Birla Corporation: A Century of Cement, Jute, and the M.P. Birla Legacy

I. Introduction & Episode Roadmap

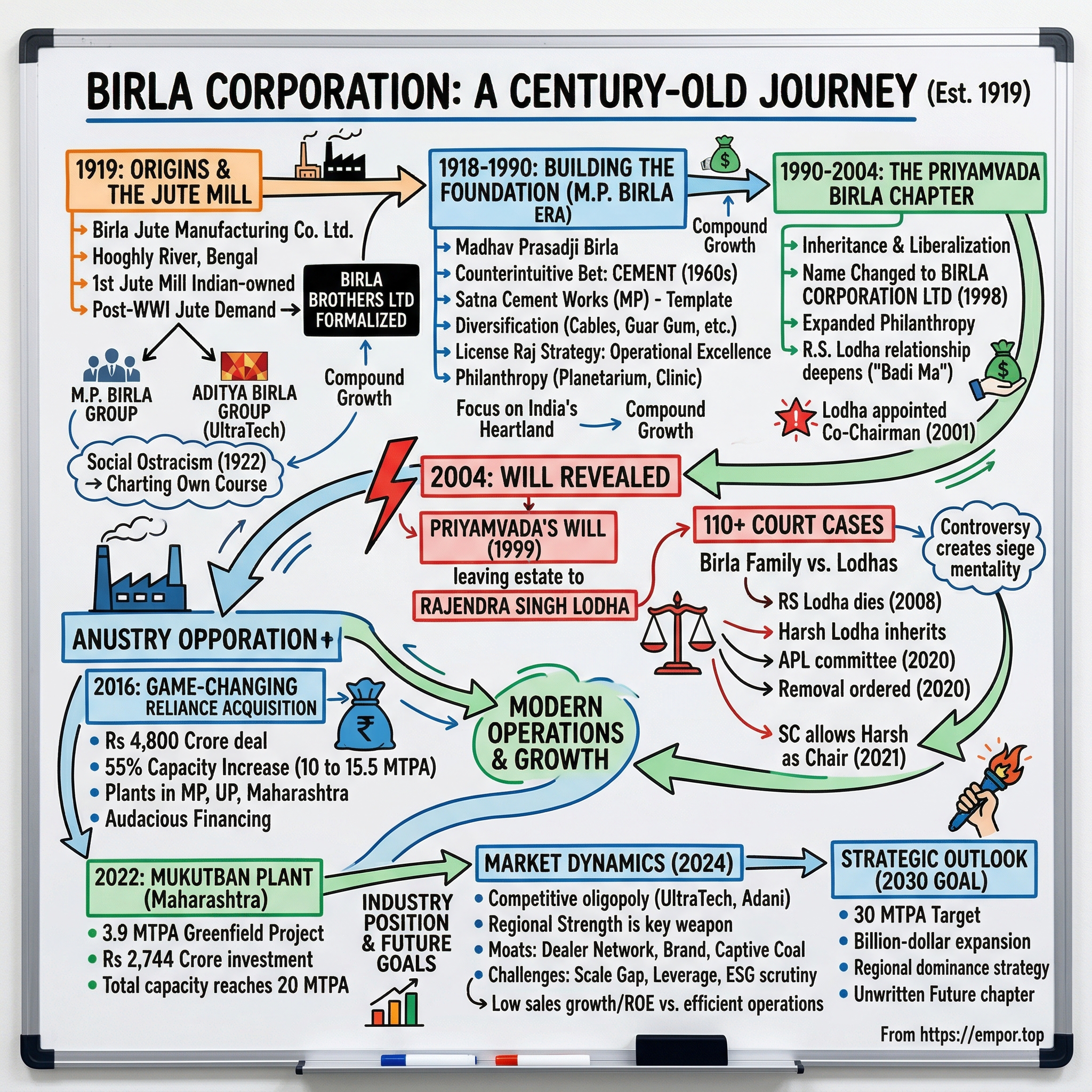

Picture this: 1919, the banks of the Hooghly River in Bengal. The Great War has just ended, and the world is hungry for jute—golden fiber, they call it—to rebuild what was destroyed. A young Indian entrepreneur, part of a merchant family from Rajasthan, stands before a sprawling mill complex. This isn't just any acquisition. It's the first jute mill to be owned entirely by an Indian business house, wrested from British control at a time when Indians were meant to be traders, not industrialists.

That mill, Birla Jute Manufacturing Company Limited, would become the cornerstone of what is today Birla Corporation Limited—a 20-million-tonne cement behemoth trading on the NSE as BIRLACORPN. But the path from jute bags to cement plants is anything but straightforward. It's a saga spanning five generations, featuring family feuds worthy of a Shakespearean drama, a will that shocked corporate India, and strategic pivots that transformed a colonial-era textile operation into a modern infrastructure play.

The compelling question isn't just how a jute mill became a cement powerhouse—it's how this particular branch of the legendary Birla family, the M.P. Birla Group, carved out its distinct identity, separate from the more famous Aditya Birla Group. It's about survival through Partition, the License Raj, liberalization, and now the great infrastructure boom of modern India.

This is a story of three transformative leaders: M.P. Birla, who built the foundation; Priyamvada Birla, who modernized it; and the unexpected inheritor R.S. Lodha, whose family now controls this century-old enterprise. Each brought their own vision, their own controversies, and their own legacy to a business that has somehow managed to stay relevant through every major economic shift India has witnessed.

What makes Birla Corporation particularly fascinating for investors isn't just its longevity—plenty of Indian companies are old. It's the company's ability to execute massive strategic shifts while maintaining family control, even when that family changed through perhaps the most controversial inheritance in Indian corporate history. Today, as India stands on the precipice of a massive infrastructure buildout, the question becomes: Can this hundred-year-old company, with its complex history and 62.9% promoter holding, compete with giants like UltraTech while maintaining its independence?

The themes we'll explore go beyond mere corporate history. This is about family legacy in the age of professional management, about how traditional industries adapt to modern markets, and about what it really means to build something that lasts a century in a country that has transformed as dramatically as India has. As we'll see, the journey from that first jute mill to today's cement empire tells us as much about India's economic evolution as it does about the Birla Corporation itself.

II. The Birla Dynasty: Origins & Context

The story begins not in a boardroom or factory floor, but in the narrow lanes of a Rajasthani village called Pilani. In 1911, a seventeen-year-old named Ghanshyamdas Birla arrives in Calcutta—the commercial heart of the British Raj—with little more than ambition and the backing of his father's modest trading business. Ghanshyamdas Birla laid the foundation of his industrial empire by establishing GM Birla Company, trading in jute, in 1911. He's entering a world where European merchants control the jute trade, where Indians are meant to be intermediaries, not industrialists. The Scottish jute barons of Calcutta view him as an upstart, a nuisance to be crushed.

Then comes 1914—the guns of August echo across Europe, and suddenly the world needs jute. Desperately. The First World War began in 1914 greatly increasing the demand for gunny bags. During the war, the Birla's worth is estimated to have risen from ₹2 million to ₹8 million. Gunny bags for sandbags, for transporting supplies, for the sinews of war. In four years, young Ghanshyamdas watches his family's fortune quadruple. By 1919, he's ready for his masterstroke.

That year marks a turning point in Indian industrial history. In 1919, he became among the first group of Indian entrepreneurs to become owner of a jute mill named Birla Jute. Not just any jute mill—this was the first to be owned entirely by an Indian business house, wrested from British control at a time when the colonial government's policies actively favored European merchants. He had to scale a number of obstacles as the British and Scottish merchants tried to shut his business by unethical and monopolistic methods, but he was able to persevere.

But here's where the Birla story takes its first fascinating turn. GD Birla and his brothers—Jugal Kishore, Rameshwar Das, and Braj Mohan—formalize their partnership that same year, 1919, creating Birla Brothers Limited. The family firm, which in 1918 was run as Baldeodas Jugalkishore, was made into a limited company known as Birla Brothers Limited. Each brother would eventually spawn their own business empire, but it's the lineage through Rameshwar Das that concerns us here. Understanding the family tree requires a crucial distinction that many investors miss. It is not a part of the Aditya Birla Group, a multinational conglomerate with products ranging from metals, cements, textiles, agricultural businesses, telecommunications, IT, and financial services. While both share the illustrious Birla surname and trace their roots to Ghanshyamdas Birla, they diverged generations ago. The Aditya Birla Group—today a $70 billion behemoth under Kumar Mangalam Birla—descends through GD Birla's lineage. The M.P. Birla Group, which controls Birla Corporation, descends through GD's brother, Rameshwar Das Birla.

This split wasn't just genealogical—it was philosophical and strategic. As has been noted in the press, some of the branches have been more successful than others. The GD-Basant Kumar-Aditya Vikarm-Kumar Mangalam Birla branch has performed the best, with a group turnover of ₹29,000 Crore in 2004. Meanwhile, the M.P. Birla branch chose a different path—more conservative, more regional, less aggressive in expansion.

The family was outcasted in 1922 when Rameshwar Das Birla remarried a Kolvar woman. This social ostracism from the conservative Maheshwari community would ironically free the M.P. Birla branch from certain traditional constraints, allowing them to chart their own course. While the Aditya Birla Group would go global, establishing operations from Thailand to Egypt, the M.P. Birla Group remained focused on India, particularly the eastern and central regions.

The distinction matters for investors because it explains much about Birla Corporation's trajectory. Without the global ambitions and access to capital that characterized the Aditya Birla Group, Birla Corporation would need to be more opportunistic, more patient, and ultimately more creative in its growth strategy. This separate identity would become both a limitation and, as we'll see with the Reliance acquisition, occasionally an advantage—allowing them to move quickly when larger groups were constrained by regulatory scrutiny or balance sheet considerations.

By understanding this family separation, we can better appreciate how a company with the Birla name could remain a mid-sized player in cement while its distant cousins built UltraTech into India's largest cement manufacturer. It's not a story of failure versus success, but of two different visions of what it means to build an industrial legacy in modern India. The M.P. Birla Group's journey, starting from that original jute mill in 1919, would prove that sometimes the road less traveled leads to its own form of endurance.

III. The M.P. Birla Era: Building the Foundation (1918-1990)

The monsoon of 1918 brings more than rain to Mumbai—it brings the birth of a child who would transform a jute mill into an industrial empire. Madhav Prasadji Birla, born on July 4, 1918, enters a world where his family's fortune is still counted in gunny bags and cotton bales. But young Madhav, son of Rameshwar Das Birla, carries a different vision. While his more famous cousins in the GD Birla line chase global expansion, Madhav sees opportunity in India's heartland.

Born in 1918, Madhav Prasad of Bombay, son of RD Birla, was a part of the Birla Jute Manufacturing Company since the beginning. By the time he finished college, he was already in charge of Birla Jute which had suffered economic downturns and wars. Think about that—a young man barely out of college, inheriting a business battered by the Great Depression and then World War II. The jute industry, once the golden goose during WWI, had become a burden by the 1940s. Partition in 1947 would sever East Bengal (now Bangladesh), the source of raw jute, from West Bengal's mills. Lesser men might have liquidated and moved on.

Madhav Prasadji Birla, born on July 4, 1918, was a pioneer industrialist and philanthropist. Syt. Birla was a living example of simplicity, humanity, discipline and dedication-qualities he imbibed owing to the deep influence of Mahatma Gandhi on his life. A true karmayogi, he always regarded himself as a trustee of his empire, his credo being "From God we receive and to God we offer".

This philosophy—seeing wealth as trusteeship rather than ownership—would define M.P. Birla's approach to business. Unlike the aggressive expansion of his cousins, he focused on steady, strategic diversification. Madhav changed the company from Birla Jute Manufacturing Company to a company with activities across a wide spectrum of industries.

The masterstroke comes in the 1960s when M.P. Birla makes a counterintuitive bet: cement. While others chase the glamour industries of independent India—steel, automobiles, chemicals—he sees the future in gray powder. Foundation of Satna Cement Works, the birthplace of Samrat Cement. The location choice is brilliant: Satna in Madhya Pradesh, sitting on massive limestone deposits, connected by rail to the growing markets of central and eastern India.

For about 25 years, from the 1950s to the 1980s, Sudarshan Birla (Madhav Prasad's cousin Lakshmi Niwas' son) managed Satna Cement, a unit of Birla Corporation. This detail matters—M.P. Birla wasn't building a personal fiefdom but a family enterprise, bringing in talented relatives and giving them real responsibility. The Satna plant becomes the template for future expansion.

Through the License Raj years—that suffocating period from the 1950s to 1991 when every business decision required government permission—M.P. Birla plays a different game than his peers. While others court politicians in Delhi for licenses to expand capacity, he focuses on operational excellence and cost reduction. Even when Madhav Prasad was the Chairman, Birla Corporation was run by professional managers. This professionalization, unusual for family businesses of that era, allows the company to navigate the treacherous waters of Indian bureaucracy without becoming entirely dependent on political patronage.

He had set up a host of companies like Birla Corp, Universal Cables, Vindhya Telelinks, Hindustan Gum & Chemicals, Digvijay Woollen Mills, Indian Smelting. Notice the pattern—each business complementary but not dependent on the others. Cables for the growing power sector, guar gum for the food industry, each generating cash to fund the next expansion. This conglomerate structure, now unfashionable, provided crucial diversification during India's volatile pre-liberalization economy.

The philanthropic impulse runs deep. He also established Birla Planetarium & Belle Vue Clinic and several schools in Calcutta. The Birla Planetarium, opened in 1962, becomes Asia's first modern planetarium—an oddly poetic gesture from a cement magnate, bringing the stars to earth while his factories transformed earth into buildings reaching for the sky.

By the time of his death on July 30, 1990, M.P. Birla had transformed Birla Corporation beyond recognition. Net sales grew from Rs 468 crore in 1990, at the time Madhav Prasad's death—a testament to steady, compound growth rather than flashy acquisitions. The company now operated across Kolkata, Birlapur and Durgapur, the group has plants located in Rewa, Maihar, Satna, Raebareli City, Kundanganj (Raebareli), Chanderia (Chittorgarh), Jodhpur, Viramgam, Bhiwani, Butibori and Goa.

What M.P. Birla built wasn't just an industrial empire—it was a particular vision of Indian capitalism. Conservative in finance, progressive in management, rooted in Indian soil rather than global ambition. He proved you could build something substantial without the headlines, without the foreign partnerships, without abandoning the original jute mill that started it all. As India stood on the brink of liberalization in 1990, his widow Priyamvada would inherit not just companies and factories, but a philosophy of business that would soon be tested by forces neither of them could have imagined.

IV. The Priyamvada Birla Chapter: Transformation & Controversy (1990-2004)

The year is 1990. India stands at the cusp of economic liberalization, and at 15 Birla Park, Kolkata, a widow inherits not just a business empire but the weight of transforming it for a new era. Priyamvada Birla, now in her seventies, takes charge of a company that her late husband had built with patience and conservatism. What follows is perhaps the most dramatic fourteen years in the company's history—ending not with a whimper but with a bombshell that would shake corporate India.

Sometime before Madhav Prasad's death, Priyamvada Birla took charge and followed the same pattern of management, restricting personal involvement to policy decisions and relying on some trusted lieutenants to manage the company. This management style—delegating operational control while maintaining strategic oversight—would prove both her strength and, ultimately, the source of unprecedented controversy.

The numbers tell a story of quiet competence: Net sales grew from Rs 468 crore in 1990, at the time Madhav Prasad's death, to Rs 1,034 crore in 2004 under the leadership of Priyamvada Birla. That's more than doubling revenues during a period of massive economic upheaval—the 1991 liberalization, the Asian financial crisis, the dot-com bubble. While flashier companies rose and fell, Birla Corporation ground forward.

When he died in 1990, his wife, Priyamvada Birla took over as the chairman of Birla in 1998 and changed the name to Birla Corporation Limited. The name change matters more than it might seem. Dropping "Jute Manufacturing" from the company name wasn't just cosmetic—it was a declaration that this was no longer a single-product company clinging to colonial-era glory. Under the Chairmanship of Mrs. Priyamvada Birla, the Company crossed the Rs. 1,300 - crore turnover mark.

Priyamvada was known for her active roles in the community, healthcare, and education. Priyamvada Birla showed an interest in health care, helping to build hospitals and funding research ranging from eye health to cardiology, oncology, neurology, and orthopedics. She also founded the Priyamvada Birla Cancer Research Institute and joined with Aravind Eye Care Center to build the Priyamvada Birla Aravind Eye Hospital. This philanthropic bent wasn't just noblesse oblige—it reflected a worldview where business success carried social responsibility.

But the real story of Priyamvada's tenure isn't in the balance sheets or the charitable foundations. It's in a relationship that would redefine corporate succession in India. Enter Rajendra Singh Lodha—chartered accountant, trusted advisor, and the man who would inherit an empire.

His entry into Birla's inner circle was via Basant Kumar's son, the late Aditya Vikram Birla. Lodha's financial acumen gained him the position of financial advisor in many Birla companies, including Madhav Prasad's. In the years leading to Priyamvada's death, Lodha had secured her confidence, too. The relationship deepens over the years. Priyamvada Birla was "Badi Ma" for Lodha and he carried out her wishes to the hilt.

In 2001, three years before her death, Priyamvada makes a move that telegraphs what's coming: Lodha was appointed co-chairman of Birla Corporation in 2001, roughly three years before Priyamvada Birla's death. The board minutes from that meeting reveal the depth of their relationship and her intentions: "The Chairman mentioned how Shri R S Lodha had, on the request of Late Syt M P Birla been helping all these years in many of the Group's matters from time to time and how she keenly wanted him to succeed her."

What happens next would trigger the most sensational corporate inheritance battle in Indian history. Priyamvada Birla, widow of Birla Corporation promoter Madhav Prasad (grand uncle to Kumar Mangalam Birla of the Aditya Birla Group, probably the best-known Birla today) had bequeathed her estate, believed to be around Rs 5,000 crore, to well-known Kolkata-based chartered accountant, Rajendra Singh Lodha in July 2004.

In July 2004, Priyamvada Birla, chairperson of the Birla Corporation, died and was revealed to have bequeathed the entire assets of the company to Lodha in 1999. Lodha was also the will's executor. The will, dated April 18, 1999, was a registered document—not some deathbed scrawl but a deliberate act executed five years before her death.

The Birla family's reaction was swift and furious. The Birlas, who in turn, claimed that in July 1983, Priyamvada Birla and MP Birla had created a mutual will. As per this will, the estate fortune would be distributed for charity among the Hindustan Medical Institution, Eastern India Educational Institution and the MP Birla Foundation. The battle lines were drawn: Was the 1999 will valid, or did the alleged 1983 mutual will take precedence?

Birla Corporation had a humdrum existence till the purported will of Priyamvada Birla catapulted it to enthralled public attention, with all its attendant accusations of fraud, malfeasance and misconduct. This marked the first time this reserved and storied business family, with links to the freedom movement, had faced a controversy of this nature.

The irony is palpable. A woman who had quietly stewarded the company through fourteen years of solid if unspectacular growth, who had maintained the Birla tradition of philanthropy and social responsibility, had in death created the kind of scandal the family had avoided for nearly a century. This sparked a protracted legal battle between members of the Birla family and Lodha that included more than 110 court cases at one time.

What makes Priyamvada's decision particularly fascinating is what it says about succession in Indian family businesses. Here was a childless widow with no direct heirs, facing the question every business dynasty must confront: What happens when bloodline ends? Her answer—choosing competence over kinship, selecting a trusted professional over distant relatives—was revolutionary for its time. Whether it was the right answer would be debated in courtrooms for the next two decades.

V. The Lodha Transition & Legal Drama (2004-2016)

October 3, 2008. London. Rajendra Singh Lodha, the man who inherited a Rs 5,000 crore empire from Priyamvada Birla, suffers a fatal heart attack at the residence of Basant Kumar Birla—ironically, one of the very Birlas contesting his inheritance. The case changed course with the sudden death of RS Lodha in October 2008. He had been chairman for just four years, but what years they were.

Under his leadership, the Company posted its best ever results in the years ended 31.3.2006, 31.3.2007 and 31.3.2008. Think about this achievement: While fighting more than 110 court cases simultaneously, while being called a usurper and fraud by one of India's most powerful business families, Lodha delivered the best financial performance in the company's nine-decade history. It's either a testament to his managerial brilliance or proof that controversy can sometimes focus the mind wonderfully.

The Supreme Court held that KK Birla, BK Birla and Yashovardhan Birla did not have any right to oppose the probate proceeding filed by RS Lodha. The issue was conclusively decided in favour of the Lodhas in three successive litigations. The Supreme Court on March 31, 2008, threw out all challenges to the late Priyamvada Devi Birla's will from members of the extended Birla family, while imposing a fine of Rs 250,000 for starting frivolous litigation.

But Lodha's death doesn't end the drama—it escalates it. In her will, Priyamvada declared that after RS Lodha, his son, Harsh Lodha would inherit the estates. Harsh Lodha, his son, then became the chairman of Birla Corporation. The baton passes to a younger generation, but the battle intensifies.

Harsh Vardhan Lodha represents a different breed of industrialist. An eminent Chartered Accountant, Mr. Harsh V. Lodha is a member of the Managing Committee of Assocham and Executive Committee member of the Indian Chamber of Commerce where he has also served as Vice President. Unlike the older generation of Birlas who built their legitimacy through proximity to Gandhi and the freedom movement, Harsh must build his through professional credentials and institutional positions.

The legal warfare becomes Byzantine in its complexity. The court appointed an Administrator Pendente Lite, who would be responsible for the administration of the Birla estate until the resolution of the case. Think about the absurdity: A century-old company, publicly listed, with thousands of employees and shareholders, being run by committee while lawyers argue about a will written in 1999.

The numbers tell their own story of resilience. Despite the chaos, despite having legitimacy questioned at every turn, the company continues to grow. The Company continued to record impressive growth in 2008-09 and 2009-10. By 2011, however, Birla Corporation faced problems with overproduction of cement during a long period of decreasing demand. The global financial crisis hits just as the leadership crisis peaks—a perfect storm that would have destroyed weaker organizations.

Then comes 2013, and things get personal. Harsh Lodha and his brother, Aditya Lodha, were indicted in 2013 for malpractice. Three members of the Birla Corporation claimed there was malpractice in the firm and alleged misconduct in falsifying the information about the number of partners in the firm. The issue? Lodha and Company was the auditor of Birla Corporations while Harsh was chairman—a potential conflict of interest. As a result, the ICAI suspended Harsh and Aditya Lodha for 3 months.

The corporate governance questions multiply. Can a family that inherited through a controversial will, rather than blood, command the loyalty of professional managers? Can they make long-term strategic decisions while fighting for their very right to make decisions? Meanwhile, Birla Corporation has signed a Memorandum of Understanding (MoU) with Assam Mineral Development for a cement plant in Assam where Birla will invest Rs 2500 crores over a time span of three years. Even amid the chaos, expansion continues.

The turning point comes at the 2020 Annual General Meeting. The APL committee in July, 2020, decided by majority, not to support the reappointment of Lodha. Yet when it goes to shareholders, the results show that the resolution pertaining to Lodha's reappointment got carried by 97.985 per cent votes in favour and the payment of remuneration/compensation was carried by 97.513 per cent votes in favour. Nearly 98% support—either the shareholders believe in Harsh Lodha's vision, or they simply want stability after sixteen years of drama.

On 19 September 2020, the Calcutta High Court ordered the removal of Harsh Vardhan Lodha from all the directorships and other positions in the trust's and societies of the MP Birla Group of Companies. Rock bottom. The judge in September 2020 passed an order directing the removal of Harsh Vardhan Lodha as the chairman of the MP Birla Group on the basis of a contentious concept of "extended estate". The Birlas seem to have won.

But the story isn't over. In July 2021, The Supreme Court ruled that Harsh Vardhan Lodha can continue as director and chairman in Birla Corporation, Universal Cables, Vindhya Telelinks and Birla Cable. The pendulum swings back. The floodgates of litigation opened by the petitioners over the years before every legal forum, and the exorbitant cost at which such litigation is being fought, prima facie creates an impression that it is not the interest of the R-1 Company which the petitioners seek to protect, but it is the continuance of HV Lodha as the chairman and director of R-1 that has become the eyesore of the petitioners.

By 2016, as this period draws to a close, Birla Corporation stands at a crossroads. The legal battles have consumed enormous resources—financial, emotional, managerial. The cement industry is consolidating rapidly. Competitors have grown through acquisitions while Birla Corporation fought in courtrooms. Something has to give. Either the company finds a transformative opportunity, or it risks becoming a footnote in Indian business history—the company that spent more time fighting over ownership than building value. As we'll see, the opportunity that emerges will be as unexpected as everything else in this saga.

VI. The Game-Changing Reliance Acquisition (2016)

February 5, 2016. While lawyers still battle over the Priyamvada Birla will in courtrooms across India, Harsh Lodha makes a move that will define his legacy—and perhaps finally silence his critics. The Kolkata-based diversified company signed a deal with RIL whereby it took over cement production unit for Rs 4,800 crore at a valuation of $140 a tonne. It's the kind of bold acquisition that the company hasn't attempted in decades, perhaps ever.

To understand the audacity of this deal, consider the context. Birla Corporation's own enterprise value as on 19th February 2016, was approximately INR 3600 crore which is almost 0.75 times the enterprise value assigned to the deal. They're buying assets worth more than their entire company. It's as if David decided to swallow Goliath.

The backstory makes it even more compelling. In August last year, Birla Corp had acquired 5.15 mtpa cement capacity of Lafarge India in Chhattisgarh and Jharkhand for Rs 5,000 crore. But the deal failed as an amendment in the Mining Act prohibited transfer of mining rights in case of asset sale. A crushing disappointment—the kind that might make a less determined CEO retreat into conservatism.

Instead, Harsh Lodha doubles down. On the other side of the table sits Anil Ambani, whose Reliance Infrastructure desperately needs to deleverage. RInfra had a consolidated debt of Rs 25,800 crore at the end of the last financial year and the sell off of the cement business is being seen as a move to improve the financial health of the company. One company's distress becomes another's opportunity.

This acquisition provides Birla Corporation Limited with ownership of high-quality assets, taking its total capacity from 10 MTPA to 15.5 MTPA. RCCPL has three cement units — an integrated cement plant at Maihar and grinding units at Kundanganj and Butiburi, with aggregated capacity of 5.58 mtpa. These aren't distressed assets being sold at fire-sale prices. It started actual production in FY 2014 however in a current financial year it became completely operational. Today, Reliance Cement has 3 plants (Maihar, Kundanganj, and Butibori) with total installed capacity of 5.5 Million Tonne Per Annum (MTPA).

The strategic logic is impeccable. "Reliance Cement fits our plans to grow the business profitably very well and offers lucrative prospects for creating synergy with existing operations," Harsh Lodha says. The plants are in Madhya Pradesh, Uttar Pradesh, and Maharashtra—perfectly complementing Birla Corporation's existing footprint in central and eastern India.

But here's where it gets truly interesting: the financing. As on 30th September 2015, a Total consolidated debt of Birla Corp was approximately INR 1241 crore. While cash and cash equivalent stood at INR 468 crore. The acquisition has been funded through existing cash reserves and incremental debt. They're leveraging up at a time when the cement industry faces overcapacity and pricing pressure. It's either brilliant timing or dangerous overreach.

The valuation tells its own story. With a total capacity of 5.5 MTPA (Including 0.5 MTPA grinding unit capacity), consideration per tonne comes out to be around $140. While considering the enterprise value of Birla Corp as on 19th February 2016, EV per tonne of Birla Corp comes out to be around $53. They're paying nearly three times their own valuation multiple. Why?

The answer lies in quality and potential. The reason behind this could be Reliance Cement plants are newly established, a captive coal mine near Maihar project and its strategic locations of its plants. Modern plants with the latest technology, a captive coal mine when coal linkages are increasingly scarce, strategic locations near growing markets—these aren't just cement plants, they're platforms for future growth.

Since Rinfra has mineral concessions in Madhya Pradesh, Maharashtra, Rajasthan, Karnataka, Andhra Pradesh and Himachal Pradesh, Birla Corp hopes to utilise the same by creating new capacities in the near future. The deal includes not just existing capacity but options for expansion—crucial in an industry where getting environmental clearances for greenfield projects has become nearly impossible.

On August 22, 2016, the deal closes. "We have got not only modern and efficient plants but also excellent opportunity of synergizing the business of Birla Corp and RCCPL to gain maximum advantage in the region we operate in and increase our share in the rapidly growing cement market," Harsh V Lodha declares. That apart, there is scope for further optimisation of the operation of RCCPL that would yield substantial benefit to the company.

The market's reaction is telling. The company's stock closed at Rs 680.95 a share on the Bombay Stock Exchange, up by Rs 5.80 over Friday's closing price of Rs 675.15. Modest appreciation, but appreciation nonetheless—the market sees potential, even if it's cautious about the debt load.

What makes this acquisition transformative isn't just the 55% capacity increase. It's what it represents: A company that spent twelve years defending its right to exist has just made one of the boldest moves in the Indian cement sector. A management team questioned at every turn has executed a complex acquisition that larger, more established players couldn't or wouldn't attempt.

For Harsh Lodha, this is vindication. While the Birlas argued in court that he had no right to run the company, he was busy transforming it from a regional player into a pan-Indian force. The acquisition catapults the company's cement production capacity to 15.4 million tonnes per annum (mtpa) from 9.8 mtpa. In one stroke, Birla Corporation moves from being a mid-sized player to knocking on the doors of the top tier.

The irony is delicious. The company that was supposed to be paralyzed by succession disputes has just pulled off one of the smartest acquisitions in recent cement industry history. As competitors struggled with overcapacity and weak pricing, Birla Corporation used others' distress to build scale at attractive valuations. Sometimes, the best time to be bold is when everyone expects you to be defensive.

VII. Modern Operations & Market Position (2016-Present)

January 21, 2022. Mukutban, Maharashtra. In the midst of a global pandemic, as supply chains collapse worldwide and construction projects grind to a halt, Harsh Lodha lights a kiln that represents the biggest bet in Birla Corporation's 103-year history. In 2022, Birla Corporation Limited added the 3.90 Million ton per annum Integrated Plant at Mukutban, with total production capacity reaching 20 million tonnes per annum.

The numbers are staggering: Set up at an investment of Rs 2,744 crores it is the largest greenfield investment by the Company in the history of the Group. This isn't just expansion—it's transformation. A company that took a century to reach 15 million tonnes capacity adds another 4 million tonnes in a single project.

What makes Mukutban special isn't just its size. This will be the fourth integrated cement unit of the Group and the biggest single line/kiln cement plant in Maharashtra, by capacity. It represents a technological leap forward—Air-Cooled Condenser (ACC) technology to minimize water consumption by 90 per cent, built exclusively by MP Birla Cement Perfect Plus brand, one of the few cement plants built entirely by Portland Pozzolana Cement which has 30%-35% component of fly ash.

The timing seems either prescient or insane. The project was conceived before COVID-19, executed during the pandemic's worst phases. The commissioning of the plant got delayed by a few months, thanks to the pandemic and more particularly thanks to the flight of the migrant workers from the project site. Yet they persevered. Moreover, to achieve 10-million man hours of construction with zero accidents and completion of the entire project without a single major accident or fatality, I am told, is a unique achievement in the cement industry, Lodha notes with pride. The modern Birla Corporation presents a paradox. Revenue: 9,478 Cr, Profit: 382 Cr—respectable numbers for any company. Yet The company has delivered a poor sales growth of 5.91% over past five years with low return on equity of 4.10% over last 3 years. The transformation from litigation-plagued uncertainty to operational expansion hasn't translated into stellar financial performance.

The geographic footprint tells a story of strategic positioning. The Cement Division of Birla Corporation Limited has 11 plants at eight locations, Satna & Maihar (Madhya Pradesh), Raebareli & Kundanganj (Uttar Pradesh), Chanderia (Rajasthan), Mukutban & Butibori (Maharashtra) and Durgapur (West Bengal). They manufacture varieties of cement like Ordinary Portland Cement (OPC), 43 & 53 grades, Portland Pozzolana Cement (PPC), fly ash-based PPC, Low Alkali Portland Cement, Portland Slag Cement (PSC), Low Heat Cement and Sulphate Resistant Cement.

The company operates across 13 states with a product portfolio of 11 brands, operating in 13 states with a family of more than 10000 dealers and 20000 retailers and 100000 influencers. The distribution network, built over a century, remains one of their strongest assets. The cement is marketed under the brand names of MP Birla Cement PERFECT PLUS, RAKSHAK, SAMRAT ADVANCED, ULTIMATE ULTRA, UNIQUE, SAMRAT, ULTIMATE, CHETAK, PSC, MULTICEM & CONCRECEM.

The sustainability angle has become central to their positioning. Currently, renewable energy accounts for about 22 per cent of Birla Corporation's total power consumption. Blended cement makes up more than 90 per cent of the Company's total cement production, the highest in India. In an industry facing increasing ESG scrutiny, this positions them well for the future. Looking forward, the ambition is clear: Birla Corporation Ltd is committed to increasing its annual cement production capacity to approximately 30 million tonnes (MT) by 2030. Our current production capacity stands at 20 million tonnes. Plans to increase cement production capacity by 50 per cent to 30 million tonnes per annum by 2030 represent both opportunity and challenge.

The investment required is substantial: Birla Corporation plans to invest a total of US$1bn in realising its planned 50% cement capacity footprint expansion. The breakdown is strategic—2 MTPA would come from de-bottlenecking of existing operations, 4 MTPA from greenfield projects and another 4 MTPA from brownfield expansion. It's a balanced approach, mixing low-risk optimization with higher-risk new projects.

But here's the challenge: The major cement companies are likely to add capacities of nearly 250 MTPA in the next few years which is almost 60% of the total existing capacity today. The Big-3 are expanding aggressively—UltraTech plans to reach 200 MTPA by 2030, Adani Group targets 140 MTPA by 2027, Shree Cement aims for 80 MTPA by 2030. Birla Corporation's 30 MTPA target, while ambitious for them, still leaves them far behind the leaders.

The strategic positioning remains focused on regional dominance rather than national scale. Birla Corporation Limited will expand in markets where the company has an edge over competition and demand for cement is projected to get stronger. They're not trying to compete everywhere but doubling down on markets where they have logistics advantages, brand recognition, and established relationships.

The jute business—that original mill from 1919—still operates. More than a century's experience. Modern spinning technology. Skilled workforce. Above all, an innovative, customer-focused outlook. It's almost quaint in an era of digital disruption, but it represents continuity, heritage, and a reminder of where this journey began.

Today's Birla Corporation is a study in contrasts. A company that spent nearly two decades in courtrooms now plans billion-dollar expansions. A business that traces its roots to the freedom struggle now competes with global giants. A management that inherited through controversy now seeks to build legitimacy through performance.

The market remains skeptical—that 5.91% five-year revenue growth and 4.10% three-year ROE tell their own story. But with infrastructure spending accelerating, urbanization continuing, and cement demand expected to grow, the opportunity exists. Whether Birla Corporation can capitalize on it while maintaining independence in a consolidating industry remains the billion-dollar question. The next chapter of this century-old story is still being written.

VIII. Competitive Dynamics & Industry Analysis

The Indian cement industry in 2024 presents a paradox: massive demand potential meeting brutal competition. To understand Birla Corporation's position, imagine a chess board where UltraTech is the queen—powerful, mobile, dominant—while players like Birla Corporation are bishops and knights, needing to be clever about their moves.

UltraTech Cement, with 67 MTPA capacity expanding to 200 MTPA by 2030, operates at a scale that creates its own gravity. When UltraTech enters a market, pricing dynamics shift. When it builds a plant, logistics networks reorganize. Against this behemoth, Birla Corporation's 20 MTPA seems almost quaint. Yet David versus Goliath isn't always about size—sometimes it's about finding the right stone.

The competitive landscape has fundamentally shifted post-2022. The Adani Group's acquisition of ACC and Ambuja for $10.5 billion created India's second-largest cement player overnight. Suddenly, the industry structure changed from UltraTech-and-everyone-else to a genuine oligopoly at the top. For mid-sized players like Birla Corporation, this consolidation is both threat and opportunity—threat because the giants have deeper pockets, opportunity because they're often distracted by integration challenges.

Regional strength becomes Birla Corporation's primary weapon. In central India—Madhya Pradesh, Chhattisgarh, eastern Maharashtra—they're not number five or six nationally but number two or three regionally. Cement is ultimately a regional game; nobody ships cement 1,000 kilometers if they can avoid it. Transport costs can easily exceed manufacturing costs beyond 300-400 kilometers. This geographic moat protects Birla Corporation's core markets even as national players expand.

The cost structure tells an interesting story. While Birla Corporation can't match UltraTech's procurement scale for inputs like coal and petcoke, they have specific advantages. The captive coal mine near Maihar, acquired with Reliance Cement, provides partial insulation from volatile coal prices. At the Mukutban plant, government incentives of Rs 650 per tonne make it one of India's lowest-cost production sites. These pocket advantages matter in a commodity business where EBITDA per tonne differences of Rs 100-200 determine profitability.

Brand positioning reflects market reality. Birla Corporation doesn't try to compete with UltraTech's premium "UltraTech Cement" brand nationally. Instead, they've built a portfolio approach—SAMRAT for premium institutional sales, CHETAK as a regional powerhouse in North India, PERFECT PLUS for quality-conscious retail buyers. It's segmentation by geography and customer type rather than trying to build a single national brand against better-funded competitors.

The trade channel dynamics favor incumbents, which helps Birla Corporation in its stronghold markets. A cement dealer stocks 3-4 brands maximum. Once you're in, you're in—but getting in when UltraTech, Ambuja, and ACC are already there? Nearly impossible. This is why Birla Corporation's network of 10,000 dealers and 20,000 retailers, built over decades, represents a moat that money alone can't quickly replicate.

Technology and sustainability are becoming differentiation factors, though still secondary to price and availability. Birla Corporation's 90% blended cement ratio—using fly ash and slag—positions them well for increasingly ESG-conscious institutional buyers. But let's be honest: most customers still buy primarily on price, payment terms, and delivery reliability.

The financial metrics reveal the competitive pressure. That 5.91% five-year revenue CAGR compares poorly to industry growth of 8-9%. The ROE of 4.10% sits well below the 15-20% that leaders generate. These numbers reflect a company that's surviving but not thriving, maintaining position but not gaining share.

Yet the consolidation wave creates opportunities for those who wait. As UltraTech and Adani focus on integrating massive acquisitions, as global players like Holcim exit India, as smaller regional players struggle with new environmental norms, Birla Corporation's stability becomes an asset. They're not the predator, but they're also too large to be easy prey.

The pricing dynamics in cement are fascinating and brutal. Unlike steel or aluminum, cement has no LME price, no global benchmark. Prices are hyperlocal—varying by district, by season, even by customer segment. In this environment, regional players with deep market knowledge can compete effectively against national giants who often rely on algorithmic pricing models that miss local nuances.

Looking at utilization rates across the industry, Birla Corporation's 95% compares favorably to the industry average of 65-70%. This suggests efficient operations and strong regional demand, even if growth has been modest. High utilization also means that incremental volume growth flows almost directly to the bottom line—a key advantage when demand accelerates.

The working capital dynamics favor Birla Corporation's regional focus. Cement is largely a cash business at the retail level, but infrastructure and institutional sales require credit periods. Birla Corporation's average collection period of 15-20 days compares well to larger players who often extend 30-45 day credits to win infrastructure contracts. This cash generation ability matters when funding expansion without excessive leverage.

What emerges from this analysis is a company that has found its niche—not trying to win everywhere but determined not to lose anywhere that matters. In an industry consolidating toward 5-6 major players controlling 70-80% of capacity, Birla Corporation seems positioned to remain one of those survivors. Not the biggest, not the most profitable, but resilient enough to maintain independence while others sell or merge.

The question isn't whether Birla Corporation can compete—they've proven they can. It's whether competing as a subscale player in an increasingly consolidated industry makes long-term economic sense. For now, with infrastructure spending booming and cement demand growing, there's room for everyone. But when the music stops—and it always does in cyclical industries—will Birla Corporation have a chair?

IX. Playbook: Business & Investment Lessons

Every business story teaches lessons, but Birla Corporation's century-long saga offers a masterclass in survival, succession, and strategic patience. These aren't theoretical frameworks from business school but hard-won insights from navigating India's economic evolution, family dynamics, and capital allocation decisions that compound over decades.

Lesson 1: Managing Succession in Family-Controlled Businesses

The Priyamvada Birla will controversy offers a radical solution to succession: choose competence over bloodline. Most family businesses destroy value in third-generation transitions, caught between entitled heirs and professional management. Priyamvada's choice—bequeathing everything to her chartered accountant—was shocking but perhaps brilliant. R.S. Lodha and later Harsh Lodha brought professional rigor while maintaining the family business ethos. The 97.98% shareholder support for Harsh Lodha's reappointment suggests that sometimes the best family member is the one you choose, not the one you're born with.

Lesson 2: The Art of Patient Capital Allocation in Cyclical Industries

Cement is viciously cyclical. Birla Corporation's approach—steady expansion during downturns, selective acquisitions from distressed sellers, avoiding leverage binges during booms—reflects an understanding that in cyclical industries, survival is strategy. The Reliance Cement acquisition in 2016, buying 5.5 MTPA for Rs 4,800 crore when Anil Ambani needed to deleverage, exemplifies opportunistic patience. They waited for the right asset at the right price rather than overpaying during industry euphoria.

Lesson 3: When to Be Opportunistic

The failed Lafarge deal in 2015 could have paralyzed management. Instead, within six months, they pivoted to Reliance Cement. This mental flexibility—abandoning sunk costs, moving quickly when opportunities emerge—distinguishes survivors from casualties. In industries where scale matters, you can't afford to nurse wounds. The lesson: have a pipeline of opportunities, so one failed deal doesn't freeze your growth strategy.

Lesson 4: Balancing Heritage with Growth

Most conglomerates would have shuttered the jute business decades ago. Birla Corporation still operates that original 1919 mill. Why? It's not nostalgia—it's signaling. Maintaining the heritage business tells stakeholders: we honor commitments, we think long-term, we don't abandon ship when seas get rough. This reputation capital has value, especially when raising debt or negotiating with governments. The jute business might contribute less than 5% of revenues, but its symbolic value in establishing trust is immeasurable.

Lesson 5: Corporate Governance in Promoter-Driven Companies

With Promoter Holding: 62.9%, Birla Corporation challenges conventional governance wisdom. High promoter holding usually signals either exceptional confidence or inability to attract outside capital. Here, it's both. The inheritance controversy made raising equity difficult, but it also aligned management with long-term value creation. The lesson: concentrated ownership works when promoters think like owners, not emperors. The Lodhas' willingness to reinvest profits rather than extract dividends demonstrates this owner-mindset.

Lesson 6: Building Strategic Moats in Commodity Businesses

Cement is the ultimate commodity—one company's PPC cement is chemically identical to another's. Yet Birla Corporation maintains pricing power in core markets. How? Three moats: distribution density (those 10,000 dealers), local brand equity (CHETAK in North India has 50+ year heritage), and logistics advantages (plants near demand centers). The lesson: in commodities, competitive advantage comes from everything except the product itself.

Lesson 7: The Power of Regional Focus

While peers chased national footprints, Birla Corporation doubled down regionally. This concentration risk became concentration advantage—deeper market knowledge, better government relations, optimized logistics. Being number two in Madhya Pradesh beats being number ten nationally. The lesson: in businesses with high transport costs, regional density trumps national presence.

Lesson 8: Managing Through Controversy

From 2004 to 2021, Birla Corporation fought over 110 court cases while running a capital-intensive business. They compartmentalized—legal team fought battles while operations team built plants. The company delivered its best-ever results during peak controversy years (2006-2008). The lesson: organizations can handle more stress than leaders think, if you separate crisis management from daily operations.

Lesson 9: Capital Structure Discipline

Despite massive expansion needs, Birla Corporation maintains conservative leverage. Debt-to-EBITDA stays below 2x even while funding 50% capacity expansion. This isn't financial timidity—it's learned wisdom from watching leveraged competitors collapse during downturns. The lesson: in cyclical industries, the aggressive capital structure that maximizes returns in good times guarantees destruction in bad times.

Lesson 10: The Value of "Good Enough"

Birla Corporation will never be India's largest cement company. Their 5.91% revenue growth won't excite growth investors. The 4.10% ROE won't attract value investors. Yet they've survived a century, maintained independence, and continue expanding. The lesson: in business, as in evolution, survival doesn't require being the best—just being good enough to persist while others perish.

Lesson 11: Acquisition Integration

The Reliance Cement integration succeeded where many fail because Birla Corporation didn't try to immediately "Birla-fy" everything. They retained local management, maintained existing supplier relationships, and gradually integrated systems. The lesson: in acquisitions, day-one control matters less than year-three performance. Cultural integration can wait; operational continuity cannot.

Lesson 12: The Hidden Value of Controversy

Counterintuitively, the inheritance controversy might have helped Birla Corporation. It lowered acquisition multiples (who wants to buy into a legal mess?), reduced competitor attention (let them fight while we expand), and created a siege mentality that unified management. The lesson: corporate adversity, if survived, can become competitive advantage.

Investment Implications

For investors, Birla Corporation presents a fascinating puzzle. The numbers—low growth, modest ROE, high promoter holding—screen poorly. Yet the strategic position—20 MTPA capacity in infrastructure-hungry India, strong regional presence, demonstrated acquisition capability—suggests hidden value.

The key insight: Birla Corporation is a survival play, not a growth play. In an industry consolidating toward oligopoly, being the last independent mid-sized player has option value. They could be an acquisition target (though promoter holding makes this difficult), a consolidator of smaller players, or simply a steady cash generator as cement demand grows with India's infrastructure build-out.

The investment case isn't about multiple expansion or explosive growth. It's about a business trading at replacement cost that has survived everything India could throw at it for a century. In a world of disruption and creative destruction, sometimes the best investment is the company that simply refuses to die.

X. Bear vs. Bull Case & Valuation

The investment case for Birla Corporation splits minds like few other stocks. Bears see a subscale player in a consolidating industry with poor financial metrics. Bulls see hidden asset value and strategic optionality. Both are right—and that's what makes this interesting.

The Bull Case: Infrastructure Dreams and Hidden Value

India's infrastructure story is just beginning. The government plans to spend $1.4 trillion on infrastructure by 2025. Every kilometer of highway needs 50,000 tonnes of cement. Every metro project, every affordable housing scheme, every smart city—all need cement. At 300 kg per capita consumption versus China's 1,600 kg and the global average of 500 kg, India's cement demand could double or triple over the next decade.

Birla Corporation sits perfectly positioned for this boom. Their 20 MTPA capacity expanding to 30 MTPA by 2030 times an infrastructure supercycle equals explosive volume growth. Central and eastern India, their strongholds, are precisely where the government focuses infrastructure spending—connecting the hinterland to economic centers.

The M.P. Birla brand equity deserves attention. In cement, brand matters more than most realize. Contractors specify brands in government tenders. The M.P. Birla name, with its century-long heritage and association with nation-building, carries weight that new entrants can't replicate. This intangible asset doesn't appear on balance sheets but drives pricing power.

Asset replacement cost tells a compelling story. Building 20 MTPA of new cement capacity would cost roughly Rs 15,000-18,000 crore at current prices. Birla Corporation's enterprise value? Around Rs 14,000 crore. You're essentially buying 20 MTPA of modern capacity at less than replacement cost, with the jute business, brand value, and distribution network thrown in free.

The regional consolidation opportunity excites. As environmental norms tighten, smaller 1-2 MTPA players struggle with compliance costs. Birla Corporation, with its balance sheet strength and operational expertise, could roll up these distressed assets at attractive valuations. They've proven acquisition capability with Reliance Cement—why not repeat?

Management quality has surprised skeptics. Despite the controversial inheritance, Harsh Lodha has delivered operational improvements, completed major expansions on time and budget, and maintained financial discipline. The 97.98% shareholder approval suggests institutional investors see competence beyond the controversy.

The sustainability angle becomes increasingly valuable. With 90% blended cement and 22% renewable energy, Birla Corporation leads peers in environmental metrics. As carbon taxes loom and ESG mandates tighten, their early positioning could translate to cost advantages and preferred vendor status with environmentally conscious buyers.

Hidden optionality exists in the land bank. Cement plants sit on large land parcels, often near expanding cities. The real estate value of strategically located plants could exceed their industrial value. While not core to the investment case, this provides downside protection.

The Bear Case: Structural Disadvantages and Eternal Also-Ran Status

The numbers don't lie. Poor sales growth of 5.91% over past five years and low return on equity of 4.10% reflect structural, not cyclical, problems. In an industry where scale drives returns, Birla Corporation lacks scale. UltraTech generates 20% ROE with superior procurement power, logistics optimization, and overhead absorption. Why should Birla Corporation's returns improve when the scale gap keeps widening?

Industry consolidation threatens independence. Cement is consolidating globally toward 5-6 players controlling 80% of capacity. India won't be different. Birla Corporation faces a stark choice: sell at whatever price they can get, or slowly bleed market share to larger, more efficient competitors. Neither path rewards minority shareholders.

The corporate governance concerns persist. Yes, courts validated the Lodha inheritance, but the fact remains: this is a professionally managed family business where the "family" acquired control through a controversial will. The 62.9% promoter holding means minority shareholders have no real say. If management decides to sell assets cheap to related parties or take the company private at an unfavorable valuation, minorities are powerless.

Commodity businesses deserve commodity multiples. Cement is ultimately a commodity. No amount of branding changes the fact that customers buy primarily on price and availability. In commodities, the low-cost producer wins. Birla Corporation isn't the low-cost producer nationally and faces larger players even in regional markets.

The expansion plans look questionable. Spending Rs 8,000+ crore to add 10 MTPA when the industry is adding 250 MTPA seems like throwing good money after bad. By the time their expansion completes, industry utilization could drop from 70% to 50%, crushing margins for everyone, especially subscale players.

Input cost pressures remain structural. Without captive coal for most plants, Birla Corporation faces permanent disadvantage versus integrated players. Coal constitutes 30-40% of cement production costs. Even a 10% disadvantage in coal costs translates to 3-4% EBITDA margin differential—massive in a business where leaders generate 20% margins and laggards struggle at 15%.

Technology disruption looms. New construction technologies—3D printing, alternative materials, improved concrete efficiency—could reduce cement intensity in construction. If cement demand grows slower than capacity additions, the weakest players suffer first. Guess who's weakest?

The debt burden constrains flexibility. While leverage appears manageable, funding 50% capacity expansion will strain the balance sheet. If cement prices correct during their expansion phase, they could face the deadly combination of high debt and low cash generation that has killed many cement companies.

Valuation Reality Check

At current levels around Rs 1,200-1,300 per share, Birla Corporation trades at: - EV/EBITDA of ~7-8x versus peers at 10-12x - P/B of ~1.8x versus replacement cost suggesting 2.5-3x - EV per tonne of $70-80 versus recent transactions at $100-140

The valuation appears cheap, but cheap for good reason. The market prices in execution risk on expansion, continued competitive pressure, and limited strategic options. Bulls argue this creates opportunity—even modest improvement in fundamentals could drive rerating. Bears counter that value traps look cheap for years before destroying capital.

The Verdict: A Special Situation, Not a Core Holding

Birla Corporation isn't a simple buy or sell. It's a special situation requiring specific catalysts: - A successful acquisition that demonstrates capital allocation skill - Industry consolidation that reduces competitive intensity - Significant improvement in regional market share - Government infrastructure spending exceeding expectations - A strategic investor taking a stake, validating the story

Without catalysts, it remains a value trap—optically cheap but fundamentally challenged. The binary nature makes position sizing crucial. For enterprising investors, a small position betting on optionality makes sense. For conservative investors seeking steady compounders, look elsewhere.

The ultimate question: Is Birla Corporation a survivor adapting to new realities or a dinosaur awaiting extinction? The answer determines whether today's price represents opportunity or illusion. History suggests betting against hundred-year survivors is dangerous. But then, history also suggests most industrial dynasties eventually fall. Place your bets accordingly.

XI. Epilogue: The Future of a Century-Old Legacy

As dawn breaks over the Hooghly River in 2024, that original jute mill still stands—a testament to endurance in a nation that has transformed beyond recognition. From the site where Indian entrepreneurship first challenged colonial industrial monopoly, you can now see the Kolkata skyline dotted with towers built with Birla cement. It's poetic, really—the journey from making bags to hold goods to making materials that house dreams.

The question facing Birla Corporation isn't whether they can survive—they've proven that through world wars, partition, license raj, liberalization, and legal battles that would have destroyed lesser organizations. The question is whether survival is enough in an industry racing toward consolidation at breakneck speed.

Can Birla Corporation remain independent? The math suggests it's possible but increasingly difficult. At 20 MTPA today, 30 MTPA by 2030, they'll remain subscale nationally but potentially dominant in chosen regions. Independence requires threading a needle—growing fast enough to maintain relevance but not so aggressively that leverage destroys flexibility. The 62.9% promoter holding provides protection against hostile takeovers but also limits access to growth capital.

The ESG challenge looms larger than most appreciate. Cement production contributes 8% of global CO2 emissions. As carbon taxes materialize and construction methods evolve, the industry faces existential questions. Birla Corporation's early moves—90% blended cement, 22% renewable energy—position them better than most. But the real challenge isn't reducing emissions by 20-30% but reimagining cement for a net-zero world. Can a century-old company innovate radically enough?

Digital transformation in traditional industries separates future winners from walking dead. Birla Corporation has made modest progress—dealer apps, supply chain optimization, predictive maintenance. But digital isn't about apps; it's about business model innovation. Imagine AI-optimized logistics reducing transport costs by 20%, or blockchain-enabled supply chains eliminating working capital needs, or direct-to-consumer cement sales bypassing traditional distribution. The company that cracks digital in cement gains insurmountable advantage. Will it be Birla Corporation or a competitor?

The next generation question has no clear answer. The Lodhas have proven capable custodians, but they're professionals, not founders. Do they have the emotional commitment to fight through the next crisis? Or when an attractive offer comes—and it will—do they cash out? The difference between family businesses that last centuries and those that don't often comes down to whether leadership sees themselves as owners or managers.

India's infrastructure boom provides tailwind, but tailwinds eventually become headwinds. When infrastructure spending slows—and it will—overcapacity will savage margins. The companies that survive will be those with the lowest costs, best brands, and strongest balance sheets. Birla Corporation has two of three; whether that's enough remains to be seen.

Three Scenarios for 2030

Scenario 1: The Consolidator (30% probability) Birla Corporation successfully executes its 30 MTPA expansion, acquires 2-3 distressed regional players, and emerges as India's solid number 5 cement company. Strong regional presence and operational excellence drive ROE to 12-15%. The stock re-rates to industry multiples, delivering 15-20% annual returns.

Scenario 2: The Target (40% probability) By 2027-28, industry consolidation accelerates. A global major or domestic giant makes an offer the Lodhas can't refuse—perhaps $150-180 per tonne, valuing the company at Rs 20,000-25,000 crore. Shareholders receive a 40-60% premium to current prices, but the century-old independent journey ends.

Scenario 3: The Struggler (30% probability) Expansion plans face delays and cost overruns. Industry overcapacity crushes margins. Debt levels constrain flexibility. The company survives but generates sub-par returns, becoming a permanent value trap. The stock delivers 0-5% annual returns, underperforming both market and industry.

Final Reflections

Birla Corporation embodies the complexity of Indian business—where colonial history meets modern ambition, where family emotion confronts market logic, where tradition and disruption uneasily coexist. It's a company that shouldn't exist by conventional analysis yet continues to persist through sheer institutional will.

For investors, it represents a fascinating asymmetric bet. Limited downside (trading near replacement cost with strong asset backing) but uncertain upside (requiring successful execution in an increasingly difficult industry). It's not a stock for passive indexing or momentum trading but for patient capital willing to bet on mean reversion and management execution.

For students of business, it offers richer lessons. How do organizations survive existential threats? What's the value of institutional memory in industries obsessed with disruption? Can professional management successfully steward family legacies? Birla Corporation doesn't provide clean answers but rather lived experience of navigating these tensions.

The cement will keep flowing from those 11 plants across India. Construction workers will keep specifying M.P. Birla Cement, often unaware of the century of history in each bag. The company will keep generating cash, expanding capacity, fighting competitive battles. Whether it thrives or merely survives, whether it remains independent or gets absorbed into a larger entity, whether the Lodhas build on the Birla legacy or eventually exit—these questions will be answered not in boardrooms or courtrooms but in the market's daily verdict.

As we close this exploration, remember that every business story is ultimately a human story. Behind the numbers and strategies are people making decisions with imperfect information, balancing stakeholder interests, trying to build something that lasts. Birla Corporation has lasted 105 years not because it always made the right decisions but because it survived the wrong ones.

In an era that celebrates disruption and scorns tradition, perhaps there's value in studying organizations that simply endure. They remind us that in business, as in life, the race doesn't always go to the swift or the battle to the strong, but that's usually the way to bet. Whether Birla Corporation proves the exception or confirms the rule—well, that's what makes markets.

The story continues. The next chapter remains unwritten. And somewhere in Kolkata, that original jute mill keeps running, a century-old heart still beating in a corporation that refuses to accept its obituary. In Indian business, as in Indian mythology, nothing truly dies—it just transforms and continues in another form. What form Birla Corporation takes next might surprise us all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube