HDFC AMC: India's Mutual Fund Powerhouse

I. Introduction & Episode Setup

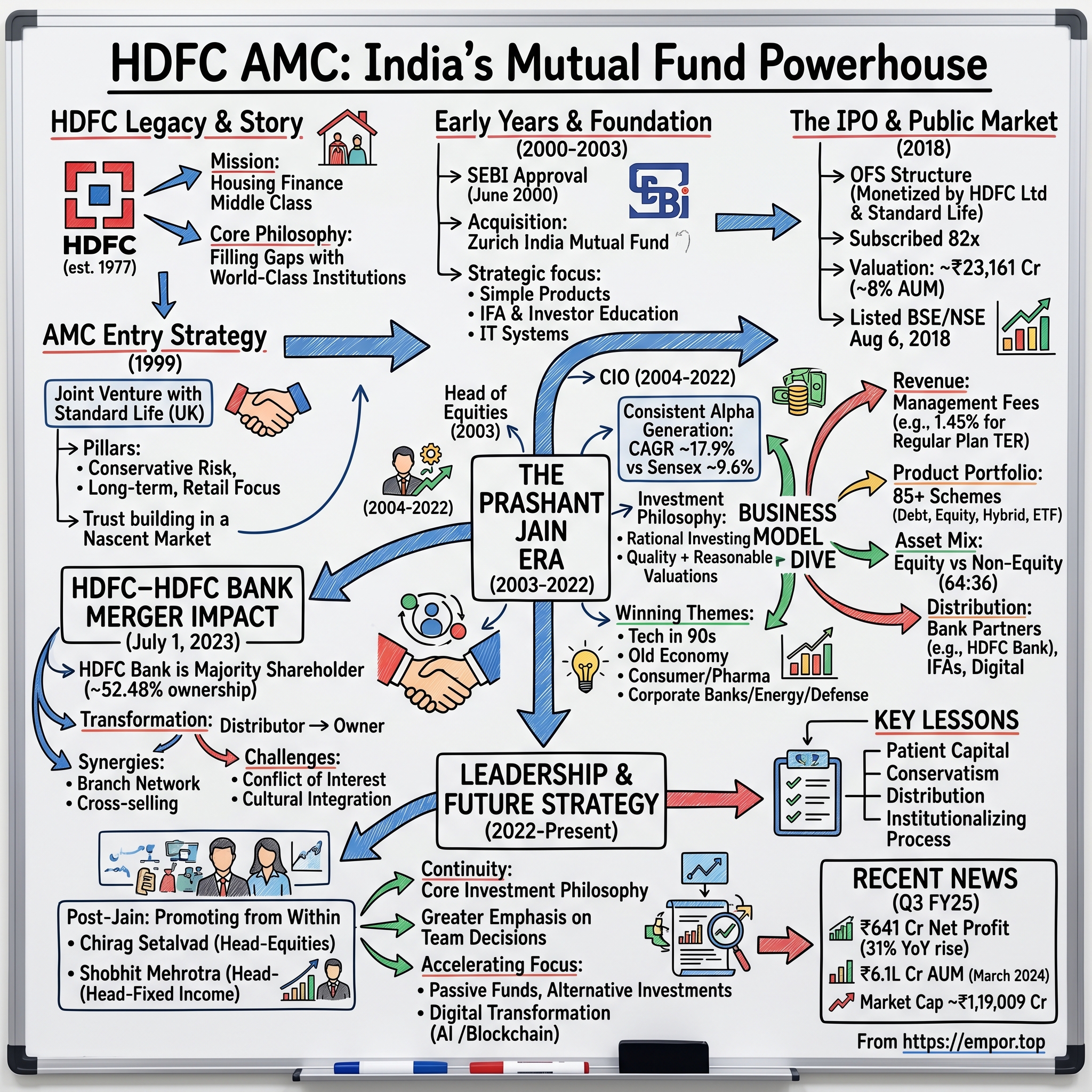

The story of HDFC Asset Management Company is fundamentally about timing, trust, and transformation. With ₹641 crore net profit in Q3 FY25, marking a 31.4% year-on-year rise, HDFC AMC stands as India's largest mutual fund house—a position it has carefully cultivated over two and a half decades. As of March 2024, the company manages assets worth Rs. 6.1L Cr crores, representing over 11% of the entire Indian mutual fund industry's assets under management.

But here's the central paradox that makes this story fascinating: How did a company that entered the mutual fund business in 1999—when giants like UTI already dominated the landscape—become not just the largest, but also the most profitable asset management company in India? The answer lies not in first-mover advantage, but in something far more nuanced: the art of building trust at scale in a market where financial literacy was nascent and skepticism ran deep.

The Indian mutual fund industry itself tells a story of transformation. From a monopolistic structure dominated by UTI until the early 1990s to today's vibrant ecosystem managing over ₹50 trillion, this journey mirrors India's own economic liberalization. HDFC AMC didn't just ride this wave—it helped shape it. The company's trajectory from managing a few thousand crores in 2003 to becoming a ₹6 lakh crore behemoth represents more than just business success; it embodies the financialization of Indian household savings.

What makes HDFC AMC particularly intriguing is its ability to navigate multiple transitions successfully. The shift from institutional to retail dominance in mutual funds. The evolution from active to passive investing pressures. The digital transformation of distribution. And most recently, the integration challenges following the mega-merger of parent HDFC with HDFC Bank in 2023. Each of these transitions could have derailed a lesser organization. Instead, HDFC AMC emerged stronger, with Market Cap ₹ 1,19,009 Cr as of recent data.

Consider the context of India's savings revolution. For decades, Indian households parked their savings primarily in gold, real estate, and bank fixed deposits. The mutual fund penetration in India, even today, stands at less than 15% of household savings. Yet within this relatively small pie, HDFC AMC has carved out the largest slice, managing money for over 13 million unique investors across the country. This isn't just about selling financial products; it's about changing deeply ingrained cultural attitudes toward money and investing.

The company's story also illuminates broader themes about building financial institutions in emerging markets. How do you create sophisticated investment products for a market where the majority of participants are first-time investors? How do you balance the star power of individual fund managers with institutional stability? How do you maintain margins in an industry facing constant regulatory pressure to reduce fees? These questions aren't just academic—they're central to understanding HDFC AMC's playbook and its implications for the future of asset management globally.

II. The HDFC Legacy & Founding Story (1977–1999)

The genesis of HDFC AMC cannot be understood without first appreciating the revolutionary institution that spawned it. Housing Development Finance Corporation, established in 1977, wasn't just India's first specialized mortgage company—it was a radical reimagining of what financial inclusion could mean in a country where home ownership was a distant dream for most middle-class families.

The founding of HDFC itself reads like a nation-building narrative. In 1977, India was a very different place. The economy was closed, capital was scarce, and the idea of a private sector company providing long-term housing finance was almost unthinkable. Banks wouldn't touch home loans—the tenure was too long, the ticket sizes too large for most Indians, and the regulatory framework virtually non-existent. Into this void stepped Hasmukhbhai Parekh, a visionary who had spent years at ICICI understanding project finance, along with support from institutions like ICICI itself.

Parekh's insight was profound yet simple: India's growing middle class desperately needed homes, but lacked access to organized finance. The informal lending market charged usurious rates, often exceeding 36% annually. HDFC would bridge this gap, offering loans at reasonable rates with systematic processes. But this wasn't just about business—it was about transforming how Indians thought about debt, savings, and asset creation. A home wasn't just shelter; it was the primary vehicle for wealth creation for millions of Indian families.

By the 1990s, HDFC had become more than a mortgage lender. Under the leadership of Deepak Parekh, who took over as Chairman in 1993, it evolved into a financial conglomerate with a unique philosophy: identify gaps in India's financial services landscape and fill them with world-class institutions. This led to HDFC entering banking (though initially unsuccessful with HDFC Bank being set up as a separate entity), insurance, and eventually, asset management.

The decision to enter asset management wasn't opportunistic—it was strategic. By the late 1990s, HDFC's leadership recognized several converging trends. First, India's savings rate was among the highest in the world, consistently above 30% of GDP. Second, these savings were predominantly in physical assets and bank deposits, earning returns that barely beat inflation. Third, the equity markets were developing rapidly post-liberalization, creating wealth but remaining inaccessible to most Indians due to lack of knowledge and trust.

The mutual fund industry in 1999 presented both opportunity and challenge. UTI, the government-backed behemoth, controlled over 80% of the market. Foreign players like Morgan Stanley and Templeton had entered but struggled to gain significant market share. The industry's reputation had been tarnished by the US-64 crisis, where UTI's flagship scheme faced massive redemption pressure. Trust was at a premium.

HDFC's entry strategy was distinctive. Rather than going alone, it partnered with Standard Life Investments of the UK, bringing international expertise while maintaining local control. The joint venture structure—with Standard Life initially holding a significant stake—provided credibility and access to global best practices in fund management. The company was incorporated on December 10, 1999, at a time when the total mutual fund industry AUM was less than ₹1 lakh crore.

The founding team understood that success wouldn't come from merely replicating existing models. Indian investors had different needs, risk appetites, and investment horizons compared to their Western counterparts. Products needed to be simple, transparent, and suited to the Indian context. Distribution had to reach beyond metros to tap into the vast savings pool in smaller cities. Most importantly, the company needed to build trust in a market scarred by previous failures.

HDFC AMC's foundation was thus built on three pillars borrowed from its parent's DNA: conservative risk management, long-term thinking, and an unwavering focus on retail customers. The company didn't aim to be the most innovative or aggressive player. Instead, it positioned itself as the safe, reliable choice for Indian families taking their first steps into market-linked investments. This positioning would prove prescient as the Indian economy entered a period of sustained growth in the 2000s.

The regulatory environment also played a crucial role. SEBI, the market regulator, was systematically strengthening the framework for mutual funds, introducing measures like daily NAV disclosure, standardized risk metrics, and strict investment guidelines. HDFC AMC didn't just comply with these regulations; it often exceeded them, understanding that in a low-trust market, regulatory compliance was a competitive advantage.

III. Early Years & Building the Foundation (2000–2003)

The dawn of the new millennium brought both promise and peril for HDFC AMC. With approval from SEBI on June 30, 2000, under registration number MF/044/00/6, the company was officially ready to launch its mutual fund schemes. But the timing couldn't have been more challenging. The dot-com bubble was bursting globally, the Indian technology sector was in turmoil, and investor confidence in equity markets was shaken.

The Indian mutual fund landscape in 2000 was a study in contrasts. UTI still dominated with its massive investor base of over 20 million accounts, built over three decades. Private sector players like Prudential ICICI, Birla Sun Life, and DSP Merrill Lynch were gaining ground but still commanded less than 20% market share combined. Foreign players were struggling with distribution and cultural adaptation. The total industry AUM stood at approximately ₹90,000 crore, with equity funds accounting for less than 15% of assets.

HDFC AMC's initial product strategy reflected deep market understanding. Rather than launching complex, high-risk products that might generate buzz, the company started with simple, easy-to-understand schemes. The focus was on balanced funds and income funds—products that offered stability and regular income, appealing to risk-averse Indian investors making their first foray beyond fixed deposits.

Distribution emerged as the critical challenge. Unlike banks that had branches or insurance companies with agent networks, mutual funds had limited direct customer touchpoints. HDFC AMC leveraged its parent's relationships, partnering with HDFC Bank (a separate entity but sharing the HDFC brand) for distribution. But this wasn't enough. The company needed to build its own distribution network, particularly in smaller cities where banking penetration was low but savings rates were high.

The company adopted a multi-pronged distribution strategy. First, it invested heavily in building relationships with Independent Financial Advisors (IFAs), the backbone of mutual fund distribution in India. These advisors, often operating from small offices in residential neighborhoods, had deep relationships with local communities. HDFC AMC didn't just sign them up; it invested in their education, providing training, marketing support, and technology tools.

Second, recognizing that most Indians were unfamiliar with mutual funds, HDFC AMC launched extensive investor education programs. These weren't just marketing exercises but genuine attempts to demystify investing. Company executives would conduct sessions in housing societies, corporate offices, and community centers, explaining concepts like systematic investment plans (SIPs), rupee cost averaging, and asset allocation in simple, relatable terms.

The technology infrastructure built during these early years would prove foundational. While competitors relied on manual processes, HDFC AMC invested in robust IT systems for transaction processing, customer service, and distributor management. This wasn't cutting-edge by global standards, but in the Indian context, where many transactions still happened on paper, it was revolutionary.

A defining moment came in 2003 with the acquisition of Zurich India Mutual Fund. This wasn't just about adding assets under management; it was a strategic move that brought in talent and expanded distribution reach. The Zurich acquisition added approximately ₹600 crore in AUM, but more importantly, it brought in a team of experienced fund managers and a network of distributors in markets where HDFC AMC had limited presence.

The integration of Zurich India was handled with remarkable finesse. Rather than imposing HDFC's culture wholesale, the company retained key talent and selectively adopted best practices from both organizations. Schemes were rationalized to avoid overlap, but popular funds were retained with enhanced mandates. The message to investors was clear: HDFC AMC was a stable, growth-oriented player that could be trusted with long-term savings.

By the end of 2003, HDFC AMC had established itself as a serious player in the Indian mutual fund industry. Assets under management had crossed ₹3,000 crore, the company was profitable, and more importantly, it had built a foundation of trust with distributors and investors. The company's conservative approach—often criticized as too slow by market observers—was vindicated as several aggressive competitors faced redemption pressures and fund closures.

The regulatory environment during this period was evolving rapidly. SEBI introduced measures like the requirement for mutual funds to disclose portfolio holdings monthly, standardized expense ratios, and strict guidelines on advertisement and marketing claims. HDFC AMC not only complied but often went beyond requirements, publishing detailed investment rationales and fund manager commentaries that helped investors understand market movements.

Customer service emerged as a key differentiator. In an industry notorious for poor service standards, HDFC AMC invested in call centers, dedicated relationship managers for high-value investors, and systematic complaint resolution processes. The company understood that in a relationship business like asset management, every customer interaction was an opportunity to build or erode trust.

The early years also saw the development of HDFC AMC's investment philosophy. Unlike the momentum-driven strategies popular at the time, the company adopted a value-oriented, research-driven approach. Fund managers were encouraged to take contrarian positions, backing their convictions even when markets moved against them. This philosophy would soon find its ultimate expression in the arrival of a fund manager who would define HDFC AMC's trajectory for the next two decades.

IV. The Prashant Jain Era: Building a Juggernaut (2003–2022)

The appointment of Prashant Jain as Head of Equities in 2003 marked a watershed moment not just for HDFC AMC, but for the entire Indian mutual fund industry. Having worked with SBI Mutual Fund (1991-1993) as well as Zurich India Mutual Fund (1993-2003) in different capacities, he moved to HDFC Mutual Fund, subsequent to the takeover of Zurich India Mutual Fund by HDFC in 2003. What followed was perhaps the most successful fund management tenure in Indian financial history.

Jain brought with him more than just experience; he brought a philosophy that would fundamentally reshape how HDFC AMC approached investing. An IIT Kanpur engineer with an IIM Bangalore MBA, Jain combined analytical rigor with deep market understanding. But what set him apart wasn't his pedigree—it was his contrarian conviction and remarkable ability to identify value in unfashionable sectors.

He thus has an unbroken track record of managing the same fund for over 28 years. This Fund, HDFC Balanced Advantage Fund, delivered a CAGR of ~17.9% vs Sensex CAGR of ~9.6% from Jan 1994 - July 2022. This wasn't just outperformance; it was consistent alpha generation at a scale rarely seen globally. To put this in perspective, generating nearly 8 percentage points of annual outperformance over almost three decades, while managing increasingly large sums of money, defies conventional wisdom about the limits of active management.

Jain's investment philosophy was deceptively simple but remarkably difficult to execute. He believed in buying quality businesses at reasonable valuations and holding them through cycles. This wasn't classic value investing in the Benjamin Graham sense, nor was it growth investing in the Philip Fisher tradition. Jain called it "rational investing"—buying businesses where the risk-reward equation was favorable, regardless of whether they were classified as value or growth stocks.

His key winning themes over these three decades were technology in 90's, old economy from early 2000 to pre-Lehman, consumer and pharma from pre-Lehman to mid-2010's and corporate banks, energy, defense, utilities etc. in the last phase. He also successfully called the tech bubble and avoided the excesses of pre-Lehman in infra, power and more recently in new age tech stocks.

The transformation of HDFC AMC under Jain's leadership as CIO from 2004 to 2022 was extraordinary. Assets under management grew from approximately ₹3,000 crore to around ₹4,40,000 crore—a 146-fold increase. But the quantitative growth only tells part of the story. Jain fundamentally changed how Indian investors thought about equity investing.

Consider the evolution of HDFC Balanced Advantage Fund (formerly HDFC Prudence), the flagship scheme Jain managed. When he took over, it was a modest fund with a few hundred crores in assets. By the time he left, it had become India's largest equity-oriented fund with over ₹43,000 crore in AUM. More remarkably, it had created wealth for hundreds of thousands of investors, many of whom had started with small SIPs of ₹500 or ₹1,000 per month.

Jain's approach to portfolio construction was distinctive. While most fund managers chased momentum and crowded into popular stocks, Jain often took contrarian positions. In the mid-2000s, when infrastructure and real estate stocks were market darlings, Jain was underweight. When these sectors crashed post-2008, his funds outperformed dramatically. Similarly, his early recognition of the potential in private sector banks, pharmaceuticals, and consumer goods companies created enormous wealth for investors.

But perhaps Jain's greatest contribution was in institutionalizing a culture of research and conviction at HDFC AMC. He built a team of analysts who shared his philosophy of deep fundamental research. Company visits weren't photo opportunities but intensive sessions to understand business models, competitive advantages, and management quality. The investment team would often visit factories, meet dealers and suppliers, and conduct channel checks to verify investment theses.

The star fund manager phenomenon that Jain represented was both a blessing and a challenge for HDFC AMC. On one hand, his track record attracted enormous inflows. Investors didn't just invest in HDFC funds; they invested in "Prashant Jain's funds." This created a powerful brand pull that competitors struggled to match. On the other hand, it created key person risk. What would happen to these funds if Jain left?

HDFC AMC managed this risk carefully. While Jain was the face of equity investing, the company built strong teams across fixed income, liquid funds, and other categories. It also developed a clear succession planning process, grooming internal talent who understood and could execute the investment philosophy. The company's institutional processes—risk management, compliance, operations—were robust enough to function independently of any individual.

The period from 2014 to 2017 tested Jain's philosophy severely. His value-oriented approach underperformed as markets rewarded momentum and growth at any price. Critics questioned whether his style had become outdated. Some investors redeemed their holdings, moving to funds showing better recent performance. But Jain remained steadfast, continuing to back his convictions even as his funds underperformed benchmarks.

The vindication came dramatically from 2018 onwards. As markets corrected and quality companies with reasonable valuations outperformed, Jain's funds delivered spectacular returns. The lesson was profound: in investing, as in life, conviction and patience are often rewarded, but only if backed by rigorous analysis and risk management.

Under Jain's leadership, HDFC AMC also pioneered several investor-friendly practices. The company was among the first to launch systematic investment plans (SIPs) in a big way, making equity investing accessible to small investors. It introduced trigger-based investing, allowing investors to automate investment decisions based on market levels. The company's investor education initiatives, often featuring Jain himself, demystified equity investing for millions of Indians.

V. The IPO & Public Market Story (2018)

The decision to take HDFC AMC public in 2018 represented a critical inflection point in the company's evolution. After nearly two decades of private ownership, why go public now? The answer lay in a complex interplay of strategic considerations, market dynamics, and stakeholder interests that would reshape the company's trajectory.

HDFC AMC IPO is a main-board IPO of 2,54,57,555 equity shares of the face value of ₹5 aggregating up to ₹2,800.33 Crores. The issue is priced at ₹1100 per share. The IPO opens on July 25, 2018, and closes on July 27, 2018. The timing was deliberate and strategic. The Indian equity markets were near all-time highs, investor sentiment was bullish, and the mutual fund industry was experiencing unprecedented growth.

The context is crucial to understand. By 2018, the Indian mutual fund industry had crossed ₹22 trillion in AUM, growing at over 20% annually. Equity markets had delivered strong returns, creating wealth for investors and attracting new participants. The government's demonetization drive in 2016 had pushed savings from physical assets to financial instruments. Digital platforms were making mutual fund investing as easy as ordering food online. HDFC AMC, as the largest player, was perfectly positioned to capitalize on these trends.

The IPO structure was notable for being entirely an offer for sale (OFS), meaning no fresh capital was raised for the company. Instead, existing shareholders—HDFC Limited and Standard Life—partially monetized their holdings. This sent a strong signal: the company didn't need capital for growth; it was generating sufficient cash from operations. The sellers retained majority stakes, indicating continued confidence in the business.

According to CRISIL, as of December 31, 2017, HDFC AMC has been the most profitable AMC of the country in terms of net profits since Fiscal 2013 with a total AUM (Assets Under Management) of Rs 2,932.54 billion. Its profits has grown every year since 2002. It has been the largest AMC in equity-oriented AUM since the last quarter of Fiscal 2011 and has consistently been among the top two asset management companies in India in terms of total average AUM since the month of August 2008.

The market reception was enthusiastic but not euphoric. The IPO was subscribed 82 times overall, with the qualified institutional buyer portion subscribed 164 times. Retail participation was strong but measured, with the retail portion subscribed 1.38 times. The shares got listed on BSE, NSE on August 6, 2018, and traded at a modest premium to the issue price, reflecting realistic expectations rather than irrational exuberance.

The valuation metrics were particularly interesting. At ₹1,100 per share, the company was valued at approximately ₹23,161 crore, close to 8% of its AUM. This was premium pricing by global standards, where asset managers typically trade at 2-3% of AUM. But investors were paying for more than just current assets; they were betting on HDFC AMC's ability to capture a disproportionate share of future growth in Indian financial savings.

The post-IPO ownership structure created interesting dynamics. HDFC Limited retained a majority stake, ensuring continuity of vision and strategy. Standard Life (later abrdn) maintained a significant holding, providing continued access to global expertise. The free float of about 25% included some of India's most sophisticated institutional investors, creating a high-quality shareholder base that understood the long-term nature of the asset management business.

Going public brought new responsibilities and pressures. Quarterly earnings calls meant greater scrutiny of short-term performance. Market expectations for consistent growth created pressure to launch new products and enter new segments. The stock price became a daily report card, influencing employee morale and market perception. HDFC AMC had to balance the demands of being a public company with the long-term orientation essential for successful asset management.

The IPO proceeds, while not coming to the company directly, had indirect benefits. The partial exit by Standard Life was handled smoothly, removing any overhang concerns. HDFC Limited's continued majority ownership provided stability. The public listing created a currency for potential acquisitions and employee stock options. Most importantly, it enhanced the company's profile and credibility, particularly important in attracting institutional mandates.

The regulatory implications of being a listed entity were significant. SEBI's regulations for listed companies added another layer of compliance and disclosure requirements. Related party transactions with HDFC Limited and HDFC Bank came under greater scrutiny. The company had to manage potential conflicts between maximizing shareholder returns and fulfilling fiduciary duties to mutual fund investors.

The IPO also marked a generational transition in the Indian mutual fund industry. HDFC AMC's successful listing paved the way for other AMCs to consider public listings. It validated the asset management business model in India, demonstrating that these companies could generate consistent profits and returns for shareholders. The premium valuations achieved set benchmarks for the sector and attracted greater investor interest in financial services businesses.

Employee wealth creation through the IPO was substantial. Many long-serving employees who had received stock options saw life-changing wealth creation. This had profound implications for talent retention and attraction. HDFC AMC could now compete with technology companies and startups in offering equity-based compensation, crucial in India's increasingly competitive talent market.

The market's verdict on HDFC AMC post-IPO has been largely positive. The stock has delivered strong returns, outperforming broader market indices. The company has maintained its market leadership position while navigating regulatory changes, market volatility, and increased competition. The successful IPO and subsequent performance validated the company's strategy and execution capabilities.

VI. Business Model Deep Dive

Understanding HDFC AMC's business model requires appreciating the elegant simplicity underlying apparent complexity. At its core, the company earns fees for managing other people's money—a straightforward proposition. But the execution of this model in the Indian context, with its unique challenges and opportunities, reveals sophisticated strategic thinking and operational excellence.

The revenue model starts with management fees, typically ranging from 0.1% for liquid funds to 2.5% for equity funds (before regulatory caps). Our largest equity-oriented fund is HDFC Balanced Advantage Fund. The current AUM of that is around INR 64,000 crores, INR 65,000 crores and the regular plan TER as per formula comes to 1.45%. And at that point in time, this fund had an AUM of INR 40,000 crores and the TER at that point in time was 1.78%. So over the last say 3, 4-odd years, TER has gone down by 33 basis points or for that matter by around 19%, 20%. This demonstrates how scale benefits are passed to investors through lower expense ratios.

The company's product portfolio spans the entire risk-return spectrum. Offering approximately 85 primary schemes, HDFC Mutual Fund caters to various investment preferences, including debt funds, equity-oriented schemes, hybrid schemes, and others (such as ETFs and Gold). This diversification serves multiple purposes: it caters to different investor needs, provides stability through market cycles, and maximizes wallet share from existing customers.

The asset mix is strategically balanced. The ratio of equity and non-equity oriented QAAUM is 64:36, compared to the industry ratio of 56:44 for the quarter ended June 30,2024. This higher proportion of equity assets is significant because equity funds command higher management fees and tend to be stickier during market upturns. However, it also means greater volatility in revenues during market corrections.

Distribution strategy has been HDFC AMC's masterstroke. The company operates through multiple channels: direct sales, banking partnerships (particularly with HDFC Bank), national distributors, independent financial advisors, and increasingly, digital platforms. With a vast reach, the company serves over 75,000 distribution partners across 210 branches spanning more than 200 cities in India.

The HDFC Bank relationship deserves special attention. While HDFC Bank is a separate entity (until the 2023 merger of HDFC Ltd with HDFC Bank), the shared brand and cross-selling opportunities created significant advantages. Bank customers were natural targets for mutual fund products, and the trust in the HDFC brand facilitated conversions. Post-merger, with HDFC Bank holds a 94.63 percent stake in HDFC Securities, followed by a 94.54 percentage stake in HBD Financial Services, 52.48 percent stake in HDFC AMC, these synergies are expected to strengthen further.

The focus on retail investors has been a defining characteristic. One of the most preferred choices of individual investors, with a market share of 13.3% of the individual monthly average AUM for June 2024. Retail money, particularly through SIPs, provides stable, long-term assets. These investors are less likely to churn based on short-term performance and provide predictable fee income.

Technology transformation has been crucial but understated. HDFC AMC wasn't an early adopter of cutting-edge technology, but it invested steadily in building robust, scalable systems. Online transaction platforms, mobile apps, and straight-through processing reduced operational costs while improving customer experience. The company's technology spending focused on reliability and scale rather than innovation for its own sake.

The systematic investment plan (SIP) revolution that HDFC AMC helped pioneer transformed the business model. 8.76 million Systematic transactions with a value of Rs 32.1 billion processed during the month of June 2024. SIPs provide predictable inflows, reduce market timing risk for investors, and create a stable asset base for the company. The operational complexity of managing millions of small transactions was offset by the stability and growth these brought.

Customer acquisition and retention strategies reflect deep market understanding. Total Live Accounts stood at 24.3 million as on June 30,2025. Unique customers as identified by PAN or PEKRN now stands at 13.7 million as on June 30,2025 compared to 55.3 million for the industry, a penetration of 25%. This means HDFC AMC manages money for one in four mutual fund investors in India—extraordinary market penetration.

The company's approach to costs has been disciplined but not miserly. Employee costs are higher than industry average, reflecting the premium paid for talent. Marketing spending is substantial but focused on brand building rather than product pushing. Technology investments are significant but always tied to clear business outcomes. This balanced approach to cost management has resulted in industry-leading operating margins.

Risk management, often overlooked in discussions of business models, is fundamental to HDFC AMC's approach. Investment risk is managed through diversification, research, and systematic processes. Operational risk is mitigated through robust systems and controls. Regulatory risk is addressed through proactive compliance and engagement with regulators. Reputation risk, perhaps most critical in the trust business of asset management, is managed through conservative practices and transparent communication.

The competitive moat that HDFC AMC has built is multi-layered. Brand trust, particularly important in a market where financial literacy is still developing, is the strongest layer. Distribution reach, especially in smaller cities, creates barriers for new entrants. Performance track record, built over decades, cannot be replicated quickly. Scale economies allow lower costs and better talent acquisition. These advantages reinforce each other, creating a formidable competitive position.

VII. The HDFC-HDFC Bank Merger Impact (2023)

The Boards of both the companies at their respective meetings held today noted that the merger would be effective from July 1, 2023. This merger, valued at $40 billion, represented the largest transaction in Indian corporate history and fundamentally altered the landscape for HDFC AMC.

The merger's impact on HDFC AMC was both immediate and profound. Post merger, the key HDFC Bank subsidiaries include HDFC Securities Ltd., HDB Financial Services Ltd., HDFC Asset Management Co. Ltd, HDFC ERGO General Insurance Co. Ltd., HDFC Capital Advisors Ltd. and HDFC Life Insurance Co. HDFC AMC transformed from being a subsidiary of a housing finance company to being part of India's largest private sector bank—a shift that brought both opportunities and challenges.

The ownership structure change was significant. HDFC Bank inherited HDFC Limited's stake in the AMC, making it the majority shareholder with approximately 52.48% ownership. This created interesting dynamics. Banks globally have coveted asset management businesses for their fee income and low capital requirements. HDFC Bank now had direct ownership of one of India's most profitable AMCs, but also had to navigate potential conflicts of interest and regulatory scrutiny.

It also marks the transformation of HDFC Bank into a financial services conglomerate that offers a full suite of financial services, from banking to insurance, and mutual funds through its subsidiaries. So far, the Bank was a distributor for these products. This transformation from distributor to owner changed incentive structures. HDFC Bank's massive customer base—over 80 million—became an even more valuable asset for cross-selling mutual funds.

The distribution synergies were immediately apparent. HDFC Bank's extensive branch network, digital platforms, and customer relationships could be leveraged more effectively. The bank's relationship managers could now offer mutual funds as proprietary products rather than third-party investments. The trust customers placed in HDFC Bank for their banking needs could be extended to investment products.

However, the merger also brought complexities. Regulatory requirements for banks owning AMCs are stringent. Chinese walls need to be maintained to prevent information leakage. The bank cannot show preference to its AMC subsidiary in distribution, maintaining arm's length relationships. SEBI and RBI both scrutinize these relationships carefully to ensure no unfair advantages are created.

For now, RBI has approved the transfer of HDFC Life (life insurance) and HDFC Ergo (general insurance) holdings to HDFC Bank, with the bank allowed to acquire a majority stake in both. HDFC's stake in HDFC AMC has also moved to the bank. This created a comprehensive financial services offering under one umbrella, potentially the most complete in Indian financial services.

The cultural integration aspects were subtle but important. HDFC Limited had a more entrepreneurial, relationship-driven culture. HDFC Bank, while also customer-focused, operated with more systematic processes and controls. HDFC AMC, sitting between these two cultures, had to navigate the transition carefully. The company maintained its operational independence while aligning with the bank's broader strategic objectives.

Market perception of the merger's impact on HDFC AMC was initially mixed. Some investors worried about potential conflicts of interest or the AMC becoming too dependent on bank distribution. Others saw the enormous cross-selling potential and balance sheet strength of the parent. Shares of HDFC Bank Ltd and HDFC Asset Management Company (AMC) also climbed more than 2 per cent, each. HDFC Life Insurance Company Ltd got the maximum boost as the stock surged 6.63 per cent immediately after merger announcements, indicating overall positive sentiment.

The competitive implications were significant. Other bank-sponsored AMCs like SBI Mutual Fund and ICICI Prudential AMC suddenly faced a more formidable competitor. Independent AMCs worried about distribution access if banks increasingly favored their own subsidiaries. Foreign players reassessed their India strategies given the scale advantages of integrated financial conglomerates.

Technology integration became a priority post-merger. HDFC Bank's digital platforms needed to seamlessly integrate mutual fund transactions. The bank's mobile app, used by millions daily, became a powerful distribution channel for HDFC AMC products. Data analytics capabilities of the bank could be leveraged (within regulatory boundaries) to better understand customer needs and preferences.

The merger also impacted talent management at HDFC AMC. Being part of a larger banking group provided more career opportunities for employees. The bank's resources could be leveraged for training and development. However, maintaining the entrepreneurial spirit and investment focus that defined HDFC AMC's culture became a key management priority.

From a strategic perspective, the merger positioned HDFC AMC uniquely for the next phase of growth in Indian financial services. As India's economy grows and financialization deepens, customers increasingly seek integrated financial solutions. The ability to offer banking, insurance, and investment products through a single trusted brand becomes a powerful proposition.

VIII. Leadership Transition & Future Strategy (2022–Present)

The departure of Prashant Jain in July 2022 marked the end of an era for HDFC AMC. "I could have continued but I felt it is appropriate to move now as all the stars were aligned. The leadership transition at the company is behind, performance has strongly recovered, "value investing" (rational investing is more appropriate in my opinion) has proven its mettle once again over GAAP (growth at any price) investing and most important the investment team (both equity and debt) at HDFC AMC is second to none in the country and the best that I have had in my career," Jain explained in his farewell letter.

The transition was remarkably smooth, defying skeptics who predicted massive redemptions. At present, HDFC Mutual Fund has appointed Chirag Setalvad as Head - Equities and Shobhit Mehrotra as Head-Fixed income. Setalvad has been part of the investment team at HDFC AMC since inception, except for a brief stint of 2.5 years outside the company between October 2004 and March 2007. Mehrotra has been with the company for over 18 years and is presently managing few fixed income schemes.

The succession planning had been meticulous. Rather than bringing in external stars, HDFC AMC promoted from within, ensuring continuity of investment philosophy and culture. The new leadership team had been groomed over years, understanding not just investment strategies but also the nuances of managing retail investor expectations in India.

The post-Jain era strategy reflects both continuity and evolution. The core investment philosophy remains unchanged—focusing on quality businesses at reasonable valuations. But there's greater emphasis on team-based decision making rather than individual star power. Multiple fund managers now share responsibility for large funds, reducing key person risk.

The company has accelerated its push into new areas. Passive funds, largely ignored during the Jain era when active management was delivering strong alpha, are now a focus area. QAAUM in actively managed equity-oriented funds i.e. equity oriented QAAUM excluding index funds stood at Rs 4,072 billion for the quarter ended June 30,2024 with a market share of 12.9%. While still dominant in active management, HDFC AMC recognizes the global shift toward passive investing.

Alternative investments represent another growth frontier. The company has launched funds focusing on real estate, infrastructure, and private equity—areas where India's growth story creates enormous opportunities. These products cater to high-net-worth individuals and institutions seeking diversification beyond traditional assets.

Digital transformation has accelerated post-transition. The company is investing heavily in artificial intelligence for customer service, robo-advisory platforms for mass-affluent segments, and blockchain for transaction processing. The goal is to make investing as seamless as e-commerce while maintaining the trust and security paramount in financial services.

The competitive landscape has intensified dramatically. New-age fintech players like Zerodha, Groww, and Paytm Money have democratized mutual fund investing, acquiring millions of customers with zero-commission models. International players are entering through strategic partnerships. Passive funds and ETFs are gaining market share. HDFC AMC's response has been measured but decisive—competing on trust and track record rather than pricing.

Environmental, Social, and Governance (ESG) investing, still nascent in India, is becoming a strategic priority. HDFC AMC has launched ESG-focused funds and integrated ESG criteria into investment processes. This isn't just about following global trends; it's recognition that sustainable investing will become mainstream as Indian investors become more sophisticated.

The company's international ambitions are gradually taking shape. While domestic opportunities remain enormous, HDFC AMC is exploring managing offshore funds for global investors seeking India exposure. Partnerships with international asset managers for knowledge sharing and product development are being strengthened.

Regulatory changes continue to shape strategy. SEBI's restrictions on expense ratios, requirements for direct plans, and guidelines on fund categorization have compressed margins industry-wide. HDFC AMC's response has been to focus on scale and efficiency rather than fighting regulatory changes. The company actively engages with regulators, often pioneering industry best practices.

The talent strategy has evolved significantly. 22 Jul - Q1 FY26 earnings call: 21% AUM growth requires continuous investment in people. The company is hiring from diverse backgrounds—technology, data science, behavioral finance—not just traditional finance. Creating a culture that blends HDFC's traditional values with innovation and agility is an ongoing challenge.

Customer engagement strategies are being revolutionized. The company is moving beyond traditional investor education to behavioral coaching—helping investors avoid common mistakes like panic selling or performance chasing. Digital tools provide personalized insights and nudges to improve investment outcomes.

The role of artificial intelligence and machine learning in investment management is being carefully evaluated. While not replacing human judgment, these tools are enhancing research capabilities, risk management, and operational efficiency. HDFC AMC is investing selectively, focusing on areas where technology provides clear advantages.

Looking ahead, the company's strategy balances multiple priorities: maintaining market leadership in active management while building passive capabilities; serving existing customers while acquiring new ones; preserving margins while investing for growth; maintaining the trust-based culture while embracing innovation. This balancing act defines HDFC AMC's evolution from a traditional asset manager to a comprehensive wealth solutions provider.

IX. Playbook: Key Lessons & Strategies

The HDFC AMC story offers a masterclass in building and scaling a financial services business in an emerging market. The playbook that emerges from their journey contains lessons that transcend geography and industry, offering insights for anyone building in markets characterized by low trust, rapid growth, and evolving regulations.

First, the power of patient capital cannot be overstated. HDFC AMC didn't chase quick wins or hot trends. The company took nearly five years to become profitable, focusing on building infrastructure, distribution, and trust rather than maximizing short-term returns. This patience, rare in today's venture-backed world, allowed the company to make decisions with 10-20 year horizons. When competitors were launching complex derivative products during bull markets, HDFC AMC stuck to simple, transparent offerings that investors could understand.

Building trust in a low-trust market requires extraordinary commitment to transparency and conservatism. India in the early 2000s had seen numerous financial scams and failures. Investors, particularly retail ones, were deeply skeptical of market-linked products. HDFC AMC's response wasn't marketing campaigns but consistent, conservative behavior. The company often held higher cash levels than competitors during uncertain times, sacrificing returns for safety. It disclosed more information than required, published detailed investment rationales, and admitted mistakes openly. This approach built trust slowly but surely.

The distribution advantage in India's complex geography proved decisive. India isn't one market but thousands of micro-markets, each with unique characteristics. HDFC AMC understood that distribution wasn't just about reach but about relationships. The company invested heavily in training independent financial advisors, often conducting sessions in regional languages. It established offices in tier-2 and tier-3 cities when competitors focused only on metros. This distributed presence created a moat that technology alone cannot replicate.

Managing the star fund manager paradox required delicate balancing. Prashant Jain's exceptional track record was HDFC AMC's greatest asset but also its biggest risk. The company managed this by building strong institutional processes around the star. Investment decisions, while ultimately Jain's responsibility, involved team discussions and devil's advocacy. Risk management operated independently. Succession planning started years before it was needed. The message was clear: individuals might be stars, but the institution endures.

Navigating regulatory changes requires a partnership mindset rather than adversarial approach. SEBI's regulations often compressed margins and increased compliance costs. Rather than resisting or finding loopholes, HDFC AMC engaged constructively with regulators. The company often implemented higher standards than required, understanding that in financial services, regulatory alignment is a competitive advantage. This approach paid off when regulations later moved in directions HDFC AMC had already anticipated.

The art of managing Other People's Money at scale involves profound psychological understanding. Money is emotional, not rational. HDFC AMC recognized that investors need hand-holding during market volatility, education during calm periods, and restraint during euphoria. The company's investor communication struck a balance between sophistication and simplicity, ensuring both institutional and retail investors felt informed and confident.

Technology adoption should be purposeful, not fashionable. HDFC AMC was never a technology leader, but it invested steadily in systems that improved customer experience and operational efficiency. The company avoided expensive experiments with unproven technologies, focusing instead on reliable, scalable solutions. This pragmatic approach meant fewer headlines but better returns on technology investments.

The importance of cultural alignment in financial services cannot be underestimated. HDFC AMC inherited a culture of conservatism and customer focus from its parent. This culture acted as an invisible hand guiding thousands of daily decisions. New hires were selected as much for cultural fit as technical skills. This cultural consistency created predictability and trust, essential in managing people's life savings.

Scale economics in asset management create winner-take-all dynamics. As HDFC AMC grew, its costs per unit of AUM declined, allowing lower fees while maintaining margins. This created a virtuous cycle: lower fees attracted more assets, which further reduced costs. Competitors found it increasingly difficult to match HDFC AMC's pricing while maintaining profitability. Understanding and exploiting these dynamics early proved crucial.

The value of brand in financial services extends beyond marketing. The HDFC brand, built over decades, stood for trust, conservatism, and customer focus. This brand equity reduced customer acquisition costs, increased retention, and provided pricing power. More importantly, it attracted quality talent and distribution partners who wanted association with a respected institution.

Cross-selling within financial conglomerates requires careful orchestration. The HDFC group's various entities—bank, insurance, AMC—served overlapping customer bases. But cross-selling couldn't be pushy or inappropriate. HDFC AMC benefited from warm introductions from group companies but had to win business on merit. This balanced approach maximized synergies while maintaining customer trust.

X. Bear vs. Bull Case Analysis

The future of HDFC AMC presents a fascinating dichotomy of enormous opportunity shadowed by significant challenges. Understanding both the bull and bear cases is essential for grasping where this financial juggernaut might head in the coming decade.

The Bull Case: Riding India's Financialization Wave

The optimistic view starts with the massive underpenetration of mutual funds in India. With mutual fund assets at roughly 15% of GDP compared to over 100% in developed markets, the runway for growth appears endless. India's demographic dividend—400 million millennials entering peak earning years—creates a natural tailwind for financial savings. As this generation, more comfortable with market risks than their parents, accumulates wealth, mutual funds become the natural destination.

31.4% y/y rise in December-qtr consol net profit demonstrates that HDFC AMC continues to capture disproportionate value from this growth. The company's 25% share of unique mutual fund investors in India positions it perfectly to benefit from increasing financialization. Every percentage point increase in mutual fund penetration translates to potentially ₹5-10 trillion in additional AUM.

The HDFC Bank synergies post-merger multiply growth possibilities. With access to 80 million banking customers and thousands of branches, cross-selling opportunities are enormous. The bank's digital platforms, used by millions daily, become powerful distribution channels. The trust customers place in HDFC Bank for loans and deposits naturally extends to investment products. Conservative estimates suggest the bank channel alone could drive 20-30% annual AUM growth.

India's economic growth story strengthens the bull case. As GDP grows at 6-7% annually and corporate earnings compound, equity markets should deliver attractive returns over the long term. This creates wealth effects that draw more investors to mutual funds. HDFC AMC's track record of generating alpha positions it to capture premium market share in equity products, which command higher fees.

Regulatory tailwinds, often overlooked, are becoming significant. The government's push for financial inclusion, tax benefits for equity investments, and pension reforms all channel savings toward mutual funds. The National Pension System, where HDFC AMC is a major player, could become a multi-trillion rupee opportunity as pension coverage expands.

Technology democratization works in HDFC AMC's favor, contrary to conventional wisdom. While fintech platforms have made investing easier, they've also expanded the market dramatically. HDFC AMC's brand trust becomes even more valuable when investors have infinite choice. The company's digital investments ensure it captures both traditional and digital-native customers.

International opportunities remain largely untapped. Global investors seeking India exposure increasingly prefer local managers with on-ground expertise. HDFC AMC could manage offshore funds, partner with global asset managers, or even acquire international capabilities. The brand's association with India's growth story resonates globally.

The Bear Case: Structural Headwinds and Disruption Risks

The pessimistic view starts with margin compression, already evident in recent years. SEBI's regulations have consistently pushed expense ratios lower, and this trend will likely continue. Direct plans, now 25-30% of AUM, eliminate distributor commissions but also reduce fees. As the industry matures, the race to the bottom on fees could devastate profitability.

Passive funds represent an existential threat that's growing rapidly. Global markets have seen active management's share plummet as investors realize most active managers don't beat indices after fees. India's markets are becoming more efficient, reducing alpha opportunities. If passive funds grow from current 15% to 40-50% of AUM over the next decade, HDFC AMC's business model faces fundamental challenges.

Competition is intensifying from unexpected quarters. Technology platforms offer investing at zero commissions, subsidized by other revenue streams. International giants like BlackRock and Vanguard are entering India through partnerships. New-age wealth managers use technology and personalization to capture high-value customers. Even traditional competitors are becoming more aggressive, compressing market share.

The key person risk, while managed, hasn't disappeared. The post-Prashant Jain era is still being written. While the transition has been smooth so far, sustained underperformance could trigger redemptions. Building new star fund managers takes decades, not years. The institution's strength is being tested in real-time.

Market volatility impacts both AUM and flows. A significant market correction could reduce equity AUM by 30-40%, directly impacting revenues. More concerningly, retail investors traumatized by losses might avoid equity funds for years, as happened after the 2008 crisis. HDFC AMC's high exposure to equity funds makes it vulnerable to market cycles.

Regulatory risks remain omnipresent. SEBI could further cap expense ratios, mandate additional disclosures, or restrict distribution practices. RBI's oversight of HDFC Bank's ownership adds another regulatory layer. Any regulatory action against the parent bank could impact the AMC's reputation and business.

Technological disruption could fundamentally alter asset management. Robo-advisors could eliminate the need for traditional fund management. Artificial intelligence might democratize alpha generation. Blockchain could enable peer-to-peer investing without intermediaries. While these changes seem distant, technology transitions can happen rapidly.

Customer behavior shifts pose risks. Younger investors show less brand loyalty, more fee sensitivity, and greater willingness to switch providers. The relationship-based model that worked for decades might not resonate with digital natives. DIY investing through direct stocks or international markets could bypass mutual funds entirely.

The Balanced View

Reality likely lies between these extremes. HDFC AMC will probably maintain market leadership but with compressed margins. The company will capture significant absolute growth even if market share declines marginally. Technology will be both threat and opportunity, requiring continuous adaptation. The true test will be generating consistent alpha in increasingly efficient markets while managing costs in a regulated environment.

XI. Epilogue & Reflections

What would success look like for HDFC AMC in ten years? The answer transcends simple metrics like AUM or profitability. Success would mean democratizing wealth creation for millions of Indian families, helping them achieve financial goals previously impossible. It would mean navigating the transition from active to passive investing while maintaining relevance. Most importantly, it would mean preserving trust across generational and technological shifts.

The lessons from HDFC AMC's journey extend far beyond Indian financial services. Building financial institutions in emerging markets requires patient capital, deep local understanding, and unwavering focus on trust. The company's success demonstrates that in markets where formal financial systems are still developing, the opportunity isn't just in serving existing demand but in creating new markets through education and innovation.

For global asset managers, HDFC AMC's story offers both inspiration and warning. The inspiration comes from seeing how a local player can dominate despite global competition. The warning is that success in emerging markets requires more than transplanting developed market strategies. It demands humility, adaptation, and long-term commitment that quarterly earnings pressures often preclude.

The India opportunity in context remains extraordinary. A country adding $500 billion to GDP annually, with a savings rate exceeding 30%, where financial markets are still nascent, presents perhaps the largest wealth management opportunity globally. HDFC AMC's journey from managing ₹3,000 crore to ₹6 lakh crore might be just the first chapter in a much larger story.

The broader implications for building financial institutions in emerging markets are profound. Trust, once lost, takes generations to rebuild. Regulatory partnership yields better outcomes than confrontation. Technology amplifies but doesn't replace human relationships. Scale advantages in financial services create powerful moats but also responsibilities. These lessons apply whether building in India, Southeast Asia, Africa, or Latin America.

The human element in HDFC AMC's story deserves special mention. Behind the numbers are thousands of employees who chose to build careers in asset management when technology or banking offered quicker rewards. Millions of investors who trusted their savings to mutual funds when fixed deposits seemed safer. Thousands of distributors who educated clients about market risks when selling insurance paid better commissions. These individual choices, aggregated over decades, created an institution.

XII. Recent News

HDFC AMC's recent performance demonstrates resilient execution amid challenging conditions. HDFC Asset Management Company (AMC) on January 14 reported a net profit of Rs 641 crore in the October-December quarter (Q3) of financial year 2025 (FY25). This marks an increase of 31% from the net profit reported in Q3 of the previous financial year (FY24). This robust growth, despite market volatility and regulatory pressures, validates the company's strategic positioning.

The revenue growth story is equally impressive. rev up 39.3% y/y in the recent quarter showcases the company's ability to grow both AUM and maintain pricing discipline. The market has responded positively, with HDFC Asset Management NSE:HDFCAMC climbs 3.5% to 3,999.95 rupees following results announcement.

Analyst sentiment has turned increasingly bullish. At least six brokerages hike PT post results; three upgrade stock - LSEG** Centrum Broking says co reported strong Q3 numbers despite market volatility; upgrades to "buy", hikes PT by 9% to 4,990 rupees. The consensus view appears to be that HDFC AMC is successfully navigating the post-Jain transition while capitalizing on merger synergies.

The company continues to strengthen its market position with steady growth in systematic transactions and unique customers. The digital transformation initiatives are showing results, with online transactions growing substantially. New product launches in passive funds and alternative investments are gaining traction, diversifying revenue streams beyond traditional active management.

XIII. Links & Resources

For deeper understanding of HDFC AMC and the Indian asset management industry, several resources prove invaluable:

Company Resources: - HDFC AMC Investor Relations: Quarterly results, annual reports, and investor presentations - HDFC Mutual Fund Website: Product information, NAVs, and fund factsheets - Regulatory Filings: BSE and NSE disclosures for real-time updates

Industry Resources: - AMFI (Association of Mutual Funds in India): Industry statistics and trends - SEBI: Regulatory circulars and policy changes - Value Research: Independent fund analysis and ratings - Morningstar India: Fund performance analytics and research

Books and Publications: - "The Indian Mutual Fund Industry" by various authors - comprehensive industry overview - HDFC Group's annual reports - insights into strategic thinking - Prashant Jain's investor letters - investment philosophy and market views - Economic surveys and RBI reports - macroeconomic context

Academic Research: - Papers on emerging market asset management from IIMs and ISB - Studies on Indian household savings behavior - Research on financial inclusion and market development

The HDFC AMC story continues to evolve, shaped by market forces, regulatory changes, and strategic choices. What remains constant is the company's central role in India's financial transformation—a position earned through decades of patient building, conservative management, and unwavering focus on investor interests. As India's economy grows and millions more enter the formal financial system, HDFC AMC's next chapter promises to be as significant as its remarkable past.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube