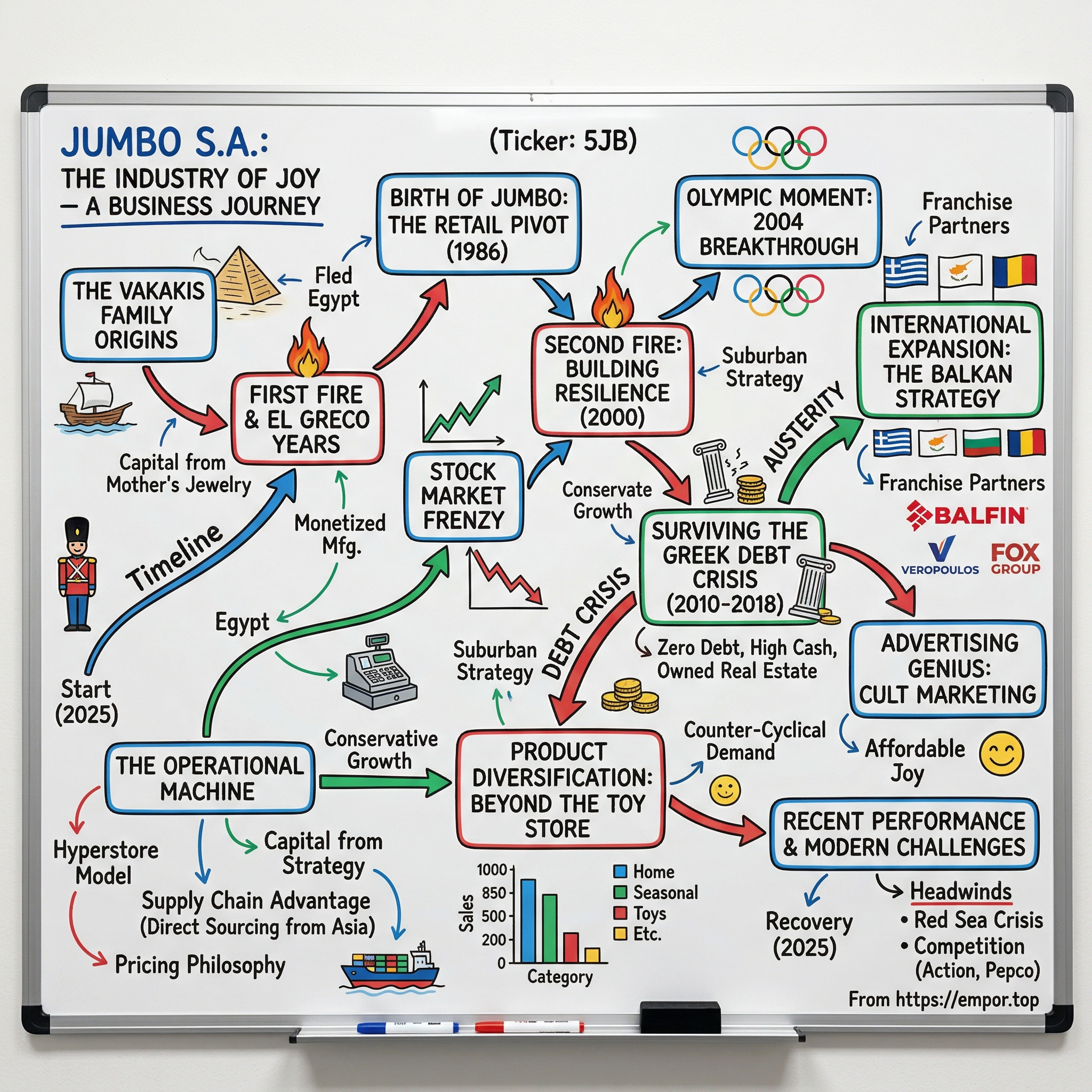

Jumbo S.A.: The Industry of Joy — Greece's Retail Phenomenon

Picture a single toy store opening in the affluent Athens suburb of Glyfada in 1986. Greece had only recently emerged from the Colonels' dictatorship, and the country was scrambling to modernize its economy while struggling with endemic inflation and a weak drachma. The idea that this modest retail venture would one day become a dominant force across Southeast Europe—surviving currency crises, the greatest peacetime economic collapse in Greek history, and a global pandemic—seemed laughably implausible.

Yet nearly four decades later, Jumbo S.A. reported a 6% year-over-year increase in sales, reaching €1.15 billion for 2024, while EBITDA rose by 7% to €425 million. The company has delivered an impressive 14.6% annual total shareholder return since IPO, built on conservative growth, operational discipline, and a product mix designed to endure across cycles.

How did a single toy store in a Southern Athens suburb become the dominant value retailer across Southeast Europe—while surviving Greece's worst economic catastrophe since World War II? The answer lies in understanding one of the most compelling founder stories in European retail, a tale of fires both literal and economic, contrarian bets on real estate during market euphoria, and an almost religious devotion to affordable joy.

The Jumbo Group currently operates 89 stores: 53 in Greece, 6 in Cyprus, 10 in Bulgaria, and 20 in Romania. Through partnerships, the Group has a presence with 40 branded stores in 7 countries including Albania, Kosovo, Serbia, North Macedonia, Bosnia, Montenegro, and Israel.

What makes this story particularly fascinating is not just the growth trajectory, but the strategic choices that enabled it. Over the period FY15 to FY24, the Company depicted a revenue CAGR of 7.4% and operating income CAGR of 11.7%, reaching FY24 revenue of €1.1 billion and adjusted operating income of €372 million. Jumbo has cash and short-term investments of €444.8 million compared to nil total debt and lease liabilities of €75 million.

This is the story of "The Industry of Joy."

The Vakakis Family Origins: From Alexandria to Athens

The Jumbo story begins not in Athens, but in the cosmopolitan port city of Alexandria, Egypt—a city that once housed one of the ancient world's greatest libraries and, in the mid-20th century, thrived as a melting pot of Greek, Jewish, Italian, and Egyptian communities. Born in Alexandria in 1954, Apostolos Vakakis immigrated to Greece in 1962 with his family, and for a time he also lived in Italy where his father worked in a company producing stuffed toys.

The Italian experience was decisive for the future, as it was the first real contact of the Vakakis family with the world of toys. This wasn't merely an accident of geography—George Vakakis, the patriarch, had developed genuine expertise in toy manufacturing during his time working at an Italian stuffed toy factory. The family was absorbing knowledge that would prove instrumental in the decades to come.

The Vakakis family's departure from Egypt wasn't a choice but a necessity. The Nasser revolution had upended the lives of hundreds of thousands of Greeks, Jews, and other foreigners who had called Egypt home for generations. Vakakis came from a family that fled political unrest during the Nasser revolution, resettling in Greece in 1962.

There's a poignant detail about how the family financed their new beginning. The first working capital for the development of what would become the El Greco toy company came from the sale of jewelry which Sophia Vakakis, Apostolos's mother, had brought from Egypt. This wasn't a family with deep institutional capital or wealthy backers—they were immigrants rebuilding from near-scratch with whatever portable wealth they could carry across borders.

The family returned to Greece and with capital provided by Prodromos Athanasiadis Bodossakis, then owner of Larco, his father George founded the El Greco toy company. Bodossakis was one of Greece's most prominent industrialists of the era, and his backing provided crucial legitimacy and capital. El Greco would become one of the largest toy manufacturers in Greece, "Pioneering Greek toy makers El Greco and Lyra were gigantic by that era's standards, employing hundreds of staff."

"With steady development in the 1960s and the greatest boom in the 1970s, kids' toys made a dynamic entrance in Greek households. Demand rose, family revenue increased, and, most importantly, there were no imports, due to controls in foreign currency exchange." This was the environment in which young Apostolos grew up—watching his father build a manufacturing empire in a protected market, absorbing lessons about production, distribution, and the peculiarities of the Greek consumer.

At the age of 20, Apostolos Vakakis went to Warwick, UK to study accounting and finance with the dream of ending up in Berkeley. That Californian dream would never materialize, but the Warwick education—particularly in accounting and finance—would prove invaluable. While other Greek entrepreneurs of his generation might have focused on political connections or family networks, Vakakis was developing a financial literacy that would later enable him to make counter-cyclical bets and maintain conservative capital structures when his competitors borrowed to extinction.

The young Apostolos seemed destined for an academic path that might have led him to American business schools and eventually to corporate careers far from the family toy business. Fate, however, had other plans.

The First Fire & El Greco Years: Crucible of Entrepreneurship

A major fire that broke out in the mid-1980s destroyed one of the two El Greco factories located in Ano Glyfada. Apostolos Vakakis rushed back from his studies in London and took over the management of the company.

This fire was the first of two conflagrations that would shape Vakakis's business philosophy. At just 23 years old, he abandoned his dreams of Berkeley and returned to Greece to salvage the family business from the ashes. The experience was formative—it taught him that businesses can be destroyed overnight, that insurance and reserves matter, and that survival often depends on having backup options.

He tried to rebuild the industry, continuing the production of its products, with the help of El Greco's second production plant, which was located in Zakynthos. He stayed on the island for three years. On this Ionian island, Apostolos received what amounted to a crash course in operational management. Working alongside his father to resurrect a business from catastrophe, he learned lessons about resilience that would prove invaluable during the Greek debt crisis decades later.

On the island of the Ionian Islands, Apostolos Vakakis lived an explosive "apprenticeship" alongside his father during the three years of his stay on the island, until in 1985 he took over the position of President of El Greco.

The timing of what happened next reveals Vakakis's strategic acumen. By the mid-1980s, Greece was beginning to open its economy. Import restrictions that had protected domestic toy manufacturers for decades were easing. The flood of cheap Asian toys that would soon devastate European manufacturing was visible on the horizon to anyone paying attention.

Eventually, the reins of El Greco were taken over entirely by Apostolos Vakakis in 1985, who then sold the company to the multinational toy company Hasbro. El Greco was a Greek company that held the license to manufacture and market Transformers toys in Greece during Generation 1.

The Hasbro deal was brilliant timing. Rather than fighting the inevitable decline of Greek toy manufacturing in an increasingly globalized world, Vakakis monetized the family asset at peak value while retaining deep knowledge of the Greek market and relationships with suppliers. Seeing the multinationals operating in Greece in 1990, he decided to sell El Greco to the multinational Hasbro while running the company while serving on Hasbro Europe's management committee.

In 1985, he took over leadership of the company and eventually sold it to Hasbro in 1990, remaining involved as an executive within Hasbro Europe. By then, Vakakis had already shifted toward retail, having founded Jumbo in 1986.

This overlap is crucial—Vakakis was simultaneously selling the manufacturing business while building the retail business. He wasn't abandoning toys; he was repositioning the family's involvement in the value chain. Instead of fighting global manufacturing scale, he would become the conduit through which those products reached Greek consumers.

"Then, the early 1990s signaled the mass import of toys from abroad—not only in Greece, but in the entire European market, which was stormed by cheap Chinese toys. The result was many craft units to close, or to transform from producers to importers." Vakakis had seen this coming years before most of his peers and had already positioned himself on the winning side of the transformation.

Birth of Jumbo: The Retail Pivot (1986-1997)

In 1986 the first toy store called "Jumbo" opened in Greece. Jumbo S.A. was founded in 1986 as Babyland S.A. by Apostolos Vakakis, who established the company's initial focus on toy retail with the opening of its first store in Glyfada, a suburb of Athens.

The choice of Glyfada was not accidental. This affluent southern Athens suburb was home to middle and upper-middle-class families with children—precisely the demographic most likely to spend on toys. But the strategic insight went deeper: rather than competing with department stores in central Athens, Vakakis was pioneering suburban retail in a country that barely had suburbs in the American sense.

"This marked the beginning of what would become a prominent retail chain specializing in toys and related products, capitalizing on the growing demand for affordable family-oriented goods in the post-dictatorship Greek market. During its early expansion phase from 1989 to 1991, Babyland S.A. opened three additional stores in key Athens suburbs: Psychiko, Holargos, and Piraeus."

The early years established what would become Jumbo's distinctive approach: large-format stores in accessible suburban locations, with a focus on value rather than premium positioning. From the outset, Jumbo has maintained a low-price strategy to foster trust and long-term customer loyalty.

By the mid-1990s, the company pursued strategic growth through acquisitions, buying majority stakes in and absorbing Mamouth S.A., Panther S.A., and Primo S.A. These weren't just competitors—they were potential real estate sites, supplier relationships, and customer bases. Vakakis was consolidating a fragmented market while his competitors were still figuring out how to respond to import liberalization.

The company's international expansion began earlier than most realize. In 1998, it acquired Jumbo Trading Ltd in Cyprus. Cyprus was a natural first step—a Greek-speaking island with cultural affinity, strong economic ties to Greece, and a growing consumer class. The acquisition demonstrated that Vakakis was thinking regionally, not just nationally, even before the company went public.

In 1997 the company crossed the threshold of the Athens Stock Exchange, raising a total of €2 million in capital. Jumbo S.A. has been listed on the Athens Stock Exchange under the ticker symbol BELA since July 19, 1997. Since June 2010, Jumbo has been included in the FTSE/Athex 20 index, underscoring its status among Greece's leading blue-chip companies.

The €2 million raised in the IPO seems modest by today's standards, but it provided crucial capital for expansion at exactly the right moment. Greece in 1997 was preparing for Eurozone entry, interest rates were falling, and consumer confidence was rising. The timing was impeccable.

The Stock Market Frenzy & Second Fire: Building Resilience (1997-2004)

The late 1990s were a period of collective madness in Greece's equity markets. The Athens Stock Exchange experienced one of the most spectacular bubbles in European financial history, with the general index rising from under 1,000 in 1997 to nearly 6,500 in September 1999 before collapsing. Regular Greeks—housewives, pensioners, taxi drivers—were quitting their jobs to day-trade stocks. It was the Greek version of the dot-com bubble, but even more pervasive.

In the golden age of the stock exchange, in 1999, when the whole of Greece was buying shares, he invested in land.

This single sentence captures Vakakis's contrarian philosophy. While Greece was gripped by speculative fever, he was quietly acquiring real estate. This wasn't capital preservation born of timidity—it was a strategic bet that physical assets would outlast market euphoria. The decision would prove prescient both in the immediate aftermath of the bubble's collapse and, more importantly, during the debt crisis a decade later.

However, a devastating fire destroyed the warehouses and headquarters of the management in 2000. After this, the company moved to new offices in Moschato.

The second fire. Lightning doesn't usually strike twice, but for Vakakis it did. It's worth noting that apart from the fire during the El Greco years, bad luck struck again in 2000 when a fire destroyed Jumbo's headquarters and warehouse. The Company then moved its base to Moschato, where it is still located today.

These twin conflagrations—one destroying the family's manufacturing base, the other destroying the retail company's headquarters—would have broken lesser entrepreneurs. Instead, they reinforced Vakakis's emphasis on liquidity, insurance, and redundancy. The company's later insistence on maintaining large cash reserves and avoiding debt can be traced directly to these early experiences with catastrophic loss.

In recent years, Jumbo has strategically moved from leasing to owning stores to reduce operating costs. Between FY2020–FY2024, the Company acquired five previously leased stores for €39M, and most new store rollouts in 2023–2025 are company-owned.

Vakakis's real estate philosophy crystallized during this period. "Leasing a store would cost us, let's say, 7.5%, 7% on the estimated value of the store, while owning the store, especially if you are liquid, is 0%."

Critics argue this ties up capital that could generate higher returns elsewhere. With returns on capital near 20%, critics argue that the capital tied up in real estate could be better used to fund growth or returned to shareholders, a classic opportunity cost trade-off. But Vakakis's approach reflects a different optimization function—one that prioritizes survival over short-term returns. When your formative business experiences involve watching assets burn to the ground, owning the underlying real estate provides a psychological and financial foundation that rent payments cannot.

The Olympic Moment: 2004 Athens Games Breakthrough

The 2004 Athens Olympics represented Greece's grand reentry onto the world stage—the first time the Games had returned to their birthplace in modern times. The Greek government had spent lavishly on infrastructure, and the entire nation was caught up in Olympic fever.

A decisive moment for the entrepreneur was the moment when he took over the production and marketing of the official mascot of the 2004 Olympic Games in Athens. It was then that Jumbo's turnover reached 500 million euros per year.

One of its most noticeable achievements came in 2004, when Jumbo secured exclusive rights to produce and distribute the Athens Olympic mascot, helping push annual revenues towards €500 million.

An international competition for the design of the Olympic mascots was launched by the Athens Organizing Committee for the Olympic Games (ATHOC) on 26 February 2001: on 18 May 2001, ATHOC shortlisted seven proposals out of the 127 entries. The winning proposal, submitted by Spyros Gogos of Paragraph Design Limited, was announced on 26 October 2001.

The mascots—Athena and Phevos—were the official mascots of the 2004 Summer Olympics. Athena and Phevos are one of the few examples of anthropomorphic mascots in the history of the Olympics. The mascots have been emblazoned on a variety of items for sale, including pins, clothing and other memorabilia.

For Jumbo, this wasn't just a revenue opportunity—it was a brand-building exercise of unprecedented scale. Millions of Greeks and visitors encountered Jumbo-branded products during the Games. The company demonstrated it could handle mass-market logistics at scale, fulfilling Olympic demand while maintaining its regular retail operations.

The Olympic contract also showcased Vakakis's willingness to bid aggressively when the stakes were high. The infrastructure and logistics leap required to fulfill Olympic demand forced the company to scale its operations in ways that would prove beneficial for subsequent international expansion.

In the years that followed, the company was at the height of its success, which peaked in 2004 when, following an auction, it took over the exclusive right to produce and market the mascot for the 2004 Olympic Games.

But if 2004 represented the high-water mark of pre-crisis Greece, what followed would test every Greek business—and Jumbo's unique positioning would prove decisive.

Surviving the Greek Debt Crisis: The Defining Test (2010-2018)

No discussion of Jumbo can be complete without understanding the cataclysm that engulfed Greece beginning in 2010. The Greek debt crisis wasn't merely a recession—it was an economic collapse comparable to the Great Depression, compressed into a few devastating years.

Three bailouts, totaling €246 billion, coupled with draconian austerity measures, partially stabilized the situation but at a tremendous human cost in terms of generating chronically high unemployment, widespread poverty, and plummeting incomes. Real GDP contracted by approximately one-fourth between 2009 and 2015.

In 2012, GDP was 20% lower in real terms than it had been in 2009, just three short years before, and the fall in real GDP would reach 26% by 2013, relative to 2008, an unprecedented drop for a social market economy in a democratic western European state. The extent of the austerity measures exacerbated the impact of the recession, and between 2009 and 2015, the unemployment rate trebled.

Greece's economy collapsed. Its economic output declined by 25 percent from the 2010 level. Wages and pensions fell. Unemployment reached 27 percent. And the medicine did not even work in reducing Greece's debt-to-GDP ratio, which climbed from 130 percent of GDP in 2009 to 180 percent at the end of 2014.

The human toll was staggering. According to Eurostat, 44% of Greeks lived below the poverty line in 2014. In 2015, the OECD calculated that 20% of the Greek population lacked the funds to meet their daily food requirements. Soup kitchens doled out free food to the long-term unemployed, homeless, and poverty stricken.

Most Greek retailers faced extinction. Banks froze lending, consumers stopped spending, and businesses that had borrowed to expand found themselves unable to service debts. In this environment, Jumbo's distinctive characteristics—zero debt, substantial cash reserves, owned real estate—transformed from conservative quirks into survival essentials.

The critical insight was counter-intuitive: in an economy where a quarter of the population was unemployed and another quarter was at risk of poverty, affordable joy became more valuable, not less. Parents still wanted to give their children gifts at Christmas and Easter. Families still needed household goods. The impulse to celebrate—to maintain some normalcy amid catastrophe—didn't disappear; it simply became more price-sensitive.

Jumbo's value proposition—low prices across a vast selection—aligned perfectly with this new reality. While premium retailers struggled, Jumbo's traffic held steady or grew. The company didn't just survive the crisis; it emerged stronger, gaining market share as competitors retrenched or failed.

In order to understand his philosophy, Apostolos Vakakis, during the regular general meeting of shareholders, tried to justify his cautious optimism or even "pessimism" about the group's forecast for 2023. It was a forecast that once again appears below the real potential of the business and the performance that ultimately comes at the end of the year. Jumbo's sales in 2023 are estimated by its management to increase by 15% from 949.38 million euros in 2022. As usual, however, the growth it ultimately shows is much higher than Vakakis' initial forecasts.

This pattern—conservative guidance followed by outperformance—isn't just sandbagging. It reflects a management philosophy forged in crisis: always assume the worst, prepare for catastrophe, and be pleasantly surprised when things turn out better.

The largest listed company in retail trade on the Athens bourse, a share that is especially popular with foreign institutional investors, had accustomed the market to continuous growth, high profitability and a generous dividend policy. The last year that Jumbo shareholders remember as being difficult was in 2013, when profitability was hit hard when 58 million euros in deposits in Cyprus took a haircut.

Even when disaster struck—as it did when Cyprus implemented deposit haircuts in 2013—Jumbo's diversification and liquidity allowed it to absorb the blow and continue operating.

International Expansion: The Balkan Strategy

While many Greek companies retreated to their home market during and after the crisis, Jumbo pursued the opposite strategy. In 1998, it acquired Jumbo Trading Ltd in Cyprus, followed by entry into Bulgaria in 2007 and Romania in 2013. Vakakis essentially expanded into neighboring markets with cultural similarities and logistical advantages.

The geographic logic was compelling. These markets shared proximity to Greece (enabling efficient logistics from centralized distribution), growing middle classes hungry for affordable consumer goods, and retail sectors less developed than Western Europe—meaning less competition from sophisticated international players.

At the end of 2024, products are marketed through a network of 88 hypermarkets located in Greece (53), Romania (19), Bulgaria (10) and Cyprus (6), and 3 online stores. Net sales are distributed geographically as follows: Greece (57.5%), Romania (21.9%), Cyprus (10.6%) and Bulgaria (10%).

Jumbo's geographic expansion strategy leverages opportunities in both established and emerging markets. The company continues to grow its store network across Greece, Cyprus, Bulgaria, and Romania, with a particular emphasis on Romania due to its favorable demographics and growth potential. By utilizing franchise partnerships, Jumbo has also entered non-EU markets such as Israel and the Balkans, achieving cost-efficient growth through royalties while limiting capital expenditure.

Romania represents the most significant growth opportunity. With a population of roughly 19 million and rising disposable incomes, it offers a market nearly twice the size of Greece. The group currently operates 20 stores in the country along with an online platform, and plans to double its network there over the next eight years.

The franchise model for non-core markets demonstrates sophisticated capital allocation. The company, through collaborations, had presence with 27 stores operating under the Jumbo brand in seven countries. Jumbo collaborates with Balfin Group in Albania, Bosnia and Herzegovina, Kosovo and Montenegro, Veropoulos in North Macedonia and Serbia, and Fox Group in Israel.

Jumbo expanded its market presence by opening a second store in Timisoara, Romania, and launching an online store in Bulgaria. Franchise sales grew significantly by 52%, contributing €38 million to the total sales.

An exciting development: The Fox Group plans to open franchise stores under the Jumbo brand in Canada by the end of 2026. This would represent Jumbo's first presence in North America and a significant vote of confidence in the brand's global applicability.

Product Diversification: Beyond the Toy Store

A key insight for investors: Jumbo is not a toy retailer in any traditional sense. Net sales break down by family of products as follows: decorative items and home products (39.1%); seasonal products (23.4%); toys (18.8%); stationery items (7.5%); baby items (2.7%); other (8.5%): primarily snacks and sweets.

Non-toy categories encompassing decor, household goods, baby items, stationery, and snacks represented 81% of total sales, underscoring the diversification beyond core toy offerings. This evolution from "toy store" to "value hypermarket without food, fashion, or electronics" happened gradually but deliberately.

Today, the company operates 89 owned or leased stores in Greece, Cyprus, Bulgaria, and Romania, along with 40 franchised stores in Southeast Europe and Israel. Its retail model, a hypermarket without food, fashion, or electronics, features over 40,000 SKUs and continues to draw strong consumer traffic.

The strategic brilliance of this positioning lies in what Jumbo doesn't sell. By avoiding food (with its perishability and thin margins), fashion (with its rapid obsolescence and return rates), and electronics (with its margin pressure and service requirements), Jumbo concentrates on categories where its sourcing advantages translate directly to consumer value.

Jumbo's sales are highly seasonal, with approximately 28% of annual revenue generated in December (Christmas), 12% in April (Easter), and 10% in September (back-to-school). This seasonality requires excellent inventory management, but it also creates natural traffic peaks that drive impulse purchases across categories.

The Operational Machine: What Makes Jumbo Work

The Hyperstore Model

Jumbo's operational model focuses on large hyper-stores, with an average size of 9,000 square meters, which helps maintain cost efficiency. The company leverages its direct purchasing strategy and low-cost production sources to offer competitive prices.

Store design plays a central role in the retail model, featuring wide aisles for easy navigation, thematic product displays to engage shoppers, and family-friendly layouts that accommodate strollers and children's exploration. The experience is designed to encourage browsing—parents can spend time with children while discovering products they didn't know they needed.

The Supply Chain Advantage

Roughly 70% of Jumbo's products are sourced from Asia, particularly China. The Company acts as the exclusive importer for several international toy manufacturers not represented in Greece, while also purchasing from 200+ local suppliers.

A key strength of Jumbo's business model lies in its procurement strategy. The company sources products directly from low-cost production hubs, primarily in Asia, bypassing intermediaries to achieve significant cost savings. This approach enables it to maintain low retail prices while preserving healthy profit margins.

The direct sourcing model creates a moat that smaller competitors cannot replicate. Establishing relationships with Chinese factories requires scale, expertise, and creditworthiness that take years to develop. Jumbo's procurement team has built these relationships over decades, enabling access to products at costs that would be impossible for smaller players to match.

The Pricing Philosophy

Founder Apostolos Vakakis recently reaffirmed this focus, stating: "There's absolutely no desire to adjust prices upwards. We would be more than happy to adjust prices downwards and pass theoretical gains to our customers in order to consolidate our future…So we always have to be very careful not to create a gap."

This philosophy—prioritizing long-term customer relationships over short-term margin optimization—explains why Jumbo maintained customer loyalty through the Greek crisis. Consumers trust that Jumbo prices are fair, and that trust translates to repeat visits.

The Advertising Genius: Cult Marketing on a Budget

One of the most distinctive aspects of Jumbo's success lies in its unconventional approach to marketing.

He is the person behind the advertisements that are occasionally shown on television or played on the radio. "Hit, hit like a man", "Hey, this is why you need Jumbo", and "Suck it up, see ya, see ya" are just a few of the provocative phrases heard on TV and radio spots. He has even chosen the central faces of the advertisements with a popular or often cult character.

These advertisements are intentionally low-budget, often cheesy, and always memorable. Rather than competing with sophisticated marketing from international brands, Jumbo has leaned into authenticity and humor. The ads have become cultural touchstones in Greece—people quote them, parody them, and share them. This earned media extends the impact far beyond the modest advertising spend.

The approach reflects Vakakis's broader philosophy: don't try to be what you're not. Jumbo isn't a luxury brand and doesn't pretend to be. The advertising reinforces the value proposition while creating emotional connections that transcend price.

Recent Performance & Modern Challenges (2020-2025)

The pandemic tested Jumbo in ways the Greek debt crisis had not. The pandemic and the restrictive measures imposed on trade twice in 2020 affected Jumbo more than expected. The final result announced was much worse, with the reduction of sales approaching 20%. The lockdown cut sales by 35%, while December, traditionally one of the strongest months for Jumbo, was much worse as consolidated sales plummeted by 54%.

At a strategy level, Vakakis showed a difficulty in adopting new e-commerce practices. This channel was not sufficiently developed before the pandemic, as only 2.5% of total sales were made online.

However, the company has since recovered strongly. In the first half of 2025, Jumbo S.A. sales grew by 8%, reaching €497 million. On a comparable basis, EBITDA increased by 7% to €165 million, and net profit increased by 5% to €117 million.

The geographical breakdown showed sales growth across all regions, with Greece and Cyprus each recording a 9% year-on-year increase, Bulgaria up by 3%, and Romania by 7% for the first eight months of 2025. Sales to franchisees grew by 52% year-on-year, amounting to €38 million.

Recent Headwinds

The company faces several challenges:

Supply Chain Concentration: With 70% of products originating from China, Jumbo is exposed to geopolitical risks. Any embargo on Chinese imports, increased tariffs, or disruption to manufacturing could interrupt product supply.

Red Sea Crisis: With 30% of global container trade passing through the Suez Canal, the Red Sea shipping crisis is upending supply chains. From December of 2023 to February of 2024, Asia-Europe container rates tripled to $5,500/FEU. The Red Sea crisis has led to delays in product deliveries and increased transportation costs.

Emerging Competition: Dutch non-food discounter Action opened its first store in Romania on September 24, 2025, entering a market where Jumbo is actively expanding. The new outlet, located in the Supernova Shopping Center in Pitești, covers more than 840 square meters. On 24 September, Action opened its first store in Romania, marking the start of operations in its 14th market. Since then, Action added four more stores already.

Gross profit margin declined due to market conditions, including increased VAT in Romania and geopolitical events. The company faces challenges in maintaining profitability, with a cautious outlook on achieving last year's net profit levels.

Porter's Five Forces Analysis

1. Threat of New Entrants: MODERATE-LOW

Capital requirements for the large hyperstore format create significant barriers. The average Jumbo store requires 9,000 square meters of retail space, substantial inventory investment, and sophisticated logistics capabilities. Direct sourcing relationships with Asian suppliers take years to develop. Prime retail real estate in target markets has been largely secured by Jumbo.

Brand awareness in the core Greek market approaches saturation—virtually every Greek consumer knows Jumbo. New entrants would need massive marketing investments just to achieve visibility.

2. Bargaining Power of Suppliers: LOW

Jumbo's scale provides leverage when negotiating with Chinese factories. As the exclusive importer for several international toy manufacturers in Greece, the company enjoys preferential terms. The diversified supplier base across 200+ local suppliers and Asian manufacturers prevents dependence on any single source. The commodity-like nature of many products enables supplier switching without significant disruption.

3. Bargaining Power of Buyers: MODERATE

Price-sensitive consumers can comparison shop, and digital platforms make price discovery easier than ever. However, Jumbo's breadth of selection (40,000+ SKUs) creates one-stop-shop convenience that partially offsets price sensitivity. No individual customer represents meaningful revenue concentration. Switching costs are low but convenience factors are high.

4. Threat of Substitutes: MODERATE-HIGH

E-commerce platforms including Amazon and local players serve similar needs. Chinese direct-to-consumer platforms like Temu and Shein target similar value propositions. Supermarkets are expanding into seasonal and household goods. However, none offer the complete package of selection, price, and physical browsing experience that Jumbo provides.

5. Competitive Rivalry: MODERATE

Action has become one of Europe's fastest-growing discount chains, appealing to budget-conscious shoppers with its rotating stock and low prices. In Romania, it will compete primarily with Pepco, a Polish retailer with a strong foothold in the region, and German discount chain Kik.

Jumbo's dominant position in Greece reduces direct competition intensity there. Regional competitors exist in the Balkans but remain fragmented. The entry of Action into Romania represents the most significant emerging competitive threat.

Hamilton's 7 Powers Framework Analysis

1. Scale Economies: ✓ STRONG

Jumbo is the largest retailer in its category across Greece and the Balkans. Fixed costs are absorbed across 89 owned stores, enabling per-unit cost advantages unavailable to smaller competitors. Procurement leverage with Asian manufacturers is unmatched by regional players. Marketing costs spread across a larger revenue base than any competitor.

2. Network Effects: ✗ WEAK

Limited network effects exist in the retail model. Unlike platform businesses, Jumbo doesn't become more valuable as more customers use it. There are no meaningful user-generated value or data network effects.

3. Counter-Positioning: ✓ MODERATE

Incumbent retailers would need to fundamentally restructure to compete with Jumbo's model. Traditional toy retailers can't match breadth across 17 categories. Supermarkets lack specialized merchandising expertise. Department stores carry higher cost structures that prevent matching Jumbo's prices.

4. Switching Costs: ✗ WEAK-MODERATE

No contractual lock-in exists for consumers. However, habitual shopping behavior and store familiarity create soft switching costs. Parents with young children develop store loyalty for convenience. The breadth of selection creates a "why go elsewhere?" dynamic.

5. Branding: ✓ STRONG

Brand recognition in Greece is exceptional—Jumbo is synonymous with affordable family retail. The cult advertising creates emotional connections beyond price. Consumer trust built through decades of consistent value proposition creates intangible brand equity.

6. Cornered Resource: ✓ MODERATE

Prime retail locations across Greece and expanding Balkan markets represent a cornered resource. Once secured, these locations cannot be replicated by competitors. Long-term supplier relationships, particularly exclusive import agreements, provide protected access to products.

7. Process Power: ✓ MODERATE

Decades of operational refinement have created institutional knowledge in procurement, logistics, and store operations that would take years for competitors to replicate. The ability to identify and source products at scale from diverse Asian suppliers represents accumulated process expertise.

Overall Assessment: Jumbo possesses meaningful competitive advantages, particularly in scale economies, branding, and process power. The absence of network effects and limited switching costs represent structural limitations common to physical retail. The competitive moat is real but requires continuous reinforcement through operational excellence.

Key Metrics to Watch

For long-term investors tracking Jumbo's performance, three KPIs deserve particular attention:

1. Same-Store Sales Growth

This metric strips out the effect of new store openings to reveal organic demand trends. During the Greek crisis, Jumbo's ability to maintain positive same-store sales while competitors collapsed demonstrated the resilience of its value proposition. Watch for this metric to remain positive in Greece while outperforming in international markets.

2. Gross Margin Trajectory

Our gross margin came at 54%. However, gross margins have come under pressure from multiple sources—franchise expansion (which carries lower margins than own-operated stores), transportation cost increases from Red Sea disruptions, and VAT changes in Romania. The ability to maintain margins above 50% while absorbing cost pressures would signal pricing power and operational discipline.

3. Romania Revenue as Percentage of Total

Romania accounts for 21.9% of net sales. As Greece approaches market saturation, Romania represents the primary growth driver. Tracking Romania's contribution to total revenue provides insight into whether the international expansion strategy is succeeding. A rising share indicates successful geographic diversification; a declining share might signal competitive pressure or execution challenges.

Myth vs. Reality

Myth: Jumbo is a toy retailer benefiting from Greek parents spoiling their children.

Reality: Toys represent less than 19% of revenue. Jumbo is a value-oriented variety retailer competing across home goods, seasonal items, and household essentials.

Myth: Jumbo succeeded because of weak competition in Greece.

Reality: Jumbo succeeded despite intense competition—they consolidated a fragmented market while international players entered post-EU accession. Their survival and growth through the debt crisis, when competitors with similar market positions failed, demonstrates execution superiority, not weak competition.

Myth: The Greek market is saturated, limiting growth potential.

Reality: Greece contributes 57% of revenue, but Romania's 22% contribution is growing faster. The franchise model in seven additional countries provides growth optionality without significant capital deployment.

Bull and Bear Cases

Bull Case

Continued Balkan Penetration: Romania offers a market nearly twice Greece's size with rising disposable incomes and limited competition. Successful execution could drive double-digit growth for years.

Franchise Model Expansion: The capital-light franchise approach enables market entry without significant investment. Canadian expansion through Fox Group could validate the model's global applicability.

Operational Leverage: Fixed-cost absorption across a growing store base drives margin expansion. Investment in distribution centers positions the company for the next phase of growth.

Counter-Cyclical Demand: In uncertain economic times—whether inflation, recession, or geopolitical disruption—value retailers historically outperform. Jumbo's positioning for "affordable joy" could prove prescient.

Bear Case

China Concentration Risk: With 70% of products sourced from China, any significant tariff increase or trade disruption could devastate margins or availability. Supply chain diversification would require years and significant investment.

Action Entry: Action operates stores in 14 countries including Romania as of 2025. The Dutch discounter's rapid expansion into Central and Eastern Europe directly threatens Jumbo's growth markets. Action's scale (3,000+ stores) dwarfs Jumbo's 89.

E-Commerce Disruption: Despite improvements, Jumbo remains primarily a brick-and-mortar retailer in an increasingly digital world. The browsing experience that differentiates physical stores may become less compelling for younger consumers.

Succession Risk: Jumbo remains a family-influenced business, as Vakakis still owns 16.4% and serves as Chairman. At 71 years old, Vakakis's eventual transition creates uncertainty. His younger daughter Christina pursued her passion for culinary arts, while his son George tragically passed away in a car accident in 2017, a loss that deeply affected the family.

Material Risk Disclosures

Geographic Concentration: Despite international expansion, Greece still contributes 57% of revenue. Extended Greek economic weakness would disproportionately impact results.

Supply Chain Vulnerability: Heavy reliance on Chinese manufacturing creates exposure to geopolitical risks, tariff changes, and shipping disruptions. The Red Sea crisis demonstrated how quickly transportation costs can spike.

Currency Exposure: Operations in Bulgaria (non-euro) create currency translation risk, though this is modest given the country's EU candidacy and currency board arrangement.

Regulatory Risk: Changes to import duties, VAT rates, or retail regulations in any operating market could impact profitability. The recent VAT increase in Romania illustrates this risk.

Key Person Risk: Apostolos Vakakis has led the company since 1986. While a CEO, Konstantina Demiri, handles day-to-day operations, Vakakis's strategic vision remains central to the company's identity.

Closing Perspective

The Jumbo story offers a masterclass in retail entrepreneurship under adversity. From Alexandria to Athens, through fires both literal and economic, Apostolos Vakakis built something remarkable—a value retailer that survived Greece's greatest peacetime economic collapse and emerged stronger.

The company's success rests on principles that seem simple but prove difficult to execute: maintain liquidity when others borrow, own assets when others lease, expand when others retrench, and never sacrifice the value proposition that earned customer trust.

Management said that if the annual growth rate remains at 8%, there is a likelihood that net profits will stay at last year's organic levels.

For investors, Jumbo presents an unusual combination: emerging market growth exposure (Romania, Bulgaria) with developed market governance (Athens Stock Exchange listing), family founder alignment (16.4% ownership) with professional management, and recession-resistant positioning with expansion optionality.

The risks are real—China concentration, emerging competition from Action, e-commerce disruption, and succession uncertainty all warrant monitoring. But the fundamental business model has proven itself through crises that destroyed competitors.

As Vakakis himself might say, with characteristic Greek pessimism covering underlying confidence: expect the worst, prepare for catastrophe, but keep building. In nearly four decades, that philosophy has transformed a single toy store in Glyfada into "The Industry of Joy" across Southeast Europe. The next chapter is being written in Romania, Bulgaria, and perhaps Canada—but the principles remain the same ones forged in fire, both literal and economic, generations ago.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube