Pokarna Limited: From Fabric Trader to Global Quartz Surface Leader

I. Introduction & Episode Roadmap

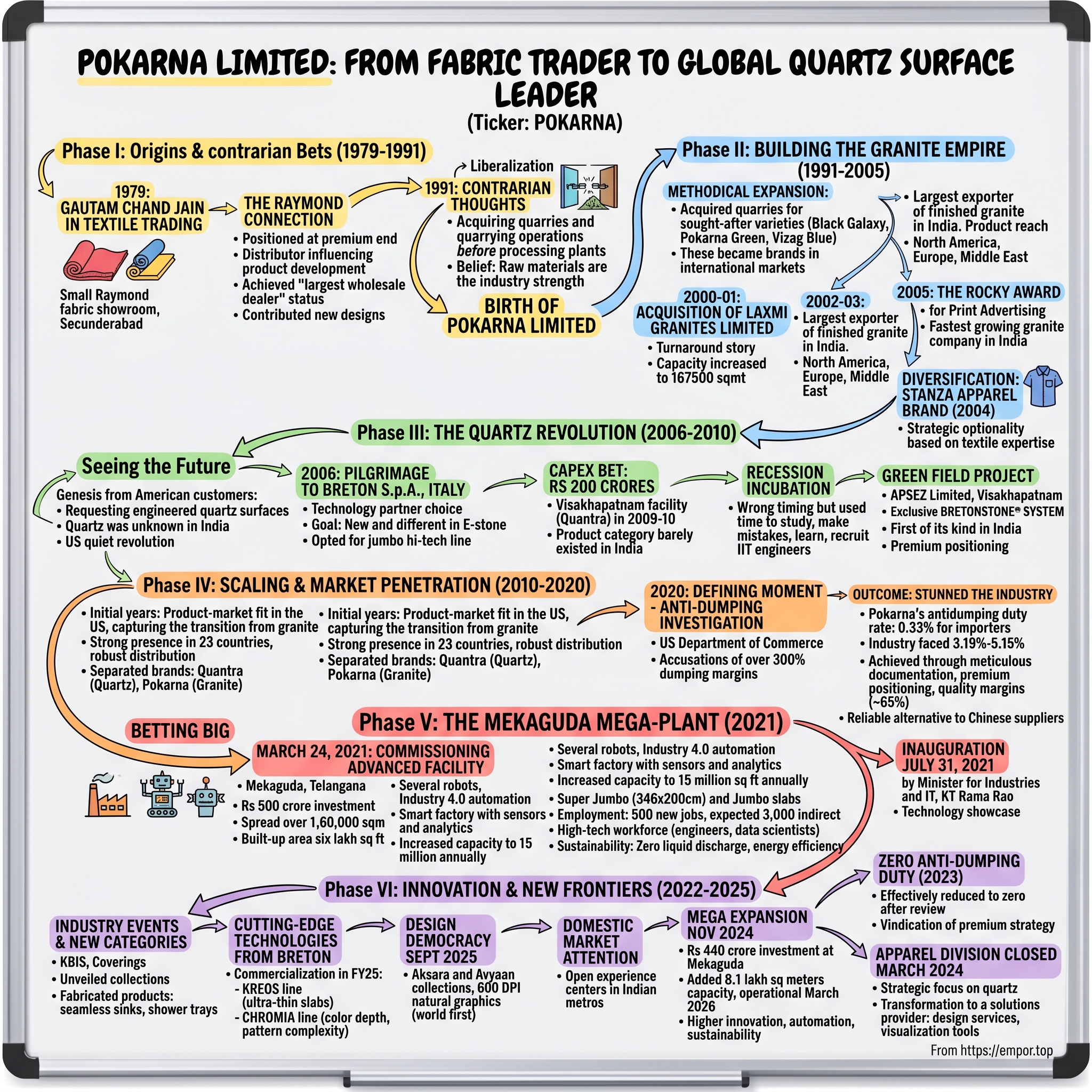

Picture this: A man stands in his Raymond fabric showroom in Secunderabad in 1979, surrounded by bolts of premium suiting material. Fast forward four decades, and that same entrepreneur helms India's largest exporter of premium quartz surfaces, with a market capitalization touching Rs 2,442 crores. This is the unlikely journey of Gautam Chand Jain and Pokarna Limited—a story that weaves through textile trading floors, granite quarries, and ultimately to the gleaming quartz countertops of American kitchens.

The hook here isn't just the transformation—it's the contrarian thinking that drove it. While India's economic liberalization in 1991 saw entrepreneurs rushing to set up processing plants and manufacturing facilities, Jain kick started granite business in an unconventional way by acquiring quarries and commencing with quarrying operations, which was a paradigm shift from the traditional thinking of starting with processing plants. His fundamental belief? Raw materials was the strength of the industry.

Today's episode traces an extraordinary pivot from being Raymond's top distributor in India to building a vertically integrated stone empire that competes with Italian giants and navigates complex US anti-dumping investigations. We'll explore how a fabric trader spotted the future of engineered stone before most Indians had heard of it, why he bet Rs 200 crores on Italian technology when quartz was virtually unknown in India, and how Pokarna achieved what seemed impossible—an antidumping duty rate of 0.33% for importers when others faced significantly higher penalties.

This is more than a business story. It's about seeing opportunities where others see commodities, about building technology moats in traditional industries, and about the patience required to make 15-year bets on new categories. From the textile lanes of Secunderabad to the design studios of Manhattan, this is the Pokarna story.

II. The Gautam Chand Jain Story & Origins (1979-1991)

The year was 1979. India was a different country—the Emergency had just ended, color television was arriving, and economic liberalization was still a distant dream. In Secunderabad's bustling commercial district, a young Gautam Chand Jain, born on 15th August, 1955, took his first steps into the family textile business.

Founded by Shri Gautam Chand Jain in 1981, the company started with a small shop in M.G. Road, Secunderabad. But this wasn't going to remain a small operation for long. Jain brought something different to the traditional fabric distribution business—an eye for quality that bordered on obsession and a knack for understanding what customers wanted before they knew it themselves.

The Raymond connection was crucial. In an era when most fabric dealers were content with local brands and lower margins, Jain positioned himself at the premium end. His achievement of racing ahead of several established firms is more due to his individual skill in identification of good material both in terms of designs and fabric quality to suit the changing tastes and fashions from time to time and adoption of a combination of marketing strategies. This wasn't just distribution—it was curation.

The results were swift and dramatic. Within a very short span of time, he earned the distinction of being Raymond's top distributor in India. But what made this achievement remarkable wasn't just the volume—it was the innovation. He is also credited with bringing out new designs, which were adopted by Raymond Limited. Think about that for a moment: a distributor influencing the product development of one of India's most prestigious textile companies.

By the late 1980s, Pokarna Fabrics had become more than just a distribution business. They have maintained the title of 'the largest wholesale dealer's for Raymond's for the last two decades, managing relationships with over 500 partners. The company had built what would today be called a platform business—connecting Raymond's manufacturing prowess with a vast network of retailers across India.

But as 1991 approached, Jain was already looking beyond fabrics. India was changing. The economy was opening up. New opportunities were emerging. And in the ancient granite quarries of South India, Jain saw something others had missed. While his textile business was thriving—it would eventually grow to Rs. 4000 Crore+ conglomerate status—he was preparing for a completely different adventure.

The question wasn't why leave a successful business. It was why not explore what else was possible? Extending his skills in colors and designs from fabrics to natural stone, Jain was about to make a leap that would define the next three decades of his entrepreneurial journey. The year 1991 wouldn't just mark India's economic liberalization—it would mark the birth of Pokarna Limited and a contrarian bet on granite that would reshape an industry.

III. Building the Granite Empire (1991-2005)

Pokarna Limited was founded in the year 1991 under the vision of Mr. Gautam Chand Jain, Chairman and Managing Director, at a time when India was undergoing seismic economic shifts. The timing was no coincidence—liberalization had opened doors, but Jain's approach to entering the granite business was remarkably unconventional.

While established players rushed to set up processing plants with imported machinery, believing that manufacturing capability was the key differentiator, Jain looked at the value chain differently. His years in textiles had taught him that controlling quality at the source mattered more than anything else. He began by acquiring granite quarries before setting up processing facilities. This backward integration approach ensured control over raw material supply and was a paradigm shift from the traditional "processing-first" model.

The early years were about methodical expansion. Jain didn't just buy any quarries—he went after the ones with the most sought-after varieties. Black Galaxy, Coffee Brown, Flash Blue, Pokarna Green, Sapphire Blue, Seaweed Green, Silver Pearl and Vizag Blue became the crown jewels of Pokarna's portfolio. These weren't just stones; they were brands in themselves, commanding premium prices in international markets.

The year 2000 marked a significant acceleration. During 2000-01, the company purchased the assets of Laxmi Granites Limited from Financial Institutions (IDBI, IIBI & SBT) at a price of Rs.752.58 lakhs. With this acquisition the capacity is increased by 80000 Sqmt slabs, and the total capacity stands at 167500 sqmt. This wasn't just an asset purchase—it was a turnaround story. In an industry where many units were struggling, Jain saw opportunity where others saw distress.

By 2002-03, The installed capacity was enhanced to 300000 Sq Mtrs. Pokarna was no longer a startup—it was becoming a force in the global granite trade. The company was the largest exporter of finished granite in India (and one of the largest in Asia), with its products finding markets across North America, Europe, and the Middle East.

The recognition came quickly. In 2005, Pokarna received The Rocky Award for Print Advertising from the Marble Institute of America—a significant achievement for an Indian company in a field dominated by Italian and Brazilian competitors. The same year, it was recognized as the Fastest growing and Largest Granite & Stone company in India by Construction World Magazine.

But even as the granite business flourished, Jain was diversifying. In 2003-04, in what seemed like a return to his roots, Pokarna Limited successfully diversified into apparel manufacturing during 2003 – 04. The company launched Stanza, a premium men's shirts and trousers brand, leveraging Jain's deep understanding of the textile industry. Stanza was launched in the year 2004, with a vision to become a premium lifestyle brand for men.

This wasn't a distraction—it was strategic optionality. While granite gave Pokarna its industrial backbone, Stanza connected it back to Jain's expertise in understanding premium consumer preferences. The brand established itself with around 100 leading retail outlets across India, with a product range covering classic formal shirts (Linea Classica), sport wear (Linea Sport) and fashion wear (Linea Moda).

By 2005, Pokarna had transformed from a single quarry operation to a diversified conglomerate with interests spanning natural stones and premium apparel. The company had built two state-of-the-art processing facilities, established its quarries as sources of some of the world's most sought-after granite varieties, and even ventured back into textiles with a premium positioning.

But the most important development of this period wasn't visible in the numbers or awards. In 2006, as the granite business matured and Stanza found its market, Jain was already contemplating his next move. He had noticed something interesting: The first requests of quartz slabs came from the American market. In the beginning, I didn't know anything about quartz slabs but after a little research I realized that quartz business could be a valid option to differentiate my activity.

The granite empire was built. The apparel venture was launched. But the real revolution was just beginning.

IV. The Quartz Revolution: Seeing the Future (2006-2010)

The story goes that successful entrepreneurs see the future before others. But in 2006, when Gautam Chand Jain conceived the idea of entering into the business of engineered stone, even he couldn't have predicted how prescient this move would prove to be.

The genesis came from an unexpected source—his American granite customers. They kept asking for something Pokarna didn't make: engineered quartz surfaces. In India, quartz was virtually unknown. Granite was king, marble had its devotees, but engineered stone? That was science fiction to most Indian manufacturers. Yet in the US, a quiet revolution was underway as homeowners increasingly chose quartz over natural stone for its consistency, durability, and lower maintenance.

Jain's research journey led him to Italy, to a company called Breton S.p.A. Once I understood that Breton was the company behind this new technology, I scheduled a meeting at Breton's headquarters in Italy to learn more about this technology; it was 2006. This wasn't just a vendor visit—it was a pilgrimage to the source of the technology that would define Pokarna's next chapter.

The decision to partner with Breton was crucial. He believed that just with Breton machineries and technologies, he could get into a new industry and become soon a recognized brand. But choosing the right technology was just the beginning. The choice of the first Bretonstone® line was complex... The only thing that I knew at that time was that I wanted to be new and different in the E-stone business. I opted for the most innovative plant Breton could offer: a jumbo hi-tech line.

The numbers were staggering. Pokarna Ltd has developed a state-of-the-art facility at a CAPEX of 200 Cr for producing its own line of quartz surfaces- named Quantra- in Visakhapatnam, India, in 2009-10. This was a Rs 200 crore bet on a product category that barely existed in India.

The timing, as it turned out, was both terrible and perfect. When we switched on the machines, unfortunately, the recession came, and the US market stopped. It was a wrong timing but, at the same time, we could learn a lot. We had time to study the quartz markets - understanding its dynamics and volumes, we had time to make our mistakes and learning from them, before entering the market.

This period of forced incubation proved invaluable. Additionally, I started recruiting people from the Indian Institute of Technology to be surrounded by the best engineers. Pokarna wasn't just building a factory; it was building capability.

The facility that emerged was unlike anything in India. Pokarna Limited has set up a green field project for manufacturing of Engineered stone, the first of its kind in India, at APSEZ Limited in Achutapuram near Vishakapatnam, Andhra Pradesh. The plant deployed BRESTONE® SYSTEM exclusively sourced from Breton s.p.a, Italy, making Pokarna the exclusive licensee of this technology in India.

What made Quantra different wasn't just the technology—it was the positioning. While others might have seen engineered stone as a cheaper alternative to granite, Jain positioned it as a premium product. The brand name itself—Quantra—suggested quantum leaps, transformation, and cutting-edge technology. It is part of Pokarna Limited, a large group of companies founded in 1991 by Mr. Gautam Chand Jain, who is the current Chairman and Managing Director.

By 2010, as the global economy recovered from the financial crisis, Pokarna was ready. Quantra has been the first one worldwide in installing the jumbo press in the Bretonstone® plant. The company had spent the recession years perfecting its processes, training its workforce, and understanding the nuances of a completely new product category.

The quartz revolution wasn't just about adding a new product line. It was about recognizing a fundamental shift in consumer preferences—from natural variability to engineered consistency, from high maintenance to easy care, from traditional to contemporary. And Pokarna, having spent nearly two decades understanding stone, was uniquely positioned to bridge that gap.

As the new decade dawned, the foundations were laid. The technology was in place. The team was trained. The market was recovering. The real test was about to begin: Could an Indian company compete in a global market dominated by established players? Could Quantra become more than just another quartz brand?

V. Scaling & Market Penetration (2010-2020)

The 2010s began with Pokarna at an inflection point. The quartz facility was operational, but success was far from guaranteed. The engineered stone market was dominated by established players like Caesarstone from Israel and Silestone from Spain. Breaking into this oligopoly would require more than just good products—it would need strategic positioning, operational excellence, and perhaps most importantly, navigating complex trade dynamics.

The initial years were about finding product-market fit. His exploration into quartz slabs was driven by the growing demand in the U.S. market, leading to the establishment of Quantra in 2009. By focusing on the US market from day one, Pokarna avoided the mistake of trying to educate the nascent Indian market about quartz surfaces. The US was already transitioning from granite to quartz—Pokarna just needed to capture that wave.

They have strong presence in 23 countries and a robust distribution network which enables them to maintain uninterrupted and steady supply of products. This wasn't achieved overnight. Each market entry was carefully orchestrated, often starting with private label manufacturing for established brands before introducing the Quantra brand.

The brand architecture was deliberate and clear: Their Quartz surfaces are marketed under the brand name Quantra, while their granite products are sold under the Pokarna brand. This separation allowed each brand to develop its own identity without cannibalization.

But the decade's defining moment came in 2020, during the COVID pandemic, of all times. The US Department of Commerce had initiated anti-dumping investigations against quartz surface imports from India and Turkey. For many Indian exporters, this could have been catastrophic. The initial accusations suggested dumping margins exceeding 300%.

The investigation's outcome stunned the industry. Commerce calculated a dumping margin of 2.67% for Pokarna's products, which corresponds to an antidumping duty rate of 0.33% for importers. To put this in perspective, Pokarna was one of two mandatory respondents in this investigation, and others faced anti-dumping rate designation of between 3.19% and 5.15%.

How did Pokarna achieve this near-zero duty rate? The answer lay in years of meticulous documentation, transparent pricing, and most importantly, the premium positioning that justified higher prices. Caesarstone's gross margins have been trending down in the 26-27% range compared to ~65% for Pokarna. These weren't dumping margins—they were quality margins.

The financial performance during this period validated the strategy. Quartz Surfaces (97% in 9M FY25 vs 89% in FY22). The transformation was complete—what started as a diversification experiment had become the company's core business.

Technology continued to be a differentiator. Pokarna Ltd uses imported Italian machines from Breton Systems vs. the Chinese machines used by many other players. This wasn't just about having better equipment—it was about signaling to customers and regulators alike that Pokarna was committed to quality over cost-cutting.

The product portfolio expanded dramatically during this period. The company's WOS Pokarna Engineered Stone Ltd (PESL) is India's largest exporter of premium quartz surfaces, offering 100+ quartz designs including collections with names that evoked luxury and aspiration: Moon Walk, Champs-Elysees, Pirouette, La Dolce Vita, Pantheon.

By 2020, as the pandemic reshaped global supply chains, Pokarna had established itself as a reliable alternative to Chinese suppliers. The anti-dumping victory wasn't just a legal win—it was validation of a strategy that prioritized sustainable pricing and quality over volume at any cost. The company had successfully navigated the treacherous waters of international trade while building a brand that could command premium prices.

The decade ended with Pokarna at an interesting juncture. The quartz business was thriving, but capacity constraints were becoming apparent. The US market was recovering strongly from the pandemic, driven by a home renovation boom. The question was no longer whether Pokarna could compete globally—it was how fast it could scale to meet demand.

VI. The Mekaguda Mega-Plant: Betting Big (2021)

March 24, 2021. As the world grappled with successive COVID waves, Pokarna quietly commissioned what would become one of the most advanced quartz manufacturing facilities in the world. The Mekaguda plant wasn't just an expansion—it was a statement of intent.

Pokarna Engineered Stone Limited, a subsidiary of Pokarna Ltd, established a state-of-the-art quartz surfaces manufacturing facility, one of the largest in the world, with an investment of Rs 500 crore in Telangana. The scale was breathtaking: spread over 1,60,000 square meters and has a built-up area of six lakh square feet.

The timing seemed counterintuitive. The pandemic had disrupted global supply chains. International travel was restricted. Yet Jain saw opportunity where others saw crisis. The US housing market, fueled by low interest rates and remote work trends, was experiencing an unprecedented boom. Pokarna needed capacity, and it needed it fast.

What set Mekaguda apart wasn't just its size. Equipped with several robots and other high levels of process automation for supporting wide range of Industry 4.0 applications, this plant increases our installed capacity to 15 million square feet annually. This was a smart factory in the truest sense—sensors tracking every parameter, robots handling heavy slabs, and advanced analytics optimizing production in real-time.

The technological capabilities were particularly impressive. The facility will be used mainly for the production of Super Jumbo size 346X200 cm and Jumbo size 330x165 cm slabs. These weren't just bigger slabs—they were game-changers for commercial projects where fewer seams meant better aesthetics and easier installation.

July 31, 2021, marked the official inauguration. Minister for Industries and Information Technology KT Rama Rao is scheduled to inaugurate the new plant. The presence of Telangana's IT minister wasn't coincidental—this was as much a technology showcase as a manufacturing facility.

The employment impact was significant: This plant has created 500 new jobs and is expected to generate about 3,000 indirect jobs through spin-off employment. But these weren't traditional factory jobs. Pokarna was hiring engineers from IITs, data scientists, and automation specialists. The workforce looked more like a tech company than a traditional manufacturer.

Sustainability was built into the facility's DNA. Zero liquid discharge systems, energy-efficient processes, and waste recycling weren't afterthoughts—they were design principles. In an industry often criticized for environmental impact, Pokarna was positioning itself as a responsible manufacturer.

When the installed capacity is fully reached at the new plant, the company expects turnover of about Rs 400 crore from this plant. The financial projections were conservative, but the strategic implications were transformative. With Mekaguda operational, Pokarna could serve its existing customers better while pursuing new market segments.

The plant's automation capabilities proved particularly valuable. With 4 multi-axis anthropomorphic robots, the new plant would be able to reproduce exotic natural stones with very high level of design detailing including veins of different size & structure across the slab. This wasn't just manufacturing—it was artistry at industrial scale.

The Mekaguda investment represented something deeper than capacity expansion. It was a bet that the shift from natural stone to engineered surfaces was not a trend but a fundamental change in consumer preferences. It was a bet that Indian manufacturing could compete not just on cost but on technology and quality. Most importantly, it was a bet that the post-pandemic world would value supply chain resilience and sustainable manufacturing.

As 2021 drew to a close, the new facility was ramping up faster than expected. Orders were flowing in from the US, where the housing market continued its tear. The anti-dumping victory from the previous year meant Pokarna could compete on a level playing field. The pieces were falling into place for the next phase of growth.

VII. Innovation & New Frontiers (2022-2025)

The post-pandemic era brought new challenges and opportunities. Consumer preferences were evolving rapidly, sustainability had become non-negotiable, and technology was reshaping what was possible in engineered stone manufacturing. Pokarna's response was to double down on innovation.

2022 saw Pokarna making waves at industry events. The company unveiled new collections at KBIS (Kitchen & Bath Industry Show) and Coverings, North America's largest tile and stone exhibitions. But these weren't just new patterns—they were new product categories. Seamless sinks and shower trays represented Pokarna's entry into fabricated products, moving up the value chain from raw slabs to finished applications.

The real technological leap came with the commercialization of two cutting-edge technologies from Breton. During FY25, PESL will commercialize two cutting-edge technologies from BRETON S.p.A of Italy: the KREOS and CHROMIA lines. KREOS enabled the production of ultra-thin slabs, opening up new applications in furniture and wall cladding. CHROMIA brought unprecedented color depth and pattern complexity, allowing Pokarna to compete in the ultra-premium segment.

September 2025 marked another milestone. Pokarna unveiled Aksara and Avyaan collections at Design Democracy, described as having 600 DPI natural graphics—a world first. This wasn't just about resolution; it was about creating surfaces that were indistinguishable from natural stone while maintaining all the benefits of engineered quartz.

The domestic market, long neglected in favor of exports, finally got attention. Pokarna began opening experience centers in Indian metros, recognizing that the Indian consumer was finally ready for engineered stone. The timing was perfect—rising disposable incomes, increased awareness through social media, and a construction boom in luxury housing created the perfect storm of demand.

But the biggest announcement came in November 2024. Pokarna Engineered Stone Limited (PESL), a leading player in premium engineered stones, announced its mega plans to invest Rs 440 crore on expanding its state-of-the-art manufacturing facility at Mekaguda in Telangana. This wasn't just another production line—This new Bretonstone line represents more than just expanded capacity - it's a leap forward, bringing in world class technology to elevate our standards of innovation, automation, and sustainability.

The new production line, which will be operational by March 2026, will help the company meet the surging demand for its innovative products. It will add 8.1 lakh square meters of production capacity. The timing was strategic—the facility would come online just as the US market was expected to recover from the rate-hike-induced slowdown.

The international recognition continued to pour in. In 2023, another breakthrough: Pokarna Engineered Stone Limited (PESL) did not make sales of subject merchandise at less than normal value during the period of review (POR) June 1, 2021, through May 31, 2022. The anti-dumping duty was effectively reduced to zero—a vindication of Pokarna's premium pricing strategy.

The apparel division, which had been a drag on profitability, was finally closed in March 2024. This wasn't a failure—it was strategic focus. Every resource was now directed toward the quartz business, where Pokarna had clear competitive advantages.

Innovation wasn't limited to products. Pokarna was pioneering new business models, offering design services to architects, providing technical support to fabricators, and even developing software tools for visualization. The company was transforming from a manufacturer to a solutions provider.

The sustainability narrative strengthened further. Pokarna began incorporating recycled glass and other materials into its products, reduced energy consumption through process optimization, and achieved certifications that opened doors to green building projects.

As 2025 progresses, Pokarna stands at another inflection point. The third Bretonstone line represents not just capacity addition but capability enhancement. With advanced automation and AI-driven quality control, the new line will produce surfaces that push the boundaries of what's possible in engineered stone.

VIII. The Numbers & Business Model

Let's get into the financials—because ultimately, strategy without execution is just hallucination, and execution shows up in the numbers.

Market cap Rs 2,442 Crore, Revenue Rs 909 Cr, Profit Rs 183 Cr—these headline numbers tell part of the story, but the real insights lie deeper. The transformation of Pokarna's business mix is striking: Quartz surfaces now 97% of revenue (vs 89% in FY22). This isn't diversification—it's focused execution on the highest-value opportunity.

The ownership structure provides stability in an otherwise volatile industry. CEO Gautam Chand Jain holds 53% stake, with promoter holding at 56.7%. This concentrated ownership enables long-term thinking—crucial when you're making Rs 440 crore bets on new production lines that won't be operational for two years.

But the number that really matters? Gross margins. Gross margins ~65% vs competitors like Caesarstone at 26-27%. This isn't just a pricing premium—it's a fundamental difference in business model. Where others compete on volume, Pokarna competes on value.

The unit economics tell a compelling story. Start with raw materials: Approximately 62% of the total quartz was from several suppliers in Turkey, with the major part acquired from Mikroman and Polat. This concentration might seem like risk, but it's actually strategic—Turkey produces some of the highest-quality quartz globally, and long-term relationships ensure supply stability.

The revenue concentration is equally focused: The US is the largest market for its countertop products, contributing around 83% to Pokarna Ltd's revenue as of FY24. Again, this isn't diversification failure—it's market selection success. The US represents the world's largest and most profitable market for engineered surfaces.

Capital allocation has been disciplined yet aggressive. The Visakhapatnam facility required Rs 200 crores in 2009. The Mekaguda plant consumed Rs 500 crores in 2021. The latest expansion announced in November 2024 needs Rs 440 crores. Total: Rs 1,140 crores invested in quartz manufacturing over 15 years. The return on this investment? A business generating Rs 900 crores in revenue with 20% net margins.

The recent financial performance validates the strategy. For the half year, total revenue was INR 450.8 crores, a growth of 22.47% compared to H1 FY '24. The company also achieved an EBITDA of INR 154.1 crores, showing a growth of 26.55%. Notably, profit after tax (PAT) soared to INR 78.05 crores, reflecting a remarkable growth of 54.18%. Earnings per share (EPS) also increased significantly, reaching INR 25.17, up 54.18%.

The Q2 FY25 numbers were equally impressive: Pokarna Limited posted a net profit of Rs 44.96 crore for the second quarter ending on September 30, 2024, an increase of 37.49 per cent compared to the same period a year ago. The company's total revenues zoomed 24.33 per cent to Rs 253.46 crore during the quarter under review. Its EBITDA stood at Rs 88.29 crore, a growth of 20.67 per cent compared to Q2FY24.

Working capital management has been a hidden strength. Despite rapid growth, the company has maintained efficient inventory turns and receivables collection. The cash conversion cycle has actually improved even as the business scaled—a rare achievement in manufacturing.

The technology investments aren't just capital expenditure—they're moats. Pokarna Ltd uses imported Italian machines from Breton Systems vs. the Chinese machines used by many other players. This creates barriers to entry that go beyond capital. It's about know-how, relationships, and years of learning curve.

Debt levels have been managed conservatively despite aggressive expansion. The company has funded growth through a mix of internal accruals and selective borrowing, maintaining debt-to-equity ratios that provide flexibility for future investments.

The forward-looking metrics are perhaps most exciting. New capex expects revenue potential from the new capacity of ₹450-525 Cr with an asset turn of 1x to 1.25x. Pokarna Ltd anticipates an EBITDA of ₹145-165 Cr and a PAT of ₹100-110 Cr from this new line. These aren't aggressive projections—based on current utilization rates and pricing, they might even be conservative.

IX. Playbook: Key Strategic Lessons

After decades of transformation, what are the strategic lessons from Pokarna's journey? Not the MBA-textbook platitudes, but the real, hard-won insights that separate successful industrial transformations from the also-rans.

Lesson 1: Vertical Integration as Competitive Advantage

Taking forward his belief that raw materials was the strength of the industry, he kick started granite business in an unconventional way by acquiring quarries and commencing with quarrying operations. This wasn't just about cost control—it was about quality assurance and supply security. When you control the source, you control the story. Today, while competitors scramble for raw materials, Pokarna's quarries and long-term supplier relationships provide stability.

Lesson 2: Technology Partnerships Over Technology Purchase

The Breton relationship exemplifies this. He believed that just with Breton machineries and technologies, he could get into a new industry and become soon a recognized brand. This wasn't a one-time equipment purchase—it was an ongoing technology partnership. The exclusive license for Bretonstone technology in India created a moat that money alone couldn't buy.

Lesson 3: Market Timing Through Customer Pull

Pokarna didn't enter quartz because of a consultant's report or market study. The first requests of quartz slabs came from the American market. They listened to customers and moved when the demand signal was clear. This customer-pull strategy ensured product-market fit from day one.

Lesson 4: Premium Positioning in Commodity Markets

While others raced to the bottom on price, Pokarna went premium. Many exporters of Quartz Surfaces cater to the low end of the market with low realizations, whereas Pokarna Ltd commands higher realizations and gross margins. In commoditized industries, the only sustainable strategy is to de-commoditize through quality, service, or innovation.

Lesson 5: Navigate Regulation Through Transparency

The anti-dumping investigation could have been catastrophic. Instead, The agency also applied all of the subsidy rate against the company's anti-dumping penalty, lowering it to an effective 0.33%. This wasn't luck—it was years of maintaining transparent pricing, proper documentation, and arms-length transactions.

Lesson 6: Use Downturns to Build Capability

It was a wrong timing but, at the same time, we could learn a lot. We had time to study the quartz markets - understanding its dynamics and volumes, we had time to make our mistakes and learning from them, before entering the market. The 2008 recession, rather than killing the quartz venture, gave Pokarna time to build capabilities without competitive pressure.

Lesson 7: Family Business with Professional Excellence

Despite 53% promoter ownership, Pokarna runs with professional discipline. The recruitment of IIT engineers, partnerships with global technology leaders, and focus on automation show that family ownership doesn't mean nepotism or insularity.

Lesson 8: Exit Businesses Decisively

The closure of the apparel division in 2024 wasn't portrayed as failure but as focus. When a business doesn't fit the core strategy, holding on for emotional reasons destroys value. Pokarna's willingness to exit Stanza—despite it being Jain's return to his textile roots—showed strategic maturity.

Lesson 9: Build for Scale Before You Need It

When PESL launched Unit 2 in March 2021 at Mekaguda, the facility was designed with scalability in mind. This forward-thinking approach enables PESL to integrate the new production line seamlessly. The infrastructure investments anticipated growth, making expansion cheaper and faster.

Lesson 10: Long-Term Thinking in Short-Term Markets

Making Rs 440 crore investments with 2-year deployment timelines requires conviction that transcends quarterly earnings calls. Pokarna's 15-year journey in quartz—from conception in 2006 to market leadership in 2021—exemplifies patience in an impatient world.

These aren't just lessons—they're a playbook for industrial transformation. From a fabric trader to a global quartz leader, Pokarna's journey shows that with the right strategy, even traditional industries can be transformed through technology, quality, and relentless execution.

X. Bear vs. Bull Case & Future

Bull Case: The Optimist's View

The bullish thesis on Pokarna starts with the macro and works down to the micro. The US housing market, despite recent interest rate pressures, has a fundamental supply-demand imbalance. There are simply not enough homes for the millennial generation entering prime homeownership years. Every new home and every renovation is a potential quartz surface customer.

The technology leadership position strengthens by the day. During FY25, PESL will commercialize two cutting-edge technologies from BRETON S.p.A of Italy: the KREOS and CHROMIA lines. These aren't incremental improvements—they're step-changes that open new market segments. Ultra-thin slabs from KREOS enable furniture applications. CHROMIA's advanced aesthetics compete with ultra-luxury natural stones.

The capacity expansion math is compelling. 8.1 lakh square meters of production capacity coming online by March 2026, with projected revenues of Rs 450-525 crores at full utilization. At current margins, that's Rs 100+ crores of incremental profit from a single line.

Cost advantages versus global competitors remain substantial. Caesarstone's gross margins have been trending down in the 26-27% range compared to ~65% for Pokarna. This isn't just labor arbitrage—it's operational excellence, vertical integration, and strategic sourcing combining to create a structural advantage.

The domestic Indian market is finally awakening. As Indian consumers see quartz in international contexts through social media and travel, demand is building. Pokarna's brand and manufacturing presence give it first-mover advantage in what could become a multi-thousand-crore market.

The anti-dumping victory creates a regulatory moat. With effectively zero duties while competitors face higher rates, Pokarna has a multi-year window to capture market share in the US before any potential policy changes.

Bear Case: The Skeptic's Concerns

The concentration risk is undeniable. 83% revenue from the US market means any US recession hits directly. The Federal Reserve's inflation fight could tip the economy into recession, crushing housing demand and with it, demand for quartz surfaces.

Raw material dependency remains a vulnerability. 62% of quartz from Turkey creates geopolitical risk. Any disruption—whether from regional conflicts, trade disputes, or natural disasters—could severely impact production.

Competition is intensifying from multiple directions. Chinese manufacturers continue to improve quality while maintaining cost advantages. Indian competitors are copying Pokarna's playbook, setting up Breton lines and targeting the US market. Even natural stone is fighting back with new treatments and marketing campaigns.

The real estate cycle is turning. After years of unprecedented growth, US home prices are softening. Higher mortgage rates are crushing affordability. The renovation boom driven by pandemic-era savings and work-from-home trends is ending. The next few years could see significantly lower demand.

Health concerns around silica dust in quartz fabrication are gaining attention. ongoing investigations into the health risks, particularly Silicosis, associated with Quartz manufacturing and fabrication. While Pokarna manufactures safely, fabricator injuries could lead to regulatory changes or demand shifts.

Technology disruption could come from unexpected quarters. New materials like porcelain slabs or recycled glass surfaces could capture the innovation premium. 3D printing of surfaces could eliminate traditional manufacturing advantages.

Valuation has run ahead of fundamentals. The stock has had a tremendous run, and any disappointment in execution or market conditions could lead to sharp corrections.

The Balanced View

Reality likely lies between these extremes. Pokarna has built a resilient business with multiple competitive advantages, but it operates in a cyclical industry with real risks. The key variables to watch:

-

US Housing Data: Monthly existing home sales, building permits, and renovation spending will telegraph demand 6-12 months forward.

-

Capacity Utilization: How quickly the new line ramps will indicate whether demand projections are realistic.

-

Margin Trajectory: Any compression would signal either competitive pressure or raw material inflation.

-

Geographic Diversification: Success in Europe, Canada, or India would reduce concentration risk.

-

Technology Adoption: Market reception for KREOS and CHROMIA products will validate the innovation strategy.

The next decade will likely see Pokarna evolve from a manufacturing company to a materials technology company. The investments in automation, AI, and advanced materials position it well for this transition. Whether it can maintain its margins while scaling to become a global top-5 player remains the key question.

XI. Recent Developments & Analysis

The latest financial results paint a picture of a company firing on all cylinders. For the six months period ending with September 30, 2024, Pokarna Limited reported 54.18 per cent upswing in net profit to Rs 78.05 crore. During the period, the company's total revenues surged by 22.47 per cent to Rs 450.8 crore compared to H1FY24. Its EBITDA stood at Rs 154.10 crore, up 26.55 per cent. Pokarna limited declared an EPS of Rs 25.17 for the six-month period, up 54.18 per cent.

These aren't just good numbers—they're accelerating numbers. The profit growth outpacing revenue growth indicates operating leverage kicking in. The expanded EBITDA margins suggest pricing power remains intact despite global economic uncertainties.

The November 2024 capacity expansion announcement deserves deeper analysis. Rs 440 crore investment at current interest rates and construction costs represents serious conviction. Management is essentially betting that demand in 2026-27 will be robust enough to absorb 50% more capacity.

The technology roadmap is crystallizing. The KREOS line commercialization in Q3 FY25 will be the first test of Pokarna's ability to create new product categories rather than just compete in existing ones. Early customer feedback and order patterns will be critical indicators.

Stock performance has been volatile but generally positive, reflecting both the company's strong execution and broader market concerns about global growth. The achievement of the 52-week high of Rs 1,451.65 before pulling back suggests investor enthusiasm tempered by valuation concerns.

The competitive landscape is evolving rapidly. Caesarstone's acquisition of Lioli in India signals that global players see the Indian market opportunity. Chinese manufacturers are getting more sophisticated in their US market approach despite trade tensions. Regional players in the US are consolidating, creating larger, more formidable competitors.

The regulatory environment remains favorable but fluid. The zero anti-dumping duty is a significant advantage, but trade policies can change with administrations. Pokarna's strategy of maintaining transparent pricing and high quality standards provides some insulation, but vigilance is required.

Sustainability initiatives are becoming more than just corporate responsibility—they're becoming competitive advantages. Customers, particularly in the commercial segment, increasingly demand environmental certifications and carbon footprint data. Pokarna's investments in zero liquid discharge and energy efficiency position it well for this trend.

The domestic market strategy is finally showing results. Experience centers in metros are generating leads, and Indian architects are beginning to specify quartz in luxury projects. While still small relative to exports, domestic sales provide diversification and typically higher margins due to lower logistics costs.

Looking ahead to the remainder of FY25 and into FY26, several catalysts could drive performance:

- US Interest Rate Cuts: Any Federal Reserve pivot to lower rates would immediately boost US housing demand

- New Product Launches: Market reception for KREOS ultra-thin slabs

- Domestic Traction: Whether Indian market adoption accelerates

- Operational Efficiency: How quickly the company can optimize the Mekaguda facility

The story of Pokarna is far from over. From its origins in a Secunderabad fabric shop to its position as India's largest quartz exporter, the company has consistently defied conventional wisdom. The next chapter—becoming a global top-5 player—will require navigating new challenges: managing rapid scaling, maintaining culture amid growth, and continuing to innovate in an increasingly competitive market.

As we close this deep dive into Pokarna's remarkable transformation, one thing becomes clear: this isn't just a story about stones and surfaces. It's about vision, patience, and the courage to make contrarian bets. Gautam Chand Jain's journey from fabric trader to quartz pioneer encapsulates the broader Indian entrepreneurial story—ambitious, resilient, and increasingly global.

The question now isn't whether Pokarna can compete globally—it has proven that definitively. The question is whether it can maintain its entrepreneurial edge while scaling to become an industrial giant. If history is any guide, betting against Pokarna would be as contrarian as Jain's original bet on granite quarries in 1991—and potentially just as wrong.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube