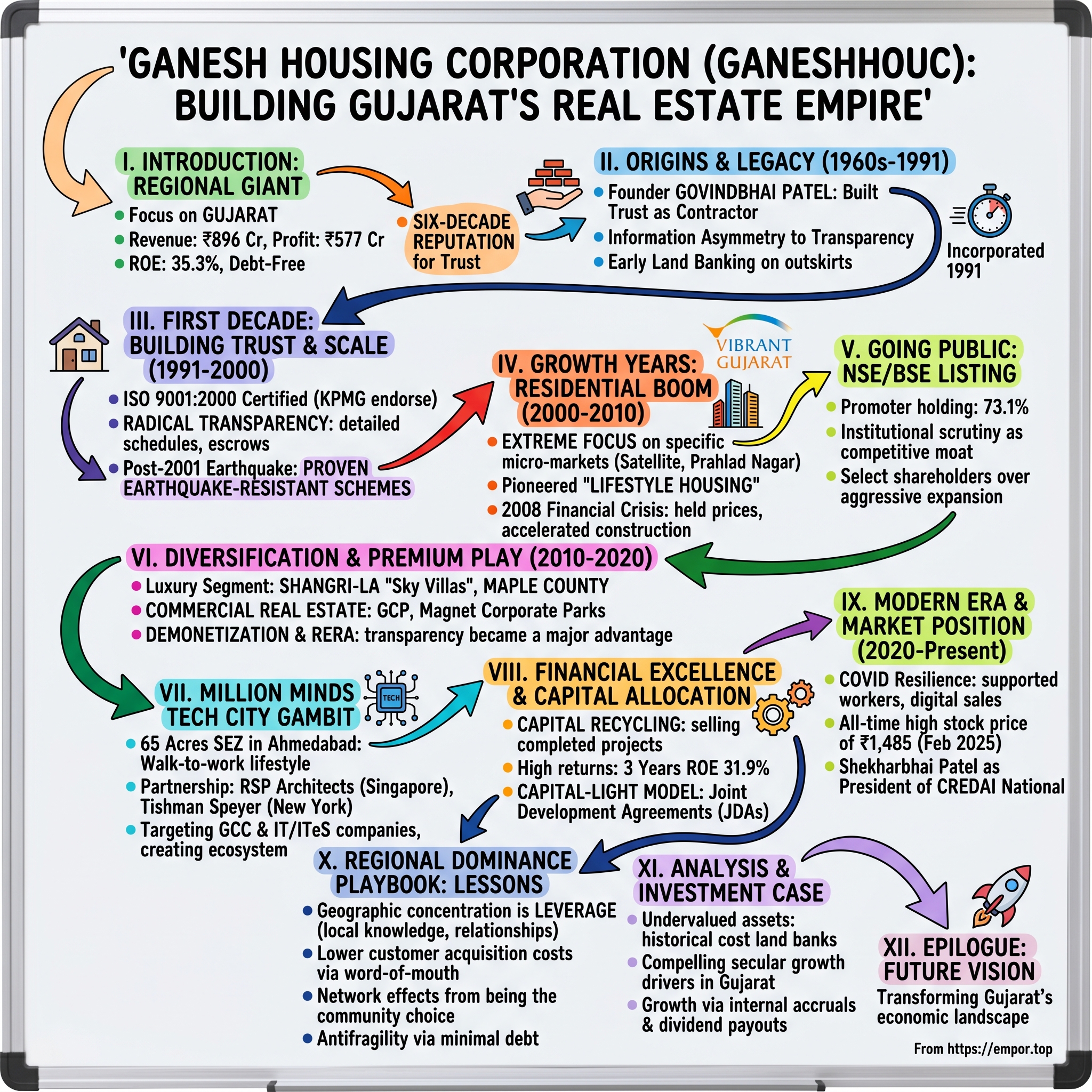

Ganesh Housing Corporation: Building Gujarat's Real Estate Empire

I. Introduction & Episode Roadmap

Picture this: A dusty construction site in 1960s Ahmedabad. A young Govindbhai Patel stands amid bamboo scaffolding and hand-mixed concrete, watching laborers carry bricks on their heads. The city is transforming—textile mills humming, businesses sprouting—but housing remains chaotic, unorganized, a maze of informal builders and uncertain quality. Govindbhai sees something others don't: the opportunity to bring order, trust, and scale to Gujarat's housing market.

Fast forward to 2025. That vision has morphed into Ganesh Housing Corporation—a ₹7,142 crore market cap giant that has sold over 22 million square feet of real estate with another 35 million square feet in the pipeline. The company posts eye-popping numbers: ₹896 crore in revenue, ₹577 crore in profit, ROE of 35.3%, and virtually debt-free operations. In an industry notorious for leverage and boom-bust cycles, Ganesh Housing runs like a Swiss watch.

But here's what makes this story remarkable: While national real estate titans expanded aggressively across India, often stumbling on execution and debt, Ganesh Housing stayed laser-focused on Gujarat. They turned regional concentration—what most investors would call a weakness—into their greatest strength. They didn't just build homes; they built a six-decade reputation that let them command premium prices in a commodity business. How does a company transform construction—one of the world's most cyclical, capital-intensive, and relationship-dependent industries—into a machine that generates 35% returns on equity? The answer lies not in what Ganesh Housing built, but in how they chose not to build.

This episode explores a counterintuitive playbook: While peers chased national expansion and leveraged growth, Ganesh Housing doubled down on a 200-kilometer radius around Ahmedabad. While others fought price wars, they commanded premiums. While the industry binged on debt, they ran virtually debt-free. The result? Revenue of ₹896 Cr and profit of ₹577 Cr, with metrics that would make a software company jealous.

We'll trace this journey from post-independence India's construction chaos through the digital age, uncovering how a regional player built competitive moats that national giants couldn't breach. Along the way, we'll examine the economics of land banking, the art of capital allocation in real estate, and why sometimes the best growth strategy is knowing exactly where to stop growing.

Ready? Let's dive into how Ganesh Housing built Gujarat's real estate empire—one carefully chosen project at a time.

II. Origins & The Patel Legacy (1960s–1991)

The year is 1965. Ahmedabad's textile mills are running three shifts, their chimneys painting the sky gray with prosperity. The city—once Gandhi's headquarters for India's independence movement—is transforming into Gujarat's commercial heart. But amid this industrial boom, a peculiar problem emerges: Where do all these workers live?

Into this chaos steps Govindbhai C. Patel, not with grand ambitions of empire-building, but with a simple observation. Late Shree Govindbhai C. Patel embarked on this remarkable journey in the 1960s, when construction in India meant something entirely different than today. No organized developers. No mortgage markets. No building codes worth mentioning. Just informal contractors, cash transactions, and a handshake economy where your word was your bond—if you were lucky.

Govindbhai didn't start by building houses. He started by building trust. In those early years, he worked as a civil contractor, taking on government projects, industrial construction, whatever paid the bills. But he noticed something: While factories were being built with precision and planning, housing remained haphazard. A textile worker might save for years only to get cheated by a fly-by-night builder. A middle-class family might buy land but never see construction begin.

The construction industry of 1960s India operated on what economists call "information asymmetry"—buyers knew nothing, sellers knew everything, and the gap between them was where fortunes were made and lost. Govindbhai saw opportunity not in exploiting this gap, but in bridging it.

By the 1970s, his reputation had spread through Ahmedabad's business community. "Govindbhai no problem nathi"—there's no problem with Govindbhai—became a common refrain. He delivered projects on time, didn't inflate costs midway, and most importantly, didn't disappear after collecting advances. In an industry where trust was scarce, he was accumulating it like compound interest.

The 1980s brought liberalization whispers and economic optimism. Gujarat, always India's entrepreneurial heartland, was buzzing with new energy. The state government launched industrial estates. The middle class expanded. And suddenly, housing wasn't just about shelter—it was about aspiration. Families didn't just want four walls; they wanted addresses that announced their arrival in India's emerging prosperity.

Govindbhai recognized this shift before most. He began transitioning from pure construction to development, buying land parcels in what were then Ahmedabad's outskirts. His peers thought he was crazy—why buy agricultural land when the city's boundaries seemed fixed? But he understood something fundamental: Cities don't grow linearly; they grow in sudden spurts when infrastructure catches up to ambition.

On June 13, 1991, Ganesh Housing Corporation Ltd was incorporated, marking the formal beginning of what would become one of India's most profitable real estate companies. The timing was no accident. India was weeks away from its historic economic liberalization. The License Raj was crumbling. Private enterprise was about to be unshackled.

But the company's initial avatar seems almost quaint in retrospect—it started as Ganesh Housing Finance Corporation Limited, focusing on housing finance rather than construction. This wasn't a pivot; it was strategic positioning. In 1991, India's housing finance market was dominated by a few large players. By entering finance first, Govindbhai was learning the customer's perspective—understanding how families thought about their biggest financial decision.

The name itself—Ganesh, the remover of obstacles—wasn't just religious symbolism. It was a promise. In an industry full of obstacles (regulatory, financial, operational), the company positioned itself as the entity that would clear the path to homeownership.

What Govindbhai built in those pre-incorporation decades wasn't just a construction business. He built something far more valuable: a network of relationships, a reputation for reliability, and most critically, an understanding that in real estate, you're not selling property—you're selling trust. This foundation would prove invaluable when the company began its transformation from a local contractor to a listed corporation.

The lesson from these origin years is profound: In industries where trust is scarce, accumulating it slowly can be more valuable than accumulating capital quickly. While others rushed to scale, Govindbhai spent three decades building something that couldn't be replicated with money alone—credibility.

As India entered the 1990s, the stage was set. The economy was opening up, the middle class was expanding, and urbanization was accelerating. Ganesh Housing had spent 30 years preparing for a moment that was about to arrive. The question wasn't whether they could build homes—they'd proven that. The question was whether they could build a company that would outlast its founder.

III. The First Decade: Building Trust & Scale (1991–2000)

The conference room at Ganesh Housing's modest Ahmedabad office, January 26, 2001, 8:46 AM. The earth suddenly lurches sideways. Tea cups crash to the floor. For 90 seconds that feel like hours, the 7.7 magnitude Bhuj earthquake reshapes Gujarat's landscape—and its construction industry—forever. When the dust settles, over 20,000 are dead, 167,000 injured, and a million homes destroyed. But in this tragedy, Ganesh Housing sees not opportunity for profit, but responsibility for transformation.

Let's rewind to 1991. The newly incorporated Ganesh Housing Finance Corporation Limited faced an identity crisis from day one. Were they a finance company that happened to do construction, or a construction company that happened to do finance? The answer would define their trajectory.

The early 1990s Indian real estate market was the Wild West. No Real Estate Regulatory Authority (RERA). No standardized agreements. No consumer protection. Builders routinely collected money for projects that existed only on paper. Delivery delays were measured in years, not months. Quality? That was whatever the builder decided after taking your money.

Ganesh Housing's initial finance focus gave them unique insights. They saw families getting rejected for loans because projects lacked proper approvals. They watched customers struggle with builders who demanded cash payments to avoid taxes. They understood the gap between what customers needed and what the industry offered.

By 1993, the pivot was clear: They would become developers, but different ones. The company began acquiring land parcels strategically, focusing on areas where they could control the entire development process. No joint ventures with unreliable partners. No dependence on external contractors who might compromise quality. Vertical integration before it became a buzzword.

The company obtained ISO 9001:2000 certification, endorsed by KPMG, USA—a remarkable achievement for a regional player in the 1990s. Think about what this meant: While competitors operated on informal systems and paper ledgers, Ganesh Housing was implementing international quality standards. They were documenting processes, standardizing procedures, creating systems that could scale.

The certification wasn't just about impressing customers. It was about internal discipline. Every project had defined milestones. Every vendor had quality parameters. Every customer complaint had a resolution timeline. In an industry that ran on "we'll see" and "adjust kar lenge," Ganesh Housing was building an operating system.

But systems alone don't build trust. The company's masterstroke was transparency—radical for its time. While competitors hid behind complex payment structures and vague timelines, Ganesh Housing published detailed project schedules. They invited customers to site visits. They created escrow accounts for customer advances—unheard of in 1990s India.

The results were immediate. Word-of-mouth became their primary marketing engine. "Ganesh Housing ma book karo, tension nahi"—book with Ganesh Housing, no tension—became common advice in Ahmedabad's middle-class communities. Customers began booking flats in new projects sight unseen, purely based on the company's track record.

Then came January 26, 2001. The Bhuj earthquake didn't just destroy buildings; it destroyed faith in construction quality. Suddenly, everyone was asking: Is my building safe? Will it survive the next earthquake? The Gujarat government mandated new construction standards. The market shifted overnight from price-consciousness to safety-consciousness.

Ganesh Housing was among pioneers in utilizing earthquake-resistant schemes in projects. But here's what's remarkable: They'd started implementing these measures before the earthquake. Not because regulations required it—they didn't. Not because customers demanded it—they didn't know to ask. But because the company understood that cutting corners on structural safety was borrowing from the future.

Post-earthquake, while competitors scrambled to understand new building codes, Ganesh Housing was already compliant. They turned their foresight into marketing gold, becoming the "safe choice" in a suddenly safety-obsessed market. Projects launched in 2001-2002 sold out in weeks, not months.

The earthquake also triggered another transformation: the professionalization of Gujarat's real estate market. Fly-by-night operators couldn't meet new standards. Customers became more discerning. Banks became stricter about project approvals. The industry began consolidating around serious players—exactly the environment where Ganesh Housing thrived.

By decade's end, the company had built over 2 million square feet, established relationships with major banks, and more importantly, created a template for organized real estate development in Gujarat. They'd proven that you could run a real estate company like a manufacturing business—with systems, standards, and predictability.

The lesson from this decade is counterintuitive: In chaotic markets, discipline is a differentiator. While competitors chased quick profits through shortcuts, Ganesh Housing invested in systems and standards that seemed like overhead at the time but became competitive moats when the market matured.

As the new millennium dawned, India was changing. The IT boom was creating wealth. Nuclear families were replacing joint families. Urbanization was accelerating. And in Gujarat, a new chief minister named Narendra Modi was about to launch an economic transformation that would supercharge the state's growth. Ganesh Housing had spent a decade building credibility and capability. Now it was time to scale.

IV. The Growth Years: Residential Boom (2000–2010)

October 2003, Vibrant Gujarat Summit, Mahatma Mandir. A young CEO from Bangalore steps up to the podium, slightly bewildered. He'd come expecting the usual government summit—long speeches, longer delays, and promises that evaporate with the evening tea. Instead, he's signing an MOU for a 500-crore IT park. Within six months, construction begins. Within two years, his company is operational. Word spreads through India Inc: Gujarat means business.

This anecdote captures the transformation that supercharged Ganesh Housing's growth decade. Under new leadership, Gujarat wasn't just growing—it was being reimagined. "Minimum Government, Maximum Governance" wasn't just a slogan; it was creating an economic miracle that would transform Ahmedabad from a textile town to a metropolitan powerhouse.

For Ganesh Housing, the timing was perfect. They'd spent the 1990s building systems and credibility. Now, a tsunami of demand was coming. Gujarat's GDP grew at 10%+ annually. Ahmedabad's population swelled from 3.5 million to 5.5 million. The IT corridor along SG Highway emerged from farmland. The city needed homes—lots of them, fast, and built to international standards.

But here's where Ganesh Housing's strategy diverged from competitors. While others rushed to launch projects everywhere, Ganesh Housing made a counterintuitive choice: extreme focus. They identified specific micro-markets within Ahmedabad where they could dominate—Satellite, Prahlad Nagar, Bodakdev, Thaltej. Instead of being a small player in many markets, they became the dominant player in select markets.

The economics were brilliant. By concentrating projects in specific areas, they achieved economies of scale in everything—land acquisition, construction materials, labor deployment, marketing. Their project managers could oversee multiple sites within a 5-kilometer radius. Their reputation in these areas became so strong that projects sold through word-of-mouth alone.

Take their Satellite area developments. Between 2003-2007, Ganesh Housing built over 3,000 units in a 2-square-kilometer area. They didn't just build apartments; they shaped the neighborhood. They influenced where commercial complexes came up, where schools opened, where banks placed branches. They weren't just developers; they were micro-urban planners.

The company also pioneered what they called "lifestyle housing" in Gujarat—a concept that seems obvious now but was revolutionary then. Middle-class Indian housing had traditionally meant maximum square footage for minimum price. Amenities were afterthoughts. Ganesh Housing flipped this: They offered slightly smaller apartments but with amenities previously reserved for luxury projects—swimming pools, gyms, landscaped gardens, children's play areas.

The market response was electric. Their 2005 project in Prahlad Nagar—offering 2/3 BHK apartments with a clubhouse—sold out in 72 hours. Pre-launch bookings became frenzied affairs with customers camping outside sales offices. The company could have exploited this demand through price gouging. Instead, they used it to improve terms—reducing construction-linked payments, offering clearer contracts, providing better finish quality.

Competition was intensifying. National players like DLF and Unitech were eyeing Gujarat's boom. Local players were scaling aggressively with private equity funding. The market was getting crowded. But Ganesh Housing had an advantage others couldn't replicate: three decades of local relationships.

When prime land parcels came up for sale, Ganesh Housing often knew before others—not through insider information, but through relationships with farmers, brokers, and government officials built over generations. When customers chose between similar projects, Ganesh Housing won—not through price cuts, but through trust accumulated over decades.

The 2008 global financial crisis tested everyone. Real estate markets across India froze. Projects stalled. Developers defaulted. But Gujarat's economy, driven by manufacturing and domestic consumption rather than IT exports, weathered the storm better. And Ganesh Housing, with its conservative leverage and strong cash flows, didn't just survive—it thrived.

While competitors desperately offered 20-30% discounts, Ganesh Housing held prices with minor adjustments. While others stopped construction to conserve cash, Ganesh Housing accelerated, taking advantage of lower material costs. While banks became wary of real estate exposure, they continued lending to Ganesh Housing based on their track record.

By 2010, the company had transformed from a local builder to Gujarat's premier residential developer. They'd built over 10 million square feet, housed over 50,000 families, and more importantly, created a brand that commanded premium pricing in a commodity business.

The lesson from this decade: In boom times, discipline matters more than growth. While competitors leveraged up to chase every opportunity, Ganesh Housing grew selectively, maintaining the operational excellence and financial conservatism that would prove invaluable in the next phase—going public.

The Indian real estate industry was about to face its biggest transformation yet—regulatory oversight, transparency requirements, and public market scrutiny. Most developers would struggle with this transition. Ganesh Housing was about to show why building trust slowly pays off exponentially when markets demand transparency.

V. Going Public: The NSE/BSE Listing Story

March 2010, a mahogany-paneled boardroom in Mumbai's Bandra-Kurla Complex. Investment bankers from a bulge bracket firm are making their pitch to Ganesh Housing's board. "Sir, we'll value you at 3x book value, maybe 4x if markets are hot. But you'll need to change everything—your disclosure practices, capital structure, maybe even your business model. Markets don't understand regional players."

Shekhar Patel, who'd taken over leadership from his father, listens patiently. Then responds: "What if we don't want markets to understand us? What if we want to select our shareholders as carefully as we select our projects?"

This exchange captures the philosophical divide that Ganesh Housing had to bridge. One of the first real estate developers to be listed on both NSE and BSE, they weren't just accessing capital markets—they were attempting something far more audacious: proving that a regional, family-run, conservative real estate company could thrive under public scrutiny.

The Indian real estate sector's relationship with capital markets had been tumultuous. DLF's 2007 IPO, India's largest at the time, had ended in tears with the stock falling 80% from its peak. Unitech, Parsvnath, Omaxe—the graveyard of destroyed shareholder value was littered with real estate companies that had promised the moon and delivered dust.

The problem was structural. Real estate companies wanted public capital but private operations. They wanted premium valuations but wouldn't provide basic transparency. They wanted growth capital but wouldn't explain how they'd deploy it. Markets, burned repeatedly, had become deeply cynical about the sector.

Ganesh Housing took a radically different approach. Instead of hiring investment bankers to "dress up" the company for listing, they spent two years internally preparing for public life. They hired Big Four auditors not just for the IPO but for regular operations. They implemented SAP when Excel would have sufficed. They created board committees before regulations required them.

Most remarkably, they began voluntarily disclosing information that regulations didn't require. Project-wise sales data. Construction progress reports. Land bank details with acquisition costs. The logic was simple: If you're hiding nothing, why not show everything?

The IPO roadshow was unlike anything bankers had seen. Instead of promising aggressive expansion into new cities (the standard pitch), Ganesh Housing promised to stay focused on Gujarat. Instead of projecting hockey-stick growth, they showed steady, sustainable expansion. Instead of complex financial engineering, they presented a simple business model: buy land, build homes, sell them, repeat.

Institutional investors were skeptical initially. "No pan-India presence? No commercial real estate? No township projects? What's the growth story?" But as they dug deeper, they discovered something unusual: a real estate company that actually generated cash, maintained low debt, and delivered projects on time.

The retail investor response was extraordinary. In Ahmedabad, the IPO became a cultural phenomenon. Families that had bought Ganesh Housing homes wanted to own the stock. It wasn't just investment; it was validation of their housing choice. The grey market premium reached levels that made bankers nervous—what if the stock fell post-listing and destroyed this carefully built credibility?

It didn't. The stock's post-listing performance validated the company's approach. While other real estate stocks gyrated wildly with market cycles, Ganesh Housing showed remarkable stability. The reason was simple: their shareholder base wasn't trading volatility; they were investing in a business they understood.

Promoter holding at 73.1% sent another powerful signal. The founding family wasn't cashing out; they were inviting co-owners. This alignment of interests—rare in Indian real estate—created trust that translated into valuation premiums.

Being public brought unexpected benefits. Banks, always wary of lending to real estate companies, became more comfortable with Ganesh Housing's transparency. Customers felt additional security buying from a listed company with quarterly scrutiny. Land sellers preferred dealing with a company whose finances were public. Even employees felt pride—their company was on the same exchanges as Reliance and TCS.

But public markets also brought challenges. Quarterly pressure was real. When competitors announced grand projects or entry into new cities, analysts asked why Ganesh Housing wasn't following suit. When land prices spiked, markets questioned their conservative bidding. When peers showed faster growth through leverage, investors wondered if management was too cautious.

The company's response was consistent: judge us by returns on capital, not size of capital. And the numbers spoke: ROEs consistently above 25%, cash generation that funded growth without dilution, and dividend yields that attracted long-term investors.

The public listing transformed Ganesh Housing from a successful regional developer into a case study for sustainable real estate development. They proved that you could be in real estate without being leveraged, regional without being limited, family-run without being opaque.

As the decade progressed, regulations would tighten with RERA, demonetization would shock the sector, and COVID would test everyone's resilience. But Ganesh Housing had done something crucial: they'd built a public company that thought in decades, not quarters. This long-term orientation would prove invaluable as they entered their next phase—moving beyond pure residential into commercial, retail, and the audacious Million Minds Tech City project.

VI. Diversification & Premium Play (2010–2020)

December 2016, midnight. Across India, ATM lines snake around blocks. Real estate offices are ghost towns. In Mumbai's Bandra-Kurla Complex, a prominent developer's CFO stares at his laptop screen, calculating how many months they can survive without sales. The demonetization announcement has just vaporized 40% of real estate transactions that happened in cash. For over-leveraged developers, it's an extinction event.

In Ahmedabad, Ganesh Housing's management watches the chaos with an emotion they rarely experience: relief. Their insistence on transparent, banked transactions—mocked by competitors as leaving money on the table—has just become their greatest strategic advantage.

The 2010s would test every assumption about Indian real estate. Demonetization, RERA, GST, NBFC crisis, and finally COVID—each disruption killed weak players and strengthened those with robust foundations. For Ganesh Housing, this decade wasn't about survival; it was about transformation.

The transformation began with a simple insight: Ahmedabad was changing. The IT corridor along SG Highway wasn't just creating jobs; it was creating a new customer segment. These weren't traditional Gujarati business families buying homes for stability. These were young professionals—engineers, designers, consultants—who viewed homes as lifestyle statements.

Ganesh Housing's response was the luxury segment push that would redefine their portfolio. The Shangri-La series, launched in 2012, wasn't just premium housing—it was a statement of ambition. These weren't apartments; they were "sky villas" with private elevators, temperature-controlled swimming pools, and home automation systems that wouldn't look out of place in Singapore or Dubai.

The market's response surprised everyone, including Ganesh Housing. The first Shangri-La project, priced at ₹8,000 per square foot (when Ahmedabad's average was ₹3,000), sold out in pre-launch. But here's what's fascinating: 60% of buyers were upgrading from existing Ganesh Housing properties. The company hadn't just built homes; they'd built a customer base that grew with them.

The Maple County series targeted a different segment—families wanting villa-style living without leaving the city. These weren't just independent houses but curated communities with central greens, community centers, and something revolutionary for Ahmedabad: HOA-style community management.

But the real strategic masterstroke was commercial real estate. While competitors saw commercial as a completely different business, Ganesh Housing saw synergy. Their residential projects had created micro-markets. Now, these markets needed offices, retail, and hospitality. Why let others capture that value?

The GCP Business Centre, launched in 2014, wasn't just another commercial project. It was strategically located amid their residential clusters, offering something unique: walk-to-work convenience for Ahmedabad's emerging professional class. Tenants included IT companies, design studios, and consultancies—businesses whose employees lived in nearby Ganesh Housing projects.

Magnet Corporate Park took this integration further. It wasn't just office space but an ecosystem—offices, retail, food courts, and service apartments. The vision was simple: create spaces where Gujarat's traditional businesses could modernize. The execution was complex: convincing textile traders to move from cramped old-city offices to modern facilities required cultural sensitivity that only a local developer could provide.

Technology adoption accelerated through the decade. But unlike peers who adopted tech for marketing buzz, Ganesh Housing focused on operational efficiency. Building Information Modeling (BIM) reduced construction errors. IoT sensors monitored construction quality in real-time. Customer relationship management systems tracked every interaction from inquiry to possession.

The smart home push was particularly instructive. While luxury developers in Mumbai and Delhi were adding smart features as premium add-ons, Ganesh Housing made them standard in higher-end projects. The logic was simple: in a market where customers compared features obsessively, technology became a differentiator that competitors couldn't easily copy.

Company has reduced debt. Company is almost debt free. This financial discipline during a diversification phase seems paradoxical. How do you enter new segments without leverage? The answer lay in brilliant capital allocation.

Instead of debt-funded land banking like peers, Ganesh Housing used operational cash flows to gradually accumulate land. Instead of launching multiple projects simultaneously, they sequenced launches to optimize capital deployment. Instead of external construction finance, they used customer advances efficiently. The result: expansion without leverage.

RERA implementation in 2017 was supposed to hurt established players who'd benefited from opacity. Instead, it became Ganesh Housing's competitive moat. While competitors scrambled to comply with disclosure requirements, Ganesh Housing simply continued practices they'd followed for years. Their RERA registrations were among the fastest approved because their documentation was already institutional-grade.

The NBFC crisis of 2018-19 devastated leveraged developers. As liquidity dried up, projects stalled across India. Ganesh Housing, with minimal debt and strong banking relationships, became a buyer's safe haven. Flight to quality wasn't just a concept; it was happening in real-time as customers abandoned stalled projects for Ganesh Housing's guaranteed delivery.

By 2020's dawn, the company had successfully transformed from a residential developer to a full-spectrum real estate company. They'd proven that diversification didn't require abandoning discipline, that premium segments could be conquered by regional players, and most importantly, that financial conservatism was a growth strategy, not a growth constraint.

The lesson from this decade: In volatile markets, antifragility beats aggression. While competitors grew faster through leverage and shortcuts, Ganesh Housing built a business that got stronger with each crisis. This strength would be tested ultimately by COVID but would also position them for their most ambitious project yet—Million Minds Tech City.

VII. The Million Minds Gambit: SEZ & Tech Parks

February 2022, a gleaming conference room in Hyderabad's HITEC City. Karnataka's IT minister is explaining Bangalore's infrastructure challenges to an audience of CEOs. Traffic gridlock. Water shortage. Astronomical real estate costs. A young founder raises his hand: "Where else can we go?" Before the minister can respond, a voice from the back: "Have you considered Ahmedabad?"

The speaker is Shekhar Patel, and he's not just offering an alternative—he's unveiling Gujarat's most ambitious play for India's trillion-dollar digital economy. Million Minds Tech City, unveiled at Gujarat's first-ever roadshow jointly presenting the GCC and IT/ITeS Policy 2022–27, held in Hyderabad. Spanning 65 acres in Ahmedabad, the development brings together next-generation office spaces, co-living, luxury residences, hospitality, and retail—all designed around a seamless walk-to-work lifestyle. Designed by Singapore-based RSP Architects and managed by New York based Tishman Speyer.

To understand the audacity of this project, consider the context. India's IT industry has been geographically concentrated—Bangalore, Hyderabad, Pune, Chennai, and NCR capture 90% of the sector. Breaking this oligopoly isn't just about building nice offices; it's about creating an entire ecosystem from scratch.

Gujarat had tried before. GIFT City, launched with fanfare in 2007, struggled for years to attract tenants beyond financial services. Ahmedabad's IT corridor existed but housed mostly back-offices and support centers, not innovation hubs. The perception problem was real: Gujarat meant manufacturing and trading, not technology and innovation.

Ganesh Housing's approach to this challenge revealed strategic thinking beyond traditional real estate development. They didn't just build an IT park; they architected an ecosystem. The master plan, developed with Singapore's RSP Architects, wasn't copied from Bangalore or Gurgaon—it was designed for how technology companies would operate in 2030, not 2010.

The walk-to-work concept seems simple but represents radical rethinking. Indian IT professionals waste 2-4 hours daily in commutes. Million Minds offers everything within walking distance—offices, homes, retail, entertainment. It's not just convenience; it's 10-15 hours of weekly productivity returned to employees and employers.

The partnership with Tishman Speyer, managers of New York's Rockefeller Center, sent a powerful signal. This wasn't a local developer's ambitious dream but a project meeting global institutional standards. For international companies evaluating India locations, this credibility mattered immensely.

But the real innovation was in solving Gujarat's talent problem. IT companies consistently cited talent availability as the barrier to Gujarat expansion. Ganesh Housing's solution was holistic: partner with universities for campus placements, create co-living spaces for young professionals, and most critically, offer quality of life that would attract talent from tier-1 cities.

The economics of SEZ development are brutal. Land acquisition costs are massive. Infrastructure requirements are enormous. Revenue realization takes years. Most developers avoid SEZs or partner with government for subsidies. Ganesh Housing self-funded, betting that long-term value creation would justify short-term capital intensity.

Gujarat's first IGBC Platinum-rated SEZ IT Park wasn't just about environmental compliance but operational efficiency. Green buildings reduce operating costs by 30-40%. For IT companies evaluating total cost of ownership, these savings matter. For Ganesh Housing, it meant premium pricing justified by lower lifetime costs.

The timing was perfect. Post-COVID, companies were desperate to diversify location risk. Bangalore's infrastructure was creaking. Hyderabad was getting expensive. Pune was saturated. Suddenly, Ahmedabad's proposition—lower costs, better infrastructure, proximity to Mumbai—looked attractive.

The Gujarat government's IT/ITeS Policy 2022-27 provided additional tailwinds. Subsidies for companies, infrastructure support, and most importantly, a committed push to position Gujarat as India's next IT destination. Million Minds became the policy's showcase project.

Early traction validated the strategy. Global Capability Centers (GCCs), which house offshore operations of multinational corporations, showed particular interest. These centers need quality infrastructure, reliable governance, and cost efficiency—exactly what Gujarat offered and Million Minds delivered.

The project also revealed Ganesh Housing's evolution from developer to urban planner. They weren't just constructing buildings but creating a micro-city. Traffic patterns, utility infrastructure, social spaces—everything was designed holistically. They even created a separate management company for ongoing operations, understanding that in IT parks, development is just the beginning.

The risk was substantial. If Million Minds failed to attract anchor tenants, it would become a massive capital sink. If Gujarat's IT ecosystem didn't develop, the project would remain underutilized. If talent didn't relocate, companies wouldn't come. Everything had to work together.

But Ganesh Housing had advantages others lacked. Three decades of local relationships meant better government support. Conservative balance sheet meant patient capital for long-term value creation. Most importantly, their reputation meant that companies trusted them to deliver on promises.

By early 2024, validation was arriving. Major IT companies signed letters of intent. GCCs began site visits. The Gujarat government featured Million Minds prominently in international roadshows. What started as an ambitious gambit was becoming reality.

The lesson from Million Minds: In real estate, the biggest returns come from creating markets, not just serving them. While competitors fought for share in established IT hubs, Ganesh Housing was creating a new hub. The risk was higher, but so was the potential reward—not just financial returns but transformation of Gujarat's economic landscape.

VIII. Financial Excellence & Capital Allocation

Picture two real estate companies in 2019. Company A has ₹10,000 crore in assets, ₹7,000 crore in debt, and generates ₹300 crore in annual profit—a 3% ROA. Company B has ₹2,000 crore in assets, minimal debt, and generates ₹400 crore in profit—a 20% ROA. Wall Street would call Company A "scaled" and Company B "subscale." But which would you rather own?

This mental model explains why Ganesh Housing's financial metrics look like they belong to a software company, not a real estate developer. ROE track record: 3 Years ROE 31.9% with current returns even higher. In an industry where 15% ROE is considered excellent, how does a real estate company generate returns that would make a consumer goods company envious?

The answer lies in a radical reimagination of real estate economics. Traditional developers operate on a simple formula: leverage land ownership to maximize project scale. Borrow at 12%, build projects yielding 18%, pocket the 6% spread, and multiply by leverage. It works beautifully—until it doesn't.

Ganesh Housing inverted this model. Instead of asking "How much can we borrow?", they asked "How little capital do we need?" This wasn't financial conservatism; it was financial engineering of a different sort.

Start with land acquisition. While competitors participated in government auctions—bidding up prices and paying upfront—Ganesh Housing focused on private negotiations with farmers. The key innovation: joint development agreements (JDAs) where landowners received a share of developed area instead of upfront payment. This reduced capital requirements by 60-70% while aligning landowner interests with project success.

The working capital management was equally sophisticated. Traditional developers have a working capital cycle of 18-24 months—buy land, get approvals, construct, sell. Ganesh Housing compressed this to 12-15 months through several innovations. Pre-launch sales (before construction begins) generated early cash flows. Phased construction reduced upfront capital deployment. Just-in-time material procurement minimized inventory costs.

But the real magic was in customer advance management. Real estate companies typically use customer money inefficiently—it sits in banks earning minimal returns while companies borrow at high rates for construction. Ganesh Housing created a treasury operation that managed customer advances like a fund manager manages investments. Short-term deployments in liquid funds. Systematic transfer to project accounts based on construction milestones. Result: negative working capital in many projects.

Revenue growth at 27.72% CAGR over 5 years while maintaining these returns seems impossible. How do you grow rapidly without capital dilution? The answer: brilliant capital recycling.

Instead of holding completed commercial projects for rental income (the traditional model), Ganesh Housing sold them to REITs or institutional investors, recycling capital into new developments. Instead of developing entire townships alone, they partnered selectively, reducing capital requirements while maintaining development fees. Instead of competing in land auctions, they focused on off-market deals where their reputation commanded better terms.

The land banking strategy deserves special attention. 35 million sqft under development represents massive future value. But unlike peers who borrowed to accumulate land banks, Ganesh Housing built theirs gradually through operational cash flows. They bought land in down cycles when prices were attractive. They negotiated long-term payment schedules. They converted agricultural land to residential/commercial, capturing conversion premiums.

In Q3 FY25, the company demonstrated robust financial performance, driven by significant growth in revenue and profit, while maintaining a strong balance sheet with minimal debt. The Ahmedabad real estate market is thriving, particularly in the residential and commercial sectors, with increasing demand for premium properties and a strategic focus on existing developments. Despite a cautious approach to new project launches due to anticipated cost changes, the company is well-positioned to capitalize on its substantial land bank and innovative construction technologies. Future revenue is expected to transition from land sales to project developments.

The capital allocation framework was institutionalized through clear priorities. First: maintain 25%+ ROE. Second: fund growth through internal accruals. Third: maintain debt/equity below 0.5x. Fourth: return excess capital to shareholders through dividends. This framework forced discipline—projects that didn't meet hurdle rates weren't pursued regardless of size or prestige.

Dividend policy reflected confidence in cash generation. While most real estate companies retained everything for growth, Ganesh Housing consistently paid dividends, signaling that growth and shareholder returns weren't mutually exclusive. This attracted a different investor base—those seeking sustainable yield, not just capital appreciation.

The financial discipline extended to cost management. While industry EBITDA margins ranged from 20-30%, Ganesh Housing consistently delivered 35-40%. How? Not through premium pricing alone but operational efficiency. Centralized procurement reduced material costs by 10-15%. In-house construction teams eliminated contractor margins. Technology adoption reduced rework and delays.

Risk management was embedded in financial strategy. Customer concentration was monitored—no single project exceeded 20% of development portfolio. Geographic concentration within Gujarat was balanced by segment diversification. Market cycle risk was managed through phased launches and flexible construction schedules.

The result is a financial model that's antifragile. In good times, high ROEs generate substantial cash for growth. In bad times, low leverage and strong cash flows provide resilience. In crisis (like COVID), the ability to defer new launches while completing existing projects provides flexibility competitors lack.

The lesson from Ganesh Housing's financial excellence: In capital-intensive industries, the highest returns come not from using more capital but from using less. While competitors measured success by assets under development, Ganesh Housing measured it by return on assets deployed. This focus on capital efficiency rather than capital deployment created a compounding machine that generated wealth sustainably.

IX. Modern Era & Market Position (2020–Present)

March 2020, Day 1 of India's COVID lockdown. Construction sites across India stand frozen, workers fled to villages, sales offices shuttered. In Mumbai, a leading developer's board conducts an emergency video call—their CFO projects they have 45 days of cash remaining. In Gurgaon, another developer begins negotiating with private equity funds, desperate for rescue capital at any terms.

In Ahmedabad, Ganesh Housing's management team also meets virtually, but their discussion is different: How do they protect workers stranded on sites? Can they accelerate digital sales infrastructure? Should they prepare for distressed asset opportunities? When you're virtually debt-free with strong cash reserves, crisis becomes opportunity.

COVID was real estate's perfect storm. Sales collapsed 80% during lockdown. Migrant workers—the industry's backbone—disappeared overnight. Raw material supply chains shattered. Customers, facing job uncertainty, deferred purchases. For leveraged developers, it was existential.

Ganesh Housing's response revealed organizational character. Within 72 hours of lockdown, they'd arranged food and shelter for 3,000+ construction workers. Not because regulations required it—enforcement was non-existent. Not for PR—nobody was watching. But because these workers had built their business.

Digital transformation, planned for years, happened in weeks. Virtual property tours using 3D modeling. Online booking systems with digital document execution. Video consultations replacing site visits. WhatsApp becoming a sales channel. While competitors struggled with basic video calls, Ganesh Housing launched completely digital sales processes.

The market recovery, when it came, was K-shaped. Premium properties rebounded strongly as wealthy Indians, flush with stock market gains and unable to travel, upgraded homes. Affordable housing struggled as lower-income segments faced job losses. Ganesh Housing, positioned in mid-to-premium segments, caught the recovery wave perfectly.

But the real story was market share gain through trust. During lockdown, news broke daily of stalled projects, developer defaults, and customer funds stuck in incomplete developments. Ganesh Housing's track record—zero stalled projects, consistent delivery despite disruptions—became their greatest marketing asset. Customers fled risky developers for safe havens.

Stock performance: All-time high of ₹1,485 reached in February 2025 reflects this flight to quality. While real estate indices struggled, Ganesh Housing commanded premium valuations. The market was differentiating between real estate companies (risky, cyclical, unreliable) and Ganesh Housing (steady, reliable, trustworthy).

Post-COVID demand dynamics shifted fundamentally. Work-from-home made space precious—families wanted extra rooms for home offices. Health consciousness drove demand for projects with open spaces and amenities. Multi-generational living returned as families sought proximity during uncertainty. Ganesh Housing's product portfolio, with larger units and integrated amenities, aligned perfectly with new preferences.

The competitive landscape transformed. National developers, burned by leverage and geographic dispersion, retreated to core markets. Local players without balance sheet strength disappeared or merged. Private equity, previously aggressive, became selective. In this consolidation, strong regional players like Ganesh Housing gained power.

Shekharbhai Patel has officially taken over as the President of CREDAI National, marking recognition of Ganesh Housing's stature. This wasn't just ceremonial—it positioned the company at the center of policy discussions, regulatory evolution, and industry transformation.

ESG (Environmental, Social, Governance) initiatives, previously nice-to-have, became business imperatives. Ganesh Housing's decade-long sustainability investments—green buildings, water recycling, solar adoption—suddenly mattered to institutional investors and premium customers. What started as operational efficiency became brand differentiation.

The company's response to inflation and input cost increases showcased pricing power. While construction costs rose 20-30% post-COVID, Ganesh Housing passed through increases without demand destruction. Premium positioning, trusted brand, and limited alternatives allowed pricing flexibility competitors lacked.

Technology adoption accelerated beyond digital sales. Artificial intelligence for demand prediction. Drone surveillance for construction monitoring. Blockchain experiments for property registration. Internet of Things for building management. While competitors talked digital transformation, Ganesh Housing implemented it.

Geographic expansion discussions intensified but strategy remained unchanged: dominate locally rather than dilute nationally. The logic was compelling—Gujarat's economy was booming, infrastructure investments were massive, and demographic trends favorable. Why chase unknown markets when home markets offered decades of growth?

The current market position is enviable. Promoter holding at 73.1% signals confidence. Institutional ownership includes quality names seeking exposure to India's real estate recovery without typical sector risks. Retail investors, many of them customers, provide stable ownership.

Recent financial performance validates the strategy. Net profit rose 46.19% to Rs 164.90 crore in the quarter ended March 2025. For the full year, net profit rose 29.81% to Rs 598.06 crore in the year ended March 2025. Sales rose 7.60% to Rs 959.76 crore in the year ended March 2025.

Looking ahead, catalysts abound. Infrastructure investments—Metro expansion, bullet train project, new airports—will reshape Ahmedabad's geography, benefiting landowners like Ganesh Housing. Formalization of real estate post-RERA advantages organized players. Gujarat's manufacturing renaissance creates employment driving housing demand.

The lesson from the modern era: Resilience compounds. Every crisis survived makes the next one easier. Every cycle navigated builds institutional knowledge. Every challenge overcome strengthens organizational culture. Ganesh Housing didn't just survive COVID; they emerged stronger, more focused, and better positioned than ever.

X. Playbook: Lessons from Regional Dominance

Here's a thought experiment: You're given $100 million to build a real estate company in India. Do you: A) Launch projects across 10 cities to diversify risk? B) Focus on one city and dominate it? C) Build a few trophy projects in Mumbai or Delhi?

Conventional wisdom says A. Private equity would push for B but in a tier-1 city. Nobody would recommend Ganesh Housing's approach: spend 60 years becoming synonymous with one tier-2 city's real estate market. Yet this seemingly limiting strategy created returns that embarrass nationally diversified players.

The power of local focus seems counterintuitive in our globalized world. But real estate remains stubbornly local. Regulations vary by state. Customer preferences differ by region. Land acquisition depends on relationships. Construction requires local knowledge. What works in Mumbai fails in Chennai. What succeeds in Gurgaon struggles in Pune.

Ganesh Housing turned geographic concentration into competitive advantage. They knew every micro-market in Ahmedabad—which areas attracted investors versus end-users, where infrastructure would develop, what configurations sold. Competitors with national presence had surface-level knowledge; Ganesh Housing had institutional memory spanning generations.

Consider land acquisition. While national players relied on brokers charging 2-3% commissions, Ganesh Housing dealt directly with farmers they'd known for decades. While competitors participated in public auctions against unknown bidders, Ganesh Housing negotiated privately with sellers who trusted them. While others discovered encumbrances after purchase, Ganesh Housing knew every plot's history.

The relationship moat went beyond land. Local contractors preferred working with Ganesh Housing—steady payments, respectful treatment, long-term relationships. Banks eagerly funded their projects—proven track record, local management accessibility, zero NPAs. Government officials expedited approvals—not through corruption but credibility built over decades.

Customer acquisition costs tell the story. National developers spend 6-8% of revenues on marketing—billboards, celebrity endorsements, aggressive advertising. Ganesh Housing spends less than 2%. Their marketing is existing customers recommending to friends, families buying multiple properties across generations, and projects selling through word-of-mouth.

Capital efficiency in focused markets is remarkable. Marketing expenses are shared across projects. Management bandwidth isn't stretched across cities. Construction teams move seamlessly between nearby sites. Material procurement achieves scale economies. Every efficiency compounds when operations are concentrated.

But the greatest advantage of regional dominance is pricing power. In Ahmedabad's premium micro-markets, Ganesh Housing commands 10-20% premiums over identical products from national brands. Why? Trust accumulated over generations, proven delivery track record, and most importantly, network effects—buying Ganesh Housing means joining a community of successful Ahmedabadis.

The trust-building playbook deserves examination. It started with radical transparency—showing customers exactly where their money went. Then came consistent delivery—not one project delayed beyond promised dates. Add financial conservatism—never stretching beyond capacity. Layer on community engagement—supporting local causes, employing local talent. Multiply by time—60 years of consistent behavior. Result: a brand that transcends business.

Capital allocation in regional markets requires different thinking. Instead of growth at any cost, it's profitable growth within constraints. Instead of market share battles, it's premium positioning in chosen segments. Instead of diversification for its own sake, it's deepening presence where you're already strong.

The debt-free discipline seems almost anachronistic in modern finance. Every MBA teaches that leverage amplifies returns. Private equity pushes for aggressive capital structures. Yet Ganesh Housing's virtually debt-free status created optionality worth more than leveraged returns. In good times, they could pursue opportunities others couldn't afford. In bad times, they survived while leveraged competitors collapsed.

Managing cyclicality through diversification—but within geography—was brilliant. Residential provided steady cash flows. Commercial offered development fees. Retail generated long-term value. SEZs created future options. Different segments peaked at different times, smoothing cycles while maintaining local focus.

The institutional knowledge accumulated over decades is irreplaceable. Which government officials are decision-makers versus paper-pushers? Which contractors deliver quality versus cutting corners? Which areas will gentrify versus stagnate? This knowledge, undocumented but embedded in organizational memory, is worth more than any strategic plan.

The family ownership structure, often seen as weakness, became strength when combined with professional management. Family ownership provided patient capital and long-term thinking. Professional management brought systems and scalability. The combination—rare in Indian business—created sustainable competitive advantage.

Why can regional champions outperform national players? Because real estate isn't about financial engineering or scale—it's about trust, relationships, and local knowledge. National players have breadth but lack depth. Regional champions have depth that creates defensibility. In markets where trust is scarce and relationships matter, depth beats breadth.

The lesson from Ganesh Housing's playbook: In relationship businesses, geographic focus isn't limitation—it's leverage. While competitors spread thin chasing growth, Ganesh Housing built thick advantages through concentration. They proved that owning a city beats visiting many.

XI. Analysis & Investment Case

The P/E (price-to-earnings) ratio of Ganesh Housing Corp Ltd (GANESHHOUC) is 13.33—in any other industry, this would signal either distress or decline. In Indian real estate, it signals something different: the market's persistent inability to value quality in a sector scarred by destruction.

To understand this valuation paradox, consider the graveyard of real estate wealth destruction. DLF, once India's largest developer, destroyed 80% of shareholder value from its peak. Unitech, former darling of markets, trades at 90% below IPO price. Jaypee, Amrapali, HDIL—the list of value destroyers reads like a casualty report.

Against this backdrop, Ganesh Housing's consistent value creation seems almost miraculous. But the market, scarred by sector-wide disappointment, applies a "real estate discount" even to exceptional operators. This creates opportunity for investors who can distinguish between sector risk and company quality.

Start with valuation metrics. The P/B (price-to-book) ratio is 5.08, seemingly expensive until you realize book value understates reality. Land bought decades ago sits at historical cost while market values have multiplied 10-50x. If marked to market, book value would double, making current valuations appear reasonable.

The earnings quality is remarkable for real estate. No aggressive revenue recognition—sales recorded only at possession. No financial engineering—minimal debt means no interest coverage manipulation. No related party transactions—arms-length dealing even with promoter entities. This conservative accounting means reported profits understate economic reality.

Growth drivers for the next decade are compelling. Gujarat's economy, growing at 10%+ annually, creates sustained housing demand. Infrastructure investments—metro, bullet train, expressways—will reshape urban geography, benefiting landowners like Ganesh Housing. Formalization post-RERA advantages organized players over informal competitors.

The demographic dividend is particularly powerful. Gujarat's median age of 28 means prime home-buying population expanding for two decades. Rising incomes—per capita GDP growing 8% annually—expand addressable market. Nuclear family trend—average household size declining from 5 to 3—multiplies housing units needed.

Million Minds Tech City represents optionality markets haven't valued. If Gujarat captures even 5% of India's IT growth, the project's value exceeds Ganesh Housing's current market cap. If GCCs proliferate as expected, commercial rentals provide annuity income streams. If successful, it transforms from developer to infrastructure owner—a rerating catalyst.

But risks are real and must be acknowledged. Geographic concentration in Gujarat means local economic shocks hurt disproportionately. Regulatory changes—new taxes, approval delays, policy shifts—impact immediately. Market cycles—real estate's inherent volatility—affect even quality operators. Execution risk on 35 million square feet pipeline requires flawless management.

The competitive dynamics are evolving. National players, having retreated during COVID, might return with vengeance. New-age players, armed with technology and venture capital, could disrupt traditional models. Customer preferences, shifting toward sustainability and technology, require continuous adaptation.

Key person risk deserves attention. While professional management exists, promoter family's reputation and relationships remain critical. Succession planning, though addressed, hasn't been tested. Institutional knowledge, accumulated over decades, might not transfer seamlessly.

The bull case rests on sustainable competitive advantages. Brand value in Ahmedabad translates to pricing power and lower customer acquisition costs. Land bank acquired cheaply provides years of development pipeline. Operational excellence generates returns competitors can't match. Financial conservatism ensures survival through any crisis.

The bear case highlights structural challenges. Real estate remains cyclical despite operational excellence. Gujarat concentration, while advantageous now, could become liability if state growth slows. Technology disruption might commoditize traditional advantages. Young homebuyers might not value legacy brands like parents did.

Debtor days have increased from 77.9 to 131 days, suggesting collection challenges or changing sales mix. While not alarming given strong balance sheet, it bears monitoring for trends.

Scenario analysis reveals asymmetric risk-reward. Base case assumes Gujarat grows 8% annually, Ganesh Housing maintains market share, and margins remain stable—implying 15-20% annual returns. Bull case with successful Million Minds, market share gains, and multiple expansion suggests 25-30% returns. Bear case with prolonged downturn and execution failures limits downside to 20-30% given asset backing.

The investment case ultimately depends on belief in India's urbanization story and Gujarat's economic trajectory. If India needs 100 million new homes by 2030, quality developers will thrive regardless of cycles. If Gujarat maintains growth momentum, Ganesh Housing's positioning ensures participation. If quality eventually gets valued appropriately, multiple expansion provides additional upside.

For long-term investors, Ganesh Housing offers rare combination: secular growth exposure with downside protection, operational excellence with financial conservatism, proven execution with ambitious vision. The market's skepticism, while understandable given sector history, creates opportunity for patient capital.

XII. Epilogue & Future Vision

Imagine Ahmedabad in 2035. The bullet train has reduced Mumbai commute to two hours. The metro network connects every corner. Million Minds houses 50,000 IT professionals. The city rivals Pune as India's secondary tech hub. In this transformed landscape, who captures value?

The answer shapes Ganesh Housing's next chapter. They're not just building for today's Ahmedabad but tomorrow's metropolis. Every land parcel acquired, every project launched, every capability developed aims at this future city.

The strategic choices facing management are fascinating. Should they finally expand beyond Gujarat, leveraging their operational excellence in new markets? Should they backward integrate into construction materials, capturing more value chain? Should they forward integrate into property management, creating annuity income streams? Should they partner with global funds for larger township projects?

The conservative path—stick to Gujarat, maintain current model, grow steadily—virtually guarantees success. Gujarat's economy ensures decades of demand. Their competitive position remains defensible. Returns stay attractive. It's the rational choice.

But is it the right choice? India's real estate industry needs institutional-quality developers. Markets beyond Gujarat need alternatives to unreliable local players. Technology disruption requires scale for investment. Global capital seeks trusted partners. Perhaps Ganesh Housing's responsibility extends beyond shareholders to industry transformation.

The transition from family-led to institution is crucial. While professional management exists, cultural DNA remains family-influenced. This brings advantages—long-term thinking, relationship focus, conservative values. But also limitations—decision speed, risk appetite, organizational scale. Balancing preservation with evolution requires delicate management.

Technology transformation presents opportunity and threat. PropTech startups are reimagining customer experience, construction technology, and transaction processes. Ganesh Housing must decide: build capabilities internally, acquire startups, or partner with technology providers? Their response will determine relevance to digital-native customers.

Environmental sustainability, from compliance burden, must become competitive advantage. Net-zero buildings, water recycling, renewable energy—these aren't just certifications but operational imperatives. Ganesh Housing's early investments position them well, but continued leadership requires continuous innovation.

What would different leadership do? Private equity ownership would leverage the balance sheet, expand nationally, and exit within five years—potentially destroying long-term value for short-term gains. Strategic buyer would integrate operations but lose local focus. Next generation family leadership might pursue aggressive growth or maintain conservatism—unknown until tested.

The lessons for founders are profound. Building trust slowly creates compound value that money can't buy quickly. Geographic focus isn't limitation but leverage if executed correctly. Financial conservatism preserves optionality worth more than leveraged returns. Family businesses can professionalize without losing soul.

For investors, Ganesh Housing demonstrates that sector doesn't determine destiny—execution does. Even in difficult industries, exceptional operators generate exceptional returns. Patient capital invested with quality management compounds wealth sustainably. Sometimes the best investments hide in plain sight, dismissed by markets fighting last war.

The future of regional champions in India is bright. As tier-2/3 cities grow, local knowledge becomes more valuable. As customers seek trust, reputation matters more. As markets formalize, organized players win. As technology democratizes capabilities, execution excellence differentiates. Ganesh Housing's playbook—deep local presence, operational excellence, financial conservatism—might be the template for India's next generation of wealth creators.

The most profound lesson from Ganesh Housing's journey isn't about real estate—it's about business building. In an era obsessed with blitzscaling, they show that slow, steady, sustainable growth creates more value. In markets chasing the next new thing, they prove that executing basics brilliantly beats innovation without implementation. In industries where trust is scarce, they demonstrate that reputation is the ultimate moat.

As we conclude this exploration, remember that Ganesh Housing's story isn't finished—it's entering its most interesting chapter. The foundations built over 60 years now support ambitions that would have seemed impossible to that young contractor in 1960s Ahmedabad. The question isn't whether they'll succeed—their track record suggests they will. The question is how they'll redefine success for Indian real estate.

The journey from dusty construction sites to gleaming tech cities, from handshake deals to institutional governance, from local builder to regional powerhouse, offers a masterclass in building enduring value. In an industry known for destruction, they've created wealth. In markets demanding growth, they've delivered returns. In cycles requiring resilience, they've demonstrated antifragility.

That's the Ganesh Housing story—not just building homes, but building trust, not just developing projects, but developing markets, not just creating structures, but creating value that compounds across generations. It's a distinctly Indian story of entrepreneurship, perseverance, and the power of thinking in decades while executing in quarters.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube