SRF Limited: From Tyre Cords to Global Chemical Champion

I. Introduction & Episode Setup

The sprawling chemical complex in Bhiwadi, Rajasthan, hums with a peculiar rhythm—the sound of refrigerant gases being compressed, fluoropolymers being synthesized, and specialty molecules taking shape in gleaming reactors. This is the nerve center of SRF Limited, a company that today commands an ₹85,000+ crore market capitalization and exports to more than 90 countries. Yet few outside India's chemical industry circles know the remarkable transformation story behind these numbers.

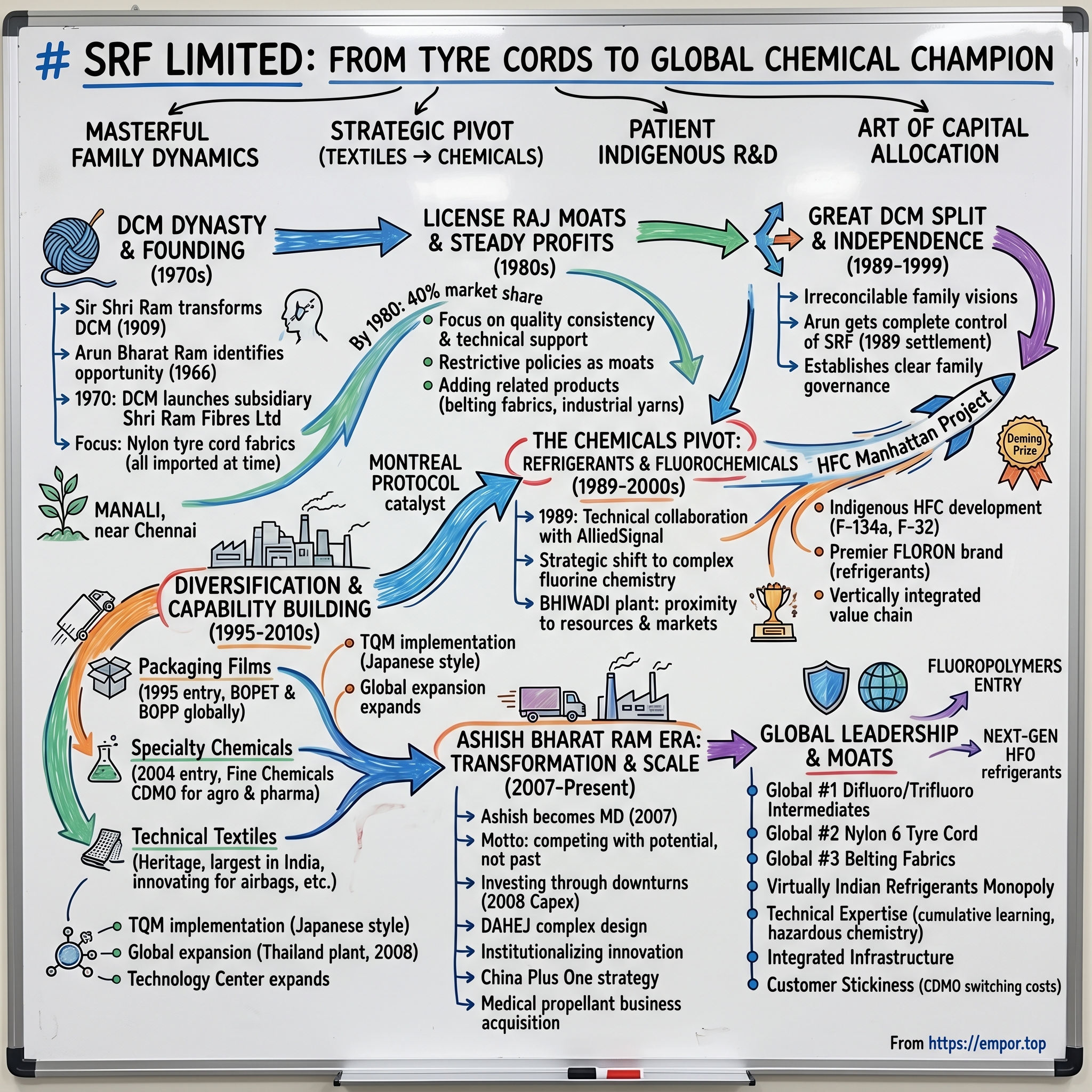

Picture this: In 1970, a young Arun Bharat Ram, fresh from identifying opportunities in India's nascent technical textiles sector, convinces his family's industrial conglomerate DCM to launch a subsidiary focused solely on nylon tyre cords. Fast forward five decades, and that tyre cord manufacturer has morphed into India's refrigerant monopoly, a global top-three player in multiple specialty chemical segments, and a critical supplier to pharmaceutical and agrochemical giants worldwide.

The fascinating question at the heart of this story isn't just how a company pivots from textiles to chemicals—plenty have tried that. It's how SRF managed to build genuine technological moats in businesses where Indian companies traditionally played catch-up to Western and Japanese competitors. How did they become the only Indian manufacturer of ozone-friendly refrigerants using indigenous technology? Why do global pharma companies trust them with complex fluorination chemistry that even Chinese manufacturers struggle with? Today's story begins with understanding four critical themes that define SRF's evolution. First, the masterful navigation of family business dynamics—how the Bharat Ram family managed not one but two major splits while maintaining business continuity. Second, the strategic pivot from commoditized textiles to specialty chemicals at precisely the right moment in global regulatory shifts. Third, the patient building of indigenous R&D capabilities that now rival global leaders. And finally, the art of capital allocation in cyclical businesses—knowing when to expand aggressively and when to consolidate.

SRF today commands a market capitalization of approximately ₹85,000-90,000 crore, with current revenue (TTM) of $1.62 billion USD. The company manufactures technical textiles, chemicals, packaging films, aluminum foils, and other polymers across four countries—India, Thailand, South Africa, and Hungary. But these numbers only hint at the deeper transformation story.

Consider the breadth of their current dominance: They're the global number one in Difluoro & Trifluoro Alkyl Intermediates, global number two in Nylon 6 Tyre Cord, and global number three in Belting Fabrics. In refrigerants, they hold a virtual monopoly in India as the only domestic manufacturer of ozone-friendly variants like F-134a and F-32, both developed using indigenous technology. Their specialty chemicals division has commercialized more than 100 molecules, with another 50+ in various stages of development, supported by over 400 R&D personnel and 300+ patent applications.

This episode explores how a company born in the License Raj era, starting with a single tyre cord plant in Manali near Chennai, transformed itself into a global specialty chemicals powerhouse. It's a story of strategic foresight, family business management, technological capability building, and perhaps most importantly, the ability to spot and capitalize on massive regulatory shifts before competitors even understood what was happening.

So what for investors: SRF represents a rare case study in successful business transformation—from commoditized textiles to high-margin specialty chemicals. Understanding their playbook offers insights into identifying similar transformation opportunities in other traditional Indian manufacturing companies.

II. The DCM Dynasty & Founding Story (1970-1989)

The year is 1909. A young Sir Shri Ram joins a modest trading firm called Delhi Cloth Mills Company Limited, better known as DCM. What follows over the next five decades is the stuff of Indian industrial legend—he transforms this textile trader into a sprawling conglomerate manufacturing everything from textiles and sugar to chemicals, vanaspati, pottery, fans, sewing machines, electric motors, and capacitors. By the time of his death in 1963, DCM had become synonymous with Indian industrial ambition.

But Sir Shri Ram's greatest challenge would come posthumously. He left behind two sons—Bharat Ram and Charat Ram—along with a massive industrial empire and no clear succession plan. The brothers initially worked together, but beneath the surface, fundamental differences in vision and temperament were brewing. Bharat Ram, the elder, was methodical and focused on consolidation. Charat Ram was entrepreneurial, constantly seeking new ventures.

Enter the third generation in 1966. Arun Bharat Ram, fresh from his education, joins DCM's textile division. Unlike his father and uncle who were managing the existing empire, Arun had the hunger of a founder. He spent his early years studying the textile value chain, traveling to Japan and Europe, observing how technical textiles were becoming critical components in emerging industries. While cotton textiles were becoming commoditized, he noticed something interesting—nylon tyre cord fabrics were growing at double-digit rates globally.

The insight was elegant: As India's automobile industry grew, tyre manufacturers would need high-quality reinforcement materials. At the time, all tyre cord was imported, creating both a foreign exchange drain and supply chain vulnerability. Arun saw an opportunity to apply DCM's textile expertise to this technical application. But convincing the family board wasn't easy.

"Why venture into unknown territory when we have profitable textile mills?" was the prevailing sentiment. Arun's response was prophetic: "The future belongs to specialty applications, not commodity textiles. We need to move up the value chain before someone else does."

In 1970, after months of persuasion, DCM finally agreed to establish Shri Ram Fibres Limited as a wholly-owned subsidiary. The initial investment was modest by DCM standards—₹5 crores for a plant in Manali, near Chennai. The location choice was strategic: close to major tyre manufacturers in South India, with access to Chennai port for importing raw materials and eventually exporting finished products.

The Manali plant, commissioned in 1973, was more than just a manufacturing facility—it was Arun's laboratory for understanding technical textiles. The early years were brutal. Quality issues plagued production. Tyre manufacturers were skeptical of an Indian supplier. MRF, Apollo, and CEAT had long-standing relationships with international suppliers. Why risk switching to an unproven domestic player?

Arun's approach was methodical. Rather than competing on price—a race to the bottom—he focused on three things: quality consistency, technical support, and supply reliability. SRF engineers were embedded at customer plants, understanding their specific requirements. When a tyre manufacturer faced a technical issue, SRF's team would work through nights to find solutions. Slowly, order by order, the company built credibility.

The License Raj context is crucial here. In the 1970s, India's industrial policy was a maze of permits, quotas, and restrictions. Getting a license to manufacture was just the first hurdle. Importing technology required separate approvals. Expanding capacity needed government permission. Foreign exchange for importing raw materials was rationed. Most entrepreneurs saw these as insurmountable barriers. Arun saw them as moats.

"Every restriction that made our life difficult made it equally difficult for potential competitors," he would later reflect. The license to manufacture nylon tyre cord became SRF's first regulatory moat—one that would protect its domestic market for nearly two decades.

By 1980, SRF had captured 40% of India's tyre cord market. The company was generating steady profits, reinvesting everything back into R&D and capacity expansion. But Arun knew that being a single-product company was dangerous. He began studying adjacent markets where SRF's technical textile expertise could be applied. Belting fabrics for conveyor belts, industrial yarns for fishing nets, coated fabrics for automotive applications—each represented a logical extension.

The 1980s saw SRF methodically adding these products, turning the Manali plant into a technical textiles complex. But the real transformation was happening in Arun's mind. Through his travels and customer interactions, he kept encountering one recurring theme: the future of materials wasn't in mechanical properties alone, but in chemistry. Advanced materials would require chemical treatments, coatings, and modifications. The seeds of SRF's chemical pivot were being planted.

Meanwhile, tensions within the DCM family were escalating. By the mid-1980s, it was clear that the joint family business structure wasn't sustainable. Three branches of the family—Bharat Ram's sons, Charat Ram's sons, and the sons of Sir Shri Ram's daughter Murli Dhar—had different visions for the future. Some wanted to focus on traditional businesses, others on new ventures. Some preferred conservative growth, others aggressive expansion.

The first family split in 1989 would prove to be SRF's liberation moment. As part of the settlement, Arun Bharat Ram would get complete control of SRF, finally free to execute his vision without family board politics. But that liberation came with a challenge—SRF would no longer have access to DCM's resources and had to stand on its own.

The timing couldn't have been more fortuitous. Just as SRF was gaining independence, a global environmental treaty was about to create the opportunity of a lifetime. The Montreal Protocol on Substances that Deplete the Ozone Layer was signed in 1987, mandating the phase-out of chlorofluorocarbons (CFCs). For most Indian companies, this was just another international agreement. For Arun Bharat Ram, it was the strategic opening he had been waiting for.

Myth vs Reality Box: Myth: SRF's entry into chemicals was opportunistic, driven by the Montreal Protocol. Reality: Arun Bharat Ram had been studying chemical opportunities since the early 1980s, even sending teams to scout for technology partners. The Montreal Protocol provided the catalyst, but the strategic intent preceded it by years.

The transformation from Shri Ram Fibres to SRF Limited in 1990 wasn't just a name change—it symbolized a fundamental shift in identity. The company was no longer defining itself by its products (fibres) but by its purpose (creating value through technical excellence). This subtle but crucial rebranding would guide every strategic decision for the next three decades.

So what for investors: The DCM-SRF story illustrates how family business splits, often seen as value-destructive, can actually unlock focused execution. Look for similar situations where complex family structures are simplifying—the newly independent entities often outperform significantly.

III. The Great DCM Split & SRF's Independence (1989-1999)

The mahogany-paneled boardroom at DCM's Connaught Place headquarters had witnessed many heated discussions, but the meetings of early 1989 carried a different weight. Three generations of the Shri Ram family sat across from each other, lawyers and advisors flanking them, dividing an empire built over eight decades. The atmosphere was cordial—this was still family, after all—but underneath lay the tension of irreconcilable visions.

"The split had been coming for years," recalls a former DCM executive who witnessed the negotiations. "You had Bharat Ram's sons wanting to modernize and globalize, Charat Ram's family focused on diversification into new sectors, and the third branch wanting to maintain traditional businesses. Something had to give."

The 1989 settlement was remarkably civil by Indian business family standards. No courtroom battles, no media leaks, no public acrimony. The empire was divided roughly along existing business lines. Arun Bharat Ram's branch received SRF Limited, DCM's technical textiles subsidiary, along with some other industrial assets. On paper, it seemed like Arun got the smaller piece of the pie—SRF's revenues were a fraction of DCM's sugar or textile operations.

But Arun saw something others didn't. "Managing the family is as important as managing the business," he would later tell colleagues. "In India, we neglected our families and concentrated on managing the business. I was determined not to repeat that mistake." His first move post-split was establishing clear governance structures within his own family—professional boards, defined roles, and succession planning from day one.

The newfound independence coincided with a massive global shift. In 1987, the Montreal Protocol had been signed, requiring the phase-out of ozone-depleting substances. By 1989, developed nations were scrambling to find alternatives to CFCs used in refrigeration and air conditioning. India hadn't yet signed the protocol, but Arun knew it was inevitable. More importantly, he recognized this as SRF's chance to leapfrog into high-value chemicals.

The refrigerant opportunity was compelling but complex. Manufacturing fluorochemicals required sophisticated technology, massive capital investment, and expertise SRF didn't possess. Traditional refrigerants like R-12 and R-11 were being phased out, replaced by HCFCs (hydrochlorofluorocarbons) as transitional substances and eventually HFCs (hydrofluorocarbons). Whoever could master this transition in India would essentially own the market for decades. In 1989, SRF made its boldest move yet. The company signed a technical collaboration with AlliedSignal (now Honeywell) of USA for manufacturing fluorochemicals (CFCs and HCFCs) at a new plant in Bhiwadi, Rajasthan. The collaboration was crucial—AlliedSignal brought technology and know-how, while SRF provided local manufacturing expertise and market access.

The Bhiwadi location was carefully chosen. Unlike the coastal Manali plant built for textiles, Bhiwadi offered proximity to North Indian industrial markets, access to raw materials from Gujarat's chemical belt, and critically, distance from populated areas—essential for chemical manufacturing. The initial investment was substantial: ₹50 crores, nearly equal to SRF's entire net worth at the time.

"People thought we were crazy," recalls a former SRF executive involved in the project. "Here we were, a textile company, suddenly talking about anhydrous hydrogen fluoride, chloroform, and complex chemical reactions. The board meetings were like chemistry classes."

But Arun's vision extended beyond just manufacturing refrigerants. He understood that the Montreal Protocol would create a cascade of opportunities. First, CFCs would be phased out, replaced by HCFCs. Then HCFCs would be phased out, replaced by HFCs. Each transition would require new technology, new products, and new investments. Companies that could navigate all three waves would dominate the market for decades.

In 1989, the company entered the chemicals business to manufacture refrigerants. Consequently, in 1990, it changed its name to SRF Limited. The name change was more than cosmetic—it signaled to customers, investors, and employees that SRF was no longer just about fibres. It was about creating value through technical excellence, whether in textiles or chemicals.

The early 1990s were a period of intense learning. The Bhiwadi plant faced numerous technical challenges. Fluorine chemistry is notoriously difficult—highly corrosive, requiring specialized materials and extreme safety protocols. Several minor accidents and near-misses led to temporary shutdowns. Quality consistency was a major issue. International customers, particularly Japanese air conditioning manufacturers, had stringent purity requirements that SRF initially struggled to meet.

But the team persevered. Engineers were sent to AlliedSignal's facilities in the US for training. Quality systems were upgraded to meet international standards. Safety protocols were enhanced with help from DuPont's safety consultants. By 1992, the Bhiwadi plant was running at full capacity, producing CFC-11, CFC-12, and HCFC-22 for the domestic market.

The real breakthrough came with backward integration. In 1995, SRF set up a chloromethanes plant in collaboration with Atofina (now Arkema) to meet requirements for carbon tetrachloride (raw material for CFCs) and chloroform (raw material for HCFC-22). This move was strategic genius—it reduced dependence on imported raw materials, improved margins, and most importantly, gave SRF control over its entire value chain.

Meanwhile, another significant development was unfolding. In 1995, the company acquired a BOPET film plant at Kashipur in India from Flowmore, marking its entry into packaging films. This wasn't random diversification—Arun saw synergies between chemical processing capabilities and film manufacturing. Both required precision engineering, quality control, and understanding of polymer chemistry.

The second family split in 1999 further clarified SRF's ownership structure. Vivek Bharat Ram took DCM Financial Services and DCM Benetton, while Arun secured complete control of SRF. This final separation eliminated any lingering ambiguity about leadership and strategic direction. SRF was now truly Arun's company to shape.

By 1999, SRF had successfully transformed from a tyre cord manufacturer to a diversified technical products company. The chemicals business was generating higher margins than textiles. The packaging films business was growing rapidly. The company had built capabilities in complex chemistry, international collaborations, and multi-site manufacturing. But the biggest opportunities—and challenges—lay ahead.

So what for investors: The 1989-1999 period demonstrates how regulatory changes (Montreal Protocol) can create massive opportunities for prepared companies. Watch for similar regulatory shifts in areas like carbon emissions, plastic waste, or battery recycling—early movers with technical capabilities can build decades-long moats.

IV. The Chemicals Pivot: Refrigerants & Fluorochemicals (1989-2000)

The conference room at the Bhiwadi plant in 1995 was thick with cigarette smoke—this was before corporate India discovered wellness. Arun Bharat Ram sat at the head of the table, surrounded by his technical team, poring over molecular diagrams and phase-out schedules. The Montreal Protocol's first deadline had passed, CFCs were being phased out globally, and SRF had a critical decision to make: stick with transitional HCFCs or leap directly to HFCs, the final destination chemicals.

"The safe choice was HCFCs," remembers Dr. R.K. Sharma, then head of R&D. "They were easier to manufacture, required less investment, and had assured demand for at least 15-20 years. But Arun kept asking, 'Why should we invest in transitional technology when we know where the world is headed?'"

The decision to develop HFC technology indigenously was audacious. SRF became the only Indian manufacturer of ozone-friendly refrigerants, namely F-134a and F-32, both developed using indigenous technology. While competitors were content importing technology or manufacturing under license, SRF chose the harder path of building internal capabilities.

The development of HFC-134a became SRF's Manhattan Project. Unlike HCFCs which could use modified CFC equipment, HFCs required entirely new chemistry, new catalysts, and new processes. The raw material was different—instead of chloroform, they needed trichloroethylene. The reaction conditions were more severe, requiring higher pressures and temperatures. The purification standards were stricter—automotive air conditioning systems couldn't tolerate even trace impurities.

SRF's R&D team, now expanded to over 50 scientists, worked in shifts around the clock. They collaborated with the Indian Institute of Technology Delhi for catalyst development, with the National Chemical Laboratory Pune for process optimization. Small pilot plants were built to test different configurations. Failures were frequent—batches would fail purity tests, catalysts would deactivate prematurely, yields would be uneconomical.

The breakthrough came in 1996 when a young chemical engineer suggested a novel purification technique borrowed from pharmaceutical manufacturing. Instead of traditional distillation, they used a combination of membrane separation and cryogenic purification. It was expensive but delivered the ultra-high purity that automotive customers demanded. More importantly, it could be retrofitted into existing equipment, saving millions in capital investment.

By 1997, SRF's Bhiwadi plant was producing commercial quantities of HFC-134a, years ahead of any Indian competitor. The timing was perfect. The Indian automobile industry was booming, with Maruti Suzuki, Hyundai, and Honda setting up local manufacturing. These companies needed local suppliers for refrigerants to meet localization requirements. SRF was the only domestic option.

But the real masterstroke was the brand strategy. Instead of selling refrigerants as commodities, SRF created the FLORON brand, positioning it as a premium, environmentally responsible choice. SRF's Floron brand of refrigerants enjoys an over 40% share of the Indian market. Marketing materials emphasized the ozone-friendly nature, the indigenous technology, and the technical support that came with every drum.

The expansion beyond refrigerants into industrial chemicals was a natural progression. The same fluorination chemistry used for refrigerants could produce intermediates for pharmaceuticals and agrochemicals. These were higher-margin, lower-volume products that leveraged SRF's chemical expertise without requiring massive additional investment.

With the addition of F-125, SRF is now the largest producer and seller of refrigerants in India. But achieving this position required navigating complex global dynamics. In 1998, Chinese manufacturers began flooding global markets with cheap refrigerants, often below production cost. Many Indian importers switched to Chinese products, pressuring SRF's market share.

Arun's response was counterintuitive: instead of cutting prices, SRF increased investment in quality and service. They established a nationwide network of technical service centers. When a customer faced a refrigerant-related issue, SRF engineers would be on-site within hours. They conducted training programs for air conditioning technicians. They offered extended credit terms to build loyalty. The strategy worked—customers stayed with SRF despite the price premium.

The vertical integration strategy accelerated in this period. SRF built plants for every critical raw material. Anhydrous hydrogen fluoride, the key starting material for all fluorochemicals, was manufactured in-house. Chloroform and carbon tetrachloride production was expanded. In 2012, SRF started producing trichloroethylene (raw material for HFC-134a) and perchloroethylene (raw material for HFC-125), though the capability building started much earlier.

Environmental compliance became a critical differentiator. While competitors cut corners on effluent treatment, SRF invested heavily in environmental systems. The Bhiwadi plant installed thermal oxidizers to destroy fluorinated waste gases. Effluent treatment plants were upgraded to zero liquid discharge. These investments, while expensive, built credibility with global customers who were increasingly sensitive to supply chain sustainability.

The R&D capabilities built during this period would prove invaluable later. The team that developed HFC-134a went on to develop dozens of other fluorinated molecules. The analytical capabilities built to ensure refrigerant purity were applied to pharmaceutical intermediates. The safety systems developed for handling hydrogen fluoride became the foundation for handling other hazardous chemicals.

By 2000, SRF's chemical business had crossed ₹200 crores in revenue, with EBITDA margins exceeding 25%—nearly double that of the textile business. The company had filed its first international patents for novel refrigerant blends. Global customers like Carrier, Daikin, and Trane were sourcing from SRF. The transformation from textile manufacturer to chemical company was complete.

The organizational culture had also transformed. The hierarchical, process-driven culture of textiles gave way to a more innovative, risk-taking mindset. Scientists and engineers were encouraged to experiment. Failures were tolerated if they led to learning. Cross-functional teams became the norm. The company that entered the 1990s as a traditional manufacturer exited as a technology-driven enterprise.

Myth vs Reality Box: Myth: SRF succeeded in chemicals because of the Montreal Protocol creating a protected market. Reality: While the Protocol created opportunity, SRF's success came from indigenous technology development, vertical integration, and service excellence. Many companies had the same opportunity; only SRF fully capitalized on it.

So what for investors: SRF's refrigerant journey illustrates the power of regulatory tailwinds combined with execution excellence. The company didn't just ride the wave—it positioned itself ahead of each transition. Similar opportunities exist today in areas undergoing regulatory transformation like EVs, renewable energy, and sustainable packaging.

V. Diversification & Capability Building (1995-2010)

The acquisition announcement in 1995 caught everyone by surprise. SRF, known for its methodical, organic growth, was buying Flowmore Polyesters' BOPET film plant in Kashipur for ₹25 crores. The plant was struggling, operating at 40% capacity, bleeding cash. Industry observers were puzzled—what did a chemicals and textiles company want with plastic films?

Arun Bharat Ram saw what others missed. The global packaging industry was undergoing a revolution. Traditional materials like paper and aluminum were being replaced by polymer films—lighter, cheaper, more versatile. BOPET (Biaxially Oriented Polyethylene Terephthalate) films were at the forefront, used in everything from food packaging to magnetic tapes. India's consumption was growing at 15% annually, mostly met through imports.

But the real insight was deeper. "Films are not just polymers," Arun explained to his skeptical board. "They're precision products requiring chemical knowledge, process control, and quality systems—all capabilities we've built in chemicals and technical textiles. This is a logical adjacency, not random diversification."

The Kashipur plant transformation became a template for SRF's acquisition strategy. Within six months, capacity utilization crossed 80%. The quality issues that plagued Flowmore—thickness variation, optical defects, poor adhesion—were systematically addressed. SRF's engineers applied Statistical Process Control techniques learned in textiles. The R&D team developed new formulations for better clarity and strength. Operations were streamlined using Total Quality Management principles being implemented across SRF.

SRF has since then manufactured both BOPET and BOPP films globally, but the journey to global scale wasn't straightforward. In 1997, just as the Kashipur plant stabilized, the Asian Financial Crisis struck. Demand collapsed as customers destocked. Thai and Korean producers dumped inventory at distressed prices. SRF's film business posted its first loss.

The crisis became a learning opportunity. Instead of retrenching, SRF accelerated product development. They identified niche applications—release films for adhesive tapes, metallized films for flexible packaging, ultra-thin films for capacitors—where technical requirements created entry barriers. Each niche required specific modifications: surface treatments, coating chemistries, lamination techniques. SRF's chemical expertise proved invaluable in developing these specialties.

The entry into specialty chemicals in 2004 marked another pivotal transformation. The company entered the specialty chemicals business in 2004 as a supplier of fine chemicals to the agrochemicals and pharmaceuticals industry. The business is engaged in custom synthesis, and contract research and manufacturing.

The trigger was a serendipitous meeting between Arun and the procurement head of a global agrochemical major at a conference in Singapore. The executive mentioned their struggle finding reliable suppliers for fluorinated intermediates outside China. "Can SRF help?" he asked. Arun's response was immediate: "Give us the molecule, we'll figure out the rest."

The specialty chemicals model was fundamentally different from refrigerants. Instead of making standard products for multiple customers, SRF would develop custom molecules for specific clients. The customer would provide the target molecule and sometimes basic chemistry. SRF would develop the process, scale up production, and manufacture exclusively for that customer. It was essentially contract manufacturing, but with deep technical collaboration.

The first project was a disaster. The molecule—a complex fluorinated intermediate for a herbicide—seemed straightforward in the lab. But scaling up revealed unexpected problems. The reaction was highly exothermic, causing runaway conditions. Yields dropped from 80% in the lab to 30% in the pilot plant. Impurities that were negligible at gram scale became major issues at kilogram scale. The project consumed twice the budgeted resources and missed every deadline.

But SRF persisted, and the learning from that failure proved invaluable. They realized that specialty chemicals required different capabilities than commodity chemicals. Project management became critical—customers needed reliable timelines, not just quality products. Analytical capabilities were upgraded—identifying and quantifying trace impurities required sophisticated instrumentation. Safety systems were enhanced—many molecules were not just toxic but potentially explosive.

The breakthrough came with the second project, ironically from the same customer. This time, SRF applied all the lessons learned. They started with extensive lab work before committing to scale-up. They built a dedicated pilot plant for customer projects. They hired project managers from the pharmaceutical industry who understood regulated manufacturing. The project was delivered on time, within budget, and exceeding quality specifications.

Word spread quickly in the close-knit world of agrochemical procurement. By 2006, SRF was working with three of the top five global agrochemical companies. Each relationship started small—a single intermediate, modest volumes—but expanded as trust built. Customers appreciated SRF's unique combination: Chinese cost levels, Western quality standards, and Indian English-speaking technical support.

The R&D infrastructure expansion during this period was remarkable. The Technology Center at Bhiwadi grew from 50 to 200 scientists. Analytical labs were equipped with NMR spectrometers, mass spectrometers, and X-ray diffraction equipment—investments of crores for instruments that might be used only occasionally. But Arun insisted on having capabilities in-house. "You can't develop molecules if you can't analyze them," became a company mantra.

The pace of innovation accelerated. SRF developed a novel route to a key pharmaceutical intermediate that reduced steps from seven to three. They pioneered a fluorination technique using elemental fluorine—extremely hazardous but enabling unique chemistries. They mastered cryogenic reactions, conducting chemistry at -80°C for temperature-sensitive molecules. Each capability opened new customer opportunities.

International expansion followed naturally. In 2008, SRF established its first overseas manufacturing facility in Thailand for packaging films. The location offered several advantages: proximity to Southeast Asian markets, free trade agreements with key countries, and lower energy costs than India. But the real reason was customer demand—global brands wanted supply chain redundancy and local manufacturing.

The 2008 financial crisis tested SRF's diversification strategy. Textile demand collapsed as consumers cut spending. Chemical prices crashed as customers destocked. Film margins evaporated as overcapacity plagued the industry. But the portfolio approach proved its worth—while individual businesses struggled, the company overall remained profitable. Specialty chemicals, being custom products with contracted volumes, provided stability.

The Total Quality Management journey initiated in this period deserves special mention. In 2006, SRF embarked on implementing Japanese-style TQM across all operations. This wasn't just about quality circles and suggestion schemes. It was a fundamental transformation in how the company operated. Every process was documented and standardized. Every deviation was analyzed for root cause. Every employee was trained in problem-solving techniques.

The impact was dramatic. Defect rates in films dropped from 3% to 0.3%. Batch failure rates in chemicals fell from 5% to less than 1%. Customer complaints reduced by 80%. The culmination came in 2012 when SRF's Chemicals Business won the prestigious Deming Prize for TQM—one of the few Indian companies to achieve this recognition. The Chemicals Business of SRF won the coveted Deming Prize in 2012, joining a select group of organizations globally. The Chemicals Business of SRF has joined a select group of organisations globally to win the coveted Deming Prize. Awarded by the Union of Japanese Scientists and Engineers (JUSE), the Deming Prize award is considered the Nobel Prize equivalent in the world of quality. This was particularly remarkable as Earlier in 2004, SRF had earned the distinction of becoming the first tyre cord company outside Japan to win the award.

The decade ended with SRF commercializing more than 100 molecules, with another 50+ molecules at different stages of development. More than 400 people were engaged in R&D, engineering, and scale-ups. The company had filed over 300 patent applications in exotic and extreme chemistries. From a single-product tyre cord manufacturer, SRF had transformed into a diversified specialty products company with global reach.

So what for investors: The 1995-2010 period showcases the power of capability-led diversification. SRF didn't chase unrelated opportunities but systematically built adjacent businesses leveraging core competencies. This patient, capability-first approach created multiple growth engines while maintaining return on capital.

VI. The Ashish Bharat Ram Era: Transformation & Scale (2007-Present)

The board meeting on January 15, 2007, marked a generational transition. Ashish Bharat Ram, 47, was taking over as Managing Director from his father Arun, who would remain Chairman. The handover was smooth—Ashish had been groomed for years, heading various businesses, spending time in operations, understanding the culture. But everyone wondered: Could the son match the father's transformational legacy?

Ashish's first address to employees was telling. "My father built SRF from ₹5 crores to ₹2,000 crores. But that's not the benchmark. The question is: What does SRF need to become for the next generation? We're not competing with our past; we're competing with our potential."

Ashish Bharat Ram, Managing Director of SRF Ltd. named India's Best CEO in the emerging companies category by Business Today in January, 2021 But this recognition came after years of systematic transformation. Under his leadership, SRF Ltd. has grown into a major global conglomerate with operations in four countries across India, Thailand, South Africa, and Hungary covering Fluorochemicals, Specialty Chemicals, Packaging Films, Technical Textiles, Coated and Laminated Fabrics.

The first major decision under Ashish's leadership was counterintuitive. In 2008, as the global financial crisis decimated demand, most chemical companies were cutting capacity. Ashish saw opportunity. "Downturns are when you build competitive advantage," he told the board. "Our competitors are retrenching. If we expand now, we'll be ready when recovery comes."

SRF invested ₹500 crores in 2008-09, its highest capital expenditure ever during a downturn. A new specialty chemicals plant was built in Dahej, Gujarat. The Thailand film facility was expanded. R&D spending was increased, not cut. The bet paid off spectacularly—when demand recovered in 2010, SRF had capacity while competitors scrambled to restart mothballed plants.

The Dahej complex deserves special attention. Unlike Bhiwadi, which had grown organically into a sprawling site, Dahej was designed from scratch as an integrated chemical complex. The 400-acre site would eventually house multiple plants sharing utilities, waste treatment, and logistics infrastructure. The location offered proximity to Hazira port for exports, access to Gujarat's chemical ecosystem, and importantly, a supportive state government that understood chemical manufacturing.

But Ashish's most significant contribution was institutionalizing innovation. While Arun had built R&D capabilities, Ashish transformed them into a competitive weapon. The Chemicals Technology Group (CTG) was established as a separate entity, with its own P&L, serving both internal businesses and external customers. This structure ensured R&D wasn't just a cost center but a value creator.

The innovation philosophy shifted from "fast follower" to "first mover." Instead of waiting for customers to provide molecules, SRF began proposing new chemistries. The R&D team would identify patent expirations, anticipate generic requirements, and proactively develop processes. When customers were ready to source, SRF already had proven technology.

The acquisition of DuPont's Dymel® HFA 134a/P medical propellant business in January 2015 exemplified this new aggression. SRF acquired the Dymel® HFA 134a/P regulated medical pharmaceutical propellant business from DuPont™ in January 2015 and became one of the few manufacturers of Pharma grade HFA 134a/P in the world. This wasn't just buying assets—it was acquiring regulatory approvals, customer relationships, and most importantly, credibility in the highly regulated pharmaceutical propellant market.

The strategic focus on sustainability became a major differentiator under Ashish's leadership. As environmental regulations tightened globally, SRF positioned itself ahead of the curve. The company began developing next-generation refrigerants with lower Global Warming Potential (GWP). SRF's R&D teams are also committed to developing the next generation of fluorinated gases and has set up a pilot plant to manufacture HFO 1234yf. This breakthrough initiative will make SRF one of the few technology developers in the world to manufacture HFO 1234yf using indigenous technology, which is expected to find increasing use in car air-conditioning systems globally in future. In addition, the in-house technology will also allow SRF to manufacture, brand and sell HFO 1234yf in India and in global markets and develop other HFO refrigerants in future.

The "China Plus One" strategy, which gained prominence after 2018, had been anticipated by Ashish years earlier. SRF positioned itself as the alternative to Chinese suppliers for global companies seeking supply chain diversification. The pitch was compelling: Indian cost structure, global quality standards, English-language support, IP protection, and democratic governance. When US-China trade tensions escalated, SRF was ready to capture the opportunity.

The organizational transformation under Ashish was equally important. SRF had always been professionally managed, but Ashish took it further. Independent directors were given real power. The board was diversified with experts in chemicals, sustainability, and international business. Performance management systems were upgraded with clear KPIs and accountability. A leadership development program identified and groomed high-potential employees.

The digital transformation initiated in 2018 was another key initiative. While many saw digitalization as IT upgrades, Ashish viewed it as business transformation. Predictive maintenance using IoT sensors reduced unplanned downtime by 30%. AI-based process optimization improved yields by 5-10%. Digital twins of chemical plants enabled virtual experimentation. Customer portals provided real-time order tracking and technical support. The financial performance under Ashish's leadership tells the story. The consolidated revenue of the company increased 21% from ₹3,570 crore to ₹4,313 crore in Q4FY25 when compared with Corresponding Period Last Year. The company has demonstrated resilience through multiple cycles, with According to SRF Limited's latest financial reports the company's current revenue (TTM) is $1.62 Billion USD, an increase over the revenue in the year 2023 that were of $1.58 Billion USD.

The COVID-19 pandemic tested every aspect of Ashish's leadership. When India went into lockdown in March 2020, SRF faced an existential challenge. Chemical plants can't simply be switched off—reactors need temperature control, storage tanks need monitoring, effluent treatment must continue. Ashish made a bold decision: volunteer the Bhiwadi and Dahej plants as "continuous operation" facilities to the government, allowing workers to stay on-site in specially created quarantine bubbles.

The pandemic response showcased SRF's operational excellence. Workers voluntarily stayed at plants for weeks, sleeping in makeshift dormitories, separated from families. Management, including Ashish, regularly visited plants (following protocols) to boost morale. Not a single day of production was lost. When competitors struggled to restart, SRF captured market share, particularly in specialty chemicals where customers valued supply reliability above price.

The recent strategic moves under Ashish's leadership position SRF for the next decade of growth. The board approved investment for a pilot plant to manufacture next-generation refrigerant gas, HFO 1234yf—positioning SRF as the first technology developer outside US and Europe. The company has allocated capital to enter the fluoropolymers business, a natural adjacency to fluorochemicals but with significantly higher margins and technical barriers.

The cultural transformation under Ashish has been equally significant. SRF today feels more like a technology company than a traditional manufacturer. The average age of employees has dropped from 45 to 35. Engineers and scientists comprise 30% of the workforce versus 10% two decades ago. The company regularly recruits from IITs and international universities. Stock options, unusual in Indian manufacturing, are now part of compensation for key employees.

Ashish's most important contribution might be institutionalizing excellence. Arun Bharat Ram built SRF through personal drive and vision. Ashish has built systems and processes that don't depend on individual brilliance. The strategic planning process involves multiple stakeholders and scenario planning. The capital allocation framework clearly defines hurdle rates and payback requirements. The succession planning identifies multiple candidates for key positions.

On April 1, 2022, Ashish Bharat Ram was appointed as Chairman and Managing Director, completing the transition. His vision for SRF's future is ambitious yet grounded: "We want to be the partner of choice for complex chemistry. Not the biggest, but the best. Not in every molecule, but in molecules that matter."

So what for investors: The Ashish Bharat Ram era demonstrates how second-generation leaders can accelerate growth by institutionalizing capabilities built by founders. SRF's transformation from ₹2,000 crores to ₹15,000+ crores revenue under Ashish shows the power of combining inherited strengths with modern management practices.

VII. Global Leadership Positions & Competitive Moats

The conference call with a Fortune 500 pharmaceutical company in late 2023 captured SRF's evolved positioning perfectly. The customer's head of procurement opened with: "We're looking for an alternative to our Chinese supplier for a critical intermediate. But honestly, we're skeptical anyone can match their scale and cost." The SRF team's response was telling: "We're not trying to match Chinese scale. We're offering something different—reliability, innovation, and partnership. Let us show you."

SRF's global leadership positions today read like a carefully curated portfolio: Global no. 1 in Difluoro & Trifluoro Alkyl Intermediates, global no. 2 in Nylon 6 Tyre Cord, and global no. 3 in Belting Fabrics. Each position was built methodically over decades, but understanding the moats requires going beyond market share statistics.

Take the Difluoro and Trifluoro Alkyl Intermediates leadership. These tongue-twisting chemicals are critical building blocks for advanced pharmaceuticals and agrochemicals. The chemistry involves introducing fluorine atoms at specific positions in organic molecules—seemingly simple, actually fiendishly complex. Fluorine is the most electronegative element, making reactions violent and unpredictable. The intermediates often require cryogenic conditions, specialized reactors, and handling protocols that few companies master.

SRF's dominance stems from three interconnected advantages. First, cumulative learning—having run thousands of fluorination reactions over 30 years, they've seen every possible failure mode. Second, integrated infrastructure—from hydrogen fluoride production to waste treatment, everything happens within their complexes. Third, regulatory credentials—their facilities are approved by FDA, EU-GMP, and other global regulators, a process taking years and costing millions.

The refrigerants monopoly in India illustrates a different moat: regulatory timing. SRF is the only Indian manufacturer of ozone friendly refrigerants, namely F 134a and F 32, both of which it has developed using indigenous technology. When the Montreal Protocol mandated CFC phase-out, SRF moved immediately while competitors hesitated. By the time others recognized the opportunity, SRF had locked up technology, built capacity, and established customer relationships. With the addition of F 125, SRF is now the largest producer and seller of refrigerants in India.

But monopolies attract competition and regulatory scrutiny. SRF's strategy has been to stay ahead through innovation rather than protectionism. When Chinese players entered with HFC-32, SRF responded by developing blends with superior performance. When environmental concerns emerged about HFC's high global warming potential, SRF proactively developed HFO alternatives. The monopoly persists not through barriers but through continuous innovation.

The specialty chemicals CDMO (Contract Development and Manufacturing Organization) business represents SRF's newest moat: customer stickiness. Once a pharmaceutical or agrochemical company approves SRF for a molecule, switching suppliers requires re-qualification, stability studies, and regulatory re-filing—a process taking 18-24 months and costing millions. This creates enormous switching costs, especially for molecules already in commercial production.

The customer roster reads like a who's who of global chemicals: Bayer, Syngenta, BASF in agrochemicals; Pfizer, Merck, GSK in pharmaceuticals. But what's remarkable is the depth of these relationships. SRF doesn't just manufacture molecules; they're involved from early development through commercial production. When a customer is developing a new drug or pesticide, SRF's chemists work on process development years before commercial launch.

The China Plus One strategy has become SRF's most powerful tailwind, but it's often misunderstood. It's not just about companies reducing China dependence—it's about fundamental supply chain restructuring. Post-COVID, global companies realized that single-source dependence, regardless of country, is risky. They want multiple suppliers, in different geographies, with different risk profiles.

SRF positioned itself perfectly for this shift. Unlike Vietnam or Bangladesh which compete on cost, or Japan and Germany which compete on technology, SRF offers a unique combination: 70% of Chinese costs, 90% of Western quality, English-language support, democratic governance, and intellectual property protection. For companies seeking China alternatives, SRF often becomes the default choice.

The backward integration strategy deserves special attention. In chemicals, controlling raw materials is everything. SRF manufactures anhydrous hydrogen fluoride, the starting material for all fluorochemicals. They produce chloromethanes, intermediates for various products. They make their own utilities—steam, power, cooling water. This integration provides cost advantages, quality control, and most importantly, supply security when raw materials become scarce.

The technical capabilities moat is perhaps the deepest. With more than 400 people engaged in R&D and over 300 patent applications filed, SRF has built innovation capabilities rivaling much larger companies. But it's not just about numbers—it's about expertise in specific, difficult chemistries. Fluorination at -80°C. Reactions with elemental fluorine. Handling of explosive intermediates. These capabilities took decades to build and can't be quickly replicated.

The manufacturing excellence reflected in the Deming Prizes creates operational moats. SRF's batch failure rates are below 1%, compared to industry averages of 3-5%. Their capacity utilization exceeds 85%, versus 60-70% industry norms. These operational metrics translate directly to cost advantages and reliability that customers value. The HFO 1234yf development exemplifies SRF's evolution into a technology leader. The Board of Directors of SRF Ltd. approved an investment proposal for setting up of a pilot plant to manufacture next generation refrigerant gas, HFO 1234yf. The breakthrough initiative will make SRF the first technology developer outside US and Europe for manufacture of HFO 1234yf, which is expected to find increasing use in car air-conditioning systems globally in future. The in-house technology will also allow SRF to manufacture, brand and sell HFO 1234yf in India and in global markets and develop other HFO refrigerants in future.

The global supply chain positioning creates network effects. As SRF serves more global customers, it gains insights into emerging trends, upcoming molecules, and regulatory changes. This information advantage allows proactive capability building. When a new environmental regulation is proposed, SRF often has products ready before the regulation takes effect.

The sustainability moat is becoming increasingly important. Global customers face pressure to reduce supply chain emissions. SRF's investments in renewable energy, zero liquid discharge, and low-emission processes make them attractive to sustainability-conscious customers. The company's ESG ratings consistently rank among the highest in Indian chemicals, opening doors to customers with strict supplier requirements.

Myth vs Reality Box: Myth: SRF's leadership positions are primarily in niche, low-volume products. Reality: While specialized, these products are essential inputs for massive industries. The global market for fluorinated intermediates alone exceeds $10 billion. SRF's "niche" products often have better economics than commodity chemicals.

So what for investors: SRF's competitive moats are multilayered and reinforcing—technical expertise enables customer relationships, which fund R&D, which deepens expertise. These recursive advantages are extremely difficult for competitors to replicate, providing sustainable competitive advantages that should translate to consistent returns above cost of capital.

VIII. Business Unit Deep Dives

Fluorochemicals: The Crown Jewel

The Dahej fluorochemicals complex at 6 AM is a symphony of industrial precision. Steam plumes rise from cooling towers as the morning shift takes over. In the control room, operators monitor dozens of screens showing real-time data from thousands of sensors. A single parameter deviation triggers immediate alerts. This is where SRF manufactures products that literally keep the world cool—refrigerants that go into every air conditioner, refrigerator, and car cooling system.

Set up in the year 1989, SRF's Fluorochemicals Business (FCB) drives its work through the sale of refrigerants, pharma propellants, and industrial chemicals. The business has evolved far beyond simple refrigerant manufacturing. Today, it encompasses three distinct segments, each with unique dynamics and growth drivers.

The refrigerants portfolio remains the foundation. With the addition of F 125, SRF is now the largest producer and seller of refrigerants in India and has further consolidated its market leadership. But the real story is the evolution up the technology curve. From CFCs to HCFCs to HFCs, and now to HFOs, SRF has navigated every transition. Each generation required new chemistry, new equipment, new capabilities. Companies that missed one transition never recovered.

The pharma propellants business, acquired from DuPont in 2015, represents a different game entirely. SRF acquired the Dymel® HFA 134a/P regulated medical pharmaceutical propellant business from DuPont™ along with the technology to convert technical grade F 134a to the propellant grade. These aren't commodity chemicals—they're ultra-pure products going into metered dose inhalers for asthma patients. A single impurity could render medication ineffective or dangerous. The regulatory requirements are stringent, with FDA inspections, batch genealogy tracking, and extensive stability testing.

The industrial chemicals segment leverages the same fluorination capabilities for diverse applications. Chloromethanes for pharmaceuticals. Specialty solvents for electronics cleaning. Fluorinated intermediates for agrochemicals. Each product might be small volume, but margins often exceed 40%. The key is managing complexity—hundreds of products, different specifications, varying regulatory requirements.

Specialty Chemicals: The Growth Engine

The specialty chemicals plant in Dahej operates differently from fluorochemicals. Instead of continuous processes running for months, it's a campaign-based operation. This month, they're making an intermediate for a blockbuster herbicide. Next month, it could be a building block for a new cancer drug. Flexibility is everything.

The company entered the specialty chemicals business in 2004 as a supplier of fine chemicals to the agrochemicals and pharmaceuticals industry. The business model is fundamentally different from commodity chemicals. Customers come with a molecule and ask, "Can you make this?" SRF's chemists study the structure, design a synthetic route, optimize the process, and scale up production. The entire cycle from inquiry to commercial production typically takes 18-24 months.

The capabilities required are immense. Multi-step synthesis involving 10-15 sequential reactions. Handling of hazardous reagents like phosgene and hydrogen cyanide. Cryogenic reactions at -100°C. High-pressure hydrogenations. Photochemical reactions. Each capability opens doors to new molecules and customers. SRF has commercialized more than 100 molecules, with another 50+ molecules at different stages of development.

The customer concentration is deliberate. Rather than serving hundreds of small customers, SRF focuses on 20-30 global giants. These relationships go deep—SRF chemists work at customer R&D centers, understanding not just current needs but future pipelines. When a customer develops a new agrochemical, SRF is involved from the pilot stage, ensuring smooth scale-up when commercialization happens.

Packaging Films: Scale and Efficiency

The packaging films plant in Kashipur operates on a different scale altogether. Massive extruders melt polyester chips, creating sheets that are stretched simultaneously in two directions—hence "biaxially oriented." The resulting BOPET film is incredibly strong for its thickness, with excellent clarity and barrier properties. A single production line can produce enough film to wrap around the Earth in weeks.

The company started its packaging films business in 1995 when it acquired a BOPET film plant at Kashipur in India from Flowmore. SRF has since then manufactured both BOPET and BOPP films globally. The business has evolved from commodity films to specialized products. Metallized films for chip packets that need moisture barriers. Ultra-thin films for capacitors requiring precise electrical properties. Release films for adhesive applications needing specific surface chemistry.

The challenge in films is different from chemicals. It's a capital-intensive, scale-driven business where efficiency determines profitability. A 1% improvement in production yield or energy consumption can mean millions in savings. SRF's operational excellence, honed through decades of TQM implementation, provides the edge. Their production efficiency exceeds 95%, compared to industry averages of 85-90%.

Technical Textiles: The Heritage Business

The Manali plant where SRF began still manufactures tyre cord, but it's unrecognizable from the 1970s operation. Modern draw-winders create nylon yarns with precise properties. Weaving machines operate at speeds invisible to the human eye. Quality control systems detect defects measured in microns. This isn't traditional textile manufacturing—it's precision engineering with polymers.

SRF is the largest manufacturer of technical textiles in India. SRF's technical textile products contain tyre cord fabrics, belting fabrics, and industrial yarn. Despite being the oldest business, it continues to innovate. New products include fabrics for airbags, requiring burst strength and controlled porosity. Geotextiles for infrastructure projects. Specialty yarns for fishing nets that must withstand ocean conditions for years.

The strategic value of technical textiles goes beyond financial returns. It provides stable cash flows that fund growth in higher-margin businesses. The customer relationships built over decades create trust that opens doors in other businesses. The operational discipline required for consistent quality became the foundation for SRF's manufacturing excellence across all divisions.

Synergies: The Hidden Advantage

The real power of SRF's portfolio lies in synergies that aren't immediately obvious. The fluorochemicals business generates hydrogen fluoride as a byproduct, which becomes raw material for specialty chemicals. The packaging films business shares polymer expertise with technical textiles. Quality systems developed for one business are applied across all. R&D insights in one area spark innovations in another.

Infrastructure synergies are equally important. The Dahej complex houses both fluorochemicals and specialty chemicals, sharing utilities, waste treatment, and logistics. This reduces capital investment by 20-30% compared to standalone facilities. Environmental compliance, increasingly expensive and complex, is managed centrally with expertise applied across businesses.

Customer synergies are perhaps most valuable. A relationship that starts with refrigerants can expand to specialty chemicals. A packaging films customer might need technical textiles. Global companies appreciate dealing with a single supplier for multiple needs, simplifying procurement and ensuring consistent quality standards.

The portfolio also provides resilience. When refrigerant prices crashed in 2019 due to Chinese oversupply, specialty chemicals compensated with record profits. When COVID impacted technical textiles demand, packaging films boomed as e-commerce exploded. This wasn't planned diversification—it emerged from pursuing adjacent opportunities. But the result is a business that can weather cycles better than focused competitors.

So what for investors: Understanding SRF's individual businesses is important, but the real value lies in the portfolio construction. Each business has different growth rates, margin profiles, and cyclicality. Together, they create a resilient platform for consistent value creation. Investors should evaluate SRF as an integrated chemicals platform, not a collection of separate businesses.

IX. Recent Strategic Moves & Future Bets

The board presentation in March 2024 was unusually detailed. Ashish Bharat Ram walked directors through molecular diagrams, market projections, and technology roadmaps. The proposal: invest ₹2,000 crores over three years in fluoropolymers, a completely new business for SRF. "This isn't diversification," Ashish emphasized. "It's the logical culmination of 35 years in fluorine chemistry."

The company has allocated capital to enter the fluoropolymers business, marking SRF's most ambitious expansion since entering chemicals. Fluoropolymers—think Teflon and its cousins—represent a $7 billion global market growing at 6-7% annually. They're used in everything from non-stick cookware to semiconductor manufacturing, from medical devices to aerospace components. The technology barriers are formidable, which is precisely why SRF is interested.

The fluoropolymer entry strategy reflects lessons from three decades of chemical expansion. Rather than competing in commodity PTFE dominated by Chinese producers, SRF is targeting specialty grades: modified PTFE for automotive applications, FEP for wire insulation, PFA for semiconductor equipment. Each requires different polymerization techniques, processing methods, and quality standards. But fundamentally, they're extensions of fluorine chemistry that SRF has mastered.

The HFO development continues to progress. Furthermore, SRF's R&D teams are also committed to developing the next generation of fluorinated gases and has set up a pilot plant to manufacture HFO 1234yf. This breakthrough initiative will make SRF one of the few technology developers in the world to manufacture HFO 1234yf using indigenous technology. But SRF isn't stopping at 1234yf. The R&D team is working on HFO blends for commercial refrigeration, heat pump applications, and specialized cooling for data centers.

The sustainability transformation goes beyond products. SRF has committed to carbon neutrality by 2035, ambitious for a chemical company. Solar installations now cover 20% of energy needs. Waste heat recovery systems capture energy from exothermic reactions. More radically, SRF is exploring electrochemical fluorination, potentially eliminating the need for hydrogen fluoride—dangerous to handle and environmentally problematic.

The BOPP-BOPE films facility in Indore represents a different bet: sustainable packaging. BOPE (Biaxially Oriented Polyethylene) films are recyclable, unlike traditional multi-layer laminates. As brands face pressure to reduce plastic waste, demand for mono-material packaging solutions is exploding. SRF's new facility, operational by 2025, will be among the first in India to offer both BOPP and BOPE from a single location.

Digital transformation initiatives, often overlooked in chemical companies, are yielding surprising returns. AI models now predict equipment failures three weeks in advance, preventing unplanned shutdowns. Machine learning algorithms optimize reaction conditions in real-time, improving yields by 2-3%—seemingly small but worth crores annually. Digital twins of chemical plants allow virtual experimentation, reducing physical trial runs by 60%.

The specialty chemicals expansion is accelerating. Three new multi-purpose plants are under construction, each designed for maximum flexibility. Unlike dedicated plants for single products, these can manufacture dozens of different molecules by reconfiguring equipment. This allows SRF to say "yes" to more customer requests while maintaining capital efficiency.

Geographic expansion is taking new forms. Instead of building plants globally, SRF is creating "virtual manufacturing networks" through partnerships. A toll manufacturing agreement in Europe provides local presence without capital investment. A joint venture in China (minority stake, protecting IP) offers market access while managing risk. These asset-light models preserve capital for core investments while expanding market reach.

The R&D strategy is evolving from reactive to proactive. Instead of waiting for customer requests, SRF now anticipates needs. The team monitors patent expirations, identifying molecules going off-patent in 3-5 years. Process development starts immediately, so when generic opportunities emerge, SRF is ready with proven technology. This forward-looking approach has already secured contracts for molecules not yet commercialized.

ESG initiatives, once seen as compliance costs, are becoming competitive advantages. SRF's water recycling achieves 90% recovery, crucial in water-stressed regions. The zero liquid discharge systems, while expensive, eliminate effluent-related risks that have shuttered competitor plants. Green chemistry initiatives—using bio-based solvents, avoiding hazardous reagents—appeal to sustainability-conscious customers willing to pay premiums.

The capital allocation framework has become more sophisticated. Each investment is evaluated not just on IRR but on strategic value: Does it deepen customer relationships? Does it build new capabilities? Does it create options for future growth? This options-based thinking led to the fluoropolymer decision—the immediate returns might be modest, but it opens doors to high-value applications in semiconductors, EVs, and renewable energy.

Risk management has evolved from defensive to strategic. Supply chain mapping now extends to tier-3 suppliers, identifying vulnerabilities before they become problems. Dual sourcing is mandatory for critical raw materials. Inventory policies balance working capital efficiency with supply security. Currency hedging strategies protect margins while allowing upside participation. These might seem like operational details, but they're what enable SRF to make bold strategic bets while managing downside risks.

The organizational capability building continues. SRF has partnered with IITs for advanced research, creating PhD programs where students work on company-specific problems. Mid-career hiring brings expertise from global chemical companies. Leadership development programs identify high-potential employees early, rotating them through businesses and functions. The goal isn't just growing the business but building an institution that outlasts any individual.

So what for investors: SRF's recent strategic moves reveal a company transitioning from fast follower to innovation leader. The fluoropolymer entry, HFO development, and sustainability investments require patient capital but offer asymmetric upside. Investors should evaluate these bets not on immediate returns but on option value—the possibilities they create for future growth.

X. Playbook: Business & Investment Lessons

The Power of Backward Integration in Chemicals

The visiting MBA students at SRF's Bhiwadi plant in 2023 asked the obvious question: "Why make your own hydrogen fluoride? Wouldn't it be easier to just buy it?" The plant manager's response was illuminating: "In 2018, when global HF supply tightened, prices tripled overnight. Our competitors shut down. We kept running. That quarter alone justified twenty years of investment in backward integration."

SRF's backward integration strategy offers a masterclass in strategic thinking. It's not about making everything in-house—that's inefficient. It's about controlling critical nodes in the value chain where supply disruptions or price volatility can cripple operations. Hydrogen fluoride for fluorochemicals. Chloroform for refrigerants. Trichloroethylene for HFC-134a. Each backward integration decision followed careful analysis: Is supply concentrated? Are there technical barriers to entry? Does it provide cost advantages beyond supply security?

The real lesson: backward integration in chemicals isn't just about economics—it's about optionality. When you control raw materials, you can pursue opportunities others can't. SRF could commit to long-term customer contracts because they controlled their supply chain. They could develop new products requiring specific raw material modifications. They could even sell intermediates to competitors during shortages, turning a defensive strategy into a profit center.

Managing Family Businesses: Separation vs. Collaboration

The Bharat Ram family's approach to business offers a counternarrative to typical family business sagas. Instead of bitter feuds and value destruction, they executed two major splits—1989 and 1999—without destroying relationships or businesses. The secret wasn't legal structures but philosophical alignment: separating business ownership while maintaining family bonds.

"Managing the family is as important as managing the business," Arun Bharat Ram's insight goes deeper than it appears. He instituted formal governance before it was fashionable: family councils separate from boards, clear succession policies, professional CEOs in operating roles. Family members wanting to join had to qualify like any employee. Those not interested in operations received dividends but not positions.

The transition to Ashish illustrates evolved thinking. Unlike typical successions announced suddenly, Ashish's elevation was telegraphed years in advance. He worked in every division, spent time in factories, understood operations before strategy. When he became MD in 2007, employees saw continuity, not disruption. The lesson: successful family business transitions are processes, not events.

Timing Market Transitions

SRF's history is essentially a series of well-timed transitions. Montreal Protocol and refrigerants. China Plus One and specialty chemicals. Sustainability concerns and HFOs. Each time, SRF moved before the transition was obvious, capturing first-mover advantages. But how did they consistently time these moves?

The answer lies in their market sensing capabilities. SRF executives spend 30% of their time with customers, understanding not just current needs but future concerns. They participate in industry associations, tracking regulatory developments years before implementation. They maintain relationships with academics and consultants who provide early signals of change. This isn't genius-level foresight—it's systematic information gathering and pattern recognition.

The key insight: major transitions are rarely sudden. The Montreal Protocol was signed in 1987 but implementation took years. China's environmental crackdowns were telegraphed through five-year plans. ESG concerns built gradually before becoming boardroom priorities. Companies that track weak signals and prepare accordingly can position themselves ahead of discontinuities.

Building R&D Capabilities in Emerging Markets

Conventional wisdom suggests emerging market companies should focus on low-cost manufacturing while developed countries handle innovation. SRF's R&D journey challenges this narrative. With more than 400 people engaged in R&D and 300+ patent applications, they've built innovation capabilities rivaling global leaders. How?

First, they started with application development, not basic research. Modifying products for local conditions. Solving customer-specific problems. This built practical expertise and customer trust. Second, they hired strategically—PhDs from top institutes for fundamental research, experienced professionals from MNCs for applied development. Third, they invested in infrastructure—analytical equipment, pilot plants, safety systems—even when utilization was low initially.

The crucial lesson: R&D capability in emerging markets isn't built through moonshot projects but through accumulation of incremental innovations. Each solved problem builds expertise. Each successful project funds further investment. Each patent filed builds confidence. Over time, these compound into genuine innovation capabilities.

Adjacent Business Expansion Strategy

SRF's expansion from tyre cord to chemicals to films might seem random, but there's an underlying logic: capability-based adjacencies. Technical textiles required polymer chemistry, which enabled packaging films. Refrigerants required fluorine handling, which enabled fluorochemicals. Each expansion leveraged existing capabilities while building new ones.

The discipline is in what SRF didn't do. Despite opportunities, they didn't enter pharma manufacturing (different regulatory requirements). They avoided commodity chemicals despite scale advantages (different success factors). They stayed away from consumer products despite brand strength (different go-to-market). The lesson: successful adjacency expansion leverages core capabilities while recognizing boundaries.

Capital Allocation in Cyclical Businesses

Chemical businesses are inherently cyclical, but SRF has delivered consistent returns through cycles. Their capital allocation framework is sophisticated yet practical. During upturns, resist the temptation to over-expand; instead, strengthen balance sheets and fund R&D. During downturns, when competitors retrench, selectively expand capacity and capabilities.

The 2008 financial crisis investment program exemplifies this thinking. While competitors conserved cash, SRF invested ₹500 crores in new capacity. When recovery came, they had capacity while competitors scrambled. The 2020 pandemic response was similar—maintaining investment while others cut. This countercyclical approach requires financial strength and organizational courage but creates lasting advantages.

The portfolio approach to capital allocation is equally important. High-return but volatile specialty chemicals. Steady but lower-return packaging films. Capital-intensive but strategic backward integration. Each business has different capital needs and return profiles. Managing them as a portfolio—rather than optimizing each independently—creates resilience and consistent value creation.

So what for investors: SRF's playbook offers lessons beyond chemicals. The principles—capability-based expansion, countercyclical investment, patient R&D building—apply across industries. For investors, the implication is clear: companies following these principles might appear suboptimal in the short term but create substantial long-term value.

XI. Analysis & Bear vs. Bull Case

The Bull Case: Structural Winners in Chemical Transition

The bull thesis on SRF starts with a simple observation: the global chemical industry is undergoing its most significant restructuring in decades. Environmental regulations in China. Supply chain diversification post-COVID. Sustainability requirements from customers. Each trend benefits established players with proven capabilities, regulatory approvals, and customer relationships. SRF sits at the intersection of all three.

The monopolistic positions in Indian refrigerants provide a cash flow foundation that bulls find compelling. SRF is the only Indian manufacturer of ozone friendly refrigerants, with F 134a and F 32 developed using indigenous technology. With the addition of F 125, SRF is now the largest producer and seller of refrigerants in India. In a country where air conditioning penetration is still below 10% compared to 90%+ in developed markets, the growth runway extends decades. Every percentage point increase in AC penetration translates directly to SRF's top line.

The China Plus One opportunity is perhaps even larger. Global chemical companies aren't just reducing China dependence—they're fundamentally restructuring supply chains. SRF's sweet spot—complex chemistry requiring technical expertise but not massive scale—is exactly what companies want to move from China. The specialty chemicals order book, growing at 20%+ annually, validates this thesis.

Technical moats continue deepening. Fluorination chemistry expertise took decades to build and can't be easily replicated. Customer relationships, particularly in regulated industries like pharmaceuticals, create switching costs measured in years and millions of dollars. The patent portfolio, while not blocking competition entirely, provides breathing room to maintain margins.

Bulls point to management quality as an underappreciated asset. The successful navigation of family business dynamics. The prescient strategic pivots. The capital allocation discipline through cycles. The ability to attract and retain technical talent. In industries where execution matters as much as strategy, management quality translates directly to shareholder returns.

The valuation argument is compelling in the bull framework. SRF trades at a meaningful discount to global specialty chemical peers despite similar or superior growth rates and margins. As Indian capital markets mature and global investors increase emerging market allocations, this valuation gap should narrow, providing rerating potential beyond fundamental growth.

The Bear Case: Cyclical Risks and Structural Challenges

Bears start with cyclicality. Chemical businesses are inherently volatile—demand fluctuates with economic cycles, supply additions create periodic oversupply, raw material costs swing wildly. In 2024, SRF Limited's revenue was 146.93 billion, an increase of 11.83% compared to the previous year's 131.39 billion. Earnings were 12.51 billion, a decrease of -6.36%. This earnings decline despite revenue growth illustrates the margin pressure that concerns bears.

Chinese competition looms large in the bear thesis. While China Plus One benefits SRF today, Chinese chemical companies aren't standing still. They're moving up the value chain, improving quality, and increasingly competing in specialty products. Their cost advantages—scale, government support, integrated complexes—remain formidable. When Chinese demand recovers, global oversupply could pressure margins across SRF's portfolio.

Regulatory risks multiply with each business line. Refrigerants face continuous environmental scrutiny—HFCs are being phased out just as SRF completes HFC investments. Specialty chemicals for agrochemicals face increasing restrictions in Europe and North America. Packaging films confront plastic waste regulations. Each regulatory change requires investment, often without commensurate returns.