The Travelers Companies: America's Insurance Pioneer

I. Introduction & Episode Roadmap

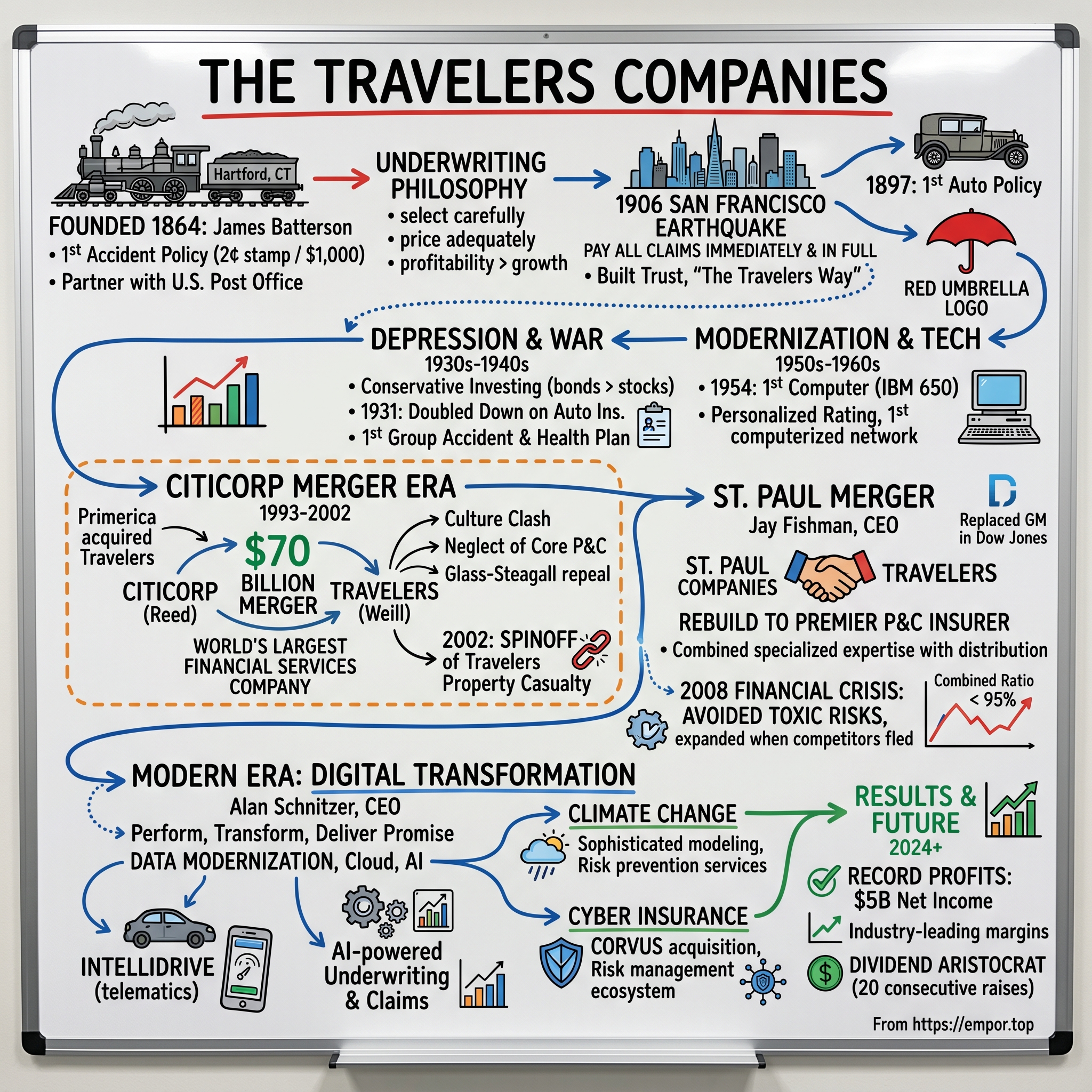

Picture Hartford, Connecticut, 1864. The Civil War rages on, claiming thousands of lives daily. Railroad accidents kill more Americans than any other form of transportation. Into this chaos steps James Batterson, a stonecutter turned entrepreneur, holding what would become America's first accident insurance policy—a simple two-cent stamp that promised $1,000 if you died on your train journey. That humble beginning would grow into The Travelers Companies, now a $40 billion revenue giant and stalwart of the Dow Jones Industrial Average.

How does a company that started by selling insurance to nervous train passengers transform into America's second-largest commercial property and casualty insurer? How did it survive the San Francisco earthquake, the Great Depression, two world wars, merge with (and divorce from) Citigroup, and emerge from the 2008 financial crisis stronger than ever while competitors like AIG needed government bailouts?

This is a story of conservative underwriting meeting aggressive expansion, of technological innovation balanced with old-school relationship building, and most importantly, of understanding risk when others saw only opportunity. It's about building a 170-year fortress in an industry where one bad year can destroy decades of profits.

We'll explore how Travelers pioneered products we take for granted—from auto insurance to cyber coverage—while maintaining the disciplined underwriting culture that has produced industry-leading margins for decades. We'll dissect the Sandy Weill era and the audacious Citicorp merger that created the world's largest financial services company, only to unwind spectacularly. And we'll examine how today's Travelers, under Alan Schnitzer's leadership, navigates climate change, digital disruption, and a hardening insurance market that's delivering record profits.

The insurance industry might seem boring—until you realize it's the ultimate business model: collect premiums upfront, invest the float, and if you price risk correctly, print money for centuries. Warren Buffett built Berkshire Hathaway on this insight. But few have executed it as consistently as Travelers. This is that story.

II. The Beginning: Post Office, Trains, and America's First Accident Policy

The mahogany-paneled offices of James G. Batterson's marble importing business in Hartford must have seemed an unlikely birthplace for American accident insurance. But in 1863, as Batterson prepared for a business trip to England, something remarkable happened. His friend, a local banker named James Bolter, joked about the dangers of transatlantic travel and suggested Batterson get some of that newfangled "accident insurance" he'd heard about in London.

Batterson didn't just buy a policy—he studied the entire British accident insurance industry during his trip. The Brits had been selling Railway Passengers Assurance since 1848, but America had nothing comparable. Railroad accidents were killing over 1,000 Americans annually by the 1860s, with injury rates ten times higher. Newspaper headlines screamed about boiler explosions, bridge collapses, and head-on collisions. Yet American insurers focused solely on fire and marine coverage, viewing accident insurance as unpredictable gambling.

Returning to Hartford, Batterson saw opportunity where others saw chaos. He understood something fundamental: Americans were becoming mobile at unprecedented rates. The railroad network had exploded from 9,000 miles in 1850 to over 30,000 by 1860. People weren't just traveling more—they were anxious about it. Every trip carried genuine mortal risk.

On June 17, 1863, Batterson secured a charter from the Connecticut legislature for The Travelers Insurance Company, capitalized at $500,000. But here's where Batterson's genius emerged: rather than compete with established insurers for agents and distribution, he partnered with the U.S. Post Office.

The post office connection was brilliant. By 1864, America had over 28,000 post offices—more outlets than all bank branches combined. Postmasters, trusted federal employees in every town, could sell simple accident "tickets" alongside stamps. No complex underwriting, no medical exams—just walk in, pay your premium, walk out insured.

The first policy, issued on April 1, 1864, went to James Bolter (Batterson's banker friend who'd inspired the whole venture). For two cents, Bolter received $1,000 of coverage for his walk from the post office to his home at 13 Buckingham Street—a journey of exactly four blocks. It was more publicity stunt than actuarial science, but it worked. Within months, Travelers was selling thousands of policies daily.

But Batterson wasn't content with simple accident tickets. By 1865, he'd introduced America's first annual accident policy—continuous coverage rather than trip-by-trip protection. This seemingly small innovation transformed the business model. Instead of volatile daily sales dependent on travel patterns, Travelers could build a predictable premium base.

The timing proved perfect. The Civil War's end in 1865 unleashed pent-up economic energy. Railroad construction resumed at breakneck pace. Industrial accidents soared as factories expanded. Travelers rode this wave, expanding from $200,000 in premiums in 1865 to over $1 million by 1870—a five-fold increase when most businesses struggled with post-war deflation.

Batterson's early underwriting philosophy shaped Travelers for generations: "Select carefully, price adequately, and never chase growth at the expense of profitability." While competitors offered rock-bottom prices to gain market share, Travelers maintained strict standards. They rejected applicants in obviously dangerous occupations, charged higher premiums for risky territories, and most importantly, paid claims promptly and fairly.

This last point—claims payment—became Travelers' secret weapon. In an era of financial panics and fly-by-night insurance schemes, Travelers built trust by doing something radical: actually paying when disasters struck. The company's response to the Great Chicago Fire of 1871, though they had minimal exposure, demonstrated this commitment. While other insurers delayed or disputed claims, Travelers paid immediately and in full.

By 1875, Travelers had expanded beyond accident insurance into life insurance, recognizing that the same middle-class Americans buying accident protection needed death benefits. The infrastructure was already there—the agents, the actuarial expertise, the claims-handling apparatus. More importantly, Batterson understood that selling multiple products to the same customer dramatically improved economics.

The foundation was set. From that two-cent policy in 1864, Travelers had built a multi-line insurance company with national reach, conservative underwriting, and a reputation for reliability. The next challenge would be adapting to the most transformative technology of the early 20th century: the automobile.

III. Expansion & Innovation: Building the Insurance Empire (1865–1920s)

The year was 1897, and Dr. Truman Martin of Buffalo, New York, had a problem. He'd just purchased one of those newfangled "horseless carriages"—a Oldsmobile, to be precise—but no insurance company would touch it. Fire insurers said it wasn't a building. Marine insurers said it wasn't a boat. Life insurers just laughed. Enter Gilbert Heublein, a Travelers agent who saw opportunity where others saw confusion. He wrote Dr. Martin a policy for $5,000 of liability coverage, premium: $11.25. America's first automobile insurance policy was born.

This moment crystallized Travelers' expansion strategy: identify emerging risks before competitors, price them intelligently, and build market share while others hesitated. Between 1897 and 1920, Travelers would transform from a specialty accident insurer into a full-spectrum insurance powerhouse, pioneering products that defined modern coverage.

The automobile revolution accelerated everything. In 1900, America had 8,000 registered vehicles. By 1910: 468,000. By 1920: 9.2 million. Each car represented multiple insurance needs—liability, collision, comprehensive, medical payments. Travelers didn't just write policies; they shaped the entire auto insurance framework. They introduced the concept of "comprehensive coverage" in 1898, protecting against theft, fire, and vandalism. They created the first automobile liability policy in 1899. They even pioneered what would become uninsured motorist coverage in 1902.

But the real test of Travelers' mettle came at 5:12 AM on April 18, 1906. The San Francisco earthquake—8.3 magnitude, followed by three days of fires—destroyed 80% of the city. Insurance claims totaled $235 million (roughly $7 billion today), bankrupting dozens of insurers. Travelers faced $1.5 million in claims, a staggering sum against their $3 million surplus.

CEO Sylvester Dunham made a decision that would define Travelers for a century: pay every claim, immediately, in full, no questions asked. While competitors disputed "fire vs. earthquake" causation (earthquake damage wasn't covered, fire was), Travelers simply paid. While others offered 50 cents on the dollar, Travelers paid 100%. The company's San Francisco agent, William Nelson, famously set up a tent in the ruins and started writing checks within days.

The financial hit was severe—Travelers' surplus dropped by half—but the reputational gain was priceless. California newspapers ran headlines praising "The Company That Paid." Agents reported that mentioning San Francisco closed sales from coast to coast. Within two years, Travelers had not only recovered its surplus but doubled its premium income.

This episode revealed something profound about insurance: trust was the product, coverage was just the manifestation. Batterson had understood this with prompt claims payment in the 1860s, but San Francisco elevated it to corporate religion. The company codified what became known as "The Travelers Way": conservative underwriting beforehand, generous claims handling afterward.

The 1910s brought systematic innovation in distribution. While competitors relied on exclusive agents (expensive) or direct mail (ineffective), Travelers pioneered the independent agency system. Rather than employing thousands of salespeople, Travelers contracted with independent insurance agencies who represented multiple carriers. This gave Travelers massive distribution—13,000 outlets by 1920—without the fixed costs.

The model required sophisticated support. Travelers created America's first comprehensive agent training program in 1912, complete with correspondence courses, regional seminars, and detailed underwriting manuals. They introduced graduated commission structures that rewarded quality over quantity. Most innovatively, they developed territory protection that gave successful agents exclusive rights to geographic areas, incentivizing long-term relationship building.

World War I accelerated institutional innovation. With millions of men deployed overseas, Travelers introduced war risk insurance for civilians, covering everything from submarine attacks on passenger ships to zeppelin bombings (yes, that was a real fear). They created specialized coverage for defense contractors, munitions manufacturers, and shipbuilders. Premium volume surged from $42 million in 1914 to $78 million by 1918.

But the most enduring innovation of this era was the red umbrella logo, introduced in 1870 but perfected in marketing during the 1920s. The story goes that Travelers' president noticed people huddling under awnings during rainstorms and thought: "Insurance should be like an umbrella—protection when you need it." The image resonated perfectly with post-WWI Americans seeking security in uncertain times.

By 1920, Travelers had become something unprecedented: a truly national, multi-line insurance company with dominant positions in life, accident, automobile, and liability coverage. Premium income exceeded $100 million annually. The company employed over 5,000 people and worked with 15,000 independent agents. From that first two-cent accident policy, an empire had emerged.

Yet success bred conservatism. As the Roaring Twenties gained steam, Travelers' leadership grew increasingly cautious. They avoided the stock market speculation that consumed competitors. They maintained strict underwriting standards while others loosened requirements to chase growth. They built reserves while others paid special dividends. This conservatism would seem foolish in 1928, prescient by 1930.

IV. Depression, War, and Modernization (1930s–1960s)

October 29, 1929. Black Tuesday. As panicked investors leaped from Wall Street windows and breadlines formed across America, Travelers' president Louis Butler sat in his Hartford office reviewing a remarkable document: the company's investment portfolio showed 92% government and high-grade corporate bonds, only 8% common stocks. While competitors had chased Jazz Age returns in equities and real estate speculation, Travelers had stayed boring. That boringness would prove salvation.

The Great Depression decimated the insurance industry. Between 1929 and 1933, over 40 insurance companies failed outright. Hundreds more merged or required emergency capital. Industry premium volume collapsed by 35%. Yet Travelers not only survived—it thrived, gaining market share as competitors retreated. The company's surplus actually grew from $47 million in 1929 to $52 million by 1933, even while paying full dividends and honoring every claim.

The secret wasn't just conservative investing. Throughout the 1920s, while others loosened standards to write more business, Travelers had maintained strict underwriting discipline. They'd refused to insure speculative ventures, rejected applicants with questionable finances, and avoided the exotic products competitors created to juice growth. When defaults cascaded through the economy, Travelers' loss ratios barely budged.

This stability allowed aggressive moves during the depths of the Depression. In 1931, as competitors pulled back from automobile insurance (fewer people could afford cars), Travelers doubled down, cutting rates 20% to maintain volume. They introduced payment plans allowing customers to pay premiums monthly rather than annually—revolutionary for the time. By 1935, Travelers had become America's largest automobile insurer, a position built on Depression-era market share gains.

The 1930s also saw Travelers pioneer what would become modern employee benefits. In 1936, they created the first group accident and health insurance plan for corporate employees. The logic was brilliant: insuring entire workforces eliminated adverse selection (only sick people buying coverage) while providing stable, predictable premium streams. General Motors signed on as the first major client, covering 50,000 workers. By 1940, Travelers covered over 1 million employees nationwide.

World War II transformed everything. Within weeks of Pearl Harbor, Travelers had mobilized its entire actuarial department to support the war effort. They administered life insurance for 2 million servicemen, managed disability benefits for defense workers, and created specialized coverage for everything from Liberty Ships to atomic research facilities (though they didn't know that's what Oak Ridge was at the time).

The war's deepest impact came through government partnerships. Travelers executives served on War Damage Corporation boards, designing insurance programs for civilian property damage from enemy attack. They helped create the National Service Life Insurance program, providing $10,000 policies for every servicemember. These experiences gave Travelers unparalleled expertise in large-scale program administration—capabilities that would prove invaluable in the post-war boom.

The post-war suburban explosion of the late 1940s and 1950s created unprecedented opportunity. Returning GIs, armed with VA loans and steady jobs, bought houses at record rates. Every new suburban home needed homeowners insurance. Every new family needed life insurance. Every new car needed auto coverage. Travelers' premium income exploded from $287 million in 1945 to $742 million by 1955.

But the real revolution was technological. In 1954, Travelers became the first insurance company to install an IBM 650 computer—a room-sized behemoth that could process 2,000 punch cards per minute. While executives joked about the $3 million "electronic brain," actuaries understood its transformative power. Complex rate calculations that took weeks by hand could be completed in hours. Risk correlations invisible to human analysis suddenly became clear.

The computer's first major application was revolutionary: personalized auto insurance rating. Instead of broad categories (urban/rural, male/female), Travelers could price based on dozens of variables simultaneously—age, driving record, vehicle type, usage patterns, geographic location. Competitors using manual rating systems simply couldn't match this precision. Travelers could offer lower prices to safe drivers while avoiding risky ones, a selection advantage that drove superior profitability.

By 1959, Travelers had installed IBM 705 systems in regional offices, creating America's first computerized insurance network. Agents could receive policy quotes in minutes rather than days. Claims could be processed in hours rather than weeks. The operational advantages were so significant that CEO Sterling Pierson declared: "The computer is not just a tool—it's our future competitive advantage."

The 1950s also marked Travelers' aggressive expansion into commercial lines. They created specialized divisions for different industries—manufacturing, retail, construction, transportation. Each division developed deep expertise in sector-specific risks. The construction division, for example, pioneered "wrap-up" insurance covering all contractors on major projects under a single policy, dramatically simplifying coverage for complex builds like the Interstate Highway System.

This specialization strategy peaked with the 1957 creation of the "Travelers Protective Association," offering comprehensive liability protection for businesses. Instead of buying separate policies for general liability, auto, workers' compensation, and property, companies could purchase integrated coverage with consistent terms and single-point claims handling. It was the first true "commercial package policy," a product category that would generate billions in premiums.

By 1960, Travelers had evolved from a Depression-era survivor into a modern insurance conglomerate. Premium income exceeded $1 billion annually. The company employed 18,000 people, operated 150 field offices, and worked with 20,000 independent agents. More importantly, it had built technological and operational capabilities that positioned it perfectly for the go-go 1960s.

Yet beneath this success lay strategic tension. Insurance was becoming commoditized. Competitors copied Travelers' innovations within months. State regulations limited pricing flexibility. Growth required either geographic expansion (expensive), acquisition (risky), or product innovation (uncertain). The conservative culture that had saved Travelers in the 1930s now seemed to constrain it. The stage was set for dramatic strategic shifts that would culminate in the most audacious merger in financial services history.

V. The Citicorp Merger Era: Financial Supermarket Dreams (1993–2002)

The mahogany conference table at the Four Seasons restaurant in Manhattan had witnessed countless Wall Street deals, but nothing quite like the conversation on February 24, 1997. Sandy Weill, the Brooklyn-born son of Polish immigrants who'd built Travelers into a financial services giant through sheer dealmaking prowess, sat across from John Reed, the cerebral technologist running Citicorp, the world's largest bank. Within hours, they'd shake hands on a $70 billion merger—the biggest in corporate history.

To understand this moment, we need to rewind to 1993. Travelers Insurance Company, the staid Hartford insurer we've been following, had just been acquired by Primerica, Sandy Weill's financial services conglomerate, for $4.2 billion. Weill saw in Travelers what others missed: a massive pool of investable premiums, a respected brand, and most importantly, a platform for his grand vision of a financial supermarket where customers could get insurance, banking, brokerage, and credit cards under one roof.

Weill was the anti-Travelers executive—aggressive where they were conservative, acquisitive where they were organic, Brooklyn brass where they were Hartford propriety. He'd already built and sold one financial empire (Shearson to American Express), and at age 60, he was building another. Between 1993 and 1997, he transformed Travelers from a property-casualty insurer into a diversified financial colossus, acquiring Shearson Lehman Brothers, Smith Barney, and Salomon Brothers. Revenue surged from $14 billion to $37 billion.

But banking—that was the missing piece. The Glass-Steagall Act of 1933 had separated commercial banking from investment banking and insurance for six decades. But Weill believed the walls were crumbling. Foreign competitors like Deutsche Bank and UBS faced no such restrictions. American regulators were increasingly sympathetic to "modernization." Weill decided to force the issue.

The Citicorp merger announcement on April 6, 1998, shocked everyone. Two companies with combined assets of $700 billion, 180,000 employees, and operations in 100 countries would merge as equals. Reed and Weill would be co-CEOs. The new Citigroup would be the world's largest financial services company, serving 100 million customers. The stock market loved it—both stocks soared 25% on announcement.

But there was a massive problem: the merger was technically illegal. Glass-Steagall prohibited banks from owning insurance companies. Weill and Reed were betting Congress would change the law before the Fed's two-year grace period expired. It was audacious, arrogant, and classic Weill.

The lobbying campaign was unprecedented. Citigroup spent $12 million on lobbying in 1998-99, deployed armies of executives to Washington, and mobilized customers to contact representatives. The argument was simple: American finance needed scale to compete globally. The opposition was fierce: community banks feared being crushed, consumer advocates worried about privacy, insurance agents dreaded bank competition.

The cultural integration proved even harder than regulatory approval. Citicorp's bankers, who prided themselves on intellectual rigor and global sophistication, looked down on Travelers' insurance agents and Smith Barney brokers as unsophisticated salespeople. Travelers' executives, who'd built businesses through entrepreneurial hustle, viewed Citibankers as entitled bureaucrats.

The co-CEO structure lasted exactly 18 months. By December 1999, Reed was gone, Weill had won, and the insurance guys were in charge of the world's largest bank. The Gramm-Leach-Bliley Act, signed November 12, 1999, finally repealed Glass-Steagall, retroactively blessing the merger. Weill had his financial supermarket.

But did it work? The numbers suggested yes—sort of. Citigroup earned $13.5 billion in 2000, making it America's most profitable company. The stock price doubled between 1998 and 2000. Cross-selling initiatives showed promise: 23% of Smith Barney clients bought Travelers insurance, 15% of insurance customers opened Citi bank accounts.

Yet beneath the surface, fundamental tensions festered. Insurance runs on long-term thinking—underwriting discipline, careful risk selection, patient capital accumulation. Investment banking thrives on velocity—quick trades, aggressive risks, quarterly bonuses. Travelers' insurance executives grew increasingly frustrated watching Salomon traders earn multiples of their compensation while taking risks that could destroy decades of underwriting profits.

The property-casualty business, Travelers' historic core, suffered from neglect. While Weill focused on investment banking and consumer finance, competitors like AIG and Chubb cherry-picked Travelers' best commercial accounts. Combined ratios deteriorated from 96% in 1997 to 104% in 2001—the business was losing money on underwriting. Market share in commercial lines dropped from 8% to 6%.

September 11, 2001, crystallized the strategic confusion. Travelers faced $500 million in World Trade Center claims—manageable for an insurer, devastating when Wall Street expected quarterly earnings growth. Weill publicly complained about the insurance division's "volatility," seemingly forgetting that insuring catastrophes was literally the business model.

By early 2002, the financial supermarket dream was dying. Cross-selling had plateaued—customers didn't actually want their insurance agent to be their stockbroker. Regulatory oversight was nightmarish—banking, securities, and insurance regulators all claimed jurisdiction. Most fundamentally, the cultures never meshed. Insurance executives who'd spent careers thinking in decades couldn't adapt to investment bankers focused on daily P&L.

On January 31, 2002, Citigroup announced it would spin off Travelers Property Casualty as an independent company. The official reason was "unlocking shareholder value." The real reason was simpler: oil and water don't mix, no matter how hard you shake the bottle. The IPO in March 2002 raised $3.9 billion, valuing Travelers at $15 billion—less than half what Weill had implied it was worth during the merger.

The Citigroup era seemed like a costly detour, but it taught invaluable lessons. Insurance isn't just another financial service—it's a distinct business with unique economics, risks, and culture. The patient accumulation of premiums and careful risk selection that built Travelers over 140 years couldn't be subordinated to quarterly earnings targets. Most importantly, trying to be everything to everyone often means being nothing to anyone.

VI. The St. Paul Merger & Modern Travelers (2004–2010)

Jay Fishman didn't look like an insurance revolutionary. Soft-spoken, bespectacled, partial to quiet sweater vests rather than power suits, the 51-year-old CEO who took charge of the newly independent Travelers in 2002 seemed more professor than corporate titan. But beneath that mild exterior burned fierce ambition: to rebuild Travelers into America's premier property-casualty insurer. His first move would stun the industry.

On November 17, 2003, Fishman announced Travelers would merge with The St. Paul Companies in a $16 billion deal. St. Paul wasn't just any insurer—it was older than Travelers (founded 1853), larger in commercial lines, and deeply embedded in specialized markets like medical malpractice, surety bonds, and technology errors-and-omissions coverage. The combination would create America's second-largest commercial insurer, trailing only AIG.

The strategic logic was compelling. Travelers had strong middle-market commercial capabilities but lacked specialty expertise. St. Paul had world-class specialty underwriting but weak distribution. Together, they'd offer comprehensive commercial solutions through Travelers' 11,000 independent agents. The projected synergies—$400 million annually—came from consolidating operations, not the mythical "cross-selling" that doomed the Citi merger.

But Fishman's genius lay in the integration philosophy: "preserve what makes each company special while eliminating what doesn't." Unlike typical mergers that forced uniform systems and processes, Fishman maintained separate underwriting teams for different specialties. St. Paul's medical malpractice experts stayed in Minneapolis. Travelers' construction specialists remained in Hartford. The only mandate: share data, best practices, and distribution channels.

The timing proved perfect. Commercial insurance was entering a "hard market"—industry-speak for rising prices after years of ruinous competition. September 11th had destroyed $40 billion of industry capital. Hurricane Katrina in 2005 would destroy another $60 billion. Reinsurance costs soared. Suddenly, disciplined underwriters could name their price. Travelers' gross written premiums surged from $17 billion in 2004 to $24 billion by 2007.

Fishman's management philosophy, shaped by watching the Citigroup dysfunction, emphasized long-term thinking over quarterly earnings. He eliminated earnings guidance, telling Wall Street: "Insurance is inherently volatile. Pretending otherwise leads to stupid decisions." He instituted "through-the-cycle" compensation, where bonuses reflected five-year average returns, not annual performance. Most radically, he created a "risk committee" with veto power over any transaction, no matter how profitable, if risks seemed mispriced.

This discipline would prove invaluable as the financial system careened toward disaster. By 2006, Wall Street banks were packaging increasingly exotic risks into securities, desperately seeking insurance coverage to make them saleable. AIG's Financial Products division famously wrote $500 billion in credit default swaps. Other insurers dove into mortgage insurance, financial guarantees, and structured products.

Travelers said no to all of it. Fishman's risk committee analyzed these products and concluded they violated basic insurance principles: risks weren't independent (mortgage defaults would cascade), losses weren't capped (financial contagion could explode liabilities), and pricing models relied on recent history (housing had never declined nationally, until it did). The opportunity cost seemed enormous—AIG's Financial Products generated $3 billion in profits in 2005 alone—but Fishman held firm.

The decision to avoid financial engineering went deeper than risk management. Fishman believed insurance companies should stick to actual insurance—protecting businesses and individuals from real-world perils, not enabling Wall Street speculation. In a 2007 speech that now seems prophetic, he said: "We're in the business of helping people recover from disasters, not creating them."

When disaster struck in September 2008, the wisdom became obvious. Lehman Brothers collapsed. AIG required a $182 billion government bailout. The Hartford, Genworth, and Lincoln Financial teetered on bankruptcy. Travelers? They reported a modest profit, maintained their dividend, and never touched government assistance. Their stock fell 40% (everything did), but recovered within 18 months. AIG wouldn't recover its 2007 stock price for a decade.

The crisis created opportunity. As competitors retreated, Travelers expanded. They hired 500 underwriters from AIG's imploding commercial division. They acquired clients fleeing troubled carriers. They raised prices 15-20% as capacity disappeared. Between 2008 and 2010, Travelers gained three points of commercial market share—massive movement in a typically static industry.

The crowning validation came June 8, 2009: Travelers replaced General Motors in the Dow Jones Industrial Average. GM, symbol of American industrial might, had declared bankruptcy. Travelers, the company that started insuring horse-and-buggy accidents, now represented American business resilience. The symbolism was perfect—old economy stability replacing new economy excess.

Fishman's post-crisis strategy focused on technology and data analytics. While competitors had spent the 2000s on financial engineering, Travelers had quietly built sophisticated pricing models, claims databases, and risk assessment tools. They could price workers' compensation claims 20% more accurately than competitors using traditional methods. Their catastrophe models incorporated climate data, building codes, and geographic concentration to predict hurricane losses within 5% accuracy.

The human element remained crucial. Fishman instituted "Travelers University," a comprehensive training program for underwriters, claims adjusters, and agents. New underwriters spent two years in rotational assignments before specializing. Claims adjusters learned not just coverage interpretation but empathy and communication. The message was clear: in a commoditized industry, service and expertise created differentiation.

By 2010, the transformation was complete. Travelers had emerged from the financial crisis as America's most respected property-casualty insurer. Return on equity averaged 14% from 2004-2010, despite the crisis. The combined ratio stayed below 95%, indicating profitable underwriting even before investment income. Market capitalization reached $28 billion, triple the 2002 spinoff value.

But Fishman's greatest achievement was cultural. He'd restored the conservative underwriting discipline that defined Travelers' first century while embracing the technology and analytics necessary for the next. He'd proven that insurance companies could succeed by actually doing insurance well, not by pretending to be investment banks. Most importantly, he'd demonstrated that in a world of quarterly capitalism, long-term thinking still won.

VII. The Digital Transformation & Modern Era (2010s–Today)

The smartphone screen glowed at 2 AM in Alan Schnitzer's Hartford bedroom, displaying another catastrophe alert: Hurricane Milton, headed for Florida's Gulf Coast, potential losses in the billions. As CEO of Travelers since 2015, Schnitzer had seen this movie before—the scramble to deploy claims adjusters, the models predicting losses, the investor calls demanding explanations. But this time was different. The company had just posted its best bottom-line during the worst catastrophe year in U.S. history in 2024: $5 billion of net income.

How did a 170-year-old insurance company built on paper policies and human underwriters transform itself into a digital powerhouse that could thrive amid climate chaos? The answer lies in one of the most comprehensive technological transformations in insurance history—one that began quietly in 2010 under Jay Fishman's steady leadership and accelerated dramatically under Schnitzer's vision of "perform, transform, and deliver on the Travelers Promise."

The journey from Fishman's analog insurance company to Schnitzer's AI-powered enterprise represents more than technological evolution—it's a masterclass in how established financial institutions can reinvent themselves without losing their soul. Between 2017 and 2024, Travelers simultaneously increased technology spending while improving its strategic mix, more than doubling investments in cyber, analytics, and AI over eight years. The company poured more than $1.5 billion into IT in 2023 alone, with nearly half directed to strategic initiatives.

But let's rewind to 2015, when Schnitzer, a former Simpson Thacher lawyer who'd advised on the St. Paul merger, took the helm. The insurance industry was under siege from multiple fronts. InsureTech startups like Lemonade and Root promised to "disrupt" traditional insurers with AI-driven underwriting and mobile-first experiences. Climate change was accelerating catastrophe losses at terrifying rates. And a new generation of customers expected Amazon-like digital experiences from their insurance providers.

Schnitzer's response was counterintuitive: embrace the disruption while doubling down on Travelers' traditional strengths. His philosophy centered on three pillars: perform (executing long-term financial strategy), transform (technological innovation), and making good on the Travelers Promise (being there for customers in their time of need). This wasn't corporate speak—it was a blueprint for survival in the digital age.

The transformation started with data. Travelers had been collecting information for 170 years, but most of it sat in silos—claims data separate from underwriting, personal lines disconnected from commercial, historical losses divorced from forward-looking models. Schnitzer authorized a massive data lake project, consolidating billions of data points into unified, AI-ready repositories. The cost: hundreds of millions. The payoff: the ability to price risk with unprecedented precision.

Consider IntelliDrive, Travelers' telematics program launched in 2017 and continuously refined since. The smartphone app captures driving behaviors of enrolled drivers—braking, acceleration, speed, time of day, and distraction—rewarding safer driving with savings on auto insurance up to 30%. But the real innovation wasn't the technology—it was the behavioral science. The 90-day program scores driving performance, with safer drivers eligible for 20% or 30% savings while riskier driving results in higher premiums—incentivizing safer driving as a win-win that gives customers more control over rates, helps agents offer competitive products, and allows insurers to price risk more accurately.

The program's sophistication goes deeper than simple tracking. IntelliDrive captures information about driving habits including distraction—any handheld interaction with the phone while driving negatively impacts scores, including in-hand calls, texting, typing and tapping, though vehicle infotainment systems and Bluetooth calls don't count against drivers. By 2024, the program had expanded into multiple variants—IntelliDrive 365 for continuous monitoring, IntelliDrivePlus for mileage-based pricing—each tailored to different customer segments and state regulations.

Climate change represented the existential challenge. A decade ago, Travelers' leadership decided to build separate teams for every peril—hurricane, wind and hail, and wildfire teams—while investing in hiring data scientists, climatologists, environmental engineers and professionals in various disciplines beyond meteorology. This wasn't incremental improvement; it was wholesale reimagination of catastrophe management.

The results spoke volumes. Before implementing this strategy, Travelers' catastrophe losses were consistent with market share, but in the decade since, they've meaningfully outperformed while continuing to grow the book. When asked about this success, Schnitzer revealed the deeper philosophy: "Running this business for uncertainty is just a way of life for us."

The company's approach to climate modeling exemplifies this uncertainty management. Travelers uses various analyses and methods to evaluate climate-related risks and make underwriting, pricing and reinsurance decisions designed to manage the company's exposure. But unlike competitors who relied solely on historical data, Travelers invested in forward-looking climate models that incorporated tipping points, feedback loops, and cascade effects that traditional actuarial models missed.

Digital transformation extended beyond risk assessment into customer experience. The traditional claims process—call your agent, wait for an adjuster, negotiate settlements, receive checks—took weeks. Travelers' digital claims platform, powered by AI image recognition and automated workflows, could process simple claims in hours. A customer could photograph hail damage on their car, submit through the app, and receive direct deposit within 24 hours. No adjuster visit required.

But Schnitzer understood that pure digital plays missed something crucial: the human element when disasters strike. During record-breaking natural catastrophes, Travelers' team of more than 30,000 employees rose to the occasion with countless individual acts of excellence—helping families and businesses recover, building resilience in affected communities. Technology enhanced but didn't replace the human touch.

The cyber insurance opportunity showcased Travelers' ability to create entirely new business lines through technology. The 2024 Travelers Risk Index revealed unprecedented concern about cyber threats, with the need for businesses to bolster cybersecurity risk management measures becoming critical. Travelers didn't just sell cyber policies; they built comprehensive risk management ecosystems.

Cyber threats topped the 2024 Travelers Risk Index as the main concern for 62% of business participants, marking the fourth time in six years. The company's response went beyond traditional insurance. Through partnerships with companies like HCLTech, Travelers offered pre-breach services including risk assessments, employee training, and ongoing consulting. Post-breach, they provided immediate access to cyber breach coaches, forensics investigators, and crisis communications professionals.

The 2024 acquisition of Corvus Insurance, a cyber-focused MGA using AI for underwriting, signaled Travelers' commitment to leading in this space. Travelers acquired Corvus in early 2024, with Corvus continuing as a wholly owned subsidiary building safer world through insurance products that reduce cyber risk for policyholders. Rather than compete with InsureTech, Travelers absorbed their innovations while providing the capital and distribution they lacked.

Artificial intelligence became the force multiplier across all operations. In 2023, Travelers spent $1.5 billion on technology, including meaningful investments in cutting-edge AI capabilities built on modern cloud technology, aimed at extending risk expertise, providing great experiences, and optimizing productivity. But unlike tech companies that deployed AI indiscriminately, Travelers focused on specific, high-impact use cases.

Underwriting transformation showcased this targeted approach. Traditional commercial underwriting required weeks of document review, site inspections, and manual risk assessment. Travelers' AI-powered platform could ingest thousands of pages of submission documents, extract relevant information, identify missing data, and generate preliminary quotes in minutes. Human underwriters still made final decisions, but AI eliminated 80% of routine tasks, allowing focus on complex risk evaluation.

The company's approach to generative AI proved particularly sophisticated. Rather than rushing to deploy ChatGPT-style interfaces, Travelers built proprietary models trained on their vast historical data. These models could generate first drafts of policy language, claims correspondence, and risk assessments, always with human review. The goal wasn't replacing professionals but amplifying their capabilities.

Leadership philosophy underpinned technological success. Schnitzer encouraged young professionals to read newspapers daily, including columnists with opposing political views, while rejecting cancel culture and encouraging the sharing of ideas. This intellectual openness extended to technology adoption—willing to experiment, quick to pivot, but always grounded in insurance fundamentals.

The financial results validated the strategy. Net income increased 67% year-over-year to nearly $5 billion in 2024, with annual revenues growing 12% to more than $46 billion. But more importantly, Travelers achieved something rare: technological transformation without cultural destruction. The company that started insuring train travelers in 1864 had become a digital leader without forgetting its purpose.

Competition from InsureTech forced continuous innovation. Companies like Lemonade promised instant quotes, AI-driven claims, and radical transparency. Root used smartphone driving data to price policies. Metromile charged by the mile driven. Each challenged different aspects of traditional insurance, forcing Travelers to respond strategically rather than reactively.

Travelers' response was nuanced. Where InsureTechs excelled at user experience, Travelers matched them while leveraging superior data and capital. Where startups promised AI-driven efficiency, Travelers delivered it at scale. Most importantly, when catastrophes struck and InsureTechs struggled with reinsurance costs and claims surges, Travelers' 170 years of experience proved invaluable.

The distribution strategy balanced digital innovation with traditional strengths. While pure digital players struggled with customer acquisition costs—sometimes spending $500 to acquire customers generating $300 in annual premiums—Travelers leveraged its 11,000 independent agents as digital enablers. Agents received AI-powered tools for quoting, binding, and servicing policies, combining high-tech efficiency with high-touch relationships.

Cloud transformation enabled this hybrid model. Moving from on-premises data centers to cloud infrastructure wasn't just about cost savings—it enabled real-time data sharing between agents, underwriters, and claims adjusters. An agent in Phoenix could instantly access underwriting decisions made in Hartford, claims history from Chicago, and catastrophe modeling from San Francisco.

The pandemic accelerated digital adoption by five years in five months. Suddenly, property inspections needed to happen virtually, claims had to be settled remotely, and agents had to sell policies without face-to-face meetings. Travelers' prior technology investments paid immediate dividends. While competitors scrambled to enable remote work, Travelers seamlessly shifted 30,000 employees home without missing a beat.

But technology also brought new risks. Cyber attacks on insurers increased 300% between 2020 and 2024. Nation-state actors targeted insurers' vast data repositories. Ransomware groups recognized insurance companies as prime targets—rich enough to pay ransoms, critical enough to need rapid recovery. Travelers' response involved not just defensive cybersecurity but offensive threat hunting, partnering with government agencies to identify and neutralize threats before they materialized.

Climate technology became increasingly critical. Travelers, one of California's largest home insurers, won approval to increase California rates by an average of 15% in 2024 as catastrophe losses increased from $1.85 billion in 2021 to $2.99 billion in 2023. But rate increases alone wouldn't solve climate risk. Travelers invested in parametric insurance products that paid automatically when specific weather conditions occurred, eliminating claims processes entirely for certain events.

The company also pioneered resilience services, using IoT sensors to detect water leaks before they became claims, providing wildfire-resistant building materials at discounted rates, and offering premium credits for climate adaptation measures. This shifted the business model from purely transferring risk to actively reducing it—a fundamental reimagination of insurance's societal role.

Regulatory technology became a differentiator as compliance complexity exploded. With 50 state insurance departments, each with unique rules, maintaining compliance manually was impossible. Travelers built RegTech platforms that automatically updated policy forms for regulatory changes, flagged potential compliance issues, and generated required filings. What once required armies of compliance officers now happened algorithmically.

The investment community initially questioned the massive technology spending. Why pour billions into IT when that money could be returned to shareholders? Schnitzer's answer was blunt: "Some of the competitive advantages and capabilities that have fueled our achievements over the past decade won't necessarily be the same advantages and capabilities we'll need to lead for the next decade. That's why we're focused on transformation."

By 2024, doubters were silenced. Travelers' combined ratio consistently beat industry averages by 5-10 points. Return on equity exceeded 14% even in heavy catastrophe years. The stock price tripled between 2015 and 2024, dramatically outperforming both insurance peers and the broader market. Technology investment had become competitive moat.

The future promises even more dramatic change. Autonomous vehicles will eliminate most auto accidents—great for society, existential for auto insurers generating 40% of premiums from that line. Travelers' response involves pivoting toward cyber coverage for connected vehicles, liability insurance for AI decisions, and new products for mobility-as-a-service providers.

Quantum computing looms as both opportunity and threat. The ability to break current encryption could devastate the financial system, but quantum-resistant algorithms and quantum-powered risk modeling could provide unprecedented competitive advantages. Travelers partnered with IBM's quantum research division, preparing for a post-quantum world while maintaining current security.

Blockchain technology, overhyped in the 2010s, found practical applications in the 2020s. Travelers participated in industry consortiums building blockchain-based claims processing, reducing fraud through immutable audit trails and enabling instant payments through smart contracts. The technology that promised to eliminate intermediaries instead made them more efficient.

Environmental, Social, and Governance (ESG) considerations increasingly influenced technology decisions. AI models needed to avoid discriminatory bias. Data centers needed renewable power. Supply chains required carbon accounting. Travelers integrated ESG metrics into every technology investment, recognizing that sustainable technology was both ethical imperative and business necessity.

The talent war intensified as every company became a technology company. Travelers competed with Google and Amazon for data scientists, with startups for software engineers, with consulting firms for AI specialists. The response involved not just competitive compensation but cultural transformation—creating an environment where technologists could innovate within insurance rather than despite it.

Partnerships became force multipliers. Rather than building everything internally, Travelers partnered with Microsoft for cloud infrastructure, Palantir for data analytics, and numerous startups for specialized capabilities. "When we think about our continued success, we have to do three things really well: perform, transform and keep the Travelers Promise. Performing means successfully executing our long-term financial strategy to generate industry-leading returns on equity over time."

The transformation continues accelerating. What seemed revolutionary in 2020—AI underwriting, digital claims, telematics pricing—became table stakes by 2024. The next frontier involves predictive prevention (stopping losses before they occur), embedded insurance (coverage integrated seamlessly into other products), and dynamic pricing (premiums adjusting real-time based on risk factors).

Yet through all this change, constants remained. Conservative underwriting discipline, built over 170 years, guided AI models. The mutual trust between Travelers and its agents, cultivated through generations, enabled digital distribution. The promise to be there when customers needed them most, established by James Batterson in 1864, motivated every innovation.

Standing in that Hartford office at 2 AM, monitoring Hurricane Milton's approach, Alan Schnitzer embodied this duality. His smartphone displayed real-time catastrophe models powered by supercomputers processing petabytes of weather data. But his concerns remained fundamentally human: Were claims adjusters safely positioned? Did customers have evacuation resources? Would Travelers honor its promise when dawn broke over the devastation?

The answer, built on 170 years of trust and a decade of transformation, was unequivocal: yes. Technology had made Travelers faster, smarter, more efficient. But the company's soul—that original promise to be there when disaster strikes—remained unchanged. In an industry where one catastrophe can destroy decades of profits, that combination of digital capability and human purpose wasn't just competitive advantage. It was survival itself.

VIII. Playbook: Business & Investing Lessons

The conference room on the 24th floor of Travelers Tower overlooks Hartford's skyline, a city that owes much of its prosperity to insurance money. It's here that Alan Schnitzer holds his quarterly "deep dive" sessions with institutional investors, walking them through Travelers' playbook with the patience of a professor and the precision of an actuary. "Insurance," he often begins, "is the only business where you sell your product before you know what it costs." That fundamental uncertainty, and how Travelers manages it better than almost anyone, contains profound lessons for both operators and investors.

The Power of Conservative Underwriting Through Cycles

Insurance markets move in cycles as predictable as tides and twice as powerful. Soft markets see prices fall as insurers chase growth, accepting marginal risks at inadequate prices. Hard markets follow inevitably when losses mount, capital flees, and survivors can name their price. Most insurers surf these waves, growing aggressively in soft markets and retrenching in hard ones. Travelers does the opposite.

During the soft market of 2014-2017, when competitors dropped prices 20-30% chasing market share, Travelers actually shrank its book in certain lines. Commercial auto, where competitors were practically giving away coverage? Travelers walked away from $500 million in premiums. Professional liability during the SPAC boom? Thanks, but no thanks. The stock market punished this discipline—why wasn't Travelers growing like Progressive or Chubb?

Then 2018-2020 happened. Social inflation exploded. Nuclear verdicts—jury awards exceeding $10 million—increased 300%. COVID-19 triggered thousands of business interruption claims. Competitors who'd chased growth at any price faced combined ratios above 110%, losing money on every dollar of premium. Travelers? Their combined ratio stayed below 100% throughout, generating underwriting profits while competitors bled capital.

The lesson transcends insurance: price discipline beats growth theater every time. Whether you're running a software company, a restaurant chain, or an investment portfolio, the temptation to sacrifice margins for growth is ever-present. Travelers proves that saying no to bad business, even when everyone else is saying yes, creates long-term value. Warren Buffett captured this perfectly: "It's only when the tide goes out that you learn who's been swimming naked."

Distribution Advantages: The 13,000-Agent Moat

Travelers' network of 13,000 independent agents seems anachronistic in the digital age. Why maintain expensive human distribution when Geico sells direct and Lemonade sells through apps? The answer reveals a profound truth about competitive advantages: the best moats are those competitors can't cross even if they want to.

Independent agents aren't just distribution—they're local risk assessors, customer advocates, and relationship managers rolled into one. When a tornado devastates a town, the local Travelers agent is often at the scene before adjusters arrive, providing immediate comfort and initiating claims. When a business needs complex coverage combining property, liability, cyber, and management protection, an experienced agent structures solutions no algorithm can match.

The economics are compelling. Customer acquisition cost through agents runs about $150 per policy versus $400+ for direct digital marketing. Retention rates exceed 90% with agents versus 80% for direct. Lifetime customer value through agents is 2.5x higher. Most importantly, agents provide free market intelligence—which risks to avoid, which prices competitors offer, which customers are shopping coverage.

But here's the kicker: this distribution advantage is essentially unreplicable. Progressive spent two decades and billions of dollars trying to build an agency network to match their direct business. They gave up. Lemonade promised to eliminate agents entirely. They're now partnering with brokers. Even Amazon, with infinite capital and technical capability, couldn't crack insurance distribution and shut down Amazon Protect.

The investing lesson is powerful: sustainable competitive advantages rarely come from things you can buy (technology, talent, assets) but from things you must build over time (relationships, trust, culture). Travelers' agency network, cultivated over 170 years, provides pricing power, customer stickiness, and market intelligence that no amount of venture capital can replicate.

Risk Selection and Pricing Discipline

In Travelers' underwriting training program, new associates learn a simple mantra: "There are no bad risks, only bad prices." This sounds obvious until you realize most insurers do the opposite—they decide what risks to take, then price them to hit revenue targets. Travelers prices first, then decides whether to write the business.

Consider their approach to coastal property. After Hurricane Katrina, many insurers fled coastal markets entirely. State Farm stopped writing new homeowners policies in Florida. Allstate pulled back from Long Island. Travelers stayed but transformed their approach. They developed proprietary storm surge models accurate to individual properties. They priced policies not by ZIP code but by exact elevation, distance from water, and building construction. A house 100 feet from the beach might pay 10x more than one 500 feet away.

This granular pricing revealed surprising truths. Many "high-risk" coastal properties were actually profitable at the right price. Many "safe" inland properties were underpriced relative to flood risk. By pricing accurately rather than avoiding broadly, Travelers maintained profitable coastal exposure while competitors either fled markets or accumulated catastrophic losses.

The pricing discipline extends to timing. Travelers typically leads price increases, accepting temporary market share loss for long-term profitability. In 2019, they raised commercial rates 7% while the market averaged 3%. Agents screamed. Customers defected. The stock fell 10%. By 2021, competitors were raising prices 15% to catch up while Travelers' early moves had already earned through. The lesson: price for where the market is going, not where it is.

Capital Management and the Dividend Aristocrat Status

Travelers has increased its dividend for 20 consecutive years, earning "Dividend Aristocrat" status. During the 2008 financial crisis, when Bank of America eliminated its dividend and AIG needed bailouts, Travelers raised its payout. During COVID-19, when regulators pressured insurers to conserve capital, Travelers maintained its dividend while growing it at the next opportunity.

This isn't financial engineering—it's profound discipline. Insurance is inherently volatile. A single hurricane can erase years of profits. Yet Travelers generates such consistent cash flow that they've never cut their dividend since going public. How? By managing capital like a three-dimensional chess player.

First dimension: underwriting discipline ensures base profitability regardless of catastrophes. Even in 2017, with Hurricanes Harvey, Irma, and Maria, Travelers generated positive underwriting income. Second dimension: investment portfolio management. With $75 billion in fixed income securities, each 1% rise in rates generates $750 million in annual income. Third dimension: dynamic reinsurance. Travelers buys protection for extreme events but retains moderate risks, optimizing the cost-benefit of risk transfer.

The capital allocation framework is elegantly simple. First, maintain fortress balance sheet strength (AA rating, 2x regulatory minimum capital). Second, invest in the business for 15%+ returns. Third, pay growing dividends. Fourth, buy back stock when it trades below 1.5x book value. This hierarchy never changes regardless of market conditions, CEO preferences, or investor pressure.

The Insurance Float Advantage

Here's the magic of insurance economics: customers pay premiums upfront, claims get paid later. That timing difference creates "float"—money Travelers invests while waiting to pay claims. With $90 billion in reserves, earning even 4% generates $3.6 billion in annual investment income—pure profit if underwriting breaks even.

But Travelers optimizes float beyond simple investment. They structure policies to accelerate premium collection—offering discounts for annual payment versus monthly. They manage claims to optimize timing—settling quickly when advantageous, litigating when appropriate. They match asset duration to liability duration—short bonds for auto claims paid within months, long bonds for liability claims resolved over years.

The float advantage compounds over time. Investment income funds technology improvements, which enhance underwriting, which grows profitable premiums, which increases float, which generates more investment income. It's a virtuous cycle that accelerates with scale. This is why subscale insurers struggle—without sufficient float, they can't invest in capabilities needed to generate profitable growth.

Warren Buffett built Berkshire Hathaway on insurance float, calling it "free money" when underwriting is profitable. Travelers has achieved this holy grail—combined ratios below 100% plus billions in investment income—for most of the past decade. Few businesses offer this double-barreled profit mechanism.

Culture as Competitive Advantage

Walk Travelers' Hartford headquarters and you'll notice something unusual for a financial services company: people stay forever. Average tenure exceeds 15 years. Senior executives often spend entire careers there. The head of claims started as an adjuster. The chief underwriting officer began as an actuarial analyst. This continuity creates something invaluable: institutional memory.

When Hurricane Sandy approached in 2012, Travelers executives remembered Hurricane Gloria in 1985. They knew which neighborhoods would flood first, which contractors could mobilize fastest, which claims patterns would emerge. This experience-based pattern recognition beats any AI model. When cyber risks emerged, underwriters who'd seen the birth of auto insurance, product liability, and employment practices coverage knew how to price uncertainty.

The culture emphasizes long-term thinking over quarterly earnings. Bonuses vest over five years. Promotions reward decade-long performance, not annual spikes. Strategic planning horizons extend to 2040. This temporal alignment shapes every decision. Why invest in climate modeling that won't pay off for years? Because executives will still be here to benefit. Why maintain pricing discipline during soft markets? Because the same team will navigate the hard market.

Risk management permeates the culture beyond underwriting. Travelers maintains multiple headquarters—Hartford, Minnesota, and New York—ensuring continuity if disaster strikes one location. Critical systems have triple redundancy. Every process has documented backups. The company could lose any 100 employees and continue operating seamlessly. This resilience mindset, born from insuring others' disasters, makes Travelers antifragile.

The Technology Integration Paradox

While InsureTech startups promised to revolutionize insurance through technology, Travelers quietly built superior capabilities without fanfare. They spend $1.5 billion annually on technology—more than most InsureTech companies are worth—but integrate it invisibly into traditional operations.

The key insight: technology amplifies expertise, it doesn't replace it. Travelers' AI models are trained by underwriters with 30 years of experience, not fresh computer science graduates. Their catastrophe models incorporate adjuster observations from thousands of storms, not just meteorological data. Their fraud detection systems combine algorithmic pattern recognition with investigator intuition.

This human-machine collaboration extends throughout operations. Underwriters use AI to process routine submissions but personally handle complex risks. Claims adjusters employ computer vision for standard damages but physically inspect unusual losses. Agents leverage digital tools for quotes but build relationships face-to-face. Technology makes everyone more effective without making anyone redundant.

The Paradox of Conservatism and Innovation

Travelers embodies a paradox: deeply conservative in risk-taking, radically innovative in risk assessment. They'll walk away from profitable business if risks seem mispriced, yet invest billions in unproven technologies. They maintain Depression-era underwriting standards while deploying bleeding-edge AI. They honor 170-year-old promises while reimagining insurance for autonomous vehicles.

This paradox resolves through a simple framework: be conservative with capital, aggressive with capabilities. Never risk the franchise on single bets, but constantly experiment with small tests. Maintain fortress balance sheet strength while investing heavily in future competencies. Honor traditional values while embracing modern methods.

The framework manifests in specific practices. New products launch in single states before national rollout. Technology investments follow 90-day proof-of-concept sprints. Acquisitions rarely exceed $1 billion, avoiding "bet the company" deals. Innovation happens through thousands of small experiments rather than massive transformations.

The Compound Effect of Incremental Advantages

Travelers doesn't dominate through single breakthrough advantages but through dozens of small edges that compound into insurmountable leads. Their claims costs run 2% lower through better fraud detection. Their acquisition costs are 3% lower through agent efficiency. Their retention rates exceed peers by 5% through superior service. Their investment yields beat benchmarks by 0.5% through duration management.

Individually, these advantages seem modest. Collectively, they transform economics. A combined ratio 5 points better than competitors means Travelers earns 10% return on equity while peers earn 5%. Compounded over decades, that difference creates enormous value. A dollar invested in Travelers in 2000 is worth $8 today versus $3 for insurance industry indices.

This accumulation of marginal gains resembles Toyota's kaizen philosophy—continuous small improvements rather than revolutionary changes. Every quarter, Travelers identifies dozens of optimization opportunities. Reduce claims processing time by one day. Improve pricing accuracy by 1%. Increase agent productivity by 2%. These gains, invisible individually, compound into competitive dominance.

The Ultimate Lesson: Time Horizon Arbitrage

The deepest lesson from Travelers' playbook involves time horizons. Public markets obsess over quarterly earnings. Competitors chase annual growth targets. Travelers thinks in decades. This temporal arbitrage—accepting short-term pain for long-term gain—creates most of their advantages.

Consider their response to climate change. While competitors debate whether warming is real, Travelers has spent a decade building climate resilience. They've sacrificed billions in premiums by avoiding risky coastal properties. They've invested hundreds of millions in modeling capabilities without immediate return. Yet when climate losses accelerate—and they will—Travelers will capture outsized profits while competitors face existential threats.

Or examine their talent development. Travelers spends more on training than any insurance peer—over $100 million annually. New underwriters remain unproductive for two years while learning. The company maintains higher staffing levels to enable mentorship. These investments destroy short-term margins but create long-term expertise advantages.

For investors, the lesson is profound: the best investments often look mediocre in the short term. Travelers' stock underperformed from 2015-2018 as they maintained pricing discipline. It then doubled from 2019-2024 as that discipline paid off. Patient capital, aligned with management thinking in decades, captures value invisible to quarterly traders.

For operators, the message is similar: building sustainable competitive advantages requires accepting periods of underperformance. Every moat—whether distribution networks, underwriting expertise, or technological capabilities—takes years to construct during which returns disappoint. But once built, these moats generate excess returns for decades.

Standing in that Hartford conference room, overlooking a city built on insurance profits, the full picture emerges. Travelers' playbook isn't about brilliant strategies or breakthrough innovations. It's about doing ordinary things extraordinarily well, maintaining discipline when others lose it, and thinking in timeframes others can't fathom. In a world obsessed with disruption, Travelers proves that sometimes the most radical act is staying the course.

IX. Industry Analysis & Competitive Dynamics

The war room at Travelers' Hartford headquarters updates in real-time: Progressive's latest rates in Ohio, Chubb's new cyber product features, AIG's exposure to European floods, State Farm's withdrawal from California markets. In insurance, unlike most industries, competitors' moves are transparent—every rate filing public, every product form accessible, every earnings call scrutinized. Yet despite this transparency, sustainable advantages persist. Understanding why requires diving deep into insurance industry structure, competitive dynamics, and the subtle differences that separate winners from casualties.

The Great Divide: Personal vs. Commercial

The insurance industry isn't monolithic—it's two distinct businesses awkwardly sharing a label. Personal lines (auto, home) operate like consumer goods: standardized products, mass marketing, price-driven competition. Commercial lines (business property, general liability, professional liability) resemble consultative B2B services: customized solutions, relationship-based distribution, expertise-driven differentiation.

This divide explains seemingly contradictory dynamics. Progressive dominates personal auto through algorithmic pricing and direct distribution, yet barely registers in commercial lines. Chubb commands premium prices in high-net-worth personal lines and large commercial accounts, but can't compete in mass-market auto. AIG, once the world's largest insurer, retreated from personal lines entirely to focus on complex commercial risks.

Travelers straddles both worlds—a rare strategic position. They're the #2 commercial insurer while maintaining significant personal lines presence. This diversification provides ballast during market cycles. When personal auto hardens (2019-2024), commercial property might soften. When catastrophes devastate homeowners' results, liability lines remain profitable. Few competitors successfully manage this duality.

The strategic challenges differ fundamentally between segments. Personal lines require massive technology investments for marginal cost advantages—Progressive spends $1 billion annually on technology to shave pennies off processing costs. Commercial lines demand human expertise for risk assessment—evaluating a chemical plant's safety requires engineers, not algorithms. Travelers maintains dual capabilities: digital efficiency for personal lines, human expertise for commercial.

Hard vs. Soft Market Cycles: The Insurance Pendulum

Insurance markets oscillate between hard and soft cycles with metronomic regularity. Soft markets (2010-2017 most recently) see abundant capital, aggressive competition, falling prices, and loosening terms. Hard markets (2018-2024) bring capital scarcity, disciplined competition, rising prices, and tightening terms. Understanding these cycles—and positioning accordingly—separates successful insurers from roadkill.

The mechanics are simple. During soft markets, investment returns compensate for underwriting losses. Insurers chase growth, accepting marginal risks at inadequate prices. New capital floods in, attracted by seemingly easy profits. Competition intensifies. Prices fall further. Then catastrophe strikes—literal hurricanes or figurative financial crises—destroying capital. Survivors raise prices dramatically. Profitability soars. New capital arrives. The cycle repeats.

Travelers has mastered cycle management through contrarian positioning. During the soft market of 2014-2017, they shrank exposure in underpriced lines. Workers' compensation, priced for 3% medical inflation when actual was 6%? Reduced by 40%. Commercial auto, where juries awarded nuclear verdicts? Cut in half. The stock market hated this discipline—why wasn't Travelers growing?

When markets hardened in 2018, Travelers pounced. While competitors scrambled to rebuild capital, Travelers had dry powder. They hired 500 underwriters from struggling competitors. They expanded in profitable lines while others retrenched. Prices rose 7% in 2019, 10% in 2020, 12% in 2021. Combined ratios improved from 98% to 92%. The stock price doubled.

The current hard market, extending into 2024, shows unusual persistence. Social inflation—jury awards rising faster than economic inflation—continues accelerating. Climate losses mount annually. Reinsurance capacity remains constrained. These structural factors suggest the hard market could persist longer than typical cycles, advantaging disciplined players like Travelers.

The Competitive Landscape: Analyzing Key Players

Chubb: The Premium Prestige Player

Chubb operates like insurance's Mercedes-Benz—premium products for premium customers at premium prices. Their high-net-worth personal lines offer white-glove service: appraisers who catalog wine collections, adjusters who source identical Persian rug replacements, risk consultants who evaluate yacht crews. Commercial lines focus on Fortune 500 companies with complex global exposures.

Strengths include unmatched expertise in specialized risks, global capabilities spanning 54 countries, and premium pricing power from brand reputation. Weaknesses involve limited mass-market presence, high expense ratios from boutique service model, and concentration risk in high-severity lines.

Against Travelers, Chubb wins in large-account commercial and high-net-worth personal. But Travelers' middle-market commercial strength and broader distribution provide more consistent growth. Chubb's combined ratio averages 87% (exceptional) but with higher volatility. Travelers' 95% combined ratio delivers steadier returns across cycles.

AIG: The Fallen Giant Reborn

AIG's journey from near-death in 2008 to profitability in 2024 represents history's greatest insurance turnaround. After the financial crisis necessitated $182 billion in government bailouts, AIG shed non-core assets, exited personal lines, and refocused on commercial specialty lines where expertise matters more than scale.

Today's AIG specializes in complex risks others won't touch: cyber liability for Fortune 100 companies, political risk insurance for emerging markets, aviation coverage for experimental aircraft. Their Lexington subsidiary leads excess liability, providing coverage above primary limits. The strategy works—combined ratios improved from 110% in 2017 to 94% in 2024.

Travelers competes directly with AIG in large commercial accounts. The key differentiation: Travelers offers comprehensive solutions while AIG provides specialty pieces. A Fortune 500 company might buy primary coverage from Travelers and excess from AIG. This complementary competition benefits both—Travelers gets steady primary premium, AIG earns higher-margin excess coverage.

The Hartford: The Perpetual Turnaround

The Hartford perpetually teeters between breakthrough and breakdown. Strong in small commercial (under $1 million revenue businesses) and group benefits (employer-provided disability and life insurance), they struggle with execution consistency. Every five years brings new management, new strategy, new promises of transformation.

Recent focus on small commercial through digital distribution shows promise. Their ICON platform processes simple business quotes in minutes, competing with InsureTech startups. But technology alone doesn't ensure success—underwriting discipline, claims efficiency, and distribution relationships matter equally. The Hartford's combined ratio of 98% trails best-in-class competitors.

Travelers views Hartford as a useful competitor—aggressive enough to maintain market discipline but not threatening enough to disrupt pricing. When Hartford chases growth with low prices, Travelers lets them have unprofitable business. When Hartford retreats, Travelers captures their better accounts. This dynamic—Hartford as perpetual challenger never quite succeeding—benefits established players.

Progressive: The Algorithmic Assassin

Progressive represents insurance's most successful transformation—from niche high-risk auto insurer to personal lines juggernaut. Their secret: treating insurance like a math problem rather than relationship business. Every decision—pricing, underwriting, claims, marketing—follows algorithmic optimization.

Their data advantage compounds daily. With 30 million auto policies generating billions of data points, Progressive's pricing models exceed competitors' accuracy. They know the accident probability difference between Honda Accord and Toyota Camry drivers, between 32-year-olds and 33-year-olds, between Tuesday and Wednesday commutes. This granular pricing lets them cherry-pick profitable customers while competitors rely on crude segments.

Travelers respects Progressive's personal auto dominance but doesn't chase it. The investment required—billions in technology, decades of data accumulation—doesn't justify returns when commercial lines offer better economics. Instead, Travelers bundles auto with homeowners for retention, accepting lower auto margins for total account profitability.

State Farm: The Mutual Behemoth

State Farm remains America's largest property-casualty insurer through sheer inertia. Their 19,000 exclusive agents, embedded in communities for generations, provide unmatched distribution. The mutual structure, owned by policyholders rather than shareholders, enables long-term thinking without quarterly earnings pressure.

But structural advantages mask operational challenges. State Farm's technology lags competitors by years. Their exclusive agency model, while providing loyalty, costs significantly more than independent agents. Their concentration in catastrophe-prone states—Florida, Texas, California—exposes them to climate risks. Recent retreats from California and Florida markets signal strategic stress.