Swan Energy: From Century-Old Textile Mill to India's LNG Ambitions

I. Introduction & Cold Open

Picture this: A sprawling textile mill in colonial Mumbai, 1909. The looms clatter rhythmically as cotton transforms into cloth, the air thick with fiber dust and the promise of British Empire commerce. Fast forward 115 years—those same grounds now house gleaming IT towers, while the company that once wove cotton dreams is anchoring massive floating vessels off Gujarat's coast, ready to gasoline India's energy future with liquefied natural gas.

This is Swan Energy Limited—a company that shouldn't exist, at least not in its current form. By every law of corporate evolution, a textile mill founded when King Edward VII ruled India should have either died in the great Mumbai mill closures or become a real estate play. Instead, it's betting everything on becoming India's next energy infrastructure champion, competing with the Adanis and Ambanis of the world.

The paradox is striking: How does a company go from processing cotton fibers to importing super-cooled methane from Qatar? How does a family-owned textile operation transform into a ₹13,000 crore energy infrastructure play? And perhaps most intriguingly—why would anyone attempt such an audacious pivot when safer paths existed?

The answer lies in a uniquely Indian story of industrial transformation, one that mirrors the nation's own economic journey from colonial manufacturing to modern infrastructure ambitions. It's a tale of three distinct eras, three different ownership groups, and three completely different business models—all housed within the same corporate entity.

What makes Swan Energy particularly fascinating for investors isn't just its survival—plenty of old Indian companies have managed that through real estate windfalls. It's the sheer audacity of its current bet: building India's first greenfield FSRU (Floating Storage and Regasification Unit) LNG terminal, a project so complex that even energy giants approach it cautiously. For context, when Swan announced this pivot, it had zero experience in energy infrastructure. Zero.

Yet here we are in 2024, with the stock hitting all-time highs, major oil companies signed up as customers, and the terminal mere months from commissioning. Either this is one of India's great untold transformation stories, or it's a disaster waiting to unfold. The truth, as always, is more nuanced.

This is the story of how patient capital, regulatory navigation, and strategic opportunism can transform a dying textile mill into an energy infrastructure player. It's about reading India's economic transitions—from textiles to real estate to energy—and surfing each wave at precisely the right moment. And it's about the families and personalities who engineered these transitions, often against conventional wisdom.

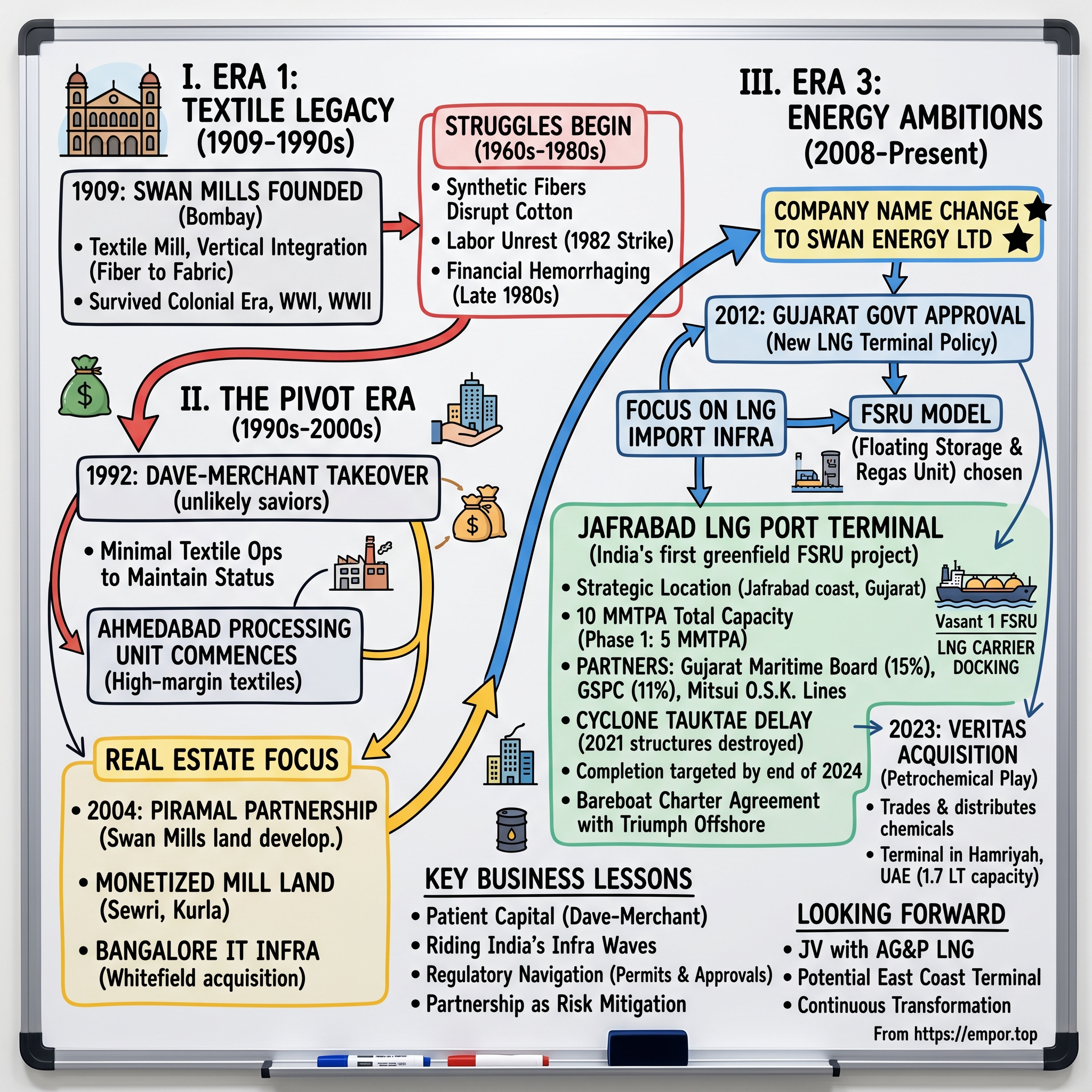

II. The Colonial Era Beginnings & Textile Legacy (1909-1990)

The year 1909 was a peculiar time to start a textile mill in Mumbai. The city, then Bombay, was already establishing itself as the "Manchester of the East," with over 80 textile mills employing nearly 100,000 workers. The American Civil War had ended decades earlier, but its disruption of cotton supplies had permanently shifted global textile dynamics in India's favor. Into this milieu stepped Swan Mills Limited, incorporated with the modest ambition of joining Mumbai's cotton boom.

The founding wasn't driven by grand industrial vision but by practical commercial opportunity. Mumbai's natural humidity made it perfect for cotton spinning—the fibers wouldn't break as easily as in drier climates. The city's port provided easy access to raw cotton from Gujarat and Maharashtra's hinterlands, while its growing railway network opened distribution channels across the subcontinent. Swan Mills set up operations in Sewri and Kurla, areas that would later become some of Mumbai's most valuable real estate but were then industrial outposts on the city's edge.

What distinguished Swan Mills in those early decades wasn't innovation or scale—it was survival instinct. The mill witnessed the twilight of the British Raj, navigating through World War I when cotton exports boomed as Europe's mills shut down. The interwar years brought different challenges: Japanese textile competition, global depression, and the growing independence movement that often targeted British-owned businesses. Swan, being locally managed though British-incorporated, walked a tightrope.

The original business model was straightforward: buy raw cotton, spin it into yarn, weave it into cloth, and sell to wholesalers who distributed across India. The company operated as a "composite mill"—industry parlance for handling the entire production chain from fiber to fabric. This vertical integration provided better margins but required substantial working capital and sophisticated management. Swan's early managers, whose names are largely lost to history, proved adept at both.

World War II transformed the business overnight. Military contracts for tent canvas, uniforms, and parachute silk became the lifeline for Mumbai's mills. Swan Mills, like its peers, pivoted from producing saris and shirting to military supplies. Production ran round the clock, labor relations were suspended under wartime regulations, and profits soared. But this wartime boom contained seeds of future crisis—it delayed modernization and created unsustainable cost structures.

Independence in 1947 brought euphoria and chaos in equal measure. Partition disrupted cotton supplies from regions that became Pakistan. The new government's socialist policies favored employment over efficiency, making it nearly impossible to close unproductive units or lay off workers. Swan Mills, like Mumbai's entire textile sector, entered a slow-burning crisis that would define the next four decades.

By the 1960s, the writing was on the mill walls. Synthetic fibers were disrupting cotton's monopoly. Power looms in smaller towns could produce cloth cheaper than Mumbai's composite mills. Labor unrest became chronic—the great textile strike of 1982 would last 18 months and essentially break Mumbai's textile industry. Swan Mills adapted by adding polyester production capacity, but this was expensive band-aid on a structural wound.

The composite mill model that had served Swan for seven decades was becoming obsolete. The company's sprawling properties in Sewri and Kurla, once assets for their proximity to rail and port, were now liabilities due to high labor costs and urban congestion. Yet these same properties would soon become Swan's salvation—though not in ways anyone imagined in 1909.

III. The J.P. Goenka Era & Crisis Years (1970s-1992)

The summer of 1971 marked the beginning of Swan Mills' darkest chapter. The J.P. Goenka Group, part of the larger industrial clan that included luminaries like R.P. Goenka and Keshav Prasad Goenka, acquired the struggling textile operation. The company was taken over from J.P. Goenka Group by Dave and Merchant families in 1992, but those two decades under Goenka stewardship would prove nearly fatal.

Jagdish Prasad Goenka, who took over jute, wool, cotton, textiles, carbon black, oil lubricants and engineering as part of the family's business split in 1979, was no stranger to textiles. He held prestigious positions including Chairman-Indian Woollen Mills Federation (1969-70), Chairman-Indian Jute Mills Association (1973-74), and Chairman-Indian Cotton Mills Federation (1978-80). Yet even his experience couldn't overcome the structural headwinds battering Mumbai's textile industry.

The 1970s brought a perfect storm. Oil shocks made synthetic fibers suddenly expensive, undermining Swan's polyester investments. Labor militancy reached new heights—strikes became monthly occurrences, each one bleeding cash and disrupting customer relationships. The government's Monopolies and Restrictive Trade Practices Act limited expansion options for larger groups like the Goenkas. Meanwhile, power looms in Gujarat and Tamil Nadu, unencumbered by Mumbai's high costs, captured market share relentlessly.

By 1982, when Mumbai's Great Textile Strike erupted, Swan Mills was already gasping. The strike, lasting 18 months and involving 250,000 workers, essentially delivered the death blow to Mumbai's century-old textile industry. Mills closed by the dozen. Those that survived did so by abandoning textiles entirely or drastically downsizing. Swan Mills limped on, but the writing wasn't just on the wall—it was spray-painted in giant letters.

The financial hemorrhaging accelerated through the 1980s. Banks, already nursing massive textile sector NPAs, tightened credit. Swan's working capital dried up. Suppliers demanded cash upfront. Buyers migrated to more reliable sources. The company's Sewri and Kurla properties, sitting on increasingly valuable Mumbai real estate, became its only real assets—but selling them would mean admitting defeat.

Enter the Board for Industrial and Financial Reconstruction (BIFR), India's corporate ICU for sick companies. By the late 1980s, Swan Mills was referred to BIFR, joining hundreds of other textile mills in financial purgatory. BIFR's rehabilitation packages typically involved debt restructuring, asset sales, and promises of modernization that rarely materialized. For the Goenka Group, managing a BIFR-referred company meant endless meetings with bureaucrats, bankers, and unions—energy better spent on their profitable ventures.

The human toll was devastating. Workers who'd spent decades at the mills faced uncertain futures. Many were the children and grandchildren of Swan's original employees from 1909. The mill culture—with its chawls (worker housing), cooperative stores, and festival celebrations—was disintegrating. Sewri and Kurla, once thriving industrial neighborhoods, became symbols of Mumbai's deindustrialization.

What made Swan's crisis particularly acute was timing. The 1991 economic liberalization was about to unleash unprecedented opportunities in Indian business. Real estate values in Mumbai were set to explode. Energy demand would surge. But Swan Mills, trapped in BIFR proceedings and bleeding cash, seemed destined to miss everything. The Goenka Group, recognizing a lost cause, began looking for exits.

The irony wasn't lost on observers: Swan Mills had survived British colonialism, two world wars, and independence, only to be felled by the very market forces that liberalization was about to unleash. The company needed not just capital but complete reimagination. It needed owners willing to take extraordinary risks, to see opportunity where others saw only decay.

IV. The Dave-Merchant Takeover & Turnaround (1992-2005)

The boardroom at Swan Mills in early 1992 felt more like a funeral parlor than a corporate headquarters. The BIFR proceedings had dragged on for years. Workers hadn't been paid in months. The Goenka Group, having extracted whatever value they could, were eager to exit. Into this morass stepped two unlikely saviors: Navinbhai Chandulal Dave, an eminent Industrialist with an experience of more than 60 years in various areas of real estate, textiles and education, and the Merchant brothers—Nikhil Merchant who completed his B.S. in Textile Engineering from the U.S.A. and his M.E.P. degree from IIM Ahmedabad with over 35 years experience across textile, real estate, and oil & gas sectors, along with his brother Paresh.

The takeover price was nominal—the real cost would come in rehabilitation. Dave and Merchant families took over the Company from J.P Goenka Group in 1992, inheriting massive liabilities, hostile unions, obsolete machinery, and properties encumbered with legal disputes. Most industry observers gave them six months before throwing in the towel.

What distinguished Dave and the Merchants wasn't deep pockets—they didn't have those. It was their unconventional approach to rehabilitation. Rather than immediately shutting mills and selling land (the standard playbook), they attempted something audacious: actually reviving the textile business while simultaneously planning for its eventual transformation.

Nikhil Merchant, with his American engineering degree and IIM Ahmedabad management education, brought a technocratic approach rarely seen in Mumbai's old textile families. He understood that survival required not just financial restructuring but operational excellence. The first move was counterintuitive: instead of cutting all textile operations, they consolidated and modernized selectively.

A state-of-the-art textile processing unit in Ahmedabad commenced operations with a capacity of 20 lakh meters per month. This wasn't nostalgia—it was strategic. The Ahmedabad unit, away from Mumbai's high costs and labor issues, could actually generate positive cash flows. It specialized in high-margin technical textiles and processing, not the commodity cotton that had doomed Mumbai's mills.

Meanwhile, Navinbhai Dave, leveraging his six decades of experience, navigated the treacherous waters of Mumbai's real estate regulations. The mill lands couldn't be sold outright—Mumbai's Development Control Regulations mandated that one-third go to MHADA (housing authority), one-third remain with the mill, and only one-third could be commercially developed. This regulation, meant to protect workers, had paradoxically trapped many mills in perpetual losses.

The Dave-Merchant strategy was patience personified. They kept minimal textile operations running to maintain the company's legal status as a functioning mill. This prevented forced liquidation while they negotiated with authorities, unions, and potential partners. Every month survived was a small victory.

The human dimension couldn't be ignored. Unlike the Goenkas, who managed from Kolkata, Dave and the Merchants were Mumbai locals. They understood the mill workers' culture, spoke their language, attended their festivals. This wasn't corporate PR—it was survival strategy. Hostile workers could derail any turnaround through strikes or legal challenges.

By 1995, three years into their ownership, the company was still losing money but showing signs of life. The Ahmedabad unit was operational. Worker relations had stabilized. Most importantly, they'd begun quiet discussions with developers about the mill lands' potential. The real estate boom that would transform Mumbai was still years away, but the seeds were being planted.

The late 1990s brought unexpected tailwinds. India's economic liberalization was creating a new middle class hungry for housing and office space. Mumbai, as the commercial capital, was ground zero for this boom. Suddenly, the mill lands that had been albatrosses around textile companies' necks were looking like golden geese.

But Dave and the Merchants showed remarkable restraint. While other mill owners rushed to monetize land, often getting trapped in legal battles or selling too cheap, Swan moved deliberately. They understood that real estate wasn't just about selling land—it was about creating value through development. This insight would prove transformational.

The rehabilitation of Swan Mills between 1992 and 2005 wasn't a dramatic turnaround story—it was a slow, grinding battle of attrition against entropy. By 2005, thirteen years after the takeover, the company was stable but not thriving. It had survived when dozens of peer mills had died. More importantly, it was positioned for something bigger. The real transformation was about to begin.

V. The Real Estate Pivot: Mumbai's Mill Land Gold Rush (2000-2010)

The year 2004 marked Swan's entry into an entirely different game. Swan forayed into real estate; partnered with Piramal Holdings Limited to develop Swan Mills land in Mumbai. This wasn't just diversification—it was metamorphosis. The partnership with Ajay Piramal, one of India's most sophisticated real estate developers, signaled that Swan was serious about extracting maximum value from its land assets.

To understand the magnitude of this opportunity, consider Mumbai's geography. Hemmed in by the Arabian Sea, the city can only grow northward. The mill lands, once on the periphery, were now in the heart of the city. Sewri and Kurla, where Swan's mills stood, were transforming from industrial wastelands into prime commercial corridors. The Bandra-Kurla Complex, India's answer to Canary Wharf, was just kilometers away.

The Piramal partnership was masterfully structured. Swan brought land; Piramal brought development expertise and capital. The risk-sharing arrangement meant Swan could participate in the upside without bearing the full development risk. This was crucial—many mill owners who tried to become developers themselves failed spectacularly, lacking the expertise to navigate Mumbai's byzantine approval processes.

The third tower was completed in the I.T. Park developed (2,17,000 sq ft) at Kurla, Mumbai, and handed over to Equinox Business Parks Pvt. Ltd. This wasn't just any development—IT parks commanded premium rents from multinational technology companies flooding into India. The timing was perfect: India's IT services boom was creating insatiable demand for Grade A office space.

But Swan's real estate ambitions extended beyond Mumbai. Recognizing that land values in India's tech capital Bangalore were also soaring, Swan made a bold move. The company acquired significant IT infrastructure in Bangalore's Whitefield area, a suburb that would become synonymous with India's tech boom. The 2,95,000 sq. ft. commercial tower in Whitefield, Bengaluru, was completed and leased out to Harman Connected Services Corp (India) Pvt. Ltd.

The numbers told the story of transformation. In 2000, Swan was primarily a textile company with some valuable but encumbered land. By 2010, real estate was contributing the majority of profits. The company had successfully monetized its mill lands without triggering the legal and social conflicts that plagued many peers.

What made Swan's real estate strategy particularly clever was its focus on commercial rather than residential development. Commercial projects faced fewer regulatory hurdles, commanded higher margins, and generated recurring rental income. The residential project at Sewri, Ashok Gardens, was completed and delivered, but this was the exception rather than the rule.

The financial engineering was equally sophisticated. Rather than selling land outright for one-time gains, Swan created special purpose vehicles (SPVs) for each project. This structure allowed them to raise project-specific debt, limiting parent company exposure while maintaining equity upside. It also made the company more attractive to institutional investors who could evaluate each project independently.

The cash generation from real estate served a larger purpose. Dave and the Merchants weren't content to become just another Mumbai real estate company. They saw real estate as a means to an end—generating capital for an even bigger bet. While competitors celebrated their land windfalls with dividends and bonuses, Swan was quietly researching India's energy infrastructure gaps.

By 2008, Swan's transformation from textile manufacturer to real estate developer was complete. But this was merely Act II of a three-act play. The company's name change would signal the beginning of Act III—the most audacious transformation yet.

VI. The Energy Vision: Betting on LNG (2008-2017)

The name of the company changed to Swan Energy Ltd—a declaration of intent that shocked market watchers. A textile mill pivoting to real estate was understandable, even predictable. But energy? That was either visionary or delusional.

The genesis of Swan's energy ambitions lay in a simple observation: India's natural gas demand was growing at 8-10% annually, but domestic production was stagnating. The Krishna-Godavari basin discoveries that had promised energy independence were disappointing. India would need to import liquefied natural gas (LNG) at scale. The question was: who would build the infrastructure? The Government of Gujarat announced a New LNG Terminal Policy in 2011 under which Swan Energy submitted a detailed proposal and received approval in 2012. Swan Energy received final environmental clearance from MOEF and letter of intent from Gujarat Maritime Board in 2013. These weren't just permits—they were validation that a textile-turned-real-estate company could credibly enter the energy infrastructure space.

The choice of LNG wasn't random. Nuclear was politically toxic post-Fukushima. Coal was environmentally problematic. Solar and wind were still expensive and intermittent. But natural gas? It was cleaner than coal, more reliable than renewables, and critically, the infrastructure could be built relatively quickly using proven technology.

Swan's research revealed a gap in the market. Existing LNG terminals at Dahej (Petronet) and Hazira (Shell) were operating at capacity. New terminals were needed, but the capital requirements—typically $1-2 billion—deterred most players. Swan's solution was ingenious: use a Floating Storage and Regasification Unit (FSRU) instead of building onshore tanks.

An FSRU is essentially a specialized ship that stores LNG at -162°C and converts it back to gas for pipeline distribution. The advantages were compelling: 40% lower capital cost than onshore terminals, 2-3 years faster to deploy, and critically, the ability to relocate if market conditions changed. For a company with zero LNG experience, it reduced both technical and financial risk.

The terminal has a regasification capacity of 10 MMTPA of LNG off the Jafrabad coast in Amreli district, Gujarat. The location is highly strategic owing to proximity to international shipping routes. The distance from Gulf countries to Swan LNG Port is shortest compared to all other LNG terminals in India.

The site selection at Jafrabad wasn't accidental. Located between Pipavav and Jafrabad ports, it offered natural deep water (14.5 meters), reducing dredging costs. More importantly, it was close to Gujarat's industrial heartland—factories hungry for cleaner fuel to replace coal and diesel.

But Swan faced a chicken-and-egg problem: banks wouldn't finance without customers, customers wouldn't commit without certainty of operations. The breakthrough came through strategic partnerships. Swan LNG was established with Swan Energy (63%), Gujarat Maritime Board (15%), Gujarat State Petronet (11%), and FSRU Venture India One (11%) under Shareholders Agreement of October 2017.

The Gujarat Maritime Board's participation was crucial—it provided regulatory comfort. Gujarat State Petronet brought pipeline connectivity expertise. FSRU Venture India One, a subsidiary of Mitsui O.S.K. Lines, brought FSRU operational experience. Swan retained majority control while de-risking execution.

Gujarat State Petroleum Corporation Limited, Bharat Petroleum Corporation Limited, Indian Oil Corporation Limited and ONGC Limited executed Re-gasification Agreements with the company. These weren't speculative MOUs but firm, bankable contracts covering the entire 5 MMTPA first phase capacity for 20 years.

The financial engineering was sophisticated. SLPL achieved Financial Closure with State Bank of India as lead bank for a loan averaging INR 1810.88 crores from various banks. For a company that had never built energy infrastructure, securing project finance from India's largest bank was remarkable validation.

Construction began in 2016, with SLPL executing an EPC contract for Marine and Dredging works worth Rs. 2115 crore with National Marine & Infrastructure India. The scale was staggering—8.52 million cubic meters of dredging, specialized cryogenic equipment, high-pressure pipelines. Every component had to work perfectly at -162°C.

Then nature intervened. The project was expected to commence operations in second half of 2020 but was delayed because under-construction facilities were destroyed by cyclone Tauktae. For any company, this would be devastating. For Swan, betting everything on an unfamiliar industry, it could have been fatal. But the partnerships held, banks extended support, and reconstruction began.

VII. The Jafrabad LNG Terminal: India's First FSRU Project (2017-Present)

The Swan LNG Terminal is India's first greenfield Liquefied Natural Gas port terminal project—a distinction that sounds impressive until you understand what "greenfield" actually means. Unlike brownfield projects that expand existing infrastructure, Swan was building from scratch in an area with no prior LNG facilities. No learning from predecessors' mistakes. No shared infrastructure to reduce costs. Just empty coastline and ambitious plans.

The technical complexity cannot be overstated. LNG exists at -162°C, a temperature where most materials become brittle and shatter. The entire supply chain—from ship to storage to regasification to pipeline—must maintain this temperature perfectly. A single leak doesn't just waste product; it can cause catastrophic explosions. The engineering tolerances are measured in millimeters across structures hundreds of meters long.

The FSRU is 294m long and 48m broad with cargo capacity of 180,000 cubic metres and deadweight of 85.4 thousand metric tons. The FSRU has regasification capacity of 50-1,000 million standard cubic feet per day. Four dual fuel diesel engines power the FSRU with design service speed of 12 knots.

To put this in perspective, the FSRU "Vasant 1" is longer than two football fields, stores enough energy to power a city of 5 million for a month, and must remain perfectly stable while massive LNG carriers dock alongside in open water. The engineering precision required makes semiconductor fabrication look forgiving.

The marine infrastructure alone was a massive undertaking. The harbour area has minimum depth of 14.5m with estimated dredging volume of 8.52 million m3. That's equivalent to excavating 3,400 Olympic swimming pools worth of seabed, in an ecologically sensitive coastal area, while maintaining navigational safety for existing shipping.

Black & Veatch, the global engineering giant, was brought in as EPC contractor for critical infrastructure. Their scope included the jetty topside—the platform where ships dock—and onshore facilities. Every component had to meet international safety standards while adapting to local conditions including monsoons, cyclones, and earthquake risks.

The partnership dynamics evolved significantly. Triumph Offshore Private Limited, a subsidiary of Swan Energy, took delivery of Vasant 1, India's first FSRU, in partnership with Indian Farmers Fertiliser Cooperative (IFFCO). IFFCO's involvement wasn't just financial—as India's largest fertilizer cooperative, they brought assured gas demand from urea plants.

Cyclone Tauktae in May 2021 was the project's darkest hour. With winds exceeding 185 km/h, it was the strongest cyclone to hit Gujarat in decades. The under-construction marine structures—designed to withstand storms—were obliterated. Years of work disappeared overnight. Insurance claims, contractor disputes, and force majeure declarations followed.

Yet the project survived. By March 2023, the project was 79.11% complete. The resilience came from aligned incentives—all stakeholders had too much invested to walk away. The oil companies needed the gas capacity. Banks had disbursed too much to write off loans. The Gujarat government wanted the economic development.

The commercial structure reveals sophisticated risk management. Swan Energy signed a Bareboat Charter Agreement with Triumph Offshore to charter the FSRU for 20 years. This separated vessel ownership from terminal operations, allowing different financing structures and risk profiles for each component.

The inaugural phase with investment of Rs.42bn ($504m) is set for completion by end of 2024. The subsequent phase, involving investment of Rs.8bn ($96m), will construct an additional jetty. The phased approach reduces execution risk while preserving expansion optionality.

What makes Jafrabad particularly strategic is its integration with India's gas grid. A 24-inch pipeline transports high-pressure gas from the FSRU to Gujarat State Petroleum's gas grid 2km away. This seemingly simple connection required years of negotiations, right-of-way acquisitions, and technical specifications to ensure seamless integration.

The operational model is equally sophisticated. Mitsui O.S.K. Lines signed agreement with SLPL for long-term operations/maintenance of FSRU and FSU. Mitsui is also investing in the project. This brings world-class operational expertise—critical for an industry where small mistakes can cause disasters.

As of late 2024, the terminal stands on the cusp of commissioning. The FSRU is in place, pipelines are connected, customers are waiting. After sixteen years since Swan first entered energy, seven years since construction began, and multiple near-death experiences, India's most unlikely energy infrastructure project is about to become operational.

The irony is palpable: a company that once wove cotton now handles cryogenic methane. The Sewri mill workers of 1909 would find the transformation incomprehensible. Yet in India's infrastructure story, such transformations aren't just possible—they're necessary.

VIII. The Veritas Acquisition & Petrochemical Play (2023)

In January 2023, company completed acquisition of majority stake in Veritas India Ltd for Rs. 260 Cr. VIL trades and distributes chemicals and petrochemical products used in paint, oil refining, etc. It operates a terminal in Hamriyah, UAE, with capacity of 1,70,000 MT.

This wasn't a random diversification. Veritas India represented a strategic bridge between Swan's LNG ambitions and the broader energy value chain. Petrochemicals and LNG share common customers—refineries and chemical plants that need both feedstock and fuel. The acquisition instantly gave Swan relationships with chemical manufacturers across India and the Middle East.

The Hamriyah terminal in UAE was the hidden gem. Located in Sharjah's free zone, it provided Swan with Middle East presence—crucial for LNG sourcing since Qatar and UAE dominate global LNG exports. The terminal's 170,000 MT capacity meant Swan could store and trade petrochemicals, generating cash flows while the LNG terminal was under construction.

Veritas's business model was asset-light but relationship-heavy. They didn't manufacture chemicals; they aggregated demand from Indian buyers, sourced from global suppliers, and managed logistics. Their value lay in market intelligence—knowing which refinery needed which grade of catalyst, which paint manufacturer was expanding capacity, which prices were moving where.

For Swan, this intelligence was invaluable. LNG and petrochemicals are complementary—natural gas is both fuel for chemical plants and feedstock for ammonia, methanol, and other chemicals. Understanding chemical demand patterns helps predict gas consumption. Relationships with chemical companies provide anchor customers for gas supply.

The integration revealed Swan's evolved corporate sophistication. Unlike the chaotic textile-to-real-estate transition, the Veritas acquisition was smooth. Management was retained, systems were integrated gradually, and synergies were captured methodically. The company had learned how to execute M&A.

The financial impact was immediate. Distribution & Development segment contribution jumped to 74% in H1 FY25 from 21% in FY23. Veritas's trading operations provided steady cash flows, reducing Swan's dependence on lumpy real estate sales and pre-operational LNG investments.

More importantly, Veritas provided optionality. If LNG demand disappointed, Swan could pivot to petrochemical storage. If chemical trading margins compressed, the LNG terminal would provide new revenue streams. In India's volatile energy market, such flexibility is invaluable.

The acquisition also signaled Swan's ambitions beyond Jafrabad. A successful LNG terminal operator needs multiple revenue streams—regasification fees, storage charges, trading margins. Veritas provided the trading capability. The Hamriyah terminal provided international presence. Piece by piece, Swan was assembling an integrated energy platform.

IX. Playbook: Lessons in Conglomerate Transformation

Swan Energy's journey from textile mill to LNG terminal offers a masterclass in corporate transformation, though not the kind taught at business schools. This is transformation through opportunism, patience, and a uniquely Indian ability to navigate chaos.

The Power of Patient Capital The Dave-Merchant families' greatest advantage wasn't wealth but time horizon. Unlike listed MNCs answering to quarterly earnings calls, or private equity funds with 5-7 year exits, they could wait decades for value creation. The mill lands acquired in 1992 weren't fully monetized until 2010. The LNG terminal conceived in 2008 won't generate revenues until 2025. This patience enabled contrarian bets that faster money couldn't make.

Riding India's Infrastructure Waves Swan's genius lay not in predicting the future but in recognizing present transitions. When textile manufacturing died, they didn't fight it—they pivoted to real estate. When real estate matured, they moved to energy. Each transition aligned with India's economic evolution: manufacturing (1909-1990s) → urbanization (2000-2010s) → infrastructure (2010s-present).

The Art of Regulatory Navigation In India, regulatory expertise is competitive advantage. Swan mastered this art across three different industries. Textile labor laws, real estate development codes, environmental clearances for LNG—each required different relationships, different approaches. Their ability to secure Gujarat's LNG terminal approval in 2012 and MOEF clearance in 2013 when established energy players couldn't demonstrates this capability.

Partnership as Risk Mitigation Swan never tried to go alone in unfamiliar territory. Piramal for real estate development. Gujarat Maritime Board for regulatory cover. Mitsui for FSRU operations. Each partner brought expertise Swan lacked, reducing execution risk while preserving upside. The 63% stake in Swan LNG shows they kept control while sharing risk.

Capital Allocation Across Cycles The company's capital allocation reveals sophisticated cycle timing. They invested in textiles during distress (1992), monetized real estate during boom (2004-2010), and entered LNG during planning phase (2008-2017) to commission during demand growth (2024+). This countercyclical approach—buying when others are selling, building when others are waiting—created enormous value.

Diversification vs. Focus Debate Swan challenges conventional wisdom about focus. Business schools preach core competency; Swan practices opportunistic diversification. Yet there's logic: each business generated capital for the next. Textiles provided land for real estate. Real estate provided capital for LNG. LNG will likely fund whatever comes next.

X. Bear vs. Bull Case & Financial Analysis

Market Cap: 13,134 Crore, Revenue: 4,938 Cr, Profit: 874 Cr tells only part of Swan's story. These consolidated numbers hide the transformation underneath—a profitable petrochemical trader, a soon-to-commission LNG terminal, and legacy real estate assets.

Company has low return on equity of 7.93% over last 3 years. For value investors, this is concerning. Why accept 8% ROE when fixed deposits offer similar returns? The answer lies in understanding Swan's capital cycle. The LNG terminal has consumed massive capital without generating revenues. Once operational, ROE should inflect dramatically.

The Bear Case

Execution risk dominates bearish concerns. The LNG terminal is 16 years in making, survived multiple cyclones, and still isn't operational. At 79.11% completion in March 2023, the remaining 21% could hide enormous problems. Marine construction is notorious for last-mile delays and cost overruns.

Competition is intensifying. Adani's Dhamra LNG terminal, H-Energy's Jaigarh facility, and Petronet's Dahej expansion are all coming online. India might face LNG terminal overcapacity just as Swan commissions. Utilization rates and tariffs could disappoint.

The customer concentration is concerning. Oil majors like IOC, BPCL, ONGC signed 20-year contracts, but these are take-or-pay agreements with escape clauses. If gas demand weakens or cheaper alternatives emerge, contracts can be renegotiated.

Global LNG markets add another risk layer. Qatar's massive expansion, US shale gas exports, and potential Russian return post-sanctions could crash LNG prices, making imports uneconomical versus domestic coal or renewable energy.

The Bull Case

India's energy demand growth is structural, not cyclical. With per capita energy consumption at one-third of global average, decades of growth lie ahead. Natural gas's share of India's energy mix at 6% versus global 24% suggests massive catch-up potential.

Swan LNG's location advantage—shortest distance from Gulf to any Indian terminal—provides structural cost advantage. In commodity markets, logistics costs determine competitiveness. Swan's proximity could mean 10-15% lower delivered costs.

The FSRU model provides flexibility that onshore terminals lack. If Indian demand disappoints, the vessel can be redeployed to Bangladesh or Sri Lanka. If demand exceeds expectations, additional FSRUs can be added quickly. This optionality has value beyond DCF models.

The integrated platform—LNG + petrochemicals + real estate—provides multiple growth vectors. Even if one disappoints, others can compensate. This diversification, often criticized by purists, provides downside protection in India's volatile markets.

AG&P LNG's recent partnership to form an LNG logistics venture and acquire stake in Swan LNG terminal provides external validation. AG&P, backed by Osaka Gas and JBIC, wouldn't partner without extensive due diligence.

Valuation Considerations

At ₹13,134 crore market cap, Swan trades at interesting multiples. The Veritas acquisition at ₹260 crore suggests the petrochemical business alone could be worth ₹1,000+ crore. The real estate assets, though legacy, have substantial value in Mumbai's market. The LNG terminal, with ₹4,200 crore invested, should be worth at least book value if operational.

Sum-of-parts valuation suggests significant upside if LNG terminal commissions successfully. But this requires faith in execution, confidence in India's gas demand, and patience for value realization—not every investor's cup of tea.

XI. Looking Forward: The Next Chapter

The new JV with AG&P LNG represents Swan's next evolution. Swan will hold 51% in the LNG supply company while AG&P takes 49%; the vessel company structure reverses with AG&P at 51% and Swan at 49%. This complex structure separates vessel ownership from trading operations, allowing specialized financing and risk management for each.

AG&P brings more than capital. Backed by Osaka Gas and Japan Bank for International Cooperation (JBIC), they provide access to Japanese LNG markets, technology, and financing. Japan, the world's largest LNG importer, offers partnership possibilities from upstream supply to downstream distribution.

India's energy transition creates unprecedented opportunities. The government's target of net-zero by 2070 requires massive infrastructure investment. Natural gas, as transition fuel between coal and renewables, will play crucial role. Swan's early mover advantage in LNG infrastructure positions them well.

Competition from Adani and Reliance is inevitable. Both conglomerates have announced LNG ambitions. But infrastructure isn't winner-take-all. India needs multiple terminals for energy security. Swan's operational terminal (when commissioned) provides first-mover advantages in customer relationships and operational learning.

The company's recent name change consideration (to Swan Corp Limited as of July 2025) signals ambitions beyond energy. Like Reliance's evolution from textiles to telecom, or Adani's from trading to infrastructure, Swan appears positioned for continuous transformation.

What success looks like in 2030: The LNG terminal operating at 80%+ utilization, generating ₹500+ crore EBITDA annually. A second terminal under development, possibly on India's east coast. The petrochemical business expanded to $1 billion revenues. Real estate monetization complete, providing growth capital. ROE normalized at 15-20%.

The risks remain substantial. Execution delays, demand disappointments, competitive pressure, regulatory changes—any could derail the story. But for patient investors who believe in India's energy demand, Swan Energy offers rare exposure to LNG infrastructure at reasonable valuations.

XII. Recent News

The revenue of Swan Energy for Sep '24 was ₹1063 crore compared to Jun '24 revenue of ₹1161 crore, representing decline of -8.44%. The EBITDA for Sep '24 was ₹151.43 crore compared to Jun '24 EBITDA of ₹400.71 crore, declining -62.21%. The net profit for Sep '24 was ₹67.13 crore compared to Jun '24 net profit of ₹267.67 crore, declining -74.92%.

Swan Energy's net profit jumped 406.31% since last year same period to ₹582.81Cr in Q3 2024-2025. The volatility in quarterly results reflects the lumpy nature of real estate sales and petrochemical trading, while the LNG terminal continues consuming capital without generating revenues.

Company name changed to Swan Corp Limited effective July 29, 2025. This rebranding signals broader ambitions beyond energy, though the strategic rationale remains unclear.

Nebula Energy revealed that its majority-owned AG&P LNG struck a new deal to create an LNG joint venture company in India with Swan Energy Limited. AG&P LNG's heads of agreement with Swan enables the duo to drive LNG innovation and supply, with AG&P acquiring a stake in the Swan LNG regasification terminal.

Stock performance has been volatile. Swan Energy share price was Rs 421.25 at 04:00 PM IST on 6th Aug 2025, down 2.24% from previous closing of Rs 430.90. Last 1 Month: share price moved down by 5.73%. Last 3 Months: share price moved up by 6.04%. Last 12 Months: share price moved down by 35.87%.

The all-time high of ₹809.80 in December 2024 reflects market excitement about LNG commissioning, though subsequent correction suggests execution concerns persist.

XIII. Links & Resources

Company Resources: - Official Website: swan.co.in - Investor Relations: swan.co.in/investor-corner - Annual Reports: Available on BSE/NSE websites

Regulatory Filings: - BSE: bseindia.com (Code: 503310) - NSE: nseindia.com (Symbol: SWANENERGY) - MCA Filings: mca.gov.in

Industry Research: - Petroleum Planning & Analysis Cell (PPAC): ppac.gov.in - Gujarat Maritime Board: gmbports.org - India Energy Outlook: IEA reports

Related Reading: - "Mumbai's Mill Lands: A Century of Change" - Economic & Political Weekly - "India's Natural Gas Market" - Oxford Institute for Energy Studies - "FSRU Technology and Applications" - International Gas Union

Note: This analysis is based on publicly available information and does not constitute investment advice. Potential investors should conduct their own due diligence and consult financial advisors before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube