Transrail Lighting Limited: From Partnership Firm to Infrastructure Powerhouse

I. Introduction & Episode Roadmap

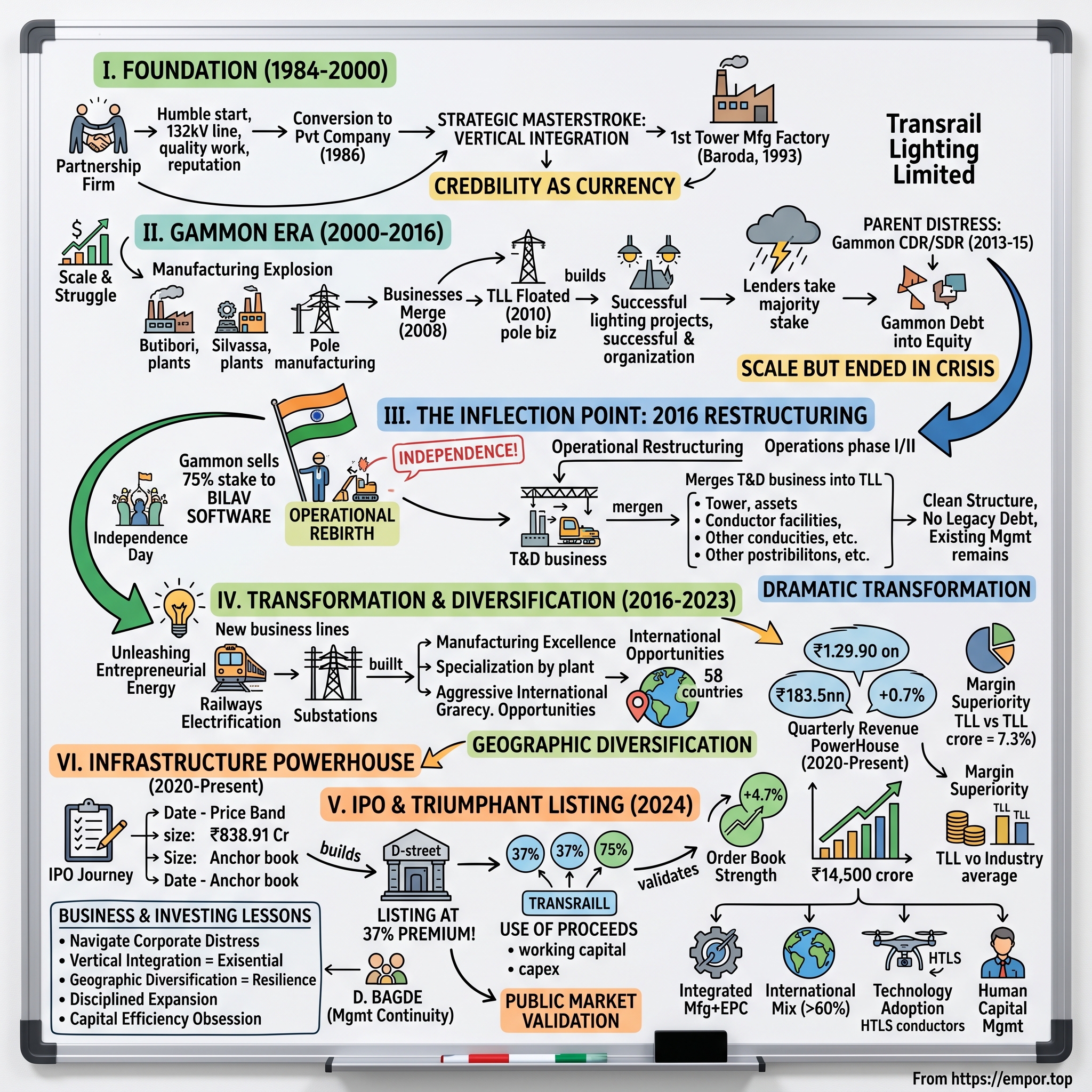

Picture this: It's 1984, and in a small corner of India's bustling infrastructure landscape, a partnership firm takes on its first foundation work for a 132kV transmission line between Ode and Anand in Gujarat. The contractor? Dodsal. The client? Gujarat Electricity Board. The ambition? Modest—just to execute quality work and build a reputation. In 1984, the Company started with first foundation work on 132kV line.

Fast forward four decades, and that humble partnership—Transrail Engineering Company—has metamorphosed into Transrail Lighting Limited with a market capitalization of ₹9,863 crore, executing projects across 58 countries. The company has constructed over 34,654 circuit kilometers of transmission lines and 30,000 CKM of distribution lines as of June 2024, while supplying over 800,000 tonnes of galvanized steel towers and 100,000 kilometers of conductors.

How does a small transmission line contractor transform into one of India's leading EPC companies, surviving parent company distress, navigating strategic debt restructuring, and eventually commanding a premium valuation in public markets? This is a story of resilience, strategic pivots, and the unglamorous but essential business of keeping the lights on—literally—across continents.

The narrative arc we'll follow today traces five critical inflection points: the early partnership years when credibility was currency, the Gammon era that brought scale but ended in crisis, the dramatic 2016 restructuring that gave the company its independence, the post-restructuring transformation under Digambar Bagde's leadership, and the triumphant 2024 IPO that saw the stock list at a 37% premium. Each phase reveals lessons about survival, adaptation, and the art of building infrastructure businesses in emerging markets.

What makes Transrail's story particularly compelling isn't just the numbers—though jumping from a partnership firm to executing ₹1,340 crore in quarterly revenue is impressive—but the strategic chess moves that enabled this transformation. Vertical integration when others outsourced. Geographic diversification when peers stayed domestic. Business line expansion when conventional wisdom suggested focus. These contrarian bets, we'll discover, weren't random—they were deliberate responses to market realities and competitive dynamics.

As we dissect this journey, we'll encounter a cast of characters who shaped the company's destiny: Digambar Bagde, who has been at the forefront of India's T&D infrastructure sector for more than 35 years, the Gammon India management who provided scale but couldn't sustain it, the mysterious Bilav Software that emerged as a white knight in 2016, and the public market investors who validated the transformation with their capital in 2024.

The structure of our exploration mirrors the company's evolution: from foundation to crisis, from crisis to transformation, from transformation to public validation. We'll examine not just what happened, but why it mattered—for investors, for India's infrastructure development, and for understanding how industrial companies navigate distress and emerge stronger. So let's begin where all great infrastructure stories start: with ambitious engineers, modest capital, and the audacity to dream bigger than circumstances suggest.

II. The Foundation Years: Partnership to Private Company (1984-2000)

The monsoons of 1984 brought more than just rain to Gujarat—they marked the birth of an infrastructure story that would span continents. Transrail Engineering Company (TEC) emerged as a partnership firm with a singular focus: executing foundation work for transmission lines. The Rs.1,900-crore EPC major, Transrail started with a humble beginning as a partnership firm called Transrail Engineering Company (TEC), which commenced business with the first foundation on 132kV Ode–Anand transmission line for Gujarat Electricity Board (GEB).

The man behind this venture wasn't a typical entrepreneur with deep pockets or political connections. Prior to starting Transrail Engineering Company in 1984, Digambar worked for 13 years at a transmission line company. "I was known as a transmission line man," he says. This wasn't venture-backed disruption—this was old-school, boots-on-the-ground infrastructure building, where reputation was earned one foundation at a time.

By 1986, the partnership had proven viable enough to warrant formal incorporation. It quickly scaled up and got converted into a private company in 1986. But the real strategic masterstroke came in 1993, revealing early signs of the vertical integration philosophy that would define Transrail's competitive advantage. In 1993, Associated Transrail Structures Ltd (ATSL) was incorporated to set up 1st factory for Tower manufacturing in Baroda.

Think about the audacity of this move. Here's a services company, barely nine years old, deciding to backward integrate into manufacturing. Most EPC contractors in the 1990s were content to remain asset-light, sourcing towers from third parties and focusing on execution. But Digambar Bagde saw what others missed: in a market where project delays could kill margins and supply chain unreliability could destroy reputations, controlling your critical inputs wasn't just strategic—it was existential.

The Baroda factory wasn't just about manufacturing towers; it was about controlling destiny. When you're bidding for transmission line projects, being able to guarantee both manufacturing quality and delivery timelines gives you an edge that pure-play contractors can't match. This integration would prove prescient when, years later, commodity price volatility and supply chain disruptions would cripple competitors who remained dependent on third-party suppliers.

The 1990s Indian infrastructure market was a peculiar beast. Liberalization had begun, but the sector remained dominated by public sector undertakings and established players with decades-old relationships. For a company like Transrail, breaking in meant competing on two fronts: price and reliability. The former was table stakes; the latter required building credibility project by project, deadline by deadline.

Transrail Engineering started off purely as a service company. Then, in 1993, Digambar incorporated another company called Associated Transrail Structures. The objective of Associated Transrail Structures was to manufacture the towers for transmission lines. This dual-company structure—TEC for services, ATSL for manufacturing—might seem unnecessarily complex, but it served a purpose. It allowed focused management attention on two very different business models while maintaining operational synergies.

The late 1990s brought validation. Projects were completed. Payments were received. The order book grew. But more importantly, the company had solved the fundamental challenge that kills most infrastructure startups: working capital management. By manufacturing their own towers, they could better manage inventory, control credit terms, and most critically, reduce the cash conversion cycle that strangles so many EPC companies.

What's remarkable about this period isn't the growth—though scaling from a partnership to a private company with manufacturing capabilities in 16 years is impressive—but the strategic patience. While dot-com mania gripped India and fortunes were being made in software and services, Transrail stayed focused on the decidedly unsexy business of erecting transmission towers. No pivots to IT services. No diversification into real estate. Just towers, lines, and foundations, executed with the precision of engineers who understood that in infrastructure, reputation compounds slower than software valuations but lasts infinitely longer.

"We were operating with the two different companies," he explains. Digambar then decided to merge the two companies in 2001. This merger of TEC and ATSL in 2001 marked the end of the foundation phase and the beginning of a new chapter. The company had proven it could execute, it could manufacture, and it could grow. What it needed now was capital and scale. Enter Gammon India, stage left, with promises of transformation that would prove both blessing and curse.

III. The Gammon Era: Scale & Struggle (2000-2016)

The millennium brought new ambitions. After showing viable growth, Digambar invited India's leading civil construction company, Gammon India, to take a stake in the company in 2000. This wasn't just any investor—Gammon India was infrastructure royalty, a company whose DNA traced back to 1922, with landmark projects across India's landscape. For Transrail, this was like a promising startup getting acquired by Google, except the currency was concrete and steel instead of code and algorithms.

The initial years under Gammon's umbrella delivered on the promise. Manufacturing capacity exploded with strategic precision: one plant at Nagpur's Butibori in 2004 for tower manufacturing; a conductor manufacturing plant at Silvassa in 2007; a tower manufacturing unit along with a tower testing station at Deoli in 2009; and a steel pole manufacturing plant at Silvassa in 2010. Each facility represented a calculated bet on India's infrastructure boom, positioning Transrail to capture value across the transmission and distribution value chain.

The businesses eventually merged in 2008. In 2009, ATSL was merged with Gammon India Ltd. In 2010 GIL floated a company under the name of "Transrail Lighting Ltd" for the pole manufacturing business. The restructuring seemed logical—consolidate operations, streamline reporting, leverage Gammon's balance sheet for larger projects.

The 2010 entry into lighting infrastructure revealed Gammon's ambitions for Transrail. This wasn't just about transmission lines anymore. The company won contracts for prestigious projects like the Pallekele Cricket Stadium in Sri Lanka and the Maharashtra Cricket Association Stadium—high-profile wins that showcased capabilities beyond traditional T&D work. The vision was clear: transform Transrail from a transmission specialist into an integrated infrastructure player.

But while Transrail was building towers and stringing conductors, storm clouds were gathering over the parent. Gammon India, like many infrastructure giants of that era, had gorged on debt during the boom years. Projects were delayed. Receivables stretched. The aggressive bidding that won contracts became the aggressive financing that killed cash flows. By 2013, Gammon entered Corporate Debt Restructuring (CDR), a polite euphemism for "we can't pay our debts but please don't liquidate us."

The numbers were staggering. Gammon India's Lenders faced a daunting task of restructuring Rs 14,810 crore Debt. In January 2016, Banks & Financial Institution acquired majority stake (52%) in Gammon India by converting Rs 14,810 crore debt into equity. This wasn't a restructuring—it was a financial earthquake that would reshape India's infrastructure landscape.

For Transrail, being a subsidiary of a distressed parent was like being a healthy organ in a failing body. The business was sound—orders were flowing, factories were producing, projects were executing. But the Gammon association created perception problems. Suppliers worried about payments. Customers questioned continuity. Employees wondered about their futures. The very association that had provided scale now threatened survival.

The Strategic Debt Restructuring (SDR) mechanism, introduced by RBI in 2015, offered a lifeline—but with strings that looked more like chains. In Nov 2015, lenders decided to convert part of Gammon India's Rs.14,810 crore debt into equity in a prelude to changing its management in a so-called strategic debt restructuring (SDR) exercise. Gammon India is the sixth company in which bankers have decided to take majority control by converting debt into equity. Banks now control 63% stake in debt-laden Gammon India.

The lenders' plan was surgical: separate the viable businesses from the distressed parent, find credible buyers, and recover what they could. Gammon India restructured its power transmission and distribution (T&D) business by transferring part of its T&D unit to its subsidiary, Transrail Lighting Ltd (TLL) on a slump sale basis & later sold 75% stake in TLL to Bilav Software Pvt to revive the business.

The Gammon years, viewed in retrospect, were both accelerator and anchor. The infrastructure, manufacturing capabilities, and market presence built during this period provided the foundation for future growth. The four manufacturing units, the international project experience, the technical capabilities—all were Gammon-era additions that would prove invaluable. But the financial distress, the reputation challenges, and the uncertainty of restructuring nearly destroyed what two decades had built.

What saved Transrail wasn't just the SDR mechanism or lender forbearance. It was the underlying business quality—a profitable operation trapped in a distressed structure, waiting for the right financial engineering to set it free. The stage was set for the most dramatic transformation in the company's history.

IV. The Critical Inflection Point: 2016 Restructuring

February 26, 2016, marked Transrail's independence day. Gammon India has transferred 75% of its shareholding in Transrail Lighting (TLL) to Bilav Software on February 26, 2016. Pursuant to this transfer, Transrail Lighting ceases to be a subsidiary of Gammon India. The buyer's name—Bilav Software Private Limited—raised eyebrows. A software company buying a transmission tower manufacturer? The optics were puzzling, but the transaction was real: The shareholder agreement is already signed with Bilav Software Private Limited for the T&D Businesses wherein they have acquired 75% stake in TLL at a cost of Rs. 2.33 Crore from GIL. They will also invest another Rs. 47.67 Crore approximately in TLL.

The price—₹2.33 crore for 75% of a company that would be worth ₹9,863 crore eight years later—seems absurd in hindsight. But context matters. This wasn't a normal M&A transaction; it was a distressed sale under SDR, where speed mattered more than price discovery. The lenders needed to move assets off Gammon's books. Bilav Software, despite its incongruous name, brought what Transrail desperately needed: capital, credibility, and most importantly, independence from a toxic parent.

The restructuring wasn't just about changing shareholders. Later, in 2016, under the restructuring of Gammon group, the T&D business of Gammon India Ltd was merged into Transrail Lighting Ltd and Gammon sold its 75 per cent stake to a new investor. The real genius lay in the operational restructuring that followed. April 19, 2017, marked the completion of the second phase: Gammon India Limited GIL transferred its Transmission and Distribution Business including the tower testing facility located at Deoli Maharashtra and tower manufacturing facilities located at Baroda and Nagpur division of conductor factory at Silvassa Dadra and Nagar Haveli and the tower manufacturing facility at Deoli Maharashtra to the Company. And as a result said Scheme of Arrangement was made effective from April 20 2017.

What emerged was a clean structure: one company, four manufacturing units, complete T&D capabilities, and no legacy debt. The management, led by Digambar Bagde who had been with the business since 1984, remained in place—critical for maintaining customer relationships and operational continuity. Transrail Lighting Limited is managed by the Board of Directors led by Mr. Digambar Bagde, Managing Director, who has an experience in transmission lines designing.

The immediate post-restructuring period tested everyone involved. Customers needed reassurance that project execution wouldn't suffer. Suppliers required comfort on payment terms. Employees sought clarity on career prospects. Banks, burned by the Gammon experience, demanded conservative financial management. The company's response was pragmatic: keep executing projects, maintain quality, and let performance speak louder than promises.

The capital structure post-restructuring was deliberately conservative. As part of the carve out proposal of T&D Business Rs. 505 Crore funded and Rs. 3,350 Crore non-funded exposure will be transferred to TLL. This wasn't the leveraged buyout playbook of loading debt onto the acquired company. Instead, it was a careful balance—enough leverage to fund operations but not enough to constrain growth.

The strategic decisions made in 2016-2017 would define Transrail's trajectory. First, maintain focus on the core T&D business while selectively diversifying. From 2016, the company has seen next phase of growth and has further diversified into railways and substation businesses. Second, leverage the manufacturing infrastructure inherited from Gammon but optimize it for efficiency rather than scale. Third, pursue international opportunities aggressively—geography diversification would reduce dependence on Indian government contracts and provide natural hedging against domestic economic cycles.

The 2016 restructuring wasn't just financial engineering—it was organizational rebirth. The company that emerged bore the same name and operated the same factories, but the mindset had fundamentally shifted. No longer a subsidiary executing someone else's vision, Transrail was now master of its own destiny. The proof would come in the numbers: revenue growth, margin expansion, and eventually, public market validation. But first, the company had to prove it could not just survive independence, but thrive in it.

V. Business Diversification & Capability Building (2016-2023)

Liberation from Gammon unleashed entrepreneurial energy that had been dormant for years. The management, no longer constrained by a parent company's financial distress, began executing a diversification strategy that was both ambitious and calculated. Railways and substations weren't random additions—they were logical adjacencies that leveraged existing capabilities while opening new revenue streams.

The railway electrification opportunity was particularly compelling. India's massive push toward electric traction—targeting 100% electrification of broad-gauge routes—created a ₹100,000 crore market opportunity. For a company with expertise in stringing conductors and erecting structures, railway overhead equipment was a natural extension. The early wins, including a ₹395 crore order from IRCON, validated the strategy.

But the real story of this period wasn't just business line expansion—it was operational excellence. The four manufacturing units inherited from the Gammon era were transformed from capacity assets into efficiency engines. The Vadodara facility specialized in heavy towers. Deoli focused on testing and specialized structures. The two Silvassa plants handled conductors and monopoles. Each unit was optimized for its specific product line, creating manufacturing synergies that pure-play EPC competitors couldn't match.

The company has executed 34,654 circuit kilometers (CKM) of transmission lines and 30,000 CKM of distribution lines as of June 2024. It provides EPC services for substations up to 765 kilovolts and specialises in high voltage (HV) and extra high voltage (EHV) segments. These aren't just numbers—they represent thousands of villages electrified, industrial corridors powered, and cities illuminated.

The international expansion during this period was particularly strategic. While Indian competitors focused on domestic orders, Transrail aggressively pursued opportunities in Africa, Southeast Asia, and even Europe. By 2024, the company had established a presence in 58 countries. This wasn't just about revenue diversification—it was about learning. African projects taught them to operate in challenging logistics environments. Southeast Asian contracts exposed them to different technical standards. Each international project added to the company's capability repertoire.

Transrail expects its lighting infrastructure division's revenue to grow at a 15–17% compound annual rate over the next three years. The international market initially made up 10–15% of the company's product portfolio, but this year its order book has substantially risen from 15 to 30%. The shift toward international orders wasn't accidental—it was a deliberate strategy to reduce dependence on Indian government contracts and their associated payment delays.

The lighting division, initially seen as a small diversification, began showing promise. LED technology was transforming street lighting globally, and Transrail's ability to provide integrated solutions—poles, fixtures, and installation—positioned it well for smart city projects. The division might have contributed only 2% of revenues, but it provided strategic optionality for future growth.

Technology adoption during this period was pragmatic rather than revolutionary. The company didn't chase digital transformation buzzwords but focused on practical improvements: better project management systems, real-time inventory tracking, and automated quality control at manufacturing units. The tower testing facility at Deoli, with its ability to test structures up to 765kV, became a differentiator in winning high-value contracts.

The workforce evolution was equally important. As of June 2024, the company has 114 employees in the design and engineering team. This wasn't just headcount growth—it was capability building. Engineers trained on international projects brought back best practices. The design team's ability to customize solutions for specific geographies and technical requirements became a competitive advantage.

Financial discipline underpinned everything. Working capital management—the Achilles heel of many EPC companies—was treated as a core competency. The company's ability to maintain EBITDA margins above industry average while growing rapidly demonstrated that growth and profitability weren't mutually exclusive.

By 2023, Transrail had transformed from a distressed subsidiary into a formidable independent player. The order book had grown substantially, international presence was established, and operational metrics were best-in-class. The company was ready for its next act: accessing public capital markets to fuel further growth. The IPO wasn't just about raising money—it was about validation, visibility, and creating a currency for future acquisitions.

VI. The IPO Journey & Market Debut (2024)

The IPO preparation began long before the December 2024 launch. Management knew that public market investors would scrutinize everything: the Gammon history, the mysterious Bilav Software ownership, the concentrated customer base, the international execution risks. The prospectus had to tell a story that acknowledged the past while focusing on the future.

Transrail Lighting IPO opens on 19th - 23rd Dec 2024. IPO Price band: ₹410 to ₹432 per share, IPO lot size: 34 shares. Transrail Lighting IPO opens from 19 December to 23 December 2024. The size of Transrail Lighting IPO is ₹838.91 Cr. The price of Transrail Lighting IPO is fixed at ₹410 to ₹432 per share.

The structure was deliberately balanced: a fresh issue of 0.93 crore shares aggregating ₹400 crore and an offer for sale of 1.02 crore shares amounting to ₹438.91 crore. The fresh capital would fund working capital and growth capex. The OFS gave early investors partial exit while maintaining majority control—a signal of continued confidence.

The anchor book told the story. ₹245.97 crore raised from institutional investors before the public opening provided validation. These weren't retail punters betting on listing gains—these were sophisticated funds that had done their diligence, studied the order book, and believed in the story.

Day 1 subscription of over 2x, with retail at 2.97x, signaled broad-based interest. The retail enthusiasm was particularly telling—despite the complex history and B2B nature of the business, individual investors saw value. By close, QIBs had warmed up, taking the overall subscription to healthy levels.

Transrail Lighting listed on the D-street at 37% premium. The shares listed at ₹590 on NSE, 36.57% higher from the issue price of ₹432 and at ₹585.15 on BSE. The listing day pop wasn't just about favorable market conditions—it was validation of the transformation story. The market was saying: we believe this company has successfully separated from its distressed past and has a compelling future.

The post-listing performance has been even more impressive. From the listing price of ₹590 in December 2024 to ₹748.50 by September 2025, the stock has delivered substantial returns. But more importantly, the trading volumes and institutional participation suggest this isn't just momentum—it's fundamental revaluation.

The use of IPO proceeds was conservative and strategic. Working capital funding would reduce reliance on expensive short-term debt. Capacity expansion would be selective, focusing on high-margin products. No grandiose acquisitions or unrelated diversifications—just steady execution of the core strategy.

What made the IPO successful wasn't just timing—though launching during a bull market certainly helped—but the quality of the underlying business transformation. The company that listed in 2024 bore little resemblance to the distressed subsidiary of 2015. Revenue had grown, margins had expanded, and most importantly, the business had proven it could thrive independently.

The promoter structure post-IPO maintained continuity. The Promoters of the Company are Ajanma Holdings Private Limited, Digambar Chunnilal Bagde and Sanjay Kumar Verma. Digambar Bagde's continued involvement—four decades after founding the original partnership—provided continuity that investors valued.

The IPO wasn't an end—it was a beginning. Access to capital markets meant easier fundraising for growth. Listed stock provided currency for acquisitions. Public scrutiny would enforce discipline. Most importantly, it completed the transformation from distressed subsidiary to independent public company, a journey that few companies successfully navigate.

VII. Modern Operations & Competitive Position (2020-Present)

The quarterly results tell the transformation story in numbers. Revenue from Operations: ₹1,340.36 crore, a significant increase of 62.8% compared to ₹823.01 crore in Q3 FY24. Net Profit: The company posted a profit of ₹93.24 crore, a 91.1% jump compared to ₹48.59 crore YoY. These aren't just growth rates—they're validation that the business model works at scale.

The order book strength provides multi-year visibility. It had order book worth Rs. 10213 cr. as of June 30, 2024. Transrail's revenue is expected to register growth of more than 20% on-year in fiscal 2025 driven by healthy execution of the order book which stood at Rs ~10,213 crore as on June 30, 2024. Recent updates suggest further strength: Transrail Lighting Ltd (TLL) recorded an outstanding order book of over Rs.14,500 crore, as of March 31, 2025.

The margin profile sets Transrail apart from peers. EBITDA increased by 80.0% YoY, reaching Rs 179.80 crore compared to Rs 99.91 crore, with EBITDA Margin expanding by 131 bps to 13.24%. In an industry where 7-8% EBITDA margins are common, Transrail's double-digit margins reflect operational excellence and pricing power.

The geographic mix has evolved strategically. International orders now constitute over 60% of the order book, providing natural hedging against domestic economic cycles and government spending patterns. But this isn't random international expansion—it's focused on markets where Indian EPC capabilities have competitive advantages: Africa's infrastructure deficit, Southeast Asia's grid modernization, and Middle East's renewable integration needs.

The competitive positioning is unique. Unlike pure-play EPC contractors who compete solely on price and execution, Transrail's integrated manufacturing provides cost advantages. Unlike pure manufacturers who depend on third-party contractors, Transrail's execution capabilities ensure quality control. This integrated model—manufacturing plus EPC—creates a moat that's difficult to replicate.

Financial metrics validate the operational success. Working capital days have improved despite rapid growth—a rare achievement in the EPC sector. Return on capital employed has expanded even as the capital base has grown. The company's ability to self-fund growth while maintaining healthy dividend payouts demonstrates cash generation capabilities.

The technology adoption strategy remains pragmatic. While competitors chase digital transformation narratives, Transrail focuses on practical applications: drone surveys for transmission line routing, automated welding for tower fabrication, real-time project monitoring systems. The recent innovation partnership with Epsilon Composite from France for HTLS (High Temperature Low Sag) conductors shows selective technology adoption where it creates real competitive advantage.

Human capital management has evolved significantly. In the next 12–18 months, the company's focus will be on improving the order book, on-time delivery and developing the organisation through good HR policies. "We are trying to develop a young team of people and show them a career growth plan," he says. "We are also encouraging job rotation, trying to retain talents and conducting training programs.

The customer concentration risk, while still present with 70% revenues from government entities, is actively being managed. Private sector renewable developers, data center operators, and industrial clients are being cultivated. The railway electrification business provides diversification within the government spending umbrella.

Recent order wins validate the strategy. Transrail Lighting Ltd on February 27, 2025, secures new contracts worth ₹2,752 crore, mainly in the transmission & distribution (T&D) segment. The momentum continues with management confidence: Transrail aims to sustain an annual order inflow of ₹5,000-6,000 crore in the 2024-25 financial year (FY25), spanning both domestic and international markets.

The credit rating upgrade provides external validation. CRISIL's upgrade to 'A+/Stable' reflects improved financial metrics and business stability. For a company that emerged from a distressed parent just eight years ago, achieving investment-grade ratings represents remarkable progress.

VIII. Playbook: Business & Investing Lessons

The Transrail story offers a masterclass in navigating corporate distress. When your parent company has ₹14,810 crore in debt and banks are circling, most subsidiaries don't survive independently. Transrail did more than survive—it thrived. The key? Never let the parent's problems infect the subsidiary's operations. Keep executing projects, paying suppliers, and maintaining customer relationships. When the restructuring comes—and it will—operational excellence becomes your leverage.

Vertical integration in infrastructure isn't fashionable—asset-light is the mantra everyone chants. But Transrail's integration strategy reveals a deeper truth: in industries where supply chain reliability determines project success, controlling critical inputs isn't just strategic—it's existential. The ability to guarantee tower delivery because you manufacture them, to ensure conductor quality because you produce them—these become competitive advantages that pure-play contractors can't match.

Geographic diversification sounds obvious but execution is treacherous. Transrail's international expansion wasn't scattershot—it was surgical. Focus on markets where Indian engineering costs provide advantage. Build local partnerships for navigation. Most importantly, learn from each market and apply lessons elsewhere. The Bangladesh concentration (₹3,500 crore orders) shows both the opportunity and risk of international expansion.

Business line expansion requires discipline. Railways and substations weren't random additions—they leveraged existing capabilities while opening new markets. The lighting division might be small, but it provides optionality. The key is expanding into adjacencies where your core capabilities provide competitive advantage, not chasing growth for growth's sake.

Capital efficiency in EPC requires obsession. Working capital is where EPC companies die—receivables stretch, payables compress, and cash evaporates. Transrail's ability to maintain industry-leading margins while growing rapidly shows that operational excellence and growth aren't mutually exclusive. The secret? Integrate manufacturing to control payment terms, diversify geographically to reduce concentration, and maintain financial discipline even during boom periods.

Building credibility post-restructuring takes time and consistency. Markets have long memories—the Gammon association could have been an albatross. But consistent execution, conservative financial management, and transparent communication gradually rebuilt trust. The 37% listing premium wasn't just about market conditions—it was validation that the transformation was real.

Timing public markets requires patience and preparation. The 2024 IPO came eight years after independence from Gammon—enough time to establish track record, clean up the structure, and demonstrate sustainable growth. Going public earlier might have been possible, but the valuation would have reflected uncertainty. Patience paid off with a ₹9,863 crore market cap.

The management continuity lesson is underappreciated. Digambar is confident that with this organisation being mostly technology-driven and with the emphasis on technical competence, Transrail Lighting will continue to be a market leader. Having the founder still involved after 40 years provides institutional knowledge that no MBA can replace. In infrastructure, relationships and reputation compound over decades.

The financing strategy post-restructuring was deliberately conservative. No leveraged growth, no aggressive acquisitions, no financial engineering. Just steady execution funded by operations. This might seem boring, but in an industry littered with overleveraged corpses, boring is beautiful.

For investors, Transrail offers several lessons. First, distressed situations can create opportunity if the underlying business is sound. Second, integration in unfashionable industries can create sustainable moats. Third, management quality matters more than market momentum—Bagde's four-decade commitment is worth more than any quarterly earnings beat.

IX. Industry Analysis & Future Outlook

India's power infrastructure opportunity is staggering in scale. India's domestic transmission lines expanding to 485,544 CKM by 2024 and an anticipated ₹3 trillion investment in the sector between 2025 and 2029. For context, that's equivalent to building transmission infrastructure covering the distance from Earth to the Moon—and back—twice over. The investment pipeline isn't just government wishful thinking—it's necessity driven by electricity demand growing at 7% annually.

The renewable energy transition creates complexity that benefits sophisticated players. Solar and wind generation requires new transmission infrastructure, often in remote locations. The intermittent nature demands grid stabilization investments. Battery storage integration needs specialized engineering. Transrail's technical capabilities position it perfectly for this complexity premium.

Railway electrification represents a ₹100,000 crore opportunity over the next decade. India targets 100% electrification of broad-gauge routes, requiring 30,000 route kilometers of overhead equipment. For companies with transmission line expertise, railway electrification is a natural adjacency. Transrail's early entry and execution track record provide first-mover advantages.

The competitive landscape is consolidating. Smaller players lack balance sheets for large projects. Regional contractors struggle with technology requirements. Even established players like KEC International and Kalpataru Power face margin pressure. Transrail's integrated model—manufacturing plus EPC—provides structural advantages in this consolidation.

International opportunities multiply as emerging markets build infrastructure. Africa's electricity access remains below 50%. Southeast Asia needs grid modernization for renewable integration. Latin America requires transmission infrastructure for resource development. Indian EPC companies, with their cost-competitive engineering and execution expertise, are natural beneficiaries.

Technology shifts create both opportunity and threat. Smart grids require digital capabilities beyond traditional engineering. HTLS conductors enable higher capacity without new towers. Drone surveying and AI-powered project management are becoming table stakes. Transrail's partnership with Epsilon Composite for HTLS conductors shows awareness, but continuous innovation is essential.

The regulatory environment remains supportive. Government's focus on 24x7 power for all drives transmission investment. Renewable purchase obligations force distribution companies to strengthen infrastructure. Cross-border power trading requires international interconnections. Each policy thrust creates order opportunities.

Risks are real and multiplying. Commodity price volatility can destroy project economics—steel and aluminum constitute 60% of project costs. Currency fluctuation impacts international projects. Payment delays from government utilities stress working capital. Execution challenges in difficult terrains test project management capabilities.

The Bangladesh concentration deserves special attention. With ₹3,500 crore of orders, Bangladesh represents significant revenue concentration. Political instability, currency devaluation, or payment delays could impact performance. Geographic diversification is progressing, but concentration risk remains.

Competition from Chinese players in international markets intensifies. Chinese EPC companies, backed by state financing, often underbid dramatically. However, quality concerns and geopolitical considerations are shifting preferences toward Indian companies. The "China Plus One" strategy adopted by many countries benefits Indian infrastructure exporters.

ESG considerations increasingly influence project awards. Environmental clearances for transmission lines face scrutiny. Social impact of land acquisition requires careful management. Governance standards for public contracts are tightening. Companies with strong ESG credentials will have advantages in project selection.

The outlook remains constructive despite challenges. Infrastructure spending correlates with economic development—as India targets $5 trillion economy, infrastructure investment must follow. The energy transition requires massive grid investments. Urban expansion demands distribution infrastructure. Each trend supports multi-year growth visibility.

For Transrail specifically, the opportunity set is expanding. The order book provides 2+ years visibility. International diversification reduces domestic concentration. Manufacturing integration provides margin protection. The challenge will be execution—scaling operations while maintaining quality, expanding internationally while managing risks, growing rapidly while preserving culture.

X. Bear vs. Bull Case

Bull Case:

The order book tells the growth story. ₹14,500 crore as of March 2025 provides visibility through FY27. With execution capabilities proven and manufacturing capacity available, revenue growth appears mechanical rather than speculative. If the company maintains its historical execution rate, 25% annual growth seems conservative.

Margin superiority reflects structural advantages, not temporary benefits. The 13.24% EBITDA margin isn't from one-time gains—it's from integrated operations, selective bidding, and operational excellence. As revenue scales and fixed costs leverage, margins could expand further. A 15% EBITDA margin by FY27 isn't unrealistic.

Infrastructure spending tailwinds are multi-decade, not cyclical. India's per capita electricity consumption at 1,331 kWh remains a fraction of China's 5,500 kWh or US's 12,000 kWh. Reaching even China's level requires tripling transmission infrastructure. This isn't a 5-year opportunity—it's a 25-year structural growth story.

International diversification provides multiple engines of growth. While peers depend on Indian government spending, Transrail's 60% international order book provides resilience. Africa's infrastructure deficit, Middle East's renewable ambitions, and Southeast Asia's grid modernization create diverse growth avenues.

The balance sheet strength enables aggressive bidding. Post-IPO, the company has minimal debt and strong cash generation. This financial flexibility allows bidding for larger projects, better payment terms, and strategic investments. In an industry where balance sheet strength determines project wins, Transrail has competitive advantage.

Management's four-decade commitment provides stability rare in Indian infrastructure. Digambar Bagde's continued involvement ensures continuity. The professional management team brings modern practices. This combination of entrepreneurial DNA and professional management creates sustainable competitive advantage.

Valuation remains reasonable despite the rally. At 24.9x P/E versus Bajel Projects at 161.6x, relative valuation appears attractive. The PEG ratio, considering 25% growth potential, suggests room for multiple expansion. If the company delivers on execution, a 30-35x P/E isn't unreasonable.

Bear Case:

Government dependence creates vulnerability. Despite diversification, 70% of revenues come from government entities. Payment delays, policy changes, or fiscal constraints could impact cash flows. The recent history of distribution company financial stress shows this isn't theoretical risk.

Working capital intensity limits cash generation. EPC businesses are structurally working capital intensive. As growth accelerates, working capital needs multiply. Even with perfect execution, cash conversion remains challenging. The company might show profits but struggle with cash generation.

Execution risks multiply with scale. Managing projects across 58 countries isn't just about engineering—it's about logistics, regulations, and local politics. One major project failure could damage reputation and finances. The Bangladesh concentration exemplifies this risk concentration.

Competition from larger players intensifies. L&T, KEC International, and Kalpataru have deeper pockets and longer track records. Chinese companies compete aggressively in international markets. As projects become larger and more complex, scale disadvantages could limit Transrail's competitiveness.

Commodity price volatility threatens margins. Steel and aluminum constitute majority of project costs. Fixed-price contracts provide no protection against input cost inflation. While the company has managed historically, a sustained commodity spike could destroy project economics.

Technology disruption could obsolete capabilities. Alternative transmission technologies like underground cables or wireless power transmission could disrupt traditional tower-and-line business. While these seem distant, technology transitions can happen faster than expected.

Management succession remains unclear. Digambar Bagde's four-decade involvement is both strength and risk. Succession planning isn't transparent. The transition, whenever it happens, could create uncertainty.

The international execution track record, while growing, remains limited. Large international projects in challenging geographies test capabilities differently than domestic projects. Payment risks, currency fluctuations, and political instability add layers of complexity.

Valuation has run ahead of fundamentals. The stock's 73% gain in nine months reflects high expectations. Any execution disappointment could trigger sharp correction. The current valuation provides limited margin of safety.

XI. Epilogue & Recent Developments

The stock market's verdict has been decisive: from ₹432 IPO price to ₹748.50 in nine months represents a 73% gain that outperformed the broader market significantly. But beyond the price appreciation, the trading patterns reveal institutional accumulation and retail participation that suggests this isn't just momentum—it's fundamental reappreciation.

Bagged ₹421 crore orders including large African transmission-line; FY26 inflows exceed ₹3,500 crore (78% Y-o-Y) as of Aug 2025. The order momentum continues to accelerate, validating management's guidance of ₹5,000-6,000 crore annual inflows. Each order win isn't just revenue—it's validation of execution capabilities and competitive positioning.

The innovation partnership with Epsilon Composite deserves attention. HTLS conductors represent the future of transmission—higher capacity, lower sag, reduced tower requirements. This isn't just technology adoption—it's positioning for the next generation of transmission infrastructure. Early mover advantage in HTLS could provide differentiation in commodity-like EPC business.

Randeep Narang, MD & CEO, noted: "We are pleased to close FY25 with an excellent performance across all key operational parameters, marked by strong revenue growth, benchmark margins, and record order inflows. Our continued focus on core strengths, disciplined execution, and operational efficiencies has enabled our encouraging results. As we step into FY26, we do so with a strong order book and a positive outlook for the sector which continues to offer meaningful opportunities. We remain committed to leveraging our integrated capabilities to drive balanced growth and deliver value to all stakeholders".

The management's vision for the next phase focuses on three pillars: operational excellence, selective diversification, and technology adoption. No moonshot announcements or transformational acquisitions—just steady execution of a proven strategy. In an industry littered with ambitious failures, such conservatism is refreshing.

Key metrics to watch going forward: order inflow momentum (target: ₹6,000 crore annually), EBITDA margin trajectory (target: maintain above 12%), working capital days (target: below 120 days), and international mix (target: maintain above 50%). These aren't just numbers—they're health indicators of the business model.

The biggest surprise from researching Transrail isn't the successful IPO or the margin superiority—it's the resilience. Surviving a parent company's ₹14,810 crore debt crisis, navigating strategic debt restructuring, and emerging as a ₹9,863 crore market cap company requires more than luck. It requires operational excellence, strategic clarity, and most importantly, the ability to execute when everything around you is falling apart.

Looking ahead, Transrail represents a bet on three mega-trends: India's infrastructure build-out, the global energy transition, and the competitive advantage of Indian engineering. If you believe India will build the infrastructure required for economic growth, that renewable energy will require massive grid investments, and that Indian EPC companies can compete globally, then Transrail offers a vehicle to participate in these themes.

The journey from a partnership firm doing foundation work in Gujarat to a public company executing projects across 58 countries is remarkable. But perhaps the most remarkable aspect is how unremarkable the strategy has been: vertical integration when others outsourced, geographic diversification when peers stayed local, steady execution when competitors chased growth. Sometimes, in business as in life, the boring path proves most rewarding.

For long-term investors, Transrail offers an interesting proposition: exposure to infrastructure growth with demonstrated execution capability, attractive margins with improving returns, and management alignment with four-decade commitment. The risks are real—government dependence, working capital intensity, execution challenges—but the opportunity appears larger than the obstacles.

The story of Transrail Lighting isn't finished—in many ways, it's just beginning. The IPO marked not an end but a transition from survival to growth, from regional player to international competitor, from distressed subsidiary to independent powerhouse. The next chapter—whether it involves acquisitions, international expansion, or technology transformation—remains unwritten. But if the past four decades are any indication, it will be written with the same steady hand that has guided the company from foundation to fortune.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube