Hindalco Industries: From Independence to Global Aluminum Giant

I. Introduction & Episode Roadmap

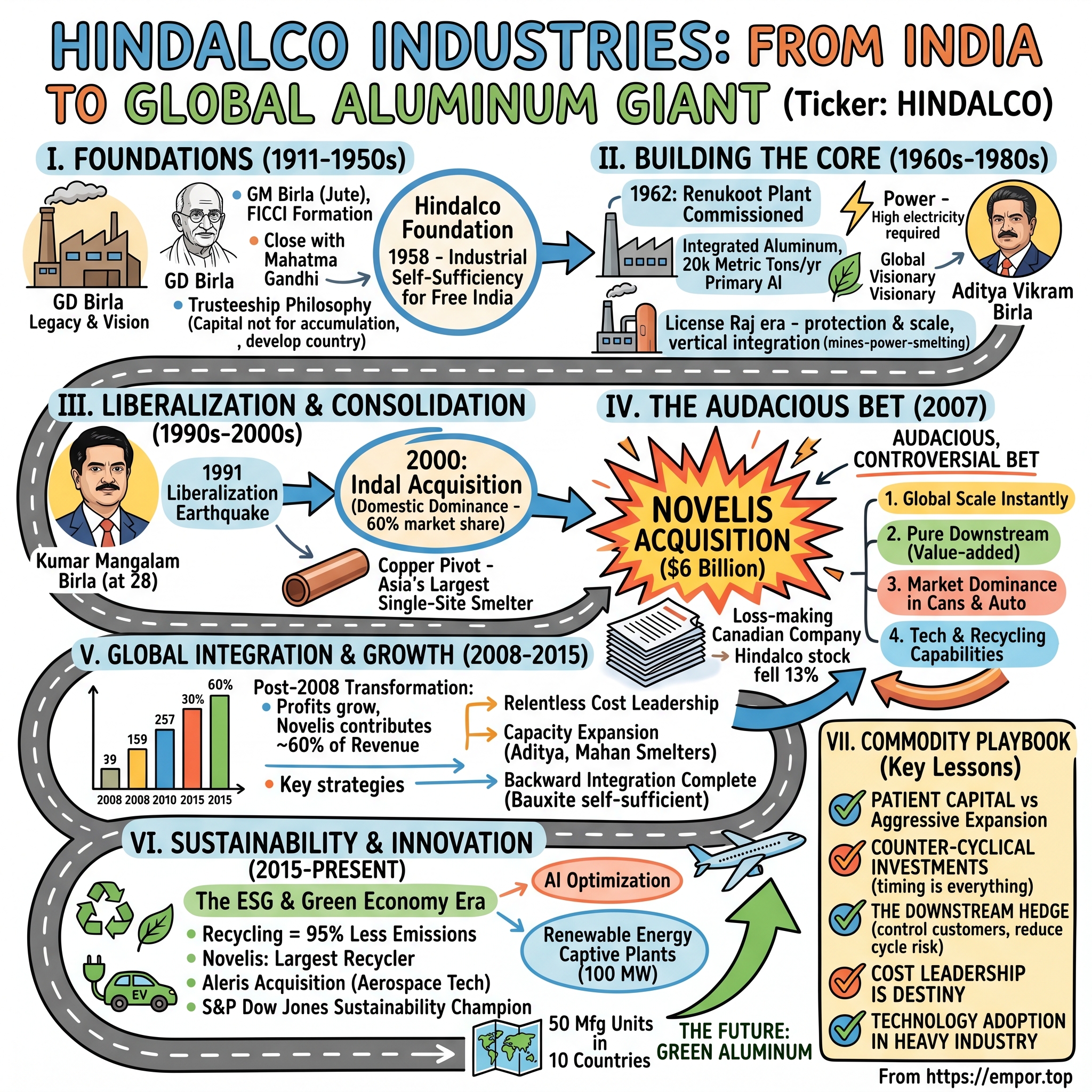

The year is 1958. India, barely a decade into independence, dreams of industrial self-sufficiency. In this crucible of nation-building, Ghanshyam Das Birla laid the foundation for Hindalco Industries Ltd., marking the inception of India's robust aluminum industry. What began as a post-independence vision to reduce import dependence has transformed into a $26 billion metals powerhouse—the world's largest aluminium company by revenues, and a major player in copper.

Today's Hindalco story is one of audacious bets, generational transitions, and the relentless pursuit of downstream value. How did a company that started with 20 thousand metric tons per year of aluminium production in a small town in Uttar Pradesh become the world's largest rolled-aluminium producer through one of India's most controversial acquisitions? How did the Birla family navigate the treacherous waters of the License Raj, survive the liberalization earthquake of 1991, and emerge stronger through global financial crises?

This is the story of three remarkable leaders across three generations: Ghanshyam Das Birla, the freedom fighter-industrialist who laid the foundation; Aditya Vikram Birla, the global visionary who died too young; and Kumar Mangalam Birla, who at 28 had to prove himself worthy of a legacy while betting $6 billion on a loss-making Canadian company that everyone said he overpaid for.

At its core, this is a masterclass in commodity business strategy—how to thrive in cyclical industries, when to integrate vertically versus horizontally, and most importantly, how to transform from a producer of raw materials into a provider of sophisticated solutions. It's about understanding that in commodities, you either control your costs or your customers control your destiny.

We'll explore how Hindalco's journey mirrors India's own economic evolution—from import substitution to liberalization, from domestic focus to global ambitions. We'll dissect the Novelis acquisition that shocked the markets, understand the aluminum industry's peculiar economics where electricity costs can make or break you, and examine how a traditional metals company is positioning itself for the green economy revolution.

This episode will take you from the dusty construction sites of Renukoot in 1962 to the boardrooms of Atlanta in 2007, from the bauxite mines of Odisha to the beverage can factories of North America. Along the way, we'll uncover the strategic lessons that every business leader should understand about managing capital-intensive businesses, timing market cycles, and building global scale while maintaining local advantages.

II. The Birla Legacy & Industrial Foundation

To understand Hindalco, we must first understand the extraordinary man who created it and the family dynasty that would shape modern Indian industry. Ghanshyam Das Birla, founder of the Aditya Birla Group, was born in 1894 into a family that supported India's small-scale cotton and jute sectors. But G.D. Birla, as he came to be known, had ambitions that transcended traditional trading.

The Birla story begins not with aluminum but with jute and cotton in colonial Calcutta. Ghanshyamdas Birla laid the foundation of his industrial empire by establishing GM Birla Company, trading in jute, in 1911. In 1919, he became among the first group of Indian entrepreneurs to become owner of a jute mill named Birla Jute. In the next few years he acquired several cotton mills. This was revolutionary—Indian entrepreneurs challenging the British monopoly on manufacturing.

But what set G.D. Birla apart wasn't just his business acumen; it was his unique position at the intersection of commerce and nationalism. Birla was a close associate and a steady supporter of Mahatma Gandhi, whom he met for the first time in 1916. Gandhi stayed at Birla's home in New Delhi during the last four months of his life. This wasn't merely a friendship—it was a strategic alliance between political freedom and economic independence.

Leading the charge for Indian businesses, he played a pivotal role in the formation of the Federation of Indian Chambers of Commerce and Industry (FICCI). As Piramal wrote, "In record time, Birla and Thakurdas managed to endow FICCI with an all-India character." Unlike other Indian business associations at the time, FICCI and the Indian Chamber of Commerce expressed their support for the freedom struggle.

The Birla philosophy of business was revolutionary for its time. Mahatma Gandhi's concept of trusteeship served as a philosophical foundation for Shri G D Birla. He once said, "It has been the policy of the House of Birla not to build up business with a view to the accumulation of capital but to develop unexplored lines, harness the undeveloped resources of the country, promote know-how, create skilled labour and managerial talent, spread education and above all, add to the efforts of the leaders of the country who have been struggling to build a new, independent India, free from want, the curse of unemployment, ignorance and disease".

After independence in 1947, G.D. Birla saw an opportunity to build the industrial infrastructure that a free India desperately needed. In newly independent India, he established the critical factories that would deliver much-needed industrial inputs for a growing nation – from viscose staple fibres and textiles, to infrastructural necessities such as aluminium, cement and chemicals.

Why aluminum? In the 1950s, aluminum wasn't just another commodity—it was a strategic metal, essential for electrification (transmission lines), transportation (railways, automobiles), defense (aircraft), and construction. India was importing virtually all its aluminum, draining precious foreign exchange. The government, under Nehru's socialist framework, wanted import substitution, and G.D. Birla saw the opportunity to build a national champion.

In the late 1950s, when India was giving shape to its economic vision, one visionary leader, the late G.D. Birla took the bold step to set up the country's first integrated aluminium facility at Renukoot, Uttar Pradesh. That vision gained strength as Hindalco Industries Ltd., grew in size and scale under the dynamic leadership of the late Aditya Vikram Birla.

The choice of aluminum was strategic on multiple levels. First, India had substantial bauxite reserves, particularly in Odisha, Jharkhand, and Chhattisgarh. Second, the technology, while complex, was mature enough to be transferred from the West. Third, the government was willing to provide protection through high import duties and licensing restrictions. Fourth, aluminum demand was set to explode as India industrialized.

But perhaps most importantly, aluminum represented the kind of capital-intensive, technology-driven industry that could showcase Indian entrepreneurial capability. This wasn't trading or textiles—this was heavy industry, the kind that transformed nations.

The Birla approach to business was distinct. While other business houses focused on trading or light manufacturing, the Birlas bet on capital-intensive industries with high barriers to entry. They understood that in commodities, scale and integration were everything. They also understood something else crucial: in a relationship-driven economy like India, trust and reputation were invaluable assets.

By 1958, when Hindalco was founded, G.D. Birla had already established himself as one of India's foremost industrialists. For his role in shaping India's destiny, Mr. G.D. Birla was awarded the Padma Vibhushan, India's second-highest civilian honour. But he wasn't content with past achievements. At 64, an age when many would be thinking of retirement, he was embarking on his most ambitious project yet.

The establishment of Hindalco represented more than just another business venture. It was a statement of faith in India's industrial future, a bet that the country could master complex metallurgical processes, and a commitment to building institutions that would outlast their founders. As we'll see, this long-term thinking would become a hallmark of the Birla approach to business, passed down through generations and tested through crises.

III. Genesis: Building India's Aluminum Industry (1958–1980s)

The Hindustan Aluminium Corporation Limited was established in 1958 by the Aditya Birla Group. The name itself—Hindustan Aluminium—reflected the nationalist sentiment of the era. This wasn't just a business; it was a contribution to nation-building.

The real work began in Renukoot, a small town in eastern Uttar Pradesh, chosen for its proximity to coal mines (crucial for power generation) and reasonable access to bauxite reserves. Commissioned in 1962, just four years after our inception, this plant marked a major milestone in our contribution to the vision of an industrial India. In 1962 the company began production in Renukoot in Uttar Pradesh making 20 thousand metric tons per year of aluminium and 40 thousand metric tons per year of alumina.

Building an aluminum smelter in 1960s India was an extraordinary challenge. The technology was complex—the Hall-Héroult process for aluminum smelting required massive amounts of electricity (about 13-15 MWh per ton of aluminum), precise temperature control, and sophisticated electrochemical knowledge. India had limited domestic expertise in these areas.

Here's where G.D. Birla's strategic thinking shone through. Rather than trying to reinvent the wheel, Hindalco sought technical collaboration with established Western players. The company worked with international consultants and equipment suppliers, learning and adapting global best practices to Indian conditions. This pragmatic approach—nationalist in purpose but internationalist in method—would become a template for Indian industrialization.

The Renukoot plant wasn't just a factory; it was an entire ecosystem. Originally commissioned with an annual smelting capacity of 20,000 tonnes, the unit has undergone various brownfield expansions and asset-sweating measures over the years to reach its current capacity of 410,000 tonnes. The company had to build not just the smelter but also power plants, townships for workers, schools, hospitals, and roads. This was typical of the era—large industrial houses didn't just build factories; they built communities.

The economics of aluminum production in the 1960s were challenging but favorable for an integrated player like Hindalco. The government's import substitution policies meant high tariffs on imported aluminum (often exceeding 100%), providing a comfortable cushion for domestic producers. The License Raj, much maligned for its inefficiencies, actually protected early manufacturers from competition, giving them time to achieve scale and efficiency.

Power was the critical factor—and remains so today. Aluminum smelting is essentially a process of converting electrical energy into metal. Electricity typically accounts for 30-40% of the production cost of aluminum. Recognizing this, Hindalco invested heavily in captive power generation. Renusagar Power Plant. An 826.57 MW (10 generating units of various capacities) captive power plant which is about 40 km from Renukoot, Sonebhadra district, Uttar Pradesh. This vertical integration into power would prove to be a crucial competitive advantage.

The technical challenges were immense. The alumina refinery had to handle the complex Bayer process, converting bauxite into alumina through a series of chemical reactions involving caustic soda at high temperatures and pressures. The smelter required thousands of electrolytic cells operating at temperatures exceeding 960°C, with precise control of electrical current and chemical composition.

Quality was initially a challenge. Early production often didn't meet international standards, limiting export potential. But Hindalco persistently invested in technology upgrades and process improvements. By the 1970s, the company's aluminum was good enough to be registered on the London Metal Exchange (LME), a crucial recognition that opened up international markets.

The 1970s brought new challenges and opportunities. The global oil crisis of 1973 sent energy costs soaring, squeezing margins for aluminum producers worldwide. But it also increased the value of energy-efficient production and captive power generation—areas where Hindalco had invested heavily. The company's integrated model, from bauxite mining to aluminum smelting, provided a buffer against commodity price volatility.

Under the leadership of Aditya Vikram Birla, who had joined the business in the late 1960s, Hindalco began to think beyond just primary aluminum. Aditya Vikram Birla was an Indian industrialist and philanthropist. Born into one of the largest business families of India, he oversaw the diversification of his group into textiles, petrochemicals and telecommunications. He was one of the first Indian industrialists to expand abroad, setting up plants in Southeast Asia, the Philippines and Egypt.

The company started investing in downstream facilities—rolling mills, extrusion plants, and foil manufacturing. This was strategic: while primary aluminum is a commodity with thin margins, downstream products command premium prices and offer differentiation opportunities. A ton of aluminum foil, for instance, could fetch several times the price of primary aluminum ingots.

By 1980, Hindalco had established itself as India's largest aluminum producer, but the company and its leaders knew that domestic dominance was just the beginning. The controlled economy of the License Raj had provided a protective cocoon, but winds of change were beginning to blow. Global aluminum giants like Alcoa, Alcan, and Reynolds were achieving scales that dwarfed Indian producers. Technology was advancing rapidly, with new smelting processes promising dramatic efficiency improvements.

The 1980s would prove to be a decade of preparation for the dramatic changes ahead. Hindalco continued to expand capacity, modernize technology, and strengthen its vertical integration. The company also began to look seriously at international markets, both for exports and for technology partnerships. In 1989 the company was restructured and renamed Hindalco, signaling a new phase in its evolution.

IV. The Liberalization Leap (1990s–2000s)

The year 1991 changed everything. India's balance of payments crisis forced the government to liberalize the economy, dismantling the License Raj and opening doors to foreign competition. For Hindalco, this was both a threat and an opportunity. The protective tariffs that had shielded domestic producers began to come down. Suddenly, Hindalco wasn't just competing with Vedanta or NALCO—it was competing with global giants.

But 1991 brought another crisis that would prove even more consequential for Hindalco's future. In 1993, Birla was diagnosed with prostate cancer. His aged father and young son took over many of the responsibilities of the group. He received medical treatment at the Johns Hopkins Hospital in Baltimore, where he died on 1 October 1995.

The death of Aditya Vikram Birla at just 51 years old created a succession crisis that could have destroyed the group. Kumar Mangalam Birla took over as chairman of the Aditya Birla Group in 1995, at the age of 28, following the death of his father. After his death at the age of 51, his son Kumar Mangalam Birla took charge of the group.

The young Kumar Mangalam faced enormous skepticism. Here was a 28-year-old chartered accountant with an MBA from London Business School, suddenly thrust into leading one of India's largest conglomerates. The old guard within the company questioned whether he had the experience and gravitas to lead. Competitors circled, sensing weakness. The financial press was brutal in its assessment of his prospects.

Misra, the newcomer, witnessed at close quarters the attitudes towards Aditya Birla's son. "People admired his father and they found him different," Misra recalls about Birla's first years. "Anything new he tried to do was seen as a departure from the past. People also expected him to work at the same speed and with the same decision-making agility as his father. But having been given the role so suddenly, he needed time to make up his mind".

But Kumar Mangalam had been quietly preparing. Unlike his father, who was a chemical engineer with a deep understanding of operations, Kumar Mangalam was a finance professional who understood capital markets, M&A, and modern management practices. He recognized that in the post-liberalization era, Hindalco needed to transform from a domestically focused, operationally excellent company into a globally competitive, strategically sophisticated corporation.

His first major move was consolidation. Under the leadership of the Aditya Birla Group's current Chairman, Mr. Kumar Mangalam Birla, Hindalco acquired Indal, the domestic aluminium major and the Australian Nifty and Mt Gordon copper mines, merging the Aditya Birla Group's copper division to create a non-ferrous metals powerhouse. The acquisition of Indian Aluminium Company (Indal) from Alcan in 2000 was masterful. Indal was Hindalco's biggest domestic competitor, and its acquisition immediately gave Hindalco a dominant 60% market share in Indian aluminum.

The Indal acquisition also brought valuable downstream assets—rolling mills, extrusion plants, and a strong brand in the retail market. More importantly, it brought international exposure and technology. Indal, as a former Alcan subsidiary, had access to global best practices and technical know-how that Hindalco could now leverage.

The late 1990s and early 2000s were also a period of massive capacity expansion. Kumar Mangalam understood that in commodities, scale is destiny. The company invested heavily in expanding its smelting capacity, but more importantly, in backward integration into bauxite mining and alumina refining. By controlling the entire value chain from mine to market, Hindalco could capture margins at every stage and insulate itself from raw material price volatility.

The copper pivot was another strategic masterstroke. Its subsidiary, Birla Copper, operates Asia's largest single-site copper smelter. While aluminum was Hindalco's heritage business, Kumar Mangalam recognized that copper offered attractive growth opportunities. India's rapid electrification and infrastructure development would drive massive copper demand. The acquisition of the Birla Copper assets and their subsequent expansion created a second leg for Hindalco's growth.

Technology became a key focus area. The company invested heavily in modernizing its smelters, implementing computer-controlled processes, and improving energy efficiency. The development of its own technical capabilities through the Hindalco Innovation Centre allowed the company to customize global technologies for Indian conditions and even develop proprietary processes.

The 2000s also saw Hindalco's first serious international forays. In 2003, Hindalco Industries acquired Nifty Copper Mines in Australia, while the Aditya Birla Group acquired the Mount Gordon Copper mines in Australia. These acquisitions weren't just about securing raw material supplies; they were about learning to operate in developed markets with different regulatory frameworks, labor practices, and stakeholder expectations.

Financial engineering became as important as metallurgical engineering. Kumar Mangalam leveraged India's growing capital markets to raise funds for expansion. The company's GDR (Global Depository Receipt) listings gave it access to international capital. Debt was carefully structured to match cash flows, and the company maintained strong relationships with both domestic and international banks.

By 2006, Hindalco had transformed itself from a domestic aluminum producer into an integrated metals powerhouse. Revenues had grown from $2 billion when Kumar Mangalam took over in 1995 to over $4 billion. The company was profitable, had strong cash flows, and possessed one of the lowest cost positions globally in aluminum production.

But Kumar Mangalam wasn't satisfied with being a big fish in the Indian pond. He had global ambitions. The aluminum industry was consolidating globally, with major players acquiring smaller ones to achieve scale and market power. Chinese producers were expanding aggressively, threatening to reshape global markets. Kumar Mangalam knew that Hindalco needed to make a transformative move to remain relevant on the global stage.

The stage was set for what would become one of the most audacious—and controversial—acquisitions in Indian corporate history.

V. The Novelis Acquisition: $6 Billion Bet on Downstream (2007)

On February 11, 2007, Hindalco Industries Limited (BSE: HINDALCO), India's largest non-ferrous metals company, and Novelis Inc., the world's leading producer of aluminum rolled products, announced that they have entered into a definitive agreement for Hindalco to acquire Novelis in an all-cash transaction which values Novelis at approximately $6.0 billion, including approximately $2.4 billion of debt. Mr. Kumar Mangalam Birla, Chairman of the Aditya Birla Group, said, "The acquisition of Novelis is a landmark transaction for Hindalco and our Group. It is in line with our long-term strategies of expanding our global presence across our various businesses and is consistent with our vision of taking India to the world. The combination of Hindalco and Novelis will establish a global integrated aluminum producer with low-cost alumina and aluminum production facilities combined with high-end aluminum rolled product capabilities".

The announcement sent shockwaves through corporate India and global aluminum markets. The day after Hindalco announced the acquisition its stock fell by 13% resulting in a US$600 million drop in market capitalisation. Shareholders criticised the deal but Kumar Mangalam Birla responded that he had offered a fair price for the company and stated, "When you are acquiring a world leader you will have to pay a premium".

To understand why this acquisition was so controversial, we need to understand what Novelis was and wasn't. The company was incorporated in 2004 after being spun off from Alcan, a now defunct Canadian mining and aluminum manufacturer. In 2007 the company was acquired by Hindalco Industries for $6 billion. Novelis was a pure-play downstream aluminum company—it didn't mine bauxite or smelt aluminum. Instead, it took primary aluminum and converted it into high-value rolled products used in beverage cans, automobiles, and aerospace applications.

At the time of acquisition, Novelis was struggling. The company had been spun off from Alcan just two years earlier as part of Alcan's strategy to focus on primary aluminum. Novelis was saddled with debt, had declining profitability, and faced significant operational challenges. In 2006, it had reported a net loss of $263 million on revenues of $8.4 billion. Many analysts questioned why Hindalco would pay $6 billion for a loss-making company.

But Kumar Mangalam saw what others didn't. First, he understood that the future of aluminum wasn't in producing primary metal—where China was building massive capacity—but in downstream value-added products. While primary aluminum is a pure commodity, rolled products for specific applications command premium prices and customer relationships create switching costs.

Second, Novelis gave Hindalco instant global scale and presence. Novelis is the global leader in aluminum rolled products and aluminum can recycling. The Company operates in 11 countries, has approximately 12,500 employees, and reported $8.4 billion in 2005 revenue. Post-acquisition, Hindalco would become the world's largest aluminum rolling company, with a presence across North America, South America, Europe, and Asia.

Third, the beverage can market was particularly attractive. Its wholly-owned subsidiary Novelis Inc. is the world's largest producer of aluminium beverage can stock and the largest recycler of used beverage cans (UBCs). Aluminum cans were gaining share from glass and plastic bottles due to their recyclability, light weight, and cooling properties. The beverage can market was also relatively stable, with long-term contracts and predictable demand patterns.

Fourth, Novelis brought technological capabilities that would take Hindalco decades to develop organically. The company had sophisticated rolling technology, deep customer relationships with companies like Coca-Cola and Anheuser-Busch, and expertise in aluminum recycling—increasingly important as sustainability became a key concern.

The financing of the deal was complex and demonstrated Kumar Mangalam's financial sophistication. Original lead arrangers and book-runners ABN AMRO, Bank of America and UBS (Singapore Branch) funded the deal in May 2007. The dual-tranche facility was split between the two subsidiaries with a US $2.2 billion financing for AV Minerals and a US $900 million portion for AV Metals, both with a tenor of 18 months. The deal was structured through overseas subsidiaries to optimize tax efficiency and regulatory compliance.

The timing of the acquisition, in retrospect, was both fortunate and unfortunate. Fortunate because it was completed just before the 2008 global financial crisis, which would have made such a large acquisition impossible. Unfortunate because Novelis had to navigate the worst economic downturn since the Great Depression just as it was being integrated into Hindalco.

The integration challenges were immense. Hindalco also assumed US $2.8 billion of Novelis' debt for a total transaction value of US $6.2 billion (Aggregate Purchase Price for Novelis' common shares of US $3.4 billion + Novelis' Total Debt of US $2.8 billion). Novelis had a completely different corporate culture—North American, decentralized, and focused on customer service rather than operational efficiency. Hindalco's managers, used to running integrated smelting operations in India, had to learn to manage a global downstream business with different economics and success factors.

The early years were brutal. The 2008 financial crisis caused aluminum demand to plummet. Automotive production, a key market for Novelis, collapsed. The company's debt burden became crushing as EBITDA fell. Many analysts wrote off the acquisition as a costly mistake, pointing to the high price paid and the timing just before the crisis.

But Kumar Mangalam and his team persevered. They brought in professional management, including hiring Steve Fisher as CEO of Novelis in 2009. They focused relentlessly on operational improvements, cost reduction, and customer service. They invested in recycling capabilities, recognizing that recycled aluminum required only 5% of the energy needed for primary production.

The transformation was gradual but dramatic. In the past seven years, Novelis' revenue have grown at a CAGR of 11.1 per cent against 11.5 per cent growth reported by other segments. In the same period, Novelis' PBIT and assets have grown at a CAGR of 16.8 per cent and 13.1 per cent, respectively, compared to 15.5 per cent and 6.9 per cent CAGR growth reported by Hindalco's other segments.

By 2015, Novelis had become highly profitable, generating over $1 billion in EBITDA. The automotive market had become a key growth driver, with aluminum increasingly replacing steel in vehicles to reduce weight and improve fuel efficiency. The company's recycling capabilities became a competitive advantage as customers increasingly demanded sustainable solutions.

The Novelis acquisition fundamentally transformed Hindalco. In the first nine months of FY24, Novelis accounted for 62.7 per cent of Hindalco's consolidated revenue of Rs 1.6 trillion. Similarly, Novelis accounted for 56.3 per cent of Hindalco's consolidated profit before interest and taxes (PBIT) in 9MFY24 worth Rs 19,950 crore. Novelis reported a PBIT of Rs 11,237 crore during the April-December 2023 period, compared to a full-year PBIT of Rs 14,543 crore in FY23.

VI. Building the Integrated Giant (2008–2015)

The period following the Novelis acquisition was one of intense consolidation and operational improvement. While the global financial crisis had created immediate challenges, it also presented opportunities for a well-capitalized player like Hindalco to strengthen its position while competitors struggled.

The integration of Novelis was the immediate priority. Rather than imposing an Indian management style on a Western company, Kumar Mangalam took a nuanced approach. Novelis was allowed to maintain its operational independence while being integrated into Hindalco's financial and strategic planning processes. Key performance indicators were aligned, best practices were shared, but local management was empowered to make operational decisions.

Back in India, Hindalco didn't slow down its domestic expansion. The company recognized that its low-cost Indian operations were the cash generation engine that would support global ambitions. Major capacity expansions were undertaken at the Aditya Aluminium smelter in Odisha and the Mahan smelter in Madhya Pradesh. These new smelters incorporated state-of-the-art technology and achieved some of the lowest production costs globally.

The Utkal Alumina project in Odisha became a showcase for Hindalco's project execution capabilities. In July 2007, Hindalco announced it is acquiring the stake of Alcan Inc. in the Utkal Alumina Project located in Doraguda, Odisha. This massive integrated project included bauxite mining, alumina refining, and captive power generation. Despite the complex environmental and social challenges typical of large projects in India, Hindalco successfully commissioned the project, adding significant alumina capacity.

Vertical integration remained a key strategic focus. By 2015, Hindalco had achieved complete self-sufficiency in bauxite and substantial self-sufficiency in alumina and power. This integration provided a crucial cost advantage—while standalone smelters were at the mercy of raw material price fluctuations, Hindalco could maintain stable margins across the value chain.

The company's approach to power generation was particularly innovative. Recognizing that energy costs were the single largest component of aluminum production costs, Hindalco invested heavily in captive power plants. But unlike competitors who relied solely on coal, Hindalco diversified its energy mix. The company invested in hydroelectric projects and began exploring renewable energy options, anticipating future carbon regulations.

Technology and innovation became increasingly important differentiators. The Hindalco Innovation Centre, established in the early 2000s, was expanded and given greater resources. The center focused not just on process improvements but on developing new alloys and applications. Custom alloys for automotive applications, special grades for aerospace, and innovative packaging solutions were developed in collaboration with customers.

The copper business, often overshadowed by aluminum, quietly became a star performer. Hindalco's copper facility in India comprises a world-class copper smelter, downstream facilities, a fertiliser plant and a captive jetty. The Birla Copper smelter was expanded to become one of the largest single-location custom smelters globally. The focus on copper cathodes and continuous cast copper rods—value-added products with better margins than raw copper—proved prescient as India's electrical infrastructure expanded rapidly.

Financial discipline was paramount during this period. Despite the large debt taken on for the Novelis acquisition, Hindalco maintained a strong balance sheet. Cash flows from Indian operations were carefully managed, debt was steadily paid down, and the company maintained investment-grade credit ratings. This financial strength would prove crucial in navigating subsequent market volatility.

The period also saw important organizational changes. Kumar Mangalam built a professional management team, bringing in talent from global companies and consulting firms. Traditional family-run management styles gave way to modern corporate governance practices. Performance management systems were implemented, executive compensation was linked to long-term value creation, and succession planning was institutionalized.

Environmental and social sustainability, long important to the Birla tradition of trusteeship, became embedded in operations. Hindalco invested in pollution control equipment, water recycling systems, and rehabilitation of mined areas. The company's corporate social responsibility programs, particularly in education and healthcare around its plants, created goodwill that proved invaluable in securing social license to operate.

By 2015, the transformation was complete. Hindalco had evolved from an Indian aluminum producer into a global metals major. The company generated revenues exceeding $15 billion, operated across 13 countries, and employed over 80,000 people. More importantly, it had successfully navigated the post-crisis commodity downturn that had crippled many competitors.

The Novelis gamble had paid off. The subsidiary was generating consistent profits, had strengthened its market position, and was investing in new capacity. The automotive market, in particular, was booming as fuel efficiency regulations drove aluminum adoption. The circular economy concept was gaining traction, and Novelis's recycling capabilities positioned it perfectly for this trend.

But the commodity cycle was turning again. Chinese overcapacity was flooding global markets with cheap aluminum. New environmental regulations were increasing costs. The electric vehicle revolution was beginning to reshape automotive markets. Hindalco would need to evolve again to maintain its leadership position.

VII. The Sustainability & Innovation Era (2015–Present)

The late 2010s marked another inflection point for Hindalco and the global aluminum industry. Climate change moved from corporate social responsibility reports to boardroom strategy sessions. The Paris Agreement in 2015 set the stage for carbon pricing and emissions regulations that would fundamentally reshape energy-intensive industries like aluminum.

For Hindalco, this shift represented both challenge and opportunity. The company's Indian smelters, largely powered by coal-based captive power plants, faced pressure to reduce emissions. But Novelis's focus on recycling suddenly became a massive competitive advantage. Recycled aluminum produces 95% fewer emissions than primary aluminum, making it the material of choice for sustainability-conscious customers.

The electric vehicle (EV) revolution became a game-changer for aluminum demand. EVs require 40-50% more aluminum than traditional vehicles due to the need for lightweight materials to offset heavy batteries. Novelis's automotive aluminum sheets, already used by premium manufacturers like BMW and Mercedes, were perfectly positioned for this trend. The company invested heavily in new capacity specifically designed for EV applications.

On 15 April 2020, Novelis acquired Aleris Corporation for $2.8 billion. Through this acquisition Novelis entered into the high-end aerospace segment. The acquisition of the US-based rolled products major, Aleris Corporation, positions Hindalco as one of the world's largest aluminium companies, with a global footprint spanning 49 state-of-the-art manufacturing facilities in North America, Europe and Asia.

The Aleris acquisition was strategic on multiple levels. It brought aerospace capabilities—the highest margin segment in aluminum rolling. It expanded Novelis's presence in Asia, particularly in China, the world's largest aluminum market. And it added specialized products like aluminum lithium alloys crucial for next-generation aircraft.

Mr. Kumar Mangalam Birla said: "The Aleris deal marks a major milestone for Hindalco and Novelis, on their path to global leadership. The closure of this deal amidst challenging market conditions, reflects our conviction in the Aleris business and its value to our metals portfolio. Periods of turmoil have historically seen the emergence of champions, powered by quality leadership and sound business fundamentals. This is a long-term strategic bet, much like Novelis was in 2007".

Back in India, Hindalco embraced the sustainability agenda with remarkable speed. Hindalco featured among the top 1% in the aluminium industry for the fourth consecutive year globally - 2020, 2021, 2022, and 2023, in S&P Global's Corporate Sustainability Assessment 2024 Yearbook. This year Hindalco scored 78 (out of 100) in the 2023 S&P Global Corporate Sustainability Assessment. Hindalco achieved industry-best scores in various dimensions including Resource Efficiency and Circularity, Climate Strategy, Biodiversity, Customer Relationship Management, Supply Chain Management, Social Impacts on Communities, and more, reaffirming its position as an industry leader.

The company set ambitious targets for carbon neutrality and began investing in renewable energy. Solar power projects were developed to supply clean energy to smelters. Energy efficiency improvements reduced power consumption per ton of aluminum. Water recycling systems were upgraded to achieve water neutrality at several plants.

Innovation accelerated across the value chain. The development of new alloys for specific applications—high-strength alloys for automotive, corrosion-resistant alloys for marine applications, specialized alloys for electronics—allowed Hindalco to command premium prices. The company's R&D centers collaborated with customers to develop customized solutions, moving beyond commodity supplier to technology partner.

Digital transformation became a priority. Artificial intelligence and machine learning were deployed to optimize smelting operations, predict equipment failures, and improve quality control. Digital twins of plants allowed for virtual testing of process improvements. Blockchain technology was piloted for supply chain transparency, particularly important for customers concerned about responsible sourcing.

The COVID-19 pandemic in 2020 created unprecedented challenges but also validated Hindalco's strategy. While primary aluminum demand collapsed temporarily, packaging demand surged as consumers shifted to packaged goods. The company's diversified portfolio—spanning packaging, automotive, construction, and electrical—provided resilience. Strong balance sheet management allowed Hindalco to continue investing while competitors retrenched.

Financial performance reflected the success of the transformation. Revenue: 2,38,496 Cr · Profit: 16,002 Cr for the consolidated entity, with Novelis contributing the majority of revenues. More importantly, the company had achieved its goal of becoming a global leader, not just in scale but in technology, sustainability, and customer relationships.

Current market dynamics favor Hindalco's integrated model. China's carbon neutrality commitments are forcing its aluminum industry to reduce capacity and increase costs. Developed markets are implementing carbon border adjustments that favor low-carbon aluminum. The infrastructure spending boom in India and other developing countries is driving demand for primary aluminum.

The company's recent strategic moves reflect confidence in the future. Major capacity expansions are underway in both India and through Novelis globally. Investments in downstream facilities continue, with new plants for automotive sheets and beverage can stock. The focus on recycling is intensifying, with Novelis targeting 100% recycled content for certain products.

On 6 February 2024, Hindalco announced it is acquiring 26% stake in Ayana Renewable Power Four (ARPFPL) for a value of Rs 1.62 crore. Hindalco will operate a captive power generation plant for supplying 100 MW Renewable energy to Hindalcos smelter in Odisha. This investment in renewable energy represents the future direction—aluminum production powered by clean energy, creating truly green aluminum.

Today's Hindalco is unrecognizable from the company founded in 1958. Hindalco's global footprint spans 50 manufacturing units across 10 countries. It's a global technology leader, a sustainability champion, and a critical supplier to some of the world's most demanding customers. The journey from Renukoot to global leadership is complete, but the next chapter—building a sustainable metals company for the 21st century—has just begun.

VIII. Playbook: Commodity Business Mastery

After six decades of navigating commodity cycles, technological disruptions, and global competition, Hindalco has developed a playbook for succeeding in capital-intensive, cyclical businesses. These lessons, learned through both triumphs and tribulations, offer valuable insights for any company operating in commodity or industrial markets.

The Birla Way: Patient Capital Meets Aggressive Expansion

The Birla approach to business combines seemingly contradictory elements—conservative financial management with bold strategic bets. The family's philosophy of maintaining strong balance sheets and low leverage during good times provides the firepower for aggressive expansion during downturns. The Novelis acquisition exemplified this—years of careful capital accumulation enabled a $6 billion bet that transformed the company.

This patient capital approach extends to returns. Unlike private equity or activist investors demanding immediate returns, the Birla family takes a generational view. Investments in technology, sustainability, or market position that might not pay off for years are evaluated based on long-term strategic value, not quarterly earnings impact.

Managing Cyclicality: Counter-Cyclical Investment Philosophy

Commodity businesses are inherently cyclical, with prices swinging wildly based on supply-demand imbalances. Most companies invest pro-cyclically—expanding when prices are high and cutting back during downturns. Hindalco does the opposite. Major capacity expansions and acquisitions are timed for cycle troughs when assets are cheap and competition is weak.

The company maintains financial flexibility specifically for these opportunities. During upturns, excess cash is used to pay down debt rather than pay special dividends. This creates the balance sheet strength to invest aggressively during downturns while competitors are struggling to survive.

The Downstream Hedge: Why Vertical Integration Changes Everything

The Novelis acquisition fundamentally changed Hindalco's business model. Primary aluminum is a pure commodity—price is set by the LME, and producers have no pricing power. But downstream products like automotive sheets or beverage can stock are differentiated products with customer relationships, technical specifications, and switching costs.

This downstream integration provides multiple benefits. It captures additional margin along the value chain. It provides stability through long-term contracts. It creates customer intimacy that pure commodity producers lack. And it provides a natural hedge—when primary aluminum prices fall, downstream margins often expand.

Cost Leadership Through Integration and Scale

In commodities, you don't control price—the market does. The only thing you control is cost. Hindalco's relentless focus on cost reduction through vertical integration has created one of the lowest-cost positions globally. Captive bauxite mines eliminate raw material price risk. Captive power generation controls energy costs. Integrated logistics reduce transportation expenses.

Scale amplifies these advantages. Larger plants have lower unit costs. Bigger companies get better terms from suppliers. Market leaders can invest more in technology and efficiency improvements. Hindalco's strategy has been to achieve leadership positions in chosen markets rather than sub-scale presence across many markets.

Technology Adoption in Traditional Industries

Aluminum smelting technology hasn't fundamentally changed since the Hall-Héroult process was developed in 1886. But incremental improvements in energy efficiency, process control, and automation can dramatically impact competitiveness. Hindalco has consistently been an early adopter of new technologies, from computer-controlled smelting to AI-powered optimization.

The company's innovation strategy focuses on three areas: process efficiency to reduce costs, product innovation to capture premium pricing, and sustainability technologies to meet environmental regulations. The Hindalco Innovation Centre and partnerships with technology providers ensure access to cutting-edge developments.

Managing Stakeholders in Complex Environments

Operating in India requires navigating complex stakeholder relationships—government officials, local communities, environmental activists, labor unions. Hindalco's approach combines proactive engagement, transparent communication, and genuine community development. The company's CSR programs aren't just compliance exercises but strategic investments in social license to operate.

Government relations are particularly crucial in a regulated industry like mining and metals. Hindalco maintains strong relationships across political parties and bureaucratic levels. The company's reputation for ethical business practices and contribution to economic development provides political capital during challenging times.

Capital Allocation in Capital-Intensive Businesses

Capital allocation is the most important driver of long-term returns in capital-intensive businesses. Hindalco's framework prioritizes investments based on strategic importance, return on capital, and risk. Maintenance capex is non-negotiable. Growth capex is evaluated against strict return hurdles. Acquisitions must provide strategic value beyond financial returns.

The company maintains a portfolio approach—some investments are for current returns, others for future options. Investments in sustainability or technology might not meet traditional ROI hurdles but are essential for long-term competitiveness. This balanced approach has allowed Hindalco to both deliver current returns and position for future growth.

Building Organizational Capabilities

Hindalco's transformation from a family-run Indian company to a global corporation required fundamental changes in organizational capabilities. Professional management was brought in for specialized roles. Global best practices were adopted in operations, finance, and governance. Performance management systems were implemented to drive accountability.

But the company also maintained elements of its family business heritage—long-term thinking, stakeholder orientation, and values-based leadership. This hybrid model combines the best of professional management with the stability and vision of family ownership.

The Power of Purpose

Throughout its history, Hindalco has maintained a sense of purpose beyond profit. From G.D. Birla's vision of industrial nation-building to today's focus on sustainable development, the company has positioned itself as contributing to societal progress. This purpose provides meaning to employees, credibility with stakeholders, and resilience during difficult times.

IX. Analysis & Investment Case

Competitive Positioning: The Moat Question

In the Indian aluminum market, Hindalco enjoys a dominant position with approximately 40% market share. The company's integrated operations from bauxite to finished products create significant barriers to entry. A new entrant would need to invest $5-10 billion to achieve comparable scale and integration—a daunting proposition given current return profiles.

Globally, through Novelis, Hindalco holds leading positions in attractive niches. The company is the largest producer of aluminum beverage can sheet globally, with 20%+ market share. In automotive aluminum, Novelis is a preferred supplier to premium manufacturers. These positions are defended by customer relationships, technical capabilities, and scale advantages.

The competition differs by segment. In primary aluminum, Chinese producers dominate with 57% of global production. But China is increasingly focused on domestic consumption and facing environmental constraints. In India, Vedanta is the primary competitor, while NALCO, the state-owned producer, lacks Hindalco's downstream capabilities and efficiency.

The China Factor: Threat and Opportunity

China's role in global aluminum markets cannot be overstated. The country's massive capacity additions in the 2000s and 2010s depressed global prices and drove consolidation among Western producers. Chinese exports of semi-fabricated products continue to pressure prices in commodity grades.

But China's carbon neutrality commitments by 2060 are changing the game. The country is curtailing capacity in high-emission smelters and imposing production restrictions. This is supporting global aluminum prices and creating opportunities for efficient producers like Hindalco. Moreover, China's growing domestic consumption is reducing export pressure.

For Hindalco, China represents both competition and opportunity. The company's cost position allows it to compete with Chinese exports in commodity products. Meanwhile, Novelis's focus on technical products and customer service provides differentiation that Chinese producers cannot easily replicate. And China's growing automotive and packaging markets offer expansion opportunities.

The EV Revolution and Aluminum Demand

The transition to electric vehicles is one of the most important demand drivers for aluminum. EVs use 40-50% more aluminum than conventional vehicles—250-300 kg per vehicle versus 150-180 kg. With global EV sales expected to reach 30-40% of total vehicle sales by 2030, this represents massive incremental demand.

Hindalco is well-positioned for this transition. Novelis already supplies aluminum to major EV manufacturers including Tesla, BMW, and Mercedes. The company's investment in new rolling capacity specifically for automotive applications ensures participation in this growth. Moreover, the focus on recycled aluminum aligns with EV manufacturers' sustainability goals.

Beyond direct aluminum content, EVs drive demand through infrastructure. Charging stations require aluminum conductors. Battery enclosures use aluminum for thermal management. The broader electrification trend—from renewable energy to grid upgrades—creates additional aluminum demand.

ESG Challenges and Carbon Border Taxes

Environmental regulations are reshaping the aluminum industry. The European Union's Carbon Border Adjustment Mechanism (CBAM), which imposes tariffs on high-carbon imports, advantages producers with low carbon footprints. Similar mechanisms are being considered in other developed markets.

Hindalco's sustainability investments position it well for this transition. The company's renewable energy investments, energy efficiency improvements, and Novelis's recycling capabilities create a lower carbon footprint than many competitors. The company's sustainability ratings and transparent reporting build credibility with ESG-focused investors and customers.

However, challenges remain. The Indian smelters' reliance on coal-based power is a weakness in carbon-conscious markets. Water usage in water-stressed regions raises sustainability concerns. Mining operations face ongoing environmental and social challenges. Addressing these issues requires continued investment and stakeholder engagement.

Valuation Framework: Complexities of Cyclical Businesses

Valuing Hindalco requires understanding both commodity cycles and business quality. On simple metrics, the stock often appears cheap—trading at 6-8x EV/EBITDA versus global peers at 8-10x. But this discount reflects several factors: emerging market discount, commodity cycle positioning, and complexity discount for the integrated structure.

The key is distinguishing between cyclical variations and structural improvements. Novelis's transformation from a struggling manufacturer to a profitable market leader represents structural improvement worth a rerating. The company's sustainability leadership and EV exposure deserve premium valuations. But commodity price volatility and China concerns create ongoing uncertainty.

A sum-of-the-parts valuation highlights hidden value. Novelis alone could be worth $12-15 billion based on peer multiples. The Indian aluminum business, with its low-cost position and growth potential, could be worth $8-10 billion. The copper business adds another $3-4 billion. Together, these suggest significant upside from current valuations.

Bear Case: Multiple Headwinds

The bear case for Hindalco rests on several concerns. Commodity prices could face prolonged weakness from Chinese oversupply or global recession. Energy costs, particularly in Europe where Novelis operates, could spike due to geopolitical tensions. Environmental regulations could impose unexpected costs or operational restrictions.

Technology disruption is another risk. Solid-state batteries could reduce aluminum content in EVs. Alternative packaging materials could challenge aluminum's dominance. New smelting technologies like inert anode could advantage competitors who adopt them first.

Financial risks persist despite balance sheet improvements. The company's net debt of $7-8 billion requires careful management. Rising interest rates increase financing costs. Currency fluctuations impact earnings translation and competitiveness. Any major acquisition could stretch the balance sheet.

Bull Case: Structural Growth Story

The bull case sees Hindalco as a structural winner in the green transition. Aluminum is essential for renewable energy, electric vehicles, and sustainable packaging. The company's integrated model, global presence, and sustainability leadership position it to capture this growth.

India's growth story adds another dimension. The country's infrastructure build-out, urbanization, and industrial growth will drive massive aluminum demand. Hindalco's dominant domestic position and expansion plans ensure participation in this growth. Government initiatives like "Make in India" favor domestic producers.

The Novelis transformation continues to create value. Growing automotive aluminum adoption, particularly in EVs, drives volume and margin expansion. The circular economy trend favors Novelis's recycling capabilities. Customer focus on supply chain sustainability advantages integrated producers.

Valuation upside appears significant. As the company demonstrates consistent earnings growth and ESG leadership, valuation multiples should expand toward global peers. The potential Novelis IPO could unlock value and provide growth capital. Strategic actions like special dividends or buybacks could accelerate value realization.

X. Strategic Lessons & Future Scenarios

Emerging Market Industrialization: The Hindalco Template

Hindalco's journey offers valuable lessons for emerging market companies aspiring to global leadership. The progression from import substitution to domestic champion to global player follows a clear pattern. First, build scale and capabilities in a protected home market. Second, consolidate domestic industry to achieve leadership. Third, expand internationally through acquisitions rather than organic growth.

The importance of timing cannot be overstated. Hindalco benefited from protective policies during its formative years, liberalization when it had achieved scale, and global consolidation when it had capital to deploy. Companies attempting similar transformations must understand their position in this cycle.

Patient capital is essential. The transformation from domestic to global player takes decades and requires weathering multiple cycles. Family ownership or similar long-term oriented shareholders provide stability that public market investors might not tolerate.

The M&A Playbook: When to Bet Big

The Novelis acquisition offers a masterclass in transformative M&A. The key insights: buy assets that provide capabilities you cannot build organically, time acquisitions for market distress when valuations are attractive, and ensure cultural fit is manageable even if not perfect.

Due diligence must go beyond financial metrics. Understanding industry dynamics, customer relationships, and technological capabilities is crucial. Hindalco recognized that Novelis's customer relationships and technical capabilities were more valuable than its current profitability suggested.

Post-merger integration requires balance. Imposing the acquirer's culture can destroy value, but inadequate integration fails to capture synergies. Hindalco's approach—maintaining operational independence while integrating strategic planning—preserved Novelis's strengths while improving performance.

Technology Transitions in Heavy Industry

The aluminum industry's technological evolution demonstrates how traditional industries can innovate. While breakthrough innovations are rare, continuous incremental improvements compound over time. Companies that consistently adopt new technologies gain cumulative advantages.

The key is balancing proven technologies with emerging innovations. Hindalco's approach—fast follower on proven technologies, selective pioneer on strategic innovations—manages risk while maintaining competitiveness. Partnerships with technology providers and universities provide access to innovations without bearing full development risk.

Digital transformation is increasingly important even in traditional industries. Data analytics, artificial intelligence, and automation can dramatically improve operational efficiency. But implementation requires changing organizational culture, not just installing technology.

The Next Decade: Strategic Imperatives

Looking forward, several strategic imperatives will shape Hindalco's future. Green aluminum—produced with renewable energy and recycled content—will command premium prices. The company must accelerate its renewable energy transition and expand recycling capabilities.

Geographic expansion remains important. While Hindalco has global presence through Novelis, the Asian market outside India remains underpenetrated. China's transition from exporter to importer creates opportunities. Southeast Asian growth offers expansion potential.

Product innovation must accelerate. As aluminum applications expand—from batteries to 3D printing—new alloys and products are required. Companies that co-develop solutions with customers will capture value. The shift from material supplier to solution provider continues.

Future Scenarios: Multiple Paths

Several scenarios could unfold over the next decade. In the green transition scenario, aggressive climate policies drive aluminum demand while penalizing high-carbon production. Hindalco's sustainability investments pay off handsomely, and the company emerges as a global green aluminum leader.

In the technology disruption scenario, breakthrough innovations like solid-state batteries or alternative materials challenge aluminum demand. Companies must adapt quickly or face obsolescence. Hindalco's diversified portfolio and innovation capabilities provide resilience.

In the geopolitical fragmentation scenario, trade wars and reshoring fragment global supply chains. Regional champions emerge as global integration reverses. Hindalco's presence across multiple regions positions it well for this world.

The most likely path combines elements of all scenarios. The green transition accelerates but unevenly across regions. Technology evolution continues but doesn't eliminate aluminum's advantages. Geopolitical tensions create volatility but don't destroy global trade. Success requires strategic flexibility and operational excellence.

XI. Recent News

The momentum at Hindalco continues to build with strong operational and financial performance across all business segments. Hindalco Industries Limited reported a consolidated quarterly Net Profit of Rs.3,174 crore, an increase of 32% YoY, driven by a robust performance and improved margins across all business segments. Novelis reported a strong fourth quarter performance with EBITDA per tonne at $540, up 25% YoY. Copper Business delivered a new record-breaking performance in Q4, with EBITDA at an all-time high of Rs.776 crore, up 30% YoY, backed by record sales. Aluminium Upstream EBITDA margins at 32% were the best in the industry, globally. Hindalco maintained a strong balance sheet and liquidity position which helped the company keep the Net Debt to EBITDA ratio below 2x.

The company's sustainability leadership continues to gain recognition. Hindalco's recognition as the World's Most Sustainable Aluminium Company for the fourth year in a row in the S&P Global Corporate Sustainability Assessment rankings 2023 validates its ESG strategy and positions it well for increasingly sustainability-conscious markets.

Strategic expansion continues with focus on downstream and renewable energy. The recent acquisition of stakes in renewable power projects signals the company's commitment to green aluminum production. New capacity additions in automotive sheets and beverage can stock through Novelis position the company for continued growth in high-value segments.

The financial performance reflects successful execution. Aluminium and copper producer Hindalco Industries reported a 31.6 per cent year-on-year rise in consolidated net profit at Rs 3,174 crore for the March quarter in the financial year 2023-24, driven by robust sales and low input costs across business segments. Consolidated revenue from operations grew marginally by 0.25 per cent to Rs 55,994 crore. The company announced earnings before interest, taxes, depreciation, and amortisation (Ebitda) of Rs 7,201 crore, marking a 24 per cent Y-o-Y increase.

Looking ahead, management guidance remains optimistic despite global uncertainties. Continued focus on operational excellence, strategic growth investments, and sustainability initiatives position Hindalco well for long-term value creation. The potential Novelis IPO, while delayed, remains a strategic option to unlock value and fund further growth.

XII. Links & Resources

For those seeking to dive deeper into the Hindalco story and the aluminum industry, the following resources provide valuable insights:

Company Resources: - Hindalco Annual Reports and Investor Presentations - Novelis Sustainability Reports and Financial Filings - Aditya Birla Group Corporate Website and Archives

Industry Analysis: - International Aluminium Institute Reports - CRU Aluminum Market Analysis - Wood Mackenzie Aluminum Industry Reports - S&P Global Platts Aluminum Coverage

Historical Context: - "Business Maharajas" by Gita Piramal (Birla family history) - "India After Gandhi" by Ramachandra Guha (economic policy context) - "The House of Tatas" by Carnegie Endowment (comparative business history)

Technical Resources: - "Aluminum: Properties and Physical Metallurgy" (ASM International) - LME Aluminum Contract Specifications and Historical Data - World Bank Commodity Price Database

Sustainability and ESG: - Aluminium Stewardship Initiative Standards - CDP Climate Change Reports - Science Based Targets Initiative (SBTi) Guidelines

M&A and Strategy: - Harvard Business School Case: "Hindalco's Acquisition of Novelis" - McKinsey Global Institute: "India's Path to 2030" - BCG: "Winning in Metals and Mining"

Academic Research: - "The Evolution of Indian Business Groups" (Journal of Economic Perspectives) - "Commodity Price Cycles and Financial Investment" (IMF Working Papers) - "Vertical Integration in Natural Resource Industries" (NBER)

News and Analysis: - The Economic Times Industry Coverage - Metal Bulletin Daily - Bloomberg Commodities - Reuters Metals Coverage

This comprehensive exploration of Hindalco's journey from a post-independence startup to a global aluminum giant reveals timeless lessons about building enduring businesses in challenging industries. The story continues to unfold, with new chapters being written in sustainability, innovation, and global expansion. For students of business strategy, Hindalco offers a masterclass in navigating complexity, managing cycles, and creating long-term value in capital-intensive industries.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube