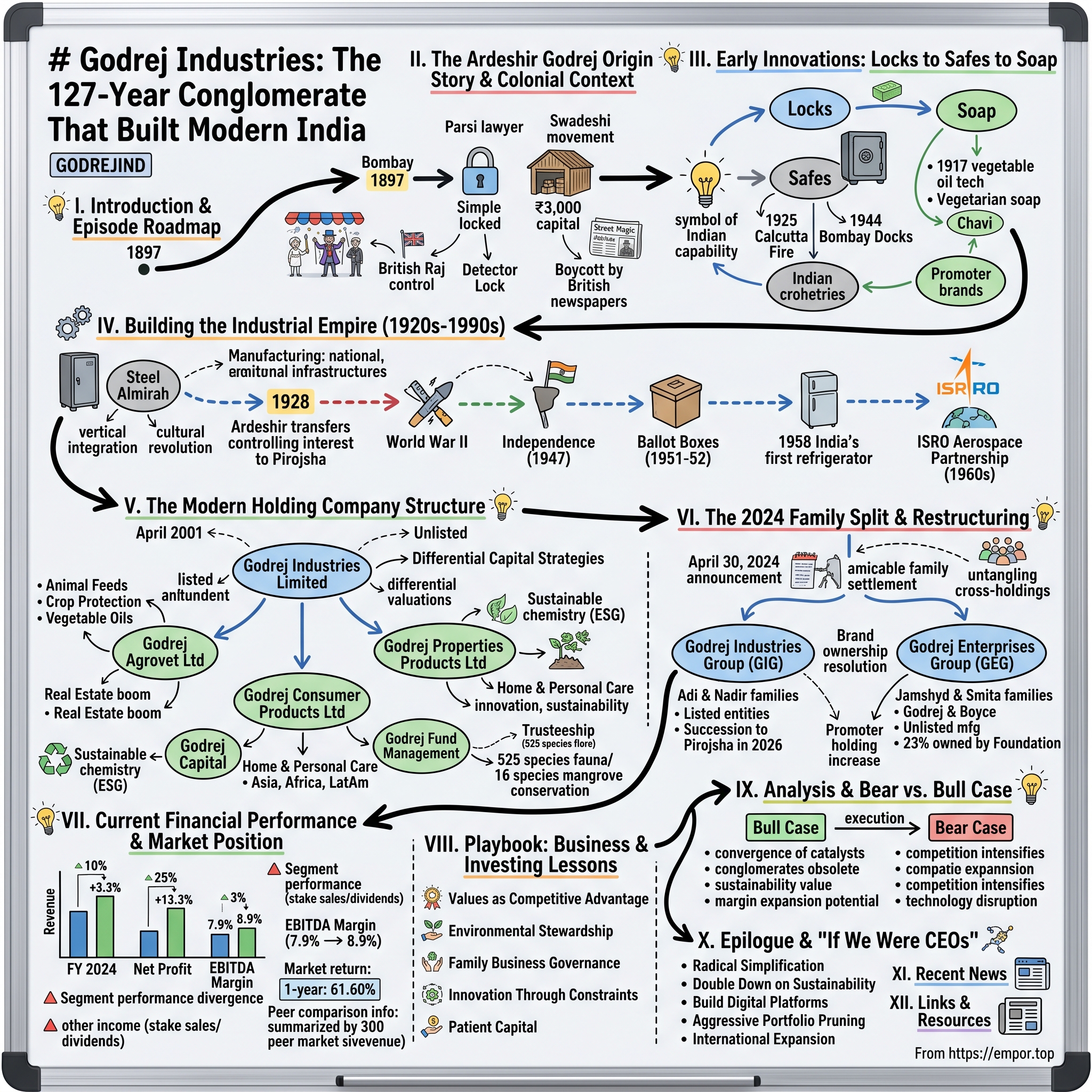

Godrej Industries: The 127-Year Conglomerate That Built Modern India

I. Introduction & Episode Roadmap

Picture this: It's 1897 in colonial Bombay. The British Raj controls every aspect of Indian commerce, from the locks on doors to the soap in bathrooms. A young Parsi lawyer named Ardeshir Godrej, disgusted by the colonial legal system's demand for compromise over truth, decides to abandon his legal career entirely. In a small shed with his brother Pirojsha and a capital of just ₹3,000, he begins manufacturing locks—not just any locks, but ones superior to British imports. This rebellious act of industrial defiance would spawn a ₹19,657 crore revenue empire that touches nearly every aspect of Indian life today. How did a lock manufacturer during British colonial rule become one of India's most diversified conglomerates? The answer lies not in MBA case studies or Wall Street strategies, but in the convergence of personal ethics, anti-colonial resistance, and 127 years of relentless adaptation. Today, Godrej Industries commands a market capitalization of ₹39,881 crore with revenue of ₹19,657 crore, touching everything from the chemicals in your soap to the apartments you might buy.

This is a story that begins with a lawyer's disgust at compromise, evolves through India's independence movement, navigates socialist planning and liberalization, and culminates in a 2024 family split that fundamentally restructured one of India's oldest business houses. It's a tale of how values-driven capitalism, often dismissed as naive idealism, built an empire that serves markets in over 65 countries while conserving mangroves larger than Central Park.

Over the next several hours, we'll unpack how Godrej Industries became what it is today—a complex holding company structure spanning chemicals, real estate, agribusiness, and financial services. We'll examine the strategic decisions, the family dynamics, the financial engineering, and most importantly, the playbook that allowed a company founded in the 19th century to remain relevant in the 21st. The company's Q1 FY26 results show this evolution continuing: consolidated net profit stood at ₹349 crore, marking an 8.2% year-on-year increase, with revenue rising 5% YoY to ₹4,459 crore and EBITDA jumping 18% YoY to ₹395.5 crore, while EBITDA margin improved to 8.9% from 7.9% a year earlier.

But beyond the numbers lies something more profound: a case study in how conglomerates navigate the tension between diversification and focus, between family control and professional management, between Indian values and global ambitions. Buckle up—this is going to be quite a journey through Indian business history.

II. The Ardeshir Godrej Origin Story & Colonial Context

The year was 1894. In a Bombay courtroom, a young Parsi lawyer named Ardeshir Burjorji Sorabji Godrej faced a moment that would redirect not just his life, but the trajectory of Indian industry. Born in 1868 to a wealthy Zoroastrian family, Ardeshir had followed the predictable path of privileged Parsis—English education, law degree, promising legal career. But then came the Zanzibar case.

The details of the case have been lost to history, but what remains crystal clear is Ardeshir's reaction: his senior counsel demanded he compromise the truth for a favorable verdict. For a man raised in the Zoroastrian tradition where truth—asha—forms the fundamental principle of existence, this was unconscionable. Ardeshir walked away from law forever, declaring he would rather fail honestly in business than succeed through deception in courts.

This wasn't mere youthful idealism. The Parsi community in 19th-century Bombay occupied a unique position—wealthy enough to challenge British commercial dominance, yet culturally committed to ethical business practices that often put them at odds with colonial exploitation. When Ardeshir partnered with his brother Pirojsha Burjorji in 1897, armed with just ₹3,000 in capital and operating from a shed in Lalbaug, they weren't just starting a business. They were joining the Swadeshi movement through industrial action.

The timing was explosive. The Swadeshi movement, which would formally crystallize during the 1905 Bengal partition protests, was already brewing in the 1890s. Indian intellectuals and industrialists recognized that political freedom required economic self-sufficiency. While politicians made speeches and writers penned manifestos, the Godrej brothers decided to make locks—but not just any locks. They would manufacture locks superior to British imports, proving Indian technical capability while keeping profits within the country.

The British lock manufacturers had a stranglehold on the Indian market, flooding it with products from Birmingham and Manchester. Their locks came with the implicit message of British superiority—even the security of Indian homes depended on British ingenuity. The colonial government's procurement policies favored British products, and British-owned newspapers dominated advertising channels. When these newspapers boycotted Indian manufacturers who supported Swadeshi, refusing their advertisements, it could have been a death sentence for a startup.

But Ardeshir turned this boycott into opportunity. Unable to advertise conventionally, he took to the streets with a traveling magic show. Picture this: A well-dressed Parsi gentleman arriving in town squares with an assistant, a table, and a collection of locks. He would challenge onlookers to pick his locks, offering rewards to anyone who succeeded. When British-made locks opened easily while his "Detector Lock" remained impregnable, the message was clear—Indian engineering had arrived.

The Detector Lock itself was a masterpiece of reverse engineering and improvement. Based on the Chubb lever tumbler lock design (Chubb being the gold standard from England), Ardeshir didn't just copy—he enhanced. His version featured a mechanism that would jam if anyone attempted to pick it with duplicate keys, literally detecting intrusion attempts. In an era where industrial espionage was considered a Western specialty, an Indian company had out-innovated the colonizers.

By 1902, just five years after founding, Godrej locks were specified for government buildings—a shocking reversal of colonial procurement practices. The company's reputation spread through word-of-mouth, traveling along trade routes and railway lines. Indian merchants, tired of British commercial dominance, became evangelists for these indigenous locks. The Godrej name began appearing on doors across the subcontinent, each lock a small act of resistance against colonial economic control.

The workshop in Lalbaug became a pilgrimage site for aspiring Indian industrialists. Here was proof that Indians could compete with British manufacturing not by copying or undercutting prices, but through genuine innovation. Ardeshir's insistence on quality—every lock personally inspected, every mechanism tested multiple times—established a tradition that would define Godrej for generations.

Financial records from this period, though fragmentary, suggest remarkable growth. From initial revenues of a few thousand rupees, the company was generating lakhs by 1910. But Ardeshir and Pirojsha weren't content with locks alone. They recognized that true industrial independence required diversification. The British controlled entire supply chains—from raw materials to finished products, from finance to distribution. To truly compete, Godrej needed to expand.

This expansion would take an unexpected turn. As World War I disrupted global supply chains and revealed India's dangerous dependence on imports for basic necessities, the Godrej brothers would make their boldest move yet—entering the soap business with technology that British experts declared impossible for Indians to master.

III. Early Innovations: Locks to Safes to Soap

The success of the Detector Lock had established Godrej's reputation, but safes would cement it—literally. In 1902, as British banks and trading houses dominated Indian commerce, they imported massive safes from England, symbols of imperial financial power. These safes took months to arrive, cost fortunes to transport, and came with the message that Indians couldn't be trusted to protect even their own wealth.

Ardeshir saw opportunity in this arrogance. Working with a small team of craftsmen, many of whom had never seen the inside of a British safe, he began developing India's first fire- and burglar-resistant strongbox. The technical challenges were staggering. Creating fire-resistant materials required understanding metallurgy and heat transfer. Building burglar-proof mechanisms meant anticipating every possible attack vector. The British safe manufacturers had centuries of expertise; Godrej had enthusiasm and ingenuity.

The breakthrough came through systematic experimentation. Ardeshir created a testing regime that would make modern R&D departments envious. Safes were subjected to blowtorches, sledgehammers, explosives, and the most sophisticated lock-picking tools available. Each failure taught a lesson, each success raised the bar. By 1903, Godrej launched safes that didn't just match British quality—they exceeded it in crucial ways, particularly in resistance to India's extreme heat and humidity.

But the real validation came through disasters. In 1925, a massive fire engulfed the business district of Calcutta. British-made safes cracked under the heat, their contents reduced to ash. In the rubble, investigators found Godrej safes intact, their contents unharmed. Photographs of these surviving safes, standing like monuments among the destruction, became the most powerful advertisement imaginable. Then came 1944's Bombay docks explosion—one of the worst industrial disasters in colonial history. Ships loaded with cotton, gold, and ammunition caught fire, creating an inferno that destroyed much of the port area. Again, Godrej safes survived where others failed.

These weren't just product victories; they were symbolic triumphs. Each surviving safe represented Indian engineering's superiority in extreme conditions. British insurance companies, initially skeptical, began recommending Godrej safes for lower premiums. The colonial government, despite its procurement biases, couldn't ignore the evidence. By the 1920s, Godrej safes protected everything from royal treasures to freedom movement funds hidden from British surveillance.

But the most audacious innovation was yet to come. In 1917, as World War I created soap shortages across India, the Godrej brothers decided to enter the soap business. This wasn't a casual diversification—it was technological rebellion. Soap manufacturing in early 20th century India meant importing animal fats, processing them with imported chemicals, and competing against established British brands like Lever Brothers (later Unilever) who controlled the entire supply chain.

The challenge seemed insurmountable. British experts, when consulted, declared it impossible to make quality soap from vegetable oils. The chemistry, they insisted, wouldn't work. The saponification process required specific fatty acid profiles found only in animal tallow. Vegetable oils would produce soft, quickly deteriorating bars unsuitable for India's climate. This "expert" opinion wasn't just technical—it was political. Vegetable oil soap would align with Hindu vegetarianism and Gandhian philosophy, threatening the cultural hegemony of Western products.

Ardeshir approached the problem like he had with locks and safes—through relentless experimentation. Working with Pirojsha and a young chemist named Shapurji Sorabji, they spent months in a makeshift laboratory, testing different vegetable oil combinations, adjusting alkali concentrations, experimenting with fragrances that would mask the natural vegetable oil smell. The breakthrough came through an unexpected source—coconut oil from Kerala, combined with groundnut oil, created a stable soap base that actually performed better in Indian conditions than animal fat soaps.

In 1918, Godrej launched 'Chavi' soap. The name itself was clever marketing—'Chavi' meant 'key' in Hindi, linking the new product to Godrej's established lock business. But the real genius was in the positioning. This wasn't just soap; it was Swadeshi soap, vegetarian soap, soap that aligned with Indian values while delivering superior quality.

The endorsements that followed read like a who's who of the independence movement. Mahatma Gandhi, who had been advocating for village industries and self-reliance, publicly praised Godrej soap as an example of Indian industrial capability. Rabindranath Tagore, the Nobel laureate poet, wrote about the cultural significance of Indians creating products that reflected their values. Annie Besant, the British-born Indian independence activist, used Godrej soap as an example of how Indians could economically undermine colonial rule.

The market response was extraordinary. Within two years, Godrej soaps captured significant market share from established British brands. The company expanded from one soap variety to dozens—sandal, rose, lime, each targeting different segments while maintaining the vegetable oil base. The soap division's profits funded further diversification, creating a virtuous cycle of innovation and growth.

By 1923, Godrej wasn't just a lock company that also made safes and soaps. It had become a symbol of Indian industrial capability. The company's factory in Vikhroli, then on Bombay's outskirts, became a model township with worker housing, schools, and healthcare facilities—revolutionary for its time. The Godrej brothers had proven that Indian companies could compete on quality, innovation, and values.

This success set the stage for decades of expansion. Each new product category—from furniture to refrigerators—would follow the same pattern: identify a market dominated by imports or inferior local products, develop superior indigenous alternatives, and build trust through quality and values. It was a playbook that would carry Godrej through independence, industrial licensing, liberalization, and into the modern era.

IV. Building the Industrial Empire (1920s-1990s)

The roaring twenties brought jazz to America and almirahs to India. In 1923, Godrej made another unexpected pivot—into furniture manufacturing with the launch of Godrej almirahs (steel wardrobes). This wasn't random diversification; it was strategic vertical integration. The company had mastered metalworking for locks and safes, developed distribution networks across India, and built a reputation for security. Steel furniture was the logical next step.

But logic alone doesn't explain the cultural revolution these almirahs sparked. Traditional Indian homes used wooden furniture, vulnerable to termites, monsoon humidity, and fire. The wealthy imported furniture from Europe; the middle class made do with local carpenters of varying quality. Godrej's steel almirahs offered something unprecedented: affordable, durable, secure storage that could survive generations. In a society where daughters received almirahs as part of their dowry, Godrej wasn't just selling furniture—they were selling family heritage.

The almirahs became so ubiquitous that "Godrej" became generic for any steel wardrobe, much like "Xerox" for photocopying. By the 1930s, the company was producing thousands of units monthly, each one carrying the distinctive Godrej lock, creating an ecosystem of products that reinforced each other. A customer buying a Godrej almirah was also buying Godrej security, Godrej quality, and increasingly, Godrej prestige.

Then came 1928, a pivotal year that would reshape the company's ownership structure for the next century. Ardeshir, now 60 and perhaps seeing the empresa growing beyond what he'd imagined, made a remarkable decision—he transferred his controlling interest to his brother Pirojsha and moved to agriculture. This wasn't retirement in the conventional sense. Ardeshir purchased 3,500 acres of marshland in the Western Ghats, determined to prove that scientific farming could transform Indian agriculture just as industrial innovation had transformed manufacturing.

The timing of this transition proved fortuitous. Pirojsha, more operationally minded than the visionary Ardeshir, steered the company through the Great Depression, World War II, and Indian independence with steady hands. While global markets collapsed in 1929, Godrej continued expanding, recognizing that economic crises create opportunities for companies with strong balance sheets and local market knowledge.

World War II, devastating as it was globally, accelerated Godrej's industrial development. Cut off from British imports, India needed domestic production of everything from office equipment to medical supplies. Godrej pivoted its manufacturing capabilities with remarkable agility. The same facilities that produced safes now made surgical equipment. The soap factories developed special formulations for military use. This wartime flexibility established Godrej as more than a consumer products company—it was becoming industrial infrastructure for the emerging nation.

Independence in 1947 brought both celebration and responsibility. When India held its first general election in 1951-52—the world's largest democratic exercise—the Election Commission faced a unique challenge: how to ensure ballot security across a vast nation with limited infrastructure? The answer came from Vikhroli: Godrej manufactured over a million ballot boxes, each one secure, portable, and designed for India's diverse conditions from Himalayan cold to Rajasthani heat. These ballot boxes became symbols of Indian democracy, carrying votes from remote villages to counting centers, protected by locks that had once defied colonial authority.

The 1950s Nehruvian socialist era, with its emphasis on self-reliance and import substitution, aligned perfectly with Godrej's philosophy. When the government restricted imports of consumer durables, Godrej was ready. In 1958, the company launched India's first indigenously manufactured refrigerator. The technical achievement was remarkable—creating refrigeration systems that could handle India's power fluctuations, designing for kitchens without standardized dimensions, pricing for middle-class affordability while maintaining quality.

The refrigerator project revealed Godrej's evolving capabilities. This wasn't just metalworking anymore; it required understanding thermodynamics, electrical engineering, and consumer behavior. The company hired India's brightest engineers, many trained at newly established IITs, creating an R&D culture that balanced frugal innovation with quality obsession. The "Godrej refrigerator" became a middle-class aspiration, a wedding gift that announced a family's arrival into modernity.

But perhaps the most remarkable partnership began quietly in the 1960s when India established its space program. ISRO, working with minimal budgets and international technology sanctions, needed precision engineering support. Godrej, with its metalworking expertise and quality standards, became an unlikely aerospace partner. For over three decades, Godrej would manufacture critical components for Indian satellites and launch vehicles, from the Aryabhata satellite in 1975 to modern Mars missions. The same company that started with locks was now helping India reach for the stars.

The 1970s and 1980s brought new challenges. Indira Gandhi's socialist policies, including bank nationalization and restrictive industrial licensing, constrained private sector growth. Many Indian conglomerates struggled, but Godrej adapted through patient capital allocation and strategic diversification within permitted sectors. When the government emphasized agricultural development, Godrej expanded into agricultural products. When environmental concerns grew, the company developed eco-friendly technologies.

This period also saw crucial organizational evolution. The company transformed from family-managed to professionally-run while maintaining family control—a delicate balance many Indian businesses failed to achieve. The third generation of Godrejs, educated at MIT and Harvard, brought global perspectives while respecting institutional memory. They recognized that survival required more than manufacturing excellence; it needed financial sophistication.

The 1990s would bring India's economic liberalization, and with it, both unprecedented opportunities and existential threats. Global competitors could now enter India freely. Consumer preferences were shifting rapidly. Technology was disrupting traditional industries. As India opened its markets, the question became: could a company built on Swadeshi principles compete in a globalized world?

The answer would come through two strategic moves that seemed minor at the time but would prove transformative: the 1990 establishment of Godrej Properties, entering the booming real estate sector, and the 1991 incorporation of Godrej Agrovet, formalizing agricultural operations. These weren't just new divisions; they were bets on India's fundamental transformation from a socialist economy to a market-driven powerhouse. As we entered the new millennium, these bets would pay off spectacularly, setting the stage for Godrej Industries' modern avatar as a diversified holding company.

V. The Modern Holding Company Structure

April 2001 marked a watershed moment that most investors missed. Godrej Soaps Limited, the public face of the empire since its vegetable oil breakthrough, quietly transformed into Godrej Industries Limited. This wasn't mere rebranding—it was architectural reconstruction of a 104-year-old conglomerate for 21st-century capital markets. The name change signaled a fundamental shift from operating company to strategic holding company, a structure that would define its next two decades.

The transformation addressed a problem plaguing Indian conglomerates: the market's inability to properly value diverse businesses housed under one roof. Investors valuing Godrej Soaps struggled to price soap manufacturing alongside real estate development, agricultural inputs, and aerospace components. The conglomerate discount—where diversified companies trade below the sum of their parts—was crushing valuations. The solution was elegant: create a holding company structure where each business could be valued independently while maintaining strategic control.

Under this new structure, Godrej Industries became the promoter of Godrej Agrovet Ltd and Godrej Properties Ltd, while also maintaining a stake in Godrej Consumer Products Ltd. Each subsidiary could now access capital markets independently, pursue focused strategies, and be valued on its own merits. The parent company transformed into a capital allocator, moving resources to the highest-return opportunities while maintaining the Godrej values and governance standards.

The business portfolio that emerged revealed remarkable strategic coherence beneath apparent randomness. Godrej Industries became one of the leading manufacturers of oleochemicals on a standalone basis, serving markets across diverse industrial applications through one of India's oldest and largest oleo-chemicals, derivatives and speciality chemical portfolios. This wasn't the glamorous consumer-facing business, but it generated steady cash flows with high barriers to entry.

The chemicals division, the empire's oldest business dating back to the vegetable oil soap innovation, became the cash cow funding growth elsewhere. Oleochemicals—derived from natural fats and oils—positioned Godrej perfectly for the global shift toward sustainable chemistry. While competitors relied on petroleum-based feedstocks, Godrej's vegetable oil expertise from 1917 suddenly looked prescient in an ESG-conscious world. The division quietly grew to serve over 70 countries, generating hard currency earnings that funded domestic expansion.

Animal feeds through Godrej Agrovet addressed India's protein revolution. As rising incomes drove meat and dairy consumption, efficient animal nutrition became critical. The business leveraged Godrej's agricultural expertise from Ardeshir's farming experiments while applying modern nutritional science. This wasn't just selling cattle feed; it was enabling India's white revolution in dairy, supporting millions of small farmers improving productivity.

The crop protection business addressed key challenges faced by Indian agriculture, helping improve productivity of Indian farmers through innovative products and services that sustainably increase crop and livestock yields. In a country where post-harvest losses exceeded 30% for some crops, Godrej's integrated agricultural solutions—from seeds to storage—created value across the agricultural value chain.

The vegetable oils business, evolved from the original soap manufacturing, now served both industrial and consumer markets. The vertical integration from oil processing to finished products created cost advantages while ensuring quality control. This seemingly mundane business generated consistent returns with minimal capital requirements, funding more capital-intensive ventures.

But the crown jewels were the listed subsidiaries. Godrej Properties, established in 1990, had perfect timing for India's real estate boom. As India's leading real estate developer by sales, it brought the Godrej philosophy of innovation, sustainability, and excellence to the real estate industry. The company pioneered transparent practices in an industry notorious for black money, creating trust that commanded premium pricing.

Godrej Consumer Products emerged as an FMCG leader in Home and Personal Care with a growing presence in Asia, Africa and Latin America. The business leveraged the original soap innovation into a portfolio spanning hair colors, household insecticides, and air fresheners—categories with high margins and brand loyalty.

The newest additions reflected evolving opportunities. Godrej Fund Management became the real estate private equity arm of the group, allowing participation in India's infrastructure boom without balance sheet strain. Godrej Capital, the newest company in the group, developed a fast-growing financial services business, recognizing that financial inclusion would drive India's next growth phase.

This portfolio wasn't random diversification—it was strategic positioning across India's economic transformation. Chemicals provided industrial backbone, agriculture supported rural development, real estate captured urbanization, consumer products leveraged rising incomes, and financial services enabled it all. Each business reinforced others: agricultural products supported dairy, which drove consumer demand, which increased real estate values, which created financial services opportunities.

The financial engineering was equally sophisticated. Cross-holdings between group companies created control with minimal capital, though this complexity would later necessitate restructuring. The holding company structure allowed differential capital strategies—high leverage for real estate, conservative balance sheets for consumer products, venture capital approaches for new businesses.

By 2024, this structure had created enormous value but also complexity that obscured it. Group revenue stood at USD 6.1 billion with a market capitalisation of USD 27.5 billion, but investors struggled to value the maze of subsidiaries, associates, and cross-holdings. The market applied a conglomerate discount despite each business being a leader in its sector.

The modern structure also reflected governance evolution. Independent directors dominated subsidiary boards, professional CEOs ran operations, and family members focused on strategy and capital allocation. This separation of ownership and management, rare in Indian family businesses, attracted institutional investors while maintaining promoter control.

Yet beneath the corporate structure remained the original Godrej DNA. The company maintained trusteeship and conservation of over 525 species of fauna and 16 different species of mangrove flora for the past 80 years. Environmental stewardship wasn't CSR window-dressing but embedded in operations—from vegetable-based chemicals to sustainable real estate, the company walked the talk on sustainability before ESG became fashionable.

As we moved into 2024, this carefully constructed architecture would face its biggest test: untangling 127 years of family cross-holdings while maintaining operational excellence. The April 2024 restructuring wouldn't just be about family separation—it would determine whether the holding company structure could unlock value that markets had long ignored.

VI. The 2024 Family Split & Restructuring

The announcement came on April 30, 2024, delivered with characteristic Godrej understatement: an "amicable family settlement" would divide the 127-year-old conglomerate. But beneath the polite corporate language lay a seismic shift—one of India's most storied business families was formally splitting, untangling generations of cross-holdings, shared brands, and intertwined destinies.

The protagonists read like a Shakespearean drama. Adi Godrej, the patriarch who'd modernized the group through the liberalization era. His brother Nadir, the quiet strategist who'd built the international businesses. Their cousin Jamshyd, who'd shepherded the unlisted Godrej & Boyce manufacturing empire. And Smita Godrej Crishna, Jamshyd's sister, whose children were being groomed for leadership. Four branches of a family tree, each with different visions for the future, somehow finding common ground for separation.

The restructuring created two distinct entities: Godrej Enterprises Group (GEG) and Godrej Industries Group (GIG). This wasn't a hostile takeover or court battle—remarkably, the family managed what most Indian business dynasties fail at: peaceful succession planning. The split reflected not acrimony but acknowledgment that different family branches had different ambitions, and forcing unity might destroy value for all.

Under the new structure, Godrej Industries Group came under the control of Adi and Nadir Godrej families, with Nadir assuming chairmanship. The succession plan showed remarkable foresight—Pirojsha Godrej, Adi's son, would become executive vice chairperson immediately and succeed as chairperson in August 2026. This wasn't just nepotism; Pirojsha had proven himself through operational roles, earning respect from professional management and institutional investors.

The asset division revealed strategic thinking. The Adi-Nadir combine retained control of listed entities—Godrej Industries, Godrej Consumer Products, Godrej Properties, and Godrej Agrovet—businesses that needed capital market access and professional management. The Jamshyd-Smita faction kept Godrej & Boyce, the unlisted manufacturing conglomerate with its aerospace, defense, and precision engineering businesses that required patient capital and technical expertise.

But the real complexity lay in untangling cross-holdings accumulated over decades. Imagine a corporate structure where subsidiaries owned stakes in parent companies, where family members held direct and indirect interests through trusts, where brand licensing agreements crisscrossed entity boundaries. Unraveling this without triggering tax events, regulatory violations, or market panic required financial engineering worthy of Wall Street's best.

The brand ownership resolution showed Solomon-like wisdom. Both groups would continue using the "Godrej" name—recognition that the brand transcended family ownership. But they'd operate in different sectors, minimizing confusion and competition. Godrej Industries Group would focus on consumer-facing businesses where brand equity mattered most. Godrej Enterprises Group would concentrate on B2B operations where technical capability trumped branding.

Market reaction was surprisingly positive. Promoter holding increased by 1.33% over the last quarter to 71%, signaling family commitment post-split. Investors who'd long complained about corporate complexity suddenly saw clarity. Each entity could now pursue focused strategies without consensus-building across extended family. The conglomerate discount that had plagued valuations might finally lift.

The restructuring also addressed generational transition—the Achilles heel of family businesses. Third-generation members like Pirojsha, Tanya, and Nisa Godrej had different educational backgrounds (Wharton, Harvard, INSEAD) and global perspectives from their parents. They understood that competing in global markets required different structures than building in protected ones. The split allowed each generation to pursue its vision without being constrained by legacy.

International precedents influenced the structure. The family had studied splits at Reliance (Ambani brothers), Birla Group, and internationally at Kering, Dassault, and Wallenberg. They learned that successful splits required clear asset division, brand agreements, and most importantly, emotional closure. The April announcement came after two years of negotiations, mediated by trusted advisors who'd served the family for decades.

The financial implications were substantial. Eliminating cross-holdings would improve transparency, potentially unlocking value worth thousands of crores. Simplified structures would attract foreign investors previously confused by ownership complexity. Each entity could optimize capital structure for its business mix rather than accepting compromise solutions.

For Godrej Industries specifically, the split meant focus. No longer would management attention be divided between listed and unlisted entities. Capital allocation decisions wouldn't require consensus across extended family. The company could pursue aggressive growth in chosen sectors without worrying about impact on cousin companies. The burden of 127 years of history, while honored, wouldn't constrain future strategy.

The human dimension deserved recognition. In an era where Indian business families often feuded publicly—the Ambanis, Hindujas, and Singhs making headlines for all wrong reasons—the Godrejs showed it could be done differently. The joint statement emphasized "shared values" and "continued respect," language that seemed genuine rather than legal boilerplate. Family members continued attending each other's functions, serving on each other's foundations, maintaining personal relationships despite professional separation.

Looking deeper, the split reflected India's economic evolution. The businesses suited for industrial India—manufacturing, engineering, defense—went to one group. The businesses aligned with consumer India—FMCG, real estate, financial services—went to another. This wasn't just dividing assets; it was acknowledging that different Indias required different strategies.

As markets digested implications through 2024 and into 2025, the wisdom became apparent. Following the announcement of Q1 FY26 results, Godrej Industries shares surged nearly 10% in intraday trade. The post-split clarity was unlocking value that had been trapped in complexity. The question now wasn't whether the split was successful—early indicators suggested it was—but whether this model could inspire other Indian conglomerates struggling with similar succession challenges.

VII. Current Financial Performance & Market Position

The numbers tell a story of transformation and challenge. In FY 2024, Godrej Industries posted ₹16,601 crore revenue and ₹595.16 crore net profit, figures that mask underlying volatility. The company has delivered a poor sales growth of 11.7% over past five years, with a low return on equity of 7.20% over last 3 years—metrics that would concern any fundamental investor.

But context matters. The past five years included COVID-19, global supply chain disruptions, commodity super-cycles, and the complex family restructuring. Judging performance without acknowledging these headwinds misses the resilience story. That the company maintained profitability and growth, albeit modest, while navigating existential changes speaks to operational strength.

The quarterly trajectory reveals momentum building post-restructuring. The Q1 FY26 results announced in August 2025 showed green shoots across metrics. The robust performance in Q1 FY26 indicates positive momentum for the company, with both profitability and margins showing healthy growth despite macroeconomic headwinds. Revenue growth of 5% year-over-year might seem pedestrian, but in a quarter where many conglomerates reported declines, it represented market share gains.

The margin story deserves particular attention. EBITDA margins expanding from 7.9% to 8.9% in a single year indicates operational efficiency improvements. This wasn't through cost-cutting alone—the company invested in automation, supply chain optimization, and product mix enhancement. The chemicals business, traditionally low-margin, improved through specialty product focus. Real estate margins expanded through better project selection and execution.

Earnings include other income of ₹2,921 Cr—a red flag for quality of earnings analysis. This other income primarily came from stake sales and dividend income from subsidiaries, not sustainable operating performance. Strip away these one-time gains, and core profitability looks less impressive. But this also represents the holding company model working—monetizing investments at optimal times, recycling capital into higher-return opportunities.

The balance sheet reveals both strength and concern. The company's 1-year return stood at 61.60%, 3-year return at 34.60%, and 5-year return at 30.50%, reflecting strong growth and investor confidence. These returns outpaced broader markets, suggesting investors recognized value despite operational challenges. But high debt-to-equity ratio of 1.5 in FY24 raised leverage concerns, particularly with interest rates rising globally.

Segment performance showed divergence. The chemicals business, despite being oldest, generated steady cash flows with improving margins. Global customers increasingly preferred sustainable oleochemicals over petroleum derivatives, playing to Godrej's strengths. The company's ability to serve over 70 countries from Indian manufacturing bases demonstrated competitive advantage in a sector where China previously dominated.

The agricultural businesses faced headwinds from erratic monsoons and commodity price volatility. Godrej Agrovet's performance—while consolidated separately—impacted parent company valuations. The crop protection segment struggled with generic competition and regulatory changes. Animal feed margins compressed as input costs spiked faster than selling price adjustments. Yet the long-term thesis remained intact: India's protein consumption would double by 2030, driving structural demand.

Real estate, through Godrej Properties, became the surprise performer. In Q1FY26, Godrej Properties reported total income of ₹1620.34 crores with net profit of ₹598.40 crore, reflecting 15.3% year-over-year growth. The company benefited from India's residential revival post-COVID, with remote work driving demand for larger homes. Godrej's reputation for quality and transparency commanded premiums in markets where buyers remained scarce.

The consumer products division showed resilience despite intense competition. Godrej Consumer Products posted consolidated net profit of ₹452.5 crore for Q1 FY26, up just 0.4% year-over-year, though revenue marked healthy 10% growth to ₹3,662 crore. The margin pressure—EBITDA declining 4% with margins shrinking from 21.7% to 19%—reflected brutal competition from both multinationals and D2C startups.

International operations contributed increasingly to consolidated performance. The chemicals business's exports to 70+ countries provided natural currency hedging. Consumer products' expansion into Africa and Southeast Asia, while currently loss-making, positioned for future growth as these markets matured. The global presence also provided learning opportunities—innovations from Indonesia improved Indian operations, Nigerian distribution strategies informed rural Indian expansion.

Peer comparison revealed relative underperformance. While Godrej Industries generated ₹16,601 crore revenue, pure-play competitors in each segment often showed better metrics. Chemical companies like Aarti Industries had higher margins. Real estate players like DLF generated superior returns. FMCG competitors like Dabur showed faster growth. The conglomerate structure, despite recent simplification, still carried a valuation discount.

Yet focusing solely on current numbers missed the option value embedded in the portfolio. Each business represented a call option on India's economic transformation. Chemicals benefited from China Plus One strategies. Real estate captured urbanization. Agriculture served food security needs. Consumer products leveraged demographic dividends. Financial services rode the inclusion wave. The portfolio's diversity, while diluting near-term returns, provided resilience and optionality worth more than current metrics suggested.

VIII. Playbook: Business & Investing Lessons

The Godrej story offers a masterclass in building enduring value through principles that seem anachronistic in today's growth-at-all-costs environment. The playbook that emerged over 127 years challenges conventional wisdom while delivering results that speak for themselves.

Lesson 1: Values as Competitive Advantage

From Ardeshir's refusal to compromise truth in 1894 to modern ESG leadership, Godrej proved that values create value. This wasn't corporate social responsibility as marketing—it was embedded in strategy. The vegetable oil soap wasn't just ethical; it opened markets closed to animal-based products. The transparent real estate practices weren't just honest; they commanded premium pricing. 23% of Godrej Enterprises Group's shares are held by the Pirojsha Godrej Foundation which is a philanthropic foundation—structuring ownership to ensure values survived generations.

When competitors cut corners during downturns, Godrej maintained quality, earning customer loyalty worth more than short-term savings. When others exploited regulatory grey areas, Godrej's compliance created trust with governments that became competitive moats. Values weren't constraints on business; they were strategic differentiators in markets where trust remained scarce.

Lesson 2: Environmental Stewardship as Business Strategy

Long before ESG became mandatory, Godrej practiced environmental capitalism. The company's mangrove conservation, started in the 1940s, now represents biodiversity assets worth billions. The water-positive operations—returning 4.4 billion litres to the planet—created resilience against water scarcity that threatens competitors. Conservation of over 525 species of fauna and 16 different species of mangrove flora for the past 80 years built knowledge assets in biodiversity that informed product development.

This wasn't philanthropy—it was risk management and opportunity identification. Understanding ecosystems helped develop natural pesticides. Mangrove conservation taught lessons applied in sustainable real estate. Water management expertise became sellable consulting services. Environmental stewardship created option value that traditional accounting couldn't capture but markets increasingly recognized.

Lesson 3: Managing Conglomerate Complexity

While business schools teach focus, Godrej showed how to manage diversity. The key wasn't avoiding complexity but structuring it intelligently. The holding company architecture allowed focus within diversity—each business had dedicated management while the parent provided patient capital and governance standards. Cross-business synergies were pursued where natural (chemicals to consumer products) but not forced where artificial.

The conglomerate structure provided resilience through cycles. When real estate crashed, chemicals carried the group. When agriculture struggled, consumer products compensated. This portfolio approach—different from private equity's financial engineering—created stability that focused competitors lacked. The challenge was communicating this value to markets trained to penalize complexity.

Lesson 4: Family Business Governance

The 2024 split demonstrated that family businesses could evolve professionally without losing family character. The solution wasn't choosing between family and professional management but integrating both. Family members focused on values, vision, and capital allocation while professionals managed operations. Independent directors provided oversight without threatening control.

The succession planning—announcing leadership transitions years in advance—provided stability rare in family businesses. By grooming next-generation leaders through operational roles rather than parachuting them into corner offices, competence was demonstrated before authority was granted. The split itself, recognizing different family branches had different aspirations, showed maturity few business families achieve.

Lesson 5: Building Trust in Low-Trust Markets

Operating in India, where contract enforcement remained weak and corruption endemic, Godrej built trust as infrastructure. Every Godrej lock that survived theft attempts, every safe that survived fires, every soap bar that delivered promised quality built trust accounts that compounded over decades. This trust became the ultimate moat—customers paid premiums for Godrej products not because they were technically superior but because the brand promise was credible.

Trust also attracted talent. In markets where employees expected exploitation, Godrej's worker townships and welfare programs attracted the best minds. Engineers who could work anywhere chose Godrej for the values. This talent density created innovation capabilities competitors couldn't match with higher salaries alone.

Lesson 6: Innovation Through Constraints

Godrej's greatest innovations came from constraints. British advertising boycotts led to street marketing innovations. Import restrictions drove indigenous technology development. Vegetarian requirements created new product categories. Capital scarcity encouraged frugal innovation. Each constraint, rather than limiting growth, forced creative solutions that became competitive advantages.

This constraint-driven innovation created products suited for emerging markets. While multinationals designed for developed markets then stripped features for India, Godrej designed for India then enhanced for exports. This reverse innovation—before the term existed—created products that succeeded globally because they'd survived India's extreme conditions.

Lesson 7: Patient Capital in Impatient Markets

While markets demanded quarterly results, Godrej invested in decades. The aerospace partnership with ISRO generated minimal returns for years before becoming strategic. Mangrove conservation consumed resources for decades before environmental value was recognized. R&D investments in sustainable chemistry seemed wasteful until petroleum alternatives became essential.

This patient capital approach required structure. The family ownership provided permanence that public markets wouldn't tolerate. The diversified portfolio allowed long-term bets funded by short-term cash flows. The values-based culture attracted investors who understood the strategy. Patient capital wasn't just about having money—it was about having conviction.

Lesson 8: The Compound Effect of Reputation

Every ethical decision, every quality product, every kept promise added to a reputation account that paid compound interest. When Godrej entered new markets, the name opened doors. When regulations changed, governments consulted Godrej. When crises hit, stakeholders gave benefit of doubt. Reputation became currency more valuable than cash.

But reputation also created constraints. The company couldn't pursue opportunities that conflicted with values. Growth was slower because shortcuts weren't taken. Margins were lower because quality wasn't compromised. Yet over 127 years, this reputation-constrained growth created more value than unconstrained growth would have, because it was sustainable.

IX. Analysis & Bear vs. Bull Case

The Bull Case: A Convergence of Catalysts

The optimistic view sees Godrej Industries at an inflection point where multiple forces converge to unlock trapped value. Start with the restructuring benefits. The April 2024 family settlement removed the biggest overhang—succession uncertainty that had plagued valuations for years. With clear ownership, focused strategy, and simplified structure, the conglomerate discount should narrow from current 30-40% to more reasonable 15-20%.

The portfolio positioning looks prescient for India's next decade. The company serves over 1.1 billion consumers globally through businesses with market leadership positions. As India's per capita income crosses $3,000—the inflection point for consumption explosion—every Godrej business benefits. Real estate captures urbanization, consumer products ride premiumization, chemicals benefit from manufacturing growth, agriculture serves food security needs, financial services enable everything.

The sustainability angle becomes increasingly valuable. Global supply chains are restructuring around ESG criteria. Godrej's eight-decade environmental track record provides credibility competitors can't buy. The vegetable-based chemicals position perfectly for the shift from petroleum. The sustainable real estate commands green building premiums. The company has conserved mangroves and reduced pollution while being water positive and efficient, with conservation of over 525 species—credentials that open doors globally.

Margin expansion potential remains significant. The chemicals business, transitioning from commodities to specialties, could see margins double. Real estate margins should expand as land banks acquired cheaply get developed. Consumer products, having invested in distribution and brands, should see operating leverage. Current 8.9% EBITDA margins could reach 12-15% as mix improves and scale benefits materialize.

The balance sheet, while leveraged, has capacity for growth. Asset-light businesses like consumer products and financial services can scale without proportional capital. Real estate's negative working capital model generates cash for growth. The chemical business's export earnings provide natural hedging. Rising interest rates hurt less when pricing power exists.

Hidden assets provide additional upside. The Mumbai real estate—3,500 acres in prime locations—worth multiples of book value. The brand value, not on balance sheet, worth thousands of crores. The biodiversity assets, as carbon credits become tradeable, potentially worth billions. The aerospace technology, as India's space program commercializes, increasingly valuable.

Management quality post-restructuring looks stronger. Nadir Godrej's international experience, Pirojsha's operational expertise, and professional CEOs at subsidiaries create balanced leadership. The board's independence, with majority independent directors, ensures governance. The incentive alignment, with promoters holding 71%, ensures skin in the game.

The Bear Case: Structural Challenges in a Changing World

The pessimistic view sees structural challenges that no restructuring can solve. Start with the fundamental problem: conglomerates are obsolete in modern capital markets. Investors can create their own diversification; they don't need companies to do it. The complexity penalty will persist regardless of simplification efforts. Pure-play competitors will always command premium valuations.

The financial performance raises red flags. Poor sales growth of 11.7% over five years and low ROE of 7.20% over last 3 years suggest structural, not cyclical, issues. The quality of earnings, with ₹2,921 crore of other income, indicates core operations aren't generating adequate returns. The debt-to-equity ratio of 1.5 limits financial flexibility as interest rates rise globally.

Competition intensifies across every segment. In chemicals, Chinese overcapacity threatens margins. In real estate, new players with technology platforms disrupt traditional models. In consumer products, D2C brands attack profitable niches. In agriculture, generic manufacturers destroy pricing power. The company faces disruption everywhere without disrupting anywhere.

The India story might disappoint. Political uncertainty, infrastructure constraints, and execution challenges could delay the consumption boom. Global recession risks threaten export markets. Climate change makes agriculture increasingly volatile. Urbanization might slow as remote work reduces city migration. The portfolio positioned for yesterday's India might miss tomorrow's opportunities.

The ESG credentials, while impressive, might not translate to returns. Markets increasingly question whether sustainable business equals profitable business. The conservation efforts, while admirable, consume resources without generating returns. The values-based approach, while building trust, constrains growth opportunities. In capitalism's harsh reality, nice guys might finish last.

The execution risk post-split remains high. Managing diverse businesses requires different skills than managing integrated operations. The brand sharing between separated entities could create confusion. The loss of synergies might exceed benefits of focus. The family harmony, while admirable now, might not survive business pressures.

Technology disruption threatens traditional advantages. The physical locks business faces smart home competition. Chemical customers increasingly backward integrate. Real estate platforms disintermediate developers. E-commerce challenges traditional distribution. The company's manufacturing heritage becomes liability in an asset-light world.

The Balanced View: Cautious Optimism with Clear Risks

Reality likely lies between extremes. Godrej Industries represents a complex bet on India's transformation with both significant upside and material risks. The restructuring removes one uncertainty but doesn't guarantee success. The portfolio positioning makes strategic sense but requires execution excellence.

For investors, the key question isn't whether Godrej will survive—127 years of history suggests it will. The question is whether it can generate returns exceeding India's growth opportunity cost. With pure-play alternatives available in every segment, why accept conglomerate complexity?

The answer might be optionality. In uncertain times, diversification provides resilience. When nobody knows which sectors will win, betting on all makes sense. The Godrej portfolio isn't just diversified across industries but across India's development stages—from agriculture to aerospace, serving rural to urban, basic to premium.

The valuation at ₹39,881 crore market cap seems neither cheap nor expensive—it's uncertain. Bulls see 50% upside as discounts narrow and growth accelerates. Bears see 30% downside as reality disappoints expectations. Both could be right at different times.

X. Epilogue & "If We Were CEOs"

If we were sitting in the corner office at Godrej One in Mumbai's Vikhroli, looking out at those carefully preserved mangroves while contemplating the next chapter of this 127-year story, what would we do?

Priority 1: Radical Simplification Beyond the Split

The 2024 restructuring was necessary but insufficient. We'd go further—eliminating every cross-holding, merging overlapping businesses, and creating clear reporting lines. Each business would have one owner, one strategy, one set of metrics. The market rewards clarity, and we'd deliver it even if it meant sacrificing some control. Consider spinning off mature businesses entirely, letting them trade independently while retaining only strategic stakes.

Priority 2: Double Down on Sustainability Leadership

While others talk ESG, we'd make Godrej the global benchmark. Launch India's first certified carbon-neutral real estate project. Transform the chemicals business into bio-based alternatives completely. Create the world's largest private biodiversity preserve. But here's the key—monetize this leadership through premium pricing, carbon credits, and sustainability consulting. Values must create value, not just consume it.

Priority 3: Build Digital Platforms, Not Just Products

The future belongs to platforms, not manufacturers. We'd create GodrejHome—a super-app connecting every home need from security to cleaning to furniture. GodrejFarm would link farmers directly to consumers, cutting middlemen while ensuring quality. GodrejSpace would commercialize our aerospace expertise for the satellite boom. These platforms would leverage the trust while creating asset-light growth.

Priority 4: Aggressive Portfolio Pruning

Sacred cows make poor investments. We'd exit businesses where we lack competitive advantage, regardless of history. If chemicals can't achieve global scale, sell to someone who can. If certain consumer categories face permanent margin pressure, exit gracefully. The capital released would fund winners, not subsidize losers. This isn't betraying legacy—it's ensuring survival.

Priority 5: International Expansion with Indian Diaspora

The 30 million Indian diaspora represents an underserved market craving authentic Indian brands. We'd create Godrej International, specifically targeting Indians abroad with products that evoke home—from traditional soaps to modern apartments. Start with Dubai, London, and New York, then follow the diaspora globally. This isn't just exports; it's building global Indian brands.

Priority 6: Talent Revolution Through Ownership

Transform employees into owners through aggressive stock options, making wealth creation democratic. Recruit globally, bringing Silicon Valley product managers, Chinese manufacturing experts, and European sustainability specialists. Create Godrej University, training not just employees but ecosystem partners. Make Godrej where India's best want to work, not where they settle.

Priority 7: Financial Engineering for Value Unlock

The holding company structure needs financial innovation. Create tracking stocks for each division, allowing targeted investment. Issue sustainability bonds for green projects. Explore REITs for real estate assets. Consider dual listings in Singapore or London for better valuations. Use financial markets as tools, not just funding sources.

Priority 8: Bold Bets on Future Technologies

While honoring manufacturing heritage, we'd invest aggressively in frontier technologies. Partner with IITs for quantum computing applications in chemicals. Collaborate with startups on vertical farming for agriculture. Explore blockchain for supply chain transparency. These might fail, but some will define the next century.

The meta-strategy would be "Timeless Values, Timely Execution." Keep the ethical core that defined Godrej while adapting everything else. The next 127 years won't respect the last 127 years unless we earn that respect through performance.

XI. Recent News

The August 2025 earnings season brought renewed attention to Godrej Industries' transformation. Following the Q1 FY26 results announcement, shares surged nearly 10% in intraday trading, with investors clearly appreciating the post-restructuring clarity. The results themselves validated the bull case—margins expanding, revenue growing, and operational efficiency improving across segments.

In the broader ecosystem, subsidiary performance showed divergence. Godrej Agrovet reported Q1 FY26 consolidated net profit of Rs. 160.52 crores, compared to Rs. 70.78 crores in the previous quarter, demonstrating the agricultural business's recovery potential. Meanwhile, Godrej Consumer Products faced headwinds with EBITDA declining 4% to ₹694.8 crore and margins shrinking to 19% from 21.7% a year ago, highlighting intense competition in FMCG sectors.

Real estate continued its strong run. Godrej Properties reported net profit of ₹598.40 crore in Q1 FY26, reflecting 15.3% year-over-year growth, benefiting from India's residential recovery and the company's reputation for quality delivery in a sector plagued by delays and defaults.

Looking ahead, several catalysts could drive rerating. The sustainability initiatives are gaining recognition globally, with European customers increasingly preferring Godrej's bio-based chemicals. The financial services expansion through Godrej Capital addresses India's credit gap, potentially becoming a significant value driver. The upcoming chairmanship transition in 2026 provides another milestone for governance evolution.

XII. Links & Resources

For those seeking deeper understanding, several resources prove invaluable:

Primary Sources: - Annual Reports (2001-2024): Available on BSE/NSE websites, tracking the transformation from Godrej Soaps to Godrej Industries - The April 2024 restructuring announcement: Critical for understanding the family settlement - Quarterly investor presentations: Best source for segment-wise performance

Historical Context: - "No Guns, Only Roses" by Ratan Tata: Contains chapters on Indian industrial history including Godrej - Godrej Archives (Mumbai): Physical repository of 127 years of documents - "India's Industrialists" by Gita Piramal: Excellent context on Parsi business houses

Industry Analysis: - CRISIL reports on Indian conglomerates - McKinsey's "India's Century" report: Positions where Godrej businesses fit - BCG's analysis of family business transitions in Asia

Academic Studies: - IIM Ahmedabad case studies on Godrej's various businesses - Harvard Business School's analysis of emerging market conglomerates - ISB's research on family business governance in India

Regulatory Filings: - SEBI disclosures for related party transactions - Competition Commission of India filings for acquisitions - Environmental clearances showcasing sustainability practices

The Godrej story continues evolving, making it essential viewing for anyone interested in how traditional businesses adapt to modern realities. Whether the next chapter brings triumph or challenge, it will certainly provide lessons worth learning.

The Godrej Industries journey from a colonial-era lock manufacturer to a modern conglomerate encapsulates India's economic evolution. Through principled leadership, strategic diversification, and recent restructuring, the company has positioned itself at the intersection of India's transformation themes. While challenges remain—from conglomerate discounts to competitive pressures—the fundamental story remains compelling: a values-driven enterprise adapting to each era while maintaining core principles.

For investors, Godrej Industries represents a complex but potentially rewarding opportunity. The post-restructuring clarity, improving operational metrics, and exposure to India's structural growth themes offset concerns about leverage and competition. Whether the stock delivers market-beating returns depends on execution, but the foundation—built over 127 years—appears solid.

As India stands at the cusp of potentially explosive growth, companies like Godrej Industries offer a way to participate in this transformation. The question isn't whether India will grow—demographics and economics make that nearly certain. The question is which companies will capture disproportionate value from this growth. With its diversified portfolio, trusted brand, and renewed focus post-restructuring, Godrej Industries has positioned itself as a credible candidate.

The ultimate judgment belongs to markets and time. But if history provides any guide, betting against a company that survived colonialism, world wars, socialism, and family transitions might prove premature. The next 127 years likely won't resemble the last 127, but Godrej Industries seems determined to remain relevant regardless of what comes. For patient investors willing to navigate complexity for potential reward, that resilience might prove valuable.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube