Deepak Fertilisers: India's Ammonia-to-Everything Chemical Empire

I. Introduction & Episode Roadmap

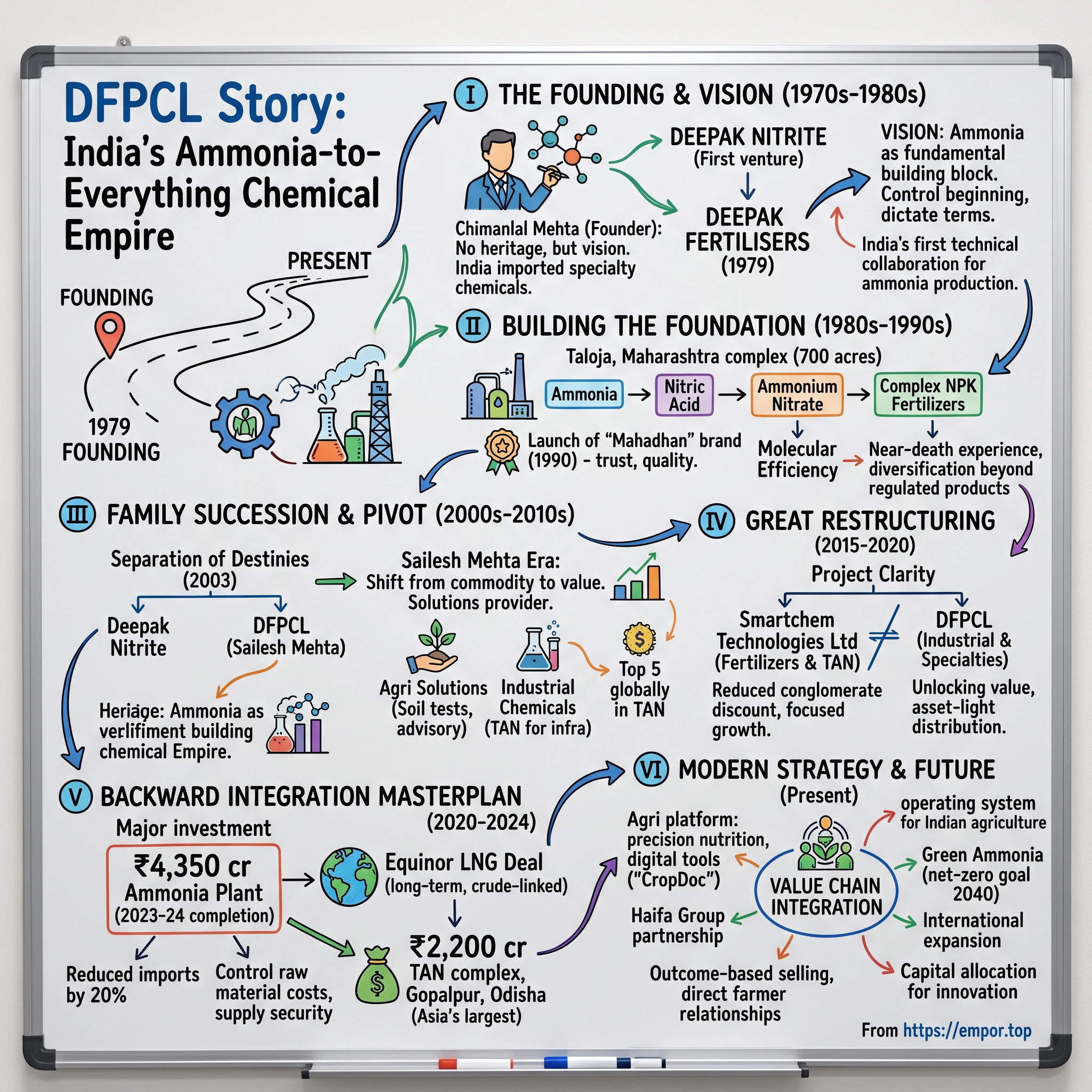

Picture this: A sprawling 700-acre chemical complex in Taloja, Maharashtra, where towering distillation columns pierce the humid monsoon sky. Inside the control room, engineers monitor real-time data streams as ammonia—the invisible building block of modern agriculture and industry—flows through a maze of steel pipes at 500,000 tonnes per year. This is the nerve center of Deepak Fertilisers and Petrochemicals Corporation (DFPCL), a company that quietly became one of the world's top five manufacturers of Technical Ammonium Nitrate and Asia's leading producer of Nitric Acid.

The story of DFPCL isn't just another Indian industrialization tale. It's a masterclass in chemical engineering meets family business dynamics, where a first-generation entrepreneur from Gujarat built what would become one of Asia's most integrated chemical conglomerates. Today, DFPCL touches everything from the explosives that blast through mountains for infrastructure projects to the fertilizers that feed millions of Indian farmers.

But here's what makes this story fascinating for investors and business strategists alike: How did Chimanlal Mehta, starting with zero industrial heritage, build a chemical empire that would eventually split between his sons and still thrive? How did a company that began importing ammonia transform into one that reduced India's ammonia imports by 20%? And perhaps most intriguingly—how did they navigate the treacherous waters of commodity chemicals to build defensible moats in specialty products?

The themes we'll explore read like a playbook for emerging market industrialization: vertical integration as competitive advantage, the delicate art of family succession, the pivot from commodities to solutions, and the strategic chess game of import substitution. This isn't just a chemicals story—it's about building industrial capacity in a developing nation, one molecule at a time.

What unfolds is a four-decade journey from a single ammonia plant to a fully integrated gas-to-chemicals value chain, with plot twists including brotherly empire splits, billion-dollar backward integration bets, and a transformation from B2B commodity supplier to B2C agricultural solutions provider. Along the way, we'll decode why ammonia—that pungent gas most people only know from cleaning products—became the foundation of an industrial empire.

II. The Chimanlal Mehta Origin Story & Founding Context

In 1970, while America was landing on the moon and India was still finding its industrial feet, a young Jain entrepreneur from Gujarat named Chimanlal Mehta was sketching molecular diagrams in a modest Mumbai office. He had no family business to inherit, no industrial legacy to lean on—just an engineer's understanding of chemistry and an entrepreneur's instinct that India's chemical industry was about to explode.

Mehta's first venture, Deepak Nitrite, began that year with a simple observation: India was importing nearly all its specialty chemicals, paying precious foreign exchange for molecules that could be manufactured domestically. The License Raj era meant getting industrial permits was like navigating a bureaucratic maze blindfolded, but Mehta saw opportunity where others saw obstacles. He understood that whoever could crack the code of basic chemical production in India would ride the wave of industrialization for decades.

By 1979, Mehta was ready for his boldest move yet. He established Deepak Fertilisers as a private limited company, converting it to public limited by 1982. But this wasn't just another fertilizer company—Mehta had a grander vision. He wanted to start with ammonia, the fundamental building block of all nitrogen chemistry. It's like deciding to manufacture silicon in the computer age; control ammonia, and you control the entire nitrogen value chain.

The ammonia bet was audacious for its time. Here was India, still recovering from the Emergency, with foreign exchange reserves that could barely cover three weeks of imports, and Mehta wanted to build capital-intensive chemical plants. But he had studied the post-war industrialization of Japan and Korea, noting how chemical companies there had become the backbone of economic transformation. Why couldn't India follow the same playbook?

Mehta secured something unprecedented: India's first technical collaboration with US-based Fish International for ammonia production. This wasn't just technology transfer—it was industrial DNA transplantation. The Americans brought process knowledge; Mehta brought local execution capability and an understanding of Indian market dynamics that no foreign company could match.

The early 1980s plant construction was a marvel of jugaad meets precision engineering. Equipment had to be imported piece by piece, with each shipment requiring multiple government clearances. Mehta would personally camp in Delhi's bureaucratic corridors, armed with technical drawings and economic impact studies, convincing skeptical officials that domestic ammonia production was a national priority.

When the first ammonia synthesis loop was fired up in 1982, it wasn't just a chemical reaction—it was India's declaration of industrial independence in nitrogenous chemicals. DFPCL became the country's first domestic ammonia producer, breaking the import monopoly that had constrained Indian agriculture and industry for decades.

But Mehta understood something his competitors missed: ammonia alone wouldn't build an empire. It was just the first domino. The real game was in downstream integration—converting that ammonia into increasingly sophisticated and valuable products. While others were content being traders or simple manufacturers, Mehta was already planning a vertical kingdom that would span from basic gases to complex fertilizer formulations.

The founding philosophy was deceptively simple yet profound: "If you control the beginning of the value chain, you can dictate terms all the way to the end." This would become the operating principle that would guide DFPCL through four decades of growth, multiple economic cycles, and eventually, one of Indian industry's most successful family business transitions.

III. Building the Foundation: Ammonia to Fertilizers (1979-1990s)

The Taloja complex in 1985 looked nothing like the industrial marvel it would become. Chimanlal Mehta stood on barren land outside Mumbai, visualizing storage spheres, prilling towers, and reaction vessels where others saw only rocky terrain and scattered villages. The location was strategic—close enough to Mumbai's ports for raw material imports, far enough to avoid the city's congestion, and critically, sitting on top of solid basalt rock that could support heavy industrial infrastructure.

Building a chemical complex in 1980s India was an exercise in extreme project management. Every piece of specialized equipment—compressors from Germany, heat exchangers from Italy, control systems from Japan—had to be individually licensed, imported, and somehow integrated into a cohesive production system. Mehta's team became experts at what they called "technical jugaad"—adapting foreign technology to Indian conditions, where power cuts were routine and skilled operators scarce.

The journey from ammonia to fertilizers wasn't just about adding downstream capacity; it was about understanding Indian agriculture's unique demands. India's Green Revolution had created massive fertilizer demand, but most farmers couldn't afford or didn't need the sophisticated formulations used in developed markets. Mehta's insight: create products that worked for Indian soil conditions, monsoon patterns, and critically, farmer economics.

By 1990, DFPCL launched "Mahadhan"—a brand name that would become synonymous with quality fertilizers across western India. The Sanskrit-derived name (Maha meaning great, Dhan meaning wealth) wasn't accidental. While competitors used technical names or English brands, Mehta understood that Indian farmers bought from brands they trusted, names that resonated with their aspirations.

The Mahadhan launch coincided with India's economic liberalization, but DFPCL faced a peculiar challenge. Fertilizer prices were controlled by the government, margins were wafer-thin, and yet demand was exploding. The solution wasn't to fight the system but to optimize within it. DFPCL pioneered what they called "molecular efficiency"—extracting maximum value from every unit of ammonia by converting it into the highest-value downstream products the regulations would allow.

Technical collaborations became Mehta's secret weapon. While Indian companies typically licensed old technology cheaply, DFPCL partnered with global leaders for cutting-edge processes. A collaboration with Weatherly Inc. brought advanced nitric acid technology; partnerships with European firms introduced concentrated fertilizer formulations. Each partnership was structured not just as technology transfer but as ongoing technical support—ensuring DFPCL's processes remained world-class.

The early 1990s brought a near-death experience that would define DFPCL's financial discipline forever. A combination of regulated fertilizer prices, rising input costs, and delayed government subsidies created a severe cash crunch. Banks were circling, and bankruptcy seemed imminent. Mehta's response was to completely restructure operations—cutting costs by 30% without reducing output, renegotiating every supplier contract, and most importantly, diversifying beyond government-controlled fertilizers into industrial chemicals where pricing was market-determined.

The turnaround strategy worked spectacularly. By 1995, DFPCL wasn't just profitable—it was generating enough cash to fund expansion without excessive debt. The lesson was seared into company DNA: never be wholly dependent on regulated products, always maintain product diversity, and cash flow is oxygen.

The 1990s ended with DFPCL as western India's largest fertilizer producer, but more importantly, as a company that had mastered the full ammonia-to-fertilizer value chain. Every molecule of ammonia could be converted into nitric acid, then to ammonium nitrate, and finally to complex NPK fertilizers—each step adding value, each product serving different customer segments from farmers to industrial users.

What started as one man's vision to produce basic chemicals had evolved into an integrated chemical complex producing over 20 different products. The foundation was set, but the real test would come with the next generation's entry into the business.

IV. Family Succession & The Sailesh Mehta Era (2000s-2010s)

The conference room at Deepak Group's Mumbai headquarters in 2003 witnessed one of Indian industry's most meticulously planned family separations. Chimanlal Mehta, now in his seventies, had called his sons together not for a typical board meeting, but for what he termed "the allocation of destinies." Unlike the messy public feuds that had torn apart the Ambanis or the Modis, Mehta had spent two years crafting a succession plan that would split his chemical empire cleanly between his sons.

The solution was surgical: Deepak, the elder son, would take Deepak Nitrite with its specialty chemicals and fine chemicals portfolio. Sailesh, the youngest, would get DFPCL with its fertilizers and industrial chemicals. It wasn't just a division of assets—it was a separation of strategic paths. Deepak Nitrite would pursue high-margin specialty chemicals for global markets; DFPCL would dominate bulk chemicals and fertilizers for domestic consumption.

Sailesh Mehta had actually joined DFPCL in 1991, spending over a decade learning the business from the shop floor up. Unlike many second-generation industrialists who parachuted into corner offices, Sailesh had worked in the Taloja plant, understood the chemistry, knew the customers, and critically, had earned the respect of senior managers who had worked with his father. When he became Managing Director in 2002 and Chairman & MD in 2012, it wasn't nepotism—it was succession planning executed with Japanese-level precision.

The early days of Sailesh's leadership coincided with a brutal reality check. He gathered his strategic team in 2005 and posed a question that would redefine DFPCL: "What should we do over the next decade with our businesses?" The data was sobering. Fertilizer margins were shrinking, Chinese chemical imports were flooding India, and DFPCL was increasingly looking like a commodity producer in a world that rewarded specialty players.

Sailesh's diagnosis was sharp: "There's too much talk about price, but it's important to make the shift to value." This wasn't just management consultant speak—it was a fundamental reimagining of what DFPCL could become. Instead of competing on price in commoditized fertilizers, why not become a solutions provider? Instead of selling products, why not sell outcomes?

The transformation began with seemingly small changes that revealed larger ambitions. The R&D budget was tripled. Scientists were hired from IITs and international universities. A new technical center was established focused not on producing chemicals but on understanding crop nutrition, soil science, and farming economics. DFPCL wasn't just making fertilizers anymore—it was engineering agricultural productivity.

The market initially didn't understand the strategy. Analysts questioned why a commodity chemical company was investing in agronomists and digital systems. The stock price languished as investors preferred the simpler story of pure-play specialty chemical companies. But Sailesh was playing a longer game, one his father would have appreciated: building moats through integration and customer relationships that commodity producers could never match.

By 2010, the strategy was bearing fruit. Mahadhan had evolved from a fertilizer brand to an agricultural solutions platform. Farmers weren't just buying bags of chemicals; they were buying soil testing, crop advisory services, and customized nutrient programs. The business model had shifted from B2B commodity sales to B2C solutions, with margins expanding accordingly.

The real masterstroke came in industrial chemicals, particularly Technical Ammonium Nitrate (TAN). While others saw TAN as a simple mining explosive ingredient, Sailesh recognized it as India's infrastructure play. Every tunnel, every quarry, every mining operation needed TAN. As India embarked on its infrastructure building spree, DFPCL positioned itself as the dominant domestic supplier, eventually becoming one of the world's top five TAN manufacturers.

The brothers' separation, rather than weakening the Deepak empire, had actually strengthened it. Free from the potential conflicts of shared ownership, both companies pursued focused strategies. They even collaborated when it made sense—Deepak Nitrite would supply certain intermediates to DFPCL, creating synergies without ownership complexity.

The 2010s ended with DFPCL at an inflection point. Revenues had doubled, margins had expanded, and the company had successfully transitioned from commodity producer to solutions provider. But Sailesh knew the biggest transformation was yet to come. The next decade would require DFPCL to solve its greatest vulnerability: dependence on imported ammonia, the very molecule his father had started with forty years earlier.

V. The Great Restructuring: Smartchem & Mining Chemicals (2015-2020)

The National Company Law Tribunal in Mumbai had seen many corporate restructurings, but DFPCL's 2018 proposal was unusual in its surgical precision. Sailesh Mehta's team had spent two years designing what they internally called "Project Clarity"—a complete reorganization that would finally solve DFPCL's biggest investor relations problem: nobody understood what the company actually did.

The complexity was staggering. DFPCL manufactured fertilizers but also mining explosives. It produced industrial acids but also crop nutrients. It served farmers buying 50kg bags and mining companies ordering thousands of tonnes. Analyst calls inevitably devolved into confusion: "So are you an agricultural company or an industrial company?" The answer—"both"—satisfied nobody.

The restructuring solution was elegant: create Smartchem Technologies Limited as a wholly-owned subsidiary housing all fertilizer and TAN businesses. DFPCL would retain industrial chemicals and specialty products. It was like separating conjoined twins who had different destinies—each would be stronger alone than together.

Smartchem wasn't just a legal entity—it was a philosophy shift. The name itself signaled ambition: smart chemistry for smarter agriculture. Within months of formation, Smartchem launched "Mahadhan Smartek," NPK complexes with organic compound coating that released nutrients based on soil temperature and moisture. This wasn't your grandfather's fertilizer—it was precision nutrition, with 35,000 tonnes sold in Maharashtra and Gujarat in the first year alone.

The TAN business, now clearly housed within Smartchem, revealed its true potential. India's infrastructure boom—highways, metros, tunnels through the Western Ghats—all required controlled explosions, and every explosion needed ammonium nitrate. Smartchem commanded 40% market share, with relationships spanning from Coal India's massive mining operations to boutique construction firms building mountain roads.

But the real strategic insight came in 2019 when Sailesh's team presented their analysis of global TAN markets. Australia's mining boom was consuming massive quantities, African markets were opening up, and environmental regulations were shutting down polluting Chinese producers. The opportunity wasn't just to dominate India but to become a global player. The constraint? Ammonia availability.

The December 2022 decision to demerge mining chemicals into a separate listed entity was the final piece of the restructuring puzzle. The logic was compelling: mining chemicals had different customers, different growth dynamics, and critically, different valuations. Fertilizer companies traded at 8-10x earnings; specialty mining chemical companies at 15-20x. Why should DFPCL shareholders suffer from conglomerate discount?

The demerger process revealed hidden value. The mining chemicals business wasn't just selling commodities—it had developed proprietary explosive formulations, on-site mixing capabilities, and technical expertise that commanded premium pricing. Mining companies weren't buying ammonium nitrate; they were buying blast optimization, safety protocols, and guaranteed supply reliability.

International interest was immediate. Global mining giants who had ignored DFPCL as a confused conglomerate suddenly saw a focused mining chemicals player with Asian cost advantages and world-scale production. Partnership inquiries flooded in from Australia, South Africa, and Latin America.

The restructuring also enabled something critics had said was impossible: making a commodity chemical business asset-light. Through Smartchem's innovative distribution model, inventory was pushed closer to consumption points, working capital cycles were shortened, and return on assets improved by 30%. The fertilizer business, freed from the capital intensity of the industrial side, could finally optimize for its own dynamics.

Market reaction was swift and positive. DFPCL's stock, which had languished in the "too complex to analyze" bucket, suddenly became a clear story. Investors could value each piece appropriately, analysts could model distinct business segments, and management could allocate capital based on specific segment returns rather than blended metrics.

The restructuring revealed an unexpected benefit: operational excellence through focus. The Smartchem team, no longer distracted by industrial chemical challenges, developed new fertilizer grades at twice the previous pace. The mining chemicals team, freed from fertilizer seasonality concerns, could pursue international contracts previously considered too complex.

By early 2020, the restructuring was complete. What started as a complex conglomerate had been transformed into a focused industrial chemicals company with clearly delineated subsidiaries. But this organizational clarity was just preparation for DFPCL's most ambitious move yet: solving the ammonia problem once and for all.

VI. The Backward Integration Masterplan (2020-2024)

The spreadsheet on Sailesh Mehta's laptop in early 2020 told a stark story: DFPCL imported 70% of its ammonia requirements, spending hundreds of crores annually on a commodity whose price swung wildly with global energy markets. Every geopolitical hiccup—whether in the Middle East or Ukraine—sent tremors through DFPCL's cost structure. The company that Chimanlal Mehta had founded to produce ammonia had somehow become one of India's largest ammonia importers.

The board meeting where Sailesh proposed building a ₹4,350 crore ammonia plant was electric with tension. India was entering COVID lockdowns, capital markets were frozen, and here was the CEO proposing the largest single investment in company history. The skeptics had valid points: ammonia was a commodity, global capacity was abundant, and wouldn't it be safer to remain asset-light?

Sailesh's response was a masterclass in strategic thinking: "We're not building an ammonia plant. We're completing our value chain." He pulled up global ammonia trade flows, showing how supply was concentrated in regions with cheap gas, how shipping routes were vulnerable to disruption, and critically, how India's ammonia demand would double by 2030. The question wasn't whether to build but whether they could afford not to.

The Taloja ammonia project, greenlit in 2021, was engineering ambition on steroids. The plan: build a 500,000 TPA world-scale plant using the latest KBR Purifier technology, making it one of the most energy-efficient ammonia plants globally. But this wasn't just about scale—it was about integration. The new plant would sit literally next to existing downstream units, with ammonia traveling meters, not thousands of kilometers, to become nitric acid, ammonium nitrate, or fertilizers.

The real coup came with the Equinor LNG deal. While competitors relied on spot LNG markets or domestic gas allocations, DFPCL secured a long-term contract with Norway's energy giant. The deal structure was innovative: pricing linked to crude oil rather than spot gas markets, providing predictability in a volatile world. It was like buying insurance against energy market chaos.

Construction through 2021-2022 was a logistical ballet performed during a pandemic. Equipment arrived from Europe in carefully orchestrated shipments, specialized welders were flown in from South Korea, and commissioning engineers worked in biosecure bubbles. The project team developed what they called "milestone medicine"—breaking the massive project into weekly milestones, each celebrated to maintain morale during lockdowns.

When the ammonia synthesis loop was successfully started in Q2 FY2023-24, it wasn't just another plant commissioning. It was transformation. DFPCL went from importing 300,000 tonnes annually to having surplus for merchant sales. The numbers were staggering: import substitution worth ₹2,000 crores annually, foreign exchange savings of $250 million, and critically, complete control over their primary raw material.

But Sailesh's team wasn't done. Even as the Taloja ammonia plant was coming online, ground was being broken at Gopalpur, Odisha for a ₹2,200 crore TAN complex. The location was strategic: eastern India's mining belt desperately needed local TAN supply, currently trucked expensively from western plants. The August 2024 commissioning would take DFPCL's TAN capacity to 850,000 tonnes annually—making it Asia's largest producer.

The backward integration wasn't just about ammonia; it was about energy security. DFPCL pioneered floating LNG storage at Taloja, becoming one of the few chemical companies with dedicated gas infrastructure. When European gas prices spiked 5x during the Ukraine crisis, DFPCL's locked-in LNG contracts looked prescient. Competitors scrambling for feedstock watched DFPCL operate at full capacity.

The integration philosophy extended beyond physical assets. DFPCL developed India's first integrated gas-to-fertilizer digital twin—a virtual model that optimized everything from LNG regasification to final product dispatch. AI algorithms predicted equipment failures, optimized energy consumption, and even adjusted production based on weather-driven fertilizer demand patterns.

The financial impact was immediate and dramatic. EBITDA margins expanded by 500 basis points. Working capital cycles shortened as import financing disappeared. Most importantly, earnings volatility—the bane of commodity chemical companies—dropped significantly. DFPCL could now offer customers price stability that import-dependent competitors couldn't match.

The strategic implications went beyond economics. The government's Atmanirbhar Bharat (self-reliant India) initiative suddenly had a poster child. DFPCL's ammonia plant reduced India's ammonia imports by 20%, saving precious foreign exchange and enhancing supply security. Policy makers in Delhi took notice—this was industrial strategy executed at the enterprise level.

By 2024, the backward integration masterplan was complete. DFPCL had transformed from an ammonia importer to a fully integrated producer with surplus for merchant sales. The company that started with ammonia had come full circle, but at a scale Chimanlal Mehta could barely have imagined.

VII. Value Chain Integration & Modern Strategy (2020s-Present)

The Monday morning strategy session in April 2024 at DFPCL's Mumbai headquarters wasn't your typical PowerPoint marathon. Sailesh Mehta had invited not just his executives but also data scientists, agronomists, and surprisingly, a behavioral economist from IIM Ahmedabad. The agenda: reimagining what a chemical company could be in the digital age.

"Getting the size right is just table stakes," Sailesh opened, gesturing at charts showing their doubled fertilizer capacity and expanded TAN footprint. "The real game is strengthening the value chain—not just vertically, but horizontally into customer minds." This wasn't MBA jargon; it was a fundamental rethinking of DFPCL's business model from molecule manufacturer to outcome optimizer.

The transformation started with a simple observation: farmers didn't want fertilizer; they wanted yield. Mining companies didn't want ammonium nitrate; they wanted efficient blasting. The chemical was just a means to an end, yet the entire industry was organized around selling bags of chemicals. DFPCL's insight: own the outcome, not just the input.

The Mahadhan transformation exemplified this philosophy. What began as a fertilizer brand evolved into a full-stack agricultural solutions platform. Soil testing vans equipped with IoT sensors and AI-powered analysis tools roamed rural Maharashtra, providing real-time nutrient deficiency mapping. Farmers received customized fertilizer prescriptions via WhatsApp, with application timing optimized for weather patterns. The tagline shifted from "Quality Fertilizers" to "Maximum Yield, Minimum Input."

The game-changing partnership with Israel's Haifa Group in March 2024 wasn't just another distribution deal—it was technology and innovation transfer at scale, aimed at promoting high-performing specialty fertilizers to improve quality and productivity of crops in India and developing nations. Haifa brought global expertise in precision nutrition; MAL (Mahadhan Agritech Limited) provided on-ground execution and deep understanding of Indian farming realities.

The partnership revealed DFPCL's strategic evolution: from competing on price in commodity fertilizers to competing on performance in specialty nutrition. Indian farmers gained access to advanced plant nutrition solutions and effective Nutrigation practices to improve crop yields and quality, while focusing on resource preservation and environmental protection. It was sustainability meeting profitability—a combination that had eluded Indian agriculture for decades.

Digital transformation wasn't bolted on; it was embedded in the value chain. DFPCL developed "CropDoc," an AI-powered diagnostic tool that could identify nutrient deficiencies from smartphone photos of leaves. Machine learning models trained on millions of images could prescribe corrective measures with 94% accuracy—better than most human agronomists. The app had 200,000 active users within six months, creating direct farmer relationships that bypassed traditional distribution inefficiencies.

The integrated gas-to-ammonia-to-chemicals strategy wasn't just about cost advantages—it was about supply chain resilience. When global supply chains broke during COVID and the Ukraine crisis, DFPCL's integrated model meant uninterrupted supply to customers. Competitors scrambling for imported ammonia watched DFPCL fulfill every contract, building trust that translated into long-term partnerships and premium pricing.

The mining chemicals business showcased value chain mastery differently. DFPCL didn't just supply TAN; they provided complete blasting solutions. Engineers were stationed at major mining sites, optimizing explosive formulations for specific geological conditions. IoT sensors tracked blast efficiency, with data feeding back to R&D teams for continuous improvement. Mining companies weren't buying explosives; they were buying "cost per tonne of ore extracted"—a metric DFPCL could optimize better than any competitor.

The B2B-to-B2C pivot in fertilizers was particularly audacious. While competitors sold to dealers who sold to retailers who sold to farmers, DFPCL built direct farmer relationships. "Mahadhan Farm Centers" weren't just retail outlets but knowledge hubs where farmers could get soil tested, attend training sessions, and access credit. The 500+ centers across Maharashtra and Gujarat created a moat competitors couldn't replicate—customer relationships worth more than any manufacturing asset.

International ambitions were carefully calibrated. Rather than competing globally in commodities, DFPCL targeted specific niches where Indian cost structures and technical capabilities created advantages. East African markets needed affordable fertilizers adapted to tropical soils—DFPCL's R&D had spent decades perfecting exactly such formulations. Southeast Asian palm oil plantations required specialized nutrition programs—Mahadhan's crop-specific expertise translated perfectly.

The financial elegance of the integrated strategy showed in the numbers. Return on capital employed jumped from 12% to 18% as value addition increased. Working capital turns improved as direct customer relationships reduced channel inventory. Most impressively, EBITDA per tonne of ammonia consumed—a metric Sailesh invented to track value creation—had tripled in five years.

By 2024, DFPCL had evolved into a publicly listed, multi-product Indian conglomerate with annual turnover exceeding a billion USD, spanning industrial chemicals, bulk and specialty fertilizers, farming diagnostics and solutions, and technical ammonium nitrate. But more than scale, it was the integration—from gas molecules to farmer outcomes—that defined the company's modern identity.

The vision for the next decade was even more ambitious: becoming the "operating system for Indian agriculture," where Mahadhan wouldn't just supply inputs but orchestrate the entire crop cycle from soil preparation to harvest optimization. It was chemical manufacturing reimagined as platform business—a transformation that would have seemed like science fiction when Chimanlal Mehta started with basic ammonia in 1979.

VIII. Playbook: Business & Investing Lessons

The DFPCL story reads like a masterclass in industrial strategy, but the real lessons aren't in the what—they're in the how. After four decades of evolution, certain patterns emerge that transcend chemicals and speak to building enduring businesses in emerging markets.

The Vertical Integration Paradox

Conventional wisdom says vertical integration is dead—killed by globalization, specialization, and asset-light business models. DFPCL proved the opposite in chemicals: vertical integration isn't about owning everything; it's about owning the critical choke points. By controlling ammonia production, they controlled their destiny. By integrating forward into solutions, they captured value that pure manufacturers missed.

The key insight: integrate where technology or supply security creates competitive advantage, outsource where markets are efficient. DFPCL makes its own ammonia (strategic) but sources packaging materials (commodity). They develop proprietary fertilizer formulations (differentiation) but use third-party logistics (scale economics). It's selective integration—surgical rather than wholesale.

Managing Cyclicality Through Portfolio Architecture

Chemical businesses are notoriously cyclical, but DFPCL's portfolio construction created natural hedges. When fertilizer prices are regulated and margins compressed, industrial chemicals compensate. When monsoons fail and fertilizer demand drops, infrastructure spending on TAN typically increases. It's not diversification for its own sake but thoughtful portfolio construction where businesses have different cycles, customers, and margin structures.

The portfolio math is elegant: fertilizers provide volume and cash flow stability, industrial chemicals deliver margins, TAN offers growth, and specialty products create differentiation. No single business drives more than 40% of profits, preventing concentration risk. Yet all businesses share the ammonia backbone, creating operational synergies without complexity.

The Family Business Succession Formula

Most Indian family businesses implode during succession—ego, emotion, and entitlement creating destructive dynamics. The Mehta family's surgical separation stands as a counter-example. The formula: divide by strategic logic, not by equal parts. Give each successor a coherent business they can shape independently. Eliminate operational interdependencies that create friction. Allow collaboration where mutually beneficial.

Deepak got specialty chemicals requiring global market development and technical sophistication—matching his international education and temperament. Sailesh got bulk chemicals and fertilizers requiring operational excellence and government relations—aligning with his hands-on style and local network. Both businesses thrived because leaders matched businesses, not because assets were divided equally.

From Commodity to Solutions: The Margin Expansion Journey

The shift from selling products to selling outcomes isn't just marketing—it's business model transformation. When DFPCL sold fertilizer bags, they competed on price with 20% gross margins. When they sold yield improvement solutions, margins expanded to 35%. The product was similar; the value proposition was transformed.

The transformation required three elements: technical capability to deliver superior outcomes, data systems to measure and prove value, and customer relationships deep enough to share in value creation. It's not enough to claim superior products; you must prove superior outcomes and capture fair share of value created.

Import Substitution 2.0: Beyond Simple Manufacturing

First-generation import substitution was simple: make in India what was being imported. DFPCL's approach was sophisticated: don't just substitute imports, create products better suited for Indian conditions. Their fertilizers weren't copies of international products but formulations optimized for Indian soils, climate, and crops.

This required deep technical capability—understanding not just how to manufacture but why products were designed certain ways and how to improve them. It meant investing in R&D when competitors were content being toll manufacturers. The payoff: products that commanded premium pricing despite being "import substitutes."

Capital Allocation as Competitive Advantage

Over four decades, DFPCL made three transformative capital allocation decisions: the initial ammonia investment (1979), the Mahadhan brand building (1990s), and the backward integration into ammonia (2020s). Each required betting the company, each was contrarian at the time, and each created step-function value creation.

The pattern: make few but transformative bets, time them for maximum impact, and execute flawlessly. Between big bets, optimize operations and strengthen balance sheet. It's episodic transformation rather than continuous tinkering—preserving organizational energy for moves that matter.

The Atmanirbhar Advantage

Contributing to the vision of Aatmanirbhar Bharat (self-reliant India) by reducing Indian ammonia imports by ~20% and conserving foreign exchange wasn't just good PR—it was strategic positioning. Government support follows companies that align with national priorities. Policy benefits—from PLI schemes to priority sector lending—flow to businesses solving India's strategic vulnerabilities.

DFPCL understood this early: frame business strategy in national interest terms. Don't just build an ammonia plant; reduce import dependence. Don't just make fertilizers; ensure food security. Don't just produce TAN; enable infrastructure development. It's capitalism with Indian characteristics—profit through national purpose.

Building Technical Moats in Commodity Businesses

Even in commodities, technical differentiation is possible. DFPCL's TAN isn't just ammonium nitrate—it's precisely prilled particles with controlled density, porosity, and oil absorption for optimal blasting. Their nitric acid isn't just 68% concentration—it's ultra-pure grade meeting pharmaceutical standards. These technical specifications, developed over decades, cannot be easily replicated.

The lesson: commodities become specialties through technical excellence. Invest in process optimization, quality control, and application engineering. Build customer specifications into competitive moats. Make switching costs about performance risk, not just price.

IX. Analysis & Bear vs. Bull Case

The Bull Case: India's Chemical Champion in the Making

The optimistic view sees DFPCL at an inflection point where multiple growth drivers converge. The complete ammonia self-sufficiency achieved in 2024 isn't just a one-time benefit—it's a permanent structural advantage in an industry where feedstock security determines competitive position. With ammonia import savings of ₹2,000 crores annually, DFPCL can invest in growth while competitors struggle with volatile input costs.

The company's leadership positions are formidable: only manufacturer of prilled and medical-grade ammonium nitrate in India, leading manufacturer of IPA, only producer of NP prill 24:24:0 fertilizer, and market leader in bentonite sulphur and water-soluble fertilizers. These aren't just market shares—they're technical moats built over decades that new entrants cannot easily replicate.

India's infrastructure boom is still in early innings. The government's ₹100 trillion infrastructure pipeline through 2030 requires massive quantities of TAN for tunneling, road cutting, and mining. DFPCL's 850,000 TPA capacity positions them as the domestic supplier of choice, with import substitution benefits and supply security that foreign suppliers cannot match.

The specialty fertilizer transition is accelerating. As Indian farmers become more sophisticated and outcomes-focused, demand for customized nutrition solutions grows exponentially. The Haifa partnership provides technology access, while Mahadhan's distribution network ensures execution. This combination—global technology with local execution—is devastating for competitors lacking either element.

Valuation remains compelling despite recent gains. At 12x forward earnings, DFPCL trades at a discount to specialty chemical peers (18-20x) despite similar growth profiles and superior integration. As the market recognizes the transformation from commodity to specialty player, multiple expansion could drive 50% returns independent of earnings growth.

The Bear Case: Commodity Cyclicality Never Dies

The skeptical view worries that DFPCL remains fundamentally a commodity chemical company dressed in specialty clothing. Ammonia and fertilizers are global commodities where Indian producers have no structural advantage. When global ammonia prices crash—as they do cyclically—DFPCL's backward integration becomes a liability, not an asset.

Natural gas price volatility remains the Achilles heel. Despite long-term LNG contracts, energy costs represent 60% of ammonia production costs. A sustained spike in global gas prices—driven by geopolitical events or supply disruptions—could destroy margins regardless of operational efficiency. The Europe energy crisis of 2022 showed how quickly gas-dependent businesses can become uncompetitive.

Government policy risk in fertilizers is perpetual. Fertilizer pricing, subsidies, and distribution remain politically sensitive. A populist government could mandate price cuts or direct sales that destroy profitability. The sector's history is littered with companies destroyed by adverse policy changes—why should DFPCL be different?

Chinese competition looms large. As China's domestic demand slows, their massive chemical capacity will seek export markets. Chinese producers, with scale advantages and government support, could flood Indian markets with cheap imports, destroying pricing power across commodities and semi-specialties. No amount of customer relationship or technical service can overcome 30% price disadvantages.

Environmental regulations pose growing threats. Ammonia and nitric acid production are carbon-intensive, with significant emissions. As India implements carbon taxes or emission trading, DFPCL's cost structure could deteriorate significantly. Investors increasingly avoid carbon-intensive businesses, potentially creating permanent valuation discounts.

The Balanced View: Transformation in Progress

The realistic assessment recognizes DFPCL as a company mid-transformation, with both commodity and specialty characteristics. The next five years will determine whether they successfully complete the pivot or remain stuck between two models.

Key monitorables for investors: - Specialty product revenue mix reaching 50% (currently ~35%) - EBITDA margin sustaining above 15% through cycles - Return on capital employed exceeding 20% consistently - Free cash flow generation funding growth without leverage - International revenue exceeding 25% of total

The valuation math suggests risk-reward favors bulls but requires patience. At current prices, the market values DFPCL at replacement cost of assets—essentially giving the business for free. Even modest success in specialty transition justifies 50% upside. However, execution risks and cyclical pressures could create 30% downside volatility along the way.

The institutional imperative matters: DFPCL must transform because standing still means commoditization. Whether they succeed depends on execution, market conditions, and competitive dynamics—all uncertain. But the strategic direction is clear, capabilities are building, and early results are encouraging.

For fundamental investors, DFPCL represents a classic "transformation option"—paying commodity multiples for potential specialty outcomes. The risk is time—transformations take longer than expected, testing investor patience. The opportunity is multiple expansion as the market recognizes change. It's not a trade but a three-to-five-year investment thesis requiring conviction through volatility.

X. Epilogue & "If We Were CEOs"

Standing at the Taloja complex in 2024, watching the massive ammonia reactor that now anchors DFPCL's entire value chain, it's worth pondering the road ahead. The journey from importer to producer, from commodity to specialty, from product to solution has been remarkable. But in chemicals, standing still means falling behind. What would the next decade look like if we were steering this ship?

The Green Ammonia Imperative

The elephant in the room is carbon. Traditional ammonia production generates 2 tonnes of CO2 per tonne of ammonia. With global carbon prices inevitable and customers demanding sustainable supply chains, green ammonia isn't optional—it's existential. If we were CEO, we'd announce a 200,000 TPA green ammonia project by 2027, using renewable energy-powered electrolysis. Yes, it's currently uneconomical, but first movers will capture regulatory benefits, customer premiums, and technological learning curves. Partner with a renewable energy major, secure government incentives, and position DFPCL as India's sustainable chemical champion.

The Southeast Asian Opportunity

India's chemical story is compelling, but Southeast Asia's is just beginning. Vietnam, Indonesia, and the Philippines are where India was 20 years ago—massive agricultural sectors, growing infrastructure needs, and minimal domestic chemical production. If we were CEO, we'd establish a "DFPCL International" division, starting with a small acquisition in Vietnam. Don't replicate Indian operations—adapt to local needs. Build local partnerships, understand regulatory nuances, and create an ASEAN beachhead for the next growth chapter.

Digital Agriculture at Scale

The Mahadhan digital initiatives are promising but subscale. Agriculture is becoming precision science—drones monitoring crop health, AI optimizing nutrient application, blockchain ensuring supply chain transparency. If we were CEO, we'd acquire an agri-tech startup and integrate it deeply with Mahadhan. Create India's first "Digital Farming as a Service" platform where farmers pay for outcomes, not products. Start with 10,000 progressive farmers, prove the model, then scale to millions. The defensibility isn't in chemicals but in data and algorithms.

The Specialty Chemicals Moonshot

DFPCL has specialty products but not specialty scale. The global specialty chemical market is $800 billion and growing. If we were CEO, we'd identify one mega-trend—perhaps battery chemicals for EVs or biodegradable polymers—and commit ₹5,000 crores over five years to build global scale. Don't dabble in twenty specialties; dominate one. Acquire technology, hire global talent, and build a business that can IPO separately at specialty multiples.

Capital Allocation 2.0

DFPCL generates significant cash but capital allocation remains traditional—reinvest in existing businesses or pay dividends. If we were CEO, we'd create a "DFPCL Ventures" arm with ₹500 crores to invest in chemical and agri-tech startups. Don't just invest money—provide market access, technical expertise, and scale-up support. Build an ecosystem where DFPCL is the nucleus of Indian chemical innovation. The returns aren't just financial but strategic—early visibility into disruptions and acquisition pipelines.

The Organizational Transformation

Chemical companies traditionally hire chemical engineers and build hierarchical organizations. If we were CEO, we'd reshape DFPCL for the 21st century. Hire data scientists, sustainability experts, and customer experience designers. Create autonomous business units with P&L responsibility. Implement OKRs replacing annual budgets. Build a culture of experimentation where failure is learning, not punishment. The goal: organizational agility to match market velocity.

The Sustainability Narrative

ESG isn't compliance—it's competitive advantage. If we were CEO, we'd commit DFPCL to net-zero emissions by 2040, with clear intermediate milestones. Publish detailed sustainability reports with third-party verification. Create products that help customers reduce their environmental footprint. Build the narrative that choosing DFPCL means choosing sustainability. In a world where capital flows to ESG leaders, this isn't altruism—it's value creation.

Final Reflections

The DFPCL story is ultimately about industrial transformation in an emerging economy. It shows that commodity businesses can evolve, family companies can professionalize, and import substitution can become innovation leadership. The next chapter isn't about making more chemicals but creating more value—for farmers seeking prosperity, industries seeking reliability, and investors seeking returns.

Chimanlal Mehta started with a simple question: why import what we can make? Sailesh evolved it to: why sell products when we can deliver solutions? The next generation must answer: how do we transform Indian agriculture and industry while building a sustainable future?

The ammonia molecule that started this journey remains central—it feeds the world and builds nations. But the company built around it has become something more: a platform for India's chemical ambitions, a bridge between global technology and local needs, and perhaps, a model for industrial companies navigating the transition from commodity to specialty, from product to platform, from local to global.

The journey from that first ammonia reactor in 1982 to today's integrated chemical conglomerate has been remarkable. The next forty years promise to be even more transformative. For investors, employees, and stakeholders, the DFPCL story is still being written—and the best chapters may be yet to come.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube