Uno Minda: From a Small Delhi Garage to India's Auto Component Giant

I. Introduction & Episode Roadmap

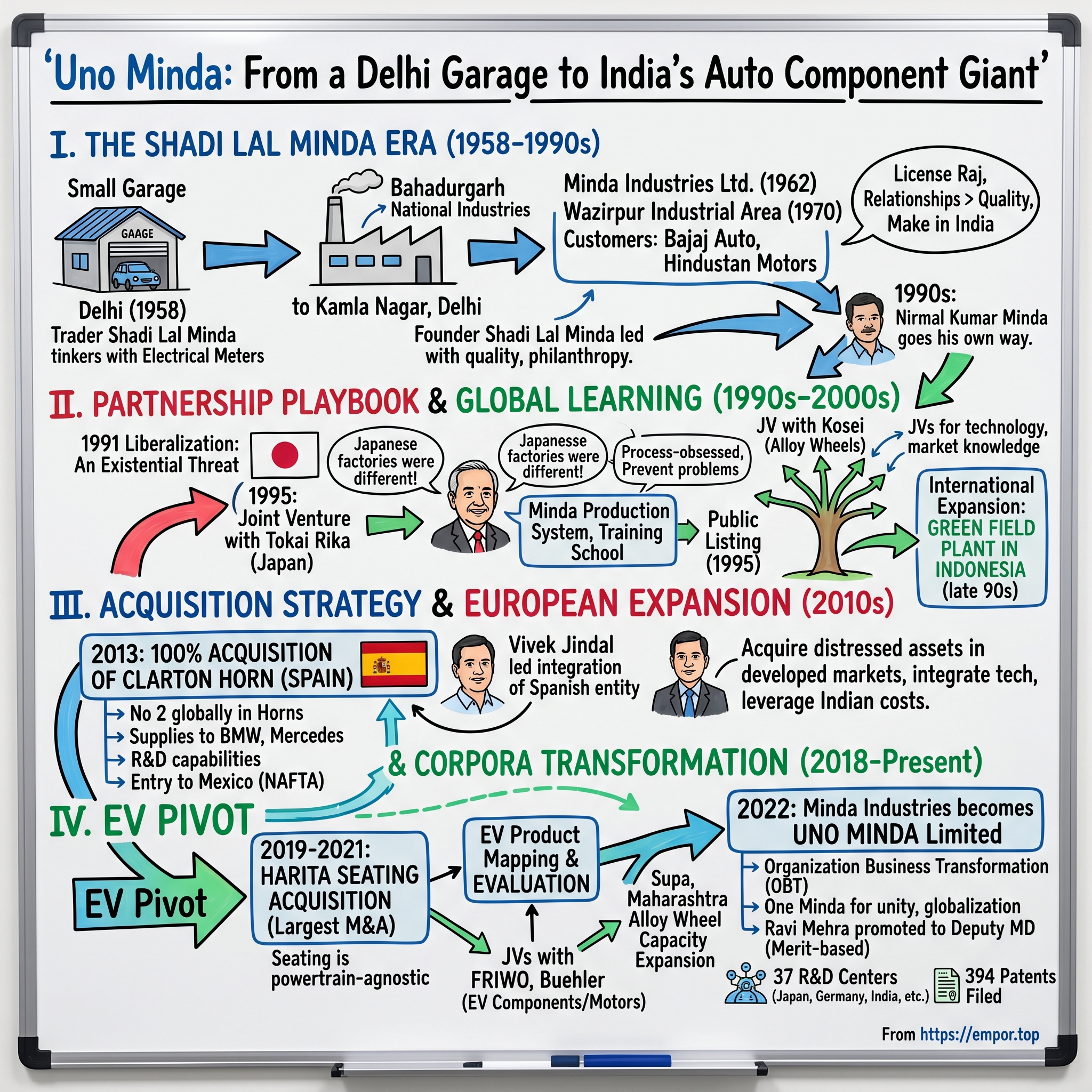

Picture this: A nondescript garage in Delhi's Kamla Nagar, 1958. India has been independent for barely a decade. The nation's industrial landscape is sparse—dominated by British-era textile mills and nascent public sector enterprises. In this unlikely setting, a trader-turned-entrepreneur named Shadi Lal Minda tinkers with electrical meters, dreaming of building something substantial for the newly independent nation.

Fast forward to 2024: Uno Minda commands a market capitalization of ₹62,284 crore with revenue of ₹17,446 crore. The company that started with three partners and a handful of workers now operates presence in 13 countries with 75 manufacturing facilities across India, Indonesia, Vietnam, Germany, Spain, and Mexico. It manufactures 25+ types of components and systems, such as acoustics, switches, lights, alloy wheels, and seats, for vehicles across various segments.

The central question isn't just how a small garage operation became one of India's leading auto component manufacturers—it's how a family business navigated India's economic liberalization, forged unlikely partnerships with Japanese giants when "quality" meant something entirely different in India, and managed to stay relevant through the ICE-to-EV transition that's upending century-old automotive supply chains.

This is a story of three distinct eras: the protected economy where relationships mattered more than quality, the post-liberalization scramble where survival meant learning from global leaders, and today's technology transition where the playbook is being rewritten in real-time. It's about understanding when to partner, when to acquire, and when to build. Most importantly, it's about how a company with "Minda" in its DNA transformed into "Uno"—signaling not just a name change but a fundamental shift in ambition.

II. Origins: The Shadi Lal Minda Era (1958-1990s)

The monsoon of 1958 brought more than just rain to Delhi. In a small workshop, Shadi Lal Minda founded what would become Spark Minda (now Uno Minda) in 1958. But this wasn't some grand industrial vision from the start. The group began as a small auto parts trading firm from Kolkata and Siliguri in India, and later developed into National Industries in 1958 with three partners - Mr. S.L. Minda, Mr. J.P. Minda and Mr. R.N. Minda. National Industries started manufacturing AMMETER at Bahadurgarh (Haryana) in 1958 and later the factory shifted to Kamla Nagar in Delhi.

The India of 1958 was a peculiar place for manufacturing ambitions. Nehru's socialist vision meant the License Raj controlled everything—from how much you could produce to whom you could sell. Foreign technology was viewed with suspicion. Quality was whatever the protected market would accept. In this environment, relationships were currency.

National Industries was renamed to Minda Industries Ltd. in 1962. Soon the company had customers like Bajaj Auto and Hindustan Motors and therefore opened a manufacturing unit in Wazirpur Industrial Area. Think about that—Hindustan Motors, makers of the Ambassador, the car that would define Indian roads for decades. Bajaj Auto, which would become synonymous with Indian mobility. These weren't just customers; they were nation-builders seeking local suppliers.

In 1970-71, more products were added for Original Equipment manufacturers (OEMs). Five years later, the construction started for a modern design factory at Wazirpur Industrial Area. The factory was inaugurated in 1976. This Wazirpur facility wasn't just another factory—it represented a bet on India's automotive future when the entire country produced fewer vehicles annually than a single modern plant does today.

Late Shri Shadi Lal Minda, doyen of the Minda Group was a leading industrialist, who was also renowned for his philanthropy. As founder of the Minda Group, he steered it since 1958 and helped it emerge as a leading player in the Indian automotive industry on the sheer merit of uncompromising quality of its range of automotive parts.

But here's what the official histories don't tell you: survival in the License Raj wasn't about innovation or efficiency. It was about navigating bureaucracy, managing scarcity, and most importantly, maintaining relationships. When imported components were either banned or prohibitively expensive, "Make in India" wasn't a choice—it was the only option. Quality? That was a luxury the protected market didn't demand.

The transition to the next generation began even before liberalization. Nirmal Kumar Minda, son of the founder, joined the family business in 1977. Nirmal Kumar Minda joined the family enterprise in 1977 but went his own way after splitting from his brother (name unknown) in the 1990s. This split—rarely discussed in official narratives—would prove pivotal. While family businesses splitting often weakens both entities, in this case, it freed Nirmal to pursue a radically different vision.

By the late 1980s, cracks in India's protected economy were showing. Japanese motorcycles were creating a new consumer class. Maruti Suzuki's entry in 1983 had already begun reshaping quality expectations. The Minda of 1990 was profitable, established, but utterly unprepared for what was coming.

III. The Partnership Playbook: Learning from Japan (1990s-2000s)

July 24, 1991. Finance Minister Manmohan Singh rises in Parliament to present a budget that would reshape India. For Minda Industries, watching from their Delhi headquarters, this wasn't liberation—it was an existential threat. Global auto giants could now enter India. Quality standards that worked in a protected market would be ruthlessly exposed.

The response would define Uno Minda's next three decades. Long and protracted negotiations led to the creation in 1995 of the first joint venture in India for the manufacture of automotive switches and heater control panels. What began as a technical collaboration has ended up in equity participation and further partnerships, with 60% control held by the Mindas, 35% by Tokai Rika and 5% by Japan's Sumitomo.

But the real story begins earlier. After training along with other Indian entrepreneurs in Japan with Tokai Rika in 1995, Nirmal Kumar Minda experienced what he later described as a revelation. Japanese factories weren't just cleaner or more organized—they operated on fundamentally different principles. Where Indian manufacturing focused on output, the Japanese obsessed over process. Where Indians fixed problems, the Japanese prevented them.

The company got a positive response from Tokai Rika of Japan, a Toyota Group company specialising in switches and sensors. Suzuki management told Tokai Rika that its Indian success depended on quality lapses being bridged at suppliers like Minda. This wasn't charity—Suzuki needed local suppliers to meet their cost targets, and Tokai Rika needed growth beyond Japan's saturating market.

The negotiations for this first JV were comedy and tragedy in equal measure. The Japanese would arrive with 100-page contracts detailing quality parameters Indians had never heard of. Minda's team would counter with relationships and promises. The cultural gap was so wide that early meetings required not just translators but cultural interpreters.

Its first joint venture was signed in 1995 when the company collaborated with Tokai Rika to manufacture automotive switches for four-wheelers. This partnership has thrived over the past three decades, securing over 50% of the market share in India for four-wheeler automotive switches. Think about that—from zero to 50% market share. This wasn't just technology transfer; it was a complete reimagining of what an Indian auto component company could be.

The following of Japanese production systems and methods has since become a core activity for Minda's joint ventures, including the founding of a fully-fledged training school for employees. "That's how we learnt what quality means," says Sanjay Walia, vice-president of corporate marketing. "This focus on the smallest details helped us bridge the quality gap we faced." To ensure it could maintain Maruti Suzuki's quality parameters, Minda has also began paying more attention to supply quality from its own suppliers.

The public listing came in the midst of this transformation. MIL was incorporated as a public limited company in the same year (1995). Going public while simultaneously restructuring operations around Japanese quality standards was like rebuilding a plane mid-flight. But it provided capital for what would become an acquisition and JV spree.

By 2000, Minda had joint ventures sprouting across segments. Entered into joint venture with Kosei for manufacturing alloy wheels for passenger vehicles. Each JV followed a similar template: foreign partner brings technology, Minda brings local knowledge and relationships, both share equity with Minda maintaining majority control. This wasn't just business strategy—it was sovereignty. Nirmal Kumar Minda had seen too many Indian companies become mere subsidiaries of foreign giants.

The international expansion began almost simultaneously. Made first international foray with green field plant in Indonesia. Indonesia in the late 1990s was like India in the 1980s—a protected market beginning to open, dominated by Japanese automakers. Minda could offer something unique: Japanese-quality products at Indian costs with emerging market understanding.

IV. The Acquisition Strategy: Clarton & European Expansion (2010s)

April 15, 2013. A conference room in Barcelona. Nirmal Kumar Minda signs papers acquiring a company older than independent India itself. Uno Minda Ltd had acquired 100% stake in Clarton Horn S.A.U. of Spain in April 2013 from a US-based private equity investment firm Quantum Kapital. The acquisition catapulted Uno Minda to the No 2 position among horn manufacturer worldwide.

Incepted in 1973, Clarton Horn is headquartered in La Carolina (Jaèn, Spain) with modern and state of the art manufacturing facilities in La Carolina (Jaèn, Spain) and Mexico. The company supplied to European automotive royalty—BMW, Mercedes-Benz, Volkswagen. For a company that started in a Delhi garage, this was like a street cricket player signing for Manchester United.

The price? The estimated cost of the acquisition is Euro 7.5 million approx—roughly ₹65 crore at 2013 exchange rates. For context, this was more than many Indian auto component companies' entire annual revenue. The annual turnover of Clarton Horn for 2012 was Euro 38 million.

But why would a profitable European company sell to an Indian player? The 2008 financial crisis had devastated European automotive. Clarton Horn's private equity owners wanted out. European labor costs were crushing margins. Meanwhile, Minda could offer something unique: access to growing Asian markets and Indian cost structures while maintaining European quality standards.

N K Minda, CMD, UNO MINDA, said on the occasion, "The current acquisition will push us in the top league of suppliers of automotive horns. It complements UNO MINDA's strategy to drive innovation through organic and inorganic growth. Clarton Horn is renowned for its technical competence, innovation and quality products. With this acquisition, we would be able to service OEM needs from multi locations and expand our genre of offerings".

The integration wasn't smooth. Spanish workers were skeptical of Indian ownership. European customers worried about quality. The Mexican operations were losing money. Minda's response was counterintuitive: instead of imposing Indian management, they sent their best engineers to learn from Clarton Horn's R&D center. Instead of cutting costs immediately, they invested in upgrading the Mexican facility.

Vivek Jindal is also Director of Clarton Horns Spain and Mexico and successfully led the merger and acquisition of Spanish entity into Uno Minda folds. Vivek, son-in-law of Nirmal Kumar Minda, represented a new generation—IIT Delhi educated, Harvard Business School trained, comfortable in both Barcelona boardrooms and Bahadurgarh factories.

The Clarton Horn acquisition opened doors Minda couldn't have imagined. Suddenly, they were supplying to BMW's main plants. They had a foothold in Mexico just as automotive manufacturing was shifting from the U.S. to take advantage of NAFTA. They had European R&D capabilities that complemented their Japanese manufacturing expertise.

This wasn't Minda's only international play. Through the 2010s, a pattern emerged: acquire distressed assets in developed markets, integrate their technology, leverage Indian cost structures. Each acquisition was a chess move—not just for revenue but for capability building.

V. The EV Pivot & Harita Seating Acquisition (2018-Present)

February 2019. The boardrooms of Mumbai and Delhi buzzed with the same question: Is the internal combustion engine dying? Tesla's Model 3 was proving EVs could be desirable. China was mandating electric vehicles. Even in India, the government was making noises about going all-electric by 2030.

For Uno Minda, with decades invested in ICE components, this could have been catastrophic. Instead, they made their boldest move yet. The flagship company of Uno Minda group, Minda Industries Limited has announced the merger of listed Harita Seating Systems Limited (HSSL), part of the TVS Group, with itself in a share swap deal. This is the largest M&A transaction that Uno Minda has ever undertaken.

HSSL with the market capitalisation of circa 350 crores operates 12 manufacturing plants across India and offers solutions for driver and cabin seating for commercial vehicles, tractors and buses. On paper, this made no sense. What did seating have to do with the EV transition? Everything, as it turned out.

Uno Minda's Seating Division was added with the completion of amalgamation of Harita Seating Systems Ltd with Uno Minda Ltd in 2021. The genius wasn't in the product—it was in the timing and structure. The appointed date for the transaction is 1st April 2019, right when the auto industry was hitting its worst slump in decades.

Here's what most analysts missed: seating is agnostic to powertrain. Whether ICE or EV, vehicles need seats. Moreover, as vehicles become autonomous, seating becomes even more critical—it's where the experience happens. Minda wasn't just hedging against EV transition; they were positioning for a future where the vehicle interior matters more than the engine.

The merger structure was financial engineering at its finest. For every 100 shares held in Harita seats you will get 152 shares of Minda industries. At todays price you buy 100 shares of Harita at 447.00 for a total value of Rs 44,700. You will get 152 shares of Minda, post record date.

But the real EV pivot was happening simultaneously. Entered into Joint venture agreement with FRIWO AG and Buehler motors for various 2W/3W Electric vehicle component and traction motors respectively. FRIWO brought battery management expertise. Buehler brought motor technology. Classic Minda playbook—but executed at unprecedented speed.

The challenge was existential. It is closely reviewing and watching the situations for electric vehicle disruption. It is also mapping all of its existing products vis-à-vis EV vehicles to capitalise on the opportunities. Every product line was evaluated: which would survive electrification, which would die, which would transform.

Switches? Still needed, but different—EVs need different human-machine interfaces. Horns? Absolutely, maybe even more important as silent vehicles need to announce themselves. Lighting? Critical, as EVs use LED technology extensively. Alloy wheels? Even more important, as weight reduction extends battery range.

The two-wheeler alloy wheel story deserves special mention. Uno Minda first entered the two-wheeler alloy wheel segment in FY 21, with a greenfield facility in Supa, Maharashtra, with an initial capacity of 4.0 million wheels. Since then, the company has almost doubled its production capacity at Supa to 8.0 million units. This wasn't just capacity expansion—it was import substitution at scale. India was importing most two-wheeler alloy wheels from China. Minda saw an opportunity to leverage both EV growth and nationalistic policies.

VI. Corporate Transformation & Going "Uno" (2020-2023)

March 25, 2022. A seemingly simple press release announces a name change. Minda Industries Limited becomes Uno Minda Limited. For a company where the founder's name was everything, this was revolutionary. But the story behind this transformation reveals how profoundly Indian family businesses are evolving.

The trigger was complexity. By 2020, the Minda group had become a sprawling empire. The Group has 5 major domains under its umbrella post an Organizational Business Transformation (OBT) exercise in the financial year 2020-21. Multiple listed entities, dozens of subsidiaries, joint ventures that had joint ventures. Customers were confused. Investors couldn't properly value the business. Even employees weren't sure which Minda they worked for.

The NCLT-approved restructuring was Indian corporate history in the making. Merging multiple entities, especially listed ones, through Indian courts is like performing surgery with spectators voting on each incision. Yet they pulled it off, creating a cleaner structure that markets could understand and value.

But "Uno" meant more than simplification. It signaled unity—one Minda, not the various factions that family businesses often devolve into. It suggested globalization—"Uno" works in Spanish, Italian, and English markets where "Minda" was unpronounceable. Most importantly, it represented a psychological shift from family enterprise to professional corporation.

He has been conferred with 'EY Entrepreneur of the Year' Award in Manufacturing Category in 2019. When Nirmal Kumar Minda received this award, he spoke not about past achievements but about institutional building. The company was actively reducing family involvement in operational roles while maintaining strategic control.

Mr. Mehra's association with Uno Minda dates back to 1995, when he joined the Group as General Manager (Finance). Ravi Mehra's elevation to Deputy Managing Director symbolized this shift. A chartered accountant who joined as a middle manager was now second-in-command—merit over bloodline.

The governance structure evolved remarkably. Independent directors weren't just regulatory checkboxes but industry veterans who challenged management. The audit committee actually audited. The compensation committee benchmarked against global standards, not Indian family business norms.

We operate 37 R&D and engineering centers across India, Germany, Japan, Taiwan, Korea, and Spain. This R&D expansion wasn't just about technology—it was about changing the company's DNA from manufacturer to innovator. The company has filed 394 patents, obtained 344 design registrations.

VII. The Business Model & Competitive Moat

Let's talk about moats—not the Buffett kind with crocodiles, but the kind that keeps competitors awake at night. Uno Minda's moat isn't one deep trench; it's a series of interconnected defensive positions that would make a military strategist proud.

First, the product portfolio breadth. We design and produce over 28 categories of components for vehicles across all segments—including passenger cars, commercial vehicles, and two- and three-wheelers—serving both internal combustion engine (ICE) and electric/hybrid vehicles. This isn't diversification for its own sake. Each product category shares customers, technologies, or supply chains with others. When Maruti designs a new car, they can source switches, horns, lighting, and now seats from one supplier. That's not convenience—it's switching cost.

The customer relationships run deeper than most realize. When you've been supplying to Bajaj for 60 years, through family successions, management changes, and market cycles, you're not just a vendor—you're part of their industrial DNA. These relationships survive price pressures that would break purely transactional arrangements.

We have 19 such partnerships with globally renowned manufacturers from Japan, Germany, Korea, and China. Each JV is a moat within a moat. Competitors can't just reverse-engineer products—they need the tacit knowledge embedded in these partnerships. When Tokai Rika shares technology with Minda, they're not just transferring blueprints but decades of know-how.

The capital allocation philosophy is particularly clever. Look at the pattern: JVs for technology-intensive products where partners bring irreplaceable expertise. Acquisitions for market access or when assets are distressed. Organic expansion for commodity products where scale matters more than technology.

Take the alloy wheel business. The Group is market Leader in Alloy Wheel in PV segment with 45% market share in India. They didn't achieve this through breakthrough technology but through relentless focus on localization and scale. Every percentage point of aluminum they source locally, every fraction they shave off conversion costs, makes the moat wider.

The R&D strategy is equally nuanced. 37 R&D and engineering centers sounds impressive, but the distribution tells the real story. Centers in Japan for advanced electronics, Germany for precision engineering, India for frugal innovation. They're not trying to out-innovate Bosch—they're trying to innovate appropriately for their markets.

Manufacturing footprint is its own advantage. 75 manufacturing facilities means they're within trucking distance of almost every major OEM plant in India. In an industry where just-in-time delivery can make or break contracts, geography is destiny.

The balance sheet discipline often goes unnoticed. Unlike many Indian conglomerates that leveraged aggressively during good times, Minda maintained conservative debt levels. This wasn't timidity—it was preparation. When COVID hit and overleveraged competitors struggled, Minda could acquire distressed assets and invest in new technologies.

VIII. Financial Analysis & Performance

The numbers tell a story, but you need to read between the lines. For the full fiscal year FY24, Uno Minda achieved consolidated revenue of INR 14,031 crore, marking a 25% year-over-year growth from INR 11,236 crore in FY23. The EBITDA for the year was INR 1,585 crore, up 28% from INR 1,242 crore in the previous year. The PAT, excluding exceptional income, for FY24 was INR 860 crore, a 32% increase from INR 654 crore in FY23.

These aren't tech company growth rates, but for an auto component manufacturer, 25% revenue growth is exceptional. More importantly, EBITDA growing faster than revenue (28% vs 25%) indicates improving operational efficiency—the Japanese training paying dividends decades later.

Stock is trading at 10.9 times its book value with a PE of 59.8. For context, global auto component companies trade at 15-20x earnings. The premium isn't just India growth story euphoria—it's the market pricing in the successful EV transition and consolidation benefits.

ROCE 18.8%, ROE 17.5%—these returns would make most manufacturers envious. But here's the concern: 19% YoY revenue growth requires constant capital investment. The question isn't whether they can maintain these returns, but whether they can maintain them while funding growth.

The segment mix reveals strategic priorities. Approximately 29% of Uno Minda Limited's revenue in FY23 came from the switches segment. Around 23% came from the lighting segment, 19% from the casting segment, 9% from the seating business, 7% from the acoustic segment and 13% from others. The switches dominance isn't surprising—it's their oldest and most successful JV. But watch the seating segment—at 9% post-merger, it has room to double.

Working capital management deserves attention. Auto component businesses typically struggle with working capital as OEMs squeeze payment terms. Minda's ability to maintain reasonable working capital levels while growing rapidly suggests either exceptional negotiating power or clever supply chain financing—probably both.

The dividend policy signals confidence. The company's board has recommended a final dividend of INR 1.35 per share, a 35% increase from the previous year, bringing the total dividend for FY24 to INR 2.00 per share. In a capital-intensive business undergoing technology transition, maintaining and growing dividends shows remarkable confidence in cash generation.

Currency exposure is the hidden story. With operations across multiple countries and significant import content, Minda faces complex currency dynamics. Their natural hedging through export revenues partially offsets this, but INR depreciation generally helps margins—a macro tailwind that's often underappreciated.

IX. Playbook: Lessons for Founders & Investors

If you're building a manufacturing business in an emerging market, Uno Minda's playbook offers lessons worth more than any MBA. But these aren't feel-good aphorisms—they're battle-tested strategies with scar tissue attached.

Lesson 1: Technology Partnerships Over Technology Ownership

The temptation for emerging market companies is to either remain low-tech manufacturers or attempt to become technology leaders. Minda chose a third path: permanent technology student. Every JV was structured to ensure continuous technology transfer, not just one-time licensing. They didn't try to out-innovate Tokai Rika—they ensured Tokai Rika's innovations reached Indian markets profitably.

Lesson 2: Timing Market Transitions

Three major transitions defined Minda's growth: economic liberalization (1991), global supply chain integration (2000s), and vehicle electrification (2020s). In each case, they moved neither too early (bleeding edge) nor too late (catching up). The Harita acquisition during the auto slowdown, EV JVs before EV adoption—timing that looks lucky was actually calculated.

Lesson 3: The Art of Maintaining Control

Promoter Holding: 68.7%—after decades of JVs, acquisitions, and public listings, the family still controls the company. This wasn't accident but architecture. Every deal was structured to maintain majority control. Every board seat carefully allocated. They got global technology and capital without becoming a subsidiary.

Lesson 4: Localization as Strategy, Not Tactic

When Minda talks about "Make in India," they mean something different than politicians. For them, localization isn't import substitution—it's capability building. Each localized component teaches something: metallurgy from alloy wheels, electronics from switches, precision engineering from sensors. The knowledge compounds.

Lesson 5: Family Business Modernization

The transition from Shadi Lal to Nirmal Kumar to the next generation (Vivek Jindal, Paridhi Minda) shows how family businesses can modernize without imploding. Gradual professionalization, merit-based promotions for non-family executives, and clear succession planning—boring but essential.

Lesson 6: Multi-Generational Vision with Quarterly Execution

Listed companies face quarterly pressure. Family businesses think in generations. Minda somehow does both. The 2019 Harita acquisition wouldn't pay off for years but was executed with quarterly milestone precision. Long-term vision doesn't excuse short-term sloppiness.

Lesson 7: The Compound Effect of Reputation

In industries where switching costs are high and relationships matter, reputation compounds like interest. Every delivered order, every quality issue resolved, every commitment kept adds to a reputational bank account that pays dividends decades later. Minda's 60-year relationships with OEMs are impossible for new entrants to replicate quickly.

X. Bear vs. Bull Case & Future

Bear Case: The Structural Headwinds

The bear case isn't about one catastrophic risk but multiple erosion factors. Start with the obvious: Chinese competition. Chinese auto component manufacturers aren't just cheaper—they're increasingly sophisticated. As Indian OEMs face pressure to reduce costs, especially in EVs where battery costs dominate, the pressure to switch to Chinese suppliers intensifies.

The EV transition timeline remains the biggest unknown. If ICE vehicles decline faster than expected, stranded assets become real. Those 75 manufacturing facilities optimized for ICE components? The decades of combustion engine expertise? The supplier relationships built on ICE platforms? All potentially obsolete faster than depreciation schedules assume.

OEM consolidation presents another challenge. As global automakers merge or form alliances, supplier bases consolidate too. Being a big fish in the Indian pond matters little if global procurement decisions shift to Detroit, Tokyo, or Wolfsburg. The Stellantis formation, Nissan-Renault-Mitsubishi alliance evolution—each reshapes supplier dynamics unpredictably.

The complex corporate structure, despite simplification, remains a concern. Multiple JVs mean multiple boards, competing interests, and decision paralysis potential. When your Japanese partner wants one thing, German partner another, and Indian market demands a third, whom do you satisfy?

Margin pressure is structural, not cyclical. OEMs globally are facing Tesla's vertical integration challenge. The response? Squeeze suppliers harder. Demand annual price reductions. Push inventory costs downstream. Minda's improving margins might be swimming against a tide that eventually wins.

Bull Case: The Convergence of Tailwinds

The bull case starts with India's auto market potential. Vehicle penetration remains among the lowest globally. As per capita income crosses $3,000—the typical motorization inflection point—demand could surprise everyone. We're talking about hundreds of millions of potential first-time vehicle buyers.

We hold a leadership position in India across nearly all our product categories. This isn't just market share—it's standard-setting power. When Minda designs a switch, it becomes the de facto standard Indian consumers expect. New entrants must match their quality, price, and service—a three-dimensional challenge.

The EV transition, counterintuitively, might be an opportunity. Legacy suppliers are distracted protecting ICE businesses. New EV-only suppliers lack manufacturing scale. Minda, with feet in both camps, can optimize transition timing. Their early EV partnerships are already generating revenue while competitors debate strategy.

Content per vehicle is increasing secularly. Modern vehicles have more switches (power windows, electronic controls), more lighting (LED, ambient), more acoustic needs (pedestrian warning systems for EVs). Even as vehicle production moderates, revenue per vehicle grows.

The export opportunity remains underpenetrated. The near-term target is to achieve 25% from overseas business. With manufacturing costs 30-40% lower than developed markets and quality approaching global standards, the export potential is substantial. The Clarton Horn acquisition provided market access—now it's about execution.

Government policy alignment provides tailwinds. Production-linked incentives, import duties on Chinese components, "Atmanirbhar Bharat" procurement preferences—policy explicitly favors domestic manufacturers. Unlike market forces, policy support can change quickly, but current direction strongly favors Minda.

XI. Epilogue & Final Thoughts

Standing in Uno Minda's Gurugram headquarters, you see three photographs: Shadi Lal Minda, the founder; Nirmal Kumar Minda, the transformer; and a group photo of the current leadership team—family and professionals together. It's a visual metaphor for Indian capitalism's evolution.

What would we do as management? First, double down on the EV transition but hedge bets carefully. The future isn't ICE or EV—it's both, for longer than purists expect. Second, accelerate the export engine. Indian manufacturing's moment is now, with global supply chains diversifying from China. Third, simplify further. Despite progress, complexity remains Minda's biggest internal enemy.

The surprises in researching this story? The depth of relationships that survived decades and disruptions. The willingness to dilute family control for strategic partnerships when most family businesses guard equity zealously. The patience—waiting years for JVs to fructify, decades for strategies to pay off.

For investors, Uno Minda represents a bet on Indian automotive growth, successful EV transition, and management execution. The valuation isn't cheap, but transformation stories rarely are. The question isn't whether they'll face challenges—they will. It's whether six decades of navigating Indian industrial evolution has prepared them for what's next.

For founders, especially in emerging markets, the lesson is clear: technology partnerships can be as valuable as technology development. Market transitions create opportunities for prepared companies. Family businesses can modernize without losing their soul.

The Uno Minda story isn't finished. The EV chapter is just beginning. Chinese competition is intensifying. Global supply chains are reshaping. But if history is any guide, that garage startup from 1958 will find a way to not just survive but thrive. After all, they've been doing it for 66 years.

In the end, Uno Minda's story is India's story—protection to competition, isolation to integration, imitation to innovation. It's messy, complicated, sometimes contradictory, but ultimately progressive. And like India itself, it's far from over.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube