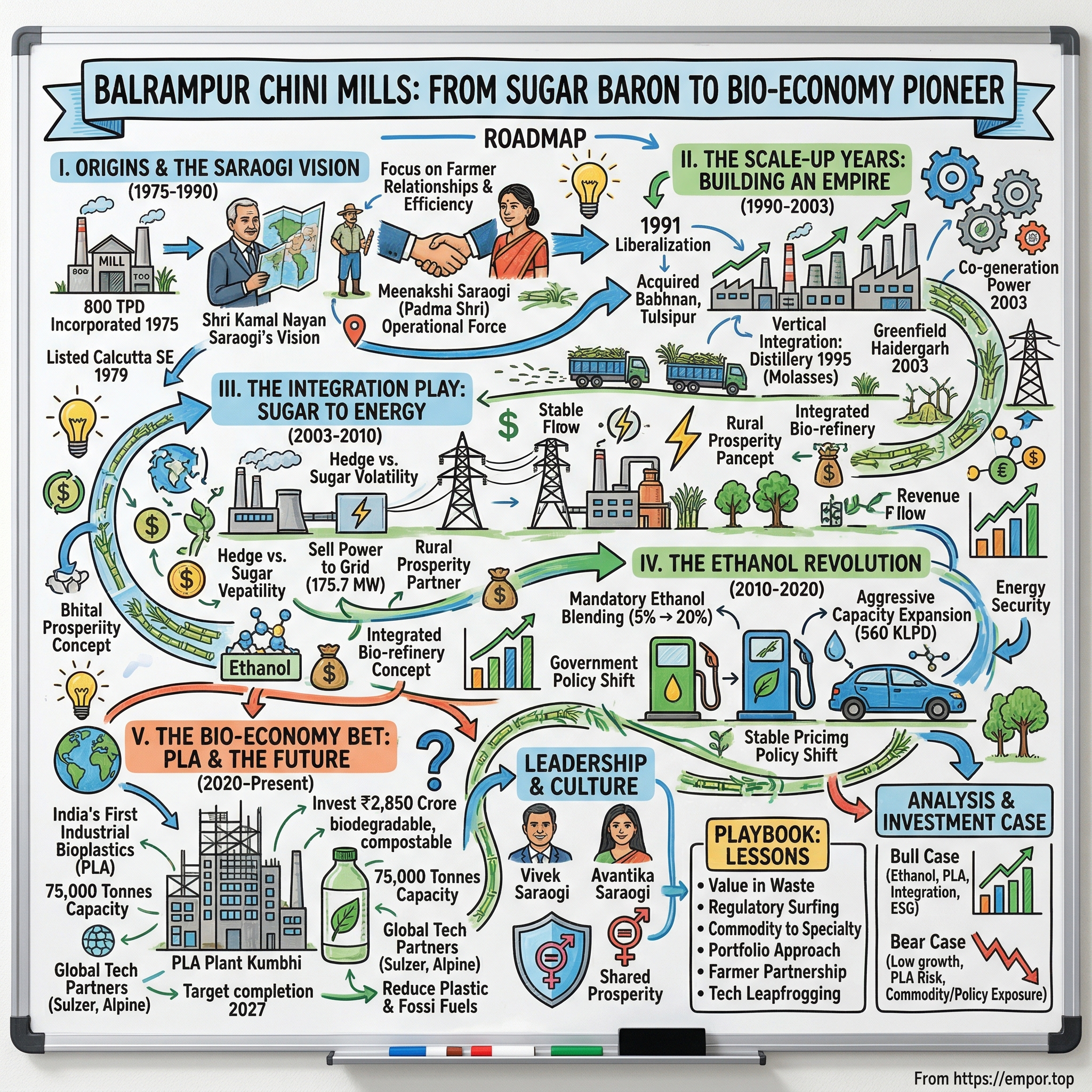

Balrampur Chini Mills: From Sugar Baron to Bio-Economy Pioneer

I. Introduction & Episode Roadmap

Picture this: It's 2024, and in the heart of Uttar Pradesh's sugar belt, massive fermentation tanks are churning not just ethanol, but the building blocks of India's first industrial-scale bioplastic facility. This isn't Silicon Valley disruption—it's something arguably more profound: a 49-year-old sugar company betting ₹2,850 crore that the future of materials isn't petroleum, but sugarcane.

Balrampur Chini Mills Limited stands today as one of India's largest integrated sugar companies, commanding a market capitalization of ₹11,180 crore (approximately $1.3 billion) with revenues of ₹5,415 crore. But those numbers only hint at a more fascinating transformation story. How does a traditional commodity processor—operating in one of India's most regulated, cyclical, and politically sensitive industries—reinvent itself as a bio-economy pioneer?

The answer lies in a multi-decade journey of calculated pivots, each building on the last: from sugar miller to power generator, from distiller to ethanol supplier, and now, from commodity producer to specialty chemicals manufacturer. It's a playbook for navigating India's complex business environment while riding successive waves of government policy, from the License Raj through liberalization to today's sustainability mandates.

This is the story of how the Saraogi family built an empire in India's heartland, turning what others saw as agricultural waste into profit centers, transforming farmer relationships into competitive moats, and positioning a traditional business at the forefront of India's green transition. It's about understanding when to be patient with commodities and when to make bold bets on emerging technologies. Most importantly, it's about recognizing that in India, the most innovative companies aren't always the ones starting from scratch—sometimes they're the ones that have been around long enough to truly understand the terrain.

II. Origins & The Saraogi Vision (1975–1990)

The year was 1975. India was under Emergency rule, the economy was tightly controlled, and obtaining an industrial license was like winning a lottery ticket. In this environment, on July 14th, a new entity was incorporated: Balrampur Chini Mills Limited. But the real story begins slightly earlier, with a man who saw opportunity where others saw only regulation and red tape.

Shri Kamal Nayan Saraogi wasn't building a startup in a garage—he was navigating the labyrinthine world of India's sugar industry, where success depended as much on managing government quotas as on operational efficiency. The company's first mill, transferred from Balrampur Commercial Enterprises Limited through an indenture of conveyance dated February 21, 1976, had a modest capacity of 800 tonnes per day. By today's standards, that's tiny. By 1975 standards in socialist India, it was a foothold in one of the economy's most essential sectors. The location mattered immensely. Eastern Uttar Pradesh wasn't just India's sugar belt—it was a region where relationships between mills and farmers determined everything. The License Raj meant that getting permission to expand capacity was harder than actually running the mills efficiently. But the Saraogis understood something crucial: in a controlled economy, the real competitive advantage wasn't technology or capital—it was navigating the system while building unbreakable bonds with your suppliers.

Meenakshi Saraogi, who would later be awarded the Padma Shri in 1992, became the operational force behind the company. While Kamal Nayan provided the vision and capital, she looked after factory operations for more than 31 years and became the driving force behind the organisation. This wasn't a Silicon Valley story of disruption—it was about patience, relationships, and understanding that in India's sugar industry, your real partners weren't investors or customers, but the thousands of farmers whose sugarcane fed your mills.

The company's structure evolved quickly. BCEL transferred the land, building, other assets and entire staff of its Balrampur sugar factory to BCML with effect from July 1, 1975. By 1979, a significant milestone: BCML ceased to be a subsidiary of BCEL and its shares were listed on the Calcutta Stock Exchange. This wasn't just a corporate restructuring—it was a declaration of independence, allowing the Saraogis to chart their own course.

The 1980s tested this independence severely. Sugar prices were controlled, distribution was regulated, and every ton of production needed government approval. While other industrialists chased licenses in Delhi's corridors of power, the Saraogis focused on something different: operational excellence and farmer relationships. They understood that in a commodity business with regulated prices, the only real differentiation was efficiency and reliability of supply.

By 1990, as India stood on the brink of economic transformation, Balrampur Chini had grown its original 800 TPD capacity significantly. But more importantly, it had built something intangible: trust. Trust with farmers who knew their payments would come on time. Trust with workers who saw the company as family. Trust with regulators who knew Balrampur wouldn't cut corners. This foundation would prove invaluable as India opened its economy and the real expansion began.

III. The Scale-Up Years: Building an Empire (1990–2003)

The year 1991 changed everything. As P.V. Narasimha Rao and Manmohan Singh dismantled the License Raj, Indian businesses faced a choice: stay comfortable in protected mediocrity or compete in an open market. For Balrampur Chini, liberalization wasn't a threat—it was the moment they'd been preparing for.

The company acquired a controlling stake in Babhnan Sugar Mill Ltd in 1990, which had a crushing capacity of 1,000 TCD. This wasn't just about adding capacity; it was about establishing a playbook for growth through acquisition—identifying underperforming assets, integrating them into Balrampur's operational framework, and turning them profitable. The Babhnan acquisition would become the template for future expansion.

But the real strategic insight came in 1995. While competitors focused solely on sugar production, Balrampur diversified into distillery operations at the Balrampur unit through commissioning a 60 klpd distillery. This wasn't diversification for its own sake—it was vertical integration at its most logical. Molasses, the byproduct of sugar production that most mills sold cheaply or discarded, could be converted into industrial alcohol and later ethanol. Every ton of sugarcane now had multiple revenue streams.

In 1998, the company acquired Tulsipur Sugar Company Limited with a capacity of 2,500 TCD. Each acquisition wasn't just about scale—it was about geographic diversification within Uttar Pradesh's sugar belt, ensuring that local weather variations or pest attacks couldn't cripple the entire operation.

The year 2003 marked a watershed moment. The company ventured into a 19.55 MW bagasse-based power generation unit at the Balrampur facility and set up an integrated greenfield sugar complex at Haidergarh with a crushing capacity of 4,000 TCD and co-generation capacity of 20.25 MW. This wasn't just about power generation—it was about reimagining what a sugar company could be.

Consider the elegance of the model: sugarcane comes in, gets crushed for juice which becomes sugar. The leftover bagasse, traditionally burned as waste, now fuels power plants. The molasses goes to distilleries for alcohol production. Nothing is wasted. Everything generates value. In an era before "circular economy" became a buzzword, Balrampur was living it.

The early 2000s also saw the company's most ambitious moves. In 2004, distillery operations were set up at Babhnan with 60 klpd capacity, and in 2005, the company acquired the Rauzagaon unit from Dhampur Sugar Mills with 7,500 TCD crushing capacity and 12 MW co-generation capacity.

By 2003, what started as a single 800 TPD mill had transformed into an integrated sugar complex with multiple facilities, distilleries, and power plants. Revenue wasn't just from sugar anymore—it was from power sold to the grid, industrial alcohol sold to chemical companies, and increasingly, ethanol that would soon become crucial for India's energy security.

IV. The Integration Play: Sugar to Energy (2003–2010)

The mid-2000s brought a fundamental question to India's sugar industry: were they food companies or energy companies? For Balrampur Chini, under the leadership that had now passed to Vivek Saraogi, the answer was both—and more.

The integration strategy accelerated dramatically. By 2005, the company had built what few understood at the time: a hedge against sugar price volatility built into its very structure. When sugar prices crashed, power generation and distillery operations provided stable cash flows. When molasses prices spiked, in-house distilleries captured the margin. This wasn't financial engineering—it was operational integration at its finest.

The co-generation power plants, with a collective saleable capacity of 175.7 megawatts, became integral to manufacturing facilities, with the business becoming a stable and substantial contributor to overall revenue. Think about what this meant: while competitors shut down during sugar downturns, Balrampur kept running, selling power to the grid, maintaining farmer relationships, and preparing for the next upturn.

The numbers tell a story of transformation. What started as experimental co-generation in 2003 had become, by 2010, a significant profit center. The company wasn't just burning bagasse for its own power needs—it was selling excess electricity to the state grid, turning what was once waste disposal cost into a revenue stream.

But perhaps the most prescient move was the quiet buildup of distillery capacity. While the ethanol blending program was still in its infancy, Balrampur was positioning itself for what it saw as inevitable: India's need to reduce oil imports and move toward renewable fuels. By 2010, the company had multiple distilleries operational, ready for the ethanol boom that was about to come.

The integration model also changed relationships with farmers. Now, Balrampur wasn't just buying their sugarcane—it was a partner in rural prosperity. The mills provided employment, the power plants lit up villages, and the company's agricultural extension services helped farmers improve yields. This wasn't corporate social responsibility as marketing—it was building a sustainable supply chain that would outlast any competitor who treated farmers as mere suppliers.

A significant corporate event occurred when Khalilabad Sugar Mills Pvt. Ltd was merged with the company pursuant to an order dated August 14, 2013, from the Board for Industrial and Financial Reconstruction, further consolidating Balrampur's position in the sector.

V. The Ethanol Revolution (2010–2020)

If sugar was the first act and power generation the second, ethanol would become the transformative third act of Balrampur Chini's evolution. The 2010s began with India importing over 70% of its oil needs, a massive drain on foreign exchange and energy security. The government's solution—mandatory ethanol blending with petrol—would transform Balrampur from a sugar company into an energy company.

The initial ethanol blending program targeted just 5% blending. For most sugar companies, this was a compliance requirement. For Balrampur, it was the future. The company began aggressively expanding distillery capacity, understanding that this wasn't just another byproduct—this was potentially more valuable than sugar itself.

The government's intention to accelerate the transition to an ethanol-based economy by advancing the 20% ethanol blending target from 2030 to 2023 created a massive opportunity. Balrampur was ready. By 2020, the company had commissioned a huge 170 kilo litres per day capacity distillery to manufacture ethanol.

The economics were compelling. Unlike sugar, where prices were volatile and often politically influenced, ethanol prices were set by oil marketing companies with reasonable margins. The offtake was guaranteed—oil companies had to buy ethanol to meet blending targets. For the first time in Indian sugar history, here was a product with stable pricing and assured demand.

Balrampur Chini Mills' distilleries, located in Balrampur, Babhnan, Mankapur and Gularia in Uttar Pradesh, reached a combined production capacity of 560 KLPD. This wasn't incremental growth—it was a complete transformation of the business model. By 2020, distillery operations were contributing 21% of revenue, up from virtually nothing two decades earlier.

The strategic implications were profound. Balrampur could now choose whether to produce sugar or divert sugarcane juice directly to ethanol production, depending on relative prices. This flexibility—unimaginable in the controlled economy of the 1970s—meant the company could optimize production in real-time based on market conditions.

The transformation wasn't without challenges. Building distilleries required massive capital investment. Environmental clearances were complex. Technology had to be imported and adapted. But Balrampur had something most competitors lacked: patient capital from a family that thought in decades, not quarters, and operational expertise built over forty years.

By 2020, as India announced even more ambitious ethanol blending targets, Balrampur wasn't scrambling to build capacity—it was already there. The company that started as a small sugar mill had become one of India's largest ethanol producers, supplying directly to oil marketing companies and helping India reduce its oil import dependence.

VI. The Bio-Economy Bet: PLA and the Future (2020–Present)

The boardroom discussions in 2020 must have been intense. Here was Balrampur Chini, having successfully navigated from sugar to power to ethanol, contemplating its biggest bet yet: becoming India's first industrial-scale bioplastic producer. The investment required was staggering—₹2,850 crore, more than a quarter of the company's market cap at the time.

The company announced plans to launch India's first industrial bioplastics plant, marking the inception of the country's first industrial-scale PLA production unit. Polylactic acid (PLA) isn't just another chemical—it's potentially the answer to the global plastic crisis. Made from fermenting sugarcane into lactic acid and then polymerizing it, PLA is biodegradable, compostable, and can replace petroleum-based plastics in everything from packaging to textiles.

The ambition was breathtaking. The planned facility at Kumbhi, Uttar Pradesh, would have a capacity of 75,000 tonnes per year and is expected to be completed by mid-2027. To put this in perspective, the global PLA market was only about 400,000 tonnes annually. Balrampur wasn't just entering the market—it was positioning itself as a major global player. The technology partnerships revealed the sophistication of the approach. Balrampur announced agreements with Sulzer, Alpine Engineering GmbH, and Jacobs Solutions for technology services, with Switzerland-based Sulzer delivering manufacturing technologies for key process stages including lactide synthesis, lactide purification, and polymerisation. This wasn't trying to reinvent the wheel—it was partnering with the best global technology providers to leapfrog into world-class production.

Sulzer's expertise is used in most PLA manufacturing plants in the world, signaling that Balrampur wasn't content with just entering the market—they wanted to be competitive with established players in Thailand, the USA, and China from day one.

The strategic rationale was compelling. India imports billions of dollars worth of plastics annually. Environmental regulations are tightening globally. Consumer brands are desperately seeking sustainable packaging alternatives. And here was Balrampur, with guaranteed sugarcane supply, integrated operations that could provide steam and power at cost, and decades of experience in fermentation technology through its distilleries.

As Vivek Saraogi, Chairman & Managing Director, stated: "The establishment of India's first PLA biopolymer manufacturing facility represents a monumental leap in our nation's industrial sustainability journey. By producing PLA at industrial scale, we are not only reducing dependence on fossil fuels but also setting new benchmarks for responsible manufacturing".

The investment structure showed financial prudence despite the bold vision. The ₹2,850 crore would be invested in phases, with ₹800 crore from internal accruals and ₹1,200 crore through debt—a conservative financing mix for such a transformative project.

VII. Current Operations & Scale

Step into any of Balrampur Chini's facilities today, and you're witnessing industrial integration at a scale that would make Henry Ford proud. The company operates 10 sugar factories, 5 distilleries, and 10 cogeneration units across Uttar Pradesh, creating an industrial ecosystem where every output from one process becomes input for another.

The numbers are staggering. The sugar factories, mainly located in the cane-rich belts of Eastern and Central Uttar Pradesh, have a combined crushing capacity of 76,500 tonnes per day. To put that in perspective, that's roughly the weight of 150 fully loaded Boeing 747s worth of sugarcane, crushed every single day during the season.

In fiscal year 2023, the company crushed 93.66 lakh tonnes of sugarcane and produced 8.83 lakh tonnes of sugar. But here's where the integration story gets interesting: The co-generation power plants, with a collective saleable capacity of 175.7 megawatts, have become a stable and substantial contributor to overall revenue, showcasing resilience and success in the power sector for over two decades.

The revenue breakdown tells the story of transformation. While 76% of business still comes from sugar, around 21% is now contributed by distillery operations. That might seem like sugar still dominates, but remember: distillery revenues are far more stable and carry higher margins. When sugar prices crash, ethanol prices hold steady. When molasses prices spike, the integrated model captures the value internally.

The operational footprint extends far beyond the factory gates. Balrampur Chini directly impacts thousands of farmer families across Uttar Pradesh. The company doesn't just buy sugarcane—it provides agricultural extension services, quality seeds, and technical support. As noted, educating farmers on enhancing profitability has been a focus since the time of founder Meenakshi Saraogi, whose vision led to the formation of a 'seed supermarket' where a seed nursery programme generated healthy seeds, with the company consulting farmers on seed development and customizing cane to the region's topography.

The distilleries, with their 560 KLPD capacity, aren't just producing industrial alcohol anymore. They're strategic assets in India's energy transition, with the ethanol produced majorly supplied to Oil Marketing Companies for blending with petrol. Every liter of ethanol produced is a liter of petroleum India doesn't have to import.

But perhaps the most impressive aspect of current operations is the flexibility. During sugar season, the mills run at full capacity. During off-season, the distilleries keep running on stored molasses. The power plants run year-round, switching between bagasse during crushing season and other biomass during off-season. This isn't just a sugar company that happens to make other products—it's an integrated bio-refinery that happens to make sugar.

VIII. Leadership & Culture

In Indian business, few things matter more than the people at the helm, and Balrampur Chini's leadership tells a story of evolution from traditional family business to professional management while retaining the best of both worlds.

Vivek Saraogi, who took over as Managing Director, represents the bridge between generations. Unlike the stereotype of the heir who coasts on family legacy, Saraogi has been the architect of Balrampur's transformation from sugar miller to integrated bio-economy player. His management philosophy can be summed up in a simple principle: in commodity businesses, you don't control prices, so you must control everything else—costs, efficiency, and optionality.

But the real story of modern Balrampur might be Avantika Saraogi, appointed as Executive Director effective January 1, 2024. She represents not just generational change but a fundamental shift in how the company thinks about its role in society. Under her influence, Balrampur has seen significant changes, especially in gender equality and agricultural innovation. One of her most notable achievements has been increasing the number of women in the workforce, promoting diversity within what has traditionally been a male-dominated industry.

The culture at Balrampur reflects this leadership evolution. Walk through the corporate office in Kolkata or the mills in Uttar Pradesh, and you'll notice something unusual for a traditional Indian commodity business: a surprising number of young professionals, many of them women, in operational roles. This isn't corporate window dressing—it's a recognition that managing modern bio-refineries requires different skills than running traditional sugar mills.

Meenakshi Saraogi, who was awarded the Padma Shri in 1992, set the tone for the company's relationship with its stakeholder ecosystem decades ago. Her philosophy—that the company's success was inseparable from farmer prosperity—became embedded in Balrampur's DNA. Today, that translates into programs that go beyond simple procurement: soil testing, crop advisory, advance payments during distress, and even education support for farmers' children.

The management structure reflects a careful balance. Family members hold key positions but are surrounded by professional managers. The CFO, technology heads, and operational leaders are industry veterans hired for expertise, not connections. Board meetings, according to those familiar with them, are rigorous affairs where family members are held to the same performance standards as professional managers.

What's particularly interesting is how the company manages the inherent tension in Indian family businesses between short-term market pressures and long-term family legacy. The PLA investment—requiring patient capital with returns expected only after 2027—could only happen in a company where leadership thinks in decades, not quarters.

The ESG initiatives aren't just compliance checkboxes. The company's sustainability report reads like a strategic document, with clear metrics on water usage, carbon footprint, and farmer welfare. This isn't greenwashing—when your raw material comes from thousands of small farmers and your factories operate in rural areas, sustainability isn't corporate responsibility; it's business continuity.

IX. Playbook: Lessons from Balrampur Chini

After nearly five decades of evolution, Balrampur Chini has inadvertently written a playbook for how traditional businesses can transform themselves in emerging markets. These aren't MBA case study theories—they're battle-tested strategies that worked in the complex reality of Indian business.

The Integration Strategy: From Waste to Wealth

The first lesson is about seeing value where others see waste. Every sugar company produces bagasse and molasses. Most treat them as disposal problems. Balrampur saw energy and chemical feedstock. The integration strategy wasn't implemented overnight—it evolved over decades, each addition building on the last. First sugar, then power from bagasse, then alcohol from molasses, then ethanol from alcohol, and now PLA from sugarcane. Each step used existing capabilities to build new ones.

The key insight: in commodity businesses, horizontal integration (buying more sugar mills) gives you scale but not pricing power. Vertical integration gives you optionality and margin stability. When sugar prices crash, you divert cane to ethanol. When power prices spike, you maximize generation. This flexibility is worth more than scale alone.

Riding Policy Waves: The Art of Regulatory Surfing

The second lesson is about policy as opportunity. Balrampur didn't fight government intervention in sugar—they surfed it. When the government mandated ethanol blending, Balrampur was ready with distillery capacity. When renewable power got priority dispatch, Balrampur had co-generation plants running. When plastic bans started appearing globally, Balrampur began planning PLA production.

The playbook: Don't wait for perfect policy. Build capabilities in anticipation of directional trends. India will need renewable energy—build power plants. India will reduce oil imports—build distilleries. The world will regulate plastic—prepare alternatives. Policy changes create sudden demand that rewards those who prepared, not those who react.

From Commodity to Specialty: The Value Migration

Sugar is the ultimate commodity—identical product, volatile prices, thin margins. But each move up the value chain improved economics. Power generation has regulated returns. Ethanol has assured offtake. PLA will have proprietary technology and brand value. The migration from commodity to specialty wasn't a single leap but a series of steps, each funded by cash flows from the previous business.

Managing Cyclicality: The Portfolio Approach

Sugar is cyclical. But sugar, power, and ethanol have different cycles. When they're combined in one company with operational flexibility, the volatility decreases dramatically. This isn't financial portfolio theory—it's operational portfolio management. The same sugarcane can become different products based on relative prices. The same farmers supply raw material for multiple value streams. The same management team optimizes across businesses in real-time.

The Farmer Partnership Model: Shared Prosperity as Strategy

In Indian sugar, your real competitive advantage isn't your factory—it's your catchment area farmers. Balrampur understood this decades ago. By investing in farmer education, providing quality seeds, ensuring timely payments, and supporting rural development, they created switching costs that no competitor can overcome with higher prices alone.

The deeper insight: in businesses dependent on agricultural raw materials, treating farmers as partners rather than suppliers creates a moat that's nearly impossible to replicate. New entrants can build factories and hire managers. They cannot quickly build trust with thousands of farmers developed over decades.

Technology Leapfrogging: Build vs. Partner Decisions

For PLA, Balrampur could have tried developing technology internally or buying a small technology company. Instead, they partnered with global leaders—Sulzer for process technology, Alpine for fermentation, Jacobs for project management. This wasn't lack of ambition—it was recognition that in specialty chemicals, being second-best in technology means being uncompetitive in global markets.

The lesson: in commodity businesses, operational excellence can be developed internally. In technology businesses, partnering with leaders accelerates time to market and reduces execution risk. Know when to build and when to buy.

X. Analysis & Investment Case

Standing back from the operational details, what do investors really need to know about Balrampur Chini? The investment case isn't simple—it requires understanding both the current business generating cash and the future business consuming capital.

Bull Case: The Bio-Economy Transformation Story

The bull case starts with India's ethanol opportunity. India imports over 85% of its crude oil needs, spending hundreds of billions of dollars annually. The government's 20% ethanol blending target by 2025 isn't just policy aspiration—it's economic necessity. Balrampur, with 560 KLPD distillery capacity already operational, is positioned to capture disproportionate value from this transition.

The math is compelling. At 20% blending, India needs about 10 billion liters of ethanol annually. Current production is less than half that. Prices are set by the government with assured margins. Offtake is guaranteed through oil marketing companies. This isn't a market that might develop—it's a market that must develop.

The PLA project adds a different dimension. The new plant will produce 75,000 tonnes of compostable, wholly recyclable bioplastic per year, entering a global market growing at 20% annually. With plastic bans spreading globally and brands desperately seeking sustainable alternatives, being India's first mover in industrial-scale PLA production could be transformative.

The operational metrics support the transformation story. The integrated model provides margin stability through cycles. The balance sheet is strong enough to fund growth without excessive leverage. Management has successfully executed multiple expansions and integrations. The ESG credentials attract institutional capital increasingly focused on sustainability.

Bear Case: The Execution and Market Risks

The bear case starts with sobering numbers. The company has delivered poor sales growth of just 2.69% over the past five years. For a company supposedly riding mega-trends, that's concerning. Sugar still represents 76% of revenues, meaning the company remains highly exposed to commodity price volatility and regulatory uncertainty.

The PLA project, while exciting, is massive and risky. ₹2,850 crore is a huge bet on unproven demand in India. Global PLA producers like NatureWorks and Total Corbion have decades of experience and established customer relationships. Breaking into global supply chains won't be easy, regardless of production capability.

Regulatory risk remains omnipresent. Sugar pricing, ethanol blending mandates, power purchase agreements—all depend on government policy that can change with political winds. The company's improving economics over recent years coincided with favorable policies. What happens when policies turn unfavorable?

Competition is intensifying. Every sugar company is building distillery capacity. New entrants are eyeing the ethanol opportunity. In PLA, global giants won't cede the Indian market without a fight. The first-mover advantage in capital-intensive commodity businesses often becomes the first-mover disadvantage when technology improves or demand disappoints.

Valuation & Market Position

At current levels, the stock trades at 2.96 times book value and a PE ratio of approximately 27x—elevated for the sugar sector but perhaps justified for a company transforming into specialty chemicals. The market cap of ₹11,180 crore implies significant value creation from the PLA project and continued ethanol growth.

Compared to peers like Shree Renuka Sugars or Dhampur Sugar Mills, Balrampur commands premium valuations. This premium reflects superior operational metrics, stronger balance sheet, and the PLA optionality. Whether this premium is justified depends on execution of the transformation strategy.

The key question for investors: Is this a sugar company with some interesting side businesses, or a bio-economy company that happens to make sugar? The market is betting on the latter, but the proof will come over the next three years as ethanol scales and PLA comes online.

XI. The Next Chapter: 2025 and Beyond

As 2025 unfolds, Balrampur Chini stands at an inflection point. The decisions made and executed over the next few years will determine whether it becomes India's bio-economy champion or remains a well-run sugar company with diversification ventures.

The PLA plant, breaking ground and targeting mid-2027 completion, represents more than just capital investment. The project is expected to generate 225 direct jobs in manufacturing, R&D, and operations, while creating over 2,000 indirect jobs across the value chain. This isn't just about Balrampur—it's about India establishing itself in the global bioplastics value chain.

The global context is favorable. The bioplastics market, currently around $15 billion, is projected to exceed $30 billion by 2030. Environmental regulations are tightening globally. Consumer brands are making ambitious sustainability commitments they must fulfill. India, with its agricultural base and growing manufacturing capabilities, is perfectly positioned to capture value in this transition.

But success isn't guaranteed. The next three years will test Balrampur's execution capabilities like never before. Building and commissioning a world-scale PLA plant while maintaining sugar operations, scaling ethanol production, and managing farmer relationships—it's an operational challenge that would stress any organization.

The strategic questions facing management are profound. Should they partner with global consumer brands to secure PLA offtake? Should they backward integrate into lactic acid production beyond fermentation? Should they explore other bio-based chemicals? Each decision shapes the company's trajectory for decades.

The competition is watching and preparing. If Balrampur succeeds with PLA, others will follow. The first-mover advantage is real but temporary. The company must not just build the plant but also develop markets, create brands, and establish distribution channels. This requires capabilities beyond traditional sugar industry competencies.

India's bio-economy ambitions provide tailwinds. The government's push for sustainable materials, reducing import dependence, and rural prosperity aligns perfectly with Balrampur's strategy. But government support can be fickle, and the company must build a business that succeeds without subsidies or protection.

Can Balrampur become India's Cargill—a diversified agribusiness giant that touches multiple points in the food and materials value chain? The pieces are in place: agricultural sourcing capabilities, processing expertise, technology partnerships, and capital access. What remains is execution.

The sustainability imperative adds urgency. Climate change threatens agricultural productivity. Water scarcity challenges traditional farming. Plastic pollution demands solutions. Balrampur's integrated model—turning renewable sugarcane into food, fuel, and materials—offers a template for sustainable industrialization. But templates must become reality, and reality is always messier than strategy documents.

Looking ahead, several factors will determine success. The ethanol blending program must proceed as planned—any rollback would impact revenues significantly. The PLA plant must commission on time and budget—delays or cost overruns would stress finances and credibility. Global PLA markets must remain favorable—a price crash would devastate project economics. And through it all, sugar operations must remain stable, generating cash to fund transformation.

XII. Recent News & Developments

The recent financial performance reflects both the opportunities and challenges of transformation. In Q3 FY2024-2025, Balrampur Chini's revenue fell 6.37% to ₹1,207.95 crore compared to the same period last year, while net profit fell 22.84% to ₹70.47 crore. However, on a quarterly basis, the company generated a 4.9% jump in net profits compared to the previous quarter.

The market's assessment remains optimistic despite near-term headwinds. According to 7 analysts, 100% recommend a 'BUY' rating for Balrampur Chini Mills with an average target price of ₹677.86, representing an upside of 15.06% from current levels, with JM Financial maintaining a 'Buy' rating and raising the target price to Rs 700.

A significant milestone was reached in May 2025. Balrampur Chini Mills signed a memorandum of understanding with the Uttar Pradesh government to invest Rs 2,850 crore in a 250 TPD polylactic acid plant at Kumbhi Chini Mills, emphasizing innovation in bioplastics. The construction has begun, with the company breaking ground on what will be India's first industrial-scale PLA facility.

The operational momentum continues to build. Revenue has been up for the last 2 quarters, from ₹1.20K crore to ₹1.52K crore, with an average increase of 20.7% per quarter, while net profit has been up for the last 3 quarters, from ₹67.18 crore to ₹229.12 crore, with an average increase of 37.0% per quarter.

Governance changes signal the next generation taking charge. On August 12, 2025, the board approved the allotment of 41,587 equity shares as part of employee stock options, indicating a focus on talent retention as the company enters more sophisticated businesses.

The sugar industry context remains challenging. Sugar prices continue to be volatile, and regulatory uncertainty persists around cane pricing mechanisms. But Balrampur's integrated model is proving its worth—when sugar margins compress, ethanol and power provide stability.

Looking at the broader market position, Balrampur Chini commands a market cap of ₹11,180 crore (up 11.4% in 1 year) with promoter holding at 42.9%. The stock is trading at 2.96 times book value—a premium valuation for the sugar sector but potentially justified given the transformation underway.

The company's strategic priorities for the remainder of 2025 are clear: execute the PLA project on schedule, maximize ethanol production to capitalize on blending mandates, and maintain operational excellence in sugar operations to fund the transformation. With construction underway on the PLA plant and distillery operations running at high capacity, Balrampur Chini is at a critical juncture where execution will determine whether it becomes India's bio-economy champion or remains a well-run sugar company with interesting side ventures.

The investment case ultimately comes down to a simple question: Can a traditional sugar company successfully transform into a modern bio-materials company? The pieces are in place—technology partnerships, capital commitment, operational expertise, and favorable policy environment. What remains is execution, and the next 24 months will be decisive in determining whether Balrampur Chini Mills can complete its remarkable transformation from sugar baron to bio-economy pioneer.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube