needed reliable non-Chinese suppliers of complex APIs, Concord was ready—not because they predicted this specific need but because they had built fundamental capabilities.

What Makes a Great Fermentation Business