CERA Sanitaryware: India's Bathroom Revolution

I. Introduction & Episode Setup

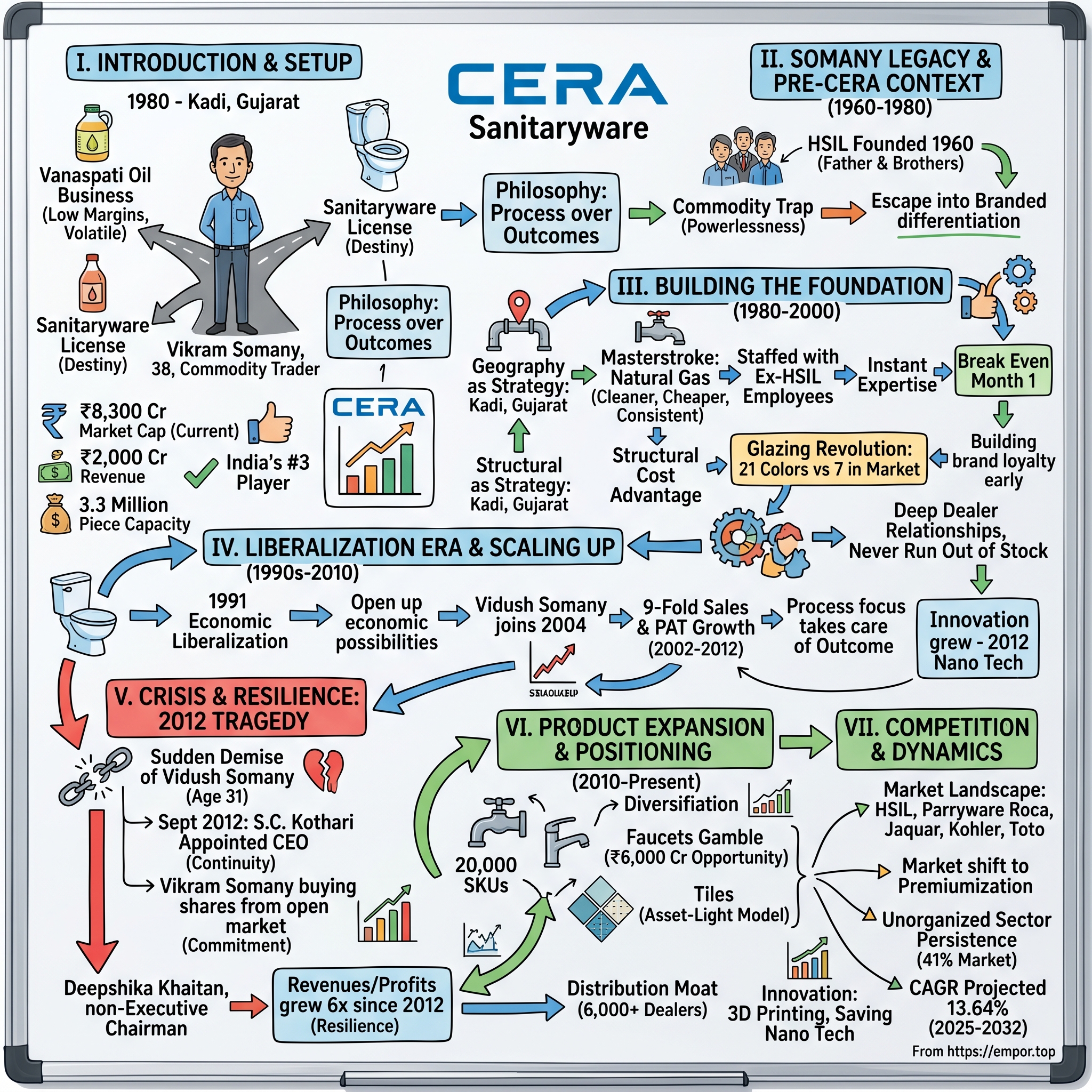

Picture this: It's 1980 in Kadi, a dusty town in Gujarat's Mehsana district, better known for its oil fields than manufacturing prowess. A 38-year-old commodity trader named Vikram Somany stands at a crossroads. Behind him lies a modest vanaspati oil business—brutal margins, volatile prices, zero differentiation. Ahead? A license to manufacture sanitaryware, an industry his father helped pioneer two decades earlier. Most would see a risky pivot. Somany saw destiny.

Fast forward to today: CERA Sanitaryware commands an ₹8,300 crore market capitalization, generates nearly ₹2,000 crores in annual revenue, and ranks as India's third-largest organized sanitaryware player with 3.3 million piece production capacity. The company that began in a single Gujarat factory now offers everything from smart toilets to designer faucets, competing toe-to-toe with century-old multinationals and homegrown giants alike.

But here's what makes this story truly remarkable: Unlike the typical Indian business saga of rapid expansion through debt and acquisition, CERA built its empire methodically, almost stubbornly, through internal accruals and an obsessive focus on manufacturing excellence. No flashy acquisitions. No private equity gymnastics (until much later). Just a relentless pursuit of what Somany calls "process over outcomes"—a philosophy that would be tested by personal tragedy, market upheavals, and competitive onslaughts.

The central question isn't just how a vanaspati oil trader built one of India's premium bathroom brands. It's how CERA managed to thrive in an industry where global giants like Kohler and Roca deploy unlimited capital, where unorganized players undercut prices by 40%, and where your product literally goes down the drain. This is a story about contrarian bets that created lasting moats, about finding competitive advantage in the most unlikely places, and about building a premium brand in a market obsessed with price.

As we unpack CERA's four-decade journey, we'll explore the pivotal decisions that shaped its trajectory: the natural gas gamble that slashed production costs, the 21-color revolution in a 7-color market, the vertical integration into faucets that nearly derailed growth, and the succession crisis that could have destroyed everything. We'll examine how a company can grow revenues six-fold after losing its heir apparent, why Gujarat produces 75% of India's sanitaryware, and whether CERA can truly become India's answer to Kohler.

This isn't just a business story—it's a masterclass in navigating India's unique market dynamics, from License Raj constraints to liberalization opportunities, from GST disruptions to real estate cycles. It's about understanding that in India, distribution is destiny, brands are built in decades not quarters, and sometimes the best strategy is simply outlasting your competition.

II. The Somany Legacy & Pre-CERA Context

The roots of CERA stretch back to 1960, when Vikram Somany's father and brothers did something audacious: they founded Hindustan Sanitaryware & Industries Limited (HSIL), India's first organized sanitaryware company. Think about that timing. This was Nehru's India—socialist, inward-looking, where importing a toilet was considered bourgeois excess. The Somanys weren't just starting a business; they were creating an entire industry category.

By the late 1970s, HSIL had become synonymous with modern bathrooms in urban India. But Vikram Somany, the younger generation, found himself on a different path entirely. While his family shaped India's bathroom habits, he traded in vanaspati oil and de-oiled cakes—classic commodity businesses where your biggest competitor could be your customer tomorrow, where a 2% margin felt like victory, and where global commodity prices could wipe out a year's profits overnight. The commodity trap wasn't just about thin margins—it was about powerlessness. Vikram Somany's vanaspati oil and de-oiled cakes manufacturing business was exposed to brutal commodity economics, where success depended on factors entirely outside his control: monsoons, global soybean prices, government import policies. Every day was a knife fight for survival. An employee once earned more than Vikram Somany himself, an indication of his ability to recognize and pay for talent, and lack of ego—a management philosophy that would later define CERA's culture.

To understand CERA's genesis, you need to grasp India circa 1980. This was peak License Raj—an economic system where producing an extra toilet required government permission, where waiting lists for scooters stretched years, where "choice" meant picking between two brands if you were lucky. The sanitaryware market was a seller's paradise: demand far exceeded supply, quality was an afterthought, and innovation meant changing from white to off-white. Customers literally queued outside factories with cash in hand.

Around 1980, Mr. Somany received a license to set up a sanitaryware manufacturing facility—a piece of paper that would change everything. But why sanitaryware? The answer combines family DNA with economic logic. Somany had watched his father's company HSIL dominate the market for two decades. He understood the industry's technical nuances, knew the suppliers, recognized the talent. More importantly, he saw what others missed: sanitaryware wasn't really a commodity business at all. Unlike oil or grains, you could differentiate through design, build brand loyalty, command pricing power. A toilet wasn't just porcelain—it was aspiration, modernity, status.

In 2001, Mr. Somany decided to exit the commodity segment entirely and focus purely on sanitaryware. In those times, the focus of majority of entrepreneurs was to grow their 'empire'. Size meant success. Mr. Somany, by selling the business that he spent most of his life running, showed remarkable maturity. This allowed his entire entrepreneurial energy to be focused on just one business. The decision was well thought out—the sanitaryware business had become quite profitable, and 20 years was enough to understand the difference in economics. He realized sanitaryware inherently has better and more stable margins and return profiles compared to the commodity business.

This wasn't diversification—it was escape. Escape from commodity hell into a business where brand mattered, where manufacturing excellence created moats, where you could actually shape your destiny. The stage was set for one of Indian manufacturing's most unlikely success stories.

III. Building the Foundation (1980-2000)

The location seemed insane. Kadi, in Gujarat's Mehsana district, was known for exactly one thing: oil fields. Not ceramics expertise. Not skilled labor. Not proximity to raw materials. When Vikram Somany decided to build his sanitaryware plant there in 1980, industry veterans thought he'd lost his mind. Twenty years later, they'd realize he was playing three-dimensional chess while everyone else played checkers.

The masterstroke was natural gas. While competitors hauled coal hundreds of kilometers to fire their kilns, Somany tapped directly into the oil fields' associated gas—cleaner, cheaper, more consistent. This wasn't just a cost advantage; it fundamentally altered the economics of production. Natural gas burns cleaner, reducing defects. It heats more evenly, improving quality. It costs less, enabling price competitiveness without sacrificing margins. That single decision—geography as strategy—would provide CERA a structural cost advantage that persists to this day.

The business broke even in the first month itself. This is a stupendous achievement, that too in a complex business like sanitaryware which sees substantial teething issues in the beginning. How does a capital-intensive manufacturing business break even in month one? Mr. Somany staffed CERA with many ex-employees of Hindustan Sanitaryware—instant expertise without the learning curve. While competitors struggled with technical issues for years, CERA started with decades of accumulated knowledge.

But the real revolution happened in the glazing department. In 1980's India, sanitaryware meant white. Maybe ivory if you were adventurous. The market offered seven colors total. CERA launched with twenty-one. Twenty-one! In a seller's market where customers would buy anything available, Somany was offering choice. Critics called it wasteful—why complicate production when everything sells anyway? They missed the point entirely. Those fourteen extra colors weren't about current demand; they were about building a brand that would matter when competition arrived.

The production philosophy was counterintuitive: excellence in a seller's market. While competitors maximized volume with acceptable quality, CERA obsessed over reducing defects, improving finish, perfecting curves. Remember, this was an era when customers would accept minor cracks because alternatives didn't exist. Somany was preparing for a market that didn't yet exist—one where customers had choice, where brand mattered, where quality commanded premiums.

Distribution in pre-liberalization India required a different playbook. You couldn't advertise on television (there was one channel). You couldn't build massive showrooms (real estate was controlled). You couldn't even transport freely across state borders (permit raj). CERA's solution? Build deep relationships with a smaller set of dealers, offer better margins, provide superior service, and most importantly—never run out of stock. In a shortage economy, availability was marketing.

The numbers tell a remarkable story. From a standing start in 1980, CERA built capacity methodically—1,000 pieces per day initially, doubling every few years, reinvesting every rupee of profit. No debt-fueled expansion. No marquee acquisitions. Just compound growth through operational excellence. By the late 1990s, CERA had quietly become a formidable player, though still dwarfed by HSIL's inherited dominance.

His new company was named Cera Sanitaryware and was incorporated in 1998, marking a formal corporate restructuring that would set the stage for the next phase of growth. The foundation was complete: advantaged manufacturing location, superior product range, loyal dealer network, debt-free balance sheet. As India stood on the cusp of economic liberalization, CERA was perfectly positioned for what came next.

IV. The Liberalization Era & Scaling Up (1990s-2010)

July 24, 1991: Finance Minister Manmohan Singh rises in Parliament to present the Union Budget. His words would unleash forces that would transform every Indian industry: "No power on earth can stop an idea whose time has come." For CERA, liberalization was both threat and opportunity. Foreign brands could now enter India. Import duties would fall. The seller's market would end. But for a company that had spent a decade preparing for competition that didn't exist, this was the moment of vindication.

The immediate impact was brutal. International brands flooded the market with designs Indians had never seen—European minimalism, American functionality, Japanese technology. Suddenly, CERA's 21 colors looked quaint. The new battlefield wasn't variety but sophistication. While established players like HSIL leveraged their incumbency advantage, CERA faced an existential question: stick to the mass market or move upmarket? By 2002, Vikram Somany tightened his reins on Cera Sanitaryware and brought the first hand experience he had gained in the past two decades of being in the market. The progress was accelerated by the entry of Vidush Somany, Mr. Somany's only son into the business in 2004. Vidush Somany, who joined in 2004, played a pivotal role in the steady growth of the brand all over the country. This wasn't just succession planning—it was transformation.

From 2002-2012, sales improved nine-fold, PAT margins improved nine-fold while returns went from mid-single digits to low-30s. Think about those numbers: not nine-fold over a century, but in a single decade. The company's revenues and profits were increasing by more than 20%-25% every year since Vidush's joining. This wasn't lottery-ticket growth from a low base—CERA was already a substantial business. Something fundamental had changed.

The secret sauce was systematic capability building. Even when it was a tiny entity with sales of less than $10 million, the Somany family spent considerable amount to improve its manufacturing process by employing foreign consultants. In 2008, they also employed a ceramic scientist of repute on their board. While competitors fought price wars, CERA invested in reducing defects, improving efficiency, maximizing throughput.

The management philosophy during this period crystallized into something distinctive. In conference calls across different years, the top management responds similarly to questions on market leadership - that the focus is manufacturing good products, marketing them well and ensuring they are available when the customers need them; and then the outcome will take care of itself. In short, the focus is the process and not the end-result. This wasn't corporate speak—it was lived reality.

Market dynamics were shifting dramatically. The real estate boom from 2003-2008 drove unprecedented demand for premium sanitaryware. Nuclear families were replacing joint families, creating more households. Bathrooms were becoming lifestyle statements, not just functional spaces. CERA rode this wave perfectly—premium enough to capture value, accessible enough to achieve scale.

Competition intensified as global players recognized India's potential. Roca acquired Parryware. Jaquar expanded aggressively into sanitaryware from faucets. Chinese imports flooded the lower end. Yet CERA maintained its trajectory, proving that in India's fragmented market, execution beats strategy every time.

The manufacturing expansion during this period was methodical. Capacity grew from 1 million pieces to over 2.2 million, but always funded through internal accruals. No debt binges. No dilutive equity raises. Just reinvested profits funding measured growth—a rarity in capital-intensive manufacturing.

By 2011, CERA had achieved something remarkable: it was simultaneously growing faster than the market, improving margins, and maintaining near-zero debt. The company seemed unstoppable, with Vidush Somany, eventually appointed as the Executive Director of the business, fully involved in running it while Vikram Somany was slowly taking a back seat. Everything was perfectly positioned for the next phase of growth. And then tragedy struck.

V. Crisis & Resilience: The 2012 Tragedy

In Aug 2012, there was news of the sudden demise of Vidush Somany. He was 31 years old.

The news sent shockwaves through India's business community. Vidush Somany, the then Executive Director of Cera Sanitary Ware Ltd. and the only son of Shree Vikram Somany whose sad and sudden demise happened at the age of 31. This wasn't just a family tragedy—it was an existential crisis for CERA. The heir apparent who had driven 25% annual growth for eight years was gone. The succession plan everyone assumed would unfold over decades had evaporated overnight. The stock market's reaction was swift and brutal. Questions swirled: Who would lead operations? Would the family sell? Could CERA maintain its growth trajectory? People had started questioning succession plans at Cera Sanitaryware. For a company where the founding family was synonymous with the brand, the uncertainty was paralyzing.

What happened next revealed the depth of CERA's institutional strength. Within weeks—not months—the board of directors of the company at its meeting held on September 12, 2012, appointed Shri. S.C. Kothari, as C.E.O. of the company. The company brought back Mr. Kothari as CEO in September 2012. He had retired earlier. This wasn't a panicked external hire or a placeholder appointment. Kothari knew CERA's culture, understood its dealers, had relationships with suppliers. The message was clear: continuity, not disruption.

Meanwhile, Vikram Somany responded to personal tragedy with remarkable fortitude. Mr. Somany had always had a strong focus on delegation and employee empowerment. In the past, an employee earned more than Vikram Somany himself, an indication of his ability to recognize and pay for talent, and lack of ego. For me, the grace and strength with which Mr. Somany dealt with this tragedy is worth remembering and emulating. Rather than withdraw, he doubled down—literally. Somany began systematically buying shares from the open market, signaling his unwavering commitment to CERA's future.

The operational response was equally impressive. Production schedules weren't disrupted. New product launches continued. Dealer relationships remained intact. The company that Vidush had helped build over eight years didn't just survive his absence—it thrived. This wasn't luck; it was the result of building systems larger than any individual, of creating a culture where excellence was institutionalized, not personalized.

The numbers tell a story of extraordinary resilience. Despite GST implementation, demonetization, and real estate headwinds, revenues and profits grew 6x since 2012. Six times! Most companies would have been satisfied with maintaining status quo after such tragedy. CERA accelerated. Family continuity was addressed thoughtfully. Eventually he brought his daughter, Deepshika Khaitan, on to the board as the non-Executive Chairman to further indicate the family's long-term intention to be part of the business. Deepshikha Khaitan, Vice Chairman, CERA Sanitaryware Limited, represents the next generation—actively associated with CERA for over 7 years, involved in Design Innovation, Product, R&D, Channel Outreach and Sales with equal focus on profitability and product development.

The institutional response was equally important. Rather than depending solely on family leadership, CERA strengthened its professional management team. A new COO was appointed from within, signaling internal bench strength. Key executives who had worked with Vidush stepped up, ensuring operational continuity. The message to dealers, suppliers, and investors was unambiguous: CERA was bigger than any individual.

What's remarkable about this period isn't just survival—it's acceleration. New products launched on schedule. The faucets business, despite teething problems, expanded. Tiles were introduced as a new category. The company that could have retreated into defensive mode instead pushed forward aggressively.

Looking back, the 2012 crisis revealed CERA's true strength: institutional resilience built over three decades. The systems Vikram Somany had painstakingly created—from manufacturing excellence to dealer relationships—proved robust enough to withstand the ultimate test. As one investor noted, "You should never, when facing one tragedy, let it increase to two or three through failure of will." CERA didn't just avoid additional tragedy; it transformed crisis into catalyst.

VI. Product Expansion & Market Positioning (2010-Present)

Walk into a CERA Style Studio today—14,000 square feet across two floors in Hyderabad's Jubilee Hills—and you'll witness a transformation that would have seemed impossible in 2010. What began as a pure-play sanitaryware manufacturer now offers over 20,000 SKUs across sanitaryware, faucets, tiles, wellness products, kitchen sinks, and mirrors. This isn't diversification for its own sake; it's a calculated bet on becoming India's one-stop bathroom solutions provider.

The faucets gamble deserves special attention. The market size of faucet ware is more than double of that of the size of sanitary ware—a ₹6,000 crore opportunity versus sanitaryware's ₹3,000 crores. The synergies seemed obvious: same dealers, same customers, complementary products. But execution proved brutal. Faucets require entirely different manufacturing competencies—precision metalworking versus ceramic molding, chrome plating versus glazing, completely different supply chains. Early products faced quality issues. Margins compressed. Growth stalled.

Yet CERA persisted. With established brand and settled distribution channel of over 6000 retailer dealers, they were poised to capture larger share. The company set up a state-of-the-art manufacturing unit for faucets in Kadi with a daily production of over 7,000 pieces, the faucet plant has latest automatic chrome-plating facilities, low pressure die-casting machines. Today, faucets contribute meaningfully to revenues, though margins remain a work in progress.

The tiles entry in 2013 followed a different playbook entirely. Rather than manufacturing—which would require massive capital investment—CERA chose an asset-light model: import premium tiles from Spain and Italy, leverage the CERA brand, distribute through existing channels. The company launched premium Italian and Spanish designer tiles through exclusive tie-ups with major manufacturers like Rondine, Gigacer, Todagress. Smart? Absolutely. But also an admission that not every product needs to be manufactured in-house.

The product portfolio now spans three distinct brands targeting different segments. Senator serves the mass market. CERA addresses the mid-premium segment. CERA Luxe targets the luxury buyer with imported European designs and smart technology. This isn't just segmentation; it's acknowledgment that India's bathroom market has stratified dramatically, from affordable housing seeking basic functionality to luxury villas demanding Italian marble and Japanese bidets.

Innovation became institutionalized during this period. The company introduced 3-D printing technology to convert a product idea to a manufactured sample within a week's time. This technology is unique to CSL and hence, launch of new products has become much faster. Some of Cera's innovations have become benchmark for the industry—like water-saving twin-flush coupled WCs, 4-litre flush WCs, one-piece WCs. The Nano technology ensures a microbial free surface for the products that impedes bacterial growth—marketed brilliantly to hygiene-conscious Indian consumers.

But the real masterstroke was positioning. "Though we have online presence for product promotion, sale through online platforms is currently insignificant. However, we are future-ready. Our current brick-and-mortar distributors are quite well-entrenched," says Deepshikha Khaitan. While competitors chased e-commerce dreams, CERA doubled down on what works in India: dealer relationships, touch-and-feel experiences, local availability.

The sustainability angle emerged as unexpected differentiation. CERA set up wind and solar power for captive use in Gujarat—not just for cost savings but as brand positioning for environmentally conscious consumers. The natural gas advantage from 1980 suddenly looked prescient in an ESG-obsessed world.

By 2024, CERA's transformation was complete: from a single-product manufacturer to a comprehensive bathroom solutions provider. The one-stop shop strategy had worked, though not without casualties. Growth slowed. Margins compressed. Complexity increased exponentially. But in India's fragmented bathroom market, breadth had become its own moat. The company that once competed on 21 colors now competed on 20,000 choices.

VII. Competition & Market Dynamics

Here's a number that should make you sit up: With an installed capacity already in excess of 40 million pieces/year, India is the world's second largest sanitaryware producer. 75% of production comes from Gujarat. Let that sink in—three-quarters of India's toilets originate from a single state. This isn't random clustering; it's the result of deliberate industrial policy, ceramic expertise concentration, and what economists call agglomeration effects.

Major players operating in the India Ceramic Sanitaryware market include HSIL Ltd, Cera Sanitaryware Ltd., Roca Sanitario, S.A. Indian Sanitary Ware Market is dominated by some major key players such as Parryware India, Hindustan Sanitaryware Industries Limited (HSIL), and Cera Sanitaryware dominate the Indian Sanitary Ware Market, though some operate outside Gujarat. The market structure reveals fascinating dynamics. Parryware India, a subsidiary of Roca, has a total capacity of 6.3 million pieces across four facilities in Tamil Nadu, Madhya Pradesh, and Rajasthan. HSIL has a declared capacity of 3.8 million pieces, with plants in Telangana and Haryana. Cera Sanitaryware, the third-largest producer, operates a plant in Mehsana with a capacity of 3.3 million pieces.

The Big Three—HSIL (26% share), Parryware Roca (23%), CERA (18%)—together control 45% of the industry and 65% of the organized market. But here's where it gets interesting: the organized segment dominates the India bath fittings market, commanding approximately 59% of the market share in 2024, while the unorganized sector accounts for the remaining 41%. This means roughly 16 million pieces annually come from small, unbranded manufacturers—CERA's real competition isn't always Kohler; sometimes it's a nameless factory in Morbi selling at 60% of CERA's price.

Competition has evolved dramatically since 2010. Other companies include Jaquar Group, which increased its production to 1.8 million pieces after acquiring Euro Ceramics, and Kohler India, producing 1.5 million pieces annually. International players such as RAK Ceramics, Duravit, and Toto have also established production facilities in India. Toto's plant in Gujarat, with an initial capacity of 500,000 units per year, serves both domestic and overseas markets.

Jaquar deserves special attention as CERA's most formidable competitor. Originally a faucets specialist with 35% market share in that segment, Jaquar entered ceramic sanitaryware in May 2017 by acquiring Euro Ceramics for $15.5 million. Their yearly production capacity was increased in 2018 from 1.2 to 1.8 million pieces. The message was clear: category specialists were becoming full-line competitors.

The MNC invasion accelerated post-2015. Duravit India started its factory in Tarapur producing 200,000 pieces annually with plans for 500,000. Toto's ultra-modern plant in Halol, built with a 6 billion yen investment (around 49 million euros), represents the largest investment made by the group in South Asia. These aren't just manufacturing facilities; they're technology showcases designed to premiumize the market.

Distribution battles have intensified. Large organized players such as Jaquar, Hindware, Roca, Kohler, and Cera have established strong distribution networks and brand recall. These companies are continuously investing in technology upgrades, expanding their manufacturing capabilities, and focusing on innovative designs to provide ergonomically convenient solutions. The game isn't just about products anymore; it's about dealer financing, display quality, service capabilities, and increasingly, digital presence.

Market dynamics are shifting toward premiumization. Premium segment now contributes almost 20% to the overall sanitaryware market revenues. This growth can be attributed to reasons like increasing disposable income, rapid urbanization and changing end user preferences. For CERA, positioned in the mid-to-premium segment, this is both opportunity and threat—opportunity to move upmarket, threat from luxury brands moving down.

The unorganized sector remains stubbornly persistent. The unorganized players manufacture sanitaryware items using conventional technologies and cater mainly to the mass market or low-income strata group. Whereas organized players employ latest world class technologies for production and majorly serve to premium and super-premium market segments. These players compete on price alone, forcing organized players like CERA to justify premium pricing through brand, quality, and service.

Looking ahead, the competitive landscape will be shaped by three forces: consolidation as smaller players exit or get acquired, technology as smart bathrooms become mainstream, and sustainability as water conservation becomes mandatory. The CAGR of the India Ceramic Sanitaryware Market is projected to be 13.64% from 2025 to 2032. In this high-growth market, the question isn't whether CERA can compete—it's whether it can maintain its position as multinationals deploy unlimited capital and digital-first brands challenge traditional distribution.

VIII. Financial Performance & Capital Allocation

The numbers tell a story of disciplined capital allocation meeting growth challenges. Company is almost debt free. Mkt Cap: 8,271 Crore, Revenue: 1,937 Cr, Profit: 246 Cr. Company has been maintaining a healthy dividend payout of 32.5%. The company has delivered a poor sales growth of 9.63% over past five years. That last statistic deserves unpacking—after decades of 20%+ growth, CERA has hit a wall.

The recent quarterly performance reveals the ongoing struggle. Revenue from operations stood at INR 437 crores in Q3 financial year '24 versus INR 456 crores in Q3 financial year '23, a decline of 4.2%. Net profit of Cera Sanitaryware declined 16.38% to Rs 47.06 crore in the quarter ended June 2024. These aren't crisis numbers, but they're far from the heady growth of the Vidush Somany era.

The capital allocation strategy remains conservative to a fault. Long-term debt down at Rs 26 million as compared to Rs 42 million during FY23, a fall of 38.0%. In an industry where competitors leverage balance sheets for rapid expansion, CERA operates virtually debt-free. This is either admirable discipline or missed opportunity, depending on your perspective.

Margin management tells a nuanced story. The gross margin remained stable, and stood at 54.2% in Q3 financial year '24 against 54.5% in Q3 financial year '23. Operating profit margins witnessed a fall and stood at 15.3% in FY24 as against 16.3% in FY23. The company is maintaining pricing power but struggling with operating leverage as growth slows.

Segment performance reveals strategic challenges. For quarter 3 financial year '24, 52% of the top line was from sanitaryware, 36% from faucetware, tiles represented 10% and wellness 2%. On a Y-o-Y basis, faucetware revenues registered an increase of 5%, sanitaryware revenues declined by 8%, tiles decreased by 19% and wellness increased by 29%. The core business is struggling while new ventures show mixed results.

The working capital story is concerning. Current assets rose 12% while revenues stagnated, suggesting either inventory buildup or collection challenges. In a dealer-driven business, working capital management directly impacts returns—and CERA's returns have compressed from the 30% ROCE of the glory days to mid-teens today.

Cash flow generation remains healthy but uninspiring. Cera closed the quarter with cash and cash equivalents up 29% year-over-year and maintained a positive cash flow. But what's the point of generating cash if it's not deployed for growth? The company sits on substantial cash while growth decelerates—a classic value trap scenario.

The dividend policy reflects this conservatism. A 32.5% payout ratio is reasonable, but in a business generating limited growth opportunities, why not return more to shareholders? The answer likely lies in management's belief that growth will return—but after five years of sub-10% revenue growth, that faith seems increasingly misplaced.

Investment in growth has been modest. EBITDA fell to INR 75.41 crores, with the margin down to 16.7% primarily due to increased ad spending aimed at premium product promotion. Increased ad spending is mentioned as a margin pressure, but the amounts are trivial relative to what's needed to compete with Jaquar's marketing blitz or Kohler's brand power.

The post-IPO funding story adds complexity. Post-IPO funding: $11.5M round (2015) from WestBridge Capital, Nalanda Capital, Lighthouse. These sophisticated investors presumably saw something in CERA's future—but nearly a decade later, that vision remains unrealized.

Financial performance must be contextualized within industry dynamics. Real estate headwinds, GST implementation, demonetization—CERA faced multiple shocks. But so did competitors, many of whom navigated better. The question isn't why growth slowed, but why CERA couldn't adapt faster.

Looking ahead, the financial strategy seems stuck between two stools: too conservative to drive aggressive growth, too growth-oriented to maximize cash returns. Without clarity on capital allocation, CERA risks becoming a permanently subscale player in an industry increasingly dominated by giants.

IX. Playbook: Business & Management Lessons

The CERA story offers a masterclass in contrarian thinking that creates lasting advantage. When everyone zigs, zag—but make sure you're zagging toward something valuable, not just away from the crowd.

The Contrarian Geographic Advantage: Setting up in Kadi near oil fields when everyone else clustered in traditional ceramic hubs seemed foolish. But proximity to natural gas created a permanent cost advantage that no amount of operational excellence elsewhere could match. The lesson? Sometimes the best strategy is to find a structural advantage that others can't replicate, even if it means accepting other disadvantages. CERA accepted distance from suppliers and skilled labor pools in exchange for energy costs that competitors couldn't match.

Process Over Outcomes—But Outcomes Matter: Vikram Somany's philosophy of focusing on manufacturing good products, marketing them well, and ensuring availability sounds like management consultant speak. But it worked because it was genuinely lived. When asked about market leadership targets, management consistently deflects to process metrics. This isn't false modesty—it's recognition that in manufacturing, sustainable advantage comes from doing ordinary things extraordinarily well, repeatedly, at scale.

The Talent Paradox: An employee earned more than Vikram Somany himself—this isn't just humility, it's strategic genius. In a relationship business where key salespeople and plant managers hold enormous leverage, paying them well isn't generosity—it's insurance. The best companies make their people rich; the worst make only their owners rich. CERA understood this decades before Silicon Valley made it fashionable.

Crisis as Catalyst: The 2012 tragedy could have destroyed CERA. Instead, it revealed the depth of institutional capability Somany had built. The real lesson isn't about succession planning—though that matters—but about building organizations that can survive their founders. Most family businesses are really founder businesses with family members hanging around. CERA built systems, processes, and culture that transcended individuals.

Premium Positioning in Price-Sensitive Markets: Launching 21 colors when 7 sufficed, focusing on quality in a seller's market, building brand before it mattered—CERA consistently chose the harder path. The lesson? In emerging markets, premium positioning isn't about serving today's premium customers (they don't exist yet); it's about being ready when mass market customers become premium customers. CERA built for India's future, not its present.

The Distribution Moat: In India, distribution is destiny. CERA's 6,000+ dealer network isn't just a sales channel—it's a competitive moat that would take competitors decades and hundreds of crores to replicate. The playbook: invest in dealer relationships during good times so they stick with you during bad times. Finance their inventory, train their staff, protect their margins. Your dealers are your real customers; end consumers are theirs.

Vertical Integration Versus Focus: CERA's expansion into faucets, tiles, and wellness products violated the focus principle—but made strategic sense. In a market where bathroom purchases are project-based, offering complete solutions reduces customer transaction costs. The lesson? Sometimes the right strategy violates conventional wisdom. The key is knowing why you're violating it.

Family Business Governance: Bringing daughter Deepshikha Khaitan onto the board after Vidush's death wasn't nepotism—it was signaling. Family commitment matters in India, where relationships span generations. But CERA balanced this with professional management, independent directors, and institutional processes. The playbook: maintain family control but run it like it's publicly owned (because it partly is).

The Sustainability Edge: Wind and solar power for captive use sounds like ESG window dressing. But in energy-intensive manufacturing, renewable power is a hedge against both energy costs and carbon taxes. CERA's early moves into sustainability weren't about virtue signaling—they were about cost structure. The lesson? The best ESG strategies make business sense even without the ESG label.

Building Moats in Commodity Businesses: Sanitaryware is ultimately porcelain shaped into toilets. Yet CERA built a brand that commands premium pricing for what's essentially a commodity. How? By recognizing that in consumer-facing categories, the product is never just the product. It's the brand, the service, the availability, the dealer relationship, the color options, the warranty, the installation support. CERA built a moat by doing a hundred small things better than competitors bothered to do them.

The Capital Allocation Paradox: CERA's near-debt-free status is both strength and weakness. It survived 2012, 2016 (demonetization), 2017 (GST), and COVID because it had no debt. But it also couldn't scale as fast as leveraged competitors. The lesson? In volatile markets, survival trumps growth. But surviving too conservatively can mean slowly losing relevance.

Management Depth Through Crisis: When SC Kothari returned from retirement to become CEO after Vidush's death, it wasn't desperation—it was depth. CERA had built relationships with former employees that transcended employment. The playbook: treat exits gracefully because you never know when you'll need someone to return.

The CERA playbook ultimately reduces to this: build for the long term in everything—relationships, quality, brand, distribution. Accept lower returns today for sustainable advantage tomorrow. And when crisis strikes—as it inevitably will—your preparation will look like prescience.

X. Analysis & Investment Thesis

The investment case for CERA presents a fascinating paradox: a company with all the ingredients for success—brand, distribution, manufacturing excellence, debt-free balance sheet—yet struggling to deliver growth. At ₹8,300 crores market cap trading at premium multiples, the market is pricing in a return to growth that has remained elusive for five years.

The Bull Case rests on several pillars:

Market tailwinds are undeniable. India sanitaryware market 13.64% CAGR projected through 2032. With India's market context as the world's second-largest sanitaryware producer, the structural growth story remains intact. Rising urbanization, increasing nuclear families, growing hygiene awareness post-COVID, and government initiatives like Swachh Bharat create sustained demand drivers.

CERA's brand strength in the mid-premium segment positions it perfectly for India's consumption upgrade. As customers move from unorganized to organized, from basic to premium, CERA sits in the sweet spot—not as expensive as Kohler, more premium than local brands. The 6,000+ dealer network and 3.3 million piece capacity provide the infrastructure for growth—when it returns.

The company's debt-free status provides strategic flexibility. In an industry where competitors are leveraged and global players need returns, CERA can play the long game. It can accept lower margins to gain share, invest countercyclically, or pursue acquisitions. The balance sheet is a weapon waiting to be deployed.

Management quality, despite recent struggles, remains high. The company that survived its founder's son's death and multiple macro shocks has proven resilience. With family commitment through Deepshikha Khaitan and professional management through seasoned executives, governance remains strong.

The Bear Case is equally compelling:

The company has delivered a poor sales growth of 9.63% over past five years. This isn't a blip—it's a trend. While the market grew, CERA stagnated. Market share has been ceded to aggressive competitors like Jaquar. The core sanitaryware business is declining while new ventures like tiles struggle to gain traction.

Competition is intensifying from every direction. MNCs like Kohler and Toto bring global brands and unlimited capital. Jaquar has successfully transformed from faucets specialist to full-line competitor. Unorganized players continue to undercut prices. New D2C brands target millennials with digital-first strategies. CERA seems caught in the middle—too small to match MNC scale, too traditional to compete with digital natives.

Real estate headwinds persist. The Indian property market's structural issues—inventory overhang, delayed projects, financing challenges—directly impact sanitaryware demand. With real estate cycles typically lasting 7-10 years, the recovery may be prolonged.

Category dynamics are challenging. Sanitaryware is a derived demand product—you don't wake up wanting a new toilet. Purchase cycles are long (10-15 years), price sensitivity is high, and differentiation is difficult. Unlike tiles where fashion drives replacement demand, sanitaryware replacement is purely functional.

Valuation Considerations:

At current levels, CERA trades at premium multiples to its history despite deteriorating fundamentals. The market is paying for quality and potential, but how long can premium valuations sustain without growth? Comparison with peers reveals the challenge: HSIL trades at similar multiples with better growth, Jaquar (if listed) would command higher multiples given superior execution.

The key question for investors: Is this a value trap or a coiled spring? The answer depends on whether you believe CERA's growth challenges are cyclical or structural. If real estate recovers and CERA regains its mojo, current valuations could prove reasonable. If the company has permanently lost its edge, further derating seems likely.

The Sustainability Angle:

ESG considerations increasingly matter. CERA's renewable energy investments, water-saving products, and governance standards position it well for ESG-focused funds. But does ESG matter in Indian mid-caps? The jury's out, but global trends suggest it will matter more over time.

The Investment Decision:

CERA represents a classic "quality at the wrong price" dilemma. Everything about the company screams quality—the business, the management, the balance sheet. But quality without growth is just an expensive bond. For value investors, CERA needs to become cheaper or growth needs to return. For growth investors, there are better stories elsewhere. For quality investors, the price demands perfection the company isn't currently delivering.

The most likely scenario? CERA muddles through—not failing but not excelling, generating high single-digit returns that disappoint growth investors but satisfy conservative ones. The transformational outcome—through successful new products, acquisitions, or market share gains—remains possible but increasingly improbable.

Perhaps the real lesson is that in investing, as in business, timing matters. CERA was a phenomenal investment from 2002-2012. Today, it's a good company at a full price facing structural headwinds. Sometimes the best investment decision is to admire a company from afar while deploying capital where the risk-reward is more favorable.

XI. Future & Strategic Options

The path forward for CERA requires confronting an uncomfortable truth: the strategies that built the company may not be the ones that secure its future. At an inflection point between remaining a successful regional player or becoming a national champion, CERA faces choices that will define its next decade.

Next Generation Leadership Transition

The elephant in the room is succession. Vikram Somany, now in his 80s, has led CERA for over four decades. Deepshikha Khaitan represents family continuity but hasn't been positioned as an operational successor. The professional management team, while competent, lacks a visible leader with the founder's vision and drive.

The template exists in Indian business—look at how Godrej or Marico managed generational transitions. CERA needs to clarify whether the future is family-led, professionally-managed, or some hybrid. Ambiguity creates uncertainty, and uncertainty destroys value. The board must act decisively—either prepare Deepshikha for operational leadership or identify and empower a professional CEO with full autonomy.

International Expansion Opportunities

India sanitaryware market's projected 13.64% CAGR sounds impressive until you realize it's from a small base. The real opportunity might lie beyond India's borders. Middle East and Africa present natural markets—similar price sensitivity, appreciation for value, growing construction sectors. CERA's cost structure could compete effectively against Chinese imports that currently dominate these markets.

But international expansion requires capabilities CERA hasn't demonstrated—managing foreign subsidiaries, navigating different regulatory environments, building new distribution networks. The conservative approach would be exports through agents. The bold move would be local manufacturing through joint ventures. History suggests CERA will choose conservatism, potentially missing a generational opportunity.

M&A Possibilities in Fragmented Market

With 41% of the market still unorganized and numerous small players struggling post-GST, consolidation seems inevitable. CERA's debt-free balance sheet positions it as a natural acquirer. Targets could include regional brands with strong local distribution, distressed assets from overlevered competitors, or capability acquisitions in adjacent categories.

The Jaquar example is instructive—they acquired Euro Ceramics for $15.5 million and gained 1.8 million pieces capacity. CERA could execute multiple such deals, rapidly scaling capacity and market presence. But acquisition requires skills CERA hasn't shown—integration capabilities, cultural flexibility, risk appetite. The company that grew organically for 40 years must learn new tricks.

Technology Integration: Smart Bathrooms and IoT

The bathroom of 2035 won't just be about sanitaryware—it'll be about wellness, monitoring, and connectivity. Smart toilets that analyze health indicators, mirrors with embedded displays, voice-controlled showers—science fiction becoming reality. Toto already sells toilets costing more than motorcycles. Kohler has entire smart bathroom ecosystems.

CERA must decide: compete in smart bathrooms or cede the premium segment? The investment required is substantial—R&D, partnerships with tech companies, entirely new manufacturing capabilities. But not investing guarantees irrelevance in premium segments. The middle path—licensing technology from global partners—might preserve capital while maintaining relevance.

The Affordable Housing Opportunity

India needs 10 million affordable homes annually. Each needs a bathroom. This isn't CERA's traditional market—it requires different products (smaller, simpler, cheaper), different distribution (direct to builders), different economics (volume over margin). But the scale is staggering.

The challenge is avoiding commoditization. How does CERA serve affordable housing while maintaining brand premium? The answer might be a separate brand, distinct manufacturing, dedicated team—essentially a new business. Does CERA have the organizational capability to run multiple businesses? Evidence suggests otherwise.

Can CERA Become India's Kohler?

This is the billion-dollar question. Kohler is a 150-year-old, $8 billion company dominating American bathrooms. Can CERA replicate this in India? The parallels exist—family-owned, manufacturing excellence, premium positioning. But differences matter too—Kohler had first-mover advantage, a protected home market, and decades of consolidation.

CERA's path to becoming India's Kohler requires three transformations. First, from regional to national—strengthening presence in South and East India where it's weak. Second, from product to solutions—offering complete bathroom experiences, not just components. Third, from premium to luxury—building aspirational brands that command Kohler-like pricing.

The Platform Play

A radical option: become a platform, not just a manufacturer. Leverage the dealer network and brand to distribute other home improvement products. Aggregate demand from dealers to negotiate better terms with suppliers. Provide financing to dealers and customers. Essentially, become the Amazon of bathrooms.

This requires different thinking—from manufacturing-centric to distribution-centric, from product focus to service focus. It's not clear CERA has the DNA for this transformation. But with physical distribution increasingly valuable in India's fragmented markets, the dealer network might be CERA's most undervalued asset.

The Sustainability Leadership Position

Climate change and water scarcity will reshape bathrooms. Water-saving products will shift from premium features to regulatory requirements. Carbon-neutral manufacturing will become table stakes. CERA's early investments in renewable energy provide a foundation, but much more is needed.

The opportunity is to lead, not follow—set industry standards for water conservation, pioneer sustainable materials, create India's first carbon-neutral sanitaryware plant. This positions CERA for regulatory tailwinds and creates differentiation competitors can't easily match. But it requires investment with uncertain returns—anathema to CERA's conservative culture.

The Strategic Choice

CERA faces a fundamental strategic choice: remain a successful, profitable, mid-sized player generating steady but unspectacular returns, or transform into something larger but riskier. The former preserves the company's culture and legacy but risks gradual irrelevance. The latter offers growth but requires capabilities CERA hasn't demonstrated.

The most likely path? Incremental evolution rather than revolutionary change. CERA will expand gradually, add products selectively, invest cautiously. It will remain a good company generating decent returns. But without boldness, it won't become a great company defining India's bathroom industry.

The tragedy isn't that CERA will fail—it won't. The tragedy is that it might not achieve its full potential. In a market growing at 13.64% CAGR, with structural advantages and strong foundations, CERA should be conquering, not surviving. Whether it finds the courage to transform remains the question that will define its next chapter.

XII. Recent News

The most significant recent development is CERA's share buyback program announced on August 5, 2024, with a buyback price of Rs 12,000 per share and record date of August 16, 2024. The tender process commenced on August 22, 2024 and closed on August 28, 2024. The issue size was 1,08,333 equity shares at ₹12,000 per share aggregating up to ₹130.00 Crores.

This buyback signals management's confidence in the business despite recent challenges, though the acceptance ratio for retail investors (holding shares worth less than Rs 2 lakhs on the record date) was just 1%, suggesting limited participation opportunity for small shareholders.

Q2 FY2025 Performance Shows Mixed Signals

Cera Sanitaryware's net profit in Q2FY25 jumped 13.7% year-on-year to Rs 91.1 crore, compared to Rs 80.1 crore in Q2FY24. Revenue rose 20% to Rs 523.7 crore in Q2FY25. EBITDA grew 27.5% Y-o-Y to Rs 146.14 crore, with EBITDA margin improving to 27.9% from 26.2%. However, this followed a weak Q1 where net profit declined 16.38% to Rs 47.06 crore in the quarter ended June 2024, with sales declining 6.51% to Rs 400.71 crore.

Stock Performance Reflects Challenges

Market cap stands at 8,271 Crore (down -36.9% in 1 year), reflecting investor concerns about growth prospects. Shares have a 52-week range of Rs 10,789.95 - 6,591.20 on the NSE. Cera Sanitaryware shares have dropped 11% year-to-date.

Corporate Restructuring and Focus

Cera Sanitaryware, formerly known as Madhusudan Oils and Fats, was incorporated on July 17, 1998. The company specialises in manufacturing and marketing building products including sanitaryware, faucetware, and bathware. Additionally, Cera leverages non-conventional renewable energy sources such as wind and solar power to meet its captive energy requirements in Gujarat.

Operational Updates

The CERA sanitary ware factory in Kadi in North Gujarat is the largest single-site plant in India with a capacity of 3 million units per year. The state-of-the-art faucet manufacturing plant with a capacity of 7,200 pieces per day is equipped with the latest low-pressure die-casting machines, an automatic chrome plant, and a range of CNC and automatic polishing machines.

The recent news paints a picture of a company trying to navigate challenging market conditions through financial engineering (buyback) rather than operational improvement. While Q2 showed recovery, the volatility in quarterly performance and significant stock price decline suggest deeper structural issues remain unresolved.

XIII. Links & Resources

Annual Reports and Investor Presentations - CERA Sanitaryware Official Website: https://www.cera-india.com/ - Latest Annual Reports: Available on BSE/NSE websites - Investor Presentations: Company investor relations section

Industry Reports and Analysis - India Ceramic Sanitaryware Market analysis by Coherent Market Insights - projecting market size of US$ 10,635.3 Mn by 2030 with CAGR of 13.64% from 2025 to 2032 - Indian Sanitary Ware Market report by Maximize Market Research - valued at USD 812.17 Billion in 2023 with expected CAGR of 7.38% - Ceramic World Web analysis on Indian sanitaryware industry - India as world's second largest producer with 75% from Gujarat

Market Research Platforms - Screener.in - Comprehensive financial analysis and peer comparison - Trendlyne - Quarterly results and financial statements - Tijori Finance - Market share and product geography data - ValuePickr Forum - Investor discussions and analysis

Books and Long-form Articles - "Cera Sanitaryware - Strength in the depth of darkness" by Lucky Marshmallow (Substack) - Various industry reports on Indian ceramic and sanitaryware sector evolution - Case studies on family business management in Indian manufacturing

Relevant Podcasts and Interviews - MoneyControl interviews with Vikram Somany (referenced but specific links not available) - Industry leader interviews in Entrepreneur India on legacy businesses

Academic Papers and Industry Studies - Studies on Gujarat's dominance in Indian sanitaryware production - Research on organized vs unorganized sector dynamics in Indian manufacturing - Papers on family business succession in emerging markets

Regulatory Filings and Exchanges - BSE (Stock Code: 532443) - NSE (Symbol: CERA) - SEBI filings for corporate governance and disclosures

Industry Associations and Bodies - Indian Council of Sanitaryware Manufacturers (INCOSAM) - Construction Industry Development Council (CIDC) - Builders Association of India (BAI)

Competitor Resources - HSIL Limited (Hindustan Sanitaryware) - Jaquar Group - Parryware (Roca India) - Industry comparison tools on financial platforms

This comprehensive resource list provides investors, analysts, and industry observers with the tools needed to conduct deeper research into CERA Sanitaryware and the broader Indian sanitaryware industry. The combination of financial data, industry reports, and qualitative analysis offers multiple perspectives on the company's position and prospects.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube