Bandhan Bank: From Village Microfinance to Universal Banking Giant

I. Introduction & Episode Setup

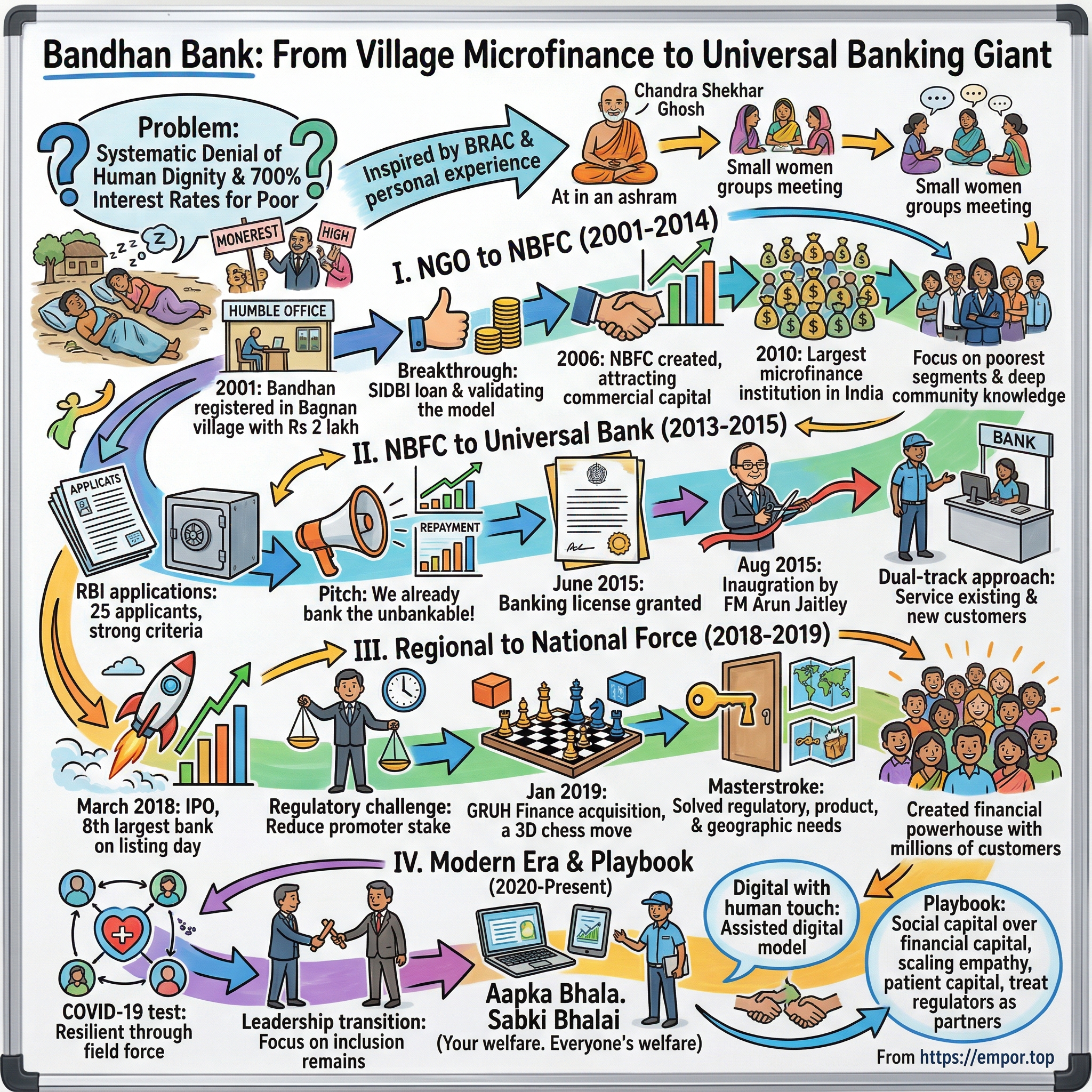

Picture this: A young man in rural Bangladesh watches villagers sleep for three consecutive days without food, their hunger so profound it forces them into unconsciousness rather than endure the pain. That image—seared into Chandra Shekhar Ghosh's memory in the 1990s—would eventually birth one of India's most remarkable banking stories. On August 23, 2015, when Finance Minister Arun Jaitley inaugurated Bandhan Bank in Kolkata, it marked the first universal bank to emerge from Eastern India since Independence. More remarkably, it was the first microfinance institution globally to transform into a universal bank.

The numbers tell only part of the story: From a Rs 2 lakh bootstrap in 2001 to becoming India's 8th largest bank by market capitalization on its IPO day in 2018, Bandhan's trajectory defies conventional banking wisdom. Today, with a market cap exceeding Rs 26,000 crore, it serves over 3.45 crore customers through 6,300+ outlets across India. But the real story isn't about size—it's about how a sweet shop owner's son from Tripura built a financial institution that would challenge centuries-old lending practices and create a new template for inclusive banking.

This is a story of three transformations: first, from NGO to NBFC; second, from NBFC to universal bank; and third, from regional microfinance player to national banking force through strategic M&A. Each transition required not just capital and regulatory navigation, but a fundamental reimagining of what banking could be for India's underserved millions. The Bandhan playbook offers lessons in patient capital deployment, regulatory chess, and most critically, how to scale empathy without losing touch with grassroots reality.

II. The Founder's Journey: Chandra Shekhar Ghosh

The sweet shop in Agartala, Tripura, where young Chandra Shekhar Ghosh worked alongside his father, seemed worlds away from the gleaming towers of Mumbai's banking district. Born in 1960 into a middle-class Bengali family, Ghosh's early years were marked by the kind of financial constraints that would later inform his banking philosophy. His father's modest sweet shop business taught him the basics of credit and cash flow—vendors needed advances to supply ingredients, customers sought credit during festivals, and trust, not collateral, governed most transactions.

In 1978, Ghosh enrolled at Dhaka University to study Statistics, a decision that required him to live in an ashram and tutor children to afford his education. The spartan conditions—shared rooms, simple meals, rigid schedules—instilled a discipline that would later characterize Bandhan's operational culture. But it was his exposure to rural Bengal's economic realities during university breaks that began shaping his worldview. He witnessed how lack of formal credit trapped families in generational poverty, forcing them to borrow from moneylenders at rates that would make modern-day payday lenders blush.

The turning point came when Ghosh joined BRAC, Bangladesh's largest NGO, in the early 1990s. BRAC had pioneered a microfinance model that seemed almost magical in its simplicity: small loans to groups of women, peer pressure ensuring repayment, and gradual graduation to larger credit amounts. But it was a field visit to Rangpur, a district in northern Bangladesh, that provided his Damascus moment. Ghosh encountered entire villages where hunger had become so routine that families would simply sleep through it—three, sometimes four days without food, choosing unconsciousness over the agony of empty stomachs. "That's when I realized," Ghosh would later recount, "that poverty wasn't just about lack of money. It was about the systematic denial of human dignity."

Returning to India, Ghosh conducted his own research in Kolkata's sprawling informal markets. What he discovered defied economic logic: vegetable vendors were paying moneylenders interest rates of 700% annually—10% per day in some cases—yet they called these predatory lenders their "godsends." Why? Because formal banks wouldn't even let them through the door. A vendor needing Rs 500 to buy vegetables at dawn for sale by noon had no options. Banks demanded collateral, proof of income, permanent addresses—documents that existed in a parallel universe from these vendors' reality.

By 2000, Ghosh had seen enough. Despite holding a stable Rs 5,000 monthly job—decent money for the time—he decided to quit and start his own microfinance operation. The family reaction was predictable: his wife Nilima wept, relatives questioned his sanity, and friends warned about the folly of leaving secure employment. But Ghosh had calculated something they hadn't: the market opportunity in serving India's unbanked wasn't just massive—it was transformational. If he could crack the code of lending profitably to the poor, he wouldn't just build a business; he'd redefine banking itself.

The philosophy that would guide Bandhan was crystallizing: banking wasn't about buildings or technology or even capital—it was about understanding human behavior at the intersection of poverty and aspiration. The poor weren't unbankable; they were just being offered the wrong products by institutions that didn't understand their lives. This insight would prove worth Rs 26,000 crore.

III. Building Bandhan: The NGO to NBFC Evolution (2001–2014)

The village of Bagnan, 60 kilometers from Kolkata, hardly seemed the birthplace of a banking revolution. Yet in July 2001, when Ghosh registered Bandhan as a not-for-profit entity under the West Bengal Societies Registration Act, this dusty hamlet became ground zero for an experiment in financial inclusion. The initial capital—Rs 2 lakh cobbled together from friends and family—wouldn't even qualify as seed funding by today's standards. Banks, ironically, refused to lend money for lending to the poor, viewing it as charity rather than business.

For eighteen months, Ghosh and his skeleton team operated on fumes, proving the model one loan at a time. They developed what would become the Bandhan methodology: individual loans delivered through group formation, where five to eight women would form a unit, meeting weekly to discuss finances and ensure mutual accountability. The genius wasn't in the structure—similar models existed—but in the execution. Bandhan recruited loan officers from the communities they served, often hiring candidates with third-division marks in higher secondary education, around 23 years old, who understood local dialects and social dynamics. September 2002 marked the breakthrough: SIDBI approved Rs 20 lakh loan after 18 months of proving the model. This wasn't just capital—it was validation. The money allowed Bandhan to expand from one village to ten, then fifty, then hundreds. The repayment rates were astonishing: 98-99%, demolishing the myth that the poor were credit risks. The secret lay in the selection process and ongoing support. Bandhan didn't just lend money; they provided financial literacy training, helped borrowers plan businesses, and created a social infrastructure where default meant letting down not just a faceless bank but neighbors and friends.

By 2006, the model had proven so successful that Ghosh made a crucial strategic decision: acquire an existing NBFC license rather than wait for regulatory approval. Bandhan acquired a Non-Banking Financial Company and created Bandhan Financial Services Private Limited to scale up its microfinance activities. This move transformed Bandhan from an NGO dependent on donor funding to a for-profit entity that could attract commercial capital. The timing was perfect—India's microfinance sector was exploding, with international investors suddenly awakening to the potential of financial inclusion. By 2010, Bandhan became the largest microfinance institution in the country, a remarkable achievement in less than a decade. The numbers were staggering: over 80 lakh women touched, Rs 10,000+ crore in cumulative disbursements, and operations across 19 states. But what set Bandhan apart wasn't scale—it was discipline. While competitors chased growth at any cost, Bandhan maintained its focus on the poorest segments, refusing to drift upmarket despite the temptation of higher margins.

The culture Ghosh built was deliberately contrarian. In an industry obsessed with MBAs and pedigreed hires, Bandhan recruited from the communities it served. The typical loan officer was a local youth with modest educational qualifications but deep community knowledge. Training was intensive—six months of classroom and field work—but the investment paid off in lower delinquency rates and deeper customer relationships. By 2014, Bandhan had created an army of 12,000+ employees who didn't just understand poverty; they had lived it.

As the NBFC grew, Ghosh began preparing for what seemed impossible: transforming a microfinance company into a universal bank. The groundwork was meticulous—building treasury operations, risk management systems, technology infrastructure—all while maintaining the core microfinance business. When the RBI announced in 2013 that it would issue new banking licenses, Bandhan was ready. The fourteen-year journey from NGO to NBFC had been preparation for this moment.

IV. The Banking License: Breaking New Ground (2013–2015)

The Reserve Bank of India's February 2013 announcement inviting applications for new banking licenses triggered a gold rush. Twenty-five applicants, including corporate giants, NBFCs, and microfinance institutions, threw their hats in the ring. For Bandhan, this wasn't just an opportunity—it was the culmination of Ghosh's vision. A banking license would mean access to low-cost deposits, ability to offer full-service banking, and most importantly, legitimacy in the eyes of customers who still viewed microfinance with suspicion.

The application process was grueling. RBI's criteria were stringent: minimum capital of Rs 500 crore, complex corporate structure requirements, and detailed business plans demonstrating how the bank would further financial inclusion. Bandhan's pitch was simple yet powerful: they had already banked the unbankable. With 67 lakh active microfinance borrowers and a proven track record of 99%+ repayment rates, they weren't promising financial inclusion—they were already delivering it.

In April 2014, Bandhan received in-principle approval from the RBI. On June 17, 2015, RBI granted the banking licence to Bandhan, making it the first microfinance institution to become a universal bank in India. The transformation required herculean effort. Bandhan had to create a non-operative financial holding company (NOFHC) structure, transfer the microfinance portfolio to the new bank, build banking infrastructure from scratch, and hire thousands of employees—all within 18 months.

The capital raise was equally impressive. Bandhan started with Rs 2,570 crore in capital, more than five times the RBI's minimum requirement. The investors - GIC Private Limited, International Finance Corporation (IFC) and the Small Industries Development Bank of India (SIDBI) – provided a solid backing. This wasn't just about meeting regulatory requirements; it was about signaling strength and stability to a market skeptical of a microfinance institution's ability to run a universal bank.

The Bank commenced operations on August 23, 2015 with 501 branches, 2,022 Doorstep Service Centres (DSCs – the erstwhile microfinance branch offices) and 50 ATMs spread across 24 States. The then Union Finance Minister, Arun Jaitley, inaugurated the Bank in Kolkata. The launch was symbolic on multiple levels: the first bank from Eastern India since Independence, the first microfinance institution globally to become a universal bank, and proof that financial inclusion could be profitable.

The operational challenge was immense. On day one, Bandhan had to seamlessly transfer 67 lakh microfinance accounts to the banking platform, train thousands of employees on banking operations, and ensure business continuity across 2,500+ touchpoints. The Doorstep Service Centres—essentially the old microfinance branches—continued to serve existing customers while new bank branches offered the full suite of banking products. This dual-track approach ensured that the core microfinance customers weren't abandoned in the rush to become a "real" bank.

The market's initial reaction was mixed. While the achievement was historic, questions remained: Could a microfinance-focused institution attract deposits? Would the universal banking model dilute the social mission? How would Bandhan compete with established players? Ghosh's response was characteristically measured: "We're not trying to be everything to everyone. We're building a bank for the people traditional banks ignore."

The early numbers validated the strategy. Within six months, deposits crossed Rs 10,000 crore, the microfinance portfolio continued growing at 30%+ annually, and new products like affordable housing loans and MSME lending gained traction. But the real victory was cultural: Bandhan had proven that the poor were bankable, not as charity cases but as profitable customers. The banking license wasn't just a regulatory approval—it was validation of an entirely new banking philosophy.

V. IPO & Public Markets Entry (2018)

March 27, 2018, marked another watershed moment as Bandhan Bank's shares began trading on the BSE and NSE. The IPO, comprising 9.76 crore fresh shares and a 2.16 crore share offer for sale, was priced at Rs 375 per share. The market's verdict was immediate and emphatic: the stock opened at Rs 485, a 29% premium, valuing the bank at over Rs 80,000 crore. It emerged as the eighth most-valued bank in India based on market capitalisation on the day of its listing on stock exchanges.

The IPO wasn't just about raising capital—Rs 4,473 crore from the fresh issue would strengthen the capital base—but about solving a unique regulatory puzzle. RBI regulations required Bandhan's promoter (Bandhan Financial Holdings) to reduce its stake from 82% to 40% within three years of receiving the banking license. The public listing was the first step in this mandated dilution, bringing the promoter stake down to around 70%.

The investor roadshow revealed fascinating dynamics. International investors were intrigued by the microfinance-to-banking story but worried about asset quality in unsecured lending. Domestic institutions saw the Eastern and rural market dominance as both opportunity and risk. Retail investors, particularly in West Bengal, viewed Bandhan as "their" bank—a homegrown success story. The IPO was oversubscribed 14.6 times, with the QIB portion seeing 47.8 times subscription.

But the honeymoon was short-lived. By September 2018, RBI imposed restrictions on Bandhan for not meeting the promoter stake dilution timeline—freezing branch expansion, capping MD Ghosh's remuneration, and requiring prior approval for opening new branches. The stock price, which had touched Rs 650 in August, began a gradual decline. The message was clear: regulatory compliance wasn't negotiable, even for a poster child of financial inclusion.

The restrictions forced Bandhan to get creative. With organic branch expansion frozen, growth had to come from deepening existing relationships, digital channels, and most importantly, inorganic expansion. The search for an acquisition target wasn't just about growth—it was about survival. Bandhan needed a deal that would simultaneously reduce promoter stake (through share dilution), add new business lines, and satisfy RBI's concerns about geographic and product concentration.

The public market experience was sobering. Unlike the microfinance world where Bandhan set the rules, capital markets demanded quarterly performance, clear communication, and predictable outcomes. The stock's volatility—swinging 40% within months—reflected the market's struggle to value a hybrid model that was neither pure microfinance nor traditional banking. Analysts couldn't decide if Bandhan deserved the premium valuation of a high-growth fintech or the discount applied to asset-quality-sensitive microfinance companies.

What emerged from this period was a more sophisticated Bandhan—one that understood that being public meant balancing multiple constituencies. The social mission remained but had to be articulated in terms of ROE and asset quality. Financial inclusion was reframed as "untapped market opportunity." The founder's vision now had to align with quarterly earnings calls. This tension between purpose and profit would define Bandhan's next chapter, leading directly to its biggest strategic move yet.

VI. The GRUH Finance Acquisition: Strategic Masterstroke (2019)

The boardroom at Bandhan Bank's Kolkata headquarters on January 7, 2019, witnessed one of Indian banking's most intriguing deals. Bandhan Bank acquired HDFC Limited's stake in GRUH Finance, a leading affordable housing finance company in India. The all-share transaction, valued at approximately Rs 81,800 crore, wasn't just an acquisition—it was a three-dimensional chess move solving multiple problems simultaneously.

GRUH Finance, HDFC's affordable housing finance subsidiary, was a crown jewel in its own right. Founded in 1986, it had built a Rs 17,000+ crore loan book focused on home loans to lower and middle-income segments in Gujarat, Maharashtra, Karnataka, and Madhya Pradesh. With an average ticket size of Rs 11 lakh and negligible NPAs (under 1%), GRUH represented everything Bandhan aspired to be: profitable financial inclusion at scale.

The deal structure was elegant: 568 Bandhan shares for every 1,000 GRUH shares, valuing GRUH at Rs 385 per share—a 15% premium to its closing price. HDFC would receive 15% stake in the merged entity, while Bandhan's promoter stake would fall from 82.3% to 61%—a crucial step toward meeting RBI's dilution requirements. The merger would create a financial services powerhouse with 4,182 banking outlets, over 31,000 employees, and 1.5 crore customers.

The strategic rationale was compelling on multiple fronts. Product diversification: Bandhan's loan book would shift from 85% unsecured microfinance to a more balanced mix with 28% secured housing loans. Geographic expansion: GRUH's strength in Western and Southern India perfectly complemented Bandhan's Eastern and Northern presence. Cultural fit: Both institutions served similar customer segments with comparable philosophies on financial inclusion. Risk mitigation: Adding secured assets would improve the overall portfolio quality and reduce concentration risk.

But the market's reaction was brutal. GRUH shares plummeted 17% on announcement day, while Bandhan fell 5%. Investors worried about integration challenges, cultural differences between a Gujarat-based housing finance company and a Bengal-based microfinance bank, and the dilution impact on both sets of shareholders. HDFC shareholders questioned why their gem was being sold; Bandhan investors wondered if they were overpaying for regulatory compliance.

The execution, however, was flawless. By October 2019, the merger was complete, with GRUH becoming a wholly-owned subsidiary of Bandhan Bank and subsequently merged into the bank. The integration prioritized customer continuity—GRUH's 5 lakh customers saw no disruption, while Bandhan's microfinance borrowers gained access to housing finance products. Technology integration took longer but was managed without major glitches.

The real masterstroke became apparent over time. The merger didn't just solve the promoter dilution issue—it transformed Bandhan's business model. The housing finance portfolio proved remarkably resilient, maintaining sub-1% NPAs even through COVID-19. Cross-selling opportunities emerged: microfinance customers graduating to home loans, housing finance customers taking small business loans. The combined entity's cost of funds dropped as deposit mobilization improved in GRUH's markets.

HDFC's role as a 15% shareholder brought unexpected benefits. The HDFC brand lent credibility to Bandhan in Western India, while HDFC's board representation (through nominees) brought institutional knowledge and governance standards. The partnership was particularly valuable during COVID-19, as HDFC's experience with crisis management helped Bandhan navigate the pandemic's challenges.

By 2020, the acquisition's wisdom was evident. The merged entity's loan book had grown to Rs 76,000+ crore, ROA improved to 3.4%, and the geographic concentration risk had significantly reduced. More importantly, Bandhan had proven it could execute complex M&A while maintaining operational excellence—a capability that would be crucial for future growth. The GRUH acquisition wasn't just a transaction; it was Bandhan's graduation from regional microfinance player to national universal bank.

VII. Business Model & Operations Deep Dive

Step into any of Bandhan Bank's 6,300+ outlets, and you'll notice something different. 73% of branches are situated in rural and semi-urban areas, often in locations where the nearest ATM might be 50 kilometers away. The branch design itself tells a story: low counters that don't intimidate, local language signage, and staff who look like the communities they serve. This isn't just architecture; it's anthropology applied to banking.

The product suite has evolved far beyond basic microfinance. The bank's products and services include savings and current accounts, fixed deposits, credit cards, home loans, personal loans, insurance and mutual funds. But the innovation lies in how these products are delivered. The Suraksha loan provides emergency medical credit within 24 hours. The Sushiksha loan funds children's education with repayment schedules aligned to agricultural cycles. The Suvriddhi loan helps women scale micro-enterprises into small businesses.

Post-GRUH merger, the loan book composition reveals strategic evolution: micro loans (58%), retail home loans (28%), MSME and other loans (14%). This isn't random diversification—it's a carefully orchestrated customer lifecycle strategy. A vegetable vendor starts with a Rs 25,000 micro loan, graduates to a Rs 2 lakh business loan, and eventually takes a Rs 10 lakh home loan. The same customer, served across different life stages, with products designed for their evolving needs.

The risk management framework defies conventional banking wisdom. While traditional banks rely on credit scores and collateral, Bandhan's model uses social capital and behavioral patterns. Group lending creates peer pressure for repayment. Weekly collection meetings double as financial literacy sessions. Loan officers, recruited from local communities, have intimate knowledge of borrower circumstances. The result: maintaining 95%+ collection efficiency even during demonetization and pandemic—crises that crippled conventional lenders.

Technology adoption has been pragmatic rather than flashy. While fintech competitors chase digital-only models, Bandhan's approach is "phygital"—physical presence enhanced by digital tools. Loan officers use tablets for customer onboarding, reducing account opening time from days to minutes. The core banking system handles 3.45 crore accounts seamlessly. But the killer app is simple: voice-enabled ATMs that serve illiterate customers, providing banking access to those excluded even from the digital revolution.

The human capital strategy remains unconventional. Of 75,000+ employees, a significant portion are first-generation graduates from the communities they serve. Training isn't just about banking products but about empathy, cultural sensitivity, and problem-solving. The Bandhan Academy runs continuous education programs, from basic financial literacy to advanced credit assessment. Career progression is deliberately visible—branch managers who started as loan officers become role models for new recruits.

The mission evolution from "financial inclusion" to "Aapka Bhala. Sabki Bhalai" (Your welfare. Everyone's welfare) reflects philosophical maturation. It's no longer just about providing credit but about comprehensive financial wellness. This includes insurance to protect against shocks, savings products to build resilience, and advisory services to improve financial decision-making. The metrics of success have expanded from loan disbursement to customer prosperity.

Navigating crises has become a core competency. Demonetization in 2016 threatened the cash-dependent microfinance model, but Bandhan pivoted quickly, opening 2.5 million new accounts in three months. Cyclone Fani in 2019 devastated Odisha operations, but rapid response teams rebuilt customer trust through relief efforts. The Assam microfinance crisis saw politically motivated loan waivers, but careful stakeholder management minimized losses. COVID-19 pushed NPAs to 6.81% in 2020-21, but aggressive provisioning and collection efforts brought them down to manageable levels.

The operational philosophy can be summarized in one practice: the "Doorstep Banking" model. Loan officers don't wait for customers to come to branches; they go to customers' homes and businesses. This isn't just convenience—it's recognition that for daily wage earners, a day spent at a bank means a day without income. By taking banking to the customer, Bandhan doesn't just reduce transaction costs; it demonstrates respect for their time and circumstances.

VIII. Modern Era & Current Position (2020–Present)

The Bank has mobilised deposits of ₹1,54,666 crore and its total advances stand at ₹1,33,625 crore as of June 30, 2025. These numbers represent more than growth—they mark Bandhan's transformation into a systemically important financial institution. With a market capitalization hovering around Rs 26,855 crore and operations across 35 states, the bank that started in a single village now touches nearly every corner of India.

The pandemic years tested every assumption about banking, but for Bandhan, they revealed hidden strengths. While urban-focused banks struggled with remote work and digital adoption, Bandhan's field force—already accustomed to doorstep banking—adapted quickly. The moratorium period saw 65% of customers opting for relief, but by December 2020, collection efficiency had bounced back to 93%. The crisis validated the relationship-banking model: customers who knew their loan officers personally were more likely to communicate distress and work out solutions.

Leadership transition marked a defining moment. On July 9, 2024, Chandra Shekhar Ghosh stepped down as MD & CEO after building Bandhan from scratch over 23 years. The succession—planned years in advance—saw internal candidate Ratan Kumar Kesh take charge, ensuring continuity of vision. Ghosh's departure wasn't just a retirement; it was a test of whether Bandhan's culture could survive without its founder-prophet. Early indications suggest the DNA remains intact: the same focus on inclusion, the same operational discipline, the same resistance to mission drift.

Digital transformation accelerated, but with a distinctly Bandhan twist. While neo-banks target urban millennials, Bandhan's digital initiatives focus on rural inclusion. The Bandhan Shagun savings account can be opened with just Aadhaar and PAN, targeting the 40 crore Indians with feature phones but no smartphones. Voice-enabled banking in nine regional languages serves customers who can speak but not read. The "assisted digital" model deploys tablets with field officers, combining human touch with digital efficiency.

The competitive landscape has intensified dramatically. Payment banks like Paytm and Airtel Payments Bank compete for the same customers with lower-cost models. Small finance banks—many led by former Bandhan executives—replicate the microfinance playbook. Fintech lenders use algorithms to approve loans in minutes versus Bandhan's days. Traditional banks have awakened to the rural opportunity, with HDFC Bank alone adding 1,000 rural branches. Yet Bandhan's moat—deep community relationships built over decades—proves surprisingly durable.

Asset quality remains the perpetual concern. The microfinance portfolio, while generating high yields (18-22%), carries inherent volatility. Political risks—loan waivers, populist interventions—lurk in every state election. Climate events disproportionately impact rural borrowers. The lack of credit bureau coverage for new-to-credit customers makes risk assessment challenging. Yet Bandhan's provisioning coverage ratio of 70%+ and diversified portfolio provide buffers against shocks.

Geographic expansion continues strategically. Unlike the pre-IPO land grab, new branches target specific micro-markets with unmet demand. The Northeast—long ignored by formal banking—sees aggressive expansion. Southern states, where GRUH's legacy provides entry, witness rapid growth. But the core remains Eastern India, where Bandhan commands 30%+ market share in several districts—a dominance that generates both pricing power and regulatory scrutiny.

Current performance metrics tell a story of resilience and evolution. Net Interest Margin at 7.8% remains among India's highest, reflecting the premium customers willingly pay for accessible credit. Cost-to-income ratio at 36% demonstrates operational efficiency despite the high-touch model. Return on Assets at 2.4% and Return on Equity at 17% place Bandhan in the top quartile of Indian banks. But beyond numbers, the impact metrics matter more: 3.45 crore customers served, 80% of them women, 60% first-time borrowers from formal sources.

The modern Bandhan faces a fundamental tension: How to remain a development finance institution while satisfying public market expectations? How to serve the poorest while generating competitive returns? How to maintain grassroots presence while building digital scale? These aren't just strategic questions but existential ones. The answers will determine whether Bandhan remains a unique institution bridging social and commercial banking, or becomes another bank that started with noble intentions but succumbed to market pressures.

IX. Playbook: Key Business & Investment Lessons

The Bandhan story offers a masterclass in building trust where none existed. Traditional banks demanded collateral, credit history, and formal income proof—documents the poor couldn't provide. Bandhan flipped the model: start with trust, build credit history through small loans, and gradually increase exposure. The first loan might be Rs 10,000; five years later, the same customer qualifies for Rs 5 lakh. This "graduation model" doesn't just build creditworthiness; it builds customer lifetime value.

Patient capital proves its worth in Bandhan's trajectory. The journey from NGO in 2001 to IPO in 2018 took 17 years—an eternity in today's hyper-growth startup world. Early investors like IFC and SIDBI waited over a decade for exits. But this patience allowed Bandhan to build robust operations, deep customer relationships, and sustainable unit economics. The lesson: In businesses serving the poor, quick returns and lasting impact rarely coexist.

Regulatory navigation emerges as a core competency, not a compliance burden. Ghosh spent as much time in RBI offices as in villages, understanding that regulatory partnership was essential for scale. The banking license wasn't just about meeting criteria but demonstrating alignment with national priorities. Even when faced with restrictions, Bandhan used regulatory pressure as catalyst for innovation—the GRUH acquisition being the prime example. The playbook: treat regulators as stakeholders, not adversaries.

M&A as simultaneous solution to multiple problems represents strategic sophistication. The GRUH acquisition solved promoter dilution, geographic concentration, product concentration, and brought a strategic partner (HDFC)—all in one transaction. This "multiple birds with one stone" approach to M&A differs from typical banking consolidation focused solely on scale or cost synergies. The insight: In regulated industries, M&A can be a tool for compliance as much as growth.

Scaling microfinance without losing touch with grassroots seems paradoxical, but Bandhan cracked the code. The secret lies in organizational design: autonomous regions with local decision-making, promotion from within ensuring cultural continuity, and technology that enhances rather than replaces human interaction. The branch manager in rural Assam has more autonomy than her counterpart at a typical commercial bank. This distributed model maintains entrepreneurial energy despite institutional scale.

Founder vision and persistence matter more in financial inclusion than perhaps any other sector. Ghosh's 23-year journey—through skepticism, crises, and regulatory challenges—required almost messianic belief in the mission. But equally important was his ability to evolve: from activist to entrepreneur, from entrepreneur to banker, from banker to institution builder. The lesson: In businesses requiring systemic change, founders must transform themselves as radically as their organizations.

Creating a service culture in banking—an industry often associated with bureaucracy and indifference—required deliberate cultural engineering. Every employee, from security guard to CEO, undergoes customer service training. Performance metrics balance financial outcomes with customer satisfaction. The morning huddle at every branch begins with customer success stories, not sales targets. This cultural architecture ensures that growth doesn't dilute service quality.

Balancing social mission with public market expectations remains Bandhan's ongoing experiment. The quarterly earnings pressure pushes toward safer, higher-margin products. The social mission pulls toward riskier, underserved segments. Bandhan's solution: segment reporting that separates microfinance from other businesses, allowing investors to value each appropriately. Clear communication about the long-term value of financial inclusion—reduced inequality, expanded markets, social stability—helps align stakeholder interests.

The ultimate lesson from Bandhan's playbook: Profitable financial inclusion isn't an oxymoron but requires rethinking every assumption about banking. Risk assessment through social capital rather than financial capital. Distribution through feet on street rather than digital apps. Products designed for irregular income rather than steady salaries. Patience to build trust rather than aggressive sales. These inversions of conventional banking wisdom create a moat that's difficult to replicate—and a model for serving the next billion customers globally.

X. Bear vs. Bull Case Analysis

The Bull Case: Unlocking India's Greatest Untapped Market

India's financial inclusion gap represents one of the world's largest market opportunities. With 200 million adults still unbanked and 40% of the population lacking access to formal credit, the addressable market dwarfs Bandhan's current scale. Rural India, contributing 46% of GDP but receiving only 9% of total credit, offers decades of growth runway. As per capita income rises and financial awareness spreads, Bandhan's first-mover advantage in 500+ districts positions it to capture disproportionate value.

The brand equity in core markets approaches fortress-like strength. In rural West Bengal, Odisha, and Assam, "Bandhan" has become synonymous with banking itself—like "Xerox" for photocopying. This mindshare, built over two decades of grassroots presence, creates customer acquisition costs that are fraction of competitors'. New entrants must spend heavily on marketing; Bandhan grows through word-of-mouth referrals from 3.45 crore existing customers.

Post-GRUH diversification fundamentally improved the risk-return profile. The housing finance portfolio generates stable 10-11% yields with sub-1% NPAs, providing ballast during microfinance volatility. The product suite now covers customer lifecycle from first loan to retirement planning. Geographic diversification reduced Eastern India exposure from 65% to 45%. This transformed Bandhan from a regional microfinance player to a national universal bank with multiple growth engines.

The execution track record inspires confidence. Management navigated demonetization, GST implementation, Assam crisis, and COVID-19 without existential threat. The GRUH integration proceeded flawlessly. Technology adoption balanced digital innovation with human touch. The leadership transition from founder to professional management occurred smoothly. This operational excellence suggests Bandhan can handle future challenges while capturing opportunities.

First-mover advantage in financial inclusion creates durable competitive moats. Bandhan's data on 3 crore previously unbanked customers—their payment patterns, business cycles, social networks—provides underwriting insights competitors lack. The field force of 50,000+ employees with deep community relationships can't be replicated quickly. The trust earned through decades of service creates switching costs beyond mere economics.

The Bear Case: Structural Challenges in a Changing Landscape

The low interest coverage ratio and modest ROE of 11.5% over three years raise profitability concerns. Despite charging 18-22% interest on microloans, the high operating costs of doorstep banking and elevated credit costs compress margins. The promised operating leverage from scale hasn't fully materialized. Public market investors expecting 20%+ ROE from leading private banks question whether Bandhan's model can deliver comparable returns.

Asset quality in unsecured microfinance remains structurally vulnerable. Without collateral or reliable income documentation, the portfolio depends entirely on borrower willingness to repay. Political interference—loan waivers, payment moratoriums—can destroy repayment culture overnight. Climate events disproportionately impact rural borrowers. The next crisis could push NPAs to unsustainable levels, requiring massive provisions that erode capital.

Regulatory overhang persists despite compliance improvements. RBI's wariness about microfinance concentration, promoter stake, and rapid growth creates constant supervision risk. New regulations on interest rate caps, customer protection, or priority sector lending could impact profitability. The banking license that enabled growth also brought constraints that pure NBFCs avoid. Regulatory tightening remains a permanent Damocles sword.

Competition intensifies from multiple directions. Fintech lenders approve loans in minutes using alternative data, while Bandhan takes days with traditional processes. Payment banks leverage technology for near-zero customer acquisition costs. Small finance banks replicate Bandhan's model with younger, hungrier teams. Traditional banks have discovered rural markets. The competitive moat might be narrower than bulls believe.

Geographic and segment concentration creates vulnerability despite diversification efforts. Eastern India still contributes 45% of business, exposing Bandhan to regional economic shocks. The customer base remains predominantly rural, low-income women—a segment vulnerable to economic cycles. Product concentration in small-ticket loans limits pricing power. True diversification would require entering urban markets and affluent segments where Bandhan lacks competitive advantage.

The technology deficit versus digital-native competitors widens daily. While Bandhan deploys tablets and apps, the core remains human-intensive operations. Digital natives achieve 10x productivity with automated underwriting and collection. Younger customers prefer digital-only interactions. The high-touch model that built Bandhan might become a liability in an increasingly digital world. Catching up requires massive technology investment that could pressure margins.

The post-founder transition risk shouldn't be underestimated. Ghosh's personal relationships with regulators, investors, and stakeholders smoothed difficult periods. The new leadership, while competent, lacks founder charisma and moral authority. Mission drift—prioritizing profits over purpose—becomes likelier without the founder's vigilance. History shows few founder-dependent institutions successfully navigate succession.

XI. Epilogue & Future Outlook

As monsoon clouds gather over Kolkata in 2025, Bandhan Bank stands at an inflection point eerily similar to its founding moment. The question isn't whether a bank can serve the poor profitably—Bandhan proved that definitively. The question now is whether an institution built on human relationships can thrive in an algorithmic age, whether a mission-driven bank can satisfy quarterly capitalism, and whether the second generation of leadership can maintain the founder's revolutionary spirit while adapting to new realities.

The post-founder era brings both liberation and vulnerability. Liberation from the constraints of a single vision, allowing experimentation with new business models, technologies, and markets. Vulnerability from losing the moral authority and stakeholder trust that Ghosh personally embodied. The new leadership must navigate between preserving Bandhan's soul while evolving its body—maintaining grassroots presence while building digital scale, serving existing customers while attracting new segments, honoring the social mission while delivering market returns.

Digital transformation emerges as the defining challenge. But Bandhan's version won't mirror Silicon Valley fintech. Instead, expect "appropriate technology"—solutions designed for feature phones not smartphones, voice interfaces for illiterate users, assisted digital models combining human warmth with algorithmic efficiency. The investment required—estimated at Rs 2,000+ crore over five years—will pressure margins but is existential for relevance.

M&A opportunities abound as India's financial sector consolidates. Distressed microfinance institutions, struggling small finance banks, and regional rural banks offer acquisition targets. But the GRUH playbook—solving multiple problems through strategic acquisition—sets a high bar. Future deals must bring either technology capabilities, new customer segments, or geographic presence that organic growth can't achieve efficiently.

The role in India's financial inclusion journey extends beyond banking. Bandhan has become a template for institutions worldwide seeking to serve the unbanked profitably. The model influences policy discussions at RBI, World Bank, and development finance institutions globally. This soft power—being the reference case for inclusive banking—creates responsibilities beyond shareholder returns.

Key metrics to watch going forward include the pace of digital adoption among existing customers, success in attracting urban and younger demographics, asset quality trends in the unsecured portfolio, and ability to maintain NIMs as competition intensifies. But perhaps the most critical metric is harder to quantify: whether Bandhan remains a place where a sweet shop owner's son would choose to revolutionize banking.

The next chapter of Bandhan's story will be written not in boardrooms or regulatory offices but in the small towns and villages where credit remains scarce and opportunity abundant. Whether serving a vegetable vendor in Kolkata, a weaver in Assam, or a farmer in Bihar, Bandhan's future depends on maintaining the radical proposition that every individual, regardless of economic status, deserves access to financial services that respect their dignity and enable their dreams.

The ultimate question facing Bandhan—and indeed all institutions attempting to balance profit with purpose—is whether capitalism can be reformed from within or only disrupted from without. Bandhan's answer, demonstrated through two decades of practice, is that patient capital, operational excellence, and unwavering focus on underserved segments can create both social impact and financial returns. Whether this synthesis survives the pressures of public markets, technological disruption, and leadership transition will determine not just Bandhan's fate but the future of inclusive finance itself.

XII. Recent News**

Latest Quarterly Results Analysis**

Bandhan Bank presented its financial results for the quarter and nine months ended December 31, 2024, during its meeting on Friday, January 31, 2025, in Kolkata. The Q3 FY25 results revealed mixed performance with strong operational growth but pressure on profitability due to asset quality challenges in the microfinance segment.

Bandhan Bank on Friday, January 31 announced a 41.79% year-on-year (YoY) decline in its standalone net profit to ₹426.49 crore in the third quarter of the 2024-25 fiscal year (Q3 FY25). The net profit stood at ₹732.72 crore in the corresponding period last year. Despite the profit decline, net interest income (NII) was Rs. 2,830 crore, up 12% year on year from Rs. 2,525 crore in Q3 FY24.

The bank's business fundamentals showed resilience with Advances: INR1.32 lakh crore, 14% YoY growth. Deposits: INR1.41 lakh crore, 20% YoY growth. The CASA Ratio: 32%. Secured Book: 49% of total advances, 34% YoY growth. This indicates continued progress in the strategic shift toward secured lending and stable deposit mobilization.

Asset Quality Concerns and Strategic Response

The primary challenge emerged from the microfinance portfolio. Gross NPA: 4.7% as of December 2024. Net NPA: 1.2% as of December 2024. The bank maintained strong provision coverage with Provision Coverage Ratio (PCR): 85.4% including write-offs.

The bank faced higher gross slippages in Q3 FY25, particularly in the EEB book, leading to increased credit costs. Net interest margin (NIM) declined to 6.9% in Q3 FY25 from 7.4% in the previous quarter due to changes in the product mix and higher slippages.

Management's outlook suggests cautious optimism. The CEO acknowledged that slippages remain a concern, with expectations of substantial slippages in Q4, though possibly lower than Q3's INR1,196 crore. The bank is seeing improvements in SMA-0, indicating a reversal trend, and expects lower slippages by Q1 of the next financial year.

Q2 FY25 Performance Highlights

Earlier in the fiscal year, During the quarter under review, profit came at Rs 937.45 crore as against Rs 721.17 crore in the year-ago period. The bank had maintained stronger margins with Net interest margin (NIM) for the quarter was 7.4 per cent compared to 7.2 per cent in Q2 FY24.

Ratan Kumar Kesh, MD & CEO, said, "Bandhan Bank's strong performance in the second quarter reflects the momentum in quality growth with our focus on effective risk management and compliance. Our success is anchored in the trust of our customers and the dedication of our employees. By focusing on innovation in technology, refining our processes, and enhancing products and people capabilities, we are well-positioned to drive the next phase of growth for Bandhan Bank 2.0."

Strategic Initiatives and Digital Transformation

Bandhan Bank Ltd (BOM:541153) has implemented strategic initiatives such as forming a transformation management team and a Digital and Transaction Excellence unit to drive innovation and efficiency. The focus on "Bandhan Bank 2.0" represents a comprehensive modernization effort aimed at balancing the traditional microfinance roots with contemporary banking requirements.

The bank continues to navigate the challenging microfinance environment while executing its diversification strategy. The shift toward secured lending, geographic expansion beyond Eastern India, and digital initiatives position Bandhan for long-term sustainability, though near-term pressures from asset quality concerns in the unsecured portfolio remain a key monitorable.

XIII. Links & References

Official Sources: - Bandhan Bank Investor Relations: bandhanbank.com/investor-relations - Quarterly Results Archive: bandhanbank.com/quarterly-report - Annual Reports: bandhanbank.com/annual-report - Stock Exchange Filings: nseindia.com/companies/BANDHANBNK

Regulatory Documents: - Reserve Bank of India Banking License Guidelines - RBI Master Directions on NBFC-MFI - SEBI Listing Regulations and Disclosures - Banking Regulation Act Documentation

Books and Academic Resources: - "The Fortune at the Bottom of the Pyramid" by C.K. Prahalad - "Banker to the Poor" by Muhammad Yunus - "Creating a World Without Poverty" by Muhammad Yunus - Academic papers on Indian microfinance sector evolution

Industry Reports: - MFIN (Microfinance Institutions Network) Industry Reports - Sa-Dhan Bharat Microfinance Report - World Bank Financial Inclusion Reports - IFC Studies on Microfinance in South Asia

Historical Documentation: - GRUH-Bandhan Merger Scheme Document (2019) - IPO Prospectus (March 2018) - RBI Banking License Application (2013) - Bandhan Financial Services NBFC Documentation

Market Analysis: - Bloomberg Terminal: BANDHANBNK IN Equity - Reuters: BDBK.NS - Morningstar India Coverage - Credit Rating Reports (CRISIL, ICRA, CARE)

Media Archives: - Economic Times Banking & Finance Section - Business Standard Financial Inclusion Coverage - Mint Analysis on Microfinance Sector - Forbes India Profile on Chandra Shekhar Ghosh

Competitor Analysis: - Small Finance Banks Association Reports - Ujjivan Small Finance Bank Investor Presentations - Equitas Small Finance Bank Annual Reports - Traditional Banks' Financial Inclusion Initiatives

Technology and Digital Banking: - BCG-FICCI Reports on Indian Banking Digital Transformation - McKinsey India Banking Reports - Deloitte Banking Industry Outlooks - PwC Fintech Collaboration Studies

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube