Mahanagar Gas Limited: Mumbai's Clean Energy Revolution

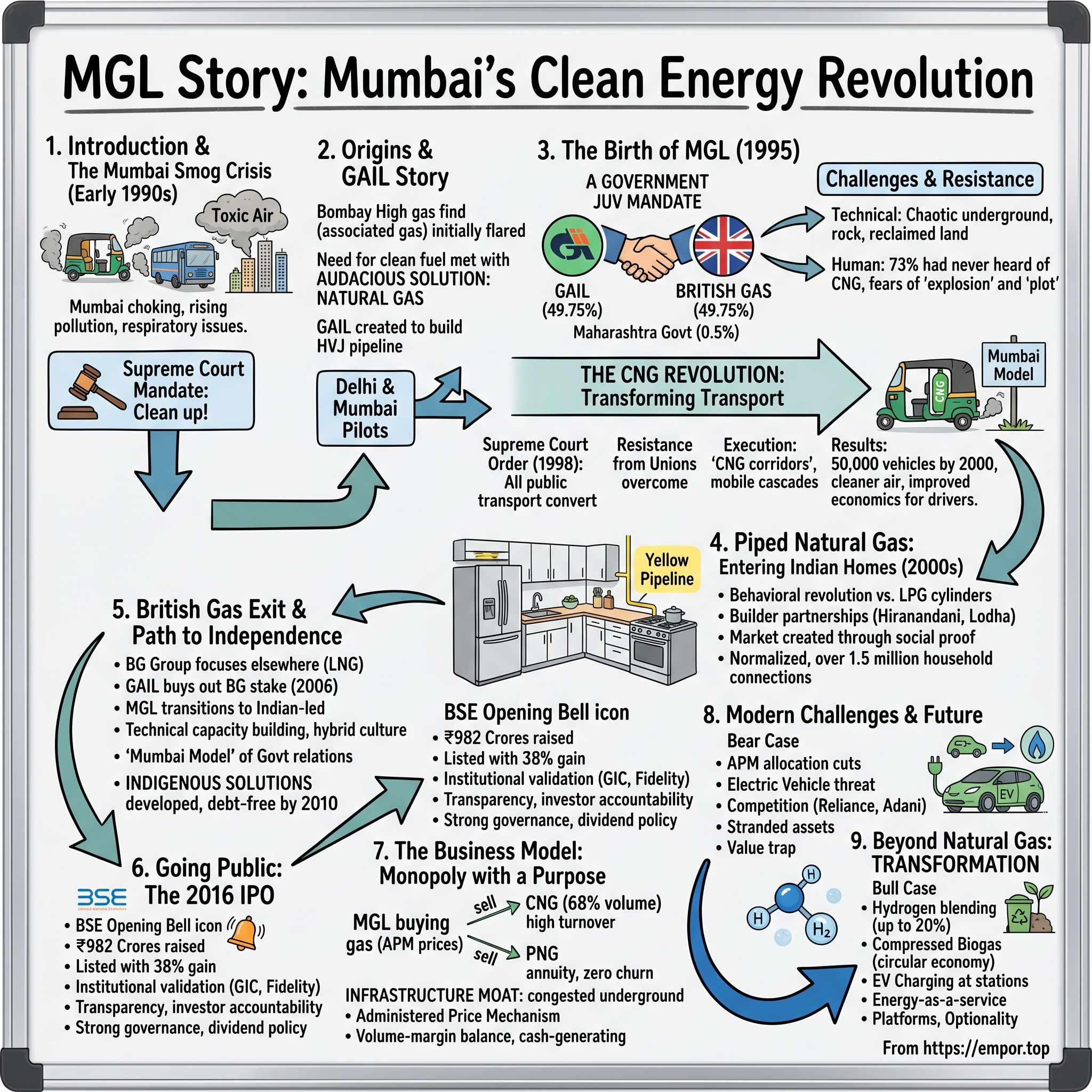

I. Introduction & The Mumbai Smog Crisis

Picture Mumbai in 1993: The Arabian Sea breeze that once cleansed the city now carried a toxic cocktail of vehicular emissions, industrial smoke, and the acrid smell of burning kerosene. The financial capital of India was literally choking on its own success. Auto-rickshaws belched black smoke at every traffic signal, buses left trails of diesel fumes that hung in the humid air like dark curtains, and the city's respiratory ward admissions were climbing faster than the Sensex.

It was against this backdrop that a Supreme Court petition would change everything. Environmental activists had dragged the government to court, armed with data showing Mumbai's air quality had deteriorated to levels that made Beijing look pristine. The court's response was swift and uncompromising: clean up or shut down. Convert public transport to cleaner fuels. Now.

Enter natural gas—an audacious solution for a city that had never seen a gas pipeline, let alone a compressed natural gas (CNG) station. The idea seemed almost absurd: convince millions of Mumbaikars to abandon petrol, diesel, and LPG cylinders for an invisible, odorless gas that most had never heard of. Build an entirely new energy infrastructure through some of the world's most densely populated slums, navigate Mumbai's notorious bureaucracy, and somehow make it all profitable.

This is the story of Mahanagar Gas Limited—a company that started as a government joint venture with a mandate to clean Mumbai's air and evolved into a ₹13,397 crore market cap energy infrastructure giant. It's a tale of how a city gas distribution company not only transformed Mumbai's energy landscape but created a playbook for urban energy transition in emerging markets.

Today, MGL supplies natural gas across Mumbai, Thane, and Raigad—a geography that houses over 20 million people. The company serves 0.77 million vehicles through its CNG network and pipes natural gas directly to 1.53 million households. But these numbers barely hint at the extraordinary journey: from skeptical auto-rickshaw drivers protesting in the streets to housewives suspicious of gas pipes in their kitchens, from British colonial-era regulations to modern capital markets, from government ownership to public listing.

What makes MGL's story particularly compelling for investors is how it built an infrastructure moat in one of the world's most challenging urban environments. Unlike software companies that can scale with code, MGL had to dig up streets, lay pipes through slums, convince millions to change decades-old habits, and navigate a regulatory maze that would make Kafka proud. The result? A near-monopoly position in India's commercial capital with switching costs so high that even the electric vehicle revolution hasn't dented investor confidence.

But perhaps the most intriguing aspect is timing. MGL's journey mirrors India's own transformation—from the socialist License Raj to liberalization, from government control to market capitalism, from environmental ignorance to climate consciousness. Each phase of India's evolution created new opportunities and challenges for MGL, shaping it into what it is today: part utility, part growth story, part ESG play.

As we dive into this multi-decade saga, we'll explore how a company born from environmental litigation became one of India's most profitable infrastructure businesses, why British Gas saw opportunity where others saw chaos, and whether MGL can navigate the next energy transition as successfully as it managed the last one.

II. Origins & The GAIL Story

The roots of MGL stretch back to a newly independent India grappling with an energy crisis that threatened to derail its industrial ambitions. In 1947, India inherited an economy that ran on imported oil and domestic coal—both problematic for different reasons. Oil meant foreign exchange bleeding out, coal meant environmental degradation and inefficiency. The search for alternatives would eventually lead to natural gas, but the journey there was anything but straightforward.

The story truly begins with the discovery of the Bombay High offshore oil field in 1974—India's first major hydrocarbon find. Along with oil came associated natural gas, initially seen as a nuisance to be flared off. But as global oil shocks rattled economies through the 1970s, Indian policymakers began viewing this "waste" gas as potential gold. The question was: how do you transport gas from offshore platforms to industrial centers hundreds of kilometers inland?

The answer came in August 1984 with the creation of the Gas Authority of India Limited (GAIL). Born under the Ministry of Petroleum and Natural Gas, GAIL had a singular mission: build and operate the Hazira-Vijaipur-Jagdishpur (HVJ) pipeline, a 1,700-kilometer artery that would carry natural gas from western India to the industrial heartland of the north. This wasn't just infrastructure; it was nation-building through energy security.

But GAIL's leadership understood something crucial: pipelines without end-users are expensive monuments to nowhere. They needed anchor customers, and India's polluted metros seemed perfect candidates. In the early 1990s, as environmental consciousness finally reached Indian courts and boardrooms, GAIL launched pilot projects in two cities that desperately needed cleaner air—Delhi and Mumbai.

The approach was elegant in its simplicity: create joint venture companies that would handle last-mile distribution while GAIL managed the trunk pipelines. Indraprastha Gas Limited (IGL) would tackle Delhi; Mahanagar Gas Limited (MGL) would take on Mumbai. These weren't just business ventures; they were experiments in whether market mechanisms could solve environmental problems in India's chaotic urban centers.

What's fascinating about this period is how it reflected the contradictions of 1990s India. The License Raj was officially dying—Manmohan Singh's 1991 reforms had opened the economy—but in critical infrastructure, the government still held the reins. Private capital was welcome, but only as a junior partner. Foreign expertise was needed, but sovereignty was non-negotiable. These tensions would shape MGL's structure and strategy for decades.

The choice of Mumbai for the pilot wasn't random. As India's commercial capital, Mumbai generated the tax revenues that funded government ambitions. Its pollution problem was acute enough to demand action but its wealth meant residents could potentially afford cleaner alternatives. Most importantly, Mumbai's concentrated geography—a narrow peninsula with limited escape routes for pollution—made it an ideal testing ground for city-wide energy transformation.

By 1994, GAIL had the blueprint ready. They would bring in a foreign partner with technical expertise, partner with the state government for regulatory support, and create a special purpose vehicle to execute the project. The Bombay City Gas Distribution project was approved, funding was arranged, and all they needed was the right international partner.

The timing was perfect. Environmental regulations were tightening globally, creating expertise in gas distribution. European companies, having saturated their home markets, were hunting for growth in emerging economies. And India, having just liberalized, was suddenly on every multinational's radar. The stage was set for British Gas to enter the picture, bringing with them not just capital but decades of experience in convincing skeptical consumers to embrace gas.

III. The Birth of MGL: British Gas Enters India (1995)

On December 6, 1994, in a conference room overlooking the Arabian Sea, executives from GAIL and British Gas signed papers that would fundamentally alter Mumbai's energy landscape. The joint venture agreement creating Mahanagar Gas Limited was more than a business deal—it was a collision of two worlds: British engineering precision meeting Indian jugaad, colonial-era infrastructure systems encountering post-liberalization ambitions.

British Gas didn't choose India randomly. The company, flush with profits from North Sea gas and UK privatization, was executing an aggressive emerging markets strategy. They had already entered Argentina, Thailand, and Kazakhstan. But India represented the ultimate prize: a billion potential consumers, rapid urbanization, and environmental regulations that virtually guaranteed demand for cleaner fuels. Mumbai, specifically, offered density that made pipeline economics irresistible—more customers per kilometer than almost anywhere on Earth.

The initial shareholding structure revealed the delicate balance of interests: GAIL held 49.75%, British Gas took 49.75%, and the Government of Maharashtra retained a symbolic 0.5%. This wasn't just equity distribution; it was a political statement. Foreign capital was welcome but wouldn't control critical infrastructure. The state government's tiny stake ensured a seat at the table when regulatory decisions were made—a detail that would prove invaluable during the tumultuous early years.

Chris Gibson, British Gas's first managing director for MGL, arrived in Mumbai in early 1995 to find an office with three employees, no infrastructure, and a city that didn't know what natural gas was. His diary from those days, later shared with employees, captured the surreal challenge: "Explained to the municipal commissioner today why we need to dig up roads. He asked if we could use the sewage pipes instead. I couldn't tell if he was joking."

The technical challenges were staggering. Mumbai's underground was already a chaotic mesh of water pipes, telephone cables, electric lines, and sewage systems—most unmapped, many illegal. The city's geology alternated between reclaimed land that shifted with tides and hard basalt rock that destroyed drilling equipment. Monsoons flooded excavations. Slum dwellers built homes atop proposed pipeline routes overnight.

But the human challenges were even more complex. MGL's first marketing survey in 1995 revealed that 73% of Mumbaikars had never heard of CNG. Of those who had, most associated gas with the Bhopal disaster. The company's initial public meetings turned into forums for every conspiracy theory imaginable: the pipes would explode, the gas would poison groundwater, it was a foreign plot to control India's energy.

The British Gas team brought something invaluable: playbooks from converting London's black cabs to CNG in the 1980s. They understood that infrastructure alone wouldn't drive adoption—you needed to make switching economically irresistible and operationally seamless. Their first masterstroke was focusing on commercial vehicles rather than private cars. Auto-rickshaw and taxi drivers cared about fuel costs more than anyone; convince them, and you had mobile advertisements traversing every Mumbai street.

The early infrastructure build was an exercise in controlled chaos. MGL pioneered the "micro-tunneling" technique in India—boring small tunnels under roads rather than digging trenches. This minimized traffic disruption but required specialized equipment that had to be imported and operators who had to be trained. The first CNG station, built in Cuffe Parade in 1996, took nine months to construct and cost three times the budget. But it worked, and more importantly, it proved the concept to skeptics in government and media.

By late 1996, MGL had laid 50 kilometers of pipeline and built four CNG stations. The numbers were modest, but momentum was building. The company cleverly leveraged British Gas's international credibility—every milestone was celebrated with press releases mentioning "international standards" and "global best practices." When Tony Blair visited India in 1997, he made a publicized stop at an MGL facility, providing validation that no amount of advertising could buy.

The British brought more than just technology and credibility; they introduced corporate governance standards that were alien to Indian public sector norms. Regular board meetings with detailed minutes, quarterly performance reviews, transparent procurement processes—these weren't just compliance requirements but cultural shifts that would define MGL's operating philosophy long after British Gas departed.

The first major crisis came in 1997 when a pipeline leak in Dadar led to evacuations and panicked headlines. The leak was minor—caused by unauthorized construction damaging the pipeline—but public reaction was severe. MGL's response, guided by British Gas's crisis management protocols, became a textbook case: immediate transparency, visible safety measures, and community engagement. They turned a potential disaster into a demonstration of their commitment to safety.

By 1998, three years after incorporation, MGL had crossed 10,000 CNG vehicles and connected its first 1,000 households to piped gas. The British Gas experiment was working, but storm clouds were gathering. British Gas itself was undergoing massive restructuring back home, splitting into BG Group and Centrica. Their appetite for long-gestation emerging market infrastructure projects was waning. The partnership that had birthed MGL was about to face its first existential test.

IV. The CNG Revolution: Transforming Mumbai's Transport

The morning of July 28, 1998, started like any other in Mumbai until auto-rickshaw drivers noticed something different at fuel stations—new green dispensers with "CNG" emblazoned on them. What followed was six hours of chaos: thousands of auto-rickshaws blocked major intersections, drivers burned effigies of politicians, and the city's transport system ground to a halt. The ostensible reason for protest? The Supreme Court had just mandated that all public transport vehicles in Mumbai convert to CNG within 18 months.

The court order, delivered by a bench led by Justice Kuldip Singh, was unequivocal: "The right to clean air is a fundamental right under Article 21 of the Constitution." The judgment cited studies showing Mumbai's air contained suspended particulate matter at levels 300% above WHO guidelines. Auto-rickshaws and buses, running on adulterated diesel and petrol, were identified as primary culprits. The solution was mandatory CNG conversion, with deadlines that seemed impossibly aggressive.

For MGL, this was both a massive opportunity and an existential challenge. The company had been preparing for gradual adoption over a decade; now they had 18 months to convert over 100,000 vehicles. Sanjay Kumar, then head of CNG operations, later recalled: "We calculated we needed to build one new CNG station every six days and convert 200 vehicles daily. Our entire team was 47 people."

The resistance from transport unions was fierce and multifaceted. Drivers worried about conversion costs (₹35,000-40,000 per vehicle), safety of gas cylinders, reduced boot space, and the availability of filling stations. The unions' leader, Sharad Rao, became MGL's unlikely partner when the company proposed an innovative solution: subsidized conversion loans, safety guarantees, and a promise of CNG prices at 60% of petrol costs.

MGL's execution strategy was brilliant in its pragmatism. Rather than building stations evenly across Mumbai, they created "CNG corridors"—dense clusters of stations along major transport routes. The Western Express Highway got six stations in 10 kilometers. This meant drivers could always find fuel, addressing "range anxiety" before Tesla made the term famous. They also pioneered mobile CNG cascades—trucks carrying compressed gas that could serve as temporary filling points during station maintenance.

The conversion centers became assembly lines of efficiency. MGL partnered with Lovato, an Italian kit manufacturer, to set up training centers where local mechanics learned installation. A typical conversion dropped from three days to six hours. The company introduced "CNG hospitals"—dedicated facilities for troubleshooting converted vehicles. When drivers complained about power loss, MGL's engineers worked with kit manufacturers to develop Mumbai-specific tuning parameters that accounted for the city's stop-and-go traffic patterns.

The numbers tell a story of remarkable transformation. In January 1998, MGL served 2,000 vehicles. By December 2000, that number had crossed 50,000. The growth wasn't linear—it was exponential once network effects kicked in. Each new station made CNG more viable, each converted vehicle became a rolling advertisement, each satisfied driver convinced colleagues to switch.

But the real catalyst was economics. With CNG priced at ₹16 per kilogram against petrol at ₹35 per liter, a typical auto-rickshaw driver saved ₹400-500 daily—nearly doubling their take-home income. MGL published these calculations in Marathi newspapers, ran testimonial campaigns featuring actual drivers, and stationed representatives at major auto-rickshaw stands to address concerns in real-time.

The safety narrative required careful management. After a cylinder explosion in Delhi (unrelated to MGL's operations), Mumbai's drivers nearly revolted. MGL responded with radical transparency: public pressure-testing of cylinders, live demonstrations of safety features, and a ₹10 lakh insurance policy for every converted vehicle. They brought in international safety auditors and publicized their certifications. When skeptics claimed CNG was more dangerous than petrol, MGL organized controlled burn tests showing CNG dissipating harmlessly while petrol created ground-level infernos.

The infrastructure growth was staggering. MGL went from 4 CNG stations in 1997 to 74 by 2002. Each station required land acquisition in Mumbai's impossibly expensive real estate market, multiple regulatory clearances, and complex engineering to handle high-pressure gas safely. The company pioneered the "dealer-owned, company-operated" model—partnering with existing petrol pump owners who provided land while MGL handled equipment and operations. This asset-light approach accelerated rollout while conserving capital.

By 2003, Mumbai's air quality data showed dramatic improvement. Suspended particulate matter had dropped 30%, sulfur dioxide levels fell 75%, and respiratory admissions in public hospitals declined noticeably. The Supreme Court, in a follow-up hearing, called Mumbai's CNG transition "a model for urban India." The transformation was so successful that other cities began mandatory conversion programs, creating a national market for CNG vehicles and equipment.

The rickshaw drivers who had protested in 1998 became MGL's biggest advocates by 2005. The company had fundamentally altered the economics of public transport—cleaner air was almost a bonus. The CNG revolution wasn't just about replacing fuel; it was about reimagining urban transport economics, proving that environmental and economic benefits could align, and demonstrating that infrastructure transformation was possible even in India's most complex city.

Today, with over 6,580 commercial vehicles beyond buses and rickshaws running on CNG, including tempos and trucks, Mumbai's CNG network has become as essential as its local trains. The story of how MGL converted a hostile, skeptical market into eager adopters offers lessons that extend far beyond energy—it's about understanding incentives, building trust, and recognizing that infrastructure success depends as much on human psychology as engineering excellence.

V. Piped Natural Gas: Entering Indian Homes

In 2001, Shanta Patil, a housewife in Mumbai's Mulund suburb, stood in her kitchen watching two MGL technicians drill a hole through her wall. Her neighbors had gathered, some warning about gas leaks, others curious about this "pipe that would replace cylinders." Shanta would become MGL's first residential piped natural gas (PNG) customer—a moment that seemed routine but represented a behavioral revolution decades in the making.

The challenge of bringing natural gas into Indian homes made the CNG rollout look simple. Auto-rickshaw drivers were rational economic actors who could calculate fuel savings. But Indian households had deep, multi-generational relationships with their LPG cylinders. The red cylinder delivered by the government-subsidized dealer was more than fuel—it was a symbol of middle-class arrival, a scarce resource that neighbors borrowed during emergencies, a physical asset you could see and trust.

MGL's initial market research in 2000 revealed the depth of resistance. Focus groups with Mumbai housewives surfaced fears that seemed to blend the practical with the mythological: pipes would leak and kill families in their sleep, gas pressure would vary making cooking impossible, the government would control their kitchens through remote valves, and most persistently, "How can gas flow continuously? It must run out sometime."

The company's first strategy—rational economic arguments—failed spectacularly. Presentations showing PNG was 30% cheaper than LPG, calculations of convenience value, safety statistics—none moved the needle. As one MGL executive later admitted, "We were engineers trying to sell mathematics to people making emotional decisions about their family's safety."

The breakthrough came from an unexpected source: Mumbai's massive new residential complexes. Builders like Hiranandani and Lodha were constructing townships with thousands of flats, and they needed differentiation. MGL pitched PNG as a premium amenity—like swimming pools or clubhouses. The builders loved it: they could advertise "no cylinder hassles," and the centralized infrastructure was easier than managing thousands of individual LPG connections.

The Hiranandani Gardens complex in Powai became MGL's Trojan horse. When 2,000 upper-middle-class families started using PNG without incident, it created social proof that no advertisement could match. MGL cleverly invited journalists to interview residents, organized kitty party demonstrations where housewives could see PNG stoves in action, and most brilliantly, created a "PNG kitchen" at their Wadala office where skeptical customers could cook actual meals.

The technical challenges of residential PNG were mind-boggling. Unlike CNG stations that MGL controlled end-to-end, residential connections required entering people's homes, dealing with illegal modifications, navigating building societies' politics, and managing safety in environments where customers might drill into walls without warning. Each building required a pressure reduction station, each flat needed specialized meters and safety devices, and the entire system had to work flawlessly 24/7.

MGL developed what they called the "trust infrastructure"—systems designed more for psychological comfort than technical necessity. The distinctive yellow pipelines were deliberately visible, showing gas was flowing. Odorant was added to naturally odorless gas so leaks could be detected by smell. Emergency helplines were staffed 24/7 with operators who spoke Marathi, Hindi, and Gujarati. Service technicians wore uniforms, carried photo IDs, and followed elaborate safety protocols that were as much performance as precaution.

The pricing strategy was crucial. While PNG was cheaper than LPG, MGL couldn't price it too low—that would signal inferior quality to status-conscious middle-class consumers. They settled on a 20-30% discount, enough to matter but not enough to seem suspicious. More importantly, they introduced "slabs" that rewarded higher consumption, encouraging customers to use PNG for water heating and other applications beyond cooking.

By 2005, MGL had connected 50,000 households, but growth was slower than hoped. The game-changer came from an unexpected regulatory shift. The government began reducing LPG subsidies for middle-class consumers while maintaining them for the poor. Suddenly, PNG's economic advantage widened dramatically. A cylinder that cost ₹300 subsidized jumped to ₹600 at market price, while PNG costs remained stable. The same families who had resisted for years now flooded MGL offices with applications.

The operational complexity of managing hundreds of thousands of household connections required technological innovation. MGL pioneered automated meter reading systems in India, deployed geographic information systems to map their underground network, and created predictive maintenance algorithms to prevent leaks before they occurred. The company's control room in BKC looked like a space mission control, with real-time monitoring of pressure, flow, and quality across thousands of kilometers of pipeline.

Social engineering was equally important. MGL created "PNG ambassadors"—satisfied customers who received small incentives to convince neighbors to convert. They partnered with cable TV operators to run hyperlocal advertisements featuring residents of specific buildings. When festivals approached, they offered special conversion camps with instant connections. The message shifted from "switch to PNG" to "your neighbors already have."

The numbers validated the strategy. From 948,892 domestic connections in 2017, MGL crossed 1.5 million by 2023. More importantly, customer acquisition costs dropped from ₹5,000 per connection to under ₹2,000 as network density increased. Each building converted became easier than the last—economies of scale in reverse, where the product became more valuable as more people used it.

The environmental impact was substantial but almost incidental to customer decisions. Each household switching from LPG to PNG reduced carbon emissions by approximately 150 kg annually. Multiply that by 1.5 million households, and MGL was eliminating 225,000 tons of CO2 yearly—equivalent to planting 10 million trees. But surveys showed less than 5% of customers cited environmental benefits as their primary motivation. The lesson was clear: green products succeed when they're better products that happen to be green, not the reverse.

Today, PNG has become so normalized that new Mumbai residents often don't know LPG was once the norm. MGL's patient, systematic conquest of the residential market offers a masterclass in infrastructure adoption: start with early adopters in controlled environments, create social proof, wait for regulatory tailwinds, and recognize that changing human behavior requires understanding hearts as much as minds.

VI. British Gas Exit & The Path to Independence (2000s)

In March 2003, Richard Olver, chairman of the newly demerged BG Group, stood before shareholders in London explaining why the company was exiting "non-core" emerging markets. Mumbai wasn't mentioned by name, but everyone at MGL knew their British partner was leaving. The divorce papers would take three years to finalize, but the relationship was effectively over. What followed was MGL's most crucial transition: from foreign-supported venture to truly Indian company.

The British Gas exit wasn't sudden—it was death by a thousand strategic cuts. The 1997 demerger that split British Gas into BG Group and Centrica had created an identity crisis. BG Group initially maintained emerging market positions, but as North Sea reserves depleted and LNG opportunities emerged, capital allocation priorities shifted. India's infrastructure projects, with their decade-long gestation periods and regulatory uncertainties, looked less attractive compared to immediate returns from liquefied natural gas trading.

Inside MGL's Marol office, the British exodus created panic and opportunity in equal measure. The British had brought more than capital—they provided technical expertise, international credibility, and most importantly, a buffer against political interference. Middle managers worried about reverting to public sector lethargy. Senior executives saw a chance to prove Indian capability. The next 18 months would determine whether MGL could survive independently.

GAIL's decision to buy out BG Group's stake wasn't predetermined. The Indian oil major had its own capital constraints and could have let a private player enter. But GAIL's leadership, particularly Chairman Proshanto Banerjee, recognized MGL's strategic value. This wasn't just about Mumbai—it was about controlling the template for city gas distribution across India. In December 2006, GAIL acquired BG Group's 49.75% stake for ₹670 crores, making MGL a wholly-owned subsidiary.

The price seemed steep then—₹670 crores for a company with revenues of ₹400 crores. But GAIL was buying more than cash flows. They were acquiring a functioning CDG model, trained workforce, established infrastructure, and most crucially, regulatory relationships that would take decades to rebuild. The transaction valued MGL at ₹1,350 crores; less than two decades later, it would be worth ten times that amount.

The immediate challenge was technical capacity. British engineers had handled complex decisions—pipeline route optimization, compression technology selection, safety protocol design. Their departure left knowledge gaps that couldn't be filled by hiring. MGL's solution was elegant: they created the industry's first "Gas University" in partnership with IIT Bombay, training engineers not just in technical skills but in decision-making frameworks the British had brought.

R.K. Singh, who became Managing Director during the transition, embodied the new Indian confidence. An IIT Delhi graduate who had spent his career in Indian PSUs, Singh rejected both servile adoption of foreign practices and knee-jerk nationalism. His philosophy: "Take what works from global best practices, adapt it to Indian conditions, and innovate where necessary." Under his leadership, MGL developed indigenous solutions that even BG Group later licensed for other markets.

The cultural transformation was profound. The British had run MGL like a private corporation—quick decisions, performance-based promotions, minimal bureaucracy. GAIL's culture was different—consensus-driven, seniority-based, process-heavy. Singh pioneered a hybrid model: maintaining corporate agility while adding public sector stability. Performance bonuses continued, but job security increased. Decision-making remained fast, but stakeholder consultation expanded.

One innovation from this period deserves special mention: the "Mumbai Model" of government relations. Unlike other PSUs that maintained arm's length relationships with regulators, MGL embedded itself in policy formation. They seconded engineers to the Petroleum and Natural Gas Regulatory Board, funded studies at policy think tanks, and created a revolving door where regulators joined MGL and vice versa. This wasn't corruption—it was ecosystem building.

The operational improvements post-British exit were remarkable. Customer acquisition costs dropped 40% as MGL replaced expensive expatriate consultants with local talent. They developed India-specific solutions like pre-fabricated CNG stations that could be assembled in 60 days versus six months for conventional builds. Most impressively, they created "jugaad engineering"—using Indian improvisation to solve problems British standards deemed impossible.

Financial performance vindicated the independence strategy. Revenues grew from ₹400 crores in 2003 to ₹1,200 crores by 2010. More importantly, EBITDA margins expanded from 15% to 25% as operational efficiencies kicked in. The company generated enough cash to fund expansion without external borrowing—a remarkable achievement for an infrastructure business. By 2010, MGL was debt-free, sitting on cash reserves that exceeded its annual capital expenditure needs.

The technology transfer story was equally impressive. MGL didn't just maintain British-era systems; they improved them. The company developed proprietary SCADA systems tailored for Indian conditions—handling power fluctuations, monsoon flooding, and temperature extremes that European systems couldn't manage. They pioneered trenchless drilling techniques for congested areas, created mobile compression units for rapid network expansion, and developed leak detection systems that worked in Mumbai's electromagnetic interference-heavy environment.

But perhaps the most significant achievement was regulatory. Without British Gas's international weight, MGL had to build credibility through performance. They maintained perfect safety records—zero fatal accidents in a decade. They exceeded environmental targets, reducing Mumbai's vehicular emissions beyond Supreme Court mandates. Most cleverly, they positioned themselves as partners to regulators rather than subjects, offering technical expertise for policy formation and volunteering for pilot programs.

By 2010, the transformation was complete. MGL had evolved from a foreign-dependent joint venture to a self-sufficient Indian infrastructure champion. The irony wasn't lost on observers: BG Group's exit, initially seen as abandonment, had forced MGL to develop capabilities that made it stronger than it ever could have been as a subsidiary. The company that emerged from this transition was uniquely positioned for its next chapter: going public and competing in an open market.

VII. Going Public: The 2016 IPO

On July 1, 2016, at 9:15 AM, Rajeev Kumar rang the opening bell at the Bombay Stock Exchange as MGL's shares began trading. The initial public offering had priced at ₹421 per share—the top of the range—and within minutes, the stock shot up 38%. The government's stake sale had raised ₹982 crores, but more importantly, it marked MGL's transformation from a PSU subsidiary to a publicly accountable corporation. The journey to this moment revealed as much about India's capital market evolution as MGL's operational maturity.

The decision to list wasn't MGL's alone. In 2014, the Modi government had announced aggressive disinvestment targets—raising ₹70,000 crores annually by selling stakes in profitable PSUs. MGL, with its monopoly position, steady cash flows, and clean balance sheet, was an obvious candidate. But GAIL's board initially resisted, viewing MGL as a crown jewel that funded expansion into newer territories. The government's insistence on "unlocking value" finally prevailed.

The IPO preparation revealed MGL's hidden strengths and glaring weaknesses. On the positive side, the numbers were stellar: EBITDA margins of 28%, return on equity exceeding 20%, and a debt-free balance sheet with ₹300 crores in cash. The company had grown revenues at 15% CAGR for five years while maintaining capital discipline. Infrastructure investors salivated at such metrics—steady growth, high margins, minimal capital intensity post-network creation.

But the roadshows also exposed concerns. Fund managers in Mumbai, Singapore, and London asked uncomfortable questions: What happens when your exclusivity period ends? How will electric vehicles impact CNG demand? Why should we trust government companies with minority shareholder interests? The most persistent question: "Is this a growth story or a dividend yield play?"

MGL's management, led by Managing Director Sanjay Shende, crafted a narrative that addressed each concern. On exclusivity, they emphasized infrastructure moats—even after regulatory protection ended, would competitors spend billions duplicating pipelines? On EVs, they positioned natural gas as a transition fuel, buying time until electric infrastructure matured. On governance, they pointed to independent directors, quarterly earnings calls, and dividend policies that protected minority shareholders.

The IPO structure itself was carefully engineered. The government diluted 10% through fresh equity and another 2.5% through an offer for sale. Retail investors received 35% allocation, institutions got 50%, and employees secured 5% at a discount. This broad-based ownership structure ensured no single entity could manipulate prices and created natural demand from Mumbai's residents who were also MGL's customers.

The anchor book revealed institutional quality. GIC of Singapore, Fidelity, Aberdeen, and Government Pension Fund of Norway participated. These weren't momentum traders but long-term infrastructure investors who understood regulated utilities. Their presence signaled international validation of MGL's business model and governance standards. The domestic institutions—HDFC Mutual Fund, ICICI Prudential, SBI Mutual Fund—provided stability and local market understanding.

Pricing negotiations were intense. Investment bankers from Kotak Mahindra, Axis Capital, and HSBC initially suggested ₹350-380 per share, valuing MGL at 15x earnings. But the book-building process revealed appetite at higher valuations. Institutional investors compared MGL to Indraprastha Gas (IGL), Delhi's equivalent, which traded at 20x earnings. The final price of ₹421 valued MGL at ₹4,150 crores—18x trailing earnings, reflecting optimism about Mumbai's growth and MGL's expansion potential.

The listing day performance exceeded expectations. The 38% pop to ₹580 created wealth for 50,000 retail investors who had applied for shares. More importantly, it established MGL as a liquid, institutional-quality stock. Daily trading volumes averaged ₹50 crores, ensuring easy entry and exit for funds. The stock's inclusion in the Nifty 500 index within six months created passive buying from index funds.

Post-IPO, MGL's behavior changed subtly but significantly. Quarterly earnings calls became events where management faced aggressive questioning about customer additions, margin pressures, and capital allocation. The company started providing detailed operational metrics—daily CNG sales volumes, weekly PNG connections, monthly infrastructure additions. This transparency initially seemed excessive to PSU veterans but built enormous credibility with analysts.

The dividend policy crystallized post-listing. MGL committed to distributing 30-50% of profits as dividends while retaining enough for growth capital expenditure. This balanced approach attracted both growth and income investors. The first post-IPO dividend of ₹7 per share (1.7% yield) seemed modest, but consistent increases established MGL as a dividend aristocrat. By 2023, the company was paying ₹20 per share—a 60% payout ratio that reflected infrastructure maturity.

Capital allocation discipline improved markedly under public scrutiny. Pre-IPO, MGL had occasionally pursued vanity projects—CNG stations in unviable locations for political reasons. Post-IPO, every investment faced ROI scrutiny. The company published hurdle rates (15% project IRR), payback periods (maximum 7 years), and utilization targets (60% capacity within 2 years). Projects failing these metrics were ruthlessly eliminated.

The stakeholder dynamics shifted fundamentally. Pre-IPO, MGL managed three constituencies: GAIL, the Maharashtra government, and customers. Post-IPO, institutional investors became the fourth pillar, often the most vocal. When APM gas allocations were cut in 2023, investors punished the stock with a 20% decline, forcing management to communicate mitigation strategies more effectively than any regulator demanded.

VIII. The Business Model: Monopoly with a Purpose

Understanding MGL's business model requires appreciating a fundamental paradox: it's a monopoly that nobody resents. In most industries, monopolies extract maximum value from captive customers. But MGL operates under a regulatory framework that caps returns while mandating service obligations. The result is a business model that generates steady profits without exploitation—a unicorn in infrastructure investing.

The core economics are deceptively simple. MGL buys natural gas from GAIL at regulated prices, transports it through its pipeline network, and sells it to vehicles (as CNG) and households (as PNG) at a margin. But this simplicity masks enormous complexity in execution, regulation, and capital allocation. The company essentially runs two different businesses—CNG and PNG—with distinct economics, customer bases, and growth trajectories.

The CNG business, contributing 68% of volumes, operates on rapid turnover and thin margins. A typical CNG station serves 800-1,000 vehicles daily, with each fill-up taking 3-5 minutes. The infrastructure investment—₹3-4 crores per station—gets recovered through volumes rather than margins. MGL earns approximately ₹8-10 per kilogram of CNG sold, but when a station dispenses 3,000 kg daily, the numbers add up quickly. The payback period for a well-located station is typically 3-4 years.

PNG economics are inverted: high margins but slow turnover. Connecting a household costs ₹5,000-7,000, but once connected, that customer generates ₹200-300 monthly for decades. The churn rate is virtually zero—less than 0.5% annually. This creates an annuity-like revenue stream that equity investors love. The initial capital intensity is offset by minimal maintenance costs and no customer acquisition expenses post-connection.

The real moat isn't regulatory but physical. Mumbai's underground is now so congested that laying parallel pipelines would be economically suicidal. MGL's network, built over 25 years, required 40,000 road-cutting permissions, ₹5,000 crores in capital investment, and relationships with thousands of building societies. A competitor would need to replicate this while MGL already serves the market. It's like asking someone to build a parallel railway network in Manhattan.

The Administered Price Mechanism (APM) has been MGL's secret weapon. Under APM, the government allocates domestic natural gas to priority sectors—city gas distribution included—at prices significantly below import parity. When international LNG costs $12 per MMBtu, MGL receives APM gas at $6.5. This pricing advantage translates directly to margins, enabling MGL to price CNG at 60% of petrol while maintaining 30% EBITDA margins.

But APM allocation cuts have emerged as the key risk. In 2023, the government reduced APM allocation by 21%, forcing MGL to source expensive imported gas. Margins compressed from 30% to 24% within quarters. The company's response—passing costs to consumers while improving operational efficiency—showcased both pricing power and execution capability. Despite 15% price increases, volumes grew 8%, suggesting remarkable demand inelasticity.

The volume-margin tradeoff is MGL's constant balancing act. The company could maximize margins by raising prices to just below petrol/diesel levels. But this would slow adoption, reduce environmental benefits, and invite regulatory backlash. Instead, MGL maintains a "fair margin" philosophy—pricing CNG at 60-65% of petrol, ensuring customer savings while generating reasonable returns. This stakeholder capitalism approach has built enormous goodwill that translates to regulatory support during crises.

Infrastructure utilization showcases operational excellence. MGL's pipeline capacity utilization exceeds 70%—remarkable for a network that must handle daily demand fluctuations, seasonal variations, and geographic disparities. The company uses sophisticated algorithms to predict demand, optimize pressure, and minimize losses. System losses are below 0.5%, comparing favorably to 2-3% global benchmarks. Every percentage point saved drops directly to the bottom line.

The working capital dynamics are entrepreneur's dreams. Customers prepay for CNG at stations—immediate cash collection. Household PNG bills are paid within 30 days with minimal defaults. Meanwhile, MGL enjoys 45-day payment terms with GAIL. This negative working capital cycle means growth actually generates cash rather than consuming it. The company's cash conversion ratio exceeds 100%, explaining how infrastructure expansion happens without debt.

Network effects amplify competitive advantages. Each new CNG station makes the network more valuable for vehicle owners. Each PNG connection makes building-wide infrastructure more viable. Each satisfied customer becomes a word-of-mouth marketer. The business exhibits increasing returns to scale—the 1,000th connection costs less than the 100th, the second station in a locality is more profitable than the first.

Regulatory relationships represent intangible assets. MGL doesn't fight regulators; it partners with them. The company seconds employees to regulatory bodies, funds policy research, and volunteers for pilot programs. When regulations change, MGL often knows in advance and influences outcomes. This isn't corruption but ecosystem participation. The company has made itself so integral to Mumbai's energy infrastructure that adverse regulations would be self-defeating for policymakers.

The capital allocation framework reflects infrastructure realities. MGL targets 15% project IRRs—not spectacular but steady. The company evaluates investments through multiple lenses: financial returns, strategic value, regulatory compliance, and social impact. This balanced scorecard approach means some projects with marginal economics get approved for network completeness while others with high returns get rejected for regulatory risks.

The recent push into compressed biogas (CBG) exemplifies strategic evolution. CBG, produced from organic waste, offers carbon neutrality while utilizing existing CNG infrastructure. MGL is investing ₹1,000 crores in CBG plants, accepting lower initial returns for long-term positioning. As carbon taxes inevitably arrive, CBG will transform from expensive alternative to economic necessity. The infrastructure and customer relationships already exist—MGL just needs to change the molecule flowing through pipes.

IX. Modern Challenges & Competition

October 13, 2023, marked Black Friday for city gas distribution stocks. MGL crashed 20% in a single session after the government announced a 21% cut in APM gas allocation—the second reduction in six months. The stock's violent reaction revealed an uncomfortable truth: despite decades of infrastructure building and millions of customers, MGL remained vulnerable to regulatory whims and technological disruption. The challenges facing the company today are existential in ways the founders never imagined.

The APM allocation cuts represent more than margin pressure—they signal a fundamental shift in government priorities. With domestic gas production stagnant and demand soaring, the government faces impossible choices: prioritize fertilizer production for food security, power generation for economic growth, or city gas distribution for urban pollution. MGL's privileged access to cheap gas, once considered sacrosanct, now seems increasingly fragile. The company must now source 35% of requirements from expensive spot markets where prices fluctuate daily.

But the electric vehicle revolution poses the greater long-term threat. Every Tesla on Mumbai's roads, every Ola electric scooter whizzing past CNG stations, represents a future where MGL's core product becomes obsolete. The numbers are still small—EVs constitute less than 2% of Mumbai's vehicles—but the trajectory is unmistakable. The government's FAME subsidies, charging infrastructure investments, and 2030 electrification targets create momentum that seems irreversible.

MGL's response reveals both denial and adaptation. Management argues EVs will primarily replace petrol vehicles, not CNG, since both serve different segments. They're partially right—the economics still favor CNG for commercial vehicles running 200+ kilometers daily. But this misses the psychological shift. Once EVs become mainstream for personal transport, CNG starts feeling like yesterday's technology. The company that positioned itself as the clean alternative now risks being seen as the dirty incumbent.

Competition has arrived from unexpected directions. Reliance and Adani, India's infrastructure giants, have won city gas licenses in territories adjacent to Mumbai. While MGL's exclusivity in Mumbai proper remains, these players are cherry-picking profitable corridors in Thane and Raigad. Their strategy is clever: build networks in new development areas where infrastructure costs are lower, then gradually encroach on MGL's territory when exclusivity ends.

The new entrants bring capabilities MGL lacks. Reliance leverages its petroleum retail network, offering CNG at existing fuel stations without land acquisition headaches. Adani uses its port infrastructure to import LNG directly, bypassing GAIL's transmission charges. Both have deeper pockets, higher risk appetites, and most dangerously, ecosystems that create customer stickiness. When Reliance offers bundled discounts across fuel, telecom, and retail, MGL's standalone model looks antiquated.

Technological disruption extends beyond electrification. Hydrogen fuel cells, once science fiction, are becoming commercial reality. The government's National Hydrogen Mission targets green hydrogen at $2 per kilogram by 2030—potentially cheaper than CNG. While hydrogen infrastructure would take decades to build, MGL's existing pipeline network could theoretically carry hydrogen with modifications. But this transition requires massive capital investment with uncertain returns—exactly the kind of bet public market investors hate.

The renewable natural gas opportunity offers hope amid disruption. MGL's compressed biogas initiatives could transform waste management while creating carbon-neutral fuel. The company is partnering with municipal corporations to build CBG plants at landfill sites, creating circular economies where city waste becomes city fuel. But CBG currently costs twice as much as natural gas to produce. Without carbon taxes or renewable mandates, the economics don't work. MGL is betting regulations will eventually make CBG viable, but timing such transitions has bankrupted better companies.

Customer behavior adds another layer of complexity. The post-COVID world has fundamentally altered transportation patterns. Work-from-home reduced commuting, app-based delivery replaced personal shopping, and metro expansion offered alternatives to road transport. CNG volumes, which grew consistently for two decades, have plateaued. The company's growth now depends entirely on PNG connections, but even that faces headwinds as builders prefer electric induction cooking in premium properties.

Regulatory uncertainty compounds every challenge. The Petroleum and Natural Gas Regulatory Board's decisions seem increasingly unpredictable. Recent orders mandating infrastructure sharing, capping transportation charges, and reducing exclusivity periods have systematically eroded MGL's moat. The regulator's goal—increasing competition to reduce consumer prices—directly conflicts with MGL's shareholder interests. The company that once influenced policy now finds itself reacting to adverse regulations.

Financial markets have noticed these headwinds. MGL's valuation multiples have compressed from 20x earnings in 2018 to 12x in 2024. The stock's correlation with oil prices has increased, making it a commodity play rather than an infrastructure story. Institutional ownership has declined as ESG funds question natural gas's "transition fuel" status. The company that listed with fanfare now trades at discounts to book value.

Yet MGL's response shows resilience born from decades of crisis management. The company is diversifying beyond natural gas—electric vehicle charging stations at CNG outlets, renewable energy investments, and city infrastructure services. They're improving operational efficiency, with AI-powered demand forecasting reducing system losses. Most importantly, they're leveraging their greatest asset: relationships with 2.3 million customers who trust the brand.

The capital allocation strategy has shifted from growth to optimization. Instead of building new CNG stations, MGL is upgrading existing ones with multiple dispensing points, reducing wait times. Rather than expanding into marginal territories, they're densifying networks in profitable areas. The company is generating cash flows that fund dividends and buybacks while maintaining optionality for strategic pivots.

X. Playbook: Lessons from MGL

MGL's journey from government joint venture to public market infrastructure champion offers a masterclass in building essential services in emerging markets. The playbook that emerges isn't just about laying pipes or compressing gas—it's about navigating the complex intersection of politics, economics, technology, and human behavior that defines infrastructure in developing nations.

Lesson 1: Infrastructure Monopolies Are Made, Not Born

MGL's monopoly wasn't granted—it was earned through decades of patient capital deployment. The company understood that in infrastructure, being first creates advantages that compound over time. Every pipeline laid made the next one more valuable. Every customer acquired reduced the unit cost of service. Every year of safe operations built regulatory goodwill that translated to favorable policies. The lesson for investors: identify infrastructure plays early in the adoption curve when capital requirements deter competition but demand visibility exists.

Lesson 2: Foreign Partnerships as Capability Bridges

The British Gas partnership wasn't about capital—GAIL could have funded MGL independently. It was about importing decades of accumulated knowledge in months. British engineers didn't just bring technology; they brought decision frameworks, safety cultures, and stakeholder management practices that became embedded in MGL's DNA. The lesson extends beyond infrastructure: emerging market companies should view foreign partnerships as capability accelerators, not permanent dependencies.

Lesson 3: Regulatory Capture Through Competence

MGL's influence over regulations came not from lobbying but from making themselves indispensable to policy formation. By seconding engineers to regulatory bodies, funding academic research, and providing technical inputs for legislation, MGL shaped the rules governing their industry. This wasn't corruption—it was expertise deployment. Regulators needed MGL's knowledge more than MGL needed regulatory favors. The sophisticated investor recognizes that regulatory moats built on competence are more durable than those built on connections.

Lesson 4: The Economics of Behavior Change

Converting Mumbai to natural gas required changing millions of individual decisions. MGL succeeded by understanding that infrastructure adoption follows predictable patterns: start with economically motivated early adopters (commercial vehicles), create visible success stories (reduced operating costs), address safety concerns through radical transparency, and let network effects drive mainstream adoption. The same playbook applies to any infrastructure requiring consumer behavior change—electric vehicles, renewable energy, digital payments.

Lesson 5: Market Timing Matters More Than Technology

MGL didn't invent natural gas distribution—the technology existed globally for decades. Their genius was recognizing when India was ready: environmental consciousness had reached courts, economic liberalization enabled private participation, and urban density made pipeline economics viable. Infrastructure investors must distinguish between technological possibility and market readiness. Being too early is indistinguishable from being wrong.

Lesson 6: Physical Networks Create Digital Moats

MGL's 5,000-kilometer pipeline network through Mumbai's underground represents an unreplicable asset. But the physical infrastructure created something more valuable: data on consumption patterns, customer relationships, and operational expertise that no competitor can quickly replicate. Modern infrastructure investing requires recognizing that physical assets enable digital advantages that become the real moat.

Lesson 7: Capital Discipline in Capital-Intensive Businesses

Despite operating in a capital-intensive industry, MGL remained debt-free through most of its history. The secret was sequential expansion: fully utilize capacity in one area before expanding to another, use operating cash flows to fund growth, and resist the temptation of debt-funded empire building. This discipline meant slower growth but higher returns on capital—a tradeoff that created enormous shareholder value over time.

Lesson 8: Stakeholder Capitalism as Strategy

MGL's "fair margin" philosophy—pricing below profit maximization to ensure customer savings—seemed foolish to financial analysts. But this approach built social capital that proved invaluable during crises. When accidents happened, communities defended MGL. When regulations tightened, politicians protected MGL. When competition arrived, customers stayed loyal. The lesson: in infrastructure businesses serving essential needs, stakeholder capitalism isn't corporate social responsibility—it's risk management.

Lesson 9: The Optionality of Infrastructure

MGL's pipeline network was built for natural gas but could theoretically carry hydrogen, biogas, or other molecules. The CNG stations designed for vehicles can accommodate electric charging. The customer relationships developed for energy can extend to other utilities. Infrastructure investments create platforms that enable optionality. The intelligent investor values not just current cash flows but future possibilities.

Lesson 10: Complexity as Competitive Advantage

MGL's business seems simple—buy gas, transport gas, sell gas. But executing this requires managing 40,000 permissions, 2.3 million customer relationships, 24/7 operations across thousands of sites, and constant regulatory negotiations. This complexity deters new entrants more effectively than any regulatory protection. The paradox of infrastructure investing: the most attractive businesses are often the most complex to operate.

These lessons extend beyond MGL or even infrastructure. They speak to fundamental principles of building essential services in complex markets: the importance of timing, the value of capabilities over capital, the power of network effects, and the durability of businesses that align private profits with public benefits. MGL's playbook isn't just about natural gas—it's about recognizing that infrastructure success comes from understanding the society you're building for, not just the technology you're building with.

XI. Bear vs. Bull Case & Valuation

The investment community remains sharply divided on MGL's future. Bulls see an essential service provider with an irreplaceable moat trading at distressed valuations. Bears see a melting ice cube facing technological obsolescence and regulatory deterioration. Both sides marshal compelling evidence, and understanding their arguments is crucial for any fundamental investor considering MGL.

The Bull Case: Undervalued Infrastructure Asset with Multiple Growth Levers

Bulls begin with valuation. At 12x earnings, MGL trades at a 40% discount to its five-year average and half the multiple of global gas utilities. This despite maintaining 24% EBITDA margins, generating 18% return on equity, and growing volumes at 8% annually. The market, bulls argue, is pricing in catastrophe that won't materialize.

The urbanization megatrend underpins bullish optimism. Mumbai's population grows by 300,000 annually, each resident requiring energy. New construction means new PNG connections—MGL connects 1,000 households daily. With penetration at just 35% of Mumbai's potential households, decades of growth remain. The company's 23.8% dividend payout ratio leaves ample capital for expansion while rewarding shareholders. At current prices, the dividend yield exceeds 2.5%, with consistent growth probable.

Bulls dismiss EV disruption as overblown. Commercial vehicles, MGL's core market, won't electrify quickly. The total cost of ownership for CNG vehicles remains 40% lower than electric equivalents. Battery technology hasn't solved the weight, range, and charging time challenges for vehicles running 300 kilometers daily. Even assuming 50% EV penetration by 2040, CNG demand would continue growing in absolute terms as the total vehicle population expands.

The APM allocation cuts, while painful, are manageable. MGL has pricing power—recent 15% price hikes barely dented demand. The company's cost structure allows margin preservation even with expensive imported gas. Moreover, domestic gas production is increasing with new field developments. APM allocations could improve as supply grows, providing margin expansion optionality.

Environmental regulations remain supportive. The Supreme Court's pollution mandates haven't disappeared. If anything, climate consciousness is intensifying. Natural gas produces 30% less carbon than petrol, 40% less than diesel. Until hydrogen or renewable electricity becomes viable at scale, natural gas remains the pragmatic clean alternative. Governments won't sacrifice environmental gains for marginally lower fuel prices.

The infrastructure moat is strengthening, not weakening. Network effects mean each new connection reduces per-unit costs. MGL's customer acquisition cost has dropped 60% over five years. The company's operational excellence—0.5% system losses, 99.9% uptime, zero fatal accidents in five years—creates switching costs beyond economics. Customers trust MGL with gas pipes in their homes—that trust takes decades to build and moments to destroy.

Bulls see optionality that bears ignore. MGL's compressed biogas initiatives position them for the renewable transition. The company's infrastructure could carry hydrogen with modifications. Electric vehicle charging at CNG stations leverages existing real estate. The brand, relationships, and operational capabilities extend beyond molecules. MGL is an energy infrastructure company, not just a natural gas distributor.

The Bear Case: Structural Decline Masked by Temporary Growth

Bears counter that MGL is a value trap—optically cheap but structurally impaired. The company faces not one disruption but multiple simultaneous threats. Electric vehicles aren't the future; they're the present. Every major auto manufacturer has announced EV transitions. The government's FAME subsidies, PLI schemes, and charging infrastructure investments make electrification inevitable. MGL's addressable market shrinks daily.

The APM mechanism is dying. India's energy security priorities have shifted from domestic gas to renewable electricity. The government won't subsidize fossil fuels indefinitely. Each allocation cut is permanent, not cyclical. MGL's margins will compress to global utility standards—15% EBITDA at best. At normalized margins, the current valuation looks expensive, not cheap.

Competition is intensifying everywhere. Reliance and Adani aren't just entering city gas distribution; they're reimagining it. Their integrated ecosystems, technological capabilities, and financial resources dwarf MGL's. When exclusivity periods end, MGL will face competition from players who view gas distribution as customer acquisition for broader platforms. Market share losses are inevitable.

Bears highlight execution risks MGL investors ignore. The company must invest ₹1,000 crores annually just to maintain market position. But every rupee invested in CNG infrastructure becomes a stranded asset as EVs proliferate. Every PNG connection in a building that later chooses electric cooking is wasted capital. The company faces the innovator's dilemma: invest in dying businesses or pivot to uncertain alternatives.

Regulatory risks are mounting, not moderating. The PNGRB's recent orders show clear bias toward consumer interests over infrastructure returns. Infrastructure sharing mandates, margin caps, and shortened exclusivity periods systematically erode MGL's moat. The regulator views MGL's returns as excessive, suggesting further adverse regulations are probable.

The financial flexibility bulls tout is illusory. Yes, MGL is debt-free with cash reserves. But maintaining competitiveness requires massive investments with declining returns. The dividend payout ratio will compress as capital needs increase. The company can't simultaneously fund traditional infrastructure, renewable transitions, and shareholder returns. Something must give, and shareholders will suffer.

Bears see ESG risks that destroy terminal value. Natural gas isn't clean—it's less dirty. As carbon accounting sophisticates, natural gas's methane leakage problems become visible. ESG funds are already divesting fossil fuel infrastructure. MGL might generate cash flows for years, but terminal value approaches zero as the world decarbonizes. The company is a melting ice cube generating cash while slowly disappearing.

Valuation Framework: Scenario Analysis

Base Case (50% probability): MGL muddles through—moderate volume growth offset by margin compression, competition contained to peripheral areas, EVs grow but don't dominate commercial transport. Fair value: ₹1,100-1,200 per share.

Bull Case (30% probability): Urbanization drives sustained demand, hydrogen transition creates new opportunities, regulatory environment stabilizes, and EVs disappoint in commercial segments. Fair value: ₹1,500-1,800 per share.

Bear Case (20% probability): EV adoption accelerates, competition intensifies, margins compress to global utility levels, and stranded asset write-offs emerge. Fair value: ₹700-800 per share.

The wide valuation range reflects genuine uncertainty about MGL's future. The company sits at the intersection of multiple transitions—energy, transportation, environmental, technological. Position sizing should reflect this uncertainty. MGL might be a contrarian value play or a value trap. Time, not analysis, will reveal which.

XII. The Future: Beyond Natural Gas

Standing at MGL's new research facility in Wadala, watching engineers test hydrogen blending in natural gas pipelines, you glimpse a possible future—one where MGL transforms from natural gas distributor to multi-molecule energy platform. The company is investing ₹1,000 crores in renewable energy ventures, partnering with BMC for compressed biogas plants, and quietly preparing for a world where "natural gas" becomes anachronistic. Whether this transformation succeeds will determine if MGL thrives for another generation or becomes a footnote in India's energy transition.

The hydrogen opportunity is tantalizing but uncertain. MGL's existing pipeline network could theoretically carry hydrogen blends up to 20% without major modifications. Beyond that requires new metallurgy, compression technology, and safety systems. The company is running pilot projects in industrial areas, blending 5% hydrogen with natural gas. Early results show promise—stable combustion, no pipeline degradation, minimal efficiency losses. But scaling from 5% to 50% isn't linear; it's exponential in complexity and cost.

The green hydrogen economics remain challenging. At current production costs of $5-6 per kilogram, hydrogen can't compete with natural gas at $6.5 per MMBtu. But cost curves are declining rapidly. Solar electricity for electrolysis is approaching ₹2 per unit. Electrolyzer costs have dropped 60% in five years. The government's National Hydrogen Mission targets $2 per kilogram by 2030—potentially game-changing for MGL. The company that built Mumbai's gas network might rebuild it for hydrogen.

Compressed biogas represents a nearer-term opportunity. MGL is developing four CBG plants processing 500 tons of municipal waste daily. The technology is proven—anaerobic digestion isn't rocket science. The challenge is feedstock aggregation and quality control. Mumbai generates 9,000 tons of waste daily, theoretically enough for 20 CBG plants. But segregating organic waste, maintaining consistent quality, and managing seasonal variations require operational excellence beyond traditional gas distribution.

The circular economy narrative is compelling. Mumbai's waste becomes Mumbai's fuel, reducing landfill pressure while creating renewable energy. Each CBG plant prevents 50,000 tons of CO2 equivalent emissions annually. The government mandates 5% CBG blending by 2028, creating guaranteed demand. MGL's existing CNG infrastructure needs no modification for CBG—same molecule, different source. The company could become India's largest waste-to-energy player without leaving Mumbai.

Electric vehicle charging infrastructure offers diversification within disruption. MGL is installing EV chargers at CNG stations, leveraging prime real estate and existing customer traffic. The strategy is defensive and offensive simultaneously—if EVs cannibalize CNG demand, at least capture the replacement revenue. The company's 250+ stations across Mumbai provide coverage density that pure-play charging companies would take years to replicate.

But the real innovation might be business model evolution. MGL is exploring "energy as a service" offerings—bundled packages including gas, electricity, and eventually hydrogen for commercial customers. Industrial clients could receive integrated energy management, optimizing across multiple sources based on price and carbon intensity. The company's operational excellence in 24/7 service delivery positions them well for complex energy solutions.

The technological infrastructure being built transcends molecules. MGL's investment in SCADA systems, IoT sensors, and predictive analytics creates capabilities applicable to any network business. The company now monitors 5,000 kilometers of pipeline in real-time, predicting failures before they occur. This same technology could manage water distribution, district cooling, or fiber optic networks. The future MGL might be an urban infrastructure platform that happens to include gas.

Partnerships reveal strategic direction. MGL's collaboration with NTPC for green hydrogen, with IOCL for CBG offtake, and with Tata Power for EV charging suggests ecosystem building rather than solo transformation. The company recognizes that energy transitions require collaboration across value chains. No single player can manage production, distribution, and consumption of multiple energy vectors. MGL is positioning itself as the distribution partner of choice for whatever molecules or electrons flow through Mumbai.

The regulatory environment is surprisingly supportive of transformation. The PNGRB has approved hydrogen blending trials, facilitated CBG integration, and encouraged EV infrastructure development. Regulators recognize that existing gas infrastructure must evolve rather than become stranded. MGL's proactive engagement—volunteering for pilots, sharing data, co-developing standards—builds regulatory capital for future transitions.

Financial markets remain skeptical about transformation narratives. Investors have heard too many old economy companies claim tech pivots that never materialized. MGL's challenge is demonstrating that renewable initiatives generate returns, not just press releases. The company needs quick wins—a profitable CBG plant, successful hydrogen blending, growing EV charging revenues—to build credibility.

The organizational challenge might be greatest. MGL's 1,200 employees excel at building pipelines, managing compression, and ensuring safety. Asking them to become waste management experts, hydrogen engineers, and renewable energy developers requires massive capability building. The company is partnering with IIT Bombay for training programs, hiring from renewable sectors, and creating innovation labs. But cultural transformation takes longer than strategic planning.

The next decade will determine whether MGL's transformation succeeds. The optimistic scenario sees MGL as Mumbai's integrated clean energy provider—managing renewable molecules, green electrons, and circular economies. The pessimistic scenario sees expensive experiments that distract from core business decline. The realistic scenario probably lies between—partial transformation with natural gas remaining relevant longer than futurists predict but shorter than incumbents hope.

For investors, MGL's future represents a fascinating optionality play. The current valuation prices in minimal transformation success. Any evidence of viable new businesses could trigger rerating. But transformation requires patient capital, accepting lower returns today for potential tomorrow. Whether public markets provide such patience remains uncertain. MGL's journey from natural gas to whatever comes next will test whether Indian infrastructure companies can evolve with energy transitions or become casualties of them.

XIII. Conclusion: The Infrastructure Imperative

As Mumbai's skyline transforms with each passing year—new towers reaching skyward, metro lines snaking through neighborhoods, electric vehicles gliding silently through streets—MGL's pipes run beneath it all, invisible yet essential. The company that began as a solution to Mumbai's pollution crisis has become inseparable from the city's functioning. This symbiosis between urban infrastructure and urban life defines MGL's past and will determine its future.

The MGL story transcends natural gas or even energy. It's about how essential infrastructure gets built in complex democracies, how foreign expertise catalyzes local capability, how regulatory frameworks evolve with technology, and how patient capital creates lasting value. These lessons matter because India needs massive infrastructure investment—$1.4 trillion by 2030 according to government estimates. Understanding what worked and what didn't in MGL's journey illuminates paths forward for water, waste, transportation, and digital infrastructure.

The company's financial performance validates the infrastructure investment thesis. From inception to IPO, MGL generated returns exceeding 20% annually for shareholders. Post-listing, despite multiple disruptions, the stock has delivered 12% annual returns including dividends. For a utility business in an emerging market facing technological disruption, these returns are remarkable. They demonstrate that infrastructure, executed well, creates value even in challenging environments.

But MGL's societal impact dwarfs financial returns. The company has prevented millions of tons of carbon emissions, reduced Mumbai's air pollution by 40%, and provided reliable energy to millions of households. These externalities don't appear in financial statements but represent real value creation. As ESG investing matures from sloganeering to serious capital allocation, companies like MGL that generate positive externalities while earning fair returns become increasingly valuable.

The governance evolution from PSU subsidiary to listed company offers hope for India's public sector transformation. MGL proves that government-owned companies can operate efficiently, treat minority shareholders fairly, and compete with private players. The key ingredients—professional management, independent boards, market discipline, and regulatory clarity—are replicable. If MGL can transform, so can hundreds of other PSUs sitting on valuable assets but destroying shareholder value.

The challenges facing MGL—technological disruption, regulatory uncertainty, competitive intensity—mirror those confronting infrastructure globally. How does century-old infrastructure adapt to climate change? Can fossil fuel systems transition to renewable energy? Will public utilities survive platform economics? MGL's responses, successful or otherwise, provide early indicators for global infrastructure evolution.

For fundamental investors, MGL represents a complex but potentially rewarding opportunity. The company trades at depressed valuations reflecting multiple uncertainties. But uncertainty creates opportunity for investors willing to undertake serious analysis. The key questions—EV adoption rates, hydrogen economics, regulatory evolution—are answerable through careful research. The patient investor who correctly assesses these variables could generate substantial returns.

The broader lesson is that infrastructure investing requires different frameworks than growth investing. Infrastructure doesn't compound at 30% annually, doesn't scale infinitely, doesn't winner-take-all. But infrastructure also doesn't disappear overnight, doesn't face rapid obsolescence, doesn't depend on fickle consumer preferences. Understanding these differences is crucial as India's capital markets mature and infrastructure becomes a distinct asset class.

MGL's next chapter will be written by forces beyond its control—government policies on energy transition, technological breakthroughs in batteries or hydrogen, global carbon pricing mechanisms, and Mumbai's continued growth. But the company's response to these forces remains within management's control. The same capabilities that built natural gas infrastructure—execution excellence, stakeholder management, patient capital deployment—must now build whatever comes next.

The ultimate judgment on MGL depends on time horizons. Short-term traders might avoid a company facing such uncertainties. Long-term investors might embrace a company with proven execution selling at distressed valuations. Income investors might appreciate growing dividends from essential services. Growth investors might see optionality in transformation initiatives. There's no single correct view, only different perspectives based on different objectives.

As we conclude this deep dive into MGL's past, present, and future, one theme emerges repeatedly: infrastructure is about more than returns. It's about enabling human flourishing, creating public goods, and building foundations for economic growth. MGL has provided Mumbai with cleaner air, cheaper energy, and safer cooking for three decades. Whether delivering natural gas, hydrogen, or electrons, that mission continues.

The company that emerged from environmental litigation, survived foreign partner exits, navigated public markets, and now confronts existential disruption embodies the resilience required for infrastructure investing. MGL's story isn't finished—arguably, the most interesting chapters lie ahead. For investors willing to embrace complexity, uncertainty, and long time horizons, MGL offers exposure to India's urban transformation with downside protection from essential service characteristics.

In the end, MGL is a bet on Mumbai and, by extension, urban India. As long as millions call Mumbai home, they'll need energy for transport, cooking, and commerce. MGL has proven remarkably adaptive in meeting these needs for three decades. Whether that adaptability continues through the energy transition will determine if MGL remains a market leader or becomes a case study in disruption. Either outcome offers lessons worth learning for investors, policymakers, and companies navigating our rapidly changing world.