Gallantt Ispat: From Kolkata Metal Trader to India's Steel Underdog

I. Cold Open & The Puzzle

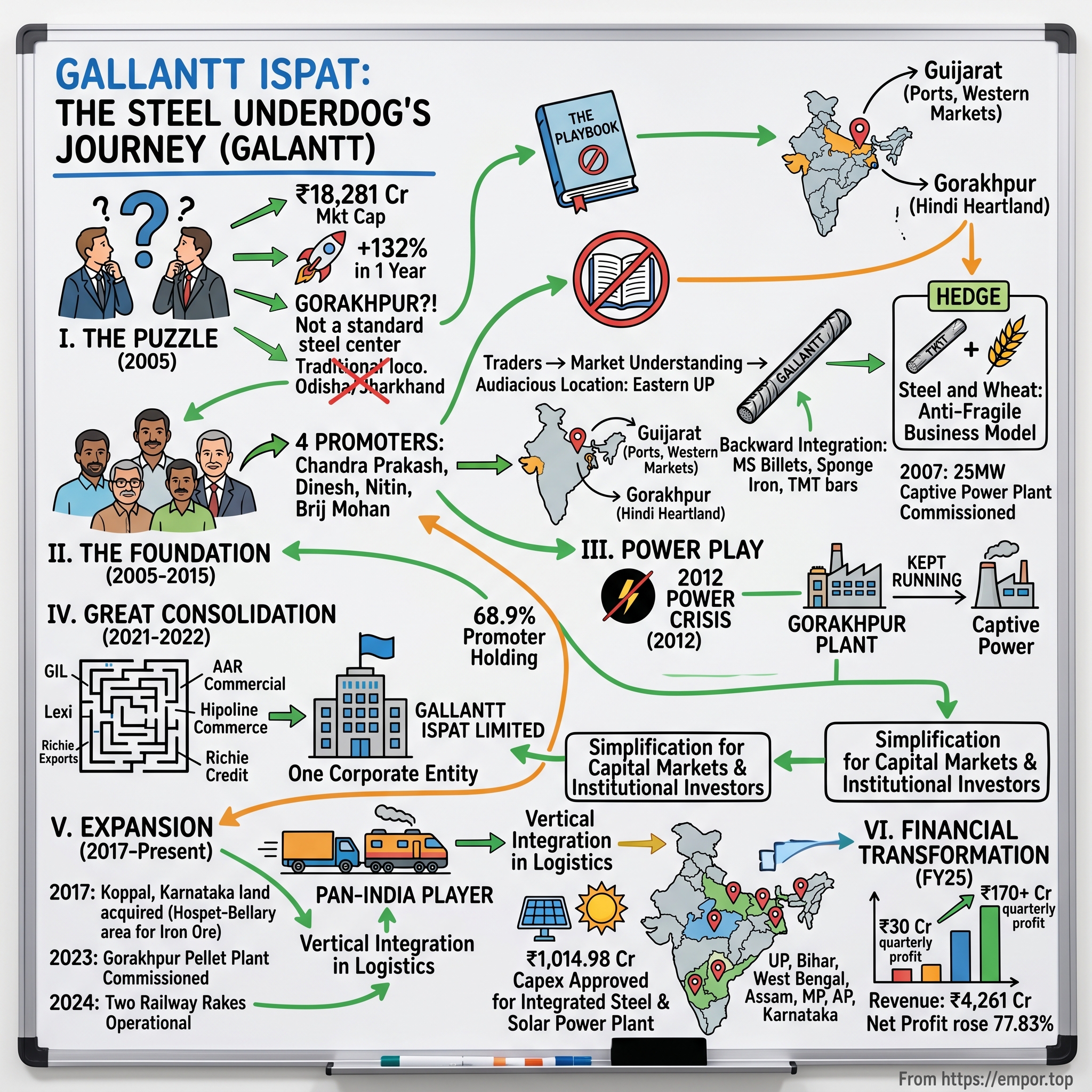

The numbers tell a story that shouldn't exist. ₹18,281 crores in market capitalization, up 132% in a single year. In the brutal, capital-intensive world of Indian steel—where giants like Tata Steel and JSW have spent decades and billions building moats—a company founded just 19 years ago in Kolkata has somehow carved out a multi-billion dollar niche. Not in Mumbai, not in the iron ore-rich corridors of Odisha or Jharkhand, but in Gorakhpur, Eastern Uttar Pradesh—a place better known for its railway junction than its industrial prowess. This is the Gallantt Ispat puzzle that shouldn't make sense in the steel industry playbook. Market cap of ₹17,122 Crore (up 97.1% in 1 year), commanding valuations that would make established steel majors envious—trading at 6.02 times its book value. Yet this isn't SAIL with its government backing, or JSW with its billions in capital. This is a company that started life as Gallantt Metal Limited in a Kolkata office, far from the iron ore mines, far from the traditional centers of Indian steel power.

The counterintuitive geography alone should have killed this venture. Eastern Uttar Pradesh? Gorakhpur? In 2005, when infrastructure meant the Golden Quadrilateral and everyone was rushing to set up shop near ports or mines, four promoters—Chandra Prakash Agrawal, Dinesh R Agarwal, Nitin Kandoi and Brij Mohan Joshi—decided the future of Indian steel lay in the Hindi heartland. They weren't wrong. They were early.

What unfolds from here is not your typical commodity story. The company is engaged in the business of Iron & Steel, Agro, Power and Real Estate—yes, you read that right. A steel company that also mills wheat flour and builds apartments. In the brutally cyclical world of commodities, where giants have fallen to single bad quarters, Gallantt built something different: an anti-fragile business model that confused analysts but delivered returns.

The roadmap ahead takes us through three distinct acts of corporate evolution. First, the scrappy startup years when commercial operations began with little fanfare in December 2005. Then, the great consolidation of 2021-2022—a complex corporate restructuring that would make investment bankers dizzy. Finally, the current expansion phase, where a company that shouldn't exist is deploying over ₹1,000 crores in fresh capacity while the steel cycle turns.

This is that story—of how a Kolkata trading mindset met UP's industrial ambitions, how wheat flour subsidized steel dreams, and how sometimes the best place to build a steel empire is exactly where no one expects you to.

II. Origins: The Kolkata Beginning (2005)

February 2005. The air in Kolkata's business district hung thick with humidity and opportunity. India had just unveiled its National Steel Policy with the long-term goal of establishing a modern and efficient steel industry, aiming to achieve over 100 million metric tonnes of steel per year by 2019-20 from the 2004-05 level of 38 mt—implying annual growth of around 7.3% per year. The country was in the grip of an infrastructure transformation that would redefine its economic trajectory for the next two decades.

Into this moment stepped four men with a vision that defied conventional wisdom. Gallantt Metal Limited was incorporated in February 2005 at Kolkata, promoted by Chandra Prakash Agrawal, Dinesh R Agarwal, Nitin Kandoi and Brij Mohan Joshi. These weren't steel barons with generational wealth. They were traders who understood markets, who had watched the flow of metal through India's arteries and spotted an inefficiency so glaring it bordered on absurd.

The geography alone was audacious. While established players clustered around iron ore mines in Odisha and Jharkhand, or built near ports for easy import access, the Gallantt founders looked at a map and saw something different. Eastern Uttar Pradesh—dismissed by most as an industrial backwater—sat at the crossroads of India's most populous states. Here was a region crying out for steel, surrounded by millions of consumers, yet forced to transport materials from hundreds of kilometers away.

The company was established to set up a plant in Kutch, Gujarat, for manufacturing Sponge Iron, M.S. Billets, Re-Rolled products (TMT bars) with a captive power plant. But the real strategic masterstroke was the dual-location strategy. Gujarat gave them access to ports and western markets. Gorakhpur would serve the Hindi heartland—UP, Bihar, MP—markets that big players had essentially ceded through neglect.

The timing was more than fortuitous; it was prescient. Construction and infrastructure were estimated to account for roughly 40 per cent of steel consumption, with India's consumption of steel relative to the size of its economy very low by international standards. The founders weren't just betting on steel—they were betting on India's transformation from a country of villages to a nation of cities.

What made Gallantt different from day one was its refusal to think like a steel company. Where others saw vertical integration as building bigger furnaces, Gallantt's founders saw it as controlling the entire value chain—from raw material to the construction site. The diversification DNA wasn't an afterthought; it was embedded in the company's genetic code from inception.

The company positioned itself to be engaged in the business of Iron & Steel, Agro, Power and Real Estate. This wasn't corporate attention deficit disorder. It was a sophisticated understanding of India's commodity cycles. When steel margins compressed, wheat flour could carry the company. When power shortages crippled competitors, their captive generation would keep furnaces running.

The initial vision extended beyond mere production. In an industry where relationships were everything, where payment terms could stretch for months, where quality was often compromised for volume, Gallantt would build something radical: a brand in a commodity business. The "Gallantt" name would stand for consistency in a market plagued by volatility.

By December 2005, less than a year after incorporation, the company was ready for its first commercial operations. The speed of execution was breathtaking—in an industry where projects routinely faced multi-year delays, Gallantt had gone from incorporation to production in ten months. This wasn't luck. It was the trader's mindset applied to manufacturing: move fast, stay lean, capture opportunity before it evaporates.

The Eastern UP bet was already paying dividends. While competitors fought over customers in saturated markets, Gallantt found itself with virtually no competition in its immediate geography. Local construction companies, previously forced to source from distant suppliers, suddenly had a reliable local partner. The transportation cost advantage alone—often 10-15% of delivered cost—gave Gallantt pricing power that shouldn't have existed in a commodity business.

But perhaps the most prescient decision was the commitment to backward integration from the start. Phase I commercial operations started in December 2005, and by March 2007, the Phase II project was commissioned with a 25MW Captive Power Plant. In a country where power cuts could shut down operations for hours, where grid electricity costs could swing wildly with coal prices, having captive power wasn't just an advantage—it was survival.

As 2005 drew to a close, Gallantt Metal Limited had laid the foundation for something unprecedented: a steel company that thought like a trader, operated like a conglomerate, and positioned itself where no one else wanted to be. The Kolkata beginning was just that—a beginning. The real story was about to unfold in the furnaces of Gorakhpur and the fields of Eastern UP.

III. The First Decade: Building the Foundation (2005-2015)

The morning of September 15, 2008, should have been the death knell for a company like Gallantt. Lehman Brothers had just collapsed. Steel prices, which had soared above $1,000 per ton earlier that year, were in freefall. Commodity-related stocks had soared as oil traded above $140/barrel for the first time and steel prices rose above $1,000 per ton, but lack of investor confidence in bank solvency and declines in credit availability led to plummeting stock and commodity prices in late 2008 and early 2009. For a three-year-old steel company operating out of Gorakhpur with limited capital buffers, this should have been game over.

But Gallantt didn't just survive 2008—it thrived in the aftermath. The secret lay in decisions made years before the crisis hit. Company was promoted by Chandra Prakash Agrawal, Dinesh R Agarwal, Nitin Kandoi and Brij Mohan Joshi, and these promoters had built something unusual: a business designed for volatility, not stability.

The integrated model was already operational: Sponge Iron → MS Billets → TMT Bars. Each step in the chain provided optionality. When finished steel prices crashed, they could sell semi-finished products to other mills desperate for inventory. When raw material costs spiked, their sponge iron capacity gave them a hedge. This wasn't theoretical—it was playing out in real-time as competitors shuttered furnaces across India.

In December 2005, they started their Phase I commercial operations and in March 2007, the Phase II project was commissioned, i.e. the 25MW Captive Power Plant. That power plant, commissioned just 18 months before the crisis, became their lifeline. While other mills faced production cuts due to erratic power supply and soaring grid electricity costs, Gallantt's furnaces kept running. The mathematics were brutal but simple: every hour of downtime meant lakhs in losses. Every megawatt of captive power meant independence from a collapsing grid.

Then there was the wheat flour business—the decision that made industry veterans shake their heads. Why would a steel company mill wheat? In 2008, the answer became crystal clear. Crude oil prices showed a dramatic decline from $ 145 per barrel on July 3, 2008 to around $60. Inflation which had reached 12:76 per cent in August, has now declined below 11 per cent. While steel demand evaporated, food demand remained rock solid. The wheat products—Atta, Maida, Suji, Bran—generated steady cash flows when steel revenues vanished. It was the ultimate hedge: when construction stopped, people still needed roti.

Since 2009-10 they have taken many strategic decisions to increase their volume and profitability, and have expanded market in Gujarat, Maharashtra and Rajasthan. This expansion timing was counterintuitive but brilliant. While competitors were retrenching, Gallantt was buying market share at distressed prices. They weren't just surviving the crisis; they were using it as a strategic opportunity.

The geographic expansion followed a specific logic. Gujarat gave them access to ports and export markets. Maharashtra meant proximity to Mumbai's insatiable construction demand. Rajasthan opened up the Delhi-NCR corridor. Each state was chosen not randomly but as a chess move in a larger game—surrounding the Hindi heartland with a ring of supply points, each one a day's truck journey from their core markets.

Building the "Gallantt" brand during this period seemed almost quixotic. Who builds brands in commodities during a global financial crisis? But the promoters understood something fundamental about Indian markets: trust matters more than price, especially in chaos. While competitors were dumping inventory at any price, Gallantt maintained quality standards. The products are sold under the brand name "Gallantt" in the states of Uttar Pradesh, Bihar, West Bengal, Assam, Madhya Pradesh, Andhra Pradesh and Karnataka.

The company's approach to customer relationships during the crisis years became legendary in Eastern UP's construction circles. When liquidity dried up and builders couldn't pay, many steel companies cut supplies immediately. Gallantt extended credit selectively, betting on relationships over short-term cash. They identified builders who would survive and backed them through the crisis. When construction resumed in 2010, these builders remembered.

By 2012, a curious thing had happened. The company that should have been a crisis casualty had emerged stronger. Revenue grew steadily even as the broader steel sector struggled with overcapacity and Chinese dumping. The diversification that analysts mocked—steel and wheat, power and real estate—had created an anti-fragile business model.

The lessons from this period would define Gallantt's DNA permanently. First, backward integration wasn't just about cost savings; it was about survival. Second, unrelated diversification that seemed irrational in good times became a lifeline in bad times. Third, building in Tier-2 cities meant lower costs but also unexpected resilience—these markets recovered faster from the crisis than metropolitan India.

They have also acquired 106 acres of land in Koppal, Karnataka for their expansion plans. This 2017 acquisition signaled the next phase: the company wasn't content being Eastern UP's steel champion. They wanted to replicate the model across India's growth corridors. Karnataka represented the southern frontier—proximity to Bangalore's construction boom, access to iron ore from Bellary, and a state government desperate for industrial investment.

The first decade had transformed Gallantt from a trading mindset with manufacturing ambitions into something more complex: a conglomerate disguised as a steel company, a brand builder in a commodity business, a Tier-2 champion with Tier-1 ambitions. The foundation was set. Now came the hard part—scaling without losing what made them special.

IV. The Power Play: Vertical Integration Strategy

The summer of 2012 brought India's power crisis into sharp relief. The largest power failure in history—a cascading blackout that plunged 600 million people into darkness at its peak. For steel manufacturers across the country, it was a catastrophe. In the summer of 2012, India suffered the largest power failure in history – a cascading blackout that plunged 600 million people into darkness at its peak. But in Gorakhpur, the furnaces at Gallantt kept running. Their captive power plants hummed steadily while competitors scrambled for diesel generators or simply shut down.

The economics of captive power in Indian steel were brutal but straightforward. The average reported level of shortages reduces annual plant revenues and producer surplus of the average plant by 5-10%. For steel plants without generators, Plants without generators stop production during outages – as if facing an infinite input tax on electricity. But Gallantt had made its bet early—the 25MW Captive Power Plant commissioned in March 2007 was just the beginning.

What made Gallantt's power strategy different wasn't just having captive generation—many steel plants did. It was the philosophy of complete energy independence embedded in their operational DNA. Electricity-intensive industries consume the cheaper electricity (average price Rs 2.5 per kWhr) available from the grid instead of running their own coal/gas/oil fired captive power plants. The captive power generation capacity by such plants is nearly 53,000 MW, and they are mainly established in steel, fertilizer, aluminium, cement, etc. industries. While others saw captive power as backup, Gallantt saw it as primary infrastructure.

The strategic calculus went deeper than just avoiding outages. Energy costs in steel manufacturing typically account for 15-20% of total production costs. Every percentage point saved on power translated directly to margins. In Eastern UP, where grid power was notoriously unreliable—with shortages and voltage fluctuations that could destroy sensitive equipment—the value of stable, predictable power went beyond mere cost calculations.

Then came the complexity of 2021-2022. In 2021-22, Honorable National Company Law Tribunal, Kolkata Bench and Honorable National Company Law Tribunal, New Delhi Bench, vide their orders dated September 22, 2021 and May 20, 2022 respectively, approved the Scheme of Amalgamation providing for Slump Sale of 18 MW Power Plant of the Company to Gallantt Metal Limited. This wasn't just a corporate restructuring—it was a sophisticated piece of financial engineering that would redefine how the company thought about energy assets.

The 18 MW Power Plant slump sale was part of a larger amalgamation scheme that consolidated multiple entities under one umbrella. Why sell a power plant to yourself through a complex scheme? The answer lay in optimizing capital structure, tax efficiency, and most importantly, creating flexibility in how energy assets were deployed across the growing empire.

The power play extended beyond just generation. Gallantt understood that in India's power-deficit regions, having excess capacity wasn't a liability—it was an asset that could be monetized. When their own steel operations didn't need full capacity, they could sell power to the grid or to neighboring industries desperate for reliable supply. The captive power plant became not just a cost center but a potential profit center.

Shortages more severely affect plants that do not have generators, and generator costs have significant economies of scale. We simulate that as a result, variable profit losses average two to three times larger for small plants compared to large plants. This reality created a massive competitive advantage for Gallantt. Smaller competitors in Eastern UP couldn't justify the capital expenditure for captive power. They remained hostage to the grid, facing production disruptions that Gallantt could exploit by capturing their customers during shortage periods.

The integrated model amplified these advantages. A steel plant with unreliable power faces cascading problems: furnaces cool down, requiring expensive restarts; quality suffers from interrupted processes; delivery schedules slip, destroying customer trust. Gallantt's energy independence meant they could guarantee delivery schedules that competitors couldn't match—a critical differentiator in construction projects with tight timelines.

By 2015, the lessons from integrated players versus standalone mills were clear. Companies like JSW and Tata Steel had built massive integrated complexes with captive power, ports, and mines. But they had done so with billions in capital. Gallantt had achieved similar integration benefits at a fraction of the scale and cost, proving that smart vertical integration didn't require infinite capital—it required strategic thinking about which parts of the value chain truly mattered.

The power infrastructure also enabled Gallantt's diversification strategy. The wheat flour business, which seemed so incongruous with steel, suddenly made more sense when viewed through the lens of capacity utilization. Flour mills could run during off-peak hours when steel production was lower, smoothing out power demand and improving overall asset utilization. Every megawatt-hour generated had to be used or lost—diversification ensured nothing was wasted.

Looking ahead, the company's power strategy positioned it perfectly for India's green transition. With solar and renewable energy becoming increasingly viable, having existing power infrastructure and grid connections meant Gallantt could add renewable capacity incrementally. They weren't starting from zero—they were building on a foundation that competitors lacked.

The vertical integration strategy that began with a 25MW power plant in 2007 had evolved into something more sophisticated: an energy-independent manufacturing ecosystem that could weather any crisis, exploit any opportunity, and guarantee reliability in an unreliable market. This wasn't just about making steel—it was about controlling destiny in a country where a power cut could destroy millions in value in minutes.

V. The Great Consolidation: 2021-2022 Restructuring

The boardroom at Gallantt's Kolkata office in early 2021 must have resembled a war room more than a corporate meeting space. Spread across the table were corporate structure charts that looked like abstract art—boxes connected by dotted lines, solid lines, arrows pointing in every direction. Five companies, multiple shareholders, cross-holdings, inter-company transactions that would make an auditor's head spin. This was the legacy of 16 years of opportunistic growth, and it was becoming a liability.

The trigger for what would become one of Indian steel's most complex corporate restructurings wasn't crisis—it was ambition. The company had grown like a banyan tree, spreading roots and branches organically, creating subsidiaries and affiliates as opportunities arose. But to access capital markets seriously, to attract institutional investors, to eventually rival the giants, they needed simplicity. They needed to become Gallantt Ispat Limited.

The scheme was breathtaking in its complexity. Gallantt Ispat Limited (GIL), AAR Commercial Company Limited, Hipoline Commerce Private Limited, Lexi Exports Private Limited and Richie Credit and Finance Private Limited would all amalgamate with Gallantt Metal Limited. Each entity had its own history, its own assets, its own stakeholder interests. The negotiations must have been Byzantine—convincing promoters to exchange shares, aligning valuations, managing tax implications.

The NCLT applications alone would have filled filing cabinets. The Kolkata Bench and New Delhi Bench had to be convinced that this wasn't financial engineering for the sake of it, but a genuine business reorganization. The orders dated September 22, 2021 and May 20, 2022 respectively, approved the Scheme of Amalgamation, but those dates mask months of legal arguments, creditor meetings, and shareholder negotiations.

Why go through this corporate root canal? The answer lay in what Gallantt had become versus what it needed to be. The fragmented structure made sense when they were traders becoming manufacturers, when each new venture needed ring-fencing from the others. But now, with revenues in the thousands of crores, with institutional investors circling, with expansion plans that required serious capital, the structure had become a straitjacket.

The 18 MW Power Plant slump sale embedded within the amalgamation was particularly clever. By selling the asset to the amalgamated entity before the merger, they could optimize the tax treatment, clean up inter-company loans, and create a cleaner asset base for the merged entity. It was financial engineering at its finest—completely legal, utterly complex, and ultimately value-creating.

On June 2022, Gallantt Metal Limited officially became Gallantt Ispat Limited. The name change was more than cosmetic. "Ispat"—the Hindi word for steel—signaled a shift from trading roots to manufacturing destiny. This wasn't a metal trading company that happened to make steel; this was a steel company, period. The messaging to markets was clear: take us seriously.

The post-merger integration challenges were immense. Five company cultures had to become one. Accounting systems had to be unified. Vendor contracts had to be renegotiated. Employee contracts had to be harmonized. The company essentially had to rebuild its administrative backbone while keeping the furnaces running and customers satisfied.

But the benefits started showing almost immediately. The consolidated balance sheet was stronger than the sum of its parts. Inter-company transactions that had clouded the financial statements disappeared. The debt-to-equity ratio improved as inter-company loans were eliminated. Suddenly, Gallantt's true profitability became visible to external observers.

The timing of the consolidation was prescient. India's infrastructure boom was accelerating post-COVID. Steel demand was surging. Capital was cheap and looking for growth stories. A complex, opaque corporate structure would have been a handicap in accessing this opportunity. The clean, consolidated structure made Gallantt investible for a new class of shareholders.

The promoter holding at 68.9% post-consolidation showed another strategic benefit. The restructuring had been accomplished without diluting promoter control. The founders who had started this journey in 2005 still held the reins firmly, but now they had a vehicle that could access public markets efficiently when needed.

The consolidation also enabled better capital allocation. Previously, cash trapped in one entity couldn't easily be deployed to another's opportunities. Now, with a single corporate entity, capital could flow to its highest and best use instantly. If the Karnataka expansion needed funds, they didn't need complex inter-company loans—they could simply allocate capital internally.

Perhaps most importantly, the restructuring cleared the path for the next phase of expansion. The company further invested Rs. 1.80 crores to make Gallantt Metalliks Limited a wholly owned subsidiary, effective from May 10, 2022. This wasn't just tidying up—it was preparing for war. The steel industry was consolidating globally, and Gallantt needed a structure that could participate in that consolidation, whether as acquirer or as a formidable standalone player.

The great consolidation of 2021-2022 transformed Gallantt from a confederation of related businesses into a unified industrial force. The complex became simple. The opaque became transparent. The family business became an institution. What emerged from the NCLT courtrooms and boardroom negotiations wasn't just a cleaner corporate structure—it was a company ready to compete with anyone, anywhere, on any terms.

VI. The Expansion Years: Karnataka & Beyond (2017-Present)

The dusty plains of Koppal district in Karnataka, 2017. A team from Gallantt stood surveying 106 acres of barren land, the Karnataka sun beating down mercilessly. To most observers, this looked like nowhere—300 kilometers from Bangalore, in a district known more for drought than development. But to Gallantt's expansion team, this was the future. They have also acquired 106 acres of land in Koppal, Karnataka for their expansion plans.

The choice of Koppal wasn't random. This corridor is proposed to be located around the Hospet-Bellary area in the state. This area is known to be rich in iron ore. The steel zone will cover districts like Bagalkot, Gadag, Koppal, Haveri, Raichur, and Bellary. Karnataka has emerged as a critical player in India's steel industry, contributing 13.7% to the country's total steel production. With an estimated 2 billion metric tonnes of iron ore reserves, the state continues to supply a significant portion of India's raw material requirements for steel production.

The Karnataka expansion represented a fundamental shift in Gallantt's ambitions. This wasn't about serving local markets anymore—this was about becoming a national player. The southern market was different from the Hindi heartland. Here, they would compete directly with JSW's Vijayanagar plant, one of India's largest integrated steel facilities. The audacity was breathtaking.

But Gallantt had learned something crucial over their first decade: in commodity businesses, logistics is destiny. The Koppal location sat strategically between iron ore mines and consumption centers. Proposed steel plant is strategically located in Koppal district of Karnataka and has seamless road as well as railway access & to major ports. More importantly, it gave them access to southern India's booming construction market—Bangalore's tech parks, Hyderabad's pharma cities, Chennai's auto corridor.

The real masterstroke came in 2023 when The Company commissioned a Pellet Plant at Gorakhpur facility with a capacity of 7,92,000 MTPA in 2023. Pelletization wasn't sexy, but it was transformative. Iron ore pellets command premium prices over raw ore, travel better, and feed more efficiently into blast furnaces. While competitors fought over raw ore supplies, Gallantt was moving up the value chain.

Then came the railway gambit. The Company acquired two railway rakes, with an investment of Rs.55 crore and made them operational in 2024. To outsiders, buying railway rakes seemed like a distraction. To Gallantt, it was about controlling their destiny. In India, where railway freight allocation could make or break a commodity business, owning your own rakes meant guaranteed transportation capacity. No begging for allocations, no delays during peak season, no surprise freight hikes.

The economics were compelling. A single rake could move 4,000 tonnes of steel. With two rakes making multiple trips monthly, Gallantt could move nearly 100,000 tonnes annually with complete control over timing and routing. In a business where transportation costs could be 10-15% of delivered price, this vertical integration into logistics was genius disguised as capital expenditure.

The expansion years also saw Gallantt's most aggressive capacity additions yet. The Board of Gallantt Ispat at its meeting held on 16 April 2025 has approved capex of Rs 1,014.98 crore for capacity addition at its integrated steel plants at Gorakhpur and setting up of captive solar power plant. Further, the total project capex shall be funded by the company through internal accruals without borrowing any debt. Since expansion in capacities of above units are brown field expansion projects company has scheduled the completion of the Project tenure by March 2026.

The decision to fund expansion entirely through internal accruals was both conservative and bold. Conservative because it avoided leverage in a cyclical industry. Bold because it signaled supreme confidence in cash generation ability. This wasn't a company stretching for growth—this was measured, calculated expansion funded by operational excellence.

The solar power component of the expansion revealed another evolution in thinking. From coal-fired captive power to solar—Gallantt was future-proofing against both carbon regulations and energy costs. In an industry where environmental compliance was becoming existential, being ahead of the curve on green energy was more than ESG box-ticking—it was competitive advantage.

Meanwhile, the company's geographic footprint kept expanding. The products are sold under the brand name "Gallantt" in the states of Uttar Pradesh, Bihar, West Bengal, Assam, Madhya Pradesh, Andhra Pradesh and Karnataka. Each new state meant new relationships, new logistics challenges, new competitive dynamics. But Gallantt had learned to be a chameleon—adapting to local requirements while maintaining standardized quality.

The expansion wasn't just physical—it was strategic. The Company acquired the equity shares of Gallantt Medicity Devlopers Private Limited, thereby making it an Associate in 2024. Real estate development might seem disconnected from steel, but in India's infrastructure boom, controlling downstream construction gave insights into demand patterns that pure-play steel companies missed.

The numbers validated the strategy. Revenue had grown from hundreds of crores to Revenue: 4,261 Cr. More importantly, margins were expanding as operational leverage kicked in. Each new tonne of capacity utilized meant lower fixed costs per unit, higher margins, better returns.

The Karnataka expansion also demonstrated Gallantt's evolved playbook: identify underserved regions rich in raw materials, establish integrated operations with captive power, control logistics through owned assets, build slowly but steadily with internal cash, and diversify intelligently into related sectors. It was a formula that could be replicated across India's industrial corridors.

As 2024 drew to a close, Gallantt was no longer Eastern UP's steel company. It was a pan-Indian player with ambitions that stretched from the iron ore mines of Karnataka to the construction sites of Assam. The expansion years had transformed not just the company's footprint but its identity. The next chapter would test whether this regional champion could truly compete with India's steel titans.

VII. The Numbers Story: Financial Transformation

The spreadsheet tells a story that Excel alone cannot capture. For the full year, net profit rose 77.83% to Rs 400.74 crore in the year ended March 2025 as against Rs 225.35 crore during the previous year ended March 2024. Sales rose 1.55% to Rs 4292.73 crore in the year ended March 2025 as against Rs 4227.12 crore during the previous year ended March 2024. On the surface, modest revenue growth with explosive profit growth—the hallmark of operational leverage finally kicking in.

But dig deeper into the quarterly cadence and you see something more nuanced. Net profit of Gallantt Ispat rose 296.71% to Rs 121.87 crore in the quarter ended June 2024 as against Rs 30.72 crore during the previous quarter ended June 2023. Sales rose 11.92% to Rs 1159.69 crore in the quarter ended June 2024 as against Rs 1036.17 crore during the previous quarter ended June 2023. A near-quadrupling of profits on barely double-digit revenue growth—this wasn't just margin improvement; it was transformation.

The Q1 FY25 numbers validated the trajectory. Net profit of Gallantt Ispat rose 42.60% to Rs 173.79 crore in the quarter ended June 2025 as against Rs 121.87 crore during the previous quarter ended June 2024. Sales declined 2.75% to Rs 1127.78 crore in the quarter ended June 2025 as against Rs 1159.69 crore during the previous quarter ended June 2024. Revenue declined, yet profits surged—the ultimate demonstration of pricing power and cost control in a commodity business.

The December 2024 quarter crystallized the transformation. On a consolidated basis, Gallantt Ispat's net profit surged 118.68% to Rs 113.67 crore on 5.24% increase in net sales to Rs 1,118.32 crore in Q3 December 2024 over Q3 December 2023. More than doubling profits on single-digit revenue growth—this was the payoff from years of vertical integration and operational excellence.

What drove this margin expansion miracle? First, the integrated model was finally firing on all cylinders. When you control sponge iron production, steel melting, power generation, and logistics, every efficiency compounds. The captive power plants that seemed like capital sink in good times became profit centers when grid electricity costs spiked. The railway rakes that looked like unnecessary capex turned into margin protectors when freight rates surged.

Second, product mix evolution. The company wasn't just making more steel; they were making better steel. TMT bars command premiums over basic billets. Iron ore pellets generate higher margins than raw ore trading. Each step up the value chain meant better realization per tonne.

Third, the diversification hedge was working. While steel is cyclical, the wheat flour business provided steady cash flows. Real estate development offered lumpy but high-margin revenues. Power generation could be monetized externally when steel demand was soft. This portfolio approach smoothed earnings in ways pure-play steel companies couldn't achieve.

The working capital story was equally impressive. In commodity businesses, working capital can kill you—receivables stretch, inventory piles up, cash evaporates. But Gallantt had learned to manage the cycle. The strong brand meant better payment terms from customers. Vertical integration meant less cash trapped in inter-company transactions. The result: cash generation that funded expansion without debt.

The total project capex shall be funded by the company through internal accruals without borrowing any debt. Since expansion in capacities of above units are brown field expansion projects company has scheduled the completion of the Project tenure by March 2026. This wasn't financial conservatism—it was financial confidence. In an industry where debt-funded expansion is the norm, Gallantt was self-funding over ₹1,000 crores of capex.

The market's response has been emphatic. Stock is trading at 6.02 times its book value—a valuation multiple that suggests the market sees something beyond just cyclical earnings growth. For context, established steel majors often trade at 1-2x book value. Gallantt's premium valuation reflects both growth potential and execution credibility.

But there's a shadow in the numbers. Company has a low return on equity of 10.7% over last 3 years. For a company generating such impressive profit growth, why is ROE still modest? The answer lies in the capital-intensive nature of steel and the company's conservative balance sheet. As new capacity comes online and utilization improves, ROE should inflect higher.

The quarterly volatility also tells a story. Net profit of Gallantt Ispat rose 21.93% to Rs 116.31 crore in the quarter ended March 2025 as against Rs 95.39 crore during the previous quarter ended March 2024. Sales declined 8.94% to Rs 1072.15 crore in the quarter ended March 2025 as against Rs 1177.39 crore during the previous quarter ended March 2024. Revenue swings of nearly 10% quarter-to-quarter—this is the reality of commodity businesses, where prices can move violently and volumes can disappear overnight.

Yet through this volatility, the profit trajectory remained upward. This wasn't luck—it was the result of a business model designed for volatility. When steel prices fall, power sales increase. When construction slows, wheat flour picks up. When one cylinder misfires, others compensate.

Looking ahead, the numbers suggest we're still in early innings. Current capacity utilization leaves room for significant volume growth. The Karnataka expansion will add another growth vector. The shift to renewable energy will structurally lower costs. The financial transformation from 2020 to 2025—from ₹30 crores quarterly profit to ₹170+ crores—might just be the warm-up act.

VIII. Market Position & Competitive Dynamics

The Indian steel industry in 2024 resembles a chess board where the kings and queens are well established—Tata Steel with its century-old legacy, JSW with its entrepreneurial aggression, SAIL with its government backing. In this game of giants, Gallantt occupies the peculiar position of a knight—capable of unexpected moves, jumping over obstacles, attacking from angles others don't see coming.

Promoter Holding: 68.9%—this number tells you everything about control dynamics. In an era where professional management and dispersed shareholding are considered governance gold standards, Gallantt's concentrated ownership might seem anachronistic. But in the Indian context, this concentration has been a competitive weapon. Quick decisions, long-term thinking, patience through cycles—advantages that committee-run companies struggle to match.

The regional dominance story is where Gallantt's true moat emerges. The products are sold under the brand name "Gallantt" in the states of Uttar Pradesh, Bihar, West Bengal, Assam, Madhya Pradesh, Andhra Pradesh and Karnataka. This isn't random market presence—it's strategic encirclement of India's most underserved steel markets. While JSW dominates the west and south, while Tata rules the east, Gallantt has quietly built a kingdom in the Hindi heartland and is expanding into the peripheries.

Consider the customer base evolution. Real estate developers, construction companies, government organizations—these aren't the sophisticated industrial buyers that major steel companies court. These are price-sensitive, relationship-driven customers who value reliability over cutting-edge metallurgy. Gallantt speaks their language, extends their credit, delivers to their sites. It's a different game entirely.

The competitive dynamics shift dramatically when you move from national to regional lens. In Eastern UP and Bihar, Gallantt isn't competing with Tata Steel's blast furnaces—they're competing with traders, with small rolling mills, with unreliable suppliers. In this context, having integrated production, captive power, and owned logistics isn't just an advantage—it's a different league altogether.

The brand building in commodities deserves special attention. "Gallantt" has become synonymous with reliability in markets where product quality varies wildly. Local contractors don't specify IS standards—they specify "Gallantt TMT bars." This brand equity, built over two decades, creates switching costs that pure commodity players can't replicate.

Stock performance tells the market's verdict. Mkt Cap: 17,122 Crore (up 97.1% in 1 year)—nearly doubling in twelve months while established steel stocks struggled. The market is pricing in something beyond the current numbers: the optionality of the business model, the expansion potential, the possibility that this regional champion could become something more.

But let's address the elephant in the room—competing with giants. JSW Steel's capacity is over 28 million tonnes annually. Tata Steel produces over 30 million tonnes globally. Gallantt's entire capacity is a rounding error for these behemoths. How does David compete with multiple Goliaths?

The answer lies in choosing your battles. Gallantt doesn't compete for automotive-grade steel contracts with Maruti or Hyundai. They don't bid for railway infrastructure projects requiring specialized alloys. Instead, they dominate the unglamorous but massive market for construction steel in Tier-2 and Tier-3 cities. It's a market the giants have essentially ceded through neglect.

The economics of regional dominance are compelling. Transportation costs in steel can be ₹2,000-3,000 per tonne over long distances. When Gallantt delivers to a construction site in Gorakhpur from their local plant, while competitors ship from Jharkhand or Gujarat, that cost advantage flows directly to margins. Multiply this across millions of tonnes, and you have a structural advantage that scale alone can't overcome.

The customer acquisition cost dynamics further favor the regional player. Gallantt's sales team speaks local dialects, understands local construction practices, extends credit based on local reputation. A JSW sales representative from Mumbai, however talented, can't replicate this ground-level intimacy. Relationships in India's heartland are built over decades, not quarters.

There's also the speed advantage. When a local builder needs emergency supplies for a government project with penalty clauses, Gallantt can deliver within hours from local inventory. Larger players, with their complex approval processes and distant warehouses, can't match this responsiveness. In construction, where delays cost lakhs daily, this speed premium commands pricing power.

The regulatory and environmental landscape increasingly favors integrated regional players. As pollution norms tighten, small rolling mills without pollution control infrastructure face closure. As GST compliance requirements increase, informal sector players struggle. Gallantt, with its formal structure and environmental investments, benefits from this formalization of the economy.

Looking at market share data, Gallantt might represent less than 1% of India's total steel production. But in specific micro-markets—TMT bars in Eastern UP, construction steel in North Bihar—their share could be 20-30%. This concentrated regional strength is more defensible than thin national presence.

The competitive response from majors has been telling—or rather, the lack of it. No major steel company has announced significant capacity additions in Eastern UP. The returns don't justify the investment for companies used to 15-20% ROEs. For Gallantt, with lower capital costs and higher regional pricing power, the same investment generates superior returns.

The next five years will test whether regional dominance can translate into national relevance. The Karnataka expansion suggests ambitions beyond the Hindi heartland. But even if Gallantt remains a regional champion, the market opportunity is enormous. India's steel consumption is expected to double by 2030. Even maintaining current market position means doubling the business.

IX. The Diversification Gambit: Beyond Steel

The conference room in Lucknow, 2019. Across the table sat executives from the Shalimar Group, one of North India's established real estate developers. The discussion wasn't about steel supply contracts—it was about joint venture terms for a group housing project. To industry observers, this scene encapsulated everything bizarre about Gallantt's strategy. Why was a steel company developing apartments?

Shalimar Gallantt: It is a group housing project located in Lucknow. It is developed as a JV with The Shalimar Group in Lucknow. This wasn't opportunistic diversification—it was strategic positioning in the construction value chain. When you supply steel to real estate developers, you see their margins, understand their cash flows, recognize their risks. The logical next step? Become a developer yourself, but with a crucial advantage—your primary input cost is at manufacturing price, not market price.

The wheat flour business raises even more eyebrows. The food grain business of the Co includes wheat flour products like Atta, Maida, Suji and Bran. In boardrooms from Mumbai to New York, the first question analysts ask is: "Why wheat?" The answer requires understanding the peculiar dynamics of Eastern UP, India's wheat bowl.

The geography that made Gorakhpur attractive for steel—central location, transport connectivity, proximity to markets—made it equally attractive for food processing. The same trucks that delivered steel to construction sites could carry wheat products to retail outlets. The same banking relationships that financed steel working capital could support agricultural procurement. The same brand trust that sold TMT bars could sell atta to households.

But the real genius of wheat diversification was risk management. Steel is cyclical, with demand swinging 20-30% through cycles. Wheat consumption is stable—people need rotis regardless of GDP growth. When construction slumps and steel demand evaporates, wheat flour generates cash to keep operations running. It's portfolio theory applied to industrial operations.

The power business adds another layer. The captive power plants, originally built for steel production, became profit centers themselves. When steel furnaces ran below capacity, excess power could be sold to the grid or neighboring industries. In India's power-deficit regions, reliable electricity supply commands premium pricing. What started as backward integration became forward integration into energy markets.

The Company acquired the equity shares of Gallantt Medicity Devlopers Private Limited, thereby making it an Associate in 2024. Healthcare real estate? The logic becomes clearer when you understand Gorakhpur's demographics. As Eastern UP's commercial hub, the city desperately needs modern healthcare infrastructure. Gallantt's land banks, construction expertise, and steel supply create natural advantages in developing medical facilities.

The risk management philosophy underlying diversification deserves examination. In 2008, when steel companies globally faced existential crisis, Gallantt survived partly because wheat flour sales continued. In 2020, when COVID shut down construction, the food business saw demand surge. This isn't correlation—it's anti-correlation, the holy grail of portfolio construction.

Critics argue this diversification dilutes focus, that Gallantt should stick to steel like JSW or Tata. But this criticism misunderstands the nature of regional conglomerates in emerging markets. In Tier-2 India, business isn't specialized—it's relationship-based. The same promoter credibility that sells steel can sell real estate. The same political connections that secure industrial licenses can win housing project approvals.

There's also operational synergy that spreadsheets don't capture. The wheat flour business provides deep understanding of rural markets, agricultural cycles, and commodity procurement—insights valuable for steel distribution in rural areas. Real estate development offers intelligence on construction trends, upcoming projects, and builder creditworthiness—information that helps steel sales.

The capital allocation across divisions reveals strategic thinking. Steel gets the bulk of growth capital—it's the core engine. Real estate is opportunistic, pursued only when returns exceed 25%. Wheat is steady-state, generating cash without major reinvestment. Power is transitioning to renewables, positioning for the green future. Each division has a role in the portfolio.

The management bandwidth question is valid—how does one team manage such diversity? The answer lies in Gallantt's organizational structure. Each division has operational autonomy with separate P&L responsibility. The promoters focus on capital allocation and strategic direction, not operational minutiae. It's a holding company model disguised as an operating company.

Financial metrics validate the strategy. In quarters when steel margins compress, consolidated results remain stable due to other divisions. Return on capital employed across divisions exceeds industry averages. Most importantly, cash flow volatility is lower than pure-play steel companies—critical for a company funding expansion internally.

Looking forward, the diversification strategy faces evolution. The steel business is scaling rapidly and will demand increasing capital. Non-core assets might be monetized to fund steel expansion. The wheat business might be spun off once it reaches critical mass. Real estate projects might shift from development to pure land banking.

But abandon diversification entirely? Unlikely. In India's volatile economy, with infrastructure cycles, monsoon dependencies, and political shifts, diversification isn't a luxury—it's survival. Gallantt's model might seem unfocused to Western MBA standards, but it's perfectly adapted to Indian reality.

The ultimate test will be whether Gallantt can maintain this diversification while scaling to become a major steel player. Can they be both conglomerate and focused steel company? The answer might redefine how we think about industrial strategy in emerging markets. The diversification gambit isn't about being everything to everyone—it's about being antifragile in a fragile world.

X. Playbook: Lessons for Founders & Investors

If you gathered India's top industrialists in a room and asked them to design a steel company from scratch in 2005, none would have designed Gallantt. Start in Gorakhpur, not near mines or ports? Diversify into wheat flour? Build apartments while running blast furnaces? The playbook Gallantt wrote violates every rule taught in business schools—yet it worked. Here's what founders and investors can learn from this unlikely success.

Lesson 1: Start Where No One Else Wants To Be

The Tier-2 city advantage is real but counterintuitive. Lower land costs, state government incentives, and minimal competition create structural advantages that compound over time. When Infosys started in Bangalore (then a Tier-2 city), when Haldiram built from Bikaner, when Gallantt chose Gorakhpur—they all understood something fundamental: in business, being a big fish in a small pond beats being plankton in the ocean.

For founders, this means resisting the gravitational pull of established hubs. That Mumbai office, that Gurgaon headquarters—they signal credibility but destroy economics. Build where your customers are, not where your competitors are. The prestige deficit of a Gorakhpur address disappears when your EBITDA margins are double the industry average.

Lesson 2: Backward Integration Is Forward Thinking

In an era of asset-light models and outsourcing everything, Gallantt's radical backward integration seems prehistoric. Captive power plants, owned railway rakes, pelletization facilities—capital intensive and complex. But in India's infrastructure reality, controlling your critical inputs isn't inefficiency—it's insurance.

When power cuts shut down competitors, Gallantt's furnaces keep running. When railway capacity gets allocated politically, Gallantt's owned rakes ensure delivery. This isn't about cost savings—it's about reliability in an unreliable ecosystem. For founders in infrastructure-dependent sectors, the lesson is clear: control what can kill you.

Lesson 3: Diversification Isn't Distraction If Done Right

The focused versus diversified debate misses the point. The question isn't whether to diversify, but how. Gallantt's diversification follows clear principles: adjacent value chains (real estate uses steel), counter-cyclical hedges (wheat versus steel), shared infrastructure (transportation, banking, brand). This isn't random expansion—it's portfolio construction.

For investors, this means looking beyond Western portfolio theory. In emerging markets, unrelated diversification can reduce risk if managed properly. The key is ensuring each business can stand alone while benefiting from group synergies. Judge conglomerates not by their focus but by their capital allocation track record.

Lesson 4: Patient, Concentrated Ownership Matters

Promoter Holding: 68.9%—in an era of distributed ownership and professional management, this concentration seems anachronistic. But patient capital with skin in the game makes decisions that quarterly-focused managers won't. Investing ₹1,000 crores from internal accruals, waiting years for capacity to ramp up, building brands in commodities—these require ownership mindset, not employee mindset.

The lesson for founders: don't dilute too early or too much. The pressure to bring in institutional investors, to "professionalize" management, to distribute ownership—resist it until you've built something defensible. For investors: concentrated ownership isn't a governance red flag if the promoters have a track record of treating minorities fairly.

Lesson 5: Building Brands in Commodities Is Possible

Conventional wisdom says commodities can't be branded—steel is steel, wheat is wheat. Gallantt proved otherwise. By maintaining consistent quality, reliable delivery, and relationship-based selling, they built brand equity in supposedly undifferentiable products. Local contractors don't ask for "TMT bars"—they ask for "Gallantt."

The playbook: focus on trust over technology, reliability over innovation, relationships over transactions. In markets where quality varies wildly and trust is scarce, brand becomes the ultimate moat. This requires patient investment in reputation, something quarterly capitalism struggles to value.

Lesson 6: Capital Allocation Is Everything

Gallantt's capital allocation reveals masterful thinking. Steel expansion gets funded from internal accruals—no debt risk. Real estate projects are joint ventures—shared risk, leveraged returns. Wheat business runs steady-state—cash cow, not growth engine. Each rupee deployed has clear return expectations and risk parameters.

For founders, this means developing capital allocation as a core competency, not delegating it to CFOs. For investors, judge companies not by their stated strategy but by where they deploy capital. Money flows reveal true priorities in ways presentations never will.

Lesson 7: Timing Matters More Than Size

Gallantt's major moves—starting in 2005 during infrastructure boom, expanding during 2008 crisis, consolidating in 2021, deploying capital in 2024—reveal exquisite timing. They weren't always first movers or fast followers. They moved when conditions aligned: demand emerging, competition struggling, capital available.

The lesson: in cyclical industries, when you invest matters more than how much. Building capacity at cycle peaks destroys value. Expanding during downturns creates it. This requires patience to wait and courage to act—qualities in short supply in modern capitalism.

Lesson 8: Geography Is Strategy

Gallantt's arc from Kolkata incorporation to Gorakhpur manufacturing to Karnataka expansion wasn't random wandering—it was strategic positioning. Each location unlocked specific advantages: Kolkata for trading heritage, Gorakhpur for market access, Karnataka for raw materials. Geography shaped strategy rather than strategy determining geography.

For founders, this means thinking deeply about location economics beyond obvious factors. Where are your customers' customers? Where will infrastructure develop? Where can you build sustainable advantages? For investors, map portfolio companies literally—geographic positioning often predicts competitive dynamics.

Lesson 9: The Power of Saying No

What Gallantt didn't do is as instructive as what they did. They didn't chase automotive steel contracts. They didn't build coastal facilities for exports. They didn't acquire distressed assets during downturns. They didn't raise private equity capital at dilutive valuations. Each "no" preserved focus and capital for better opportunities.

The discipline to not do obvious things—international expansion, marquee customers, financial engineering—requires confidence in your chosen path. In a world that celebrates hyperactivity, strategic inaction is undervalued.

Lesson 10: Build for Anti-fragility, Not Just Efficiency

Gallantt's model—diversified revenue, multiple locations, integrated operations—isn't optimally efficient. But it's anti-fragile. When shocks hit—2008 crisis, 2020 pandemic, commodity cycles—the company doesn't just survive; it gains strength. Efficiency is about doing things right. Anti-fragility is about surviving to do things.

For founders building in volatile markets, optimize for survival over growth. For investors, value resilience over returns. The companies that compound wealth over decades aren't the fastest growers—they're the survivors who capture opportunities when competitors can't.

The Gallantt playbook won't work everywhere or for everyone. But it offers an alternative mental model for building industrial businesses in emerging markets. Sometimes the best strategy isn't following global best practices—it's understanding local reality and building accordingly.

XI. Analysis: Bull vs Bear Case

The Bull Case: Why Gallantt Could 5x From Here

The optimist's view starts with a simple observation: India needs massive amounts of steel, and someone has to make it. India's steel demand is projected to grow significantly over the next decade, with consumption expected to double by 2030. Even if Gallantt just maintains market share, the business doubles. But the bull case goes deeper than rising tides.

First, the infrastructure super-cycle is real and sustained. India's infrastructure spending as percentage of GDP is rising from 4% to targeted 7% by 2030. Every kilometer of highway needs 7,000 tonnes of steel. Every metro project, every airport expansion, every smart city—they all need steel, specifically the construction-grade steel that Gallantt specializes in. This isn't speculative demand; it's committed government expenditure.

Second, operational leverage is just beginning to show. Net profit rose 77.83% to Rs 400.74 crore in the year ended March 2025 on modest revenue growth. As capacity utilization increases from current 60-70% to 85-90%, incremental revenues flow almost entirely to bottom line. Fixed costs are already absorbed; marginal costs are manageable. The profit trajectory could be parabolic.

Third, the regional dominance model is replicable. What worked in Eastern UP can work in Central India, in the Northeast, in other underserved markets. Each new region offers similar dynamics: fragmented competition, infrastructure deficits, relationship-based selling. Gallantt has the playbook; they just need to execute it repeatedly.

Fourth, the balance sheet enables aggressive expansion. Funding ₹1,000+ crores of capex from internal accruals demonstrates cash generation capability. Zero debt means infinite flexibility. When opportunities arise—distressed assets, strategic acquisitions, new territories—Gallantt can move fast without board approvals or lender negotiations.

Fifth, the valuation re-rating potential is significant. Stock is trading at 6.02 times its book value, but established players like Tata Steel trade at higher multiples on EV/EBITDA basis despite slower growth. As Gallantt scales and institutional ownership increases, multiple expansion could drive returns independent of earnings growth.

Finally, the hidden assets are undervalued. The 106 acres in Karnataka, the real estate ventures, the brand value in regional markets—none fully reflected in current valuations. The company is valued as a commodity steel producer, not as an integrated industrial conglomerate with multiple growth vectors.

The Bear Case: Why This Rally Could Reverse

The skeptic's view starts with an uncomfortable truth: Company has a low return on equity of 10.7% over last 3 years. In a capital-intensive industry, low ROE suggests either overcapitalization or operational inefficiency. Why should investors accept 10% returns when fixed deposits offer 7% risk-free?

First, the commodity cycle risk is existential. Steel is among the most cyclical industries globally. China's property crisis, global recession risks, or simply oversupply could crash prices 30-40% in months. Gallantt's regional focus offers no protection from global price transmission. When steel prices fall, everyone bleeds.

Second, the competition is awakening. JSW, Tata Steel, and even SAIL are expanding aggressively. As infrastructure improves, their cost disadvantage in serving Tier-2 markets diminishes. What happens when JSW builds a plant in Eastern UP? Gallantt's regional moat could evaporate overnight.

Third, China's shadow looms large. Despite duties and restrictions, Chinese steel finds ways into Indian markets. If China's domestic demand remains weak, they could dump excess capacity globally, destroying margins for everyone. Gallantt lacks the scale to survive a price war with Chinese giants.

Fourth, environmental regulations are tightening. Steel production is carbon-intensive, water-consuming, and polluting. As India commits to net-zero targets, compliance costs will surge. Smaller players like Gallantt might struggle to afford required technology upgrades that larger players can amortize over greater volumes.

Fifth, execution risk multiplies with expansion. Managing steel plants in Gorakhpur and Gujarat is complex enough. Adding Karnataka, solar power, and capacity expansions simultaneously could overwhelm management bandwidth. One operational mishap—a blast furnace failure, a labor strike, an environmental violation—could derail the entire story.

Sixth, the diversification is value-destructive. Why is a steel company in real estate? Why wheat flour? These distractions prevent focus on core operations. The market values focused pure-plays, not confused conglomerates. The sum-of-parts might be worth less than the whole.

Finally, the liquidity concern is real. Despite market cap of ₹17,000+ crores, daily trading volumes are thin. Large institutional investors can't build meaningful positions without moving prices. When selling pressure emerges, who will provide exit liquidity?

The Balanced View: Probabilistic Thinking

Reality likely lies between extremes. Gallantt isn't becoming Tata Steel, but it doesn't need to. Success means becoming India's best regional steel player, not its biggest national player. The risks are real but manageable; the opportunities are significant but not guaranteed.

The key monitorables: capacity utilization trends, regional market share data, ROE improvement trajectory, competitive capacity additions in core markets, and working capital cycles. These metrics will reveal whether the bull or bear case is playing out.

For investors, position sizing matters more than directional calls. Gallantt offers asymmetric risk-reward for small positions but concentration risk for large ones. It's a complement to portfolios, not a core holding. The volatility isn't a bug—it's a feature that creates opportunity for patient capital.

XII. Power & Conclusion

The dusty roads leading to Gallantt's Gorakhpur plant don't look like the path to India's industrial future. There are no glass towers, no MBA presentations, no foreign consultants. Just furnaces running round the clock, railway rakes loading steel, and trucks heading to construction sites across the Hindi heartland. Yet this unremarkable scene represents something profound about Indian capitalism: the power of building where others won't, serving whom others ignore, and surviving when others can't.

What makes Gallantt different isn't technological innovation or financial engineering. It's the paradoxical combination of trader's opportunism and manufacturer's discipline, of regional focus and national ambition, of commodity production and brand building. They've created a template for industrial success that's uniquely Indian—messy, diversified, relationship-driven, but ultimately effective.

The next five years will test whether this model scales. Can a company born in Kolkata's trading lanes and raised in Gorakhpur's furnaces compete with giants nurtured in Mumbai's boardrooms? Can regional dominance translate to national relevance? Can patient promoter capital coexist with impatient public markets?

The answers matter beyond Gallantt's stock price. India needs 300 million tonnes of steel capacity by 2030, up from 150 million tonnes today. The giants—Tata, JSW, SAIL—will build their share. But the gap between their mega-plants and India's dispersed demand creates space for regional champions. Gallantt's success or failure will signal whether this middle path is viable.

The biggest surprise from researching Gallantt isn't what they've achieved—it's what they've chosen not to do. No international ventures despite export opportunities. No marquee customers despite capability. No private equity despite offers. No debt despite cheap capital. This restraint, this discipline to say no, might be their greatest strength in an industry littered with overleveraged ambitions.

For investors watching this story unfold, the key insight is timing. Gallantt is past startup risk but before maturity returns. They're proven but not priced for perfection. The operational leverage is built but not fully utilized. The expansion is funded but not completed. This is the sweet spot—when risk-reward is most favorable, when patient capital can still make impatient returns.

For entrepreneurs, Gallantt offers a different model of industrial success. You don't need Silicon Valley's venture capital or South Mumbai's connections. You need deep market understanding, operational excellence, and infinite patience. Build where you have advantages, not where others have succeeded. Serve customers others ignore, not those everyone chases. Survive cycles others can't, then expand when they're weakened.

For India's policymakers, Gallantt demonstrates the dynamism beyond headlines. While unicorns and tech startups capture attention, companies like Gallantt quietly build the physical infrastructure for India's growth. They employ thousands in Tier-2 cities, source from local suppliers, pay taxes without exemptions. This is the unsexy but essential economy that needs policy support.

The ultimate judgment on Gallantt won't come from stock markets or analysts. It will come from the construction sites of Eastern UP, where contractors choose between suppliers. It will come from the blast furnaces of Gorakhpur, where operational excellence meets market opportunity. It will come from the rail sidings and truck depots, where logistics enable ambition.

As India builds its future—100 smart cities, 50,000 km of highways, metros in every major city—someone has to make the steel. The question isn't whether demand exists; it's who captures it. Gallantt has positioned itself at the intersection of India's infrastructure ambition and industrial capability. They might not become India's largest steel company, but they're becoming something perhaps more valuable: India's most interesting steel company.

The story that began with four promoters in a Kolkata office has evolved into something larger—a testament to building industrial businesses differently, to finding opportunity in overlooked markets, to creating value through operational excellence rather than financial engineering. Whether this story ends with Gallantt as a regional champion or a national force remains to be written. But the chapters so far suggest that sometimes the best businesses are built not where the spotlight shines, but in the shadows where real work gets done.

In Gorakhpur's summer heat, where the furnaces never cool and the railway rakes never stop loading, Gallantt isn't just making steel. They're forging a different path for Indian industry—one that leads not from Mumbai to New York, but from Tier-2 to tomorrow.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube