Amer Sports: From Finnish Tobacco to Global Premium Sports Empire

I. Introduction: The Unlikely Empire

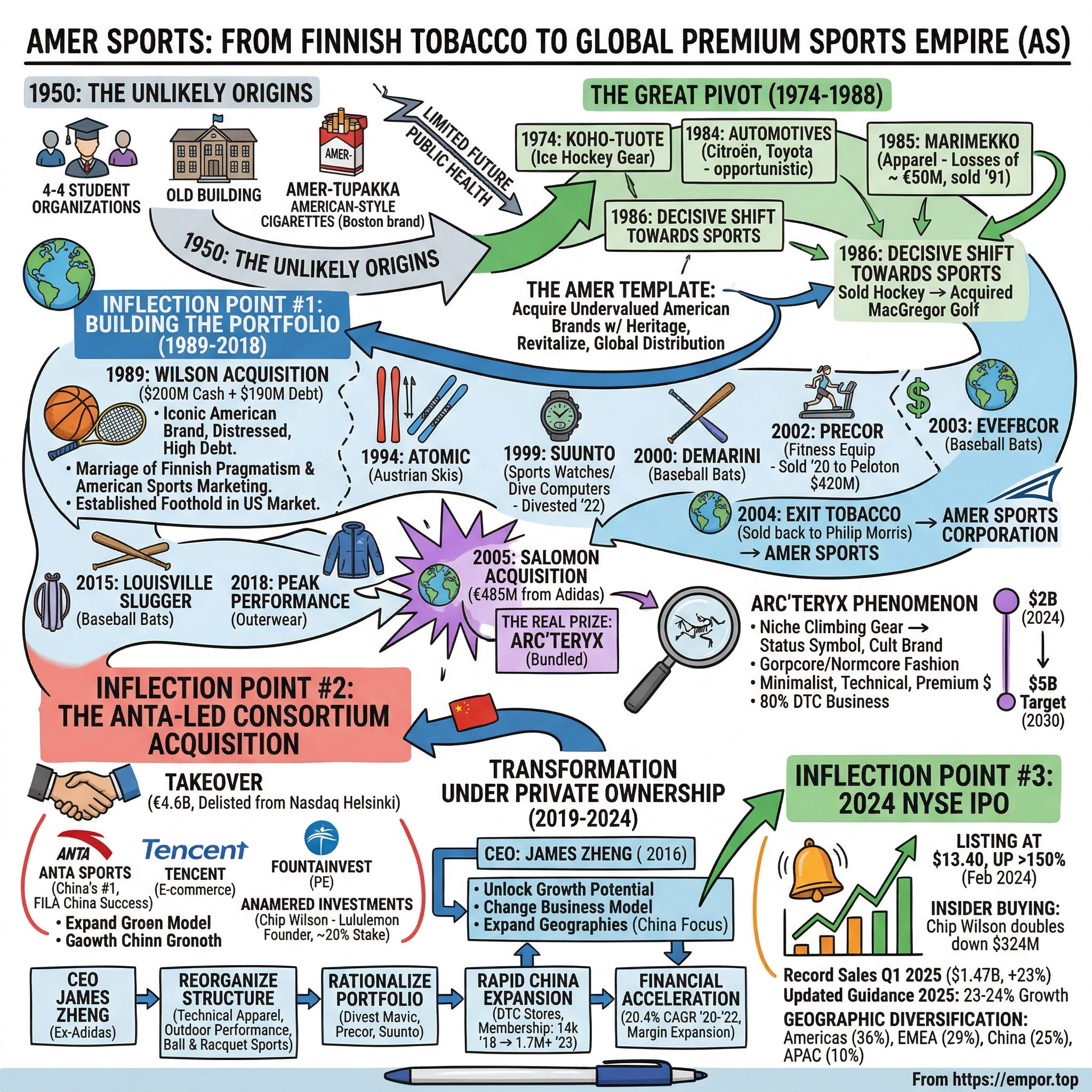

Picture this: A group of Finnish university students, barely a decade removed from World War II, pool their resources to sell American-style cigarettes to their war-weary countrymen. Now fast-forward seventy-five years—that same corporate entity now owns Arc'teryx jackets worn by Wall Street executives and Silicon Valley engineers, Wilson basketballs used in the NBA, and Salomon trail runners adorning the feet of celebrities like Bella Hadid and Rihanna.

How did a Finnish tobacco company founded by four student organizations become the owner of some of the most coveted premium sports brands on Earth?

Amer Sports manages a diverse portfolio of 10 outdoor and action sports brands that collectively generated revenue of $5.2 billion in 2024. Although primarily owned by the Chinese conglomerate Anta Sports, Amer operates with a degree of autonomy.

The Amer Sports story is one of radical corporate metamorphosis—a company that has reinvented itself across three different industries over seven decades, each transformation more audacious than the last. It's a tale of Finnish pragmatism colliding with American brand power, ultimately merging with Chinese capital to create one of the most remarkable success stories in the global sporting goods industry.

In Q3 2025, revenue increased 30% to $1,756 million, with strong momentum continuing. All four regions accelerated and achieved double-digit revenue growth, with Greater China growing 47%. The company that once sold Boston-brand cigarettes now commands a portfolio of technical outdoor and sports equipment brands that has delivered stockholders a return of more than 150% since its February 2024 IPO.

The journey from tobacco to triumph offers profound lessons for investors and business strategists alike: about the power of brand portfolios, about timing pivots correctly, about the marriage of Western brand heritage with Eastern capital and market access. It's also a cautionary tale about leverage, geopolitical risk, and the fine line between fashion trends and enduring demand.

Let's trace the arc of this extraordinary corporate odyssey—from post-war Helsinki to the trading floor of the New York Stock Exchange.

II. The Unlikely Origins: Student Organizations & Tobacco (1950–1974)

In the gray Helsinki of 1950, Finland was still rebuilding. The nation had fought two brutal wars against the Soviet Union during World War II, emerged independent but impoverished, and was now navigating the treacherous shoal of Cold War neutrality. In this environment, a peculiar business venture emerged—one that would eventually evolve into a global sporting goods powerhouse.

The founders were not industrialists or wealthy magnates, but four Finnish educational organizations: the Finnish Association of Graduate Engineers, the Finnish Association of Graduates in Economics and Business Administration, the Land and Water Technology Foundation, and the Student Union of the Helsinki School of Economics. These academic bodies saw an opportunity in the post-war reconstruction to generate income while supporting Finnish society.

Their vehicle was Amer-Tupakka—literally "Amer Tobacco"—a company established to introduce American-style tobacco products to Finnish consumers. The timing was shrewd. Post-war Finland, like much of Europe, had a population hungry for the tastes of modernity and American culture. The company began by producing Boston-brand cigarettes, tapping into the considerable cachet that anything American possessed in those years.

The business proved remarkably successful. By 1961, Amer-Tupakka had secured an exclusive license from Philip Morris to produce and distribute its brands in Finland—a partnership that would position the company as the dominant player in the Finnish tobacco market for decades to come. By 1988, Amer held a commanding 62 percent share of the Finnish tobacco market, making it the nation's leading tobacco producer.

But the founders' educational backgrounds made them keenly aware of one fundamental truth: tobacco, however profitable, was a business with a limited future. Public health concerns were already emerging in the 1960s, and these academically-minded owners understood that diversification was essential.

The tobacco profits became the fuel for broader expansion. By the mid-1960s, Amer had moved beyond cigarettes into shipping operations. The company began transforming from a single-product tobacco company into a diversified Finnish conglomerate—a transformation that would only accelerate in the decades ahead.

For investors today, the tobacco origins matter for two reasons. First, they explain the company's conservative Finnish corporate DNA—a bias toward operational discipline, strategic patience, and careful capital allocation that remains visible today. Second, the tobacco profits provided the capital base that enabled Amer's aggressive acquisition strategy in the decades that followed. Without those cigarette revenues, there would be no Arc'teryx jackets, no Wilson footballs, no Salomon skis.

The student organizations that founded Amer-Tupakka couldn't possibly have imagined that their tobacco venture would one day manufacture gear for Olympic athletes and fashion-forward urbanites alike. But they built something more valuable than they realized: a corporate platform with the capital resources and strategic discipline to recognize new opportunities and seize them decisively.

III. The Conglomerate Era & First Steps into Sports (1974–1988)

The 1970s marked Amer's first tentative steps into the sports equipment market—steps that would eventually define the company's entire future. The pivot began in 1974, when Amer acquired Koho-Tuote, a Finnish manufacturer of ice hockey gear. This wasn't an obvious choice for a tobacco company, but Finland's passion for hockey made the acquisition strategically sensible.

Amer proved to be an aggressive consolidator. In 1978, the company acquired Koho Sporting Goods Corporation, Koho's North East US distributor. The following year, it purchased Les Industries du Hockey Canadien Inc., the manufacturer of Canadien hockey sticks, along with an ice hockey protective equipment manufacturer. Within five years, Amer had assembled a modest but coherent portfolio of hockey-related businesses.

The public markets recognized this emerging strategic capability. In 1977, Amer obtained a listing on the Helsinki Stock Exchange, raising capital for further expansion. Seven years later, in 1984, the company achieved a listing on the London Stock Exchange—only the second Finnish company ever to do so. This dual listing gave Amer access to international capital markets and signaled its ambitions beyond the Nordic region.

The 1984 move into automotives demonstrated both Amer's opportunism and its lack of strategic focus during this period. The company acquired Korpivaara Oy, Finland's largest vehicle importer, gaining exclusive rights to distribute Citroën and Toyota brands in Finland. The acquisition was profitable but revealed a company still searching for its true identity—a conglomerate adding assets without a clear unifying vision.

More intriguing was the 1985 acquisition of Marimekko, the iconic Finnish design company famous for its bold prints and modernist aesthetic. This purchase brought Amer into apparel and design—categories that would eventually become central to its identity. Unfortunately, Amer proved unable to nurture the creative brand. Marimekko incurred losses of approximately €50 million under Amer's ownership before being sold to Kirsti Paakkanen in 1991.

Then came 1986—the year Amer made its decisive pivot toward sports. The company sold all its ice hockey-related businesses, which might have seemed counterintuitive given the five-year acquisition spree. But the hockey divestiture financed something far more significant: a majority stake in MacGregor Golf, acquired from none other than Jack Nicklaus. MacGregor was a faded American golf equipment brand with heritage dating back to 1897. Amer saw potential to revitalize it.

The MacGregor deal established a template that would define Amer's strategy for the next four decades: acquire undervalued American sports brands with authentic heritage, then invest in their revitalization while leveraging global distribution capabilities. The strategy required patience, operational skill, and access to capital—all attributes that Amer possessed.

But the late 1980s also brought controversy that foreshadowed tobacco's declining social acceptance. A movement called Klubi 88 made a provocative statement at Amer's annual general meeting, claiming the company was "the single largest causer of cancer in Finland." The activists called for an end to tobacco sponsorships by athletes like sailor Hjallis Harkimo and Formula 1 driver Keke Rosberg. While Amer didn't immediately respond by exiting tobacco, the writing was on the wall.

The company that had been built on cigarettes was evolving into something very different—a sporting goods platform with the capital, operational capabilities, and international reach to compete on the global stage. The MacGregor acquisition was just an appetizer for what was to come.

IV. The Wilson Acquisition: A Bold Finnish Play for American Sports (1989)

February 1989 marked the moment Amer transformed from a Finnish conglomerate dabbling in sports equipment into a serious player in the global sporting goods industry. The acquisition of Wilson Sporting Goods Company from Chicago was, at the time, the largest foreign acquisition ever undertaken by a Finnish company.

The Wilson Sporting Goods Company is an American sports equipment manufacturer based in Chicago, Illinois. Wilson makes equipment for many sports, among them baseball, badminton, American football, basketball, fastpitch softball, golf, racquetball, soccer, squash, tennis, pickleball, and volleyball. The company has been a subsidiary of Finnish retailer Amer Sports since 1989.

Wilson's heritage was extraordinary. The company traces its roots to the "Schwarzschild & Sulzberger" meatpacking company based in New York, that operated meat packing slaughterhouses. Sulzberger & Son's founded the "Ashland Manufacturing Company" in 1913 to use animal by-products from its slaughterhouses. It started out in 1914, making tennis racket strings, violin strings, and surgical sutures, but soon expanded into baseball shoes and tennis racquets.

The Wilson origin story is a classic American tale of industrial ingenuity—transforming animal gut by-products into tennis racket strings, then leveraging that manufacturing foothold to expand into the broader sporting goods market. By the late 1980s, Wilson supplied official balls to both the NBA and NFL, provided uniforms to Major League Baseball teams, and equipped U.S. Olympic teams.

In 1967, the company was acquired by Ling-Temco-Vought. Only three years later, PepsiCo became Wilson's new owner. In those days, the company manufactured and commercialized the official balls of both the NBA and NFL, and provided most of the uniforms of teams in Major League Baseball and the United States Summer Olympics teams. In 1979, Wilson tennis balls were first used in the US Open, and still are used to this day.

But by the late 1980s, Wilson had become heavily indebted under its private equity ownership. The brand retained enormous value—instant recognition with American consumers, deep relationships with professional sports leagues, and technical manufacturing expertise—but it needed capital investment and strategic focus.

PepsiCo divested Wilson in 1985 to the private equity firm Wesray Capital Corp., and in 1989, it was acquired by the Finnish company Amer Group for $200 million in cash plus $190 million in debt obligations, marking Wilson's entry into a broader international sports conglomerate.

The deal represented audacious strategic thinking. Amer, a Finnish company with annual revenues far smaller than Wilson's, was acquiring an iconic American brand in the world's largest sports market. Finnish executives would now be responsible for products used by Michael Jordan and John McEnroe. The cultural and operational challenges were immense.

The integration proved difficult. Amer's management had to learn quickly how to operate in the American market, understand the rhythms of professional sports seasons, and navigate complex licensing relationships. The company made mistakes—the Marimekko debacle, where losses accumulated to €50 million, served as a painful reminder that brand management required skills Amer was still developing.

But the Wilson acquisition established two crucial capabilities. First, it gave Amer a foothold in the American market—distribution infrastructure, retail relationships, and brand recognition that would prove invaluable for future acquisitions. Second, it demonstrated that Finnish pragmatism could be married successfully with American sports marketing. Wilson's heritage remained intact; Amer simply provided the capital and operational discipline to stabilize and grow the business.

During the early 1990s, Wilson had the largest market share of all the sporting goods companies around the world, with total sales amounting to 8.5 percent of the market. Its closest competitors, Anthony Industries, Inc., Johnson Worldwide Associates, and Spalding & Evenflo Co., Inc., had achieved seven percent, 4.9 percent, and 4.6 percent shares of the market, respectively. Clearly, the international manufacturing and distribution network Wilson was building owed much of its success to the contacts and resources provided by its parent company, the Amer Group.

For investors, the Wilson acquisition illustrates a recurring theme in Amer's history: the willingness to make contrarian bets on undervalued brands with authentic heritage. Wilson wasn't trendy in 1989; it was a workhorse brand associated with traditional American sports. But that very authenticity—the same quality that might make fashion-focused investors look elsewhere—created durable value that compounded over decades.

V. Building the Portfolio: The 1990s-2000s Acquisition Spree

The Wilson acquisition established the playbook. Over the next fifteen years, Amer would execute it repeatedly—acquiring brands with genuine technical heritage, investing in their development, and integrating them into an increasingly sophisticated global distribution network.

The pace of deal-making was relentless. In 1994, Amer acquired Atomic, the Austrian ski equipment manufacturer known for its high-performance alpine skis and bindings. Atomic brought expertise in a new category—winter sports—and established Amer's presence in the European mountain sports market. The acquisition also introduced the company to the technical product development capabilities required for high-performance skiing equipment.

In 1999, Amer purchased Suunto, the Finnish manufacturer of sports watches and dive computers. Suunto represented a bet on the emerging wearables category—the idea that athletes would want sophisticated instrumentation to track their performance. This was prescient, though the category would later become crowded with competition from Apple and Garmin. Suunto was eventually divested in 2022.

The year 2000 brought DeMarini Sports into the fold. DeMarini was a specialist in high-performance baseball and softball bats, a natural complement to Wilson's ball sports portfolio. Two years later, in 2002, Amer acquired Precor, a manufacturer of commercial fitness equipment found in gyms around the world. Precor was sold to Peloton in December 2020 for $420 million—a transaction that predated Peloton's subsequent struggles but demonstrated Amer's increasing focus on its core outdoor and sports equipment businesses.

The most strategically significant development of this era came not through acquisition but through divestiture. In 2004, Amer finally exited the tobacco business, selling its operations back to Philip Morris. The company that had been founded to sell cigarettes was now entirely focused on sporting goods. To mark this transformation, the company changed its name to Amer Sports Corporation.

This name change was more than symbolic. It represented a complete reinvention of corporate identity—from tobacco conglomerate to specialized sporting goods platform. The Finnish educational organizations that had founded Amer-Tupakka in 1950 had long since exited their positions, but their creation had evolved into something they could never have imagined: a global sports empire with brands recognized on tennis courts, ski slopes, and playing fields worldwide.

By 2005, Amer Sports had assembled a diverse portfolio spanning golf (MacGregor, divested in 1997), ball sports (Wilson, DeMarini), winter sports (Atomic), fitness (Precor), and wearables (Suunto). The company had proven it could identify attractive acquisition targets, execute transactions, and integrate acquired businesses into a coherent operational structure.

But something was still missing. The portfolio was diversified across multiple categories, but none of the brands occupied the fast-growing outdoor and trail running segments that were beginning to capture consumer attention. The acquisition that would transform Amer from a solid sporting goods conglomerate into a premium brand powerhouse was still to come.

VI. INFLECTION POINT #1: The Salomon Acquisition (2005)

The 2005 acquisition of Salomon from Adidas for €485 million stands as the most transformative deal in Amer Sports' history—not because of Salomon itself, but because of what came bundled with it.

Salomon SAS is a French sports equipment manufacturing company headquartered in Annecy, France. It was founded in 1947 by François Salomon in the heart of the French Alps and is a major brand in outdoor sports equipment. Salomon is owned by Finnish retail conglomerate Amer Sports. Salomon was founded in 1947 in the city of Annecy in the heart of the French Alps. François Salomon launched the company by producing ski edges in a small workshop, with only his wife and son, Georges, to help. Georges Salomon is credited with taking the company and evolving it toward the global outdoor sports brand it is today.

Salomon's story paralleled Wilson's in some ways—a family business with authentic heritage in outdoor sports that had passed through corporate ownership without losing its technical credibility. The Salomon Group was purchased by Adidas in 1997 and the official name was changed to Adidas-Salomon AG. The purchase also included TaylorMade and Maxfli. Adidas then later sold the company to Amer Sports in 2005.

The Adidas marriage had never quite worked. Adidas was fundamentally a footwear and apparel company focused on athletic performance and lifestyle markets. Salomon's core competency—technical equipment for skiing, hiking, and trail running—didn't mesh naturally with Adidas's urban-focused brand positioning. When Adidas decided to divest, Amer saw its opportunity.

But the real prize wasn't obvious from the headlines. When Amer acquired Salomon, a small Canadian outdoor apparel company called Arc'teryx came bundled with the deal. Arc'teryx had been acquired by Salomon in 2001, and when Adidas sold Salomon to Amer, Arc'teryx transferred along with it.

Arc'teryx was founded in 1989 in North Vancouver, British Columbia, originally under the name Rock Solid, focused on climbing gear. Co-founder Dave Lane later sold a 50% interest to Jeremy Guard, who changed the company name to Arc'teryx in 1991. The name and logo reference the Archaeopteryx, the transitional fossil representing the evolution from dinosaurs to birds—a choice intended to represent the idea of accelerating evolution in outdoor equipment design.

At the time of the acquisition, Arc'teryx was a niche brand beloved by serious climbers and mountaineers but essentially unknown to the broader consumer market. Its products commanded premium prices—sometimes dramatically higher than competitors—based on technical innovations like WaterTight™ zippers, proprietary construction techniques, and obsessive attention to performance details.

In early 2024, we've been introduced to sustainable improvements through rolling updates to Arc'teryx's flagship Alpha SV and Beta LT shells that update necessary synthetics with 100% recycled and bio-based components, respectively.

The Alpha SV Jacket, introduced in 1998 featuring GORE-TEX technology, had established Arc'teryx's reputation for creating the most technically advanced outerwear on the market. The brand worked with Polartec to create the soft shell category. These weren't marketing innovations—they were genuine technical advances that serious outdoor athletes recognized and paid premium prices for.

Amer Sports' management understood that they had acquired something special, but the full potential of the Arc'teryx brand wouldn't become apparent for another decade. In 2005, the global outdoor apparel market was growing steadily but hadn't yet experienced the explosive expansion driven by wellness culture, social media, and the "gorpcore" fashion phenomenon.

The Salomon acquisition gave Amer four critical capabilities it had previously lacked: entry into the outdoor performance footwear market (a category with enormous growth potential), a platform in trail running, presence in technical apparel through Arc'teryx, and a European operational hub in the French Alps. The €485 million price looked reasonable at the time; it would prove to be one of the most value-creating acquisitions in sporting goods history.

VII. Building Out the Portfolio (2005–2018)

With Salomon and Arc'teryx in the fold, Amer Sports continued to expand and refine its portfolio over the next thirteen years. The acquisitions during this period were largely complementary—filling gaps in existing categories rather than entering entirely new markets.

In 2015, Amer strengthened its ball sports position by acquiring Louisville Slugger, the iconic American baseball bat brand. Louisville Slugger brought heritage reaching back to 1884—the bat had been endorsed by Honus Wagner in 1905 and used by Babe Ruth. Combined with Wilson and DeMarini, Amer now controlled a dominant position in baseball equipment.

ENVE Composites, a manufacturer of carbon fiber bicycle rims and components, was acquired in 2016, representing a brief foray into cycling. ENVE was divested in 2024 as Amer sharpened its focus on core categories. In 2017, the US ski brand Armada joined the portfolio, adding another winter sports franchise alongside Atomic and Salomon.

The 2018 acquisition of Peak Performance, the iconic Swedish outerwear and streetwear brand, signaled Amer's increasing interest in the intersection of technical outdoor performance and urban fashion. Peak Performance occupied a market position slightly more accessible than Arc'teryx but still premium relative to mass-market competitors.

Internally, Amer reorganized its operations to reflect the evolving portfolio. In 2008, the company divided operations into three business units: winter sports, outdoor sports, and ball sports (Wilson, Louisville Slugger, and DeMarini). This segmentation allowed for more focused management attention and clearer accountability for financial performance.

By 2018, Amer Sports had assembled a portfolio that spanned multiple outdoor and sports categories: premium technical apparel (Arc'teryx, Peak Performance), outdoor performance footwear and equipment (Salomon), winter sports (Atomic, Salomon hardgoods, Armada), ball sports (Wilson, Louisville Slugger, DeMarini), and several smaller brands. Revenue had grown to approximately €2.7 billion.

But the company faced limitations. As a publicly traded Finnish company with modest market capitalization, Amer's ability to invest aggressively in brand development and geographic expansion was constrained. The Arc'teryx opportunity, in particular, seemed under-exploited. The brand had cult following in outdoor communities but minimal mainstream awareness. Accelerating Arc'teryx's growth would require significant capital investment in stores, marketing, and supply chain—capital that a public company focused on quarterly earnings might struggle to deploy.

The strategic question facing Amer in late 2018 was whether to continue as a public company, incrementally growing its brands, or to pursue a more aggressive trajectory under different ownership. An unexpected consortium of investors would soon provide an answer.

VIII. INFLECTION POINT #2: The Anta-Led Consortium Acquisition (2019)

The announcement in December 2018 sent shockwaves through the sporting goods industry: a consortium of investors led by Anta Sports, China's largest sportswear manufacturer, was making a tender offer for all outstanding shares of Amer Sports. The deal would value Amer at €4.6 billion—a 40 percent premium over the average market value—and take the company private.

The consortium members represented a remarkable combination of global capital and strategic expertise. Anta Sports Products Limited is a Chinese sports equipment multinational corporation headquartered in Jinjiang, China. It is the world's third-largest sportswear company by revenue, behind Nike and Adidas, and ahead of Li-Ning. Founded in 1991, its operations involve the business of designing, developing, manufacturing and marketing products, including sportswear, footwear, apparel and accessories under its own brand name. Its main subsidiary is Finnish sport retailer Amer Sports, which itself manages 25 apparel brands such as Arc'teryx, Salomon, and Wilson.

Anta was founded by Ding Shizhong in 1991. In 2008, the Beijing Olympics gave Anta the opportunity to expand its business marketing footwear. Anta Sports was listed as 2020.HK on the Hong Kong Stock Exchange in 2007, with its IPO price at HK$5.28 per share. In 2009, the company acquired the Fila trademark in mainland China, Hong Kong and Macao from Belle International.

Anta's FILA China acquisition in 2009 had proven transformational—the company had taken a struggling Western brand and turned it into a premium powerhouse in the Chinese market. This track record suggested Anta understood how to unlock value from international brands.

But Anta wasn't acting alone. Tencent Holdings, the Chinese technology giant, brought capital and e-commerce expertise. FountainVest Partners contributed private equity capabilities and deal experience. And perhaps most intriguingly, Anamered Investments—the investment vehicle of Chip Wilson, founder of Lululemon Athletica—provided both capital and strategic credibility.

In 2018, I purchased 20% of Amer Sports with partners Anta Sports (largest athletic company in China), Tencent and Fountainvest. Amer is an athletic conglomerate owning Arc'teryx, Salomon, Peak Performance, Wilson Sports and Atomic Ski.

Chip Wilson's involvement was particularly significant. Dennis J. "Chip" Wilson is an American-Canadian businessman, investor, and philanthropist who has founded several retail apparel companies, most notably the yoga-inspired athletic apparel company Lululemon Athletica. As of March 2025, Forbes estimates his net worth to be $6.3 billion USD. Wilson is widely regarded as the progenitor and a pioneering figure of the athleisure phenomenon.

If anyone understood how to build premium athletic apparel brands and drive them from niche markets to mainstream success, it was the founder of Lululemon. His willingness to commit significant personal capital—ultimately around €550 million for a roughly 20% stake—provided powerful validation of the investment thesis.

The acquisition closed on April 2, 2019, and Amer Sports was delisted from Nasdaq Helsinki on September 5, 2019. The company had been public since 1977; it was now entering a new chapter under private ownership.

The consortium's strategic rationale centered on unlocking growth potential that public market pressures had constrained. The company's prospectus later described the thesis succinctly: the consortium acquired Amer Sports with the goal of unlocking substantial underlying brand growth potential by transforming the business model, investing in the brands, expanding geographies, and developing a multi-channel strategy.

The investors were excited to bring these premium international brands to Chinese consumers, who increasingly sought high-end products with outstanding qualities and heritage in various niche and specialized sports segments. After acquiring Amer Sports, Anta set a "EUR 1 billion development plan" aiming to develop Arc'teryx, Salomon, and Wilson into billion-euro brands respectively, and achieve EUR 1 billion in revenue for the China market and the direct retail model.

The €1 billion targets seemed ambitious at the time. They would prove conservative.

IX. The Transformation Under Private Ownership (2019–2024)

The five years under private ownership witnessed the most dramatic transformation in Amer Sports' history. Under the leadership of CEO James Zheng, who joined from Anta Sports in 2020, the company reorganized its structure, rationalized its portfolio, expanded aggressively in China, and prepared for an eventual return to public markets.

James Zheng joined the company in 2020. Education: B. Sc. Management Science, Shanghai Fudan University, China. Primary work experience: Group President, ANTA Sports Products Ltd. Various senior executive and sales roles in large publicly listed companies such as Adidas, Reebok, and P&G.

Zheng brought precisely the experience the role demanded. His early career was marked by senior roles at Procter & Gamble, followed by pivotal positions at Adidas and Reebok. At Adidas, he served as General Manager of Reebok (China) and Executive Vice President of Sales for Adidas Greater China. In 2020, he was appointed Chief Executive Officer of Amer Sports, from which he has driven extensive brand transformation and market expansion initiatives.

The operational overhaul began immediately. In 2019, the company reorganized and simplified its corporate structure to reflect a brand-direct model within three core segments designed to empower the brands and drive accountability. The segments—Technical Apparel (led by Arc'teryx), Outdoor Performance (led by Salomon), and Ball & Racquet Sports (led by Wilson)—each received dedicated management teams and clear financial targets.

Portfolio rationalization followed. Mavic was divested in 2019. Precor was sold to Peloton in December 2020 for $420 million. Suunto followed in 2022. Each divestiture sharpened Amer's focus on its highest-potential brands while generating capital for investment in growth initiatives.

The China expansion was extraordinary in its scale and ambition. As of September 2023, Amer Sports operated 63 Arc'teryx company-owned retail stores in Greater China, accounting for nearly half of the global total store count, along with 30 Salomon company-owned retail stores and 67 distribution stores—far surpassing the 13 stores in 2019. From 2020 to 2022, Amer Sports' revenue in the Greater China region increased from USD 202 million to USD 524 million at a compound annual growth rate of 60.9%.

The Arc'teryx membership program illustrated the brand's rising prominence: from a brand perspective, Amer Sports attributes its rapid growth in China primarily to Arc'teryx, which, as of September 30, 2023, had over 1.7 million members in the Greater China region, compared to 14,000 in 2018.

Arc'teryx, which transitioned from an 80% wholesale business to an 80% DTC business from 2020 to 2024, is planning to double its 150-store count to 300 by 2030.

This wholesale-to-DTC transformation represented a fundamental shift in business model—one that improved gross margins, enhanced customer relationships, and built brand equity more effectively than traditional wholesale distribution could achieve.

The financial results validated the strategy. Following the acquisition, revenue growth accelerated, with a compound annual growth rate of 20.4% from 2020 to 2022, while gross margins expanded from 47.0% to 49.7% over the same period. The company was growing faster and more profitably than it had as a public company.

By late 2023, the consortium concluded the time had come to return to public markets. The transformation was working; the brands were accelerating; the China platform was established. An IPO would provide liquidity for investors, capital for continued expansion, and the currency of public stock for potential acquisitions.

X. INFLECTION POINT #3: The 2024 NYSE IPO

On February 1, 2024, Amer Sports returned to the public markets with a listing on the New York Stock Exchange—a geographic shift from its previous Helsinki listing that reflected the company's increasingly global profile and its ambitions in the American market.

Amer Sports stock was originally listed at a price of $13.40 in Feb 1, 2024. If you had invested in Amer Sports stock at $13.40, your return over the last 1 years would have been 175.82%, for an annualized return of 175.82%.

The IPO didn't unfold exactly as planned. The company raised $1.37 billion at $13 a share, down from a previous range of $16 to $18 a share. The IPO valued the company at $6.3 billion—well below the $10 billion figure that had been floated in media reports. Investors expressed concern about the company's reliance on China for sales, its $2.1 billion debt load, and the absence of profits between 2020 and September 2023.

Chip Wilson doubled down on his investment in Amer Sports, buying $324 million worth of shares at the company's IPO. Wilson, best known for founding Lululemon Athletica, bought 24.9 million shares of Amer Sports at its IPO price of $13 a share. The billionaire had previously indicated he would buy up to $220 million worth during the offering, meaning he upped his bet by 50%, taking advantage of a perceived bargain as Amer's IPO fell short of expectations.

Wilson's willingness to increase his investment at the IPO—from $220 million to $324 million—sent a powerful signal to outside investors. If the Lululemon founder saw the lower pricing as a buying opportunity rather than a red flag, perhaps other investors had been too pessimistic.

Overall, Wilson and those insiders purchased 63 million of the 105 million shares offered to investors with the IPO. The syndicate has strong incentive to support shares of the business: Based on information contained in the prospectus, Wilson and partners took out more than $4 billion in debt to finance the 2019 purchase of the conglomerate. The $1.3 billion proceeds from the IPO went to pay off some of that debt, while the rest of it was converted into equity in Amer Sports. As of today, Wilson owns about 21% of Amer stock, making him the second largest shareholder, behind Anta Sports' 48% stake.

The ownership structure that emerged from the IPO left public shareholders with approximately 20% of the company, while the consortium retained control. Anta Sports remained the largest shareholder with a 48% stake. This concentrated ownership meant public investors were essentially betting on the continued success of the Anta/Wilson strategy rather than expecting any near-term changes in corporate governance.

CEO James Zheng articulated the use of proceeds clearly: the company planned to improve its balance sheet and fund growth initiatives at Wilson, Arc'teryx, and Salomon. He pointed out that Arc'teryx, known for its pricy winter jackets, had very low unaided brand awareness in North America, particularly in the U.S.—meaning there was substantial room to grow.

The IPO skeptics were proven wrong quickly. Amer Sports, which owns Salomon and Arc'teryx as well as several other outdoor brands, doesn't seem to have been affected in any way by the receding gorpcore trend. It reported record sales of $1.47 billion for the first quarter of 2025, up 23 percent from the same period the year before. Its shares are up 150 percent since its 2024 IPO, and up 55 percent in the past month.

XI. The Arc'teryx Phenomenon: A Deep Dive

To understand Amer Sports' investment case, you must understand Arc'teryx. The Canadian brand has transformed from a niche climbing equipment company into a cultural phenomenon that transcends its outdoor sports origins.

The brand's journey from technical niche to mainstream aspiration is a case study in authentic brand building. Arc'teryx emerged from North Vancouver's climbing community, founded by people who genuinely used the products they designed. Early innovations—the WaterTight zipper, proprietary GORE-TEX constructions, meticulous attention to seam sealing—established credibility with serious outdoor athletes that marketing alone could never achieve.

Arc'teryx has become something more than an outdoor brand. It is seen as a high-end status symbol among youth, "just shy of Stone Island and Moncler," according to industry observers. The Financial Times noted one of their largest demographics as "urbanites" in 2022. Labeled a cult brand by Fast Company in 2021, Arc'teryx is worn by "both hikers and hype-beasts" according to The New York Times. The company is a major influence in the "gorpcore" and "normcore" fashion movements—the wearing of minimalist, outdoor apparel in urban settings. Arc'teryx has become a staple of Generation Z and zillennial fashion, particularly in the U.S.

Gorpcore is a fashion trend in which outerwear typically designed for outdoor recreation is worn as streetwear. It has been described as "wearing functional outdoor wear in an urban, trendy style". This includes technical garments such as puffer jackets, hiking boots and fleeces, and brands such as The North Face, Patagonia and Arc'teryx. While the trend has a practical basis, it has also been embraced for its stylish appeal, with celebrities incorporating outdoor gear into everyday outfits. Coined in 2017, gorpcore emerged as a popular trend in the 2020s; some analysts suggest that the COVID-19 pandemic in part influenced this.

The COVID-19 pandemic from 2020 to 2022 accelerated gorpcore's transition from niche interest to widespread appeal, as remote work and a surge in urban exploration prompted consumers to adopt functional outdoor apparel for everyday use. Revenues in the outdoor category reached 24 percent higher than pre-pandemic levels by 2022, reflecting heightened demand for versatile gear amid lockdowns and a reevaluation of lifestyle priorities.

The growth trajectory has been remarkable. Amer Sports is reporting that its Arc'teryx technical outdoor brand achieved over $2 billion of sales in 2024, and delivered another great result in the fourth quarter of the year, again leading growth for the parent of Arc'teryx, Salomon and Wilson Sports. Company CEO James Zheng told analysts and investors that strong growth at Arc'teryx came across all regions, channels, and categories — especially in footwear and women's, which grew faster than the brand overall. "Our differentiated stores continue to be at the heart of Arc'teryx growth strategy and are critical to how we engage with consumers and the community." Arc'teryx opened net eight new retail stores in the 2024 fourth quarter, bringing total net new store openings in 2024 to 33 doors.

High-end outdoors brand Arc'teryx has high expectations for its sales growth over the next five years. CEO Stuart Haselden said on an investor's day call last week that he expects the brand to reach $5 billion in top-line sales by 2030.

From $2 billion in 2024 to a $5 billion target in 2030—a 2.5x increase in six years—requires continued execution on multiple fronts.

Arc'teryx CEO Stuart Haselden stated, "Arc'teryx is special, and I hope you'll get a deeper understanding of that today. It's a unique brand with a unique market position. We do not see a direct competitor for Arc'teryx and how we're positioned. We span at least three distinct market segments. We are the pinnacle in the outdoor market. We compete and win share in the luxury and premium outerwear segment."

The footwear expansion represents a significant growth vector. Plans to operate 290 stores by 2030, up from 170 in 2025. Renée Augustine, the general manager of Arc'teryx footwear, said during the company presentation that the brand's shoe offerings, launched just 18 months ago, has thus far "driven over $250 million revenue."

XII. Current State & Recent Performance (2024–2025)

Amer Sports' financial performance since the IPO has exceeded expectations, silencing many of the skeptics who questioned the company's premium valuation.

Full-year 2024 results demonstrated the portfolio's strength. Revenue increased 18% to $5,183 million, or 19% on a constant currency basis. Technical Apparel (Arc'teryx and Peak Performance) increased 36% to $2,194 million. Gross margin expanded 290 basis points to 55.4%. Net income increased 135% to $73 million; adjusted net income increased 329% to $236 million.

CFO Andrew Page said, "With over 20% revenue growth, healthy margin expansion, significant free cash flow generation, and the transformation of our capital structure, the fourth quarter of 2024 marked a financial turning point in Amer Sports' journey. Although foreign currency exchange headwinds will weigh slightly on our 2025 financial results, continued strong momentum from our highest-margin Arc'teryx franchise and accelerating momentum in Salomon footwear, plus strong and stable positions from our market-leading Hardgoods franchises, gives me confidence that Amer Sports is well positioned to deliver another year of strong and profitable growth in 2025."

The momentum has continued into 2025. In Q3 2025, revenue increased 30% to $1,756 million, with strong momentum continuing into Q4. All four regions accelerated in Q3 and achieved double-digit revenue growth, with Greater China growing 47%.

"All three segments performed extremely well led by exceptional Salomon footwear growth, an Arc'teryx omni-comp reacceleration, and solid growth from Wilson Tennis 360 and our Winter Sports Equipment franchises. We believe our specialized, highly technical brands are well positioned within the premium sports and outdoor market, which continues to be one of the healthiest segments across the global consumer landscape."

"As we begin to look beyond this year, we expect to deliver 2026 Group revenue growth towards the high-end of our long-term algorithm of low-double-digit to mid-teens annual sales growth. And we expect to deliver adjusted operating margin expansion within our long-term algorithm of 30-70+ basis points annually."

The company has raised guidance multiple times throughout 2025. Amer Sports is updating guidance for the year ending December 31, 2025 to reported revenue growth of 23% – 24%, including an approximate 100 basis point benefit from favorable Fx impact at current exchange rates.

In 2024, the firm generates 36% of its revenue from the Americas, 29% from Europe, the Middle East, and Africa, 25% from China, and 10% from Asia-Pacific, excluding China.

This geographic diversification—with no single region dominating excessively—provides some insulation against regional economic weakness or geopolitical disruption.

XIII. Competitive Landscape & Strategic Position

Amer Sports operates in a competitive sporting goods landscape populated by both larger diversified players and specialized premium brands. Understanding this competitive context is essential for evaluating the company's strategic position.

Amer Sports operates in highly competitive sporting goods markets, facing competition from both large diversified companies and specialized brands. In outdoor and technical apparel, the company competes primarily with Patagonia, The North Face (owned by VF Corporation), and Columbia Sportswear. Arc'teryx's premium positioning places it in direct competition with brands like Patagonia and Mammut for high-end mountaineering and outdoor enthusiasts. In the tennis equipment segment, Wilson faces competition from Babolat, Head, and Yonex. The baseball equipment market sees Louisville Slugger and DeMarini competing against Rawlings, Easton, and Marucci Sports.

In 2000, The North Face was acquired by VF Corporation in a deal worth US$25.4 million and became a wholly owned subsidiary. VF Corporation, with its portfolio including The North Face, Vans, and Timberland, represents the most directly comparable publicly traded competitor. However, VF has struggled with inventory challenges and declining consumer demand at some of its brands—challenges Amer Sports has largely avoided.

Porter's Five Forces Analysis:

Threat of New Entrants: LOW The technical outdoor apparel market has high barriers to entry. Developing credible technical products requires years of R&D investment, relationships with material suppliers like Gore-Tex, and brand heritage that cannot be manufactured overnight. Arc'teryx's 35-year history of product innovation creates a moat that new entrants would struggle to replicate.

Bargaining Power of Suppliers: MODERATE Amer Sports depends on suppliers like Gore-Tex for critical components. However, the company's scale provides negotiating leverage, and it has invested in vertical integration where strategically important (Salomon operates an automated production facility in France).

Bargaining Power of Buyers: MODERATE The shift to direct-to-consumer (80% of Arc'teryx revenue) reduces retailer bargaining power. End consumers demonstrate brand loyalty and willingness to pay premium prices.

Threat of Substitutes: LOW TO MODERATE For technical outdoor products, functional performance requirements limit substitution. Fashion trends like gorpcore can shift, but core outdoor enthusiasts will continue purchasing high-performance gear.

Competitive Rivalry: HIGH Nike, Adidas, VF Corporation, Columbia, and numerous specialized brands compete aggressively. However, Arc'teryx's premium positioning creates differentiation from mass-market competitors.

Hamilton Helmer's 7 Powers Framework:

Brand Power: Arc'teryx has developed powerful brand equity that commands premium pricing. The brand's association with technical excellence and authentic outdoor heritage creates consumer willingness to pay 50-100% premiums versus competitors.

Process Power: Arc'teryx's proprietary construction techniques—developed over 35 years—create manufacturing advantages difficult for competitors to replicate. The company's obsessive attention to quality and performance has created internal processes that drive product excellence.

Counter-Positioning: Arc'teryx's premium pricing and technical focus make it difficult for mass-market competitors to respond without cannibalizing their own brand positioning. A North Face or Columbia cannot easily launch products at Arc'teryx price points without confusing their core customer base.

XIV. Investment Considerations: Bull & Bear Cases

The Bull Case

Secular Tailwinds: The outdoor and wellness market benefits from long-term demographic and lifestyle trends. Millennials and Gen Z consumers prioritize experiences, health, and sustainability—values aligned with outdoor recreation. These aren't cyclical trends; they represent structural shifts in consumer preferences.

Brand Portfolio Optionality: Amer Sports owns multiple brands with significant growth runway. Arc'teryx is the current star, but Salomon footwear is inflecting rapidly (CEO Zheng said that for the Arc'teryx brand, footwear continues to be a key growth driver with 35 percent growth), and Wilson maintains steady positions in ball sports. Each brand represents optionality on different growth vectors.

China Opportunity: While holding a modest 1% global market share in the competitive sportswear and equipment industry, Amer Spots has carved out a strategic niche such as outdoor apparel, hiking footwear, and tennis. Following its acquisition by Anta Sports in 2019, Amer underwent a strategic shift, pivoting away from growth primarily driven by acquisitions and wholesale operations. Instead, the company is now prioritizing the expansion of its product range and a direct-to-consumer approach.

Margin Expansion: The shift to direct-to-consumer and the growing mix of higher-margin Technical Apparel creates a multi-year margin expansion story. Arc'teryx margins significantly exceed corporate averages.

Proven Management: James Zheng and team have delivered consistent execution since 2020, validating the consortium's investment thesis.

The Bear Case

China Dependency Risk: Approximately 25% of revenue comes from Greater China. Geopolitical tensions, economic slowdown, or regulatory changes could significantly impact this key growth market.

Fashion Risk: Some portion of Arc'teryx and Salomon demand reflects gorpcore fashion trends rather than core outdoor usage. A quick look at Google Trends data shows that global searches for "gorpcore" peaked in 2023 and have been tailing off ever since. If fashion consumers rotate to other trends, demand could soften.

Valuation: AS is trading at a 166% premium to fair value, according to some analyst estimates. Investors are paying for continued execution of the growth algorithm; any stumbles could result in significant multiple compression.

Concentrated Ownership: With Anta Sports controlling 48% of shares and insiders holding another 20%+, public shareholders have limited influence on corporate governance. The company's interests may not always align with minority shareholders.

Debt Overhang: While improved from the 2019 acquisition, the balance sheet still carries meaningful leverage that constrains financial flexibility.

XV. Key Metrics to Track

For investors monitoring Amer Sports, three KPIs deserve primary attention:

1. Arc'teryx Omni-Comp Growth The Technical Apparel segment's comparable sales growth (combining owned stores and e-commerce) is the single most important indicator of brand health. Management targets mid-teens annual revenue growth for the segment. Sustained deceleration below this level would signal weakening brand momentum. In Q3 2025, Technical Apparel omni-comp reaccelerated to +27%, with broad-based strength across regions, categories and channels.

2. Greater China Revenue Growth Given China's importance to the growth thesis, tracking regional revenue performance is essential. The 47% growth in Q3 2025 is exceptional; investors should watch for normalization versus deceleration. Management has indicated that China and North America should be approximately equal in size by 2030.

3. Gross Margin Progression The company's algorithm calls for 30-70+ basis points of annual adjusted operating margin expansion. Gross margin improvement—driven by DTC mix shift and Arc'teryx revenue contribution—is the primary driver. Sustained margin expansion validates the brand transformation strategy; margin compression would indicate execution challenges.

XVI. Conclusion: From Smoke Rings to Summit Gear

The Amer Sports story defies easy categorization. It's part corporate metamorphosis, part East-meets-West capitalism, part luxury fashion masquerading as technical gear. A company founded to sell American cigarettes to post-war Finns now commands a portfolio of brands that outfit Olympic athletes, Wall Street executives, and fashion-conscious urbanites alike.

The strategic logic connecting tobacco profits in 1950s Helsinki to Arc'teryx jackets on Manhattan sidewalks runs through a consistent thread: the ability to identify undervalued brands with authentic heritage, acquire them at reasonable prices, and invest patiently in their development. From Wilson to Salomon to Arc'teryx, Amer Sports has demonstrated this capability repeatedly.

The Anta-led consortium's 2019 privatization represented a bet that aggressive investment—particularly in China—could unlock growth that public market pressures had constrained. Five years later, that bet has proven correct by virtually every financial measure. Revenue has more than doubled. Margins have expanded. Arc'teryx has transformed from outdoor niche to cultural phenomenon.

Yet challenges remain. China dependency creates geopolitical risk. Fashion trends can shift. Premium valuations leave little room for error. The concentrated ownership structure means public shareholders are essentially passengers on a journey controlled by Anta and Chip Wilson.

For investors evaluating Amer Sports today, the central question is whether the transformation of the past five years represents a new steady state—with continued premium growth justified by brand strength and market positioning—or whether today's exceptional performance simply pulled forward demand that will eventually normalize.

The answer likely depends on one's view of the premium outdoor and athleisure markets. If wellness culture, outdoor recreation, and the "outdoors-as-lifestyle" positioning continue to resonate with global consumers, Amer Sports owns some of the best-positioned brands in the world. If fashion cycles rotate and consumer preferences shift, even strong brands will feel pressure.

What seems undeniable is that Amer Sports has executed one of the most remarkable corporate transformations in modern business history. From tobacco to sports equipment to premium outdoor lifestyle—each transition required strategic courage, operational excellence, and patient capital allocation. The Finnish student organizations that founded Amer-Tupakka in 1950 could never have imagined the company they created would one day manufacture gear for conquering Everest and braving New York winters alike.

The journey from smoke rings to summit gear isn't complete. Arc'teryx's $5 billion revenue target lies ahead. Salomon footwear is only beginning its acceleration. Wilson continues its steady march through ball sports. For Amer Sports, the climb continues—and based on recent performance, the summit views may be worth the altitude.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube